Credit Logement · This publication does not announce a credit rating action. For any credit...

8

FINANCIAL INSTITUTIONS ISSUER PROFILE 2 November 2017 TABLE OF CONTENTS Company Overview 1 Financial Highlights 2 Business Description 2 Distribution Channels 3 Ownership Structure 3 Subsidiaries 4 Company Management 4 Related Websites and Information Sources 6 Moody’s Related Research 6 Contacts Andreea Prodea +33.1.5330.1055 Associate Analyst [email protected] Yasuko Nakamura +33.1.5330.1030 VP-Sr Credit Officer [email protected] Benjamin Serra +33.1.5330.1073 VP-Sr Credit Officer [email protected] CLIENT SERVICES Americas 1-212-553-1653 Asia Pacific 852-3551-3077 Japan 81-3-5408-4100 EMEA 44-20-7772-5454 Credit Logement Key Facts and Statistics - FY December 2016 Company Overview Crédit Logement is a Paris-based financial institution, which, through its shareholders, is the leading provider in France of guarantees for non-mortgage-backed residential housing loans to individuals. As of 31 December 2016, Crédit Logement guaranteed approximately one third of the domestic home loans (including traditional mortgage loans) originated during the year and around 30% of the entire stock of residential housing loans (excluding loan renegotiation flows) in France. At year-end 2016, the institution’s share of outstanding home loan guarantees accounted for approximately 51%. Crédit Logement has opted for the new licence of “Société de Financement” (financing company) provided for under L.511-11 II of the French Monetary and Financial Code following the implementation of CRD IV starting 1 January 2014. The institution has to comply with banking regulations (solvency, liquidity, etc.), and it is supervised by the French supervisory authority (Autorité de Contrôle prudentiel et de Régulation - ACPR). As of 31 December 2016, the institution reported an unconsolidated asset base of €10.6 billion, and an off-balance-sheet guaranteed loan portfolio of €301.1 billion, which is reflective of its core activity as a guarantor. Crédit Logement was incorporated in 1975. Its shareholders are French financial institutions that offer “prêts cautionnés”. They comprise some of the largest participants in the French banking sector, including BNP Paribas, Crédit Agricole, LCL – Le Crédit Lyonnais, Société Générale/Crédit du Nord, Crédit Mutuel/CIC, SF2 – Groupe La Banque Postale, and HSBC France. At year-end 2016, each of the institution’s four largest shareholders (BNP Paribas, Crédit Agricole, LCL – Le Crédit Lyonnais and Société Générale/Crédit du Nord) held a 16.5% stake in the institution. Source: Company Report (annual report Dec 2016), Moody’s research

Transcript of Credit Logement · This publication does not announce a credit rating action. For any credit...

FINANCIAL INSTITUTIONS

ISSUER PROFILE2 November 2017

TABLE OF CONTENTSCompany Overview 1Financial Highlights 2Business Description 2Distribution Channels 3Ownership Structure 3Subsidiaries 4Company Management 4Related Websites and InformationSources 6Moody’s Related Research 6

Contacts

Andreea Prodea +33.1.5330.1055Associate [email protected]

Yasuko Nakamura +33.1.5330.1030VP-Sr Credit [email protected]

Benjamin Serra +33.1.5330.1073VP-Sr Credit [email protected]

CLIENT SERVICES

Americas 1-212-553-1653

Asia Pacific 852-3551-3077

Japan 81-3-5408-4100

EMEA 44-20-7772-5454

Credit LogementKey Facts and Statistics - FY December 2016

Company OverviewCrédit Logement is a Paris-based financial institution, which, through its shareholders, is theleading provider in France of guarantees for non-mortgage-backed residential housing loansto individuals. As of 31 December 2016, Crédit Logement guaranteed approximately onethird of the domestic home loans (including traditional mortgage loans) originated duringthe year and around 30% of the entire stock of residential housing loans (excluding loanrenegotiation flows) in France. At year-end 2016, the institution’s share of outstanding homeloan guarantees accounted for approximately 51%.

Crédit Logement has opted for the new licence of “Société de Financement” (financingcompany) provided for under L.511-11 II of the French Monetary and Financial Code followingthe implementation of CRD IV starting 1 January 2014. The institution has to comply withbanking regulations (solvency, liquidity, etc.), and it is supervised by the French supervisoryauthority (Autorité de Contrôle prudentiel et de Régulation - ACPR).

