CPA Report 2nd Quarter 2011

21

CPA Report CPA Report South Carolina Association of Certified Public Accountants Second Edition 2011 Meet James Etter, New Director of DOR Why IFRS Matters Now Community Banking Perspective

-

Upload

south-carolina-association-of-cpas -

Category

Documents

-

view

232 -

download

5

description

CPA Report 2nd Quarter 2011

Transcript of CPA Report 2nd Quarter 2011

CPA ReportCPA ReportSouth Carolina Association of Certified Public Accountants

S e c o n d E d i t i o n 2 0 1 1

Meet James Etter, New Director of DOR

Why IFRS Matters Now

Community Banking Perspective

South Carolina CPA Report 2 (888) 557-4814 | www.scacpa.org South Carolina CPA Report 3(888) 557-4814 | www.scacpa.org

In This Issue

In Every Issue

OfficersTimothy L. Baker, cPA, President

Michael r. Putich, cPA, President-elect

sharon e. Mann, cPA, Vice President

Malynda M. Grimsley, cPA, Secretary-Treasurer

charles e. “eddie” Brown, cPA, Past President

BOArD Of DirecTOrsWilliam R. Barefoot, CPAPatrick P. Carey Jr., CPA

Clarence Coleman Jr., CPA, Ph.D.Mark S. Crocker, CPA

Alys Anne Dennis, CPAJ. Bratton Fennell, CPA

Cheryl O. Lang, CPAPenny A. Lewis, CPA

A.D. “Dave” Masters, CPAJ. Patrick McDermott, CPA

James W. McIlrath, CPAPhilip R. Snipes, CPA

Michael J. Targia, CPA, CFARobert M. Tilton, CPABeth T. Zamorski, CPA

eXecUTiVe DirecTOr Erin P. Hardwick, CAE

MANAGiNG eDiTOrsAllison K. Caldwell

Maureen Taylor

GrAPHic DesiGNer Lisa S. McGee

cONTriBUTiNG wriTersReva Brennan, MPA, CAE, IOM

Allison CaldwellWilliam M. Grooms, CPA, Ph.D.

Erin P. Hardwick, CAEMark T. Hobbs, CPA, CFF

Derrick B. Stark, CPAMaureen Taylor

Dr. Laura D. Ullrich

2011 eDiTOriAL BOArDCharles E. Alvis, CPA, MPA, MBA, Chair

Ellen K. Adkins, CPA, MBAJohn B. Brantley, CPA

Neil A. Brown, CPA, MAcc, CFPAmanda S. Colgate, CPA

Lisa S. Cooke, CPAErin P. Hardwick, CAEKaren A. Hursey, CPALesley H. Kelly, CPA

Margaret L. Lattimore, CPAMarsha G. LePhew, CPAAnthony G. Masino, CPAA. D. “Dave” Masters, CPA

Derrick B. Stark, CPAVictor C. Webster, CPA, MBA

South Carolina Association of Certified Public Accountants Magazine

Volume 41, Second Edition 2011

Statements of fact and opinion are made by the authors alone and do not imply an opinion on the part of the officers or members of the SCACPA. Advertising rates will be furnished on request to SCACPA, 570 Chris Drive, West Columbia, SC 29169, (803) 791-4181. Publication of an advertisement in The CPA Report does not constitute an endorsement of the product or service by The CPA Report or the SCACPA.

CPA ReportSouth Carolina Association of CPAs

Charleston 2430 Mall Drive, Suite 360 Greenville

843-884-3912 Charleston, SC 29406 864-245-8788

www.american-pensions.com

5 From the President

6 Association News

8 On Your Behalf

24 Board of Accountancy News

27 Member Profile Doug Warner

29 Welcome New Members

31 Member News

32 Chapter Connections | Chapter Profile Kara Shealy

34 Upcoming CPE

38 Classifieds/Advertiser Index

9 Tax Tuesday Feedback

10 State of the South Carolina Economy

13 Financial Outlook 2011: A Community Banking Perspective

14 Meet James Etter, New Director of DOR

16 Why IFRS Matters Now

18 Calling Star Students | Support SCACPA’s Education Fund

20 Workplace Leaders in Financial Education Awards

20 Young CPA Leadership Academy Nominations

21 SCACPA’s Blue Ribbon Panel Update

22 Major Provisions of the Health Care Reform Act

COALITION FOR PRIVATE COMPANY STANDARDS

In conjunction with AICPA’s efforts for private company financial standards, SCACPA is seeking volunteers to serve on a coalition that will be advancing this issue. Volunteers should be a preparer or user of financial statements, an auditor or a lender. This task force will develop and execute a plan to educate South Carolina CPAs about the issue and spearhead a letter-writing campaign to advocate for a separate set of financial standards for private companies. If you are interested in serving, please send your contact information along with a brief description of your credentials to SCACPA Executive Director Erin Hardwick, [email protected].

Many of our members in industry have passed their busiest season with year-end activities, and our many

practitioners are counting down their last days of tax season. During this very active time of year, our fantastic SCACPA staff has also been hard at work. Here are a few of the latest happenings and what we can do to get involved:

• Blue Ribbon Panel on Private Company Report-ing. The latest in this piece of profession news is that the Panel’s final recommenda-tions have been made to the Finan-cial Accounting Foundation (see page 21 for more information). I will be appointing

a task force to assist with advancing this issue and need your help — please see the sidebar on this page to learn more. SCACPA will be asking each CPA that prepares or uses small company financial statements to write a personal letter in support of differential standards and a separate standard-setting board. We also ask that you reach out to your clients and request that their CFO, CEO or other significant user (such as a banker) write a letter of support.

• Past SCACPA President John Camp, Executive Director Erin Hardwick and I met in February with Catherine Templeton, the new director at the South Carolina Department of Labor, Licensing and Regulation (LLR). We discussed the workings of LLR and the changes she is making. As you are aware, LLR is the administrative arm of our state government that administers the South Carolina Board of Accountancy. SCACPA has a long-standing relationship with the Board of Accountancy and LLR, and it is important to maintain a good working relationship. We will be monitoring the changes in LLR and how it affects the BOA, our profession and the citizens of South Carolina.

DOr MeeTiNGp L-R: Darren Hardin, Jason Sweatt, DOR Director Jim Etter, Erin Hardwick, Mark Hobbs and Todd Dailey at the South Carolina Department of Revenue.

South Carolina CPA Report 5(888) 557-4814 | www.scacpa.org

Aon Insurance Services is a division of Affinity Insurance Services, Inc.; in CA, MN & OK, (CA License #0795465) Aon Insurance Services is a division of AIS Affinity Insurance Agency, Inc.; and in NY, AIS Affinity Insurance Agency.

One or more of the CNA companies provide the products and/or services described. The information is intended to present a general overview for illustrative purposes only. It is not intended to constitute a binding contract. Please remember that only the relevant insurance policy can provide the actual terms, coverages, amounts, conditions and exclusions for an insured. All products and services may not be available in all states and may be subject to change without notice. CNA is a registered trademark of CNA Financial Corporation. Copyright © 2011 CNA. All rights reserved. E-5929-0411 SC

Endorsed by: Endorsed by: Underwritten by: Nationally Administered by:

Don’t get backed into a cornerwith a malpractice claim

Cover your firm with professional liability insurance.

There’s a way out with the AICPA-endorsed Premier Plan.

Contact Charles Cauthen at BB&T Insurance Services, Inc. today.(800) 868-3721 or (704) 954-3033

As a CPA, you work too hard to let a malpractice claim ruin your business.The AICPA-endorsed Premier Plan can provide your firm with broad coverage and a comprehensive risk control program designed to help your firm reduce its risk of claims. Our plan offers insureds:

• A risk control hotline with specialists who provide advice

• Training in three convenient formats: live seminar, webcast or online self-study

• Online policyholder resource center, which offers engagement letter guides, 14 sample engagement letter templates, case studies and other useful tools to assist your firm

In the event that you do incur a claim, the Program provides insureds experienced claims management. CNA, the Plan

underwriter, insures over 25,000 firms and has handled more than 14,000 accountants malpractice claims

and potential claims over the past 10 years.

NEW! 5% Premium Credit to AICPAPrivate Companies Practice Section

(PCPS) Members!

E-5929-0411 SC_E-5929-0411 SC 3/23/11 10:32 AM Page 1

Timothy L. Baker, cPA, ciTP, cMA2011 SCACPA President

SCACPA member since 1994

• A cadre of tax professionals along with our executive director also met recently with the new director of the state Department of Revenue, Jim Etter (see page 14 for an interview with Jim). As with LLR, this was a relationship-building meeting to ensure there is open communication between the agency and SCACPA. We hope this results in enhanced working relationships between SCACPA members and the agency.

