Credit Appraisal - Term Loans

92

UNIT UNIT -1 (contd) (contd) CREDIT APPRAISAL CREDIT APPRAISAL Part I Part I -Term Loans Term Loans

-

Upload

poppyeolive -

Category

Documents

-

view

229 -

download

2

Transcript of Credit Appraisal - Term Loans

8/6/2019 Credit Appraisal - Term Loans

http://slidepdf.com/reader/full/credit-appraisal-term-loans 1/92

UNITUNIT --11 (contd)(contd)

CREDIT APPRAISALCREDIT APPRAISALPart IPart I --Term LoansTerm Loans

8/6/2019 Credit Appraisal - Term Loans

http://slidepdf.com/reader/full/credit-appraisal-term-loans 2/92

Topics coveredTopics covered1.1. Sources of financeSources of finance long termlong term

2.2. Term loansTerm loans featuresfeatures

3.3. Project appraisalProject appraisal

4.4. Lending norms and policies of banksLending norms and policies of banks

8/6/2019 Credit Appraisal - Term Loans

http://slidepdf.com/reader/full/credit-appraisal-term-loans 3/92

Sources of financeSources of finance long termlong term

SharesSharesEquity & retained earningsEquity & retained earnings

PreferencePreference

Debentures / bondsDebentures / bonds

Lease financingLease financing

Deferred credit Deferred credit

Term loansTerm loans Foreign sourcesForeign sources GDRs/ADRs, ForeignGDRs/ADRs, Foreign

bonds and foreign currency loansbonds and foreign currency loans

8/6/2019 Credit Appraisal - Term Loans

http://slidepdf.com/reader/full/credit-appraisal-term-loans 4/92

EQUITY SHARESEQUITY SHARES --FE ATURESFE ATURES Ownership securitiesOwnership securities

Right to controlRight to control -- Voting rights Voting rights

Right to residual profitsRight to residual profits

Right in liquidationRight in liquidation residual claim overresidual claim overassetsassets

Returns in the form of dividends andReturns in the form of dividends andcapital appreciationcapital appreciation

Riskier than debt instrumentsRiskier than debt instruments

8/6/2019 Credit Appraisal - Term Loans

http://slidepdf.com/reader/full/credit-appraisal-term-loans 5/92

EQUITY SHARESEQUITY SHARES Advantages to investor Advantages to investor

* Higher returns expected than debt * Higher returns expected than debt

* Dividends tax free in hands of investor* Dividends tax free in hands of investor

* Liquidity* Liquidity -- traded in stock exchangetraded in stock exchange

* Wealth sharing* Wealth sharing

Disadvantages to investorDisadvantages to investor* Higher risk* Higher risk

* Not obligatory for issuer to pay* Not obligatory for issuer to pay

dividendsdividends

8/6/2019 Credit Appraisal - Term Loans

http://slidepdf.com/reader/full/credit-appraisal-term-loans 6/92

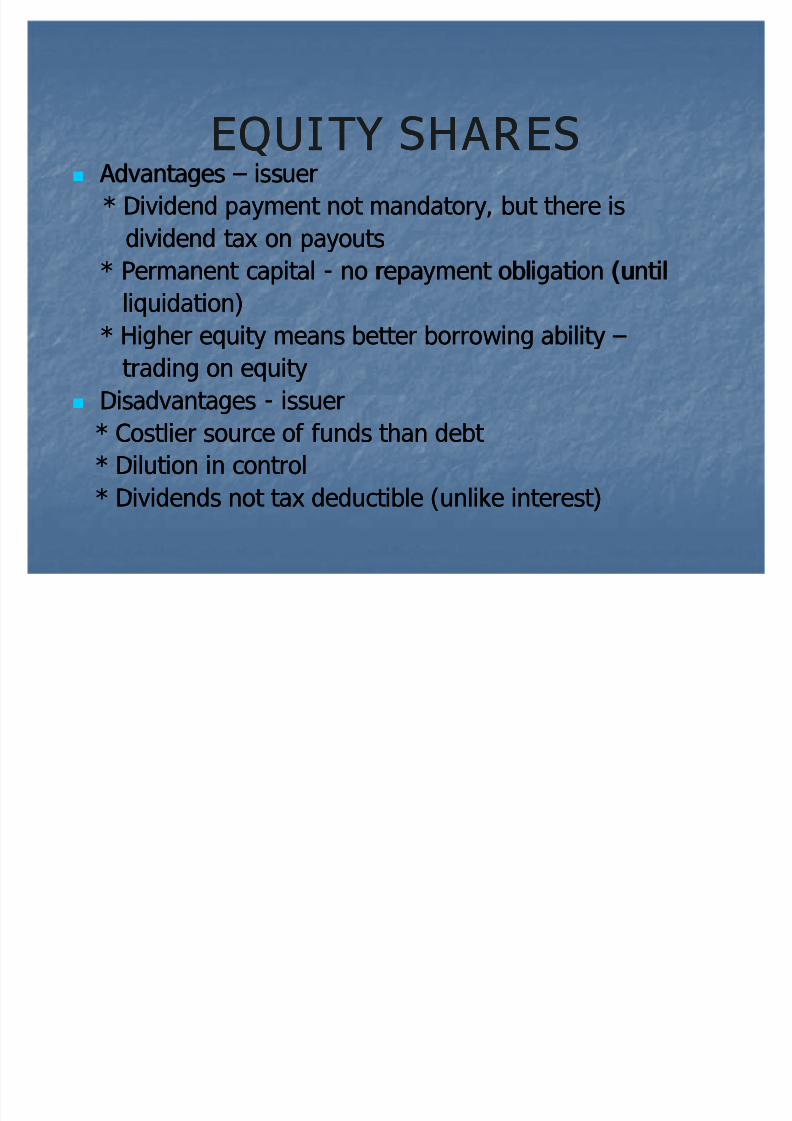

EQUITY SHARESEQUITY SHARES Advantages Advantages issuerissuer

* Dividend payment not mandatory, but there is* Dividend payment not mandatory, but there is

dividend tax on payoutsdividend tax on payouts

* Permanent capital* Permanent capital -- no repayment obligation (untilno repayment obligation (untilliquidation)liquidation)

* Higher equity means better borrowing ability* Higher equity means better borrowing ability

trading on equitytrading on equity

DisadvantagesDisadvantages -- issuerissuer* Costlier source of funds than debt * Costlier source of funds than debt

* Dilution in control* Dilution in control

* Dividends not tax deductible (unlike interest)* Dividends not tax deductible (unlike interest)

8/6/2019 Credit Appraisal - Term Loans

http://slidepdf.com/reader/full/credit-appraisal-term-loans 7/92

RET AINED E ARNINGSRET AINED E ARNINGS

Readily available internally (internalReadily available internally (internalequity)equity)

No issue costsNo issue costs

No dilution in controlNo dilution in control

Reflects the robustness of companysReflects the robustness of companyshealth and reduces dependance onhealth and reduces dependance on

outside fundingoutside funding The only point to be remembered isThe only point to be remembered is

retained earnings also has a cost in termsretained earnings also has a cost in termsof opportunity cost to investorsof opportunity cost to investors

8/6/2019 Credit Appraisal - Term Loans

http://slidepdf.com/reader/full/credit-appraisal-term-loans 8/92

PREFERENCE SHARESPREFERENCE SHARES

Preference over equity shareholders in payment Preference over equity shareholders in payment of dividends and in repayment of capitalof dividends and in repayment of capital

While their claim is above equity shareholders, it While their claim is above equity shareholders, it

is subordinate to the claims of all otheris subordinate to the claims of all otherstakeholdersstakeholders Preference dividend generally paid as a fixed %Preference dividend generally paid as a fixed %

of face value of sharesof face value of shares No voting rights except in matters whichNo voting rights except in matters which

concern themconcern them Types of preference sharesTypes of preference shares--

redeemable,irredeemable, participating,nonredeemable,irredeemable, participating,non--participating, cumulative,nonparticipating, cumulative,non-- cum.cum.

8/6/2019 Credit Appraisal - Term Loans

http://slidepdf.com/reader/full/credit-appraisal-term-loans 9/92

PREFERENCE SHARES (contd)PREFERENCE SHARES (contd)

Advantag es to inv estor Advantag es to inv estor : : Lesser ris k t han in equiti es Less er ris k t han in equiti es No ta x on divid ends No ta x on divid ends

Disadvantag es to inv estor:Disadvantag es to inv estor: Less er r et urns t han equiti es Less er r et urns t han equiti es Less li quid t han equiti es Less li quid t han equiti es

Advantag es to iss uer Advantag es to iss uer : :

Less er cost o f ca pita lLess er cost o f ca pita l Divid end pa yment not o bligator yDivid end pa yment not o bligator y No loss o f contro lNo loss o f contro l

Disadvantag es to iss uer Disadvantag es to iss uer : : Divid ends not ta x d ed ucti ble f or iss uer Divid ends not ta x d ed ucti ble f or iss uer

8/6/2019 Credit Appraisal - Term Loans

http://slidepdf.com/reader/full/credit-appraisal-term-loans 10/92

DEBENTURES / BONDSDEBENTURES / BONDS Debt instrument bearing Face value, coupon rate of Debt instrument bearing Face value, coupon rate of

interest, maturity periodinterest, maturity period

Interest to be paid every year at coupon rateInterest to be paid every year at coupon rate

Redemption on maturityRedemption on maturity

Redemption valueRedemption value at par, at premium,at discount at par, at premium,at discount

Generally market price is at a discount to face valueGenerally market price is at a discount to face value

Yield (return w.r.t market price) inversely related to Yield (return w.r.t market price) inversely related to

market pricemarket price Current yield/ Yield to maturity (YTM )Current yield/ Yield to maturity (YTM )

