CREDIT · PDF fileIntroduction to Capital Markets and Private Banking ... Our Sustainable...

126

2005 ANNUAL REPORT 2005

Transcript of CREDIT · PDF fileIntroduction to Capital Markets and Private Banking ... Our Sustainable...

2 0 0 5A N N U A L R E P O R T 2 0 0 5

Our Values are our compass. CL values include mutual trust and respect, customer focus, creativity, achievement, and integrity.

Mutual trust and respectWe want all staff in our working community to trust and respect each other. We should accept diversity, be open to new ways ofthinking and be prepared to help one another in times of need. The joy of success lies in sharing experiences.

Customer focusWe want to understand, anticipate and meet our customers’ present and future needs. Close cooperation with customers willensure fulfillment of their needs and their problems steer both our immediate and long-term actions.

V a l u e s

Credit LibanaisTraining Report 2005 1

CreativityWe embrace change. We continuously seek better solutions for the customers and the Bank.

High AchievementWe strive to be the best in our field, by developing products, services and solutions that reflect financial excellence.

Integrity We value each other’s ideas and opinions. We treat colleagues fairly, sincerely and courteously, irrespective of differences inbackground or beliefs.

Contents

Chairman’s Address

Human Resources Manager’s Report

Performance-Driven Culture

Spreading the ISO Culture at Credit Libanais

Employee-Management Communication Channels

HR-Employee CommunicationEmployee NewsletterValued Suggestions for Improvement

Major Training Activities

In-house Training Programs

Enhancing Credit SkillsIntroduction to Capital Markets and Private BankingIntegrated Risk Management SystemsPbViews for Performance EvaluationPotential Assistant Branch ManagerHuman Resources Culture EnhancementLetters of Credit TrainingCustomer Relationship Management: Entreprise Data WarehouseGroup Ethics and Compliance with AML best practices in the Banking Profession

External Training Programs

Statistics of the Year

Trainers’, Employees’, and Customers’ Feedback

2

4

6

8

10

101112

13

14

141415151515161616

17

18

20

Credit Libanais Group Annual Report 20052

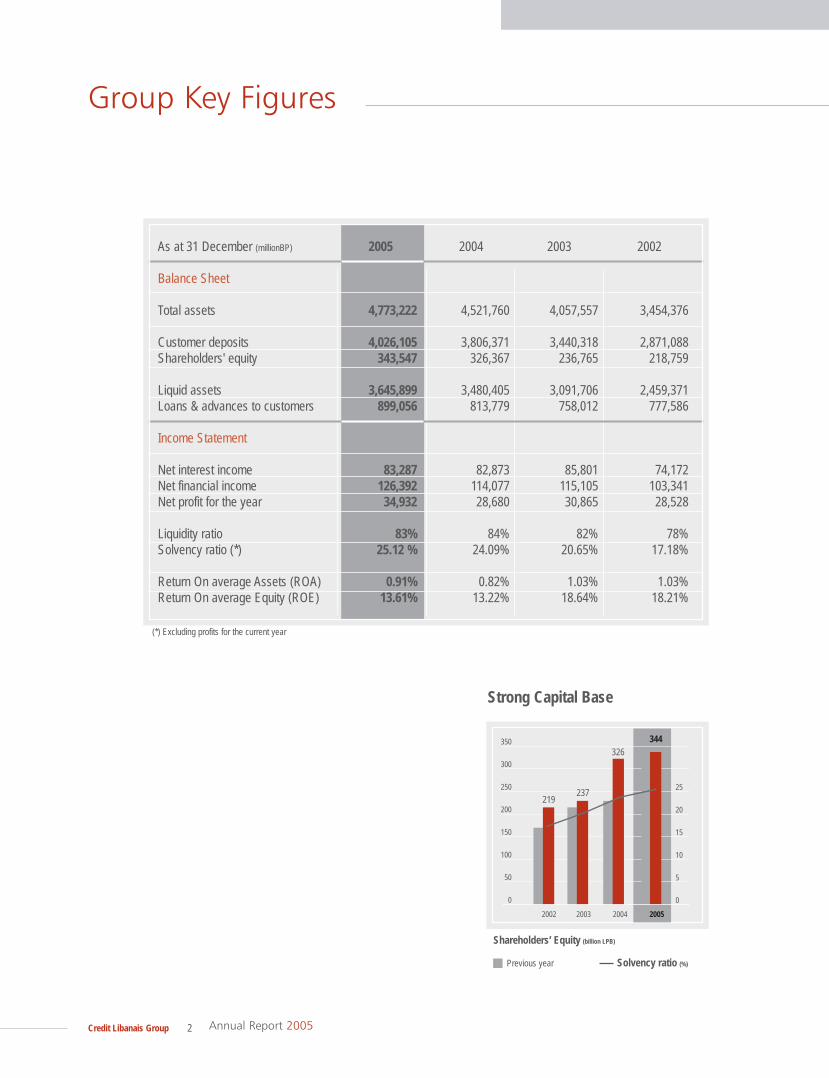

Group Key Figures

(*) Excluding profits for the current year

As at 31 December (millionBP)

Balance Sheet

Total assets

Customer depositsShareholders' equity

Liquid assetsLoans & advances to customers

Income Statement

Net interest incomeNet financial incomeNet profit for the year

Liquidity ratioSolvency ratio (*)

Return On average Assets (ROA)Return On average Equity (ROE)

2005

4,773,222

4,026,105343,547

3,645,899899,056

83,287126,39234,932

83%25.12 %

0.91%13.61%

2004

4,521,760

3,806,371326,367

3,480,405813,779

82,873114,07728,680

84%24.09%

0.82%13.22%

2003

4,057,557

3,440,318236,765

3,091,706758,012

85,801115,10530,865

82%20.65%

1.03%18.64%

2002

3,454,376

2,871,088218,759

2,459,371777,586

74,172103,341

28,528

78%17.18%

1.03%18.21%

Strong Capital Base

Shareholders’ Equity (billion LPB)

Previous year Solvency ratio (%)

350

300

250

200

150

100

50

0

2002 2003 2004 2005

25

20

15

10

5

0

219237

326344

Credit Libanais GroupAnnual Report 2005 3

Group Key Figures

Total Assets (billion LPB)

Previous year

Growth Trend in Banking Activity

Sustainable Profitability and Value Creation

Liquid Assets (billion LPB)

Previous year

Net Financial Income (billion LPB)

Net interest income Non-interest income Previous year

Total Customer Deposits (billion LPB)

Previous year

Loans & Advances to Customers (billion LPB)

Previous year

200

150

125

100

75

50

25

0

2002 2003 2004 2005

103115 114

126

3,500

3,000

2,500

2,000

1,500

1,000

500

0

2002 2003 2004 2005

2,459

3,4803,646

5,250

4,500

3,750

3,000

2,250

1,500

750

0

2002 2003 2004 2005

4,0574,522

4,773

1,050

900

750

600

450

300

150

0

2002 2003 2004 2005

778 758814

899

4,000

3,500

3,000

2,500

2,000

1,500

1,000

0

2002 2003 2004 2005

2,871

3,440

3,8064,026

3,454

3,092

Credit Libanais Group Annual Report 20054

Chairman’s Address

Lebanon recorded a sad year during 2005 marked by the assassination offormer Prime Minister Rafic Hariri whose contributions to the country and itseconomy are innumerable. His tragic departure perturbed the wholeLebanese economic sector during the first quarter of the year.

As a result, 2005 was a challenging year for our strategy which proved, oncemore, its resilience and flexibility in the face of such tragic events with long-lasting economic repercussions. We were able to transform adversities into astandard everyday event which translated into a substantial growth of 5.6%in total assets and 22.3% in pre-tax profits, well above average marketperformance. The pillars of our successful strategy rest in the diversificationof our sources of income, our mastering of a sound Risk Managementstrategy, our ongoing streamlining of operations, a strong brand name, awide geographic distribution of customer base, several partnerships withmajor regional and international financial institutions, and relationships withexport development and guarantee corporations. This strategy coupled withswift but vigorous daily fine-tunings of our operations allowed us to quicklyrespond to local and regional developments.

Credit Libanais unveiled a considerable 21.8% year-on-year increase in netprofits to USD 23.17 million as at end of December 2005, up from USD19.02 million during the year 2004. The Bank’s non interest incomeexpanded markedly by 38% to USD 28.59 million. Consequently, netfinancial income revealed a healthy 10.8% annual growth to USD 83.84million. On the balance sheet front, the Bank’s total assets widened by5.56% to USD 3.16 billion as at end of December 2005. Credit Libanais’pre-tax return on average assets (ROaA) stood at 0.91% in 2005, whilepre-tax return on average equity (ROaE) ended the year at 13.61%.

Credit Libanais Investment Bank (CLIB), the Group’s medium and long terminvestment subsidiary, continued to complement the product offer of CreditLibanais Group. CLIB’s investment desk explored several businessopportunities and conducted feasibility studies covering neighboringcountries including Syria, Iraq, and Yemen.

