COURT OF APPEAL FOR THE FOURTH APPELLATE … · COURT OF APPEAL FOR THE FOURTH APPELLATE DISTRICT...

53

COURT OF APPEAL FOR THE FOURTH APPELLATE DISTRICT STATE OF CALIFORNIA (Division One) ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ Docket no. D063997 San Diego County Superior Court case nos. 37-2012-00094831-CU-TT-CTL (lead case) 37-2012-00097148-CU-MC-CTL (main case) 37-2012-00100333-CU-TT-CTL (other matter) (Judge Ronald S. Prager--Department 71) ========== CITY OF SAN DIEGO, Plaintiff and Respondent, v. MELVIN SHAPIRO AND SAN DIEGANS FOR OPEN GOVERNMENT, Defendants and Appellants. ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ Appellant San Diegans for Open Government’s Opening Brief BRIGGS LAW CORPORATION [BLC file: 1593.07] Cory J. Briggs (State Bar no. 176284) Mekaela M. Gladden (State Bar no. 253673) 99 East “C” Street, Suite 111 Upland, CA 91786 Telephone: 909-949-7115 Attorneys for Appellant San Diegans for Open Government

Transcript of COURT OF APPEAL FOR THE FOURTH APPELLATE … · COURT OF APPEAL FOR THE FOURTH APPELLATE DISTRICT...

COURT OF APPEAL FOR THE FOURTH APPELLATEDISTRICT

STATE OF CALIFORNIA(Division One)

~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~

Docket no. D063997

San Diego County Superior Court case nos. 37-2012-00094831-CU-TT-CTL (lead case)

37-2012-00097148-CU-MC-CTL (main case)37-2012-00100333-CU-TT-CTL (other matter)

(Judge Ronald S. Prager--Department 71)

==========

CITY OF SAN DIEGO,Plaintiff and Respondent,

v.

MELVIN SHAPIRO AND SAN DIEGANS FOR OPENGOVERNMENT,

Defendants and Appellants.

~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~

Appellant San Diegans for Open Government’s Opening Brief

BRIGGS LAW CORPORATION [BLC file: 1593.07]Cory J. Briggs (State Bar no. 176284)Mekaela M. Gladden (State Bar no. 253673)99 East “C” Street, Suite 111Upland, CA 91786Telephone: 909-949-7115

Attorneys for Appellant San Diegans for Open Government

Appellant’s Opening Brief Page ii

CERTIFICATE OF WORD COUNT

As required by Rule 8.204(c) of the California Rules of Court, and

based on the “word count” function of the word processor on which this

petition and brief were written, I certify that there are less than 10,000

words in this document, excluding the cover sheet, tables, running

footers, and this certificate.

Date: October 15, 2013. By: Cory J. Briggs

Appellant’s Opening Brief Page iii

TABLE OF CONTENTS

I. Introduction. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1

II. Statement of Facts. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 5

A. Background. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 5

B. Trial Court Proceedings. . . . . . . . . . . . . . . . . . . . . . . . . 6

C. Statement of Appealability. . . . . . . . . . . . . . . . . . . . . . . 7

III. Legal Landscape: Californians Abhor Taxes Not Approved by Voters. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 7

IV. Argument and Analysis.. . . . . . . . . . . . . . . . . . . . . . . . . . . . . 11

A. The Special Tax Was Not Approved by San Diego’sRegistered, Natural-Person Voters and ThereforeViolates the California Constitution and the San Diego City Charter. . . . . . . . . . . . . . . . . . . . . . . . . . . . 12

1. The California Constitution Required the CityTo Obtain Approval of the Special TaxBy Registered, Natural-Person Voters. . . . . . . . 12

a. The City Must Abide by the CaliforniaConstitution. . . . . . . . . . . . . . . . . . . . . . . 13

b. Non-Registered, Non-Natural Persons DoNot Have the Right to Vote under theCalifornia Constitution.. . . . . . . . . . . . . . 14

c. Registered, Natural-Persons Have the Right to Vote on Taxes under the California Constitution.. . . . . . . . . . . . . . 19

2. The City Violated the San Diego City Charter. 25

Appellant’s Opening Brief Page iv

B. The City Violated the California Environmental Quality Act by Failing to Prepare an EnvironmentalImpact Report for the Convention Center ExpansionProject and Not Taking the Role of Lead Agency. . . . 29

1. The California Environmental Quality ActApplies to the Expansion Project. . . . . . . . . . . . 29

2. The City Firmly Committed Itself to the Expansion Project Before the EnvironmentalImpact Report Was Certified. . . . . . . . . . . . . . . 32

3. The City Failed to Act as Lead Agency for the Expansion Project. . . . . . . . . . . . . . . . . . . . . . . . 39

4. The California Environmental Quality ActIssues Are Not Moot.. . . . . . . . . . . . . . . . . . . . . 42

V. Conclusion.. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 43

Appellant’s Opening Brief Page v

TABLE OF AUTHORITIES

California Constitution

CAL. CONST., art. XIIIA, § 4. . . . . . . . . . . . . . . . . . . . . . . . . . . . Passim

CAL. CONST., art. XIIIC, § 2. . . . . . . . . . . . . . . . . . . . . . . . . . . . Passim

Judicial Authorities

Altadena Library Dist. v. Bloodgood, 192 Cal. App. 3d 585 (1987). . . . . . . . . . . . . . . . . . . . . . . . . 21

Amador Valley Joint Union High School District v. County ofAlameda, 22 Cal. 3d 208 (1978). . . . . . . . . . . . . . . . . . . . . . . . 8

Cipriano v. City of Houma, 395 U.S. 701 (1969). . . . . . . . . . . . . . . 25

Citizens Ass’n of Sunset Beach v. Orange County Local AgencyFormation Comm’n, 209 Cal. App. 4th 1182 (2012). . . . . . . 23

City of Phoenix, Arizona v. Kolodziejski, 399 U.S. 204 (1970). . . . 24

County of Amador v. City of Plymouth, 149 Cal. App. 4th 1089(2007).. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 31

County of Riverside v. Whitlock, 22 Cal. App. 3d 863 (1972). . . . . 24

Friends of Mammoth v. Board of Supervisors, 8 Cal. 3d 247 (1972). . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 30

Friends of Sierra R.R. v. Tuolumne Park & Recreation Dist.,147 Cal. App. 4th 643 (2007). . . . . . . . . . . . . . . . . . . . . . . . . 30

Foothill-De Anza Community College District v. Emerich,158 Cal. App. 4th 11 (2007). . . . . . . . . . . . . . . . . . . . . . . 17, 28

Appellant’s Opening Brief Page vi

Howard Jarvis Taxpayers Ass’n v. City of San Diego, 120 Cal. App. 4th 374 (2004). . . . . . . . . . . . . . . . . . . . . . 13, 22

Kaufman & Broad-South Bay, Inc. V. Morgan Hill Unified SchoolDist., 9 Cal. App. 4th 464 (1992). . . . . . . . . . . . . . . . . . . . . . 31

Kramer v. Union Free School Dist., 395 U.S. 621 (1969). . . . . . . . 25

Neighbors for Fair Planning v. City and County of San Francisco,217 Cal. App. 4th 540 (2013). . . . . . . . . . . . . . . . . . . . . . . . . 36

Neilson v. City of California City, 133 Cal. App. 4th 1296 (2005). . . . . . . . . . . . . . . . . . . . . 15, 28

Planning & Conserv. League v. Castaic Lake Water Agency,180 Cal. App.4th 210 (2009). . . . . . . . . . . . . . . . . . . . . . . . . 40

Rider v. County of San Diego, 1 Cal. 4th 1 (1991) . . . . . . . . 8, 14, 20

Sanchez v. City of Modesto, 145 Cal. App. 4th 660 (2006). . . . . . . 24

Save Tara v. City of West Hollywood, 45 Cal. 4th 116 (2008).. 33, 36

Silicon Valley Taxpayers Ass’n v. Garner, 216 Cal. App. 4th 402 (2013). . . . . . . . . . . . . . . . . . . . . . 10, 18

Silicon Valley Taxpayers Ass’n v. Santa Clara Open Space Auth.,44 Cal. 4th 431 (2008). . . . . . . . . . . . . . . . . . . . . . . . 3, 7, 8, 10

