Country Information Sheet: ARGENTINA - World...

275

1 Annex E International Experiences with Agricultural Insurance: Findings from a World Bank Survey of 65 Countries

Transcript of Country Information Sheet: ARGENTINA - World...

1

Annex E International Experiences with Agricultural Insurance: Findings from a World Bank Survey of 65 Countries

2

Table of Contents Acknowledgements ......................................................................................................................... 4 Introduction ..................................................................................................................................... 5 Overview on Agricultural Insurance: ARGENTINA ..................................................................... 6 Overview on Agricultural Insurance: AUSTRALIA .................................................................... 11 Overview on Agricultural Insurance: AUSTRIA ......................................................................... 14 Overview on Agricultural Insurance: BOLIVIA .......................................................................... 19 Overview on Agricultural Insurance: BRAZIL ............................................................................ 22 Overview on Agricultural Insurance: BULGARIA ...................................................................... 33 Overview on Agricultural Insurance: CANADA ......................................................................... 37 Overview on Agricultural Insurance: CHILE ............................................................................... 41 Overview on Agricultural Insurance: CHINA .............................................................................. 46 Overview on Agricultural Insurance: COLOMBIA ..................................................................... 51 Overview on Agricultural Insurance: COSTA RICA ................................................................... 55 Overview on Agricultural Insurance: CYPRUS ........................................................................... 59 Overview on Agricultural Insurance: CZECH REPUBLIC ......................................................... 62 Overview on Agricultural Insurance: DOMINICAN REPUBLIC ............................................... 65 Overview on Agricultural Insurance: ECUADOR ....................................................................... 69 Overview on Agricultural Insurance: EL SALVADOR ............................................................... 73 Overview on Agricultural Insurance: ETHIOPIA ........................................................................ 76 Overview on Agricultural Insurance: FRANCE ........................................................................... 79 Overview on Agricultural Insurance: GERMANY ...................................................................... 84 Overview on Agricultural Insurance: GREECE ........................................................................... 88 Overview on Agricultural Insurance: GUATEMALA ................................................................. 93 Overview on Agricultural Insurance: HONDURAS .................................................................... 96 Overview on Agricultural Insurance: HUNGARY ....................................................................... 99 Overview on Agricultural Insurance: INDIA ............................................................................. 102 Overview on Agricultural Insurance: IRAN ............................................................................... 110 Overview on Agricultural Insurance: ISRAEL ........................................................................... 114 Overview on Agricultural Insurance: ITALY ............................................................................. 118 Overview on Agricultural Insurance: JAMAICA ....................................................................... 123 Overview on Agricultural Insurance: JAPAN ............................................................................ 126 Overview on Agricultural Insurance: KAZAKHSTAN ............................................................. 132 Overview on Agricultural Insurance: MALAWI ........................................................................ 136 Overview on Agricultural Insurance: MAURITIUS .................................................................. 139 Overview on Agricultural Insurance: MEXICO ......................................................................... 142 Overview on Agricultural Insurance: MOLDOVA .................................................................... 153 Overview on Agricultural Insurance: MONGOLIA ................................................................... 156 Overview on Agricultural Insurance: MOROCCO .................................................................... 158 Overview on Agricultural Insurance: NEPAL ............................................................................ 162 Overview on Agricultural Insurance: NEW ZEALAND ............................................................ 166 Overview on Agricultural Insurance: NICARAGUA ................................................................. 169 Overview on Agricultural Insurance: PANAMA ....................................................................... 172 Overview on Agricultural Insurance: PARAGUAY .................................................................. 178

3

Overview on Agricultural Insurance: PERU .............................................................................. 180 Overview on Agricultural Insurance: PHILIPPINES ................................................................. 184 Overview on Agricultural Insurance: POLAND ........................................................................ 189 Overview on Agricultural Insurance: PORTUGAL ................................................................... 193 Overview on Agricultural Insurance: ROMANIA ..................................................................... 199 Overview on Agricultural Insurance: RUSSIA .......................................................................... 203 Overview on Agricultural Insurance: SLOVENIA ..................................................................... 207 Overview on Agricultural Insurance: SOUTH AFRICA ............................................................ 211 Overview on Agricultural Insurance: SOUTH KOREA ............................................................ 214 Overview on Agricultural Insurance: SPAIN ............................................................................. 219 Overview on Agricultural Insurance: SUDAN ........................................................................... 226 Overview on Agricultural Insurance: SWEDEN ........................................................................ 230 Overview on Agricultural Insurance: SWITZERLAND ............................................................ 234 Overview on Agricultural Insurance: THAILAND .................................................................... 237 Overview on Agricultural Insurance: THE NETHERLANDS ................................................... 240 Overview on Agricultural Insurance: UKRAINE ....................................................................... 247 Overview on Agricultural Insurance: URUGUAY ..................................................................... 251 Overview on Agricultural Insurance: UNITED STATES .......................................................... 256 Overview on Agricultural Insurance: VENEZUELA ................................................................. 268 Overview on Agricultural Insurance: WINDWARD ISLANDS................................................ 272

4

Acknowledgements This document provides an overview the status of agricultural insurance markets in 62 developed and developing countries. It is based on the World Bank survey of agricultural insurance markets conducted in 2008 under the leadership of Olivier Mahul (Insurance for the Poor Program Coordinator, Non-Bank Financial Institutions unit in the Global Capital Markets Development Department (GCMNB), World Bank) and Charles Stutley (International Agricultural Insurance Consultant, GCMNB, World Bank). The team also comprised of William Dick (Consultant, Commodity Risk Management Group, Agricultural and Rural Development, World Bank), Barry Goodwin (Professor of Agricultural Economics, North Carolina State University), Ramiro Iturrioz (Senior Agricultural Insurance Specialist, GCMNB, World Bank); Roman Shynkarenko (Consultant, GCMNB, World Bank), and Ligia Vado (Consultant, GCMNB, World Bank). It is Annex E of the book Government Support to Agricultural Insurance: Challenges and Options for Develpoing Countries, co-authored by Olivier Mahul and Charles Stutley. The authors sincerely thank the many respondents who kindly completed the questionnaire sent to them as part of the World Bank Survey on agricultural insurance in 2008, or who separately provided country information. They are listed below.

Agriculture Financial Services Corporation (Alberta, Canada)

Agria Djurförsäkring (Sweden) Agricultural Insurance Fund (A.P.I.F.) (Iran) Agricultural Insurance Pool (TARSIM) (Turkey) Agriculture Insurance Company of India Ltd.

(AICI) (India) Agriculture Insurance Consultant (China) Agroasemex, S.A. (Mexico) Agrodosa (Dominican Republic) Agroseguro, S.A. (Spain) Aon Re (Argentina) Aon Re (Australia) Aon Re (New Zealand) Aon Re (South Africa) Aseguradora Magallanes (Chile) Asiban SA (Romania) Banco de Seguros del Estado del (Uruguay) CA Seguros, S.A. (Portugal) Cámara Hondureña de Aseguradores (Honduras) CGM Gallagher Group (Jamaica) Concordia Polska TUW (Poland) Ethiopian Insurance Corporation (Ethiopia) Federal Agency of State Support of Insurance in

Agroindustrial Production (Russia) GlobalAgRisk (UNITED STATES) Hannover Re (Germany) Index Based Livestock Insurance Project

Implementation Unit (Mongolia) Instituto Nacional de Seguros (Costa Rica) Instituto Nicaragüense de Seguros y Reaseguros

(Nicaragua) Ismea (Italy) Kanat (Israel) League of Insurance Organizations of Ukraine

(Ukraine)

Mapfre Colombia (Colombia) Mclarens Toplis Peru S.A. (Peru) Ministère de l’Alimentation, de l’Agriculture et de

la Pêche (France) Ministerio de Ganadería, Agricultura y Pesca

(MGAP) (Uruguay) Ministry of Finance (Azerbaijan) Moldasig (Republic of Moldova) Munich Re (Argentina) Nico General Insurance Company Limited (Malawi) Nigerian Agricultural Insurance Corporation

(Nigeria) North Carolina State University (United States) Nyala Insurance S.C. (Ethiopia) Office of the Insurance Commission (Thailand) Oficina de Riesgo Agropecuario (Argentina) OTP Garancia Insurance Ltd. Co (Hungary) Paris Re (France) Partner Re (Chile) Philippine Crop Insurance Corporation (The

Philippines) Schweizer Hagel (Switzerland) Seguros Colonial (Ecuador) Shiekan Insurance & Reinsurance Co. Ltd. (Sudan) Siam Commercial Samaggi Insurance Public

Company Limited (Thailand) Société Centrale de Réassurance (Morocco) State Agency for Regulation of Finance Market and Finance Institutions (Kazakhstan) Swiss Re (Brazil) Swiss Re (Switzerland) Swiss Re America Corporation (United States) TAGH Gestión (Argentina) Thai Re Insurance Public Co., Ltd. (Thailand) Windward Islands Crop Insurance Ltd. (Dominica)

