1 February 2016 Canadian SMID E&P Americas/Canada Equity ...

1

DISCLOSURE APPENDIX AT THE BACK OF THIS REPORT CONTAINS IMPORTANT DISCLOSURES, ANALYST CERTIFICATIONS, LEGAL ENTITY DISCLOSURE AND THE

STATUS OF NON-US ANALYSTS. US Disclosure: Credit Suisse does and seeks to do business with companies covered in its research reports. As a result, investors should

be aware that the Firm may have a conflict of interest that could affect the objectivity of this report. Investors should consider this report as only a single factor in making

their investment decision.

Credit Suisse Equity Research

Americas/United States

Global BioPharma Alzheimer’s Disease Call

October 19th, 2016

A Detailed Deep-dive into Alzheimer’s Disease, Key Players and Upcoming Data Readouts RESEARCH TEAM

Alethia Young

Research Analyst +1 212-538-0640 [email protected] Matthew Weston

Research Analyst +44 020-7888 -690 [email protected]

Vamil Divan, MD

Research Analyst +1 212-538-5394 [email protected]

Jo Walton

Research Analyst +44 020- 7888-0304 [email protected]

Fumiyoshi Sakai

Research Analyst +81-4550-9737 [email protected]

2

Outline for today’s call

Why is the amyloid hypothesis still under debate?

How we look at comparing the key late stage assets?

What are the lessons we have learned from prior AD studies?

How do we think about prior Sola studies and upcoming EXPEDITION3 readout?

How do we think Lilly and Merck trade around Sola Ph3 readout?

How do we think Biogen and AC Immune trade around Sola Phase 3 readout?

How do we think about potential impacts to Roche and other EU read-throughs?

Source: Company data, Credit Suisse estimates and analysis

3

Solanezumab Phase 3 Results Will Are a Big Catalyst for AD Space, With Topline Data Expected in 4Q16

LLY’s Solanezumab Phase 3 is reading out in Q4 2016. This data could provide more

confidence in the hypothesis which both ACIU and BIIB’s lead assets are developed around.

Our team did an extensive deep-dive analysis into the preclinical and clinical data behind each of

these AD assets and we believe the Phase 3 Lilly trial could be successful.

Source: Company data, Credit Suisse estimates and analysis

Company Drug Rating TP Analyst

Biogen Aducanumab Neutral $322 Alethia Young

AC Immune Crenezumab Outperform $18 Alethia Young

Roche Crenezumab Outperform SFr300 Matthew Weston

Eli Lilly Solanezumab Outperform $96 Vamil Divan

Merck Verubacestat Outperform $73 Vamil Divan

Eisai BAN2401 Neutral ¥5,900 Fumiyoshi Sakai

4

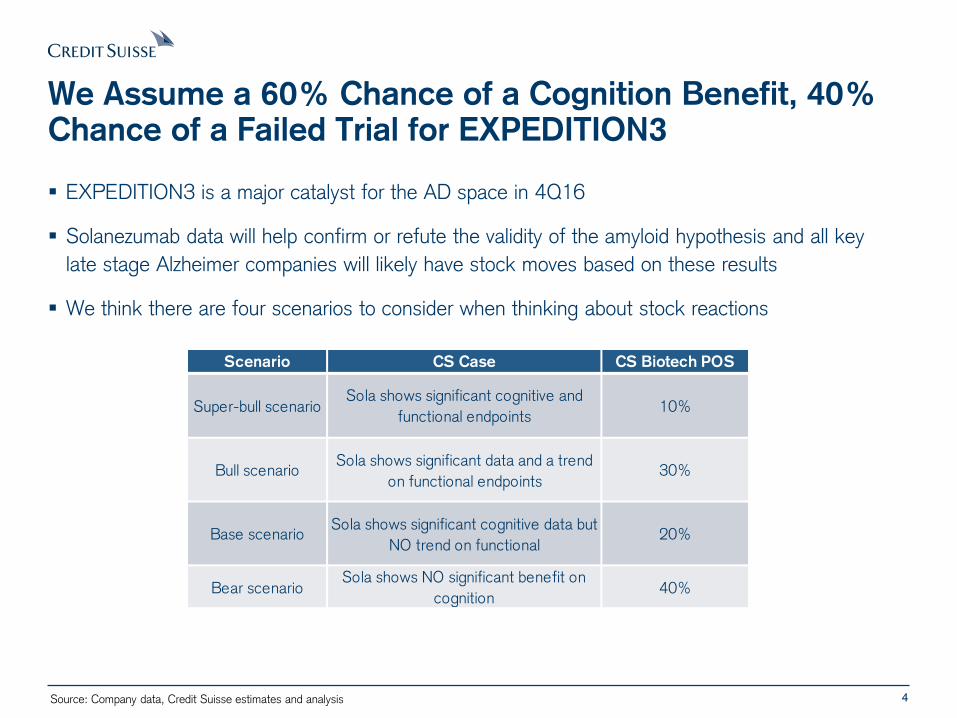

We Assume a 60% Chance of a Cognition Benefit, 40% Chance of a Failed Trial for EXPEDITION3

EXPEDITION3 is a major catalyst for the AD space in 4Q16

Solanezumab data will help confirm or refute the validity of the amyloid hypothesis and all key

late stage Alzheimer companies will likely have stock moves based on these results

We think there are four scenarios to consider when thinking about stock reactions

Scenario CS Case CS Biotech POS

Super-bull scenarioSola shows significant cognitive and

functional endpoints10%

Bull scenarioSola shows significant data and a trend

on functional endpoints30%

Base scenarioSola shows significant cognitive data but

NO trend on functional20%

Bear scenarioSola shows NO significant benefit on

cognition40%

Source: Company data, Credit Suisse estimates and analysis

5

Why is the amyloid hypothesis under debate?

Source: Company data, Credit Suisse estimates and analysis

6

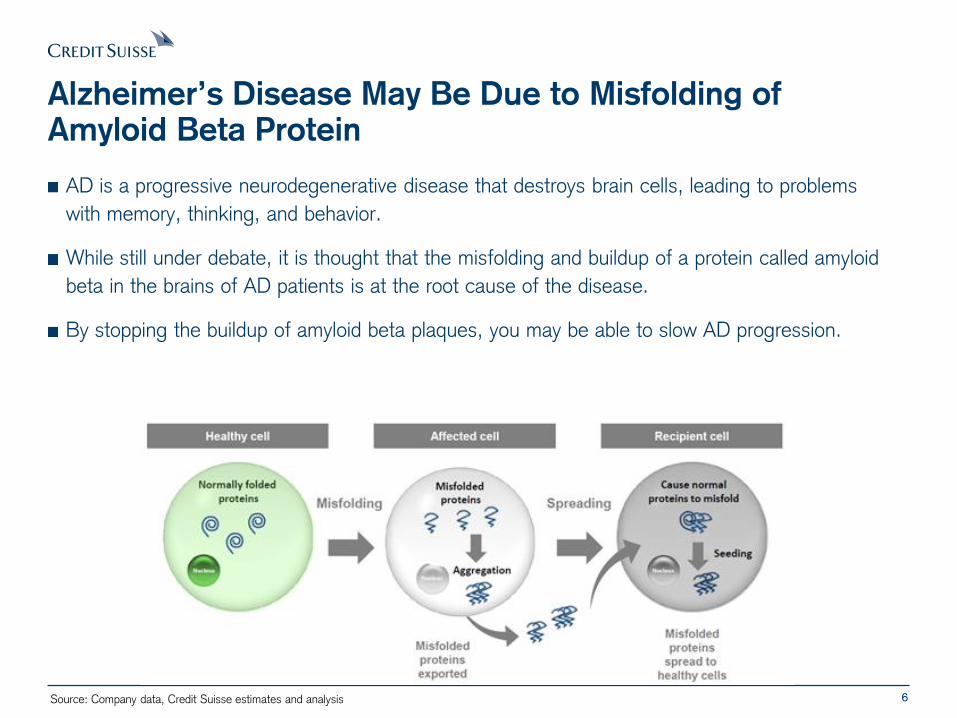

Alzheimer’s Disease May Be Due to Misfolding of Amyloid Beta Protein

AD is a progressive neurodegenerative disease that destroys brain cells, leading to problems

with memory, thinking, and behavior.

While still under debate, it is thought that the misfolding and buildup of a protein called amyloid

beta in the brains of AD patients is at the root cause of the disease.

By stopping the buildup of amyloid beta plaques, you may be able to slow AD progression.

Source: Company data, Credit Suisse estimates and analysis

7

Various Neurodegenerative Drug Targets for AD

BACE inhibitor – beta-secretase inhibitor: Beta secretase is an enzyme that cleaves the amyloid

precursor protein (APP). Beta amyloid is formed from the breakdown of the APP.

Inhibiting this enzyme is hypothesized to prevent the breakdown of the APP into amyloid beta peptides, thereby preventing the buildup of amyloid beta which is implicated in Alzheimer’s.

Amyloid beta inhibitor: Binds to beta amyloid fragments directly to prevent their accumulation into

plaques.