Sustainable Transportation Advocates of Santa Barbara v. SantaBarbara County Association of Governments, 179 Cal. App. 4th 113 (2010). . . . . . . . . . . . . . . . . . . . . . . . . 42

Weisblat v. City of San Diego, 176 Cal. App. 4th 1022 (2009). . . . . . . . . . . . . . . . . . . . . 20, 23

Western Lithograph Co. v. State Bd. of Equal., 11 Cal. 2d 156 (1938). . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 20

Appellant’s Opening Brief Page vii

Legislative Authorities

GOV’T CODE § 53722. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 10

PUB. RES. CODE § 21065. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 29

Administrative Authorities

CAL. CODE OF REGS., tit. 14, § 15352. . . . . . . . . . . . . . . . . . . . . . . . 33

CAL. CODE OF REGS., tit. 14, § 15378. . . . . . . . . . . . . . . . . . . . . 29, 30

CAL. CODE OF REGS., tit. 14, § 15051. . . . . . . . . . . . . . . . . . . . . . . . 40

Appellant’s Opening Brief Page 1

I. INTRODUCTION

This is a case, first and foremost, about the City of San Diego’s

disenfranchisement of its hundreds of thousands of registered voters. In

2012, the City enacted a jurisdiction-wide special tax on hotel property

to pay for an expansion of the San Diego Convention Center to be

financed with bonds up to $575 million. Admin. R. 4:36 (§ 4). The

parties do not dispute that the special tax is subject to voter approval

under the California Constitution and the San Diego City Charter. The

dispute concerns who the “voters” are.

In the City’s view, the appropriate “voters” consist exclusively of

hoteliers. To this end, the City enacted a local ordinance creating the

San Diego Convention Center Facilities District (“CCFD”) along the

lines of a facilities district established under the Mello-Roos Community

Facilities Act of 1982 (“Procedural Ordinance”). See generally id., 2:6-

19. The Procedural Ordinance gave the right to vote to the owners of

the land on which the hotels are located; or to leaseholders, in the case

of hotels on land owned by a government agency. Id., 2:8 (§ 61.2705

(defining “Landowner”)); 2:12 (§ 61.2710(a) (giving right to vote to

“Landowners”). The vote was conducted by the city clerk and was not

See, e.g., Admin. R. 26:5451 (city attorney memorandum “to inform the1

City Council that the proposed Convention Center Facilities District

Procedural Ordinance represents an unusual procedure for the formation of a

special tax district and no assurance can be given that the CCFD Ordinance or

the Convention Center Facilities District (CCFD) formed pursuant thereto will

be validated by a court of law”); 26:5452 (Orrick letter indicating that “firm

will not be providing an opinion to the City of San Diego on the legality of the

City’s proposed Convention Center Facilities District enabling ordinance”).

Appellant’s Opening Brief Page 2

overseen in any way by the county registrar of voters. Id., 2:12 (§

61.2710(b)).

In Appellant’s view, the City should have put the special tax up

for approval by the natural persons who reside in the City and are

registered to vote in the jurisdiction. These are the people who are

identified in the California Constitution and San Diego City Charter, in

provisions dealing with special-tax approvals, as “qualified electors” or

“the electorate.” Fearing that its registered, natural-person voters would

reject a special tax to pay off $575 million in debt, the City opted for an

end-run around state and local constitutional limitations and gave its

own meaning to the term “qualified electors” by defining them as the

“Landowners.” Id., 2:12 (§ 61.2710(a)).

The City knows that its approach is legally suspect, for its in-

house attorneys labeled it “dubious” and its outside attorneys altogether

refused to opine on the legality. In light of the uncertainty, the City1

Appellant’s Opening Brief Page 3

initiated a validation lawsuit seeking to validate the CCFD, the special-

tax and bonding schemes for the Convention Center, and everything

relating thereto.

Five years ago, the California Supreme Court made it very clear

that it is the Judiciary’s role to exercise its independent judgment when

reviewing the imposition of taxes by local agencies. See Silicon Valley

Taxpayers Ass’n v. Santa Clara Open Space Auth., 44 Cal. 4th 431, 450

(2008) (reviewing case law regarding standard of review over local

agency’s generation of revenues under California Constitution;

concluding that courts should exercise independent judgment) (“Silicon

Valley”). Significantly, that decision came down even before

California’s voters approved Proposition 26 to make abundantly clear

what local agencies refused to acknowledge after passage of Proposition

13 in 1978 and its progeny and their tight restrictions on the raising of

new revenues: namely, that the voters will not tolerate the imposition of

any new tax without their consent.

While the disenfranchisement of the City’s voters is the most

important issue raised in this appeal, it is certainly not the only one.

Even if the special tax had been properly approved, this Court would

Appellant is not raising the issue of the indebtedness through lease revenue2

bonds incurred by the City violating the Charter in this appeal because the

judgment was revised to validate only the CCFD bonds. Jt. App. (“JA”) 3:797,

¶ 4 & 798, ¶ 10. At the hearing, the City’s attorney clarified that the lease

revenue bonds were not the subject of the validation action. Rpt. Transcript,

p. 38, ln. 4-p. 40, ln. 6. Since the lease revenue bonds (also called

supplemental bonds or gap bonds) are not the subject of the validation lawsuit,

Appellant is not raising the issue here; only the CCFD bonds are an issue.

Appellant’s Opening Brief Page 4

still have to invalidate the City’s approval of the expansion project and

the associated special-tax and financing schemes because the City failed

to comply with the California Environmental Quality Act (“CEQA”)

before it took action on the project. Appellate review of a CEQA2

matter is de novo. See, e.g., Environmental Prot. Info. Ctr. v. Calif.

Dep’t of Forestry & Fire Prot., 44 Cal. 4th 459, 479 (2008).

Appellant understands that there is a lot of political momentum

behind the expansion project and even some good economic reasons for

supporting it. Everyone--Appellant included--wants the City to succeed

socially, economically, and environmentally. But no matter how great

the expansion’s economic benefit might be, the cost to our democratic

institutions and our right of self-governance is even greater if the

protections enshrined in our state and local constitutions are ignored.

Whether to get the special tax’s approval or eliminate the voter-approval

requirement, the City’s sole recourse was at the ballot box.

Appellant’s Opening Brief Page 5

II. STATEMENT OF FACTS

A. Background

Through its city council, the City enacted the Procedural

Ordinance in November 2011, thereby giving the City the legal authority

and prescribing the procedures necessary to form the CCFD. See

generally Admin. R. 2:6-19. Shortly thereafter the City passed a

resolution of intention to form the CCFD and a related resolution

declaring the need to incur bonded indebtedness to the tune of $575

million. Id., 3:20-34 & 4:35-39. Having received written protests from

less than a majority of those the City determined to be eligible voters, it

proceeded with the formation of the CCFD and scheduled an election to

approve the special tax. Id., 5:40-58. The formation resolution

explicitly stated that the CCFD’s “qualified electors”--not the City’s--

would be allowed to participate in the election. Id., 5:47 (¶ 13).

A mail-ballot election was then conducted, with only those who

met the definition of “Landowners” under the CCFD permitted to vote.

Id., 8:78-81. After tabulating the votes through a weighted-vote scheme,

the measure came back with more than two-thirds of the votes being

“yes.” Id., 141:7523 & 8:78-81 (resolution declaring election results).

It is believed that the Coalition was affiliated with unions and dropped its3

opposition to the expansion project and special tax after the City entered into

a project labor agreement with the building-trades union.

Appellant’s Opening Brief Page 6

The resolution directing the city clerk to record a Notice of Special Tax

Lien directed her to include “a statement indicating that no special tax

shall be levied until the City has obtained a final validation judgment

determining that the special tax was lawfully authorized and valid.” Id.,

9:82-87.

B. Trial Court Proceedings

The City filed a validation action on May 10, 2012. Admin. R.

9:82-87; JA I:11-23. The lawsuit was answered by Melvin Shapiro, the

Coalition for Responsible Convention Center Planning (with some

related individuals), and Appellant. JA I:36-41 (Shapiro answer); 44-51

(Appellant’s answer) & 52-63 (Coalition’s answer). The lawsuit was

consolidated with two other lawsuits. JA I:134-143. However, the other

two were dismissed and Coalition withdrew its answer here. JA I:176-3

181 (dismissals and notice of settlement).

