Credit enhancement through nancial engineering: …chitrufernando.oucreate.com/Research...

42

We thank o$cials at Freeport-McMoRan Copper and Gold Inc., especially Charles Goodyear, who stimulated our initial interest in these securities. This paper is not intended to express an opinion on the handling of any situation by Freeport McMoRan Copper and Gold Inc. or any of its a$liates. We are grateful to Gegory W. Brown, Sanjiv Das, Stephen Figlewski, Prem Jain, Kose John, Darius Miller, Thomas H. Noe, Nagpurnanand R. Prabhala, Russ Robins, Barry Schachter, G. William Schwert (the editor), Charles Smithson, Rene H Stulz, Venkat Subramaniam, Sheridan Titman, Peter Tufano, and two referees for useful comments and discussions. We thank Vladimir Gatchev for excellent research assistance. We also thank seminar participants at Boston University, Northeastern University, the 2001 American Finance Association Meetings, the 1998 FMA PACAP Meetings, the 1998 IAFE Conference, the 1998 Chicago Risk Management Conference, the 1998 San Jose Latin American Consortium, and the 1999 HBS-JFE Conference. We remain responsible for all errors. * Corresponding author. Tel.: #1-504-865-5479; fax: #1-504-865-6751. E-mail address: chiddi@tulane.edu (N.K. Chidambaran). Journal of Financial Economics 60 (2001) 487}528 Credit enhancement through "nancial engineering: Freeport McMoRan's gold-denominated depositary shares N.K. Chidambaran*, Chitru S. Fernando, Paul A. Spindt A.B. Freeman School of Business, Tulane University, 7 McAlister Drive, New Orleans, LA 70118, USA Received 3 December 1998; received in revised form 30 November 2000 Abstract In 1993 and 1994, Freeport McMoRan Copper and Gold issued two series of gold- denominated depositary shares to "nance the expansion of its mining capacity in In- donesia. The pricing of these securities re#ected their enhanced credit quality, which arose from the positive correlation between the value of the "rm and the value of the securities. This feature of the securities e!ectively bundles a gold hedge with "nancing. A bundled hedge avoids wealth transfers to senior bondholders, since junior bondholders can e!ec- tively net their bond-related claims on the "rm against their hedge-related liability to the "rm. Such securities cannot be replicated by conventional hedging strategies, and they also mitigate the asset substitution problem. 2001 Elsevier Science S.A. All rights reserved. JEL classixcation: G32; G13 Keywords: Risk management; Credit enhancement; Gold-linked; Hybrid securities 0304-405X/01/$ - see front matter 2001 Elsevier Science S.A. All rights reserved. PII: S 0 3 0 4 - 4 0 5 X ( 0 1 ) 0 0 0 5 1 - 4

Transcript of Credit enhancement through nancial engineering: …chitrufernando.oucreate.com/Research...

�We thank o$cials at Freeport-McMoRan Copper and Gold Inc., especially Charles Goodyear, whostimulated our initial interest in these securities. This paper is not intended to express an opinion on thehandling of any situation by Freeport McMoRan Copper and Gold Inc. or any of its a$liates. We aregrateful to Gegory W. Brown, Sanjiv Das, Stephen Figlewski, Prem Jain, Kose John, Darius Miller,Thomas H. Noe, Nagpurnanand R. Prabhala, Russ Robins, Barry Schachter, G. William Schwert (theeditor), Charles Smithson, ReneH Stulz, Venkat Subramaniam, Sheridan Titman, Peter Tufano, and tworeferees for useful comments and discussions. We thank Vladimir Gatchev for excellent researchassistance. We also thank seminar participants at Boston University, Northeastern University, the 2001American Finance Association Meetings, the 1998 FMA PACAP Meetings, the 1998 IAFE Conference,the 1998 Chicago Risk Management Conference, the 1998 San Jose Latin American Consortium, andthe 1999 HBS-JFE Conference. We remain responsible for all errors.

* Corresponding author. Tel.: #1-504-865-5479; fax: #1-504-865-6751.

E-mail address: [email protected] (N.K. Chidambaran).

Journal of Financial Economics 60 (2001) 487}528

Credit enhancement through "nancialengineering: Freeport McMoRan's

gold-denominated depositary shares�

N.K. Chidambaran*, Chitru S. Fernando, Paul A. Spindt

A.B. Freeman School of Business, Tulane University, 7 McAlister Drive, New Orleans, LA 70118, USA

Received 3 December 1998; received in revised form 30 November 2000

Abstract

In 1993 and 1994, Freeport McMoRan Copper and Gold issued two series of gold-denominated depositary shares to "nance the expansion of its mining capacity in In-donesia. The pricing of these securities re#ected their enhanced credit quality, which arosefrom the positive correlation between the value of the "rm and the value of the securities.This feature of the securities e!ectively bundles a gold hedge with "nancing. A bundledhedge avoids wealth transfers to senior bondholders, since junior bondholders can e!ec-tively net their bond-related claims on the "rm against their hedge-related liability to the"rm. Such securities cannot be replicated by conventional hedging strategies, and they alsomitigate the asset substitution problem. � 2001 Elsevier Science S.A. All rights reserved.

JEL classixcation: G32; G13

Keywords: Risk management; Credit enhancement; Gold-linked; Hybrid securities

0304-405X/01/$ - see front matter � 2001 Elsevier Science S.A. All rights reserved.PII: S 0 3 0 4 - 4 0 5 X ( 0 1 ) 0 0 0 5 1 - 4

1. Introduction

In 1993 and early 1994, Freeport McMoRan Copper and Gold Inc. (tickersymbol FCX) faced a substantial challenge in "nancing the expansion of itsGrasberg gold and copper mine in Irian Jaya, Indonesia. The mine, high in themountains, was the world's largest gold reserve and one of the largest copperreserves. FCX needed to invest heavily to expand mine capacity and achieve theeconomies of scale required to become more competitive. Despite a heavy debtburden and a stock that was trading below the value of its assets, FCXsuccessfully raised $359 million at a favorable "nancing cost through two seriesof gold-linked depositary shares backed by preferred stock. These claims enjoy-ed an enhanced credit quality because the link to gold prices credibly reduceddefault risk. We show that the design of the security allows the bene"ts ofthis credit enhancement to be targeted to the purchasers of the newly issuedsecurities.

The gold depositary shares issued by FCX are similar to a debt instrumentthat has all interest and principal payments in gold. Other gold-mining com-panies have also employed gold-linked "nancing to combine "nancing and riskmanagement needs. Tufano (1993) describes these instruments in general and theactivities of American Barrick in particular. The use of these hybrid instrumentscreates a liability whose value is positively correlated with the value of the "rm,thereby enhancing the credit quality of the depositary shares and enabling FCXto "nance its expansion at a lower cost despite being "nancially constrained.Reducing the costs associated with binding "nancial constraints can be valueincreasing (see Smith and Stulz, 1985; Stulz, 1990; Froot et al., 1993; Mello andParsons, 2000).

A gold-denominated depositary share is a "nancing instrument with anembedded derivative that serves to hedge the exposure to gold price risk. In thispaper, we show how this "nancially engineered security creates value beyondwhat can be achieved by conventional derivatives strategies. Our approach is asfollows. We "rst establish the credit enhancement of the gold-denominateddepositary shares relative to straight bonds. We then contrast bundled hedging,or "nancing bundled with an embedded derivative, with conventional hedging,or the standard risk management strategy of issuing a straight bond andsimultaneously initiating a hedge using derivative contracts. The e!ects of thetwo strategies appear on the surface to be identical. We show that this apparentequivalence is deceptive and that bundled hedging is vastly superior to conven-tional hedging.

The superiority of a bundled hedge arises from two e!ects. First, using"nancial engineering to bundle "nancing and hedging prevents wealth transfersto senior bondholders that arise in the case of a conventional hedge. Bundlingallows the holders of the hybrid security to (e!ectively) o!set the amount theyowe on the bundled derivative contract against the amount they stand to lose on

488 N.K. Chidambaran et al. / Journal of Financial Economics 60 (2001) 487}528

the debt contract when the "rm is in default. This netting feature circumventsthe priority order of the "rm's existing capital structure and allows the bene"tsof credit enhancement to be targeted to particular securities even if thesesecurities are junior. Wealth transfers to senior bondholders arising from creditenhancement are eliminated due to this feature. We refer to this e!ect as targetedrisk management.

Second, bundling signi"cantly mitigates the time inconsistency problem,which arises in the case of a conventional hedge because shareholders have an expost incentive for asset substitution, as shown by Smith and Stulz (1985). Smithand Stulz examine the interaction of the debt "nancing and hedging policies ofan unlevered "rm. They demonstrate that the "rm has strong incentives, oncethe "nancing is completed, to unwind the hedge, transferring wealth frombondholders to stockholders. Since bondholders know this ex ante, they will notfactor the credit enhancement into the pricing unless the "rm is able to convincethem that it will maintain the hedge after the bond sale. But it is di$cult for"rms to credibly precommit to the hedge, making this strategy time-inconsist-ent. We extend the Smith and Stulz analysis to the general case of a levered "rm,where the potential for asset substitution is even greater, exacerbating the timeinconsistency problem. Conventional hedging undertaken to enhance creditquality for new bondholders has the unintended consequence of enhancing thevalue of senior bondholders' claims, which shareholders can recapture byunwinding ex post.

