COST OF CAPITAL LECTURE NOTES - COL Campus

19

COST OF CAPITAL LECTURE NOTES Prepared by Sara du Toit CA (SA) COPYRIGHT NOTICE Copyright © CA Campus These notes enjoy copyright under the Berne Convention. In terms of the Copyright Act, no 98 of 1978, no part of this material may be reprinted or reproduced, in any form whatsoever, either in whole or in part or by any electronic or other means including the making of photocopies thereof, without the express prior written consent of the proprietor, CA Campus. No individual may share any CA Campus content or material with any other person. The proprietor will not hesitate to prosecute any such offenders to the fullest extent of the law and to report their details to: • UNISA • The South African Institute of Chartered Accountants (SAICA) for purposes of barring such persons from registering as chartered accountants (SA), as such actions constitute a gross transgression of ethical principles, which is a violation of the code of professional conduct of SAICA • South African Police Service • Any other relevant professional body / organisation, including any employer

Transcript of COST OF CAPITAL LECTURE NOTES - COL Campus

COST OF CAPITAL

LECTURE NOTES

Prepared by Sara du Toit CA (SA)

COPYRIGHT NOTICE Copyright © CA Campus

These notes enjoy copyright under the Berne Convention. In terms of the Copyright Act, no 98 of 1978, no part

of this material may be reprinted or reproduced, in any form whatsoever, either in whole or in part or by any

electronic or other means including the making of photocopies thereof, without the express prior written

consent of the proprietor, CA Campus.

No individual may share any CA Campus content or material with any other person.

The proprietor will not hesitate to prosecute any such offenders to the fullest extent of the law and to report

their details to:

• UNISA

• The South African Institute of Chartered Accountants (SAICA) for purposes of barring such persons from

registering as chartered accountants (SA), as such actions constitute a gross transgression of ethical

principles, which is a violation of the code of professional conduct of SAICA

• South African Police Service

• Any other relevant professional body / organisation, including any employer

1 FOR USE BY CA CAMPUS STUDENTS ONLY

© CA Campus

RISK AND RETURN When shareholders buy shares in a company they are exposed to risk. The return required by an investor will depend on the level of risk they are exposed to. A rational investor would expect a higher return on a high risk investment.

• Business risk is the risk that relates to the operating activities of the company.

• Financial risk is the risk that relates to the level of debt within the company. Shareholders required return (Ke) = Business risk + Financial risk

Important capital structure ratios: Capital structure is the mix of debt and equity in financing the assets of the company.

STUDY THE FOLLOWING IMPORTANT FORMULAS:

Debt: Equity ratio = Non-current liabilities / Equity OR: = Non-current liabilities : Equity

Gearing ratio = Long-term debt / (Long-term debt + Equity)

REFER TO LECTURE EXAMPLES 1.1 – 1.3.

IMPORTANT PRINCIPLES: 1. The ratios should be calculated using market values and not book values. 2. The debt: equity ratio does not always give you the capital structure of the

company. It is therefore preferable to work the gearing ratio.

2 FOR USE BY CA CAMPUS STUDENTS ONLY

© CA Campus

THE ADVANTAGES & DISADVANTAGES OF DEBT The cost of debt is lower than the cost of equity for the following reasons:

o Providers of debt capital are prepared to accept a lower return because they are exposed to less risk: ▪ Interest and capital payments must be paid regardless of financial performance. ▪ In most instances debt is secured against assets. ▪ Providers of debt capital will rank above ordinary shareholders in the case of

liquidation. o Interest is tax deductible whereas dividends are not.

As the cost of debt is less than the cost of equity companies can use debt to improve returns to shareholders. The disadvantage of debt finance is that interest and capital repayments must be made regardless of financial performance. Using debt finance therefore exposes companies to financial risk which increases the return required by shareholders (cost of equity) and the interest rate charged by providers of debt capital (cost of debt).

REFER TO LECTURE EXAMPLE 2.1.