Credit Libanais d’Assurances et de Réassurances (CLA), the Group’s insurancearm, has been rated as Lebanon’s third most profitable insurance companyaccording to industry-rating magazines, owing to the efficient managementcombined with inherent synergies with the Group’s subsidiaries.

While the Group’s long-term success has, for long, been mainly rooted in themix of core businesses namely Retail, Corporate, Investment Banking,Capital Markets, and Bancassurance, our performance has been fuelled by aSustainable Development Strategy - a strategy based on a strong commitmentto strengthen existing partnerships with each one of our stakeholders(Customers, Employees, Shareholders, Board Members, Regulators,Society,...) as part of our Corporate Governance framework.

“We regard our partnershipwith our Stakeholders,which is the core of ourSustainable DevelopmentStrategy, as a proxy forfuture growth. Althoughcautiously optimistic aboutthe near-term economic performance, Credit Libanaisshall move forward withconfidence.”

Credit Libanais GroupAnnual Report 2005 5

Chairman’s Address

For many years now, Credit Libanais has demonstrated its leadership in Information Technology and its capacityto stay one step ahead of fast moving changes in this field. Our state-of-the-art Customer RelationshipManagement (CRM) solution is a prime example. During 2005, CRM became fully operational allowing us toprofile our customers in order to better cater to their changing needs and expectations. CRM proved indispensablefor the outstanding performance of our Retail activity. Indeed, Retail as a core activity at Credit Libanais was ableto proactively anticipate customer needs before they materialize. Our future plans are to leverage the capabilitiesof this tool for the benefit of all of our core businesses.

Our Sustainable Development Strategy, which incorporates those external and internal banking and parabankingtactics most essential for a sound long-term growth, included the creation of the Planning and Organization Unit(POU). This permanent body is formed by a team of high ranking consultants from within the Bank and professionals from the Operations Division who team up with members of a department to restructure andstreamline operations, review business processes, upgrade existing systems and downsize on resources in viewof redeploying them. Throughout 2005, POU reviewed, institutionalized and automated several functions in linewith the latest best practices in the industry.

We operate in a service industry that relies heavily on trust. In order to inspire confidence, we need to prove thatwe maintain the highest levels of business ethics namely combating Money Laundering.

Our Group harness growth by combining strong performance with a proven commitment to the communites inwhich we operate. Our social involvement is not only restricted to donations and sponsorships, it also incorporatesfunding, supporting social organizations, and/or providing a helping hand to those in need.

Looking ahead, while we expect patchy growth in a region that remains vulnerable to significant uncertainties, theprospects of the Lebanese financial sector are likely to undergo far-reaching expansions on the back of a regionalgrowth fuelled by oil price surges. These developments produce promising business opportunities that CreditLibanais is ready to seize in order to extend our footprint regionally. The foremost positions we enjoy in ourvarious activities and our proven financial strength pave the way for this new regional expansion strategy - astrategy incorporating a drive to boost operating efficiency and to maintain a stringent control of risks.

Recruiting new customers, winning their new businesses, and earning their loyalty hinges on the efforts of ourEmployees. We acknowledge that our ability to move forward rests, in great part, on our human capital. Ourrecognition also goes to our Shareholders and Board Members who consistently place the interests of CreditLibanais at the forefront of their priorities. It is to them, all, that Credit Libanais owes this exceptional performanceand through their continuous support that we will maintain our competitiveness in a fast pace of consolidation inthe regional and international financial markets.

We regard our partnership with our Stakeholders, which is the core of our Sustainable Development Strategy, asa proxy for future growth. Although cautiously optimistic about the near-term economic performance, CreditLibanais shall move forward with confidence.

Joseph TorbeyChairman & General Manager

Credit Libanais Group Annual Report 20056

Board of Directors Credit Libanais SAL

Dr. Joseph TorbeyChairman &

General Manager

Mr. Abdulrahman Bin MahfoozRepresenting Capital InvestmentHolding Co. (Manama - Bahrain)

H.E. Mr. MarwanHamade

Mr. Khaldoun Barakat

Mr. MohamadWajih El-Bizri

Members

Mr. Rabah Idriss

Mr. RabahJaber

Mr. Sarkis Demirdjian

Mr. Abdul-ElahMukred Ali

Mr. Abdullah SaudiAdvisor tothe Board

Capital Investments Holding - Lebanon SALMember

Credit Libanais GroupAnnual Report 2005 7

Major Committees

Major CommitteesMANAGEMENT COMMITTEE (MC) The Management Committee is the Bank’s chief decision-making body, tackling strategic internaland external issues of prime importance to the Bank, and formulating long-term policies and orientations in-line with the Board of Directors’ guidelines and the Group’s overall strategy.

ASSET AND LIABILITY COMMITTEE (ALCO)ALCO focuses on risk and strategic issues related to interest rate monitoring, liquidity and currencyratios, counterpart credit assessments, geographical risk allocation, capital management and marketrisks. Based on committee appraisals, the Bank’s Management develops measures and controlsaimed at mitigating risks and keeping them at acceptable levels.

CREDIT COMMITTEES Every lending activity at Credit Libanais goes through a special purpose committee assigned toensure that loans and credit limits are granted based on the Bank’s credit guidelines. The CreditPolicy Committee defines risk strategies, policies and corporate credit practices and limits for thecoherent and efficient management of different credit risk areas of the Bank.

INVESTMENT COMMITTEEIn tandem with developing plans for investment banking activities, this Committee’s responsibilitiesalso extend to identifying and assessing the major investment opportunities in the fields of mergersand acquisitions, equity and loan participation, advisory and consultancy and other issues of strategic financial importance.

OPERATIONAL RISK MANAGEMENT COMMITTEE (ORMC)The ORMC’s main objective is to make Operational Risk Management an integral part of the Bank’sdaily activities by introducing measures aimed at improving the internal control function and monitoring operational risks in view of mitigating them. These operational risks include individual,departmental, branch management, as well as internal and external factors. The ORMC alsoensures the quality review of existing written procedures and updates them in line with the Basel IIrequirements and the proven best practices nationally and internationally.

ANTI-MONEY LAUNDERING COMMITTEE (AML) The AML committee closely examines and monitors suspicious cases and takes proactive steps in theprevention of money laundering or fraudulent activities within the Bank. The Committee also reportssuspicious cases to the High Special Investigations Commission at the Central Bank of Lebanon.

AUDIT AND INTERNAL CONTROL COMMITTEE (AICC)In line with the growing importance of modern audit practices, the Committee specializes in thereview, monitoring and improvement of the Bank’s overall Internal Control environment and offersrecommendations as part of the Bank’s ongoing reforms.

SALES AND BUSINESS DEVELOPMENT COMMITTEE (SBDC) The Sales and Business Development Committee monitors and evaluates branch network performance,application of sales methodology and product profitability in anticipation of evolving market conditions.SBDC also approves the launching of new products and corporate communication campaigns.

Economic and Financial Review

Credit Libanais Group Annual Report 20058

Lebanese Economy and Public Sector

The year 2005 was marked by escalations inpolitical turmoils in Lebanon and the region, hampering as such, the pace of economicgrowth witnessed in the past couple of years.Nevertheless, sustained interests by foreigninvestors, particularly Arab investors, helpedalleviate the risk of an imminent recession.

Lebanon benefited from the increasing confidenceby Arab investors in the MENA region owing toimproved liquidity from increasing oil prices.Foreign Direct Investments (FDI) in Lebanonextended its upturn in 2005 with a noticeablerebound in real estate investments. Constructionpermits accumulated to around 8.46 million m2 asat end of December 2005 up from 9.16 m2 in 2004.

The monetary policy of the Central Bank ofLebanon maintained interest rates at high levelsin 2005 in an attempt to ease the pressure on theLebanese Pound. The policy also endeavored tominimize the risk of increasing deficit in thebalance of payment in an atmosphere of politicaluncertainty and fear of jeopardizing consumerconfidence in the economy thus obstructing therapid outflow of money.

On the public finance front, the budget deficitcontracted by 7.53% in 2005, standing at LBP2,798 billion, down from LBP 3,026 billion in 2004.Total government revenues fell by 1.45% year-on-year to LBP 7,405 billion, while expenditures,including debt servicing regressed by some LBP337 billion to LBP 10,203 billion as at year-end

2005. The deficit to total expenditures ratio fell to27.42% in 2005, from 28.71% in 2004.

As far as public debt is concerned, statistics reveala 7.37% annual increase in gross public debt toUSD 38.50 billion in 2005 from USD 35.86 billionin 2004. Of the total gross public debt, 49.80% isexternal while the remaining 50.20% is domestic.Public sector deposits rose to USD 3.70 billion in2005, while net public debt rose by 5.54% year-on-year to USD 34.79 billion up from USD 32.97billion in 2004. Net domestic debt constituted44.89% of net public debt in 2005, while foreigndebt increased by 4.40% to USD 19.17 billion.

