COTTON AND CASSAVA SEED SYSTEMS - Home | Food … · COTTON AND CASSAVA SEED SYSTEMS Malawi,...

29

FOOD AND AGRICULTURAL ORGANIZATION (ZIMBABWE) COTTON AND CASSAVA SEED SYSTEMS Malawi, Mozambique and Zambia Dr Vincent Gwarazimba 9/1/2009 Cotton and cassava are significant crops in the agriculture of Malawi, Mozambique and Zambia. Cotton sectors in the three countries are characterised by unregulated and local monopolies with prices often determined by the dominant cotton companies. Government intervention on prices, for instance in Malawi set lint prices too high for ginners. Production is based on out grower smallholder farmer schemes, ginners giving inputs to farmers. Cotton seed is produced by the same ginners, compromising quality of seed and often varieties are mixed as seed is often recycled. The seed system is therefore informal. In Malawi and Mozambique, there is no government involvement in cotton seed production while in Zambia government is involved through the Seed Control and Certification Institute (SCCI), prescribing procedures of cotton seed production. All cotton seed marketed in the three countries is fuzzy seed. There is no guarantee of quality of seed. Lack of quality seed compromises farmers’ yields and profitability of cotton. Cassava is now recognized as a food security crop. However, cassava production is constrained by lack of quality planting material. Governments are now formulating policies to create sustainable production, promoting food processing and industrial use of cassava.

Transcript of COTTON AND CASSAVA SEED SYSTEMS - Home | Food … · COTTON AND CASSAVA SEED SYSTEMS Malawi,...

FOOD AND AGRICULTURAL ORGANIZATION (ZIMBABWE)

COTTON AND CASSAVA

SEED SYSTEMS Malawi, Mozambique and Zambia

Dr Vincent Gwarazimba

9/1/2009

Cotton and cassava are significant crops in the agriculture of Malawi, Mozambique and Zambia.

Cotton sectors in the three countries are characterised by unregulated and local monopolies with

prices often determined by the dominant cotton companies. Government intervention on prices, for

instance in Malawi set lint prices too high for ginners. Production is based on out grower smallholder

farmer schemes, ginners giving inputs to farmers. Cotton seed is produced by the same ginners,

compromising quality of seed and often varieties are mixed as seed is often recycled. The seed system

is therefore informal. In Malawi and Mozambique, there is no government involvement in cotton

seed production while in Zambia government is involved through the Seed Control and Certification

Institute (SCCI), prescribing procedures of cotton seed production. All cotton seed marketed in the

three countries is fuzzy seed. There is no guarantee of quality of seed. Lack of quality seed

compromises farmers’ yields and profitability of cotton. Cassava is now recognized as a food security

crop. However, cassava production is constrained by lack of quality planting material. Governments

are now formulating policies to create sustainable production, promoting food processing and

industrial use of cassava.

2

This paper has been commissioned by FAO under the All ACP Agricultural Commodities

Programme

The EU-funded All ACP Agricultural Commodities Programme (AAACP) is an interagency initiative

being implemented by the Food and Agriculture Organization of the United Nations (FAO), the

Common Fund for Commodities (CFC), the International Trade Centre (ITC), the United Nations

Conference on Trade and Development (UNCTAD) and The World Bank. This four-year programme

will end in December 2011.

The overall objective of the AAACP is to reduce income vulnerability and improve the livelihoods of

producers dependent on agricultural commodities - in the Africa, Caribbean and Pacific regions (ACP)

- by building the capacity of actors along commodity chains to develop and implement sustainable

value chain strategies.

Within FAO, the AAACP is being implemented by the Trade and Markets Division (EST), the Rural

Infrastructure and Agro-Industries Division (AGS), and the Plant Production and Protection Division

(AGP). Each division has the responsibility of the implementation of the following four outcomes:

1. Improve the capacity of chain actors to develop and implement national commodity

strategies

2. Improve access to markets, factors of production and services

3. Develop and enhance access to instruments to reduce producers’ income vulnerability

4. Capitalize on the synergies of International Organizations, EU and ACP actors in the area of

agricultural commodities

3

List of Tables

Table 1 Zoning of crop production in Malawi

Table 2 Distribution of crop production in Mozambique

Table 3 Cotton production in some SADC countries in 2000/01

Table 4 Cotton lint and seed (oil and stock feed) production in Malawi 1992-2002

Table 5 Main cotton varieties and the regions they grow in Malawi

Table 6 Concessions for cotton companies in Mozambique

Table 7 Total cotton production in Mozambique 2001-2008

Table 8 Trends in annual cotton production (mt) in Zambia 2005-09

Table 9 Seed Companies and crops in Malawi, Mozambique and Zambia

Table 10 Seed companies and major crops in Mozambique

Table 11 Percentage use of quality seed maize, rice and groundnuts in Mozambique, 2005-2008

Table 12 Local and private sector seed production activities in Mozambique 2006-2008

Table 13 Total seed production in Zambia 1998-2006

Table 14 Actual and estimates of fuzzy seed produced and supplied by cotton companies in Malawi,

Mozambique and Zambia

Table 15 Cassava varieties released in Zambia

List of Figures Fig 1 General structure of seed systems in Malawi, Mozambique and Zambia

Fig 2 Total seed production in Zambia 1998-2006

Fig 3 Common structure of the cotton seed system in Malawi, Mozambique and Zambia

4

Table of Contents List of Tables ........................................................................................................................................... 3

1. Introduction ....................................................................................................................................5

2 Crop Production..............................................................................................................................6

2.1 Food Crops ..............................................................................................................................6

2.2 Cassava....................................................................................................................................7

2.3 Cotton .....................................................................................................................................8

3 Cotton Production...........................................................................................................................8

3.1 Malawi.......................................................................................................................................10

3.2 Mozambique .........................................................................................................................11

3.3 Zambia...................................................................................................................................13

4 Seed Systems (Overview)..............................................................................................................14

5 Seed Availability ............................................................................................................................19

6 Cotton Seed System ......................................................................................................................21

7 Cassava Seed System ....................................................................................................................24

8 Observations .................................................................................................................................25

8.1 Cotton Sector ............................................................................................................................25

8.2 Cassava......................................................................................................................................26

9 Recommended Strategies.............................................................................................................26

9.1 Cotton .......................................................................................................................................26

9.2 Cassava......................................................................................................................................28

10 Conclusion.................................................................................................................................28

11 People and Organizations Contacted........................................................................................28

11.1 Mozambique .........................................................................................................................28

5

1. Introduction

Food security is a key element in the well being of a nation. Most African countries face serious

challenges ensuring food security yet agriculture contributes significantly to their GDPs. Agriculture

in Africa is largely subsistence, predominantly comprising of small holder farmers who are often very

resource poor and unable to sustain a living through agriculture. In addition, agriculture faces

serious challenges, mostly natural disasters such as droughts and floods, shortage of inputs and

credit for viable crop production, lack of equipment with most farmers using hand hoes to till the

land. The result is that yields are low to sustain families. Some countries have adopted strategies

that encourage food production while others have strengthened food imports to sustain national

food supply. In the SADC region, governments have adopted strategies of input support to small

holder farmers to produce enough food for themselves and in some cases for the nation. Other

governments have extended input support to cash crops such as cotton to enable farmers to

generate cash income. Seed availability is one of the major constraints to crop production in SADC

and other African countries. As seed industries developed across Africa, there has been an

improvement in the supply and availability of seed to farmers. However, on average less than 10% of

crop production systems in Africa use quality seed of improved varieties. 90% of the seed accessed

by farmers is from informal sector where farmers retain grain for use as seed for next planting. In

SADC, seed supply of food crops has significantly improved as governments liberalized seed sectors

and put together suitable regulatory framework that ensure timely supply of quality seed to farmers.

However, most regulatory frameworks are limited to cereal food crops. There are no regulations,

controls or support for tuber crops. Cassava is one of the most important food crops but little

recognized as such, and hence often viewed as a poor man’s crop.

Cassava is grown across the length of Africa, as a staple food crops in localized communities but as

minor crop nationwide. The crop is tolerant to moisture stress and therefore could yield food for

marginal areas prone to drought. In some developing countries such as Thailand and Brazil, cassava

has been promoted to a major industrial crop for the food processing, wood, paper and stock feed.

Thailand has turned the once dry region in the north of the country into an industrial zone based on

cassava; producing cassava pellets for stock feed for the European markets. Indeed southern Africa

is also experiencing a potential surge in demand in cassava as competition for maize increases. There

is increasing demand for cassava in South Africa for the paper, wood and stock feed industries.

Despite the potential increase in demand for cassava, limited efforts are made to increase

production. For some crops, there are policies for sustainable production through promotion and

support to use quality seed of improved varieties. For cassava, farmers still recycle poor quality

planting material. Yields are therefore low due to diseases and pests and lack of information on

appropriate technology for cassava production. In some countries, however, efforts are being taken

to improve cassava planting material supply.

It is generally expected for cash crops that adequate support will be provided by companies involved

in their production. Ideally, sectorial investors must provide technological support to enhance

productivity. Unfortunately in most countries farmers still use poor quality seed affecting yields and

investment returns for both farmers and companies. Most agro-companies in the SADC countries are

benefitting from government investments without paying dues or royalties. Cotton is one such crop.

Cotton is a major crop in some west, north and southern African countries. It is a significant crop in

SADC region although production is currently less than a million tons annually. Foreign ginners

contract farmers for cotton production, gin the seed cotton and export the lint. Many never invest in

development of crop technology to improve yields but rely on government bred varieties often

abusing the germplasm by unauthorized recycling of seed. Indeed this is exploitation must be

6

stopped and legislation must be enacted to enforce investment into the cotton sectors. Efforts are

being taken to increase production. In Malawi for example, government is promoting production of

cotton through provision of input. Zambia government has a policy on cassava to promote and

support production. These initiatives face the challenge of availability of quality seed. It is therefore

the objective of this assignment to

• Review seed sectors and identify constraints to seed supply to smallholder farmers, for

cotton and cassava (and associated crops such as maze and grain legumes).

• Review and analyse seed development and production system. Identify major stakeholders

and their role, production capacity and certification and quality assurance systems.

• Review and analyse the seed distribution system specific to cotton and cassava.

• Review regulatory and policy systems in place e.g. Intellectual Property Rights, existence and

impact on technology access.

• Analyse seed availability from the informal sector.

This assignment will be focused on Malawi, Mozambique and Zambia.

2 Crop Production

2.1 Food Crops

Malawi is basically a strip of land along Lake Malawi, the lake consisting of 35% of the country.