IMPORTANT PRINCIPLES: 1. Debt is cheaper than equity and can therefore be used to improve returns

to shareholders. 2. However, debt exposes the company to financial risk.

3 FOR USE BY CA CAMPUS STUDENTS ONLY

© CA Campus

CAPITAL STRUCTURE THEORIES

Please complete the rest of this lecture before working through this section. The discussion below will make more sense after you understand how WACC is calculated.

The Traditional Theory: The logic behind this theory is as debt increases:

• The WACC will decrease as debt is cheaper than equity.

• Moderate increases in debt do not increase the overall risk of the company and therefore the shareholders required rate of return (Ke) will not increase initially.

Therefore, initially as debt increases the WACC will decrease. As the company takes on debt the WACC continue to decrease up to a certain point. The optimal capital structure is where the WACC is at its lowest (as this is the point where the company value is maximised). After this optimal level any further increase in debt will increase financial risk and the shareholders will demand a higher return causing the WACC to increase.

The Miller and Modigliani Theory: The logic behind this theory is as debt increases:

• The WACC will decrease as debt is cheaper than equity.

• Simultaneously, due to the increase in financial risk shareholders will demand a higher return (i.e. the (Ke) will increase causing the WACC to increase).

These movements will be perfectly offset and the WACC will remain constant. This theory states that the value of a company is determine by its assets and not the manner in which those assets are financed. Therefore, as gearing increases/decreases the WACC will remain constant and no optimal capital structure exists. This theory makes a lot of assumptions which are not realistic and would seldom apply to South Africa. For example:

• Capital markets are perfect

• There are no transaction costs

• There is no taxation

• All relevant information is freely available

For the purposes of this course the traditional theory should be followed: The optimal capital structure is the point where the WACC is minimised and the company value is maximised.

4 FOR USE BY CA CAMPUS STUDENTS ONLY

© CA Campus

COST OF CAPITAL The weighted average cost of capital (WACC) represents the return that a company needs to achieve in order to fully compensate the debt and equity providers. It is the cost to finance the company.

USES OF WACC: • Capital investment appraisal

• Valuations

• Economic Value Added (EVA ⁽™⁾)

The cost of capital for the company is merely a mirror image of the return required by the investor:

• Interest paid by the company = interest received by the investor.

• Dividends paid by the company = dividends received by the investor.

COST OF EQUITY The cost of equity can be calculated using Gordon’s dividend growth model or the capital asset pricing model.