• The annual Tax Guides for state legislators were distributed to the General Assembly on February 23. SCACPA staff and 10 SCACPA members participated. The production and delivery of these guides is another way SCACPA seeks to keep CPAs on the forefront with our elected officials.

• The Association’s strategic plan implementation is under way. Several related task forces are working to achieve the goals and objectives, as outlined in the plan. Stayed tuned as we report activities and accomlishments that evolve from this multi-year process.

I’d like to thank each of our volunteer members for all you do to help SCACPA meet its obligations to our members and the profession. As always, I welcome your input and feedback as valued members of SCACPA. Please let me hear from you on how we can meet your professional needs better. n

Timothy L. Baker, CPA, CITP, CMA, is vice president of consulting for Blytheco, LLC. He can be reached at (803) 612-7500 ext. 2641 or via email at [email protected].

South Carolina CPA Report 6 (888) 557-4814 | www.scacpa.org South Carolina CPA Report 7(888) 557-4814 | www.scacpa.org

570 Chris Drive, West Columbia, South Carolina 29169(803) 791-4181 or Toll-free (888) 557-4814

Fax (803) 791-4196 | www.SCACPA.org

With the changes in the 2009 revised standards, be sure that your firm is prepared. Whether this is your firm’s first peer review or your review date is approaching, this course will help ensure you are ready.

JULY 21, 2011 Upcoming Peer Review: Is Your Firm Ready? (73611A) What does it take to have an effective quality control system that leads you to a clean, pass peer review report? Find out how to prepare for your next review and what can be done on a daily basis to create a strong quality control environment for your firm.

Level: Intermediate Credit: 8Leader: Mark T. Hobbs, CPA Area: A&ALocation: SCACPA – West ColumbiaNotes: Accepted for CMA and CFM credits; AICPA Discount: $30.Fees: Early Bird $210, Member $235, Nonmember $310

To register for this course visit www.scacpa.org/peerreview.

SCACPAscAcPA welcomes Maureen Taylor

Get the conversation Going — start BloggingHave an observation, commentary, link to a website or article you’d like to share with your peers? The SCACPA blog is the perfect place to connect. Short for web log, a blog is a website where individuals can post periodic entries and readers can comment. Whether you’re an expert on a particular subject, concerned about the current fiscal crisis or want to take a stand on a legislative issue, why not get started today? Sign up to be a SCACPA guest blogger.Staff contact: Emily Allen, ext. 106

is YOUr firM reADY fOr Peer reView?

Maureen Taylor has joined SCACPA as member services manager. Maureen is responsible for leading and managing SCACPA’s member services including membership recruitment

and retention, benefits and outreach programs. Maureen also oversees SCACPA’s quarterly magazine, the CPA Report. She serves as staff liaison for the Accounting Careers/Academic Relations Task Force, the Benefits Committee, the Membership Committee, Editorial Board Task Force and the Financial Literacy Task Force.

Maureen has over 25 years of experience in the nonprofit sector. She most recently served as program director of the South Carolina Business Initiative/Women’s Business Center where she counseled entrepreneurs on launching or growing a business with a focus on marketing. A native of Pittsburgh, Maureen is a graduate of Ohio University. She enjoys spending time with her family, boating on Lake Murray and motorcycling (with her husband) along South Carolina’s back roads.

South Carolina

CPASouth Carolina Association of Certi�ed Public Accountants

Peer Review SeminarsJuly 21 ∙ August 23-24 ∙ August 25 | West Columbia, SC

Aim High

pFor more information on peer review courses visit www.scacpa.org or request a Peer Review brochure by contacting April Cox at extension 110.

Get current on the most significant issues affecting the CPA profession in these interactive, multimedia programs held exclusively for members of SCACPA. Providing four hours of FREE CPE in eight communities across South Carolina, these events will give you up-to-date information, insight and analysis. Attendees will also have an opportunity to make their opinions count. There will be a variety of ways for you to give feedback on the top issues that make a difference in your day-to-day operations. Save the dates and join us for 2011 PIUs. Staff Contact: Sandra Oxner, ext. 112, or visit www.scacpa.org/PIU

AUGUsT

25 Florence: Southeastern Institute of Manufacturing (SIMT) 12:30 - 4:40 p.m.

26 Myrtle Beach: Horry Georgetown Tech – MB Campus 8:30 a.m. - 12:10 p.m.

sePTeMBer20 Rock Hill: Baxter Hood Center 12:30 - 4:40 p.m.

23 Columbia: Radisson Hotel 8:30 a.m. - 12:10 p.m.

29 Charleston: Embassy Suites – Convention Center 8:30 a.m. - 12:10 p.m.

30* Hilton Head: Palmetto Electric Cooperatve 8:30 a.m. - 12:10 p.m.

*Sea Island Chapter to present four hours of afternoon CPE after morning PIU.

NOVeMBer 10 Spartanburg: Converse College 12:30 - 4:40 p.m.

11 Greenville: Embassy Suites 8:30 a.m. - 12:10 p.m.

2011 Professional issues Update series

South Carolina CPA Report 8 (888) 557-4814 | www.scacpa.org South Carolina CPA Report 9(888) 557-4814 | www.scacpa.org

First Quarter Report

For the profession, by the profession—that’s what the South Carolina Association of CPAs is all about. SCACPA’s board of directors, committees and task forces and Young CPAs Leadership Cabinet are hard at work making decisions, providing guidance and embarking on projects and programs that strengthen the profession and enable members to improve their knowledge, network and technical skills.

rePOrT frOM scAcPA BOArD MeeTiNGThe SCACPA Board of Directors met January 21 in Columbia. Among many items of business, the board focused much of its time on legislative and policy issues.

Private Company Financial Standards: President-elect Michael Putich briefed the board on the work of the Blue Ribbon Panel and led a discussion about it. The Blue Ribbon Panel was sponsored by FAF, the AICPA and the National Association of State Boards of Accountancy to develop policy recommendations for private company financial standards. A report containing the panel's recommendations for a new separate standard-setting board and for modifications to U.S. GAAP to recognize the unique needs of private company financial statement users was submitted to Financial Accounting Foundation (FASB’s parent organization) in late January. A proposal for public comment is expected to be released this spring. CPAs, lenders and other users, private companies and small business owners are encouraged to be engaged in this critically important initiative to help transform the recommendations into reality.

The SCACPA board supports the creation of private company financial standards and will launch a letter-writing campaign later this year. There will also be efforts to develop

a state coalition of organizations representing CPAs, bankers and businesses to strengthen these efforts.

Legislator Award: The SCACPA board approved the creation of a new award — a state legislator award that will recognize elected officials who have gone the extra mile to help SCACPA in its legislative work. Criteria for the award is now being developed.

The Young CPAs Leadership Cabinet: Immediate Past Chair Leigh Schaefers attended the board meeting and presented the cabinet’s 2010 activities and accomplishments. The YCPAs first Emerging Leaders Conference was a success and a second conference is being planned now for August 18-19, 2011.

ADVOcAcY AT wOrK iN 2011 The Legislative and Advocacy Committee, Key Person Contacts, SCACPA staff and lobbyists were quite busy during the first quarter of 2011. Here are a few highlights.

SC DEW and Payroll Reports: Late in 2010, the S.C. Department of Employment and Workforce distributed a notice announcing a new deadline for quarterly payroll reports. The new deadlines fell on the 15th day following the end of a quarter. Needless to say, this posed a serious work-compression issue

for CPAs working in tax. SCACPA’s Legislative and Advocacy Committee drafted a detailed letter to SC DEW (which was posted on www.scacpa.org) explaining why this change was implausible. SC DEW also heard from many CPAs directly. As a result, the agency decided not to pursue the regulation change that would have imposed a new deadline for quarterly payroll reports. This was certainly a victory for the profession.

SC DOR and PT-100s: Also in late 2010, the S.C. Department of Revenue announced a change in how property tax form 100 is to be filed. Starting in 2011, all PT-100 forms are to be filed through the S.C. Business One-Stop (SC BOS) system. While most SCACPA members embrace technology and agree that electronic filing is the right path, many were surprised by this change and are not prepared to e-file the PT-100s returns this year. Filing PT-100s through the SCBOS system, while developed for the individual filer, can be adapted by third party preparers, like CPA

firms. Following several meetings and conversations with DOR staff, SCACPA released information in March that gave CPAs and their firms options for handling PT-100s. See SCACPA’s website for more information.