As of 31 December 2016, the institution reported an unconsolidated asset base of €10.6billion, and an off-balance-sheet guaranteed loan portfolio of €301.1 billion, which isreflective of its core activity as a guarantor.

Crédit Logement was incorporated in 1975. Its shareholders are French financial institutionsthat offer “prêts cautionnés”. They comprise some of the largest participants in the Frenchbanking sector, including BNP Paribas, Crédit Agricole, LCL – Le Crédit Lyonnais, SociétéGénérale/Crédit du Nord, Crédit Mutuel/CIC, SF2 – Groupe La Banque Postale, and HSBCFrance. At year-end 2016, each of the institution’s four largest shareholders (BNP Paribas,Crédit Agricole, LCL – Le Crédit Lyonnais and Société Générale/Crédit du Nord) held a 16.5%stake in the institution.

Source: Company Report (annual report Dec 2016), Moody’s research

MOODY'S INVESTORS SERVICE FINANCIAL INSTITUTIONS

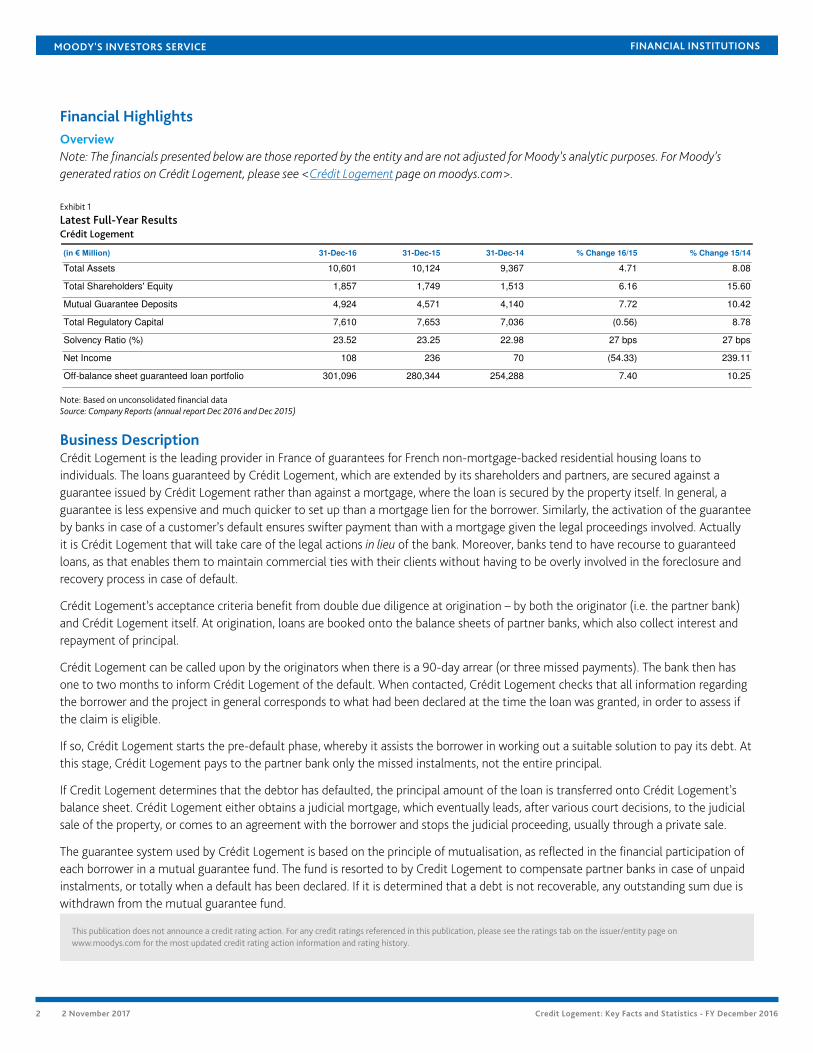

Financial HighlightsOverviewNote: The financials presented below are those reported by the entity and are not adjusted for Moody’s analytic purposes. For Moody’sgenerated ratios on Crédit Logement, please see <Crédit Logement page on moodys.com>.