5 FOR USE BY CA CAMPUS STUDENTS ONLY

© CA Campus

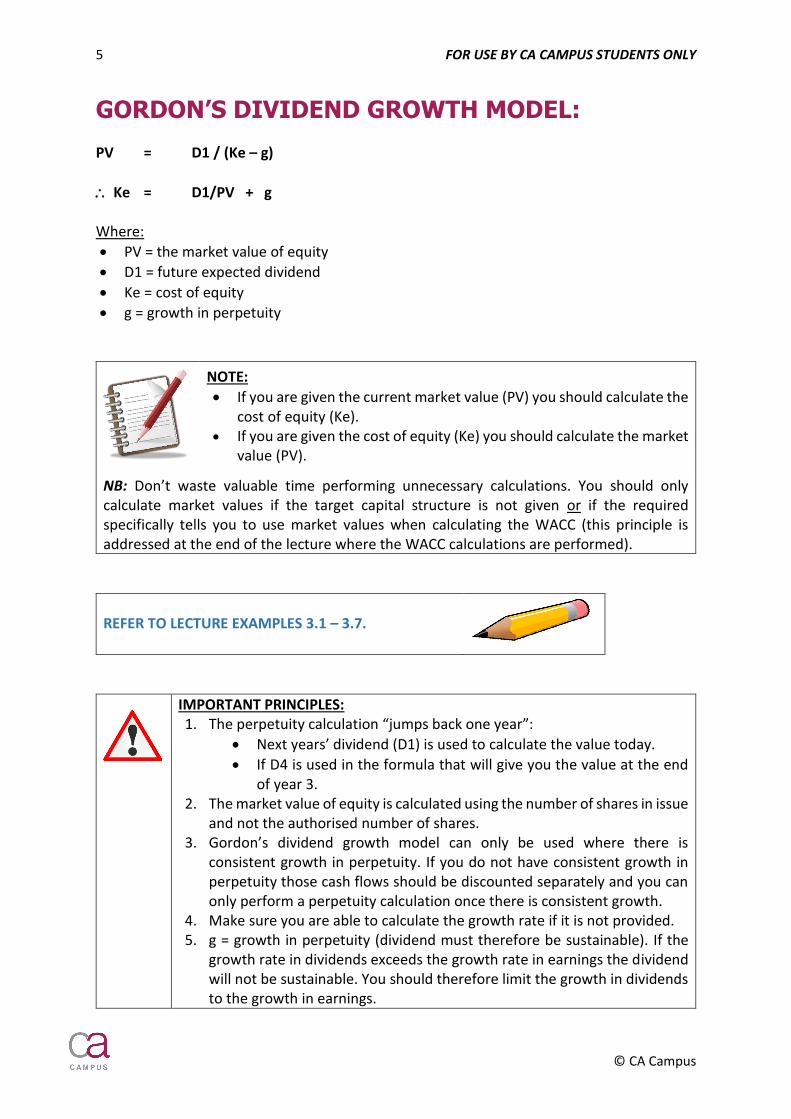

GORDON’S DIVIDEND GROWTH MODEL: PV = D1 / (Ke – g)

Ke = D1/PV + g Where:

• PV = the market value of equity

• D1 = future expected dividend

• Ke = cost of equity

• g = growth in perpetuity

NOTE:

• If you are given the current market value (PV) you should calculate the cost of equity (Ke).

• If you are given the cost of equity (Ke) you should calculate the market value (PV).

NB: Don’t waste valuable time performing unnecessary calculations. You should only calculate market values if the target capital structure is not given or if the required specifically tells you to use market values when calculating the WACC (this principle is addressed at the end of the lecture where the WACC calculations are performed).

REFER TO LECTURE EXAMPLES 3.1 – 3.7.

IMPORTANT PRINCIPLES: 1. The perpetuity calculation “jumps back one year”:

• Next years’ dividend (D1) is used to calculate the value today.

• If D4 is used in the formula that will give you the value at the end of year 3.

2. The market value of equity is calculated using the number of shares in issue and not the authorised number of shares.

3. Gordon’s dividend growth model can only be used where there is consistent growth in perpetuity. If you do not have consistent growth in perpetuity those cash flows should be discounted separately and you can only perform a perpetuity calculation once there is consistent growth.

4. Make sure you are able to calculate the growth rate if it is not provided. 5. g = growth in perpetuity (dividend must therefore be sustainable). If the

growth rate in dividends exceeds the growth rate in earnings the dividend will not be sustainable. You should therefore limit the growth in dividends to the growth in earnings.