5

Introduction Agriculture remains a source of livelihood for almost half of humanity. It is also a source of growth for national economies, and can be a provider of investment opportunities for the private sector. However, millions of poor people face prospects of tragic crop failure or livestock mortality when, as a result of climate change, rainfall patterns shift or extreme events such as drought and floods become more frequent. Agricultural insurance is key in assisting farmers, herders, and governments lessen the negative financial impact of these adverse natural events. Based on a unique survey of agricultural insurance programs in 65 advanced and emerging countries, we have pulled together collective knowledge and experiences to help policymakers promote sound agricultural insurance programs. The key objectives of the survey were to document international experience with public and private agricultural insurance in developed and developing economies and to examine the ways in which governments support agricultural insurance. The findings of the survey were used to make some recommendations for developing countries that plan to develop agricultural insurance. The survey was based on a questionnaire designed by the World Bank to elicit information about the organizational structure of agricultural insurance in each country; the type of agricultural insurer (public or private); and, in markets with public sector intervention, the nature and types of support and their cost to the public sector. The study was also designed to allow for a simple comparison of the financial performance of private and public sector agricultural insurance programs. Questionnaires were distributed to agricultural insurance companies in all 104 countries that were known to have some form of agricultural insurance provision in 2008. Sixty-five countries returned the questionnaire. The World Bank team supplemented these questionnaires with information drawn from third-party sources, including interviews and insurance company websites. In some cases, the data may have been entered incorrectly by the respondents and, despite the best efforts of the World Bank team, these errors may not have been identified by the team in the analysis and interpretation of this data. Furthermore, in order to compare financial figures across a wide number of territories, all original currency data has been converted into U.S. dollars using average currency exchange rates for each year. It is recognized that this may slightly alter the estimated long-term ratios for the transformed U.S. dollar dataset. While every attempt has been made by the World Bank team faithfully and accurately to report the original questionnaire data provided by each respondent, any errors and omissions or incorrect interpretation of the data and results presented in this chapter are the sole responsibility of the team leaders. The survey included 65 countries (62 percent of all countries with agricultural insurance), including 21 high-income, 18 upper-middle-income, 20 lower-middle-income, and 6 low-income countries. As the main focus of this study is on agricultural insurance in developing countries, the very high proportion of responses received from respondents in low- and middle-income countries make the survey highly representative of and informative about the agricultural insurance market in developing countries. We hope that this analysis provides policymakers with a current picture of the spectrum of institutional frameworks and experiences with agricultural insurance - ranging from countries in which the public sector provides no support to those in which governments heavily subsidize agricultural insurance – and will thus make a compelling case for public-private partnerships in the promotion of agricultural insurance.

6

Overview on Agricultural Insurance: ARGENTINA

1. Agricultural Insurance Market Review History of Agricultural Insurance Crop hail insurance was first introduced in 1874. This product was marketed mainly by mutual companies and cooperatives until 1994 when several private insurance companies started to offer crop insurance. The most demanded and marketed product is crop hail, damage-based insurance. Due to the high competition within the crop insurance market during the last few years, the number of products, the risks covered, and the levels of coverage have been expanded. Therefore, companies commonly offer products like multi-peril crop insurance (MPCI), MPCI portfolio coverage, and insurance coverage for hail plus additional risks like wind, freeze, excess of moisture, and other named risks. Large farms purchase some of these products; however, traditional crop hail insurance still accounts for about 95% of the total market premium volume. In spite of the importance of beef production and exports to the Argentinean economy, livestock insurance products are very under-developed in Argentina and, despite many attempts to introduce this class of business, the demand is still limited to high value animals (mainly bloodstock).

Federal government support to agricultural insurance in Argentina is limited to assisting provinces and insurance companies in the development of agricultural insurance programs, basically by providing technical support and information. However, in the recent years, several provinces have developed their own subsidized crop insurance programs in order to provide protection to their local farmers (for example Mendoza, Río Negro, and Chaco Provinces). There is no special agricultural insurance legislation. Agricultural Insurance Market Structure (2008)

In 2008 there were about 30 insurance companies offering agricultural insurance products. Twenty-three were private insurance companies, six were cooperatives, and one was a public insurance company. The two main insurers, La Segunda and Sancor, both cooperatives, have together about 50% of the market share in terms of written premiums, and the five biggest players underwrite 75% of the agricultural insurance premiums in this market. Agricultural Insurance Products Available The most popular product is traditional crop hail insurance (crop hail policy with a 6% damage franchise). Due to the strong competition in the market over the last decade, the range of products, types of coverage, and covered risk has been diversified and expanded. Therefore, products like MPCI, MPCI global portfolio covers, and traditional crop hail insurance are available for different deductible levels, and hail plus additional risk covers like wind, freeze, excess rain at harvest and, in some cases, even drought are commonly offered in the Argentinean market. Delivery Channels

The most important delivery channels are through the insurance agents and insurance brokers. There are also some cases where the delivery channel is through input suppliers. Programs with suppliers in Argentina are placed and managed as corporate programs, which are usually placed through insurance

7

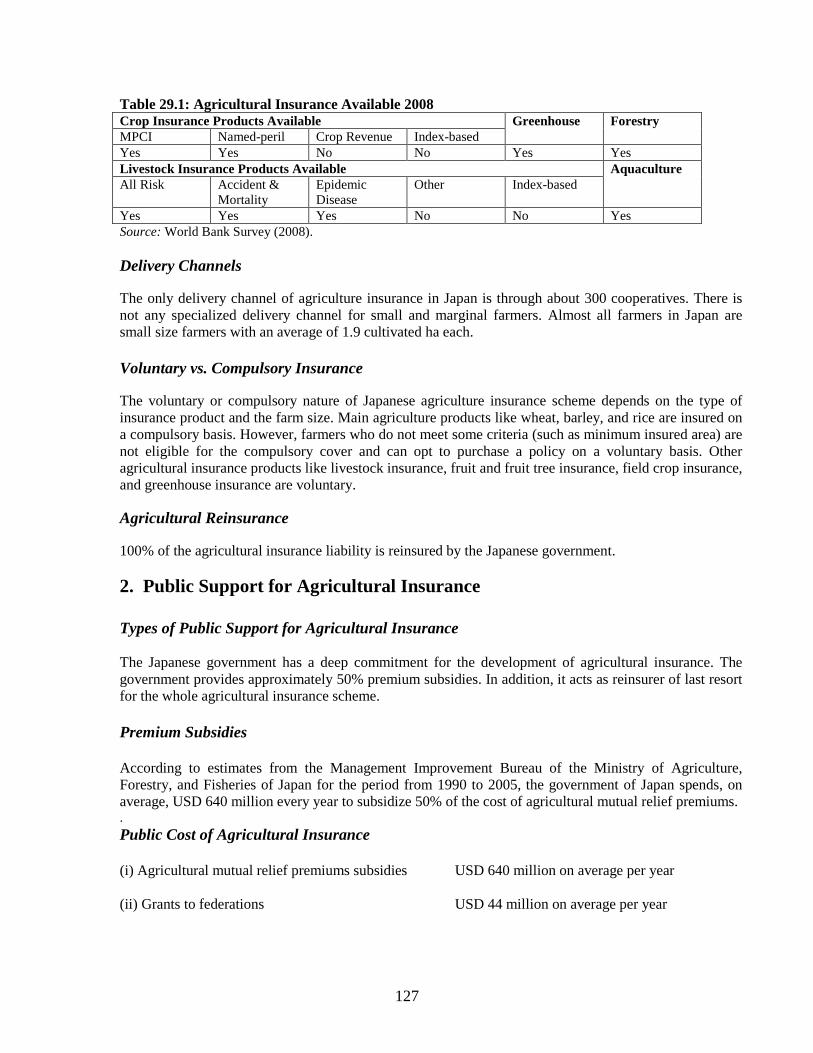

brokers. There are no specialized delivery channels for small and marginal farmers. The exception is a public-private partnership which provides greenhouse insurance for small farmers in Corrientes by using the structure of the PRODERNEA (FIDA- BID) Program with approximately 40 policies issued. Table 1.1: Agricultural Insurance Available 2008 Crop Insurance Products Available Greenhouse Forestry MPCI Named-peril Crop Revenue Index-based Yes Yes No Yes, a few

“tailor-made” frost-index products for fruit companies

Yes Yes

Livestock Insurance Products Available Aquaculture All Risk Accident &

Mortality Epidemic Disease

Other Index-based

No Yes, limited coverage

No Yes, limited voluntary market for bloodstock insurance

No Yes, one voluntary policy

Source: World Bank Survey (2008). Voluntary vs. Compulsory Insurance Crop insurance is mainly voluntary. However, there are some cases where crop insurance is compulsory for farmers who access seasonal crop loans from banks. This represents, however, less than 5% of the total premium. Livestock insurance is voluntary. Agricultural Reinsurance Argentina represented the largest crop insurance and reinsurance market in Latin America in 2008/09. Local companies can readily access reinsurance capacity for crop hail but, in the case of MPCI coverage, reinsurance capacity is much more restricted. The reinsurance capacity for standing timber fire cover is also restricted. Crop hail insurance companies have increased their risk retention in recent years, while the agricultural reinsurance markets have softened until end of 2008. Argentinean crop insurers purchase a combination of proportional and non-proportional treaty reinsurance.

