Credit Appraisal by Fawad Yaqub

85

A Study On Credit Appraisal at J&K Bank A Project on CREDIT APPRAISAL at J&K Bank Submitted in partial fulfillment of the requirement for MBA Degree of Bangalore University By Fawad Yaqub Shah (09CQCMA030) Under the Guidance of Mr.Sarvanan Laxsmanan Asst. Professor 1

-

Upload

mohammad-hemayun -

Category

Documents

-

view

130 -

download

1

Transcript of Credit Appraisal by Fawad Yaqub

A Study On Credit Appraisal at J&K Bank

A Project on CREDIT APPRAISAL at J&K Bank

Submitted in partial fulfillment of the requirement for MBA

Degree of Bangalore University

By

Fawad Yaqub Shah

(09CQCMA030)

Under the Guidance of

Mr.Sarvanan Laxsmanan

Asst. Professor

DAYANANDA SAGAR COLLEGE OF MANAGEMENT

AND INFORMATION TECHNOLOGY

Shavige Malleshwara Hills, Kumaraswamy Layout, Bangalore – 560078.

2011

1

A Study On Credit Appraisal at J&K Bank

CERTIFICATE

This is to certify that the Project titled CREDIT APPRAISAL, submitted in partial

fulfillment of the requirements for the award of degree of Master of Business

Administration to Bangalore University, is a record of original work carried out by

Fawad Yaqub Shah(Reg.No. 09CQCMA030) under the guidance of Mr.Sarvanan

Laxmanan during the academic year 2009-2011.

This has not been submitted to any other university or institution for the award of any

degree/ diploma/ certificate.

Dr. MARUTHI RAM.R Dr. M.S.RAMACHANDRA

Head-MBA, DSCMIT Director - DSCMIT

Place: Bangalore

Date:

2

A Study On Credit Appraisal at J&K Bank

STUDENT DECLARATION

I hereby declare that the Project titled ‘CREDIT

APPRAISAL’, is an original work done by me, submitted in partial

fulfilment of the requirements for the award of degree of Master of

Business Administration to Bangalore University, under the guidance of

Mr. Sarvanan Laxmanan, This has not been submitted to any other

university or institution for the award of any degree/ diploma/ certificate.

Place: Bangalore Fawad Yaqub Shah

Date: (Reg.No.09CQCMA030)

3

A Study On Credit Appraisal at J&K Bank

GUIDE CERTIFICATE

This is to certify that the Project titled ‘CREDIT APPRAISAL, submitted

in partial fulfilment of the requirements for the award of degree of Master

of Business Administration to Bangalore University, is a record of original

work carried out by Fawad Yaqub Shah (Reg.No. 09CQCMA030) under

my supervision and guidance and that no part of this report has been

submitted for awards of any degree/ diploma/ certificate.

Place: Bangalore Mr. Sarvanan Laxmanan

Date: Asst. Professor

4

A Study On Credit Appraisal at J&K Bank

AC K N O W LE D G E M E N T

I am sincerely thankful to Dr.M.S.Ramachandra,Director Dayananda Sagar Institute of Management, Bangalore for granting me the permission to do the internship project.

I am extremely greatfull to Dr.Maruthi Ram.R, HOD for his constant support and encouragement throughout this project study.

I would also like to thank Mr.Sarvanan Laxmanan,Asst. Professor for his valuable role in making this project study a learning experience.

I would like to express my sincere thanks to Mr.Shakeel Rehman,J&K bank Ltd, who has spent valuable time in giving the necessary guidance throughout the projects works.

I would like to express my profound gratitude to all the staff of J&K Bank those who have helped me directly or indirectly in the course of this study.

Last but not the least I would like to express my profound gratitude to my family and friends who have indirectly encouraged me in completing this study.

BANGALORE Fawad Yaqub ShahDATE:

5

A Study On Credit Appraisal at J&K Bank

Table of Contents

TITLE Page No.

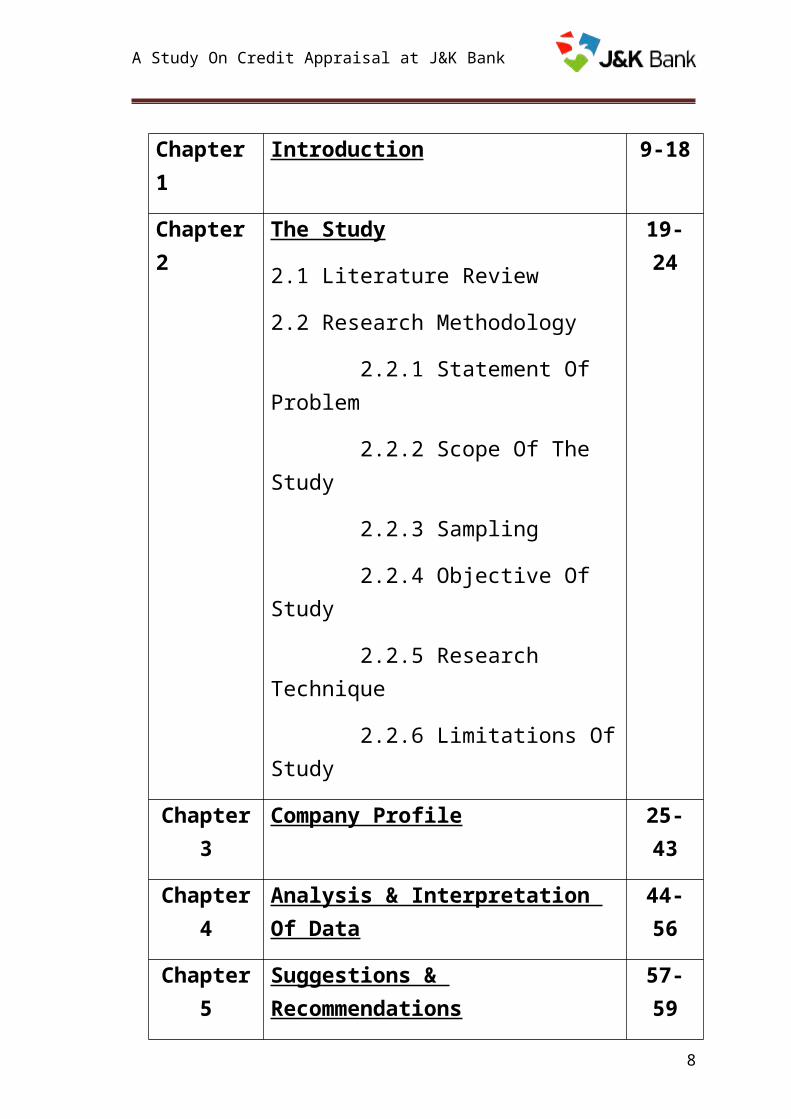

Chapter 1 Introduction 9-18

Chapter 2 The Study

2.1 Literature Review

2.2 Research Methodology

2.2.1 Statement Of Problem

2.2.2 Scope Of The Study

2.2.3 Sampling

2.2.4 Objective Of Study

2.2.5 Research Technique

2.2.6 Limitations Of Study

19-24

Chapter 3 Company Profile 25-43

Chapter 4 Analysis & Interpretation Of Data 44-56

Chapter 5 Suggestions & Recommendations 57-59

Chapter 6 Conclusion 5-61

Appendices

Bibliography 62

6

A Study On Credit Appraisal at J&K Bank

Graph No. Description

Graph 4.1 Credit-Deposit Ratio

Graph 4.2 Total Growth Of Advances

Graph 4.3 Analysis Of Net Sales

Graph 4.4 Analysis Of Capacity Utilization

Graph 4.5 Analysis Of Debt-Equity Ratio

Graph 4.6 Analysis Of Current Ratio

Graph 4.7 Analysis Of Net Profit

Graph 4.8 Analysis Of Interest Coverage Ratio

List of Graphs

7

A Study On Credit Appraisal at J&K Bank

List of Tables

Table No. Description

Table 3.1 Financial Position Of Bank

Table 4.1 Correlation Of Credit & Deposits

Table 4.2 Comparative Analysis of NPA

Table 4.3 Advances & Priority Advances

Table 4.4 Net Sales

Table 4.5 Capacity Utilization

Table 4.6 Debt-Equity Ratio

Table 4.7 Current Ratio

Table 4.8 Net Profit

Table 4.9 Interest Coverage ratio

Table 4.10 Weightage to different types of risks

8

A Study On Credit Appraisal at J&K Bank

Chapter 1INTRODUCTION

9

A Study On Credit Appraisal at J&K Bank

INDUSTRIAL PROFILE

DEFINITION:

The Indian Banking Companies Act, 1949 section 5(b), defines banking as “accepting

for the purpose of lending or investment of deposits from the public, repayable on

demand or otherwise and withdrawals by cheque, drafts, and orders or otherwise.”

ORIGIN:

Since the banking activities were started in different periods in different countries, there

is no unanimous view regarding the origin of the word bank. The word bank is derived

from the French word ‘Banco’ or ‘Bancus’, which means a Bench. In fact the early

Jews in Lombardly transacted their banking business sitting on benches. When the

business ailed, the benches were broken and hence the word bankrupt came in to vogue.

