Country by Country Reporting and its challenges. What steps need to be taken?

20

Country by country reporting – The transparent company Ralph Bohr, SCHOTT AG, 20 th October, 2014

-

Upload

torben-haagh -

Category

Business

-

view

146 -

download

0

Transcript of Country by Country Reporting and its challenges. What steps need to be taken?

Country by country reporting – The transparent company

Ralph Bohr, SCHOTT AG, 20th October, 2014

SCHOTT Konzern

© SCHOTT AG

Agenda

© SCHOTT AG

1. SCHOTT - at a glance

2. BEPS-Action plan

3. Revision OECD TP-Guidelines Chapter V (Documentation)

2

Ralph Bohr, IQPC, Oktober 2014

SCHOTT Konzern

© SCHOTT AG © SCHOTT AG

Segments and Business areas

SCHOTT at a glance

Precision Materials Optical Industries

3

Ralph Bohr, IQPC, Oktober 2014

Home Appliances

Home Tech Pharmaceutical Systems Advanced Optics

Flat Glass Electronic Packaging Lighting and Imaging

SCHOTT Konzern

© SCHOTT AG © SCHOTT AG

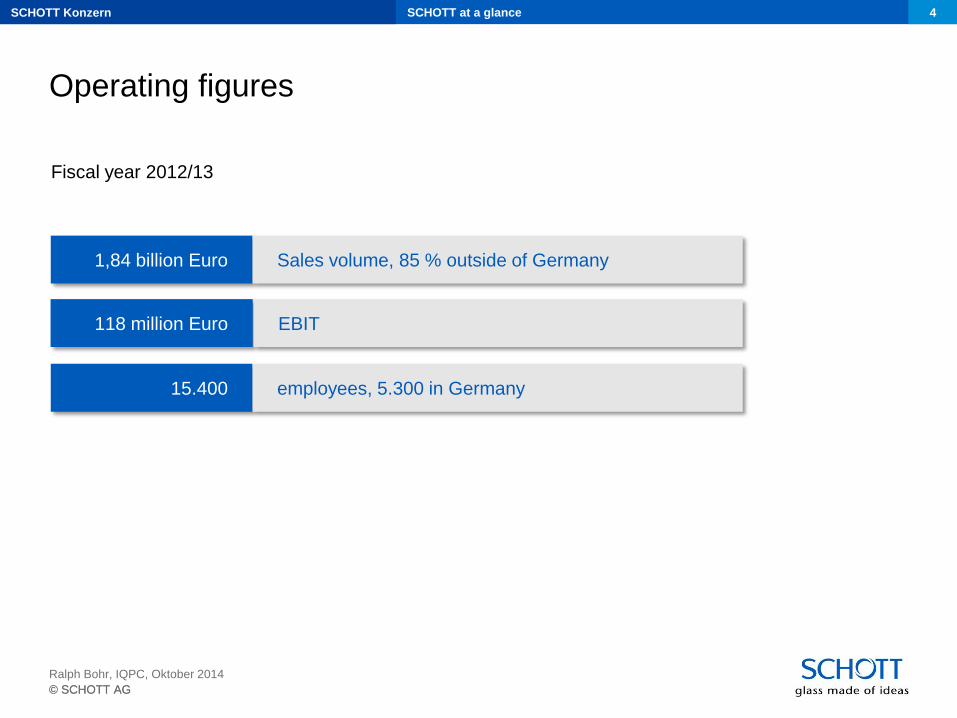

Operating figures

SCHOTT at a glance

Fiscal year 2012/13

15.400

1,84 billion Euro

118 million Euro

Sales volume, 85 % outside of Germany

employees, 5.300 in Germany

4

EBIT

Ralph Bohr, IQPC, Oktober 2014

SCHOTT Konzern

© SCHOTT AG © SCHOTT AG

Close to customers

worldwide

SCHOTT at a glance

Ralph Bohr, IQPC, Oktober 2014

5

Europe Denmark Croatia Sweden

Germany Netherlands Switzerland

France Austria Spain

Great Britain Poland Czech Republic

Italy Russ. Federation Turkey

Hungary

