Course-Bank Management Co. Compare- IDLS & Bank Asia

109

ANALYSIS & COMPARISON OF BANK ASIA LIMITED AND IDLC FINANCE LIMITED Course: FIN435 Section: 1 Submitted to: M. Morshed (MDM) Senior Lecturer School of Business Submitted by: Md. Ferdous Khan Samuel 111 0706 030 Page | 1

-

Upload

md-ferdous-khan-samuel -

Category

Documents

-

view

278 -

download

0

Transcript of Course-Bank Management Co. Compare- IDLS & Bank Asia

ANALYSIS & COMPARISON OF BANK ASIA LIMITED AND IDLC FINANCE LIMITED

Course: FIN435Section: 1

Submitted to:

M. Morshed (MDM)

Senior Lecturer

School of Business

Submitted by:

Md. Ferdous Khan Samuel 111 0706 030

Page | 1

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY....................................................................................................3

2 INTRODUCTION..................................................................................................................4

3 OBJECTIVES.........................................................................................................................5

4 METHODOLOGY.................................................................................................................6

5 LIMITATIONS......................................................................................................................7

6 OVERVIEW OF BANK ASIA LTD & IDLC FINANCE LTD.........................................8

7 FINDINGS AND ANALYSIS..............................................................................................11

7.1 EFFICIENCY................................................................................................................11

7.2 PROFITABILITY..........................................................................................................16

7.3 MARKET POSITION....................................................................................................27

7.4 LIQUIDITY....................................................................................................................29

7.5 FINANCIAL RISK.........................................................................................................33

7.6 INVESTORS’ VIEWPOINT.........................................................................................36

8 RECOMMENDATIONS.....................................................................................................42

9 CONCLUSION.....................................................................................................................44

10 BIBLIOGRAPHY................................................................................................................45

APPENDIX…………………………………………………………………………………46

Page | 2

EXECUTIVE SUMMARY

The report compares the performance of Bank Asia Limited, a commercial bank, and

IDLCFinance Limited, a non-bank financial institution, within the time period of 2008 to

2013, making use of financial statements such as balance sheet, profit & loss account, and all

other relevant data required for the purpose of analyzing the financial performances. Both the

bank and the non-bank are enlisted in the Dhaka Stock Exchange (DSE). The overall

performances were analyzed using various financial ratios regarding liquidity, efficiency,

financial risk, and profitability, market ratios. The resulting ratios were used to comparison

purposes in order to come up with the findings from the analysis.

The reportcovers the introduction, objectives, limitation, methodology, the overview of Bank

Asia Limited and IDLC Finance Limited,the findings and analysis with recommendations and

the conclusion. One of the major areas of this report is the findings and analysis section as it

discusses all the resulting information essential for potential investors. The appendix,

provided in the end, includes all the relevant calculations used throughout the report.

Page | 3

INTRODUCTION

Bank Asia Limited and IDLC Finance Limited, which is a non-bank financial institution, are

both enlisted in the Dhaka Stock Exchange (DSE). In this report, we compare the

performances between Bank Asia Limited, which is the assigned commercial bank, and IDLC

Finance Limited, which is the randomly selected non-bank financial institution. We are to

analyze both of their performances based on financial ratios and come up with the findings

and conclusion.

Bank Asia has been launched by a group of successful entrepreneurs with recognized

standing in the society. It set milestone by acquiring the business operations of the Bank of

Nova Scotia in Dhaka, first in the banking history of Bangladesh. It again repeated the

performance by acquiring the Bangladesh operations of Muslim Commercial Bank Ltd.

(MCB), a Pakistani bank. In the year 2003, the Bank again came to the limelight with

oversubscription of the Initial Public Offering of the shares of the Bank, which was a record

(55 times) in our capital market's history and its shares commands respectable premium. The

asset and liability growth has been remarkable. Bank Asia Limited started its service with a

vision to serve people with modern and innovative banking products and services at

affordable charge. Being parallel to the cutting edge technology the Bank is offering online

banking with added delivery channels like ATM, Tele-banking, SMS and Net Banking. And

as part of the bank's commitment to provide all modern and value added banking service in

keeping with the very best standard in a globalize world.

IDLC was initially established in Bangladesh in 1985 through the collaboration of

International Finance Corporation (IFC) of the World Bank, German Investment and

Development Company (DEG), Kookmin Bank and Korean Development Leasing

Corporation of South Korea, the Aga Khan Fund for Economic Development, the City Bank

Limited, IPDC of Bangladesh Limited, and SadharanBima Corporation. As the company

evolved, initial foreign shareholding of 49% was gradually withdrawn and the last foreign

shareholding was bought out by local sponsors in 2009. IDLC has grown to become the

largest multi-product non-bank financial institution of Bangladesh with almost equal focus in

Corporate, Retail and SME sectors. Moreover, IDLC has a significant presence in the Capital

Markets. Its merchant banking arm, IDLC Investments Limited, a wholly-owned subsidiary

of IDLC is a premier brand for investment banking in the country. Its stock brokerage arm,

Page | 4

IDLC Securities Limited, another wholly-owned subsidiary of IDLC is also amongst the top

five brokers in the country.

OBJECTIVES

The objective of the project is to evaluate the performances of Bank Asia Limited and IDLC

Finance Limited. The primary objective of the term paper is to analyze the performance of

Bank Asia Limited and IDLC Finance Limited in terms of their liquidity positions, financial

risk positions, efficiency ratios, profitability ratios, market positions and investors’ view

point. Their performances will be calculated and analyzed over the period between 2008 and

2013 using both time series and cross-sectional analysis. Based on the ratios calculated, the

resulting findings will be discussed.

As a result, the findings or resulting information will be useful to assess the overall

performances of Bank Asia Limited and IDLC Finance Limited which can be used as the

basis for investment decisions by potential investors. Thus, performances are also analyzed

according to investors’ view point. Lastly, some recommendations on policy implementation

are provided which can be used to enhance their performances.

Page | 5

METHODOLOGY

The financial data for all the years between 2008 and 2013 have been collected from the

annual reports of Bank Asia Limited and IDLC Finance Limited available in their respective

websites. Using the financial data provided in the annual reports, all the required ratios were

calculated accordingly. After analyzing the performances of the bank and non-bank financial

institution individually through both time series and cross-sectional analysis, their overall

performances throughout the periods were compared.Then, the resulting findings were

revealed and discusses in the findings and analysis section. Lastly, a list of suggestions and

recommendations were discussed regarding which one would be better to invest as a potential

investor.

Page | 6

LIMITATIONS

In the course of attempting to successfully complete the term paper with effective results,

certain limitations were inevitable. There were several limitationsthat restricted the ability to

disclose some of the information of both Bank Asia Limited and IDLC Finance Limited. The

number of limitations includes the following:

Since the performance analysis has been done based on the financial data of the last

few years only, the results might be limited to a certain extent.

The findings are based only on the outcomes of the financial ratios. The findings and

recommendations do not reflect the future perspectives of the bank and the non-bank

financial institution.

The annual reports may have limitations in terms of data discrepancies which make it

difficult to calculate some ratios and thus affect the quality of the analysis or

comparison to some extent.

During the completion of the term paper, few ratios could not be dealt with due to the

absence of required relevant information in the annual reports of Bank Asia Limited

and IDLC Finance Limited. Thus, some relevant information could not be addressed.

Page | 7

OVERVIEW OF BANK ASIA LIMITED

Bank Asia Limited set milestone by acquiring the business operations of the Bank of Nova

Scotia in Dhaka, first in the banking history of Bangladesh. It again repeated the performance

by acquiring the Bangladesh operations of Muslim Commercial Bank Ltd. (MCB), a

Pakistani bank.

The asset and liability growth has been remarkable. Bank Asia has been actively participating

in the local money market as well as foreign currency market without exposing the Bank to

vulnerable positions.Bank Asia Limited started its service with a vision to serve people with

modern and innovative banking products and services at affordable charge. Being parallel to

the cutting edge technology the Bank is offering online banking with added delivery channels

like ATM, Tele-banking, SMS and Net Banking. And as part of the bank's commitment to

provide all modern and value added banking service in keeping with the very best standard in

a globalize world.

Bank Asia is a third generation public limited commercial bank. It received the Certificate of

Incorporation on September 28, 1999 and came to operation on November 27, 1999. Now

after 12 faithful years of dedicated and reliable services, Bank Asia has created an envious

position for itself among the leading banks of the country with an Asset base of TK. 117

billion, Deposit of TK 95 Billion and 70+ outlets all over the country. But most importantly,

the Bank has an unsurpassed legacy attached with its image.

VISION

Bank Asia's vision is to have a poverty free Bangladesh in course of a generation in the new

millennium, reflecting the national dream. Its vision is to build a society where human dignity

and human rights receive the highest consideration along with reduction of poverty.

MISSION

To assist in bringing high quality service to our customers and to participate in the

growth and expansion of our national economy

To set high standards of integrity and bring total satisfaction to our clients,

shareholders and employees

Page | 8

To become the most sought after bank in the country, rendering technology driven

innovative services by our dedicated team of professionals

CORE VALUES

Place customer interest and satisfaction as first priority and provide customized

banking products and services

Value addition to the stakeholders through attaining excellence in banking operations

Maintain high ethical standard and transparency in dealings

Be a compliant institution through adhering to all regulatory requirements

Contribute significantly for the betterment of the society

Ensure higher degree of motivation and dignified working environment for our human

capital and respect optimal work-life balance

Committed to protect the environment and go green

OVERVIEW OF IDLC FINANCE LIMITED

IDLC was initially established in Bangladesh in 1985 through the collaboration of

International Finance Corporation (IFC) of the World Bank, German Investment and

Development Company (DEG), Kookmin Bank and Korean Development Leasing

Corporation of South Korea, the Aga Khan Fund for Economic Development, the City Bank

Limited, IPDC of Bangladesh Limited, and SadharanBima Corporation. As the company

evolved, initial foreign shareholding of 49% was gradually withdrawn and the last foreign

shareholding was bought out by local sponsors in 2009.

IDLC has grown to become the largest multi-product Non-Bank Financial Institution of

Bangladesh, with almost equal focus in Corporate, Retail and SME sectors. IDLC has a

significant presence in the capital markets.Over the years, IDLC has attained a significant

presence in the corporate sector of Bangladesh. IDLC continues to play a pioneering role in

introducing and popularizing a variety of financial instruments suiting ever-changing

requirements of its fast-growing clients.