INTRODUCTION TO BANKING

Banks are backbone of our society. A bank must meet the financial needs of a customer,

by acting as a custodian of his assets, providing credit facilities and assisting him to

speedily put through financial transaction of one type or another. Banking, when you

come to think of it are people. It is not figures, files and ledgers. Bank services needs

considerable improvement on an emergent basis. The time has come for banks to look

inward to find out what is the nature and quality of the products they sell, what is the

product demanded by the customer.

It would be unrealistic today to believe that banks are mere financial institutions,

working for profit. Banks essentially are now social organizations, regarding financial

services to sub serving the socio-economic objectives of the society.

10

A Study On Credit Appraisal at J&K Bank

IN INDIA

India has a system of indigenous banking from very early times, though it was not

similar to banking of modern times. There is evidence to show that money lending

existed even during the Vedic period. With the advent of the English traders in the

seventeenth century and the establishment of trading centres by the East India Company

encouraged the establishment of what were known as the agency houses. The trading

firms which undertook banking operations for the benefit of their constituents. Some of

the houses established during the period were Alexander and Co., and Ferguson & Co.

There were also Presidency Banks, Joint stock banks and Exchange banks which took

up gradually one after the other.

IMPERIAL BANK

The Presidency Banks referred to above were amalgamated into the Imperial Bank of

India, which was brought into existence on 27th January 1921 by the Imperial Bank of

Indian Act 1920. This Act, however, gave the Bank no power to issue notes and this left

out without control over the currency of the country. But it was allowed to hold

Government balances and to manage public debt and clearing houses till the

establishment of Reserve Bank Of India in 1935 which apart from taking over all these

functions from the Imperial Bank of India, was given the privilege of acting as an agent

of the latter in places where it had no branches.

COMMERCIAL BANKS

Amongst the banking Institutions in the organized sector, the Commercial banks

initially were established as corporate bodies with share holdings by private individuals,

but subsequently there has been a drift towards central ownership and control. Today 27

banks constitute the strong public sectors in Indian Commercial Banking. Up to late

60’s Commercial Banks are mainly engaged in financing organized trade, Commerce &

Industry, since then they are actively participating in financing agriculture, small-scale

business and small borrowers also.

11

A Study On Credit Appraisal at J&K Bank

NATIONALIZATION OF COMMERCIAL BANKS

The major historical event in the history of banking in India after Independence is

undoubtedly the nationalization of the 14 major banks on 19th July 1969. In 1980 six

more private sector bank are nationalized extending the public domain further over the

banking sector. Nationalization was deemed as a major step in achieving the socialistic

pattern of society. The nationalized banks were to increase lending to areas of

importance to the Government and to use their resources for sub-serving the common

good a detailed scheme of objectives, regulations, management etc. were drawn up for

these banks.

Nationalization was recognition of the potential of the banking system to promote

broader economic objectives. The banks had to reach out and expand their networks so

that the concept of mass banking was given importance over class banking.

THE RESERVE BANK OF INDIA [RBI]

The Central Bank of India called the Reserve Bank of India was constituted under the

Reserve Bank of India Act, 1934 to regulate the issue of bank notes and keeping of

reserves with a view to securing monetary stability in India and generally to operate the

currency and credit system of India to its advantage.

Amongst its multifarious functions affecting the Indian Financial System, the RBI

regulates and prohibits the issue of prospectus or advertisement soliciting deposits of

money, regulates the functioning of non-banking institutions and transacts Government

business. Its regulatory involvement in the Indian Capital Markets is primarily of debt

management through primary dealers, foreign exchange control and liquidity support to

market participants. The RBI regulates participants in the securities markets when a

foreign transaction is involved. Transactions that include Indian issuers issuing of

security outside India, such as GDRs and ADRs, and Financial Institutional Investors

(FIIs) or Foreign Brokers selling, buying or dealing in Indian Securities need the

permission of RBI.

12

A Study On Credit Appraisal at J&K Bank

As the central banking authority of India, the Reserve Bank of India performs the

following traditional functions of the central bank:

It provides currency and operates the clearing system for the banks.

It formulates and implements monetary and credit policies.

It functions as the banker’s bank.

It supervises the operations of credit institutions.

It regulates foreign exchange transactions.

It moderates the fluctuations in the exchange value of the rupee.

In addition to the traditional function of the central banking authority, the Reserve Bank

of India performs several functions aimed at developing the Indian financial system:

It seeks to integrate the unorganized financial sector with the organized financial

sector.

It encourages the extension of the commercial banking system in the rural areas.

It influences the allocation of credit.

It promotes the development of new institutions.

ROLE OF BANKS IN ECONOMIC DEVELOPMENT

Commercial banks are playing a crucial role in the economic development of the

country. In fact, without the development of commercial banks in 18th centuries,

industrial revolution would not have taken place in England at all. It is also true that

economic development of country depends entirely on the development of sound

commercial banking.

Banks provide short term loans which serves as capital for industrial establishment.

Without capital it is impossible to start an industry, after starting the industry, the banks

13

A Study On Credit Appraisal at J&K Bank

provide the industrialists necessary working capital. Thus by providing with investment

capital and short-term working capital, the banks encourage industrial advancement in

the country.

BANKING SCENARIO

During the year 2005-2006, the Reserve Bank of India took several initiatives aimed at

improving the prudential regulation. These include stipulating higher provisioning

requirement for NPA’s include under ‘doubtful for more than three years’ category

effective from March 31, 2006, prohibiting banks from investing in unrelated non-SLR

securities, advising banks to maintain capital charge for market risk, etc. Further,

several initiatives were also taken during the year aimed at improving the credit

delivery to the agricultural and SSI sector. The Government announced a

comprehensive policy, envisaging a 30% increase in agriculture credit in 2005-06 and

doubling the credit flow to the agriculture sector in three years.

INTRODUCTION TO FINANCE

The word ‘FINANCE’ is derived from Latin word “finis”. Finance may be defined as

the provision of money at the time it is wanted. Finance is the backbone of all economic

activity. The dimensions of business finance have undergone phenomenal

transformation during the last few decades. Until the recent past finance was considered

with procurement of funds for economic purpose and application of that funds for

various requirements.

The term ‘FINANCE’ is the application of skills (or) care to the manipulation,

the use and control of money.Different scholars have interpreted the term finance in real

world differently:

According to them finance has been categorized into three following major

groups:

14

A Study On Credit Appraisal at J&K Bank

a) The first category incorporates the views of all those who opine

that finance concerns with acquiring funds on reasonable terms and condition to

pay bills promptly.

b) The second approach holds that finance is concerned with cash. Since all business

transaction are expressed ultimately in terms of cash: every activity with in the firm

is the concern of a finance of a finance manager.

c) The third approach to finance looks on finance being concerned with procurement of

funds and their wise application. Protagonists of this approach

holds that the responsibility of a finance manager is not only limited to acquisition of

adequate cash to meet business requirement but extends beyond it to optimal utilization

of funds.

A financial system, which is inherently strong, functionally diverse and displays

efficiency and flexibility, is critical to our national objectives of creating a market-

driven, productive and competitive economy. The financial system in India comprises

of financial institutions, financial markets, financial instruments and services. The

Indian financial system is characterized by its two major segments - an organized sector

and a traditional sector that is also known as informal credit market. Financial

intermediation in the organized sector is conducted by a large number of financial

institutions which business organizations are providing financial services to the

community. Financial institutions whose activities may be either specialized or may

overlap are further classified as banking and non-banking entities. The Reserve Bank of

India (RBI) as the main regulator of credit is the apex institution in the financial system.

Other important financial institutions are the commercial banks (in the public and

private sector), cooperative banks, regional rural banks and development banks. Non-

bank financial institutions include finance and leasing companies and other institutions

like LIC, GIC, UTI, Mutual funds, Provident Funds, Post Office Banks etc.

15

A Study On Credit Appraisal at J&K Bank

BUSINESS FINANCE

The term business finance is composed of two words business and finance. Thus it

is essential to understand the meaning of these two words, which is the starting

point to develop the whole concept of finance. The study of principles, practices,

procedures and problems concerning financial management of profit making

organization engaged in the fields of industry, trade and commerce is undertaken under

the discipline of “BUSINESS FINANCE”.