Tau inhibitor: Inhibits tau protein, another protein whose accumulation (in tangles) is associated with

AD pathology

Source: Company data, Credit Suisse estimates and analysis

8

Drug Targets Have Also Focused on Tau Protein; It Remains Unclear What Role of Tau May Be in the Clinic

Tau hypothesis of AD is tested in multiple anti-Tau assets. However, most are in the early

development stage compared to amyloid beta target

Misfolded hyperphosphorylated Tau forms tangles that are extremely insoluble and may

contribute to the neurodegenerative disease

Source: Company data, Credit Suisse estimates and analysis

Asset Lead company Type Phase Reference

AADvac1Axon

NeuroscienceVaccine Phase 2 NCT02579252

ACI-35 ACImmune/JNJ Vaccine Phase 1

RO7105705 ACImmune/Gen

entechAntibody Phase 1 NCT02820896

BMS-

986168

Bristol-Myers

SquibbAntibody Phase 1 NCT02294851

C2N-8E12 AbbVie Antibody Preclinical

Select Pipeline Products Targeting Tau

9

Key drugs in development: what data do we have about these assets so far? Solanezumab, Aducanumab, Crenezumab

Source: Company data, Credit Suisse estimates and analysis

10

Many of the Drugs in Development are Targeting Amyloid Beta

Lilly: lead amyloid beta asset in development, along with BACE inhibitor and others in earlier

development

Merck expected to have data next year on BACE program

Biogen: two amyloid betas and a BACE

Roche has two an amyloid beta asset as well: our sense is that crenezumab is the higher

priority asset but Roche may begin late-stage studies with gantenerumab again

Source: Company data, Credit Suisse estimates and analysis

Compound Company Stage Patients MOA

Solanezumab Lilly Phase 3 Mild Anti-Abeta antibody

Aducanumab Biogen Phase 3 Mild Anti-Abeta antibody

Crenezumab Roche/AC immune Phase 3 Mild and moderate Anti-Abeta antibody

Verubecestat Merck Phase 3 Prodromal BACE inhibitor

Verubecestat Merck Phase 3 Mild to moderate BACE inhibitor

Gantenerumab Roche Phase 3 Mild Anti-Abeta antibody

AC-1204 Accera Phase 2/3 Mild to moderate metabolic

AZD-3293 Astrazeneca/Lilly Phase 2/3 Mild BACE inhibitor

BAN2401 Eisai / Biogen Phase 2 Mild Anti-Abeta antibody

E2609 Eisai / Biogen Phase 2 Prodromal or Mild BACE inhibitor

MEDI1814 Astrazeneca Phase 1 Mild to moderate Anti-Abeta antibody

Select Anti-Amyloid Therapies in Development

11

Solanezumab Could be At Least 2 Years Ahead of Next Antibodies Making it to the Market

LLY’s Solanezumab Phase 3 is reading out in Q4 2016

Phase 3 designs are notably different

Solanezumab

(Expedition 3)

Aducanumab

(Engage and Emerge)

Crenezumab

(CREAD)

Estimated Enrollment 2,100 1,350 (each) 750

Began Enrolling August 2013 June/July 2015 January 2016

MMSE at Baseline 20-26 24-30 22+

Primary Endpoint/s ADAS-Cog14 CDR-SB CDR-SB

Dosing Length 80 Weeks 78 Weeks 105 Weeks

Doses Studied

400mg versus

placebo

IV every 4 weeks

Low dose vs. placebo

High dose vs. placebo

IV every 4 weeks

60mg vs. placebo

IV every 4 weeks

Expected data readout 4Q 2016 2019 2019

Source: Company data, Credit Suisse estimates and analysis

12

Quick Summary of Data Presented on Key Late-Stage Assets Under Coverage

Source: Company data, Credit Suisse estimates and analysis

Asset Company Main Dataset CS Comments

Solanezumab Eli LillyPhase 3 Expedition 1 & 2 Trials

(~2,000 patients)

Studies failed overall population (MMSE 16-26)

Cognitive and some functional benefits seen in mild patients

Crenezumab AC Immune/RochePhase 2 ABBY Study

(~250 patients at the 15mg/kg dose)

Study failed in overall population (MMSE 18-26)

Cognitive and some functional trends in mild patients

Minimal ARIA seen

Haven't yet seen data on the Phase 3 60mg/kg dose

Aducanumab Biogen

Phase 1B PRIME Study

(~32 and ~30 patients at the 6mg/kg

and 10mg/kg doses)

Study showed solid CDR-SB and MMSE benefits (MMSE 20-30)

Small population

Some ARIA-E concerns

BAN2401 Biogen/Eisai

18 month trial Baysean design that

can enroll up to 800 patients. Trial

primary endpoint will measure a

change in a composite cognitive

endpoint

Status: 750th patient enrolled around (~September 2016), and if

no early or success criteria met, again at 800th (~December), and

again if no early success or failure met, IAs at every 3 months until

completion of trial (12 months).

13

Solanezumab, Aducanumab and Crenezumab have All Shown Statistically Significant Benefit on Cognitive Endpoints in Mild Patients

ADAS-Cog14 (EXPEDITION3 primary endpoint) was significant in the pooled mild cohorts from

EXPEDITION 1/2

Crenezumab has also shown a statistically significant benefit on ADAS Cog12.

We have seen statistically significant differences on MMSE in Aducanumab and Solanezumab but

not Crenezumab

MMSE is primarily used for screening purposes vs. as a clinical measure

Source: Company data, Credit Suisse estimates and analysis

14

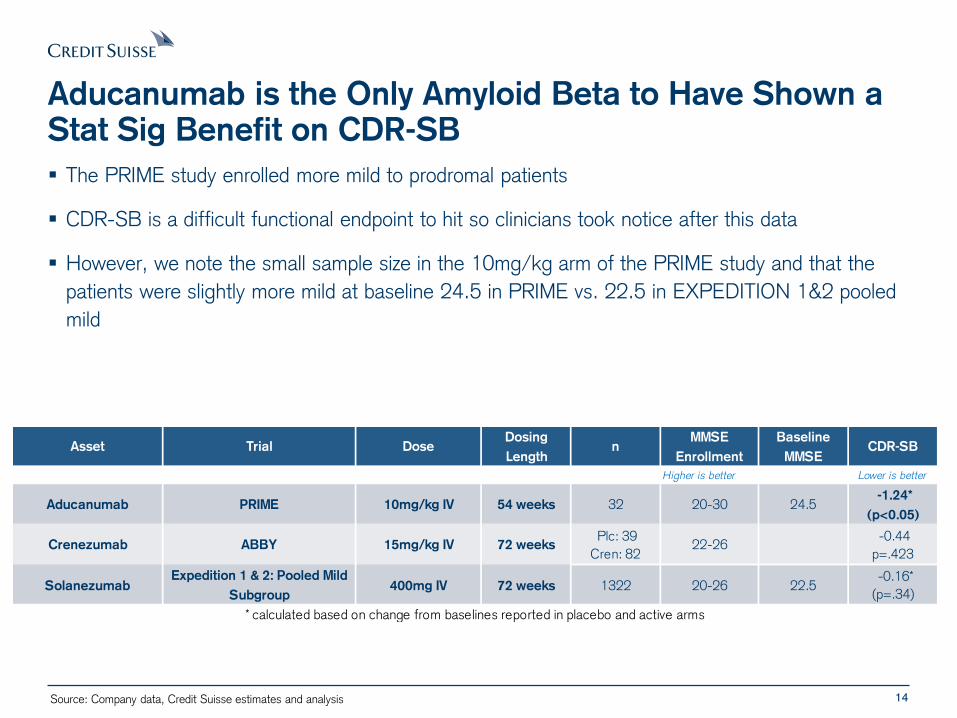

Aducanumab is the Only Amyloid Beta to Have Shown a Stat Sig Benefit on CDR-SB

The PRIME study enrolled more mild to prodromal patients

CDR-SB is a difficult functional endpoint to hit so clinicians took notice after this data

However, we note the small sample size in the 10mg/kg arm of the PRIME study and that the

patients were slightly more mild at baseline 24.5 in PRIME vs. 22.5 in EXPEDITION 1&2 pooled

mild

Asset Trial DoseDosing

Lengthn

MMSE

Enrollment

Baseline

MMSECDR-SB

Higher is better Lower is better

Aducanumab PRIME 10mg/kg IV 54 weeks 32 20-30 24.5 -1.24*

(p<0.05)

Crenezumab ABBY 15mg/kg IV 72 weeks Plc: 39

Cren: 8222-26

-0.44

p=.423

SolanezumabExpedition 1 & 2: Pooled Mild

Subgroup400mg IV 72 weeks 1322 20-26 22.5

-0.16*

(p=.34)

* calculated based on change from baselines reported in placebo and active arms

Source: Company data, Credit Suisse estimates and analysis

15

There Was a Trade-Off; ARIA-E was Higher for Aducanumab Studies than Others

ARIA-E is not an ideal safety issue but likely manageable; maybe harder for community docs

Some started to debate whether inflammation was a sign of efficacy suggesting the plaque was

moving

We think the verdict is still out and agree with Biogen exploring titration

Source: Company data, Credit Suisse estimates and analysis

16

Crenezumab Missed its Primary Endpoints in Phase 2, but Showed Activity in Mild Patients

Roughly 346 patients dosed between ABBY (cognition) and BLAZE (biomarker on amyloid

burden)

Crenezumab did not meet its co-primary endpoints in mild-to-moderate AD (MMSE 18-26)

patients but did show activity in mild (MMSE 22 26) patients

Two co-primary endpoints, ADAS-cog12 and CDR-SOB, were not significant in the

pre-specified population and had 16.8% (p=0.19) and 3.1% (p=0.85) reduction,

respectively.

ABBY BLAZE ADAD CREAD

Phase Ph 2 Ph 2 Ph 1 Ph 2 Ph 3

Cognition Biomarker Explore high dose Prevention Pivotal

Initiation

date6/7/2011 8/17/2011 Jan 2015 11/29/2013 1/28/2016

Number

enrolled431 91 72 300 750

Status Completed Completed Enrolling Enrolling Enrolling

Duration 73 wk 73 wk 10 mo 260 wk 105 wk

Patient

criteriaMMSE 18-26 MMSE 18-28

MMSE >/= 26

PSEN1 mutationMMSE >22

Primary

Endpoints

ADAS-cog11

CDR-SOB

Brain amyloid

change by

florbetapir-PET

Safety

Alzheimer's

Prevention Initiative

(API) Composite

Cognitive score

CDR-SB

Dosage 300mg SC q2w OR 15mg/kg IV q4w 60mg/kg IV q4w

Source: Company data, Credit Suisse estimates and analysis

17

Crenezumab Showed Trends on CDR-SB Based on Baseline MMSE Scores

CDR-SB, an endpoint with a functional component and the Phase 3 endpoint for both

Crenezumab and Aducanumab, was not statistically significant in MMSE 22-26 patients.

However, the data do show a trend on CDR-SB suggesting some activity the more mild the

patient cohort

Source: Company data, Credit Suisse estimates and analysis

18

Statistically Significant Difference was Seen Versus Placebo on ADAS-Cog12 in Mild Patients (MMSE 22-26)

The effect on ADAS-Cog12 was greater the milder the population at baseline, with the greatest

effect being seen in the 22-26 MMSE group (n= 121; Placebo 39, Crenezumab 82)

Source: Company data, Credit Suisse estimates and analysis

19

For Crenezumab, No Trend Yet in Functional Endpoints

Dosing is at 15mg/kg in Phase 2 but Ph3 dose is 60mg/kg. We have not seen that data

published yet; likely a smaller cohort

Data seen at 15 mg/kg on a functional basis has no effect so any info around higher dosing and

functional endpoints would be important

Source: Company data, Credit Suisse estimates and analysis

20

What went wrong in all these prior Alzheimer’s trials?