A bundled hedge, however, signi"cantly reduces this problem. Since there areno wealth transfers to senior bondholders in the "rst place, there is less value tobe realized through unwinding the hedge. Unwinding a bundled hedge can alsoimpose additional costs on shareholders. The counterparty to an unwindingtransaction would be junior to existing bondholders under bankruptcy (seeTucker, 1991; Foster, 1995). The counterparty would, therefore, extract a signi"-cant part of the stockholders' surplus associated with the unwinding, via pricingof the derivative contract and/or collateral requirements, to o!set the increase inthe "rm's credit risk. Moreover, as in Mello and Parsons (1995, 2000), unwind-ing using traded short-term derivatives contracts can generate adverse cash#ows, e.g., by requiring the "rm to cover margin cash out#ows without o!settingin#ows, thereby exacerbating "nancial constraints and increasing default risk.The asset substitution problem is therefore mitigated, though not completelyeliminated, by bundled hedging. A bundled hedge also (1) locks in risk manage-ment for the duration of the debt, and (2) could impose reputational costs if the"rm tries to unhedge, further neutralizing any residual incentive the "rm mighthave to unwind the hedge.

Thus, our analysis indicates that a strategy that bundles "nancing andderivatives is superior to a strategy that separates the two transactions. Inaddition, it should be noted that the derivative contract embedded in thegold-denominated depositary shares is of a longer maturity than conventional

N.K. Chidambaran et al. / Journal of Financial Economics 60 (2001) 487}528 489

traded derivative contracts. The short maturity and mark-to-market features ofconventional derivative instruments make it di$cult to replicate the bundledsecurity through a derivatives strategy. For example, when a "rm uses a shortgold futures position together with a straight bond to replicate the gold-linkedsecurity, it will face extremely adverse cash #ow consequences associated withmarking-to-market and rolling over the gold futures positions if the gold priceincreases in the interim. Mello and Parsons (2000) focus on how liquidity andcash #ow timing problems associated with di!erent hedging strategies can a!ecta "rm's value. They argue that a hedge that does not take account of the fundingrequirements associated with it can actually compound liquidity constraintsthat the "rm might face, thereby detracting from the "rm's value instead ofadding to it, as shown by Mello and Parsons (1995) for the case of Metallgesel-lschaft. A replicating derivatives strategy is strictly sub-optimal relative to thegold-linked security.

In theory, any derivatives strategy that allows junior bondholders to have "rstclaims to the cash #ows from the hedge, and which minimizes the ex postincentive for the "rm to unwind the hedge, will achieve credit enhancement. Inpractice, the ability to satisfy these conditions is greatly limited by currentbankruptcy law, standard debt covenants designed to protect seniority, and, asemphasized by Smith and Stulz (1985), the di$culty in preventing unwinding.These constraints are especially critical for levered "rms. Bundling debt witha derivative contract satis"es the conditions for credit enhancement. Our com-parison between FCX's bundled hedge and a conventional hedge is not to showthat such securities are the only way, or even the optimal way, to manage risk.Rather, we use the comparison to highlight the principles that a successful riskmanagement strategy should embody.

Possibly with the intention of building on the success of the two gold issues,FCX later issued a series of silver-denominated shares structured similar to thegold issues. However, FCX's exposure to silver prices was signi"cantly lowerthan its exposure to gold prices as silver is a byproduct of FCX's gold miningoperations and accounts for a much smaller share of its revenue. The value of thegold shares was highly positively correlated with FCX's revenues, whereas thevalue of the silver shares was considerably less so. Nonetheless, the silver issueprovides a useful benchmark against which to gauge the credit enhancement ofthe gold issues.

We analyze the pricing of the depositary shares for evidence of credit enhance-ment using the following approach. We decompose the cash #ow of the deposi-tary shares into the cash #ow of a risky straight bond, a riskless swap for gold orsilver, and a residual component that we call the credit enhancement residual(CER) which captures the value of the option-to-net that comes into the moneywhen the "rm defaults. We benchmark our measurements by setting the CER ofthe silver issue to zero in light of FCX's low exposure to silver price risk. Sincethe gold and silver securities were issued pari passu, we assume that the risky

490 N.K. Chidambaran et al. / Journal of Financial Economics 60 (2001) 487}528

straight bond embedded in them is attributed the same credit quality by themarket. We value the swap using contemporaneous market prices and value thebond at a yield that normalizes the silver CER to zero. We "nd that the GoldSeries I depositary shares incorporate a CER of 3.15% of their market value andthe Gold Series II depositary shares incorporate a CER of 4.68% of their marketvalue.

The higher credit enhancement for the two gold securities arises due to thesigni"cantly positive correlation between the value of the "rm and the value ofthe bundled instrument. Since gold accounts for approximately a third of FCX'srevenues, this is clearly the case for the two gold securities, and as we have noted,not the case for silver. If there were no credit enhancement or if the change incredit quality due to linking were the same for all three securities, the threeCERs should have been identical. This is not what we "nd. The relative pricingof the three securities permits us to conclude that the market was able to identifythis important di!erence for FCX between gold and silver, lending support toour conceptual arguments.

We organize the rest of the paper as follows. Section 2 describes FCX'soperations and its need for new "nancing and also discusses the role of gold-linked securities in "nancing, especially in the context of risk management. Thebene"ts of bundling are highlighted in Sections 3 and 4. In Section 3, we presenta detailed example illustrating how a gold-indexed "nancing instrument issuedby a gold mining "rm can overcome wealth transfer issues associated withconventional risk management. This representative example is designed toarticulate our general conceptual points, and is not just a simpli"ed descriptionof the Freeport situation. In Section 4, we discuss why the bundling of "nancingand risk management mitigates the asset substitution problem and enhances thecredibility of the hedge. Section 5 develops a methodology for detecting creditenhancement in the depositary shares, which is then applied to FCX's gold- andsilver-denominated issues. Section 6 concludes.

2. Freeport McMoRan Copper and Gold: operations and 5nancing

FCX is a subsidiary of Freeport McMoRan Inc. (FTX). FTX came intoexistence in 1981 following the merger of Freeport Minerals Co. and McMoRanOil and Gas Co. The former began operations in 1912 in Texas as the FreeportSulphur Company to develop a newly discovered sulfur "eld on the Texas GulfCoast. The latter was founded in 1969 in Utah as McMoRan Explorations Co.to undertake oil exploration. Following the 1981 merger, FTX began acquiringoil and gas assets, geothermal properties, and phosphate mines in a $1 billionprogram to diversify away from the sulfur business, which was then in decline. In1987, Freeport McMoRan Copper & Gold Inc. and Freeport McMoRanResource Partners Inc. were formed as subsidiaries of Freeport McMoRan Inc.

N.K. Chidambaran et al. / Journal of Financial Economics 60 (2001) 487}528 491

In 1988, the "rm made two major discoveries } the Main Pass sulfur deposit inthe Gulf of Mexico and gold, silver, and copper deposits in the Indonesianprovince of Irian Jaya. Given the enormous capital costs associated withdeveloping these deposits, FTX reversed its earlier acquisition spree and spuno! its subsidiaries. FCX was formed in 1988 when FTX's copper and goldoperations were spun o! into a separate "rm. FTX retained 73.2% ownership inFCX.

FCX's principal operating subsidiary is P.T. Freeport Indonesia (PT-FI)which mines and processes copper, gold, and silver in Indonesia, and marketsworldwide the concentrates containing these metals. FCX owns 80% of theoutstanding common stock of PT-FI, with the remaining 20% split equallybetween the Government of Indonesia and an Indonesian corporation, P.T.Indocopper Investama Corporation.

2.1. FCX's mining operations and the Grasberg Mine expansion

Fig. 1 shows FCX's revenues from copper, gold, and silver for the "ve-yearperiod 1991}1995. Copper and gold are FCX's major products, with silveraccounting for less than 1% of total revenue. Mining operations in Indonesiacommenced in 1967 with the discovery of the Ertzberg mineral reserve on theIndonesian island of Irian Jaya. The Grasberg mineral reserve, currently theworld's largest single gold reserve and one of the world's three largest open pitcopper reserves, was discovered in 1988.

FCX's publicly espoused corporate philosophy was to enhance shareholdervalue by becoming an e$cient mining "rm. FCX thought that being a low-costproducer was the most e!ective way to survive the frequent price swings that theindustry experienced, since price drops force high-cost producers out of themarket, making way for a quick recovery and return to higher pro"ts for thosethat remain. FCX saw the discovery of the Grasberg mine as an opportunity toincrease substantially the throughput of its mining operations in Indonesia,thereby reducing its average mining cost.