South America Argentina

Brasil

Columbia

North America Canada

Mexico

USA

Asien China

Dubai

India

Indonesia

Israel

Japan

Malaysia

Singapore

South Korea

Taiwan

Thailand

Production facilities Sales Offices

Africa Tunisia

Australia

SCHOTT Konzern

© SCHOTT AG

Agenda

© SCHOTT AG

1. SCHOTT at a glance

2. BEPS-Action plan

3. Revision OECD TP-Guidelines Chapter V (Documentation)

6

Ralph Bohr, IQPC, Oktober 2014

SCHOTT Konzern

© SCHOTT AG © SCHOTT AG

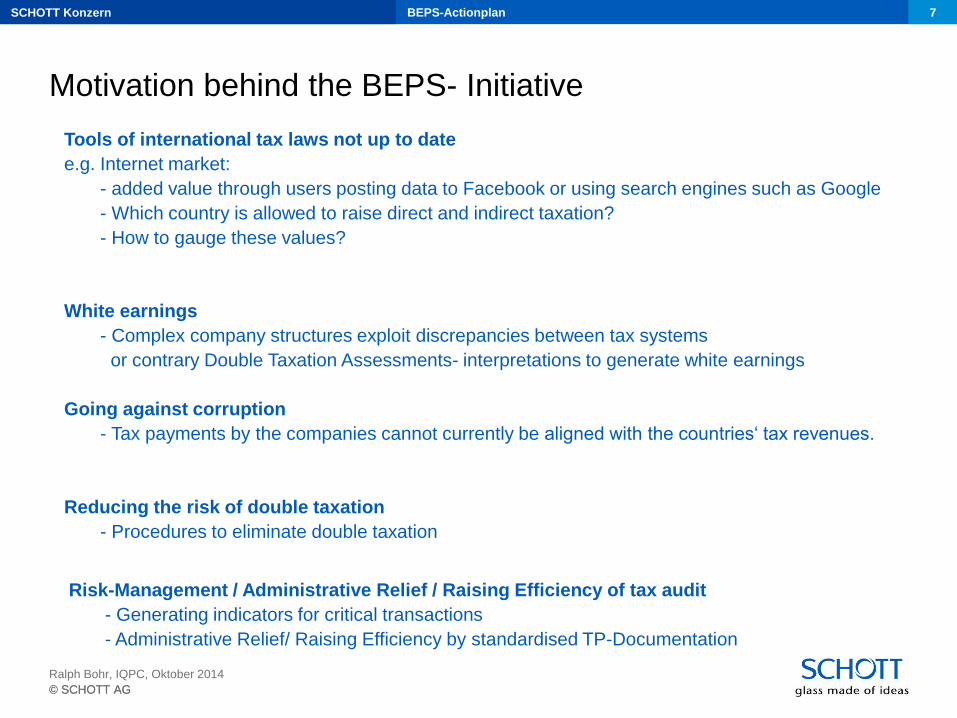

Motivation behind the BEPS- Initiative

BEPS-Actionplan 7

Tools of international tax laws not up to date

e.g. Internet market:

- added value through users posting data to Facebook or using search engines such as Google

- Which country is allowed to raise direct and indirect taxation?

- How to gauge these values?

White earnings

- Complex company structures exploit discrepancies between tax systems

or contrary Double Taxation Assessments- interpretations to generate white earnings

Going against corruption

- Tax payments by the companies cannot currently be aligned with the countries‘ tax revenues.

Reducing the risk of double taxation

- Procedures to eliminate double taxation

Risk-Management / Administrative Relief / Raising Efficiency of tax audit

- Generating indicators for critical transactions

- Administrative Relief/ Raising Efficiency by standardised TP-Documentation

Ralph Bohr, IQPC, Oktober 2014

SCHOTT Konzern

© SCHOTT AG © SCHOTT AG

BEPS- Actionplan (Juli 2013, OECD, G-20)