Source: Company data, Credit Suisse estimates and analysis

21

Has Dosing Been Pushed Enough to Lead to Efficacy?

We think that it is a key question for many drugs below which have failed

ARIA-E (brain inflammation) is the key safety issue that limits dosing

There are some questions around the current solanezuamab dosing as well

Source: Company data, Credit Suisse estimates and analysis

Drug Lead

CompanyTarget

Phase

when

failed

Type

Bapineuzumab JNJ/PfizerAmyloid

BetaPhase 3 Antibody

Idalopirdine Lundbeck 5-HT6 Phase 3 Small molecule

Gammagard BaxterAmyloid

BetaPhase 3

Immunoglobulin

s

LMTX TauRx Tau Phase 3 Small molecule

PF-04360365 PfizerAmyloid

BetaPhase 2 Antibody

22

Has Dosing Been Pushed Enough to Lead to efficacy?

In December 2014 Roche halted the Phase 3 trial of gantenerumab after a pre-planned futility

analysis in 312 patients who had reached two years of treatment (no new safety signals, so

presumably halted for efficacy)

Had enrolled a mild population (MMSE of 24+ vs. EXPEDITION3 which is in MMSE of 20-26)

However, the doses used were 105mg and 225mg vs. 400mg in Sola, 10mg/kg in

Aducanumab, and 15mg/kg for Crenezumab in ABBY (10 to 15mg/kg is equivalent to 680-

1020mg assuming average weight of 68kg)

We think the low doses could have been a cause of lack of efficacy

Source: Company data, Credit Suisse estimates and analysis

23

Maybe We Need to Look for Mild Prodromal Patients…

Many of the earlier trials worked in mild sub-group populations (mostly in post-hoc analyses)

Most of these studies studied mild to moderate which seemingly did not work

Biogen’s study made a splash because though small it worked in the defined cohort

Source: Company data, Credit Suisse estimates and analysis

Drug Trial nMMSE

population

ADAS-

Cog14

ADAS-

cog12MMSE CDR-SOB

Crenezumab ABBY 103 22-2635%

(p=0.036)

45.8%

(p=0.25)

19.6%

(p=0.42)

SolanezumabPooled

EXPEDITION1322 20-26

34.3%

(p=0.001)

33.7%

(p=0.001)

9.5%

(p=0.34)

Aducanumab PRIME 45 20-302.25

(p<0.05)

1.24

(p<0.05)

24

Is every amyloid beta created equal?

Although they are all targeting Abeta, thy have distinct molecular properties e.g. different binding sites,

epitopes and backbones

Clinically, there is no clear evidence yet to suggest that the binding sites and epitopes make a difference for

clinical efficacy

Crenezumab is the only drug on the IgG4 backbone; they think that this helps with ARIA-E profile which allows

for them to dose higher

Preclinical data (Adolfsson et al.) suggests IgG4 backbone vs. IgG1 backbone reduces inflammation by activating the microglia cells vs. IgG1 which is shown to activate complement and TNF-alpha inflammatory factors

Source: Company data, Credit Suisse estimates and analysis

Crenezumab Solanezumab Aducanumab Bapineuzumab Gantenerumab

IgG lgG4 lgG1 lgG1 lgG1 IgG1

Source Humanized Humanized Human Humanized Human

Binding

profile

Monomers;

Oligomers;

Fibrils

MonomersOligomers;

Fibrils

Monomers;

Oligomers;

Fibrils

Oligomers; Fibrils

Epitope Mid-domain mid-domain N-term N-term N-term + mid

MOA

Microglia-

mediated

clearance

Sequestration of

soluble

monomeric Aβ

Microglia-

mediated

clearance

Microglia-

mediated

clearance

Microglia-

mediated

clearance

25

Market opportunity for AD: What are the commercial implications?

Source: Company data, Credit Suisse estimates and analysis

26

Diagnosis is Still Relatively Poor But We Expect This to Improve Over Time

AD is one of the most poorly diagnosed diseases in the US given the clinical difficulty of

distinguishing between natural aging vs. disease progression

Many biomarkers and diagnostics for AD are currently in development that we think will

eventually improve diagnosis

45%

27%

93% 96% 91%84%

92% 90%84% 81%

72% 72% 70%

48%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Source: Company data, Credit Suisse estimates and analysis

27

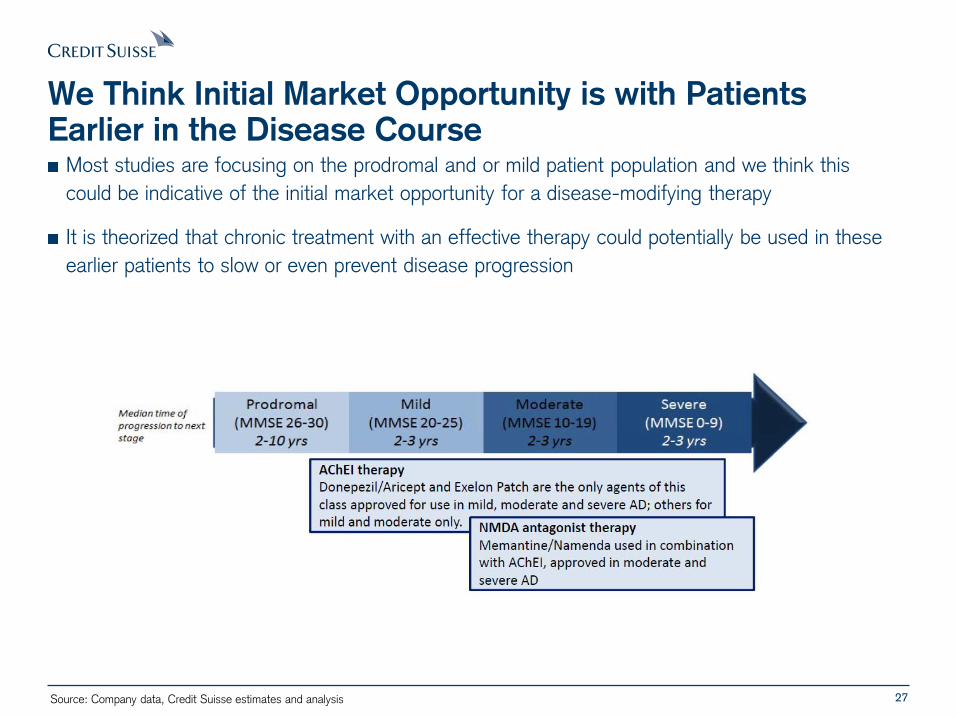

We Think Initial Market Opportunity is with Patients Earlier in the Disease Course

Most studies are focusing on the prodromal and or mild patient population and we think this

could be indicative of the initial market opportunity for a disease-modifying therapy

It is theorized that chronic treatment with an effective therapy could potentially be used in these

earlier patients to slow or even prevent disease progression

Source: Company data, Credit Suisse estimates and analysis

28

Company Prevalence Estimates

Source: Company data, Credit Suisse estimates and analysis

29

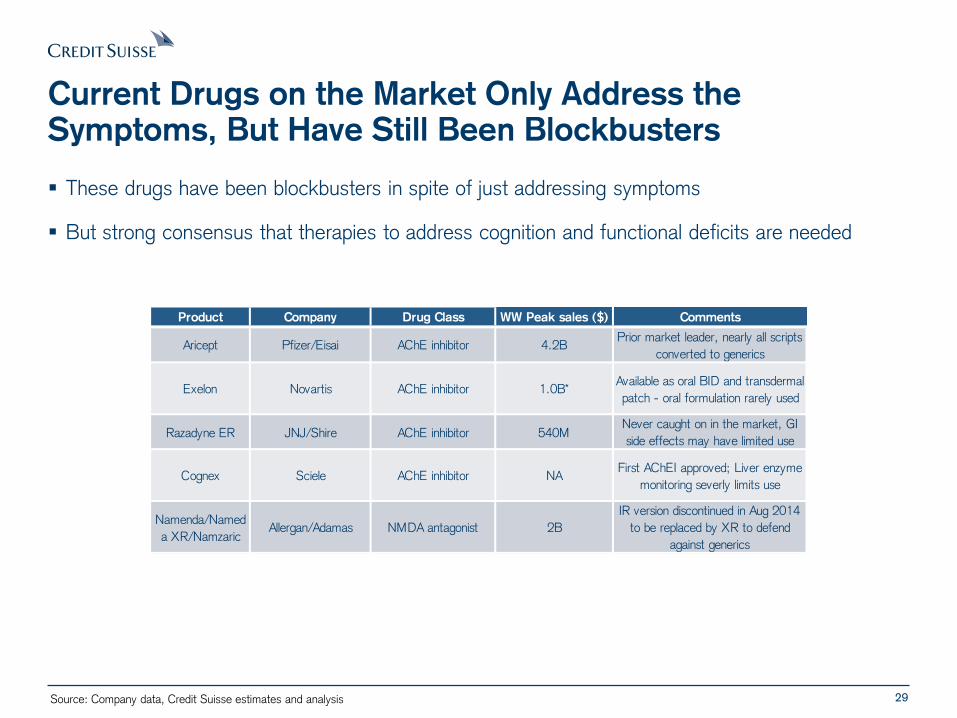

Current Drugs on the Market Only Address the Symptoms, But Have Still Been Blockbusters

These drugs have been blockbusters in spite of just addressing symptoms

But strong consensus that therapies to address cognition and functional deficits are needed

Source: Company data, Credit Suisse estimates and analysis

Product Company Drug Class WW Peak sales ($) Comments

Aricept Pfizer/Eisai AChE inhibitor 4.2BPrior market leader, nearly all scripts

converted to generics

Exelon Novartis AChE inhibitor 1.0B*Available as oral BID and transdermal

patch - oral formulation rarely used

Razadyne ER JNJ/Shire AChE inhibitor 540MNever caught on in the market, GI

side effects may have limited use

Cognex Sciele AChE inhibitor NAFirst AChEI approved; Liver enzyme

monitoring severly limits use

Namenda/Named

a XR/NamzaricAllergan/Adamas NMDA antagonist 2B

IR version discontinued in Aug 2014

to be replaced by XR to defend

against generics

30

How do we think about prior Sola studies and upcoming EXPEDITION3 readout?