Exhibit 1

Latest Full-Year ResultsCrédit Logement

(in € Million) 31-Dec-16 31-Dec-15 31-Dec-14 % Change 16/15 % Change 15/14

Total Assets 10,601 10,124 9,367 4.71 8.08

Total Shareholders' Equity 1,857 1,749 1,513 6.16 15.60

Mutual Guarantee Deposits 4,924 4,571 4,140 7.72 10.42

Total Regulatory Capital 7,610 7,653 7,036 (0.56) 8.78

Solvency Ratio (%) 23.52 23.25 22.98 27 bps 27 bps

Net Income 108 236 70 (54.33) 239.11

Off-balance sheet guaranteed loan portfolio 301,096 280,344 254,288 7.40 10.25

Note: Based on unconsolidated financial dataSource: Company Reports (annual report Dec 2016 and Dec 2015)

Business DescriptionCrédit Logement is the leading provider in France of guarantees for French non-mortgage-backed residential housing loans toindividuals. The loans guaranteed by Crédit Logement, which are extended by its shareholders and partners, are secured against aguarantee issued by Crédit Logement rather than against a mortgage, where the loan is secured by the property itself. In general, aguarantee is less expensive and much quicker to set up than a mortgage lien for the borrower. Similarly, the activation of the guaranteeby banks in case of a customer’s default ensures swifter payment than with a mortgage given the legal proceedings involved. Actuallyit is Crédit Logement that will take care of the legal actions in lieu of the bank. Moreover, banks tend to have recourse to guaranteedloans, as that enables them to maintain commercial ties with their clients without having to be overly involved in the foreclosure andrecovery process in case of default.

Crédit Logement’s acceptance criteria benefit from double due diligence at origination – by both the originator (i.e. the partner bank)and Crédit Logement itself. At origination, loans are booked onto the balance sheets of partner banks, which also collect interest andrepayment of principal.

Crédit Logement can be called upon by the originators when there is a 90-day arrear (or three missed payments). The bank then hasone to two months to inform Crédit Logement of the default. When contacted, Crédit Logement checks that all information regardingthe borrower and the project in general corresponds to what had been declared at the time the loan was granted, in order to assess ifthe claim is eligible.

If so, Crédit Logement starts the pre-default phase, whereby it assists the borrower in working out a suitable solution to pay its debt. Atthis stage, Crédit Logement pays to the partner bank only the missed instalments, not the entire principal.

If Credit Logement determines that the debtor has defaulted, the principal amount of the loan is transferred onto Crédit Logement’sbalance sheet. Crédit Logement either obtains a judicial mortgage, which eventually leads, after various court decisions, to the judicialsale of the property, or comes to an agreement with the borrower and stops the judicial proceeding, usually through a private sale.

The guarantee system used by Crédit Logement is based on the principle of mutualisation, as reflected in the financial participation ofeach borrower in a mutual guarantee fund. The fund is resorted to by Credit Logement to compensate partner banks in case of unpaidinstalments, or totally when a default has been declared. If it is determined that a debt is not recoverable, any outstanding sum due iswithdrawn from the mutual guarantee fund.

This publication does not announce a credit rating action. For any credit ratings referenced in this publication, please see the ratings tab on the issuer/entity page onwww.moodys.com for the most updated credit rating action information and rating history.

2 2 November 2017 Credit Logement: Key Facts and Statistics - FY December 2016

MOODY'S INVESTORS SERVICE FINANCIAL INSTITUTIONS

Thus, the mutual guarantee fund – constituted to cope with the portfolio’s credit risk – covers the loss ratio for the guarantee portfolioon residential loans.

In accordance with Credit Logement’s mutual guarantee fund rules, the participation of each borrower may be reimbursed after CréditLogement’s commitment has been released with the provision that Crédit Logement would deduct – on a pro rata basis – the share ofthe fund that will not be available given the portfolio’s expected loss.

Crédit Logement benefits from a commitment from its shareholders to maintain its solvency at the required level. At year-end 2016,this commitment amounted to €2.6 billion.

Crédit Logement also manages debt collection, including guaranteed and third-party debts such as non-guaranteed residential debts,mainly on behalf of one of its main shareholders.

Crédit Logement has two main sources of revenues – commission charged to individual borrowers on “prêts cautionnés” and incomefrom the investment of its capital in interbank deposits, which are mainly placed at its shareholders.