The City, Shapiro, and Appellant briefed the case. JA I:187-214

(City’s opening brief), II:322-350 (Shapiro’s trial brief), II:514-577

(Appellant’s trial brief) & III:665-682 (City’s reply brief). Following a

Appellant’s Opening Brief Page 7

hearing, the trial court issued a ruling in the City’s favor. JA III:753-

759. Judgment was entered accordingly on April 18, 2013. JA III:785-

808.

C. Statement of Appealability

Notice of entry of judgment was filed on April 19, 2013, and

served by mail. JA III:8070813. The decision is now final. This appeal

was timely filed on May 8, 2013. JA III:824-826.

III. LEGAL LANDSCAPE:CALIFORNIANS ABHOR TAXES NOT APPROVED BY VOTERS

Californians’ revolt against runaway taxation has its origins in

Proposition 13, with later efforts to close loopholes thereto through

passage of Proposition 62 and Proposition 218. Proposition 13 was

adopted by the voters in 1978. Silicon Valley, supra, 44 Cal. 4th at 442.

Article XIIIA of the California Constitution, which was added by

Proposition 13, establishes a very high bar for the imposition of special

taxes by local governments.

Cities, Counties and special districts, by atwo-thirds vote of the qualified electors ofsuch district, may impose special taxes onsuch district, except ad valorem taxes on realproperty or a transaction tax or sales tax onthe sale of real property within such City,County or special district.

Even if the CCFD is a “special district,” it is geographically coterminous4

with the City, and thus the “qualified electors” of the CCFD are the same as

the City’s qualified electors. See Rider v. County of San Diego, 1 Cal. 4th 1,

11 (1991) (holding that “special district” under Proposition 13 includes “any

local taxing agency created to raise funds. . . .”).

Appellant’s Opening Brief Page 8

CAL. CONST., art. XIIIA, § 4 (emphasis added). As explained more4

recently by the Supreme Court: “To prevent local governments from

subverting its limitations, Proposition 13 also prohibited counties, cities,

and special districts from enacting any special tax without a two-thirds

vote of the electorate.” Silicon Valley, supra, 44 Cal. 4th at 442

(emphasis added).

Charter cities are not exempt from the constitutional provisions

due to the principle known as “home rule.” Article XI, Section 5, of the

California Constitution allows charter cities to make and enforce all

ordinances and regulations with respect to municipal affairs, subject

only to limitations provided in their charters. In all other respects,

charter cities must abide by general laws. The relationship between

Proposition 13 and the home-rule principle was discussed in Amador

Valley Joint Union High School District v. County of Alameda (1978)

22 Cal. 3d 208, 224-227. “The principle of home rule involves,

essentially, the ability of local government (technically, chartered cities,

Appellant’s Opening Brief Page 9

counties, and cities and counties) to control and finance local affairs

without undue interference by the Legislature.” Id. at 224-225. The

High Court determined that Proposition 13 does not necessarily result

in abrogation of home rule because local agencies retain full authority

to impose special taxes if “approved by a two-thirds vote of the

‘qualified electors.’” Id. at 226. Local agencies retain autonomy

regarding allocation and expenditures of the relevant tax revenue. Id.

The constitutional requirement for voter approval of special taxes and

the principle of home rule are thus not in conflict.

Despite the inability of local governments to circumvent

Proposition 13 by relying on home rule, Proposition 13 was not as

effective as the voters had hoped in preventing local governments from

enacting new and increased taxes. As a result, Proposition 62, the

“Voter Approval of Taxes Act,” was passed in 1986. In furtherance of

Proposition 62, the Legislature amended the Government Code to

provide that “[n]o local government or district may impose any special

tax unless and until such special tax is submitted to the electorate of the

local government, or district and approved by a two-thirds vote of the

Appellant’s Opening Brief Page 10

voters voting in an election on the issue.” GOV’T CODE § 53722

(emphasis added).

Again, however, loopholes were popping up and Proposition 62

was found not to apply to charter cities. So Californians returned to the

polls in 1996 and enacted Proposition 218 “to plug certain perceived

loopholes in Proposition 13.” See Silicon Valley Taxpayers Ass’n v.

Garner, 216 Cal. App. 4th 402, 405 (2013) (explaining purpose of

Proposition 218 “to plug certain perceived loopholes in Proposition

13”). Proposition 218 added Articles XIIIC and XIIID to the California

Constitution. Silicon Valley, supra, 44 Cal. 4th at 443. In particular, it

provided that “[n]o local government may impose, extend, or increase

any special tax unless and until that tax is submitted to the electorate

and approved by a two-thirds vote.” CAL. CONST., art. XIIIC, § 2(d)

(emphasis added).

When local government again made progress circumventing

Proposition 218 and its predecessors, the voters likewise went back to

the ballot box. In 2010, the electorate adopted Proposition 26,

“Supermajority Vote to Pass New Taxes and Fees Act,” and expanded

what they consider a “tax” requiring voter approval.

Appellant’s Opening Brief Page 11

Locally, San Diegans care equally about the right to vote on taxes.

Approved by the City’s voters in 1983, City Charter Section 76.1 reads

(with Appellant’s emphasis):

Notwithstanding any provision of this Charterto the contrary, a special tax, as authorized byArticle XIIIA of the California Constitutionmay be levied by the Council only if theproposed levy has been approved by a two-thirds vote of the qualified electors of theCity voting on the proposition; or if thespecial tax is to be levied upon less than theentire City, then the tax may be levied by theCouncil only if the proposed levy has beenapproved by a two-thirds vote of the qualifiedelectors voting on the proposition in the areaof the City in which the tax is to be levied.

Altogether, Californians and San Diegans have consistently and

vigorously defended their right to vote on taxes. That right was violated

here, and the City’s voters are looking to this Court for redress.

IV. ARGUMENT AND ANALYSIS

This appeal raises two primary issues. The first is that the special

tax was not approved by a two-thirds vote of “the electorate” or the

“qualified electorate” and is therefore illegal. The second issue is that

the expansion approvals violated CEQA. If the Court agrees with

Appellant’s Opening Brief Page 12

Appellant on the first issue, it need not reach the second issue.

Appellant briefs both issues, however, in an abundance of caution.

A. The Special Tax Was Not Approved by San Diego’sRegistered, Natural-Person Voters and ThereforeViolates the California Constitution and the San DiegoCity Charter

The special tax levied by the City is illegal because it was not

approved by the City’s registered, natural-person voters. The California

Constitution and the San Diego City Charter both require special taxes

to be approved by “qualified electors” or “the electorate.” Yes, votes

were cast on the special tax. The problem is that they were cast by

hoteliers, not humans, and the City’s voters were disenfranchised in the

process.

1. The California Constitution Required the City toObtain Approval of the Special Tax byRegistered, Natural-Person Voters

The fundamental flaw in the City’s special-tax scheme to repay

the $575 million in bonds necessary to finance the expansion project

was the failure to obtain the tax’s approval by the City’s registered,

natural-person voters. They represent the “qualified electors” and “the

electorate” whose approval is a constitutional requirement. The City did

not have the luxury of defining “qualified electors” in the Procedural

Appellant’s Opening Brief Page 13

Ordinance and using that definition to supplant the constitution’s

registered-voter requirement. The City’s failure to obtain the approval

of registered voters renders the special tax unconstitutional.

After demonstrating that the City, as a charter city, was required

to abide by the California Constitution--all of it, in fact--Appellant will

explain why the approval of hotel businesses was not sufficient under

the Constitution and show that the approval of registered, natural-person

voters was essential to the tax’s validity.

a. The City Must Abide by the CaliforniaConstitution

It should go without saying that the City must abide by the

California Constitution. In Howard Jarvis Taxpayers Association v.

City of San Diego, 120 Cal. App. 4th 374, 384 (2004), this Court

determined that a trial court did not err when it ruled that “a city charter

may not conflict with the California Constitution.” The Court noted that

it is “well established that a charter represents the supreme law of a

charter city, subject only to conflicting provisions in the federal and

state Constitutions and to preemptive state law.” Id. at 385. “As a

constitutional initiative, Proposition 218 is binding upon charter cities.”