2. Public Support for Agricultural Insurance Types of Public Support for Agricultural Insurance Traditionally, the Argentinean crop hail insurance market has been a completely private commercial market which has operated for more than a hundred years with no support from the federal government. In 2008 there were three public sector supported programs for agricultural insurance: (i) Mendoza Province Fruits and Vineyard Hail Crop Insurance Scheme, (ii) Rio Negro Province Fruit-Hail Crop Insurance Scheme, and (iii) PRODERNEA (FIDA–BID).

Mendoza Province Fruits and Vineyard Hail Crop Insurance Scheme. The province purchased catastrophic hail coverage for all registered fruits and vineyard producers within Mendoza Provincethrough a bidding process among the insurance companies.

8

Rio Negro Province Hail Crop Insurance Scheme. The provincial government subsidizes a portion of the commercial premium for hail coverage for apples, pears, and cherries.

PRODERNEA (FIDA–BID). Under this program, the federal government provides subsidies as a percentage of commercial premiums for greenhouse insurance. There are also some studies to implement a subsidized cotton insurance scheme in Chaco Province. It is still unclear whether the government will subsidize an index product or an indemnity-based product. Premium subsidies

The estimated volume of premium subsidies for the whole market is USD 5 million.

3. Agricultural Insurance Penetration Insurance Penetration Rate

About 130,000 crop insurance policies were issued in 2007/08, and the insured area reached 16,592,000 ha, representing about 50% of total national cropped area.

The number of crop insurance policies and the insured area has been increasing after Argentina’s economic crisis in 2001. This process has been driven by two factors: (i) improvement in agricultural products’ gross margins, and (ii) increase in international commodity prices. Both factors have contributed to an increase in the value of assets at risk and therefore an increased demand for crop insurance. Table 1.3 shows that, over the past 5 years, there has been a major increase in the crop insurance market with a 240% increase in Total sum insured (TSI) to USD 6.3 billion and a 220% increase in crop insurance premiums to USD 240 million in 2007/08. The bulk, or more than 95% of this business, is crop hail insurance, and this is reflected by the relatively low average premium rate of 3.8% in 2007/08.

The demand for livestock insurance in Argentina is very low, with less than 0.5% of the total herd insured.

Forestry insurance has grown rapidly in Argentina. Insurance penetration is still low with about 123,112 hectares insured, which represents about 8% of the commercial forestry plantations surface.

4. Financial Performance 5-Year Results The average loss ratio for the whole market over the last five years is estimated at 62%1

. Despite the fact that the average premium rates remained relatively stable, the breadth of coverage offered by insurance companies has increased every year throughout this period (Table 1.3).

Cost of Agricultural Insurance Provision

Market costs are shown in Table 1.4 as a percentage of the original gross premium rate. For the whole market the cost ratios with respect to the original gross premiums (OGP) are: acquisition and local 1 All average loss ratios presented in this Annex are based on the 5-year (or actual number of years available data) long-term loss ratios which are calculated as total claims divided by total premiums and multiplied by 100%

9

brokerage, 10 to 15%; company’s administrative costs, 8 to 10%; loss adjustments expenses (LAE), 5%; and total costs, 23 to 30%. In addition, insurance sales tax (including VAT, provincial taxes, stamp duty, and issuance rights) of about 24% is payable on agricultural insurance premiums. The combined ratio is estimated at about 87% for crop insurance.

5. Public Disaster Assistance Programs Federal government ad hoc post disaster relief assistance is available under the Agricultural and Livestock Emergency Law “Ley de Emergencia Agropecuaria (22913/81)” and is implemented by the Secretariat of Agriculture, Livestock, Fisheries, and Food, SAGPyA. In addition, each province operates its own Ley de Emergencia Agropecuaria. Under this law, the farmers whose losses represent more than 50% of their production are eligible for disaster relief compensation.

Covered perils include climatic perils, earthquake, and biological perils. In practice, compensation payments to farmers under the Agricultural Disaster Relief Program are limited to subsidized interest rates for those loans issued by state-owned banks, federal and provincial tax waivers, and tax exemptions.

Since the application of this law is still not ratified, and since it therefore has no budget, it has several interpretation and application problems. The Argentine Parliament has on various occasions considered reviewing and amending the law, including its funding, but no changes have been introduced to date.

6. Additional Tables Table 1.2: Estimated Crop Insurance Penetration

Year

Number of Crop

Policies

Percentage of Farmers Purchasing

Insured Area (mil of ha)

Percentage of National Crop Area

Insured 2003 100,325 -- 10.3 35% 2004 101,964 -- 10.9 36% 2005 103,024 -- 11.6 40% 2006 115,000 -- 14.6 47% 2007 120,000 -- -- --

Source: World Bank Survey (2008).

10

Table 1.3: Crop and Livestock Insurance Results, 2003 to 2007

Year

Number of

Policies

TSI (USD

million)

Premium (USD

million)

Paid Claims

(USD million)

Average Policy

Size (USD)

Average Policy

Premium (USD)

Average Rate

Loss Ratio

Crops 2003 100,325 2,584.0 107.3 53.7 25,756 1,070 4.2% 50% 2004 101,964 2,221.3 91.3 42.3 21,785 896 4.1% 46% 2005 103,024 2,728.0 104.7 69.3 26,479 1,016 3.8% 66% 2006 115,000 4,438.3 153.8 121.6 38,594 1,338 3.5% 79% 2007 120,000 6,315.8 240.0 156.0 52,632 2,000 3.8% 65%

Average 108,063 3,657.5 139.4 88.6 33,049 1,264 3.8% 62% Including Livestock and Forestry

2003 100,325 2,584.0 107.3 53.7 25,756 1,070 4.15% 50% 2004 101,964 2,221.3 91.3 42.3 21,785 896 4.11% 46%

2005* 103,024 2,877.0 105.4 69.3 27,926 1,023 3.66% 66% 2006* 115,000 4,779.0 155.3 122.0 41,557 1,351 3.25% 79% 2007* 120,000 6,315.8 240.0 156.0 52,632 2,000 3.80% 65%

Average 108,063 3,755.4 139.9 88.7 33,931 1,268 3.72% 62% Source: World Bank Survey (2008). Table 1.4: Insurers’ Costs as a Percent of OGP

Source: World Bank Survey (2008). Source of Country Overview Information: World Bank Survey (2008).

Costs Crop

Marketing and Acquisition 10%-15%

Administration 8%-10% Loss Adjustment 5% Total A&O Costs 23%-30% Insurance Premium Taxes 24% Total 48%-58%

11

Overview on Agricultural Insurance: AUSTRALIA

1. Agricultural Insurance Market Review History of Agricultural Insurance

Crop insurance started in Australia in 1918 but did not expand much until the 1960s. Crop insurance now is very well established in Australia, is handled by private insurers, and is competitive. Expansion of the traditional broad acre hail insurance to many other crops happened from the 1980s onwards. Forestry insurance is also important. Livestock insurance is a much smaller industry than crop insurance but includes equine, livestock, and aquaculture insurance. Agricultural Insurance Market Structure (2008)

Three private sector insurers underwrite crop and livestock business; nine offer crop insurance only, and three offer livestock only. Insurance companies write most broad acre crop insurance (e.g. cereals, oilseeds). Three managing underwriting agencies write specialist lines such as cotton and horticulture, and there are a few specialist livestock agencies, mainly focusing on racehorses. Forestry insurance is also offered by insurers and through agencies. Agricultural Insurance Products Available

Crop hail and named-peril crop insurance are available, but not revenue-based or multi-peril crop insurance (MPCI) policies. Greenhouse insurance is available. Although “broad acre” crop insurance is the dominant and longstanding crop insurance, which covers principally hail and fire, in the 1980s and 1990s there was an expansion of schemes for specific crop sectors, notably cotton and viticulture. Forestry insurance is also an important product in Australia. Livestock insurance covering accident and mortality is available, as well as aquaculture insurance. A number of weather derivatives are transacted. There are no weather index insurance products, although these have been researched in the private sector. Table 2.1: Agricultural Insurance Available 2008 Crop Insurance Products Available Greenhouse Forestry MPCI Named-peril Crop Revenue Index-based No Yes No No Yes Yes Livestock Insurance Products Available Aquaculture All Risk Accident &

Mortality Epidemic Disease

Other Index-based

No Yes No No No Yes Source: World Bank Survey (2008). Delivery Channels

For crop insurance, brokers are the most important distribution channel. In decreasing order of importance after brokers are the insurer’s own agents, producer associations and cooperatives, input suppliers (“stock and station agents”), and banks. There are specialist association schemes with their own distribution channels, for example the forest growers association, the dried fruit industry, and cotton ginners. Distribution networks are well established and competitive. For livestock insurance, the same channels

12

are important, although linkages with banks are less developed. There are no special delivery channels or programs for small farmers. Voluntary vs. Compulsory Insurance Crop and livestock insurance is voluntary. Agricultural Reinsurance Private sector reinsurance (quota-share, surplus, and stop-loss) is widely developed and competitive. It is not considered a constraint for named-peril crop insurance, livestock insurance, or index insurance. For initiatives in Australia developed to investigate the possibility of multiple-peril yield insurance, reinsurance is a moderate constraint. Drought is a major catastrophic hazard in Australia.