Source: Company Report (annual report Dec 2016), Moody’s research

Distribution ChannelsCrédit Logement is headquartered in Paris. The institution distributes its products and services through the networks of over 230partner (shareholder) banks.

As the leading provider of guarantees on housing loans, Crédit Logement has a well-established and strong market position withinthe French banking sector. As of 31 December 2016, Crédit Logement guaranteed approximately one third of the domestic homeloans (including traditional mortgage loans) originated during the year and around 30% of the entire stock of residential housingloans (excluding loan renegotiation flows) in France. At year-end 2016, the institution’s share of outstanding home loan guaranteesaccounted for approximately 51%.

Source: Company Report (annual report Dec 2016), Moody’s research, Company data

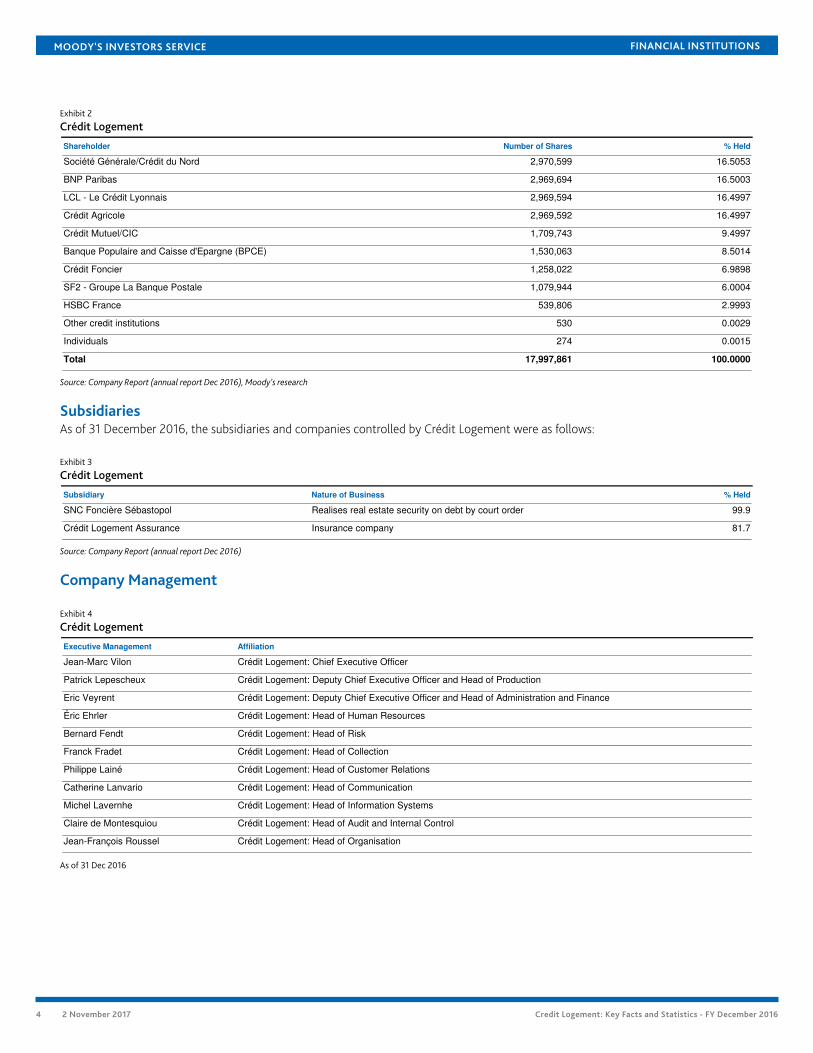

Ownership StructureCrédit Logement is a private limited company whose main shareholders are French financial institutions that offer “prêts cautionnés”,including BNP Paribas, Crédit Agricole, LCL – Le Crédit Lyonnais, Société Générale/Crédit du Nord, Crédit Mutuel/CIC, SF2 – GroupeLa Banque Postale and HSBC France. In 2016, each of the institution’s four largest shareholders (BNP Paribas, Crédit Agricole, LCL – LeCrédit Lyonnais and Société Générale/Crédit du Nord) held a 16.5% stake in the institution.

