Credit and Debt Management and Debt Management – 2008 Survey Research and analysis by the Credit...

176

2008 Credit and Debt Management Survey 2008 Credit Management Research Centre, Leeds University Business School

Transcript of Credit and Debt Management and Debt Management – 2008 Survey Research and analysis by the Credit...

Credit and Debt Management – 2008 Survey

1 Research and analysis by the Credit Management Research Centre, University of Leeds Business School

2008

Credit and Debt Management Survey 2008 Credit Management Research Centre, Leeds University Business School

Credit and Debt Management – 2008 Survey

2 Research and analysis by the Credit Management Research Centre, University of Leeds Business School

CONTENTS

1. Executive Summary

1.1 Consumer and Household Debt 1.2 Commercial Lending and Insolvency 1.3 Debt Collection Agents and Debt Sale 1.4 Survey of DCA’s 1.5 Large Volume Debt Management 2. An Overview of Consumer and Corporate Lending 2.1. Categories of Lending 2.2. Consumer Lending and Indebtedness 2.3. Consumer Credit and Indebtedness 2.3.1. Subjective Evidence 2.3.2 Statistical Evidence 2.4. A Summary of Lending Trends 2.4.1. Secured Lending 2.5 The Over-Indebtedness Debate 2.5.1 Arrears 2.5.2 Trends in Write-offs by Major Lenders 2.6 Personal Insolvency: bankruptcy and Voluntary Arrangements 2.6.1 Bankruptcy Modelling – Key Drivers 2.7 County Court Actions 2.8 Factors Affecting Indebtedness 2.9 Fraud 3. Commercial Lending and Trade Credit 3.1 Business Growth and Insolvency in the UK 3.2 Forecasting Corporate Insolvencies 3.3. Commercial Lending 3.4 Trade Credit 3.4.1 Credit Terms and Credit Management Practice 3.4.2 Motives for the Supply of and Demand for Trade Credit 3.4.3 Credit Management: The Impact on Corporate Performance 3.4.4 The Use of Trade Credit and Payment Behaviour:

The Demand Side Motivation 3.5 Late Payment and Bad Debt 3.6 Late Payment Trends 3.7 Impact of the Late Payment Legislation 3.8 Use of Third Parties in Credit Management 3.8.1 Factoring and Invoice Discounting 3.8.2 Credit Insurance and Related Services 4. Large Volume Debt Management – Case Studies 4.1 Introduction and Objectives 4.2 Background to the Credit Account Life-cycle 4.2.1 Customer Life-Cycle

Credit and Debt Management – 2008 Survey

3 Research and analysis by the Credit Management Research Centre, University of Leeds Business School

4.2.2 Account Life-Cycles 4.3 Elements of ‘Best Practice in Collections’ and Implications 4.3.1 Credit Information and Scoring Technologies 4.3.2 Customer contact and Customer Retention and Collection 4.3.3 Collection department practices

4.3.4 Use of external debt collection agencies for telephone, letter and doorstep contact; litigation

4.3.5 Benchmarking 4.4 Summary 4.5 Short Case Interviews 2007 4.5.1 Collections Department Medium Sized Bank 4.5.2 Commercial Credit Card 4.5.3 Consumer Credit Card 4.5.4 Medium Sized Retail Bank 4.6 Large Volume Collections: Interview Survey 2003 4.6.1 Delinquency Cycles 4.7 Case Studies 2003: large volume collection activities 4.7.1 Case A: Debt Recovery Division of a Major Bank 4.7.2 Case B - Credit Card Provider 4.7.3 Case C: Large Volume Lender Retail Card, Personal Loans 4.7.4 Case D: International Bank Collections and Recovery 4.7.5 Debt Management and Collection in the Utilities Sector 4.7.6 Best Practice in Collections and Recovery: Evidence from US Utilities 4.7.7 Key Performance Indicators Used in Debt Management 4.7.8 Best Practice in Collections and Recovery: The Water Sector 4.7.8.1 Areas of Disadvantage 4.7.9 Credit and Debt Management Practice in the Water Industry 4.7.9.1 General Information 4.7.9.2 Direct billing and other methods 4.7.9.3 Telephone Contact 4.7.9.5 Scoring and Customer Profiling 4.9 Use of Debt Collection Agents 4.9.1 DCA: Case Study 4.10 Debt Sale and Purchase: Trends and Developments 4.10.1 Case Study: Debt Buyer 5. A Survey of Debt Collection Agents and Debt Buyers 5.1 Debt Collection Services 5.2 The Market for Debt Collection Services 5.3 Market Size 5.4 Value and Volumes in the Debt Collection Market 5.5 Quality and Volumes in the Debt Collection Market 5.6 Debt Purchase 5.7 Litigation and Bankruptcy References

Credit and Debt Management – 2008 Survey

4 Research and analysis by the Credit Management Research Centre, University of Leeds Business School

CHARTS AND TABLES

Table 2.1 – Categories of Measurable Lending in the UK (Source:

Keynote Ltd)

Chart 2.3.1.1 – Debt Client Characteristics 2006 (source: Citizens Advice

Bureau Survey 2006)

Chart 2.3.1.2 – Consumer Credit Outstanding (source: Bank of England)

Chart 2.3.1.3 – Consumer Spending Growth (source: Bank of England)

Chart 2.3.1.4 – Total Personal Debt July 2007 (source: Bank of England)

Chart 2.3.1.5 – Total Lending to Individuals Per Month (source: Bank of

England)

Chart 2.3.1.6 – Mortgage Equity Withdrawal 1970-2006 £M (source: Bank

of England)

Chart 2.3.1.7 – Mortgage Equity Withdrawal as a % of Disposable Income

(source: ?????

Chart 2.4.1.1 – Approvals for Secured Lending to Individuals

(thousands) (source: Bank of England 2007)

Chart 2.4.1.2 – 12 Month Growth Rate of Secured Lending Approvals to

Individuals (source: Bank of England 2007)

Chart 2.4.1.3 – Monthly Value of Approvals for Secured Lending to

Individuals (source: Bank of England 2007)

Chart 2.4.1.4 – 12 Month Growth Rate of Value of Approvals for Secured

Lending to Individuals (source: Bank of England 2007)

Chart 2.4.1.5 – Monthly Number of Approvals for Secured Lending to

Individuals (source: Bank of England 2007)

Chart 2.4.1.6 – 12 Month Growth Rate of Number of Approvals for

Secured Lending to Individuals (source: Bank of England 2007)

Chart 2.4.1.7 – Monthly Value of Approvals for Secured Lending to

Individuals (source: Bank of England 2007)

Chart 2.4.1.8 – 12 Month Growth Rate of Value of Approvals for Secured

Lending to Individuals (source: Bank of England 2007)

Chart 2.4.1.9 – Monthly Amount of Total Sterling Secured Gross Lending

to Individuals and Housing Associations (in sterling millions) (source:

Bank of England 2007)

Chart 2.4.1.10– Monthly Amount of Sterling Repayments of Secured

Lending by Individuals (in sterling millions) (source: Bank of England

2007)

Chart 2.4.2.1– Monthly Amount of Total Sterling Unsecured Gross

Lending to Individuals (in sterling millions) (source: Bank of England

2007)

Chart 2.4.2.2– Monthly Amounts Outstanding of Total Sterling Net

Unsecured Lending to Individuals (source: Bank of England 2007)

Chart 2.4.2.3– Monthly Amount of UK Resident Banks’ (inc. Central Bank)

Sterling Credit Card Repayments by Individuals (in sterling millions)

(source: Bank of England

Chart 2.4.2.4– Monthly Amount of UK Resident Banks’ (inc. Central Bank)

Sterling Credit Card Repayments by Individuals/Monthly Amounts

Outstanding of Total Sterling Net Credit Card Lending to Individuals

Chart 2.4.2.5 - End Month Weighted Average Interest Rate, Bank &

Building Societies (source: Bank of England 2007)

Chart 2.5.1 – Debt to Income Ratio (source: ONS and Bank of England

2007)

Chart 2.5.2 – Income Gearing (source: ONS and Datastream 2007)

Chart 2.5.3 – Debt to Wealth Ratio (source: ONS and Bank of England

2007)

Chart 2.5.4 – Credit Card Lending (source: ???

Chart 2.5.5 – Other Unsecured Lending (source: ???

Chart 2.5.6 - SecuredLending (source: ???

Chart 2.5.7 – Ratio of Write offs to Credit Card Lending (source: ???