2. Public Support for Agricultural Insurance Types of Public Support for Agricultural Insurance There is no form of public support for agricultural insurance in Australia. Premium Subsidies There is no premium subsidy on agricultural insurance in Australia. Public Cost of Agricultural Insurance

There is no cost to the government in support of agricultural insurance.

3. Agricultural Insurance Penetration Insurance Penetration Rate

Information on the agricultural sector is an estimate and is provided for 2007. For crop insurance, it is estimated that 25,000 crop insurance policies were issued and that 50% of farmers were insured. The area insured was 15 million ha or 50% of cropped area. The figure has been relatively stable over time and reflects the significant penetration of insurance in the large broad acre crop sector in Australia. There has been growth in specialist sectors such as viticulture. For livestock insurance, it is estimated that only 5% of the national cattle herd is insured. Data for forestry insurance is not available but, as noted, forestry insurance is well developed in Australia.

4. Financial Performance 5-Year Results Estimates are not available for the industry as a whole. One company involved in all crop insurance sectors shows loss ratios varying from 29% to 71% over a five-year period. Companies writing a national portfolio have a diversification of risk, for example spatially from western to southeastern Australia and

13

Queensland for broad acre, several viticulture regions, and different product types. Premium income for the agricultural insurance market in Australia is volatile and is influenced by drought (affecting cropped area which is insured) and more recently by commodity prices (affecting the value of crops insured). An estimate of the market premium income in Australia by class of business is provided for 2008 below: Table 2.2: Estimated Crop and Forestry Premium Income 2008

Class of Business Market Premium Income (USD

million)

Comment

Broad acre crops 96.0

Substantially increased in 2008 as a result of commodity prices

Cotton 11.5 Area of cotton is still much reduced as a result of the drought. Premium income has reached USD 47.7 million in the past

Viticulture 17.2 -- Orchard 1.9 -- Forestry 28.8 --

Source: World Bank Survey (2008). Livestock accident and disease insurance premium estimates for the market are $A 50 million (USD 47.5 million). However, a majority of this figure is bloodstock insurance. There is no livestock epidemic insurance. The figure of 5% of livestock being insured is due to catastrophe cover being available for feedlot cattle, a high proportion of which are insured. There is a limited amount of aquaculture insurance, estimated at $A 1 million (USD 0.95 million) of premium income. Cost of Agricultural Insurance Provision

For both crop and livestock insurance, the following are estimates for companies in the market of costs compared to original gross premium (OGP): marketing and acquisitions (commissions) 13.0%; insurer administration excluding loss adjustment 7.0%; loss adjustment costs 2.5%, and total costs 22.5%. Note that overseas reinsurers pay a premium tax of 3% of OGP.

5. Public Disaster Assistance Programs Australian farmers have suffered from major drought problems in the last decade. These affect both rainfed annual cereal cropping areas and the major irrigation zones (for example in the tributaries to the Darling River), where headwater reservoirs have been subject to major limits on water allocations.

Australia has an "Exceptional Circumstances” (EC) payment which has especially been applied for drought and bushfire losses. These amounted to $A 1.7 billion (USD 1.6 billion) in 2007 and $A 1.3 billion (USD 1.2 billion) in 2006. Grain farmers received $A 760 million (USD 722), and dairy farmers also received subsidies. Australian government expenditure on drought assistance in the five years to 2006 was more than $A 41.6 billion (USD 39.5 billion).

EC payments provide several forms of assistance to farmers (and to small businesses deriving at least 70% of their turnover directly from agriculture). Areas must be declared as disaster-affected. Direct payments may be made (relief payments) as special exit payments for farmer quitting agriculture, for re-training or relocation, and as tax deferrals. Source of Country Overview Information: World Bank Survey (2008).

14

Overview on Agricultural Insurance: AUSTRIA

1. Agricultural Insurance Market Review History of Agricultural Insurance

Agricultural insurance in Austria is provided through the Austrian Hail Insurance Company, which is a mutual organization. The Austrian insurance system aims to provide a broad risk management framework for the agricultural sector. Multi-peril crop insurance (MPCI) has been developed since 1995. Before this date agricultural insurance companies offered crop and greenhouse insurance mostly against hail and storms. Since 1995 the insurance companies started to offer comprehensive insurance coverage against hail, drought, storms, floods, frost, and some other risks. Livestock insurance was introduced in 2003.

Blanket agricultural insurance was introduced in 1987; that is, farmers willing to insure crops against hail had to insure all arable crops. That program became the basis for the introduction of MPCI insurance.

The Austrian government has established a partnership program with the private insurance companies to control EU area-based subsidies. Under this program insurance companies receive area data (area, type of crops, yields) for preparation of annual crop insurance plans. Government contributions (in the form of premium subsidies) have stimulated farmers to adopt risk management strategies. A public-private insurance system is seen as an effective solution to substitute ex-post disaster compensations. Agricultural Insurance Market Structure

Agricultural insurance is offered through a special mutual organization founded by 17 insurance companies. The main objective of the Austrian Hail Insurance Company is to proviside high quality agricultural insurance products and services. The premium rates are established based on actuarial calculations and risk statistics. The system targets a loss ratio of 75% to leverage interests of insurance providers and farmers. Agricultural Insurance Products Available

The Austrian agricultural insurance system offers crop hail and crop MPCI products (Table 3.1). A farmer cannot insure selected fields, but rather all arable area must be insured. This rule is applied to all crops including field crops, grapes, and fruits. Insurance policies for field crops cover yield losses. For grapes and fruits, insurance policies cover both yield and quality loss. Premium rates are set by the insurer based on the loss experience. The bonus system is used separately for MPCI insurance and hail policies for field crops. The bonus-malus system is used for grapes and fruits. Settlement of claims is usually performed no later than two weeks after the harvest is completed.

There is no revenue insurance in Austria. Index insurance is not yet present. However, during the last three years insurance companies have designed a drought monitoring system based on a rainfall index. This system is used to assess crop losses due to drought. Multi-peril livestock insurance is present in Austria, but information was not available. Delivery Channels

The insurance agent network is the primary delivery channel. There are no special organizations or programs for small and marginal farmers.

15

Table 3.1: Agricultural Insurance Available 2008 Crop Insurance Products Available Greenhouse Forestry MPCI Named-peril Crop Revenue Index-based Yes Yes No No Yes No Livestock Insurance Products Available Aquaculture All Risk Accident &

Mortality Epidemic Disease

Other Index-based

No Yes No No No No Source: World Bank Survey (2008). Voluntary vs. Compulsory Insurance

Both crop and livestock insurance are voluntary in Austria. There are no mandatory requirements. Farmers cannot get ad hoc public assistance in case of hail or frost. The government considers that premium subsidies are sufficient to attract farmers to purchase insurance coverage.

Agricultural Reinsurance

Reinsurance of agricultural risks in Austria is provided through private domestic and international reinsurance companies. About 25% of the agricultural risks are ceded on a proportional basis to the pool of Austrian insurance companies. The remaining risk is reinsured through international reinsurance companies through stop-loss treaties which protect the insurance company retention against its liabilities in excess of a 110% loss ratio and up to a 150% loss ratio. The main international reinsurers are Munich Re, SCOR, Hannover Re, Swiss Re, and Sirius Re.

2. Public Support for Agricultural Insurance Types of Public Support for Agricultural Insurance There is national legislation on agricultural insurance and subsidization of insurance premiums. Ad hoc assistance is sometimes provided but not for the risks that can be insured through subsidized crop insurance products (hail and MPCI).