The “prêts cautionnés” issued by Crédit Logement’s shareholders are eligible for refinancing through one of the following: Caissede Refinancement de l’Habitat (a credit institution that funds French residential home loans), French covered bonds (“obligationsfoncières” and “obligations à l’habitat”), or residential-mortgage-backed securities.

As of 31 December 2016, the shareholding structure of Crédit Logement was as follows:

3 2 November 2017 Credit Logement: Key Facts and Statistics - FY December 2016

MOODY'S INVESTORS SERVICE FINANCIAL INSTITUTIONS

Exhibit 2

Crédit Logement

Shareholder Number of Shares % Held

Société Générale/Crédit du Nord 2,970,599 16.5053

BNP Paribas 2,969,694 16.5003

LCL - Le Crédit Lyonnais 2,969,594 16.4997

Crédit Agricole 2,969,592 16.4997

Crédit Mutuel/CIC 1,709,743 9.4997

Banque Populaire and Caisse d'Epargne (BPCE) 1,530,063 8.5014

Crédit Foncier 1,258,022 6.9898

SF2 - Groupe La Banque Postale 1,079,944 6.0004

HSBC France 539,806 2.9993

Other credit institutions 530 0.0029

Individuals 274 0.0015

Total 17,997,861 100.0000

Source: Company Report (annual report Dec 2016), Moody’s research

SubsidiariesAs of 31 December 2016, the subsidiaries and companies controlled by Crédit Logement were as follows:

Exhibit 3

Crédit Logement

Subsidiary Nature of Business % Held

SNC Foncière Sébastopol Realises real estate security on debt by court order 99.9

Crédit Logement Assurance Insurance company 81.7

Source: Company Report (annual report Dec 2016)

Company Management

Exhibit 4

Crédit Logement

Executive Management Affiliation

Jean-Marc Vilon Crédit Logement: Chief Executive Officer

Patrick Lepescheux Crédit Logement: Deputy Chief Executive Officer and Head of Production

Eric Veyrent Crédit Logement: Deputy Chief Executive Officer and Head of Administration and Finance

Éric Ehrler Crédit Logement: Head of Human Resources

Bernard Fendt Crédit Logement: Head of Risk

Franck Fradet Crédit Logement: Head of Collection

Philippe Lainé Crédit Logement: Head of Customer Relations

Catherine Lanvario Crédit Logement: Head of Communication

Michel Lavernhe Crédit Logement: Head of Information Systems

Claire de Montesquiou Crédit Logement: Head of Audit and Internal Control

Jean-François Roussel Crédit Logement: Head of Organisation

As of 31 Dec 2016

4 2 November 2017 Credit Logement: Key Facts and Statistics - FY December 2016

MOODY'S INVESTORS SERVICE FINANCIAL INSTITUTIONS

Exhibit 5

Crédit LogementBoard of Directors as at 31 December 2016

Board of Directors Affiliation

Albert Boclé Crédit Logement: Chairman of the Board of Directors

Yves Martrenchar Crédit Logement: Honorary Chairman of the Board of Directors

Julien Niwinski (representative of BNP Paribas) Crédit Logement: Member of the Board of Directors;

BNP Paribas: Head of Finance, Retail Banking in France

Olivier Belorgey (representative of Crédit Agricole SA) Crédit Logement: Member of the Board of Directors;

Credit Agricole SA: Chief Financial Officer

Emmanuelle Yannakis (representative of LCL – Le Crédit Lyonnais)

Crédit Logement: Member of the Board of Directors;

LCL – Le Crédit Lyonnais: Chief Financial Officer and in charge of Subsidiairies

Auvray-Magnin (representative of Société Générale) Crédit Logement: Member of the Board of Directors;

Société Générale: Head of Market Relations and Regulations, Retail Banking in France

Sophie Olivier (representative of Caisse Centrale Du

Crédit Mutuel)

Crédit Logement: Member of the Board of Directors;

Caisse Centrale Du Crédit Mutuel: Deputy Head of Retail Banking

Sylvain Petit (representative of BPCE) Crédit Logement: Member of the Board of Directors;

BPCE: Head of Strategy

Bruno Deletré (representative of Crédit Foncier) Crédit Logement: Member of the Board of Directors;

Crédit Foncier: Chief Executive Officer

Jean-Marc Tassain (representative of SF2 - Groupe La

Banque Postale)