Tax conformity: Each year SCACPA works to ensure tax conformity legislation is passed early in the year in order to provide tax professionals with the certainty they need in completing their client work. And 2011 is no different, except that legislative maneuvering, particularly in the senate, delayed attention on tax conformity for nearly a month. As a result, tax conformity passed later than hoped for. SCACPA is optimistic that over time, state legislators will understand more clearly the importance of tax conformity and this annual effort will become streamlined. n

Erin P. Hardwick, CAE, has served as SCACPA’s executive director since 2005. She has more than 25 years of experience in association and nonprofit executive leadership and is one of 18 Certified Association Executives

in South Carolina, the highest credential in the association management profession. She currently serves as secretary/treasurer of the CPA Society Executives Association, and a member of the S.C Secretary of State’s Nonprofit Advisory Council and the S.C. Council on Economic Education Board of Directors.

scAcPA Members field Viewer calls During Tax Tuesday

SCACPA members volunteered their time and knowledge recently to man the phones during Tax Tuesday on WIS-TV, Columbia. Bill Grooms, Leon

Maginnis, Caroline D. Strobel, Philip Betette, Tripp Newsome and Tommy Bryson fielded over 200 viewer calls during a two and a half hour period. While all agreed it is difficult for practicing CPAs to get involved during tax season, the consensus was that they would do it again. SCACPA asked the Tax Tuesday team to share their experience and some of the more unusual questions they received.

wHAT TYPes Of issUes DiD Viewers AsK ABOUT?• People receiving only social-security income wanted to know whether or

not they were required to file. • Questions related to retirement plans (how to report distributions, early

withdrawal penalties, maximum contribution amounts, etc.).• Filing questions: head of house, married filing separate.

wHAT wAs THe MOsT UNUsUAL QUesTiON YOU receiVeD?• A person who won the lottery in Georgia and lived in South Carolina

wanted to know which state they should file. • Callers wanting to take dependency exemptions for grown children who

are unemployed and living with them.

wOULD YOU eNcOUrAGe YOUr feLLOw scAcPA MeMBers TO GeT iNVOLVeD NeXT YeAr?• Yes, it is an excellent way for the profession to give back to the community.• It is a good experience and sort of gets you into the real tax world. It is nice

to get away from AMT.

HOw wOULD YOU DescriBe YOUr OVerALL eXPerieNce?• Very positive. The studio personnel were very cordial and helpful. I

enjoyed talking with my fellow CPAs, and I enjoyed helping the callers with their questions.

• It is very interesting to see what situations drive the taxpayers’ decisions. For this year, in my opinion, the biggest problems are unemployment and dependency on family as a result of unemployment, and the elderly who do not need to file but are confused about the tax credit associated with Social Security.

p L-R: Phil Betette, Tripp Newsome, Leon Maginnis, Caroline Strobel, Tommy Bryson and Bill Grooms at WIS-TV Columbia for Tax Tuesday.

“The SCACPA board supports the creation of private company financial standards and will launch a letter-writing campaign later this year.”

“Tax Conformity was signed into law by the governor on April 11.”

South Carolina CPA Report 11(888) 557-4814 | www.scacpa.orgSouth Carolina CPA Report 10 (888) 557-4814 | www.scacpa.org

by Dr. Laura D. Ullrich

for the past two years, i have consistently heard people call the recession we recently endured — and the recovery we are currently in — “different.”

i totally agree and think that most people, whether they are economists or not, recognize that this recession was not your standard economic downturn.

For the past two years, I have consistently heard people call the recession we recently endured — and the recovery we are currently in — “different.”

I totally agree and think that most people, whether they are economists or not, recognize that this recession was not your standard economic downturn. Many people also understand that although we are indeed recovering from an economic growth perspective, the unemployment rate is not falling as quickly as is generally expected post-recession. What I don’t think people fully grasp is why it was, and is, different. While there are many reasons why the most recent recession and recovery stand out from others, I will focus on a few explanations that I think are important in explaining the velocity of both, especially here in South Carolina.

Recessions begin for many different reasons. We expect there to be natural peaks and troughs within the business cycle, and specific events, such as an oil crisis or an event like September 11, can escalate an economy’s tendency towards these cyclical movements. The recent recession was driven by many factors, but the one that has gained the most attention over time was the housing boom seen across the United States.

According to Freddie Mac’s CMHPI, South Carolina’s housing prices increased 28.7 percent between the first quarter of 2004 and the second quarter of 2008 (the peak of home prices in South Carolina). Since the second quarter of 2008, home prices have fallen 5.4 percent. This compares to a national increase of 25.2 percent, and a subsequent decrease of 8.1 percent, over the same time period. While many other states have had housing crises more significant than ours (Arizona, Nevada and other “sand states”), the downturn in the housing and related industries has been extremely harmful to the South Carolina economy. At this point, housing prices are continuing to fall in many

South Carolina counties even as the overall economy is expanding, thus leading to a muted recovery. Until the trend of falling home prices and high vacancy rates ends, economic growth will remain slower than would typically be expected absent this phenomenon. This will likely take several years as excess supply is absorbed into a naturally growing economy.

State government issues have also played a significant role recently and have led to slower recoveries than previously seen. South Carolina has maintained one of the highest unemployment rates in the country throughout the recession and the recovery, along with states like Nevada, Michigan and California. It may not be clear why South Carolina belongs in the same crowd as states that have faced well-known economic challenges. However, the issues specific to South Carolina are very serious — they simply fly a little more under the radar and may not be as recession-specific as the other states with high unemployment.

In 2006 Act 388 was passed, which represented a sweeping change to the property and sales tax system in the state. The law was then phased in between 2006 and 2008 right as the recession began. Act 388 was essentially a tax swap, eliminating school taxes on owner-occupied housing and increasing the state sales tax rate by one cent (and removing the sales tax on unprepared food). While this policy may not have been a solid choice for tax policy regardless of the time frame, the timing of the phase in was terrible.

In general, property tax revenues are one of the most stable local tax revenues during an economic downturn. Sales tax revenues, on the other hand, are one of the least stable. Swapping a stable revenue source for an unstable one resulted in a significant gap between the potential

According to Freddie Mac’s CMHPI, South Carolina’s housing prices increased 28.7 percent between the first quarter of 2004 and the second quarter of 2008 (the peak of home prices in South Carolina). Since the second quarter of 2008, home prices have fallen 5.4 percent.

BY THE NUMBERS

The recent recession was driven by many factors, but the one that has gained the most attention over time was the housing boom seen across the United States.

South Carolina CPA Report 12 (888) 557-4814 | www.scacpa.org South Carolina CPA Report 13(888) 557-4814 | www.scacpa.org

revenue absent Act 388 and the level of revenue that has been collected since that time. As we move towards more steady economic growth sales tax revenues will become more stable, but they are unlikely to exceed the revenues that could have been collected absent the tax change. This policy modification was responsible for a significant percentage of the revenue losses across the state, and undoubtedly makes South Carolina’s economic recovery different, especially for K-12 education, which relied heavily on the property taxes that were eliminated.

Another very significant current issue in South Carolina is our underfunded state pension program. The South Carolina defined benefit system is currently underfunded by a staggering $13 billion. Even more concerning, for current policy, is the $88 million deficit the fund faces in this year alone. This means that $88 million must be taken out of the South Carolina budget and spent on the underfunded pension program rather than funding the public services and programs that the money was originally allocated for. Both of our neighboring states, North Carolina and Georgia, have fully-funded pensions and have been able to keep their spending on state supported programs at more stable levels than is possible at this time in South Carolina. There is no doubt that the pension shortfall will result in lower spending on K-12 and higher education, as well as spending on healthcare, prisons and other state supported programs.

For these and many other reasons, the recent recession and recovery are indeed different. Until the problems underlying the restrained growth patterns are remedied, the South Carolina unemployment rate will likely remain higher than we would see under a typical recovery. The good news is that the overall economy is on the mend, and South Carolina’s economy is currently growing at a rate higher than the national average. If we can make some important and politically brave changes, much brighter days will certainly be on the horizon. n

Dr. Laura Dawson Ullrich is an assistant professor of economics at Winthrop University in Rock Hill. Originally from Athens, Georgia, she holds a Bachelor of Business Administration in Economics from the University of Georgia and a Master’s and Doctorate in Economics from the University of Tennessee. Her research interests include school finance reform, local and state level tax and expenditure analyses, and welfare policy.

When Brian and Laura Ullrich started dating at age 19, they had already known each other for 18 years. Both

grew up in Athens, Georgia and attended the University of Georgia. Brian had dreams of becoming a CPA and Laura dreamed of one day becoming a CEO. They knew they both wanted a family, and they both wanted rewarding careers. They also knew that this wasn’t always an easy balance. Four years later, shortly after getting married in 2001, Laura decided that she wanted to go back to school and become an economics professor. The next six years were a blur as Brian became a CPA, Laura finished her masters and Ph.D. in Economics, and they brought two sons, Dawson and Reed, into the world.