31

It Has Been a Long, Winding Road for Solanezumab as we

Approach Topline EXPEDITION3 Data

Source: Company data, Credit Suisse estimates and analysis

Timeline Event Design/result

July, 2008

Lilly published results of a 12-week Phase 2

trial. 4 dosages are 100mg or 400mg Q1W or

Q4W.

No change in cognition and levels of brain

amyloid

Increase in amyloid beta in blood and CSF

which may suggest dissolving of amyloid plaques

May, 2009

Enrollment of Phase 3 trials, EXPEDITION1

and EXPEDITION2 started

18-month, 1000 pts each trial, 1:1 randomize

to 400mg QIW vs pbo

Primary endpoints: ADAS-Cog11 and ADCS-

ADL

Jan, 2011 Enrollment of EXP1 and 2 completed Overall safety "appear to be very good"

Aug, 2012

Lilly announced that both cognitive and

functional endpoints were not met in EXP1 and

2

Pre-specified secondary analysis of pooled data

showed stat sig slowing of cognition decline

Oct, 2012 Presented detailed results for EXP1 and 2

EXP1: pre-specified mild AD showed

42%(p=0.008) reduction of ADAS-Cog11

EXP2: pre-specified mild AD showed

20%(p=0.12) reduction in ADAS-Cog14

Dec, 2012

Lilly after talking to the regulatory agencies,

planned to do another Ph3 EXP3 and did not

have intend to submit BLA at this time

July, 2013Presented design of Phase 3 EXPEDITION3

trial

2100 pts, 18-month 400mg Q4W :Pbo

Primary: ADAD-Cog14 and ADCS-iADL

Jan, 2014NEJM published EXPEDITION 1 and 2 study

by Doody et al

July, 2015Presented EXPEDITION-EXT analysis at AAIC

and published in “Alzheimer’s and Dementia"

Stat sig reduction in ADAS-cog11, ADAS-

cog14, MMSE

Mar, 2016 Change primary endpoint for EXP 3Only has ADAS-Cog14 and removed ADCS-

iADL

32

Positive Results Seen On ADAScog14 in Pooled Mild

Population for EXPEDITION 1/2

Source: Company data, Credit Suisse estimates and analysis

33

Benefit Also Seen on the Function Endpoint of ADCS-iADL

in the Pooled Analysis of EXPEDITION 1/2

Source: Company data, Credit Suisse estimates and analysis

34

Mild Patients, Amyloid Screening and Larger Sample Size are Key Changes to EXPEDITION3

Company predicts last patient visited in Oct 2016

Discontinuations are also lower than EXP 1 & 2, increasing overall powering of the study

95% of patients have elected to continue in delayed start portion of trial at end of placebo

control

Source: Company data, Credit Suisse estimates and analysis

Expedition 3 Expedition 1 and 2

Phase 3 3.00

Cohort size & # of cohorts 1050 per arm 500 per arm

Dosing 400mg IV monthly 400mg IV monthly

Duration of treatment 18 months 18 months

Primary endpoint ADAS-COG14 ADAS-cog11and ADCS-ADL

Patients enrolled by MMSE MMSE 20-26 MMSE 16-26

Requirement for amyloid

pathologyAmyloid positive by PET or CSF None

Number of mild patients 2100 about 1300 (est 1000 amyloid positive)

Other notes

ADCS-iADL had been a co-

primary endpoint but this was

moved down to a key secondary

endpoint in March 2016

After analysis of data from EXPEDITION 1,

primary outcome was revised ADAS-cog14

in mild patients for EXPEDITION 2

35

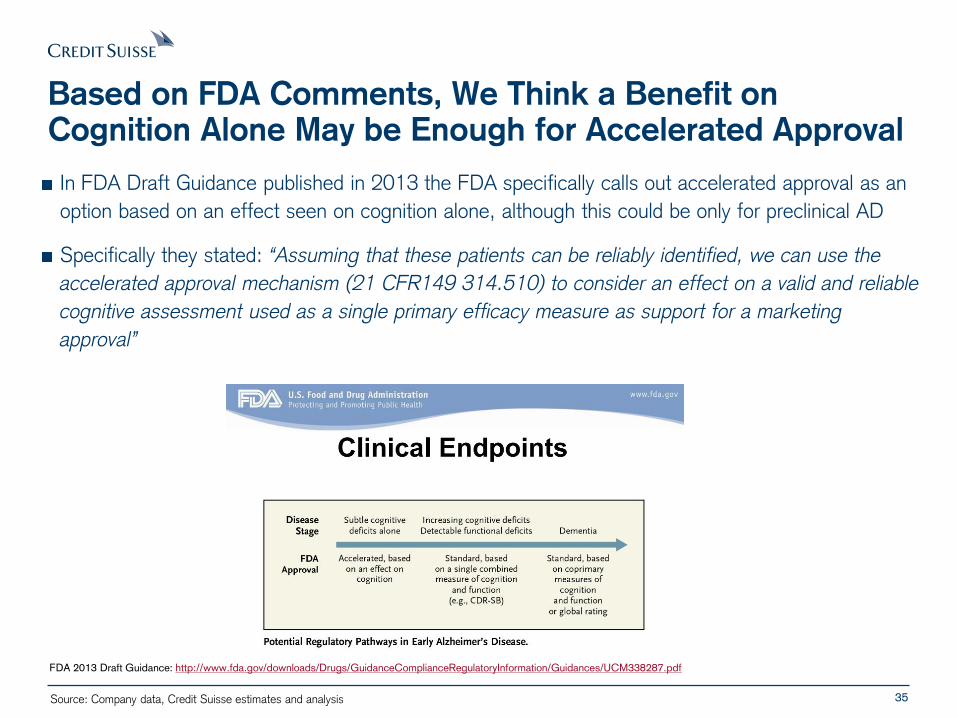

Based on FDA Comments, We Think a Benefit on Cognition Alone May be Enough for Accelerated Approval

In FDA Draft Guidance published in 2013 the FDA specifically calls out accelerated approval as an

option based on an effect seen on cognition alone, although this could be only for preclinical AD

Specifically they stated: “Assuming that these patients can be reliably identified, we can use the

accelerated approval mechanism (21 CFR149 314.510) to consider an effect on a valid and reliable

cognitive assessment used as a single primary efficacy measure as support for a marketing

approval”

FDA 2013 Draft Guidance: http://www.fda.gov/downloads/Drugs/GuidanceComplianceRegulatoryInformation/Guidances/UCM338287.pdf

Source: Company data, Credit Suisse estimates and analysis

36

The FDA’s Stated Preference is for Data on Both Cognitive and Functional Endpoints

Per FDA comments, the intent of the functional endpoints is to “ensure the clinical

meaningfulness of a cognitive benefit that may be observed”

However, they have noted that, in practice, it may be impractical to use co-primary

endpoints, especially before the onset of overt dementia

FDA has noted that they think the co-primary approach in practice may be impractical and

suggested cognition alone could be sufficient, especially for patients early in the spectrum of the

illness:

“Therefore, although the principle behind the co-primary outcome measure approach still holds,

the application of this approach in practice may be impractical in these cases and clear

evidence of an effect on delaying cognitive impairment may provide sufficient evidence of

effectiveness.”

FDA 2013 Draft Guidance: http://www.fda.gov/downloads/Drugs/GuidanceComplianceRegulatoryInformation/Guidances/UCM338287.pdf

Source: Company data, Credit Suisse estimates and analysis

37

We Think Regulators (Both EMA and FDA) Recognize Challenges of Existing Endpoints

We think it could be difficult to show large magnitude of differences on cognitive endpoints in

mild patients due to the low levels of impairment present in early AD

This sentiment has been echoed by the FDA and EMA and we think this could give some

flexibility in interpreting clinically meaningful differences

Some challenges broadly with endpoints

– Mild disease is hard to show a large difference versus placebo

– In a global study controlling for different cultures and languages is not a perfect science

– Cognitive scales have a ceiling effect which makes it hard to detect small changes

Source: Company data, Credit Suisse estimates and analysis

38

The FDA has Mentioned CDR-SB as a Single Primary Outcome Measure Suitable for Approval

This is both Biogen and Roche/AC Immune’s primary endpoint in their Phase 3s

Biogen has a special protocol assessment (SPA) with the FDA suggesting that the FDA views

this endpoint as acceptable for approval

The EMA has also mentioned the CDR-SB as useful, but they noted the pitfalls of 1) the

extensive training needed for the scoring and 2) that it is subject to variability among ethnicity

and language

FDA 2013 Draft Guidance: http://www.fda.gov/downloads/Drugs/GuidanceComplianceRegulatoryInformation/Guidances/UCM338287.pdf

EMA 2014 Draft Guideline: http://www.ema.europa.eu/docs/en_GB/document_library/Scientific_guideline/2016/02/WC500200830.pdf

Source: Company data, Credit Suisse estimates and analysis

39

US Major Pharma: Thoughts on Lilly and Merck from Vamil Divan

40

Our Recent Survey Suggested Investors are Getting a Bit More Positive on Sola

Source: Company data, Credit Suisse estimates and analysis

41

Lilly has Other Shots on Goal in Alzheimer’s Beyond Solanezumab

Source: Company data, Credit Suisse estimates and analysis

Could also support a positive stock reaction even without strong functional data

In addition, we see a lot more to the Lilly story than just Alzheimer’s

42

Expect a Significant Move in LLY Shares in Either Direction; More Modest Moves Expected in MRK

Source: Company data, Credit Suisse estimates and analysis

Positive, statistically significant data on both cognition and function could lead to a move of >20%

in LLY shares (we think there is a 10% probability of this)

Positive cognitive data with a trend on function would likely also result in a meaningful positive move

(~+5-8%), based on recent conversations with investors (30% probability)

Positive cognitive data with no trend of function would lead to the most debate (20% probability)

– May see initial positive stock reaction but then debate around regulatory and commercial potential

likely to heat up

Negative cognitive data would mean a failed study and could result in a 10-15% selloff in LLY

shares (40% probability)

Reaction in MRK will be more modest, but likely in the same direction as LLY

43

Large Cap Biotech: AC Immune and Biogen Stock Thoughts

44

We agree with our survey; we expect a big move on Biogen either way on Sola data

Source: Company data, Credit Suisse estimates and analysis

45

On BIIB, our model suggests a smaller move of 3-6% up or 3-4% down

Generally we think AC Immune is much more exposed to the Sola readout given their lead asset

and much of their pipeline is focused on AD while Biogen has other franchises

We expect all 3 stocks to be volatile come “sola” day especially as the data is likely to be

nuanced in the way that prior EXPEDITION readouts have been

We also think Biogen will likely trade higher than what our model says especially since this would

further the M&A thesis. However it probably trades more on the downside as well

We have gotten comments post launch on AC Immune that stock could move on the upside

more

Source: Company data, Credit Suisse estimates and analysis

46

Biogen Alzheimer’s Sensitivities

Every 10% success is worth ~$10/sh (or approximately 3%) to our valuation

Source: Company data, Credit Suisse estimates and analysis

0% 15% 25% 40% 50% 60% 75% 100%

$284 $298 $308 $322 $331 $341 $355 $378

DCF Valuation by POS to Aducanumab

$100 $1,074

$2,254 $3,775

$5,938

$7,792

$10,077

$12,790 $13,406 $14,056

$14,740

$0

$2,000

$4,000

$6,000

$8,000

$10,000

$12,000

$14,000

$16,000

$18,000

$20,000

20

20

20

21

20

22

20

23

20

24

20

25

20

26

20

27

20

28

20

29

20

30

Biogen AD Franchise Sales

47

AC Immune Alzheimer’s Sensitivities

AC Immune is highly levered to the AD space and we think the stock could move on a much

larger percentage basis relative to both Lilly and Biogen whatever the results.