6 FOR USE BY CA CAMPUS STUDENTS ONLY

© CA Campus

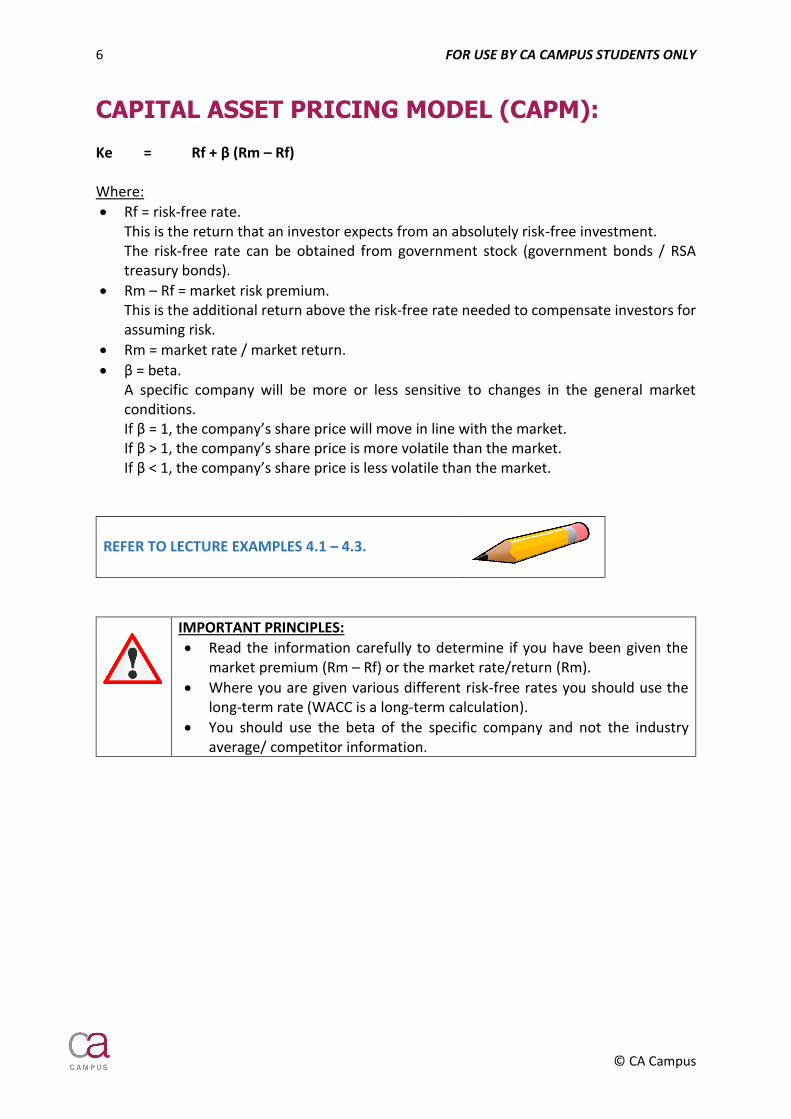

CAPITAL ASSET PRICING MODEL (CAPM): Ke = Rf + β (Rm – Rf) Where:

• Rf = risk-free rate. This is the return that an investor expects from an absolutely risk-free investment. The risk-free rate can be obtained from government stock (government bonds / RSA treasury bonds).

• Rm – Rf = market risk premium. This is the additional return above the risk-free rate needed to compensate investors for assuming risk.

• Rm = market rate / market return.

• β = beta. A specific company will be more or less sensitive to changes in the general market conditions. If β = 1, the company’s share price will move in line with the market. If β > 1, the company’s share price is more volatile than the market. If β < 1, the company’s share price is less volatile than the market.

REFER TO LECTURE EXAMPLES 4.1 – 4.3.

IMPORTANT PRINCIPLES:

• Read the information carefully to determine if you have been given the market premium (Rm – Rf) or the market rate/return (Rm).

• Where you are given various different risk-free rates you should use the long-term rate (WACC is a long-term calculation).

• You should use the beta of the specific company and not the industry average/ competitor information.