In 2007, Laura and Brian moved to Rock Hill. Laura began her academic career at Winthrop University, and Brian joined Burkett Burkett Burkett’s Rock Hill office. They have since adopted son number three, Allen, and enjoy being involved in their local church, running road races and spending time together as a family. Their oldest two boys are active in soccer, basketball, gymnastics and Cub Scouts. Life is incredibly busy and incredibly fun!

Having two tax professionals in one household has been a tremendous blessing to both Brian and Laura. They are interested in the same things, just from different angles. Laura specializes in tax policy and incidence issues, while Brian sticks to corporate and individual tax compliance. Although their degrees and specializations differ, they often consult each other on policy, law and what future tax policy may look like. They certainly feel as though their clients and students benefit from the knowledge that they share, and love having a spouse who doesn’t mind a lot of ‘tax talk.’ n

Tax Talk: A family Matter

p Laura and Brian Ullrich with their three boys. (Photo by Andrea Berry Photography.)

MIKE CRAPPS, PRESIDENT/CEO, First Community Bank: We reflect the successes and the challenges of our customers and communities. I hear stories of some businesses seeing improved activity, some feeling as though things have stabilized, and, unfortunately, some indicating that business is still declining. Overall, I feel as though the business climate has stabilized and shows signs of very gradual improvement. First Community Bank will continue its commitment to assisting local businesses and professionals achieve their financial goals. As our customers become more successful, our local economy will be enhanced.

CRAIG NIX, CFO, First Citizens Bank:Two recent signs indicate that the local economy is starting to recover: a decline in unemployment rates and a slight rise in consumer spending. Long-term unemployment continues to be a challenge, and we see very little forward momentum in the housing market. It will take time to absorb the excess supply of houses, and sustained GDP growth [is needed] to meaningfully move the unemployment rate down to pre-recession levels. We’re well-positioned to face these headwinds due to our strong capital and liquidity position. First Citizens will help boost the local economy by helping customers meet and exceed their financial goals. We’ll continue making loans to local residents and businesses, providing customers with products and services that meet their needs, and being a valued corporate citizen in our communities.

ricK sAUNDers, PresiDeNT/ceO, First Reliance Bank: Until we create jobs, not much will change in the near future. South Carolina has a relatively inexpensive work force, solid infrastructure and a port, and the state’s leadership [is] working hard to promote these assets. The Boeing plant in Charleston has a positive impact on that region. Columbia is more government-based, so while it has been fairly stable we expect more budget cuts to put greater pressure there. The Pee Dee area has seen higher unemployment than other markets, but is improving slightly. We expect continued improvement in 2011, but modest at best.

JUSTIN STRICKLAND, PRESIDENT/CEO, Southern First Bank: I’m not sure [that] the economy is recovering as much as stabilizing. A reduction in unemployment numbers is the key component reflecting a recovery. We’re also closely watching the housing market — an increase in building permits would reflect an economy that has absorbed the abundance of excess housing units, and a demand for new units. We expect to continue to grow our company profitably [this year], and that means making quality loans and expanding our client base. The pace of economic recovery and the level of continued regulatory restrictions will be key points for the ability of community banks to expand in 2011.

JOHN WINDLEY, PRESIDENT/CHIEF BANKING OFFICER, South Carolina Bank and Trust: We’re seeing a slight uptick in loan demand, which indicates some improvement in overall consumer confidence. We’ve also seen improvement in past due or “problem” loans. When an economy starts to recover, past due ratios turn down. We’re cautiously optimistic about these early signs — nothing dramatic, but we are seeing slow improvement overall. We’re constantly looking for opportunities to lend money. We’ll try to increase these opportunities in 2011, thereby becoming more successful in growing our customer base and attracting new customers. As local economies improve, we’ll definitely be playing a part. n

Financial Outlook 2011

by Allison Caldwell

A Community Banking Perspective

The nation’s economy may finally be showing signs of life, but much still needs to happen before economic recovery is strong and sure. Here in South Carolina, the leaders of several locally-headquartered banks say that even

though they’ve struggled like everyone else, their institutions and the communities they serve have managed to weather the storm. They offer a cautious but optimistic financial outlook from the community banking perspective.

What signs indicate that local economies are starting to recover, or what will you be looking for most towards that end?

Excerpted from articles published in the February 2011 issues of Greater Columbia Business Monthly and Greater Pee Dee Business Journal, www.columbiabusinessmonthly.com and www.greaterpeedeebusinessjournal.com.

South Carolina CPA Report 14 (888) 557-4814 | www.scacpa.org South Carolina CPA Report 15(888) 557-4814 | www.scacpa.org

You were appointed by Gov. Haley in January as the new director of the south carolina Department of revenue. Briefly describe your professional background and service specialties leading up to this position.

Etter: After receiving my bachelor’s and master’s degrees in business administration from the University of Cincinnati, I joined Arthur Young & Company in the Cincinnati office. I was promoted to senior auditor after one year and worked mostly on manufacturing or financial audits. After four years, I was transferred to Tokyo as an audit manager and worked on U.S. publicly traded clients that had major operations

in Japan or Korea. I returned to the states as an audit manager in the Charlotte office.

I joined Abbott Laboratories as director of international internal auditing; then moved to Puerto Rico as a group controller and then back to Chicago as director of Corporate Financial Analysis. I was then recruited to join Sam Solomon & Company in Charleston, S.C. as chief financial officer. After Sam Solomon was sold, I worked with several private companies in Charleston, including real estate operations, as their CFO and/or chief executive officer.

I then was recruited to head up a new real estate investment trust in Denver to take them public. That process took approximately two years. The company grew and was later sold to a private real estate group. I returned to South Carolina and worked as a consultant or employee for several small companies that needed my skill set to help identify areas that needed improvement both in operations as well as accounting issues. I was also appointed by the federal bankruptcy court to assist the bankruptcy trustee in administering the research and liquidation of the assets for the HomeGold case.

what about your past experiences has prepared you to lead a state agency, and what do you hope to accomplish?

Etter: Public accounting, both domestically and internationally, gave me a breadth of experiences that enabled me to quickly evaluate situations and opportunities that would help improve overall operations and hopefully improve various companies’ bottom line. The variety of experiences included very large (Fortune 50) as well as very small companies, private as well as publicly traded. These experiences helped me to develop a skill set that will enable me to help manage the Department of Revenue efficiently and effectively. My firsthand experiences dealing with the Department of Revenue from a nongovernmental point of view give me a perspective to better relate to the taxpayers as a whole.

The Department of Revenue is one of the best run agencies in the state, so to make major changes in the way the department runs is not an overriding goal. However, every organization can be improved as conditions change and new legislation is enacted. New technological changes always require changes in how the agency operates and interacts with the taxpayer. Efficiencies in operations will be a primary goal in years to come. Making the department user friendly and impartial in its dealings with taxpayers is an important objective for all concerned.

what areas and issues will be top priority in 2011? As cPAs in particular, what should our members be aware of in the near future? How do you envision working with the cPA profession to advance common areas of interest?

Etter: The one main area where I see the department and CPAs working closely together is the feedback the DOR can receive from CPAs, individually and as a group, as to issues that are causing taxpayers problems in filing returns — not only in content, but the forms themselves. I understand well that small filers have difficulty in understanding the content and the process in filing all the required tax forms. Another area where we can benefit each other is in training and seminars. The DOR would be glad to participate in CPE courses that SCACPA sponsors for CPAs and others across the state.

As a finance executive and former cPA, what made you choose the accounting/financing field? what do you enjoy most about what you do?

Etter: Choosing accounting/finance as a profession was the result of a dedicated junior high school teacher. He

An Interview with James Etter

New DOR Director Seeks to Make Agency More User-Friendly

taught general business as a one semester course. I had no prior inclination or interest in business as a career. As he presented the material, he introduced the class to many of the opportunities in the business field, and becoming a CPA was one that he stressed as being very rewarding. I then took a basic bookkeeping course and thoroughly enjoyed the challenge; thus started a journey in accounting/finance.

The most enjoyment during my career has been in treating each opportunity as a clean slate or canvas with the opportunity to start from fresh and create an efficient organization that would benefit the stakeholder and organization as a whole.

Tell us about your family, hobbies, favorite activities—what you do for fun.

Etter: I have four children, two daughters-in-law, one son-in-law and seven grandchildren. Having lived overseas twice, we are an international family with three of our kids born overseas and three of our grandchildren born overseas. My hobbies include golf and woodworking. n

Columbia Charlotte Charleston Greenville Raleigh Myrtle Beach

Experience. Service. Results.

mgclaw.com

At MG&C, our experienced professionals are committed to excellent service and innovative solutions for diverse legal and business challenges.