We think the Phase 3 Solanezumab data could move POS 10-20% for AC Immune’s program

depending on the relative strength or weakness of the data which would be a $6-$12/sh move.

We are currently at 40% POS for Crenezumab.

0% 15% 25% 40% 50% 65% 75% 100%

($9) $2 $8 $18 $24 $33 $40 $56

DCF Valuation by POS to Crenezumab

Source: Company data, Credit Suisse estimates and analysis

48

How we model AD – BIIB and ACIU

Source: Company data, Credit Suisse estimates and analysis

US 2020E

Alzheimer's Prevalence (ex-prodromal) 6,144,153

% growth 3%

Diagnosed & Treated Population 3,993,699

Diagnosis Rate 65%

Mild patients treated & diagnosed 1,078,299

% of diagnosed & treated total 27%

Prodromal patient prevalence 4,405,241

% growth 3%

Prodromal patients converting to mild 440,524

% conversion rate 10%

Total Patients Elligible for AD treatment 1,518,823

Crenezumab Share 1%

Total Patients on Crenezumab 7,594

Price $25,000

% growth

Net Price $12,250

Gross to Net 30%

Compliance 70%

AD Market US EU

Alzheimer's Prevalence

(Exluding Prodromal)5.3M 8M

Diagnosed & Treated 2.4M 3.6M

Mild Treated & Diagnosed 644k 972k

Prodromal Prevalence 3.8M 3.5M

Prodromal Patients

Converting to Mild380k 350k

Total Patients Elligible for

AD treatment1M 1.3M

Gross Price $25k $15k

Gross to Net 30% 40%

Compliance 70% 70%

Net Price $12.3k $10.5k

49

Needless to say Eisai ties up with Biogen for E2609/BACE inhibitor and BAN2401/ Aβinhibitor.

E2609: Held End-of-Phase 2 meeting with FDA and a Phase III study is planned in FY3/2017

BAN2401: P2 trial enrolled 750 patients by the end of September for 3rd interim analysis but

the trial is still ongoing. The last patient in to complete 800 patient trial is expected by the of

December. Eisai should be able to report quick read out of 800 patients data early 2017. Then

decision time if Eisai will have to opt-in Biogen to co-develop aducanumab.

Lemborexant: This could be a wild card. Initiated Phase 3 for insomnia and planning P2 aiming

for dementia related for irregular sleep wake rhythm disorder (ISWRD) to target world’s first

indication. Who knows?

Source: Company data, Credit Suisse estimates and analysis

50

Otsuka has 4 AD assets as per below:

Lu AE58054/idalopirdine selective 5-HT3 receptor blocker, as you know failed 1 of 3 ongoing

P3 trial. This is a joint trial with Lundbeck.

brexpiprazole /Rexulti is already approved for schizophrenia. P3 is ongoing for agitation related

to AD.

APV-786/NMDA receptor antagonist, P3 trial is ongoing aiming AD related agitation. Otsuka

acquired APV-786 through Avanir acquisition.

LuAF205013, this is beta amyloid vaccine. P1 stage with Lundbeck co-developing.

Source: Company data, Credit Suisse estimates and analysis

51

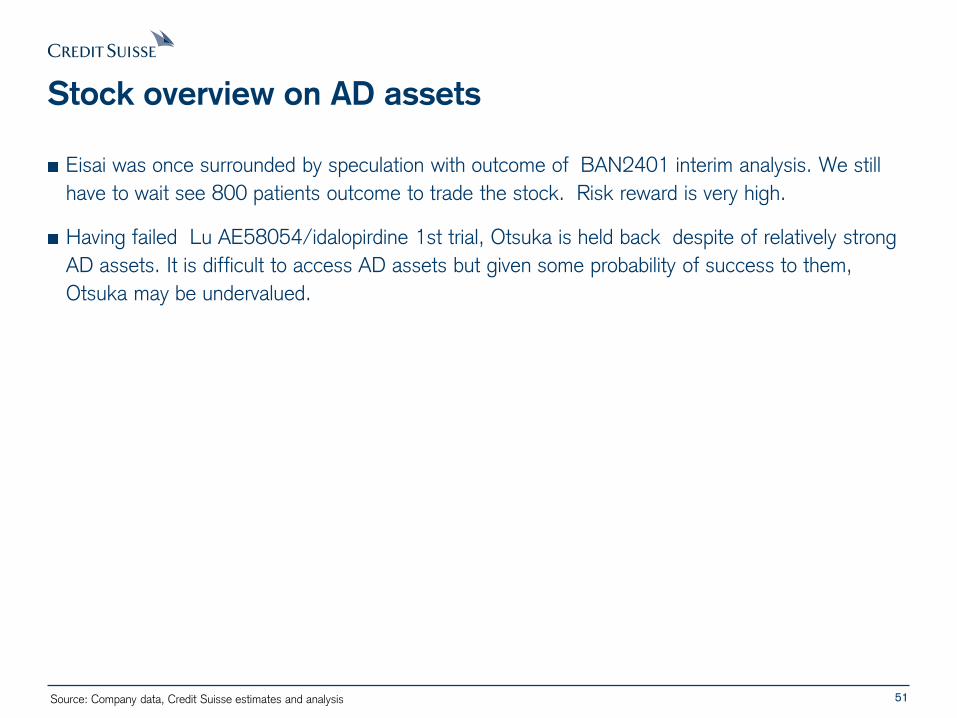

Stock overview on AD assets

Eisai was once surrounded by speculation with outcome of BAN2401 interim analysis. We still

have to wait see 800 patients outcome to trade the stock. Risk reward is very high.

Having failed Lu AE58054/idalopirdine 1st trial, Otsuka is held back despite of relatively strong

AD assets. It is difficult to access AD assets but given some probability of success to them,

Otsuka may be undervalued.

Source: Company data, Credit Suisse estimates and analysis

52

EU Pharma: Thoughts on Roche from the EU Pharma team

53

Roche – major AD investment, portfolio approach

Roche is highly committed to AD with two late-stage Abeta programs in the clinic.

Crenezumab targets all 3 forms of Abeta with a focus on oligomers, gantenerumab targets plaque.

Roche was encouraged by the aducanumab data showing a nice correlation between drug and

biomarkers of AD in a prospective analysis. A retrospective analysis of Roche’s gantenerumab

studies shows a similar correlation.

Roche’s experience with the failed SCARLET ROAD P3 study is that dose is critical. Pushed

crenezumab dose in P3 to 60mg/kg. Now using gantenerumab at 220mg flat dosing. Antibody

penetration into the brain is <1%.

COGS and manufacturing going to be a meaningful element of biologics in AD. Crenezumab

patients will be receiving over 1 gram of antibody per infusion.

Dose titration is also critical in Roche’s view. The bulk of the CNS side effects are seen in the

first 6 months. Roche philosophy is to dose titrate slowly up to peak dose levels. Roche is

currently testing 4 different dose titration schedules for gantenerumab.

Functional endpoints are what payers benefit from.

MODEL: $6bn peak of ‘Alzheimer’s franchise’ sales across crenezumab & gantenerumab

Source: Company data, Credit Suisse estimates and analysis

54

Appendix slides: More details on the data

55

Solanezumab data from publications by endpoints

Trial DoseDosing

Lengthn

MMSE

Enrollment

Baseline

MMSE

Baseline

ADAS-Cog11

ADAS-

Cog14ADCS-iADL ADCS-ADL

Expedition 1 1012 16-26 21 22 -1.4

(p=.09)

-0.4

(p=.64)

Expedition 2 1040 21Plc: 23

Sola: 24

-1.6

(p=.04)

1.6

(p=.08)

Expedition 2: Mild

Subgroup647

Plc: 23

Sola: 22

Plc: 19

Sola: 20

-1.7

(p=.06)

2.3

(p=.04)

Expedition 1 & 2: Pooled

Mild Subgroup1322 22.5

Plc: 18.9

Sola: 19.4

-2.13*

(p=.001)

1.21*

(p=.045)

1.42*

(p=.057)

Expedition Phase 3 2100Primary

Endpoint

Previously a

Primary

Endpoint

Lower is better

BaselinesChange from Baseline (ITT) Mean

Difference from Placebo In:

Higher is better

* calculated based on change from baselines reported in placebo and active arms

400mg IV

Last dose at

week 76;

last

observation

at week 80

Higher is better

20-26

Source: Company data, Credit Suisse estimates and analysis

56

Key endpoints in AD trials

Source: Company data, Credit Suisse estimates and analysis

TestShort

name

Score

range

Meaning of

scoreComments

Mini-Mental State

ExamMMSE 0-30 30 is the best

The MMSE is an assessment of

cognitive function employed in both

clinical practice and clinical trials. Scores

may be impacted by a number of factors

including education, cultural background

and literacy

Clinical Dementia

Rating-Sum of

Boxes

CDR-SB 0-18 0 is the best

Interview between patients and caregiver

measuring impairment of memory,

orientation, judgement and problem

solving, etc. Tracks early stages of AD

Alzheimer's Disease

Assessment Scale

cognitive subscale

ADAS-cogDepending

on subtypesmaller is better

Dealing with memory, language,

construction and praxis orientation. Is

widely used and can be considered as a

standard tool in trials on patients with

mild to moderate Alzheimer's disease.