Base Erosion and Profit Shifting

Action 3

Action 1

Action 2

Digital Economy

CFC- Regimes

8

Hybrid Mismatch

Action 4 Financial Payments

Action 5 Harmful Tax Practices

Action 6 Treaty Abuse

Action 7 Permanent Establishment Status

Action 8 Transfer Pricing and Intangibles

Action 9 Transfer Pricing and Risks / Capital

Action 10 Transfer Pricing and other High Risk Transactions

Action 11 Data and Methodologies

Action 12 Disclosure of Aggressive Tax Planning

Action 13

Action 14 Dispute Resolution Mechanisms

Action 15 A Multilateral Instrument

BEPS-Actionplan

Ralph Bohr, IQPC, Oktober 2014

Deadlines

09 /2014

09 / 2014

09 / 2015

9/15 - 12/15

9/14 - 9/15 - 12/15

09 / 2014

09 / 2015

9/14 – 9/15

09 / 2015

09 / 2015

09 / 2015

09 / 2015

09 / 2014

09 / 2015

9/14 - 12/15

Transfer Pricing Documentation / CbC- Reporting

SCHOTT Konzern

© SCHOTT AG

Agenda

© SCHOTT AG

1. SCHOTT at a glance

2. BEPS-Actionplan

3. Revision OECD TP-Guidelines Chapter V (Documentation)

9 Revision OECD TP-Richtlinien Kap. V (Dokumentation)

Ralph Bohr, IQPC, Oktober 2014

SCHOTT Konzern

© SCHOTT AG

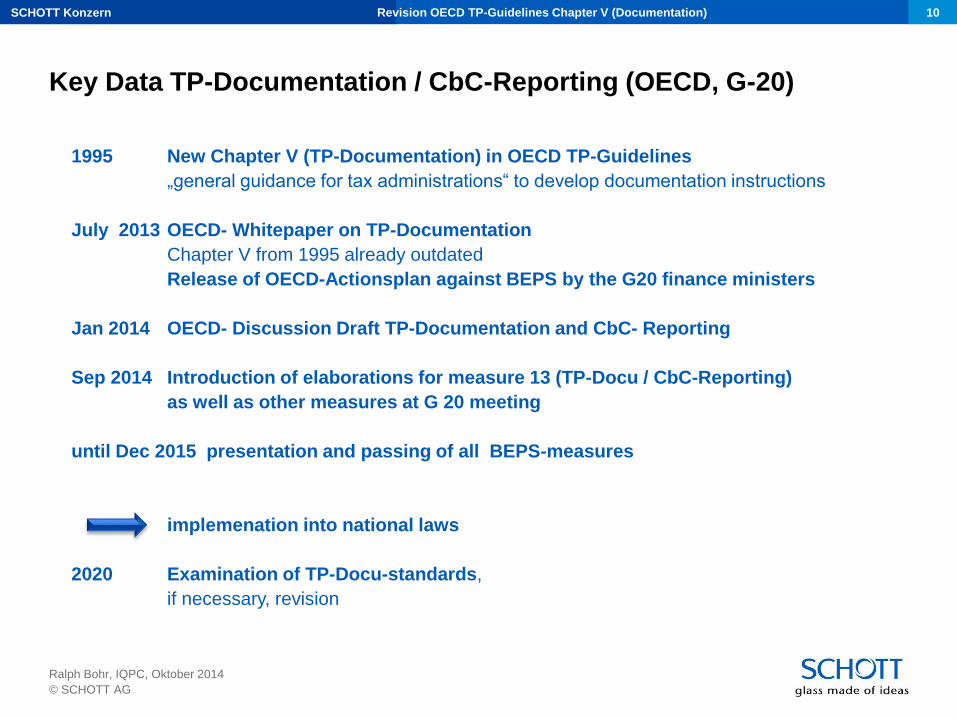

Key Data TP-Documentation / CbC-Reporting (OECD, G-20)