8/6/2019 Credit Appraisal - Term Loans

http://slidepdf.com/reader/full/credit-appraisal-term-loans 11/92

DEBENTURESDEBENTURES Advantage to investor Advantage to investor

Lesser risk than equities (though lesser return)Lesser risk than equities (though lesser return)

Advantages to issuer : Advantages to issuer : Lower cost of fundsLower cost of funds

Interest is tax deductibleInterest is tax deductible

No loss of controlNo loss of control

Disadvantages to issuer :Disadvantages to issuer : Interest payment mandatoryInterest payment mandatory

Redemption cash outflowsRedemption cash outflows

Increases financial riskIncreases financial risk

8/6/2019 Credit Appraisal - Term Loans

http://slidepdf.com/reader/full/credit-appraisal-term-loans 12/92

Types of debenturesTypes of debentures

Non convertibleNon convertible not convertible to equity sharesnot convertible to equity shares

Partly convertiblePartly convertible part of face value of debenturepart of face value of debentureconverted to equity at predetermined price, balanceconverted to equity at predetermined price, balance

as debenture with interest payableas debenture with interest payable

Fully convertibleFully convertible entire face value of debentureentire face value of debentureconverted into equity sharesconverted into equity shares

Zero coupon bondsZero coupon bonds no interim interest payment,no interim interest payment,

issued at discount to face value, redeemed at par,issued at discount to face value, redeemed at par,difference represents discount treated as capitaldifference represents discount treated as capitalgainsgains also called deep discount bondalso called deep discount bond

8/6/2019 Credit Appraisal - Term Loans

http://slidepdf.com/reader/full/credit-appraisal-term-loans 13/92

CONVERTIBLE DEBENTURESCONVERTIBLE DEBENTURES Conversion to equity after a point of Conversion to equity after a point of

time at a predetermined ratetime at a predetermined rate

The debenture will earn interest on faceThe debenture will earn interest on facevalue until conversion after which it willvalue until conversion after which it willearn dividends and capital appreciationearn dividends and capital appreciation

If partly convertible then only a part of If partly convertible then only a part of the face value is converted to equitythe face value is converted to equityand balance continues to earn interest and balance continues to earn interest

8/6/2019 Credit Appraisal - Term Loans

http://slidepdf.com/reader/full/credit-appraisal-term-loans 14/92

Advantages of conv. debentures Advantages of conv. debentures No redemption cash outflowsNo redemption cash outflows

Lower interest payments initially andLower interest payments initially and

higher dividends to investors laterhigher dividends to investors later Shown as debt until conversion afterShown as debt until conversion afterwhich it is shown under equity ( betterwhich it is shown under equity ( better

debt equity ratios)debt equity ratios) To the investor , fixed interest initially,To the investor , fixed interest initially,

possibility of profit and wealth sharingpossibility of profit and wealth sharinglaterlater

8/6/2019 Credit Appraisal - Term Loans

http://slidepdf.com/reader/full/credit-appraisal-term-loans 15/92

DEFERRED CREDITDEFERRED CREDIT

Suppliers of equipment allow buyer to paySuppliers of equipment allow buyer to payin instalments spread over several years.in instalments spread over several years.

The period over which instalments areThe period over which instalments arespread over & finance charges depend onspread over & finance charges depend on

Credit standing of the buyerCredit standing of the buyer

Value of equipment Value of equipment

Demand for the equipment in the market Demand for the equipment in the market

8/6/2019 Credit Appraisal - Term Loans

http://slidepdf.com/reader/full/credit-appraisal-term-loans 16/92

LE ASE FIN ANCINGLE ASE FIN ANCING

A contractual arrangement where the lessor A contractual arrangement where the lessorgrants the lessee the right to use an asset ingrants the lessee the right to use an asset inreturn for periodical lease rental paymentsreturn for periodical lease rental payments

Asset reverts to lessor at the end Asset reverts to lessor at the end

Operating lease vs. finance leaseOperating lease vs. finance lease

Lease rentals payable by lessee are taxLease rentals payable by lessee are tax

deductibledeductible Depreciation tax benefits to lessor/lesseeDepreciation tax benefits to lessor/lessee

Flexibility in structuring lease rental paymentsFlexibility in structuring lease rental payments

to lessee but costly source of financeto lessee but costly source of finance

8/6/2019 Credit Appraisal - Term Loans

http://slidepdf.com/reader/full/credit-appraisal-term-loans 17/92

GLOB AL DEPOSITORY RECEIPTSGLOB AL DEPOSITORY RECEIPTS (GDRs)(GDRs)

Means of raising funds from foreign investors inMeans of raising funds from foreign investors inthe form of shares issued in foreign countriesthe form of shares issued in foreign countries

Mechanism by which such foreign shares issuedMechanism by which such foreign shares issued

are held by a depositoryare held by a depository A depository is usually a large international A depository is usually a large international

bank which receives dividends , reports etc onbank which receives dividends , reports etc onbehalf of the individual investorsbehalf of the individual investors

Each depository receipt (DR) represents a claimEach depository receipt (DR) represents a claimagainst a specified number of sharesagainst a specified number of shares

They are denominated in a convertible currencyThey are denominated in a convertible currencyusually US $usually US $

8/6/2019 Credit Appraisal - Term Loans

http://slidepdf.com/reader/full/credit-appraisal-term-loans 18/92

GDRs (contd)GDRs (contd) They are listed and traded on internationalThey are listed and traded on international

stock exchangesstock exchanges

The issuer pays dividends in home currencyThe issuer pays dividends in home currencywhich is converted into dollars by thewhich is converted into dollars by thedepository and distributed to DR holdersdepository and distributed to DR holders

Shown as share capital only on conversionShown as share capital only on conversion(t wo way fungibility)(t wo way fungibility)

Represent non voting sharesRepresent non voting shares firm entersfirm entersinto an agreement with depositoryinto an agreement with depository

If ADR, listed on NYSE/ NASDAQ , adherenceIf ADR, listed on NYSE/ NASDAQ , adherenceto US GAAP , several levels (1 to 3)to US GAAP , several levels (1 to 3)

8/6/2019 Credit Appraisal - Term Loans

http://slidepdf.com/reader/full/credit-appraisal-term-loans 19/92

FOREIGN BONDSFOREIGN BONDS

Means of raising foreign funds in the formMeans of raising foreign funds in the formof bonds issued in foreign countriesof bonds issued in foreign countries

Denominated in foreign currencyDenominated in foreign currency knownknownby local names like Yankee bonds, Samuraiby local names like Yankee bonds, Samuraibondsbonds

Like domestic bonds they also have faceLike domestic bonds they also have facevalue, coupon rate, maturity period , fixedvalue, coupon rate, maturity period , fixedor floating rates of interest ( LIBOR +or floating rates of interest ( LIBOR +basis points where 100 basis points = 1%)basis points where 100 basis points = 1%)

8/6/2019 Credit Appraisal - Term Loans

http://slidepdf.com/reader/full/credit-appraisal-term-loans 20/92

FOREIGN LO ANSFOREIGN LO ANS

Foreign currency loans from banksForeign currency loans from banks Syndicated creditsSyndicated credits--Where t wo or moreWhere t wo or more

banks join together to lend largebanks join together to lend largeamounts, lead manager acts as agent amounts, lead manager acts as agent

and administers loanand administers loan disbursing fundsdisbursing funds, collecting and distributing interest +, collecting and distributing interest +principal repaymentsprincipal repayments

Foreign funds are classified as ECBsForeign funds are classified as ECBs(External commercial borrowings) and(External commercial borrowings) andinclude bank loans, suppliers credit,include bank loans, suppliers credit,foreign bonds, loans from IFC,AD B etcforeign bonds, loans from IFC,AD B etc

and GD Rsand GD Rs

8/6/2019 Credit Appraisal - Term Loans

http://slidepdf.com/reader/full/credit-appraisal-term-loans 21/92

TERM LO ANSTERM LO ANS -- featuresfeatures Loans given by banks/financial institutions onLoans given by banks/financial institutions on

long term basislong term basis Interest payments and principal repayment Interest payments and principal repayment

generally spread over 8generally spread over 8 15 yrs15 yrs

Loans available for setting up new projects andLoans available for setting up new projects andalso for expansion/renovationalso for expansion/renovation Allowed in both rupee loans and foreign currency Allowed in both rupee loans and foreign currency

loansloans for meeting cost of imported equipment ,for meeting cost of imported equipment ,cost of technology , knowhow etccost of technology , knowhow etc

Loan account maintained in foreign currency,Loan account maintained in foreign currency,interest & instalments converted to rupees oninterest & instalments converted to rupees onrepayment at prevailing ratesrepayment at prevailing rates

8/6/2019 Credit Appraisal - Term Loans

http://slidepdf.com/reader/full/credit-appraisal-term-loans 22/92

TERM LO ANS (contd)TERM LO ANS (contd)

Security/CollateralSecurity/Collateral by hypothecation /by hypothecation /mortgage of propertymortgage of property

Generally by first charge on the assetsGenerally by first charge on the assetsfinanced and second charge on all otherfinanced and second charge on all otherassets of the firmassets of the firm

Restrictive covenants imposedRestrictive covenants imposed

Asset financing vs. project financing Asset financing vs. project financing

8/6/2019 Credit Appraisal - Term Loans

http://slidepdf.com/reader/full/credit-appraisal-term-loans 23/92

Asset financing vs. project financing Asset financing vs. project financing

In asset financing, loans given for assets likeIn asset financing, loans given for assets likevehicles , equipment repayable in mediumvehicles , equipment repayable in mediumterm of 3term of 3--5 yrs5 yrs

In project financing, loans granted for largeIn project financing, loans granted for largescale investment projects on the expectationscale investment projects on the expectationthat it will realise a cash flow sufficient tothat it will realise a cash flow sufficient tocover cost of operations and debt service.cover cost of operations and debt service.