Chart 2.5.8 – Major UK Banks Annual Write Off Rates (source: Bank of

England 2007

Chart 2.5.9 – Personal Bankruptcies and Individual Voluntary

Arrangements (source: DTI 2007)

Chart 2.5.10 – Personal Bankruptcy Ratio (Source ???)

Chart 2.5.11 – Consumer County Court Judgements 2002-2007 (Source:

Registry Trust)

Chart 2.9.1 – Fraud Trends 1997- 2005 (Source: CIFAS 2007)

Chart 2.9.2 – Fraud Trends 1997- 2005 (Source: CIFAS 2007)

Chart 3.1.1 – Register Size in Great Britain (1992-2006) (Source:

Companies House)

Chart 3.1.2 – Company Birth Rate (2001-2006) (Source: Companies

House)

Chart 3.1.3 – Company Insolvencies (1975-2006) (Source: Companies

House)

Chart 3.1.4 – The Relationship between Insolvencies and the Write-off

Rates of Banks (Source: Bank of England)

Table 3.2 – Variables used to Forecast Insolvencies (Source: CMRC)

Table 3.3.1 – Bank and Building Society Lending to Industrial and

Commercial Companies 1996-2006 (Source: Bank of England)

Chart 3.3.1 – Contributions to Annual Growth Rate from Non Financial

Corporations (Source: ?????)

Chart 3.3.2 – New Leasing and HP Business Finance by Client Size and

Business Investment

(Source: FALA and ONS)

Chart 3.3.3 – Small Business Borrowing and Deposits at Year End (£

Billions) (Source: Bank of England)

Chart 3.3.4 – Changes in Sources of External Finance for SME’s

(Source: ESRC Centre of Business Research)

Chart 3.3.5 – Aggregate Capital Gearing of UK companies

(Source: ONS and Bank calculations)

Chart 3.3.6 – Aggregate Capital Gearing of UK companies

(Source: ONS and Bank calculations)

Chart 3.3.6 –Capital Gearing/Total Debt/Total Assets (Source:

Creditscorer)

Chart 3.3.7 –Income Gearing/Operating Profit (Source: Creditscorer)

Chart 3.3.8 – The Importance of Trade Debtors to the Balance Sheet

(Source: Creditscorer)

Chart 3.3.9 – DSO and Creditor Days Trends (1982-2004)

(Source: Creditscorer)

Chart 3.3.10 – Net Trade Credit Trends

(Source: Creditscorer)

Table 3.4.2.1 – Motivations for Trade Credit Extension (Source: CMRC)

Chart 3.4.4.1 – The Use of Trade Credit and Payment Behaviour – A

Strategy Map

(Source: CMRC)

Credit and Debt Management – 2008 Survey

5 Research and analysis by the Credit Management Research Centre, University of Leeds Business School

Chart 3.6.1 – % of Accounts Paying beyond the Due Date (Source:

CMRC)

Chart 3.6.2 – % of Companies Paying on Time (Source: CMRC)

Chart 3.6.3 – % of Invoices Paid on Time – Sector Analysis (Source:

CMRC)

Chart 3.6.4 – % of Invoices Paid on Time – Sub Sector Analysis for the

Manufacturing Sector (Source: CMRC)

Chart 3.6.5 – Average Debtor Days (Source: CMRC)

Chart 3.6.6 – Payment Beyond the Due Date (Source: CMRC)

Chart 3.6.7 – Debtor Days - Size Analysis

Chart 3.6.8 – Debtor Days - Turnover Analysis

Chart 3.6.9 –Debtor Days – Sector Analysis

Chart 3.6.10 – Debtor Days – Sub Sector Analysis

Chart 3.6.11 –Interest Charged on Overdue Accounts

Chart 3.6.12 – % Firms Affected by Late Payment

Chart 3.6.13–Receivables Beyond 30/90 Days

Chart 3.6.14 – Accounts Beyond 30/90 Days - Sector

Chart 3.6.15 – Accounts Beyond 30/90 Days

Table 3.6.1 – Profile of firms suffering from Bad Debt

Chart 3.6.16– Types of Customer who are Slow Payers

Chart 3.6.17– Assertions about Late Payment

Chart 3.6.18– Possible Policy Measures

Table 3.6.2– % of Companies Pursuing Late Payments through the

Courts

Table 3.6.3– Awareness of the Late Payment Legislation

Chart 3.6.19– Awareness of the Late Payment Legislation

Chart 3.6.20 – Domestic Factoring Trends (Source: FDA)

Chart 3.6.21 – Domestic Invoice Discounting Trends (Source: FDA)

Chart 3.6.22 – Export Factoring and Invoice Discounting (Source: FDA)

Chart 3.6.23 – Firms using Invoice Finance (Source: Bank of England)

Chart 3.6.24 Growth in Demand for Factoring (Source: FDA)

Chart 3.6.25 – Credit Insurance Growth (Source: ICISA)

Chart 3.6.26 – World Market for Credit Insurance (Source: ICISA)

Chart 3.6.27 – Use of Credit Insurance by SME’s (Source: ICISA)

Table 3.6.4 – Reasons for not using Credit Insurance (Source: CMRC)

Table 3.6.5 – Reasons why companies use Credit Insurance (Source:

CMRC)

Table 3.6.28 – Traditional Benefits of Credit Insurance (Source: CMRC)

Chart 4.2.1 – Customer Life-Time Management

Chart 4.2.2 – The Customer Account Life-Cycle

Table 4.2.1 – Account Management Functions (Source: CMRC)

Chart 4.2.3 – Scoring in Account Management

Chart 4.2.4 – Applications to Collections

Chart 4.2.5 – Debt Management and Collection Trends

Chart 4.2.6 – Scoring to Determine Collection Strategies

Chart 4.3.1 – New Debt Management Approaches

Chart 4.3.2 – Motives for Credit Scoring in Consumer Credit

Chart 4.3.3 – Modelling for Collections Strategies

Chart 4.3.4– Behaviour Scoring: Principles

Chart 4.3.5 – Behaviour Scoring

Chart 4.3.6 – Example Behaviour Score Card

Chart 4.3.7 – Behavioural Scoring and the Account Life-cycle

Chart 4.3.2.1 – Champion vs Challenger Strategies in Collection

Chart 4.3.3.1 – Lender Time Horizons

Chart 4.6.1.1 – Delinquency Cycles

Chart 4.7.3.1 – Computer Systems Sued from Application to Collection

Chart 4.7.5.1 – Entire Billing Process (Source SAP Business Intelligence)

Chart 4.7.5.2 – Factors Impacting on Debt in the Utilities Sector

Chart 4.7.6.1 – Revenue to Recovery – Customer Impact

Chart 4.7.8.1 – A Guide to Good Practice

Chart 4.7.8.2 – Number of Customers using Prepayment Meters

Chart 4.7.9.1 – % of Directly Billed Customers

Chart 4.7.9.2 – % of Directly Billed Customers – by size

Chart 4.8.5.1 – A Large Volumes Collections Operation

Chart 4.8.5.2 – A Credit Management Model (1)

Chart 4.8.5.2 – A Credit Management Model (2)