Due to ceiling and floor effects, its

sensitivity to change is limited in early

and late stages

Basic activities of

daily living BADL Varies Higher is better

Physical activities, such as toileting,

mobility, dressing and bathing

instrumental

activities of daily

living

iADL Varies Higher is better

Better to track early stage of AD.

Shopping, cooking, doing laundry,

handling finances, using transportation

57

Comparing Data

Trial DoseDosing

Lengthn

MMSE

Enrollment

Baseline

MMSE

Baseline

ADAS-Cog11ADCS-iADL ADCS-ADL MMSE

ADAS-

Cog11

ADAS-

Cog14CDR-SB

Solanezumab Lower is better

Expedition 1 1012 21 22 -0.4

(p=.64)

0.6

(p=.06)

-0.8

(p=.24)

-1.4

(p=.09)

0.1

(p=.51)

Expedition 2 1040 21Plc: 23

Sola: 24

1.6

(p=.08)

0.8

(p=.004)

-1.3

(p=.06)

-1.6

(p=.04)

-0.3

(p=.17)

Expedition 1: Mild

Subgroup675

Expedition 2: Mild

Subgroup647

Plc: 23

Sola: 22

Plc: 19

Sola: 20

2.3

(p=.04)

0.7

(p=.10)

-1.5

(p=.05)

-1.7

(p=.06)

-0.3

(p=.22)

Expedition 1 & 2: Pooled

Mild Subgroup1322 22.5

Plc: 18.9

Sola: 19.4

1.21*

(p=.045)

1.42*

(p=.057)

0.93*

(p=.001)

-1.74*

(p=.001)

-2.13*

(p=.001)

-0.16*

(p=.34)

Expedition Phase 3 2,100

Previously a

Primary

Endpoint

Primary

Endpoint

Aducanumab

10mg/kg IV 32 24.8 2.25*

(p<.05)

-1.24*

(p<0.05)

6mg/kg IV 30 24.4 0.85*

NS

-.76*

NS

3mg/kg IV 32 23.2 2.11*

(p<.05)

-.50*

NS

CrenezumabADAS-

Cog12

Plc: 84

Cren: 16318-26

Plc: 21.6

Cren: 21.9

.51

p=.77

.49

p=.46

-1.78

p=.190

-0.08

p=.85

Plc: 54

Cren: 11120-26

2.18

p=.26

.70

p=.351

-2.24

p=.128

.02

p=.964

Plc: 39

Cren: 8222-26

0.21

p=.95

1.05

p=.250

-3.44

p=.036

-0.44

p=.423

* calculated based on change from baselines reported in placebo and active arms

15mg/kg IV

PRIME

ABBY Trial

Last dose at

week 68;

last

observation

at week 72

400mg IV

Last dose at

week 76;

last

observation

at week 80

Change from Baseline (ITT) Mean Difference from Placebo In:

Higher is better

54 weeks

20-26

16-26

20-30

Baselines

Lower is betterHigher is better

Source: Company data, Credit Suisse estimates and analysis

58

Companies Mentioned (Price as of 18-Oct-2016)

AC Immune (ACIU.OQ, $15.19, OUTPERFORM[V], TP $18.0) AbbVie Inc. (ABBV.N, $61.55) AstraZeneca (AZN.L, 5002.0p) Baxter International Inc. (BAX.N, $48.06) Biogen, Inc. (BIIB.OQ, $295.05, NEUTRAL, TP $322.0) Bristol Myers Squibb Co. (BMY.N, $50.05) Eisai (4523.T, ¥6,664) Eli Lilly & Co. (LLY.N, $78.77, OUTPERFORM, TP $96.0)

Johnson & Johnson (JNJ.N, $115.41) Lundbeck (LUN.CO, Dkr218.6) Merck & Co., Inc. (MRK.N, $62.09) Novartis (NVS.N, $76.31) Pfizer (PFE.N, $32.69) Roche (ROG.S, SFr233.6, OUTPERFORM, TP SFr300.0) Shire Pharmaceuticals (SHP.L, 5146.0p)

Disclosure Appendix

Important Global Disclosures

The analysts identified in this report each certify, with respect to the companies or securities that the individual analyzes, that (1) the views expressed in this report accurately reflect his or her personal views about all of the subject companies and securities and (2) no part of his or her compensation was, is or will be directly or indirectly related to the specific recommendations or views expressed in this report.

3-Year Price and Rating History for AC Immune (ACIU.OQ)

ACIU.OQ Closing Price Target Price

Date (US$) (US$) Rating

18-Oct-16 15.19 18.00 O *

* Asterisk signifies initiation or assumption of coverage.

O U T PERFO RM

3-Year Price and Rating History for Biogen, Inc. (BIIB.OQ)

BIIB.OQ Closing Price Target Price

Date (US$) (US$) Rating

28-Oct-13 254.58 290.00 O

10-Dec-13 285.23 375.00

13-Feb-14 328.62 400.00

23-Jul-14 337.60 425.00

19-Nov-14 303.61 400.00

17-Mar-15 426.12 500.00

13-May-15 390.04 NR

19-Jan-16 269.85 322.00 N *

07-Jun-16 252.86 312.00

01-Aug-16 301.83 322.00

* Asterisk signifies initiation or assumption of coverage.

O U T PERFO RM

N O T RA T ED

N EU T RA L

3-Year Price and Rating History for Eli Lilly & Co. (LLY.N)

LLY.N Closing Price Target Price

Date (US$) (US$) Rating

28-Oct-13 50.88 52.00 N

07-Jan-14 51.19 54.00

19-Feb-14 58.09 56.00

24-Apr-14 58.68 61.00

02-Nov-14 66.33 65.00

17-Dec-14 70.28 71.00

04-May-15 73.05 72.00

08-Jun-15 78.52 75.00

03-Aug-15 84.14 89.00

08-Oct-15 83.77 105.00 O

12-Oct-15 79.44 99.00

04-Feb-16 74.28 94.00

01-May-16 75.53 91.00

28-Jul-16 82.93 96.00

* Asterisk signifies initiation or assumption of coverage.

N EU T RA L

O U T PERFO RM

3-Year Price and Rating History for Roche (ROG.S)

ROG.S Closing Price Target Price

Date (SFr) (SFr) Rating

18-Oct-13 242.10 280.00 O

20-Jan-14 250.00 320.00

03-Feb-14 248.20 300.00

09-Jan-15 278.10 295.00

16-Mar-15 265.30 300.00

31-Mar-15 268.10 320.00

28-Jan-16 258.10 300.00

* Asterisk signifies initiation or assumption of coverage. O U T PERFO RM

The analyst(s) responsible for preparing this research report received Compensation that is based upon various factors including Credit Suisse's total revenues, a portion of which are generated by Credit Suisse's investment banking activities

As of December 10, 2012 Analysts’ stock rating are defined as follows:

Outperform (O) : The stock’s total return is expected to outperform the relevant benchmark* over the next 12 months.

Neutral (N) : The stock’s total return is expected to be in line with the relevant benchmark* over the next 12 months.

Underperform (U) : The stock’s total return is expected to underperform the relevant benchmark* over the next 12 months.

*Relevant benchmark by region: As of 10th December 2012, Japanese ratings are based on a stock’s total return relative to the analyst's coverage universe which consists of all companies covered by the analyst within the relevant sector, with Outperforms representing the most attractiv e, Neutrals the less attractive, and Underperforms the least attractive investment opportunities. As of 2nd October 2012, U.S. and Canadian as well as European ratings are based on a stock’s t otal return relative to the analyst's coverage universe which consists of all companies covered by the analyst within the relevant sector, with Outperforms representing the most attractive, Neutrals the less attractive, and Underperforms the least attractive investment opportunities. For Latin American and non-Japan Asia stocks, ratings are based on a stock’s total return relative to the average total return of the relevant country or regional benchmark; prior to 2nd October 2012 U.S. and Canadian ratings were based on (1) a stock’s absolute total return potential to its current share price and (2) the relative attractiveness of a stock’s total return potential within an analyst’s coverage universe. For Australian and New Zealand stocks, the expected total return (ETR) calculation includes 12 -month rolling dividend yield. An Outperform rating is assigned where an ETR is greater than or equal to 7.5%; Underperform where an ETR less than or equal to 5%. A Neutral may be assigned where the ETR is between -5% and 15%. The overlapping rating range allows analysts to assign a rating that puts ETR in the context of associated risks. Prior to 18 May 2015, ETR ranges for Outperform and Underperform ratings did not overlap with Neutral thresholds between 15% and 7.5%, which was in operation from 7 July 2011.

Restricted (R) : In certain circumstances, Credit Suisse policy and/or applicable law and regulations preclude certain types of communications, including an investment recommendation, during the course of Credit Suisse's engagement in an investment banking transaction and in certain other circumstances.

Not Rated (NR) : Credit Suisse Equity Research does not have an investment rating or view on the stock or any other securities related to the company at this time.

Not Covered (NC) : Credit Suisse Equity Research does not provide ongoing coverage of the company or offer an investment rating or investment view on the equity security of the company or related products.

Volatility Indicator [V] : A stock is defined as volatile if the stock price has moved up or down by 20% or more in a month in at least 8 of the past 24 months or the analyst expects significant volatility going forward.

Analysts’ sector weightings are distinct from analysts’ stock ratings and are based on the analyst’s expectations for the fundamentals and/or valuation of the sector* relative to the group’s historic fundamentals and/or valuation:

Overweight : The analyst’s expectation for the sector’s fundamentals and/or valuation is favorable over the next 12 months.

Market Weight : The analyst’s expectation for the sector’s fundamentals and/or valuation is neutral over the next 12 months.

Underweight : The analyst’s expectation for the sector’s fundamentals and/or valuation is cautious over the next 12 months.

59

*An analyst’s coverage sector consists of all companies covered by the analyst within the relevant sector. An analyst may cover multiple sectors.