IDLC Finance Limited has two subsidiaries:IDLC Securities Limited and IDLC Investments

Limited.IDLC Securities Limited, a fully-owned subsidiary of IDLC, offers full-fledged

international standard brokerage services for both its retail and institutional clients. It has

Page | 9

seats on both Dhaka Stock Exchange Limited and Chittagong Stock Exchange Limited. It is

also a Depository Participant (DP) of Central Depository Bangladesh Limited (CDBL).As per

requirement of the Securities & Exchange Commission (SEC), IDLC formed a separate

subsidiary on May 19, 2010 in the name of ‘IDLC Investments Limited’, in order to transfer

its existing merchant banking activities to the newly formed entity. IDLC applied to SEC to

transfer the existing merchant banking license of IDLC Finance Limited to IDLC Investments

Limited. Accordingly, IDLC Investments Limited has started its operations from August 16,

2011 to offer merchant banking services to both its individual and institutional clients.

VISION

To be the best financial brand in the country.

MISSION

To focus on quality growth, superior customer experience and sustainable business practices.

Strategic Objectives – 2012/2013

Grow and develop our talent pool

Fully leverage new core banking platform

Optimize distribution points

Grow and diversify funding sources

Grow sales and service capabilities in Consumer Division

Aggressively grow SME portfolio

Focus on top-tier clients in Corporate

Consolidate capital market operations and enhance capabilities

Embrace internationally accepted corporate governance and sustainable business

practices

Page | 10

FINDINGS & ANALYSIS

EFFICIENCY RATIOS

Asset Management Efficient/ Asset Utilization

2009 2010 2011 2012 2013Bank Asia 6.01% 6.34% 5.64% 5.58% 5.16%

IDLC 8.43% 11.31% 6.93% 6.36% 5.48%

2009 2010 2011 2012 20130.00%

2.00%

4.00%

6.00%

8.00%

10.00%

12.00%

Bank AsiaIDLC

Bank Asia: For Bank Asia, every 100 TK asset generates TK 6.01in operating revenue in the

year 2009. It indicates how efficiently Bank Asia manages its assets to generate revenue.

From the year 2009 to 2010, asset utilization increased slightly from 6.01% to 6.34%, but

then started decreasing in 2011and it fell to 5.16% in 2013. It means the bank’s assets have

not been managed efficiently enough generate more profit failing to allocate resources to the

right assets.

IDLC: For IDLC, every 100 TK asset generated TK 8.43in operating revenue in the year

2009. From year 2009 to 2010, asset utilization increased fairly from 8.43% to 11.31% but

then started to decrease gradually from 2011 and fell to 5.48% in the year 2013. Thus, IDLC

has not been able to maintain stability in its asset utilization failing to allocate its resources to

the appropriate assets.

Cross-sectional analysis: Over the five year period, the asset utilization position was more

or less same for the both Bank Asia and IDLC. In 2010,both experienced an increase in asset

utilization. From the year 2011, both of them began experiencing a gradual decrease in the

ratio till the year 2013. At the end of the five year period, both of them were almost in the

Page | 11

same position in terms of the efficiency in asset management that is they were almost similar

in utilizing their assets.

Tax Management Efficiency

2009 2010 2011 2012 2013Bank Asia 58.05% 53.91% 56.54% 31.7% 39.1%

IDLC 64.54% 67.84% 41.12% 56.93% 50.52%

2009 2010 2011 2012 20130.00%

10.00%

20.00%

30.00%

40.00%

50.00%

60.00%

70.00%

80.00%

Bank AsiaIDLC

Bank Asia: From 2009 to 2010, tax management efficiency for Bank Asia decreased from

58.05% to 53.91% which indicates that the bank is paying huge taxes and it kept on

decreasing to reach at 39.1% in 2013. Overall, from the year 2009 till 2013, it shows a

decreasing trend of the ratio which is actually indicating poor efficiency of the bank

regarding its taxes.

IDLC: From 2009 to 2010, tax management efficiency for IDLC increased from 64.54% to

67.84% which indicates that it managed to reduce its tax. However, in the year 2011 the ratio

decreased significantly to 41.12% indicating its inability to manage tax efficiently resulting in

high taxes in the year 2011. The ratio again increased in the year 2012 to 56.93% but fell

again in the year 2013 to 50.52%. It shows its inability to maintain stability in tax

management efficiency.

Cross-sectional analysis: Both Bank Asia and IDLC have not been able to successfully

manage its tax expense. Both experienced a slight increase in one particular period but it was

only temporary and the ratio kept on declining till the end of 2013.Both are experiencing a

Page | 12

downward trend. However, IDLC has been able to recover and experience improvements in

some periods. Nevertheless, the ratio had declined for both of them.

Expense Control Efficiency

2009 2010 2011 2012 2013Bank Asia 55.36% 53.66% 54.31% 34% 40%

IDLC 66.58% 64.20% 56.33% 52.10% 47.97%

2009 2010 2011 2012 20130.00%

10.00%

20.00%

30.00%

40.00%

50.00%

60.00%

70.00%

Bank AsiaIDLC

Bank Asia: From 2009 to 2010, Bank Asia’s expense control efficiency declined

from55.36% to 53.66%. It means the bank was unable to efficiently control its operating

expenses in year 2010. In 2011, it increased slightly showing some efficiency in controlling

expenses. It declined again in 2012 to 34%. However, it increased again in 2013 reaching

40%. Overall, it recovered and was able to control its operating expenses in the year 2013.

IDLC: From 2009 to 2010, IDLC’s expense control efficiency decreasedfrom 66.58 % to

64.20%. It means it was also unable to efficiently control its operating expenses in the year

2010. IDLC’s expense control efficiency ratio kept on decreasing reaching at 47.97% in the

year 2013. Thus, it failed to manage and reduce its operating expenses efficiently.

Cross-sectional analysis: Overall, both of them failed to manage their operating expenses

and thus experienced decline in their expense control efficiency ratio. However, Bank Asia

was able to recover in some particular periods and manage its operating expenses. On the

Page | 13

other hand, IDLC followed a downward trend starting from 2009 till 2013 failing to manage

its operating expenses efficiently.

Operating Efficiency

2009 2010 2011 2012 2013Bank Asia 36.62% 36.31% 36.53% 36.46% 37.75%

IDLC 25.59% 31.70% 42.29% 44.03% 45.05%

2009 2010 2011 2012 20130.00%

5.00%

10.00%

15.00%

20.00%

25.00%

30.00%

35.00%

40.00%

45.00%

50.00%

Bank AsiaIDLC

Bank Asia: The operating efficiency of Bank Asia decreasedin slightly in the year 2010

showing some efficiency in managing its operating revenues to cover operating expenses. It

increased slightly in 2011 indicating somewhat inefficiency. However, it declined again to

36.46% in 2012 indicating recovery in efficiency. Lastly, in the year 2013 it increased again

to 37.75% showing that Bank Asia has been inefficient in managing its operating expenses in

relation to its generation of operating revenue.

IDLC: The operating efficiency of IDLC has increased over the five year period from

25.59% in 2009 to 45.05% in 2013. IDLC’s operating efficiency ratio shows a downward

trend and it indicates that it has been less efficient in managing its operating expenses in

relation to its operating revenue.

Cross-sectional analysis: The analysis suggests both of them have not been able to manage

their operating expenses efficiently in relation to their operating revenues. However, Bank

Asia has been somewhat efficient in managing its operating expenses in relation to its

operating revenue in some of the periods between the years 2009 and 2013.

Page | 14

Employee Productivity

2009 2010 2011 2012 2013Bank Asia TK.2,217,451 TK.2,893,711 TK.2,600,044 TK.1,760,349 TK.2,128,346

IDLC TK.5,033,256 TK.5,541,730 TK.2,974,578 TK.2,603,301 TK.2,064,176

2009 2010 2011 2012 20130

1,000,000

2,000,000

3,000,000

4,000,000

5,000,000

6,000,000

Bank AsiaIDLC

Bank Asia: The level of employee productivity increased initially in the year 2010. This

indicated that Bank Asia was able to efficiently utilize its human resources in order to

generate operating income. However, it started to decline in the year 2011 and dropped

further in 2012. In 2013, it recovered again and experienced an increase in employee

productivity compared to the year 2012.

IDLC: IDLC’slevel of employee productivity increased in the year 2010 showing its ability

to utilize its human resources efficiently to generate operating income. However, it started to

decline in the year 2011 and continued to decline till the year 2013 to reach TK.2,064,176.

This downward trend indicates that IDLC has not been able to utilize its human resources

efficiently to generate operating income.

Cross-sectional analysis: Overall, IDLC is following a downward trend and has not been

able to manage its human resources efficiently in generating operating income. Bank Asia

also experienced a decline in the two periods but was able to recover. Thus, compared to

IDLC, Bank Asia has been more efficient in managing its human resources to generate

operating income.

Page | 15

PROFITABILITY RATIOS

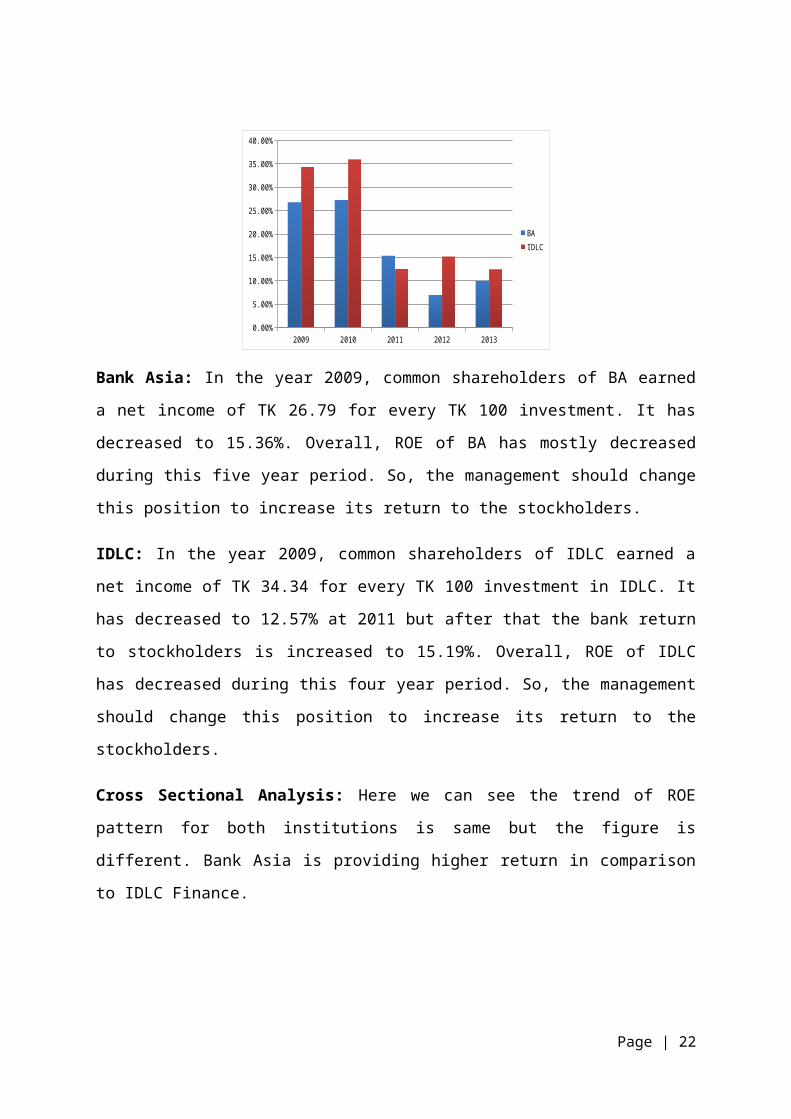

Return on Equity (ROE)

2009 2010 2011 2012 2013Bank Asia 26.79% 27.33% 15.36% 6.96% 9.99%

IDLC 34.34% 35.96% 12.57% 15.19% 12.48%

2009 2010 2011 2012 20130.00%

5.00%

10.00%

15.00%

20.00%

25.00%

30.00%

35.00%

40.00%

BAIDLC

Bank Asia: In the year 2009, common shareholders of BA earned a net income of TK 26.79

for every TK 100 investment. It has decreased to 15.36%. Overall, ROE of BA has mostly

decreased during this five year period. So, the management should change this position to

increase its return to the stockholders.