7 FOR USE BY CA CAMPUS STUDENTS ONLY

© CA Campus

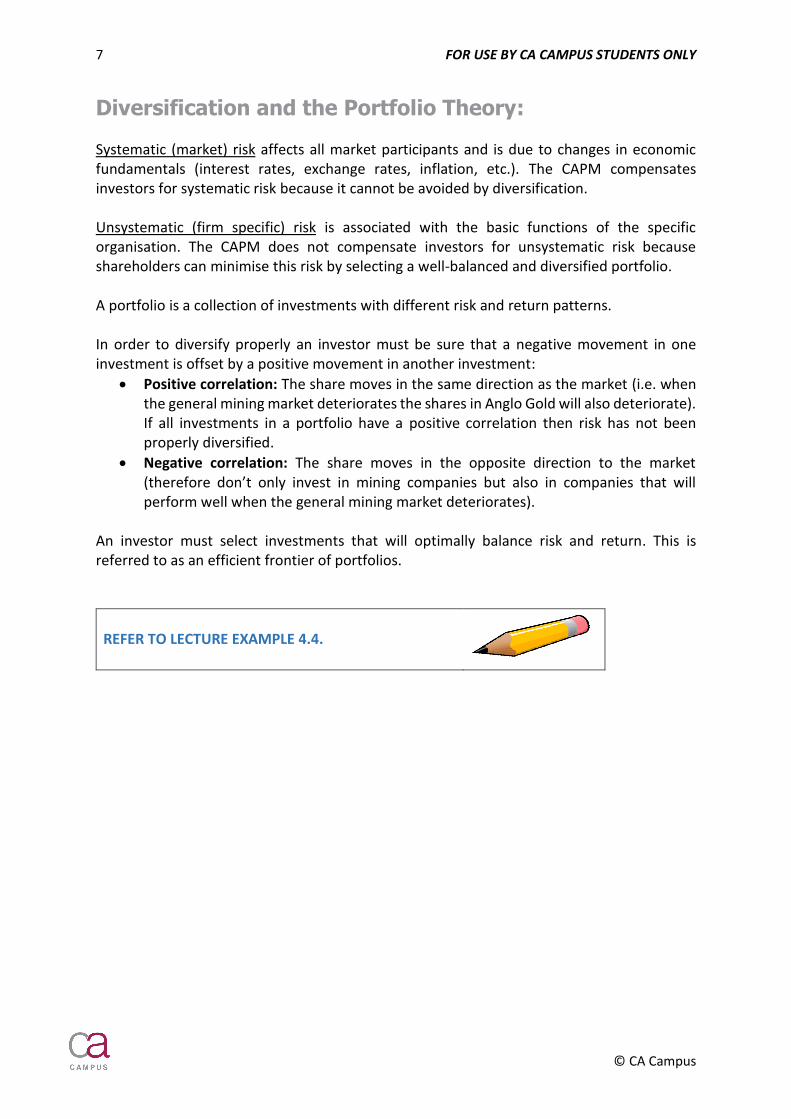

Diversification and the Portfolio Theory: Systematic (market) risk affects all market participants and is due to changes in economic fundamentals (interest rates, exchange rates, inflation, etc.). The CAPM compensates investors for systematic risk because it cannot be avoided by diversification. Unsystematic (firm specific) risk is associated with the basic functions of the specific organisation. The CAPM does not compensate investors for unsystematic risk because shareholders can minimise this risk by selecting a well-balanced and diversified portfolio. A portfolio is a collection of investments with different risk and return patterns. In order to diversify properly an investor must be sure that a negative movement in one investment is offset by a positive movement in another investment:

• Positive correlation: The share moves in the same direction as the market (i.e. when the general mining market deteriorates the shares in Anglo Gold will also deteriorate). If all investments in a portfolio have a positive correlation then risk has not been properly diversified.

• Negative correlation: The share moves in the opposite direction to the market (therefore don’t only invest in mining companies but also in companies that will perform well when the general mining market deteriorates).

An investor must select investments that will optimally balance risk and return. This is referred to as an efficient frontier of portfolios.

REFER TO LECTURE EXAMPLE 4.4.

8 FOR USE BY CA CAMPUS STUDENTS ONLY

© CA Campus

Asset vs. Equity Beta: The asset beta (ungeared or unlevered beta) does not take financial risk into account. The equity beta (geared or levered beta) takes financial risk into account.

You should use the equity beta when calculating the cost of equity using the CAPM.