The implementation of this low-cost philosophy through increased capacitycalled for $2 billion in capital investments to expand operations at the Grasbergmine and for accompanying infrastructure development projects such as power,housing, transportation, hospitals, and communications. In 1989, FCX initiatedthe "rst capacity expansion from 20,000 metric tons of ore per day (MTPD) to52,000 MTPD. Capital expenditure for the expansion was estimated at $507million. In August 1992, FCX approved a plan to expand production to 90,000MTPD at an estimated cost of $545 million. The third and "nal phase expandedproduction to 118,000 MTPD. The burden of operating in an uncertain politicalenvironment, coupled with the amount of money needed, caused FCX toexplore various innovative avenues for new "nancing.

492 N.K. Chidambaran et al. / Journal of Financial Economics 60 (2001) 487}528

Fig. 1. This "gure shows the dollar sales in copper, gold, and silver for FCX for the "ve-year period1991}1995. Data are from "rm's annual reports from 1992}1996.

2.2. Financing strategy and capital structure

Table 1 presents the securities FCX issued to "nance the "rst phase of theGrasberg expansion and reduce its dependence on short-term funds. AppendixA presents "nancial data for the "ve-year period 1989}1993.

FCX has two classes of common stock outstanding: Class A, held by thegeneral public, and Class B, wholly owned by FTX. Through May 1, 1993, ClassA common stockholders received cumulative quarterly dividends of 10.25 centsper share before payment of any dividends on Class B common stock. On thedebt side, FCX had traditionally used short-term debt "nancing. In 1989, the"rm obtained a line of credit to provide project "nancing up to $550 million to"nance capital expenditure. In 1991, the "rm converted the #oating rate line ofcredit into a "xed rate loan by entering into an interest rate swap agreement,resulting in a "xed rate of 8.3% on $100 million of debt through December 1999.In June 1993, the $550 million credit agreement was restructured as a three-yearrevolving line of credit followed by a three-and-a-half year reducing revolver.The "rm's management was dissatis"ed with its dependence on bank "nancingbecause of the cost and the re"nancing risk, especially as banks were nervousabout the political risk in Indonesia. FCX initiated new rounds of "nancing,seeking longer maturities to eliminate re"nancing risk and obtain a capitalstructure more in keeping with the long-term nature of its business. In theprocess, FCX also sought to free itself from the restrictive covenants attached toexisting debt, which included restrictions on current ratios, interest coverage

N.K. Chidambaran et al. / Journal of Financial Economics 60 (2001) 487}528 493

Table 1FCX's long-term capital structure (book value) as of Dec. 31, 1990 and signi"cant new "nancing-related activity through Dec. 31, 1994.

Balance as of Dec. 31, 1990: ($ million)Long-term bank debt 294Stockholders' equity 177

Changes through Dec. 31, 1994:

1991: Net issuance of long-term bank debt 103

July 91: Zero-coupon Liquid Yield Option Notes 219Face Value $1.035 billion, maturing in 2011, unsecured. Subordinatedwith a 7.75% yield to maturity. Exchangeable at holder's option for0.6015 oz. of gold or 7.505 shares of Class A common stock. Putableafter July 2, 1996 at issue price plus accrued original issue discount.

1992: Net issuance of long-term bank debt 74

July 92: Class A Common Shares� 1748.6 million shares issued

7% Convertible Exchangeable Special Preference Shares Cumulativedividends (quarterly)"$1.75 per year. After 8/1/94, can be exchangedfor a 7% Convertible subordinated debenture. Redeemable after 8/1/95at stated prices. Convertible into 0.992 shares of class A common stock.

218

1992: During 1992, zero coupon exchangeable notes with a facevalue of $326.4 million were converted into 4.55 millionClass A common stock (valued at $ 70.4 million) and$7.85 million in cash.

1993: Net issuance of long-term bank debt !361

July 93: Step-Up Convertible Preference Shares Dividends (quarterly) till 8/1/96- $1.25 per year and $1.75 per year thereafter. Redeemable after 8/1/96for 0.813 shares of Class A common stock subject to price level. After8/99 redeemable for $25.00. Convertible into 0.813 shares of ClassA common stock.

341

August 93: Gold-denominated Preferred Series I 221Face value of 0.1 oz. of gold and annual dividend of 0.0035oz. of gold, payable quarterly. Maturing on 08/01/2003.

1993: During 1993, zero coupon exchangeable notes with a facevalue of $322.6 million were converted into 4.84 million Class A com-mon shares (valued at $79.7 million). There were no redemptions forcash in 1993.

1994: Net issuance of long-term bank debt 416

494 N.K. Chidambaran et al. / Journal of Financial Economics 60 (2001) 487}528

Table 1 (continued )

Balance as of Dec. 31, 1990: ($ million)Long-term bank debt 294Stockholders' equity 177

January 94: Gold-denominated Preferred Series II 138

Face value of 0.1 oz. of gold and annual dividend of 0.00325oz. of gold, payable quarterly. Maturing on 02/01/2006.

July 94: Silver-denominated Preferred Series I 95

Face value of 4.0 oz. of silver and annual dividend of 0.165 oz. of silver,payable quarterly. Maturing on 08/01/2006.Redeemable annually at 0.5 oz. of silver/year beginning 08/01/99.

1994: During 1994, the remaining zero coupon exchangeable notes of $386million face value were converted into 5.8 millionClass A common shares (valued at $ 73.7 million) and $0.3 million in cash.

�FCX had planned to issue 10.25 million Class A shares and 6 million exchangeable shares butadjusted these amounts because of the higher demand for the exchangeable shares. (Bloomberg,7/14/92)

ratios, present value of future cash #ows to debt, and the amount of senior debtthat could be issued.

The political uncertainty in Indonesia and the enormous amount of capitalalready raised by FCX made it di$cult to tap traditional sources of capital forthe second and third phases of the expansion. On the one hand, FCX manage-ment did not want to issue new equity, since they felt that the stock wassigni"cantly undervalued relative even to existing assets. On the other hand, theexisting subordinated debt was already rated at a low B1 by Moody's, and newdebt issues would put further pressure on FCX's debt rating. Although FCX didissue three series of convertible securities during 1991}1993, as Table 1 reports,management viewed these securities as more attractive debt "nancing thanstraight debt because of the lower cash out#ow by way of coupons, and lessrestrictive covenants. From the standpoint of our analysis, they can be viewed asadding to FCX's leverage. Two of these series were later converted into commonstock but the third series remained unconverted as of Dec. 31, 1999.

In this environment, FCX proposed and issued the commodity-linked deposi-tary shares, getting much-needed credit enhancement for these securities andraising capital for its investment needs. Fig. 2 shows a plot of the split-adjustedstock price for FCX. The dates of issue of each of the three depositary shareseries are marked on the "gure. Appendix B describes the structure of thesesecurities, using the Series I gold-denominated depositary shares as the illustra-tive example.

N.K. Chidambaran et al. / Journal of Financial Economics 60 (2001) 487}528 495

Fig. 2. This "gure graphs the month-end split-adjusted stock price of FCX for the period January1991}January 1995. The points at which FCX issued the gold- and silver-denominated depositaryshares are also indicated.

� The depositary share structure was created purely to avoid exceeding the limit on outstandingpreferred shares authorized by the stockholders and thereby having to go back for stockholderapproval each time they needed to do a new issue (FCX issued "ve preferred stock series during the1992}1994 period.) Since the authorized preferred stock was of the `blank checka type, i.e., givingthe board of directors broad powers associated with setting the rights and preferences associatedwith a particular preferred stock issue, it was possible to create the depositary trust withoutstockholder approval. The depositary trust was a pure pass-through arrangement, unlike trustschemes that are used for securitization and enhancing credit quality. For example, the "rst goldissue comprised 300,000 preferred shares. If these shares were issued directly, each share would havehad a price of approximately $750, resulting in too few shares and too high a share price for broaddistribution and liquidity in the secondary market. Therefore, these 300,000 preferred shares wereused to back six million depositary shares, giving the `righta number of shares and share price.

As reported in Table 1, FCX raised nearly $500 million through the threeissues of commodity-linked depositary shares. The "rst series of 3.5% gold-denominated depositary shares was issued in August 1993 and had a maturity often years. FCX applied the proceeds of $221 million toward funding the 90,000MTPD expansion plan. The second series of 3.125% gold-denominated deposi-tary shares was issued in January 1994 and had a maturity of 12 years. The thirdseries was denominated in silver and was issued in July 1994 at a yield of4.125%. FCX used the $233 million raised through the latter two issues to helpfund the 118,000 MTPD expansion. All the depositary shares were backed bypreferred stock held in trust and carrying a Moody's B1 rating.� FCX was ableto raise these funds without restrictive covenants, despite having been placedunder a credit watch by the rating agencies at the time of the issues.