Id. at 391 (italics in original). Consequently, this Court ultimately

Appellant does not concede that Article XIIIA, Section 4, even applies here5

in the way the City argues because the CCFD is not a “special district” under

that constitutional provision. The Procedural Ordinance does not give the

CCFD the power to levy taxes, which puts it outside Section 4. See Rider,

supra, 1 Cal. 4th at 11 (holding that “special district” under Proposition 13

includes “any local taxing agency created to raise funds. . . .”). Thus, the

qualified electors under Section 4 must be qualified electors of the City, not

qualified electors of the CCFD, because the City, not the CCFD, is levying the

special tax. Even if the City could levy the special tax within the CCFD’s

jurisdiction--which is coterminous with the City’s geographic boundaries--the

City would have a problem because the “qualified electors” did not vote on the

special tax.

Appellant’s Opening Brief Page 14

determined that a city ballot measure was invalid because it conflicted

with Article XIIIC of the California Constitution. Fearing a similar

ruling here, the City enacted a legal provision acknowledging that

constitutional defects would render any special tax levied or bonds

issued under the Procedural Ordinance invalid. See Admin. R. 2:17

(SAN DIEGO MUN. CODE § 61.2717).

b. Non-Registered, Non-Natural Persons DoNot Have the Right to Vote under theCalifornia Constitution

Non-registered, non-natural persons were impermissibly allowed

to vote on the special tax. The California Constitution requires a vote

of “qualified electors” under Article XIIIA, Section 4, and by “the5

electorate” under Article XIIIC, Section 2. In this case, the City decided

to concoct its own definition of “qualified electors” for purposes of the

Weighting of the vote was itself illegal. The special tax is imposed on the6

real property or the leasehold interest therein. See Admin. R. 2:15 (SAN DIEGO

MUN. CODE § 61.2713). Even though Article XIIID allows weighted votes by

property owners in some cases, it nevertheless requires the qualified electors

to approve special taxes pursuant to Article XIIIA, Section 4. See CAL.

CONST., art. 13D, § 3(a)(2). Article XIIID thus offers no refuge to the City.

Appellant’s Opening Brief Page 15

weighted vote on the special tax. Under the Procedural Ordinance,

“qualified electors” refers to the “Landowners,” who are defined as the

owners and lessees of real property on which the City’s hotels are

located. Admin. R. 2:8, 12 (SAN DIEGO MUN. CODE § 61.2705, §6

61.2710(a)).

The proposition that landowners--natural persons or not,

registered voters or not--are “qualified electors” under Article XIIIA,

Section 4, was rejected in Neilson v. City of California City, 133 Cal.

App. 4th 1296 (2005). In Neilson, a non-resident landowner challenged

a parcel tax (i.e. a property tax) because, he contended, property owners

rather than registered voters were the “qualified electors.” Id. at 1312.

The appellate court disagreed. In recognizing that the word “electorate”

was not defined in the California Constitution, the Court of Appeal

looked to the Elections Code in order to determine the meaning of

“electorate” in the context of voting on special taxes:

The Court of Appeal bolstered this conclusion by pointing out that the7

challenger’s construction of “qualified electors” was predicated on the voting

procedures specified in Article XIIID, not Article XIIIA, both of which

covered a related subject but did not both include the “qualified electors”

language. Id. at 1313-1314. For similar reasons, the Court should reject any

Appellant’s Opening Brief Page 16

The Elections Code defines “elector” to mean“any person who is a United States citizen 18years of age or older and a resident of anelection precinct at least 15 days prior to anelection.” (Elec. Code, § 321.) The ElectionsCode does not contain a formal definition ofthe word “qualified,” but it does containvariations of that word that are useful indetermining its meaning. For example,division 2 of the Elections Code is titled“Voters” and it contains chapters titled “VoterQualifications” (ch. 1, beginning with § 2000)and “Registration” (ch. 2, beginning with §2100). Pursuant to section 2000 of theElections Code, “[e]very person who qualifiesunder Section 2 of Article II of the CaliforniaConstitution and who complies with this codegoverning the registration of electors mayvote at any election held within the territorywithin which he or she resides and theelection is held.” (Italics added.) Article II,section 2 provides that a “United Statescitizen 18 years of age and resident in thisstate may vote.” Also, Elections Code section359 provides that “voter” means “any electorwho is registered under this code.”

Id. at 1313. Based on this reasoning, the appellate court concluded that

“the phrase ‘qualified electors of such district’ (art. XIII A, § 4) means

the registered voters of City who voted in the election.” Id.7

attempt by the City to morph the “qualified electors” definition under Article

XIIIA into “property owners”--regardless of the legal authorities to which the

City might resort. After all, Article XIIID itself expressly distinguishes

between assessments and property-related fees, which are approved by

“owners,” and special taxes, which are to be approved in accordance with

Article XIIIA. Cf. CAL. CONST., art. 13D, § 3(a)(3) & (4), § 4, § 6 (requiring

“owner” votes for assessments and fees); CAL. CONST., art. 13D, § 3(b)

(requiring vote on special tax under Article XIIIA). The distinction cannot be

ignored. That the voters saw fit to make it speaks volumes.

Appellant’s Opening Brief Page 17

Another instructive case is Foothill-De Anza Community College

District v. Emerich, 158 Cal. App. 4th 11 (2007) (“Foothill-De Anza”),

in which the general partner in a partnership that owned real property in

a school district challenged a bond measure approved by the registered

voters in the district; the general partner did not live in the district, and

the measure would result in a special tax being indirectly imposed on

him. In rejecting his claim that not allowing him to vote on the measure

violated his constitutional right to equal protection, the Court of Appeal

concluded that the general partner was not “qualified” to vote on the

measure. Id. at 26. “A person qualifies generally as a voter if he or she

is a United States citizen at least 18 years of age residing in the state.

* * * If such a person complies with the registration requirements of the

Elections Code he or she ‘may vote at any election held within the

territory within which he or she resides and the election is held.’ * * *

Appellant’s Opening Brief Page 18

Since [the general partner] does not reside in and is not a registered

voter of the District, he is not otherwise qualified to vote there.” Id.

(bold italics added; regular italics in original; citations omitted).

The voter intent behind Proposition 218 further compels the

conclusion that only registered, non-natural persons should have been

allowed to vote. The intent of the voters is the “paramount

consideration” in construing a constitutional provision. Silicon Valley

Taxpayers’ Ass’n, supra, 216 Cal. App. 4th at 407. The rebuttal to the

argument against Proposition 218 state: “Proposition 218 expands your

voting rights. It CONSTITUTIONALLY GUARANTEES your right to

vote on taxes.” Appellant’s Req. Jud. Notice, Item 1. It further reads

(with Appellant’s emphasis): “Under Proposition 218, only California

registered voters, including renters, can vote in tax elections.

Corporations and foreigners get no new rights.” Id. The argument in

support distinguishes who can act on property assessments versus taxes.

Thus, while the rule may be different when it comes to who can vote on

property assessments, the voter intent was that registered voters are “the

electorate” for purposes of approving new taxes.

Appellant’s Opening Brief Page 19

Furthermore, to the extent Article XIIIA, Section 4, and Article

XIIIC, Section 2, are inconsistent, the latter trumps. See CAL. CONST.,

art. XIIIC, § 2 (“Notwithstanding any other provision in the

Constitution. . . .”). Even if local governments could manipulate the

term “qualified electors” in Article XIIIA, Section 4, the electorate

closed that loophole by requiring a vote of “the electorate,” not the

“qualified electors,” under Article XIIIC, Section 2, before taxes may be

imposed, extended, or increased. Id.

Altogether, the special tax is invalid under the California

Constitution--either because of Article XIIIA or Article XIIIC--because

only property owners and leaseholders were allowed to vote on the tax.

c. Registered, Natural-Persons Have theRight to Vote on Taxes under theCalifornia Constitution

The corollary to the special tax being invalid because only

hoteliers were allowed to vote is that the tax is invalid because the

City’s registered, natural-persons were not given the opportunity to vote

on it. Article XIIIC, Section 2, provides (with Appellant’s emphasis):

Local Government Tax Limitation. Notwithstandingany other provision of this Constitution:

***

This Court did the same thing recently against the City, albeit based on a8

parallel voter-approval requirement in Proposition 218. See Weisblat v. City

of San Diego, 176 Cal. App. 4th 1022, 1027 (2009) (holding that rental-unit

business tax was void because “not approved by a majority vote of the

municipal electors” under Article XIIIC.)

Appellant’s Opening Brief Page 20

(d) No local government may impose, extend, orincrease any special tax unless and until that tax issubmitted to the electorate and approved by a two-thirds vote.***

Here, the electorate--the registered, natural-person voters--was denied

the right to vote.