Moreover, on the current account side of thebalance of payment, Lebanon’s balance of tradedeficit tightened by USD 190 million year-on-yearreaching USD 7,460 million in 2005, down fromUSD 7,650 million in 2004. Total exports rose by7.61% year-on-year to USD 1,880 million, whileimports contracted by 0.61% to USD 9,340 millionin 2005. In this context, Lebanon witnessed asubstantial expansion in its Balance of Payment(BOP) surplus reaching USD 600 million as at year-end 2005, compared to a surplus of USD 168.5million in 2004 and that of USD 3.25 billion in 2003.

On the fixed income front, the Lebanese Ministryof Finance continued to issue new Republic ofLebanon (ROL) Eurobonds and Certificates ofDeposits at attractive rates in 2005 with theobjective of lessening the debt service burdenand financing public sector growth. The CentralBank of Lebanon launched in mid-April 2005 thefirst issue of Euro CDs accumulating some USD1.7 billion in total subscriptions. The issue carries

Two thousand and five was a difficult year forLebanon and for the Lebanese economy on almostevery front. Nevertheless, sustained interests byforeign investors, particularly Arab investors, alleviated the situation.

2002 2003 2004 2005

7,000

6,000

5,000

4,000

3,000

2,000

1,000

0

1,564

3,386

1,685747

Balance of Payment (million USD)

Credit Libanais GroupAnnual Report 2005 9

2005 Economic and Financial Review

a coupon rate of 10% payable semi-annually anda maturity of 10 years. Furthermore, the LebaneseMinistry of Finance launched in mid June a newROL Eurobond issue divided into two series for atotal of USD 500 million: a 3-year bond yielding7.5% per annum for a total amount of USD 250million priced at USD 99.67, and an 8-year bondyielding 8.625% for a total amount of USD 250million and a price of USD 99.28. This transactionwas lead managed by BLOM Bank and CreditSuisse First Boston. Furthermore, in the domesticEurobond market, the Lebanese Ministry ofFinance had issued in end of September a new10-year ROL Eurobonds issue worth USD 750million, maturing in January 2016. The new ROLEurobonds issue will cover old debt maturing in2005, and carrying an annual coupon of 8.75%.The 10-year ROL Eurobond issue has beenassigned a long-term foreign currency rating of B-by Fitch and Standard & Poor’s and B3 by Moody’s.

International rating agencies reiterated their creditratings for the Republic of Lebanon in 2005 whilechanging the outlook to “Positive”. Rating agenciespraised current effort by the Lebanese governmentunder a multi-pillared reform program which isexpected to improve the country’s rating. Therating agencies praised the efficiency of the VATsystem in income generation to the government,considering it the most effective tax instrumentavailable to the authorities. On the monetary policyfront, international rating agencies commentedthat the pegged exchange rate regime remainsthe appropriate monetary policy at this time,particularly in ‘the widespread dollarization andcontinued uncertainties’. The reform should alsobe accompanied by financial sector reform topreserve the banking sector and to provide capitalto the private sector in order to diversify risks andattract long term capital to the country.

As far as the inflationary environment is concerned,Lebanon’s Consumer Price Index (CPI) fell sharplyby 2.78% on a yearly basis to 99.63 in December

2005, from 102.48 in December 2004; therefore,signaling a moderate contraction in the averageprice of a Lebanese consumer good-basket.

Central Bank of Lebanon’s coincident indicator,which is an index portraying the general trend inthe economy, grew by 4.97% on a yearly basis to183.5 in December 2005, from 174.8 in December2004, implying a stimulated economic activityduring the period under consideration andportraying an improvement in general economicactivity.

On the tourism front, Lebanese Ministry ofTourism statistics revealed an annual 10.87%contraction in the number of tourist arrivals toLebanon in 2005 compared to the same period in2004. More particularly, the total number oftourists reached 1,139,524 as at end of December2005, down from 1,278,469 tourists during 2004.The number of Arab tourists outpaced othertourists’ arrivals, reaching 451,430 as at end ofDecember. European tourists occupied the secondplace, reaching 311,083 visitors, followed by Asiantourists with total reported arrivals of 177,809.

Lebanese Banking Sector

The consolidated balance sheet of commercialbanks in Lebanon revealed a moderate 3.75%annual appreciation in banking sector assets toLBP 106,015 billion in 2005 from LBP 102,187billion in 2004. Total deposits, including non-residents private sector deposits, rose by 4.10%year-on-year to LBP 89,169 billion as at year-end2005, with dollarization rate expanding to 73.13%up from 70% in 2004.

The value of returned checks rose by 10.8% toLBP 1,005 billion (229,171 checks) up toNovember 2005, from LBP 907 billion (228,977checks) during the same period in 2004. Of thetotal value of returned checks, 74.14% weredenominated in foreign currencies while theremaining 25.86% were in Lebanese Pound.

Moreover, the Central Bank of Lebanon’s statisticsrevealed a 1.48% year-on-year expansion inLebanon’s gross foreign currency reserves toreach USD 11.65 billion as at year-end 2005 upfrom USD 11.48 billion in 2004.

December2004

December2005

12,000

10,500

9,000

7,500

6,000

4,500

3,000

1,500

0

Cumulative Balance of Trade Deficit (million USD)

Exports Imports Deficit

Looking ahead, the prospectsof the Lebanese financial

sector are likely to undergofar-reaching expansions

Core Banking Activity

Credit Libanais GroupAnnual Report 2005 11

Leadership in Selected Markets12 Retail Banking16 Corporate Banking18 Financial and Capital Markets

22 Investment Banking26 Bancassurance

Credit Libanais Group Annual Report 200512

Retail Banking

Retail Banking, backed by state-of-the-art e-bankingproducts, continues with its franchise expansioninside the Lebanese market to reach its peak with afull-fledged CRM in 2005.

With the emphasis placed on retail activityunder Credit Libanais forward-looking growthstrategy, Retail Banking is now well consoli-dated at the core of the Bank’s strategicactivities and plans. As a result, CreditLibanais has confirmed its status as a leadingreference in the Lebanese retail market.

Based on the principle that ‘the product is theprocess of serving customers’, the newinnovative approach to address customers’needs during their ‘24 hours a day, all thecycles of life’ was launched. The new life-cycleapproach focuses on the customer needs atevery stage of his life, as per each angle ofsegmentation analysis. Mortgage loans,consumer loans, deposit accounts, debit and

credit cards, E-banking, Small and MediumEnterprise (SME) loans and AssetManagement services are all being re-shapedunder Credit Libanais’ new approach in RetailBanking.

Moreover, Retail Banking has concentratedon product development and on increasingdelivery channel capacities and capabilities tobetter respond with integrated solutions toevolving customer needs.

Critical success factors have been determinedto achieve Retail Banking targets through theperformance matrix and branches havebeen assigned new roles to achieve targetedgrowth.

Credit Libanais GroupAnnual Report 2005 13

Core Banking Activity

Branch Network

Currently, Credit Libanais network consists of 57 branches including a new branch inFanar, Mount Lebanon. The growth of business required the establishment of a fifth Regional Management for North Lebanon.During 2005, our International Banking Unit inLimassol was transformed into a full-fledgedbranch regulated by the Central Bank ofCyprus and subjected to European bankingstandards and regulations. Finally, theRepresentative Office in Montreal - Canadadenotes our interest in the North Americanmarket.

Channel Banking

Our e-solutions - WAP Banking, InternetBanking, SMS, ATM, Customer ServiceCenter, Phone Banking and TV Banking -with numerous services linked to each aregaining momentum year after year due totheir reliability, convenience and advantages to customers. These productsare subject to ongoing upgrading and strict security controls in line with the latest international developments in the field.

Branches have been transformed into proactiveunits for sales and customer management.

In parallel, a process of driving value through‘Yield Management in Retail Banking’ wasalso introduced to optimize yield and preventbusiness conflict. Most of the emphasis hasbeen dedicated to understanding the leveland nature of underlying customer demand inorder to make proper prioritization and salesactivity.

NetCommerce

The activity of our Internet paymentacquiring arm, NetCommerce, continuedto increase during 2005 due to the implementation of sophisticated and highlysecured Internet payment technology -“Verified by VISA” procedures andMasterCard Secure Code. Consequently,NetCommerce sales volume grew by 25% over 2004.

The Company’s strategy for 2006 is togain significant market share by acquiringnew merchants through an aggressivesales and marketing effort in the growingLebanese e-commerce market.

120

100

80

60

40

20

02004 2005

30.28%

96.16%

Iskan Loan Growth

+55.37%

2003 2004 2005

+15.13%

Sales Evolution of Retail Product

E-banking activity continued to be furtherintegrated in the life cycles of our differentcustomer segment confirming the growthacceleration registered in past years. InternetBanking and Phone Banking have increasedby 28% and 27%, respectively.

Marketing and Sales

The ongoing development of products andservices is a top priority oriented towards customer satisfaction and covering differentsectors and segments.