IDLC: In the year 2009, common shareholders of IDLC earned a net income of TK 34.34 for

every TK 100 investment in IDLC. It has decreased to 12.57% at 2011 but after that the bank

return to stockholders is increased to 15.19%. Overall, ROE of IDLC has decreased during

this four year period. So, the management should change this position to increase its return to

the stockholders.

Cross Sectional Analysis: Here we can see the trend of ROE pattern for both institutions is

same but the figure is different. Bank Asia is providing higher return in comparison to IDLC

Finance.

Page | 16

Return on Asset (ROA)

2009 2010 2011 2012 2013

Bank Asia 1.93% 1.83% 1.63% 0.65% 0.89%

IDLC 3.62% 4.93% 1.61% 1.87% 1.33%

2009 2010 2011 2012 20130.00%

1.00%

2.00%

3.00%

4.00%

5.00%

6.00%

BAIDLC

Bank Asia: In the year 2009, every TK 100 asset earned a net income of TK 1.93 for Bank

Asia. In 2010, it is decreased to 1.83% because relative increase in net income is greater than

relative increase in total assets. It means that managerial efficiency did not improved in 2010.

But in 2011, it decreased to 1.63% and continued till 2013 to 0.89% which means managers

were unsuccessful in increasing the bank’s net income after tax efficiently. Overall, ROA of

BA has decreased during this five year period.

IDLC: In the year 2009, every TK 100 asset earns a net income of TK 3.62 for IDLC

Finance Ltd. In 2010, it is increased to 4.93% because relative increase in net income is

greater than relative increase in total assets. It means that managerial efficiency is improved

in 2010. But in 2011, it decreased to 1.61% and it continued till 2013 and it was 1.33 %which

means managers failed to increase the bank net income after tax efficiently. Overall, ROA of

IDLC has decreased during this five year period.

Cross Sectional Analysis: In ROA, we can see that Bank Asia has less return than IDLC

Finance Ltd. And in 2011, Bank Asia earned more ROA than IDLC though it was declined

from previous two years. Bank Asia earned more return on its total assets.

Page | 17

Net Interest Margin

2009 2010 2011 2012 2013

Bank Asia 2.55% 2.81% 2.29% 2.62% 1.94%

IDLC 3.94% 4.69% 5.06% 4.63% 4.12%

2009 2010 2011 2012 20130.00%

1.00%

2.00%

3.00%

4.00%

5.00%

6.00%

BAIDLC

Bank Asia: From 2009 to 2010, net interest income for Bank Asia (interest income – interest

expense) increases from 2.55% to 2.81% and it continued till 2012 and it was 2.62% because

relative change in interest income is greater than relative increase in interest expense and total

assets. But in 2013 net interest margin decreases to 1.94 % because net interest income

decreased but total interest expense and total assets increased.

IDLC: From 2009 to 2010, net interest margin for IDLC increased from 3.94% to 4.69%

because relative change in net interest income is higher than relative increase in interest

expense and total assets. In 2011, it increased to 5.06% because they could not earn much

from their loan. But again can observe a positive change in NIM in 2013 which is a good sign

for bank.

Cross Sectional Analysis: Though both banks are in the decreasing rate in 2011 compare to

2010, IDLC is in the good position compare to Bank Asia In 2011but competitor bank is

doing well in net interest margin overall . So, in the cross sectional analysis we can see that

Bank Asia is in not in better position than IDLC.

Page | 18

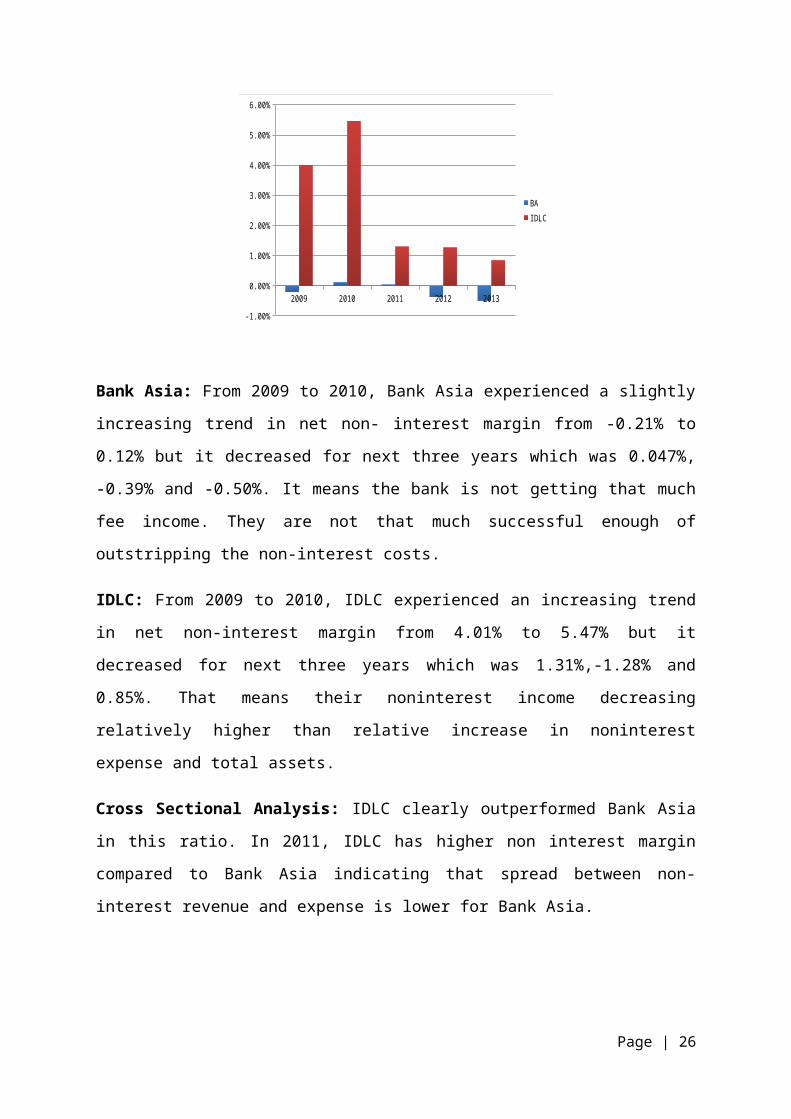

Net Non Interest Margin

2009 2010 2011 2012 2013

Bank Asia -0.21% 0.12% 0.047% -0.39% -0.50%

IDLC 4.01% 5.47% 1.31% 1.28% 0.85%

2009 2010 2011 2012 2013

-1.00%

0.00%

1.00%

2.00%

3.00%

4.00%

5.00%

6.00%

BAIDLC

Bank Asia: From 2009 to 2010, Bank Asia experienced a slightly increasing trend in net

non- interest margin from -0.21% to 0.12% but it decreased for next three years which was

0.047%, -0.39% and -0.50%. It means the bank is not getting that much fee income. They are

not that much successful enough of outstripping the non-interest costs.

IDLC: From 2009 to 2010, IDLC experienced an increasing trend in net non-interest margin

from 4.01% to 5.47% but it decreased for next three years which was 1.31%,-1.28% and

0.85%. That means their noninterest income decreasing relatively higher than relative

increase in noninterest expense and total assets.

Cross Sectional Analysis: IDLC clearly outperformed Bank Asia in this ratio. In 2011,

IDLC has higher non interest margin compared to Bank Asia indicating that spread between

non-interest revenue and expense is lower for Bank Asia.

Page | 19

Net Bank Operating Margin

2009 2010 2011 2012 2013

Bank Asia 2.34% 2.93% 2.34% 2.22% 1.44%

IDLC 6.27% 7.73% 4.00% 3.56% 3.01%

2009 2010 2011 2012 20130.00%

1.00%

2.00%

3.00%

4.00%

5.00%

6.00%

7.00%

8.00%

9.00%

BAIDLC

Bank Asia: From 2009 to 2010, net operating margin for Bank Asia increased from 2.34% to

2.93% but then decreased slowly to 2.22% in 2012 and continued till 2013 and it was 1.44%.

This tells us that in the relative spread in operating revenue and operating expense decreased

by a larger amount than relative decrease in total assets so there is lack of operating revenue

to cover the operating cost compare to 2009 & 2010.

IDLC: From 2009 to 2010, net operating margin for IDLC increased from 6.27% to 7.73%

but then decreases to 3.56% in 2012 and continued this downward trend till 2013 which was

3.01%. This tells us that in 2012 & 2013 the relative spread in operating revenue and

operating expense decreased by a larger amount than relative decrease in total assets so there

is lack of operating revenue to cover the operating cost compare to previous two years 2010

and 2009.

Cross Sectional Analysis: In 2013, operating margin decreased for both banks but over 5

years and also in 2010IDLC has higher operating margin indicating that it is more profitable.

Page | 20

Earnings Per Share (EPS)

2009 2010 2011 2012 2013

Bank Asia 6.19 6.43 3.65 1.44 2.10

IDLC 13.70 13.41 5.05 4.43 4.16

2009 2010 2011 2012 20130

2

4

6

8

10

12

14

16

BA

Bank Asia: There is a significant decrease in EPS over the last five years. It came down from

Tk. 6.19 in 2009 to Tk. 2.10 in 2013. The outcome can be explained by the huge increase in

the total number of common stock outstanding over the years. An EPS of Tk. 2.10 suggests

that BA has earned Tk. 2.10 for every unit of common stock

IDLC: There is a significant decrease in EPS over the last five years. It came down from Tk.

13.7 in 2009 to Tk. 4.16 in 2013. The outcome is such due do the huge increase in the total

number of common stock outstanding as when compared to that of 2009. An EPS of Tk. 4.16

suggests that IDLC has earned Tk. 4.16 for every unit of common stock.

