Turning Today’s Top Franchising Challenges Into Franchising Gold

CRACKING EUROPEANRESTAURANT FRANCHISING:

MARKETS, MODELS & MEGA PLAYERS

A WSP WHITE PAPER - OCTOBER 2021

WhiteSpace Partners is a strategic advisory firm, specializing in the restaurantand foodservice industry. Our focus concentrates on the development andexecution of strategies for three types of clients:

ü Restaurant brands planning to expand within or outside their home marketü Private equity firms looking to grow or acquire restaurant groupsü Landlords who are developing projects including restaurants

Our international expansion and franchising advisory practice counts on aveteran team of restaurant developers and operators who have worked forglobal and Fortune 500 companies and played integral roles in thedevelopment of some of Europe's most well-known and well-loved brands.We advise emerging and established restaurant brands on:

ü Development of international expansion strategiesü Market entry planningü Preparing for franchise expansionü Franchisee and new partner identification and acquisitionü Evolving and/or restructuring existing franchise systems

2Franchising in Europe

WhiteSpace Partners Ltd.19 Newman Street - London W1T 1PFUnited Kingdomwww.whitespace-partners.com

Follow us on Linkedin

ForewordIn the restaurant industry, franchising isone of the most popular strategies thatbrands rely on to expand operationsinternationally. There are few globalrestaurant brands with a significantinternational presence that have not usedthis strategy to reach their internationaldevelopment goals at on point or another.Franchising requires important choices tobe made among various models,agreement structures and franchiseedistribution in a market, among others.Structures of franchise agreements canrange from exclusive national or regionalarea development to master franchiseagreements or non-exclusive single-unit ormulti-unit agreements, and there are manyin between.

There are a myriad of decision drivers inchoosing the right franchise expansionstrategy, including the operational modelof the brand, supply chain requirementsand corporate goals and targets, whichwill vary greatly from one company toanother. When deciding in which marketsto start, franchisors must take intoconsideration market size anddevelopment opportunity, barriers toentry, financial and legal requirementsand, most important, availability andcapabilities of viable partners.

International brands need to understandthat Europe is far from being ahomogeneous market. There are diversefranchise disclosure laws, cultures,consumer mindsets and behaviours andbusiness practices – all of which can varyby country and region.

This white paper will take a focusedapproach on six global franchisors whohave successfully developed in Europe andtheir growth strategies in seven keymarkets. We will explore the benefits andchallenges of those strategies and obtainindustry expert perspectives on the risksand rewards, while also delivering insightsand discoveries from case studies of threelarge European franchisees who havemastered cross-border expansion.

Whether you are a franchisor, franchisee orthinking about embarking on a franchisingventure, we offer you a fascinating look intothe European franchising landscape,through the exploration of some of theregion’s biggest players.

October 2021 │ 3

Rebecca Viani, CFEHead of International Development and Franchising [email protected]

Restaurant Franchising in Europe

Tributes and Honourable Mentions Although not a focus of this particularstudy, it's important to recognize some ofthe brands who play an influential role inthe European restaurant landscape. Firstly,we must pay tribute to McDonald’s, theglobal leader in foodservice andfranchising, who has a consistent modelfocusing on single or multi-unit franchisedevelopment, with no sub-franchising - amodel in which they own about 45% of theland and 70% of the buildings in theiroperation (Wall Street Survivor, 2021). Manysay that their core business is real estate, asopposed to franchising. No matter whichperspective one takes, the company is asuccess story in either industry.

Interestingly, when it comes to internationaldevelopment, not many European-bornfoodservice brands have managed to crossborders to a considerable extent, and thefootprint of European brands outside oftheir respective domestic markets is stillrather modest. France-based PAUL leadsthe pack, having gained a foothold innumerous other European countries, theMiddle East, North America, Asia andAfrica. French Groupe Le Duff is anotherone to watch as they continue theexpansion of La Brioche Doréeinternationally. British brand, Pret AManger, who just recently began their

high-street franchising journey targeting afocused number of key Europeancountries, is well positioned to becomethe next European frontrunner. Very-promising Vapiano, from Germany, hashad a rocky franchising journey over thepast 5 years but is also one to watch sincethe start of the turnaround in 2020, led byex-Vapiano executive and currentshareholder, Mario C. Bauer. This timearound, the brand is supported by astrong and experienced investment team,including Pret A Manger co-founder,Sinclair Beecham, Vapiano’s co-founder,Gregor Gerlach, AmRest founder, HenryMcGovern and the Dutch hospitalityfamily, Van Der Valk.

Being that franchising got a later start inEurope than in its home country of theU.S., it’s not surprising that the largestinternational European franchisors stillhave plenty of room to grow in the region.They have the home court advantage overlarger, incoming international brands,which will make it interesting to see howthese budding brands compete as theymove into neighbouring markets, backedby a solid presence and brand awarenessin their local home markets.

October 2021 │ 4Restaurant Franchising in Europe

# of units worldwide 18,000 31,000 25,000 17,000 1,400 400

# of units in Europe 4,950 2,800 3,500 3,800 140 566

United Kingdom

Proceeding to the main topic, we will explore six franchise brands with some of the largest footprints in Europe: Burger King, Starbucks, KFC, Domino’s, Five Guys andPAUL. All of these brands have entered into and evolved very differently in Europe, and all of these brands have success stories of their own that are still unfolding. At the same time, the brands approach the markets differently. Breaking down each franchising model, we see a mixed picture of strategies for success in cracking the European franchise market.

Key mapAD – Area DevelopmentMF – Master FranchiseCR – Corporate RunSU – Single UnitsJV – Joint Venture

Six Brands, Seven Markets– a Mixed Picture

Source: Top 99 FS Groups in Europe 2019, FSE&ME edition 5/2020

Source: Desk research 2021

MF CR/AD AD MF JV CR

Belgium

MF/JV AD AD MF CR AD

FranceMF/JV MF AD MF JV AD

Spain

AD MF AD MF JV CR/AD

Italy

MF/JV AD AD MF AD AD

Germany

MF AD AD MF JV

The Netherlands

AD AD AD MF CR

October 2021 │ 5Restaurant Franchising in Europe

For this paper, we will classify an areadeveloper by the first definition, unlessotherwise stated.