Enhancing our Sales ForceA new sales team was recruited to complementour existing sales force, to satisfy the need ofour growing markets and to improve our

cross-selling ratio. A sales team is dedicatedto each of our five regions and headed by aSales Team Leader. The main task of everyteam is to develop sales through sales cam-paigns customized according to the Region’sparticular needs.

Both the sales force and our 57 branches followa schedule of marketing campaigns elaboratedin the Head Office. The close monitoring andfollow up of the sales teams and branchesensure a collective effort on all fronts.

Credit Libanais Group Annual Report 200514

30

25

20

15

10

5

02004 2005

22%23.8%

Personal Loan Growth

Retail as a core activity atCredit Libanais was able to

proactively anticipate customer needs beforebefore they materialize

Credit Libanais GroupAnnual Report 2005 15

Core Banking Activity

Product Development

In 2005, Credit Libanais designed severalproducts to respond to the needs of the retailmarket. These products targeted a segmentedgroup of customers, they include:

VISA Mini which is 43% smaller than aregular-sized VISA card. It is considereda convenient companion card linked toBankerNet, Ukrd or Ladies First and usedonly on Point of Sale (POS) terminals; A new local VISA Electron Vantage toreplace the old salary domiciliation product;A new international MasterCard chargecard to replace the old charge card product;Autumn Package comprising the followingproducts: VISA credit card, SMS service,Online Banking, and Phone Banking witha privileged access to the new and

improved Loyalty Scheme; andSpecial Housing Loans for public servants.

Image Consolidation ThroughMedia Advertising

Throughout 2005, Credit Libanais engaged inconsolidating corporate image through ongoingTV campaigns, sponsorships and press

ads/releases. Communication campaignswere coupled with the launching of our newTV ad, Trust, which was broadcasted on mostlocal TV stations.

Building a Strong Cross-SellingRatio

One of the main targets of the Retail Divisionand the Marketing Department for this yearwas to boost Credit Libanais cross-selling ratiofollowing the successful salary domiciliationcampaign of the public sector. To this end,several marketing campaigns were launchedbased on a database segmentation, customerbehavior and profile. The result was a substantial increase in product sales.

•

•••

•

Personal29% Iskan

20%

Iskan Personal4%

Ameen5%

Iskan Military1%

Car24%

Housing7%

Kafalat6%

Consumer4%

Retail Product Sales

KafalatCar

HousingAmeenIskan

Personal ConsumerIskan PersonalIskan Military

Credit Libanais Group Annual Report 200516

Corporate Banking

Specialized in the trading, manufacturing andservices sectors, the Corporate Division iswell-equipped to layer credit facilities andbanking services that cope with corporatecommercial needs for international and localtrading activities.

The Division is outfitted with expert RelationshipManagers committed to provide sound financialadvice and credit support to industrial andmanufacturing entities.

Our success is derived from a fundamentalcommitment to provide, through a dynamicand highly dedicated team, distinguishedquality services and financial support tocustomers. In other words, our CorporateDivision works at extending and tailoringdifferent credit packages of short-, medium-and long-term, cash and non-cash creditfacilities to finance almost all types of businessactivities.

By building a true partnership with our corporate customers based on nurturing along-term relationship and maintaining up-to-the-minute knowledge of their business, Credit Libanais has come to beviewed as a benchmark in Corporate Banking.

Credilease

Despite a difficult local and regionaleconomic environment, Credilease continues to consolidate its activities andto solidify its customer base. Leasingcontracts are customized based on thespecific needs and requirements of eachcustomer.

Its activity portfolio includes financingequipment in areas such as general contracting, hospitals, industry and transportation. Furthermore, a number ofour banking relationships are managedthrough Credilease’s leasing facilities, witha typical duration of 2 to 7 years.

Uncovered Loans41.82% Collateral

Covered Loans24.35%

Covered Loans33.83%

Collateral Covered Loans 24.35%(Mortgage + Cash Collateral + Bank Gtee + Shares)Covered Loans 33.83%(Personal Guarantee + Negative Pledge + Bills + IAIGC)Uncovered loans 41.82%

Breakdown of Corporate Portfolio by Type of Guarantee

The Corporate Division product offer includesordinary and subsidized loans, overdrafts,working capital finance, commercial draftdiscount, leasing facilities, trade finance, foreignexchange services, domestic and internationaltransfers, direct debits and standing orders.

Our Relationship Managers collaborate withall business units and bank affiliates to offercustomized solutions in varied areas of bankingand parabanking or peripheral complementaryservices.

Activity

Corporate Banking continued to grow its franchise within the Lebanese market and toattract new businesses in line with its conserva-tive risk appetite. The following increaseswere recorded by the Division during 2005:

16.4% growth in the funded and un-funded utilization implying a growth intotal outstanding facilities; and11% growth in the un-funded utilizedfacilities allowing for an increase in non-interest income of the Bank.9% increase in the number of corporatecustomers.

Lending Partnerships

Credit Libanais is engaged in partnership pro-grams with major international bodies such as:

The Export Development Canada (EDC)program, dedicated to financing andpromoting Canadian exports toLebanon;The European Investment Bank (EIB),offering eligible Lebanese firms competitive financing for industrial andtourist projects;The Arab Trade Financing Program (ATFP)promoting the export of goods of Arab origin;The Inter Arab Investment GuaranteeCorporation (IAIGC) which facilitatestrade amongst Arab countries by providing insurance guarantees forinvestment and trade;The Islamic Corporation for Insurance ofInvestment and Export Credit (ICIIEC)which, in affiliation with the Islamic Bank,guarantees exports from Islamic countries worldwide;The Saudi Fund for Development (SFD),destined to finance the trade of SaudiArabian goods and services byLebanese importers;The Cooperative Housing and Finance(CHF/USAID), which subsidizes themicro finance scheme, Ameen. Theprogram is geared towards a specificsegment of very small enterprises whichoften encounter difficulties in financing theirprojects through Lebanese banks; andThe Council for Development andReconstruction (CDR) acting for the benefit of the Economic and Social FundDevelopment (ESFD) whose aim is toalleviate poverty and mitigate the socialimpact of the economic transition on disadvantaged groups.

Several Murabaha deals were also undertakenin collaboration with major regional players inthe Islamic Banking Industry.

Credit Libanais GroupAnnual Report 2005 17

Core Banking Activity

•

•

•

•

•

•

•

•

•

•

•

Breakdown of Corporate Portfolioby Economic Sector

Commerce52.2%

Industry24.9%

Real Estate3.5%

Services18%

Agriculture0.4%

Commerce 52.2%Industry 24.9%Services 18%Real Estate 3.5%Agriculture 0.4%

Envisaged developmentsand growth in neighboring

countries produce promisingbusiness opportunities thatCredit Libanais is ready to

seize in order to extend ourfootprint regionally

Credit Libanais Group Annual Report 200518

Financial and Capital Markets

Credit Libanais’ expertise and tradingcapabilities positioned the Bank as one ofthe main players in Lebanon. During the year2005, we organized our activities with an aimto improve our coverage capabilities andbetter meet our customer expectations andneeds. Our strategy centered on revenuegrowth opportunities in order to optimizereturns while efficiently managing marketrisks.

In addition, Credit Libanais is a lead providerof sales, trading and market making servicesin every type of financial instruments includingfixed income, equities, foreign exchange andstructured products.

Our teams are formed of smart people whoaim at generating innovative solutions basedon our Bank’s values such as team spirit,respect, confidentiality, innovation and premiumquality service.

Our product offer includes:Liquidity management, money marketinstruments, foreign exchange andderivatives;Sovereign and corporate securitiesranging from high grade to high yield; Emerging markets investments, collater-alized debt obligations, securitizedobligations, equities and equity-linkedproducts;

Our objective is to structure financial solutions andoffer Capital Markets access to our customerscoupled with a continuous strive to deliver best-in-class products, services and transaction executions.

•

••

In September, Credit Libanais successfullyissued USD 60 million in Certificates ofDeposit (CD) as part of a USD 150 millionprogram which has been co-lead and managedby Deutsche Bank. The CDs have a maturityof 3 years with a fixed coupon of 6.875%.The issue was three times oversubscribeddenoting an aggressive sales and distributionstrategy.

On equity markets, we have experienced during 2005 a good improvement in the activity marked by a diversification in terms ofgeographical coverage and innovation inequity-linked structured products. Last quarterof this year witnessed a strong evolution inthe performance of the Beirut StockExchange where Credit Libanais continuedto strengthen its presence and marketshare.

By combining our fixed income, equities andforeign exchange trading capabilities, CreditLibanais offers efficiency in terms of executionand processing of transactions, allowing asmooth flow from execution to settlement.

Structured products with fixed incomeand equity underlying;Islamic banking products; andFinancing services including securitieslending and custody services.

Fixed Income Activity

Credit Libanais boosted its activities oninternational debt markets and reinforced itspresence as a major player on the LebaneseEurobonds market which translated into asignificant increase in trading volumes andmarket share. Our fixed income team offersall types of instruments ranging from highinvestment grade to yield tailored to meetthe particular investment strategy of ourcustomers.