Under Gov. Nikki Haley’s administration, South Carolina’s state agency directors are tasked with making their organizations more business-friendly and responsive. For South Carolina CPAs, the Department of Revenue (DOR) has a direct impact on the profession as a whole as well as the clients they serve. SCACPA recently asked James Etter, director of DOR, how his professional background has prepared him to lead the agency and what his priorities are for the coming year.

South Carolina CPA Report 16 (888) 557-4814 | www.scacpa.org South Carolina CPA Report 17(888) 557-4814 | www.scacpa.org

by Derrick B. Stark, CPASCACPA member since 1996

Why IFRS Matters Now The general business implications, however, are why a general understanding of IFRS is relevant to us now. Business decisions we are making today may be impacted by material changes to applicable accounting standards, and we must consider the possible scenarios. These might include the following: • For those of us who operate private businesses or

advise others on business operations, how will pending convergence or adoption of IFRS impact contract negotiations or future IT infrastructure development?

• As readers of financial statements, how can we reconcile our hard-coded expectation for conformity with the transitional guidance for IFRS adoption, draw relevant comparisons, and make good strategic business decisions?

• As we move toward the broad, principles-based IFRS, how will the fundamental reversals of event-based, Enron-type rules and standards affect overall business risk?

• Will the migration to disclosure-centric standards increase or decrease our exposure to litigation risk?

BUsiNess OPerATiON iMPLicATiONsAs U.S. GAAP and IFRS move closer to each other via

the long running convergence projects, there will no doubt be cascading business implications.

For example, operating type leases may become a thing of the past. If every lease,

big or small, is subject to capital lease treatment, material changes to the balance sheet assets and liabilities will impact loan covenants, executive bonuses and performance compensation, and tax strategy. As strategists, we have to anticipate likely

convergence and adoption scenarios for contracts executed now.

Moreover, current infrastructure decisions — particularly those related to information

technology — must consider not only the establishment of new standards and reporting

requirements, but the messy duplication of transition and change. Those entities that deal or reasonably expect to deal in the future with non-U.S. parent or subsidiary entities will need applications and hardware that can support both U.S. and international reporting and provide enough flexibility for the rapid change in both. Like office space, we want to have enough capacity when we need it, but not be so foolish as to overindulge.

fiNANciAL sTATeMeNT cONfOrMiTY AND risKAcademically, a singular body of standards for our global economic environment makes sense. Moreover, the idea of broad principles-based standards that permit issuers to exercise sound professional judgment and readers to draw their own conclusions seems more relevant than ever.

And yet, if we can reconcile our comfort in explicit rules with our purpose to present fair and relevant representations about the health and performance of an entity, we must consider the short-term impact on comparative value. For example, IFRS provides mandatory and optional exemptions for initial adopters making it difficult to compare financial statements among companies at various stages of implementation and measure trends of individual companies through the process of adoption.

Consolidations present another twist. Although both standard sets consider the substantive risks and rewards of interrelated entities for purposes of consolidation and reporting, differences in treatment of potential voting rights and finance structures can lead to components that are consolidated in one presentation and not in the other. Even when fully disclosed, the comparative value of financial statements will be diluted as readers find it more difficult to develop norms, predict outcomes and evaluate performance relative to expectations.

Convergence and/or adoption will continue to bring rapid change in the foreseeable future. Although a worthwhile and necessary exercise to reflect global economic interconnectedness, it seems a slippery slope in the near term. Like expanding major roadways that are overwhelmed by population growth, where traffic gets worse before getting better, preparing and using financial statements will surely be more complex for now. Familiarity with IFRS and a general sense of the impact on financial accounting and reporting in the United States will be an important part of our knowledge well before there are specific rules of engagement. n

Derrick B. Stark, CPA, is managing member of ClaraVista LLC, a reimbursement and consulting firm serving home medical equipment suppliers throughout the United States. He currently serves on SCACPA’s Editorial Board Task Force and has previously served on the CPA Ambassadors Task Force, the Business Valuation and Forensic & Litigation Services Task Force and the Young CPAs Task Force.

Business decisions we are making today may be impacted by material changes to applicable accounting standards, and we must consider the possible scenarios.

There is no shortage of insightful writing on the significant differences between accounting principles generally accepted in the United States (U.S. GAAP) and International Financial Reporting Standards (IFRS), the history and road map for convergence between the two,

and the popular inclination that the IFRS world tour is coming to town. If your company or clients transact business with, own, or are owned by non-U.S. entities, you are probably familiar with rules regarding initial adoption and the differences in key issues such as revenue recognition, business combinations and financial statement consolidation, inventory valuation and lease accounting.

South Carolina CPA Report 18 (888) 557-4814 | www.scacpa.org South Carolina CPA Report 19(888) 557-4814 | www.scacpa.org

INDIVIDUAL DONORSWilliam E. Abernethy Jr., CPAClaudia W. Adams, CPAT. D. AinsworthTimothy L. Baker, CPAJohn P. Barber, CPAHenry D. Barnett Jr., CPAS. C. Beckwith, CPA, CFPRoddey C. BellJames B. BlackLois R. Blanco, CPACynthia E. Bolt-Lee, CPA, MSRoger A. Borgmeier, CPABrian J. Brady, CPA, CFF CFE CIADuncan F. Breckenridge Jr., CPAK. Brodie Brigman Jr., CPAChristopher A. Brown, CPAMaurice Brown, CPAWilliam W. Brown, CPAThomas J. Bryson, CPAOrvis B. Buie, CPAMonica A. Burbano de LaraWilliam L. Byrd, CPAJohn F. Camp, CPAPierce W. Cantey, CPARobert D. Capell Jr., CPAPatrick P. Carey Jr., CPARobert B. Carpenter, CPASteven D. Carter, CPAChristine E. Cassidy, CPA, JD, LLMLinda P. Caughman, CPAJan M. Clark, CPAJames B. Cobb, CPADeanna L. Cochran, CPAMarie S. Codinha, CPAMary Jo Cole, CPAClarence Coleman Jr., CPA, PhDChristopher J. Controne, CPARobert C. Cooper, CPAGeorge L. Counts Jr., CPANeil F. Crossley Sr., CPA, PFSRobert A. Curtis, CPA, PFS, MSTAndrew T. Derajtys, CPAJames H. Derrick, CPAJulia A. DuMars, CPA

George W. DuRant, CPA, ABV, ASASpamvetta T. Edwards, CPACimberlie D. Elkins, CPADonald L. Ellis, CPA, MBAMary L. Enright, CPAPhilip O. Espy, CPA, MBABarbara J. Evans, CPA MBAMichael R. Evans, CPAA. L. Fee, CPAJohn B. Fennell, CPAWillie E. Fergusson, CPARyan F. Finklea, CPASusan S. Fitzpatrick, CPACharles R. Fliflet, CPATammy M. Flowers, CPAJennifer N. Gahl, CPAKimberly R. Getz, CPAJonathan I. Godwin, CPADennis L. Gore, CPAHenry D. Green III, CPAMary E. Green, CPAJohn M. Greene, CPARalph M. Greene Jr., CPAAmanda T. Hallman, CPADavid J. Haney, CPAErin P. Hardwick, CAEGary A. Harris, CPAMartha M. Hartley, CPALarry W. Hartsell, CPAAlice B. Hazel, CPARobert M. Heil, CPADouglas W. Henderson, CPAKenneth S. Higgenbotham, CPAJ C. Hincher, CPA MAMark T. Hobbs, CPASamuel G. Holtzclaw, CPALeonard A. Hoogenboom, CPASamuel L. Howell, CPA, MAccM. Timothy Hucks, CPADonna K. Hudson, CPADonald L. Hunter, CPAHarry A. Huntley, CPARichard A. Hutto, CPALeona L. Hydrick, CPA

Arthur L. Jayroe Jr., CPARobert M. Jones, CPAW. K. Jones, CPARichard L. Jordan, CPAKevin C. Kern, CPAMichael J. Kerscher, CPAJames D. Kidd, CPAJeffery E. Kinard, CPASusan J. Kranz, CPADouglas D. Kugley, CPAHolly L. Kyle, CPACheryl O. Lang, CPACarol C. Lawlor, CPAPaula J. Lawrence, CPADavid G. Lewis, CPAPenny Lewis, CPACarol M. Libby, CPADaniel E. Livengood, CPAKenneth E. Love, CPAMichael W. Lowrance, CPA, MBAPatrick M. Luciano, CPARoger F. Luttrell, CPA, MBALarry B. Mack, CPASharon E. Mann, CPABobby T. Mardis, CPALeigh A. Marks, CPAJ T. MasseyGlenn J. Matthews, CPAKaren R. Mattison, CPASheryl G. McAlister, CPA, CFPRenee O. McCall, CPAChristine A. McCarty, CPAChris A. McCraw, CPAJ. P. McDermott, CPAJ. P. McDermott, CPAC. Stephen McDonald, CPAAnn A. McDuff, CPAHenry A. McFaddin, CPAJames W. McIlrath, CPAHunter McKeownSheila C. McKinney, CPACharles L. McLafferty, CPA, PhDSusan P. Miller, CPADavid H. Mims, CPA