Chart 4.8.5.3 – Recovery Paths and Steps

Chart 4.9.1 – Collections: An Integrated Approach

Chart 4.9.2 – Turnover Trends in UK Debt Collection market

Chart 4.9.3 – Net Worth Trends in UK Debt Collection market

Chart 4.9.1.1 – Example of DCA Collections Process

Chart 4.9.1.2 – DCA Service Optimisation

Table 5.1 Debt Collection And Other Services Offered By Respondents

Chart 5.1 Client Base Trends For The Debt Collection Market

Chart 5.2 Number Of Debts Placed In Market

Chart 5.3 Market Size For Consumer Debt

Chart 5.4 Market Competitiveness For Consumer Debt

Table 5.2 Number Of Debts Worked Per Month – Whole Sample

Table 5.3 Value Of Debts Worked Per Month – Whole Sample

Table 5.4 Number Of Clients And Debts Worked Per Month – Agency

Size Breakdown

Table 5.5 Total Value And Total Number Of Debts Placed – Agency Size

Breakdown

Table 5.6 Sectors For Debt Collection Activities

Table 5.7 Growing And Declining Sectors For Consumer Debt

Table 5.7 Value Of Debts From Largest Client

Chart 5.5 Quality Of Consumer Debt

Chart 5.6 Age Of Consumer Debt

Chart 5.7 Number Of Clients Worked For

Chart 5.8 Debt Purchase Market Growth

Chart 5.9 Growth In Prices Paid In Debt Purchase - 2007

Table 5.8 % Of Purchased Debt Sent For Collection

Table 5.9 % Of Purchased Debt Sent For Collection

Table 5.10 % Of Purchased Debt In Litigation

Table 5.11 % Of Total Debt Referred To Court

Chart 5.10 % Of Agents With Accounts Operating Under An Iva

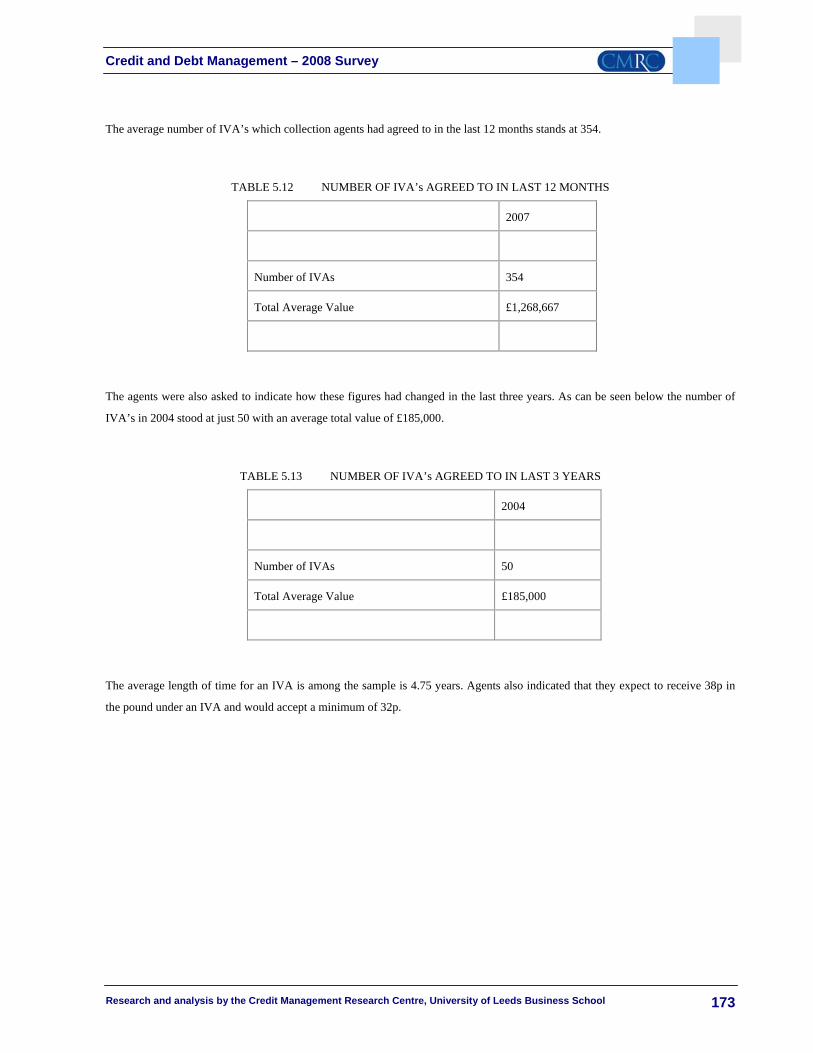

Table 5.12 Number Of Iva’s Agreed To In Last 12 Months

Table 5.13 Number Of Iva’s Agreed To In Last 3 Years

Table 5.14 Number Of Iva’s Agreed To In Last 3 Years

Table 5.15 Defaults Which Have Been Rescheduled In Last Year

Table 5.15 Number Of Iva’s Agreed To In Last 3 Years

Table 5.16 Bankruptices In The Last Two Years

Credit and Debt Management – 2008 Survey

6 Research and analysis by the Credit Management Research Centre, University of Leeds Business School

1. Executive Summary 1.1 Consumer Lending and Household

Debt

The growth in household debt, both in absolute terms and

The growth in household debt, both in absolute terms and

relative to household income, continues to cause some

concern. As the economic climate changes servicing debt

may become more problematic for a larger proportion of

the UK household sector particularly as mortgage

repayments rise and the opportunities for refinancing and

restructuring current debt decline with the tightening of

lender credit policies. Increases in financial distress and

insolvency in the corporate sector could threaten jobs and

household income in an already fragile economy.

Increases in arrears levels, bad debts and insolvencies

have peaked historically during and/or at the end of

recession due to losses of income. What is particularly

striking about the recent growth in bankruptcy and other

indicators of financial stress is that the trend increase

occurs against a background of generally good macro-

economic and monetary conditions, GDP growth, low

interest rates, high levels of employment and strong asset

prices. The 90’s peak occurred against a backdrop of

economic decline and nominal interest rates in the region

of 13-14% .

The rise in household debt in Britain gained headlines in

2005 when, for the first time, it rose to over £1trillion. By

the first quarter of 2007 the level of outstanding debts was

around £1.4 trillion. This total figure includes secured

lending, the majority of which is first mortgages and

additional ‘equity release’. This amounts to around 80% of

the total consumer lending. Unsecured lending, ‘consumer

credit’, however, has grown rapidly over the past decade

directly related to the growth in the number and type of

credit card products available to consumers. Increased

competition in financial services has fuelled the increase in

available credit products and the degree of product

differentiation. Households owe sums equivalent to 160%

of disposable income.

There are increasing signs that many households are

struggling to service their debts judging by the growth in

the use of private sector and voluntary sector debt

management services. The record levels of personal

bankruptcies as well as the steady rise in the indebtedness

of households, the dramatic increase in the number of fraud

cases, and excessive bad debt losses have prompted the

industry as well as the government to once again examine

the fundamentals of the consumer lending business.

Gauging the extent of the ‘household debt problem’

requires balancing the evidence provided by objective data

from national statistics and the Bank of England with the

vast amount of quasi-subjective information provided by

debt advice groups, lobbyists and surveys of the opinions

of debtors and lenders.

There has been much, often alarming, press and media

coverage that suggests something of a crises in household

finances. These headlines are often fuelled by surveys of

individuals that are in ‘financial difficulty’ and the

apparent increase in debt related problems being reported

to counsellors, debt advice groups, the Citizens Advice

Bureau and varies consumer lobbies.

The increased availability of credit products and the

competition for customers has facilitated a considerable

market for the ‘restructuring of debts’ i.e. moving debts to

lower interest rates (balance transfers) or more typically

extending the time period of the debt with lower monthly

Credit and Debt Management – 2008 Survey

7 Research and analysis by the Credit Management Research Centre, University of Leeds Business School

repayments but, ultimately, at a significantly higher rate

(consolidation loans).

There is considerable evidence of households ‘juggling’

finances via balance transfer, the use of loan consolidation

products, making payments on instalments of secured

credit agreements with unsecured credit (e.g. mortgage

payments with credit card cheques). The Credit Reference

Agency, Experian reported that 8.2 million individuals are

in serious debt; 2.1 million are struggling with repayments;

2.5 million are concerned about their ability to manage

debt and 2 million do not know the extent of their debts.

A notable feature of borrowing in recent periods, since

around 1998, is the extent of mortgage equity withdrawal

as a source of borrowings. This primarily concerns

releasing funds tied up in property for expenditure outside

of the housing market (i.e. not used for house purchase of

home improvements). The considerable growth in property

prices since 2000 has created significant amounts of

‘equity’ relative to initial mortgage. Clearly, households

have been able to finance consumption (and unsecured

debt re-payments) on the back of rising house prices.

The buy-to-let and sub-prime (self-certified) mortgage

market appears to be particularly vulnerable in the UK as

well as the US. The quality of lending in these areas is

suspect. The terms ‘Liar Loans’ and ‘ninanj’ (No Income

No Assets No Job’) are phrases used to describe such

lending in the US press but the quality of sub-prime

mortgage portfolios in the UK is equally a risk to the

housing market

Reported statistics on debt servicing vary considerably and

are, of course, sensitive to the sample selected. Although

the ‘average household’ is spending around 12% of its

disposable income on interest payments if we take only the

‘credit active’ population then, in 2007, households are

spending around 30% of their income servicing debt, up

from around 20% 10 years ago.

The Council for Mortgage Lenders report that the number

of mortgages in short-term arrears rose to 125,100 in June

2007 which was slightly down on the previous year. The

Bank of England’s Financial Stability Report (2007,

October) concludes that arrears will be concentrated in a

small proportion of households with low income/high debt

and that “the number of arrears spanning the majority of

the income and debt distribution is small” but with changes

in interest rates and growth in indebtedness “there is a

growing tail of vulnerable households”

The ratio of write offs-to-amounts outstanding for credit

cards is also increasing steadily with a remarkable peak in

the first quarter of 2002. The secured lending write-offs

show a considerable increase in 2005 and 2006 with a peak

similar to the end of 1999. They have started to decline in

2007.