The Bank actively participated in all the newissues of the Republic of Lebanon andcontributed to the development of a more liquidand efficient secondary market.

Credit Libanais GroupAnnual Report 2005 19

Core Banking Activity

We are committed to providing solutions based

on innovation and value generation while

balancing customer needsand risk tolerance

•••

Credit Libanais Group Annual Report 200520

Private Banking and AssetManagement

At Credit Libanais, customer satisfaction iskey to our success. We have segmented ourPrivate Banking offer according to customerwealth and the level of risk tolerance.

Moreover, our products are based on an openarchitecture model enabling us to provideclients the best available products in anapproach geared to deliver the highestpossible returns.

Our objective and investment strategies havebeen focused on maximizing returns in linewith the requirements of our sophisticatedcustomers: we maintained a controlled riskprofile and adhered to high quality compliance and investments standards andpractices.

Existing synergies between different depart-ments of the Bank have been exploited withan aim to reinforce product development anddistribution capabilities. Our Private Bankingservices focus on:

Portfolio structuring and asset allocation;Development of large variety of structuredproducts and alternative investmentsenabling clients to seize attractive marketopportunities; andDevelopment of secure online platformsto enable customers to follow theiractivities, account movements and toexecute online transactions.

Our strategy centers onrevenue growth opportu-

nities in order to maximizereturns while efficientlymanaging market risks

••

•

80

70

60

50

40

30

20

10

02004 2005

19.8%

61.2%

Non-Interest Income Driven fromTreasury and Capital Markets

Safekeeping of all types of financialinstruments.

Credit Libanais’ Asset Management closelycooperates with renowned third parties inorder to offer clients flexible and attractivealternatives to traditional investments based on innovative financial engineeringtechniques.

One area of important growth during 2005was structured products which tie derivativesto investments depending on the respectiveunderlying, with the possibility of offering ourcustomers specific benefits such as capitalprotection or a guaranteed minimum rate ofreturn.

Alternative investments represent anothergrowing area in Private Banking. The mostimportant feature of these assets lies in theirlow correlation with traditional markets suchas equities or bonds. Alternative investmentsinclude instruments such as hedge, privateequity and real estate funds. These productsrepresent attractive opportunities whenmarket conditions lack clear trends anddirections.

Credit Libanais Private Banking team coversall major international, regional as well asdomestic markets, offering a diverse range ofinvestment opportunities monitored byprofessionals each within his area of expertise.Our team is supported by an in-houseResearch Unit that helps enhancing ourinvestment capabilities through a combinationof global information sharing and local decision making.

We offer a broad spectrum of Private Bankinginstruments ranging from conventional savingproducts to sophisticated financial instruments,including:

Equities, fixed income and foreignexchange;Money markets;Multi-assets class funds;Alternative investments and hedgefunds;Structured products with various underlying instruments;Capital guaranteed products;Shariaa compliant investments;Brokerage services; and

Credit Libanais GroupAnnual Report 2005 21

Core Banking Activity

••••••••

80

70

60

50

40

30

20

10

02004 2005

30%39.8%

Financial Instruments UnderCustody

•

Credit Libanais Group Annual Report 200522

Investment Banking

Activity

Amidst a difficult economic environment,Credit Libanais Investment Bank SAL was ableto achieve the goals set by SeniorManagement for 2005. During this year,CLIB managed to complement the broadrange of products and services offered by theGroup’s subsidiaries through delivering long-term financial products and advisory services.

Credit Libanais Investment Bank SAL, the Group’s medium and long-term investment arm, wasincorporated in 1996 and is 99.83 percent owned by Credit Libanais. The investment bankextends its services to a wide range of medium and long-term investment and commerical bankingactivities, according to legislative decree number 50 and dated July 1983. CLIB and its Corporateand Project Finance Department are well-equipped to offer a full range of tailor-made financialservices and solutions to private and institutional clients, locally, regionally and internationally.

Commercial Banking ActivityCLIB developed a strategy centered aroundcompetitive pricing and fast service - approvalof housing loans was given in 24 hours, whilethe loan disbursement period did not exceed 35days. The result of this strategy contributed inmaintaining high market shares and stablegrowth.

Credit Libanais Investment Bank and its Corporateand Project Finance Department actively pursuednew business opportunities during 2005 throughoutthe Arab World, particularly in Syria and Yemen.

Corporate and Project Finance

CLIB strives to assist the Middle Easternbusiness community in undertaking soundfinancial decisions through the application of modern finance principles and methodologies.

Our objective is to maximize financial andstrategic opportunities in a collaborative effortwith customers. We focus on meeting theunique corporate finance needs for small,medium and large national and multinationalcompanies.

Through its high caliber team and broadnetwork of connections, the Corporate andProject Finance Department at CLIB is well-equipped to offer a full range of tailor-madefinancial based solutions to private andinstitutional clients, locally, regionally andinternationally, specifically in the followingareas:

Commercial loans increased by 10% - with a6% growth in the number of commercial files.Customer deposits at CLIB improved by 8.44%in 2005, 42% of which is denominated in foreigncurrency. Loans to deposits ratio reached18.41% in 2005 compared to 15.86% in 2004.

Investment Banking ActivityMoreover, our lending portfolio comprisessyndicated loans, project finance, tradefinance, subsidized loans, and financing ofclients’ capital expenditure.

During 2005, CLIB investment portfolio grewby 18.75% to include additional PreferredShares, Certificate of Deposits, asset-backedsecurities and Eurobonds.

Our financial services and solutions include:Loans to the industrial, tourism andagricultural sectors, subsidized by theCentral Bank of Lebanon; andOther long-term loans for hospitals,department stores, real estate development projects and housing loansfor individuals.

Credit Libanais GroupAnnual Report 2005 23

Core Banking Activity

•

•21

18

15

12

9

6

3

0

15.86%

18.41%

2004 2005

Loan to Deposit Ratio at CLIB

The foremost positions weenjoy in our various

activities and our provenfinancial strength pave the

way for a new regionalexpansion strategy

Financial advisory services: advising onand structuring financial solutionsdesigned to meet the strategic andorganizational needs of institutionalcustomers. This includes financialassistance to clients in need for:

1. Evaluating the financial performanceof their business;2. Assessing the viability of anexpansion/investment alternative;3. Seeking financialreengineering/turnaround;

Credit Libanais Group Annual Report 200524

4. Opening their capital to prospectiveinvestors; and5. Mergers and acquisitions;

Strategic alliances and partneringtransactions;Debt and equity placements: advisingclients to make an informed decisionregarding the appropriate capital structure.Locating sources of finance, negotiatingand representing the company mostfavorably;Mergers and acquisitions: offering compre-hensive assistance to clients seeking tomerge with or acquire other private orpublic business units. CLIB will getinvolved in every step of the transactionincluding the:

1. Preparation of the sale;2. Determination of the strategy;

3. Company valuation;4. Research analysis;5. Determination of the best

financing structure;6. Negotiation of the contract; and7. Due diligence process;

Recapitalization and strategic advisory:structuring and arranging financing forrecapitalizations allowing a company’sshareholders to achieve significant liquidity,while positioning the company more favor-ably for continued growth and success.

AchievementsThe Corporate Finance and Advisory Unitactively pursued business opportunities in thebanking sector, particularly in the Arab World,including Lebanon, Syria, Republic of Iraq,and Yemen.

•

•

•

•

175

150

125

100

75

50

25

0

168

2004 2005

142

Total Loans at CLIB (billion LBP)

Throughout 2005, this Unit embarked in abroader market coverage to include news onthe local, regional and international financialmarkets on a consistent basis. This wassupplemented with the creation of an exten-sive database, in collaboration with theBank’s Customer Service Center, in anendeavor to broaden the network of recipients,and hence, share the Unit’s Weekly Marketcommentary with a larger community.

Research UnitThe Economic Research Unit provides theGroup’s customers as well as the Lebaneseand Arab community with a broad exposureto weekly economic and financial markethighlights.

To gain further international exposure, theUnit reached an agreement to publish itsweekly report with international news serviceproviders and providers of online financialinformation to financial institutions in the Arabregion. This has served to draw the attentionof some international analysts/investors, whileat the same time raising the Bank’s corporateimage among local and internationalinvestors.

Additionally, the Research Unit played amajor role in 2005 in helping the Group reachsound financial decisions on an internationalinvestment scale. This was achieved throughthe preparation of detailed sectoral, bankingand economic analysis of countries in theMiddle East and North Africa.

Credit Libanais GroupAnnual Report 2005 25

Core Banking Activity

1,000

800

600

400

200

0

916

2004 2005

899

Total Deposits at CLIB (billion LBP)

Our strategy coupled withswift but vigorous daily

fine-tunings of our operations allowed us toquickly respond to local

and regional developments

Credit Libanais d’Assurances et de Reassurances (CLA) SAL, the Group’s insurance arm, wasincorporated in 1993 and is 66.97% owned by Credit Libanais Investment Bank SAL (CLIB) and33% by Agence Generale de Courtage d’Assurance SAL (AGCA). The Company is engaged in alltypes of insurance and reinsurance operations, in Lebanon and overseas.