InvolvesInvolves project appraisalproject appraisal of technical,of technical,economic and financial aspects for evaluatingeconomic and financial aspects for evaluatingproject feasibilityproject feasibility both strengths andboth strengths andweaknesses are considered.weaknesses are considered.

8/6/2019 Credit Appraisal - Term Loans

http://slidepdf.com/reader/full/credit-appraisal-term-loans 24/92

Significance of project appraisalSignificance of project appraisal

Since projects involveSince projects involve

Substantial cash outlays upfront Substantial cash outlays upfront Benefits extend into the futureBenefits extend into the future

Irreversible decisionsIrreversible decisions

To stop bad projects from being acceptedTo stop bad projects from being accepted To prevent good projects from beingTo prevent good projects from being

rejectedrejected

8/6/2019 Credit Appraisal - Term Loans

http://slidepdf.com/reader/full/credit-appraisal-term-loans 25/92

Project appraisalProject appraisal

A detailed feasibility study is done and Detailed A detailed feasibility study is done and Detailed

Project Report (DPR) is compiled givingProject Report (DPR) is compiled giving

Project cost estimateProject cost estimate Means of financingMeans of financing

Schedule of implementationSchedule of implementation

Projected profitabilityProjected profitability projected sales , costsprojected sales , costs

Projected cash flow and debt servicingProjected cash flow and debt servicingcapabilitycapability

Social profitabilitySocial profitability

8/6/2019 Credit Appraisal - Term Loans

http://slidepdf.com/reader/full/credit-appraisal-term-loans 26/92

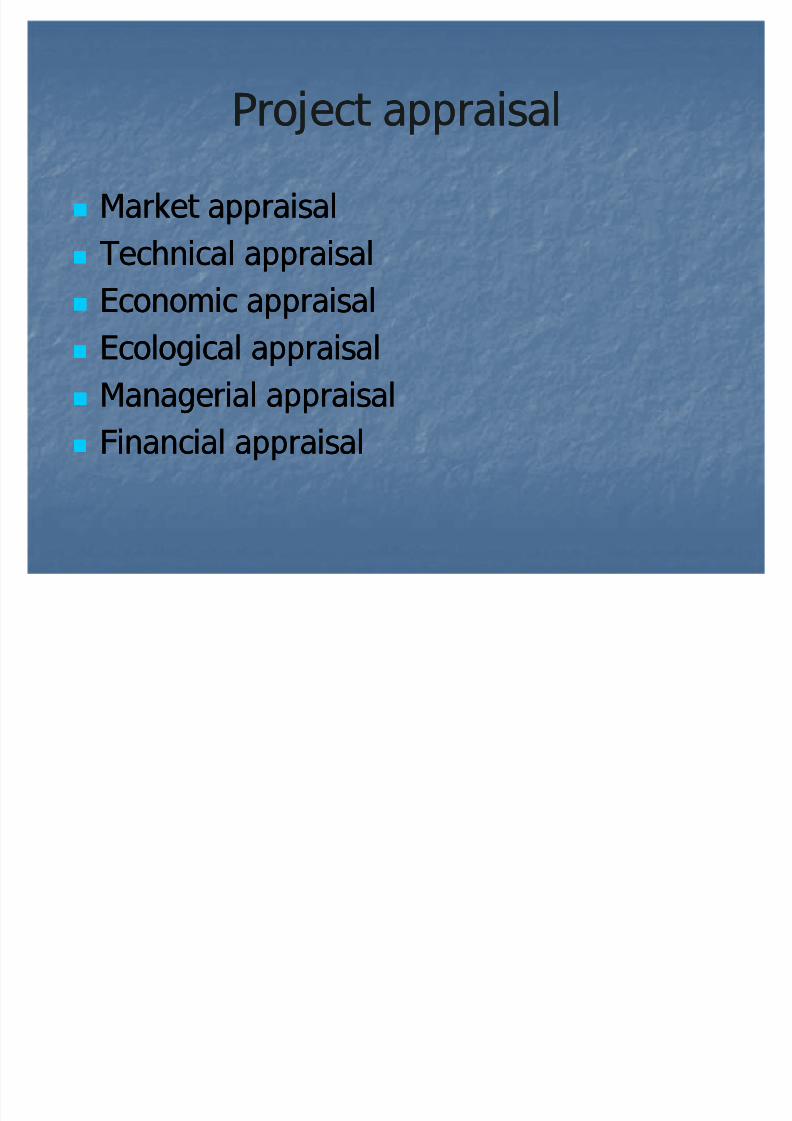

Project appraisalProject appraisal

Market appraisalMarket appraisal

Technical appraisalTechnical appraisal

Economic appraisalEconomic appraisal

Ecological appraisalEcological appraisal

Managerial appraisalManagerial appraisal Financial appraisalFinancial appraisal

8/6/2019 Credit Appraisal - Term Loans

http://slidepdf.com/reader/full/credit-appraisal-term-loans 27/92

8/6/2019 Credit Appraisal - Term Loans

http://slidepdf.com/reader/full/credit-appraisal-term-loans 28/92

Technical appraisalTechnical appraisal Seeks to determine whether the prerequisitesSeeks to determine whether the prerequisites

for successful project commisioning have beenfor successful project commisioning have beenconsidered and reasonably good choices haveconsidered and reasonably good choices havebeen made regarding location, size and processbeen made regarding location, size and process

Availability of required quality & quantity of raw Availability of required quality & quantity of raw material and inputsmaterial and inputs

Availability of utilities like power, water etc Availability of utilities like power, water etc

Appropriateness of plant design & layout Appropriateness of plant design & layout

Proposed technology vs. alternatives availableProposed technology vs. alternatives available Optimality of scale of operationsOptimality of scale of operations

Technical specifications of P&M etcTechnical specifications of P&M etc

8/6/2019 Credit Appraisal - Term Loans

http://slidepdf.com/reader/full/credit-appraisal-term-loans 29/92

Economic appraisalEconomic appraisal

Involves social cost benefit analysisInvolves social cost benefit analysis

Economic benefits & costs measured inEconomic benefits & costs measured interms of shadow (efficiency) pricesterms of shadow (efficiency) prices

Impact of project on income distribution,Impact of project on income distribution,level of savings and investmentslevel of savings and investments

Contribution of project towards economic/Contribution of project towards economic/

social objectives like self sufficiency,social objectives like self sufficiency,employment generation, social order etcemployment generation, social order etc

8/6/2019 Credit Appraisal - Term Loans

http://slidepdf.com/reader/full/credit-appraisal-term-loans 30/92

Ecological appraisalEcological appraisal

Particularly for projects like power plants,Particularly for projects like power plants,irrigation, environment polluting industriesirrigation, environment polluting industries

like bulk drugs and chemicals in terms of like bulk drugs and chemicals in terms of Likely damage to be caused to theLikely damage to be caused to the

environment environment

Cost of restoration measures for ensuring that Cost of restoration measures for ensuring that damage is minimised/within acceptable limitsdamage is minimised/within acceptable limits

8/6/2019 Credit Appraisal - Term Loans

http://slidepdf.com/reader/full/credit-appraisal-term-loans 31/92

Managerial appraisalManagerial appraisal Capacity & commitment of core promoters and topCapacity & commitment of core promoters and topmanagement (based on past performance , othermanagement (based on past performance , other

ventures, progress achieved on present venture etc)ventures, progress achieved on present venture etc) CapacityCapacity

Ability to plan clearly and set realistic goals & objectives Ability to plan clearly and set realistic goals & objectives

Ability to organise Ability to organise Ability to select right kind of people and lead them Ability to select right kind of people and lead them

effectivelyeffectively Negotiating capabilityNegotiating capability Problem solving abilitiesProblem solving abilities

Communication and HR skillsCommunication and HR skills Commitment Commitment

Willingness to bring in more capital into project if neededWillingness to bring in more capital into project if needed Ability and willingness to work hard, take on new Ability and willingness to work hard, take on new

challenges and adaptability to different circumstanceschallenges and adaptability to different circumstances

8/6/2019 Credit Appraisal - Term Loans

http://slidepdf.com/reader/full/credit-appraisal-term-loans 32/92

Financial appraisalFinancial appraisal

For evaluating profitability and financialFor evaluating profitability and financialstrength of businessstrength of business

To study financial viability in terms of debt To study financial viability in terms of debt servicing plus ability to satisfy capitalservicing plus ability to satisfy capitalproviders on their expected rates of returnproviders on their expected rates of return Project cost Project cost

Means of financing and cost of capitalMeans of financing and cost of capital

Projected profitabilityProjected profitability Breakeven point Breakeven point

Projected cash flows and financial positionProjected cash flows and financial position

Level of riskLevel of risk

8/6/2019 Credit Appraisal - Term Loans

http://slidepdf.com/reader/full/credit-appraisal-term-loans 33/92

Financial appraisalFinancial appraisal Includes identification of various elements of Includes identification of various elements of

project cost project cost

Determination of accuracy of individual cost Determination of accuracy of individual cost elementselements

Accuracy of assumptions with reference to sales Accuracy of assumptions with reference to salesfigures , growth rates and operating costsfigures , growth rates and operating costs

Suitability of proposed financing patternSuitability of proposed financing pattern

Ability of project to generate adequate cash Ability of project to generate adequate cashflows for debt servicing as well as for providingflows for debt servicing as well as for providingadequate rate of return to capital financiersadequate rate of return to capital financiers

8/6/2019 Credit Appraisal - Term Loans

http://slidepdf.com/reader/full/credit-appraisal-term-loans 34/92

Financial appraisalFinancial appraisal

Cost benefit analysis must be doneCost benefit analysis must be done capital budgeting analysiscapital budgeting analysis