Malawi economy is agro based. Agriculture contributes 42% of Malawi’s GDP. The main agricultural

activities are crop production, plantation crops, horticulture and livestock. 84% of agricultural output

is smallholder. It is characterised by subsistence, low productivity and vulnerability to droughts and

floods. Agriculture earns 90% of the foreign exchange. The main crops are divided into two: food and

cash crops, the food crops being mainly maize and rice and cash crops consisting of cotton and

tobacco. Small holder farmers produce 98% of the maize and rice. Less than 10% of these famers buy

seed. Few farmers also use fertilizers. This significantly compromises yields. Malawi has recently

become a significant maize producer, 3.7 million tons in 2008/09 due to government initiative to

provide farmers with inputs such as seed and fertilizers. Much of Malawi’s crop production is along

the lakeshore and southern and central parts of the country (Table 1)

Table 1. Zoning of crop production in Malawi

Zone Crops

Lakeshore Rice, Cassava, Cotton,

Shire valley Cotton, Maize,

Central and Uplands Maize, Cotton, Sweet potatoes

Northern Maize

Mozambique has vast agricultural potential with 46% of the land area i.e. 36 million hectares

available for cultivation. Only 13% (4.5 million hectares) is presently used. 60-70% of this land is

planted to cereals. 99% of crop production is subsistence, with small holder farmers scattered in the

large country with diversity of soils and climate. On average 4% of the farmers use fertilizer to

enhance their yields and 90% of these farmers use recycled seed (Table 2). Thus crop yields are

highly compromised by poor seed quality, lack of improved varieties and lack of inputs.

Mozambique’s crop production activity can be categorized into four zones (table). 80 percent of the

7

most vulnerable people live in the country’s rural areas, surviving through subsistence farming.

Mozambique suffers regular periods of food insecurity, due to seasonal flooding of the huge

Zambezi River and its tributaries, as well as droughts in other arid regions. Despite the much

available land and potentially suitable climatic conditions, Mozambique imports much of its wheat

and rice to meet consumption needs. In 2008, Mozambique adopted a strategic food policy to

enhance production of mostly food crops throughout the country. The policy is driven by CEPAGRI

(Centre for the Promotion of Agriculture) whose global mandate is to promote investment in

agriculture, particularly the production and marketing of sugar, coconut, poultry, tea, cassava,

wheat, horticulture, tobacco and oilseed crops. Cassava is promoted for food security through a

proposed commercialization of production and marketing of cassava planting material.

Table 2 Distribution of crop production in Mozambique.

Zone Crop/Agricultural Activity

South (Maputo and Gaza) Rice, cassava and Cattle

Central (Inhambane, Manica, Sofala) Rice, Maize, Sorghum, Tobacco and Cattle

North East (Nampula, Carpo Delgardo, Cotton, Tobacco, Maize, Sorghum, Cassava,

Legumes, Sweet potatoes

North West (Tete, Zambezia, Nassa) Cotton, Cassava, Common beans, tobacco, Irish

Potatoes

In Zambia, agriculture contributes an average of 27% to the GDP. Maize, wheat, sorghum and

cassava are the major food crops. As in Malawi and Mozambique, crop production (except wheat) is

largely smallholder based. Much of the cereal production occurs in the eastern, central and southern

provinces. Commercial crop production is very active in Zambia compared to Malawi and

Mozambique. However much of commercial activities are centred on maize, wheat and soybean. As

in Malawi and Mozambique, small holder farmers produce the bulk of the maize in Zambia. The

main cash crop is cotton, widely grown in central, southern and eastern provinces of the country.

2.2 Cassava

One of the main food crops not recognized but contributes significantly to food security is cassava. In

all the three countries cassava is regarded as a poor man’s crop and yet the crop has huge potential

as source of starch for human and livestock and industry.

In Malawi, cassava is grown by more than 30% of the small holder farmers mainly along the

lakeshore areas. Cassava production is now being encouraged and promoted by both government

and donor organizations as a food security crop. Cassava production will cushion against hunger.

1.5million tons (dry weight) of cassava is produced against an annual demand of 2million tons. There

is even a proposal for a cassava based starch plant in Malawi. Efforts are indeed underway to create

sustainable cassava production through developing a reliable supply of planting materials and

reliable markets for cassava. There are no reliable cassava varieties in Malawi.

In Mozambique, cassava is a major food crop. About 60 percent of Mozambique’s population is

involved in cassava production and consumption, covering 2.5 million of the country’s farms.

Cassava production accounts for over 6 percent of the country’s GDP with over 2million tons (dry

weight) produced each year. 31% of Mozambique’s cassava production is in the Zambezia province.

All cassava production is by small holder farmers. Government has targeted cassava promotion for

8

food security. There is a program for commercial production of cassava planting material. As in

Malawi there are no varieties resistant to diseases.

In Zambia, cassava ranks second as source of energy after maize, providing livelihoods to most

people in the Northern Province. On average, 850 000 tons (dry weight) of cassava are produced

annually. There is no exact figure for national demand. In Northern Province, cassava has displaced

sorghum and millets as first choice food crops. Donors and government are currently promoting and

strengthening cassava production for both food security and industrial use. Attempts are currently

working on market linkages, linking small holder cassava producers to commercial consumers such

as stock feed, processing, paper and wood industries.

The justification of the initiative in all the three countries is that inputs for cassava production are

very low compared to that of maize and other starch crops. On the feed industry, there is perception

that cassava is relatively low priced compared to maize and despite the low protein content, cassava

has high energy content. However, there are challenges being experienced in the cassava initiative,

such as transportation, pricing of cassava, lack of planting materials, sourcing of improved varieties

and markets. Indeed there is deficiency of information on crop husbandry practices. As a result, the

crop is sometimes planted at the end of the rainy season and matures 12 months later than other

crops.

In all the three countries, smallholder farmers dominate crop production. It is therefore expected

that 90% of seed and planting material is consumed by these small scale farmers. Unfortunately

smallholder farmers are resource poor, unable to access such inputs as seed and fertilizer for

sustainable production. Indeed governments have adopted input support programs under the cause

of food security. The impact of this policy has been increased use of quality seed and increase

production of food crops.

2.3 Cotton

Cotton is also a major cash crop, produced mostly by smallholder farmers. In 2008, Government of

Malawi developed a Cotton Sector Development Strategy (CSDS) making cotton a strategic crop, a

cash crop for farmers to enable sustain themselves when cereal crops fail due to natural disasters.

The challenge however is to produce high quality cotton. In Mozambique cotton is a major cash crop

in the north east and northwest zones (Table 10). Cotton is also recognized as an important crop but

government does not have any strategies to support and enhance its production. As a result cotton

production is controlled by cotton companies who have insisted on concession system where each

company controls production in a particular province (Table 2). In Zambia, cotton production is

supported by a government and private sector initiative to use only certified seed for planting.

3 Cotton Production

Cotton is one of the major cash crops in the SADC countries. In Malawi, cotton is a strategic crop

being a key element in poverty reduction and economic growth strategy. As a result, the

government of Malawi has developed a cotton pricing policy to promote and stabilize production,

through setting a minimum price in consultation with other stakeholders, farmers and seed

companies. Malawi government insists cotton companies pay set minimum price for seed cotton.

This policy is however, having a negative impact on the viability of the crop as price set often not at

9

parity with world market. In Mozambique, while government sets minimum price in consultation

with stakeholders, it does not insist on cotton companies paying minimum set price for seed cotton.

In Zambia, cotton prices are negotiated by stakeholders. The Cotton Association of Zambia (CAZ)

represents farmers in all fora on pricing.

Cotton yields vary between countries, ranging from as low as 400kgs/ha in Mozambique to

800kgs/ha in Zimbabwe. Yields of 3500kgs/ha are achieved under irrigation mostly in South Africa.

Ginning out turn (GOT) also varies ranging from 34% to 40%. Variations in both yield and ginning

outturn are due to type and variety of seed used. In all the three countries, low yields and GOT are

due to recycling of seed and variety mixtures (Table 3). In these countries seed is mostly recycled

while in other countries farmers use new and quality seed of pure varieties every year.

Table 3 Cotton production in some SADC countries in 2000/01

Country Total Production(Mt) Yield/Ha (kgs) GOT

Malawi 24600 500 34

Mozambique 71000 400 36

South Africa 198000 3455 40

Zambia 121000 700 38

Zimbabwe 251000 800 40

Cotton production is largely small scale through contract under out grower schemes. In all the three

countries, the cotton industry are driven by ginners and 100% produced by smallholder farmers. The

ginning companies contract small holder farmers, providing them with inputs such as seed and

pesticides. There is no support for fertilizers, except in Zambia where farmers are supplied with

foliar fertilizers in addition to seed and pesticides.

Cotton industry faces many challenges in all the three countries. First challenge is pricing of lint.

While stakeholders engage in pricing, ginners hardly adhere to agreed prices. As a result production

varies annually as farmers change to crops that give better returns. Such is the case in Mozambique,

where sesame sometimes pays four times the price of seed cotton and farmers sideline cotton in

favour of sesame. In Zambia, cotton production is often affected by government pre-planting price

of maize causing farmers to plant more maize than cotton. The second major challenge is low yields.

Yields vary between 300 and 700kgs per hectare when variety potential is sometimes in excess of

2000kgs/ha. The low yields are due to lack of fertilizer use and absence of information on cotton

husbandry practices. The third challenge is lack of quality seed. Low yields are often attributed to

poor quality seed. Another significant challenge is too many varieties on the market. Mozambique

cotton industry has more than 10 varieties, with varying lint quality. Some of the varieties are of

unknown origin brought by ginners. Zambia has three main varieties whose parent seed production

is controlled by the Cotton Development Trust. Malawi also has three main varieties but there is

little control on parent seed availability. Side marketing is also a key challenge to the cotton sector.

While farmers are contracted and supplied with inputs, some try to sell their cotton to ginners

where they have credit obligations. Another challenge to the cotton sector in the three countries is

absence of extension service in the cotton sector. While ginners provide extension services, most of

it is done by improperly trained input distributors or agro dealers.

In all three countries, the main stakeholders have been the governments, providing the regulatory

framework for cotton production, the ginners providing the inputs and markets for cotton and the

smallholder farmers for producing the cotton crop. There are also other instruments of governments

10

with specific functions such seed regulatory authorities monitoring production and distribution of

cotton seed.