Thomas P. Monahan, CPAKenda L. Monroe, CPAJeanne F. Morrisette, CPAFrances Y. Moseley, CPAAlbert A. Munn IV, CPARobert J. Nagy, CPAJames R. Newell, CPAGina S. Noble, CPAJames M. O'Cain, CPA, CFP, CLU, ChFCDonald M. Oates, CPASherry N. Ouzts, CPARenita M. Owens, CPAChristopher A. Paris, CPA, MBASara B. Penn, CPABarbara G. Pierce, CPA, PhD, MPJanet M. Pierce, CPASarah D. Pope, CPAJeffery S. Powell, CPARobert B. Privette, CPA, MBAJoseph E. Pruitt, CPABetsy M. Ragsdale, CPAKelly S. Ramirez, CPAMichael P. Ravan, CPACharles M. Redfern III, CPARenee R. Reid, CPAStephan P. Riley, CPARay L. Roberts, CPAWilliam C. Robertson Jr., CPAWilliam C. Robinson, CPADuncan M. Rogers, CPADeborah M. Rose, CPADel A. Rosebrock, CPAW. T. Rubenstein, CPAAmy H. Rubin, CPAMichael W. Saunders, CPAJanene K. Schmidt, CPA, MBADouglas P. Schmieding, CPATerry K. Schmoyer Jr., CPARuth A. Schult, CPAWilliam E. Sellars Jr., CPAPaul A. Semones Jr., CPAErnest M. Sewell III, CPARobert H. Silvers, CPATeodor D. Simeonov, CPA

Nancy F. Simonetti, CPANancy F. Simonetti, CPAClifford C. Simunek, CPARobert M. Sisk, CPACharles H. Smith, CPAJames B. Snoddy, CPADouglas A. Sparacino, CPACurtis C. Stewart, CPA, JDJames M. Stewart Jr., CPA, MBA, MSTRichard G. Stoeppler, CPAEugene F. Svatek, CPABruce K. Tallant, CPARobert T. Theodore, CPABillie H. Thomas, CPAMark E. Thorne, CPARichard C. Tiller, CPABruce E. Truesdale, CPA, MBAEdgar A. Vaughn, CPADavid R. Veldman, CPADonna G. Waga, CPAAudrey R. Waldrop, CPAMark W. Webster, CPASusan O. Weesner, CPAHarry M. White, CPADavid L. Whitehead, CPAD. Ken Whitener, CPAHowell B. Williams IV, CPAKathy B. Wine, CPAJacqueline C. Wirszyla, CPAAmy L. Wood, CPATom J. Younan, CPAYulien Yuan, CPABeth T. Zamorski, CPA

FIRM CONTRIBUTIONSGMK AssociatesBurkett Burkett & BurkettCentral Chapter of SCACPA

With sincere gratitude for each and every contribution, SCAPCA would like to recognize our 2011 Educational Fund Donors. Your generous support helps to

shape the future of the accounting profession in South Carolina.

2011 Educational Fund Donors Donors through March 30, 2011

As a CPA, what will exist beyond your lifetime? Possibly the firm

or company you work for, or the firm that bears your name. But the common thread among all CPAs is the profession itself. Kept alive by new CPAs, the profession will last long after you’re gone.

The SCACPA Educational Fund, Inc. invites you to consider contributing to the legacy. Honor a senior partner or your firm with a named scholarship. A gift of $10,000 allows you to name a scholarship, given each year to a deserving South Carolina student. This gift may be paid with a one-time payment or, if you prefer, you may

make a pledge of $10,000 and pay it over a three-year period.

What happens once a firm, company or individual makes that $10,000 pledge? It’s time to roll up your sleeves to raise funds, showing true commitment to your cause. One firm pledged $10,000 in honor of their firm’s anniversary. To meet their goal, the firm mailed letters, worked with clients and colleagues and actively spread the word about the foundation’s mission — a successful game plan. They not only met but exceeded their goal.

Our latest fundraising effort is to establish a named scholarship in memory of Francis A. Humphries, a SCACPA member from 1967 until his death in 2008 following a battle with cancer. A life member, Francis served

Support the SCACPA Educational Fund

MAiL DONATiONs TO: scAcPA educational fund, inc.570 chris Drivewest columbia, sc 29169

“It’s time to roll up your sleeves to raise funds, showing true commitment to your cause.”

as president of SCACPA in 1979, was a member of numerous committees and task forces and an active peer reviewer, conducting over 300 reviews through SCACPA’s statewide Peer Review Program. As a member of AICPA, he was a past vice president and a member of the board, and served 10 years on the AICPA Council. A contribution to the Francis A. Humphries Scholarship Fund is a fitting tribute to Francis’ memory and his contribution to the CPA profession.

The SCACPA Educational Fund Inc. is a 501(c)3, so all contributions are tax deductible. A scholarship made possible by your donation will help shape the future of the accounting profession in South Carolina. Contribute to the accounting profession by sending your check today! Staff contact: Glenna Minor, ext. 107

cALLiNG sTAr sTUDeNTs! Now Accepting Scholarship Applications

MAIL COMPLETED APPLICATIONS & MATERIALS TO:

SCACPA Educational Fund Inc.570 Chris DriveWest Columbia, SC 29169

SPREAD THE WORD! The deadline to apply for the SCACPA Educational Fund Inc. 2011-2012 accounting scholarships is Wednesday, June 1, 2011.

Each year the SCACPA Educational Fund awards thousands of dollars in scholarships to deserving accounting students just like you. The amount of the award and the number of scholarships varies depending on the number of qualified applicants. Visit www.scacpa.org to download the scholarship application, which includes the eligibility requirements. All scholarship applications and supplemental materials must be postmarked by June 1, 2011. Staff contact: Glenna Minor, ext. 107

Help Shape the Accounting Profession

South Carolina CPA Report 20 (888) 557-4814 | www.scacpa.org South Carolina CPA Report 21(888) 557-4814 | www.scacpa.org

The past year’s focus on the lack of relevance and increased complexity of information in private company GAAP financial statements culminated in

late January when the Blue Ribbon Panel on Private Company Financial Reporting presented its recommendations to the Financial Accounting Foundation (FAF), the oversight body of the Financial Accounting Standards Board. Passing of the report from the panel to FAF represented a significant step in the process to bring historic change to private company financial reporting, making it more meaningful for owners, lenders, investors and other users of private company financial statements.

The panel proposed two major shifts: u A separate board with standard-setting authority under

FAF’s oversight. The new board would consist of five to seven members with private company constituent experience. The new board would work closely with the FASB.

v Changes and modifications to existing U.S. generally accepted accounting principles, where appropriate, for private companies to reflect their financial statement users’ unique needs. All such changes would reside in the one GAAP Codification.

FAF’s Board of Trustees discussed the report at a meeting on February 15. On March 4, FAF announced it was forming a Trustee Working Group to address standard setting for nonpublic entities, including nonprofit organizations which were specifically excluded from the Blue Ribbon Panel’s charge. While the AICPA expected FAF to form such a group, the broader scope adds complexity. Still, FAF said it intends to issue an action plan in six to eight months (September–November).

According to FAF, the Working Group will conduct outreach to stakeholders in various ways, including roundtable meetings, surveys and meetings with advisory and constituent groups and others. It will also seek input on suggested improvements, including the solutions recommended by the Blue Ribbon Panel.

The Blue Ribbon Panel was formed in early 2010 by the AICPA, the FAF and the National Association of State Boards of Accountancy to explore how to address problems with standard setting for private companies. The panel’s 18 members came from a top level cross-section of financial reporting constituencies, including lenders, investors, owners, preparers and auditors. AICPA President and CEO Barry C. Melancon, CPA, also served on the panel. The panel’s mission was unlike other prior committees or groups created to study the issue over the past few decades because it looked at the standard-setting process from a policy level, rather than at specific changes to individual standards. “CPAs should get ready to respond to FAF when it seeks public input this spring,” said Tim Baker, president of the South Carolina Association of CPAs. “To make sure the profession’s ultimate goal is achieved, it is more critical than ever for CPAs, their clients, private company employers and private company financial statement users to support differential standards and a separate standard-setting board. We will have more communications and direction for you coming shortly.” n

The American Institute of CPAs and the Society for Human Resource Management have joined forces to launch the Workplace Leaders in Financial Education Award. The program recognizes organizations with exemplary workplace

financial literacy efforts to enhance employee financial well-being, and encourages employers to implement and further develop financial literacy programs.