The levels of personal insolvency as gauged by the number

of bankruptcies and individual voluntary arrangements

show a quite spectacular increase since 2000. The

beginning of this upward trend pre-dates the changes in

bankruptcy law introduced in April 2004 although there is

a clear acceleration in the levels of declared insolvencies

post-2004. The Act appears to have encouraged individuals

on the path to bankruptcy to declare early.

The number of CCj’s against consumers has grown rapidly

since 2004 and reached a ten year high by the end of 2006

with 843,853 judgment orders. The growth has continued

in 2007 with almost 250,000 judgements in Q1 and

therefore the total could reach 1 million judgements by the

Credit and Debt Management – 2008 Survey

8 Research and analysis by the Credit Management Research Centre, University of Leeds Business School

end of the year compared to just over half a million in

2004.

Registry Trust estimates that around 70% of judgements

are ‘credit related’ the remaining 30% being for unpaid tax,

utility bills and motor tax. Interviews with major lenders

found that county court action in order to gain a ‘charge on

the assets’ of a debtor were becoming common practice.

The Credit Industry Fraud Avoidance System (CIFAS)

report an escalation in fraudulent behaviour in the use of

financial products. Recent data released by CIFAS

(October 2007) suggests that fraud trends continue

upwards. Application fraud increased by 23% from 2006-7

with 57,321 detected cases reported to CIFAS and identity

fraud, although slightly down had 57,302 reported cases.

Recent international banking regulations (Basle II

agreement) have drawn much attention to the re-evaluation

of consumer credit risk (default probabilities) and portfolio

risk management. The Basel II rules have given an

impetus to banks to move debt more quickly from their

books to external debt collection agents and debt buyers.

1.2 Commercial Lending and Insolvency

There has been a trend increase in the number of active

companies registered with Companies House. The stock of

active businesses approached 2.3 million in 2006.

According to Companies House the number of new

incorporations has been growing rapidly year on year e.g

43% 2003-6. In total, unincorporated businesses and

SME’s account for a significant proportion of the business

stock. This is estimated to have grown by more than 1.4

million since 1980. The stock of small businesses is

estimated at 3.8 million. SME’s account for 52% of

aggregate business turnover and 56% of private sector

employment according to the SBS.

The number of company insolvencies (compulsory and

creditors’ voluntary liquidations) in the England and Wales

was 3,194 in the last quarter of 2006, nearly half of the

figure that was observed in the third quarter of 1992.

Although the trend fluctuated around 3,500 insolvencies

per quarter between 1995 and 2007, the figures have been

much lower than the levels of the early 1990s’ recession.

The seasonally adjusted figures provided by the Insolvency

Service show 3,032 liquidations in the second quarter of

2007, representing a 4.2% decrease on one year ago.

A forecasting model of aggregate corporate insolvencies

shows that in the long term insolvency rate increases when

income gearing or real CCJ values increase, and when the

employment rate or real money stock decrease. The

Growth in Real Short Term Loans and Business

Confidence are the short-run dynamics of the insolvency

rate. That is, whereas short term increases in the growth in

real short term loans are likely to create short term

increases in the insolvency rate, short term increases in

business confidence are likely to create short term

decreases in the insolvency rate.

The relatively high levels of indebtedness in the corporate

sector coupled with recent interest rate increases and a

decline in business confidence suggest that corporate

insolvencies are set to increase by over 20% in the next 2

years. More recent data derived from an analysis of UK

Company accounts suggests that the ratio of total debts to

total assets has risen quite sharply since 2004.

When we analyse ratios reflecting the ability of firms to

cover their interest repayments on debt we observe a

similar rise since 2004. This suggests that there are a large

number of companies that are not generating sufficient

profit to cover their interest payments. The considerable

growth in private equity-backed leveraged buyouts has

Credit and Debt Management – 2008 Survey

9 Research and analysis by the Credit Management Research Centre, University of Leeds Business School

increased the role of debt in capital structures. It is

estimated that value of investments LBO’s in 2007 was

around £22 bn. Of course, financial distress and insolvency

in the corporate sector threatens jobs and household

income in an already fragile economy.

The late payment of commercial debt as a phenomenon is

enduring. The CMRC Quarterly Review monitors payment

behavior across a sample of 2000 enterprises. Accounts

which pay at or near the due date are currently reported at

54% by sales value. This leaves 46% of all sales accounts

being reported as overdue by our panel of respondents. In

terms of the number of customer accounts, the proportion

of customers paying at or near the due date is slightly

lower. 46% of our survey panel state that customers at an

account level pay on time. This equates to 54% of all

customer accounts currently being paid late. Recent survey

statistics show a deterioration in B2B payment behavior.

This trend is likely to continue since smaller firms rely

increasingly on trade credit when bank credit is restricted.

The Late payment of Commercial Debts (Interest) Act has

had an impact of the extent of outplacement to the DCA

sector. The fact that DCA’s can impose an interest charge

and recover some collection costs has made out-placing

debt more cost effective for the commercial sector and

particularly SME’s. 1.3 Debt Collection Agents and Debt

Sale

A number of trends and industry dynamics have impacted

on the out-placed debt collection and debt purchase sector.

These include: the surge in consumer debt and increase in

the volumes of delinquent debt that have to be processed;

the increased emphasis on cost effectiveness and

performance benchmarking; the continued re-engineering

of centralised in-house collection and recovery functions

and the development of technology and information

systems devoted to account management; the speed of

response of the major lenders in dealing with delinquent

accounts and a shortening of the time period to write-off.

Basel II rules have encouraged the lenders to shift debts off

of their books more quickly and to opt for debt sale rather

than commission-based collection since the former

mechanism transfers ownership of the debt.

The Credit Services Association reported that their member

organisations handle around £15 billion of debt on a

commission basis which consisted of over 20 million

individual cases. This represents a rise of £10 billion since

2000. The CSA membership bought around £6 billion of

debt in 2007 making of total of over £21 billion being

passed to the DCA sector. The CSA estimate that their

market will be worth over £24 billion in 2008.

A source of potential revenue growth for the DC industry

is as a provider of a wider range of out-sourced business

services across the credit life-cycle. Outsourcing

receivables management has increased, particularly for

commercial debt. Government and the public sector are

beginning to utilise the services of DCA’s. The growth in

the internet B2C and B2B has translated into more

collection activity on a global scale.

There has been and continues to be a general trend

amongst the large volume collectors to streamline and

rationalise their use of 'external' collection agents alongside

their 'in-house' collection agents. Debt Collection Agents

have turned to buying debt as an alternative to collection

on commission in 2004 there were over 60 debt buyers

although the DBSG suggests that currently there are

around 40 regular buyers in the market. The growth in the

market has been facilitated by the supply-side.

Credit and Debt Management – 2008 Survey

10 Research and analysis by the Credit Management Research Centre, University of Leeds Business School

In the UK it is difficult to estimate the total size of the debt

sale market since the market continues to evolve quite

rapidly. The market size in 2005/6 was around £6bn face

value selling at an average price of around 8p in the pound.

By 2006/7 this had increased to £7bn and commentators

are expecting the market to peak at around £10bn. Debt

sale is still dominated by ‘distressed debt’ portfolios i.e.

debt that the financial sector would normally write-off

and/or is severely delinquent is sold to the highest bidder

for collection/recovery. It is clear that lenders have

developed an interest in selling younger debt as a means of

improving cash-flow and because of the costs of servicing

the debt collection sector when debt is placed on a

commission basis.

The major lenders and the majority of financial services are

now selling debt and developing specialist departments to

deal with debt sale and respond faster to debt sale

opportunities. The bulk of sales are distressed debt which

can attract only 2-5% of face value but there is evidence of

sellers selling debt earlier, as in the US, typically 90-180

days past due. The changes in accounting rules, Basel II

and resultant changes in internal default definitions and

capital requirements have had an impact on the propensity

of lenders to sell debt. A further development is the sale of

debt that has already been managed to achieve an

‘arrangement to pay’ via a debt management company.

This type of debt can attract 30-40 pence in the pound. The

development of a reseller market is expected to create

further growth in the market.

The main sources of debt sale are credit cards, loan and

overdrafts, retail credit, motor finance and increasingly

mortgage arrears. Further growth in the Debt Purchase

market is likely to come from the sale of non-delinquent

receivables, reselling and from commercial debt.