Crédit Logement: Member of the Board of Directors;

SF2 - Groupe La Banque Postale: Head of Partnership Development and Head of Market Relations

Vincent de Palma (representative of HSBC France) Crédit Logement: Member of the Board of Directors;

HSBC France: Head of Strategy and Head of Customer Offer Service and Wealth Management

Éric Pinault Crédit Logement: Member of the Board of Directors;

Fédération Nationale du Crédit Agricole: Chief Financial Officer and Risk

Brigitte Geffard Crédit Logement: Member of the Board of Directors;

LCL, Le Crédit Lyonnais: Head of Loans Acceptance and Debt Collection

Dominique Fiabane Crédit Logement: Member of the Board of Directors;

BNP Paribas: Head of Retail Banking in France

As of 31 Dec 2016Source: Company Report (annual report Dec 2016)

5 2 November 2017 Credit Logement: Key Facts and Statistics - FY December 2016

MOODY'S INVESTORS SERVICE FINANCIAL INSTITUTIONS

Related Websites and Information SourcesFor additional information, please see:

The company’s website

» www.creditlogement.fr

MOODY’S has provided links or references to third party World Wide Websites or URLs (“Links or References”) solely for your convenience in locating related information and services. Thewebsites reached through these Links or References have not necessarily been reviewed by MOODY’S, and are maintained by a third party over which MOODY’S exercises no control. Accordingly,MOODY’S expressly disclaims any responsibility or liability for the content, the accuracy of the information, and/or quality of products or services provided by or advertised on any third party website accessed via a Link or Reference. Moreover, a Link or Reference does not imply an endorsement of any third party, any website, or the products or services provided by any third party.

Moody’s Related ResearchIssuer Page on Moodys.com

» Credit Logement

Credit Opinion

» Credit Logement, July 2017

Banking System Outlook

» Banking System Outlook - France: Improving economy and steady loan growth support stable outlook, July 2017 (1079907)

Sector Comment

» France's Change in Banks' Hierarchy of Claims Increases Clarity of Resolutions, January 2016

» France Adopts European Bank Recovery and Resolution Directive, a Credit Negative, August 2015

Rating Methodology

» Mortgage Insurers, April 2016

Other

» Banking: France Macro Profile: Strong +, December 2016 (1012417)

» New Rules for France’s Specialised Financial Institutions the Sociétés Financières: Frequently Asked Questions, January 2014(163477)

To access any of these reports, click on the entry above. Note that these references are current as of the date of publication of this report and that more recent reports may be available on theissuer’s page . All research may not be available to all clients.

6 2 November 2017 Credit Logement: Key Facts and Statistics - FY December 2016

MOODY'S INVESTORS SERVICE FINANCIAL INSTITUTIONS

© 2017 Moody’s Corporation, Moody’s Investors Service, Inc., Moody’s Analytics, Inc. and/or their licensors and affiliates (collectively, “MOODY’S”). All rights reserved.