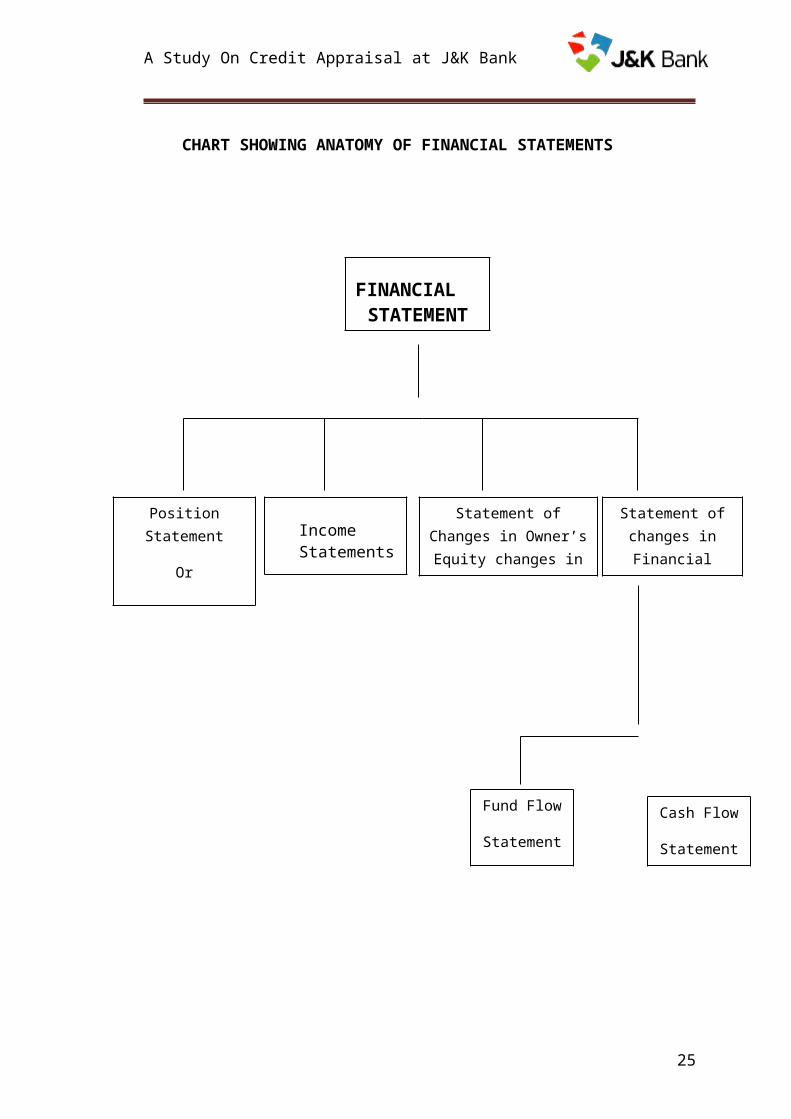

FINANCIAL STATEMENTS

An organization communicates its financial information to the users through financial

statements and reports. Financial statements contain summarized information of the

organization’s financial affairs, organized systematically. These statements comprise

the income statements or profit and loss account and the position statement or the

balance sheet.

To give a full view of the financial affairs of the undertaking it is also necessary to

include a statement of retained earnings, a statement of changes in the financial position

and a few schedules such as schedule of fixed assets and schedule of debtors.

Income Statement – the profit and loss account sets out income as well as

expenses of the same period and after matching the two, the difference being the net

profit or net loss, is shown as the difference between the two sides of the account. Thus,

the earning capacity and the potential of an organization are reflected by its profit and

loss account.

Position Statement – otherwise known as the balance sheet displays the total

resources of a business and the owners and creditor’s equity in these resources. It

16

A Study On Credit Appraisal at J&K Bank

indicates a statement of affair of a business at a particular moment of time and thus it is

static in nature.

Statement of Retained Earning – also known, as the profit and loss

appropriation account, is generally a part of the profit and loss account. It shows how

the profit of the business for the accounting period is appropriated towards reserve and

dividend and how much of the same is carried forwarded as retained earnings.

Statement of Changes in Financial Position – also known as the fund flow

statement, summarizes the changes in assets, liabilities and the owner’s equity between

two balance sheet dates. Thus, it is a statement of flows, i.e., it measures the changes

that have been taken place in the financial position of a firm between two balance sheet

dates. It summarizes the sources and uses of the funds obtained.

17

FINANCIALSTATEMENT

A Study On Credit Appraisal at J&K Bank

CHART SHOWING ANATOMY OF FINANCIAL STATEMENTS

Statement of changes in

Financial Position

Statement of Changes in Owner’s Equity changes in

Retained Earnings

Income Statements

Position Statement

Or

Balance Sheet

Fund Flow

Statement

Cash Flow

Statement

18

A Study On Credit Appraisal at J&K Bank

FINANCIAL ANALYSIS

Financial analysis is the process of identifying the financial strengths and weakness

of the firm by properly establishing relationships between the items of the balance

sheet and profit and loss account. The purpose of financial analysis is to disclose the

information contained in the financial statements so as to judge the profitability and

financial soundness of the organization.

The first task of the financial analyst is to select the information relevant to the

decision under consideration from the total information contained in the financial

statement.

Secondly, to arrange the information in a way to highlight the significant

relationships.

Finally, to interpret and draw inferences and conclusions. In brief, financial

analysis is the process of selection, relation and evaluation

19

Chapter 2THE STUDY

2.1 Literature Review

Quite often credit risk management (CRM) is confused with managing non- performing assets

(NPAs). However there is an appreciable difference between the two. NPAs are a result of

past action whose effects are realized in the present i.e. they represent credit risk that has

already materialized and default has already taken place.

On the other hand managing credit risk is a much more forward-looking approach and is

mainly concerned with managing the quality of credit portfolio before default takes place. In

other words, an attempt is made to avoid possible default by properly managing credit risk.

Considering the current global recession and unreliable information in financial statements,

there is high credit risk in the banking and lending business.

To create a defense against such uncertainty, bankers are expected to develop an

effective internal credit risk models for the purpose of credit risk management.

Credit risk is most simply defined as the potential that a bank borrower or counterparty will

fail to meet its obligations in accordance with agreed terms. The goal of credit risk

management is to maximize a bank’s risk-adjusted rate of return by maintaining credit risk

exposure within acceptable parameters. Banks need to manage the credit risk inherent in

the entire portfolio as well as the risk in individual credits or transactions. Banks

should also consider the relationships between credit risk and other risks. The effective

management of credit risk is a critical component of a comprehensive approach to risk

management and essential to the long-term success of any banking organization.

For most banks, loans are the largest and most obvious source of credit risk; however, other

sources of credit risk exist throughout the activities of a bank, including in the banking

book and in the trading book. Banks are increasingly facing credit risk (or counterparty risk) in

various advances.

Banks should now have a keen awareness of the need to identify, measure, monitor and

control credit risk as well as to determine that they hold adequate capital against

these risks and that they are adequately compensated for risks incurred.

The sound practices set out in this document specifically address the following areas:

Establishing an appropriate credit risk environment.

Operating under a sound credit granting process.

Maintaining an appropriate credit administration, measurement and monitoring

process.

Ensuring adequate controls over credit risk.

Although specific credit risk management practices may differ among banks depending upon

the nature and complexity of their credit activities, a comprehensive credit risk

management program will address these four areas.

These practices should also be applied in conjunction with sound practices related to the

assessment of asset quality, the adequacy of provisions and reserves,

A further particular instance of credit risk relates to the process of settling financial

transactions. If one side of a transaction is settled but the other fails, a loss may be

incurred that is equal to the principal amount of the transaction. Even if one party is simply late

in settling, then the other party may incur a loss relating to missed investment opportunities.

Settlement risk (i.e. the risk that the completion or settlement of a financial transaction will fail

to take place as expected) thus includes elements of liquidity, market, operational and reputation

risk as well as credit risk. The level of risk is determined by the particular arrangements for

settlement. Factors in such arrangements that have a bearing on credit risk.

2.2 Research Methodology

2.2.1 STATEMENT OF PROBLEM

To study credit management process and to manage the credit risks of the bank in order to

reduce the growing default risk problem and to develop the rating model. Hence this project is

an attempt to consider the factors while lending loan, and rating those parameters to manage

the credit risk.

2.2.2 Scope of the Study

Credit risk management is very important in every bank in order to manage the default

risk. The bank should develop an appropriate rating system.

The scope of the study is limited to the credit policy of J&K bank, while lending to customers.

2.2.3 Sampling

The sample technique used in this project is of the convent sampling where the sample are

selected as per the convince, for which the entire financial data was available to analyses all

the financial statement.

In the analysis statistical tools like simple percentages and ratios are extensively

used.

Data Collection Technique:

Primary data: Interview with employees of J&K bank in particular to the credit

management department.

Secondary data: The banks previous records for lending loans to customers.

2.2.4 OBJECTIVE OF STUDY

To study the credit risk associated while lending loans.

To study the bank credit policy while lending to customers.

To study the causes for increase in the NPA.

To study the parameters considered while lending the loans.

To study the objectives of Credit Management.

To study the manner in which funds are raised by the bank.

2.2.5 Research Technique

The research method adopted is analytical research .The study required analysis of

financial statements, ratio analysis, debt coverage ratio interest coverage ratio, and

turnover of the company, efficiency & capacity utilization of the company.

Purpose of the Study

The main purpose of this work is:

To study the parameters required while granting the loan to customers which will

help to minimize the NPA problem of the bank, and to find out as well as suggest the

remedial measures.

To understand the factors which influence in the rise of credit risk.

To understand the importance of credit risk management with the practical orientation.

The bank can consider these suggestions to decrease the default risk problem. Thereby

developing a rating system.

Tools of the Study

The tools used conducting research study is through analysis of financial statements and personal

interviews. The interview is framed with both open ended and close-ended questions.

