Creating Shareholder Value Through Market Dominance Call/100300_20020918.pdf · Creating...

26

Creating Shareholder Value Through Creating Shareholder Value Through Market Dominance Market Dominance Presentation by Presentation by Mr. Mr. Sumant Sumant Sinha Sinha President President – – Corporate Finance, The Aditya Birla Group Corporate Finance, The Aditya Birla Group Kotak Kotak Securities’ Investor Conference, New Delhi Securities’ Investor Conference, New Delhi September 2002 September 2002

Transcript of Creating Shareholder Value Through Market Dominance Call/100300_20020918.pdf · Creating...

Creating Shareholder Value Through Creating Shareholder Value Through Market DominanceMarket Dominance

Presentation byPresentation byMr. Mr. SumantSumant SinhaSinha

President President –– Corporate Finance, The Aditya Birla GroupCorporate Finance, The Aditya Birla Group

KotakKotak Securities’ Investor Conference, New DelhiSecurities’ Investor Conference, New DelhiSeptember 2002September 2002

2

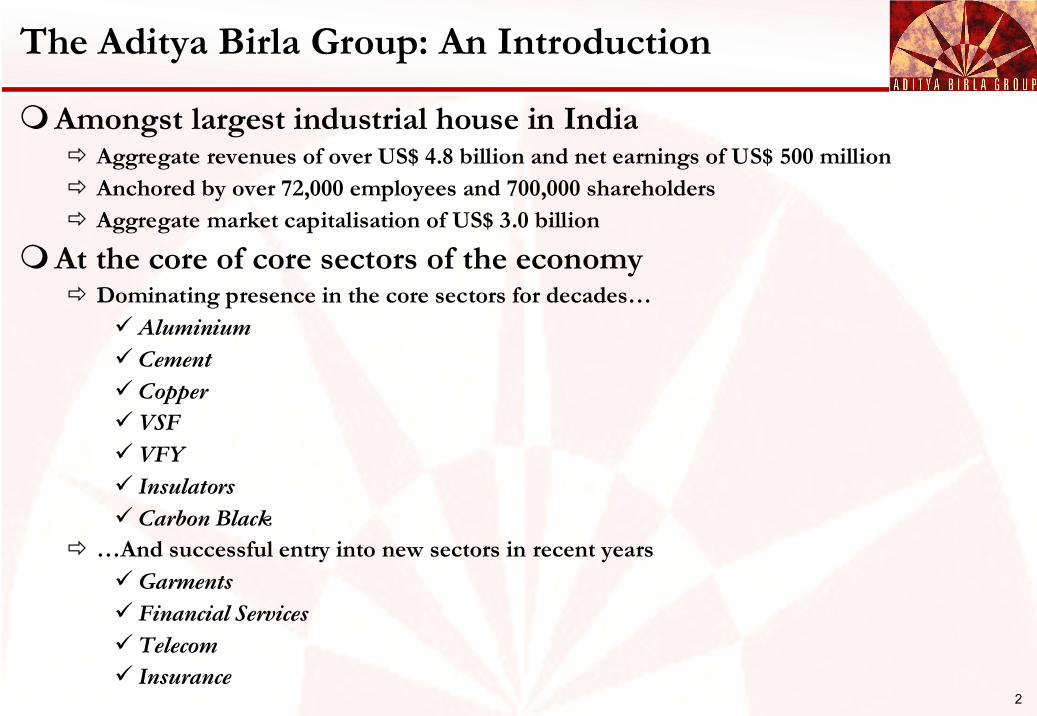

The Aditya Birla Group: An Introduction

Amongst largest industrial house in IndiaAggregate revenues of over US$ 4.8 billion and net earnings of US$ 500 millionAnchored by over 72,000 employees and 700,000 shareholdersAggregate market capitalisation of US$ 3.0 billion

At the core of core sectors of the economyDominating presence in the core sectors for decades…

AluminiumCementCopperVSFVFYInsulatorsCarbon Black

…And successful entry into new sectors in recent yearsGarmentsFinancial ServicesTelecomInsurance

