Cost of Capital- India Survey - EY - United States · EY released the second edition of ‘Cost of...

4

Cost of Capital- India Survey Lifesciences Sector

Transcript of Cost of Capital- India Survey - EY - United States · EY released the second edition of ‘Cost of...

Cost of Capital- India Survey Lifesciences Sector

• The respondents estimate that the cost of equity for the lifesciences sector has moved up to 15.5% in 2017 as compared to 14.9% in the cost of capital survey conducted by EY in 2014. This increase is despite decline in interest rates by ~200 basis points during the same period.

• 50% of respondents in the lifesciences space use an organisation specific hurdle rate (such as a thumb rule rate or IRR) to determine the discount rate vis-à-vis 43% of the overall respondents in the survey

• ~64% of the respondents suggested that long term stable growth rate for Indian businesses under Lifesciences sector is 5% or less, which is in line with expected long term inflation rate in India. 59% respondents use exit multiple method to arrive at the terminal value.

• 50% of the respondents consider the discount rate to be more than 20% while evaluating acquisitions of in-process research and development targets.

43%

14%

0%

29%

36% 36%

21%

14%

0%7%

<12% 12%-15% 15%-18% 18%-20% >20%

Resp

onde

nts

(%)

Discount rate (%)

2017

2014

14%19%

<12%

29%

37%

12%-15%

36%

28%

15%-18%

14%10%

18%-20%

7% 5%

>20%

Resp

onde

nts

(%)

Discount rate (%)

Lifesciences

Overall

More than 40% of the respondents in the 2014 survey estimated the cost of equity to be less than 12% as

compared to 14% in the current survey. On the other hand, 29% respondents estimated the cost of equity

to be in between 12 – 15% as compared to none of the respondents in the 2014 survey

In the 2014 survey, 29% of the respondents indicated that they were not making any alpha adjustments. This has gone down to 0% in the current survey and all respondents admitted to making some alpha

adjustment to arrive at their cost of capital.