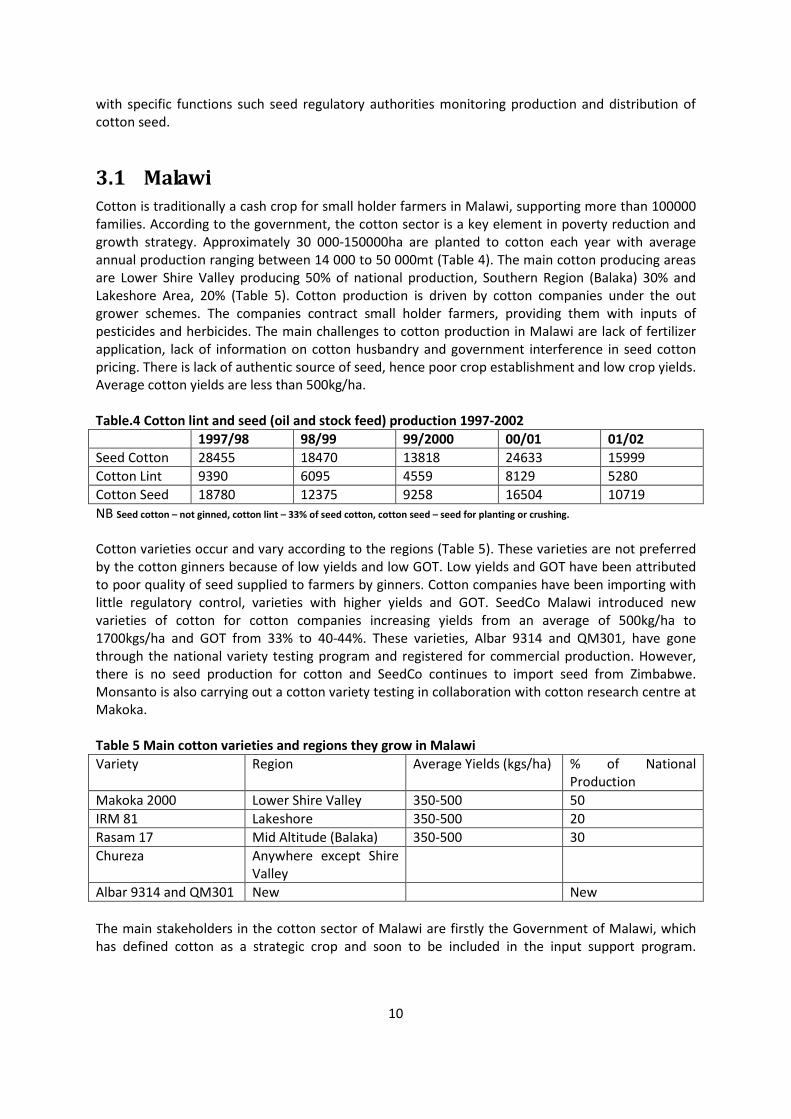

3.1 Malawi

Cotton is traditionally a cash crop for small holder farmers in Malawi, supporting more than 100000

families. According to the government, the cotton sector is a key element in poverty reduction and

growth strategy. Approximately 30 000-150000ha are planted to cotton each year with average

annual production ranging between 14 000 to 50 000mt (Table 4). The main cotton producing areas

are Lower Shire Valley producing 50% of national production, Southern Region (Balaka) 30% and

Lakeshore Area, 20% (Table 5). Cotton production is driven by cotton companies under the out

grower schemes. The companies contract small holder farmers, providing them with inputs of

pesticides and herbicides. The main challenges to cotton production in Malawi are lack of fertilizer

application, lack of information on cotton husbandry and government interference in seed cotton

pricing. There is lack of authentic source of seed, hence poor crop establishment and low crop yields.

Average cotton yields are less than 500kg/ha.

Table.4 Cotton lint and seed (oil and stock feed) production 1997-2002

1997/98 98/99 99/2000 00/01 01/02

Seed Cotton 28455 18470 13818 24633 15999

Cotton Lint 9390 6095 4559 8129 5280

Cotton Seed 18780 12375 9258 16504 10719

NB Seed cotton – not ginned, cotton lint – 33% of seed cotton, cotton seed – seed for planting or crushing.

Cotton varieties occur and vary according to the regions (Table 5). These varieties are not preferred

by the cotton ginners because of low yields and low GOT. Low yields and GOT have been attributed

to poor quality of seed supplied to farmers by ginners. Cotton companies have been importing with

little regulatory control, varieties with higher yields and GOT. SeedCo Malawi introduced new

varieties of cotton for cotton companies increasing yields from an average of 500kg/ha to

1700kgs/ha and GOT from 33% to 40-44%. These varieties, Albar 9314 and QM301, have gone

through the national variety testing program and registered for commercial production. However,

there is no seed production for cotton and SeedCo continues to import seed from Zimbabwe.

Monsanto is also carrying out a cotton variety testing in collaboration with cotton research centre at

Makoka.

Table 5 Main cotton varieties and regions they grow in Malawi

Variety Region Average Yields (kgs/ha) % of National

Production

Makoka 2000 Lower Shire Valley 350-500 50

IRM 81 Lakeshore 350-500 20

Rasam 17 Mid Altitude (Balaka) 350-500 30

Chureza Anywhere except Shire

Valley

Albar 9314 and QM301 New New

The main stakeholders in the cotton sector of Malawi are firstly the Government of Malawi, which

has defined cotton as a strategic crop and soon to be included in the input support program.

11

Government of Malawi is keen to see cotton, being a cash crop providing income to poor families in

rural areas. Government, through the research department also provides varieties for multiplication.

Makoka Cotton Research Institute bred the most grown cotton variety, Makoka 2000. The institute is

currently involved in the purification of the old varieties, production of breeder seed and selling the

seed to cotton companies for further multiplication. However, the research station lacks capacity to

meet demand. Thus, because of lack of seed, cotton companies were importing seed from other

countries. The research station is also coming up with new varieties. Another variety commonly

grown in Malawi is Chureza, bred and developed in Zambia. It is the most popular variety in the

eastern province of Zambia and brought to Malawi by ginners. It is high yielding and has high GOT.

The cotton industry in Malawi is driven by cotton companies (ginners). Ginners provide the market

for cotton but also enable production through provision of inputs, mostly pesticides. The main

cotton companies are Great Lakes and Cargill (formerly Clarke Cotton).

Farmers are also major stakeholders whose labour produces the cotton lint for the market. Indeed

their well being and support enhances production but they face serious challenges on prices, quality

seed, technical support and low yields. Although farmers may receive extension support in training

at village level (in Balaka region), there is poor crop establishment in farmers’ fields due to lack of

authentic source of seed.

In Malawi, cotton is marketed from the farmer’s field through three possible channels. Seed cotton

is either sold directly to the cotton companies (ginners), the contractors of the crop, who deduct

their input support on the farmers’ total crop sales or through farmers’ organizations although this

does not guarantee premium price. Seed cotton can also be marketed through independent traders

by farmers who independently produced the crop (without input support) and farmers who side

market to avoid paying debts to cotton companies that supported them.

Major challenges in cotton marketing are side marketing by farmers and pricing where government

insist on companies paying the minimum set price of MK75/kg. Recycling of seed by seed companies

has led to mixtures and subsequent loss of genetic quality. As a result the gin-out-turn (Got) is as low

as 35%.

3.2 Mozambique

Mozambique cotton production is based on concession system in which a company is given rights of

control on cotton production in a designated area (Table 6). The concession system is characterised

by a) geographical monopolies, in which an individual company controls a cotton producing district

or province b) the right to purchase all cotton and the responsibility to provide support to any small

farmer wishing to produce cotton c) official minimum price set by the Cotton Institute in

consultation with other stakeholders, often become the fixed price. Cotton companies and some

provincial officials defend the concession system as beneficial to farmers through a) guaranteed

market of cotton b) minimum price setting even though some companies may chose to pay below

the set price c) input support for farmers. The argument is that liberalising cotton marketing would

erode the benefits as farmers would side market the product to avoid paying their debts to

companies that supplied inputs. No cotton company would invest in farmer inputs under a

liberalized cotton production and marketing system. As a result of the concessionary system

research has no linkage with farmers.

12

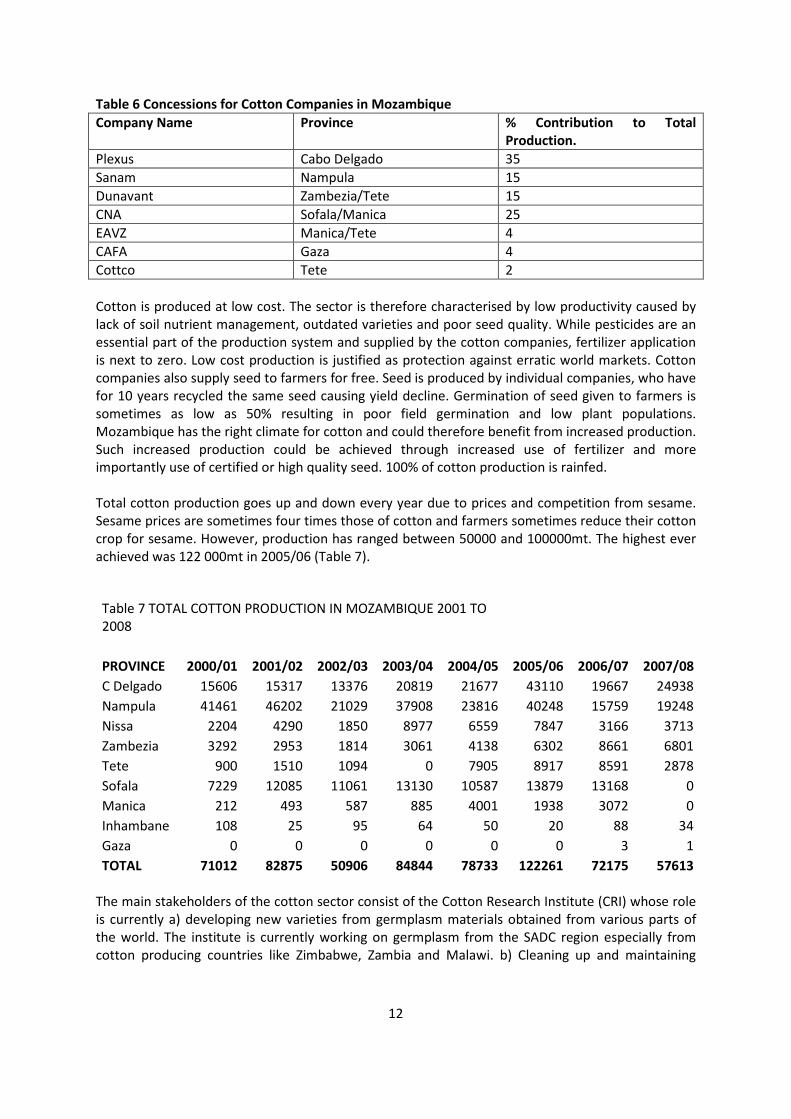

Table 6 Concessions for Cotton Companies in Mozambique

Company Name Province % Contribution to Total

Production.