Costs will be in terms of Costs will be in terms of

Capital expenditure or initial outlay to beCapital expenditure or initial outlay to beincurred generally at t incurred generally at t 00

Annual operating costs including materials, Annual operating costs including materials,labour,overheads(both variable & fixed costs)labour,overheads(both variable & fixed costs)

Benefits will be in terms of increase inBenefits will be in terms of increase inrevenues or cost savings or both over nrevenues or cost savings or both over nnumber of yearsnumber of years

8/6/2019 Credit Appraisal - Term Loans

http://slidepdf.com/reader/full/credit-appraisal-term-loans 35/92

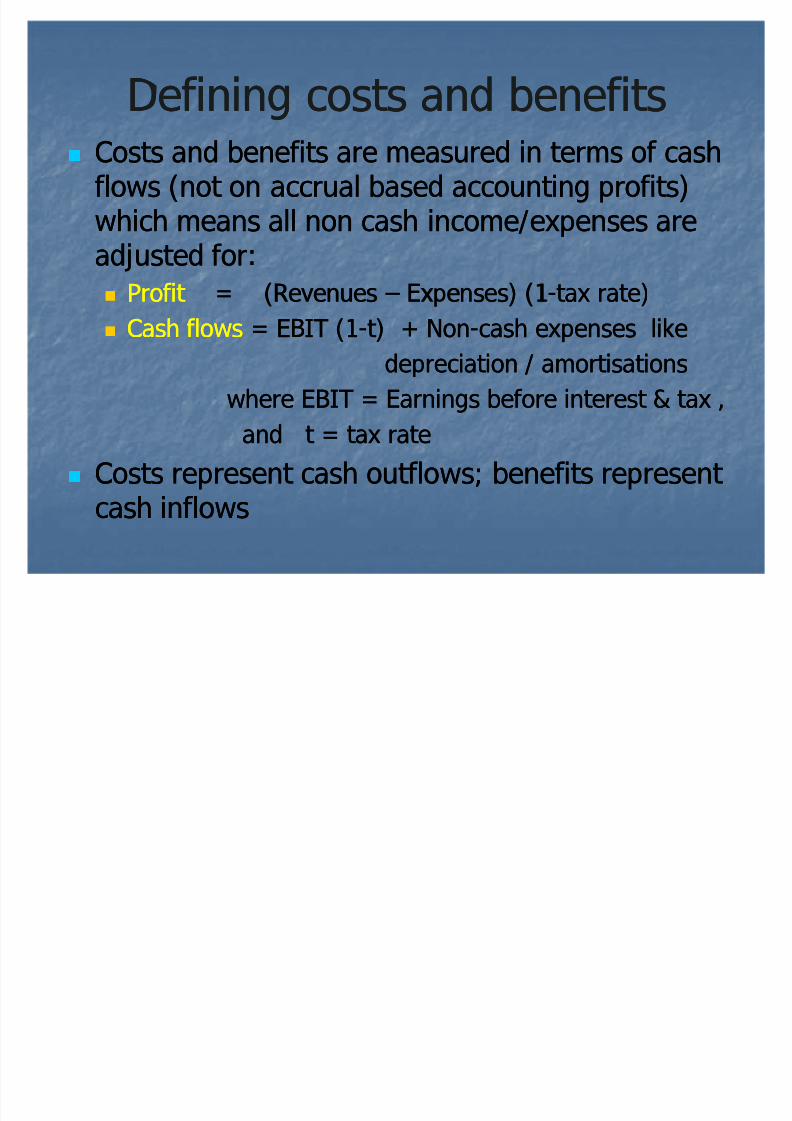

Defining costs and benefitsDefining costs and benefits Costs and benefits are measured in terms of cashCosts and benefits are measured in terms of cash

flows (not on accrual based accounting profits)flows (not on accrual based accounting profits)which means all non cash income/expenses arewhich means all non cash income/expenses areadjusted for:adjusted for:

Profit Profit = (Revenues= (Revenues Expenses) (1Expenses) (1--tax rate)tax rate)

Cash flowsCash flows = EBIT (1= EBIT (1--t) + Nont) + Non--cash expenses likecash expenses like

depreciation / amortisationsdepreciation / amortisations

where E

BIT = Earnings before interest & tax ,

where E

BIT = Earnings before interest & tax ,and t = tax rateand t = tax rate

Costs represent cash outflows; benefits represent Costs represent cash outflows; benefits represent cash inflowscash inflows

8/6/2019 Credit Appraisal - Term Loans

http://slidepdf.com/reader/full/credit-appraisal-term-loans 36/92

Defining costs and benefitsDefining costs and benefits

Post tax cash flows to be consideredPost tax cash flows to be considered

Incremental cash flows must be consideredIncremental cash flows must be considered

Opportunity costs must be consideredOpportunity costs must be considered

Net cash flows to be considered fromNet cash flows to be considered fromperspective of suppliers of long term fundsperspective of suppliers of long term funds Interest on long term loans not to be includedInterest on long term loans not to be included

as it is recognised as an opportunity cost in theas it is recognised as an opportunity cost in thediscount rate and if taken into account will leaddiscount rate and if taken into account will leadto double countingto double counting

Interest on short term borrowings is howeverInterest on short term borrowings is howeverincludedincluded

8/6/2019 Credit Appraisal - Term Loans

http://slidepdf.com/reader/full/credit-appraisal-term-loans 37/92

Determining project cost Determining project cost Land & buildingLand & building Plant & machineryPlant & machinery Technical knowhow, engineering & consultingTechnical knowhow, engineering & consulting

feesfees

Expenses on account of foreign technicians,Expenses on account of foreign technicians,training of Indian technicians abroadtraining of Indian technicians abroad Misc. fixed assets like elec. installations, furnitureMisc. fixed assets like elec. installations, furniture

& fittings& fittings Preliminary & pre operative expensesPreliminary & pre operative expenses Provisions & contingenciesProvisions & contingencies Margin on working capitalMargin on working capital

(Note: All except margin on working capital are(Note: All except margin on working capital arecapital costs)capital costs)

8/6/2019 Credit Appraisal - Term Loans

http://slidepdf.com/reader/full/credit-appraisal-term-loans 38/92

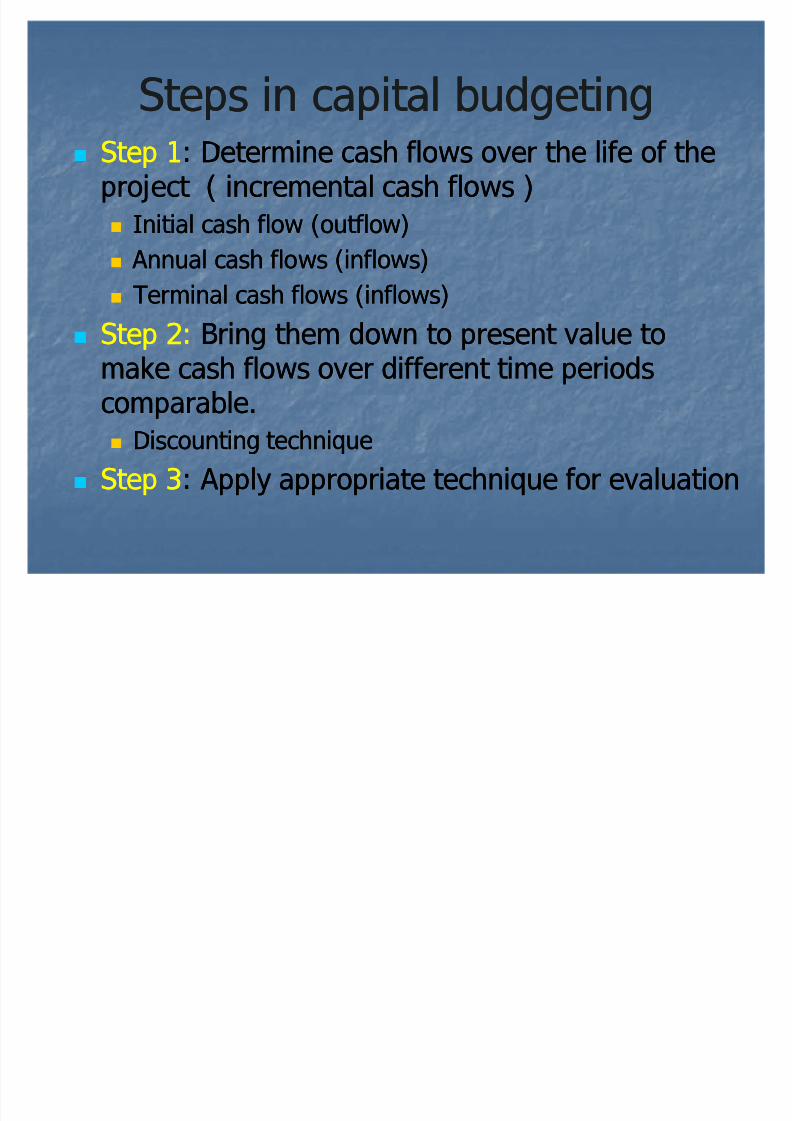

Steps in capital budgetingSteps in capital budgeting Step 1Step 1: Determine cash flows over the life of the: Determine cash flows over the life of the

project ( incremental cash flows )project ( incremental cash flows )

Initial cash flow (outflow)Initial cash flow (outflow)

Annual cash flows (inflows) Annual cash flows (inflows)

Terminal cash flows (inflows)Terminal cash flows (inflows)

Step 2:Step 2: Bring them down to present value toBring them down to present value tomake cash flows over different time periodsmake cash flows over different time periods

comparable.comparable. Discounting techniqueDiscounting technique

Step 3Step 3: Apply appropriate technique for evaluation: Apply appropriate technique for evaluation

8/6/2019 Credit Appraisal - Term Loans

http://slidepdf.com/reader/full/credit-appraisal-term-loans 39/92

Steps in capital budgetingSteps in capital budgeting

1)1) Determining Cash FlowsDetermining Cash Flows

Look at all incremental cash flows occurring asLook at all incremental cash flows occurring asa result of investment a result of investment

Initial cash outflowInitial cash outflow == Capital expenditure +Capital expenditure +initial investment in working capital (Totalinitial investment in working capital (Totalproject cost except contingency)project cost except contingency)

Annual Cash Flows Annual Cash Flows over the life of the project over the life of the project

= EBIT (1= EBIT (1--t) + Depreciation +/t) + Depreciation +/--Decrease/increase in working capitalDecrease/increase in working capital

Terminal Cash FlowsTerminal Cash Flows = = Salvage value of assetsSalvage value of assets+ working capital released at the end+ working capital released at the end

8/6/2019 Credit Appraisal - Term Loans

http://slidepdf.com/reader/full/credit-appraisal-term-loans 40/92

Step 1Step 1-- Determining cash flowsDetermining cash flows

0 1 2 3 4 5 n6 . . .