3

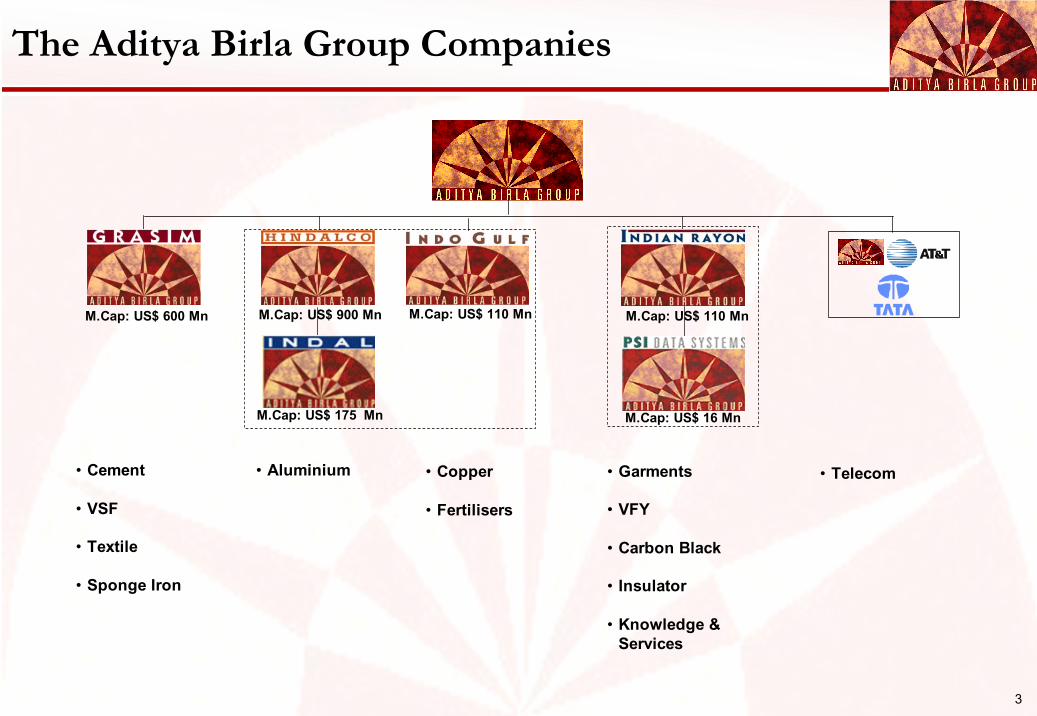

• Telecom• Cement

• VSF

• Textile

• Sponge Iron

• Aluminium • Garments

• VFY

• Carbon Black

• Insulator

• Knowledge & Services

• Copper

• Fertilisers

The Aditya Birla Group Companies

M.Cap: US$ 900 MnM.Cap: US$ 600 Mn

M.Cap: US$ 175 Mn

M.Cap: US$ 110 MnM.Cap: US$ 110 Mn

M.Cap: US$ 16 Mn

4

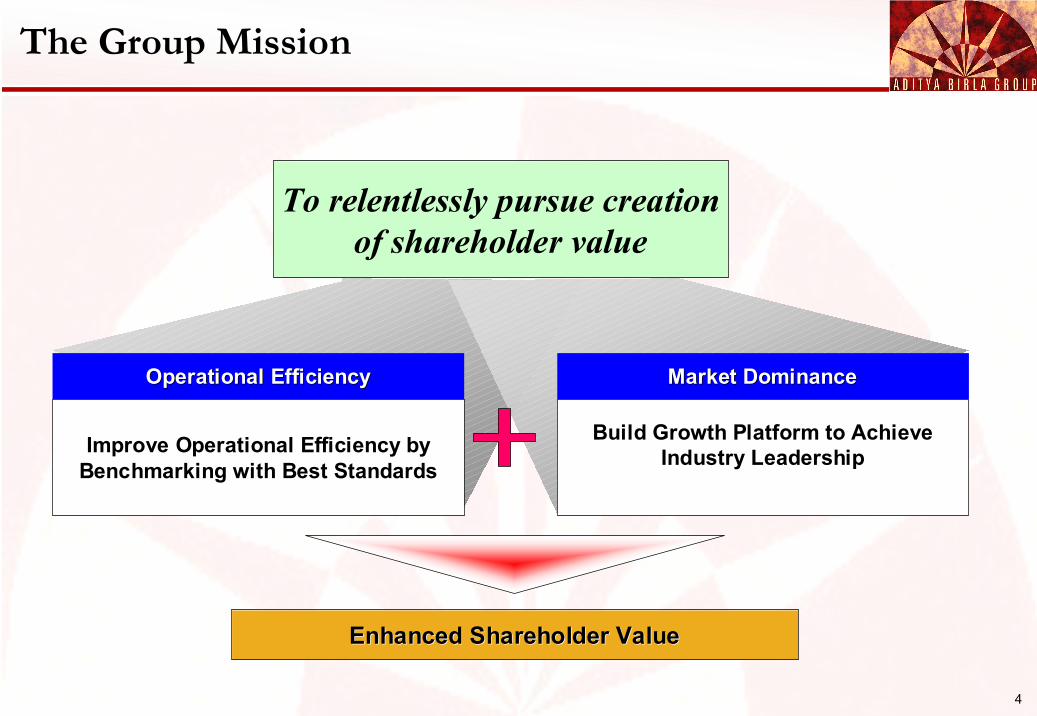

Enhanced Shareholder ValueEnhanced Shareholder Value

To relentlessly pursue creation of shareholder value

The Group Mission

Improve Operational Efficiency by Benchmarking with Best Standards

Operational EfficiencyOperational Efficiency

Build Growth Platform to Achieve Industry Leadership

Market DominanceMarket Dominance

5

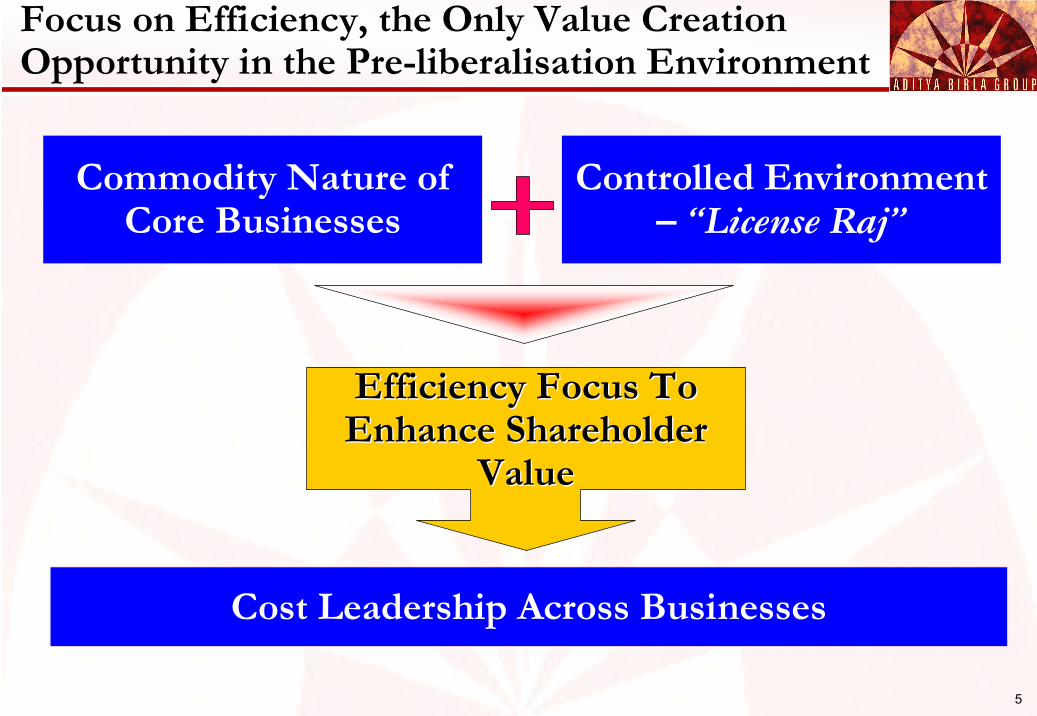

Focus on Efficiency, the Only Value Creation Opportunity in the Pre-liberalisation Environment

Controlled Environment – “License Raj”

Commodity Nature of Core Businesses

Efficiency Focus To Efficiency Focus To Enhance Shareholder Enhance Shareholder

ValueValue

Cost Leadership Across Businesses

6

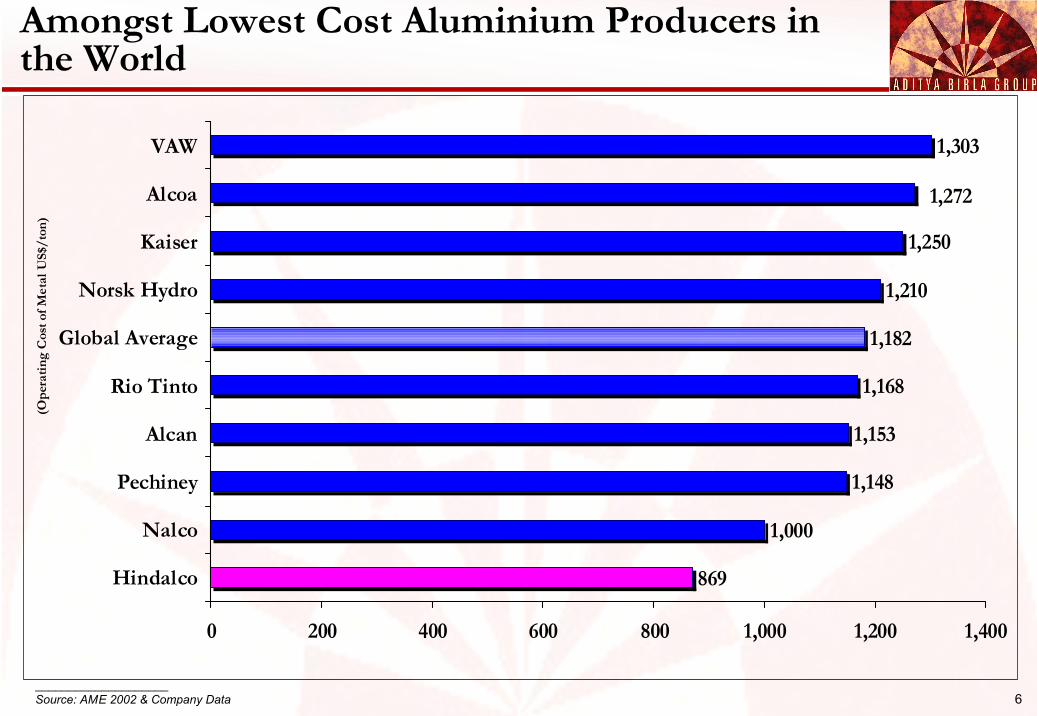

869

1,000

1,148

1,153

1,168

1,182

1,210

1,250

1,303

1,272

0 200 400 600 800 1,000 1,200 1,400

Hindalco

Nalco

Pechiney

Alcan

Rio Tinto

Global Average

Norsk Hydro

Kaiser

Alcoa

VAW

(Ope

ratin

g C

ost o

f Met

al U

S$/t

on)

Amongst Lowest Cost Aluminium Producers in the World

____________________Source: AME 2002 & Company Data

7

96

96.5

97

97.5

98

98.5

99

Birla C

oppe

rOns

anSa

ganose

kiPa

sarToy

oNor

ddeu

tsch

Harjav

alta

Huelva

Hurley

SAN

(%)