Premium Subsidies The total premium subsidy is 50% of the commercial premium with 25% paid by the central government and 25% paid by the regional government. Premium subsidies are offered only for hail and frost risks. Other agricultural insurance products are not subsidized. Public Cost of Agricultural Insurance

The government accumulates funds necessary for the 25% premium subsidy program in the National Catastrophe Fund. Another 25% subsidy is paid by the regional authorities. The total premium subsidy is 50% of premium. The national government subsidy payment is linked to the confirmation of the payments from the regional government budget. The overall public cost of agricultural insurance premium subsidies was US$ 31 million in 2006.

16

The government plays an important role in the development of agricultural insurance in Austria, though the main responsibility is with farmers and private insurers. The provision of subsidies is considered as the key factor for agricultural insurance development in the country, especially for MPCI.

3. Agricultural Insurance Penetration Insurance Penetration Rate

About 80% of crops or 1 million heactares are insured against hail. About 60% of crops are insured against multi-perils (Table 3.2). About 80% of farmers purchase crop and livestock insurance (68,000 farms). The number of policies in 2005 was 78,418. Data on agricultural insurance is limited, see Table 3.3. The data was available only for years 2003 to 2005.

4. Financial Performance 5-Year Results

Some limited data is available on the financial performance of agricultural insurance for the years 2003 to 2005 (see Table 3.4). Cost of Agricultural Insurance Provision

The overall public cost of premium subsidies to agricultural insurance was US$ 31 million in 2006.

5. Public Disaster Assistance Programs The government provides ad hoc assistance, but very rarely, and only for crop loss or damage that was caused by non-insurable risks. The national government follows the rules set by the European Union for assistance. During the period 2000-2004, the Austrian Catastrophe Fund paid US$ 72 millon mainly due to the occurrence of severe flood, frost, and drought events.

6. Additional Tables Table 3.2: Hail and MPCI Insurance Penetration

Hail Insured Area

Percentage of the Hail Area also Insured under MPCI

Field crops 79% 60% Grapes 60% 9% Fruits 58% --

Grassland 22% 90% Greenhouses 92% 85%

Source: World Bank Survey (2008).

17

Table 3.3: Estimated Crop and Livestock Insurance Penetration, 2003 to 2005

Year Number of Farms

Covered Percentage of Area Insured

Insured Area (mil of Ha)

Percentage of Animals Insured

Number of Animals Insured

2003

69,791 76.9% 1.0 9% 170,132

2004

68,896 78.0% 1.1 13% 258,783

2005

67,866 79.0% 1.1 19% 383,817 Source: World Bank Survey (2008). Table 3.4: Crop Insurance Results, 2003 to 2005

Year Number of

Policies

Total Sum Insured

(USD million)

Premium, Including Subsidies

(USD million)

Paid Claims

(USD million)

Loss Ratio

2003 -- 2,760.7 74.5 64.1 86% 2004 -- 2,925.3 77.0 41.6 54% 2005 -- 3,095.8 78.1 34.3 44%

Source: World Bank Survey (2008).

7. Other Information Types of Coverage Available In Austria there are 5 main types of crop insurance policy available including: a) Basic Hail Insurance. Available for all crops. Hail coverage indemnifies percentage damage to the

crop as determined by the insurance company’s loss adjusters. The indemnity is calculated as the percentage of loss times the sum insured less the deductible which for this case is 8% of the total sum insured over the affected area.

b) Multi-peril Crop Insurance covering yield loss in arable crops. Insured perils are hail, storm, frost, flood, rain, drought, drift, sprouting and pests. In case of hail losses are adjusted on a percentage damage basis. In the case of all other perils this insurance indemnifies losses when the actual yield obtained by the insured on its insured unit is below 50% of the expected yield. In such cases, the insured will receive a fixed indemnity of € 175 per hectare.

c) Vineyards Insurance is offered to protect wine-grape production against hail, frost and additional expenses after hail. This coverage also indemnifies qualitative losses. This coverage is a damage-based indemnity policy. In this case the basis of indemnity is the same as explained above for basic hail insurance. The difference is that in the case of frost damage the deductible to be applied is 35% of the total sum insured.

d) Fruit Hail Insurance. This insurance insures quantitative and qualitative aspects of fruit crops production against hail damage. This coverage offers protection from ground-up, subject to the application of deductibles that can vary from 10% to 30% of the total sum insured of the affected area depending on the loss experience of each insured unit.

e) Grassland and Silage Hail and Flood Coverage. This coverage protects the silage against hail damage, subject to a deductible of 8% of the total sum insured. In case of floods no deductible applies but the indemnities are limited to € 440 perhectare.

18

Options of Coverage The standard crop policy wording for the Austrian market is a named-peril damage-based indemnity policy. The policy is structured such that by purchasing basic hail coverage, the insured then has the option to select coverage for other perils in addition to hail by paying an extra premium. Under this modality farmers have the option to choose among single-risk insurance or combined-perils insurance. The top of the line option is yield insurance (multi-peril crop insurance) which is available only for arable crops. The possible combinations of perils are determined by the type of crop:

1) Hail coverage is available for all agricultural crops and greenhouses; 2) Storm insurance is available for: corn, tobacco, greenhouses and hail protection for fruits; 3) Drought protection is offered for cereals; corn; field pea; soybeans; sunflower; potatoes and oil

squash; 4) Flood insurance is offered to all arable crops, grassland and horticulture; 5) Frost coverage is available for all arable crops and vineyards; 6) Sprouting is covered on cereals and poppy crops; 7) Upsilting is protected on sugar-beets crops; 8) Damage caused by snails (pests) is available for all arable crops; 9) Damage caused by crows is a protection offered only for cereals, corn and oil-squash; 10) Unseasonal rainfall at harvest cover is offered for corn, potatoes and soybeans; and 11) Hail-coverage for round hay bales and polyethylene covering for horizontal silage clamps is also

offered. Sources of Country Overview Information: World Bank Survey (2008); European Commission (2006).

19

Overview on Agricultural Insurance: BOLIVIA

1. Agricultural Insurance Market Review History of Agricultural Insurance

Agricultural insurance was introduced in the country in 1979 by “Aseguradora Boliviana Agropecuaria” (ABA) which managed a pilot project with the support of the Organization of American States (OAS) and the Bolivian Institute of Agricultural Sciences. Due to the adverse effects of inflation and cessation of external funding in 1984 the company was closed in 1985.

In 1994 the Credit Finance Unit of CORDECRUZ (UCF) introduced the "Agricultural Insurance Study”, offering insurance to cover excess of rain peril on soybeans, corn, and wheat crops grown in Santa Cruz Province. Cyclical recurrence of excess of rainfall and, above all, lack of reinsurance, made the insurance industry reluctant to offer this product.

In 1999 the former state-owned company, Compañía Nacional de Seguros y Reaseguros, requested the authorization to market an agricultural insurance policy to cover excess rainfall, drought, and flood perils on soybean crops, again in Santa Cruz Province2

. But severe weather before the launch of the product discouraged the insurance company to offer the product.

In 2006 a rainfall index-based insurance pilot program managed by BISA Seguros y Reaseguros S.A and supported by USAID was developed to protect the farmers’ input costs against excess rainfall in Santa Cruz Province. The product was launched but then discontinued because of lack of demand. Agricultural Insurance Market Structure

Since 2008 two private commercial insurance companies, Latina Seguros Patrimoniales, S.A. and BISA have separately offered multi-peril crop insurance (MPCI) on a very selective basis and only for large soybean farmers in Santa Cruz Province. Both companies are technically supported by an Argentinean agricultural insurance company and reinsurance broker.

Up to 2009 there was no formal evidence of federal government support to agricultural insurance. Nevertheless, the government of Bolivia is currently conducting a study to implement a national Agricultural Insurance Scheme. There is no livestock insurance market in Bolivia, although some large commercial cattle owners may purchase voluntary cover from national/international markets. There is some limited demand for standing timber forestry fire insurance, which is placed in international markets on a voluntary basis. There is no form of special agricultural insurance legislation. Agricultural Insurance Products Available

The product available in this market is individual grower MPCI yield shortfall cover. Initially, MPCI policies were offered to cover soybeans (summer and winter crops) and sunflower production. The product is expected to be expanded to other crops in the near future. The policy covers all types of weather risks and fire but excludes non-controllable biological perils. Guaranteed yields under this policy

2 A risk management and insurance planning study for soybean insurance was commissioned through an international agricultural risk management specialist, ARM Ltd, UK.

20

vary from 40%-60% of the actual production history, depending on the crop/region and the product. These products are offered on an individual farmer basis and are mainly linked to input suppliers’ loans. Table 4.1: Agricultural Insurance Available 2008 Crop Insurance Products Available Greenhouse Forestry MPCI Named-peril Crop Revenue Index-based Yes No No No No Yes, facultative Livestock Insurance Products Available Aquaculture All Risk Accident &

Mortality Epidemic Disease

Other Index-based

No No No No No No Source: World Bank Survey (2008). Delivery Channels

The most important delivery channels are through the insurance brokers who usually work with input suppliers. There are no specialized delivery channels for small and marginal farmers. Voluntary vs. Compulsory Insurance

Crop insurance is voluntary. Agricultural Reinsurance

Argentinean insurance companies and International reinsurers offer reinsurance support to the local market.