Credit Suisse's distribution of stock ratings (and banking clients) is:

Global Ratings Distribution

Rating Versus universe (%) Of which banking clients (%)

Outperform/Buy* 53% (55% banking clients)

Neutral/Hold* 29% (24% banking clients)

Underperform/Sell* 18% (44% banking clients)

Restricted 0%

*For purposes of the NYSE and NASD ratings distribution disclosure requirements, our stock ratings of Outperform, Neutral, an d Underperform most closely correspond to Buy, Hold, and Sell, respectively; however, the meanings are not the same, as our stock ratings are determined on a relative basis. (Please refer to definitions above.) An investor's decision to buy or sell a security should be based on investment objectives, current holdings, and other individual factors.

Credit Suisse’s policy is to update research reports as it deems appropriate, based on developments with the subject company, the sector or the market that may have a material impact on the research views or opinions stated herein.

Credit Suisse's policy is only to publish investment research that is impartial, independent, clear, fair and not misleading. For more detail please refer to Credit Suisse's Policies for Managing Conflicts of Interest in connection with Investment Research: http://www.csfb.com/research-and-analytics/disclaimer/managing_conflicts_disclaimer.html

Credit Suisse does not provide any tax advice. Any statement herein regarding any US federal tax is not intended or written to be used, and cannot be used, by any taxpayer for the purposes of avoiding any penalties.

Target Price and Rating Valuation Methodology and Risks: (12 months) for AC Immune (ACIU.OQ)

Method: Our AC Immune $18 target price and Outperform rating are based on a probability adjusted DCF. We extend our estimates to 2030 and use a 12% discount rate and 2% terminal growth rate in line with small cap biotech peers with platform technologies.

Risk: Key risks to our AC Immune $18 target price and Outperform rating include: clinical setbacks in the AD space e.g. with Solanezumab, crenezumab fails to show significance in Phase 3, difficulty enrolling Phase 3 or a safety issue for platform.

Target Price and Rating Valuation Methodology and Risks: (12 months) for Biogen, Inc. (BIIB.OQ)

Method: Our BIIB $322TP and Neutral rating is based on a DCF. Our DCF is $322/sh based on an 8% discount rate & 2% terminal growth in-line with peers.

Risk: Risks to our BIIB $322 TP and Neutral rating: Key upside risks: Success (meaning hitting primary endpoint) on the anti-Lingo program in mid-16, Positive data that provides greater confidence around BAN2401 (anti-amyloid Beta antibody), Tecfidera sales reaccelerate, Hemophilia assets continue to take share in spite of competition, SMA program gets to market earlier than our expectations through surprise regulatory approval. Key downside risks: Anti-Lingo1 program discontinues after failure in Ph2 Synergy study, Efficacy or safety concern with aducanumab Ph3 program, Worse than expected MS and hemophilia sales during 2016, SMA program has a surprise efficacy or safety failure in Ph3.

Target Price and Rating Valuation Methodology and Risks: (12 months) for Eli Lilly & Co. (LLY.N)

Method: Our $96 target price is based 75/25 blend of DCF valuation ($95) and relative valuation ($98). We use a 7% WACC along with a -1.5% perpetuity growth forecast for our DCF valuation and apply 24 times our 2017 EPS estimate for relative valuation. Our rating of Outperform is based on positive outlook of its core product franchises above comparable peers.

Risk: Key risks to our $96 target price and outperform rating include (1) pipeline failures, particularly on their key diabetes phase 3 assets and autoimmune assets; and (2) inability to appropriately contain costs in keeping with long-term targets.

Target Price and Rating Valuation Methodology and Risks: (12 months) for Roche (ROG.S)

Method: We value Roche on a PE relative basis to the European markets modulated by our PharmaValues NPV methdology. Our European Major Pharma market relative assumption is 160% and our sector PE relative for Roche is 105%, giving a price target of SFr 300 per share. Roche

‘s 3-year historical average PE sector relative is 103%. Our Outperform rating is based on material upside to mid-term sales growth

expectations as Roche's P3 pipeline matures. We believe Esbriet, ocrelizumab, PD-L1, lebrikizumab and venetoclax offer combined peak sales potential in excess of $10bn.

Risk: In addition to the typical pharmaceutical industry risks associated with potential product approvals, withdrawals and patent challenges, key risks are the competitive development of Roche's immuno-oncology pipeline relative to peers and the mid-term potential of ocrelizumab in MS. The medium-term impact of biosimilars on Roche's in-market drugs is also key. The key ris to outperform rating is lack of delivery of sufficient pipeline to drive top quartile growth

Please refer to the firm's disclosure website at https://rave.credit-suisse.com/disclosures for the definitions of abbreviations typically used in the target price method and risk sections.

See the Companies Mentioned section for full company names

The subject company (LLY.N, ACIU.OQ, ROG.S, BIIB.OQ, ABBV.N, BMY.N, MRK.N, AZN.L, PFE.N, LUN.CO, SHP.L) currently is, or was during the 12-month period preceding the date of distribution of this report, a client of Credit Suisse.

Credit Suisse provided investment banking services to the subject company (LLY.N, ACIU.OQ, ROG.S, BIIB.OQ, ABBV.N, BMY.N, MRK.N, PFE.N, SHP.L) within the past 12 months.

Credit Suisse provided non-investment banking services to the subject company (BIIB.OQ) within the past 12 months

Credit Suisse has managed or co-managed a public offering of securities for the subject company (LLY.N, ACIU.OQ, ABBV.N, PFE.N, SHP.L) within the past 12 months.

Credit Suisse has received investment banking related compensation from the subject company (LLY.N, ACIU.OQ, ROG.S, BIIB.OQ, ABBV.N, BMY.N, MRK.N, PFE.N, SHP.L) within the past 12 months

Credit Suisse expects to receive or intends to seek investment banking related compensation from the subject company (LLY.N, ACIU.OQ, ROG.S, BIIB.OQ, ABBV.N, BMY.N, JNJ.N, MRK.N, AZN.L, 4523.T, PFE.N, LUN.CO, SHP.L) within the next 3 months.

Credit Suisse has received compensation for products and services other than investment banking services from the subject company (BIIB.OQ) within the past 12 months

As of the date of this report, Credit Suisse makes a market in the following subject companies (LLY.N, BIIB.OQ, ABBV.N, BMY.N, JNJ.N, MRK.N, PFE.N).

As of the end of the preceding month, Credit Suisse beneficially own 1% or more of a class of common equity securities of (SHP.L).

As of the date of this report, an analyst involved in the preparation of this report has the following material conflict of interest with the subject company (PFE.N). As of the date of this report, an analyst involved in the preparation of this report, Vamil Divan, has following material conflicts of interest with the subject company. The analyst or a member of the analyst's household has a long position in the common stock Pfizer (PFE.N). A member of the analyst's household is an employee of Pfizer (PFE.N).

For other important disclosures concerning companies featured in this report, including price charts, please visit the website at https://rave.credit-suisse.com/disclosures or call +1 (877) 291-2683.

For date and time of production, dissemination and history of recommendation for the subject company(ies) featured in this report, disseminated within the past 12 months, please refer to the link: https://rave.credit-suisse.com/disclosures/view/report?i=263487&v=-45y2krtz57vxa5j14t45439ll .

Important Regional Disclosures

Singapore recipients should contact Credit Suisse AG, Singapore Branch for any matters arising from this research report.

The analyst(s) involved in the preparation of this report may participate in events hosted by the subject company, including site visits. Credit Suisse does not accept or permit analysts to accept payment or reimbursement for travel expenses associated with these events.

Restrictions on certain Canadian securities are indicated by the following abbreviations: NVS--Non-Voting shares; RVS--Restricted Voting Shares; SVS--Subordinate Voting Shares.

Individuals receiving this report from a Canadian investment dealer that is not affiliated with Credit Suisse should be advised that this report may not contain regulatory disclosures the non-affiliated Canadian investment dealer would be required to make if this were its own report.

For Credit Suisse Securities (Canada), Inc.'s policies and procedures regarding the dissemination of equity research, please visit https://www.credit-suisse.com/sites/disclaimers-ib/en/canada-research-policy.html.

The following disclosed European company/ies have estimates that comply with IFRS: (BMY.N, AZN.L, LUN.CO).

Credit Suisse has acted as lead manager or syndicate member in a public offering of securities for the subject company (LLY.N, ACIU.OQ, BIIB.OQ, ABBV.N, BMY.N, MRK.N, AZN.L, PFE.N, SHP.L) within the past 3 years.

Principal is not guaranteed in the case of equities because equity prices are variable.

Commission is the commission rate or the amount agreed with a customer when setting up an account or at any time after that.

This research report is authored by:

Credit Suisse Securities (USA) LLC .................................................................................................................................................... Alethia Young

For Credit Suisse disclosure information on other companies mentioned in this report, please visit the website at https://rave.credit-suisse.com/disclosures or call +1 (877) 291-2683.