0500

100015002000250030003500400045005000

Huelva

Birla C

oppe

rHarj

avalt

aSa

ganos

eki

Toyo

Pasar

Onsan

Hurley

SAN

Nordd

eutsc

h

(MJ/T)

____________________Source: BROOK HUNT

____________________Source: BROOK HUNT

Globally Benchmarked Efficiencies in Copper

Metal RecoveryMetal Recovery Energy ConsumptionEnergy Consumption

8

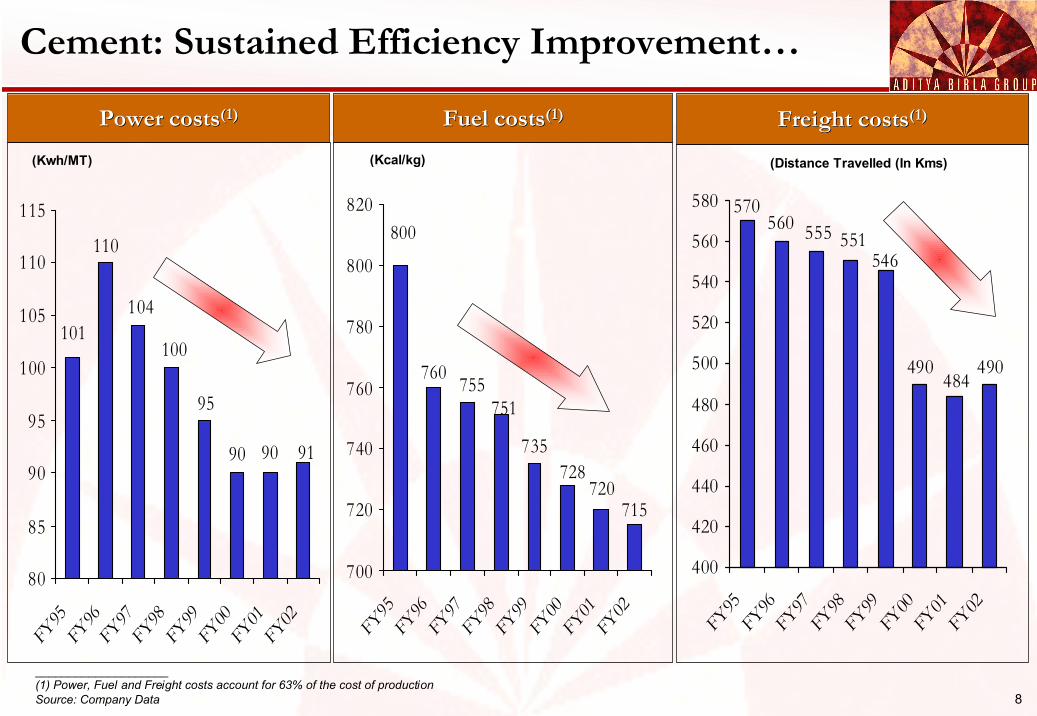

Fuel costsFuel costs(1)(1)

715720

728735

751755760

800

700

720

740

760

780

800

820

FY95FY

96FY

97FY98FY

99FY

00FY01FY

02

(Kcal/kg)

Power costsPower costs(1)(1)

919090

95

100

104

110

101

80

85

90

95

100

105

110

115

FY95

FY96

FY97FY98FY

99FY

00FY

01FY02

(Kwh/MT)

Freight costsFreight costs(1)(1)

490484

490

546551555560

570

400

420

440

460

480

500

520

540

560

580

FY95FY96FY97FY

98FY99FY

00FY

01FY02

(Distance Travelled (In Kms)

Cement: Sustained Efficiency Improvement…

____________________(1) Power, Fuel and Freight costs account for 63% of the cost of productionSource: Company Data

9

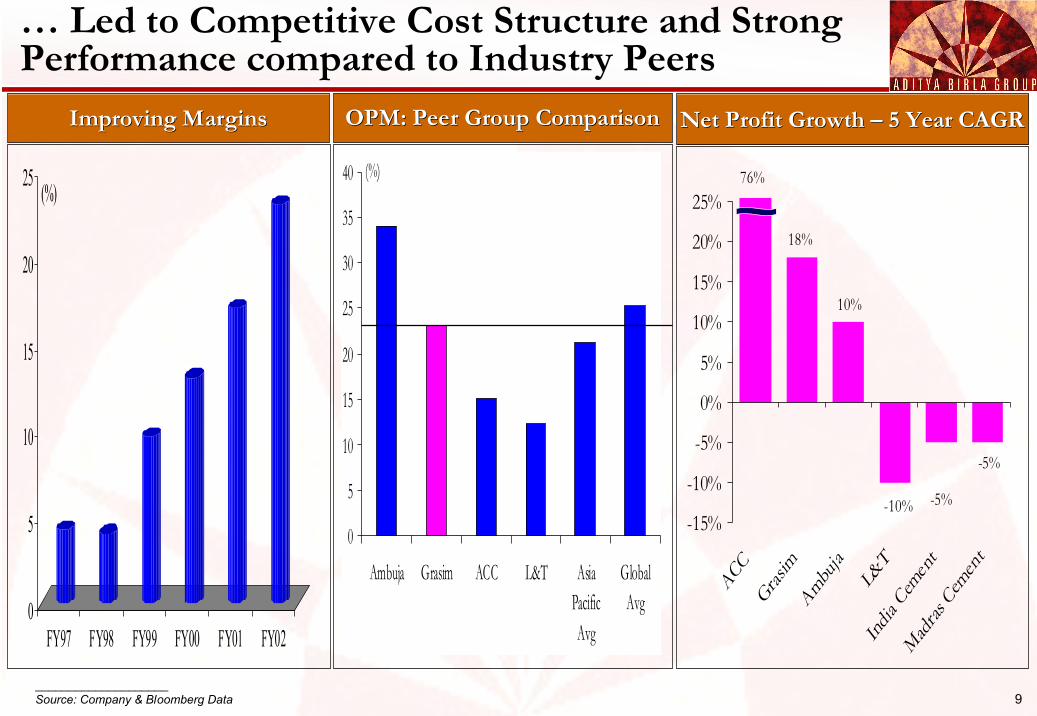

Improving MarginsImproving Margins OPM: Peer Group ComparisonOPM: Peer Group Comparison Net Profit Growth Net Profit Growth –– 5 Year CAGR5 Year CAGR

… Led to Competitive Cost Structure and Strong Performance compared to Industry Peers

0

5

10

15

20

25

FY97 FY98 FY99 FY00 FY01 FY02

(%)

0

5

10

15

20

25

30

35

40

Ambuja Grasim ACC L&T AsiaPacificAvg

GlobalAvg

(%)

-5%

-5%-10%

10%

18%

76%

-15%

-10%

-5%

0%

5%

10%

15%

20%

25%

ACCGras

imAmbu

jaL&

TIn

dia C

emen

tM

adras

Cem

ent

____________________Source: Company & Bloomberg Data

10

Need for Market Dominance Gaining Momentum

Market Market DominanceDominance

Commodity Nature of Commodity Nature of Core BusinessesCore Businesses

Industry Consolidation Industry Consolidation across sectors/regionsacross sectors/regions

Changing Changing Business Business

LandscapeLandscape

Intensifying Intensifying Global Global

CompetitionCompetition

Achieving market dominance will thus help in building growth plaAchieving market dominance will thus help in building growth platform to tform to deliver superior value for shareholders going forward…deliver superior value for shareholders going forward…