A problem that is probably hampering the growth of the

debt sale market is that of ‘pricing’. Interviews with major

lenders suggested that there is some lack of ‘trust’ in the

market as a result of extant price variations. If debt is to be

sold at earlier stages and /or segmented by ‘quality’ then

there has to be a mechanism for pricing the individual

debts and the debt portfolio. The development of a ‘broker’

market for debt sale and purchase has provided some uplift

in prices. 1.4 Survey of DCAs In terms of Debt Collection services offered by agencies in

2007 significant differences can be seen since 2003 in

Repossessions (up 25%) and Tracing (down 15%), The

offering of Process Services and Investigations/Status

Reports has declined between the two time periods. The

largest difference between services offered in 2003 and

2007 is in Debt Purchase which is up by 27% among the

sample. 46% of all agencies offer this service in the

marketplace.

The statistics suggest a healthy growth in the market for

debt collection with 75% of agencies indicate that market

size is increasing in 2007. This compares to just 45% in

2003. 99% of agencies believe market competitiveness to

be increasing.

The number of debts worked by agencies each month

across the entire sample has increased dramatically from

between 1,200 in 2003 to 19,000 in 2007. Among the

larger agencies this increase is most significant with

agencies with over 100 employess reporting a rise from

1000 debts per month to 40,000 debts per month. Overall

in the sample, the average value of a debt placed across the

Credit and Debt Management – 2008 Survey

11 Research and analysis by the Credit Management Research Centre, University of Leeds Business School

entire sample has increased from less than £1000 in 2003

to £2400 in 2007.

There appears to be growth in a number of sectors. The

sectors that are generating a faster growth for the out-

placed debt industry are the fixed line telephone sector and

broadband providers. Collections within the retail sector

show the second largest growth among respondents with

85% of collection agents indicating this to be a growing

market. The credit card industry has continued to grow

with 72% of respondents indicating this to be a growth

market.

In 2003 43% of respondents thought that the quality of out-

placed debt was generally worsening. This figure in 2007

is 51% in the sample. 18% of respondents indicated that

the quality of consumer debt was improving.

Over 60% of collection agents generate their business from

under 50 clients and generally collection agents are dealing

with fewer clients than in 2003.

The largest buyer of debt purchased a face value of £458

million compared to just £28 million in 2003. Of the total

debt purchased in 2007 an average of £30 million was

collected during the last year.

In the sample prices paid for debts varied between 5p to

18p in the pound. The average price paid in the pound is 8p

in 2007.

The collection agents were asked if any of their collectable

debts were operating under an Individual Voluntary

Arrangement. 78% of the agencies responding to the

survey had accounts which were linked with an IVA.

The average length of time for an IVA is among the sample

is 4.75 years. Agents also indicated that they expect to

receive 38p in the pound under an IVA and would accept a

minimum of 32p.

In terms of default rates collection agents were asked to

state the the percentage of IVAs which had defaulted over

the last 3 years. The default rate has more than tripled

during the last three years and now stand at 13%.

1.5 Large Volume Debt Management

Organisations faced with large volume debt management

operations are setting up sophisticated customer focused

operations aimed at 'reforming' debtors, if possible, so that

the relationship with them can continue and generate future

profits. This has been partly a response to increased

competition amongst lenders, the emergence of

'consolidation companies' and recognition that changing

life-styles and patterns of work have precipitated periods of

'over-commitment' by debtors which need be managed

longer-term.

The introduction of enterprise wide data sharing has arisen

because of the emphasis being placed on having a

'customer-level' and/or ‘customer-life cycle’ view of each

customer and detailed management information systems.

The expansion of data-sharing closed user groups in the

UK and the development of ‘indebtedness indices’ means

that lenders have access to better information on other

lenders experience of a debtor, and can include this in their

decision making process. The differences in information

costs of in-house and out-placed debt collection are thus

reduced.

Collection cycles have become much shorter in financial

services but opened opportunities for debt buyers. Basel II

rules have resulted in reclassification of debtor portfolios

in financial services with the development of new default

Credit and Debt Management – 2008 Survey

12 Research and analysis by the Credit Management Research Centre, University of Leeds Business School

probability models. Internally lenders have moved to a

‘time-based’ rather than ‘event-based’ view of the debtor

and emphasise re-aging or rescheduling debt away from

collections and back into account management where

possible and transferring ownership of delinquent debt.

The centralisation of collections activity in organizations

has produced an environment in which more sophisticated

decision support systems including statistical and

propensity models, such as behavioural/collection scores,

can be used to formulate the most effective collection

strategies by encapsulating the company's previous

experience of what works for customer segments and

creating variability in collection sequences. A range of

propensity models are employed to score the propensity to

‘self-cure’ (i.e. the customer will pay without being

chased) through to the likelihood of successful litigation.

Champion challenger methodologies coupled with activity-

based costing facilitates the evaluation of collections

effectiveness.

Sophisticated credit management in-house will inevitably

reduce the 'quality' or 'collectibility' of debt that is out-

placed. Many debts passed to debt collectors will already

have been through telephone and letter based collections

procedures, and may even effectively have already been to

one debt collector, if the company has a debt collection

subsidiary. In future it may be that such firms will only

want to make use of a sub-set of the debt collectors service

which they cannot provide for themselves, for example

outsourced services through to door-step collection.

A trend towards using debt sale as an alternative to

commission-based collection and using fewer agents with

closer contact and integrated information systems suggests

that there will continue to be rationalization with

fewer/larger and more sophisticated collection agents/debt

buyers in the future. A increasing role for debt brokers is

expected to increase the scale of the broking market.

Credit and Debt Management – 2008 Survey

13 Research and analysis by the Credit Management Research Centre, University of Leeds Business School

2. An Overview of Consumer and Corporate Lending

In this section, we analyse the main trends in consumer

lending in the UK by examining aggregate time series

statistics. First, we provide a categorisation of the types of

lending activities by the major financial institutions and the

corporate sector.

2.1. Categories of Lending

The following table (2.1) adapted from Key Note Ltd

attempts to list all the categories of lending in the economy

by the source (lender) and ultimate borrower (debtor).

The banks, building societies, finance houses, retailers,

local authorities and insurance companies make various

forms of lending to both commercial and personal

borrowers.

Commercial organisations extend trade credit to their

commercial customers and may make sales on deferred

payment basis or credit accounts to individual households

(e.g. Utilities, Cable TV). These debts are the potential

source of business for the 'out-placed' debt collection

industry.

Lender Class of Lending Debtor(s) Banks & Building Societies Commercial Other financial institutions Commercial Industrial & Commercial Organisations Personal Secured on Dwellings Personal Consumer Credit, including Credit cards Personal Unincorporated and non- Profit-making bodies Finance Houses Personal Secured and unsecured revolving credit Commercial Motor finance Personal Motor finance Retailers and finance houses Personal Retail instalment lending Personal Store and credit cards Personal Mail order credit Local Authorities Personal Various Insurance companies and others Commercial Various Industrial and Commercial Commercial Trade Credit – on invoice Businesses Business to Business Personal Sales on deferred payment (utilities, cable & satellite TV) Source : Adapted from Key Note Ltd

Table 2.1 – Categories of Measurable Lending in the UK (Source: Keynote Ltd)

Credit and Debt Management – 2008 Survey

14 Research and analysis by the Credit Management Research Centre, University of Leeds Business School

2.2. An Overview of Consumer Lending and Indebtedness: Trends

The growth in household debt, both in absolute terms and

relative to household income, continues to cause some

concern. Much of the growth in consumer debt has

occurred within a confident economy with economic

growth, high levels of employment, growing asset prices,

easy access to credit and low interest rates and inflation.

Despite obvious signs of some financial stress within the

household sector most households have managed to service

their debts. The economic climate appears to be changing:

financial markets have highlighted the potential fragility of

some lending portfolios that appear to be riskier than was

anticipated; lenders have tightened credit policies and

borrowers are becoming more cautious; interest rate rises

are impacting on both the household and corporate sector;

confidence in the housing market continues to falter; oil

prices are rising. Servicing debt may become more

problematic for a larger proportion of the UK household

sector particularly as mortgage repayments rise and the

opportunities for refinancing and restructuring current debt

decline with the tightening of lender credit policies.

‘Trading out of trouble’ and’ buying time’ are not going to

be options. Any uncertainties about future income and

property values exacerbates the problem.