CREDIT RATINGS ISSUED BY MOODY'S INVESTORS SERVICE, INC. AND ITS RATINGS AFFILIATES (“MIS”) ARE MOODY’S CURRENT OPINIONS OF THE RELATIVE FUTURE CREDITRISK OF ENTITIES, CREDIT COMMITMENTS, OR DEBT OR DEBT-LIKE SECURITIES, AND MOODY’S PUBLICATIONS MAY INCLUDE MOODY’S CURRENT OPINIONS OF THERELATIVE FUTURE CREDIT RISK OF ENTITIES, CREDIT COMMITMENTS, OR DEBT OR DEBT-LIKE SECURITIES. MOODY’S DEFINES CREDIT RISK AS THE RISK THAT AN ENTITYMAY NOT MEET ITS CONTRACTUAL, FINANCIAL OBLIGATIONS AS THEY COME DUE AND ANY ESTIMATED FINANCIAL LOSS IN THE EVENT OF DEFAULT. CREDIT RATINGSDO NOT ADDRESS ANY OTHER RISK, INCLUDING BUT NOT LIMITED TO: LIQUIDITY RISK, MARKET VALUE RISK, OR PRICE VOLATILITY. CREDIT RATINGS AND MOODY’SOPINIONS INCLUDED IN MOODY’S PUBLICATIONS ARE NOT STATEMENTS OF CURRENT OR HISTORICAL FACT. MOODY’S PUBLICATIONS MAY ALSO INCLUDE QUANTITATIVEMODEL-BASED ESTIMATES OF CREDIT RISK AND RELATED OPINIONS OR COMMENTARY PUBLISHED BY MOODY’S ANALYTICS, INC. CREDIT RATINGS AND MOODY’SPUBLICATIONS DO NOT CONSTITUTE OR PROVIDE INVESTMENT OR FINANCIAL ADVICE, AND CREDIT RATINGS AND MOODY’S PUBLICATIONS ARE NOT AND DO NOTPROVIDE RECOMMENDATIONS TO PURCHASE, SELL, OR HOLD PARTICULAR SECURITIES. NEITHER CREDIT RATINGS NOR MOODY’S PUBLICATIONS COMMENT ON THESUITABILITY OF AN INVESTMENT FOR ANY PARTICULAR INVESTOR. MOODY’S ISSUES ITS CREDIT RATINGS AND PUBLISHES MOODY’S PUBLICATIONS WITH THE EXPECTATIONAND UNDERSTANDING THAT EACH INVESTOR WILL, WITH DUE CARE, MAKE ITS OWN STUDY AND EVALUATION OF EACH SECURITY THAT IS UNDER CONSIDERATION FORPURCHASE, HOLDING, OR SALE.

MOODY’S CREDIT RATINGS AND MOODY’S PUBLICATIONS ARE NOT INTENDED FOR USE BY RETAIL INVESTORS AND IT WOULD BE RECKLESS AND INAPPROPRIATE FORRETAIL INVESTORS TO USE MOODY’S CREDIT RATINGS OR MOODY’S PUBLICATIONS WHEN MAKING AN INVESTMENT DECISION. IF IN DOUBT YOU SHOULD CONTACTYOUR FINANCIAL OR OTHER PROFESSIONAL ADVISER. ALL INFORMATION CONTAINED HEREIN IS PROTECTED BY LAW, INCLUDING BUT NOT LIMITED TO, COPYRIGHT LAW,AND NONE OF SUCH INFORMATION MAY BE COPIED OR OTHERWISE REPRODUCED, REPACKAGED, FURTHER TRANSMITTED, TRANSFERRED, DISSEMINATED, REDISTRIBUTEDOR RESOLD, OR STORED FOR SUBSEQUENT USE FOR ANY SUCH PURPOSE, IN WHOLE OR IN PART, IN ANY FORM OR MANNER OR BY ANY MEANS WHATSOEVER, BY ANYPERSON WITHOUT MOODY’S PRIOR WRITTEN CONSENT.

All information contained herein is obtained by MOODY’S from sources believed by it to be accurate and reliable. Because of the possibility of human or mechanical error as wellas other factors, however, all information contained herein is provided “AS IS” without warranty of any kind. MOODY'S adopts all necessary measures so that the information ituses in assigning a credit rating is of sufficient quality and from sources MOODY'S considers to be reliable including, when appropriate, independent third-party sources. However,MOODY’S is not an auditor and cannot in every instance independently verify or validate information received in the rating process or in preparing the Moody’s publications.

To the extent permitted by law, MOODY’S and its directors, officers, employees, agents, representatives, licensors and suppliers disclaim liability to any person or entity for anyindirect, special, consequential, or incidental losses or damages whatsoever arising from or in connection with the information contained herein or the use of or inability to use anysuch information, even if MOODY’S or any of its directors, officers, employees, agents, representatives, licensors or suppliers is advised in advance of the possibility of such losses ordamages, including but not limited to: (a) any loss of present or prospective profits or (b) any loss or damage arising where the relevant financial instrument is not the subject of aparticular credit rating assigned by MOODY’S.

To the extent permitted by law, MOODY’S and its directors, officers, employees, agents, representatives, licensors and suppliers disclaim liability for any direct or compensatorylosses or damages caused to any person or entity, including but not limited to by any negligence (but excluding fraud, willful misconduct or any other type of liability that, for theavoidance of doubt, by law cannot be excluded) on the part of, or any contingency within or beyond the control of, MOODY’S or any of its directors, officers, employees, agents,representatives, licensors or suppliers, arising from or in connection with the information contained herein or the use of or inability to use any such information.