Several Proactive Measures Taken in Recent Years

to Achieve Market Dominance in Key Businesses

12

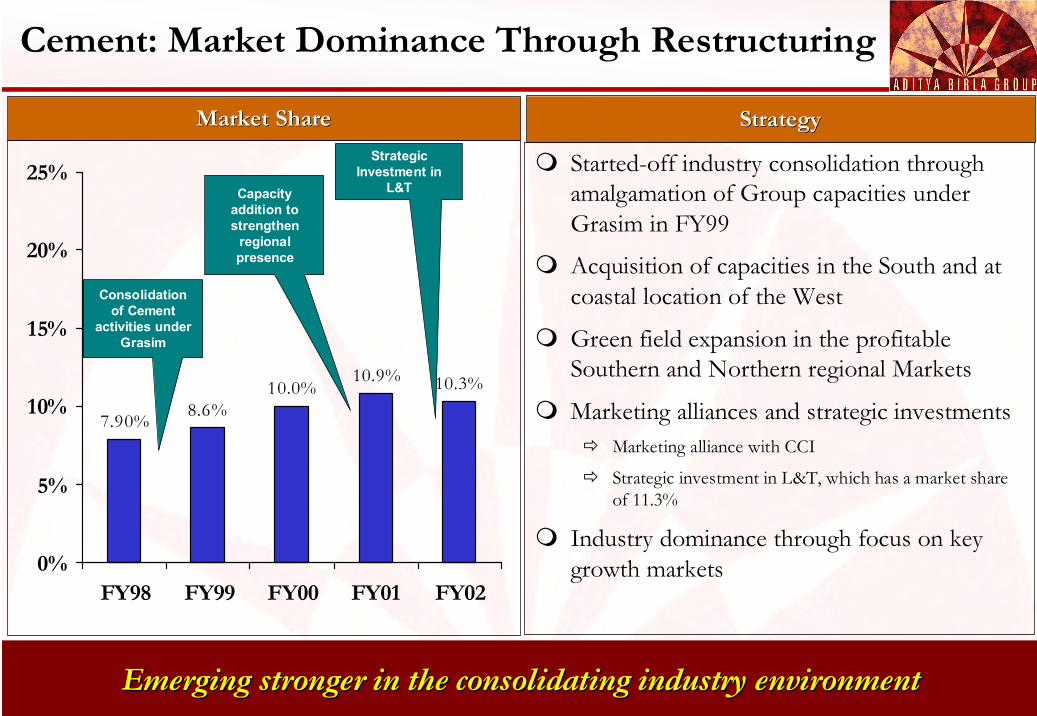

7.90% 8.6%10.0%

10.9% 10.3%

0%

5%

10%

15%

20%

25%

FY98 FY99 FY00 FY01 FY02

Consolidation of Cement

activities under Grasim

StrategyStrategy

Started-off industry consolidation through amalgamation of Group capacities under Grasim in FY99

Acquisition of capacities in the South and at coastal location of the West

Green field expansion in the profitable Southern and Northern regional Markets

Marketing alliances and strategic investmentsMarketing alliance with CCI

Strategic investment in L&T, which has a market share of 11.3%

Industry dominance through focus on key growth markets

Market ShareMarket Share

Capacity addition to strengthen

regional presence

Strategic Investment in

L&T

Emerging stronger in the consolidating industry environmentEmerging stronger in the consolidating industry environment

Cement: Market Dominance Through Restructuring

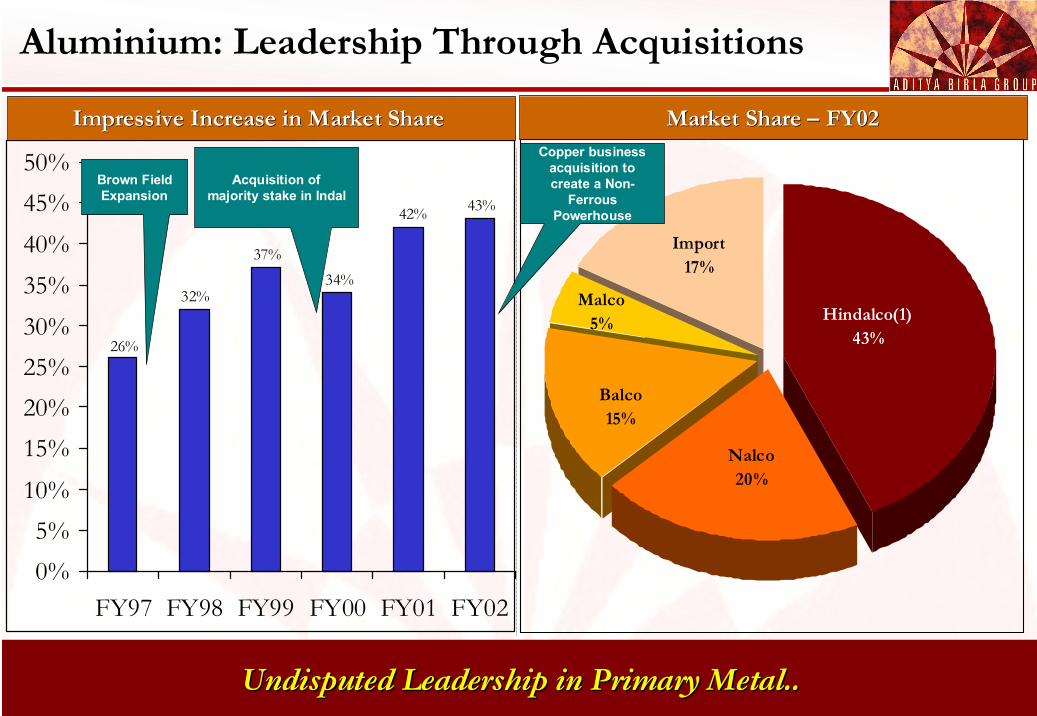

13Undisputed Leadership in Primary Metal..Undisputed Leadership in Primary Metal..

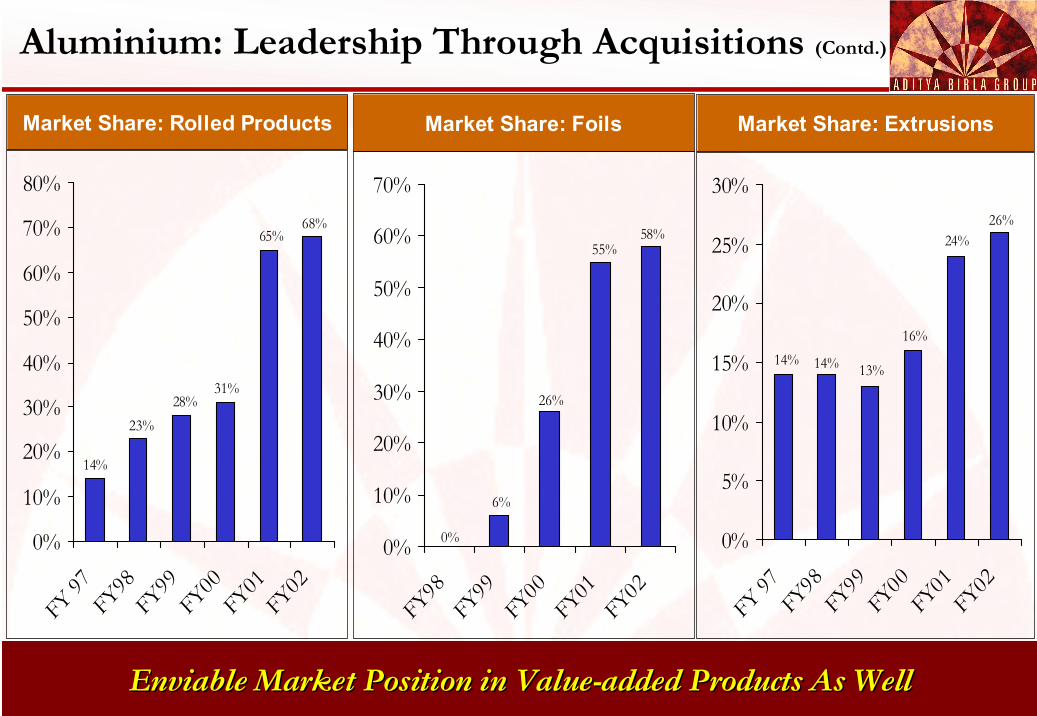

Aluminium: Leadership Through Acquisitions

43%42%

34%37%

32%

26%

0%5%

10%

15%20%25%30%35%40%45%50%

FY97 FY98 FY99 FY00 FY01 FY02

Brown Field Expansion

Acquisition of majority stake in Indal

Hindalco(1)43%

Nalco20%

Balco15%

Malco5%

Import17%

Copper business acquisition to create a Non-

Ferrous Powerhouse

Impressive Increase in Market Share Impressive Increase in Market Share Market Share Market Share –– FY02FY02