Terminal

Cash flow

Annual Cash Flows

Initial cashoutflow

8/6/2019 Credit Appraisal - Term Loans

http://slidepdf.com/reader/full/credit-appraisal-term-loans 41/92

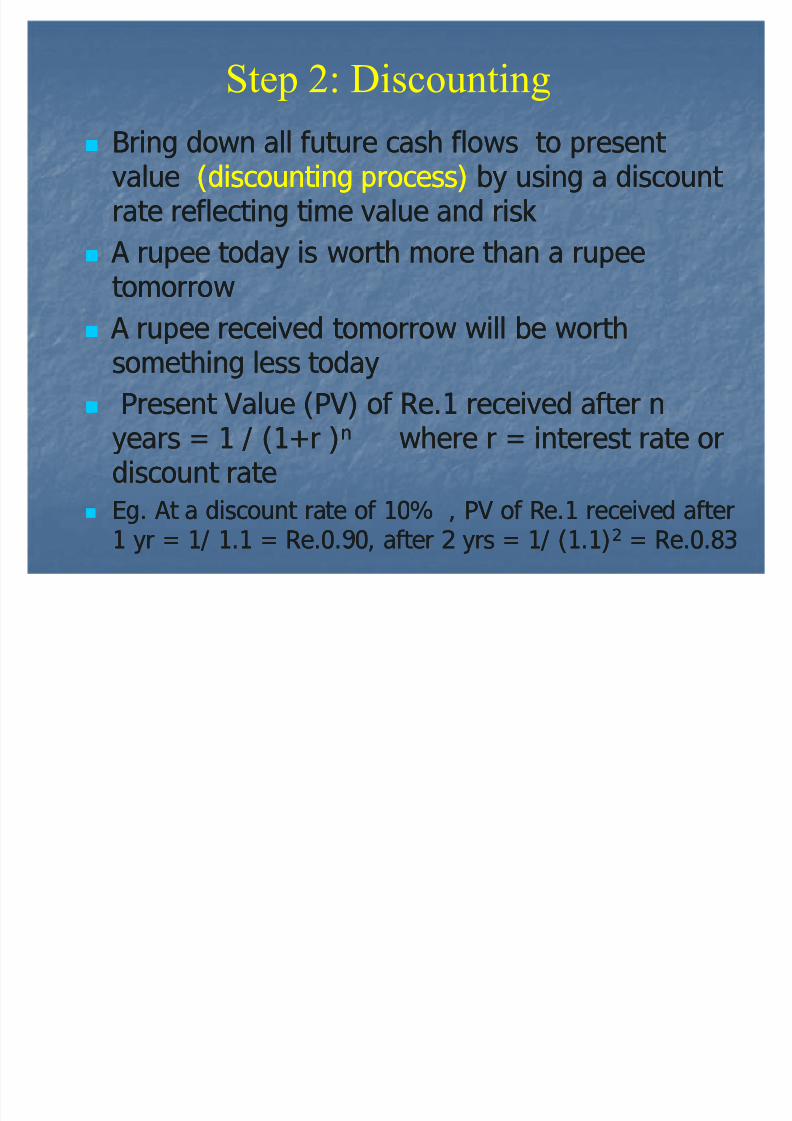

Bring down all future cash flows to present Bring down all future cash flows to present valuevalue (discounting process)(discounting process) by using a discount by using a discount rate reflecting time value and riskrate reflecting time value and risk

A rupee today is worth more than a rupee A rupee today is worth more than a rupee

tomorrowtomorrow

A rupee received tomorrow will be worth A rupee received tomorrow will be worthsomething less todaysomething less today

Present Value (PV) of Re.1 received after nPresent Value (PV) of Re.1 received after nyears = 1 / (1+r )years = 1 / (1+r )nn where r = interest rate orwhere r = interest rate ordiscount ratediscount rate

Eg. At a discount rate of 10% , PV of Re.1 received afterEg. At a discount rate of 10% , PV of Re.1 received after

1 yr = 1/ 1.1 = Re.0.90, after 2 yrs = 1/ (1.1)1 yr = 1/ 1.1 = Re.0.90, after 2 yrs = 1/ (1.1)22

= Re.0.83= Re.0.83

Step 2: Discounting

8/6/2019 Credit Appraisal - Term Loans

http://slidepdf.com/reader/full/credit-appraisal-term-loans 42/92

Step 2: DiscountingStep 2: Discounting

The discount rate represents anThe discount rate represents anopportunity cost or required rate of returnopportunity cost or required rate of return( k or r)( k or r)

We can use the firmsWe can use the firms cost of capitalcost of capital ororcost of funds as the discount rate forcost of funds as the discount rate forinvestment projects.investment projects.

Cost of capital is aw

eighted average cost Cost of capital is aw

eighted average cost of all sources of financingof all sources of financing

Cost of equity and retained earningsCost of equity and retained earnings

Cost of debt (post tax)Cost of debt (post tax)

8/6/2019 Credit Appraisal - Term Loans

http://slidepdf.com/reader/full/credit-appraisal-term-loans 43/92

Illustration for discountingIllustration for discounting

A project gives cash flows as follows: A project gives cash flows as follows:

Year 1 = Rs.4000, year 2 = Rs. 5000 Year 1 = Rs.4000, year 2 = Rs. 5000and year 4 = Rs.8000and year 4 = Rs.8000

What is the worth of the investment What is the worth of the investment today if the cost of capital is 8% ?today if the cost of capital is 8% ?

Solution: PV =Solution: PV = 40004000 ++ 50005000 ++ 80008000

(1.08) (1.08)(1.08) (1.08)22 (1.08)(1.08)44

= 3704 + 4274 + 5882 == 3704 + 4274 + 5882 = 1386013860

8/6/2019 Credit Appraisal - Term Loans

http://slidepdf.com/reader/full/credit-appraisal-term-loans 44/92

The ideal evaluation method should:The ideal evaluation method should:

a) includea) include all cash flow

sall cash flow

s that occurthat occurduring the life of the project,during the life of the project,

b) consider theb) consider the time value of moneytime value of money,,

c) incorporate thec) incorporate the required rate of required rate of returnreturn on the project on the project taking intotaking intoaccount riskaccount risk

Step 3: Evaluation techniquesStep 3: Evaluation techniques

8/6/2019 Credit Appraisal - Term Loans

http://slidepdf.com/reader/full/credit-appraisal-term-loans 45/92

Evaluation techniquesEvaluation techniques

Accounting rate of return (ARR) Accounting rate of return (ARR)

Payback period (PB)Payback period (PB)

Net Present Value ( NP V)Net Present Value ( NP V)

Profitability Index ( PI)Profitability Index ( PI)

Internal Rate of return ( IRR)Internal Rate of return ( IRR)(NPV, IRR and PI are called discounted(NPV, IRR and PI are called discounted

cash flow techniques)cash flow techniques)

8/6/2019 Credit Appraisal - Term Loans

http://slidepdf.com/reader/full/credit-appraisal-term-loans 46/92

Evaluation techniquesEvaluation techniques

ARR ARR:: Gives rate of return project is generatingGives rate of return project is generatingwith reference to accounting profits and not cashwith reference to accounting profits and not cashflowsflows it is an average return on investment (ROI)it is an average return on investment (ROI)

PaybackPayback It gives theIt gives the num ber of year snum ber of year s in whichin whichpro ject will br ea keven ie when the ca sh inf lo wspro ject will br ea keven ie when the ca sh inf lo wswill equa l the ca sh ou t f lo wswill equa l the ca sh ou t f lo ws

Net present valueNet present value Gives theGives the amoun t amoun t by whichby whichPV o f ca sh in flo ws exceeds ca sh ou tflo wsPV o f ca sh in flo ws exceeds ca sh ou tflo ws

Internal rate of returnInternal rate of return Gives theGives the ra tera te a t a t which PV of ca sh inflows = ca sh outflowswhich PV of ca sh inflows = ca sh outflows

Profitability indexProfitability index Gives theGives the ra tio ra tio o f ca sho f ca shinflo ws t o ca sh o utflo wsinflo ws t o ca sh o utflo ws

8/6/2019 Credit Appraisal - Term Loans

http://slidepdf.com/reader/full/credit-appraisal-term-loans 47/92

Accounting rate of return Accounting rate of return

ARR = ARR = Average income or Profit after tax Average income or Profit after tax