Plexus Cabo Delgado 35

Sanam Nampula 15

Dunavant Zambezia/Tete 15

CNA Sofala/Manica 25

EAVZ Manica/Tete 4

CAFA Gaza 4

Cottco Tete 2

Cotton is produced at low cost. The sector is therefore characterised by low productivity caused by

lack of soil nutrient management, outdated varieties and poor seed quality. While pesticides are an

essential part of the production system and supplied by the cotton companies, fertilizer application

is next to zero. Low cost production is justified as protection against erratic world markets. Cotton

companies also supply seed to farmers for free. Seed is produced by individual companies, who have

for 10 years recycled the same seed causing yield decline. Germination of seed given to farmers is

sometimes as low as 50% resulting in poor field germination and low plant populations.

Mozambique has the right climate for cotton and could therefore benefit from increased production.

Such increased production could be achieved through increased use of fertilizer and more

importantly use of certified or high quality seed. 100% of cotton production is rainfed.

Total cotton production goes up and down every year due to prices and competition from sesame.

Sesame prices are sometimes four times those of cotton and farmers sometimes reduce their cotton

crop for sesame. However, production has ranged between 50000 and 100000mt. The highest ever

achieved was 122 000mt in 2005/06 (Table 7).

Table 7 TOTAL COTTON PRODUCTION IN MOZAMBIQUE 2001 TO

2008

PROVINCE 2000/01 2001/02 2002/03 2003/04 2004/05 2005/06 2006/07 2007/08

C Delgado 15606 15317 13376 20819 21677 43110 19667 24938

Nampula 41461 46202 21029 37908 23816 40248 15759 19248

Nissa 2204 4290 1850 8977 6559 7847 3166 3713

Zambezia 3292 2953 1814 3061 4138 6302 8661 6801

Tete 900 1510 1094 0 7905 8917 8591 2878

Sofala 7229 12085 11061 13130 10587 13879 13168 0

Manica 212 493 587 885 4001 1938 3072 0

Inhambane 108 25 95 64 50 20 88 34

Gaza 0 0 0 0 0 0 3 1

TOTAL 71012 82875 50906 84844 78733 122261 72175 57613

The main stakeholders of the cotton sector consist of the Cotton Research Institute (CRI) whose role

is currently a) developing new varieties from germplasm materials obtained from various parts of

the world. The institute is currently working on germplasm from the SADC region especially from

cotton producing countries like Zimbabwe, Zambia and Malawi. b) Cleaning up and maintaining

13

existing varieties. Over the years, locally bread varieties have become mixed because of the absence

of a proper variety maintenance program c) production of basic seed for sale to cotton companies

for further multiplication into “certified” seed (Fig 1). The government of Mozambique recently

established the National Cotton Institute (NCI) whose functions are a) to set minimum cotton prices

in consultation with Ginner’s Association and farmers b) to enforce concessionaire right/mediate

conflicts c) to maintain statistics on the sector d) promotes cotton production. The institute also

creates and maintains dialogue among stakeholders who are researchers, companies and farmers.

The Cotton Ginner’s Association is also a major stakeholder. The association represents cotton

companies. The objectives of the association are a) to promote production of quality cotton b) set or

negotiate minimum prices with the National Cotton Institute and farmers c) raise cotton productivity

d) monitor and manage concessions sometimes defending concessions against new entrants. The

farmers constitute the main stakeholder. 100% of cotton farmers in Mozambique are small holder

farmers. Unfortunately, these farmers have no effective representation in the form of Farmers

Association; hence as producers they deal directly with members of the Cotton Ginner’s Association

and researchers. Cotton companies drive the cotton industry. They provide inputs to farmers for

contract production. The companies are also the source of cotton seed, which they distribute to

farmers as input support in addition to pesticides and other supporting chemicals.

Cotton marketing calendar is determined by cotton companies in collaboration with local farmers.

The price of cotton lint is determined by the association of cotton companies in consultation with

National Cotton Institute and farmers representatives. Because of the concessionary system, farmers

can only sell their cotton to the company owning the concession. The company would be the

supplier of inputs and in some cases technical support. There are however, several challenges to

cotton production in Mozambique. Farmers are not paid according to quality. They are just paid an

agreed price without grades. Good farmers could benefit from grading with premium price paid for

best grade. The flat price affects farmer commitment to production of quality crop, limiting crop

management input to basic agronomic practices. There is lack of fertilizer use in cotton production.

This limits yield to less than 1mt per hectare. Cotton companies have shown that application of

fertilizer can increase to more than 1.5mt per hectare despite poor seed quality and outdated

varieties. However, companies not willing to invest in fertilizer application. The reason for not

encouraging farmers to apply fertilizers could be that companies want production to remain within

their capacity to purchase. The concept of concessions cause cotton companies to chose a price to

their own benefit not farmers. The result is in some provinces such as Zambezia, Sofala and Manica,

farmers are turning to sesame as cash crop. Sesame fetches four times the price of cotton. All cotton

crops are planted from recycled seed whose production does not meet national standards and

varieties are outdated. Cotton companies have not invested in technology to enhance production.

Cotton companies should invest or contribute towards research for new varieties, crop and disease

protection.

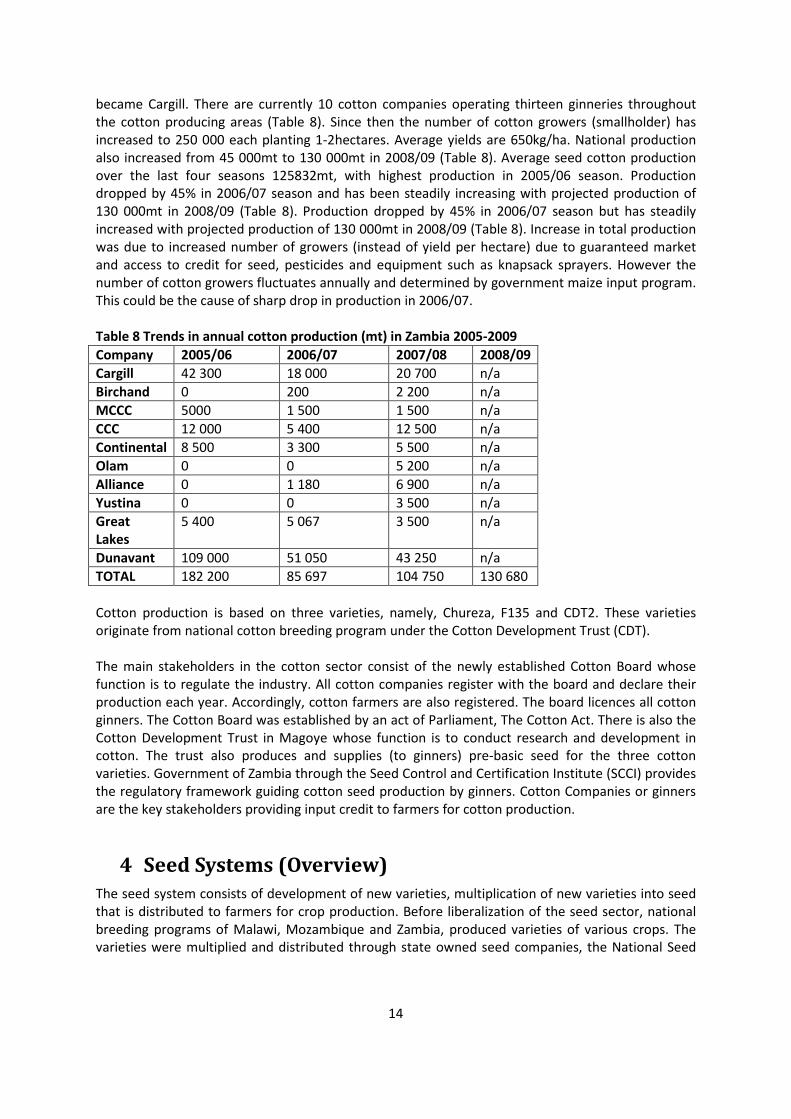

3.3 Zambia

Zambia is third largest cotton producer in SADC after Zimbabwe and South Africa. There are three

main areas of production, Central, Eastern and Southern provinces. More than 60% of the cotton is

produced in Eastern Province. All cotton production is by small holder farmers spread across these

provinces. Before 1990, there was only one player in the cotton sector, a parastatal company called

Lint co. Then there were only 97 000 smallholder cotton growers producing a total of 45 000mt.

Liberalization of the industry in 1990s brought several players some of which bought Lint co broken

into three provinces. Lint co, Southern and Central Province became Dunavant and Eastern Province

14

became Cargill. There are currently 10 cotton companies operating thirteen ginneries throughout

the cotton producing areas (Table 8). Since then the number of cotton growers (smallholder) has

increased to 250 000 each planting 1-2hectares. Average yields are 650kg/ha. National production

also increased from 45 000mt to 130 000mt in 2008/09 (Table 8). Average seed cotton production

over the last four seasons 125832mt, with highest production in 2005/06 season. Production

dropped by 45% in 2006/07 season and has been steadily increasing with projected production of

130 000mt in 2008/09 (Table 8). Production dropped by 45% in 2006/07 season but has steadily

increased with projected production of 130 000mt in 2008/09 (Table 8). Increase in total production

was due to increased number of growers (instead of yield per hectare) due to guaranteed market

and access to credit for seed, pesticides and equipment such as knapsack sprayers. However the

number of cotton growers fluctuates annually and determined by government maize input program.

This could be the cause of sharp drop in production in 2006/07.

Table 8 Trends in annual cotton production (mt) in Zambia 2005-2009

Company 2005/06 2006/07 2007/08 2008/09

Cargill 42 300 18 000 20 700 n/a

Birchand 0 200 2 200 n/a

MCCC 5000 1 500 1 500 n/a

CCC 12 000 5 400 12 500 n/a

Continental 8 500 3 300 5 500 n/a

Olam 0 0 5 200 n/a

Alliance 0 1 180 6 900 n/a

Yustina 0 0 3 500 n/a

Great

Lakes

5 400 5 067 3 500 n/a

Dunavant 109 000 51 050 43 250 n/a

TOTAL 182 200 85 697 104 750 130 680

Cotton production is based on three varieties, namely, Chureza, F135 and CDT2. These varieties

originate from national cotton breeding program under the Cotton Development Trust (CDT).