496 N.K. Chidambaran et al. / Journal of Financial Economics 60 (2001) 487}528

Table 2Three-factor model for FCX common stock returns

We estimate a three-factor model for FCX daily common stock returns. We use as factors the dailyvalue-weighted market return from the CRSP database, the daily percentage change in the LondonPM gold price "xing, and the daily percentage change in the spot price of copper on the LondonMetal Exchange (LME) for daily data from 1 January 1990 to 15 July 1993.

Variable Coe$cient(t-statistic)

INTERCEPT 0.002(2.43)�

MARKET FACTOR 0.307(2.85)�

GOLD FACTOR 0.611(6.35)�

COPPER FACTOR 0.136(2.66)�

No. of observations 856Adj. R� 5.4%F-value 17.163�

�Signi"cant at the 5% level.�Signi"cant at the 1% level.

� There is some interdependence between FCX's gold and copper risk and its political risk, whichwe have not modeled in the paper. For example, if their mines are nationalized, exposure to gold andcopper risk could change. We thank a referee for highlighting this point.

2.3. FCX's exposure to xnancial risk

As noted previously, gold and copper are FCX's two major products, sugges-ting that these two commodities were its principal sources of "nancial risk. Wecon"rm this by estimating a three-factor model for FCX's common stockreturns, which we report in Table 2. We use as factors the daily value-weightedmarket return from the CRSP database, the daily percentage change in theLondon PM gold price "xing, and the daily percentage change in the spot priceof copper on the London Metal Exchange. Silver was not a signi"cant explana-tory variable.

As in the case of other natural resource companies that operate in countrieswith political uncertainty, the other signi"cant risk faced by FCX is the politicalrisk arising from the fact that most of its assets are located in Indonesia. FCXseems to have hedged this risk by making the Indonesian government a major(10%) shareholder, by placing a further 10% of its shares with Indonesiannationals, and by a series of long-term exploration and mining agreements andguarantees that paid the Indonesian government signi"cant royalties.�

N.K. Chidambaran et al. / Journal of Financial Economics 60 (2001) 487}528 497

2.4. Risk management at FCX

FCX's policy towards hedging gold price risk varied over time. The "rmimplemented risk management in the early 1980s but reversed this policy in thelatter half of the 1980s on the premise that stockholders wanted the gold exposure.FCX reinstated its risk management program in the 1990s, adopting the objective of`separating good management from gold price risk.a The hedge bundled into thegold-linked securities was consistent with the dual policy of o!ering good manage-ment to their stockholders and being the low-cost producer in the gold market.

FCX's risk management operations in the early 1990s involved buying largepositions in gold and copper puts to set a price #oor for its output. FCX usedsequenced trades (rolling) to minimize the price impacts of its participation inthis market. The 1993 FCX annual report discloses that `PT-FI has a priceprotection program for virtually all of its estimated copper sales to be priced in1994 at an average #oor price of $0.90 per pound, while allowing full bene"tfrom prices above that amount.a This hedging program cost $6 million in 1993.FCX's Spanish subsidiary used forward contracts for approximately 61% of itsgold production and 38% of its silver production in 1994 and 1995. It alsoreported a policy of hedging the purchases of concentrate for its smelter throughthe use of forward contracts.

The lack of consistency in FCX's risk management program is not at oddswith the "ndings of Tufano's (1996) extensive study of the risk managementpractices of 48 publicly traded North American gold mining companies. Tufano(1996) shows that considerable variation exists in the hedging practices of goldmining "rms. For example, Homestake Mining sells all its production in thespot market and has taken a public position against gold price risk manage-ment, while American Barrick "rmly adheres to the policy of separating goodmanagement from gold price risk and makes its hedging program an integralpart of its business (see also Tufano, 1993).

2.5. Credit risk considerations

Gold-linked debt securities of the type issued by FCX, and similar securitiessuch as the gold "nancings undertaken by American Barrick in the 1980s(Tufano, 1993), o!er long-term exposure to gold without taking a position in thespot market, making them popular with investors who seek exposure to goldprice risk. Investors value gold and gold securities as a hedge against in#ation.In addition, some investors, known as `goldbugs,a simply like to invest in gold.Markets for spot gold and gold derivatives are incomplete because of the "nitesupply of the commodity, the control of central banks on the mined supply ofgold, and the lack of liquidity of long-term derivatives. The derivatives bundledin the gold-linked securities tend to be relatively long-term, and ful"ll the marketniche for such contracts.

498 N.K. Chidambaran et al. / Journal of Financial Economics 60 (2001) 487}528

Purchasing gold-linked securities issued by corporations exposes investors tothe issuer's default risk, which is a function of the issuer's exposure to goldprices. Consider the case when the issuer has a natural exposure to gold, as withgold mining companies. There will be a positive correlation between the issuer'sasset value and gold prices and between the issuer's revenues and gold prices.When gold prices drop, the value of the assets and cash #ows will also drop,making the issuer more vulnerable to "nancial distress. However, this risk ispartially o!set by the reduction in the issuer's liability on the bond, whichdecreases as the gold price declines. If gold prices rise, the value of the issuer'sliability is greater, but so is the issuer's ability to meet its liabilities since its assetvalue and cash #ow are also greater. Therefore, the default risk and other"nancial constraints noted by Mello and Parsons (1995, 2000) are lower fora gold-linked security issued by a gold mining "rm than for an otherwiseequivalent plain-vanilla debt instrument.

On the other hand, many gold security issuers are not naturally long in gold.For example, many industrial companies issue bonds with attached gold-linkedwarrants to take advantage of a `hota gold market. If the issuer's asset value andcash #ow are unrelated to the gold price, the gold link can signi"cantly increasethe default risk. Budd (1983) discusses the striking case of the gold-linked bonds(`Giscardsa) issued by the French government in 1973, with the gold linkapparently added to `sweetena the issue. Due to the dramatic escalation in theprice of gold, the bond appreciated more than tenfold over a ten-year period.The French government did not have a gold reserve to o!set the exposure, andthe gold price escalation led to speculation that the government might have torenegotiate the gold clause.

In the next section, we highlight the credit enhancement achieved through thebundled hedge and analyze the features of the hedge that make this creditenhancement possible. In Section 4, we discuss other bene"ts of bundling, andshow that bundling overcomes many of the shortcomings of conventional riskmanagement noted by Smith and Stulz.

3. Credit enhancement through bundling

In this section, we develop a detailed numerical example to elucidate thee!ects of bundling risk management with "nancing as in the case of gold-linkeddebt. We use the setting of a gold mining "rm with existing senior debt thatrequires additional external "nancing. The example is a representative one tofocus on our conceptual points in this section, which are not speci"c to FCX. Itis designed to highlight the following e!ects: (1) credit enhancement stemmingfrom the positive correlation between the cash in#ow to the "rm from gold salesand the cash out#ow from the "rm to holders of the gold-linked debt; (2) theimplicit netting of embedded-derivative and bond cash #ow, which, in e!ect,

N.K. Chidambaran et al. / Journal of Financial Economics 60 (2001) 487}528 499

enhances the seniority of the junior gold-linked debt on hedged cash #ow; and(3) the inability to replicate this netting e!ect through conventional derivativecontracts due to the treatment of derivatives under bankruptcy.

We contrast the embedded hedge in a gold-linked bond with a conventionalhedge using a gold forward contract. We use bankruptcy costs as a motivationfor shareholders to hedge and thereby enhance the credit quality of the claimsissued. We analyze the e!ects on cash #ow to the various claimholders underboth credit enhancement scenarios. Under conventional hedging, senior bond-holders will have priority on the increase in cash #ow. This is consistent with theinsight provided by Myers (1977). As we show, bundling greatly reduces thewealth transfers to existing bondholders that arise from credit enhancement. Werefer to this e!ect as targeted risk management. In addition, we also show thatbundling allows stockholders to capture more of the reduction in bankruptcycosts. Our example extends the analysis of Smith and Stulz (1985), and showsthat the mode of risk management a!ects the division of the bene"ts among the"rm's "nancial claimholders.

Credit enhancement through bundling will also obtain in a Modigliani-Millerworld with no bankruptcy costs. Of course, "rm and shareholder value in thatsetting are independent of the structure of "nancing used to fund investments,and shareholders would be indi!erent between the various "nancing choices. Ingeneral, hedging bene"ts shareholders by reducing "nancial constraint costs,including reductions in the costs of "nancial distress, the costs of external"nancing, and the costs of underinvestment (Mello and Parsons, 2000). In thesimpli"ed single-period context of our model, the "rm is "nancially constrainedin states of bankruptcy and hedging bene"ts arise from reduction in expectedcosts of bankruptcy. Reducing these costs bene"ts shareholders and is onepossible reason why they undertake credit enhancement through risk manage-ment.

