Exclusions as of 06/30/2018 Company Name Country ... - Wespath

Caring For Those Who Serve

CPP Funding UpdateAUMCPBO MeetingOctober 27, 2010

Comprehensive Protection Plan(CPP) Risk Management Metrics

• Brief Benefit Overview

• Premium Ratio

• Reserve Metrics■ Target

■ Minimum

■ Rate Action

J

CPP Benefits: Disability

Payable Upon Disability

While Premiums Are Paid

After Premiums

CeaseDisability income X

CRSP-DC contributions X

J

CPP Benefits: Death of Clergy

Payable Upon Death of Clergy

While Premiums Are

Paid

After Premiums

CeaseLump sum benefit:

Active/disabled clergy death X

Retired clergy death X

Annuity benefits:

Minimum survivor’s pension X

Child income X

Child education X

J

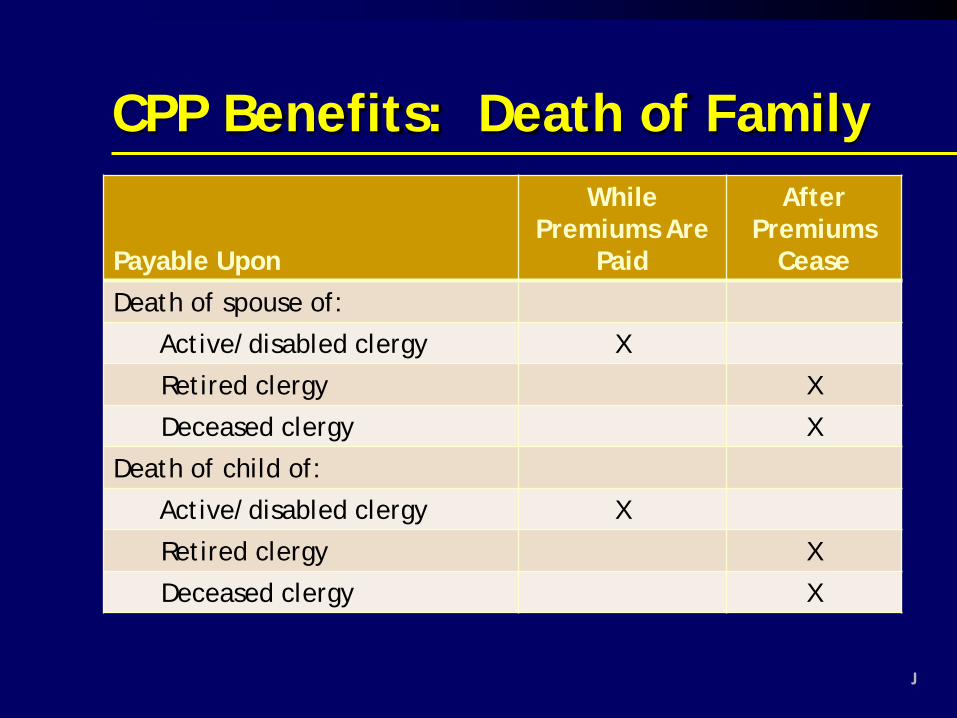

CPP Benefits: Death of Family

Payable Upon

While Premiums Are

Paid

After Premiums

CeaseDeath of spouse of:

Active/disabled clergy X

Retired clergy X

Deceased clergy X

Death of child of:

Active/disabled clergy X

Retired clergy X

Deceased clergy X

J

CPP vs. Typical Programs

• CPP provides far greater coverage than the typical life and disability program both in terms of the type of benefits provided and the guaranteed coverage of spouses and children.

• Another unique feature of CPP is the long time horizon and process in effecting changes to either premiums or benefits.

• Benefits and premiums for most life and disability benefit programs at private plan sponsors are guaranteed only one year at a time.

T

CPP vs. Typical Programs

• Previous actuarial studies have established that a market rate for the CPP program, starting new, would be approximately 4.5% of compensation compared to the pre-holiday rate of 3%.

• While historical asset levels have enabled a recent premium holiday, this is not sustainable longer term.

• The future sustainability of current benefits and the 3% premium is highly contingent upon strong investment returns and conclusion of the premium holiday.

T

Premiums and Benefit Payments

* ProjectedL

Premium Ratio

• The portion of future benefit payments that future premiums are expected to cover

• If less than 100%, CPP contributions will not be enough to pay for benefits due from the plan

L

Premium Ratio

Without Holiday

With Holiday

L

Minimum Reserve Metric

• The shortfall between expected future benefit payments and expected future premiums

• Compare to current assets

T

Minimum Reserve Illustration

Future Benefits

T

Minimum Reserve

Future Contributions

Minimum Reserve Illustration

Future Benefits

T

Target Reserve Metric

• CPP is likely to endure* most market outcomes over the next 6-7 years

• 175% of Minimum Reserve

• Compare to current assets

* To maintain assets above Minimum Reservewithout adjusting either premiums or benefits

T

Rate Action Reserve Metric

• CPP is likely NOT to make ends meet over time

• Petition General Conference to raise premiums*, lower benefits, or both

• 80% of Minimum Reserve

• Compare to current assets

* General Conference action is required to raise premiums above 4.4% T

Assets and Reserve Metrics

Assets

Minimum

L

Assets and Reserve Metrics

Assets

Target

MinimumRate Action

L

1-800-851-2201www.gbophb.org