The main stakeholders in the cotton sector consist of the newly established Cotton Board whose

function is to regulate the industry. All cotton companies register with the board and declare their

production each year. Accordingly, cotton farmers are also registered. The board licences all cotton

ginners. The Cotton Board was established by an act of Parliament, The Cotton Act. There is also the

Cotton Development Trust in Magoye whose function is to conduct research and development in

cotton. The trust also produces and supplies (to ginners) pre-basic seed for the three cotton

varieties. Government of Zambia through the Seed Control and Certification Institute (SCCI) provides

the regulatory framework guiding cotton seed production by ginners. Cotton Companies or ginners

are the key stakeholders providing input credit to farmers for cotton production.

4 Seed Systems (Overview)

The seed system consists of development of new varieties, multiplication of new varieties into seed

that is distributed to farmers for crop production. Before liberalization of the seed sector, national

breeding programs of Malawi, Mozambique and Zambia, produced varieties of various crops. The

varieties were multiplied and distributed through state owned seed companies, the National Seed

15

Company in Malawi, Semoc in Mozambique and Zambia Seeds (Zamseeds) in Zambia. Since the

liberalization of the seed industry private seed companies, regional and multinational have invested

in the seed industries of these countries (Table 9). The most successful investment is in Zambia

where more seed companies have been established in response to change of policy.

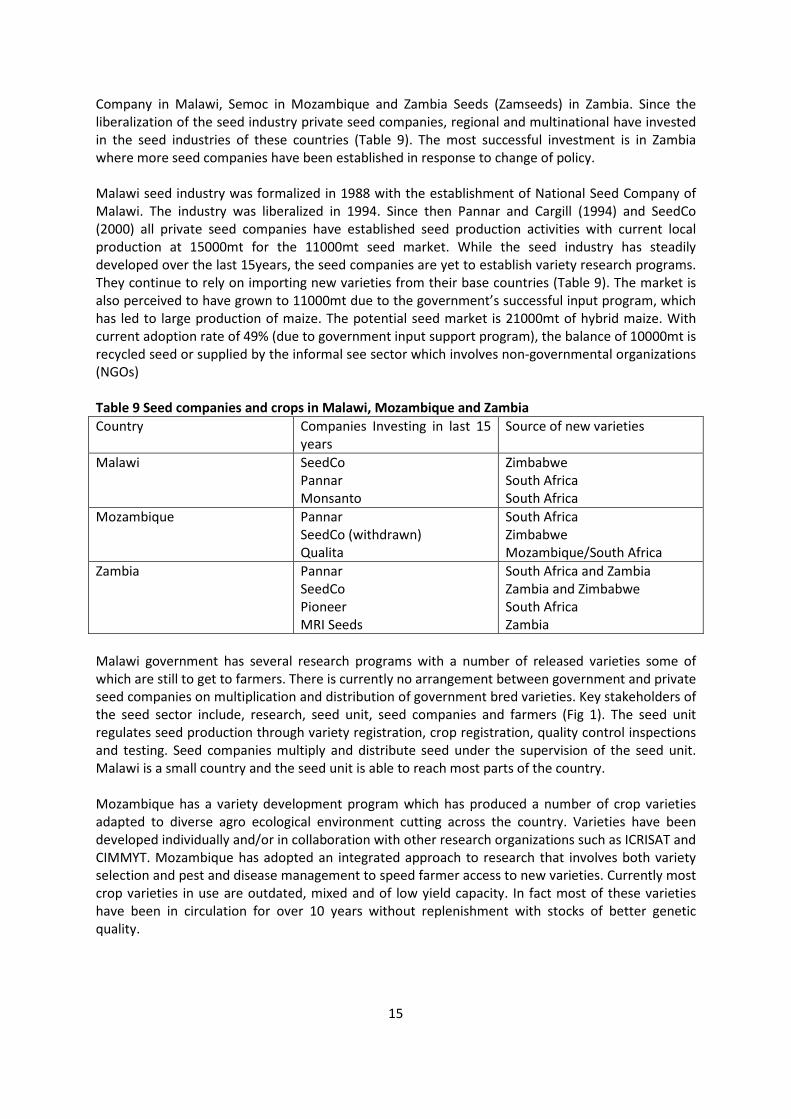

Malawi seed industry was formalized in 1988 with the establishment of National Seed Company of

Malawi. The industry was liberalized in 1994. Since then Pannar and Cargill (1994) and SeedCo

(2000) all private seed companies have established seed production activities with current local

production at 15000mt for the 11000mt seed market. While the seed industry has steadily

developed over the last 15years, the seed companies are yet to establish variety research programs.

They continue to rely on importing new varieties from their base countries (Table 9). The market is

also perceived to have grown to 11000mt due to the government’s successful input program, which

has led to large production of maize. The potential seed market is 21000mt of hybrid maize. With

current adoption rate of 49% (due to government input support program), the balance of 10000mt is

recycled seed or supplied by the informal see sector which involves non-governmental organizations

(NGOs)

Table 9 Seed companies and crops in Malawi, Mozambique and Zambia

Country Companies Investing in last 15

years

Source of new varieties

Malawi SeedCo

Pannar

Monsanto

Zimbabwe

South Africa

South Africa

Mozambique Pannar

SeedCo (withdrawn)

Qualita

South Africa

Zimbabwe

Mozambique/South Africa

Zambia Pannar

SeedCo

Pioneer

MRI Seeds

South Africa and Zambia

Zambia and Zimbabwe

South Africa

Zambia

Malawi government has several research programs with a number of released varieties some of

which are still to get to farmers. There is currently no arrangement between government and private

seed companies on multiplication and distribution of government bred varieties. Key stakeholders of

the seed sector include, research, seed unit, seed companies and farmers (Fig 1). The seed unit

regulates seed production through variety registration, crop registration, quality control inspections

and testing. Seed companies multiply and distribute seed under the supervision of the seed unit.

Malawi is a small country and the seed unit is able to reach most parts of the country.

Mozambique has a variety development program which has produced a number of crop varieties

adapted to diverse agro ecological environment cutting across the country. Varieties have been

developed individually and/or in collaboration with other research organizations such as ICRISAT and

CIMMYT. Mozambique has adopted an integrated approach to research that involves both variety

selection and pest and disease management to speed farmer access to new varieties. Currently most

crop varieties in use are outdated, mixed and of low yield capacity. In fact most of these varieties

have been in circulation for over 10 years without replenishment with stocks of better genetic

quality.

16

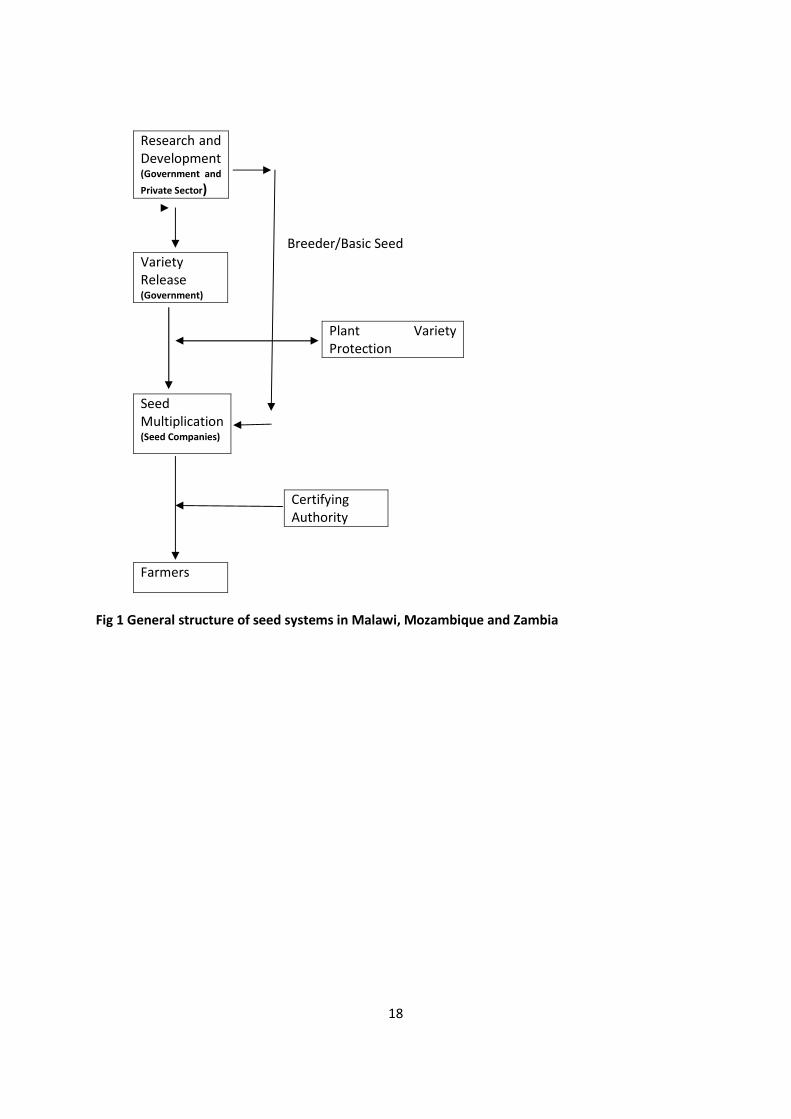

The key stakeholders of the seed system are research and development, seed services or certifying

authority, seed companies and in the case of cotton, cotton companies (Fig 2). As in Malawi, the role

of the National Seed Services (established by law, the national Seed Act) is to provide guidelines for

quality seed production through a set of regulations to enforce quality control measures and ensure

that all varieties grown in Mozambique are registered and listed on National Variety List. Through

the National Seed Committee, varieties go through a release process which involves analysis for

value for cultivation and use (VCU), analysis for distinctness, uniformity and stability (DUS) before

they can be released, listed and distributed to farmers for crop production. Currently the National

Seed Service is based in Maputo and has to reach out to various provinces such as Cabo Delgado in

the north and Tete and Niassa in the far west and north-west respectively. The distances and cost of

travel prohibit national seed service to reach out to these areas. Lack of presence of National Seed

Service in remote provinces has compromised farmer access to quality seed. Seed is produced

informally by NGOs in collaboration with farmers’ associations. Such seed is not tested for quality

(purity and germination and genetic purity).