In this regard, the tax’s payee is irrelevant. Sales taxes are levied

against and are the responsibility of retailers, not their customers. See

Western Lithograph Co. v. State Bd. of Equal., 11 Cal. 2d 156, 162

(1938) (holding that sales tax is levied against retailer, not consumer).

Yet the Supreme Court has repeatedly struck down sales taxes that were

not approved by the requisite number of natural persons who are

registered to vote in the jurisdiction proposing the taxes. See, e.g.,

Rider, supra, 1 Cal. 4th at 6 (1991) (holding that sales tax was invalid

because, as a special tax, it did not receive requisite two-thirds voter

approval of the County’s voters); Santa Clara County Local Transp.

Auth. v. Guardino, 11 Cal. 4th 220 (1995) (holding that sales tax was

invalid because it did not receive requisite two-thirds voter approval).8

Appellant’s Opening Brief Page 21

Even special taxes levied against real property must be approved not by

the property owners but by the registered, natural-person voters. See,

e.g., Altadena Library Dist. v. Bloodgood, 192 Cal. App. 3d 585 (1987)

(concluding that special tax against real property to fund library services

was invalid because of failure to receive requisite two-thirds voter

approval).

Nothing in the California Constitution allows the City to

manipulate the definition of “the electorate” or “qualified electors” to

deny the right to vote to San Diego’s registered, natural-person voters.

According to Article II, Section 2, of the California Constitution: “A

United States citizen 18 years of age and resident in this State may

vote.” Nothing in the case law allows a local government imposing a

special tax to make up its own definition of “qualified electors” or

“electorate” for purposes of satisfying the California Constitution. No

case stands for that proposition because such a glaring loophole in the

constitutional protections for taxpayers would be quickly abused by tax-

crazed local governments who raise taxes by defining “qualified

electors” in a way that ensures victory at the ballot box while

circumventing the will of The People. Nothing in the history of

Appellant’s Opening Brief Page 22

Proposition 13, 62, 218, or 26 suggests that the voters intended such an

absurd outcome.

To the contrary, this Court has determined that the City is not

allowed to modify terms in the California Constitution to suit its

purposes. In Howard Jarvis Taxpayers Association, supra, 120 Cal.

App. 4th 374, the Court was called upon to determine the

constitutionality of a proposition requiring that certain amendments to

the Charter be approved by a super-majority vote of the City’s

electorate. Article XI, Section 3(a), of the California Constitution

provided that a charter may be adopted or amended by majority vote. Id.

at 385. This Court determined that the super-majority vote requirement

in the proposition could not be harmonized with the Constitution. Just

as this Court did not allow the City to change the majority requirement

to a two-thirds vote in Howard Jarvis Taxpayers Association, supra,

because such a modification was unconstitutional, this Court should not

allow the City to modify the term “qualified electorate” to apply to a

group of hotel landowners and leaseholders that may not even otherwise

be qualified to vote in San Diego or even in California generally

Appellant’s Opening Brief Page 23

because, for example, they are not natural persons or reside outside the

jurisdiction.

It is important to keep in mind that Proposition 218 is the “Right

to Vote on Taxes Act.” See Weisblat, supra, 176 Cal. App. 4th 1022.

Proposition 218’s statement of purpose reads in part:

The people of the State of California herebyfind and declare that Proposition 13 wasintended to provide effective tax relief and torequire voter approval of tax increases.However, local governments have subjectedtaxpayers to excessive tax, assessment, feeand charge increases that not only frustratethe purposes of voter approval for taxincreases, but also threaten the economicsecurity of all Californians and the Californiaeconomy itself.

Id. at 1038-1039 (emphasis added). The voter pamphlets were littered

with references to the right to vote on taxes. For example, the backers

of Proposition 218 said: “Proposition 218 simply extends the long

standing constitutional protection against politicians imposing tax

increases without voter approval.” Citizens Ass’n of Sunset Beach v.

Orange County Local Agency Formation Comm’n, 209 Cal. App. 4th

1182, 1196 (2012). Allowing a city to contort the definition of who is

qualified to vote and manipulate the outcome through the weighting of

Denying the City’s registered, natural-person voters of their right to vote9

on the special tax also runs afoul of the Equal Protection Clause. “[T]he right

to vote is a fundamental right” under the Equal Protection Clause. Sanchez v.

City of Modesto, 145 Cal. App. 4th 660, 678 (2006). As such, a proscription

on the voting right is subject to the most exacting scrutiny. Id. “Strict scrutiny

of legislative restrictions on the right to vote extends to elections on . . .

general obligation bonds[,] . . . municipal revenue bonds[,] . . . [and] school

district bonds.” County of Riverside v. Whitlock, 22 Cal.App.3d 863, 872

(1972) (citations omitted). The City has violated the equal-protection rights

of every registered, natural-person voter in the City.

In City of Phoenix, Arizona v. Kolodziejski, 399 U.S. 204 (1970), a city

resident who was otherwise qualified to vote in an election but owned no

property challenged the constitutionality of an election approving the issuance

of general obligation bonds in which only property owners were given the

franchise. The city argued that “since general obligation bonds are in effect

a lien on the real property subject to taxation by the issuing municipality . . .

the State is justified in recognizing the unique interests of real property owners

Appellant’s Opening Brief Page 24

votes by hotel businesses cannot be harmonized with the voters’ intent

to reserve for themselves the right to vote on taxes and thereby limit

local government’s ability to raise taxes without a vote.

The foregoing analysis demonstrates that the City violated the

California Constitution when it levied the special tax based on the

hoteliers’ vote, without ever asking the City’s registered, natural-person

voters to weigh in on the matter. Ignoring the meaning of “qualified

electors” under Article XIIIA and “electorate” under Article XIIIC is not

the only constitutional violation, but it is certainly the most obvious one.

Having never been approved by the City’s qualified electors or

electorate, the special tax is constitutionally invalid.9

by allowing only property taxpayers to participate in elections to approve the

issuance of general obligation bonds.” Id. at 208. In holding that non-

propertied taxpayers should not have been excluded from the franchise, the

High Court stated: “it is unquestioned that all residents of [the City], property

owners and nonproperty owners alike, have a substantial interest in thepublic facilities and the services available in the city and will substantiallybe affected by the outcome of the bond election at issue in this case.” Id. at

209 (emphasis added). See also Kramer v. Union Free School Dist., 395 U.S.

621 (1969) (holding that state may not restrict vote in school district elections

to owners and lessees of real property and parents of school children because

exclusion of otherwise qualified voters was not shown to be necessary to

promote compelling state interest); Cipriano v. City of Houma, 395 U.S. 701

(1969) (holding that state may not restrict vote on approval of revenue bonds

to finance local improvements only to property owners).

Because the CCFD is being created “pursuant to the City’s charter powers”10

(see Admin. R. 39:5517; see also Other R. OR7:94), Appellant expects no

dispute that the special tax at the heart of the CCFD’s financing is also subject

to the requirements and limitations contained in the San Diego City Charter.

Appellant’s Opening Brief Page 25

2. The City Violated the San Diego City Charter

For the same reasons, the special tax also fails to pass muster

under the San Diego City Charter. That is because the City Charter

defines “qualified electors” in accordance with the laws governing

general state elections and requires the approval of the “qualified

electors” for any special tax. The hoteliers who voted on the special tax

are not “qualified electors” under the City Charter. 10

Consider first the City Charter section bearing the title “Qualified

Electors”:

Appellant’s Opening Brief Page 26

The qualifications of an elector at any electionheld in the City under the provisions of thisCharter shall be the same as those prescribedby the general law of the State for thequalification of electors at General StateElections. No person shall be eligible to voteat such City election until he has conformedto the general State law governing theregistration of voters.