14

Market Share: Foils

58%55%

26%

0%

6%

0%

10%

20%

30%

40%

50%

60%

70%

FY98FY

99FY

00FY01FY02

Market Share: Extrusions

26%24%

16%

13%14%14%

0%

5%

10%

15%

20%

25%

30%

FY 97FY

98FY

99FY

00FY

01FY02

Market Share: Rolled Products

68%65%

31%28%

23%

14%

0%

10%

20%

30%

40%

50%

60%

70%

80%

FY 97FY98FY99FY00FY01FY02

Enviable Market Position in ValueEnviable Market Position in Value--added Products As Welladded Products As Well

Aluminium: Leadership Through Acquisitions (Contd.)

15Concerted efforts paying offConcerted efforts paying off

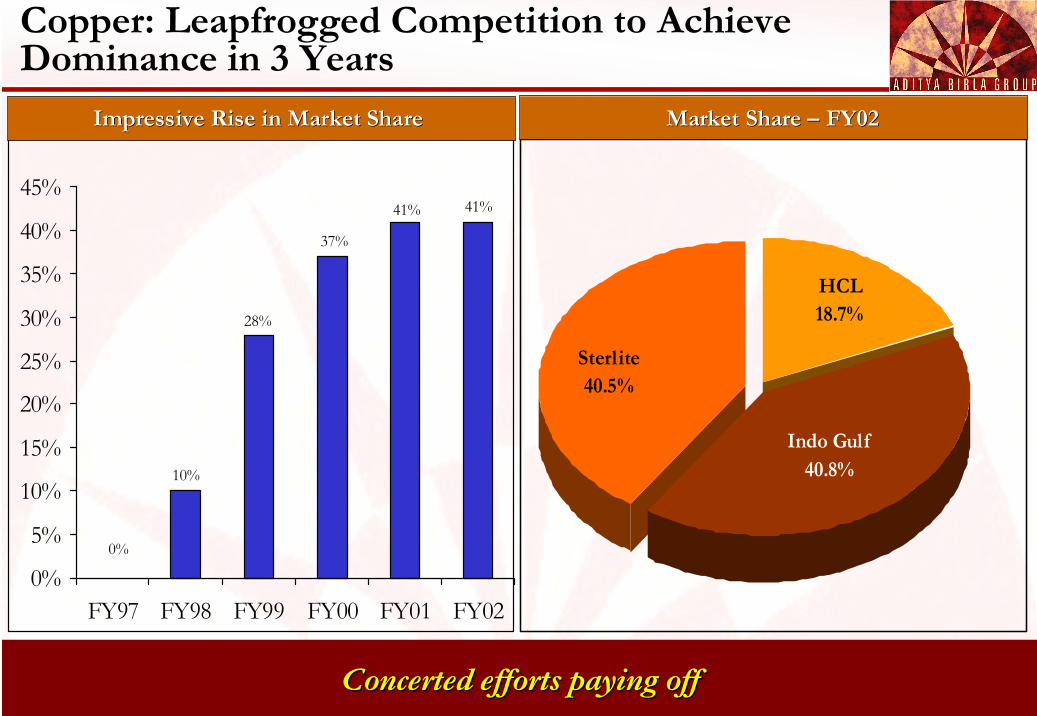

Copper: Leapfrogged Competition to Achieve Dominance in 3 Years

41%41%

37%

28%

0%

10%

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

FY97 FY98 FY99 FY00 FY01 FY02

Sterlite40.5%

Indo Gulf40.8%

HCL18.7%

Impressive Rise in Market Share Impressive Rise in Market Share Market Share Market Share –– FY02FY02

16

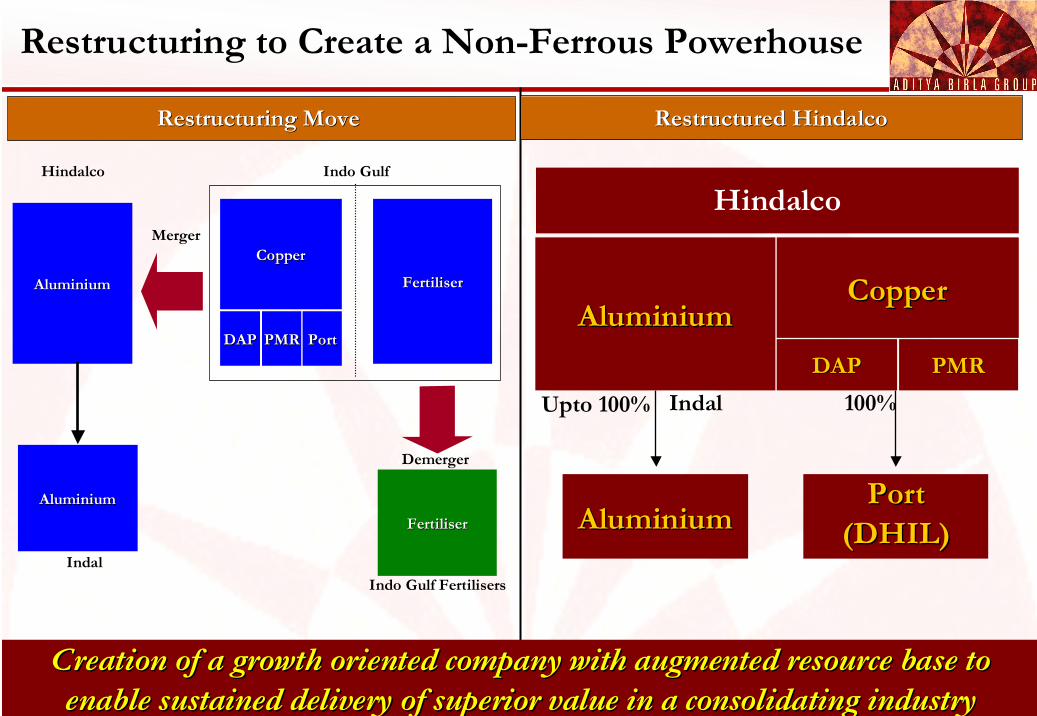

AluminiumAluminium

AluminiumAluminium

Hindalco

Indal

CopperCopper

DAPDAP PMRPMR PortPort

FertiliserFertiliser

Indo Gulf

Merger

FertiliserFertiliser

Demerger

Indo Gulf Fertilisers

Restructuring to Create a Non-Ferrous Powerhouse

Restructuring Move Restructuring Move

Upto 100%

AluminiumAluminiumPortPort

(DHIL)(DHIL)

100%Indal

AluminiumAluminiumCopperCopper

DAPDAP PMRPMR

HindalcoHindalco

Restructured HindalcoRestructured Hindalco

Creation of a growth oriented company with augmented resource baCreation of a growth oriented company with augmented resource base to se to enable sustained delivery of superior value in a consolidating ienable sustained delivery of superior value in a consolidating industry ndustry