The seed industry is still developing. Until about 15 years ago when the industry was liberalised, only

one seed company, SEMOC was the sole supplier of seed throughout Mozambique. Then, SEMOC

was the sole recipient of new varieties from government research programs for multiplication and

distribution. When the industry was liberalised, a number of companies established seed production

programs in Mozambique. This was found not viable because the farming community was not

geared for seed production and the regulatory system was not consistent. Resources limited the

functioning of National Seed Services. In addition the market was not receptive to new varieties.

Hence most companies investing in the seed sector imported from neighbouring countries where

production was economic and effectively supported by a reliable regulatory system. The seed

industry is currently made up of 4 main local and foreign companies (Table 10).

Table.10 Seed companies and major crops in Mozambique

Company Area of Activity Seed Crops

Pannar Chimoio, Maputo Maize, vegetable, sorghum

Hortimoc Maputo Vegetables(imports from South

Africa, Denmark, Italy), OPV

Maize (Matuba), Cowpea (IT18

and Mixes),

Semente Perfeita Chimoio (Manica), Vegetable, maize OPV and

sorghum

Qualita Chimoio (Manica) Vegetables, Maize and

sorghum.

Zambia’s seed system is more developed than Malawi and Mozambique. The industry is more

liberalised and more competitive, has more players and wider range of seed. However, as in Malawi

and Mozambique, before liberalization of the industry in the 1980’s, there was only one seed

company, Zamseed, owned by government and sole recipient of government bred crop varieties for

multiplication and distribution. Since liberalization Zambia is now a major supplier of seed in the

SADC region with a number of established regional and multinational seed companies (Table ). The

main stakeholders of the seed sector also include research, both public and private; producing new

crop technologies, the certifying authority, Seed Control and Certification Institute (SCCI), which

controls release of crop technology to farmers, monitors multiplication and distribution of new crop

17

technology to ensure farmers get quality seed and providing postharvest monitoring of seed (Fig 1).

SCCI also requires national listing of all varieties for certified seed production.

However, all the three countries lack effective Intellectual Property Rights (IPRs) to protect new

varieties seed companies may wish to introduce. In Malawi, Monsanto is unwilling to bring in

superior technology of maize and cotton because the country does not have effective Plant

Breeders’ Rights (PBR) system to protect patented germplasm. The same applies to Zambia where

despite the presence of the PBRs, it has not been implemented to enable the Cotton Development

Trust to claim royalties from ginners using their varieties. In Mozambique, the PBR is under

development. However, SADC is in the process of harmonizing seed regulatory processes and being

member countries, Mozambique and Malawi intend to adopt and apply SADC IPR system for the

protection of patented plant materials. It is expected the harmonized regulations will enable and

speed seed movement within SADC making available seed of much diversity to farmers in respective

countries.

18

Research and

Development (Government and

Private Sector)

Breeder/Basic Seed

Variety

Release (Government)

Plant Variety

Protection

Seed

Multiplication (Seed Companies)

Certifying

Authority

Farmers

Fig 1 General structure of seed systems in Malawi, Mozambique and Zambia

19

5 Seed Availability

Availability of seed is one of the major challenges of the agriculture sector in SADC countries. Not all

SADC countries produce enough seed for their needs. Zimbabwe for example needs as much as

50000mt of maize seed alone against national production of less than 20000mt. There is potential

for other countries to produce seed for export to Zimbabwe. Zambia has taken advantage of the

near collapse of the seed system in Zimbabwe. Since 2003/04, Zambia has produced more maize

seed than the market could absorb (Table 12). This caused a sharp increase in total seed production

(Fig 2). The excess production was for the export to Zimbabwe. South Africa also increased

production targeting the Zimbabwean market.

Malawi’s actual annual seed market is currently 11000mt (MAC, SeedCo, Monsanto) for maize only.

With other crops the seed market is 19000mt. The 11000mt seed demand recorded 2008/09 is due

to government input support program. The government input support program makes 50% of the

market. However, the country’s potential seed market is 31000mt for all crops. Potential maize seed

market is 21000mt. Current maize seed production is 15000mt. The deficit of 6000mt therefore

comes from informal seed production, where farmer retain grain from previous crops and use it as

seed.

In Mozambique, 2.8-3.5 million hectares of grain crops are planted each year. These require 60 000

to 80 000mt of annually. With adoption rates ranging between 3% and 10% maize, rice and

groundnuts for example, (Table 11) the actual seed market for maize is 6000mt and 80% of that

market is government input program. The formal seed industry consists of the two main seed

companies (Table 10), supply less than 10% of estimated annual seed required (Table 11). This

means much of the seed is retained grain by farmers or comes from informal seed sector driven

mostly by NGOs. In fact more than 50% of the estimated seed production is informal (Table 12). For

example, since 2006 a number of seed production activities were carried out throughout the country

to augment production and supply by the private seed sector (Table 12). In this program, the

National Seed Service registers these crops and seed produced meets minimum standards of purity

and germination. In addition the seed also guarantees variety purity. Aga Khan provides funding for

these production activities. Despite these efforts however, there was deficit on supply, hence most

farmers relied on retained seed (Table 12). This is also reflected by low percentage use of quality

seed in Mozambique (Table 11).

Elsewhere in the country NGOs are also involved in community seed projects to enhance seed

availability to farmers. In Sofala province the extension service coordinates some seed production

activities at least to ensure that farmers, though few have access to some form of quality seed.

There is no direct involvement of the National Seed Service in ensuring quality control throughout

the course of production. Seed of these production activities is recycled because the research

department lacks capacity to produce sufficient amount of basic seed to meet demand. Some of the

seed produced is sold to seed companies such as SEMOC but with no guaranteed genetic quality.

Seed is also sold to other NGOs.

20

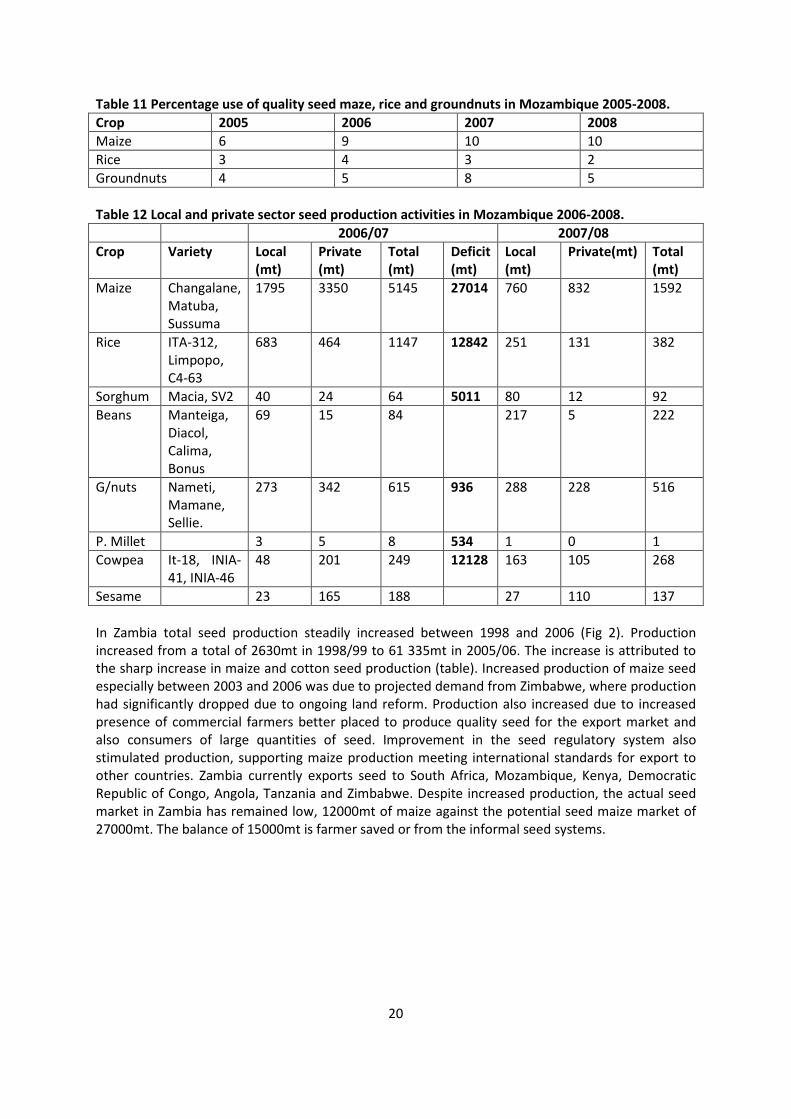

Table 11 Percentage use of quality seed maze, rice and groundnuts in Mozambique 2005-2008.

Crop 2005 2006 2007 2008

Maize 6 9 10 10

Rice 3 4 3 2

Groundnuts 4 5 8 5

Table 12 Local and private sector seed production activities in Mozambique 2006-2008.

2006/07 2007/08

Crop Variety Local

(mt)

Private

(mt)

Total

(mt)

Deficit

(mt)

Local

(mt)

Private(mt) Total

(mt)

Maize Changalane,

Matuba,

Sussuma

1795 3350 5145 27014 760 832 1592

Rice ITA-312,

Limpopo,

C4-63

683 464 1147 12842 251 131 382

Sorghum Macia, SV2 40 24 64 5011 80 12 92

Beans Manteiga,

Diacol,

Calima,

Bonus

69 15 84 217 5 222

G/nuts Nameti,

Mamane,

Sellie.

273 342 615 936 288 228 516

P. Millet 3 5 8 534 1 0 1

Cowpea It-18, INIA-

41, INIA-46

48 201 249 12128 163 105 268

Sesame 23 165 188 27 110 137

In Zambia total seed production steadily increased between 1998 and 2006 (Fig 2). Production

increased from a total of 2630mt in 1998/99 to 61 335mt in 2005/06. The increase is attributed to

the sharp increase in maize and cotton seed production (table). Increased production of maize seed

especially between 2003 and 2006 was due to projected demand from Zimbabwe, where production

had significantly dropped due to ongoing land reform. Production also increased due to increased

presence of commercial farmers better placed to produce quality seed for the export market and

also consumers of large quantities of seed. Improvement in the seed regulatory system also

stimulated production, supporting maize production meeting international standards for export to

other countries. Zambia currently exports seed to South Africa, Mozambique, Kenya, Democratic

Republic of Congo, Angola, Tanzania and Zimbabwe. Despite increased production, the actual seed

market in Zambia has remained low, 12000mt of maize against the potential seed maize market of

27000mt. The balance of 15000mt is farmer saved or from the informal seed systems.