JA III:604 (Req. for Jud. Notice, Item 2 (SAN DIEGO CITY CHARTER §

6)) (emphasis added). Next consider the prohibition on special taxes in

the City Charter section entitled “Limit on Tax Levy”:

The tax levy authorized by the Council tomeet the Municipal expenses for each fiscalyear shall not exceed the rate of $1.34 on each$100.00 of assessed valuation of the real andpersonal property within the city. * * * Nospecial tax shall be permitted except asexpressly authorized by this Charter. Theforegoing limitations shall not apply in theevent of any great necessity or emergency, inwhich case they may be temporarilysuspended, provided that. . . . * * *

JA III:615-616 (Item 3 (SAN DIEGO CITY CHARTER § 76)) (emphasis

added). Lastly, consider the “qualified electors” voting requirement

codified in the City Charter section entitled “Special Taxes”:

Notwithstanding any provision of this Charterto the contrary, a special tax, as authorized by

Appellant’s Opening Brief Page 27

Article XIIIA of the California Constitutionmay be levied by the Council only if theproposed levy has been approved by a two-thirds vote of the qualified electors of theCity voting on the proposition; or if thespecial tax is to be levied upon less than theentire City, then the tax may be levied by theCouncil only if the proposed levy has beenapproved by a two-thirds vote of the qualifiedelectors voting on the proposition in the areaof the City in which the tax is to be levied.

JA III:616 (Item 3 (SAN DIEGO CITY CHARTER § 76.1)) (emphasis

added).

The special tax is not levied upon less than the entire City. Even

if it were, the levy must be approved by a two-thirds vote of the

qualified electors “in the area of the City” in which the tax is to be

levied. The levy is City-wide; the CCFD’s geographic limits and the

City’s are the same. Because the area of the City in which the tax is to

be levied is the entire City, the special tax should have been subject to

a vote of the qualified electors of the City, not the property owners and

leaseholders of the CCFD.

Furthermore, there is no definition in the Charter that is

inconsistent with Charter Section 76.1. The Charter does not read

“Notwithstanding any provision of this Charter or some later-adopted

Neilson’s and Foothill-De Anza’s analyses of “qualified electors” under the11

Elections Code equally prove that the City’s voters--the flesh-and-blood U.S.

citizens who have registered to vote--qualify to vote under state law.

Appellant’s Opening Brief Page 28

municipal code provision to the contrary. . . ,” as the City would like.

Simply put, there is nothing in the Charter that gives the City the

authority to alter a Charter-defined term through the adoption of a

municipal code provision (viz., the Procedural Ordinance).

There can be no dispute that the City’s residents who are qualified

to vote in California general elections were not given the opportunity to

vote on the special tax. See JA II:540 (Briggs Decl., ¶ 2). So even if the

City could put forward a credible argument that Article XIIIA allows for

the hoteliers to be treated as “qualified electors” for purposes of voting

on the tax--which, of course, is impossible under Neilson and Foothill-

De Anza--and even if the City could somehow get around the vote of the

“electorate” requirement in Article XIIIC--which is even less likely--the

City cannot get around the Charter’s explicit requirement that special

taxes be approved by the registered, natural-person voters who vote

during general elections and who the Charter identifies as the “qualified

electors of the City.” The City’s hoteliers may not vote in general11

elections, and thus they were not entitled to vote on the special tax. The

Appellant’s Opening Brief Page 29

tax is therefore illegal under the City Charter because it relies on general

state law to define “qualified electors.”

B. The City Violated the California EnvironmentalQuality Act by Failing to Prepare an EnvironmentalImpact Report for the Convention Center ExpansionProject and Not Taking the Role of Lead Agency

If the Court is inclined to invalidate the special tax on state

constitutional and/or local charter grounds, there is no need to reach the

CEQA issues. If there is doubt, however, CEQA was also violated. The

City was required to certify an environmental document before taking

the actions it seeks to have validated here--that is to say, the City’s

various approvals related to the expansion project. The City also failed

to act as the lead agency. Each of these defects is discussed in turn.

1. The California Environmental Quality ActApplies to the Expansion Project

CEQA applies to the expansion project. Under CEQA, a

“project” is “[a]n activity undertaken by any public agency” that “may

cause either a direct physical change in the environment or a reasonably

foreseeable indirect physical change in the environment.” PUB. RES.

CODE § 21065(a). The term refers to “the whole of the action.” CAL.

CODE OF REGS., tit. 14, § 15378(a). The definition applies even when

Appellant’s Opening Brief Page 30

there are “several discretionary approvals” and “does not mean each

separate approval.” Id., § 15378(c). In deciding whether an activity is

a “project,” the Supreme Court has emphasized that the statute is “to be

interpreted in such a manner as to afford the fullest possible protection

to the environment within the reasonable scope of the statutory

language.” Friends of Mammoth v. Board of Supervisors, 8 Cal. 3d 247,

259 (1972).

In the trial court, the City argued that it did not commit to a

project but “only approved a funding mechanism.” JA III:701, ln. 16.

CEQA Guidelines Section 15378(b)(4) exempts from the definition of

“project” the “creation of a government funding mechanism or other

government fiscal activities, which do not involve any commitment to

any specific project which may result in a potentially significant

physical impact on the environment.” The problem here is that the

financing is committed to a specific project which may result in a

potentially significant impact.

CEQA does not apply when there is no specific plan for the use

of funds; review would not be meaningful because there would not be

an identifiable impact to study. See Friends of Sierra R.R. v. Tuolumne

Appellant’s Opening Brief Page 31

Park & Recreation Dist., 147 Cal. App. 4th 643, 657 (2007) (finding

CEQA review premature in absence of plan involving identifiable

impact; “no specific plans were on the table”). In contrast, CEQA

applies when there is a specific plan for the funds. See County of

Amador v. City of Plymouth, 149 Cal. App. 4th 1089, 1102-1103 & 1112

(2007) (holding that city’s agreement to provide municipal services to

tribe constituted commitment to specific project under CEQA and was

not mere funding mechanism exempt from review); accord Kaufman &

Broad-South Bay, Inc. v. Morgan Hill Unified School Dist., 9 Cal. App.

4th 464, 474 (1992) (concluding that CEQA review not required for

community facilities district created for purpose of generating funds for

unspecified use at unknown future date, but noting that “[w]hen it makes

those decisions, which depend in large part on the pattern of

development within the District, it will have to examine the

environmental impacts”).

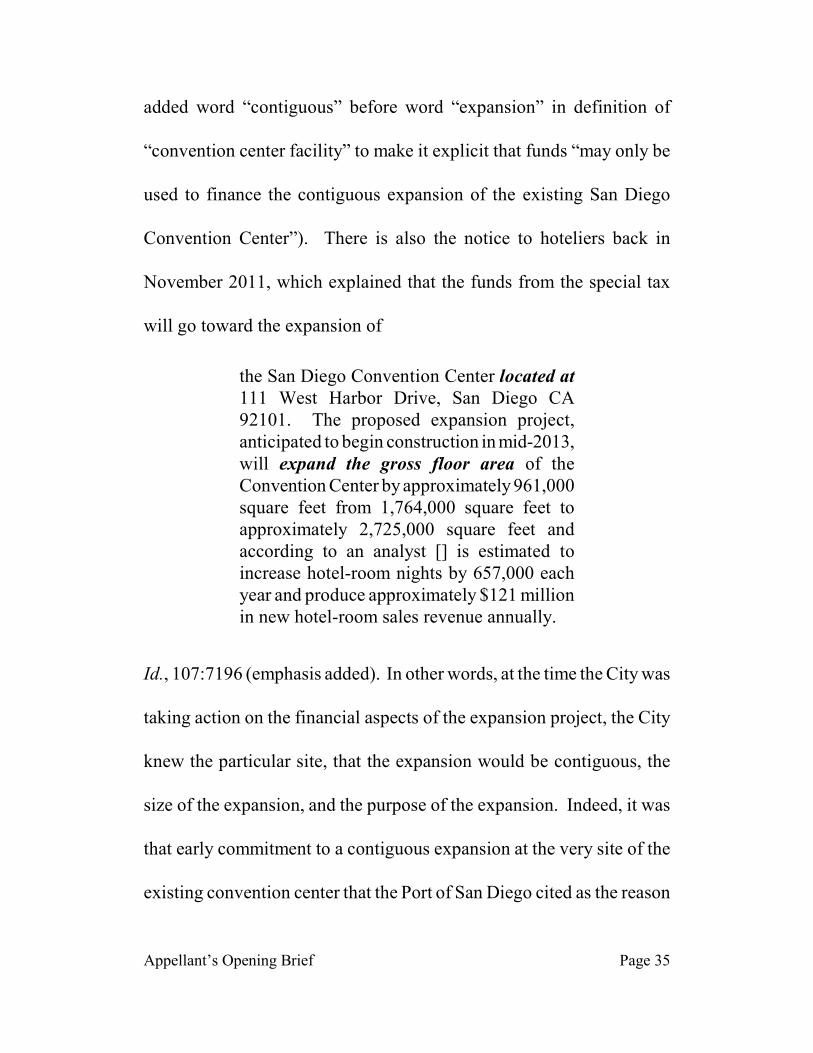

Here, there was a specific plan. There is also the notice to

hoteliers back in November 2011, which explained that the funds from

the special tax will go toward the expansion of

Appellant’s Opening Brief Page 32

the San Diego Convention Center located at111 West Harbor Drive, San Diego CA92101. The proposed expansion project,anticipated to begin construction in mid-2013,will expand the gross floor area of theConvention Center by approximately 961,000square feet from 1,764,000 square feet toapproximately 2,725,000 square feet andaccording to an analyst [] is estimated toincrease hotel-room nights by 657,000 eachyear and produce approximately $121 millionin new hotel-room sales revenue annually.