The average cost of equity for Lifesciences sector is estimated to be 15.5% as

compared to average cost of equity for all industries which is 14.9%

Survey 2017

Survey 2014

0%-2% 2%-4% 4%-7% ">7%" None

35%

0% 0%

29%

36%

18%

0%36%

46%

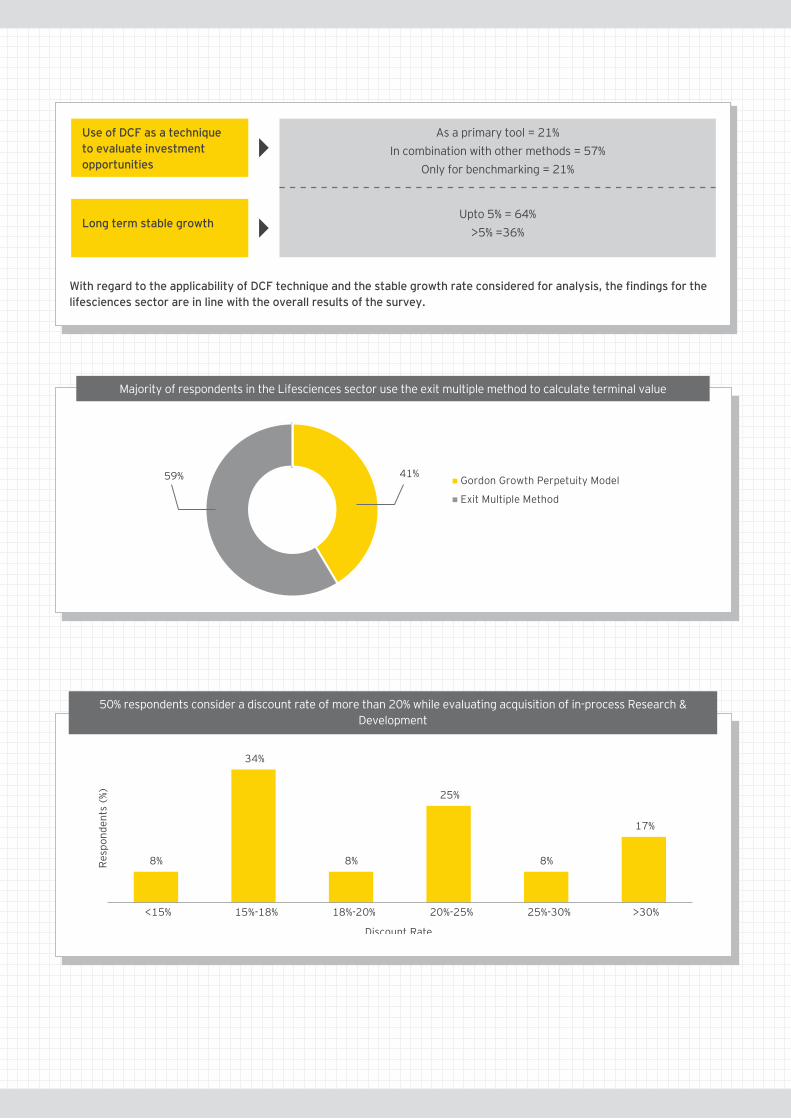

Gordon Growth Perpetuity Model

Exit Multiple Method

41%59%

Majority of respondents in the Lifesciences sector use the exit multiple method to calculate terminal value

50% respondents consider a discount rate of more than 20% while evaluating acquisition of in-process Research & Development

With regard to the applicability of DCF technique and the stable growth rate considered for analysis, the findings for the lifesciences sector are in line with the overall results of the survey.

Use of DCF as a technique to evaluate investment opportunities

As a primary tool = 21%In combination with other methods = 57%

Only for benchmarking = 21%

Upto 5% = 64%>5% =36%

Long term stable growth

8%

34%

8%

25%

8%

17%

<15% 15%-18% 18%-20% 20%-25% 25%-30% >30%

Resp

onde

nts

(%)

Discount Rate

About EYEY is a global leader in assurance, tax, transaction and advisory services. The insights and quality services we deliver help build trust and confidence in the capital markets and in economies the world over. We develop outstanding leaders who team to deliver on our promises to all of our stakeholders. In so doing, we play a critical role in building a better working world for our people, for our clients and for our communities.

EY refers to the global organization, and may refer to one or more, of the member firms of Ernst & Young Global Limited, each of which is a separate legal entity. Ernst & Young Global Limited, a UK company limited by guarantee, does not provide services to clients. For more information about our organization, please visit ey.com.

Ernst & Young LLP is one of the Indian client serving member firms of EYGM Limited. For more information about our organization, please visit www.ey.com/in.

Ernst & Young LLP is a Limited Liability Partnership, registered under the Limited Liability Partnership Act, 2008 in India, having its registered office at 22 Camac Street, 3rd Floor, Block C, Kolkata - 700016

© 2017 Ernst & Young LLP. Published in India. All Rights Reserved.

EYIN1707-075 ED None

This publication contains information in summary form and is therefore intended for general guidance only. It is not intended to be a substitute for detailed research or the exercise of professional judgment. Neither Ernst & Young LLP nor any other member of the global Ernst & Young organization can accept any responsibility for loss occasioned to any person acting or refraining from action as a result of any material in this publication. On any specific matter, reference should be made to the appropriate advisor.

VN

Ernst & Young LLPEY | Assurance | Tax | Transactions | Advisory

EY refers to the global organization, and/or one or more of the independent member firms of Ernst & Young Global Limited

ey.com/in

EY India

@EY_India EY|LinkedIn

EY India careers

About Cost of Capital – India survey, 2017

Our contacts

EY released the second edition of ‘Cost of capital - India survey, 2017’. The survey report aims to understand the threshold cost of equity that India Inc. uses for its capital allocation and investment decisions and the process by which practicing finance professionals in the industry make capital costing decisions. The survey this year covered a sample size of 135 response sets from finance professionals in companies across various sectors and representation from listed, unlisted, Indian and multinational companies.

Parag MehtaPartner – Valuations & Business Modeling, [email protected]+91 22 6192 1335

Mihir KeniaDirector – Valuations & Business Modeling, [email protected]+91 22 6192 1137

Arun RathnamAssociate Vice President – Valuations & Business Modeling ,[email protected]+91 80 6727 5602