Area development is thepreferred franchiseexpansion method forPAUL, the onlyEuropean brand on our

list, with over 700 franchised locations inFrance, Spain, Portugal, Belgium,Luxembourg, UK and 30+ other countries.Their corporate-run units can be found inthe UK and France, where their corporateunits coexist with local franchisees.

PAUL has been a family-owned companysince inception and, although they have asolid international presence, the brand hasmanaged to fly under the radarthroughout their growth journey. A large

1. Area developer is the solefranchisee in a defined territory andresponsible for developing andoperating all units, with no sub-franchising. The area developer paysfranchise fees and royalties to thefranchisor, as per the agreement.

2. In addition to the terms of the firstdefinition, the area developer is alsotasked with identifying, onboarding,training and supporting new andexisting franchisees in the market. Inthis case, the area developer is usuallypaid fees or commissions by thefranchisor. This agreement can beclassified as an area developmentagreement or corporate franchiseagreement, in some cases.

Area development is often used by fastcasual and casual dining brands headingfor Europe as opposed to master franchiseagreements, which we see morecommonly with limited service and QSR.This model allows a less crowdedfranchisee pool in a market, while thebrand maintains a certain level of control.There are 2 variations of the definition ofthis model:

Area Development

October 2021 │ 6Restaurant Franchising in Europe

majority of their sites can be found inairports and travel hubs, and this is wherethe focus of their franchising strategy liesin many markets, except for regions likethe Middle East, where they have aregional area development franchisee whocontinues to build the brand successfullyin the market. What we do notice withPAUL is that, although they have a wideinternational presence, country-wise, thereare few markets where they haveestablished a strong penetration rate.Markets like Spain, with 2 locations, bothat airports, leave one to question thestrategy behind planting a flag in a newmarket without fully capitalizing on thedevelopment opportunity of that market.With new leadership having come intoplay in the last few years, we do see abigger push for franchising in the UK (BigHospitality, 2018), which could be the startof a progression to other markets.

Area Development

Starbucks’ mainfranchising model inEurope is strictly area

development in marketslike Italy, where they have

only one corporate unit (the iconicroastery in Milan), as well as Belgium, TheNetherlands and Luxembourg. The UK isshared between Starbucks corporate-rununits and its area developmentfranchisees. However, the brand has aninteresting mix in the rest of Europe, whichwe attribute to its history. Starbucksoriginally entered a number of Europeanmarkets directly building corporate units

Being a privately held family-runcompany has its advantages, andhaving the freedom to take the time toidentify and select franchisees andpenetrate markets at a moreconservative (sometimes less risky)speed are two of the many advantagesthat their publicly traded industrycounterparts may not enjoy. PAUL hasgrown steadily over the years, and webelieve that, as engaging and well-positioned as they are, the brand hasample room to grow deeper into itscurrent markets.

October 2021 │ 7Restaurant Franchising in Europe

in specialty markets like the CanaryIslands, Andorra and airports. They havemore liberal sub-franchising rightsfor Portugal and France, where they canaward single and multi-unit licenses tosub-franchisees.

KFC is a great exampleof a brand which has a

strong focus on areadevelopment and isconsistent with this model

across all our markets of interest. Thatsaid, as of October 2021, with 35restaurants and after operating as an areadeveloper in the Dutch market formany years, Australia-based Collins

in countries like France, Germany and TheNetherlands and also signing with smallerarea developers in other regions.

Upon the purchase of the countryoperations by big franchisees, such asAmRest and Alsea, these groups acquiredboth the corporate units and the existingfranchisees in those markets. In the 2016takeover by AmRest, the franchisee giantacquired Starbucks’ corporate units inGermany, becoming the exclusive areadevelopment franchisee (AmRest, 2016),where they now operate over 130 sites.

Similarly, Alsea acquired 83 corporateunits and 177 franchised units in Franceand Benelux (Reuters, 2018), becomingthe master franchisee for France andexclusive area developer for TheNetherlands, Belgium and Luxembourg.They also currently hold the masterfranchise license in Spain and Portugal. Insome of those scenarios, although most ofthe Starbucks units are operated byAmRest or Alsea directly, we have seenexceptions made that allow for subfranchising in specific situations (i.e., travelhubs, non traditional sites, selectterritories, etc.), which the brand approveson a case-by-case basis. In Spain, forexample, Alsea confirms that of their 138units, 21 of those units are sub-franchised

Area Development

October 2021 │ 8Restaurant Franchising in Europe

Foods inked the corporate franchise dealfor The Netherlands, giving them fullcontrol of the market development (CollinsFoods Limited, 2021).

The corporate franchise agreement (CFA)appears to be more reflective of oursecond definition of the area developmentagreement, making Collins Foodsresponsible for the development,management, marketing, support andoperation of the KFC business in thecountry, along with the management ofnew and incoming franchisees, whilereceiving remuneration from KFC towardthe costs of operating the market. It isunclear as to who is collecting franchisefees and royalties directly from the in-market franchisees.

YUM! Brands, KFC’s holding company, isno stranger to franchising. Although KFCis mainly franchised via area developmentin Western Europe, its sister brand PizzaHut has a larger focus on masterfranchising. Master franchisees likeTelepizza have the rights for Spain. PizzaHut (U.K.) Ltd. has the master license inthe UK, and AmRest has the master rightsfor the Pizza Hut Express and Deliveryconcepts in France, Poland, the Czech

Area DevelopmentRepublic, Hungary, Slovakia, Russia,Armenia and Azerbaijan.

AmRest also has full master franchiserights for Pizza Hut Express, Delivery andDine-in in Germany. KFC is one to watch inthe future, with The Netherlands corporatefranchise deal showing us that YUM!Brands is open to being flexible when itcomes to adaptation of its franchisemodel, for the right scenario.