2.2.6 Limitations of Study

The research project is aimed at analyzing the credit risk, and analysis financial

statement of small scale industry’s and develops a credit rating system at J&K Bank.

There are several shortcomings, which are listed below:

1) The study is confined to J&K Bank and therefore the results and conclusions of

study may not be applicable to other banks.

2) The study size is confined to 10 financial reports due to time constraint so an

extensive research could not be undertaken.

3) Analysis is done on the assumptions that financial data obtained is accurate.

4) The study is limited to information provided by the bank.

5) In depth study was not done.

Chapter 3

COMPANY PROFILE

INCEPTION OF THE BANK

Entire banking is the state of Jammu and Kashmir was performed by traditional lenders till 1920-

30 and that too at exorbitant interest rates. At the same time some banks function at a very

limited scale, such as Punjab National Bank Limited, Grind lay’s Bank and Imperial Bank of

India

The role of these banks was reduced to the acceptance of deposits, as they could not grant loans

and advantage to the people of the state owing to the statutory limitations. Under this scenario

banks could not ameliorate the financial and social position of the people of the state. To

overcome this critical situation the then Maharaja of the state conceived an idea of setting up of

a state bank in the state. After a prolonged exercise and deliberations the assignment for

establishing of “The Jammu and Kashmir Bank Limited” was given to the late Sir Sorabji N

Pochkhanwala, the then Managing Director of the Central Bank of India.

Mr. Pochkhanwala formulated a scheme on 24-09-1930, suggesting establishment of a semi state

bank with participation in capital by state and the public under the control of state Government.

Thus the bank was formally incorporated on the Ist of October 1938 and commenced business

from 4th of July 1939 at its registered office Residency Road Srinagar, Kashmir. The Jammu &

Kashmir Bank is today one of the fastest growing banks in India with a network of more than

500 branches/offices spread across the country offering world class banking products/services to

its customers.

The J &K Bank Ltd. Incorporated on October Ist, 1938 commenced business on July 4 th, 1939.

From a small beginning the bank has grown to become a giant with a network of 440 branches

spread over the length and breadth of the country. A significant contribution factor for this fast

growth is the solid founding principles which are dedicated to the cause of transforming the bank

not only as a financial but also the social heart of the community.

The J & K Bank is the first state owned bank of the country and 53% of equity is held by the

Govt. of J&K. The bank has a consistent and track record of growth and profitability. It has a

unique distinction of being banker to the J & K State Govt. and has also been appointed by RBI

as its agency in J & K, responsible for carrying general banking business of the central Govt. and

collection of Taxes pertaining to the central board of direct taxes.

The landmark achievements in the diversification of the banks including the sponsoring of two

regional rural banks via, Kamraz Rural Bank and Jammu Rural bank ; permission for dealing in

foreign exchange, holdings the lead bank responsibilities in eight of the fourteen districts in J &

K governorship of state level bankers committee (SLBC) and state level export promotion

committee (SLEPC).

The bank is the only one non –nationalized sector, having been entrusted with such assignments

and has come up to the exception of RBI and other agencies, like CBDT.

The bank has been swift in responding to the need for technology adaptation in meeting its

commitment to the customers and offers the best of service and a wide range of products. The

bank is investing in a big way in information technology, installation of ATM at Residency road,

Srinagar and Gandhi Nagar Trikuta Nagar Jammu Ahmadabad and Mera Road Mumbai and at

other important centers, introduction of EFT and E- Mail service substantiate this fact. The tele –

banking facilities are available at 23 branches with such services being extended to 65 branches

in the near future. The anywhere banking facility available at 23 shall be raised to 65 soon. The

bank is in the process of connecting its branches through VSAT and lease lines from the existing

23 to 85. The number of ATM’S, most convenient system of extending 24 hour banking facility,

is 23. ATM at six location including B/O Ansal plaza, Delhi, Corporate headquarters, Srinagar,

B/O Trikuta Nagar, Jammu, B/O Government Medical College, Srinagar, B/O SSI Lal Chowk,

Srinagar, Kashmir, B/O SKIMS, Srinagar and B/O Ahamadabad, are having IST Switch

connectivity.J&K bank is the first to introduce the Internet banking in J & K State. A new

concept of customer’s facility touch screen kiosks shall be installed at 65 branches of the bank. J

& K bank is one of the few banks in the country which has been able to show exemplary

performance in adjusting to the prudential norms that came into force during 1992-93 and has

been able to reach capital adequacy ratio of above 17.44 per cent, this is far ahead of RBI

stipulation and is alone of the highest in the industry today.

The banking industry of the country has been reeling under the pressure of increasing

intermediation and declining profits for the past a few years. The margins have been shrinking

due to high level of competition and rising NPA’S.In view of the financial reforms, bans are

confronted with tighter capital adequacy and prudential norms, transparency and disclosures

practices, asset – liability management, risk management and monitoring. With relatively lower

inflation, interest rates continued to soften during the year.

PRODUCTS AND SERVICES

Loan facility given by the bank

The different types of loans provided by the bank to its customers as per their requirements are:

Car loan

a) Scale of finance Ranging from Rs 1.00 lacs to Rs.5.00 lacs

depending upon the net annual income / salary

Eligibility i) Employees of Govt. / Semi Govt., Civic

Bodies, PSU’s/ individual /Proprietorship

concerns /firms / limited companies known to

the bank.

ii) Net annual income should exceed Rs.

75000/=

iii) The applicant (individuals ) should have a

valid driving license in his /her own name.

iv) The employees of the state Govt. /Semi

Govt., Departments / Other Organisation

should have a minimum of 5 years active

service in the organization / department.

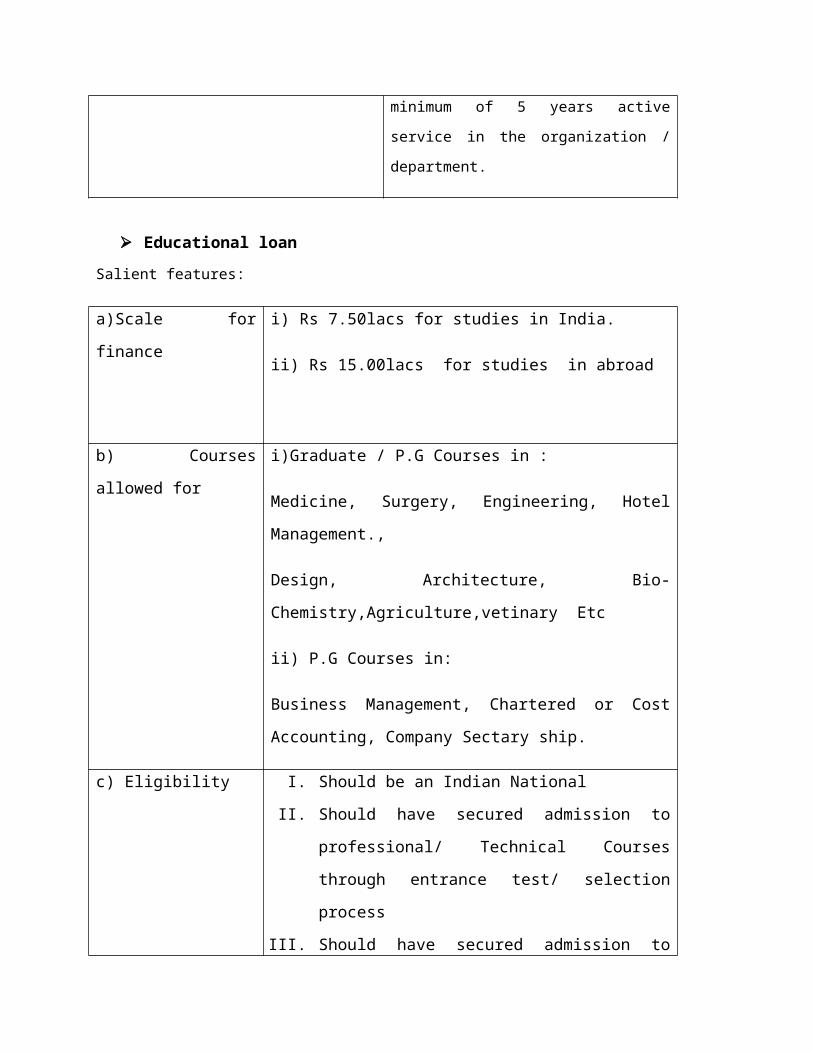

Educational loan

Salient features:

a)Scale for finance i) Rs 7.50lacs for studies in India.

ii) Rs 15.00lacs for studies in abroad

b) Courses allowed for i)Graduate / P.G Courses in :

Medicine, Surgery, Engineering, Hotel Management.,

Design, Architecture, Bio-Chemistry,Agriculture,vetinary Etc

ii) P.G Courses in:

Business Management, Chartered or Cost Accounting,

Company Sectary ship.

c) Eligibility I. Should be an Indian National

II. Should have secured admission to professional/

Technical Courses through entrance test/ selection

process

III. Should have secured admission to foreign universities/

institutions.