If you need to calculate beta for an unlisted (private) company you will use a proxy beta of a similar listed company as your starting point. The entities will have different capital structures, therefore, first calculate the asset beta of the similar listed company using the following formula: β (ungeared / asset beta) = β (geared) x E . E + D(1 – t) Then calculate the equity beta taking the unlisted (private) company’s capital structure into account: β (geared / equity beta) = β (ungeared) x E + D (1 – t) E

REFER TO LECTURE EXAMPLE 4.5.

9 FOR USE BY CA CAMPUS STUDENTS ONLY

© CA Campus

COST OF PREFERENCE SHARES IMPORTANT TERMINOLOGY:

• Coupon rate: This rate should be used to calculate the dividend cash flow.

• Market-related rate / fair rate / rate on similar preference shares (Kp): This is the current / ruling market rate of return. It is obtained from similar publically traded instruments. This should be used as the discount rate when calculating the market value of the preference shares.

NOTE:

• If you are given the current market value (PV) you should calculate the cost of the preference shares (Kp).

• If you are given the cost of the preference shares (Kp) you should calculate the market value (PV).

NB: Don’t waste valuable time performing unnecessary calculations. You should only calculate market values if the target capital structure is not given or if the required specifically tells you to use market values when calculating the WACC (this principle is addressed at the end of the lecture where the WACC calculations are performed).

Non-redeemable preference shares:

PV = D / Kp

Kp = D / PV Where:

• PV = the market value of preference shares

• D = dividend cash flow

• Kp = cost of preference shares

REFER TO LECTURE EXAMPLES 5.1 & 5.2.

COMPANY ISSUES

PREFERENCE SHARES

TO RAISE FINANCE

(CASH INFLOW)

SHARES ARE NOT REPAID.

THEREFORE DIVIDENDS ARE PAID

IN PERPETUITY (CASH OUTFLOW)

10 FOR USE BY CA CAMPUS STUDENTS ONLY

© CA Campus

Redeemable preference shares:

1. USING THE CASH FLOW FUNCTION ON YOUR CALCULATOR:

This method can always be used.

If you are given the current market value (PV) and you are required to calculate the cost of

the preference shares (Kp):

0 1 2 3 4

Dividend cash flow (XX) (XX) (XX) (XX) Redemption amount (XXXX) Market value (PV) XXXX

Total cash flows XXXX cfj

(XX) cfj

(XX) cfj

(XX) cfj

(XXXX) cfj

i = Kp

If you are given the cost of the preference shares (Kp) and you are required to calculate the

market value (PV):

0 1 2 3 4

Dividend cash flow (XX) (XX) (XX) (XX) Redemption amount (XXXX)

Total cash flows 0 cfj

(XX) cfj

(XX) cfj

(XX) cfj

(XXXX) cfj

i = Kp

NPC = Market value

COMPANY ISSUES

PREFERENCE SHARES

TO RAISE FINANCE

(CASH INFLOW)

DIVIDENDS ARE PAID AT

REGULAR INTERVALS

(CASH OUTFLOW)

SHARES ARE

REDEEMED / REPAID

(CASH OUTFLOW)

11 FOR USE BY CA CAMPUS STUDENTS ONLY

© CA Campus

2. SHORTCUT:

This method can only be used if the annual cash flows (PMT) are equal.

PMT = dividend cash flow FV = redemption amount n = number of years PV = market value i = Kp

REFER TO LECTURE EXAMPLES 5.3 & 5.4.

Convertible preference shares:

STEP 1: CALCULATE THE FUTURE VALUE OF EACH ALTERNATIVE

• If the shares are convertible at the option of the company select the alternative with

the lowest cost.

• If the shares are convertible at the option of the investor select the alternative with

the highest value.

STEP 2: CALCULATE THE MARKET VALUE / COST OF THE PREFERENCE SHARES

REFER TO LECTURE EXAMPLE 5.5.