NO WARRANTY, EXPRESS OR IMPLIED, AS TO THE ACCURACY, TIMELINESS, COMPLETENESS, MERCHANTABILITY OR FITNESS FOR ANY PARTICULAR PURPOSE OF ANY SUCHRATING OR OTHER OPINION OR INFORMATION IS GIVEN OR MADE BY MOODY’S IN ANY FORM OR MANNER WHATSOEVER.

Moody’s Investors Service, Inc., a wholly-owned credit rating agency subsidiary of Moody’s Corporation (“MCO”), hereby discloses that most issuers of debt securities (includingcorporate and municipal bonds, debentures, notes and commercial paper) and preferred stock rated by Moody’s Investors Service, Inc. have, prior to assignment of any rating,agreed to pay to Moody’s Investors Service, Inc. for appraisal and rating services rendered by it fees ranging from $1,500 to approximately $2,500,000. MCO and MIS also maintainpolicies and procedures to address the independence of MIS’s ratings and rating processes. Information regarding certain affiliations that may exist between directors of MCO andrated entities, and between entities who hold ratings from MIS and have also publicly reported to the SEC an ownership interest in MCO of more than 5%, is posted annually atwww.moodys.com under the heading “Investor Relations — Corporate Governance — Director and Shareholder Affiliation Policy.”

Additional terms for Australia only: Any publication into Australia of this document is pursuant to the Australian Financial Services License of MOODY’S affiliate, Moody’s InvestorsService Pty Limited ABN 61 003 399 657AFSL 336969 and/or Moody’s Analytics Australia Pty Ltd ABN 94 105 136 972 AFSL 383569 (as applicable). This document is intendedto be provided only to “wholesale clients” within the meaning of section 761G of the Corporations Act 2001. By continuing to access this document from within Australia, yourepresent to MOODY’S that you are, or are accessing the document as a representative of, a “wholesale client” and that neither you nor the entity you represent will directly orindirectly disseminate this document or its contents to “retail clients” within the meaning of section 761G of the Corporations Act 2001. MOODY’S credit rating is an opinion asto the creditworthiness of a debt obligation of the issuer, not on the equity securities of the issuer or any form of security that is available to retail investors. It would be recklessand inappropriate for retail investors to use MOODY’S credit ratings or publications when making an investment decision. If in doubt you should contact your financial or otherprofessional adviser.

Additional terms for Japan only: Moody's Japan K.K. (“MJKK”) is a wholly-owned credit rating agency subsidiary of Moody's Group Japan G.K., which is wholly-owned by Moody’sOverseas Holdings Inc., a wholly-owned subsidiary of MCO. Moody’s SF Japan K.K. (“MSFJ”) is a wholly-owned credit rating agency subsidiary of MJKK. MSFJ is not a NationallyRecognized Statistical Rating Organization (“NRSRO”). Therefore, credit ratings assigned by MSFJ are Non-NRSRO Credit Ratings. Non-NRSRO Credit Ratings are assigned by anentity that is not a NRSRO and, consequently, the rated obligation will not qualify for certain types of treatment under U.S. laws. MJKK and MSFJ are credit rating agencies registeredwith the Japan Financial Services Agency and their registration numbers are FSA Commissioner (Ratings) No. 2 and 3 respectively.

MJKK or MSFJ (as applicable) hereby disclose that most issuers of debt securities (including corporate and municipal bonds, debentures, notes and commercial paper) and preferredstock rated by MJKK or MSFJ (as applicable) have, prior to assignment of any rating, agreed to pay to MJKK or MSFJ (as applicable) for appraisal and rating services rendered by it feesranging from JPY200,000 to approximately JPY350,000,000.

MJKK and MSFJ also maintain policies and procedures to address Japanese regulatory requirements.

REPORT NUMBER 1083877

7 2 November 2017 Credit Logement: Key Facts and Statistics - FY December 2016

MOODY'S INVESTORS SERVICE FINANCIAL INSTITUTIONS

CLIENT SERVICES

Americas 1-212-553-1653

Asia Pacific 852-3551-3077

Japan 81-3-5408-4100

EMEA 44-20-7772-5454

8 2 November 2017 Credit Logement: Key Facts and Statistics - FY December 2016