As with any model, there are advantagesand challenges. The area developmentmodel is the franchising model that allowsthe highest amount of control for the

October 2021 │ 9Restaurant Franchising in Europe

franchisor. At the same time, dependingon one partner to develop a market,makes for a slower development processand places the success of the brand in thatmarket on one franchisee. As franchisinglegal expert, Babette Marzheuser-Wood,Global Head of Franchise Group forDentons Legal warns, “It is easy fordevelopers to be over-ambitious. Thechallenge of the model is to find someonewho is ambitious, but still realistic.“Looking at larger markets that have manydifferent regions, and each with differenteconomies, cultural differences andoperating requirements, Babetterecommends "considering smallerdevelopment territories or clusterfranchising. It is difficult to find qualifiedand viable partners for large countries thathave dynamic regional markets.“

To Babette’s point, targeting areadevelopers in large markets is easiestaddressed as a regional initiative. Bigmarkets like Germany, France and Spainhave few qualified operators who candevelop an entire country on their own,but a great number of strong regionaloperators who know their regions andlocal consumer demands extremely well,making them ideal candidates.

Area Development

October 2021 │ 10Restaurant Franchising in Europe

The same goes for other parts of Europe,where the brand has partnered withprivate equity group Kharis Capital,under the entity Burger King SEE S.A.,which is the master franchisee for Italy,operates restaurants in Poland and is themaster franchisee for Luxembourg andBelgium under affiliate, Burger BrandsBelgium.

In this model, the master franchisee isresponsible for developing the licensedbrand in a country or region, acting as amini-franchisor in that region. The model isbased on a three-step principle,comprised of the franchisor, the masterfranchisee and sub-franchisees. Themaster franchisee acts as the franchisor inthe designated market, developing thebrand by opening a minimum number ofunits (as per the agreement) as well asmarketing franchise opportunities in theterritory and identifying, onboarding,training and supporting sub-franchisees.The master franchisee collects franchisefees and royalties from the sub-franchiseesand shares a portion of these with thefranchisor, as per the agreed terms.

Burger King mainly followsthe master franchise model

in France, Germany, Italy,Spain, Benelux and the UK,but it’s important to look at

the structure of some of the masterfranchisee entities, where the brand hastaken a more active role. France, forexample, although it is a master franchisemodel, the master franchisee entity isformed as a JV between local GroupeBertrand and a minority sharefrom Bridgepoint and Burger King USA.

Master Franchise

October 2021 │ 11Restaurant Franchising in Europe

and now holds the master license for theUK and Ireland. A subsidiary of theInternational Franchise Systems holdingcompany, Domino’s Pizza Group Plc iscontrolled by sibling investors Colin andGerry Halpern who also have acontrolling stake in DPE‘s masterfranchisee entity in Germany and haverecently or are currently in the process ofdivesting from their participationSwitzerland, Iceland, Norway and Sweden(Domino’s Pizza, 2020).

For franchisors, master franchising is agrowth model with relatively low risk andlow investment costs, as the masterfranchisee takes on the majority of the risk,establishes the brand, develops theinfrastructure, oversees adaptation tonational needs and legislation rules incollaboration with the franchisor andinvests in the sub-franchisee search,onboarding and support. When notfamiliar with local conditions, working witha strong and experienced masterfranchisee can be a win-win-solution. Onthe other hand, the franchisor hasto prepare for relatively modest revenuesand less control over franchise operationsand sub-franchisee management andsupport in the market. Furthermore,master franchisees with the capabilities to

Domino’s is another one ofthe big brands that relieson master franchisingfor their international

development. One of theirlargest master franchisees is

Australian group, Domino’s PizzaEnterprises Limited (DPE), who inaddition to Australia, possesses the masterfranchise rights for New Zealand, Japan,Taiwan, Belgium, France, The Netherlands,Germany and Denmark. Spanish giant,Alsea, holds the master franchise rights forSpain, and Italian private equity group,EVCP Growth Equity, has the masterfranchise rights for Italy.

In the UK, Domino’s Pizza Group Plcstarted their franchising journey bypurchasing the master franchise for theBritish Isles from the U.S. group in 1992

Master Franchise

October 2021 │ 12Restaurant Franchising in Europe

Master Franchise

October 2021 │ 13

develop large markets are few and farbetween. “There are a small number ofestablished master franchisees in the EUmarket”, says Henry McGovern, founderand former chairman of AmRest,“Opportunity to have access to a healthypool of franchise partners sometimesrequires franchisors to deviate to othermodels in order to expand the candidatepool.” Wise words from an industry expertand an interesting point to consider whenlooking at the variation of modelsmanaged by each brand.

From the franchisee perspective, Henrytells us that this is by far his most preferredmodel to operate. “I would have loved tohave had the master franchise for all thecountries we operated in!” Interestinglyenough, being present in 25 countriesthroughout Europe and beyond, AmResthas relatively few master franchises.

Restaurant Franchising in Europe

Usually, they own and operate thebusiness themselves, often investing theirsavings. They have high motivation tosucceed, but at a slow multi-unit growthrate, if at all sometimes. What we do see isexisting master franchisees andexperienced European franchisorsincluding the single-unit model in localmarkets in which they already operatetheir own units. As Thomas Kremer,President of Franchise Excellence &Expansion at AmRest shared, “We havebeen building our own portfolio of equitybrands, such as Sushi Shop, LaTagliatella and Blue Frog. With ourexpertise and network, we are providing aone-stop franchise solution forfranchisees.”

Despite the challenges that the single unitmodel can bring for international brandsentering a new market, many times, whatcan start out as a single-unit franchise canalso turn into a privately owned multi-unitenterprise, depending on entrepreneurialintelligence and the profitability of thebusiness. Starting with just a single PizzaHut location in Wroclaw, Poland, overthree decades ago, AmRest is a perfectexample of how a single-unit business hasthe potential to become an internationalmulti-brand operation.

Whilst obvious and probably notsurprising, this growth model is notpreferred by the big brands featured inour study, and there are a limited numberof international brands who use thismodel. Gaining a considerable marketshare within a short time can be easier toachieve when awarding single unit deals,but can be difficult to manage with singleunit partners as the numbers grow. Exceptfor low-potential markets, wheresupporting single unit entrepreneurs tobecome multi-unit partners could be areasonable option, there are more consthan pros to this model, as scaleincreases.

Single-unit franchise ownership typicallyappeals to first- or part-time businessowners with limited financial resourcesand low risk tolerance.