10 Revision OECD TP-Guidelines Chapter V (Documentation)

1995 New Chapter V (TP-Documentation) in OECD TP-Guidelines

„general guidance for tax administrations“ to develop documentation instructions

July 2013 OECD- Whitepaper on TP-Documentation

Chapter V from 1995 already outdated

Release of OECD-Actionsplan against BEPS by the G20 finance ministers

Jan 2014 OECD- Discussion Draft TP-Documentation and CbC- Reporting

Sep 2014 Introduction of elaborations for measure 13 (TP-Docu / CbC-Reporting)

as well as other measures at G 20 meeting

until Dec 2015 presentation and passing of all BEPS-measures

implemenation into national laws

2020 Examination of TP-Docu-standards,

if necessary, revision

Ralph Bohr, IQPC, Oktober 2014

SCHOTT Konzern

© SCHOTT AG © SCHOTT AG

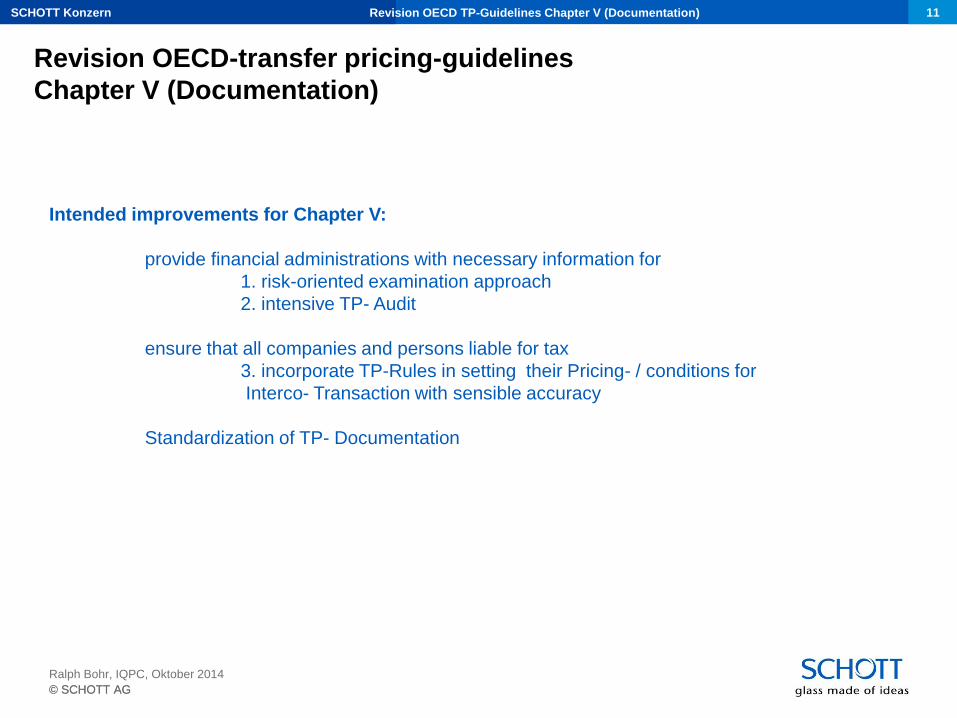

Intended improvements for Chapter V:

provide financial administrations with necessary information for

1. risk-oriented examination approach

2. intensive TP- Audit

ensure that all companies and persons liable for tax

3. incorporate TP-Rules in setting their Pricing- / conditions for

Interco- Transaction with sensible accuracy

Standardization of TP- Documentation

Revision OECD TP-Guidelines Chapter V (Documentation) 11

Ralph Bohr, IQPC, Oktober 2014

Revision OECD-transfer pricing-guidelines

Chapter V (Documentation)

SCHOTT Konzern

© SCHOTT AG © SCHOTT AG

Revision OECD TP-Guidelines Chapter V (Documentation) 12

Ralph Bohr, IQPC, Oktober 2014

Revision OECD-transfer pricing-guidelines

Chapter V (Documentation)