2. Public Support for Agricultural Insurance Types of Public Support for Agricultural Insurance There is no evidence of public support for agricultural insurance. Premium Subsidies

There are no premium subsidies to agricultural insurance. Public Cost of Agricultural Insurance

Not applicable. Role of Public Sector Intervention in Agricultural Insurance The government of Bolivia and several regional governments have expressed interest in supporting the development of weather-based crop insurance, especially as a means to reduce income variability to small farmers. They currently provide financial and technical assistance from international donors to develop pilot crop insurance projects.

21

3. Agricultural Insurance Penetration Insurance Penetration Rate

In 2008 approximately 20,000 ha of soybeans were planned to be insured in Santa Cruz Department, but the final status of this program is not known.

4. Financial Performance 5-Year Results No data available. Cost of Agricultural Insurance Provision

No data available.

5. Public Disaster Assistance Programs No data available. Source of Country Overview Information: World Bank Survey (2008).

22

Overview on Agricultural Insurance: BRAZIL 1. Agricultural Insurance Market Review History of Agricultural Insurance Public sector crop insurance in Brazil dates back to 1954 when the federal government of Brazil formed PROAGRO (Guarantee Program for Agriculture and Livestock Activities, Programa de Garantia da Actividade Agropequária), a national, individual grower multi-peril crop insurance (MPCI) program linked to crop credit. Following this, various state governments formed their own public sector state-level crop and/or livestock insurance schemes, including Sao Paulo (COSESP), Minas Gerais (COCAMIG), and Rio da Janeiro3

. These state-level public sector MPCI programs carried high levels of premium subsidies. All operated at a financial loss, and the last one, COSESP, was terminated in 2005. PROAGRO, however, continued to operate in 2008 along with several other federal government crop insurance initiatives.

Between 1939 and 2007, the Brazilian insurance market was protected by law, and all reinsurances had to be offered to the national reinsurer, the Instituto Nacional de Resseguro do Brasil (IRB). During this period the IRB acted as a monopoly reinsurer in the Brazilian market, and international reinsurers were involved on a retrocession basis only. The Brazilian market was opened up to competition in 20074

, and the IRB was registered as a local reinsurer, IRB-Brasil Resseguros S.A.

The first private sector crop insurance initiative in Brazil dates back to 1997/98 when Porto Seguro, in collaboration with Partner Reinsurance Company, Zurich Branch, started a private crop hail program for apples and pears in various southern states of Brazil.

The federal government of Brazil is highly committed to promoting agricultural insurance and since 2005 has offered premium subsidies on private commercial agricultural insurance. This has been accompanied by a major expansion in commercial crop, livestock, and forestry insurance.

Agricultural Insurance Market Structure

Commercial Agricultural Insurers. In the past decade the private insurance sector has started to

become actively involved in agricultural insurance in Brazil. In 2003 there were only two commercial agricultural crop and or livestock insurers in the market, but in 2007, seven private commercial companies were actively underwriting crops and/or forestry and/or livestock. Aliança do Brasil is the largest commercial crop insurer with about 51% of the market premium volume in 2007/08, followed by Nobre Seguros with a 22% market share (Table 5.2). In 2008, a total of eight private commercial companies were operating in the Brazilian agricultural insurance market.

Public Sector Crop Insurance. The PROAGRO program has been administered through the

Central Bank of Brazil and is a federal government individual grower subsidized MPCI program which is designed to ensure that, in the event of crop failure, the growers’ production credit repayments are guaranteed as well as a percentage of the expected net revenue for that crop. The PROAGRO traditional 3 For a detailed evaluation of PROAGRO and COSESP operations and performance up to 1983 see Hazell et al., eds. 1986. Crop Insurance for Agricultural Development: Issues and Experience. Baltimore, John Hopkins University Press.. 4 This process of liberalising the reinsurance market will be fully completed in 2010.

23

program was extensively reformulated in 2004 and two new programs were created: (a) PROAGRO MAIS (PROAGRO “More”), and SEAF (Insurance for Family Agriculture, Seguro da Agricultura Familiar). Both of these programs are compulsory crop-credit insurance programs targeted at smallholder farmers who access seasonal production credit from PRONAF (National Program for the Strengthening of Family Agriculture – Programa Nacional de Fortalecimento da Agricultura Familiar). SEAF is administered by the Secretariat of Family Agriculture (Secretaria de Agricultura Familiar) and the Ministry of Agrarian Development (Ministério do Desenvolvimento Agrário). Further details of the SEAF program are provided in Box 1.

Agricultural Insurance Products Available The range of private sector commercial crop, livestock, and forestry insurance products available in Brazil are reported in Table 5.2, and then in Table 5.3 by insurance company. Individual grower MPCI yield-based indemnity cover for soybeans, maize, wheat, and other grain crops is the most common product underwritten by six companies. This is followed by a damage-based fruit hail policy (underwritten by four companies), and since 2004 forestry fire plus allied-peril insurance (underwritten by five companies).

Livestock and/or bloodstock insurance have been offered by Porto Seguro and Seguradora Brasileira Rural for a number of years, but in 2008 Porto Seguro has exited from this class of business. Cover is restricted to accident and mortality cover in cattle and horses, and epidemic disease cover is currently not insured. There is a very small amount of mortality insurance for sheep. Brazil, Uruguay, Venezuela, Argentina, and Ecuador are the only countries in South America which currently offer commercial livestock insurance.

For a number of years, one company, Nobre Seguros, in conjunction with Agrobrasil, underwrote a crop area-yield index insurance program in Rio Grande do Sul State for hybrid maize seed, but this state government-subsidized program has not been renewed in 2008/09. The PRAGRO policy is an individual grower MPCI yield shortfall product which covers a wide range of climatic and naturally occurring perils and uncontrollable pests and diseases and which indemnifies losses that exceed 30% of the expected revenue for the insured crop. Table 5.1: Agricultural Insurance Available 2008 Crop Insurance Products Available Greenhouse Forestry MPCI Named-peril Crop Revenue Index-based Yes Yes No Yes, Area-

Yield Index No Yes

Livestock Insurance Products Available Aquaculture All Risk Accident &

Mortality Epidemic Disease

Other Index-based

No Yes No Yes, bloodstock

No No

Source: World Bank Survey (2008). Delivery channels

In Brazil, the key delivery channels for commercial agricultural crop insurance include: (1) local insurance brokers; (2) the banks (for example, Alianca do Brazil, the largest crop insurer, is owned by the Bank of Brazil and has a major crop-credit portfolio); and (3) producer associations and cooperatives, which are very active in Brazil and provide their members with a range of services including credit, input, and output marketing. The Ministry for Agrarian Development (Ministerio de Desenvolvimiento Agrario) delivers coverage through PROAGRO and SEAF to small and marginal Brazilian farmers.

24

Voluntary vs. Compulsory Insurance Private sector agricultural insurance is voluntary in Brazil. The rural banks may, however, require borrowers to take out a crop insurance policy to protect their seasonal crop production loans. The public sector PROAGRO and SEAF crop credit insurance programs are compulsory for crop credit recipients of PRONAF. Agricultural Reinsurance

The IRB acted as a monopoly national reinsurer between 1939 and 2007. The IRB retroceded the agricultural reinsurance business on a quota-share treaty or voluntary proportional basis to specialist international agricultural reinsurers.

In January 2007 legislation5

was enacted to permit foreign reinsurers to enter the Brazilian domestic reinsurance market. International reinsurers, which are registered as fully admitted local reinsurers, may now compete directly with IRB for business. The IRB is now registered as a local reinsurer under the name IRB-Brasil Resseguros S.A.; it is a privately-held mixed capital corporation linked to the Ministry of Finance (it is classified as a public sector reinsurer for the purposes of this survey).

Traditionally, the IRB managed a special government stop-loss reinsurance fund for agriculture termed FESR, Stability Fund for Rural Insurance (Fundo de estabilidade do seguro rural). This fund was open to both public and private agricultural insurers, and COSESP was a major beneficiary up to 2004/05 when the company went into receivership with major financial losses. Although FESR is open to all insurance companies that sell agricultural insurance in Brazil, currently only two companies, Aliança do Brasil and AGF Brazil, are using this fund. Currently, the Government and insurers are studying the possibility of replacing the FESR by another catastrophe reinsurance facility termed the Rural Catastrophe Fund (Fundo do Catástrofe Rural).