Single Unit Franchise

October 2021 │ 14Restaurant Franchising in Europe

Looking at the McDonald’s approach,whilst appreciating the challenges ofexpanding via single-unit partners, manyMcDonald’s franchisees have graduatedto multi-unit status, with a notable numberreaching multi-million-euro revenues overthe years. This success could be due toincredibly strong brand awareness, theunique real estate-focused franchisemodel, the strict non-compete thatMcDonald’s instills, prohibiting theirfranchisees from operating otherbusinesses, which helps keep franchiseegrowth aspirations channeled to the branditself or a combination of them all.

Although we don’t see many brandsexpanding internationally with single-unitfranchising, we do see their masterfranchisees opting for this model. BurgerKing’s German master franchisee, BAUMGruppe also has single unit franchisees, asdoes AmRest under their Pizza Hutmaster franchise, Alsea for Domino's andKharis Capital under Burger King,reinforcing the show of strength of themaster franchise model, when theright master franchisee is in control.

Single Unit Franchise

October 2021 │ 15Restaurant Franchising in Europe

Among our featuredbrands in thiswhitepaper and theseven markets weconsidered, franchisor,

Five Guys, shows us a great success storythrough corporate development and jointventure. Although they have a largefranchise network in the US and globally,they have a unique set up for WesternEurope, whereby the Five Guys family(Murrell) has a JV with UK partner CharlesDunstone (Arlidge, 2013).

This JV entity is responsible for the directdevelopment and operation of units in theUK, France, Germany, Spain and Portugal –an interesting and effective strategy forcapitalizing on supply chain, qualitycontrol and operational uniformity. Havingone central real estate division for this

Corporate Run / Joint Venturemulti-national entity employing over10,000 people, also gives them greatefficiency in the site search and acquisitionprocess. In other markets, like TheNetherlands (where their Europeanheadquarters is located) and Belgium,Five Guys has opted to operate thesemarkets themselves via affiliatecompanies.

There are a few markets in Europe wherethey have stayed with franchising, such asItaly, where they have an areadevelopment agreement in place withlocal partner and real estate developer,Gruppo Statuto, and another areadevelopment franchisee for Switzerlandand Luxembourg, backed by theAntolinos family. The brand also has afranchise agreement in place for CentralEurope, which includes Austria (ledby CEO, Sébastien Castagna) and even amaster franchising agreement for Australia(QSR Media Australia, 2020), showing usthat Five Guys has identified differentfranchise expansion strategy needs fordifferent markets.

With the other brands we are exploring,we see a sporadic presence of corporateunits within certain territories and somewhere the brand is sharing those

October 2021 │ 16Restaurant Franchising in Europe

markets with franchisees. PAUL andStarbucks operate corporate units in theUK, coexisting with franchisees. Aspreviously mentioned, the leading globalcoffee shop brand from the U.S. enteredmultiple European countries directly, onlyto eventually sell most of their corporateunits to local operators. KFC has done thesame in markets like Germany (sold toAmRest) and The Netherlands (sold toCollins Foods).

Entering new markets without localpartners is an ambitious venture forinternational brands but offers the benefitsof maximum control of the brandadaptation and growth, along withmaximum revenue potential. However,with that comes maximum risk. Brandsneed to have sufficient cash to take on aventure of this size.

Nowadays, we are seeing a large numberof international brands reducing theircorporate European footprint, where otherplayers, like Chipotle, Nando’s and PretA Manger have kept a strong hold ontheir corporate units. With their newlyinitiated franchising exploration into

markets like France, Germany andBenelux, Pret A Manger shows us thatstrategies can evolve, and developmentmodels can happily coexist (as with theirFrench operation), as brands grow.

Corporate Run / Joint Venture

October 2021 │ 17Restaurant Franchising in Europe

The entrepreneur Mario C. Bauer,shareholder of Vapiano, co-founder ofWhiteSpace Partners and co-founder &CEO of Curtice Brothers, shares hisinsights and the positive aspects of the JVmodel: “You get a better say in theadaptation”, says Mario, “It also helps youfind better partners, feel more committedand the exit option for the local partnermakes it easier to find an investor.” But asMario also shares with us, there arespecific needs to be met, if a JVrelationship is going to work. “Handling aJV needs a certain skill set, strongmanagement and strong financialcompliance. The back-office need is very,very high,” asserts Mario.

As complex a strategy as it may be, BurgerKing and Five Guys show us how to do itsuccessfully, in two very different ways,with two of the most high profileoperations in the region. Although it’s nota common practice among U.S. franchisorsto JV with international franchise partners,history shows us that it’s not uncommoneither. Looking to the future, emergingand progressive European franchisors,such as German-based dean&david andL'Osteria, are taking this practice to theforefront of their operations, showing usthat there are more creative ways to builda successful franchise system.

Both brands are well-known for opting totake a 51% ownership stake in theirfranchisee’s business, thus givingfranchisees access to financing andallowing more flexibility on growth. Bothchampions on their national playing fields,dean&david and L'Osteria are brands towatch as they continue to expand theirfranchise models across Germany, Franceand other parts of Europe.