It is estimated that consumer credit has been rising by over

to £1 billion per month with total outstanding debt in the

region of £140 billion in 20071

. Households owe sums

equivalent to 160% of income2

. Since 2000, consumer

credit and debt has been the subject of several high profile

government investigations and regulatory initiatives. The

accumulation of household debt, defaults and arrears has

made headlines in the UK and other OECD economies. In

the UK, the “Task Force on Over-indebtedness” has

produced reports that raise many issues relating to lending

practices, risk management, debt management and social

policy. Initiatives and issues relating to Sub-prime lending,

‘Affordable Lending’, The Survey of Low Income Families

and ‘Credit Constraints’ have attracted some prominence

in government. The Competition Commission’s

investigation into the lack of competition in the ‘Home

Credit’ market highlighted asymmetries in available

consumer-level information and the pricing of sub-prime

products. The Data Protection Act raised many issues and

problems for consumer lenders. Recent international

banking regulations (Basle II agreement) have drawn much

attention to the re-evaluation of consumer credit risk

(default probabilities) and portfolio risk management. The

Basel II rules have given an impetus to banks to move debt

more quickly from their books to external debt collection

agents and particularly debt buyers.

At the consumer level, there are increasing signs that many

households are struggling to service their debts judging by

the growth in the use of private sector and voluntary sector

debt management services. The record levels of personal

bankruptcies, as well as the steady rise in the indebtedness

of households, the dramatic increase in the number of fraud

cases, and excessive bad debt losses have prompted the

industry, as well as the government, to once again examine

the fundamentals of the consumer lending business.

Gauging the extent of the ‘household debt problem’

requires balancing the evidence provided by objective data

from national statistics and the Bank of England with the

vast amount of quasi-subjective information provided by

debt advice groups, lobbyists and surveys of the opinions

of debtors and lenders. In the next section we examine the

statistics.

Credit and Debt Management – 2008 Survey

15 Research and analysis by the Credit Management Research Centre, University of Leeds Business School

2.3. Consumer Credit and Indebtedness

The rise in household debt in Britain gained headlines in

2005 when, for the first time, it rose to over £1trillion. By

the first quarter of 2007, the level of outstanding debts was

around £1.4 trillion.3

This total figure includes secured

lending, the majority of which is first mortgages and

additional ‘equity release’. This amounts to around 80% of

the total consumer lending4

. Unsecured lending, or

‘consumer credit’, however, has grown rapidly over the

past decade, directly related to the growth in the number

and type of credit card products available to consumers.

Increased competition in financial services has fuelled the

increase in available credit products and the degree of

product differentiation. Lenders are concerned to cover all

segments of the personal credit market from ‘platinum’ to

‘sub-prime’ with offerings tailored to attract all types of

borrowers and interest rates (APR’s) priced to reflect the

differing risks in each segment. The scramble for market

share has led to a considerable increase in ‘balance

transfer’ activity where consumers are offered low or zero

interest rates for a period of up to 12 months if they

transfer the outstanding balance from one card to a

competitor. Moreover, the increased availability of credit

products and the competition for customers has facilitated

a sizeable market for the ‘restructuring of debts’, i.e.

moving debts to lower interest rates (balance transfers) or

more typically, extending the time period of the debt with

lower monthly repayments but, ultimately, at a

significantly higher rate (consolidation loans).

2.3.1. Survey and Subjective Evidence

There has been much, often alarming, press and media

coverage that suggest something of a crises in household

finances.

These headlines are often fuelled by surveys of individuals

that are in ‘financial difficulty’ and the apparent increase in

debt related problems being reported to counsellors, debt

advice groups, the Citizens Advice Bureau and various

consumer lobbies.

In early 2005, lenders saw a surge in payment arrears,

particularly, but not exclusively, on unsecured lending

products. The Financial Services Authority, in its Financial

Risk Outlook5

, reported that average outstanding balances

on unsecured debt had increased quite substantially for a

large proportion of households. They suggested that around

53% of households had average unsecured debts of £7,065.

The average balance on secured debts was reported as

£67,662 for around 40% of households. There were, at the

time, reported cases where individuals had over £100,000

of outstanding credit card debts set against annual income

levels of around £20,000 and examples of relatively low

income individuals who had large unsecured debts spread

across as many as 20 different credit card lines6

.

A survey by the National Consumer Council7

, in 2007,

concluded that the majority of households are managing to

service their debt commitments. They suggested that 57%

of households have no problems in meeting financial

commitments, that 31% ‘struggle’ from time to time, that

12% have difficulty managing their commitments and that

a subset of 1.6% of households are in serious difficulties.

Converting these figures into numbers of

households/individuals, 3 million are struggling to keep

payments up to date; 1.5 million are falling behind with

payments; and 0.5 million are in serious financial

difficulty, i.e. serious arrears. The trends were of concern.

The NCC suggested that mortgage arrears had increased

4%; repossessions had increased 32%; credit cards arrears

had increased 8.5% from an already high level; and contact

Credit and Debt Management – 2008 Survey

16 Research and analysis by the Credit Management Research Centre, University of Leeds Business School

with advice agencies and debt management plans had

increased by 43% and 48% respectively. A survey in 2006

by the Citizen’s Advice Bureau, “In Too Deep” analysed

567 cases of debtors seeking advice. They suggest that

“debt is a continuing and often debilitating problem for an

increasing number of people, with its effects often felt

most strongly amongst the most vulnerable members of

society”. The CAB report an average increase in household

debt of 30% between 2003 and 2006 with the average

outstanding of over £13000, twice the figure reported by

the FSA. Debts were, on average, 17.5 times the average

monthly income. The majority of individuals in the survey

were young (25-44) and single.

The average household debt reported by Creditaction8

in

November 2007 was £8,681, which rises to £20,189 if only

households with some unsecured debt are included in the

denominator. The average outstanding mortgage was

reported as £98,571.

A recent report suggests the number of house repossessions

have increased 50% in the last year to around 45,0009

. As

borrowers reach the end of fixed interest deals taken out

when interest rates were low, the number of repossessions

could well increase further. New mortgage lending has

fallen rapidly along with activity in the housing market.

Most of the major lenders have reported increases in bad

debts in the period 2005-7. Calls to the National Debt line

have more than doubled since 2005 and stand at more that

300,000 per year. The CAB10

reported that 1.7 million

people sought debt counselling last year; 40% of whom

had credit card and unsecured debt problems. They

reported a 30% rise in cases of individuals struggling to

pay energy bills. There is considerable evidence of

households ‘juggling’ finances via balance transfer, the use

of loan consolidation products, making payments on

instalments of secured credit agreements with unsecured

credit (e.g. mortgage payments with credit card cheques).

Chart 2.3.1.1 – Debt Client Characteristics 2006

(source: Citizens Advice Bureau Survey 2006)

Credit and Debt Management – 2008 Survey

17 Research and analysis by the Credit Management Research Centre, University of Leeds Business School

Attractive refinancing deals are currently harder to find as

lenders tighten credit policy and interest rates rise. The

Credit Reference Agency, Experian11

last month reported

that 8.2 million individuals are in serious debt; 2.1 million

are struggling with repayments; 2.5 million are concerned

about their ability to manage debt; and 2 million do not

know the extent of their debts.

2.3.2 Statistical Evidence

In the UK, the most recent statistics suggest that the value

of consumer credit outstanding on mortgage loans exceeds

£1150bn and around £215bn is outstanding on other forms

of consumer credit (Bank of England, 2007). The trend in

consumer credit (excluding mortgages) has shown a

substantial growth, particularly since 2000. Consumer

credit is defined as borrowing by consumers, i.e. the

household sector excluding sole proprietorships,

partnerships, and non-profit making bodies, to finance

current expenditure on goods and services. Figures from

the Central Statistical Office (on the value of consumer

credit outstanding) suggest over £215 billion outstanding

on forms of consumer credit. These figures exclude credit

where the balance has to be paid off at the end of each

period such as utility bills, but will include balances on

credit cards which are paid off on a monthly basis and

therefore do not, in the strictest sense, represent credit. The

services provided by the utilities, which are often on a

deferred payment basis, represent a sizeable proportion of

total consumer debt.

Chart 2.3.1.2 below shows the strong trend increase year

on year in consumer credit from 1994 to 2007. As the chart

illustrates, the 1980s saw a consumer credit boom; between

1979 and 1989 the volume of consumer credit outstanding

(excluding mortgages) more than doubled, and there was a

similar movement in the amount outstanding on mortgage

loans. Wilson and Summers (1998) suggested various

factors contributed to this, including:

• High inflation in the late 1970s and early 1980s. This

made buying on credit more attractive when compared

with saving for consumer goods, and also had a

negative effect on attitudes to saving which continued

even when inflation dropped;

• The de-regulation of financial markets and controls on

hire purchase;

• The 1986 Financial Services Act in the UK and

similar trends across Europe, which allowed building

societies to compete with banks, and changes in the

regulation of building societies allowing them to get a

higher percentage of funds from sources other than

their members;

• An increase in divorce rates across Europe which has

left more families needing credit to cope financially;

• Government policies encouraging home ownership.