In 2008 all the major international commercial agricultural reinsurers6

were operating in Brazil either as local or admitted or alien reinsurers. These reinsurers are offering a mix of facultative proportional reinsurance (especially for large forestry accounts) and quota-share and stop-loss treaty reinsurance to the private commercial agricultural insurers. Access to reinsurance capacity is not considered to be a constraint in Brazil for existing crop hail and MPCI business or for livestock mortality cover.

The PROAGRO crop insurance program is underwritten by the Central Bank of Brazil. It does not attract reinsurance from the IRB or International Reinsurers.

5 Supplementary Law No. 126 of January 2007 recognizes three types of reinsurer in the Brazilian market: (1) Local Reinsurer based in the country and incorporated as a company, (2) Admitted Reinsurer based abroad but with a local office and authorized to conduct reinsurance activities, and (3) Alien Reinsurer based abroad and with no local office in Brazil. 6 This list includes Swiss Re, Munich Re, Partner Re, Hannover Re, SCOR, Mapfre Re, various syndicates at Lloyd’s, and various Bermudan reinsurers.

25

2. Public Support for Agricultural Insurance Types of Public Support for Agricultural Insurance The federal government PROAGRO and SEAF programs provide subsidized crop insurance to the farmers who are automatically insured under these programs. In the case of SEAF, a fixed capped crop insurance premium rate of 2% is charged to the grower, and the government provides a 75% premium subsidy. Since 2004/05, the federal government has also provided premium subsidies to private commercial insurers for crops, livestock, and aquaculture insurance, and recently, in 2007, the premium subsidy program has been extended to forestry.

The federal government has also provided agricultural reinsurance through the national monopoly reinsurer IRB and through FESR. The government is also developing agricultural risk management training and education programs with several universities. Some state-level governments have also provided premium subsides for commercial crop insurance (including Rio Grande do Sul, Sao Paulo, and Minas Gerais).

Subsidies on Private Commercial Agricultural Insurance Premiums The Brazilian government has been very committed to supporting private commercial agricultural insurance since 2005 through the provision of premium subsidies. The following premium subsidy levels were available for each class of insurance in 2007/08:

• Livestock, forestry and aquaculture: 30% premium subsidy • Crops (cereals, fruits, etc.): 40%-60% premium subsidy • The maximum permitted premium subsidy per farmer was R$ 32,000 for each insurance group

(three crop groups, livestock, forestry; six groups in total), or a maximum of R$ 192,000 for all groups.

In 2008/09 the maximum premium subsidy level has been increased to 70 percent, and the subsidy limit per farmer has been increased to R$ 96,000.

The budgeted premium subsidy amounts of the federal government and utilization by commercial agricultural insurers are presented in Table 5.4 for the period 2005/06 to 2007/08. There has been a major expansion in agricultural insurance premiums and in the federal government’s premium subsidy budget in the past three years. In 2005/06, the total market premium amounted to only USD 18 million, with used premium subsidies amounting to about USD 111,111. In 2007/08, the government’s allocated premium subsidy budget amounted to R$ 100 million (USD 55.6 million): actual written premiums increased to USD 73.3 million (a three-fold increase in three years), and premium subsidies amounted to USD 33.9 million or 46% of premiums.

The government has budgeted agricultural insurance premium subsidies for 2008/09 of R$ 150 million (USD 94 million), and for 2009/10 of R$ 200 million.

26

3. Agricultural Insurance Penetration Insurance Penetration Rate Commercial Agricultural Insurance. The Brazilian insurance market generated R$58.6 billion (USD 30 billion) in written premiums during 2007 and about R$ 70 million (USD 36 billion) with the inclusion of health insurance, equivalent to about 3.7% of GDP7

. Agricultural production in 2007 amounted to about 3.5% of GDP, but private commercial company agricultural insurance premiums were only USD 73.3 million or 0.2% of total market premium.

In 2007 a total of 2.27 million hectares of crops were insured by private commercial insurers in Brazil, representing 2.6% of total cropped area of the insured crops. The bulk of the insured cropped area was comprised of cereals and textile crops (Table 5.5).

Livestock insurance uptake is exceedingly low in Brazil. After a decade of livestock insurance it is estimated that in 2007 there were only about 6,000 insured head of cattle out of a total national herd of nearly 206 million, and bloodstock insurance accounts for a further estimated 2,000 animals (Table 5.6).

In 2007/08 the Brazilian commercial agricultural insurance market TSI for crops, forestry, and livestock was estimated at USD 1.53 billion, with premiums of USD 73.2 million and an average rate of 4.8%. Agricultural insurance is currently purchased by medium and larger commercial farmers with an average sum insured of nearly USD 49,000 and average premium of nearly USD 2,250 per policy.

Public Sector Crop Insurance. It is not possible to report the results for the public sector

programs. It is understood that PROAGRO is currently insuring more than one million farmers. In 2004/05, the first year of operation of SEAF, 543,800 farmers were insured under this crop credit insurance program with a TSI of R$ 2.5 billion8

4. Financial Performance

, and currently it is understood that more than 600,000 smallholders are insured under SEAF.

5-Year Results

The Brazilian private commercial market crop insurance results for the past 4 years are reported in Table 5.8. On account of the major injection of premium subsidies by the Brazilian government, the demand for crop insurance has nearly doubled (in terms of premium volume) in the last two years, and in 2007/08 it stood at USD 73.0 million. In 2004/05 Brazil experienced severe drought, and companies underwriting MPCI incurred major losses as shown by the overall loss ratio of 263%. The market for crop insurance shrank in 2005/06 due to the collapse of COSESP (former public-sector agricultural insurer in Sao Paulo) and also Alianca do Brazil’s decision to highly restrict its underwriting in that year. 2005/06 was also a severe drought year in southern Brazil. The 4-year long term loss ratio at end of 2007/08 was 81% against an average annual loss ratio of 109%.

7 IRB-BrasilRe Annual Report 2007. 8 Zukowski J C 2008, Gestao de Riscos na agricultura familiar: Interccao entre o SEAF e o Sistema de ATER. www.mda.gov.br/saf/arquivos/0806509632.pdf.

27

The market livestock insurance results are not available. It is not possible to report the underwriting results for PRAGRO, PROAGRO MAIZ or SEAF over the past five years.

Cost of Agricultural Insurance Provision

Typical or average commercial insurers’ market acquisition costs and administration costs are reported in Table 5.9 for crops and livestock. 5. Public Disaster Assistance Programs Stability Fund for Rural Insurance FESR (Fundo de estabilidade do seguro rural)

As noted above, the IRB traditionally managed the FESR. This voluntary catastrophe reinsurance fund for agricultural classes of insurance provides stop-loss reinsurance for the following layering:

• Layer 1: losses from a 100% loss ratio up to 150% loss ratio, and • Layer 2: all losses exceeding a 250% loss ratio.

FESR is funded from a range of sources, including the underwriting profits of the agricultural insurers, the underwriting profits of the Penhor Rural program, and finally through federal government support in the event that the funds are inadequate to settle claims. In 2007 the government appointed a working group to study proposals to replace FESR by a Rural Catastrophe Fund (Fundo de Catástrofe Rural).

PROAGRO and SEAF

Since 1954 the federal government of Brazil has operated through the Central Bank of Brazil a subsidized crop credit insurance program called PROAGRO. In 2004/05, SEAF, a special crop credit insurance program for smallholder farmers was initiated by the Secretariat of Family Agriculture (Secretaria de Agricultura Familiar) and the Ministry of Agrarian Development (Ministério do Desenvolvimento Agrário). Features of this program are included in Box 5.1.

28

Box 5.1: SEAF Crop-Credit Insurance Program of the Federal Government of Brazil

SEAF is a federal government of Brazil compulsory crop credit insurance program for smallholder farmers who access seasonal production credit from PRONAF (National Program for the Strengthening of Family Agriculture – Programa Nacional de Fortalecimento da Agricultura Familiar). Nature of Cover: Automatic cover for beneficiaries of PRONAF Seasonal Credit. Type of Policy: Multi-Peril Yield Shortfall Policy, which indemnifies growers by the amount that actual crop revenue falls short of the sum insured (see below for definition of sum insured). Insured Crops: A wide range of crops identified under the agricultural zoning program (zoneamento agricola), including rainfed and irrigated cereals, legumes, oilseeds, fiber crops, root crops (cassava), grapes, and tree fruits. Insured perils: Drought, excess rain, frost, hail, excess variation in temperatures, strong winds, cold winds, crop pests, and diseases which are uncontrollable either technically or economically. Basis of Sum Insured: The sum insured is based on the amount of seasonal production credit loaned to the farmer, plus the interest due on the principal, plus up to 65% of the estimated net revenue of the crop, subject to a maximum of R$ 2,500 per farmer. The estimated gross and net revenue are determined by the bank and the crop inspector at the time of policy issuance. Premium Rate: 2% fixed rate paid by the insured for each insured crop. Premium Subsidy: Government pays a 75% premium subsidy on the SEAF program. Basis of Indemnity: Losses must exceed 30% of the expected gross revenue for the crop in order to qualify for an indemnity.