17

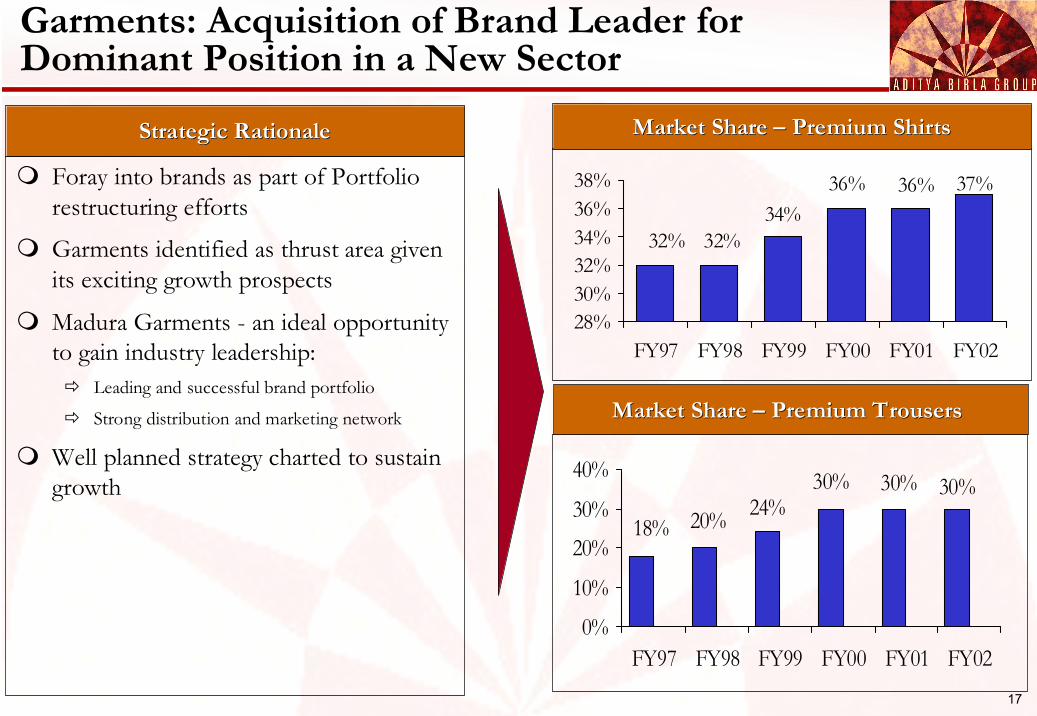

Strategic RationaleStrategic Rationale

Foray into brands as part of Portfolio restructuring efforts

Garments identified as thrust area given its exciting growth prospects

Madura Garments - an ideal opportunity to gain industry leadership:

Leading and successful brand portfolio

Strong distribution and marketing network

Well planned strategy charted to sustain growth

37%36%36%34%

32% 32%

28%30%32%34%36%38%

FY97 FY98 FY99 FY00 FY01 FY02

Market Share Market Share –– Premium ShirtsPremium Shirts

30%20%18%

24%30% 30%

0%

10%

20%30%

40%

FY97 FY98 FY99 FY00 FY01 FY02

Market Share Market Share –– Premium Trousers Premium Trousers

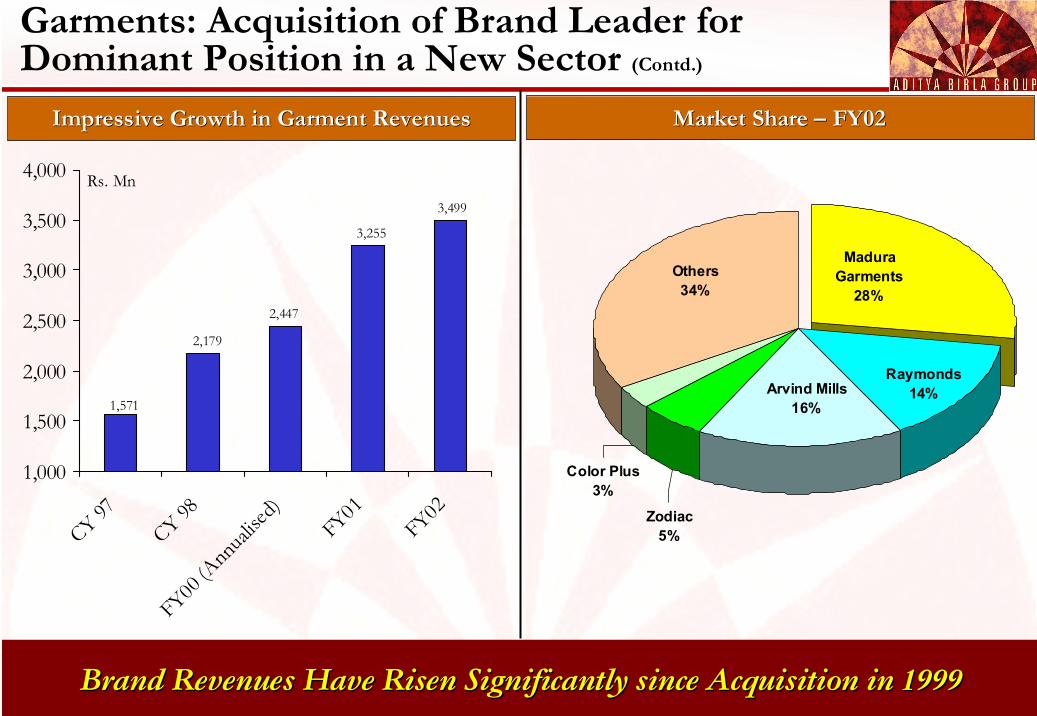

Garments: Acquisition of Brand Leader for Dominant Position in a New Sector

18Brand Revenues Have Risen Significantly since Acquisition in 199Brand Revenues Have Risen Significantly since Acquisition in 19999

Garments: Acquisition of Brand Leader for Dominant Position in a New Sector (Contd.)

Impressive Growth in Garment RevenuesImpressive Growth in Garment Revenues Market Share Market Share –– FY02FY02

3,499

3,255

2,447

1,571

2,179

1,000

1,500

2,000

2,500

3,000

3,500

4,000

CY 97

CY 98FY00

(Ann

ualise

d)

FY01

FY02

Rs. Mn

Arvind Mills16%

Raymonds14%

Zodiac5%

Color Plus3%

Madura Garments

28%Others34%

19

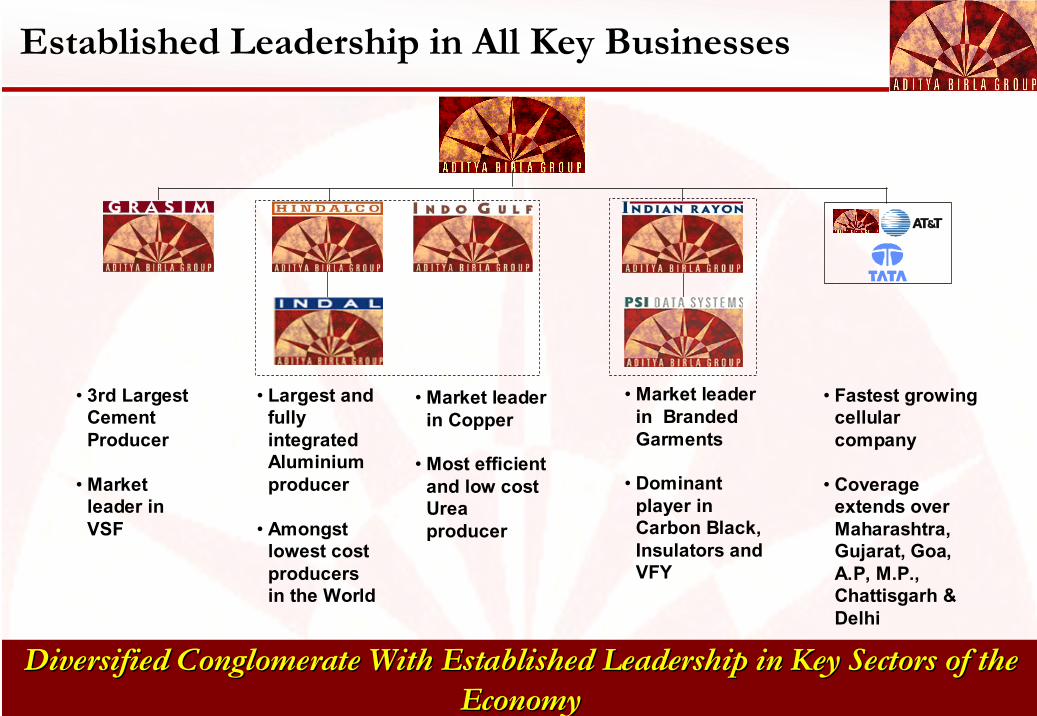

• Fastest growing cellular company

• Coverage extends over Maharashtra, Gujarat, Goa, A.P, M.P., Chattisgarh & Delhi