IV. Should have passed the qualifying examination for

admission to the courses.

V. Employed person intending to improve their

educational qualification and/ or receive training in

modern technology in India or abroad can also be

assisted under this scheme provided training offers

prospects of better placement.

Housing loans

Salient features:

i)For Construction

/purchases

The maximum amount of loan to be sanctioned under the

scheme would be 40 times the net monthly income / salary

of the applicant and there would be no ceiling vis-à-vis,

the amount of loan.

ii) For Renovation / The maximum loan granted for carrying out repairs,

GROUP HEADS FOR RESPECTIVE DIVISIONS

Addition additions, extension, improvement, completion,

renovation of existing house is Rs 4lacs (subject to 20

times net monthly salary/income.)

Also as an incentive for small borrowers, the loans up to

Rs 1.5lacs granted for repairs / renovation of existing

house would now be secured by third party of 2 persons or

LIC policies, Government securities, VIPs, NSCs, KVPs,

or such other security as is deemed appropriate by the

sanctioning authority.

However, negative lien would be stipulated over the

existing house property for which the facility is granted

and also have an ire-revocable power of attorney executed

by the borrower authorized the bank so sell the house in

case of default.

b)Eligibility i)Employees of Govt., Semi- Govt. Dept, Civic bodies,

PSU’ with min. 5 years service

ii) Reputed Business with min. 5 years standing.

iii) Professional and self employed like Doctors,

Engineers, CA’s, Advocate, with min. 5 years standing.