COMPANY ISSUES

PREFERENCE SHARES

TO RAISE FINANCE

(CASH INFLOW)

DIVIDENDS ARE PAID AT

REGULAR INTERVALS

(CASH OUTFLOW)

SHARES ARE CONVERTED AT

THE OPTION OF THE

COMPANY / INVESTOR

(SHOWN AS CASH OUTFLOW)

12 FOR USE BY CA CAMPUS STUDENTS ONLY

© CA Campus

IMPORTANT PRINCIPLES:

• The dividend cash flow is calculated using: o The nominal/par value of the preference shares (any premiums/

discounts are ignored). o The coupon rate (and not the Kp).

• Only future cash flows should be taken into account when calculating either the cost (Kp) or the market value.

• The cost of the preference shares (Kp) is used as the discount rate when calculating the market value.

EXAM TECHNIQUE:

• The direction of cash flows must be correct.

• Dividends are paid on preference shares. Dividends are not deductible for tax purposes regardless of whether the preference shares are classified as debt / equity.

13 FOR USE BY CA CAMPUS STUDENTS ONLY

© CA Campus

COST OF DEBT IMPORTANT TERMINOLOGY:

• Coupon rate: This rate should be used to calculate the interest cash flow.

• Market-related rate / fair rate / rate on similar debt instruments (Kd): This is the current / ruling market rate of return. It is obtained from similar publically traded instruments. This should be used as the discount rate when calculating the market value of debt.

NOTE:

• If you are given the current market value (PV) you should calculate the cost of debt (Kd).

• If you are given the cost of debt (Kd) you should calculate the market value (PV).

NB: Don’t waste valuable time performing unnecessary calculations. You should only calculate market values if the target capital structure is not given or if the required specifically tells you to use market values when calculating the WACC (this principle is addressed at the end of the lecture where the WACC calculations are performed).

Interest is deductible for tax purposes: The interest cash flow and the cost of debt (Kd) should always be after tax!!

14 FOR USE BY CA CAMPUS STUDENTS ONLY

© CA Campus

Non-redeemable debt: PV = I / Kd

Kd = I / PV Where:

• PV = the market value of debt

• I = interest cash flow (after tax)

• Kd = cost of debt (after tax)

A loan which does not require repayment would also be classified as non-redeemable debt:

• Company enters into loan agreement to raise finance (CASH INFLOW).

• The loan is not repaid and therefore interest is paid in perpetuity (CASH OUTFLOW).

REFER TO LECTURE EXAMPLES 6.1 & 6.2.

COMPANY ISSUES

DEBENTURES TO

RAISE FINANCE

(CASH INFLOW)

DEBENTURES ARE NOT REPAID.

THEREFORE INTEREST IS PAID IN

PERPETUITY (CASH OUTFLOW)

15 FOR USE BY CA CAMPUS STUDENTS ONLY

© CA Campus

Redeemable debt:

1. USING THE CASH FLOW FUNCTION ON YOUR CALCULATOR:

This method can always be used.

If you are given the current market value (PV) and you are required to calculate the cost of

debt (Kd):

0 1 2 3 4

Interest cash flow (after tax) (XX) (XX) (XX) (XX) Redemption amount (XXXX) Market value (PV) XXXX

Total cash flows XXXX cfj

(XX) cfj

(XX) cfj

(XX) cfj

(XXXX) cfj

i = Kd (after tax)

If you are given the cost of debt (Kd) and you are required to calculate the market value

(PV):

0 1 2 3 4

Interest cash flow (after tax) (XX) (XX) (XX) (XX) Redemption amount (XXXX)

Total cash flows 0 cfj

(XX) cfj

(XX) cfj

(XX) cfj

(XXXX) cfj

i = Kd (after tax)

NPC = Market value

COMPANY ISSUES

DEBENTURES TO

RAISE FINANCE

(CASH INFLOW)

INTEREST IS PAID AT

REGULAR INTERVALS

(CASH OUTFLOW)

DEBENTURES ARE

REDEEMED / REPAID

(CASH OUTFLOW)

16 FOR USE BY CA CAMPUS STUDENTS ONLY

© CA Campus

2. SHORTCUT:

This method can only be used if the annual cash flows (PMT) are equal.