Corporate Run / Joint Venture

October 2021 │ 18Restaurant Franchising in Europe

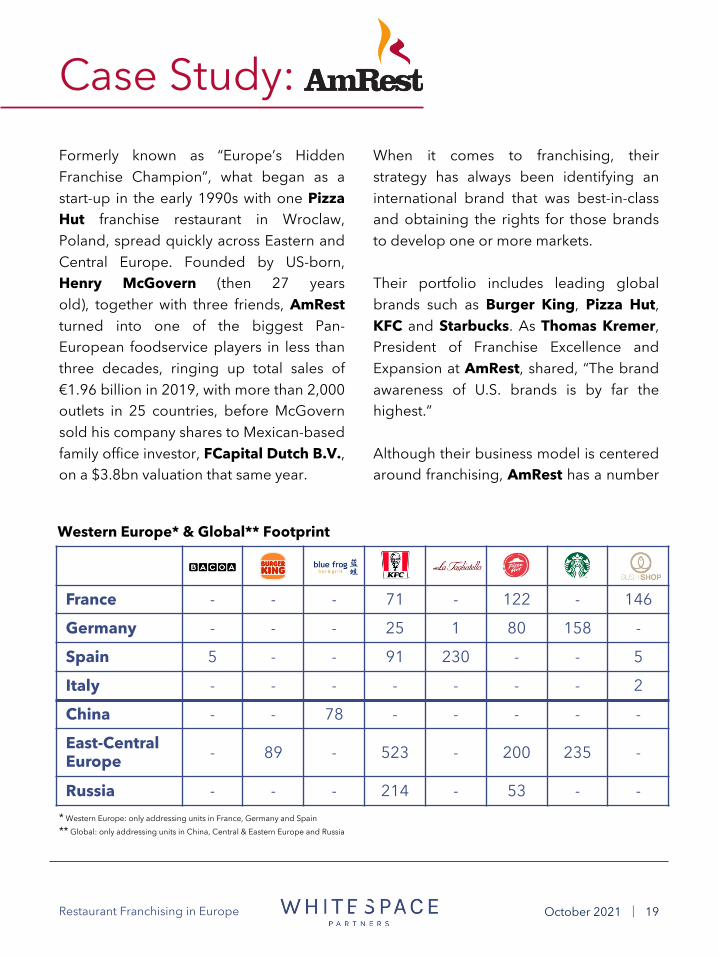

France - - - 71 - 122 - 146

Germany - - - 25 1 80 158 -

Spain 5 - - 91 230 - - 5

Italy - - - - - - - 2

China - - 78 - - - - -

East-Central Europe - 89 - 523 - 200 235 -

Russia - - - 214 - 53 - -

Western Europe* & Global** Footprint

Formerly known as “Europe’s HiddenFranchise Champion”, what began as astart-up in the early 1990s with one PizzaHut franchise restaurant in Wroclaw,Poland, spread quickly across Eastern andCentral Europe. Founded by US-born,Henry McGovern (then 27 yearsold), together with three friends, AmRestturned into one of the biggest Pan-European foodservice players in less thanthree decades, ringing up total sales of€1.96 billion in 2019, with more than 2,000outlets in 25 countries, before McGovernsold his company shares to Mexican-basedfamily office investor, FCapital Dutch B.V.,on a $3.8bn valuation that same year.

When it comes to franchising, theirstrategy has always been identifying aninternational brand that was best-in-classand obtaining the rights for those brandsto develop one or more markets.

Their portfolio includes leading globalbrands such as Burger King, Pizza Hut,KFC and Starbucks. As Thomas Kremer,President of Franchise Excellence andExpansion at AmRest, shared, “The brandawareness of U.S. brands is by far thehighest.”

Although their business model is centeredaround franchising, AmRest has a number

Case Study:

October 2021 │ 19Restaurant Franchising in Europe

* Western Europe: only addressing units in France, Germany and Spain** Global: only addressing units in China, Central & Eastern Europe and Russia

of own brands which they acquired alongthe way, with the intent of building aportfolio and continuing to scale. One ofthese brands is full-service brand, LaTagliatella, which was part of theRestauravia acquisition in Spain (AmRest,2011) followed by fast-casual chain SushiShop from France (Reuters, 2018), whichthey continue to franchise in their homemarkets and abroad. After that was theacquisition of the small, better burgerchain, Bacoa (AmRest, 2018), out ofBarcelona, Spain. Another noteworthyventure was the acquisition of the majoritystake in Chinese holding company, BlueHorizon, which operates casual diningbrands, Blue Frog and KABB (AmRest,2012). AmRest saw this as the best way toestablish operations in the Chinesemarket, with the intent of integrating LaTagliatella into the infrastructure to growthe brand there - an interesting andefficient strategy to gain market presenceand operational know-how, which weoften see in our industry.

Now under new ownership andwith management from Finaccess Capital(AmRest, 2021), it will be fascinating to seeif and how the expansion strategy changesfor the AmRest owned brands which haveso much room to grow.

Will there be more new internationalfranchise brands added to AmRest‘sportfolio, or will they capitalize on theirlearnings from some of the mostseasoned franchisors in the industry togrow their own franchise brands inEurope? AmRest has been a franchisingpowerhouse for years, and we areconfident that we will see more greataccomplishments to come from thisgroup.

Case Study:

October 2021 │ 20Restaurant Franchising in Europe

Today, Alsea Europe is one of the largestfranchisees in the region with a broadportfolio of franchise ownership modelsand a notable number of master licenses.According to the Spanish headquarters,being a master franchisee allows them togrow faster. “Sub-franchising is a solutionin areas where we have no structure toopen on our own”, the head office shares.Yet this poses challenges, like “having thecommercial capacity to find potential sub-franchisees and identifying talent thatallows us to provide adequate support tosub-franchisees.” Alsea Europe alsoteaches a valuable lesson in having a solidbalance between own locations and sub-franchised sites. “Growing so fast with ourown units had strategically diminished thepotential development of expansion viafranchising for those brands. In recentyears we consolidated areas ofdevelopment for franchisees with botheconomic and operational potential”, thecompany affirms.