Marine Motor Fire Casuality Life Total

100

90

80

70

60

50

40

30

20

10

0

60.57%

98.87%

55.86%

76.43%

3.42%8.05%

72.22%

81.41%

23.42%21.46%

39.17%43.76%

Loss Ratios

Year 2004 Year 2005

Credit Libanais Group Annual Report 200526

Bancassurance

A Year in Review

The Lebanese insurance industry recordedan 8.81% increase in premiums written in2005 compared to a 10.93% increase in 2004,mainly due to the economic and politicalsituation prevailing in the country.

CLA succeeded, once more, to achieve anoutstanding performance reflected in theconsiderable growth in premiums in all

branches of the insurance business.Another measure of growth is evident in theincrease of total assets and shareholders’equity.

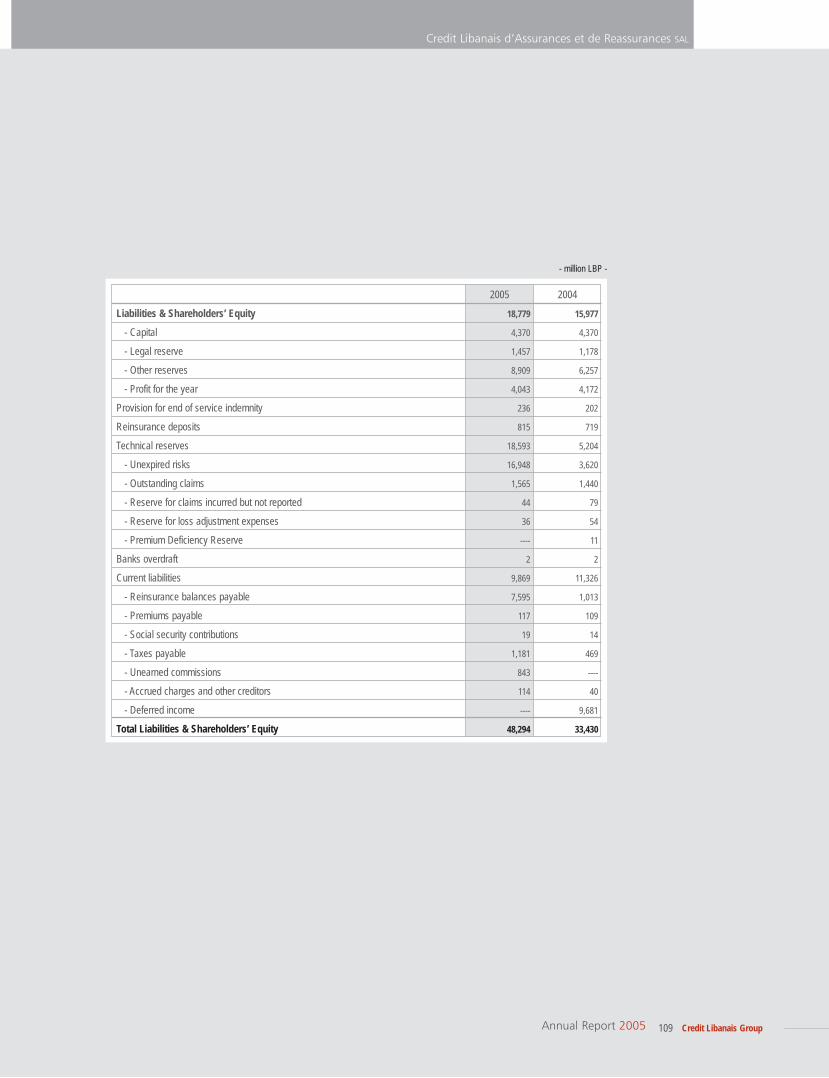

Total assets increased by 44.46% reachingLBP 48,294 million in 2005 from LBP 33,430million in 2004. This growth is attributed to asignificant increase in the volume of businesswhere gross written premiums reached LBP18,546 million in 2005.

Credit Libanais d’Assurances et de Réassurances(CLA) recorded a leap of more than 13 places withinthe Lebanese insurance industry despite its youngage due to a considerable growth in premiums.

Marine Motor Fire Casuality Life

3500

3000

2500

2000

1500

1000

500

0

1979

1480

128 165552507

3,617

3,235

999962

Premium Development per Class ofBusiness (million LBP)

Year 2004 Year 2005

Our sustainable profitabilityis mainly due to efficient

management combinedwith inherent synergies

among Group’s subsidiaries

The sound performance of CLA is evidencedin the increase in shareholders’ equity fromLBP 15,976 million in 2004 to LBP 18,779million in 2005 - an annual growth of 17.55%due retention of earnings. According to saidmagazine, CLA was ranked ninth in 2004 interms of shareholders’ equity nationwide.

Performance by Class of Business

CLA recorded in 2005 a considerable growth innet premiums. Non-life business has increasedby 20.08% while the average growth in theindustry stood at 7.4%. Ranking seventeenthin 2005 among more than 50 insurancecompanies nationwide, CLA has jumpedmore than 13 places.

The slight decrease in net profits from LBP4,171 million in 2004 to LBP 4,042 million in2005 is mainly attributed to both a new taxintroduced on premiums and a general declin-ing interest rate environment which led to a22% decrease in yields on liquidity placements of the Company.

Yet, a part of this increase is attributed tosingle premium policies contracted to covercar loans and housing loans financed throughbanks over the medium- or long-term. Thetotal volume of single premium policiesamounted to LBP 11,235 million representing60% of gross premiums written in 2005mainly in the motor, fire and life businesses.

Due to a change in the accounting treatmentenforced by the Ministry of Economy andTrade, single premium volume increasedsubstantially during 2005 to include premiumsrelating to subsequent periods extending after2005, which were differed under reserve inthe balance sheet and are not reflected in theincome statement of this year.

During 2005, CLA ranked fourth nationwide interms of profits for 2004 based on after-taxfigures and ranked first between Lebaneseinsurance companies owned by banksaccording to a study prepared by Al BayanMagazine (December 2005 issue) coveringtop 150 insurance companies operating in theArab World.

Credit Libanais GroupAnnual Report 2005 27

Core Banking Activity

Credit Libanais Group Annual Report 200528

MotorThe motor line of business achieved a substantial increase in net premiums during theyear under review from LBP 1,480 million in2004 to LBP 1,979 million in 2005 - an increaseof 33.71% (excluding single premium policies)attributed to policies issued for car loansfinanced by banks. Single premium policiesgenerated a premium income amounting to LBP2,147 million in 2005 and representing 52% ofthe premiums generated by this line of business.

The loss ratio for the motor class of businessis 76.43% compared to 55.86% in 2004 andto a 65% industry average.

MarineAn increase in net premiums generated hasalso been realized under the marine businessfrom LBP 128 million in 2004 to LBP 165 millionin 2005. This increase was mainly attributed tothe positive efforts of the Company MarketingTeam to acquire new and profitable businesses.

Despite this increase in net premiums, CLAmaintained an adequate risk assessmentstrategy. This strategy led to a decrease inthe loss ratio to 60.57% in 2005 from98.87% in 2004 in line with industry averageproving that the marine business acquired

during 2005 affected positively the loss ratioof this line of business.

FireIn 2005, CLA achieved a considerable growthin the net premiums generated under the firebusiness class. Premium income totaled LBP552 million, well above the LBP 507 millionachieved last year. This 8.87% increase ismainly due to fire policies issued during 2005for housing loans. In addition, single premiumpolicies issued in 2005 amounted to LBP 2,215million which represents 80% of the total fire busi-ness generated during the year. This businessis mainly generated through long-term policies.

The increase in premiums did not negativelyaffect the loss ratio which recorded a

6,000

5,000

4,000

3,000

2,000

1,000

0

4,879

1,667

3,631

1,573 1,645

3,487

2003 2004 2005

1,464

5,204 5,132

Technical Reserves (million LBP)

Unexpired RisksOutstanding ClaimsTotal Reserves

Credit Libanais GroupAnnual Report 2005 29

Core Banking Activity

housing and car loans granted by banks overthe medium- and long-term.

The loss ratio for this line of business is23.42% a slight increase over 21.46% recorded in the year 2004 and below a 25%industry average.

CasualtyCasualty business premium income generated for year 2005 amounted to LBP998 million as compared to LBP 962 million in2004, an increase of 3.74%. The branches ofthe insurance business falling under thecasualty class are mainly hospitalization, workmen compensation, personal accident,theft on property.

The increase in net premiums is attributed tothe development of insurance products inbanking such as credit card business andBankers Blanket Bond (BBB) coverage.

Technical ReservesAt the end of 2005, a decrease in the unexpiredrisk reserves has been recorded to reachLBP 3,487 million in 2005 compared to LBP3,631 million in 2004. This decrease is due tothe fact that no premium deficiency reserveswere accounted for in 2005.