Indemnity Examples:

Item Farmer 1 Farmer 2 Sum Insured (R$) (R$) Finance (Seasoned Production Credit) 3,000 8,000 Expected Gross Return 5,000 13,000 Net Return (Gross – Finance) 2,000 5,000 65% of Net Return or Cap of R$2,500 1,300 2,500 Sum Insured (Finance + 65% Net Return) 4,300 10,500 Claims Example 1: Total (100%) Loss Prior to Harvest, Part of Credit Not Utilized Sum Insured 4,300 10,500 Minus Saving in Credit Not Utilized -750 -2,000 Indemnity Payment 3,550 8,500 Claims Example 2: Partial Loss (50% of Gross Revenue) Sum Insured 4,300 10,500 Minus Actual Gross Revenue Obtained (50%) -2,500 -6,500 Indemnity Payment 1,800 4,000 Source: MDA, 17/08/2005: Seguro da Agricultura Familiar.

29

6. Additional Tables Table 5.2: Main Private Commercial Agricultural Insurance Companies 2007

Company Premium (USD million)

Market Share

Allianz 1.2 1.7% Aliança do Brasil 37.4 51.0%

Mapfre Seguros 9.3 12.7% Nobre Seguros 16.1 22.0%

Porto Seguro 0.2 0.2% Seguradora Brasileira Rural,

SBR 9.1 12.4% Total 73.3 100.0%

Source: World Bank Survey (2008).

Table 5.3: Type of Agricultural Insurance Product by Private Company Ceding Company Fruit/Hail Grains/MPCI Forestry Livestock Bloodstock Farm

Owners Allianz X X X Aliança do Brasil X X Itaú Seguros* X X X Mapfre Seguros X X X X Nobre Seguros X X Porto Seguro X X Seguradora Brasileira Rural, SBR

X X X X X X

Unibanco X X Source: World Bank Survey (2008). * Itaú operates as fronting in MPCI for Archer Daniel Midland's coverage.

Table 5.4: Agricultural Insurance Premium Subsidy Budget and Use, FY2005 to FY2007

Season Available Subsidy

(USD million) Used Subsidy (USD million)

Percentage Subsidy Used

Total Premium (USD million)

Subsidy as Percent of Premium

FY2006 1.7 0.1 7% 18.0 0.6% FY2007 33.3 17.6 53% 38.0 46.3% FY2008 55.6 33.9 61% 73.3 46.2%

Source: World Bank Survey (2008).

30

Table 5.5: Estimated Policy Sales and Insured Area by Crop Type FY2008

Type of Crop Number of

Policies* Planted Area

(milion ha) Insured Area (ha)

Percent of National

Crop Area Insured

Coffee 21 2.3 369 .. Forestry 100 5.8 99,309 1.7%

Fruits 5,974 1.1 35,920 3.3% Grains-Textile 24,033 49.0 2.1 mil 4.4%

Horticulture 821 29.0 5,409 .. Tobacco 0 0.5 0 0%

Total 30,949 87.7 2.3 mil 2.6% Source: World Bank Survey (2008). * In addition there were 455 policy sales for sugar cane, making a total of 31,404.

Table 5.6: Estimated Private Livestock Insurance Penetration FY2008

Species National Stock Insured Livestock Market Penetration Livestock 205.9 mil 6,000 .. Bubaline 1.2 mil 0 0%

Bloodstock 5.7 mil 2,000 0.03% Sheep 16.0 mil 1,000 0.01%

Poultry 1,013.2 mil 0 0% Pork 35.2 mil 0 0%

Source: World Bank Survey (2008). Table 5.7: Commercial Share of TSI and Premium by Crop Type FY2008

Type of Crop

Number of

Policies

TSI (USD

million)

Total Premium

(USD million)

Average Premium

Rate

Average Sum Insured

(USD)

Average Premium

(USD) Coffee 21 1.1 0.02 2.2% 53,416 1,161

Forestry 100 98.4 1.5 1.6% 983,527 15,278 Fruits 5,974 319.6 21.2 6.6% 53,493 3,544

Grains-Textile 24,033 1,010.9 45.1 4.5% 42,064 1,876 Horticulture 821 42.1 2.2 5.2% 51,339 2,652 Livestock & Bloodstock 1,645* 56.2 3.3 5.9% 34,190 2,004

Total 32,594 1,528.4 73.3 4.8% 46,891 2,248 Source: World Bank Survey (2008). * Estimated number of livestock policies

31

2007/08 PREMIUM DISTRIBUTION (%)

Grains-Textile63%

Fruits29%

Livestock & Bloodstock

3%Forestry

2%Horticulture3%

Table 5.8: Private Commercial Crop Insurance Results, 2004 to 2007

Year Sum Insured* (USD million)

Premium (USD million)

Claims (USD million) Loss Ratio

2004 494.3 23.7 62.3 263% 2005 323.3 15.5 15.2 98% 2006 813.4 39.0 11.0 28%

2007** 1,528.4 73.0 34.0 47% Total 3,159.4 151.2 122.5 81%

Annual Average 789.9 37.8 30.6 109% Source: World Bank Survey (2008). * TSI values not available; estimations made on average premium rates for 2007 of 4.8% ** 2007 estimated claims and loss ratio

Premium Claims L/R

32

Table 5.9: Insurers’ A&O Costs as a Percent of OGP Costs Crop Livestock

Marketing & Acquisition 10% 25% Administration 23% 25%

Loss Adjustment 3% 2%

Total 36%

52% Source: World Bank Survey (2008). Note: In both cases, insurance premium taxes were negligible and were therefore not included. Appendix 1: Superintendência de Seguros Privados (SUSEP) Historical Crop Insurance Results, FY1996 to FY2005

Year

Premium (USD

million)

Claims (USD

million) Loss Ratio FY1996 5.0 4.4 89.2% FY1997 6.0 3.0 48.9% FY1998 7.8 9.3 119.4% FY1999 9.9 6.4 65.1% FY2000 20.0 18.8 94.2% FY2001 14.9 67.4 451.5% FY2002 13.1 29.8 226.9% FY2003 13.0 2.0 15.5% FY2004 12.0 33.3 277.3% FY2005 14.9 30.2 202.3%

Total 254.5 483.4 190.0% Source: World Bank Survey (2008).

89%49%

119%

65%94%

452%

227%

16%

277%

202

Source of Country Overview Information: World Bank Survey (2008).

33

Overview on Agricultural Insurance: BULGARIA

1. Agricultural Insurance Market Review History of Agricultural Insurance

An agricultural insurance law on voluntary crop insurance was adopted in Bulgaria in 1910. From 1910 until 1935 agricultural insurance services were offered only by the Bulgarian Cooperative Bank. From 1935 to 1946 crop insurance was administered by the Bulgarian Agricultural and Cooperative Bank. The State Insurance Institute (DZI) was established in 1946, and this institution was appointed as the responsible authority for crop insurance.

Over time Bulgaria has tested different forms of agricultural insurance including mandatory, voluntary, and mixed systems. From 1980 to 1991 agricultural insurance was mandatory for farmers, but the system was abolished after the end of the socialist system. The insurance coverage under the mandatory agricultural insurance framework included protection against a wide list of risks numbering approximately 40 perils.

In 1992 crop insurance became voluntary. Initially, crop policies provided coverage against two risks – hail and storm. Later the list of perils was extended to include excessive rain, fire, frost, and floods. Coverage for winter crops also includes freeze, slush, and water accumulation risks. Agricultural Insurance Market Structure

Seven insurance companies offer crop insurance. The market is dominated by three insurance companies including DZI-Obsto zastrahovane, Allianz Bulgaria, and Vitosha. The market is competitive, though competition is mostly price-based. Premium rates are calculated by actuaries, but rates are subject to approval by the Financial Supervision Commission. The latter organization has a right to revise the premium rates, and in case they are inadequate, sanctions can be applied to the companies using incorrect pricing policies. In 2005, total crop insurance premium was estimated at US$ 7.9 million.

All insurers use statistical data of the DZI, which has collected insurance-related data for the last 50 years.

Four companies offer livestock insurance. Many companies declare that they have livestock insurance products developed, but actual transactions are rare. The active players in the livestock insurance segment are DZI-Obsto zastrahovane, Vitosha, Allianz Bulgaria, and Bulstrad. In 2005 the premium sum on livestock insurance amounted to USD 1.8 million.

Official information on the agricultural insurance market is not available. Crop insurance is included in the general statistical reports on fire and the natural calamities insurance class. Livestock insurance is included in the reports on property insurance.

Agricultural Insurance Products Available