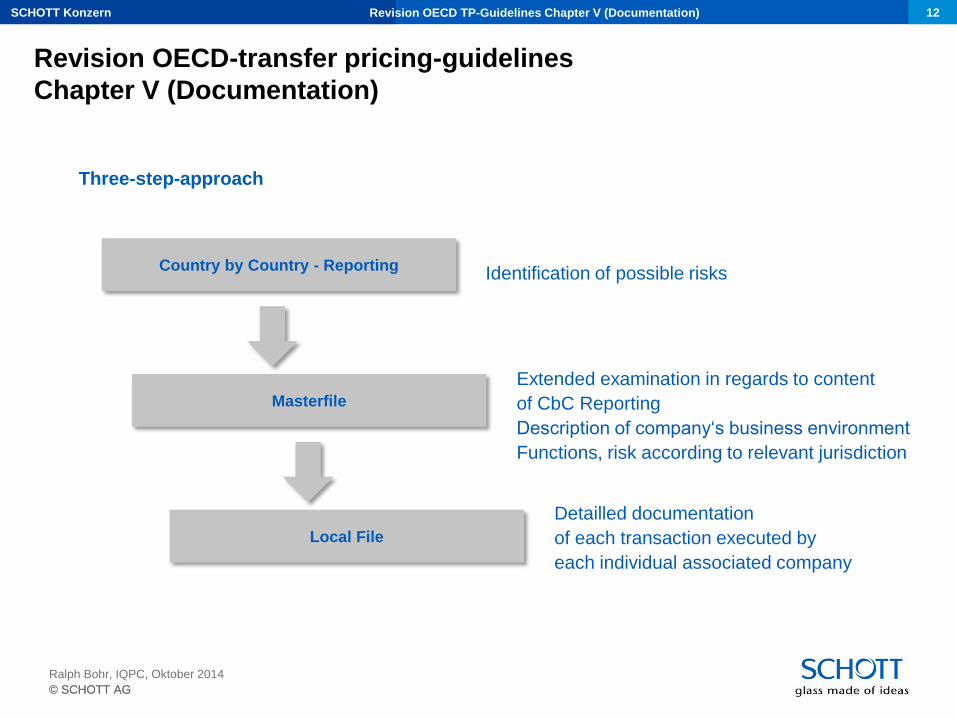

Three-step-approach

Country by Country - Reporting Identification of possible risks

Masterfile

Extended examination in regards to content

of CbC Reporting

Description of company‘s business environment

Functions, risk according to relevant jurisdiction

Local File

Detailled documentation

of each transaction executed by

each individual associated company

SCHOTT Konzern

© SCHOTT AG

TP- Documentation: Country by Country- Reporting (1/3)

Revision OECD TP-Guidelines Chapter V (Documentation)

Table 1: Overview of

distribution of income,

taxation,

corporate activities

for each tax jurisdiction

Name of Tax Jurisdiction

• Revenues

• - unrelated parties

• - related parties

• Profit (Loss) before Income Tax

• Income Tax Paid (on cash basis)

• Income Tax Accrued – Current Year

• Stated Capital and Accumulated Earnings

• Number of Employees

• Tangible Assets (Net book value)

Ralph Bohr, IQPC, Oktober 2014

Tabular Query

SCHOTT Konzern

© SCHOTT AG

TP- Documentation: Country by Country- Reporting (2/3)

Revision OECD TP-Guidelines Chapter V (Documentation)

Tax Jurisdiction

Constituent Entities per Tax Jurisdiction

Corporate activites per CE

1. R&D

2. Holding / Managing IP

3. Purchasing, Procurement

4. Manufacturing, Production

5. Sales, Marketing, Distribution

6. Admin, Management, Support Services

7. Provision of Services to Unrelated Parties

8. Internal Group Finance

9. Regulated Financial Services

10. Insurance

11. Holding Shares or other equity instruments

12. Dormant

13. Other

Ralph Bohr, IQPC, Oktober 2014

Table 2: Corporate activities

for all Constituent Entities

Tabular Query

SCHOTT Konzern

© SCHOTT AG

TP- Documentation: Country by Country- Reporting (3/3)

Revision OECD TP-Guidelines Chapter V (Documentation)