An increase in outstanding claims reserveswas calculated due to an increase in the lossratio under the motor business line. Therefore,the outstanding claims amounted to LBP 1,645million in 2005 compared to LBP 1,573 millionin the previous year, thus recording an increaseof 4.57% in outstanding claim reserves.

As a result, CLA recorded LBP 5,132 millionin total reserves for year 2005 compared toLBP 5,204 million in 2004, a slight decreaseof 1.40%.

decrease to reach 3.42% in 2005 down from8.05% in 2004 and compared to a 20%industry average.

LifeThe line of business witnessed a considerabledevelopment with respect to net premiumsgenerated for the year under review. Incomeunder the life business totaled LBP 3,617million as compared to LBP 3,235 million lastyear, an annual increase of 11,77% (excludingsingle premium policies). Single premiumpolicies were main contributors to an evenhigher increase in premiums recorded duringyear 2005 and representing 65.50% of thetotal business generated for the year andamounting to LBP 6,872 million. These singlepremium policies were issued in relation to

56.56%

0.89%

5.38%

22.25%

14.92%

Premium Breakdown into Classesof Business (million LBP)

LifeMarineMotorFireCasuality

Sustainable Development

Credit Libanais GroupAnnual Report 2005 31

Sound Growth, Long-term32 External Development34 Internal Development38 Customer Focus

40 Risk Management and Internal Audit44 Anti-Money Laundering45 Investing in Human Capital

Credit Libanais Group Annual Report 200532

External Sustainable Development

Social RoleWe are cognizant of our community role asbeing part of the way we live, work, and dobusiness every day. By being present in vitalareas such as education, arts and culture, wereinforce and confirm our civic role for theadvancement of the society we live in.

Macroeconomic RoleWe judge that our role as a financial institutiongoes beyond compliance with existing regu-lations. Therefore, we strongly believe thatthe health and solidity of the financial sectorare essential for the economic and socialdevelopment of Lebanon especially in this

Externally, our Sustainable Development Strategy is embodied in our social and economic roles. This section is dedicated to all those external banking and parabanking activities that are essential to our ongoing development in the current competitive markets.

critical period of history of our country. OurBank has been a major contributor in financingthe government in its reconstructions andinfrastructure plans. Through our investmentarm, Credit Libanais Investment Bank, wehave participated, co-managed and co-ledmost of the Lebanese sovereign issues. Thisis clear evidence that the Lebanese bankingsector is the backbone of the Lebaneseeconomy and closely tied to it.

Microeconomic roleAnother important role as a financial institutionis to offer basic financial services, providefinancial support to microfinance institutions

Although our motto ‘Close to You’ is targetedto our stakeholders, our SustainableDevelopment Strategy lays on the foundationof establishing a relationship of trust betweenall our economic players.

our strong visibility within the Lebanesebanking sector. On the other hand, the qualityof our engagement to our stakeholders is thecornerstone of our credibility. We, therefore,attach a special attention to our people andcustomers and constantly gauge their satisfaction.

CommunicationBy listening and promptly responding to allour stakeholders, we build a strong platformfor the future in line with our SustainableDevelopment Strategy. Exchange and dialogue are the cornerstones of growth andachievement. Since its implementation, theexternal feedback inbox brings customer recommendations and complaints to the forefront of our attention.

and help to limit overindebtness. In addition,our Bank is a pioneer in offering micro-financing. This function is in line with ourlong-term belief that micro-enterprises, likemultinationals, are essential to the prosperityand development of our economy. Ameen, ourmicro-finance product, is geared towards aspecific segment of very small enterpriseswhich encounter difficulties in financing theirproducts through Lebanese Banks. Anothermicro-finance program is geared towards verysmall and small enterprises with an aim toalleviate poverty and mitigate the social impactof the economic transition on disadvantagedgroups.

CultureOur commitment to sustainable developmentis reflected in our corporate values - Visionand Business Principles - that are reassertedyear after year to finally become the basis ofour culture. These values are embodied inour day to day activity with our customers andare our driving force and competitive edge.

Reputation Finally, Credit Libanais attaches a specialimportance to intangible areas of sustainablegrowth such as reputation. In evaluating ourcurrent positioning relative to competition, welook at our visibility and our credibility asbeing the basic components of our reputation.On the one hand, our social and economicroles coupled with our leading positions inselected markets such as e-banking confirm

Credit Libanais GroupAnnual Report 2005 33

Sustainable Development

Our Group harness growthby combining strong

performance with a proven commitment to

the communites in whichwe operate

Internal Sustainable Development

We aim at complementing the salesefforts of our Branches by establishingnew business units to meet the needs ofour customers. Our goal over the medium-term is to increase the mix of staff assignedto sales programs throughout the bank.

Below, we detail the methodology used toachieve our objective:

Leadership and Staff Development During the course of its assignment, POUwork closely with Department and BranchManagement to ensure that all assignedresources have the required knowledgeand skills to successfully perform theirresponsibilities and receive the neededleadership and guidance to succeed.

Work Station Operating Efficiency The Planning and Organization Teamprepares a comprehensive study for eachemployee and work unit to determine if

various ‘Time Management’ tools are usedefficiently in order to enhance productivity.The effective use of Intranet, voice mail, andelectronic archiving are just a few examplesof modern and efficient use of resources.

Work Schedule Most renowned financial institutions workaround the clock to serve their customersand improve operating efficiency. When weapplied this philosophy to our local envi-ronment, we created work shift schedulesto rapidly serve customers and reduceovertime and other operating expenses.

Measurable Performance Results Our employees embrace the reward for per-formance culture introduced several yearsago. The Planning and Organization Teamhelps Department Managers measure theproductivity of each employee so that salaryincreases, bonuses and promotional oppor-tunities are consistent with measurable results.

Planning and Organization Unit

During 2005, the Bank formed a strategictask force called the Planning andOrganization Unit (POU) in an effort toimprove operating efficiency. The Unitconsists of Senior Management who lead ateam of in-house consultants and workclosely with the Operations Division.POU’s strategy is to review the operatingperformance of selected Head OfficeDepartments and/or Branches and recommend structural changes to enhancerevenue generation and cost efficiency.

The key objective of POU is to reduceexpenses by improving efficiency of ourcost centers in view of reallocatingresources to other profit centers. Thisobjective is achieved through compre-hensive reviews of the existing operationof these cost centers and the generationof structural recommendations.

Internally, our Sustainable Development Strategy involves all banking andparabanking activities most essential to the long-lasting prosperity and organic growthof our Bank.

Credit Libanais Group Annual Report 200534

Sustainable Development

with an aim to track the processes ofcustomer transactions throughout theBank. The new system transformed theway we do business and contributed tothe enhancement of several procedures.The System tracks a transaction from themoment it leaves its originator until itreturns back to him/her. Exception reportsenable management to pinpoint at exactlywhich level a transaction is still pending.The System raises red flags every time abottleneck is encountered so that manage-ment can actively intervene to solve theproblem before its reaches the customer.

Another benefit of the System is that itautomated mail registration enabling variousparties to track and monitor their internalcorrespondence online.

Effective Quality ManagementSystem ISO 9001-2000

Credit Libanais Quality ManagementSystem (QMS) provides a framework forcontinual improvement of processes andoperations by stimulating the Bank’soperational efficiency and effectivenessthus meeting and/or exceeding customerexpectations by:

Improving business planning throughmeasurable Quality Objectives setfor Branches and Head OfficeDepartments;Greater quality awareness throughour Quality Policy, Quality Manual,Quality Procedures, and Internal andExternal Quality Audits;Improved communication through theinvolvement of Staff in the QMSprocess and by providing trainingand workshops;Reduced costs of non-quality by:

Taking the necessary action toreduce the occurrence of majorerrors or problems affecting thequality of our serviceBringing to the attention of SeniorManagement, common errors andproblems that impact customerservice or department/branch effi-ciency through the control of non-conforming products and services;Evaluating periodically our suppliersand service providers; andBuilding good habits in controllingdocuments and records;

Greater control of processes andactivities throughout the organizationby planning and conducting InternalQuality Audits, to verify whether theQMS implemented at Credit Libanaisis in compliance with the requirementsof ISO 9001:2000; andHigher Customer Satisfaction:

Through our ‘CustomerComplaints Management FollowUp System’;Through the establishment of‘Timeliness Standards’ in branchesto measure the execution ofimportant transactions. Thesestandards include the time it takesfor a customer to make a depositor withdraw funds from theiraccount. We track results andidentify corrective action whereneeded.

When our employees know how to win, theybecome highly motivated and recognizeCredit Libanais as an ‘Employer of Choice’.

Internal Communication Regular weekly and monthly staff meetingskeep employees informed on departmentand branch performance. Each employeeshould know what is expected from him/herand how he/she can grow professionallythrough continuous improvement in order tocreate job satisfaction and improve staffmorale. POU Team ensures that suchmeetings are embedded in the culture ofevery department and unit.