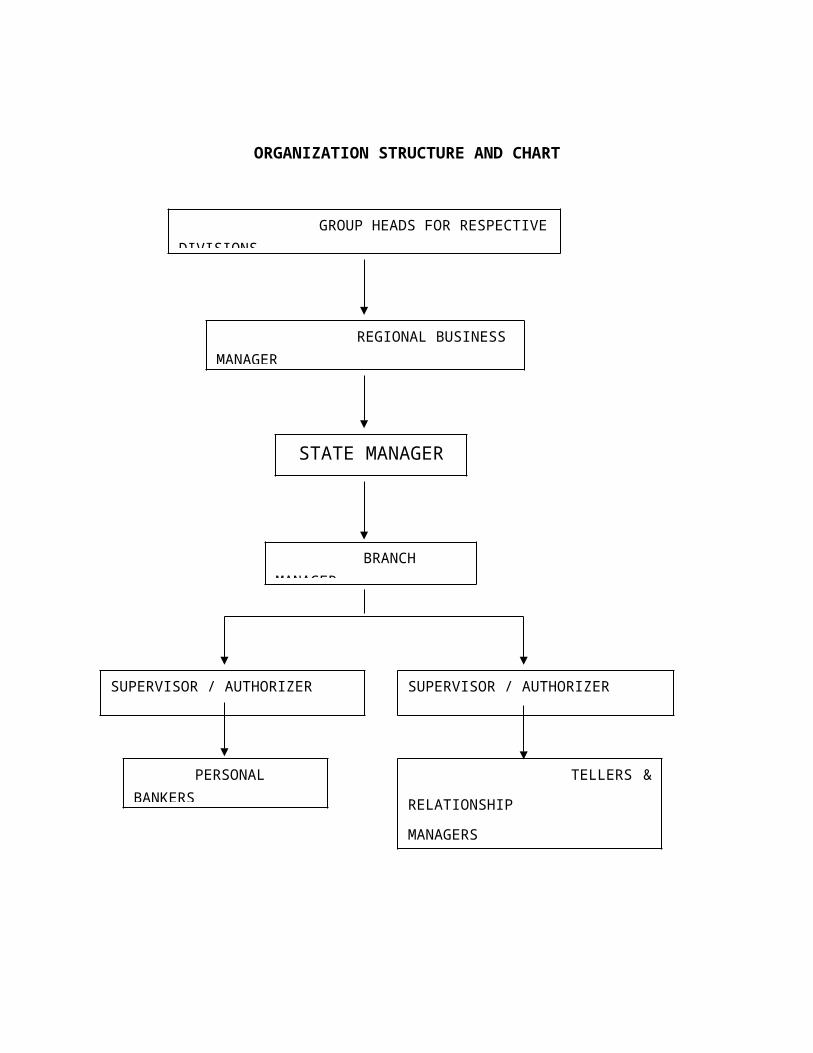

ORGANIZATION STRUCTURE AND CHART

REGIONAL BUSINESS MANAGER

BRANCH MANAGER

SUPERVISOR / AUTHORIZERSUPERVISOR / AUTHORIZER

PERSONAL BANKERS TELLERS & RELATIONSHIP

MANAGERS

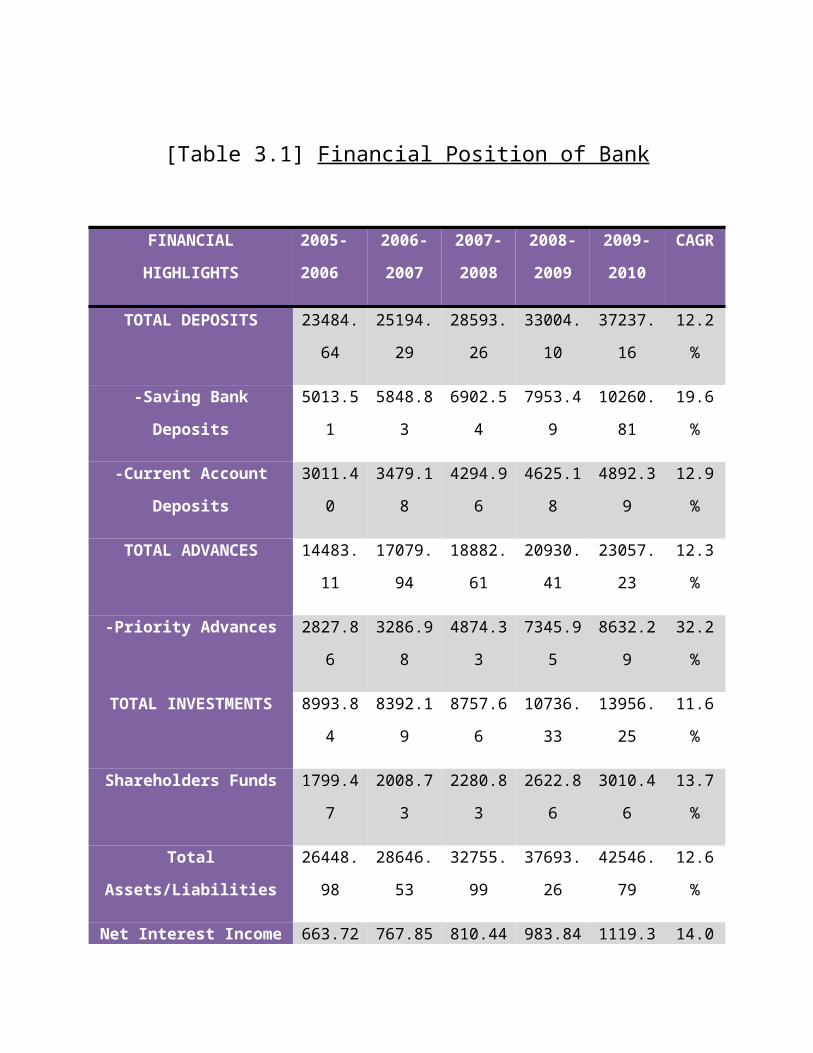

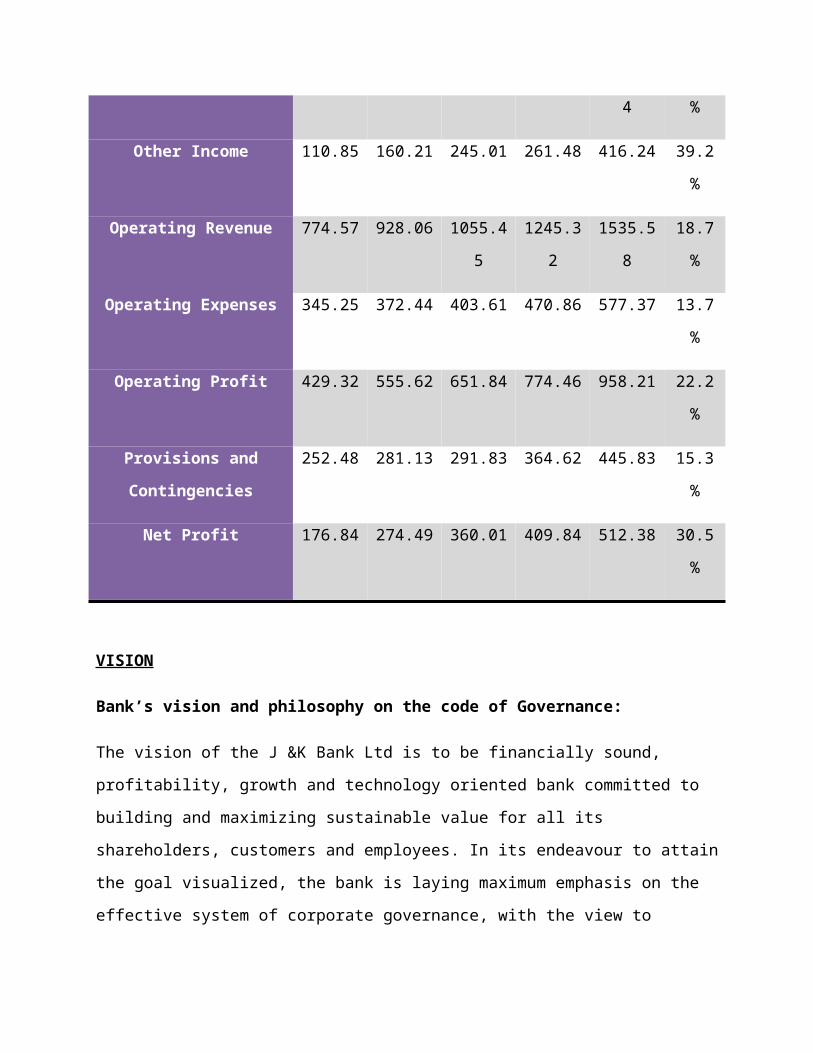

[Table 3.1] Financial Position of Bank

FINANCIAL

HIGHLIGHTS

2005-

2006

2006-

2007

2007-

2008

2008-

2009

2009-

2010

CAGR

TOTAL DEPOSITS 23484.64 25194.29 28593.26 33004.10 37237.16 12.2%

-Saving Bank Deposits 5013.51 5848.83 6902.54 7953.49 10260.81 19.6%

-Current Account Deposits 3011.40 3479.18 4294.96 4625.18 4892.39 12.9%

STATE MANAGER

TOTAL ADVANCES 14483.11 17079.94 18882.61 20930.41 23057.23 12.3%

-Priority Advances 2827.86 3286.98 4874.33 7345.95 8632.29 32.2%

TOTAL INVESTMENTS 8993.84 8392.19 8757.66 10736.33 13956.25 11.6%

Shareholders Funds 1799.47 2008.73 2280.83 2622.86 3010.46 13.7%

Total Assets/Liabilities 26448.98 28646.53 32755.99 37693.26 42546.79 12.6%

Net Interest Income 663.72 767.85 810.44 983.84 1119.34 14.0%

Other Income 110.85 160.21 245.01 261.48 416.24 39.2%

Operating Revenue 774.57 928.06 1055.45 1245.32 1535.58 18.7%

Operating Expenses 345.25 372.44 403.61 470.86 577.37 13.7%

Operating Profit 429.32 555.62 651.84 774.46 958.21 22.2%

Provisions and

Contingencies

252.48 281.13 291.83 364.62 445.83 15.3%

Net Profit 176.84 274.49 360.01 409.84 512.38 30.5%

VISION

Bank’s vision and philosophy on the code of Governance:

The vision of the J &K Bank Ltd is to be financially sound, profitability, growth and technology

oriented bank committed to building and maximizing sustainable value for all its shareholders,

customers and employees. In its endeavour to attain the goal visualized, the bank is laying

maximum emphasis on the effective system of corporate governance, with the view to improve

the company’s image, efficiency, effectiveness, and satisfying the public expectations of fairness

and ethical conduct. The interaction between the board, the executives and other functionaries is

so configured as to have a distinctly remarkable expectations role and improved corporate

performance. The bank’s corporate governance philosophy is woven around its total commitment

to the ethical practices in the conduct of its business. While striving in the constant quest to grow

with profits and enhance shareholders value and align the interest of the shareholders,

stakeholders, and society through adaptation of best international practices and standards. The

corporate governance policies of your bank recognizes the accountability of board vis–a–vis it’s

various constituents including customers, shareholders investors, employees, government and

other regulatory authorities.

Functions of the Board:

In addition to the primary responsibility of managing the affairs of your bank, the board of

directors performs various other functions for the efficient and the effective utilization of the

resources at their disposal to achieve the goals visualized. The fractions performed by the board

of bank include.

1. Setting corporate mission

Missions have been set to remain a financially strong, sound, growth oriented and profitable

bank with main focus towards providing the convenient, reliable, cost-effective and personalized

services to the customers and remain globally competitive and foray into the new sectors

compatible with the business of banking. The key objective of the bank shall be provide “value

maximization” to the shareholders i.e. shareholders customers and employees. The bank shall

also further strive to strengthen its national presence and adopt a developmentary role in the

country with the particular emphasis on J&K state.

3. Formulation of strength and other business plans

The board of directors of your bank meet frequently to take strategic postures vis-à-vis

competitions and to lay down various business plans for the achievement of the missions laid and

goals set. Your bank has engaged the services of leading management consultants – price

Waterhouse coopers for the formulation of business plan of the bank, recruiting the organization

including succession planning and HR plan and also designing an asset liability management

framework consistent with bank’s risk appetite.

On the basis of recommendations made by the said consultancy agency, bank has already

formulated the business plan for the five years christened as “Vision 2008”.

FUNCTIONAL DEPARTMENTS OF BANK

The regulatory environment for the Indian banking sector was characterized by greater

liberalization in foreign ownership and related areas, tightening of certain exposure norms and

infrastructure improvements in the market.

Some of the developments are:

Ceiling of 5% of the total advances imposed on the capital markets exposure (fund based

and non-fund based) for all commercial banks.

Better systems for trading in government securities and settlement in the foreign

exchange and government securities markets operationalised through the cleaning

corporation of India ltd. (CCIL) and the electronic negotiated dealing system (NDS).

In the growing competition faced by all the banks from various money market and its effects

bank deposits and advances, it has become necessary to design, develop new instruments which

would attack the customers by satisfying the identical needs.

The product should be evolved after studying customer’s needs and probable due to the same. To

give as idea two such products or instruments are described in the following paragraph. In the

context of products of banks in recent days bank marketing it is essential to take a look at the

following products, which attract the middle class customers and also are profitable to the bank.

Customers loan

Credit card

J&K bank offers customers the convenience of banking in a manner of their choice. Customers

can bank via their telephone, through ATMS, on the Internet or even through their mobile

phones.

The bank has several respective departments to measure its performance to decide fulfillment of

expectation, deposits that are sources of funds, and break even analysis can be used in bank

marketing for deciding pricing of a new product all these are in practice for taking the bank into

profitable wings.

As a part of bank marketing it has been introduce two main distribution channels:

Branch network

Specialized branches

CREDIT MANAGEMENT

“Credit allows the customer to buy now pay later”. So credit also constitutes the major

business activity of the banks i.e. lending loan and advances. Of all the functions of modern

banking, with or without security is by far the most important function .Advances comprise a

very large portion of total bank assets and forms to backbone of very bank structure. The

strength of the bank is thus primarily judged by the soundness of its advances. A wise and

prudent policy in regard to advances is considered an important factor inspiring confidence in

the depositors and the prospective customer of a bank.

Advances not play an important role in gross earnings of banks but also promote the

economic development of the country. All type of business activity including trade,

industry and agriculture depend on bank finance in one form or other. Banks by canalizing

accumulated savings of the nation into productive uses help both depositors and borrowers.

Bank assists in creating more avenues of employment and thus helps in raising the standard of

living of the people.

Creditability of a bank is one of the most important criteria in establishing the credit-

worthiness of a bank. Loans and advances constitute lending. Loans form the major business

activity of a bank and they need to be liquid and easily realizable as the bank is obligated

to repay the depositors as and when they are due for payment. Major part of the bank’s

income is earned from interest on the advances .So there is a need for the proper

management of loans and advances.

CREDIT MANAGEMENT can be defined as management of loans and advances in

Banks.In other words credit management means successfully managing the credit by paying the

debt obligations on time for the amount required.

FUNDS FOR LENDING

If we examine the Balance sheet of a bank, we would observe that the main Sources of funds

available for lending and investment are as follows:

Deposits of all types – fixed, current, saving and recurring.

Borrowings from other banks mostly from RBI.

Undistributed profit.

Paid-up-capital.

General reserves and other resources.

FORMS OF BANK LENDING

Banks offers different kinds of borrowing facilities to customers for various purposes

according to security, maturity, method of payment which is highlighted below:

LOANS: A loan account represents one way of lending money to a customer. In case of

loan, the banker advances a lump sum for a certain period at an agreed rate of Interest. The

entire amount is paid either in cash or by credit to his current account, which he can draw at

any time. The interest is charged for the full amount sanctioned whether he draws the

money from his account or not. To this extent, loan account loan account borrowing is

more costly than overdraft.

OVERDRAFT: Overdraft is an arrangement between a banker and his customer by which

the latter is allowed to withdraw over and above his credit balance in the current account

up to an agreed limit. This is only a temporary arrangement usually granted against

securities which may be personal or tangible.

CASH CREDIT: A cash credit is an arrangement by which the customer is allowed to borrow

money up to a certain limit. The customer need not draw the sanctioned amount at once but

draw the amount as and when required and can save the interest by reducing the debit

balance whenever he is in a position to do so. They are granted against personal security.