Average investment Average investment

Eg. By investing in a machine costingEg. By investing in a machine costingRs.90000 a company expects the followingRs.90000 a company expects the followingbenefits over the next 3 years: benefits over the next 3 years:

PAT = Rs.20000, 22000 & 24000PAT = Rs.20000, 22000 & 24000

Machine will be depreciated at Rs.10000Machine will be depreciated at Rs.10000per annum, calculate ARRper annum, calculate ARR

8/6/2019 Credit Appraisal - Term Loans

http://slidepdf.com/reader/full/credit-appraisal-term-loans 48/92

Accounting rate of return Accounting rate of return

ARR ARR = Ave. PAT / Ave. investment = Ave. PAT / Ave. investment

Average PAT = (20000+22000+24000) / 3 Average PAT = (20000+22000+24000) / 3

= 22000= 22000 Ave. investment =(90000+80000+70000)/ 3 Ave. investment =(90000+80000+70000)/ 3

= 80000= 80000

ARR ARR = 22000 / 80000 == 22000 / 80000 = 27.5%27.5%

8/6/2019 Credit Appraisal - Term Loans

http://slidepdf.com/reader/full/credit-appraisal-term-loans 49/92

Payback PeriodPayback Period

Time taken for the project to generateTime taken for the project to generateenough cash to pay for itself enough cash to pay for itself

0 1 2 3 4 5 86 7

(500) 150 150 150 150 (500) (300) 0 0

Payback period calculated by taking intoaccount cumulative cash flows until year

of full recovery of investment 3.33 years

8/6/2019 Credit Appraisal - Term Loans

http://slidepdf.com/reader/full/credit-appraisal-term-loans 50/92

Is aIs a 3.33 year3.33 year payback period acceptable?payback period acceptable?

Firms that use this method will compareFirms that use this method will compare

the payback calculation to some standardthe payback calculation to some standardset by the firm.set by the firm.

If management sets a cut If management sets a cut--off of off of 4 years4 yearsfor projects , what would be the decision?for projects , what would be the decision?

Accept the project Accept the project ..

Payback PeriodPayback Period

8/6/2019 Credit Appraisal - Term Loans

http://slidepdf.com/reader/full/credit-appraisal-term-loans 51/92

Drawbacks of Payback PeriodDrawbacks of Payback Period

Firm cutoffs areFirm cutoffs are subjectivesubjective..

Does not considerDoes not consider time value of moneytime value of money..

Does not consider anyDoes not consider any required rate of required rate of returnreturn..

Does not consider all of the projectsDoes not consider all of the projects

cash flow

scash flow

s. This project is clearly. This project is clearlyunprofitable, but we wouldunprofitable, but we would accept accept it it based on a 4based on a 4--year payback criterion!year payback criterion!

8/6/2019 Credit Appraisal - Term Loans

http://slidepdf.com/reader/full/credit-appraisal-term-loans 52/92

Discounted cash flowDiscounted cash flow-- DCF techniquesDCF techniques

NP V, IRR and PI :NP V, IRR and PI : Examines all net cash flowsExamines all net cash flows

Considers the time value of moneyConsiders the time value of money(discounting process)(discounting process)

Considers the required rate of returnConsiders the required rate of return(cost of capital is used as discount(cost of capital is used as discount

rate).rate).

8/6/2019 Credit Appraisal - Term Loans

http://slidepdf.com/reader/full/credit-appraisal-term-loans 53/92

Net Present Value

yNPV = PV of the annual net cashinflows (CF) - the initial outlay (IO)

NPV

NPV == -- IOIO

CFCFtt

(1 + k)(1 + k) tt

nn

t=1t=177

8/6/2019 Credit Appraisal - Term Loans

http://slidepdf.com/reader/full/credit-appraisal-term-loans 54/92

Net Present ValueNet Present Value

Decision RuleDecision Rule::

yy If NP V is positive, If NP V is positive, acceptaccept..

yy If NP V is negative, If NP V is negative, rejectreject..

8/6/2019 Credit Appraisal - Term Loans

http://slidepdf.com/reader/full/credit-appraisal-term-loans 55/92

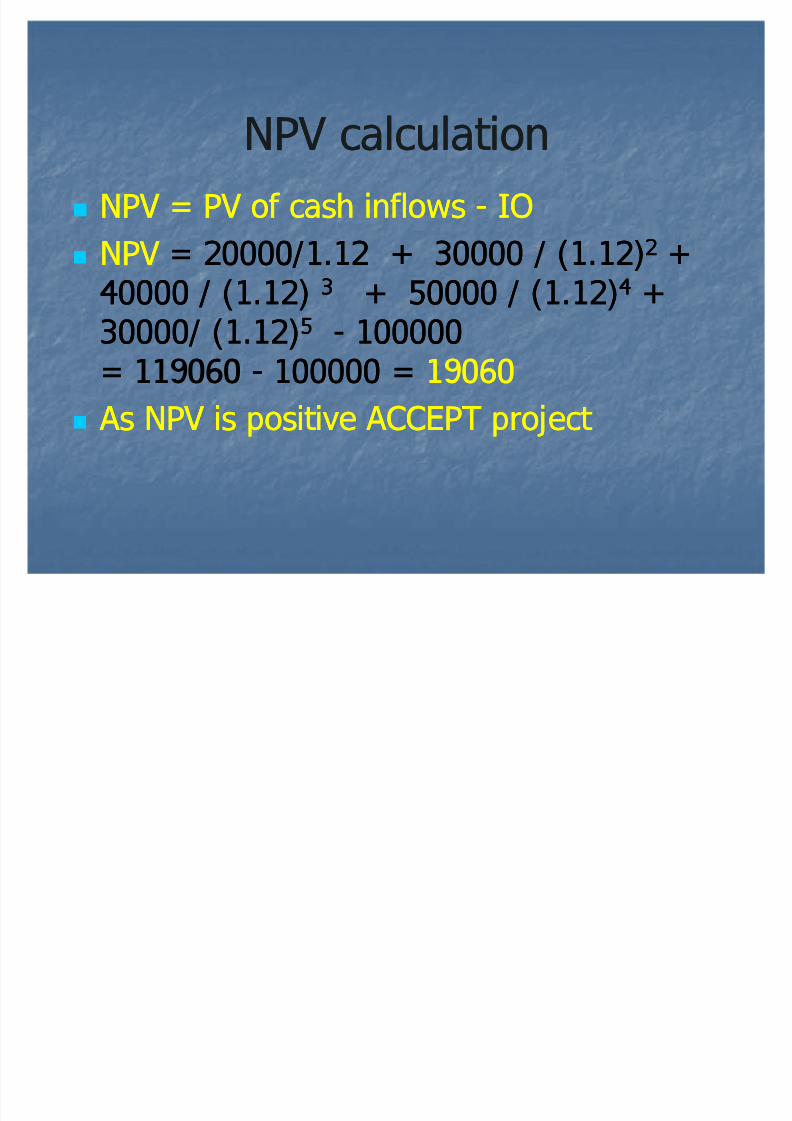

IllustrationIllustration Cash outflow at t Cash outflow at t oo = 1,00,000= 1,00,000

Cash inflows ( Years 1Cash inflows ( Years 1--5) = 20000, 300005) = 20000, 30000

, 40000,50000,30000, 40000,50000,30000

Cost of capital = 12%Cost of capital = 12%

8/6/2019 Credit Appraisal - Term Loans

http://slidepdf.com/reader/full/credit-appraisal-term-loans 56/92

8/6/2019 Credit Appraisal - Term Loans

http://slidepdf.com/reader/full/credit-appraisal-term-loans 57/92

Profitability Index

PI = IOCFt

(1 + k)

n

t=17 t

NPV = - IOCFt

(1 + k) t

n

t=1

7

8/6/2019 Credit Appraisal - Term Loans

http://slidepdf.com/reader/full/credit-appraisal-term-loans 58/92

yDecision Rule:

yIf PI is greater than or equal

to 1, accept.yIf PI is less than 1, reject.

yCalculate PI for illustration

yPI = 119060 /100000 =1.19

yAs PI > 1 , ACCEPT project

Profitability Index

8/6/2019 Credit Appraisal - Term Loans

http://slidepdf.com/reader/full/credit-appraisal-term-loans 59/92

Internal Rate of ReturnInternal Rate of Return(IRR)(IRR)

IRRIRR:: IRR is simply theIRR is simply the rate ofrate ofreturnreturn that the firm earns onthat the firm earns on

its capital budgeting projects.its capital budgeting projects. IRR is the rate of return thatIRR is the rate of return that

makes themakes the P V of the cashP V of the cash

inflowsinflows equalequal to theto the initialinitialoutlayoutlay ie where NP V = 0ie where NP V = 0

I l R f RI l R f R

8/6/2019 Credit Appraisal - Term Loans

http://slidepdf.com/reader/full/credit-appraisal-term-loans 60/92

Internal Rate of ReturnInternal Rate of Return(IRR)(IRR)

n

t=17

IRR: = IOCFt

(1 + IRR) t

8/6/2019 Credit Appraisal - Term Loans

http://slidepdf.com/reader/full/credit-appraisal-term-loans 61/92

IRRIRRyy Decision RuleDecision Rule::If IRR is greaterIf IRR is greater

than or equal to the required ratethan or equal to the required rateof return, of return, accept else rejectaccept else reject..

yy In the illustration, IRR works outIn the illustration, IRR works outto 18%to 18%

yy If required rate or cut off rate isIf required rate or cut off rate is

15% then ACCEPT project15% then ACCEPT project

8/6/2019 Credit Appraisal - Term Loans

http://slidepdf.com/reader/full/credit-appraisal-term-loans 62/92

Illustration 1Illustration 1

Find the payback periodFind the payback period

Using a discount rate ofUsing a discount rate of 15%,15%, findfindNP VNP V..