3.1. Targeted risk management using an indexed instrument

We model a gold mining "rm that requires external "nancing to develop itsgold reserves. The "rm's assets consist solely of its gold reserves, which are"nanced by both risky debt and equity. The assumption that debt is risky allowsus to incorporate bankruptcy costs in the model. We do not, however, explicitlyincorporate the tax shield and other e!ects of debt, since our focus is on theimpact of alternate risk management strategies, and the e!ects that we identifyare independent of the speci"c amounts of debt and equity levels of the "rm. Inconjunction with the new "nancing, the "rm seeks to reduce its exposure to goldprices via a risk management program, thereby enhancing the credit quality ofthe new "nancing and reducing bankruptcy costs.

We assume that the "rm's only asset is its reserve of 1.97 million ounces ofgold. It is seeking "nancing to expand this reserve to three million ounces. The

500 N.K. Chidambaran et al. / Journal of Financial Economics 60 (2001) 487}528

value of the "rm will be linearly increasing in the price of gold, and we assumethat gold prices range from $100 to $500 per ounce and are distributed uniform-ly over that range. The "rm currently has senior debt with a face value of $500million and is proposing to raise $251 million of new "nancing, either througha new equity issue or a new subordinated debt issue. This new "nancing will payfor the expansion project. We assume that the "rm faces bankruptcy costs of $50million if it were to default on any category of debt. This assumption sets thebankruptcy cost at approximately 5.7% of "rm value, which is within the rangeof 1% to 6.6% empirically measured by Weiss (1990). We assume risk neutralclaimholders and a discount rate of zero. Table 3 presents the base case and thetwo "nancing scenarios for the "rm, assuming that no risk management isundertaken at this point. Fig. 3 graphs the value of the "rm and its liabilities asa function of the gold price, for the base case and the two "nancing scenarios.

Scenario A presents the base case of the "rm prior to the expansion. The "rmwill default on its senior debt at a gold price of $253.4/ounce. The value of the"rm is $572.8 million of which (senior) debt is worth $422.8 million and equity isworth $150 million.

Since the expected value of gold is $300/ounce, the proposed scale expansionwill have a positive net present value (NPV) of $58 million. In Scenarios B andC, the "rm raises the new "nancing of $251 million required for the expansionvia new equity and new (junior) debt, respectively. In both cases, we assume thatthe new "nancing is fairly priced.

Comparing Scenarios A and B, we observe that undertaking the expansionwith new equity creates a total value of $67.9 million ($58 million project NPVplus $9.9 million bankruptcy cost reduction) to be shared between the seniorbondholders and stockholders. The value of senior debt increases by $52.2million while the value of existing equity increases by $15.7 million. In ScenarioC (junior debt "nancing), we observe that bankruptcy costs increase by $16.7million relative to Scenario B and by $6.8 million relative to Scenario A, due tothe increase in leverage. Thus, the positive project NPV is partially o!set by thehigher bankruptcy costs. Junior debt in Scenario C defaults at the gold price of$300. The senior bondholders capture the entire net value increase due to theexpansion. This exact result arises because we set the initial reserve at 1.97million ounces in order to make the stockholders indi!erent to undertaking theexpansion project with junior debt "nancing.

We next examine the case when the "rm uses junior gold-linked debt "nanc-ing. We assume that the face value of the junior debt is equal to one millionounces of gold, which is set such that junior debt is once again worth $251million. As Scenario D in Table 4 shows, issuing the gold-linked junior debt doesnot reduce the sensitivity of the "rm's value to the gold price, but it doesdecrease the sensitivity of equity to the gold price. The junior debt in ScenarioD is safer than the junior debt in Scenario C, and it defaults at the lower goldprice of $250.

N.K. Chidambaran et al. / Journal of Financial Economics 60 (2001) 487}528 501

Table 3Values of the "rm, debt, and equity before and after expansion

This table shows the change in the value of the "rm and its capital structure components for a goldmining "rm that goes through a scale expansion. The "rm has 1.97 million ounces of gold reservesand plans to expand to three million ounces of gold in reserves. We assume that the value of the "rmis linear in the price of gold and that gold prices are distributed uniformly over the range of $100 perounce to $500 per ounce. The "rm has $500 million in senior debt and needs to raise $251.0 millionfor the expansion. The "rm faces bankruptcy costs of $50 million if it defaults. Scenarios in which the"rm issues debt and equity to "nance the expansion are analyzed as described in the panel headers.Note that the NPV of the expansion from 1.97 million ounces to three million ounces is just highenough to overcome the Myers (1977) debt overhang problem if the "rm were to raise funds byissuing junior debt as in Scenario C.

Scenario A: Gold mining xrm prior to expansion, 1.97 million oz of gold in reservesMin Sr Debt -'

PaidMax Expected

value(- Default

Gold Price 100.0 253.4 300.0 500.0Reserves, million oz 1.97 1.97 1.97 1.97Firm value 147.3 500.0 600.0 986.6 $572.8Value of senior debt 147.3 500.0 500.0 500.0 $422.8Value of Equity 0.0 0.0 200.0 486.6 $150.0

Scenario B: Gold mining xrm with expands to 3 million ounces of gold reserves.Firm raises $251 million by selling equity

Min Sr Debt-'Paid

Jr Debt'Paid

Max Expectedvalue

(- Default

Gold Price 100.0 166.67 300.0 500.0Reserves, million oz 3 3 3 3Firm value 250.0 500.0 900.0 1500.0 $891.7Value of senior debt 250.0 500.0 500.0 500.0 $475.0Value of existing equity 0.0 0.0 159.0 397.6 $165.7Value of new equity 0.0 0.0 241.0 602.4 $251.0

Scenario C: Gold mining xrm expands to 3 million ounces of gold reserves.Firm raises $251 million through junior bonds, face value $400 million

Min Sr Debt-'Paid

Jr Debt-'Paid

Max Expectedvalue

(- Default

Gold Price 100.0 183.3 300.0 500.0Reserves, million oz 3 3 3 3Firm value 250.0 500.0 900.0 1500.0 $875.0Value of senior debt 250.0 500.0 500.0 500.0 $474.0Value of junior debt 0.0 0.0 400.0 400.0 $251.0Value of equity 0.0 0.0 0.0 600.0 $150.0

502 N.K. Chidambaran et al. / Journal of Financial Economics 60 (2001) 487}528

Fig. 3. This "gure shows the value of the "rm and its capital structure components for a gold mining"rm that expands reserves from 1.97 to 3 million ounces. The value of the "rm is linear in the price ofgold prices are distributed uniformly over the range of $100 per ounce to $500 per ounce. The "rmhas $500 million in senior debt and faces bankruptcy costs of $50 million if it defaults. The "rm needsto raise $251 million to fund the expansion. Scenario B and Scenario C present the cases in which theexpansion is "nanced with new equity and with junior debt, respectively.

The price of gold at which junior debt defaults in Scenario D decreases for tworeasons. First, the face value of junior debt is lower than the face value of juniordebt in Scenario C } $300 million at current gold prices versus $400 million.Second, the value of the "rm decreases at a lower rate as a function of gold prices

N.K. Chidambaran et al. / Journal of Financial Economics 60 (2001) 487}528 503

Table 4Gains from targeted risk management

This table shows the value of the "rm and its capital structure components for a gold mining "rmthat has three million ounces of gold in reserves. We assume that the value of the "rm is linear in theprice of gold and that gold prices are distributed uniformly over the range of $100 per ounce to $500per ounce. The "rm has $500 million in senior debt and raises $251.0 million by issuing junior debt.The "rm faces bankruptcy costs of $50 million if it defaults. Two scenarios are analyzed as describedin the panel headers.

Min Sr Debt-'Paid

Jr Debt-'Paid

Max Expectedvalue

(- Default

Scenario D: Gold mining ,rm with targeted risk management.Firm sells junior gold-linked bonds of face value 1.0 million oz

Gold price 100.0 183.3 250.0 500.0Reserves, million oz 3 3 3 3Firm value 250.0 500.0 750.0 1500.0 $881.3Value of senior debt 250.0 500.0 500.0 500.0 $474.0Value of junior gold-linked debt 0.0 0.0 250.0 500.0 $251.0Value of equity 0.0 0.0 0.0 500.0 $156.3

Scenario E: Gold mining xrm with risk management at the xrm level.Firm sells junior bonds of face value $345.9 million.Firm hedges by selling a gold forward for 1.0 million oz at $300/oz

Gold Price 100.0 125.0 272.9 500.0Reserves, million oz 3 3 3 3Amount managed 1 1 1 1Residual exposure, million oz 2 2 2 2Firm value 450.0 500.00 845.9 1300.0 $878.4Value of senior debt 450.0 0.0 500.0 500.0 $498.4Value of junior debt 0.0 0.0 345.9 345.9 $251.0Value of equity 0.0 0.0 0.0 454.1 $128.9

after the bundled hedge in Scenario D as compared to the face value of thejunior debt. If the "rm had issued straight junior debt of face value $300 million,default would have occurred at a gold price of $266.67. In contrast, gold-linkeddebt of face value $300 million defaults at $250. The magnitude of the seconde!ect is captured by this price di!erence.