BILLS DISCOUNTED: Bills, maturing with in 90 days are discounted by banks for approved

parties. It constitutes a clean advance against two or more signatures of independent parties,

one that of endorser and the other that of the drawer. Banks rely on credit-worthiness,

standing and means of the endorser.

BILLS PURCHASED: Bills, clean or documentary are sometimes purchased from

approved customers in whose favor regular limits are sanctioned. In case of documentary

bill, the drafts are accompanied by documents of title to goods such as railway receipts or bill

of lading. Before granting a limit the bankers satisfy himself as to the credit-worthiness of the

drawer. Sometimes banks verify the financial standing of the drawers of the bills particularly

when the amounts are large.

TERM LOANS: Since sometimes, bankers have started lending large amounts for fairly

long periods to industries and agriculture on the security of fixed asset term loan basis. Such

loans are re-payable by installment over a number of years ranging from 3 to 10 years and some

times more. Banks extended term loans for acquiring fixed assets by their customers.

Banks normally ask for project to understand the cost of project, source of finance, fund/cash

flow estimates for the period.

Unlike agency rating, which use public scales, internal ratings use propriety scales that vary

across banks. Both types of rating serve as the foundation for the internal rating based (IRB)

approach of the new accord and should play a role for differentiating credit risk of loans.

External ratings are those of debt issues, not of issuers. The ratings assigned to senior unsecured

debt are close to issuer rating since the debt default only if the issuer does. Subordinate debt

might default without a default of senior debt. The secured debt benefits from various

guarantees, acting as a shield between the debts risk and the pure issuers credit risk. The ratings

of issues of facilities capture the severity of losses, which is combination of default probability

and expected recovery.

Rating schemes use various criteria, from qualitative factors such as strengths and weakness of

firms, up to financials of corporate borrowers.

Internal rating system should use as rating scheme isolating the various ingredients of credit

risk, default probability and recovery rates. This implies distinguishing the intrinsic rating of

borrower, the role of a supporting entity if any the recoveries resulting from the guarantees

attached to each facility.To move back and forth from internal ratings to default probabilities, as

the IRB approach of regulatory requires, a mapping between external ratings and internals

ratings. This mapping remains conventional.

EXTERNAL RATING:

The main or global, rating agencies are Moody’s, standard and Poor’s (S&P) and Fitch. Ratings

are assessments of the credit standing of a debt issue, materialized by coded letters (Such as

AAA, AA, etc) that serve essentially the needs of investors to have a third party view on the

credit risk of debt. In additions, ratings rank risk rather than value risk.

This is a major distinction between ratings and default probabilities, the later being a

quantification of the default likelihood of a debt issuer. Rating agencies rate public issues

rather than issuers. The same issuers usually have several debt issues rather than issuers not all

of them having the same risk. They all share the risk that the issuer defaults. However,

issues differ by seniority levels and guarantees. Senior unsecured ratings are very close to issuer

rating because they benefits from first priority repayments in the event of default. Hence the

likelihood of less is similar to the default likelihood of the issuer. Secured debts have

collateral attached so that, in the event of default of the issuer, they benefit from the higher

recoveries.

Subordinate debts are subject to claims from more senior lenders and have a higher

risk.Therefore, the credit risk varies across debt issues of the same issuer, even though they all

share the same default risk, which is specific to the issuer because senior unsecured debt is first

to be repaid and does not benefit from any collateral other than the credit standing of the

issuer, it is possible to consider senior unsecured debt rating as issuer’s rating. Ratings depend

on the fundamental analysis under a long view. Agencies tend to rate ‘through the cycle’

based on the long -term view of ‘strength and weaknesses, opportunities and threat’ (SWOT)

of firms. Hence, ratings do not change frequently under normal conditions because short-

term deviations due to current conditions are not relevant as long as they do not alter durably

the credit standing of an obligor. However, agencies continuously review their ratings on a

periodical basis or under occurrence of contingent events that affect the credit standing of an

issuer.

An example of such an event is a merger or an acquisition, which changes significantly the

risk profile of corporate borrower.Rating agencies also provide short-term rating and signal

ratings under review to investor. External ratings apply to various debt issues from: corporate

firms; banks and financial institution; sovereign borrowers (country risk); multilateral

development banks. Ratings also apply to currencies, including local currency and foreign

currency held locally and subject to transfer risk, the risk of being unable to transfer cash

out of the country. By contrast an issuer’s rating characteristics the credit standing of an

issuer and should correlate with its default probability.

Rating from agencies exits only for issues of large listed companies. This creates a bias

when assigning default frequencies based on historical default statistics because the sample of

counter parties rated by agencies is usually not representative of the banks, portfolios. For

bank corporate loans or market counter parties, external agency ratings are usually not

available because borrowers are local public.Banks need to relay their own internal rating

scheme to differentiate the risk of their exposures to these counter parties. In general, a typical

rating scales uses such general quantifications of credit risk as ‘highest’, ‘high grade’, ‘some

risk’ or vulnerable’,’ highly vulnerable’. The quantifications of various levels do not make

fully explicit the criteria used for rating, although all agencies provide methodology notes. This

makes sense given that there are a wide variety of criteria influencing the credit standing of

borrower.

INTERNAL RATING SYSTEM:

Internal rating system is public and is customized to each bank’s need. There is a strong

tendency towards harmonization due to the new regulations putting the rating system in a

central position for evaluation capital requirements. Since capital requirements affect pricing,

the banking industry needs common benchmarks. Banks have exposure to all sorts of

counter parties and across industries and countries. Therefore, all banks also need ratings

for various types of entities; corporate firms; banks; country rating.

Like external ratings, internal ratings are grades assigned to borrowers or facilities for

ranking their risk relative to each other. Unlike external ratings, the counter parties of the banks

are usually non-rated entities. Internal rating isolates the borrowers risk from the facility

risk, which depends on how secured it is. Internal ratings result from a review of both

borrowers and facility characteristics.

Typical components of internal rating system include:

Borrowers risk.

External support from a supporting entity.

Facility risk (a facility being transaction), the equivalent to a debt issue for public

firms.

The support of another entity can strongly affect the risk of the couple ‘primarily

borrower supporting entity’ facilities might benefits from a wide spectrum of guarantees,

strongly mitigating the credit risk.

Support plays a major role in enhancing intrinsic rating.To assess support, it is necessary to

assess the credit standing of the direct borrower, that of the supporting entity and the

‘strength’ of the support. Combining support assessment with intrinsic rating provide the

borrowers overall rating. For facilities, other factors mitigate credit risk, mainly the seniority

level and the guarantees attached to single facilities.

Hence, a well-collateralized facility might have a good rating even though the role for

banks internal system.The risk mitigates of a facility relate directly to recovery in the event of

default. Recovery rates based on experience, type of transaction and type of guarantee now

serve as a substitute for facility ratings, sometimes used. Chances are that these Forfeits

will evolve into hard data with historical statistics from default built up under the

incentives of the regulators.

Internal ratings of banks should ideally include:

The intrinsic rating of the borrowers.

In the rating of the supporting entity.

The overall borrower rating, given intrinsic rating, the supporting entity rating and

the assessment of the support.

An assessment of the guarantees, which should be converted into a recovery rate of

loss, given default rate for capital requirement purposes.

Evidence from many banks in recent years suggests that collateral values and recovery rates

(RRs). This link between RRs and default rates has traditionally been neglected by credit risk

models, as most of them focused on default risk and adopted static loss assumptions, treating the

RR either asa constant parameter or as a stochastic variable independent from the

probability of default (PD). Internal Rating System in banks base their analyses on credit

performance – the servicing of debt obligations in full and on time, and several other

parameters including stress situations. This analysis is based not only on public information,

but also on private/confidential information. Inherent in this definition of ratings is the notion

that they are an ordinal measure of risk, but not necessarily a cardinal one. Accordingly, all

Credit Rating system expresses the outcome of their assessments in the form of symbols,

such as PPP, AAA, or on a scale 20.

From an operational standpoint, the purpose of ratings is to measure credit risk in terms of

probability of default, expected losses or likelihood of timely payments in accordance with

contractual terms.In Internal Rating System the Probability of default varies with different

time horizons. While agencies have been criticized, and at times rightly so, for being vague as

to the time horizon over which they are rating.

Although the recent increase in rating volatility may to some extent have been due to an

increase in economic uncertainty, questions remain as to whether this uncertainty will lead the

IRS to adjust the weights they attach to different objectives – accuracy and stability – in their

rating process more actively. Assessing the performance of rating agencies with regard to

these two objectives can be done either in relation to the methodology they use (i.e. do

ratings provide an accurate and stable picture of default risk).

Ratings provided by CRAs are a measure of the long-term fundamental credit strength of

customers, i.e. their long-term ability and willingness to meet debt-servicing obligations.

More specifically, ratings apply either to the general credit worthiness of an obligor or to its

obligations with respect to a particular debt security.