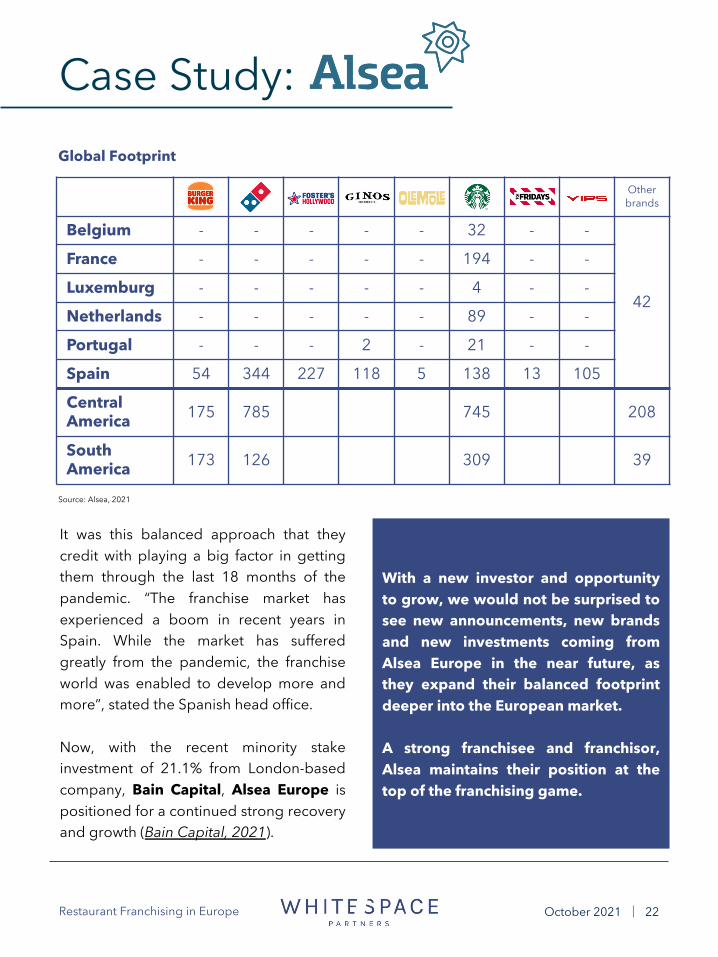

A leading foodservice operator in LatinAmerica and Spain, running circa 4,000units across over a dozen brands, Alseastarted their European journey by theacquisition of Grupo Zena, a well-established, 400+-units-strong, multi-concept company with a handfulof proprietary brands (including Foster’sHollywood with 220+ units to date),Burger King franchised units and themaster franchise license for Domino’s inSpain. This was followed by the acquisitionof Grupo VIPS, another long-timefoodservice player in the Spanish marketwith about 450 outlets. Alsea Europe notonly took over Grupo VIPS’ restaurantsand franchises but also the exclusive rightsfor Starbucks in Spain and Portugal. Thiswas followed by the acquisition of theStarbucks businesses in France and theBenelux countries, including the right todevelop the brand with direct openingsand sublicensed units in France.

Case Study:

October 2021 │ 21

Brand portfolio

Restaurant Franchising in Europe

Other brands

Belgium - - - - - 32 - -

42

France - - - - - 194 - -

Luxemburg - - - - - 4 - -

Netherlands - - - - - 89 - -

Portugal - - - 2 - 21 - -

Spain 54 344 227 118 5 138 13 105

Central America 175 785 745 208

South America 173 126 309 39

It was this balanced approach that theycredit with playing a big factor in gettingthem through the last 18 months of thepandemic. “The franchise market hasexperienced a boom in recent years inSpain. While the market has sufferedgreatly from the pandemic, the franchiseworld was enabled to develop more andmore”, stated the Spanish head office.

Now, with the recent minority stakeinvestment of 21.1% from London-basedcompany, Bain Capital, Alsea Europe ispositioned for a continued strong recoveryand growth (Bain Capital, 2021).

With a new investor and opportunityto grow, we would not be surprised tosee new announcements, new brandsand new investments coming fromAlsea Europe in the near future, asthey expand their balanced footprintdeeper into the European market.

A strong franchisee and franchisor,Alsea maintains their position at thetop of the franchising game.

Global Footprint

Source: Alsea, 2021

Case Study:

October 2021 │ 22Restaurant Franchising in Europe

Plans became known that QSRP intendedto transform the Quick units to BurgerKing. More acquisitions followed, namelyNordsee from Germany (Kharis Capital,2018) and O’Tacos from France.

Further owned brands include Go Fish!,developed in-house and praised asNordsee’s ‘rebellious younger sister’, andChick&Cheez, the latest addition to theportfolio in the chicken segment.

By the end of 2019, QSRP accounted forsome 1,000 restaurants and 200franchisees in seven countries throughoutEurope, with a sales volume close toaround one billion Euros. Rapid growthand extending the European footprint isthe declared goal for the future. “Organicas well as via further acquisitions”, explainsAlessandro Preda, Group Chief ExecutiveOfficer.

This private-equity investment companywas founded in Switzerland by twopartners, Manuel Roumain and DanielGrossmann and has evolved into a hybridfinancial and operational vehicle.Originally focused on the service andconsumer goods industries and the digitalsector, they bundled their foodserviceactivities into a platform named QSRP.

Unlike traditional private equitycompanies, QSRP is hands on in theoperations and development of itsrestaurant business. Strictly committed tothe quick-service sector, their growthstrategy is twofold: company-ownedbrands on one hand and franchisedbrands on the other.

Their first master franchise deal was withmajor brand, Burger King, for Italy andPoland back in 2014, followed by masterlicenses for the brand in Belgium andLuxembourg, two years later. At the sametime QSRP acquired the total of 101Quick restaurants in Belgium andLuxembourg (of which 85 were franchised)from French owner, Groupe Bertrand,who kept the Quick operations in France(recently sold to HIG Capital).

Case Study:

Brand portfolio

October 2021 │ 23Restaurant Franchising in Europe

Kharis has an interesting and diversified portfolio of concepts, all European based,except for Burger King. The intriguing thing about Kharis is that they aresuccessfully building brands, some of which are centered around offerings that areless mainstream and in a smaller competitive pool, thus carving out their ownmarket share. We applaud Kharis Capital for their continued ambition and growthin mainstream and non-traditional segments as they continue gaining Pan-European positioning.

Case Study:

October 2021 │ 24

Timeline

2014

2016

2018

2019

2021

Founded in Zug, Switzerland

Master Franchises Italy and Poland

Master Franchises Belgium & Luxembourg

AcquisitionBelgium & Luxembourg

Acquisition

Acquisition

LaunchBelgium

LaunchLiège, Belgium

Restaurant Franchising in Europe

What does this all mean for franchisorslooking to break into the Europeanmarket, and what does it mean forEuropean brands aiming to breachneighbouring countries?

The history of franchising in Europe showsus that slow and steady wins the race, anddifferent markets may call for differentstrategies. As our experts shared, acatalyst for these variations could be thelack of qualified partners who fit thefranchisee profile for the standard model,which forces brands to opt for a Plan B.Size of market, legal restrictions andcountry dynamics can also play a role.

We have seen that five of the six brandslooked at, and the largest franchiseconcepts in Europe, are from the USA.Coming from the original home offranchising, U.S. brands have dominatedthe (systemized) European foodservicemarket since they arrived. As most of themare QSR players, these brands have lesscomplex systems than fast-casual or full-service operations and are much easier toreplicate. They were primed to bereplicated. Also, historically, they have hadtime to mature in their home markets andgenerate the cash needed to commit to along-term international expansion plan.