• 3rd Largest Cement Producer

• Market leader in VSF

• Largest and fully integrated Aluminium producer

• Amongst lowest cost producers in the World

• Market leader in Branded Garments

• Dominant player in Carbon Black, Insulators and VFY

• Market leader in Copper

• Most efficient and low cost Urea producer

Diversified Conglomerate With Established Leadership in Key SectDiversified Conglomerate With Established Leadership in Key Sectors of the ors of the EconomyEconomy

Established Leadership in All Key Businesses

20

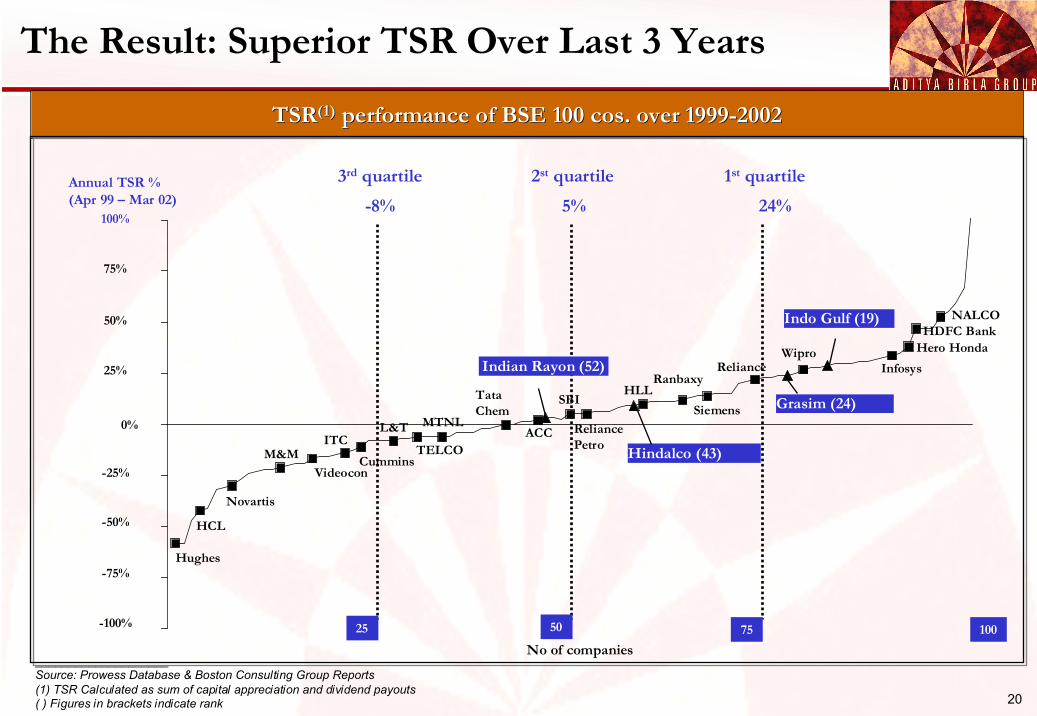

The Result: Superior TSR Over Last 3 Years

TSRTSR(1)(1) performance of BSE 100 cos. over 1999performance of BSE 100 cos. over 1999--20022002

Annual TSR % (Apr 99 – Mar 02)

Hughes

Indian Rayon (52)

HDFC BankWipro

Grasim (24)L&T ACC

Hindalco (43)

25 50 75 100

25%

50%

75%

100%

-100%

-75%

-50%

-25%

No of companies

Novartis

ITC

HLLSiemens

ReliancePetro

Hero Honda

-8% 5% 24%1st quartile 2st quartile 3rd quartile

0%

HCL

M&MVideocon

CumminsTELCO

MTNL

TataChem

SBIRanbaxy

Indo Gulf (19)

Infosys

NALCO

Reliance

____________________Source: Prowess Database & Boston Consulting Group Reports(1) TSR Calculated as sum of capital appreciation and dividend payouts( ) Figures in brackets indicate rank

21

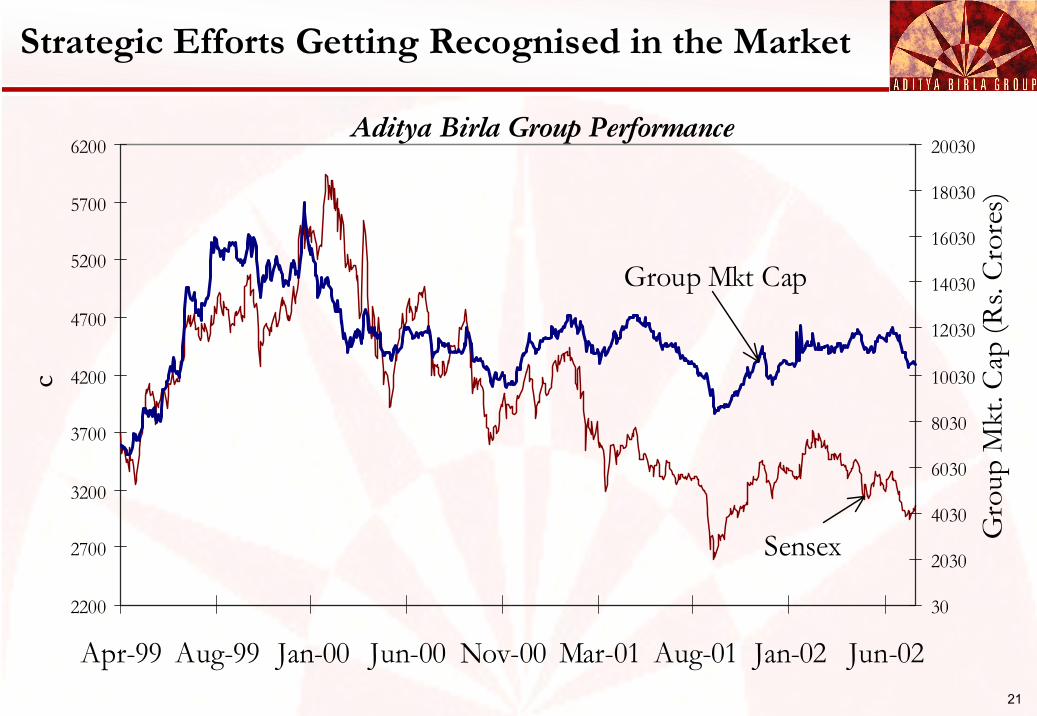

Strategic Efforts Getting Recognised in the Market

2200

2700

3200

3700

4200

4700

5200

5700

6200

Apr-99 Aug-99 Jan-00 Jun-00 Nov-00 Mar-01 Aug-01 Jan-02 Jun-02

c

30

2030

4030

6030

8030

10030

12030

14030

16030

18030

20030

Gro

up M

kt. C

ap (R

s. C

rore

s)