.Cross Sectional Analysis: Although both financial institutions show a decreasing trend in

their values of EPS, the above data suggests that overall BA has a lower EPS than that of

IDLC. This indicates that BA is earning lower income for each unit of share against IDLC.

Dividend Per Share (DPS)

Page | 21

2009 2010 2011 2012 2013

Bank Asia 4 4 2 1 1

IDLC 5.5 6.06 2.5 2.31 3

2009 2010 2011 2012 20130

1

2

3

4

5

6

7

BAIDLC

Bank Asia: There is a significant decrease in DPS over the last five years. It came down

from Tk4 in 2009 to Tk1 in 2013. This can be explained by the huge increase in the total

number of common stock outstanding when compared to that of 2009. The dividend is

distributed among greater number of stockholders so the DPS is less. A DPS of Tk. 1 in 2013

suggests that BA has provided dividend of Tk. 1 for every unit of common stock the

shareholders hold which indicates that they are receiving a lot lower return.

IDLC: There is a marginal decrease in DPS over the last five years. It came down from Tk.

5.5 in 2009 to Tk. 3 in 2013. This can be explained by the huge increase in the total number

of common stock outstanding when compared to that of 2009. A DPS of Tk. 3 in 2013

suggests that IDLC has provided dividend of Tk. 3 for every unit of common stock the

shareholders hold which indicates that they are receiving a lot lower return relative to earlier

periods.

Cross Sectional Analysis: Although both institutions show a decreasing trend in their values

of DPS, the above data suggests that overall BA is providing a lower return in the form of

dividend. Over the last two years, IDLC has been providing almost twice as much DPS than

that of BA which is a very good signal by IDLC to attract investors to purchase its shares.

Dividend Payout Ratio

Page | 22

2009 2010 2011 2012 2013

Bank Asia 64.65% 62.25% 54.85% 69.45% 47.51%

IDLC 40.13% 45.21% 49.47% 52.08% 72.09%

2009 2010 2011 2012 20130.00%

10.00%

20.00%

30.00%

40.00%

50.00%

60.00%

70.00%

80.00%

BAIDLC

Bank Asia: From 2009 to 2013 a fluctuation is visible in dividend payout ratio from 64.65%

to 47.51%. But 2012, Bank Asia’s dividend payout shows a huge increase to 69.45% showing

that it pays investor with more dividends than before in 2012. But in 2013 it became 47.51%.

That means investors did not get higher dividend as given earlier.

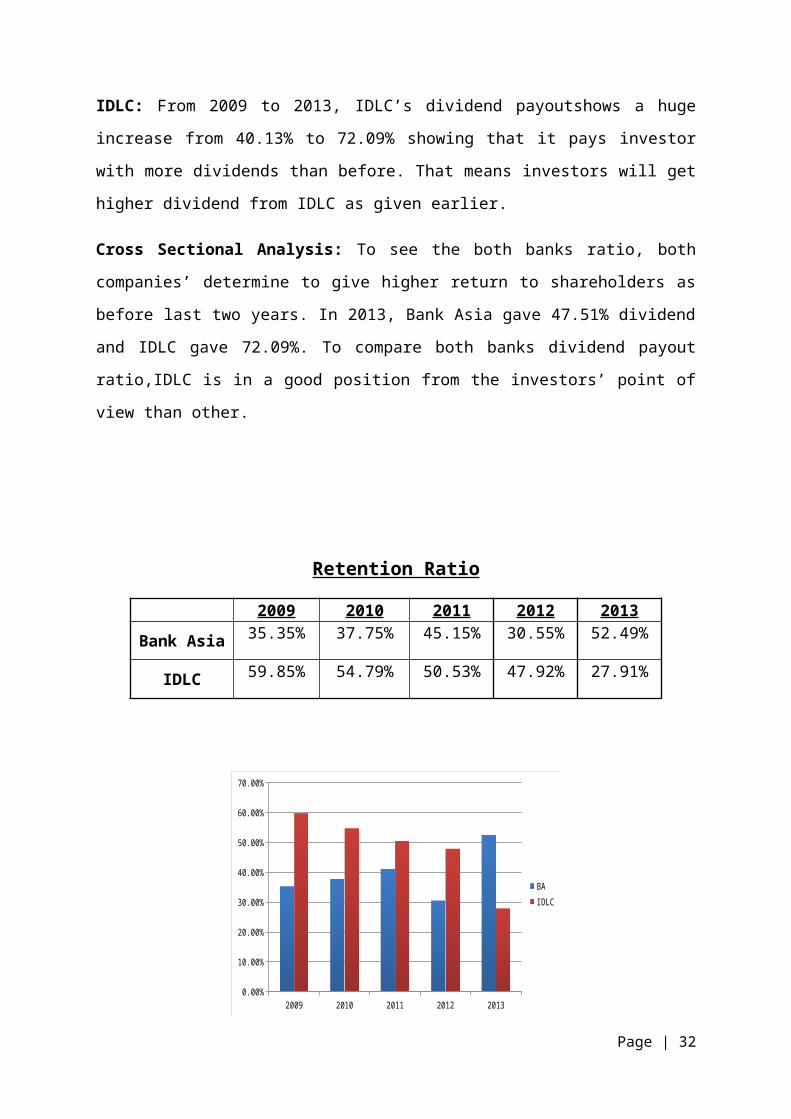

IDLC: From 2009 to 2013, IDLC’s dividend payoutshows a huge increase from 40.13% to

72.09% showing that it pays investor with more dividends than before. That means investors

will get higher dividend from IDLC as given earlier.

Cross Sectional Analysis: To see the both banks ratio, both companies’ determine to give

higher return to shareholders as before last two years. In 2013, Bank Asia gave 47.51%

dividend and IDLC gave 72.09%. To compare both banks dividend payout ratio,IDLC is in a

good position from the investors’ point of view than other.

Retention Ratio

2009 2010 2011 2012 2013

Page | 23

Bank Asia 35.35% 37.75% 45.15% 30.55% 52.49%

IDLC 59.85% 54.79% 50.53% 47.92% 27.91%

2009 2010 2011 2012 20130.00%

10.00%

20.00%

30.00%

40.00%

50.00%

60.00%

70.00%

BAIDLC

Bank Asia: In 2013, Bank has huge amount in the retained earnings. In 2010, the bank

reduced its retention rate and increase dividend. And in 2012 they decreased their retention

rate again and it was more or less stable in 2011. Overall, from bank perspective retention

rate is increased which is good for bank. But from the shareholders perspective reduced rate

of retention is good.

IDLC: In 2009 & 2010 IDLC has huge amount in the retained earnings. In 2012&

2013,IDLC reduced its retention rate and increase dividend. Overall, from the company’s

perspective retention rate is decreased which is not good for bank. But in shareholders

perspective reduced rate of retention is good.

Cross Sectional Analysis: Overall, both banks actually reduced their retention rate

bychanging their policies over the period depending on their financial conditions.

Dividend Yield Ratio

2009 2010 2011 2012 2013

Page | 24

Bank Asia 9.37% 4.66% 5.24% 4.65% 4.35%

IDLC 1.49% 4.14% 1.83% 2.51% 4.77%

2009 2010 2011 2012 20130.00%

1.00%

2.00%

3.00%

4.00%

5.00%

6.00%

7.00%

8.00%

9.00%

10.00%

BAIDLC

Bank Asia: From 2009 to 2010, Bank Asia’s Dividend yield decreases from 9.37% to 4.66%

and then it increased at a marginal rate to 5.24% in 2011. In general, the dividend yield of BA

has fluctuated during the last five years.

IDLC: From 2009 to 2010, IDLC’s dividend yield increases from 1.49% to 4.14% and then it

decreased to 1.83% in 2011 and increased to 4.77% in 2013. After 2010, the dividend yield of

IDLC is following an upward trend.

Cross Sectional Analysis: Both the bank got a downward slope in 2010. But after that they

are trying to increase ratio again. With respect to 2013,IDLC is in a better position.

Net Profit Margin

2009 2010 2011 2012 2013

Page | 25

Bank Asia 17.43% 17.65% 14.39% 5.86% 8.77%

IDLC 42.97% 43.56% 23.16% 29.66% 24.23%

2009 2010 2011 2012 20130.00%

5.00%

10.00%

15.00%

20.00%

25.00%

30.00%

35.00%

40.00%

45.00%

50.00%

BAIDLC

Bank Asia: In the year 2009, out of every TK 100 operating revenues, Bank Asia earns a

profit of TK 17.43. From 2009 to 2010, net profit margin for BankAsia increased slightly

from 17.43% to 17.65%. It means compare to 2009 in 2010 bank is efficiently managed their

operating expenses and tax. But in 2012 NPM went down to 5.86% which means they fail to

manage efficiently operating expenses and tax compare to 2010 and it increased slightly in

2013 to 8.77%.

IDLC:For IDLC from 2009 to 2010, net profit margin increased slightly from 42.97% to

43.56% because relative increase in net profit was more than relative increase in operating

revenue. It means they are successful to manage their operating expense and tax efficiently.

But in 2011, NPM goes down to 23.16% which means they fail to manage their operating

expenses and tax efficiently compare to 2010 and this fall continued in 2013 and NPM

became 24.23%.

Cross Sectional Analysis:From 2009 to 2010 both companies increased their NPM but

IDLC made higher NPM. Form 2010 and 2011, net profit margin for both banks decreased.

From 2011 to 2013, NPM for both companies reduced but Bank Asia had faced a good

portion of reduction.