Key Learnings

Another interesting observation of the U.S.brands in our study is that many of themcame into Europe through directinvestment at one time or another. We seethat, since then, these same brands(Starbucks, Burger King and KFC)eventually sold off a large portion of theirportfolio to local franchise partners,diminishing their corporate presence inthe market. Only a minority of thesebrands who rely on franchising as theirprimary expansion strategy still opt forcorporate development in some cases,

October 2021 │ 25Restaurant Franchising in Europe

gaining maximum control of the brandand maximum revenues if all goes well,but also weathering steep, sometimespainful, learning curves. Joint venturesprovide a promising alternative, as FiveGuys proves well. Yet this is not a primarypath for most international franchisors.Running a company outside of the homemarket is demanding financially, legallyand operationally.

Mainly adhering to the joint venturestructure in Europe, Five Guyshas implemented the model in a way thatall national engagements throughoutsome of the largest, European countries,are overseen by the British JV (Five GuysJV Ltd.) entity. We see the size and depthof the company is leveraged for

the maximum benefit – a family affair, so tosay, and closely resembling a corporate-run venture with the nimble ability to makebrand adaptations and decisions quicklyfor each market.

Five Guys is the only U.S. brand within ourstudy who has maintained steadfast intheir initial market entry model, withouttransactions divesting to local franchisepartners in the JV and corporate markets.However, they are the youngest of thebrands we are looking at, having enteredthe market just 8 years ago, so it could bea matter of time before they follow in thefootsteps of their American predecessorsand sell off one or more pieces of theircorporate pie.

Key Learnings

October 2021 │ 26Restaurant Franchising in Europe

PAUL is a great example of a brand whohas taken its time to grow (established in1889), opened in over 30 countries, butstill ceases to have a strong hold onEuropean markets outside of the UK andFrance.

It leads to the question of what the brand’slong-term plan is for European expansion.Being a family-run, private company,PAUL, like Five Guys, is at a greatadvantage of having the flexibility andfreedom to choose the direction, modeland speed of its growth strategy withoutthe pressure of outside forces. Aninteresting observation is that they are theonly brand of the six who relies on the areadevelopment model and has maintainedonly that model without veering into otherfranchise formats.

Could this be due to the fact that, being aprivate company, they are free of thepressure to grow quickly and meet annualunit targets, potentially being forced toalter strategy to gain time or market sharewithin target timelines? Whatever thereason, PAUL has stayed true to theirfranchising model over their years offranchise development.

We commend PAUL for their consistencyand are optimistic about their growthopportunities deeper into Europe.

Source: PAUL, 2021

Source: PAUL, 2021

Key Learnings

October 2021 │ 27Restaurant Franchising in Europe

With the big players executing their longgame via mostly standard franchisemodels, we turn an eye to emergingfranchisors in the market like dean&davidand L'Osteria, both from Munich,Germany, who show us that that thelandscape is indeed changing. Both bignational players with big plans forfranchise expansion, their unique model ofshared equity with franchisees gives theman attractive advantage over traditionalfranchise offerings. Is this a new trend thatother brands will follow, or will theseforward-thinking national brands remain ina league of their own? Their internationalgrowth trajectory over the next few yearswill answer this question, as the success ofthe implementation of their uniquestrategies will surely inspire otherfranchisors.

Craft beer game changer, BrewDog,shows us another interesting strategy inthat they produce their craft beer and sellit to their franchisees who are developing

and operating bars worldwide. Because ofthis, BrewDog’s franchise fees areextremely competitive and quitefavourable, since craft beer production istheir core business, thus they are anattractive venture for experiencedfranchisees. Other product drivenfranchisors, such as ice cream brand,Amorino, also follow a similar structure, ofminimal franchise fees and royalties, whilegaining their profits from the product salesto franchisees.

Brands like these are surely changing thecompetitive landscape of franchising inEurope, as they offer local brandawareness, simpler supply chain solutionscoming from within Europe andcompetitive franchise terms. Non-European, international players, take heed.

To bring it full circle, the study of some ofthe biggest and fastest-growing European

Emerging franchisors Source: BrewDog, 2021

Key Learnings

October 2021 │ 28Restaurant Franchising in Europe

franchisees has given much to take away.While AmRest, with their ‘Anything ispossible’ motto, started as a pure franchisecompany, they later switched to alsoacquiring existing companies. The changeof course came shortly after their IPO,followed by the entrance of new investors,now holding the majority of the company,which could have been the catalyst for thealteration in growth strategy. In AmRest’smost recent history, we see that bringingon new franchise brands with no marketpresence was no longer a part of theirstrategy. Accelerated growth in a shorttime to keep investors and shareholderssatisfied also helped them gain a footholdin Western Europe and other foodservicesectors than QSR.

Let's not forget that in the late 20thcentury, the industry also had to face theinception of a new and quickly spreadingcategory: fast casual – a threat in terms ofmarket share (which even confrontedmarket leader McDonald’s with a fewdifficult years). La Tagliatella, and laterSushi Shop, as well as better-burgerbrand Bacoa, added new formats andpopular product segments with highgrowth potential to the AmRestportfolio. Securing the future whilst stilldeveloping the established brands wasthe name of the game.

Buying Sushi Shop helped AmRestincrease their country presencedramatically from 13 countries in 2017 to26 end of 2019.

Source: AmRest, 2021

05

1015202530

2017 2019

Increase of country presence

13

26

Key Learnings

October 2021 │ 29Restaurant Franchising in Europe

Their 100% acquisition of German fishspecialist, Nordsee, was their entry intothe German and Austrian markets,propelling them closer to their goal ofbecoming a leading Pan-European QSRplayer.

So, how will we continue to see existingmulti-unit franchisees and groups expandtheir operating footprint over the next fewyears? Our big three, AmRest, AlseaEurope and Kharis Capital, show us threemain growth strategies:

Other than AmRest, Alsea Europe,backed by their huge Mexico-based, multi-franchise mother company, listed on theMexican stock exchange, entered theEuropean market via acquisition and hasgrown via that same strategy, with majoracquisitions in Spain, including company-owned ventures, as well as franchiseagreements, giving them access toneighbouring countries.

Private equity firm and operator, KharisCapital, entered the franchising worldwith Burger King and has grown steadilyin the sector via their own brands andacquiring and scaling smaller brands.

Key Learnings

October 2021 │ 30

Onboard new brand in a new segment

1 2Buy existing

brand/group to integrate and scale

3Buy out existing franchisees or

corporate units of a brand already in the

portfolio.