Winning organizations must provide financial education programs to employees that increase their ability to make sound financial decisions and improve employee financial well-being. Workplace financial education programs help employees manage all aspects of their finances, from setting a budget and managing debt to paying for college and saving for retirement.

For more information or to apply, visit www.wlife.org. Applications are now being accepted online until July 1, 2011.

Nominate a Young CPA for the 2011 AICPA Leadership AcademyHelp Shape the Future of the CPA Profession!

Workplace Leaders in Financial Education Award

LeadershipAwards

The 2011 AICPA Leadership Academy offers three days of training and a lifetime of leadership to promising young CPAs. From Oct. 4-6, 2011,

attendees will have the opportunity to forge valuable relationships with other dynamic young CPA leaders. Academy alumni will leave with an expanded leadership skill set and strategies for leading in their organizations, communities and professions. Only 30 promising young professionals will be selected. Apply or nominate a young CPA today. The application and sponsorship deadline is June 1, 2011.

Visit www.aicpa.org/leadershipacademy for details.

Blue Ribbon Panel UpdatePrivate Company Financial Reporting Initiative Takes Another Step

For more information and resources, visit www.aicpa.org/privateGAAP.

COALITION FOR PRIVATE COMPANY STANDARDS

In conjunction with AICPA’s efforts for private company financial standards, SCACPA is seeking volunteers to serve on a coalition that will be advancing this issue. Volunteers should be a preparer or user of financial statements, an auditor or a lender. This task force will develop and execute a plan to educate South Carolina CPAs about the issue and spearhead a letter-writing campaign to advocate for a separate set of financial standards for private companies. If you are interested in serving, please send your contact information along with a brief description of your credentials to SCACPA Executive Director Erin Hardwick, [email protected].

The following article was provided by AICPA.

South Carolina CPA Report 22 (888) 557-4814 | www.scacpa.org South Carolina CPA Report 23(888) 557-4814 | www.scacpa.org

The health care tax credit, which had been available to small businesses, will only continue to

be available if the insurance is acquired from an insurance exchange for years after 2013. In addition, the credit will now only be available, even to the small businesses, for 2014 and 2015.

The IRS will issue a check to a government insurance plan (state insurance exchange) for certain individuals who have secured health insurance from such an exchange. An insurance exchange is a government mandated program run by the state government. The eligible individual is an individual or family with income up to 400 percent of the federal poverty level ($43,320 for an individual or $88,200 for a family of four, using 2009 poverty level figures) that are not eligible for Medicaid, employer sponsored insurance, or other acceptable coverage. The check from the IRS to the insurance provider will depend upon the person’s income.

PeNALTY fOr NOT HAViNG iNsUrANceBeginning in 2014, if one does not have acceptable insurance, they will be required to pay a penalty for not having it. The penalty will depend upon the number of people in the family plus one’s income. The amount of the penalty goes up with the passage of time with exceptions based upon financial hardship, religious objections and those with income below a given level.

If one has insurance, the insurance company will send the individual

a form attesting to the fact that the person has insurance. This form must be attached to the 1040 just as a form W-2 is. In the absence of this, the penalty must be shown on the 1040 when filed. Failure to attach the insurance form will result in the IRS asserting the penalty. However, the IRS cannot take any enforcement action to collect this penalty other than to hold any refund. This becomes “a tiger without teeth.” Further, employers who have 50 or more full-time employees (a large employer) but no health plan, or a plan that its employees cannot afford, will have to pay a penalty. The penalty in some cases will be less than the cost of the insurance, thus some employers will find it economically better to pay the penalty than to acquire the insurance. Employers (including self-insured employers) will have to report a host of additional information to the IRS.

At the time of this writing (Feb. 17, 2011) four different U. S. District Courts have ruled on the constitutionality of the penalty provisions and the requirement that the states establish an insurance exchange. Two of the decisions have held for the act and two have held against it. These cases will be appealed to the U. S. Circuit Court of Appeals for the 4th, 6th and 11th Circuits and eventually the U. S. Supreme Court. Further, it appears that if any part of the act is unconstitutional, the entire act is. Thus, a holding that the Congress cannot require a state to establish an insurance exchange or that the Congress cannot require one to buy insurance, will abolish the entire act.

In addition, it appears certain that in the very near future, the requirement for 1099s to be issued for any business purchase of $600 or more of services or merchandise to any seller (individuals, partnerships, corporations, etc.), in 2011 will be repealed. Finally, beginning in 2018, if an employee is covered by an employer’s reimbursement plan that reimburses more than a given amount (a so-called Cadillac plan), the excess will be subject to a non-deductible excise tax of 40 percent.

The future of this act is very uncertain at this time. The current U. S. House of Representatives has voted to repeal it. The U. S. Senate did not concur. If both bodies were to repeal, it is believed that the president would veto the measure. No one believes that the Congress would override the veto. Thus, the act is here unless the courts rule against it. The timing of those decisions is uncertain. Thus, as professionals, we have a problem. n

William M. Grooms, CPA, Ph.D., is a sole practitioner in Columbia with more than 40 years experience in his field. He was previously a partner of Ernst & Young, LLP, and a CPA with Clarkson, Harden & Gantt, Arthur Young & Co. and the Internal Revenue

Service. Bill serves on SCACPA’s Taxation Committee and is a past chairman of the Taxation Committee, past president of the Central Chapter and a past member of AICPA Tax Division’s Executive Committee.

Major Provisions of the Health Care

Reform Act William M. Grooms, CPA, Ph.D.

SCACPA member since 1967

“No one believes that the Congress would override the veto. Thus, the act is here unless the courts rule against it. The timing of those decisions is uncertain. Thus, as professionals, we have a problem.”

This is the final article in the Health Care Act series. In earlier articles, the tax ramifications of the health care act were addressed in major part through the end of 2013. This article concludes a review of this very massive new act as to its tax impact on the typical taxpayer and accountant.

South Carolina CPA Report 24 (888) 557-4814 | www.scacpa.org South Carolina CPA Report 25(888) 557-4814 | www.scacpa.org

by Mark T. Hobbs, CPASCACPA member since 1981

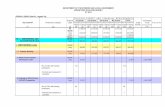

second Quarter report Comparison of South Carolina Association of CPAs and the South Carolina Board of Accountancy

Many licensees do not have a clear distinction between the roles and responsibilities of the South Carolina Board of Accountancy (the “board”) as compared and contrasted with the South Carolina Association of Certified Public Accountants (the

“association”). I believe some of this confusion has been caused by the very close working relationship that both the licensing board and the association have enjoyed in South Carolina. This is a perfect case where a good situation can lead to misunderstandings and confusion. I am hoping that this article will serve as a useful reference guide as you encounter questions about the roles and responsibilities of each organization. I would like to point out that South Carolina enjoys a unique relationship where we have established a tradition that past presidents of the association are normally recommended to the governor to be nominees for the seats open on the board. Each sitting governor has continued this tradition. This generally results in an individual who has been involved with the association for 10–15 years as a board member and officer. In addition, the individual has normally either served at the chapter level or committee levels of the association and/or both. I compare this to some other states that I have observed at the National Association of State Board of Accountancy — many appointees may be CPAs, but they have either not been active enough to understand the issues facing the profession or merely are political appointees based on some type of political litmus test. I hope our state will continue to enjoy the excellent relationship between our board and the association. n

TOPic sc AssOciATiON Of cPAs sc BOArD Of AccOUNTANcYMEMBERSHIP/LICENSURE • Professional society

• Voluntary - dues system• Licensing board • License fees- statutory- bi-annual licensure • Required by state statute

PRIMARY GOALS • Educational needs of members • Lobbying for benefit of members• Monitoring professional trends• Network of professionals

• Protection of the public (financial information credibility)• Oversight of profession, quality & integrity

RELATED ORGANIZATIONS Closely aligned with AICPA • Nationally aligned with other state boards through NASBA- membership

• State legislature/law

GOVERNANCE • Board of directors - 20• Elected by membership• Executive committee - 5

• Appointed by state government• 9 members

- 5 CPAs - 2 accounting practitioners- 2 public members

AUTHORITY Assumed by influence of members State law

FISCAL • Generally fiscally sound• AICPA provides support & resources• Active in lobbying and advocacy for

the benefit of the profession

• Budget constrained and limited resources• State government umbrella agency controls operations in state government

environment

PEER REVIEW Responsible for administering the peer review program for AICPA and S.C. licensees on behalf of the Board of Accountancy

S.C. accountancy law requires peer review and the board is responsible for making sure the program works to improve the quality and protect the the public in South Carolina