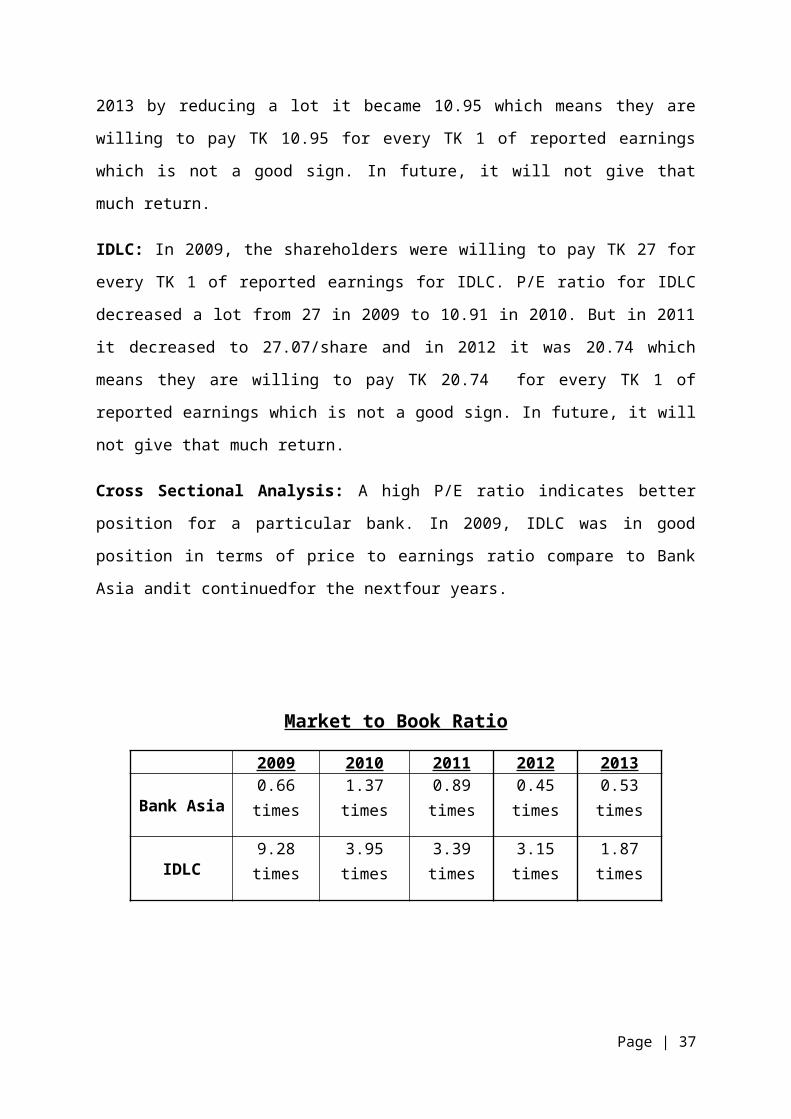

MARKET POSITION

Price Earnings Ratio

Page | 26

2009 2010 2011 2012 2013

Bank Asia 6.89 times 13.34times 10.47 times 14.93 times 10.95 times

IDLC 27 times 10.91 times 27.07 times 20.74 times 8.1 times

2009 2010 2011 2012 20130

5

10

15

20

25

30

BAIDLC

Bank Asia: In 2009, the shareholders were willing to pay TK 6.89 for every TK 1 of reported

earnings for Bank Asia. P/E ratio for Bank Asia increased gradually from 6.89 in 2009 to

10.47 in 2011. But in 2012 it increased to 14.93/share and in 2013 by reducing a lot it became

10.95 which means they are willing to pay TK 10.95 for every TK 1 of reported earnings

which is not a good sign. In future, it will not give that much return.

IDLC: In 2009, the shareholders were willing to pay TK 27 for every TK 1 of reported

earnings for IDLC. P/E ratio for IDLC decreased a lot from 27 in 2009 to 10.91 in 2010. But

in 2011 it decreased to 27.07/share and in 2012 it was 20.74 which means they are willing to

pay TK 20.74 for every TK 1 of reported earnings which is not a good sign. In future, it will

not give that much return.

Cross Sectional Analysis: A high P/E ratio indicates better position for a particular bank. In

2009, IDLC was in good position in terms of price to earnings ratio compare to Bank Asia

andit continuedfor the nextfour years.

Market to Book Ratio

2009 2010 2011 2012 2013

Bank Asia 0.66 times 1.37 times 0.89 times 0.45 times 0.53 times

Page | 27

IDLC 9.28 times 3.95 times 3.39 times 3.15 times 1.87 times

2009 2010 2011 2012 20130

1

2

3

4

5

6

7

8

9

10

BAIDLC

Bank Asia: From 2009 to 2010, market to book value ratio for Bank Asia decreased

gradually from 0.66/share to 1.37/share. Then in the year 2011, market to book ratio

decreased steadily to 0.89/share and it continued till 2013 to 0.53/share. This is because

market price per share decreases and book value per share increases for which market to book

ratio reduced in 2011 and 2012. It means the share more than its book value that is good but

compare to previous years it is not good though it is overpriced.

IDLC: From 2009 to 2010, market to book value ratio for IDLC decreased rapidly from

9.28/share to 3.95/share. Then in the year 2011, market to book ratio decreased steadily to

3.39/share and 2012 it became 3.15/share and finally in 2013 it came down to 1.87. This is

because market price per share decreases and book value per share increases for which

market to book ratio reduced in 2011 and 2012. It means the share more than its book value

that is good but compare to previous years it is not good though it is overpriced.

Cross Sectional Analysis: The overall position shows that the performance of IDLC is far

better than Bank Asia since investors value IDLC more than its book value.

LIQUIDITY RATIOS

Cash Position Indicator

Page | 28

2009 2010 2011 2012 2013

Bank Asia7.47% 6.61% 7.36% 7.49% 6.76%

IDLC 5.27% 11.05% 8.44% 10.03% 15.19%

2009 2010 2011 2012 20130.00%

2.00%

4.00%

6.00%

8.00%

10.00%

12.00%

14.00%

16.00%

Bank AsiaIDLC Finance

Bank Asia: This ratio indicates the ability of the bank or institution to handle immediate cash

needs. From 2009 to 2012, we can see that cash position indicator for Bank Asia is

fluctuating every year. It simply indicates that bank tries to increase their first line of defense

so that they can fulfill depositors’ withdrawals and customers’ loan demands.

IDLC: From 2009 to 2010 IDLC cash position indicator increases from 5.27% to 15.19%

which means they are strengthening their first line ofdefense to protect them from immediate

cash needs. In 2013 they have highest of their cash position indicator and it was 15.19% that

means it is in greater portion of cash implies the bank is in a stronger position to meet

immediate cash needs.

Cross Sectional Analysis: To see four years, both banks are close to each other in cash

position indicator but IDLC always went through a gradual improvement but, on the other

hand, Bank Asia went through fluctuations.

Capacity Ratio

2009 2010 2011 2012 201373.20% 75.57% 70.34% 65.77% 64.05%

Page | 29

Bank Asia

IDLC90.60% 83.79% 86.52% 86.54% 79.69%

2009 2010 2011 2012 20130.00%

10.00%

20.00%

30.00%

40.00%

50.00%

60.00%

70.00%

80.00%

90.00%

100.00%

Bank AsiaIDLC

Bank Asia: The capacity ratio shows a decreasing trend throughout the year 2009 and 2013

which is a positive signal for Bank Asia as loan is the least liquid asset for a bank. Lower

capacity ratio means liquidity for the bank is going up.

IDLC: IDLC has also a decrease trend in 5-year period from 2009 to 2013 where the

capacity ratio shows a decreasing trend from 90% to 79%, which is a positive signal as loan

is the least liquid asset for a bank. Lower capacity ratio means liquidity for the bank is going

up.

Cross Sectional Analysis: Overall, the capacity ratio of IDLC is larger than that of Bank

Asia which is an indicator of poor liquidity condition for IDLC.

Liquid Securities Indicator

2009 2010 2011 2012 2013

Bank Asia 1.48% 1.11% 1.09% 1.38% 1.86%

Page | 30

IDLC 2.81% 2.14% 1.76% 1.02% 1.56%

2009 2010 2011 2012 20130.00%

0.50%

1.00%

1.50%

2.00%

2.50%

3.00%

BAIDLC

Bank Asia: This shows that from 2009 to 2011, liquidity securities indicators of Bank Asia

were more or less similar and it was around 1%. But in 2013, it increases to 1.86% which is

highest in all five years. That means bank is trying to increase its second line of defense and

also try to get a little bit interest from that securities.

IDLC: This shows that from 2009 to 2010, liquidity securities indicators of IDLC decreases

2.81% to 2.14% which means it reduces its government securities or it is not buying that

much security out of its total assets. And in 2011 it decreases to 1.76% and 1.02% in 2012

which indicates the greater portion of government securities and it also indicates the more

liquid the bank position tends to be.

Cross Sectional Analysis: Here, both institutions have government securities in its total

assets. They actually want to earn some interest and also want to fulfill liquidity requirement.

In 2013, Bank Asia has 1.86% liquid securities and IDLC has 1.56% liquid securities. That

means Bank Asia, in comparison, has a higher second line of defense against customer

demands and withdrawals.

Core Deposit Ratio

2009 2010 2011 2012 2013

Bank Asia 6.76% 6.24% 8.1% 7.44% 7.27%

IDLC 17.19% 20.73% 15.98% 15.24% 11.99%

Page | 31

2009 2010 2011 2012 20130.00%

5.00%

10.00%

15.00%

20.00%

25.00%

BAIDLC

Bank Asia: The core deposit ratio has gone up during the last five years which suggests that

the relative change in core deposits was greater than the relative change in total deposits. An

increase in this ratio indicates that the liquidity requirement of Bank Asia is going down over

the years.

IDLC: The core deposit ratio of IDLC has gone down during 2012 and 2013 which suggests

that the relative change in core deposits was smaller than the relative change in total deposits.

A decrease in this ratio indicates that the liquidity requirement of IDLC is going up.

Cross Sectional Analysis: In general, the core deposit ratio of IDLC is much higher than

that of BA. This suggests that the liquidity requirement of BA is lower than IDLC because it

will have enough cash to meet fulfill its obligations.

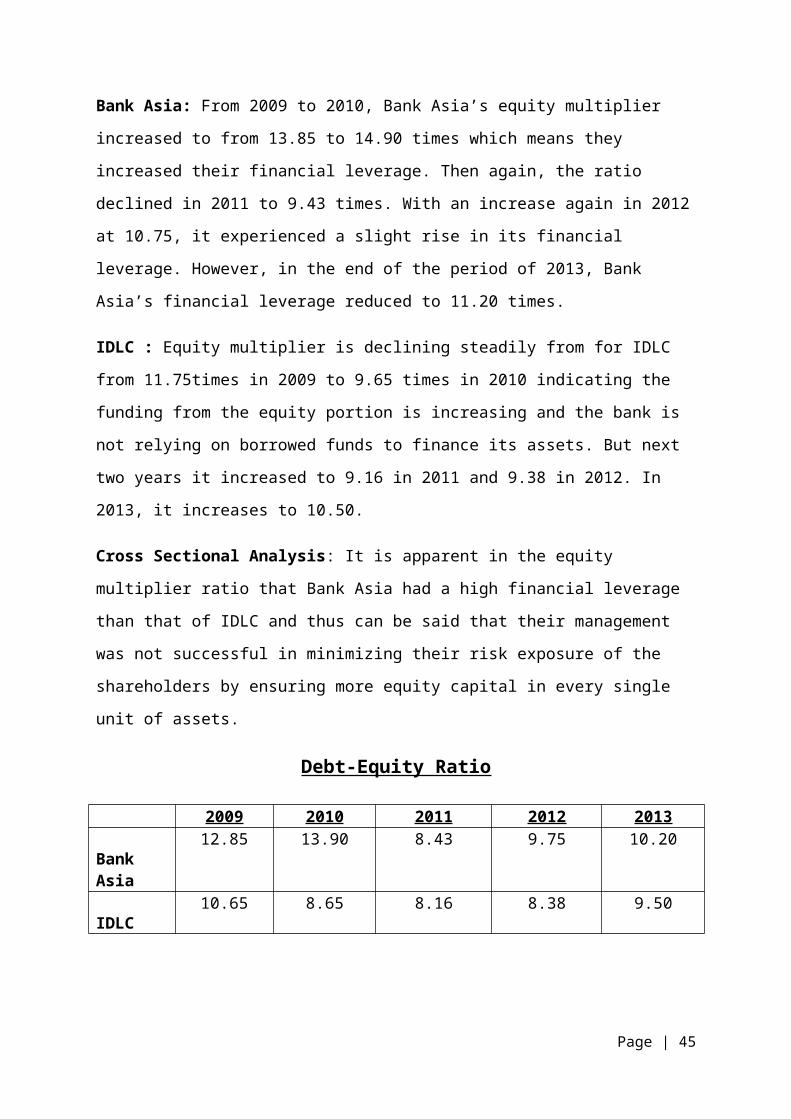

FINANCIAL RISK

Equity Multiplier

Page | 32

2009 2010 2011 2012 2013

Bank Asia13.85 14.90 9.43 10.75 11.20

IDLC11.65 9.65 9.16 9.38 10.50

2009 2010 2011 2012 20130

2

4

6

8

10

12

14

16

Bank AsiaIDLC

Bank Asia: From 2009 to 2010, Bank Asia’s equity multiplier increased to from 13.85 to