Restaurant Franchising in Europe

Big international brands have set the tone,and we have seen their evolution over theyears as franchise models have changed,evolved and grown for thesebrands. European brands are growingstrongly in their home markets, but any ofthe brands who are expandinginternationally will need to time to provetheir success. Among them are Pret AManger, dean&david, L’Osteria,BrewDog, Amorino and Vapiano who ismaking a comeback. Growinginternationally is their ambition now,relying on joint ventures and franchiseagreements. One more to watch is DodoPizza, the number one pizza brand inRussia with close to 600 stores in sevencountries and on its way west withlocations now in the UK and Germany.

A Final LookWith the franchise landscape’s continuingevolution and local European nationalchampions spreading their wings intoother European markets, Europeanfranchisees have a broad spectrum ofchoice when considering new brands fortheir portfolios. In addition, thesophistication of European franchisees atan all-time high, is making it a competitiveplaying ground for new brands looking topenetrate and cross borders in Europe.

Whether you are an international brandcoming in or a European brand crossingborders, differentiation and flexibility areking to be able to navigate the ins andouts of this complex, dynamic andrewarding continent.

Brands to watch

October 2021 │ 31Restaurant Franchising in Europe

Acknowledgements

October 2021 │ 32

A work such as this is always a group effort. We are lucky to work in an industry full of bright, inspiring and immensely experienced individuals.

WhiteSpace Partners would like to thank the following groups and individuals for their amazing contribution to this piece:

Mario C. BauerShareholder of Vapiano, Co-founder of WhiteSpace Partners and Co-founder & CEO of Curtice Brothers

Babette Marzheuser-WoodGlobal Head of Franchise Group for Dentons Legal

Henry McGovernFounder and former chairman at AmRestand Co-founder of McWin Food Ecosystem Fund

Thomas KremerPresident of Franchise Excellence & Expansion at AmRest

Jonathan DoughtyProject Director – Leasing Services at ECE Marketplaces GmbH & Co. KGSenior Advisor at WhiteSpace Partners

Josefa GläserProject Manager at WhiteSpace Partners

Marianne WachholzTrade Journalist

Iván Martín CabreroDirector of Expansion at Alsea Europe

Restaurant Franchising in Europe

AmRest. (2011, April 27). Restauravia acquisition, press release. News. Retrieved October 21, 2021, from https://www.amrest.eu/en/investors-news/restauravia-acquisition-press-release.

AmRest. (2012, December 14). AMREST acquires a unique growth platform for China. Press Release. Retrieved October 21, 2021, from https://www.amrest.eu/en/system/files/press-release-blue-horizon-en.pdf.

AmRest. (2016, April 20). AmRest acquires Starbucks business in Germany. News. Retrieved October 21, 2021, from https://www.amrest.eu/en/investors/news/amrest-acquires-starbucks-business-germany.

AmRest. (2018, July 16). AMREST expands its portfolio with a Premium Burger Brand. Press Release. Retrieved October 21, 2021, from https://www.amrest.eu/sites/default/files/aktualnosci/zalczniki/press_release_-_amrest_expands_its_portfolio.pdf.

Arlidge, J. (2013, June 14). Charles Dunstone: Why the billionaire mobile mogul is bringing Five. London Evening Standard | Evening Standard. Retrieved October 21, 2021, from https://www.standard.co.uk/lifestyle/esmagazine/charles-dunstone-why-the-billionaire-mobile-mogul-is-bringing-five-guys-burgers-to-london-8657951.html.

Bain Capital. (2021, October 1). Bain Capital Credit invests in Alsea Europe. Bain Capital. Retrieved October 21, 2021, from https://www.baincapital.com/news/bain-capital-credit-invests-alsea-europe.

Collins Foods Limited. (2021, June 29). Collins Foods Limited - FY21 RESULTS. FY21 RESULTS. Retrieved October 21, 2021, from https://www.collinsfoods.com/wp-content/uploads/2021/07/CKF_Presentation_re_FY21_Results.pdf.

Domino’s Pizza Group plc. (2017, August 11). Domino's Pizza Group plc. Domino's Pizza Group announces acquisition of majority share in franchisee partnership | Domino's Pizza Group plc. Retrieved October 21, 2021, from https://investors.dominos.co.uk/media/news/domino%E2%80%99s-pizza-group-announces-acquisition-majority-share-franchisee-partnership.

QSR Media Australia. (2020, July 28). Exclusive: American Fast Casual Chain Five Guys slated to enter Anz. QSR Media Australia. Retrieved October 21, 2021, from https://qsrmedia.com.au/franchising/in-focus/exclusive-american-fast-casual-chain-five-guys-slated-enter-anz.

Reuters. (2018, November 1). Brief-AMREST completes Sushi Shop Acquisition. Reuters. Retrieved October 21, 2021, from https://www.reuters.com/article/idUSL8N1XC14Y.

Reuters. (2018, October 18). Starbucks to let Mexico's Alsea operate stores in four European markets. Reuters. Retrieved October 21, 2021, from https://www.reuters.com/article/us-starbucks-alsea-idUSKCN1MS1Z8.

WSS Author. (2021, July 27). McDonald's real estate: How they really make their money. Wall Street Survivor. Retrieved October 21, 2021, from https://www.wallstreetsurvivor.com/mcdonalds-beyond-the-burger/.

Sources

October 2021 │ 33Restaurant Franchising in Europe

WhiteSpace Partners is a dynamic, top-tier advisory company dedicated to providing the restaurant sector with comprehensive market-leading

strategies for sustained international growth.

Deeply passionate about food service, we work with both the finest F&B brands (restaurant groups, emerging F&B concepts, food retail

businesses) and leading investors (private equity, family offices, landlords and developers).

Learn more on www.whitespace-partners.comand follow us on

WhiteSpace Partners International Ltd. is a private limited company registered in England and Wales - Company n° 11448244 - VAT n° 317 9598 55The materials and concepts contained in this proposal are the exclusive property of WhiteSpace Partners International Ltd. and are for presentation and pitch purposes only.

Such materials and concepts may not be used, reproduced, or otherwise disseminated without the express written permission of WhiteSpace Partners International Ltd.