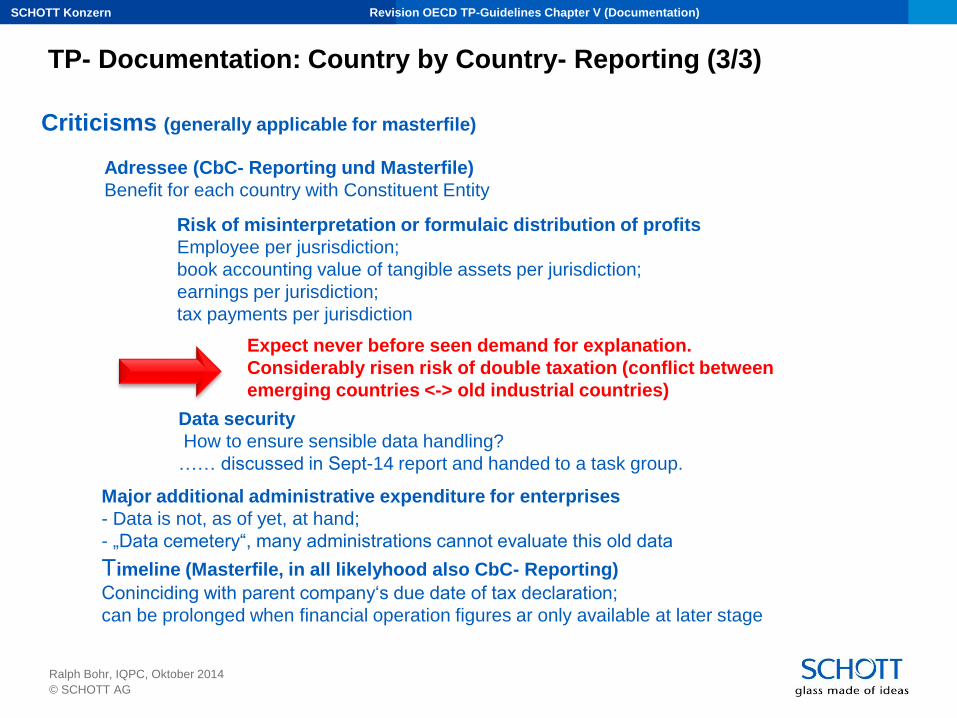

Adressee (CbC- Reporting und Masterfile)

Benefit for each country with Constituent Entity

Timeline (Masterfile, in all likelyhood also CbC- Reporting)

Coninciding with parent company‘s due date of tax declaration;

can be prolonged when financial operation figures ar only available at later stage

Major additional administrative expenditure for enterprises

- Data is not, as of yet, at hand;

- „Data cemetery“, many administrations cannot evaluate this old data

Data security

How to ensure sensible data handling?

…… discussed in Sept-14 report and handed to a task group.

Ralph Bohr, IQPC, Oktober 2014

Risk of misinterpretation or formulaic distribution of profits

Employee per jusrisdiction;

book accounting value of tangible assets per jurisdiction;

earnings per jurisdiction;

tax payments per jurisdiction

Expect never before seen demand for explanation.

Considerably risen risk of double taxation (conflict between

emerging countries <-> old industrial countries)

Criticisms (generally applicable for masterfile)

SCHOTT Konzern

© SCHOTT AG

TP- Documentation: Master File (1/2)