Chapter 4

ANALYSIS AND

INTERPRETATION OF

DATA

C red i t- Deposit R a t i o

Credit Deposit ratio is a measure of utilization of resources (deposits) by banks and has a

direct bearing on the size of the loan portfolio. It has implications for the profitability of the

banks. It is one of the most widely used banking indicators for analyzing the role of banks in

promoting productive sectors and contributing to economic growth. CD ratio assumes greater

significance as an aggressive measure for gauging the effectiveness of credit delivery

system. Higher CD ratio implies for greater credit orientation of banks.

The deployment of credit and time path of CD ratio in general is influenced by structural

transformation of the economy, the role of credit culture and lending policy of banks have a

considerable impact on the size of the ratio.

H 0: The Deposits in a financial year are not correlated to the credits given in the year.

H 1: The Deposits are correlated to the credits.

[Table 4.1]

Inference: There is a positive correlation between Deposits and credits.So change in deposits

will cause a change in the credit advanced by the bank in a particular financial year.We accept

H1 hypothesis.

[Graph 4.1]

YEAR CREDIT DEPOSITS

2006 14483.11 23484.64

2007 17079.94 25194.29

2008 18882.61 28593.26

2009 20930.41 33004.1

2010 23057.23 37237.16

Correlation 0.98076

2006 2007 2008 2009 2010

Inference: From the table it is observed that the credit deposit ratio was 61.67% during the

year 2006 which increased to 61.91% by the year 2010.

Comparative Analysis of NPA of the J&K Bank before and after introduction of Finacle.

H0 : The introduction Of IT doesn’t effect the NPA of the Bank.

H1 : The NPA decreased with the use of IT.

[Table 4.2]

(Rs.in crores)

Value of NPA before Finnacle Value after introduction

287.62 74.07(2008)

302.08 73.49(2009)

294.71 20(2010)

With the introduction of Finnacle by Infosys the bank is able to bring down the NPA as shown in

the table ,so we accept H1.

Total Growth Of Advances

[Table 4.3]

[Graph 4.2]

Year Advances Priority Advances

2006 14483.11 2827.86

2007 17079.94 3286.98

2008 18882.61 4874.33

2009 20930.41 7345.95

2010 23057.23 8632.29

Inference: The Priority advances in 2006 is Rs.2827.86 lakhs and has increased to Rs.8632.29

lakhs in 2010.

Analysis of Net Sales

[Table 4.4]

Net SalesPercentage of

NPAPercentage of

Recovery

100% 15 85>80%

<100%33 67

>50 < 60% 52 48

[Graph 4.3]

Inference:

This graph shows that when the small scales industries have meet 100% of their sales then bank

was able to recover loan on time of about 85% and when the sales is below 50% there was an

NPA of 52%.this indicates when the sales increases the credit worthiness of the borrower

increases .

Analysis of Capacity Utilization

[Table 4.5]

CapacityUtilization

Percentage ofNPA

Percentage ofRecovery

>90% 12 88

75% to 90% 41 59

50% to 75% 47 53

[Graph 4.4]

Inference:

This graph shows that when the Capacity Utilization is 90% the bank was able to recovery loan

on time of about 88% and when the capacity utilization is below 50% there was an NPA of

47%.the capacity utilization reveal about the turnover of the company which is a very good

indicator of the paying capacity of the borrower.

Analysis of Debt Equity Ratio

[Table 4.6]

Debt equity ratioPercentage of

NPAPercentage of

Recovery

below 1 20 80

1 to 1.50 25 75

above 2.50 55 45

[Graph 4.5]

Inference:

This graph shows that when the small scales industries have debt equity ratio of 1 the bank was

able to recovery loan on time of about 80% and when the debt equity mix above 2.50 there was

an NPA of 52%.this ratio is a very good indicator of the credit worthiness of the borrower.

Analysis of Current Ratio

[Table 4.7]

Current ratioPercentage of

NPAPercentage of

Recovery

1:01 32 68

1.50 to 2.50 23 77

2.50 to 4.00 45 55

[Graph 4.6]

Inference:

This graph shows that when the current ratio of 1:1 it was not a good indicator of credit

worthiness, as the ratio keep changing and the bank was able to recovery loan on time of only

about 68%where as when the current ratio was ranging from 1.5 to 2.5 the bank was able to

recovery loan of 77%.thus the current ratio is not a good indicator of credit worthiness of the

borrower.

Analysis of Net Profit

[Table 4.8]

Net Profit % of NPA% of

Recovery

>20% 9 91

>10% to<20%

57 43

<10% 66 34

[Graph 4.7]

I n f er e n ce :

This graph shows that when an increase in net profit was about >20% the bank was able to

recovery loan on time of about 91% and when the net profit is below 10% there was an NPA of

66%.this indicates that when the profit increases by 20% from the previous year the loan is

paid on the time .where as when the profit is <10% the payment is not on time.

Analysis of Interest Coverage Ratio

[Table 4.9]

Interest coverageRatio

% ofNPA

% ofRecovery

>2.5 15 85

2.00 to 2.5 28 72

<1.50 57 43

[Graph 4.8]

Inference:

This graph shows that when the interest coverage ratio is greater than 2.5%than then the

bank was able to recovery loan on time of about 85% and when the ratio was less than 1.50 there

was an NPA of 43%.

Table showing the differential weights given to various risk factors of corporate term loans by

Jammu and Kashmir bank.

[Table 4.10]

COMPONENTS WEIGHTAGE

INDUSTRY RISK 10%

BUSINESS RISK 15%

MANAGEMENT RISK 20%

FINANCIAL RISK 55%

[Graph 4.9]

Inference:

Thus, it can be inferred from the table and the chart that Jammu and Kashmir bank gives greater

weightage to the financial risk while appraising the term loans of the corporate.

FINDINGS

The findings are based on the analysis of the financial statements in order to develop a credit

rating model.

There was NPA of about 20 crores in the bank.

The net NPA for the year 31 march 2008 was 74.07 crores and the decreased to 20 crores

during the year 2010 from profit and loss account.

There existing rating system in J&K bank did not consider the rating of interest coverage

ratio, and debt service ratio.

The bank did not manage the credit risk by getting the credit risk information from the

other bank in order to lend.

The current ratio is not a very good indicator of the credit worthiness of the borrower.

Whereas the debt equity ratio and the interest coverage ratio is a very good indicator of

the credit worthiness of the borrower.

Chapter 5

Suggestions and

Recommendations

SUGGESTIONS

1. The appraisal of corporate term loan by Jammu and Kashmir bank takes about 2 to 3 months.

The appraisal process is lengthy. The banks should reduce the time taken to complete the

appraisal process computerized the appraisal process. This can be done by designing the

appraisal software with the help of software companies which would reduce the time taken to

appraise the risks involved in lending corporate term loans

2. To reduce the increasing NPA’s and NPL’s the bank can address the issues to Debt tribunals,

corporate debt restructuring national company law tribunals and assets formation reconstruction

companies to facilitate easy recovery of loan.

3. Banks have to bring down expenditure cost like labour cost, transaction and processing cost

and legal expenses to remain as competitive as possible to face the stiff challenges posed by the

multinational banking institutions in the country.

4. Banks are heavily over-staffed. When elsewhere in the world Banks were switching to

application of advanced systems of information technology computerizing all repetitive

operations completely dispensing with manual handling. Therefore nationalized banks should

adopt new technology like computerization in the banking system, and should strengthen skills

and intellectual capital formation in the banking industry.

4. The banks need to modernize as the era of '' m--commerce'' (mobile commerce) and ''e--

commerce’’. Therefore nationalized banks needs to catch up with technology, especially the

Internet. The bank should plan to invest heavily in automating the branches.

5. The bank has to reduce their interest rates as it can attract more growth in their loans and

advances. The bank has to compare the interest rates of other banks and come up with an interest

rate which is low, as this may help in more growth in the banks loans and advances.

6. There is a need of substantial upgradation of existing information systems, risk management

practices and technical skills at nationalized banks.

7. Banks concentrates more on priority sector lending, opening branches in rural and semi-urban

centers, and gives less importance to profitability, therefore nationalized banks should

concentrate on all sectors of the economy.

Chapter 6

Conclusion

CONCLUSION

Thus it can be concluded that risks faced by Jammu and Kashmir bank are numerous like credit

risk, liquidity risk, foreign exchange risk and interest rate risk. The biggest banking failure is due

to credit risk. So the bank appraise the credit risk before sanctioning corporate term loans.

Jammu and Kashmir Bank has a detailed process of appraising the corporate term loans. The

banks look into risk factors involved in lending term loans to corporate. Different weights are

being assigned to different risk factors while appraising the overall risk of the corporate term

loans.

This detailed process of appraising term loans gives a proper insight to the banks to judge

whether it should sanction the term loan or not. The Jammu and Kashmir Bank judges the

corporate on more than 40 parameters and only if the corporate are assigned a rating of excellent

and good, they sanction term loans.

BIBLIOGRAPHY

www.jkbank.net

www.rbi.org.in

finance.indiamart.com

www.business-standard.com

![Advanced taxation (cfap5) by fawad hassan [lecture3]](https://static.fdocuments.in/doc/165x107/58ece9871a28ab477f8b45db/advanced-taxation-cfap5-by-fawad-hassan-lecture3.jpg)