Id., 107:7196 (emphasis added). The funding was limited to a project

and location. See, e.g., Admin. R. 31:5473 (memorandum explaining

that city attorney’s office added word “contiguous” before word

“expansion” in definition of “convention center facility” to make it

explicit that funds “may only be used to finance the contiguous

expansion of the existing San Diego Convention Center”).

Because this is not a mere funding mechanism, but a funding

mechanism that involves a commitment to a specific project, CEQA

clearly applies.

2. The City Firmly Committed Itself to theExpansion Project Before the EnvironmentalImpact Report Was Certified

Appellant’s Opening Brief Page 33

The next question is when CEQA review had to be done. The

City made a firm commitment to the expansion project months before

the EIR was certified even though CEQA prohibits premature

commitments. The CEQA Guidelines clarify that environmental

documents should “be prepared as early as feasible in the planning

process to enable environmental considerations to influence project

program and design and yet late enough to provide meaningful

information for environmental assessment.” CAL. CODE OF REGS., tit.

14, § 15004(b). “Approval” is defined by the CEQA Guidelines to be

“the decision by a public agency which commits the agency to a definite

course of action in regard to a project intended to be carried out by any

person.” Id., § 15352 (emphasis added).

The Supreme Court has recognized that an EIR is intended to

“demonstrate to an apprehensive citizenry that the agency has in fact

analyzed and considered the ecological implications of its actions.”

Save Tara v. City of West Hollywood, 45 Cal.4th 116, 136 (2008) (citing

No Oil, Inc. v. City of Los Angeles, 13 Cal.3d 68, 86 (1974)). When an

agency reaches a binding, detailed agreement and “publicly commits

resources and governmental prestige to the project, the agency’s

Appellant’s Opening Brief Page 34

reservation of CEQA review until a later, final approval stage is unlikely

to convince public observers that before committing itself to the project

the agency fully considered the project’s environmental consequences.”

Id. Instead, the belated environmental document appears to be a post

hoc rationalization. Id. When determining whether a CEQA document

is required at any given stage, courts should determine whether “as a

practical matter, the agency committed itself to the project as a whole or

to any particular features, so as to effectively preclude any alternatives

or mitigation measures that CEQA would otherwise require to be

considered, including the alternative of not going forward with the

project.” Id. at 139. Conditional final approval on CEQA compliance

is relevant but not determinative. Id.

The City was long past the preliminary-consideration stage when

it approved various resolutions and ordinances before the EIR for the

expansion project was certified, and the evidence in this regard is

overwhelming. To start, the City has consistently promoted a

contiguous expansion of the Convention Center as a very specific

project at a specific site to be funded by the special tax. See, e.g.,

Admin. R. 31:5473 (memorandum explaining that city attorney’s office

Appellant’s Opening Brief Page 35

added word “contiguous” before word “expansion” in definition of

“convention center facility” to make it explicit that funds “may only be

used to finance the contiguous expansion of the existing San Diego

Convention Center”). There is also the notice to hoteliers back in

November 2011, which explained that the funds from the special tax

will go toward the expansion of

the San Diego Convention Center located at111 West Harbor Drive, San Diego CA92101. The proposed expansion project,anticipated to begin construction in mid-2013,will expand the gross floor area of theConvention Center by approximately 961,000square feet from 1,764,000 square feet toapproximately 2,725,000 square feet andaccording to an analyst [] is estimated toincrease hotel-room nights by 657,000 eachyear and produce approximately $121 millionin new hotel-room sales revenue annually.

Id., 107:7196 (emphasis added). In other words, at the time the City was

taking action on the financial aspects of the expansion project, the City

knew the particular site, that the expansion would be contiguous, the

size of the expansion, and the purpose of the expansion. Indeed, it was

that early commitment to a contiguous expansion at the very site of the

existing convention center that the Port of San Diego cited as the reason

Appellant’s Opening Brief Page 36

for rejecting alternative sites that would result in a non-contiguous

expansion. Id., 17:841-843 (§§ 7.4.1.2, 7.4.1.3 & 7.4.1.4 (explaining

that three alternatives were rejected because they “would not result in an

expanded SDCC contiguous to the existing SDCC”).

Other evidence confirms the City’s commitment to the expansion

project prior to certification of an EIR. When it comes to demonstrating

commitment, there is a difference between staff statements and high-

level official statements. Staff statements do not demonstrate agency

approval for CEQA purposes, but the situation is different when the

statements come from highly authoritative sources. See Neighbors for

v. City of County of San Francisco, 217 Cal. App. 4th 540, 558 (2013)

(distinguishing expressions of enthusiasm for a project by agency’s staff

members with public statements in Save Tara from highly authoritative

sources). Here, highly authoritative representatives of the City were

committed to the Project. The then-mayor’s commitment was evident

early on. See, e.g., Admin. R. 99:7011-7013 (mayor’s May 11, 2011

detailed fact sheet announcing largest component of financing plan for

expansion and describing new plans); 66:5959-5960 (mayor’s May 7,

2012 comments to city council noting that City’s approval would keep

The city council and the mayor also approved various resolutions relating12

to the expansion project long before the EIR was certified. See, e.g., Admin.

R. 1:1-5, 2:6-19, 3:20-34; 4:35-39; 5:40-58; 6:59-66; 7:67-77; 8:78-81; 9:82-

87; 10:88-90.

Appellant’s Opening Brief Page 37

expansion of Convention Center on track and thanking city council for

strong support so far). Members of the city council also expressed

public support for the expansion back in May 2012, months before the

EIR was certified. Id., 66:5986, lns. 7-8 (Kevin Faulconer’s statement12

that he remains “strongly supportive of an expanded Convention

Center”); p. 5990, lns. 8-11 (Todd Gloria’s comment: “But as a strong

supporter of expanding the Convention Center, I’m happy to cast my

vote in favor of this. Encourage my colleagues to do the same.”); p.

5993 (Carl DeMaio’s statements that he supports action in hopes that

City can move forward with project); and p. 5995, lns. 8-9 (Sherri

Lightner’s statement that she supports and has supported idea of

Convention Center expansion). Back in December 2011, the City’s

chief financial officer was urging the city council to form the CCFD and

approve a notice of intention for levying the special tax and a notice of

intention for the bonded indebtedness. Id., 113:7252 (PowerPoint

presentation). By May 8, 2012, the City was already working on the

environmental review, engineering, and architecture but needed more

Appellant’s Opening Brief Page 38

money for those firms. Id., 10:88-89 (resolution amending architectural

and consultant contracts to authorize additional funds for expansion

project).

The fact that the city council gave notice of is intention to levy the

special tax and incur the bonded indebtedness before the EIR was

certified but after the city attorney advised them that the CCFD funds

“may only be used to finance the renovation and expansion of the San

Diego Convention Center” is further proof that the City was committed

to a specific course of action before it had complied with CEQA. Id.,

28:5465 (memo dated Oct. 6, 2011). Indeed, by January 23, 2012, it was

so clear to the public that the City had committed itself to the expansion

project that it received a critical comment letter pointing out the CEQA

violation and describing some of the other evidence proving it. Id.,

127:7324-7335. The very next morning--just hours before the city

council’s afternoon session at which it approved three resolutions at

issue here (Admin. R. 4:40-58, 5:59-66, 6:67-77)--the mayor wanted a

briefing from an assistant city attorney on the “CEQA issue” and was

expecting no problems because he (wrongly) believed that “they are not

The City was concerned because the same issue had been raised in a13

pending lawsuit over the Plaza de Panama project in Balboa Park. The

Honorable Judith Hayes eventually ruled that the City made a premature

commitment to the project without certifying an EIR based on similar

municipal cheer-leading.