Error Tracking When we do things right the first time weshow pride in our work, we improve customerservice, and we avoid needless phone callsto correct mistakes. This makes life easierfor both our employees and our customers.By installing ‘Error Tracking Systems’ wehelp measure performance, upgrade train-ing wherever needed and enhance systemsand procedures to reduce common errors.

Core Competencies Another important checkpoint for thePlanning and Organization Team is tomake sure that each department hascompetent and properly trained staff toeffectively perform duties and responsi-bilities. This includes validating that workassignments are consistent with the skillsof assigned resources and proper segregation of duties is enforced bydepartment management at all times.

Mail and Tracking System

‘Mail and Tracking System’ is a manage-ment tool conceived and built in-house

•

••

•

•

•

-

-

-

-

-

-

Credit Libanais GroupAnnual Report 2005 35

Credit Libanais Group Annual Report 200536

Customer Focus

Customer care is at the heart of ourSustainable Development Strategy. 2005was the year in which we reaped the fruitof a key investment to give a major boostto customer satisfaction. It was the yearof the final implementation of ourCustomer Relationship Management(CRM) System. As of this year, our Bankwill utilize all the component of thisstrategic tool such as customer behavior,percentile analysis, product affinity as wellas communication in one direction: meetingor exceeding customer expectations.

Customer RelationshipManagement

CRM is a solution that gathers all bankinteractions with customers, analyses them,delivers them, integrates and uses them toprovide a single view of the customer from

all aspects of the business. It is, as well, abusiness strategy that selects and managesthe most valuable customer relationships.It requires a customer centric businessphilosophy and culture to support effectivemarketing, sales, and customer service.

Credit Libanais has chosen the TeradataCRM framework that consists of six logicalgrouping of product which is designedand positioned, as follow:

Analysis: analyze what business istranspiring from customer;Modeling: predict customer behaviorespecially as it pertains to customerresponses to communications andcampaigns;Communication: develop plans forcommunicating with customers andthen managing those plans;Personalization: personalize the communications down to the individualcustomer level;Optimization: optimize customercommunication by managing the frequency and number of customercommunication channels; andInteractive: deliver outbound commu-nications, respond to a customercontact with the next communicationand capture the results of all commu-nications for later analysis.

Our CRM analysis module provides ourMarketing Team with powerful tools toanalyze and understand customers and tovisualize the significant events that drivecustomer interaction with the Bank.Following is a list of the powerful functionsof the CRM module:

Define, analyze and target segmentsby behavior, demographics, location,product usage and affinities, rankingsand transactions over time;Build queries easily with graphical

••

•

•

•

•

•

•

Starting 2005, all the components of thestrategic Customer Relationship Management(CRM) tool will focus on meeting and/orexceeding customer expectations.

Credit Libanais GroupAnnual Report 2005 37

Sustainable Development

The communication with a targetedcustomer is done through an applicationthat will reside on the agent desktops andwill enable the:

Retrieval of customer profile;Registration of the complaints madeby customers;Response to complaints made bycustomers; andFollow up on campaigns made by CRM.

Customer Service Center

Our strong belief that customers are entitledfor excellent service is the raison d’être ofour Customer Service Center (CSC). Ahealthy team of young, dynamic profes-sionals are on the phone every day toassist our customers. They are trained toconvey messages of care in order to transmitpositive vibes which will automatically betranslated on the phone to our customers.

CSC handles customer calls, by monitoringthe performance of every call to ensurethe highest quality and professionalism.Hence, CSC Agents are trained on thebest industry practices in view of maintainingor improving the quality of our service.

During 2005, CSC was transformed froma cost center into a profit-generating unitcovering the cost of delivering superiorquality service from the direct sales activityof its Agents.

In addition, CSC collaborated with E-banking Department to revamp CreditLibanais website according to the latesttechnological developments. Our newwebsite, built in an integrated and scalableplatform, contains extensive and up-to-dateinformation about our products and services.

point and click interface, no SQL orpseudo SQL is needed;Analyze and evaluate customer groupsthrough a visual, ad hoc reporting inter-face and immediately include thesesegments in our marketing campaigns;Realize opportunities based on newlinks discovered between customersegments and attributes;Select and compare any two customersegments, campaigns, stores, catalogs, versions or offers;Paste or export all graphs andreports to windows application;Create a closed loop system by creating new customer segments forfuture marketing campaigns directlyfrom any of the analysis graphs;Define a new customer group bysimply highlighting any range or thegraph, which allows segments to becreated based on changes in behaviorover time;Capture new customer segment,freeze the segment and look atbehavioral changes before and aftertargeting. This powerful feature canbe used to evaluate the effectivenessof marketing actions applied onspecific segments; andCreate a demographic profile orpurchase profile for any customersegment displayed, which allows usto evaluate customer profiles andtheir correlation to customer behaviorand product spending.

Credit Libanais Group website received inearly 2006 the Golden Pan Arab WebAward under the Banks and FinancialInstitutions Category confirming ourleadership in e-banking technology.

Customer Care Unit

Credit Libanais strongly believes thatcustomer complaints are a very valuablesource of feedback. When they are handledproperly, our most dissatisfied customerscould be transformed into our bestambassadors. Our experience hasproven that attentive and reasonableresponse to customer complaints buildscustomer loyalty. Our Customer CareUnit is in the business of handling thosecomplaints and channels them, whenevernecessary, to Senior Management.

Ongoing Monitoring andEvaluation

Since customer satisfaction is one ofCredit Libanais’ most sought afterBusiness Principles, the MarketingDepartment regularly inspects the qualityof our customer service through mysteryshopper visits. This policy is applied to allCredit Libanais branches by means ofseveral waves per year depending on thequantitative or qualitative criterion underinspection. The aim of the mysteryshopper is to test employee productknowledge and sales skills in order toensure the quality of our service.

•

•

•

•

•

•

•

••••

CRM became fully operational allowing us

to profile our customersin order to better cater

to their changing needsand expectations

Credit Libanais Group Annual Report 200538

Risk Management and Internal Audit

Risk Management Function

The scope of work of the Risk ManagementDivision encompasses:

Ensuring the implementation of theBank’s strategy and policies on RiskManagement; Proactively pursuing the sound and pro-fessional implementation of strict,exhaustive and prudent RiskManagement practices in the years tocome, in line with the Basel II Accord,the Central Bank and the Banks ControlCommission requirements;

Risk Management has been for the past years an important element of Credit Libanais’ Managementphilosophy and Sustainable Development Strategy. Risk Management processes are designedalong the lines of the Central Bank of Lebanon and Banks Control Commission (BCC) directives. Itis an independent function reporting to the General Manager and the Board of Directors. RiskManagement oversees the analysis, identification, measurement, monitoring, reporting andcontrolling of risk throughout the Bank and application of Risk Management policies, guidelines andrules within principles set forth by Senior Management and approved by the Board of Directors.

Developing risk-focused policies and procedures in order to achieve the bestrisk/return ratio possible under differentmarket conditions and with the aim ofcreating and maximizing value forcustomers and enhancing return forshareholders; Maintaining an independent managementand control structure; Administrating and safeguarding docu-mentation pertaining to credit risk; and Creating a proper risk-awareness cultureamong employees, in order to achievethe goal of adequate risk recognition andmanagement.

•

•••

•

•

The ultimate goal of our Risk Managementfunction is to safeguard assets by maintaining abalance between risks and rewards in agreementwith the Bank’s philosophy and strategies.

Credit Libanais GroupAnnual Report 2005 39

Sustainable Development

Operational Risk with an aim to adopt moreadvanced approaches once the systems willbe upgraded to accommodate that level.

Credit Risk Management

Credit Risk is the risk of loss due to an obligoror counterparty defaulting or failing to meetcontractual obligations. The Bank’s credit riskis managed at both the counterparty and port-folio levels. The Bank has designed its CreditRisk Management practices to preserve theindependence and integrity of the riskassessment process.

Credit Libanais manages the credit risk of itscommercial customers by:

Analyzing potential risks associated witheach borrower’s facilities or transactions; Requiring that the Risk ManagementDivision reviews and provides an independ-ent assessment of commercial credit risk; Ensuring that credit risk decisions areeffected through delegated committeesand based on the risk rating of theindividual counterparty; Regularly checking that the utilization iscompatible with the assigned limits andensuring that the related risks areeffectively managed; and Continually assessing the risk-adjustedprofitability of the facilities.

The Bank manages the credit risk of its consumer portfolio by relying on preset productguidelines for credit approval. These guide-lines determine the standard risk acceptancecriteria used to evaluate and approveindividual credit transactions. They also aimat ensuring that the authority to approveindividual credit transactions is independentfrom the business originators, but involves areview by the related Product Manager.

Basel II and Risk Management

The basic idea behind Basel II Accord isstrengthening the Risk Management functionand capabilities in financial institutions ratherthan just being another mathematical andcalculation exercise. Such a process neces-sitates building an adequate Risk Managementculture and framework with the purpose ofidentifying, measuring, monitoring andcontrolling risks that the Bank will be subjectedto in the course of daily business operations.