21

0

10000

20000

30000

40000

50000

60000

70000

80000

1998/99 2000/01 2002/03 2004/05

Total

Maize

Cotton

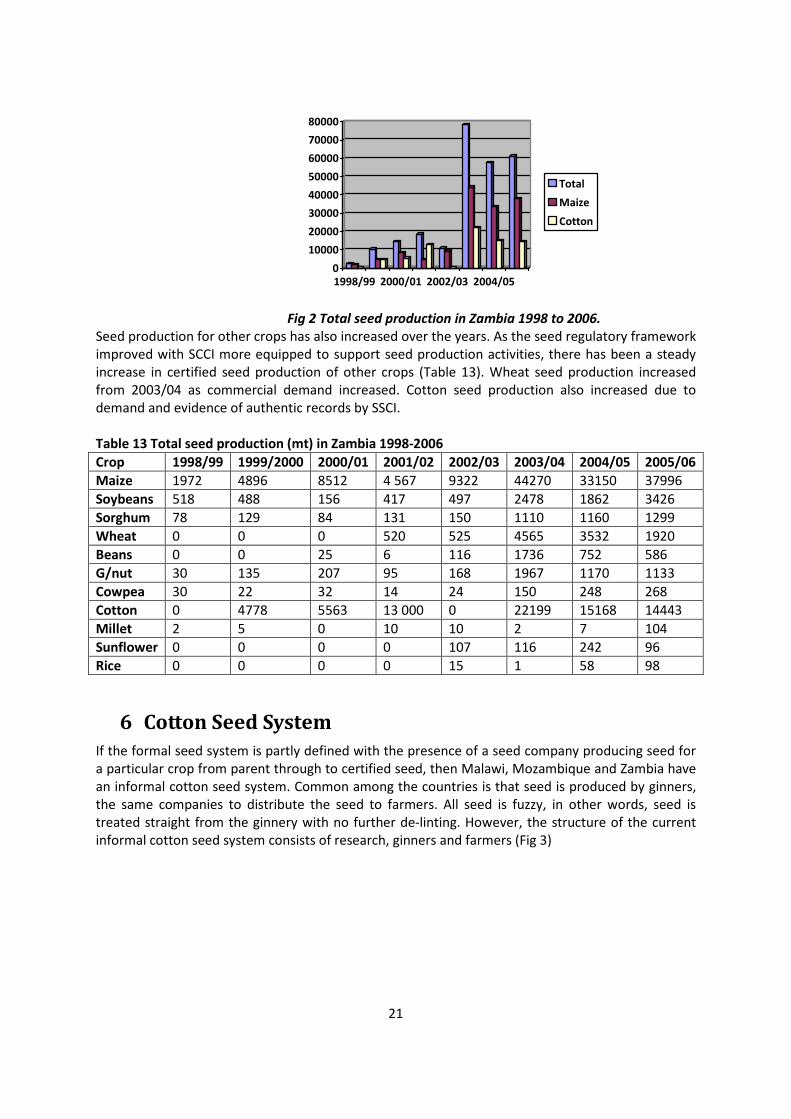

Fig 2 Total seed production in Zambia 1998 to 2006.

Seed production for other crops has also increased over the years. As the seed regulatory framework

improved with SCCI more equipped to support seed production activities, there has been a steady

increase in certified seed production of other crops (Table 13). Wheat seed production increased

from 2003/04 as commercial demand increased. Cotton seed production also increased due to

demand and evidence of authentic records by SSCI.

Table 13 Total seed production (mt) in Zambia 1998-2006

Crop 1998/99 1999/2000 2000/01 2001/02 2002/03 2003/04 2004/05 2005/06

Maize 1972 4896 8512 4 567 9322 44270 33150 37996

Soybeans 518 488 156 417 497 2478 1862 3426

Sorghum 78 129 84 131 150 1110 1160 1299

Wheat 0 0 0 520 525 4565 3532 1920

Beans 0 0 25 6 116 1736 752 586

G/nut 30 135 207 95 168 1967 1170 1133

Cowpea 30 22 32 14 24 150 248 268

Cotton 0 4778 5563 13 000 0 22199 15168 14443

Millet 2 5 0 10 10 2 7 104

Sunflower 0 0 0 0 107 116 242 96

Rice 0 0 0 0 15 1 58 98

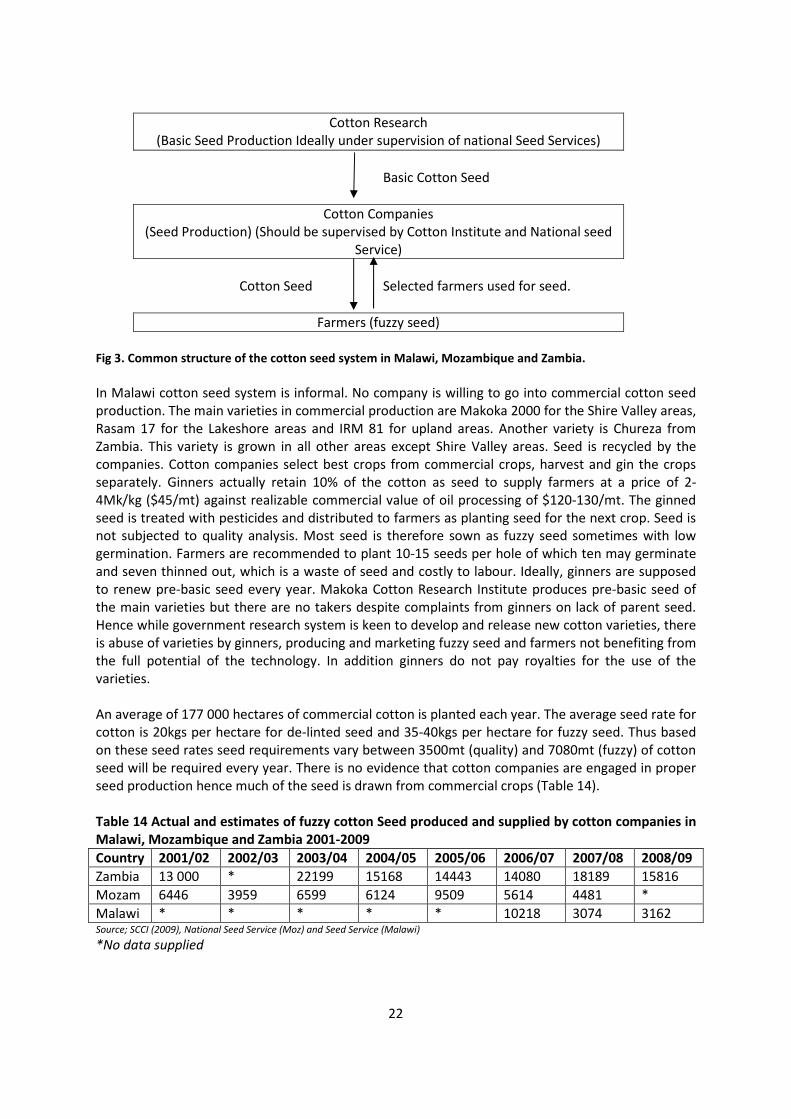

6 Cotton Seed System

If the formal seed system is partly defined with the presence of a seed company producing seed for

a particular crop from parent through to certified seed, then Malawi, Mozambique and Zambia have

an informal cotton seed system. Common among the countries is that seed is produced by ginners,

the same companies to distribute the seed to farmers. All seed is fuzzy, in other words, seed is

treated straight from the ginnery with no further de-linting. However, the structure of the current

informal cotton seed system consists of research, ginners and farmers (Fig 3)

22

Cotton Research

(Basic Seed Production Ideally under supervision of national Seed Services)

Basic Cotton Seed

Cotton Companies

(Seed Production) (Should be supervised by Cotton Institute and National seed

Service)

Cotton Seed Selected farmers used for seed.

Farmers (fuzzy seed)

Fig 3. Common structure of the cotton seed system in Malawi, Mozambique and Zambia.

In Malawi cotton seed system is informal. No company is willing to go into commercial cotton seed

production. The main varieties in commercial production are Makoka 2000 for the Shire Valley areas,

Rasam 17 for the Lakeshore areas and IRM 81 for upland areas. Another variety is Chureza from

Zambia. This variety is grown in all other areas except Shire Valley areas. Seed is recycled by the

companies. Cotton companies select best crops from commercial crops, harvest and gin the crops

separately. Ginners actually retain 10% of the cotton as seed to supply farmers at a price of 2-

4Mk/kg ($45/mt) against realizable commercial value of oil processing of $120-130/mt. The ginned

seed is treated with pesticides and distributed to farmers as planting seed for the next crop. Seed is

not subjected to quality analysis. Most seed is therefore sown as fuzzy seed sometimes with low

germination. Farmers are recommended to plant 10-15 seeds per hole of which ten may germinate

and seven thinned out, which is a waste of seed and costly to labour. Ideally, ginners are supposed

to renew pre-basic seed every year. Makoka Cotton Research Institute produces pre-basic seed of

the main varieties but there are no takers despite complaints from ginners on lack of parent seed.

Hence while government research system is keen to develop and release new cotton varieties, there

is abuse of varieties by ginners, producing and marketing fuzzy seed and farmers not benefiting from

the full potential of the technology. In addition ginners do not pay royalties for the use of the

varieties.

An average of 177 000 hectares of commercial cotton is planted each year. The average seed rate for

cotton is 20kgs per hectare for de-linted seed and 35-40kgs per hectare for fuzzy seed. Thus based

on these seed rates seed requirements vary between 3500mt (quality) and 7080mt (fuzzy) of cotton

seed will be required every year. There is no evidence that cotton companies are engaged in proper

seed production hence much of the seed is drawn from commercial crops (Table 14).

Table 14 Actual and estimates of fuzzy cotton Seed produced and supplied by cotton companies in

Malawi, Mozambique and Zambia 2001-2009

Country 2001/02 2002/03 2003/04 2004/05 2005/06 2006/07 2007/08 2008/09

Zambia 13 000 * 22199 15168 14443 14080 18189 15816

Mozam 6446 3959 6599 6124 9509 5614 4481 *

Malawi * * * * * 10218 3074 3162 Source; SCCI (2009), National Seed Service (Moz) and Seed Service (Malawi)

*No data supplied

23

Like Malawi, Mozambique does not have a cotton seed system. The key players in the cotton seed

system are Cotton Research Institute (Namialo), cotton companies, farmers and to some extent the

Seed Services Department. The Cotton Research Institute is attempting to clean the three main

varieties and produce pre-basic seed. There is no supervision of this activity from the National Seed

Services which is supposed to enforce quality measures. Pre-basic seed is sold to cotton companies

who multiply it into “certified” seed. There is again no supervision by the seed services department

to ensure seed is produced according to set standards. Crop is planted as commercial crop,

harvested, ginned and seed from the seed cotton used as seed. Seed is given to farmers for

production of commercial crop.