The credit enhancement is achieved because of the positive correlation be-tween the cash #ow of the gold-linked security and the "rm's cash #ow, as can beseen in Fig. 4, which shows the cash #ow to the various claims at di!erent goldprices. Senior debt defaults at the same price as the senior debt in ScenarioC and its value is $474 million as in Scenario C. The value of the "rm rises by$6.3 million to $881.3 million, re#ecting the reduction in expected bankruptcycosts. Stockholders capture the reduction in bankruptcy costs, and the value of

504 N.K. Chidambaran et al. / Journal of Financial Economics 60 (2001) 487}528

Fig. 4. This "gure shows the value of the "rm and its capital structure components for two riskmanagement scenarios. In Scenario D, the "rm issues gold-linked junior debt with a face value of1 million ounces. In Scenario E, the "rm sells 1 million ounces of gold forward. Values of the "rm,senior debt, junior debt, and equity are as shown in Table 4.

equity increases by $6.3 million to $156.3 million. Thus, the entire increase in thevalue of the "rm arising from a reduction in bankruptcy costs is captured by thestockholders, making them signi"cantly better o! relative to not managing risk.

As would be predicted by Myers (1977), it is important to note that gold-linked "nancing is worse than equity "nancing, by $9.4 million for the currentstockholders. Of course, this assumes that equity can be issued at its full value, in

N.K. Chidambaran et al. / Journal of Financial Economics 60 (2001) 487}528 505

� We are grateful to a referee for the important added insight gained by including the case of equity"nancing in our model. See Myers and Majluf (1984) and Smith (1986) for a discussion of some of theissues associated with the choice of security.

which case the di!erential for stockholders is 3.7% of the value of the new"nancing (FCX had ruled out a new equity issue because the stock price wasdepressed and trading well below the value of their reserves). New equity"nancing dominates all the scenarios of junior debt "nancing considered here,provided the discount on issuing new equity does not exceed its incrementalbene"t. Our example does not explain the choice of debt over equity, and givenour focus on credit enhancement conditional on debt "nancing, the morefundamental issues of the debt-equity choice are outside our model.�

We next consider the case in which the "rm seeks to enhance the credit qualityof its junior debt by conventional means. Could the "rm issue straight juniordebt and then hedge using a gold forward contract to achieve the same creditenhancement as with bundling the two? In Scenario E in Table 4, the "rmmanages the price risk associated with a third of its gold reserves, i.e., onemillion ounces, using a forward contract. Ignoring carrying costs, this riskmanagement "xes the price for this gold at $300/ounce. The gold price hedgereduces the sensitivity of "rm value to the gold price and has several conse-quences. First, the junior debt does indeed have higher credit quality (it defaultsat a lower gold price of $272.9), and the "rm needs to sell less face value of debt($345.9 million) relative to Scenario C to raise the required $251 million. Second,the existing senior debt also becomes safer (it defaults at the lower gold price of$125), increasing the value of the senior debt to $498.4 million. The value of the"rm rises by $3.4 million to $878.4 million, re#ecting the reduction in expectedbankruptcy costs. However, stockholders do not bene"t because this increase ismore than o!set by the wealth transfer to senior bondholders, and the value ofequity drops to $128.9 million from the $150 million in Scenario A. Thus,stockholders will have a strong incentive to unwind the hedge after the juniorbond issue.

The valuation di!erences between bundling and conventional risk manage-ment in Scenarios D and E in Table 4 arise because of the cash #ow di!erencesfrom the respective derivative transactions. In Scenario E, cash #ow for thederivative transaction a!ects the overall cash #ow of the "rm, and the allocationto the various claimholders takes place according to the seniority structure, i.e.,"rst to senior debt, then to junior debt, and "nally to equity. Therefore, seniorbondholders bene"t when gold prices are low and the "rm is in default becausethe "rm receives a cash in#ow from the forward contract. In Scenario D, no suchcash #ow accrues to the "rm from the bundled derivative contract when theprice of gold decreases, because junior bondholders (e!ectively) net payments tothe "rm on their bundled long forward contract when the assets of the "rm are

506 N.K. Chidambaran et al. / Journal of Financial Economics 60 (2001) 487}528

lower than the face value of the "rm's total debt. Therefore, the cash #ow fromthe bundled derivative component does not #ow through to the "rm's seniordebtors.

To further analyze the netting feature that characterizes risk managementbundled with "nancing, consider a portfolio consisting of a straight bond anda long forward contract placed with the same counterparty. When the price ofgold is below the forward price, the forward contract has a negative cash #owthat o!sets the value of the straight bond, making the value of the portfoliolower than the value of the straight bond. However, if an investor in sucha portfolio is allowed to net the value of the two securities, any shortfall in thebond proceeds due to the counterparty when the "rm is in default will be o!setagainst payments due to the "rm on the forward contract. The gold-linked bondrepresents exactly such an ability to net the potential losses on the bond againstamounts due on the long forward position.

The implicit ability to net the cash #ow on the bond and the hedge under allpossible outcomes is the crucial feature that di!erentiates a "nancing instrumentwith a bundled hedge, such as a gold-linked bond, from straight debt "nancingcoupled with a conventional hedge. The derivatives counterparty in a conven-tional hedge has no such netting privileges when the "rm hedges by trading inthe derivatives market. The bundled hedge provides a signi"cant advantage tojunior bondholders that, through the pricing of the junior bonds, can beappropriated by the stockholders. This security design has the e!ect of targetinghedging bene"ts to the junior bondholders, bypassing the traditional prioritystructure.

4. Further bene5ts of bundling

We show in this section that the gold-linked structure adopted by FCXameliorates the time inconsistency problem associated with conventional riskmanagement that gives rise to asset substitution (Smith and Stulz, 1985). Weargue that this is partially due to the adverse liquidity consequences of a conven-tional derivatives strategy required to reverse the bundled hedge (Mello andParsons, 1995, 2000). Moreover, these adverse liquidity e!ects also make itdi$cult to replicate the bundled hedge using a conventional derivatives strategy.Finally, we also discuss the advantages of linking debt to an exogenous index,such as the gold price, relative to other forms of indexation that are susceptibleto manipulation by the "rm's managers.

4.1. Asset substitution

In the Smith and Stulz framework, "rms that hedge to enhance credit qualitywhile issuing debt must convince incoming bondholders that they will maintain

N.K. Chidambaran et al. / Journal of Financial Economics 60 (2001) 487}528 507

the hedge after the bond sale in order for the bond price to re#ect the lower riskof default and for stockholders to capture the bene"ts of hedging. This problemis mitigated in the case of a "rm that employs a bundled hedge. We illustrate thisin Table 5. In Scenario F, the "rm unwinds the conventional hedge by takinga long forward position in gold to o!set the exposure arising from the previouslyestablished short forward position, and in Scenario G, the "rm attempts tosimilarly o!set the bundled short forward position.

The results for Scenario F reveal that unwinding the conventional hedge ("rstintroduced in Scenario E) increases the default risk for both classes of bond-holders, making them substantially worse o!. The value of the senior bondsdecreases by $24.5 million and the value of the junior bonds decreases by $26million. Stockholders gain by $49.4 million because higher cash #ow accrues tothem when the "rm is solvent. This wealth transfer illustrates the classic assetsubstitution problem. Firm value decreases by $1.1 million because of theincrease in distress costs associated with the higher default risk.

This illustrates the point made by Smith and Stulz that by reneging ona commitment to hedge or by unwinding an existing hedge, stockholders ina levered "rm can be made considerably better o!. The problem is clearlyexacerbated when the "rm is already levered because stockholders have anadditional incentive to unhedge stemming from the wealth transfer to seniorbondholders.

The results for Scenario G demonstrate that the e!ects of unwinding thebundled hedge ("rst introduced in Scenario D) are more complex. The counter-party in the o!setting forward transaction has a short position and, since anyforward contract obligations are junior to both classes of the "rm's debt, isexposed to the risk that the "rm will default on the forward contract when thevalue of the "rm drops below the value of its debt. The counterparty will requirecompensation through an upfront premium for the default risk. We incorporatethis as an initial cash out#ow from the "rm. The value of this premium has to bedetermined iteratively since the payment of the premium a!ects the probabilityof default and hence the size of the premium. For the parameters that character-ize Scenario G, the value of this premium is $49.6 million. This can be veri"ed bycalculating the expected cash #ow to the counterparty at this value } also $49.6million. The value of senior debt decreases by $11.4 million and junior debt by$12.8 million, which are smaller declines than for Scenario F. The increase in thevalue of equity is $20 million, also much smaller than in Scenario F. Thus,unwinding the bundled hedge results in considerably lower wealth transfers thanunwinding a conventional hedge.