14.90 times which means they increased their financial leverage. Then again, the ratio

declined in 2011 to 9.43 times. With an increase again in 2012 at 10.75, it experienced a

slight rise in its financial leverage. However, in the end of the period of 2013, Bank Asia’s

financial leverage reduced to 11.20 times.

IDLC : Equity multiplier is declining steadily from for IDLC from 11.75times in 2009 to

9.65 times in 2010 indicating the funding from the equity portion is increasing and the bank

is not relying on borrowed funds to finance its assets. But next two years it increased to 9.16

in 2011 and 9.38 in 2012. In 2013, it increases to 10.50.

Cross Sectional Analysis: It is apparent in the equity multiplier ratio that Bank Asia had a

high financial leverage than that of IDLC and thus can be said that their management was not

successful in minimizing their risk exposure of the shareholders by ensuring more equity

capital in every single unit of assets.

Debt-Equity Ratio

2009 2010 2011 2012 201312.85 13.90 8.43 9.75 10.20

Page | 33

Bank Asia

IDLC10.65 8.65 8.16 8.38 9.50

2009 2010 2011 2012 20130

2

4

6

8

10

12

14

16

Bank AsiaIDLC

Bank Asia: From the year of 2009 to 2010, there was slight increase in the debt to equity

ratio of Bank Asia. In 2009, debt to equity ratio of Bank Asia was 12.85 times which

increased to 13.90 times. Very next year it reduced to 8.43 times and the following it

increased to 9.75 times. It also increased in 2013 to 10.20. It can be said that over the period

it was more or less stable.

IDLC: The debt to equity capital ratio of the IDLC Finance is in a lower pattern from year

2009 to 2011. In 2009, it was 10.65 times but it reduced to 8.16 times in 2011 because of

relative increases in debt lower than its relative increase in equity. But next two years it

gradually increased to 8.38 times in 2012 and 9.50 times in 2013.

Cross Sectional Analysis: Bank Asia debt to equity ratio is higher than that of IDLC Finance

Limited. This tells us that the cost of equity and risk is higher for Bank Asia. So from the risk

perspective IDLC is in a better position.

Interest Coverage Ratio

2009 2010 2011 2012 2013

Bank Asia0.29 times 0.35 times 0.23 times 0.09 times 0.13 times

IDLC0.28 times 0.44 times 0.34 times 0.19 times 0.19 times

Page | 34

2009 2010 2011 2012 20130

0.05

0.1

0.15

0.2

0.25

0.3

0.35

0.4

0.45

0.5

Bank AsiaIDLC

Bank Asia: With the highest ratio in 2010 of0.35 times, the interest coverage ratio of Bank

Asia has overall decreased over this five year period. The jump in 2010 can be explained by

the fact that the relative increase in net profit was larger than the relative increase in interest

expense. A value of 0.13 times indicates that in 2013 the bank has earned a net income which

could cover its interest expense 0.13 times.

IDLC: The interest coverage ratio of IDLC has, overall, decreased over this five year period.

The jump in 2010 can be explained by the fact that the relative increase in net profit was

larger than the relative increase in interest expense. A value of 0.19 times indicates that in

2012 and in 2013 the bank has earned a net income which could cover its interest expense

0.19 times for two years.

Cross Sectional Analysis: Overall IDLC has a higher interest coverage ratio than that of

Bank Asia and the difference is quite prominent. This means that IDLC is more successful in

generating net income to cover the interest expense and is utilizing its resources more

efficiently in covering the interest expenses.

Investors’ View Point

Valuation using Gordon Growth Model:

2009 2010 2011 2012 2013 AverageBank Asia:ROE 1.93% 1.83% 1.63% 0.65% 0.89% 1.39%Retention ratio

35.35% 37.75% 45.15% 30.55% 52.49% 40.26%

Page | 35

IDLC:ROE 3.62% 4.93% 1.61% 1.87% 1.33% 2.67%Retention ratio

59.85% 54.79% 50.53% 47.92% 27.91% 48.2%

Growth Rate (ROE X Retention Ratio)Bank Asia 0.0139 X 0.4026 0.56%IDLC 0.0267 X 0.482 1.29%

Required rate of return:

K = Kf+(Km-Kf)* ß

where - Kf: Risk free rate of Return

Km: Market Return

ß: Beta

Bank Asia Ltd:

The Beta of the stock was found to be 0.74, which implies that for every 1% increase(or

decrease) in Index returns, the returns of Bank Asia Ltd would increase(or decrease) by

0.74%.

-10.00% -5.00% 0.00% 5.00% 10.00% 15.00%

-10.00%

-5.00%

0.00%

5.00%

10.00%

15.00%

f(x) = 0.743615984544353 x − 0.00902945586453816

Market Index

Bank

Asi

a Re

turn

Market return

The monthly average market return is computed to be 0.84%.

Risk Free Rate of Return

Page | 36

According to Bangladesh Bank, the yield of one year Treasury bill is considered to be the

annualized risk free rate of return, which is equal to 10.52%. Therefore, the monthly risk free

return would be 0.88% (10.52/12)

Required rate of return for Bank Asia Ltd:

K = Kf + (Km-Kf) * ß

K = 0.88 + (0.84 -0.88)*0.74

K = 0.91% (monthly)/ 10.92% (annual)

IDLC:

The Beta of the stock was found to be 1.43, which implies that for every 1% increase(or

decrease) in Index returns, the returns of IDLC would increase (or decrease) by 1.43%.

-10.00% -5.00% 0.00% 5.00% 10.00% 15.00%

-40.00%

-30.00%

-20.00%

-10.00%

0.00%

10.00%

20.00%

30.00%

40.00%

f(x) = 1.43524118116374 x − 0.0180745368089185

Market index

IDLC

Ret

urns

Required rate of return for IDLC:

K = Kf + (Km-Kf) * ß

K = 0.88 + (0.84 -0.88)*1.43

K = 0.94% (monthly)/11.28% (annual)

Intrinsic value:

BANK ASIA IDLCCurrent dividend 0.9091 3.00Growth 0.56% 1.29%Next year’s dividend 0.9142 3.0387Required rate of return/Cost of borrowing

10.92% 11.28%

Page | 37

Intrinsic value 8.82 30.42Market value 23.00 62.90

P0 (intrinsic value) = Current dividend(1+g)K−g

After calculating the intrinsic value, both Bank Asia and IDLC seems to be overpriced.

Capital Adequacy Ratio (CAR):

2009 2010 2011 2012 2013 Required(Bangladesh Bank)Bank Asia

12.27% 8.11% 14.88% 13.05% 11.05% 10%

IDLC - - 13.61% 13.88% 15.43% 10%

Currently Bangladesh Bank prescribed Minimum Capital Adequacy Ratio (CAR) is 10%,

whereas as on December 2013 the Capital Adequacy Ratio (CAR) was 11.05%, above the

minimum level. For IDLC, total Risk Weighted Assets (RWA) of the Company is determined

by multiplying the capital charge formarket risk and operational risk by the reciprocal of the

minimum capital adequacy ratio i.e. 10% and adding the resulting figuresto the sum of risk

weighted assets for credit risk. At the end of 2013, IDLC had a Capital Adequacy Ratio

(CAR) of 15.43%, well above the minimum requirement set by Bangladesh Bank. In

comparison, IDLC has been able to maintain better capital adequacy over Bank Asia.

Investors valuation based on Price-Earnings (P/E) ratio:

2009 2010 2011 2012 2013

Bank Asia 6.89 times 13.34times 10.47 times 14.93 times 10.95 times

IDLC 27 times 10.91 times 27.07 times 20.74 times 8.1 times

Among the most common and reliable tools many investors use to decide where to invest

their money is the price to earnings ratio (P/E ratio), also commonly referred to as the price

Page | 38

multiple, earnings multiple, or simply, multiple.Price (market value) is the cost of buying one

share of the company’s common stock. The price is set by investors based on such factors as

their expectations for the company’s future growth, the state of the industry it belongs to,

inflation and the overall market. Actions the company takescan have a positive or negative

effect on price, depending on how such actions are perceived by the market.

By relating share prices to actual profits, the P/E ratio highlights the connection between the

price and recent company performance. If prices get higher and profits get higher, the ratio

stays the same. The ratio only moves as price and profits become disconnected. Both Bank

Asia and IDLC have high price-earnings (P/E) ratio. For Bank Asia, the P/E ratio has

increased from 6.89 to 10.95. Theoretically, a stock's P/E indicates how much investors are

willing to pay per Taka of earnings. For this reason it's also called the "multiple" of a stock.

In other words, a P/E ratio of about 11 of Bank Asia suggests that investors in the stock are

willing to pay about TK. 11 for every TK. 1 of earnings that the bank generates.The P/E ratio

measures the level of confidence investors have in a company. A higher P/E ratio in this

casemeans that the market is more willing to pay for the earnings of the Bank Asia. Higher

price to earnings ratio indicates that the market has high hopes for the future of the stock and

therefore it has bid up the price.

On the other hand, IDLC’s P/E ratio is positive, but it has decreased over the past five year

period. Compared to Bank Asia, in the end of the year of 2013 IDLC has a lower P/E ratio.