Aditya Birla Group Performance

Sensex

Group Mkt Cap

22

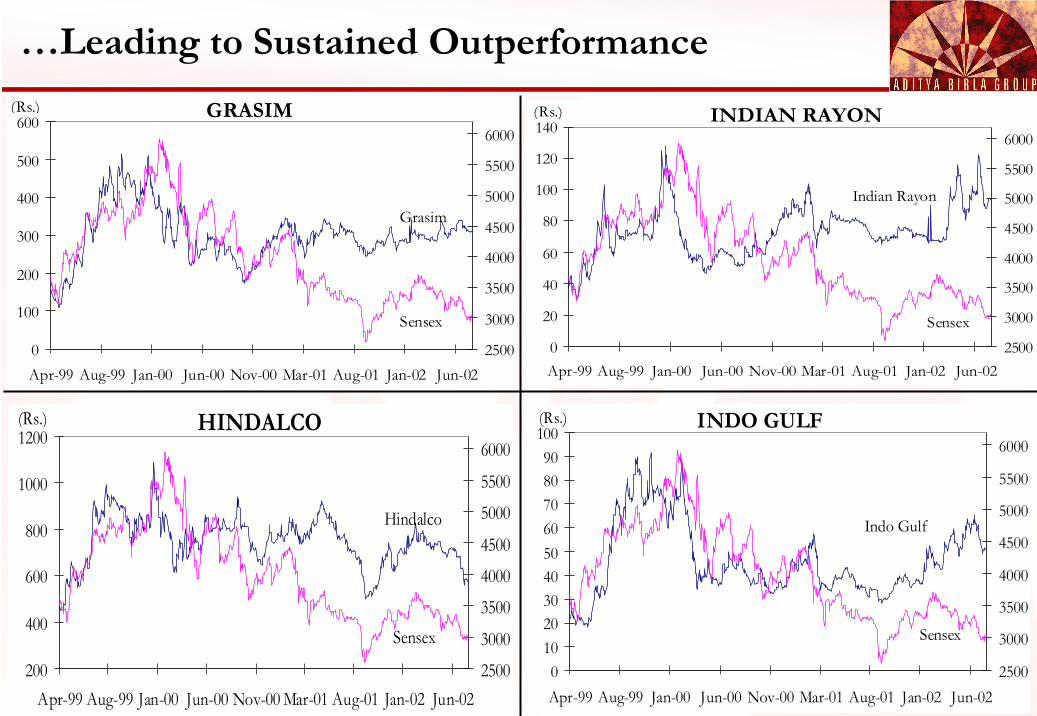

…Leading to Sustained Outperformance

0

100

200

300

400

500

600

Apr-99 Aug-99 Jan-00 Jun-00 Nov-00 Mar-01 Aug-01 Jan-02 Jun-022500

3000

3500

4000

4500

5000

5500

6000

Grasim

Sensex

(Rs.) GRASIM

200

400

600

800

1000

1200

Apr-99 Aug-99 Jan-00 Jun-00 Nov-00 Mar-01 Aug-01 Jan-02 Jun-022500

3000

3500

4000

4500

5000

5500

6000

Hindalco

Sensex

HINDALCO(Rs.)

0

20

40

60

80

100

120

140

Apr-99 Aug-99 Jan-00 Jun-00 Nov-00 Mar-01 Aug-01 Jan-02 Jun-022500

3000

3500

4000

4500

5000

5500

6000

Indian Rayon

Sensex

INDIAN RAYON(Rs.)

0102030405060708090

100

Apr-99 Aug-99 Jan-00 Jun-00 Nov-00 Mar-01 Aug-01 Jan-02 Jun-022500

3000

3500

4000

4500

5000

5500

6000

Indo Gulf

Sensex

(Rs.) INDO GULF

23

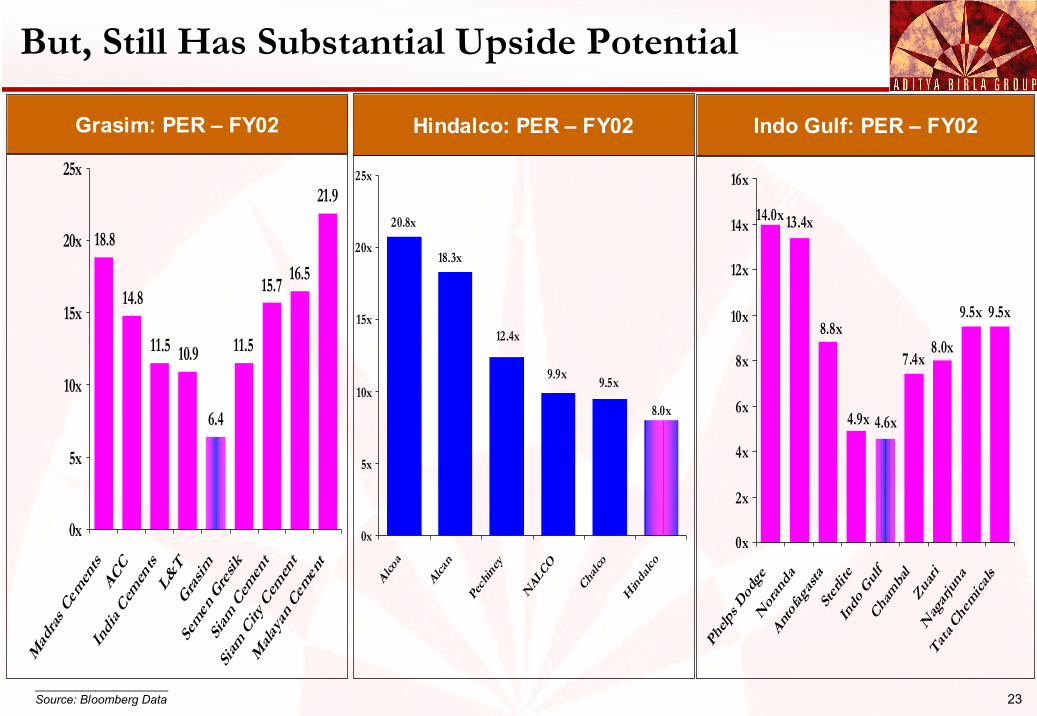

But, Still Has Substantial Upside Potential

Grasim: PER – FY02

18.8

14.8

11.5 10.9

6.4

11.5

15.7 16.5

21.9

0x

5x

10x

15x

20x

25x

Mad

ras C

emen

tsACC

Indi

a Cem

ents

L&T

Grasim

Semen

Gre

sikSia

m Cem

ent

Siam

City

Cem

ent

Mala

yan C

emen

t

Hindalco: PER – FY02

8.0x

9.5x9.9x

12.4x

18.3x

20.8x

0x

5x

10x

15x

20x

25x

Alcoa

Alcan

Pech

iney

NALCO

Chalco

Hindalc

o

Indo Gulf: PER – FY02

9.5x9.5x

8.0x7.4x

14.0x 13.4x

8.8x

4.9x 4.6x

0x

2x

4x

6x

8x

10x

12x

14x

16x

Phelp

s Dod

geN

oran

daAnto

fagas

taSte

rlite

Indo

Gulf

Cham

bal

Zuari

Nag

arjun

a

Tata C

hemica

ls

____________________Source: Bloomberg Data

24

Geography specific businesses - build and retain dominanceCement, Garments, Fertilisers and Carbon Black

Global businesses - domestic dominance coupled with cost leadership Aluminium, Copper, Viscose Staple Fibre, and Insulators

Growth through brownfield as well as inorganic opportunities Under leveraged Balance Sheets

Strong cash flows

Heightened awareness of growth imperatives

Emerging opportunities to support aggressive plansOn-going consolidation in key business sectors in India

Government dis-investment programme

Going Forward…Enhanced Dominance in Key Businesses

25

Shareholder value enhancement to remain the focal point for all decisionsCVA to drive decision making across all levels of organisation

Dispassionate evaluation of all businesses Continued value creation across companiesEarly identification of businesses with declining prospects for appropriate actionDivest value destroying businesses at an appropriate time

Listed companies to focus on identified core businesses No fresh crossholdings and concerted efforts to reduce existing crossholdings

Going Forward…Shareholder Value Will Be Key Criteria for Decisions

Thank YouThank You