ANNUAL BUDGET $1,005,000 $550,000

NUMBER OF EMPLOYEES 10 full-time employees 4 full-time employees (certain services are shared at LLR)

EXECUTIVE DIRECTOR/ADMINISTRATOR

Erin Hardwick, CAE Doris Cubitt, CPA

VOLUNTEER/GOVERNOR APPOINTED

Tim Baker, President Bobby Creech, Chairman

OTHER INFORMATION Membership allows greater participation in AICPA life insurance programs among other programs

• Civil penalties can be assessed up to $10,000 per violation

• Other punishment include revocation and suspension of licensees license to practice

• Mandatory CPE

Comparison of South Carolina Association of CPAs and the South Carolina Board of Accountancy

SOUTH CAROLINA DEPARTMENT OF LABOR, LICENSING AND REGULATIONBoard of Accountancy • (803) 896-4770

www.llr.state.sc.us/pol/accountancy

SCACPA On-site Customized Training solutionsCustomized Training to Fit Your TeamGet the highest quality CPE tailored to meet your specific needs at a fraction of the off-site cost. SCACPA can help you plan and customize educational programs for any size group. From technical topics to professional ethics to leadership and management courses, we can find a great fit for any organization and any budget. Get started! Contact reva Brennan, MPA, cAe at (803)791-4181 x103 or [email protected], or visit www.scacpa.org/onsitetraining.

The chart (at right) serves as a useful

guide about the roles and responsibilities of each organization. u

South Carolina CPA Report 27(888) 557-4814 | www.scacpa.org

the cpa report - south carolina 4th edition 4c page ad live: 8 x 10.5 trim: 8.5 x 11 bleed: 8.75 x 12.5

Special Offer for State Society Members*.ADP gives you the choice of doing business the way that best fits your firm. Whether you want to refer payroll or process it yourself, ADP provides world-class payroll and beyond payroll services, so you can focus on what matters most: growing your business and helping your clients be successful. In addition, your state society membership means that you will be rewarded with the following special benefits when you partner with ADP:

Contact your local ADP representative today.* Discount/free payroll applies to companies with 1 to 49 employees that sign complete ADP sales order and to all features of standard payroll processing invoiced on client’s

regular processing cycle and does not include additional non-payroll services; excludes pass through costs, courier and other delivery fees, including off cycle fees, hardware, or penalty and interest fees. Only available to new ADP Clients using EasyPaysm or RUN Powered by ADP® in the continental U.S. Must be set-up for direct debit of fees (“DDF”) as the payment method.

© 2010 ADP, Inc. The ADP Logo is a registered trademark of ADP. EasyPay is a service mark and RUN Powered by ADP is a registered service mark of ADP, Inc. All other trademarks are the property of their respective owners.

■ Payroll for your firm — FREE for up to 50 employees with discounted solutions to meet the needs of larger businesses

■ Special discounts for your firm’s clients

■ Free access to our Accountant HR Helpdesk

■ Free Master Tax Guides from CCH, a Wolters Kluwer business

■ 30% discount on all CCH tax and accounting publications

2610_CPAtrade_ad cpa report sc v2.indd 1 9/15/10 2:06:47 PM

what made you choose to become a cPA? Warner: I really enjoyed the logic of accounting when studying it as part of my first set of business courses. After researching the profession, I discovered how many different avenues there were and decided to commit to it.

what do you believe are the keys to a successful career? Warner: The ability to get along with people and be adaptable to change.

what do you find most rewarding working in the banking industry? Warner: I would say some of the technical advances in accounting, which have made every day a learning experience. As an employee of TD Bank, I also have a tremendous opportunity for professional growth with an organization that continues to grow. TD is one of only two North American banks that are still AAA-rated by Moody’s, which helps to attract new relationships with customers and which allows us to continue growing and expanding.

what changes have you seen as a result of recent economic events? Warner: The most challenging economic time since the Great Depression has led to an increased regulatory environment for banks.

While 2011 will continue to have its share of challenges for all banks, at TD Bank, we are incredibly well-positioned to leverage the investments the bank has made in its franchise to continue growing and taking market share from our competition.

what is the toughest issue you have had to deal with in this economy? Warner: Prior to TD Bank’s acquisition of the South Financial Group, it was dealing with issues related to the credit cycle. Since the acquisition, more of our attention has been focused on purchase accounting and conversion items.

Focus On Membership

“The most challenging economic time since the Great Depression has led to an increased regulatory environment for banks.”

what do you think are the major concerns of cPAs today, and how can they be addressed? Warner: Deadlines, workload and establishing a healthy work/life balance will probably always be a lifestyle concern for CPAs.

How have you benefited from membership in scAcPA? Warner: I know I can count on SCACPA to keep me abreast of professional issues and to provide high quality CPE.

what advice do you have for young cPAs? Warner: Always try to learn something from everything you do, even from tasks that seem the most mundane.

what have you accomplished that makes you proud to be a cPA? Warner: That’s a tough one, but I am proud that some of the folks who have worked for me have gone to other companies and are having very successful careers there. I am also proud that my son is also a CPA.

who do you admire most and why? Warner: I would say Abraham Lincoln for his ability to make decisions that were unpopular at the time, but which turned out to be nation-changing. n

SCACPA member since 1992Leonard D. “Doug” warner, cPA

Doug warner, cPACarolina First Bank

A trade name of TD Bank®Greenville, SC

scAcPA involvement: Financial Literacy Task Force

Hometown: Ashburn, VA

favorite Book: Sherlock Holmes novels by

Arthur Conan Doyle.

favorite Movie:Animal House

Member Profile

South Carolina CPA Report 28 (888) 557-4814 | www.scacpa.org South Carolina CPA Report 29(888) 557-4814 | www.scacpa.org

AFFILIATE, non-CPA Susan A. BeaufordGreenwood, SC

Kamee M. Bowlin Mount Pleasant, SC

Cathleen ClearyColumbia, SC

James Everett III West Columbia, SC

JoBeth Hite Greenwood, SC

Gloria Karlin Greenville, SC

Kristin PenistonGreenville, SC

ASSOCIATEBrenda Carroll Augusta, GA

Gary L. RogalskiMount Pleasant, SC

Lee Wagner Greenwood, SC

CPA CANDIDATE Christina M. Alvanos Charleston, SC

MacKenzie L. AndrewsGreenville, SC

Amanda D. Blagg Greenville, SC

Lucy W. Brenner Charleston, SC

Ashley M. Brouillette Greenwood, SC

Brandi G. Buff Greenwood, SC

Andrew DobsonSpartanburg, SC

Susan M. Edwards Charleston, SC

Tiffany M. Ehrhart Charleston, SC

Roger T. Godwin Jr. Greenville, SC

Travis J. Hoverman Duncan, SC

Daniel B. Howard Greer, SC

Kelly N. JewellGreenville, SC

James D. McAllister Jr.Greenwood, SC

Rachel M. Nightengale Hanahan, SC

S. C. Paul Charleston, SC

William C. PittsGreenwood, SC

Beth A. Robertson Charleston, SC

Nicole S. Robinson Charleston, SC

Barrett E. Sammons Charleston, SC

James J. Sanyi Summerville, SC

Eric S. Schoenbaechler Summerville, SC

Katherine E. Spaugh Greenville, SC

Charles M. WootenWest Columbia, SC

FELLOW – GOV’T Deron E. Smith, CPA Walterboro, SC

FELLOW Cheryl A. BeckwithReidville, SC

Jonathan W. BlanchardYork, SC

Diana C. BrayColumbia, SC

Christine DupontGreenville, SC

Philip O. EspyDaniel Island, SC

Michael W. GreeneCerro Gordo, NC

Patrick C. HallerGreenville, SC

John F. HatcherCharleston, SC

Catherine HoltFlorence, SC

Ginger R. LawrimoreFlorence, SC

Kevin S. LightHartsville, SC

Brittany LongColumbia, SC

Robert J. McMillanCharleston, SC

Christina R. MillerGreenville, SC

Matthew S. MillerColumbia, SC

Ryan MillerColumbia, SC

Stephen PelcherGreenville, SC

Joseph P. PhippsCharleston, SC

Marisa S. PhoenixCharleston, SC

Addison B. PotterColumbia, SC

Chad W. ReingardtGreenville, SC

Lacey C. SatterfieldGreenville, SC

FIRM ADMINISTRATOR Mary Preston Greenville, SC

Posey M. Royall Charleston, SC

STUDENTMonica A. Burbano de Lara Charlotte, NC

Carolyn Craven Dalzell, SC

Tracy Creech Leesville, SC

Christen N. Dail Conway, SC

Crystal L. Ferguson Moncks Corner, SC