Since 1994, however, the total amount of consumer credit

outstanding (excluding mortgages) has almost quadrupled.

Much of this increase has arisen in the credit and retail card

market. Competition has been fierce in the UK plastic card

market. It has been reported that there are over 1300

different credit cards in the UK (standard, gold, charity,

affinity, co-branded etc) with around 33 card issuers

including the major banks. Estimates suggest that there are

over 75 million credit and debit cards in circulation with

amounts outstanding around £67.25 billion12

. The credit

card market experienced unprecedented levels of

competition largely as a result of new entry by US issuers

that dramatically increased the choice of card rates and

benefits. The trend growth in consumer credit appears to

have slowed in 2007-7.

Credit and Debt Management – 2008 Survey

18 Research and analysis by the Credit Management Research Centre, University of Leeds Business School

The growth in credit outstanding is clearly closely linked to

the level and growth in consumer spending over the time

period. The chart to the right demonstrates the continued

and strong growth in consumer spending in every period

since 1994 and a continued but slowing growth in 2007.

In the context of total consumer borrowing, credit card

debt forms only 4%, with mortgages and personal loans

having the major share.

The chart to the right shows the relative shares of lending

broken down as secured (mortgages) and unsecured (cards and

unsecured loans) over the recent period. Thus, the growth in

debt is associated predominantly with asset accumulation and

house price growth rather than consumer spending.

0

50

100

150

200

250

Consumer Credit Outstanding(excluding mortgages)

‐4%

‐2%

0%

2%

4%

6%

8%

10%

1984

1985

1986

1987

1988

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

Consum

er Sp

endin

g y‐on‐y

Consumer Spending Growth

Mortages

Credit Cards

Loans etc84%

12%4%

Total Personal Debt – £1.355 bn, July 2007

0

5 000

10 000

15 000

20 000

25 000

30 000

total

secured

consumer

Total Lending to Individuals Per MonthAugust 2005 –August 2007

Totals Outstanding £ 1364742 (100%)secured £ 1150247 ( 84%)consumer £ 214495 ( 16%)

Chart 2.3.1.2 – Consumer Credit Outstanding

(source: Bank of England)

Chart 2.3.1.3 – Consumer Spending Growth

(source: Bank of England)

Chart 2.3.1.4 – Total Personal Debt July 2007

(source: Calculated from Bank of England statistics)

Chart 2.3.1.5 – Total Lending to Individuals Per Month

(source: Bank of England)

Credit and Debt Management – 2008 Survey

19 Research and analysis by the Credit Management Research Centre, University of Leeds Business School

A notable feature borrowing in recent periods, since around

1998, is the extent of mortgage equity withdrawal as a

source of borrowings. This primarily concerns releasing

funds tied up in property for expenditure outside of the

housing market (i.e. not used for house purchase of home

improvements). The considerable growth in property prices

since 2000 has created significant amounts of ‘equity’

relative to initial mortgage. The figures in Chart 2.3.1.6

below examine the total additional amounts borrowed

against properties and the percentage of disposable income

withdrawn against existing equity and reveals a marked

upward trend throughout the period and, after a sharp

decline in 2005, further growth in 2006/7. Clearly,

households have been able to finance consumption (and

unsecured debt re-payments) on the back of rising house

prices during this period.

As a percentage of disposable income Chart 2.3.1.7 shows

a sharp upward trend since 1998, reaching almost 9% by

the end of 2003. The previous high of 7.7% in 1988

coincides with the beginning of the last major UK

recession. The sharp decline in 2005 coincides with a

tightening of credit policy amongst the major lenders as a

result of record high levels of arrears on credit products at

the beginning of 2005. However, the growth in equity

release in relation to income continued to grow in 2006,

reaching 7% at the end of 2006, but has fallen again in

2007 to around 4.5%. This, however, is more likely to be a

supply constraint, as a result of the tightening of lending

terms, rather than a fall in demand.

‐5,000

0

5,000

10,000

15,000

20,000

1970 1988 1998 2003 2006

Mortgage Equity Withdrawal 1970‐2006 £m

‐2.0

0.0

2.0

4.0

6.0

8.0

10.0

Mortgage Equity Withdrawal as a % disposable income

1970 1988 1998 2003 2006

Chart 2.3.1.6 – Mortgage Equity Withdrawal 1970-2006 £M (source: Bank of England)

Chart 2.3.1.7 – Mortgage Equity Withdrawal as a % of Disposable Income (source: Bank of England/ONS)

Credit and Debt Management – 2008 Survey

20 Research and analysis by the Credit Management Research Centre, University of Leeds Business School

2.4. A Summary of Lending Trends

In this section, we report the more recent trends in lending

on secured and unsecured products that are reported by the

Bank of England.

2.4.1. Secured Lending

The latest data showed that the number of total approvals

for secured lending decreased again toward the end of 2007

after recovering from a bottom in January 2007 once again.

However, both the bottom and the top peaks failed to reach

the levels of the recent years up to 2004. This may well be

explained by the increased interest rates in 2004. Number

of UK Resident Banks’ sterling approvals and that of both

Building Societies’ and Other Specialist Lenders’ sterling

approvals have all followed the same trend with the

exception of their growth rates. Further increases in interest

rates coupled with a tightening of lending policies have

taken some effect.

The 12 month growth rates of the number of the total

approvals and UK Resident Banks’ approvals followed

almost the same route as expected from the majority share

of the banks in secured lending. Despite UK resident

banks’ majority and a negative growth rate (-0.5%), in

August 2005, building societies’ and other specialist

lenders’ positive rates (both around 15%) were enough to

make the total rate positive (4%) as well. However, UK

resident banks’ 12 month growth rate is also positive (3%)

in September 2005, which shows an overall rising trend.

However, this stabilized and has shown a steady downward

trend up to July 2007.

050

100150200250300350400450

Jan-

02

Jul-0

2

Jan-

03

Jul-0

3

Jan-

04

Jul-0

4

Jan-

05

Jul-0

5

Jan-

06

Jul-0

6

Jan-

07

Jul-0

7

UK Resident Banks Building Societies Other Specialist Lenders

Chart 2.4.1.1 – Approvals for Secured Lending to

Individuals (thousands) (source: Bank of England 2007)

-1.00000

-0.50000

0.00000

0.50000

1.00000

1.50000

2.00000

Jan-

03

Jul-0

3

Jan-

04

Jul-0

4

Jan-

05

Jul-0

5

Jan-

06

Jul-0

6

Jan-

07

Jul-0

7

Total UK Resident BanksBuilding Societies Other Specialist Lenders

Chart 2.4.1.2 – 12 Month Growth Rate of Secured Lending

Approvals to Individuals (source: Bank of England 2007)

Credit and Debt Management – 2008 Survey

21 Research and analysis by the Credit Management Research Centre, University of Leeds Business School

Similar trends could be observed on the values of

approvals for secured lending, with the other specialist

lenders’ increased share in recent years. Although the level

of numbers was relatively lower in 2005 than it was in

2003 and 2004, the level of values increased through 2006

and 2007 until the last quarter of 2007.

One of the main differences is that although the 12 month

growth rate of UK resident banks for number of approvals

was still negative in August 2005 (-0.5%).

This was the same rate of banks for value of approvals was

well positive even in July 2005 (2.5%) compared to the

negative July growth rates of building societies and other

specialist lenders (-15% and -0.8% respectively). The

growth of specialist lending shows a sharp peak in early

2006 compared to the other lenders since this peak all

trends show a steady decline with the Building Societies

being most pronounced.

0

5000

10000

15000

20000

25000

30000

35000

40000

Jan-

02

Jul-0

2

Jan-

03

Jul-0

3

Jan-

04

Jul-0

4

Jan-

05

Jul-0

5

Jan-

06

Jul-0

6

Jan-

07

Jul-0

7

UK Resident Banks Building Societies Other Specialist Lenders

Chart 2.4.1.3 – Monthly Value of Approvals for Secured

Lending to Individuals (source: Bank of England 2007)

-1

-0.5

0

0.5

1

1.5

2

2.5

Jan-

03

Jul-0

3

Jan-

04

Jul-0

4

Jan-

05

Jul-0

5

Jan-

06

Jul-0

6

Jan-

07

Jul-0

7

Total UK Resident BanksBuilding Societies Other Specialist Lenders

Chart 2.4.1.4 – 12 Month Growth Rate of Value of Approvals for

Secured Lending to Individuals (source: Bank of England 2007)

Credit and Debt Management – 2008 Survey

22 Research and analysis by the Credit Management Research Centre, University of Leeds Business School

Types of Lending

Approvals for House Purchase, Remortgaging and Other

Secured Lending have followed similar trends in recent

years, all having almost equal shares in the pie regarding

the number of approvals (112,000, 112,000 and 83,000

number of approvals in August 2005) that have remained

quite static until the fall in 2007. All types of lending see

the bottom peak in January typically.