Also calculate PI and IRR. Also calculate PI and IRR.

0 1 2 3 4 5

(900) 300 400 400 500 600

Given following cash flows:Given following cash flows:

8/6/2019 Credit Appraisal - Term Loans

http://slidepdf.com/reader/full/credit-appraisal-term-loans 63/92

Illustration 1Illustration 1 PaybackPayback == 2 ½ yrs2 ½ yrs

NPVNPV = PV of cash inflow = PV of cash inflow IO IO

= [ 300/1.15 + 400/(1.15)= [ 300/1.15 + 400/(1.15)22 ++400/(1.15)400/(1.15)33 + 500 / (1.15)+ 500 / (1.15)44 ++600/(1.15)600/(1.15)55 900 =900 = 510510

PIPI = PV of cash inflow / IO = PV of cash inflow / IO

= 1410 / 900 == 1410 / 900 = 1.571.57

IRRIRR == 34%34%

8/6/2019 Credit Appraisal - Term Loans

http://slidepdf.com/reader/full/credit-appraisal-term-loans 64/92

The cost of a new machine is Rs.The cost of a new machine is Rs.1,77,0001,77,000.. Installation will costInstallation will cost Rs.20,000Rs.20,000..

Rs.4,000Rs.4,000 in net working capital will bein net working capital will be

needed at the time of installation.needed at the time of installation. The machine will increase revenues byThe machine will increase revenues by

Rs.Rs.85,00085,000 per year, but operating costsper year, but operating costswill increase bywill increase by 35%35% of the revenueof the revenueincrease.increase.

Straight line depreciation is used.Straight line depreciation is used.

Project life isProject life is 55 yearsyears

Illustration

8/6/2019 Credit Appraisal - Term Loans

http://slidepdf.com/reader/full/credit-appraisal-term-loans 65/92

8/6/2019 Credit Appraisal - Term Loans

http://slidepdf.com/reader/full/credit-appraisal-term-loans 66/92

St 1 E l t C h FlSt 1 E l t C h Fl

8/6/2019 Credit Appraisal - Term Loans

http://slidepdf.com/reader/full/credit-appraisal-term-loans 67/92

Step 1: Evaluate Cash FlowsStep 1: Evaluate Cash Flows

a)a) Initial OutlayInitial Outlay:: What is the cashWhat is the cashflow at time 0?flow at time 0?

177,000177,000P

urchase price of assetP

urchase price of asset++ 20,00020,000 shipping and installationshipping and installation

197,000197,000 depreciable asset valuedepreciable asset value

++ 4,0004,000 net working capitalnet working capital201,000201,000 initial outlayinitial outlay

8/6/2019 Credit Appraisal - Term Loans

http://slidepdf.com/reader/full/credit-appraisal-term-loans 68/92

8/6/2019 Credit Appraisal - Term Loans

http://slidepdf.com/reader/full/credit-appraisal-term-loans 69/92

Incremental revenueIncremental revenue

-- Incremental costs *Incremental costs *

-- DepreciationDepreciation

= = Incremental earnings before taxesIncremental earnings before taxes

-- TaxTax

= = Incremental earnings after taxesIncremental earnings after taxes

+ Depreciation+ Depreciation

= = OperatingOperating Cash FlowCash Flow

-- / + Increase/decrease in working / + Increase/decrease in workingcapitalcapital

= Annual cash flow (NCF)= Annual cash flow (NCF)

8/6/2019 Credit Appraisal - Term Loans

http://slidepdf.com/reader/full/credit-appraisal-term-loans 70/92

85,00085,000 RevenueRevenue

(29,750)(29,750) CostsCosts

(29,400)(29,400) Depreciation*Depreciation*

25,85025,850 EBTEBT

(8,789)(8,789) TaxesTaxes

17,06117,061 E ATE AT

29,40029,400 DepreciationDepreciation

46,46146,461 == Annual Cash Flow Annual Cash Flow

*Depn =(Asset value*Depn =(Asset value salvage)/ No. of yrssalvage)/ No. of yrs

For Years 1For Years 1 --55

8/6/2019 Credit Appraisal - Term Loans

http://slidepdf.com/reader/full/credit-appraisal-term-loans 71/92

Step 1: Evaluate Cash FlowsStep 1: Evaluate Cash Flows

c)c) Terminal Cash FlowTerminal Cash Flow:: What is theWhat is the

cash flow at the end of the projectscash flow at the end of the projectslife?life?

Salvage valueSalvage value++ Recapture of net working capitalRecapture of net working capital

= Terminal Cash Flow= Terminal Cash Flow

8/6/2019 Credit Appraisal - Term Loans

http://slidepdf.com/reader/full/credit-appraisal-term-loans 72/92

Step 1: Evaluate Cash FlowsStep 1: Evaluate Cash Flows

c)c) Terminal Cash FlowTerminal Cash Flow:: What is theWhat is thecash flow at the end of the projectscash flow at the end of the projectslife?life?

50,00050,000 Salvage valueSalvage value

4,0004,000 Recapture of NWCRecapture of NWC

54,00054,000 Terminal Cash FlowTerminal Cash Flow

8/6/2019 Credit Appraisal - Term Loans

http://slidepdf.com/reader/full/credit-appraisal-term-loans 73/92

Payback periodPayback period IO = 201,000IO = 201,000

CF(1CF(1 -- 4) =4) = 46,461*4 = 1,85,84446,461*4 = 1,85,844

Balance to be recovered = Balance to be recovered = 15,15615,156

Recovered in 15,156 / 46461 = Recovered in 15,156 / 46461 = .33 yrs.33 yrs

Payback period is 4.33 yrs.Payback period is 4.33 yrs.

8/6/2019 Credit Appraisal - Term Loans

http://slidepdf.com/reader/full/credit-appraisal-term-loans 74/92

Project NP V:Project NP V:

IO = IO = 201,000201,000

CF(1CF(1 -- 4) = 4) = 46,461 per annum46,461 per annum

CF(5) = 46,461 + 54,000 = CF(5) = 46,461 + 54,000 =

1,00,4611,00,461

Discount rate = Discount rate = 14%14%

Discount factors = 1/ (1 + k)Discount factors = 1/ (1 + k)tt

= 1/ 1.14 , 1/ (1.14)= 1/ 1.14 , 1/ (1.14)22 , 1/, 1/(1.14)(1.14)33 etcetc

NP V = 1,87,544NP V = 1,87,544 2,01,000 =(2,01,000 =(--))

13,45613,456

8/6/2019 Credit Appraisal - Term Loans

http://slidepdf.com/reader/full/credit-appraisal-term-loans 75/92

PI & IRRPI & IRR

PI =

187544 / 201000PI =

187544 / 201000= = . 93. 93 (REJECT)(REJECT)

IRR = IRR = 1111--12 %12 % (ACCEPT if IRR >(ACCEPT if IRR >

required rate )required rate )

8/6/2019 Credit Appraisal - Term Loans

http://slidepdf.com/reader/full/credit-appraisal-term-loans 76/92

8/6/2019 Credit Appraisal - Term Loans

http://slidepdf.com/reader/full/credit-appraisal-term-loans 77/92

DCF calculationDCF calculationYEARS 1 2 3 4 5

R evenue / Cost

savings

Less: Operating

expenses

Less: Depreciation

EBIT

Less: Tax

EBIAT

Add: depreciation

Operating cash

flows

8/6/2019 Credit Appraisal - Term Loans

http://slidepdf.com/reader/full/credit-appraisal-term-loans 78/92

DCF calculation (contd)DCF calculation (contd)YEARS 1 2 3 4 5

Operating cash flow

Less: CAPEX

Less: WorkingCapital changes

Add: terminal value

Annual Cash Flow

(ACF)

Present value @discount rate

NPV = PV ( ACF ) - IO

8/6/2019 Credit Appraisal - Term Loans

http://slidepdf.com/reader/full/credit-appraisal-term-loans 79/92

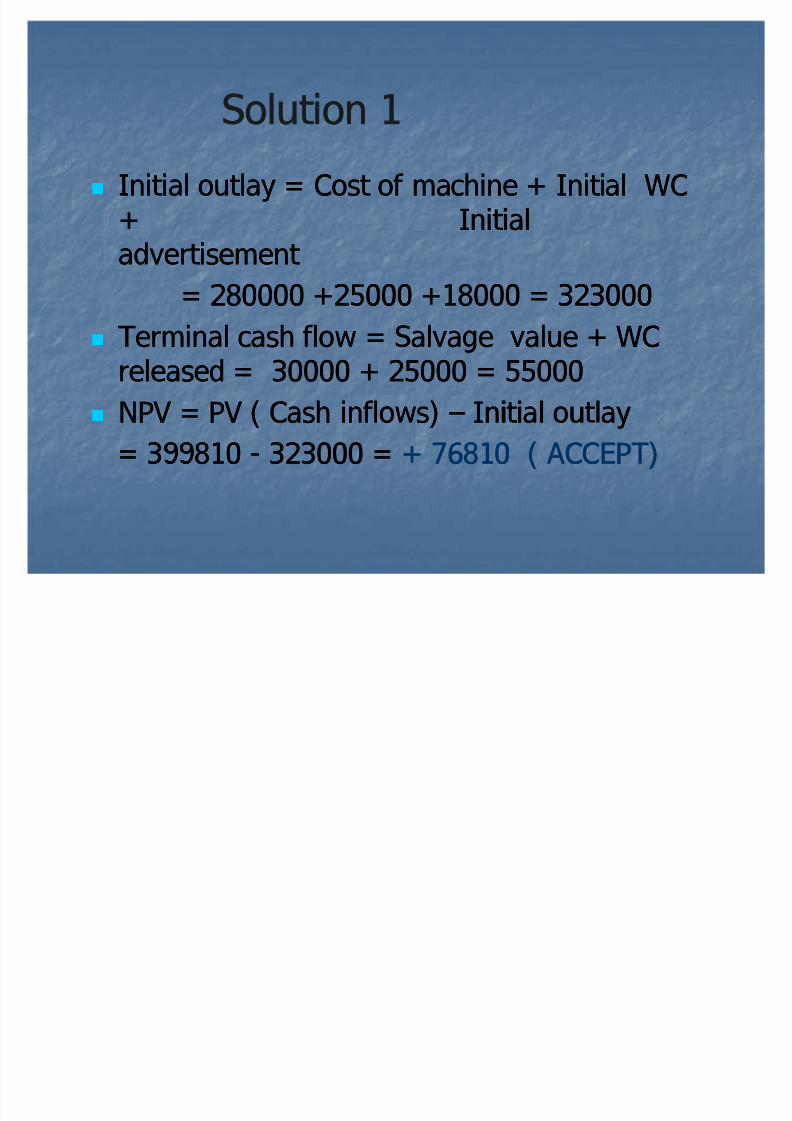

Problem 1 (New project)Problem 1 (New project) Bell ltd. is considering launching a new type of Bell ltd. is considering launching a new type of