PMT = interest cash flow (after tax) FV = redemption amount n = number of years PV = market value i = Kd (after tax)

A loan which requires repayment would also be classified as redeemable debt:

• Company enters into loan agreement to raise finance (CASH INFLOW).

• NB: Read the question carefully to determine when interest and capital repayments are made (CASH OUTFLOWS).

REFER TO LECTURE EXAMPLES 6.3 - 6.8.

Convertible debt:

STEP 1: CALCULATE THE FUTURE VALUE OF EACH ALTERNATIVE

• If the debentures are convertible at the option of the company select the alternative

with the lowest cost.

• If the debentures are convertible at the option of the investor select the alternative

with the highest value.

STEP 2: CALCULATE THE MARKET VALUE / COST OF DEBT

REFER TO LECTURE EXAMPLE 6.9.

COMPANY ISSUES

DEBENTURES TO

RAISE FINANCE

(CASH INFLOW)

INTEREST IS PAID AT

REGULAR INTERVALS

(CASH OUTFLOW)

DEBENTURES ARE CONVERTED

AT THE OPTION OF THE

COMPANY / INVESTOR

(SHOWN AS CASH OUTFLOW)

17 FOR USE BY CA CAMPUS STUDENTS ONLY

© CA Campus

IMPORTANT PRINCIPLES:

• Interest is deductible for tax purposes (both the interest cash flow and the cost of debt should be after tax).

• The interest cash flow is calculated using the nominal/par value of debentures (any premiums/discounts are ignored).

• The interest cash flow is calculated using the coupon rate (and not the Kd).

• The cost of debt (Kd) is used as the discount rate when calculating the market value.

• Only future cash flows should be taken into account when calculating either the cost (Kd) or the market value.

• Section 24J - company gets the tax deduction as the interest accrues over the period (not when it’s actually paid).

• Unless specifically told otherwise you can assume that all payments are made in arrears (i.e. at the end of the period).

EXAM TECHNIQUE:

• The direction of cash flows must be correct. Interest is deductible for tax purposes (this is a saving / cash inflow).

• Clearly show the tax rate used in your calculations.

18 FOR USE BY CA CAMPUS STUDENTS ONLY

© CA Campus

WEIGHTED AVERAGE COST OF CAPITAL (WACC)

REFER TO LECTURE EXAMPLES 7.1 – 7.7.

IMPORTANT PRINCIPLES:

• The market value of equity is calculated: o Using the number of shares in issue and not the authorised share

capital. o Using the current share price and not the price at which the shares

were initially issued. Retained income and any other capital reserves should not be added to the value calculated.

• Unless the required specifically states otherwise: o If the target capital structure is provided you should use the target to

calculate the WACC. Don’t waste valuable time calculating market values!! The target WACC is the correct rate as it reflects the desired capital structure of the company and the return required by shareholders after allowing for risk.

o If the target capital structure is not provided you should use market values to calculate the WACC. You can assume that the current market values represent the target. Companies will not always be at their target capital structure. They may be in a position of temporary disequilibrium. However, they will always strive to move closer towards the target capital structure when raising new funds.

• If preference shares / debentures are going to convert into ordinary shares then the cost of equity should be used in the WACC calculation (not the cost of the preference shares (Kp) / debentures (Kd)).

• Only include long-term / permanent sources of capital in the WACC calculation. Bank overdrafts should only be included if used as long-term capital (and not to finance working capital).

• The WACC includes the effect of inflation.

EXAM TECHNIQUE:

• Clearly show that the total weighting adds up to 100%.

• If you are provided with a bank overdraft which is used for working capital purposes don’t just ignore it! You need to show the examiner that you understand it should be excluded from the WACC calculation.