The key di!erence between the cash #ow e!ects in the two scenarios is onceagain the treatment of the derivatives counterparty when the "rm is in default.In Scenario F (unwinding the conventional hedge), we assume that the counter-party holds both the long position in the transaction that initiated the hedge andthe short position that unwinds it. Under current bankruptcy regulations, the

508 N.K. Chidambaran et al. / Journal of Financial Economics 60 (2001) 487}528

counterparty is allowed to simply net the two positions and achieve priorityover the "rm's senior bondholders in states of default (see Tucker, 1991; Foster,1995). The counterparty that has the short forward position, therefore, does notlose when the "rm goes bankrupt and demands no additional compensation. InScenario G, the counterparty has a naked short position and a claim that isjunior to debt if the "rm defaults. Payments to the derivatives counterparty too!set this risk reduce the gains that stockholders can realize by unwinding.

Boot et al. (1993) show that reputational concerns can overcome any residualincentive to unhedge, especially for companies undertaking capital-intensiveprojects that require frequent re"nancing. Unwinding a bundled hedge requiresthe "rm to explicitly initiate a derivative transaction that actually increases therisk exposure of the "rm's cash #ow. Compared to the failure to undertakea conventional hedge, such a transaction would increase the reputation problembecause it is more transparent. It is harder for stockholders to justify an act ofcommission (to increase cash #ow risk) than to justify an act of omission (afailure to hedge).

Furthermore, unwinding a long-term hedge of the sort bundled in FCX'sgold-linked instruments is also likely to be constrained by the lack of appropri-ate hedging instruments and the high costs associated with creating an equiva-lent o!setting hedge. Merton (1990) advances this argument as a rationale for"nancial innovation. Indeed, Smithson and Chew (1998) argue that "rms areusing hybrid securities to complete the market and thereby capture a surpluswhen the underlying components are not individually available in the market(see also Van Horne, 1985). Each of the FCX securities had maturity periods often years or more.

Additionally, if short-term derivative contracts are used to unhedge, theycould give rise to adverse liquidity requirements, which can be a concern forcash constrained "rms (see Mello and Parsons, 1995, 2000). For example,assume that the gold-mining "rm follows a strategy of selling a sequence ofshort-term forward contracts to hedge the face value of straight debt, whichsigni"cantly exceeds the value of gold revenues realized during the term of theforward contract. If the price of gold were high at the time of the rollover fromone forward contract to the next, the "rm would have a cash de"cit associatedwith the loss on the forward position. This will be costly if the "rm has a binding"nancial constraint. The long-term bene"ts of the hedge would be immaterial insuch a scenario and the short-term cash #ow de"cit could even result inbankruptcy. These liquidity considerations are likely to be very important forFCX, which faces "nancial constraints and needs to preserve funds for theexpansion of mining operations. The gold-denominated securities o!er a cred-ible liquidity-matched credit-enhancement strategy relative to alternative strat-egies based on conventional short-term derivative contracts.

In Scenario G, we consider the case of a "rm that manages risk only via thebundled hedge. Indeed, our analysis suggests that "rms seeking to enhance

N.K. Chidambaran et al. / Journal of Financial Economics 60 (2001) 487}528 509

Tab

le5

Gai

nsfr

om

exp

ost

unw

ind

ing

of

the

hed

ge

Th

eta

ble

bel

ow

show

sth

eva

lue

oft

he"

rman

dit

sca

pita

lstr

uct

ure

com

pon

ents

for

ago

ldm

inin

g"

rmth

ath

asth

ree

mill

ion

ozo

fgo

ldin

rese

rves

and

buy

sa

forw

ard

cont

ract

ono

nem

illio

noz

.ofg

old

atth

ecu

rren

tm

arke

tpr

ice

of$3

00/o

z.W

eas

sum

eth

atth

eva

lue

ofth

e"

rmis

line

arin

the

pri

ceo

fgo

ldan

dth

atgo

ldpr

ices

are

dist

ribu

ted

uni

form

lyov

erth

era

nge

of$

100

per

ounc

eto

$500

per

oun

ce.T

he"

rmha

s$5

00m

illio

nin

sen

ior

deb

tan

dh

asra

ised

$251

.0b

yis

suin

gju

nio

rd

ebt.

Th

e"

rmfa

ces

ban

krup

tcy

cost

so

f$5

0m

illio

nif

itde

fau

lts.

Tw

osc

enar

ios

are

anal

yzed

corr

espo

nd

ing

toth

eh

edge

des

crib

edin

Scen

ario

Dan

dSc

enar

ioE

of

Tab

le4

asd

escr

ibed

inth

ep

anel

hea

der

s.

Min

SrD

ebt

-' Pai

dJr

Deb

t-' Pai

d(

-Def

ault

Max

Exp

ecte

dva

lue

Cha

nge

du

eto

unw

indi

ng

ScenarioF

:Unwinding

thetraditionalxrm-levelriskmanagement

Firmsellsjuniorbondsofface

value$345.9million

Firmhedgesbysellingagoldforwardfor1millionoz

Firmunwindsbybuying

agoldforwardfor1millionoz

Go

ldpr

ice

100.

018

3.3

282.

050

0.0

Res

erve

s3

33

3

Hed

geC

Fs

toco

un

ter-

par

ty!

200.

0!

116.

7!

18.0

200.

0U

nw

ind

ing

CF

sto

coun

ter-

part

y20

0.0

116.

718

.0!

200.

00

Net

CF

so

nth

efo

rwar

ds0.

00.

00.

00.

0

Fir

mva

lue

250.

050

0.0

845.

915

00.0

877.

3(

1.1)

Val

ueo

fse

nio

rd

ebt

250.

050

0.0

500.

050

0.0

474.

0(2

4.5)

Val

ueo

fju

nio

rd

ebt

0.0

0.0

345.

934

5.9

225.

0(2

6.0)

Eq

uit

yca

sh#

ows

0.0

0.0

0.0

654.

117

8.3

49.4

510 N.K. Chidambaran et al. / Journal of Financial Economics 60 (2001) 487}528

ScenarioG

:Unwindingthetargetedriskmanagement

Firmsellsjuniorgold-linkedbondsofface

value1.0millionoz

Firmunwindsbybuyingagoldforwardfor1.0millionozandpays$49.6million

Go

ldpr

ice

100.

019

9.9

283.

250

0.0

Res

erve

s3

33

3

Fir

mva

lue

200.

450

0.0

800.

014

50.4

877.

1(

4.2)

Val

ueo

fse

nio

rd

ebt

200.

450

0.0

500.

050

0.0

462.

6(1

1.4)

Val

ueo

fju

nio

rgo

ld-l

inke

dd

ebt

0.0

0.0

283.

250

0.0

238.

3(1

2.7)

Cas

h#

ow

saf

ter

pay

men

tsto

bo

ndh

old

ers

0.0

0.0

16.8

450.

4C

ash#

ow

sow

edto

coun

ter-

part

y20

0.0

100.

116

.8!

200.

0A

ctu

alca

sh#

ows

pai

dto

coun

ter-

part

y0.

00.

016

.8!

200.

0!

49.6

Eq

uit

yca

sh#

ows

0.0

0.0

0.0

650.

417

6.2

19.9

N.K. Chidambaran et al. / Journal of Financial Economics 60 (2001) 487}528 511

� We thank a referee for suggesting these important caveats.

credit quality through risk management should only use bundled hedging. Inpractice, however, it is possible that "rms will have a combination of bundledand conventional hedges outstanding at a given point in time. If so, the "rm canstill `unwinda a bundled hedge by actually unwinding a conventional hedge,provided this o!setting conventional hedge is done with the original counter-party, although Tufano (1993, 1996) has noted that hedging in the gold industryis primarily undertaken by gold-linked "nancings or forward sales betweenprincipals, making it more di$cult to unwind a hedge with the same counter-party. Nor can we rule out the possibility that such a `mixed hedgera mightmodify its future risk management program to use fewer conventional hedges, inorder to o!set the e!ect of a new bundled hedge.�

Thus, while the incentives to unwind are not completely eliminated when the"rm uses a bundled hedge, they are smaller and make it less likely that the "rmwill unhedge. A risk management strategy is usually not a one-time event, and aswe have previously noted, a "rm can implicitly unhedge by not implementinga future hedge. Our analysis of the market's pricing of FCX's gold-denominateddepositary shares later in the paper suggests that the market priced the securitiesas though risk management was credible, factoring in a signi"cant enhancementin the credit quality of the two issues. Nor do we "nd any evidence of explicitunhedging by FCX after these securities were placed.

4.2. Exogenous versus endogenous indexation of debt securities

Previous studies have examined the use of indexed debt and have identi"edtwo potential agency problems. The "rst is the ability of managers to manipulatethe variable chosen as the index. Second, a negative signal is possible when themanager has private information about the variable chosen as the index. Wediscuss below how these agency issues can be addressed by using a market-determined index such as the gold price.