electronic bellelectronic bell

Expected sales are 2000 units in year 1 withExpected sales are 2000 units in year 1 with

grow

th @10% each yeargrow

th @10% each year Selling price of Rs.250 eachSelling price of Rs.250 each

Project life = 4 yearsProject life = 4 years

Unit variable cost = Rs.120 per unit andUnit variable cost = Rs.120 per unit andincremental fixed costs = Rs.1,05,000 p.aincremental fixed costs = Rs.1,05,000 p.a

New equipment costs Rs.2,80,000 which canNew equipment costs Rs.2,80,000 which canbe sold after 4 years for Rs.30,000be sold after 4 years for Rs.30,000

8/6/2019 Credit Appraisal - Term Loans

http://slidepdf.com/reader/full/credit-appraisal-term-loans 80/92

8/6/2019 Credit Appraisal - Term Loans

http://slidepdf.com/reader/full/credit-appraisal-term-loans 81/92

Op.CF Year 1 Year 2 Year 3 Year 4

R evenues 500000 550000 605000 665500

Less:VC 240000 264000 290400 319440

Less:FC 105000 105000 105000 105000

Less:Depn 56000 44800 35840 28672

PBT 99000 136200 173760 212388

Less:Tax 39600 54480 69504 84955

PAT 59400 81720 104256 127433

OCF(PAT+De

pn.)

115400 126520 140096 156105

8/6/2019 Credit Appraisal - Term Loans

http://slidepdf.com/reader/full/credit-appraisal-term-loans 82/92

Op.CF Year 1 Year 2 Year 3 Year 4

OCF (c/f) 115400 126520 140096 156105

Less: Increase

in W.Cap*

- - - -

Add: TerminalValue

55000

ACF 115400 126520 140096 211105

PVIF .862 .743 .641 .552

PV 99475 94003 89802 116530

2Schange assumed

8/6/2019 Credit Appraisal - Term Loans

http://slidepdf.com/reader/full/credit-appraisal-term-loans 83/92

8/6/2019 Credit Appraisal - Term Loans

http://slidepdf.com/reader/full/credit-appraisal-term-loans 84/92

Cash flows in replacement decisionsCash flows in replacement decisions

Initial outlay = Cost of new asset Initial outlay = Cost of new asset salvage value of old asset if sold todaysalvage value of old asset if sold today

Annual cash flows = (Increased revenues Annual cash flows = (Increased revenuesor cost savings from replacement lessor cost savings from replacement lessincrementalincremental depreciation) (1depreciation) (1 t) +t) +incremental depreciationincremental depreciation

Terminal cash flows = Salvage value of Terminal cash flows = Salvage value of new asset at end of useful life less salvagenew asset at end of useful life less salvagevalue of old asset lost (opportunity cost)value of old asset lost (opportunity cost)

8/6/2019 Credit Appraisal - Term Loans

http://slidepdf.com/reader/full/credit-appraisal-term-loans 85/92

Problem 2 (Replacement)Problem 2 (Replacement)

Bell ltd. wants to buy a new machineBell ltd. wants to buy a new machine

Old machine is being depreciated at Rs.5000 p.aOld machine is being depreciated at Rs.5000 p.aand can be sold for Rs.15000 today ; if soldand can be sold for Rs.15000 today ; if sold

after 5 years then Rs.2000 salvageafter 5 years then Rs.2000 salvage New machine costs Rs.2,50,000 and will beNew machine costs Rs.2,50,000 and will be

depreciated on straight line basis over 5 years ,depreciated on straight line basis over 5 years ,salvage value after 5 yrs would be Rs.50,000salvage value after 5 yrs would be Rs.50,000

Cost savings would be Rs.50,000 p.aCost savings would be Rs.50,000 p.a

Tax rate = 40%, cost of capital = 15%Tax rate = 40%, cost of capital = 15%

What is the NPV?What is the NPV?

8/6/2019 Credit Appraisal - Term Loans

http://slidepdf.com/reader/full/credit-appraisal-term-loans 86/92

Solution 2Solution 2

IO = Cost of new machineIO = Cost of new machine salvage valuesalvage valueof old machine =250000of old machine =250000 15000 =15000 =2,35,0002,35,000

Terminal value = 50,000Terminal value = 50,000 2000 = 48,0002000 = 48,000 Benefits =Cost savingsBenefits =Cost savings IncrementalIncremental

depn. = 50000depn. = 50000 (40000(40000--5000) = 150005000) = 15000

ACF = 15000(1 ACF = 15000(1--.4) + 35000 (depn)=.4) + 35000 (depn)=4400044000

NPV = PV (CI)NPV = PV (CI) IO IO

=171344

=171344 235000

= 235000

= (63656)(63656) REJECTREJECT

8/6/2019 Credit Appraisal - Term Loans

http://slidepdf.com/reader/full/credit-appraisal-term-loans 87/92

Annual capital charge Annual capital charge Transforms a lumpsum of investment today intoTransforms a lumpsum of investment today into

anan equivalent equivalent stream of future cash flowsstream of future cash flows(annuity)(annuity)

Used in calculating capital recovery (EMI/EAI)Used in calculating capital recovery (EMI/EAI)and evaluating project proposalsand evaluating project proposals

Where projects are mutually exclusive, haveWhere projects are mutually exclusive, havedifferent cash flow patterns and unequal livesdifferent cash flow patterns and unequal lives

eg. choosing bet ween fork lift and conveyor belt eg. choosing bet ween fork lift and conveyor belt for transportation of materials/goodsfor transportation of materials/goods

8/6/2019 Credit Appraisal - Term Loans

http://slidepdf.com/reader/full/credit-appraisal-term-loans 88/92

Annual capital charge Annual capital charge

Step 1:Step 1: Determine the initial outlay (IO) andDetermine the initial outlay (IO) andpresent value of operating costs using cost of present value of operating costs using cost of

capital (k) as the discount ratecapital (k) as the discount rate Step 2:Step 2: Divide the present value obtained in step 1Divide the present value obtained in step 1

by present value annuity factor (PVAF) for n yrs at by present value annuity factor (PVAF) for n yrs at k rate k rate

Annual capital charge = Annual capital charge = IO + PV (Op. costs)IO + PV (Op. costs)PVAFPVAF (n yrs , k%)(n yrs , k%)

8/6/2019 Credit Appraisal - Term Loans

http://slidepdf.com/reader/full/credit-appraisal-term-loans 89/92

Annual capital charge (ACC) Annual capital charge (ACC)

Eg. Initial outlay= 400 crs, Cost of capital = 7%,Eg. Initial outlay= 400 crs, Cost of capital = 7%,n = 25 yrs; how much revenue is required to ben = 25 yrs; how much revenue is required to be

earned each year to recover investment or repayearned each year to recover investment or repayloan in equated annual instalments?loan in equated annual instalments?

Annual revenue or ACC = 400 / PVAF( Annual revenue or ACC = 400 / PVAF( 25 yrs, 7%)25 yrs, 7%)

= 400 / 11.65 = 34.3 crs= 400 / 11.65 = 34.3 crs

8/6/2019 Credit Appraisal - Term Loans

http://slidepdf.com/reader/full/credit-appraisal-term-loans 90/92

IllustrationIllustration

Machine A: Machine A:

Initial cost = Rs.15 lakhsInitial cost = Rs.15 lakhs

n = 3 yrsn = 3 yrs

Operating cost p.a = Rs.5 lakhsOperating cost p.a = Rs.5 lakhs Machine B:Machine B:

Initial cost = Rs.10 lakhsInitial cost = Rs.10 lakhs

n = 2 yrsn = 2 yrs

Operating cost p.a = Rs.6 lakhsOperating cost p.a = Rs.6 lakhs

Which m achine should be bought?Which m achine should be bought?

D iscount rate = 6%D iscount rate = 6%

8/6/2019 Credit Appraisal - Term Loans

http://slidepdf.com/reader/full/credit-appraisal-term-loans 91/92

Calculating PV of costsCalculating PV of costs

CC00 CC11 CC22 CC33 PV@6%PV@6%

A = A = 1515 55 55 55 28.3728.37

B =B = 1010 66 66 -- 21.0021.00

Should B be bought?Should B be bought?

Not necessarily as it would meanNot necessarily as it would mean

replacement a year earlier than Areplacement a year earlier than A

So calculate annual capital chargeSo calculate annual capital charge

8/6/2019 Credit Appraisal - Term Loans

http://slidepdf.com/reader/full/credit-appraisal-term-loans 92/92