The City may attempt to argue that it was good enough for it to consider14

the draft EIR before it approved the resolutions and ordinances that it seeks to

validate here as items 1 through 10 in the administrative record. That

argument will fail for the simple reason that the draft EIR was not even

released until several days later: viz., on May 14, 2012. See Admin. R.

153:7669; JA 3:658-659 (Req. for Jud. Notice, Item 4). The copy of the draft

EIR’s notice of availability in the administrative record does not specify the

date on which it was issued (though it shows the date it was received by the

city: May 16, 2012). The copy in the request for judicial notice indicates that

the draft was released on May 14, 2012.

Appellant’s Opening Brief Page 39

voting on a ‘project.’” See Other R. 40:341 (assistant actually putting13

“project” in quotes). Additional evidence of the City’s premature

commitment to the expansion project was presented to the city council

in May 2012. Id., 145:7636-7651.

Altogether, the City committed specifically to the expansion

project and should not have approved it until there was a certified EIR.14

3. The City Failed to Act as Lead Agency for theExpansion Project

The first CEQA violation, discussed above, is that no approvals

related to the project could have been given prior to certification of the

EIR. CAL. CODE OF REGS., tit. 14, § 15090 (requiring certain findings

Appellant’s Opening Brief Page 40

prior to project approval, including that final EIR has been completed

in accordance with CEQA). As a separate violation, the City was the

proper lead agency and should have conducted CEQA review before

approving the many resolutions and ordinances it now seeks to validate.

“If the project will be carried out by a public agency, that agency

shall be the Lead Agency even if the project would be located within the

jurisdiction of another public agency.” CAL. CODE OF REGS., tit. 14, §

15051(a). When more than one public agency is involved in a project,

“the public agency that shoulders the primary responsibility for creating

and implementing a project is the lead agency, even though other public

agencies have a role in approving or realizing it.” Planning & Conserv.

League v. Castaic Lake Water Agency, 180 Cal. App. 4th 210, 239

(2009). When more than one agency could be the lead agency, the

agency that acts first is the lead agency. CAL. CODE OF REGS., tit. 14, §

15051(c).

Expansion of the convention center is the City’s project. The first

line of the first page of the EIR indicates that the expansion project is

the City’s proposal. Admin. R. 17:218. The Notice of Determination

identifies the City as a “project applicant.” Id., 178:8311. The EIR

Appellant’s Opening Brief Page 41

shows that the City acted first in implementing the expansion project by

approving the financial aspects. Id., 17:220 (EIR identifying financing,

which had happened before any of the other necessary approvals listed

in the EIR, as one of project’s required approvals). In 2011, the City

took over the contracts and agreements for the design of the expansion

and other related matters. Id., 1:1-5. This take-over included the

contract for the expansion project’s “environmental review consulting

services,” including those provided by EIR author ICF. Id., 1:2, ¶ 1(d)

(take-over language); 17:120 (EIR cover). The City is the agency that

entered into the construction contract for the expansion project. Id.,

182:8318-8379. Indeed, the Port will be giving money to the City in

order to finance a portion of the expansion project. Id., 164:8245 (sixth

“Whereas” clause).

There are many documents in the record that show the City is

carrying out the expansion project, but at this point going through them

would be unnecessarily cumulative. The evidence cited above is more

than sufficient to prove that the City improperly ceded its role as lead

agency to the Port and, even if it was merely a responsible agency,

approved the project before the EIR was certified.

Appellant’s Opening Brief Page 42

4. The California Environmental Quality Act IssuesAre Not Moot

The City argued in the trial court that the CEQA issues are moot

because the Port completed an EIR for the expansion project after this

lawsuit was filed. The City is wrong. In Sustainable Transportation

Advocates of Santa Barbara v. Santa Barbara County Association of

Governments, 179 Cal. App. 4th 113 (2010), the plaintiff challenged the

agency’s failure to conduct environmental review before enacting a

retail sales and use tax plan to finance transportation projects. Three

months after the measure’s approval, the agency certified an

environmental document for a transportation plan that purported to

consider all projects in the financing plan. Id. at 118. The Court of

Appeal explained that the action was not moot because the challenge

was that environmental review was required at the time of approval,

“not three months later.” Id.

Accordingly, the CEQA issues raised by this lawsuit are not moot.

Appellant’s Opening Brief Page 43

V. CONCLUSION

For all of these reasons, the trial court’s decision should be

reversed.

PROOF OF SERVICE

1. My name is _________________________________. I am over the age of eighteen. I am employed in the

State of California, County of _________________________ .

2. My _____ business _____ residence address is ___________________________________________________

_____________________________________________________________________________________.

3. On _____________________, _________, I served ____ an original copy ____a true and correct copy of the

following documents:____________________________________________________________________

_____________________________________________________________________________________

_____________________________________________________________________________________

_____________________________________________________________________________________

_____________________________________________________________________________________

4. I served the documents on the person(s) identified on the attached mailing/service list as follows:

___ by personal service. I personally delivered the documents to the person(s) at the address(es) indicated on the

list.

___ by U.S. mail. I sealed the documents in an envelope or package addressed to the person(s) at the address(es)

indicated on the list, with first-class postage fully prepaid, and then I

___ deposited the envelope/package with the U.S. Postal Service

___ placed the envelope/package in a box for outgoing mail in accordance with my office’s ordinary

practices for collecting and processing outgoing mail, with which I am readily familiar. On the same

day that mail is placed in the box for outgoing mail, it is deposited in the ordinary course of business

with the U.S. Postal Service.

I am a resident of or employed in the county where the mailing occurred. The mailing occurred in the city of

_________________________, California.

___ by overnight delivery . I sealed the documents in an envelope/package provided by an overnight-delivery

service and addressed to the person(s) at the address(es) indicated on the list, and then I placed the

envelope/package for collection and overnight delivery in the service’s box regularly utilized for receiving items

for overnight delivery or at the service’s office where such items are accepted for overnight delivery.

___ by facsim ile transmission. Based on an agreement of the parties or a court order, I sent the documents to the

person(s) at the fax number(s) shown on the list. Afterward, the fax machine from which the documents were

sent reported that they were sent successfully.

___ by e-m ail delivery. Based on an agreement of the parties or a court order, I sent the documents to the person(s)

at the e-mail address(es) shown on the list. I did not receive, within a reasonable period of time afterward, any

electronic message or other indication that the transmission was unsuccessful.

I declare under penalty of perjury under the laws _____ of the United States _____ of the State of California

that the foregoing is true and correct.

Date: _____________________, _________ Signature: __________________________________

SERVICE LISTIn the Court of Appeal of the State of California

Fourth Appellate District - Division OneD063997

City of San Diego v. All Interested Persons, etc.San Diego County Superior Court Case Nos. 37-2012-00094831-CU-MC-CTL;

37-2012-00097148-CU-MC-CTL; 37-2012-00100333-CU-TT-CTL _____________________________________________________

Jan I. GoldsmithDonald R. Worley, Glenn SpitzerM. Travis PhelpsOffice of the City Attorney1200 Third Avenue, Suite 1100San Diego, CA 92101-4100

Attorneys for Plaintiff/Respondent City ofSan Diego

Daniel C. BortSarah C. MarriottOrrick, Herrington & Sutcliffe LLPThe Orrick Building405 Howard StreetSan Francisco, CA 94105

Attorneys for Plaintiff/Respondent City ofSan Diego

Michael WeedOrrick, Herrington & Sutcliffe, LLP400 Capitol Mall, Suite 3000Sacramento, CA 95814-4497

Attorneys for Plaintiff/Respondent City ofSan Diego

Craig A. ShermanLaw Office of Craig A. Sherman1901 First Avenue, Suite 219San Diego, CA 92101

Attorneys for Defendant and AppellantMelvin Shapiro

Hon. Ronald S. Pragerc/o Civil Appeals DivisionSan Diego Superior Court220 Broadway, Room 3005San Diego, CA 92101

Superior Court

California Supreme Court350 McAllister Street, Second FloorSan Francisco, CA 941024783

By electronic service only

Office of the Attorney General1200 3rd Avenue, Suite 1620San Diego, CA 92101