Froot et al. (1989) examine the issue of indexing debt to observable variablesin the context of their study of LDC debt. They contrast two schemes ofindexation: (a) indexing debt to endogenous variables such as output or revenueand (b) indexing debt to exogenous variables such as the price of commodities.They conclude that since debtors can at least partially in#uence endogenousvariables such as the level of output, indexing debt to exogenous variables willavoid moral hazard problems.

McConnell and Schlarbaum (1981) examine income bonds used by railroadcompanies during their restructuring, and attribute the bonds' lack of popular-ity to the `smell of deatha associated with their usage. Income bonds allowa "rm to suspend interest payments during times of low earnings, and their issue

512 N.K. Chidambaran et al. / Journal of Financial Economics 60 (2001) 487}528

could represent a negative signal because managers have private informationabout future earnings. This feature can create the incentive for earnings manip-ulation by stockholders to the detriment of bondholders, paralleling the case ofoutput-indexed debt examined by Froot et al. (1989). McConnell and Schlar-baum, however, argue that the potential for such con#icts can be easily elimi-nated, and that it is the signal of "nancial trouble that explains the dearth ofincome bonds. Since FCX is unlikely to have private information about goldprices, such negative signaling consequences do not result from gold indexation.Despite providing FCX the ability to defer dividend payments in times ofearnings di$culty (the depositary shares are backed by FCX gold preferredstock), the gold depositary shares are not associated with a negative signal,unlike the income bonds.

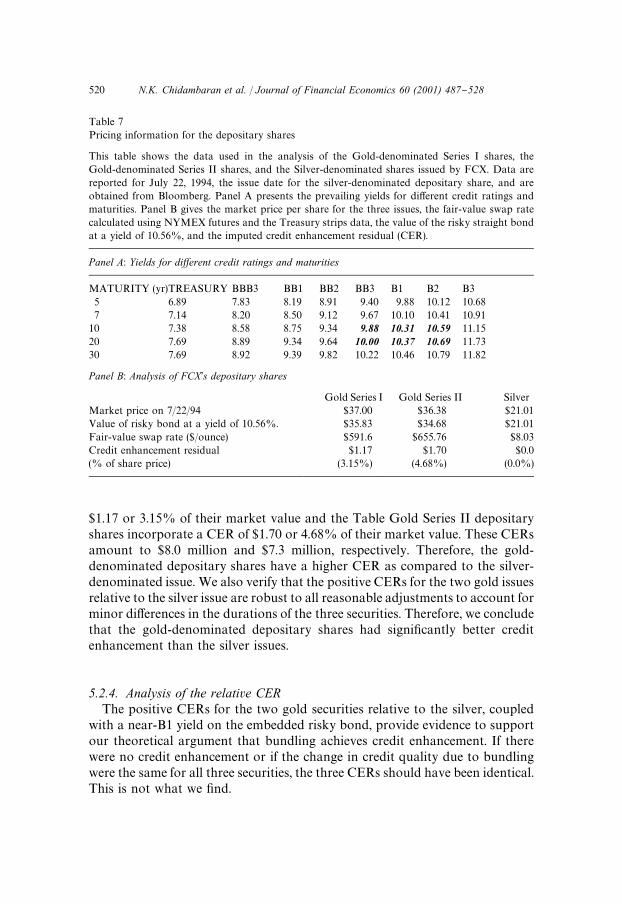

5. Detecting credit enhancement in the FCX commodity-linked depositary shares

�We analyze the pricing of the gold- and silver-denominated depositary sharesto detect whether FCX was able to enhance credit quality through bundling"nancing and risk-management, as we have hypothesized. To illustrate ourapproach, we begin with a detailed analysis of the junior gold-linked bond used inthe representative example in Section 3. We decompose the cash #ow of eachdepositary share into three components: a risky straight bond, a risk-free forwardcontract, and a credit enhancement residual (CER), which will be positive if thecredit enhancement is priced. We then calculate the di!erential in the CER foreach of FCX's two gold-denominated depositary shares relative to the silver-denominated depositary shares, and we show that this is positive in both cases.

It is important to emphasize that we do not value the depositary shares inabsolute terms. Our interest here is in determining whether the market's pricingof the depositary shares re#ects the risk management bundled by FCX. Webenchmark the pricing of the depositary shares against the pricing of similarlyrated straight debt in order to achieve this result.

5.1. Decomposition of the gold-linked bond in the illustrative example

Table 6 presents the decomposition of cash #ow for the gold-linked juniorbond (Section 3, Scenario D). Given our assumptions, both the spot and forwardprices of gold are $300/ounce, and the junior bond has a face value of onemillion ounces of gold. We decompose the cash #ow to the gold-linked bond onthe assumption that it consists of a straight bond with a face value of $300million and a riskless gold forward contract. As shown in Section 3, the bundlingof "nancing and risk management allows the bondholder to net the two cash#ows in the event of a default on the straight bond. This is shown in Table 6 asthe cash #ow to the option-to-net.

N.K. Chidambaran et al. / Journal of Financial Economics 60 (2001) 487}528 513

Tab

le6

Dec

om

po

sin

gca

sh#

ow

so

fth

ego

ld-l

ink

edbo

nd

Th

ista

ble

dec

om

pos

esth

eca

sh#ow

so

fago

ld-l

inke

db

ond

into

di!

eren

tco

mp

onen

ts.T

he

com

pon

ents

that

mak

eu

pth

ego

ld-l

inke

db

on

dar

esh

ow

nto

com

pris

eca

sh#ow

sto

ast

raig

htbo

nd

wit

ha

face

valu

eeq

ual

toth

efo

rwar

dpr

ice

ofo

ne

mill

ion

oz.o

fgol

d,a

fair

-val

uego

ld-s

wap

for

the

face

valu

e,an

dth

eca

sh#ow

so

fth

ego

ld-l

inke

db

ond

hold

ers'

opt

ion

-to-

net.

We

assu

me

that

the

valu

eo

fth

e"

rmis

linea

rin

the

pric

eo

fgo

ldan

dth

atgo

ldp

rice

sar

ed

istr

ibu

ted

unifo

rmly

ove

rth

era

nge

of$

100

per

oun

ceto

$500

per

oun

ce.T

he"

rmis

suin

gth

ego

ld-l

ink

edb

ond

has

thre

em

illio

noz

.ofg

old

rese

rves

and

sen

ior

deb

to

uts

tan

din

go

ffa

ceva

lue

$500

mill

ion

.T

he

gold

-lin

ked

bon

dan

dth

eb

und

led

risk

yb

ond

bot

hd

efau

ltat

ago

ldp

rice

of

$250

/oz.

Th

eo

ptio

n-t

o-n

etca

sh#

owo

nth

efo

rwar

dag

ain

stca

sh#

ow

so

nth

eb

ond

has

posi

tive

cash#

ows

wh

enth

eb

ond

sar

ein

defa

ult

,i.e

.,fo

ral

lgo

ldp

rice

sb

elo

w$2

50/o

z.T

he"rm

face

sb

ankr

up

tcy

cost

so

f$5

0m

illio

nif

itd

efau

lts.

Min

Sr

Deb

t-'

Pai

dJr

Deb

t-'

Pai

dM

axE

xpec

ted

valu

e(

-D

efau

lt

Go

ldp

rice

Res

erve

s,m

illio

noz

100.

018

3.3

250.

025

0.0

260.

030

0.0

500

33

33

33

3

Val

ueo

fgo

ldre

serv

es30

0.0

550.

070

0.0

750.

078

0.0

900.

015

00.0

900.

0#

CF

fro

mfo

rwar

d0

00

50.0

40.0

0.0

!20

0.0

0.0

!B

ank

rupt

cyco

st!

50.0

!50

.0!

50.0

00

00

18.7

Net

valu

e25

0.0

500.

070

0.0

800.

082

0.0

900.

013

00.0

881.

3

Dec

om

po

siti

ono

fgo

ld-l

inke

db

on

d

Val

ue

of

$300

face

bon

d0.

00.

020

0.0

300.

030

0.0

300.

030

0.0

204.

1!

CF

pai

do

nfo

rwar

d!

200.

0!

116.

67!

50.0

!50

.0!

40.0

0.0

200

0.0

#O

pti

on-t

o-N

et20

0.0

116.

6750

.00.

00.

00.

00.

046

.9T

ota

l0.

00.

020

0.0

250.

026

0.0

300.

050

0.0

251.

0

CF

togo

ld-l

ink

edbo

nd

fro

mT

able

4

Val

ueo

fju

nio

rgo

ld-l

inke

dd

ebt

0.0

0.0

200.

025

0.0

260.

030

0.0

500.

025

1.0

514 N.K. Chidambaran et al. / Journal of Financial Economics 60 (2001) 487}528