In terms of the growth rates, remortgaging and other

secured lending follow nearly the same path unlike the

house purchase one.

However, the growth rates of all three have started to show

alike trends since the middle of 2004. Although all the

three rates had negative values in late 2004 and early 2005,

remortgaging had a relatively higher level. The sharp

upward trend in house purchase in 2006 has been followed

by a decline into negative growth rates in 2007.

0

50

100

150

200

250

300

350

400

450

Jan-

02

Jul-0

2

Jan-

03

Jul-0

3

Jan-

04

Jul-0

4

Jan-

05

Jul-0

5

Jan-

06

Jul-0

6

Jan-

07

Jul-0

7

House Purchase Remortgaging Other Secured Lending

Chart 2.4.1.5 – Monthly Number of Approvals for Secured Lending to

Individuals (source: Bank of England 2007)

-0.6

-0.4

-0.2

0

0.2

0.4

0.6

0.8

Jan-

03

Jul-0

3

Jan-

04

Jul-0

4

Jan-

05

Jul-0

5

Jan-

06

Jul-0

6

Jan-

07

Jul-0

7

House Purchase Remortgaging Other Secured Lending

Chart 2.4.1.6 – 12 Month Growth Rate of Number of Approvals for

Secured Lending to Individuals (source: Bank of England 2007)

Credit and Debt Management – 2008 Survey

23 Research and analysis by the Credit Management Research Centre, University of Leeds Business School

Unlike the similar shares for the number of approvals, a big

difference is apparent for the value of approvals. The share

of other secured lending was only around 8% in August

2005. House purchase and remortgaging had analogous

shares in August 2007, and after peaking in July 2007 a

sharp decline is evident.

Whereas the 12 month growth rates of House Purchase and

Other Secured Lending were negative from July 2004 (the

rate for Other Secured Lending was still negative in August

2005), the growth rate of remortgaging went up to a

positive by the end of 2005. It is also possible to notice

here that the rate of remortgaging did not see the negative

levels of house purchase and other secured lending in late

2004 up to mid 2007.

0

5000

10000

15000

20000

25000

30000

35000

40000

Jan-

02

Jul-0

2

Jan-

03

Jul-0

3

Jan-

04

Jul-0

4

Jan-

05

Jul-0

5

Jan-

06

Jul-0

6

Jan-

07

Jul-0

7

House Purchase Remortgaging Other Secured Lending

Chart 2.4.1.7 – Monthly Value of Approvals for Secured Lending to

Individuals (source: Bank of England 2007)

-0.6

-0.4

-0.2

0

0.2

0.4

0.6

0.8

1

Jan-

03

Jul-0

3

Jan-

04

Jul-0

4

Jan-

05

Jul-0

5

Jan-

06

Jul-0

6

Jan-

07

Jul-0

7

House Purchase Remortgaging Other Secured Lending

Chart 2.4.1.8 – 12 Month Growth Rate of Value of Approvals for

Secured Lending to Individuals (source: Bank of England 2007)

Credit and Debt Management – 2008 Survey

24 Research and analysis by the Credit Management Research Centre, University of Leeds Business School

Gross Lending

The amount of total sterling secured gross lending follows

the trend of value of approvals in a very similar way,

seeing the bottom in January and increasing towards the

summer. Overall, there has been a steady trend increase

since early 2005.

Repayments

In terms of repayments of secured lending, repayments on

redemption, regular repayments, and other lump sum

repayments had alike trends. Repayments on redemption

formed the majority of repayments of secured lending at

around 80% of the total repayments. The amounts have

increased 2 and a half times since 2002.

0

5000

10000

15000

20000

25000

30000

35000

40000

Jan-

02

Jul-0

2

Jan-

03

Jul-0

3

Jan-

04

Jul-0

4

Jan-

05

Jul-0

5

Jan-

06

Jul-0

6

Jan-

07

Jul-0

7

Chart 2.4.1.9 – Monthly Amount of Total Sterling Secured Gross

Lending to Individuals and Housing Associations (in sterling millions)

(source: Bank of England 2007)

0

5000

10000

15000

20000

25000

30000

Jan-

02

Jul-0

2

Jan-

03

Jul-0

3

Jan-

04

Jul-0

4

Jan-

05

Jul-0

5

Jan-

06

Jul-0

6

Jan-

07

Jul-0

7

Chart 2.4.1.10– Monthly Amount of Sterling Repayments of Secured

Lending by Individuals (in sterling millions)

(source: Bank of England 2007)

Credit and Debt Management – 2008 Survey

25 Research and analysis by the Credit Management Research Centre, University of Leeds Business School

2.4.2 Unsecured Lending

Unsecured gross lending trend is likely to move in a zigzag

manner, having the peaks in each December. Whilst credit

card lending has a top peak in December, other consumer

credit lending tends to have a bottom peak. Furthermore,

the level of the bottom peaks of other consumer lending

has an increasing trend unlike the top peaks of credit card

gross lending.

The trend of amounts outstanding of unsecured lending

shows little fluctuation over time. The amounts outstanding

of both credit cards and other consumer credit have

increased steadily except for a short decline in credit cards

in early 2003.

0

5000

10000

15000

20000

25000

Jan-

02

Jul-0

2

Jan-

03

Jul-0

3

Jan-

04

Jul-0

4

Jan-

05

Jul-0

5

Jan-

06

Jul-0

6

Jan-

07

Jul-0

7

0

50000

100000

150000

200000

250000

Jan-

02

Jul-0

2

Jan-

03

Jul-0

3

Jan-

04

Jul-0

4

Jan-

05

Jul-0

5

Jan-

06

Jul-0

6

Jan-

07

Jul-0

7

Chart 2.4.2.1– Monthly Amount of Total Sterling Unsecured Gross Lending

to Individuals (in sterling millions) (source: Bank of England 2007)

Chart 2.4.2.2– Monthly Amounts Outstanding of Total Sterling Net

Unsecured Lending to Individuals (source: Bank of England 2007)

Credit and Debt Management – 2008 Survey

26 Research and analysis by the Credit Management Research Centre, University of Leeds Business School

Despite the apparent zigzag shape, credit card repayments

have a rising trend over time with, however, a lower

growth rate recently.

Repayments-to-Amounts Outstanding ratio has started to

decrease since April 2004 and despite some sharp short ups

and downs it continues to remain quite static.

Both credit card and personal loan interest rates show

similar trends recently, especially in 2005. Both have a

decreasing trend very recently followed by a steady

increase from the start of 2004 to the second quarter of

2005. Regardless of the time, credit card interest rates have

had a slightly higher level than personal loan interest rates

in recent years up until July 2007 where they converged.

0

2000

4000

6000

8000

10000

12000

Jan-

02

Jul-0

2

Jan-

03

Jul-0

3

Jan-

04

Jul-0

4

Jan-

05

Jul-0

5

Jan-

06

Jul-0

6

Jan-

07

Jul-0

7

0

0.05

0.1

0.15

0.2

0.25

Jan-

02

Jul-0

2

Jan-

03

Jul-0

3

Jan-

04

Jul-0

4

Jan-

05

Jul-0

5

Jan-

06

Jul-0

6

Jan-

07

Jul-0

7

0

2

4

6

8

10

12

14

16

18

Jan-

02

Jul-0

2

Jan-

03

Jul-0

3

Jan-

04

Jul-0

4

Jan-

05

Jul-0

5

Jan-

06

Jul-0

6

Jan-

07

Jul-0

7

Credit Card Personal Loans

Chart 2.4.2.3– Monthly Amount of UK Resident Banks’

(inc. Central Bank) Sterling Credit Card Repayments by

Individuals (in sterling millions)

(source: Bank of England 2007)

Chart 2.4.2.4– Monthly Amount of UK Resident Banks’

(inc. Central Bank) Sterling Credit Card Repayments by

Individuals/Monthly Amounts Outstanding of Total

Sterling Net Credit Card Lending to Individuals

(source: Bank of England 2007)