60

This report is produced by subsidiaries and affiliates of Credit Suisse operating under its Global Markets Division. For more information on our structure, please use the following link: https://www.credit-suisse.com/who-we-are This report may contain material that is not directed to, or intended for distribution to or use by, any person or entity who is a citizen or resident of or located in any locality, state, country or other jurisdiction where such distribution, publication, availability or use would be contrary to law or regulation or which would subject Credit Suisse or its affiliates ("CS") to any registration or licensing requirement within such jurisdiction. All material presented in this report, unless specifically indicated otherwise, is under copyright to CS. None of the material, nor its content, nor any copy of it, may be altered in any way, transmitted to, copied or distributed to any other party, without the prior express written permission of CS. All trademarks, service marks and logos used in this report are trademarks or service marks or registered trademarks or service marks of CS or its affiliates.The information, tools and material presented in this report are provided to you for information purposes only and are not to be used or considered as an offer or the solicitation of an offer to sell or to buy or subscribe for securities or other financial instruments. CS may not have taken any steps to ensure that the securities referred to in this report are suitable for any particular investor. CS will not treat recipients of this report as its customers by virtue of their receiving this report. The investments and services contained or referred to in this report may not be suitable for you and it is recommended that you consult an independent investment advisor if you are in doubt about such investments or investment services. Nothing in this report constitutes investment, legal, accounting or tax advice, or a representation that any investment or strategy is suitable or appropriate to your individual circumstances, or otherwise constitutes a personal recommendation to you. CS does not advise on the tax consequences of investments and you are advised to contact an independent tax adviser. Please note in particular that the bases and levels of taxation may change. Information and opinions presented in this report have been obtained or derived from sources believed by CS to be reliable, but CS makes no representation as to their accuracy or completeness. CS accepts no liability for loss arising from the use of the material presented in this report, except that this exclusion of liability does not apply to the extent that such liability arises under specific statutes or regulations applicable to CS. This report is not to be relied upon in substitution for the exercise of independent judgment. CS may have issued, and may in the future issue, other communications that are inconsistent with, and reach different conclusions from, the information presented in this report. Those communications reflect the different assumptions, views and analytical methods of the analysts who prepared them and CS is under no obligation to ensure that such other communications are brought to the attention of any recipient of this report. Some investments referred to in this report will be offered solely by a single entity and in the case of some investments solely by CS, or an associate of CS or CS may be the only market maker in such investments. Past performance should not be taken as an indication or guarantee of future performance, and no representation or warranty, express or implied, is made regarding future performance. Information, opinions and estimates contained in this report reflect a judgment at its original date of publication by CS and are subject to change without notice. The price, value of and income from any of the securities or financial instruments mentioned in this report can fall as well as rise. The value of securities and financial instruments is subject to exchange rate fluctuation that may have a positive or adverse effect on the price or income of such securities or financial instruments. Investors in securities such as ADR's, the values of which are influenced by currency volatility, effectively assume this risk. Structured securities are complex instruments, typically involve a high degree of risk and are intended for sale only to sophisticated investors who are capable of understanding and assuming the risks involved. The market value of any structured security may be affected by changes in economic, financial and political factors (including, but not limited to, spot and forward interest and exchange rates), time to maturity, market conditions and volatility, and the credit quality of any issuer or reference issuer. Any investor interested in purchasing a structured product should conduct their own investigation and analysis of the product and consult with their own professional advisers as to the risks involved in making such a purchase. Some investments discussed in this report may have a high level of volatility. High volatility investments may experience sudden and large falls in their value causing losses when that investment is realised. Those losses may equal your original investment. Indeed, in the case of some investments the potential losses may exceed the amount of initial investment and, in such circumstances, you may be required to pay more money to support those losses. Income yields from investments may fluctuate and, in consequence, initial capital paid to make the investment may be used as part of that income yield. Some investments may not be readily realisable and it may be difficult to sell or realise those investments, similarly it may prove difficult for you to obtain reliable information about the value, or risks, to which such an investment is exposed. This report may provide the addresses of, or contain hyperlinks to, websites. Except to the extent to which the report refers to website material of CS, CS has not reviewed any such site and takes no responsibility for the content contained therein. Such address or hyperlink (including addresses or hyperlinks to CS's own website material) is provided solely for your convenience and information and the content of any such website does not in any way form part of this document. Accessing such website or following such link through this report or CS's website shall be at your own risk.

This report is issued and distributed in European Union (except Switzerland): by Credit Suisse Securities (Europe) Limited, One Cabot Square, London E14 4QJ, England, which is authorised by the Prudential Regulation Authority and regulated by the Financial Conduct Authority and the Prudential Regulation Authority. Germany: Credit Suisse Securities (Europe) Limited Niederlassung Frankfurt am Main regulated by the Bundesanstalt fuer Finanzdienstleistungsaufsicht ("BaFin"). United States and Canada: Credit Suisse Securities (USA) LLC; Switzerland: Credit Suisse AG; Brazil: Banco de Investimentos Credit Suisse (Brasil) S.A or its affiliates; Mexico: Banco Credit Suisse (México), S.A. (transactions related to the securities mentioned in this report will only be effected in compliance with applicable regulation); Japan: by Credit Suisse Securities (Japan) Limited, Financial Instruments Firm, Director-General of Kanto Local Finance Bureau ( Kinsho) No. 66, a member of Japan Securities Dealers Association, The Financial Futures Association of Japan, Japan Investment Advisers Association, Type II Financial Instruments Firms Association; Hong Kong: Credit Suisse (Hong Kong) Limited; Australia: Credit Suisse Equities (Australia) Limited; Thailand: Credit Suisse Securities (Thailand) Limited, regulated by the Office of the Securities and Exchange Commission, Thailand, having registered address at 990 Abdulrahim Place, 27th Floor, Unit 2701, Rama IV Road, Silom, Bangrak, Bangkok10500, Thailand, Tel. +66 2614 6000; Malaysia: Credit Suisse Securities (Malaysia) Sdn Bhd, Credit Suisse AG, Singapore Branch; India: Credit Suisse Securities (India) Private Limited (CIN no.U67120MH1996PTC104392) regulated by the Securities and Exchange Board of India as Research Analyst (registration no. INH 000001030) and as Stock Broker (registration no. INB230970637; INF230970637; INB010970631; INF010970631), having registered address at 9th Floor, Ceejay House, Dr.A.B. Road, Worli, Mumbai - 18, India, T- +91-22 6777 3777; South Korea: Credit Suisse Securities (Europe) Limited, Seoul Branch; Taiwan: Credit Suisse AG Taipei Securities Branch; Indonesia: PT Credit Suisse Securities Indonesia; Philippines: Credit Suisse Securities (Philippines ) Inc., and elsewhere in the world by the relevant authorised affiliate of the above. Additional Regional Disclaimers Hong Kong: Credit Suisse (Hong Kong) Limited ("CSHK") is licensed and regulated by the Securities and Futures Commission of Hong Kong under the laws of Hong Kong, which differ from Australian laws. CSHKL does not hold an Australian financial services licence (AFSL) and is exempt from the requirement to hold an AFSL under the Corporations Act 2001 (the Act) under Class Order 03/1103 published by the ASIC in respect of financial services provided to Australian wholesale clients (within the meaning of section 761G of the Act). Research on Taiwanese securities produced by Credit Suisse AG, Taipei Securities Branch has been prepared by a registered Senior Business Person. Malaysia: Research provided to residents of Malaysia is authorised by the Head of Research for Credit Suisse Securities (Malaysia) Sdn Bhd, to whom they should direct any queries on +603 2723 2020. Singapore: This report has been prepared and issued for distribution in Singapore to institutional investors, accredited investors and expert investors (each as defined under the Financial Advisers Regulations) only, and is also distributed by Credit Suisse AG, Singapore branch to overseas investors (as defined under the Financial Advisers Regulations). By virtue of your status as an institutional investor, accredited investor, expert investor or overseas investor, Credit Suisse AG, Singapore branch is exempted from complying with certain compliance requirements under the Financial Advisers Act, Chapter 110 of Singapore (the "FAA"), the Financial Advisers Regulations and the relevant Notices and Guidelines issued thereunder, in respect of any financial advisory service which Credit Suisse AG, Singapore branch may provide to you. UAE: This information is being distributed by Credit Suisse AG (DIFC Branch), duly licensed and regulated by the Dubai Financial Services Authority (“DFSA”). Related financial services or products are only made available to Professional Clients or Market Counterparties, as defined by the DFSA, and are not intended for any other persons. Credit Suisse AG (DIFC Branch) is located on Level 9 East, The Gate Building, DIFC, Dubai, United Arab Emirates. EU: This report has been produced by subsidiaries and affiliates of Credit Suisse operating under its Global Markets Division This research may not conform to Canadian disclosure requirements. In jurisdictions where CS is not already registered or licensed to trade in securities, transactions will only be effected in accordance with applicable securities legislation, which will vary from jurisdiction to jurisdiction and may require that the trade be made in accordance with applicable exemptions from registration or licensing requirements. Non-US customers wishing to effect a transaction should contact a CS entity in their local jurisdiction unless governing law permits otherwise. US customers wishing to effect a transaction should do so only by contacting a representative at Credit Suisse Securities (USA) LLC in the US. Please note that this research was originally prepared and issued by CS for distribution to their market professional and institutional investor customers. Recipients who are not market professional or institutional investor customers of CS should seek the advice of their independent financial advisor prior to taking any investment decision based on this report or for any necessary explanation of its contents. This research may relate to investments or services of a person outside of the UK or to other matters which are not authorised by the Prudential Regulation Authority and regulated by the Financial Conduct Authority and the Prudential Regulation Authority or in respect of which the protections of the Prudential Regulation Authority and Financial Conduct Authority for private customers and/or the UK compensation scheme may not be available, and further details as to where this may be the case are available upon request in respect of this report. CS may provide various services to US municipal entities or obligated persons ("municipalities"), including suggesting individual transactions or trades and entering into such transactions. Any services CS provides to municipalities are not viewed as "advice" within the meaning of Section 975 of the Dodd-Frank Wall Street Reform and Consumer Protection Act. CS is providing any such services and related information solely on an arm's length basis and not as an advisor or fiduciary to the municipality. In connection with the provision of the any such services, there is no agreement, direct or indirect, between any municipality (including the officials,management, employees or agents thereof) and CS for CS to provide advice to the municipality. Municipalities should consult with their financial, accounting and legal advisors regarding any such services provided by CS. In addition, CS is not acting for direct or indirect compensation to solicit the municipality on behalf of an unaffiliated broker, dealer, municipal securities dealer, municipal advisor, or investment adviser for the purpose of obtaining or retaining an engagement by the municipality for or in connection with Municipal Financial Products, the issuance of municipal securities, or of an investment adviser to provide investment advisory services to or on behalf of the municipality. If this report is being distributed by a financial institution other than Credit Suisse AG, or its affiliates, that financial institution is solely responsible for distribution. Clients of that institution should contact that institution to effect a transaction in the securities mentioned in this report or require further information. This report does not constitute investment advice by Credit Suisse to the clients of the distributing financial institution, and neither Credit Suisse AG, its affiliates, and their respective officers, directors and employees accept any liability whatsoever for any direct or consequential loss arising from their use of this report or its content. Principal is not guaranteed. Commission is the commission rate or the amount agreed with a customer when setting up an account or at any time after that. Copyright © 2016 CREDIT SUISSE AG and/or its affiliates. All rights reserved.

Investment principal on bonds can be eroded depending on sale price or market price. In addition, there are bonds on which investment principal can be eroded due to changes in redemption amounts. Care is required when investing in such instruments.

When you purchase non-listed Japanese fixed income securities (Japanese government bonds, Japanese municipal bonds, Japanese government guaranteed bonds, Japanese corporate bonds) from CS as a seller, you will be requested to pay the purchase price only