The main cotton varieties in Mozambique are ISA205, IRMA, 2123, REMU40, Stam42 and CA324.

Other varieties found in the cotton system are SZ9314 and FQ302 (both from Zimbabwe), F135 and

Chureza (both from Zambia) BLT-PF, L484, and 742D. Most of these varieties (except those from

Zambia and Zimbabwe), are heavily contaminated and there is need for germplasm screening to

purify them. Current breeding activities are crossing and screening of segregants, characterisation of

promising lines, evaluation for cultivation and use through multi location trials. While the norm is

new, a variety is released after vetting by the National Seed Committee, research proceeds with

basic seed production and distribution of the new varieties. However, because of limiting financial

resources, promising varieties remain on the shelves of the Cotton Research Institute. The current

focus of Cotton research Institute is therefore purification of the old varieties, production of pre-

basic seed (Fig 1) to sell to cotton companies although few companies would seek such services.

Cotton seed production is by the same ginners. In Malawi and Mozambique, ginners identify and

select good commercial crops. These are harvested and ginned separately for seed. There is no

guarantee the selected crop is pure variety and free from unwanted pests and diseases. Ideally

cotton companies are supposed to get pre-basic seed from cotton breeders for further multiplication

with assistance from the same. The seed is tested for purity and germination at the company

premises and lots which have germination ranging from 60-90% is treated with pesticide. In

Mozambique for example, one company last received basic seed of CA324 ten years ago and since

then has been recycling the same. Over the years, the company experienced decline in yields and is

currently purifying the same variety, planting populations on 25 hectares plot and carrying out a

selection process to remove possible contaminants or off types. This selection process is supposed

to have input from research who are familiar with variety characteristics but instead companies use

expensive consultants from outside Mozambique. Ideally cotton companies must produce cotton

seed under the supervision of Cotton Institute but this never happens (Fig 1). Some companies

actually import basic seed after 3-5years of recycling. In Malawi, the system is the same, ginners are

recycling seed with no protection against mixtures of varieties to ensure seed of variety genetic

purity. In both countries, national seed units have no control on cotton seed production.

Zambia cotton seed system has improved over the last 10 years. While the process of seed

production is the same as in Malawi and Mozambique (Fig 1), in Zambia, the certifying agency has

some control on seed production, ensuring all seed produced is ‘certified’. The process of seed

production is that ginners buy pre-basic seed from the Cotton Development Trust. The trust is

responsible for research and development in cotton, producing new varieties and pre-basic seed for

these varieties. Once they have purchased pre-basic seed, ginners produce basic and certified seed

under the supervision of the Seed Control and Certification Institute (SCCI). Each ginner is a

certifying agency, thus able to inspect own crop with random checks by SCCI. All seed crops are

registered with SCCI. There are only three varieties of cotton grown in Zambia, Chureza, CDT2 and

F135. To avoid contamination, SCCI has insisted each variety be confined to a particular area for seed

24

production. On average, seed crops pay 40-60% more than the commercial crops. Given that seed

crops are also grown in the same area as commercial crops and often in neighbourhoods, farmers

could offload some of their commercial crops to the neighbour for higher return as seed. This

contaminates the crop hence quality of the seed crop. Ginners have confirmed there is no protection

against such behaviour by farmers hence no full proof guarantee of quality of certified cotton seed.

As in Malawi and Mozambique harvested seed crop is just ginned and seed treated with pesticide.

There is no delinting, cleaning or grading. Such seed will be mixed with dead, light, diseased and

small kernels. This type of seed is commonly referred as FUZZY across the three countries. While the

seed is tested for germination, all the other analytical tests may be impossible or recommendations

for further cleaning impossible to implement.

The use of fuzzy seed has many disadvantages however. First, because of the lint, fuzzy seed sticks

together hence cannot be machine planted. This is probably why there are no commercial farmers in

cotton production. Seed cannot be machine planted. Sticky nature of seed also makes it difficult for

farmers to plant one seed at a hole. Farmers end up planting lumps of seed in each hole. This is

costly to farmers thinning the crop to suitable population and costly to farmers as more seed is

planted, 35-40kgs/ha instead of just 20kgs/ha. Fuzzy seed is ungraded and therefore mixture of

small, infected, bad and good seed. This may result in uneven germination due to differences in

vigour and disease.

7 Cassava Seed System

While cassava is a significant food crop in Malawi and Mozambique, there is no documented supply

system for planting material. In Malawi, annual production of 4.5million tons (fresh weight from 500

000ha) of cassava will require 5billion cuttings of planting material. While government and other

stakeholders have developed keen interest in cassava as a food security crop, farmers in Malawi rely

heavily on recycled planting material. According to the Department of crops, non-governmental

organizations (NGOs) are responsible for providing cassava planting material. In some cases,

however, researchers are requested to provide virus free nucleus planting material. Starting 2009,

government of Malawi is embarking on a community seed program for cassava multiplication, where

government contracts smallholder farmers to produce planting material. The government will buy

the material from farmers and distribute it to needy farmers. However, the challenges to this

program are lack of authentic varieties and cleanliness of the planting material produced.

Mozambique has also developed a cassava policy through CEPAGRI, to promote commercialization

of cassava by way of promoting large scale production of planting material. Currently there is no

documented proper planting material except the activities of some organizations promoting food

security in the country. For example, in Zambesia province, the Food and Agricultural Organization

(FAO) of the United Nations in collaboration with Mozambique government is working on a program

to provide quality planting material for cassava. Some 25,000 farming families will receive cassava

cuttings and seeds of high-yielding, resistant varieties.

Zambia has established the Cassava Task Force to promote and oversee the production of the crop.

The Mansa Agricultural Research Institute in Luapula Province, that has released a number of

improved varieties of Cassava (Table 14) which are now being multiplied into planting material for

farmers in various parts of the country.

25

Table 15 Cassava varieties released in Zambia

Variety Date Released Yield mt/ha Taste

Bangweulu* 1993 31 Bitter

Nalumino* 1993 29 Bitter

Kapumba 1993 22 Sweet

Mweru* 2000 41 Sweet

Chila* 2000 35 Bitter

Tanganyika* 2000 36 Sweet

Kampolombo* 2000 38 Sweet *varieties being multiplied at Alulusa

Production of planting material is led by Alulusa Ltd in Chisamba. This multiplication activity was

established in 2001 to provide virus free cassava planting material. The project was driven by the

growing demand and recognition of cassava as food security crop in Zambia. Currently 40ha of six

varieties of cassava is planted at various stages of development (Table 15). All the varieties are

registered with SCCI and therefore recognised for certified multiplication. Multiplication starts with

breeders material purchased from Mansa Research Station. Each crop is registered with SCCI. The

seed crops are inspected by SCCI at various stages of development. Virus or diseased plants are

removed and destroyed. Before harvest, each crop is inspected by SCCI and certified as quality

declared seed (QDS). Material is sold to various customers including NGOs and direct to farmers at

ZK30 000 (US$6.40) per bundle of 100sticks.

Alulusa is however, not able to meet national demand for cassava planting material. Being centrally

located and far away from the main cassava areas in the Northern and Luapula Provinces, transport

cost is a major challenge to customers as materials dry up when transported over long distances.

Another challenge is lack of market consistency.

8 Observations

8.1 Cotton Sector

• The cotton sectors of the three countries are characterised by unregulated and local

monopolies. This is typical in Mozambique where the concession system recognizes

provincial monopolies of cotton companies.

• The cotton pricing system is based on a commonly accepted principle that single channel

systems require guaranteed fixed prices throughout the cotton growing area (panterritorial),

throughout the cropping season (panseasonal) and announced before planting. Malawi

adopted a slightly different approach with unnecessary policy encroachment on cotton

pricing, setting obligatory prices too high for the viability of the cotton industry.

• There is regulatory vacuum especially in Malawi and Mozambique. There are no regulations

in place to guide cotton production especially the seed multiplication activities.

• Use of certified seed is not mandatory. 100% cotton seed informal and uncertified with

germination as low as 50% for seed given to farmers. In fact much of the cotton seed

planted is undelinted and in some cases ungraded or cleaned to remove diseased or light

seed. The undelinted seed is treated with pesticide. Seeding rate for such seed is 35-40kgs

per hectare compared to 15-20kgs per hectare for ginned, delinted and treated seed.

26

• Lack of appreciation by cotton companies on value of seed. Cotton companies have no t

invested in variety development and/or modern seed equipment to improve the quality of

seed they give to their growers.

• In Malawi and Mozambique, there are no pure and well maintained varieties for

multiplication. Cotton companies do not recognize the value of germplasm for them to pay

royalties to breeders to enable them to produce breeder seed.

• Lack of extension support for cotton farmers. Farmers make random choice of crops and in

some cases fail to balance cash and food crops. The food crops normally suffer increasing

the risk of food insecurity.

• Zoning of varieties implies that research has to multiply basic seed per zone. Resources and

logistics are a serious challenge.

• Weak farmers associations. Cotton companies deal directly with individual farmers

weakening farmers ability to negotiate proper deals. Farmers associations will enhance

collective approach. This is most evident in Malawi and Mozambique. In Zambia, the Zambia

National Farmers Union through the Cotton Association of Zambia (CAZ) assists smallholder

farmers in contract negotiation with ginners.

• Competition with other crops. In Mozambique cotton production affected by competition

from sesame while in Zambia, government input program on maize shifts production to

maize at the expense of maize.

• Lack of micro credit to support cotton production by small holder farmers

• Lack of technology e.g GMO and seed coating technology.

8.2 Cassava

• Cassava regarded as a poor man’s crop but there is recognition in all the three countries that

cassava is a key food security crop and therefore needs support. Zambia has even setup a

cassava task force to promote cassava production in the relevant areas such as the Northern

Province.

• There is no policy on cassava. However, Zambia and Mozambique is developing a policy to

promote cassava production supported by provision of quality planting material. Malawi is

yet to define policy on cassava.

• There is lack of planting materials. Farmers recycle material; often diseased and causing low

yields. Except in Zambia, there are no documented seed programs.

• Few farmers except in Zambia use improved varieties of cassava.

9 Recommended Strategies