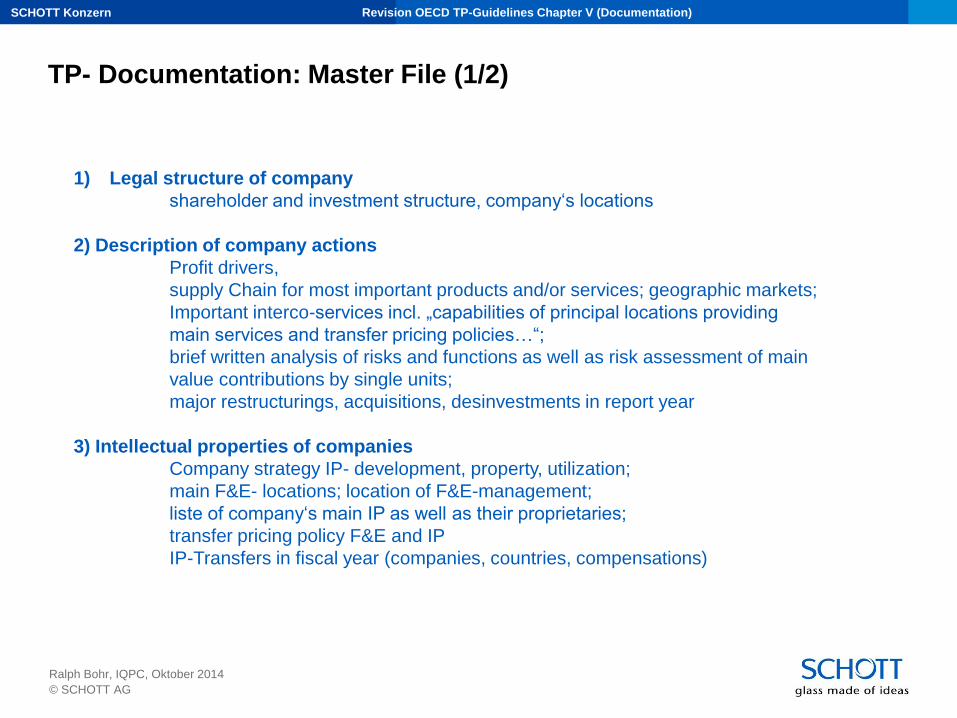

1) Legal structure of company

shareholder and investment structure, company‘s locations

2) Description of company actions

Profit drivers,

supply Chain for most important products and/or services; geographic markets;

Important interco-services incl. „capabilities of principal locations providing

main services and transfer pricing policies…“;

brief written analysis of risks and functions as well as risk assessment of main

value contributions by single units;

major restructurings, acquisitions, desinvestments in report year

3) Intellectual properties of companies

Company strategy IP- development, property, utilization;

main F&E- locations; location of F&E-management;

liste of company‘s main IP as well as their proprietaries;

transfer pricing policy F&E and IP

IP-Transfers in fiscal year (companies, countries, compensations)

Revision OECD TP-Guidelines Chapter V (Documentation)

Ralph Bohr, IQPC, Oktober 2014

SCHOTT Konzern

© SCHOTT AG

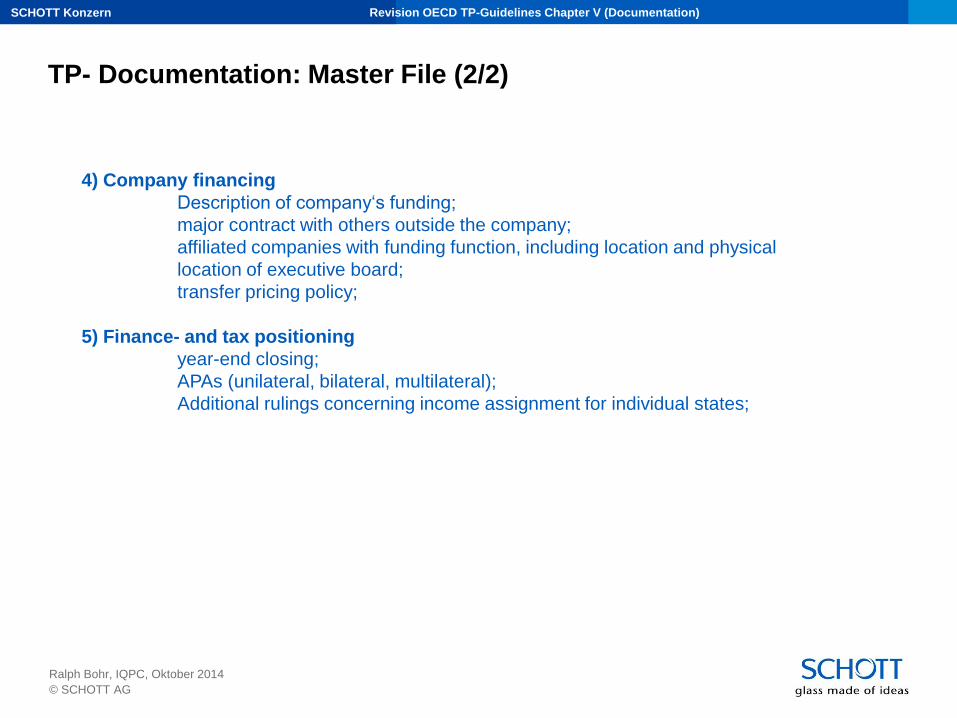

TP- Documentation: Master File (2/2)

4) Company financing

Description of company‘s funding;

major contract with others outside the company;

affiliated companies with funding function, including location and physical

location of executive board;

transfer pricing policy;

5) Finance- and tax positioning

year-end closing;

APAs (unilateral, bilateral, multilateral);