The market may not have enough confidence in the future of the stock of IDLC and thus the

P/E may have declined over time. Nevertheless, its P/E ratio is still positive. It is normally

assumed that a low P/E ratio indicates a company is undervalued. It is not always right as this

may be due to the stock market assumes that the company is headed over several issues or the

company itself has warned a low earnings than expected.In other words, there is no strict rule

of thumb when it comes to interpreting the exact relationship between a P/E ratio and the

company’s true value as an investment. Thus, a low P/E ratio might be interpreted as either

the market giving the bank a vote of no confidence or, alternatively, that the bank is

undervalued and therefore a good bargain.

Investors valuation based on Market-to-Book ratio:

2009 2010 2011 2012 2013Bank Asia 0.66 times 1.37 times 0.89 times 0.45 times 0.53 times

Page | 39

IDLC 9.28 times 3.95 times 3.39 times 3.15 times 1.87 times

Investors can also evaluate a company based on the market-to-book ratio. Market-to-book

ratio is a way of measuring the relative value of a company compared to its stock price or

market value. It is an essential figure to potential investors and analysts because it provides a

simple way of judging whether a company is under or overvalued. It offers a more tangible

measure of a company's value than earnings do and hence it is evaluated by most

conservative investors. Book value simply implies the value of the company on its books,

often referred to as accounting value. It's the accounting value once assets and liabilities have

been accounted for by a company's auditors. Whether book value is an accurate assessment of

a company's value is determined by stock market investors who buy and sell the stock.

Market value has a more meaningful implication in the sense that it is the price investors have

to pay to own a part of the business regardless of what book value is stated.

For Bank Asia, the market-to-book ratio is 0.53 indicating that its book value is greater than

the market value. This is suggesting the investors that the bank’s assets may be undervalued

by 47%. Like the price-to-earnings ratio, the lower the market-to-book ratio, the better the

value. Investors would use a low market-to-book to identify potential new investments. A

low market-to-book ratio could suggest a company’s assets are undervalued, or that the

company’s prospects are good and earnings/value should grow. The market values Bank Asia

less than its stated value or net worth. In one sense, it may be because the market has lost

confidence in the ability of the company's assets to generate future profits and cash flows.

Value investors often like to seek out companies in such a position in hopes that the market

perception turns out to be incorrect.

IDLC has a market-to-book ratio of 1.87 in the end of the period of the year 2013. Thus, its

market value is perceived to be higher than its book value. The market assigns a higher value

to IDLC due to the earnings power of its assets. Nearly all consistently profitable companies

will have market values greater than book values. A market-to-book ratio of more than one is

suggesting that the market’s perception is positive towards IDLC and that the market values

IDLC more than its book value. Thus, generally higher ratios are preferred.

Investors valuation based on financial leverage:

Page | 40

2009 2010 2011 2012 2013

Bank Asia13.85 14.90 9.43 10.75 11.20

IDLC11.65 9.65 9.16 9.38 10.50

The equity multiplier is a method of evaluating a company’s ability to use its debt for

financing its assets. The equity multiplier is also referred to as the leverage ratio or the

financial leverage ratio. The higher the equity multiplier, the higher is the financial leverage,

which indicates that the company relies more on debt to finance its assets. It is apparent in the

equity multiplier ratio that Bank Asia had a high financial leverage than that of IDLC and

thus can be said that their management was not successful in minimizing their risk exposure

of the shareholders by ensuring more equity capital in every 1tk worth of assets. The equity

multiplier gives investors an insight into what financing methods a company may be able to

use to finance the purchase of new assets. It's also an indicator of potential threats a company

may face from economic conditions that affect the debt-equity mix.

From the perspective of the investors, IDLC will be considered less risky since has a lower

equity multiplier meaning that, compared to Bank Asia, it is making less use of borrowed

funds to finance its assets. Thus, higher the financial leverage, investors will perceive the

bank as more risky.

CAMELS RATING:

CAMELS rating is used by the Bangladesh Bank as a tool for evaluating the strength and

performance of banks and non-bank financial institutions. The composite rating adjudged by

theBangladesh Bank signifies satisfactory performance of IDLC i.e. it has a B grade. Bank

Asia also has been given a B grade, signifying that it also has an overall satisfactory

performance.

Recommendations

Several recommendations can be made after analyzing the performance of both Bank Asia

and IDLC Finance Limited by assessing all the ratios. Firstly, it must be noted that both Bank

Asia and IDLC Finance Limited are assigned satisfactory (or B grade) performance according

to the CAMELS rating.

Page | 41

Both Bank Asia and IDLC Finance Limited failed to manage their operating expenses and

thus experienced decline in their expense control efficiency ratio. Even though in the end of

the five year period in 2013 IDLC had a better position in terms of expense control

efficiency, both of them struggled to maintain the ratio and failed to manage and reduce their

operating expenses efficiently.Due to these unmanageable expenses, costs are rising up and

net income is going down. They both need to concentrate harder in handling their expenses

more carefully and improve their net income. Consequently, more income will result in more

dividends and retained earnings for them. This will eventually boost investors’ confidence.

Secondly, in terms of employee productivity, both of them experienced negative results in the

year 2013 compared to 2009. Overall, both are following a downward trend and have not

been able to manage human resources efficiently in generating operating income. Both Bank

Asia and IDLC need to consider this problem and implement ways in order to improve

productivity, perhaps through providing improved incentives. More importantly, both Bank

Asia and IDLC have not been able to successfully manage their tax expense. They need to

implement appropriate tax management tools, such as tax swapping tool or portfolio shifting

tool, to enhance their incomes by efficiently controlling taxes.

IDLC uses its limited fund very aggressively and efficiently as a result its net profit margin is

higher than Bank Asia’s. IDLC has higher operating margin indicating that it is more

profitable. In addition, IDLC is paying out more dividends to its shareholders than what Bank

Asia is. Investors in general require more dividends. Thus, Bank Asia needs to give out more

dividends in order to keep its shareholders satisfied because dividends can be a motivational

factor and encourage shareholders to invest in Bank Asia. Bank Asia also needs to strive to

achieve lower financial leverage by making use of more equity to finance its assets since at

present it is making use of more and more borrowed funds for this purpose.

In terms of the market position, Bank Asia has been able to achieve higher price earnings

relative to IDLC Finance Limited. IDLC over the five year period has been experiencing a

downward trend in price earnings. They need to find out ways to improve investors’

confidence and make them believe that their shares have high future potentials. Generally,

investors consider that a bank with lower price earnings is undervalued and therefore a good

bargain.

Page | 42

Conclusion

Overall, the performance analysis of Bank Asia Limited with the non-bank IDLC Finance

Limited shows both have more or less satisfactory level of performance, which is also

indicated by the CAMELS rating. As a whole, according to the findings, it is indicating that

Page | 43

both Bank Asia and IDLC Finance Limited are following close trends in many of the aspects

of the complete analysis. However, from some of the aspects, such as the levels of

profitability, IDLC Finance Limited is outperforming Bank Asia.

Furthermore, in terms of the financial position, IDLC Finance Limited is in a better position

since it comprises of less financial leverage risk, as indicated by the equity multiplier and

debt-equity ratio, relative to Bank Asia. In addition, the investors’ perception is positive

regarding IDLC Finance Limited, as indicated by the market-to-book ratio, as they value it

more than its overall book value.

All in all, it can be concluded that IDLC Finance Limited is in a better financial position and

has been more profitable as a whole. Perhaps, it has more potential to maximize stockholders’

wealth in the future. Even though Bank Asia has also been experiencing improved

performances in various aspects, investors would rather choose IDLC Finance Limited as it is

providing higher return in the form of dividends and it also has been in a better financial

position.

Bibliography

1. Bank Asia website- http://www.bankasia-bd.com/

2. IDLC website- http://www.idlc.com/

Page | 44

3. Bank Management & Financial Services, Eighth edition, by Peter S. Rose and Sylvia

C. Hudgins.

4. Bangladesh Bank website- http://www.bb.org.bd/monetaryactivity/treasury.php

Page | 45

APPENDIX

Effic iency Ratios:

BANK ASIA - 2013

Ratio Formula Calculation

Page | 46

Asset Utilization

Total Operating Revenues/Total Assets

8,515,429,452/165,067,196,178 5.16%

Tax Management Efficiency

Net Income after tax/Net Income before tax

1,330,538,402/3,405,355,188 39.1%

Expense Control Efficiency

Net Income before tax/Total Operating Revenues

3,405,355,188/8,515,429,452 40%

.Operating Efficiency

Total Operating Expense/Total Operating revenue

3,214,731,899/8,515,429,452 37.75%

Employee

productivity ratio

Net operating income / total no. of full-time employees

3,405,355,188 /1600 TK.2,128,346

BANK ASIA - 2012

Ratio Formula Calculation

Asset Utilization

Total Operating Revenues/Total Assets

7,884,761,090/141,235,371,839 5.58%

Tax Management Efficiency

Net Income after tax/Net Income before tax

849,941,367/2,681,011,849 31.7%

Expense Control Efficiency

Net Income before tax/Total Operating Revenues

2,681,011,849/7,884,761,090 34%

.Operating Efficiency

Total Operating Expense/Total

2,874,720,292/7,884,761,090 36.46%

Page | 47

Operating revenue

Employee

productivity ratio

Net operating income / total no. of full-time employees

2,681,011,849/1523 TK.1,760,349

BANK ASIA - 2011

Ratio Formula Calculation

Asset Utilization

Total Operating Revenues/Total Assets

6,654,492,493/118,020,504,822 5.64%

Tax Management Efficiency

Net Income after tax/Net Income before tax

2,043,256,551/3,614,061,828 56.54%

Expense Control Efficiency

Net Income before tax/Total Operating Revenues

3,614,061,828/6,654,492,493 54.31%

.Operating Efficiency

Total Operating Expense/Total Operating revenue

2,430,668,241/6,654,492,493 36.53%

Employee

productivity ratio

Net operating income / total no. of full-time employees

3,614,061,828/1,390 TK.2,600,044

BANK ASIA - 2010

Ratio Formula Calculation

Page | 48

Asset Utilization

Total Operating Revenues/Total Assets

6,670,998,590/105,198,050,148 6.34%

Tax Management Efficiency

Net Income after tax/Net Income before tax

1,929,582,157/3,579,520,742 53.91%

Expense Control Efficiency

Net Income before tax/Total Operating Revenues

3,579,520,742/6,670,998,590 53.66%

.Operating Efficiency

Total Operating Expense/Total Operating revenue

2,422,133,786/6,670,998,590 36.31%

Employee

productivity ratio

Net operating income / total no. of full-time employees

3,579,520,742/1,237 TK.2,893,711

BANK ASIA - 2009

Ratio Formula Calculation

Asset Utilization

Total Operating Revenues/Total Assets

4,129,503,653/68,663,199,976 6.01%

Tax Management Efficiency

Net Income after tax/Net Income before tax

1,327,184,458/2,286,192,468 58.05%

Expense Control Efficiency

Net Income before tax/Total Operating Revenues

2,286,192,468/4,129,503,653 55.36%

.Operating Efficiency

Total Operating Expense/Total

1,512,465,951/4,129,503,653 36.62%

Page | 49

Operating revenue

Employee

productivity ratio

Net operating income / total no. of full-time employees

2,286,192,468/1,031 TK.2,217,451

IDLC - 2013

Ratio Formula Calculation

Asset Utilization

Total Operating Revenues/Total Assets

2,762,513,057/50,429,383,474 5.48%

Tax Management Efficiency

Net Income after tax/Net Income before tax

669,466,122/1,325,201,146 50.52%

Expense Control Efficiency

Net Income before tax/Total Operating Revenues

1,325,201,146/2,762,513,057 47.97%

.Operating Efficiency

Total Operating Expense/Total Operating revenue

1,244,470,721/2,762,513,057 45.05%

Employee

productivity ratio

Net operating income / total no. of full-time employees

1,325,201,146/642 TK.2,064,176

IDLC - 2012

Ratio Formula Calculation

Page | 50

Asset Utilization

Total Operating Revenues/Total Assets

2,403,239,834/37,783,865,737 6.36%

Tax Management Efficiency

Net Income after tax/Net Income before tax

712,821,226/1,252,188,166 56.93%

Expense Control Efficiency

Net Income before tax/Total Operating Revenues

1,252,188,166/2,403,239,834 52.10%

.Operating Efficiency

Total Operating Expense/Total Operating revenue

1,058,105,008/2,403,239,834 44.03%

Employee

productivity ratio

Net operating income / total no. of full-time employees

1,252,188,166/481 TK.2,603,301

IDLC - 2011

Ratio Formula Calculation

Asset Utilization

Total Operating Revenues/Total Assets

2,159,874,824/31,164,540,454 6.93%

Tax Management Efficiency

Net Income after tax/Net Income before tax

500,282,954/1,216,602,518 41.12%

Expense Control Efficiency

Net Income before tax/Total Operating Revenues

1,216,602,518/2,159,874,824 56.33%

.Operating Efficiency

Total Operating Expense/Total

913,460,730/2,159,874,824 42.29%

Page | 51

Operating revenue

Employee

productivity ratio

Net operating income / total no. of full-time employees

1,216,602,518/409 TK.2,974,578

IDLC - 2010

Ratio Formula Calculation

Asset Utilization

Total Operating Revenues/Total Assets

3,046,920,087/26,929,990,229 11.31%

Tax Management Efficiency

Net Income after tax/Net Income before tax

1,327,098,116/1,956,230,807 67.84%

Expense Control Efficiency

Net Income before tax/Total Operating Revenues

1,956,230,807/3,046,920,087 64.20%

.Operating Efficiency

Total Operating Expense/Total Operating revenue

965,919,987/3,046,920,087 31.70%

Employee

productivity ratio

Net operating income / total no. of full-time employees

1,956,230,807/353 TK.5,541,730

IDLC - 2009

Ratio Formula Calculation

Page | 52

Asset Utilization

Total Operating Revenues/Total Assets

1,912,731,103/22,681,287,226 8.43%

Tax Management Efficiency

Net Income after tax/Net Income before tax

821,879,365/1,273,413,841 64.54%

Expense Control Efficiency

Net Income before tax/Total Operating Revenues

1,273,413,841/1,912,731,103 66.58%

.Operating Efficiency

Total Operating Expense/Total Operating revenue

489,504,439/1,912,731,103 25.59%

Employee

productivity ratio

Net operating income / total no. of full-time employees

1,273,413,841/253 TK.5,033,256

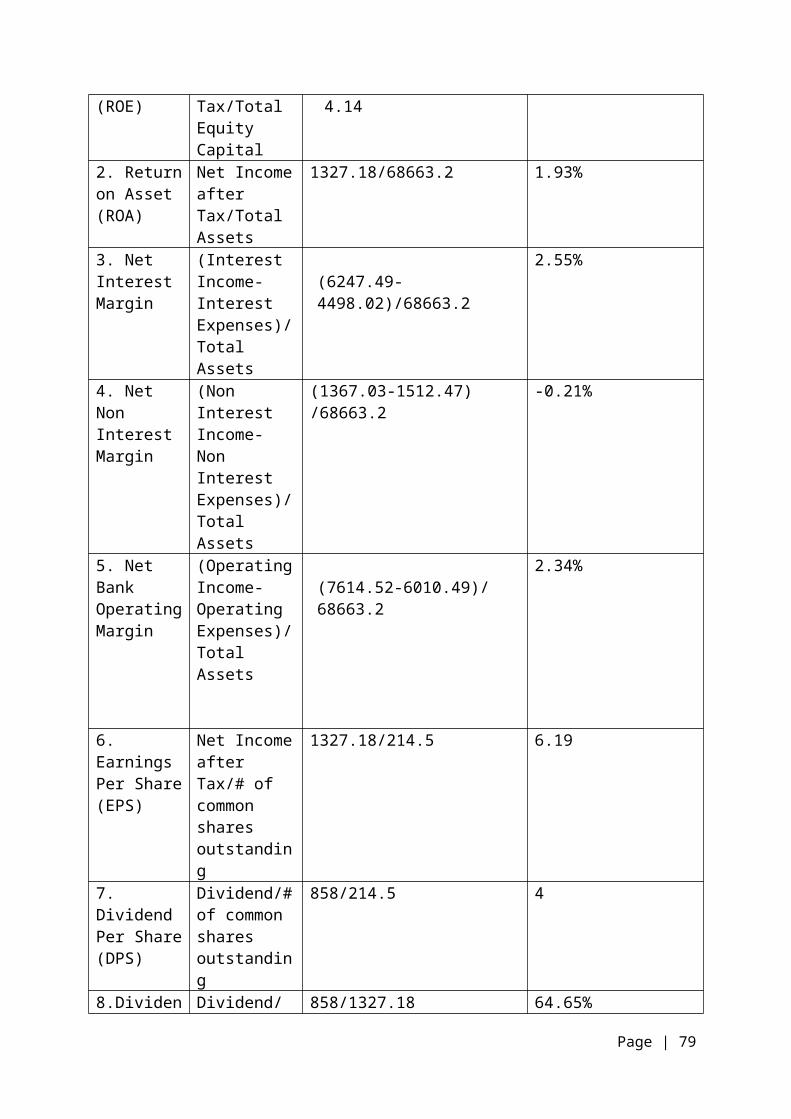

Profitability Ratios:Bank Asia Ltd 2013

Page | 53

** Taka values are in millions unless specified

Ratio Formula Calculations Answers1. Return on Equity (ROE)

Net Income after Tax/Total Equity Capital

1459.82/14617.79.99%

2. Return on Asset (ROA)

Net Income after Tax/Total Assets

1459.82/163777.74 0.89%

3. Net Interest Margin

(Interest Income-Interest Expenses)/ Total Assets

(14346.31-11166.02)/163777.74

1.94%

4. Net Non Interest Margin

(Non Interest Income- Non Interest Expenses)/ Total Assets

(2299.04-3117.36) /163777.74 -0.50%

5. Net Bank Operating Margin

(Operating Income-Operating Expenses)/ Total Assets

(16645.35-14283.38)/ 163777.74

1.44%

6. Earnings Per Share (EPS)

Net Income after Tax/# of common shares outstanding

1459.82/693.63 2.10

7. Dividend Per Share (DPS)

Dividend/# of common shares outstanding

693.63/693.63 1

8.Dividend Payout Ratio

Dividend/Net Income

693.63/1459.82 47.51%

9. Retention Ratio

Retained Earnings/Net Income

766.19/1459.82 52.49%

10. Dividend Yield Ratio

DPS/Current Market Price

1/23 4.35%

11. Net Profit Margin

Net Income/Total Operating Revenues

1459.82/16645.35 8.77%

Bank Asia Ltd 2012

Page | 54

**taka values are in millions unless specified

Ratio Formula Calculations Answers1. Return on Equity (ROE)

Net Income after Tax/Total Equity Capital

908/13045.176.96%

2. Return on Asset (ROA)

Net Income after Tax/Total Assets

908/140361.37 0.65%

3. Net Interest Margin

(Interest Income-Interest Expenses)/ Total Assets

(13296.06-9616.35)/140361.37

2.62%

4. Net Non Interest Margin

(Non Interest Income- Non Interest Expenses)/ Total Assets

(2210.32-2768.87) /140361.37 -0.39%

5. Net Bank Operating Margin

(Operating Income-Operating Expenses)/ Total Assets

(15506.38-12385.22)/ 140361.37

2.22%

6. Earnings Per Share (EPS)

Net Income after Tax/# of common shares outstanding

908/630.57 1.44

7. Dividend Per Share (DPS)

Dividend/# of common shares outstanding

630.57/630.57 1

8.Dividend Payout Ratio

Dividend/Net Income

630.57/908 69.45%

9. Retention Ratio

Retained Earnings/Net Income

277.43/908 30.55%

10. Dividend Yield Ratio

DPS/Current Market Price

1/21.5 4.65%

11. Net Profit Margin

Net Income/Total Operating Revenues

908/15506.38 5.86%

Bank Asia Ltd 2011

Page | 55

** taka values are in millions unless specified

Ratio Formula Calculations Answers1. Return on Equity (ROE)

Net Income after Tax/Total Equity Capital

1916.21/12478.9315.36%

2. Return on Asset (ROA)

Net Income after Tax/Total Assets

1916.21/117729.41 1.63%

3. Net Interest Margin

(Interest Income-Interest Expenses)/ Total Assets

(10903.58-8202.66)/117729.41

2.29%

4. Net Non Interest Margin

(Non Interest Income- Non Interest Expenses)/ Total Assets

(2416.97-2361.47) /117729.41 0.047%

5. Net Bank Operating Margin

(Operating Income-Operating Expenses)/ Total Assets

(13320.55-10564.13)/ 117729.41

2.34%

6. Earnings Per Share (EPS)

Net Income after Tax/# of common shares outstanding

1916.21/525.48 3.65

7. Dividend Per Share (DPS)

Dividend/# of common shares outstanding

1050.96/525.48 2

8.Dividend Payout Ratio

Dividend/Net Income

1050.96/1916.21 54.85%

9. Retention Ratio

Retained Earnings/Net Income

865.25/1916.21 45.15%

10. Dividend Yield Ratio

DPS/Current Market Price

2/38.2 5.24%

11. Net Profit Margin

Net Income/Total Operating Revenues

1916.21/13320.55 14.39%

Bank Asia Ltd 2010

Page | 56

** taka values are in millions unless specified

Ratio Formula Calculations Answers1. Return on Equity (ROE)

Net Income after Tax/Total Equity Capital

1929.58/7059.9427.33%

2. Return on Asset (ROA)

Net Income after Tax/Total Assets

1929.58/105198.05 1.83%

3. Net Interest Margin