Additional rulings concerning income assignment for individual states;

Revision OECD TP-Guidelines Chapter V (Documentation)

Ralph Bohr, IQPC, Oktober 2014

SCHOTT Konzern

© SCHOTT AG

TP- Documentation: Local File (1/2)

1) Local businesses

Management-structure, Organisational-Chart, report guidelines

incl. superiors in countries;

restructurings; IP-Transfers

Revision OECD TP-Guidelines Chapter V (Documentation)

3) Financial key figures

Financial statements ;

transition between financal key figures relevant for TP-guidelines (e.g. IFRS)

and the company‘s annual financial statement;

financial key figures of comparable companies with sources

Ralph Bohr, IQPC, Oktober 2014

2) Intercompany-transactions

description and context;

volume of each Interco-transaction,

companies to which Interco-transactions exist;

function and risk analysis of each transaction type;

selection of most suitable TP-method;

assignment of tested party per transaction;

List and description of outside comparison transaction;

adjustment calculations;

assessment of Interco- transactions were common for outside comparison;

overview over relevant key data for TP- guidelines

SCHOTT Konzern

© SCHOTT AG

TP- Documentation: Local File (2/2)

Revision OECD TP-Guidelines Chapter V (Documentation)

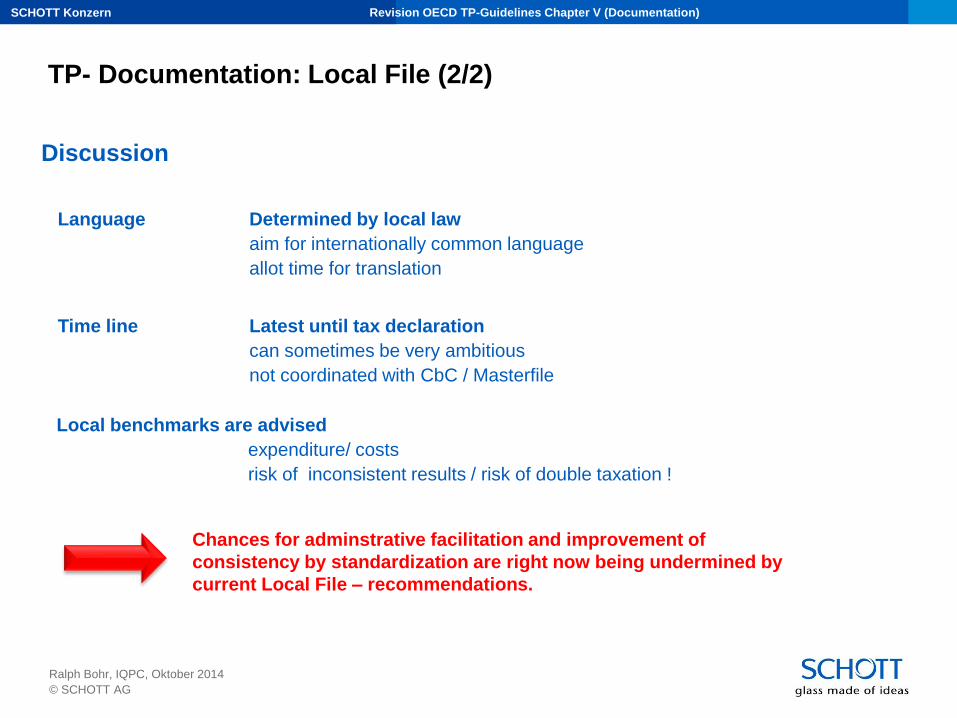

Language Determined by local law

aim for internationally common language

allot time for translation

Time line Latest until tax declaration

can sometimes be very ambitious

not coordinated with CbC / Masterfile

Local benchmarks are advised

expenditure/ costs

risk of inconsistent results / risk of double taxation !

Ralph Bohr, IQPC, Oktober 2014

Discussion

Chances for adminstrative facilitation and improvement of

consistency by standardization are right now being undermined by

current Local File – recommendations.

SCHOTT Konzern

© SCHOTT AG © SCHOTT AG

20

Ralph Bohr, IQPC, Oktober 2014

The future will be exciting!