Cortex MCP Mobile Wallet Ecosystem Q2 2014 NL

36

Mobile Wallet Ecosystem Overview and Market Analysis Rob Stringer, VP Products, Cortex MCP, Inc ABSTRACT To succeed in creating value in the mobile wallet ecosystem it helps to understand the roles, ambitions, strengths and weaknesses of the marketplace. This eBook tends towards the payment side of wallets, rather than brands.

Transcript of Cortex MCP Mobile Wallet Ecosystem Q2 2014 NL

Mobile Wallet Ecosystem Overview and Market Analysis

Rob Stringer, VP Products, Cortex MCP, Inc

ABSTRACT To succeed in creating value in the mobile wallet ecosystem it helps to understand the roles, ambitions, strengths and weaknesses of the marketplace. This eBook tends towards the payment side of wallets, rather than brands.

Mobile Wallet Ecosystem Overview

Cortex MCP, Inc. All rights reserved 2

Table of Contents

INTRODUCTION 3

CHAPTER 1: CARD CONTROLLERS 8 CARD NETWORKS 8 CARD-‐ON-‐FILE MERCHANTS 11 DIGITAL ASSET COMPANIES 14

CHAPTER 2: MERCHANTS 19

CHAPTER 3: CARRIERS 22

CHAPTER 4: DEVICE MANUFACTURERS 26

CHAPTER 5: CONSUMERS 31

LOOKING AHEAD 35

ABOUT THE AUTHOR 36

Mobile Wallet Ecosystem Overview

Cortex MCP, Inc. All rights reserved 3

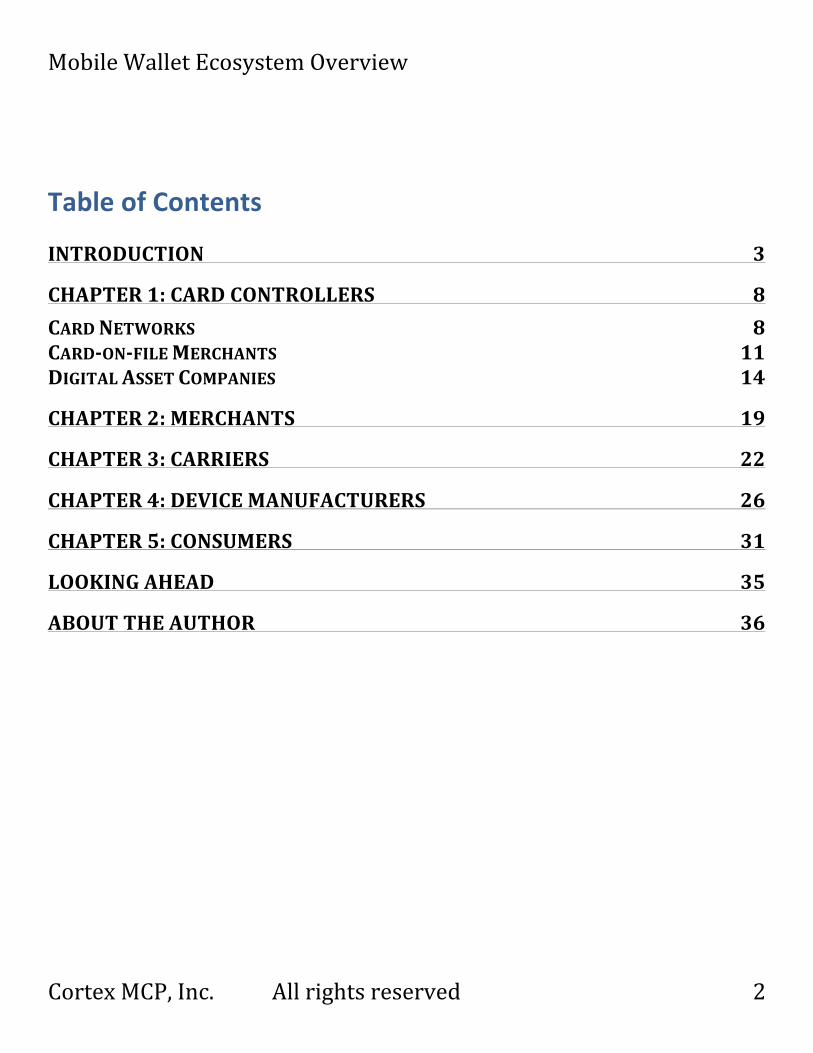

Introduction An understanding of the key stakeholders involved in the effort to make mobile payment, loyalty and digital wallets universal realities leads to a better appreciation of the complexity of the challenge. Recently, we kicked off the discussion of mobile payment, loyalty and digital wallets with a promise that we would offer insights into the state of the market with ideas on how the obstacles that have hampered development can be overcome. We want to take a step back to provide some background on the players that make up today’s electronic payment ecosystem. It is important to note that any mobile digital wallet implementation has to take each constituent into consideration. There are very few players in the world, if any, that could try and “go it alone” and force a mobile payments system on the rest of the world without giving something up in return. So with this as the backdrop, here’s a look at the current payment ecosystem.

Mobile Wallet Ecosystem Overview

Cortex MCP, Inc. All rights reserved 4

The Card Controllers First, there are those who own the “card” or the account data. There are many types of card controllers, including the incumbent payment vehicle networks: Visa, MasterCard, Discover, American Express, etc. – that are working hard to remain relevant as acceptance of mobile payments grows among merchants and consumers. These networks set the rules for the accounts and license issuers to distribute the accounts to the general population so more transactions run over their network. These incumbent players “control” their card numbers and how they are distributed, and can even set guidelines for what kind of data is accessible for an electronic transaction. Large digital entities that have no physical presence but have large card-‐on-‐file populations — Facebook, Google, e-‐Bay/PayPal, Amazon and Yahoo, to name a few -‐-‐ also can be seen as “controlling” the account data, i.e. they have access to this data in a multichannel environment, since consumers have keyed in that data to shop on their digital sites (or app stores). Also included in this second tier are entities with some physical presence under their control along with large “card-‐on-‐file” populations, such as Apple and Microsoft. These players are also interested in finding ways to retain customers as they move to mobile payments.

Merchants The merchant group includes physical retailers, with a large card-‐on-‐file population and owners of the “points of acceptance” of the

Mobile Wallet Ecosystem Overview

Cortex MCP, Inc. All rights reserved 5

electronic card account data (POS terminals. This group includes members of the Merchant Customer Exchange (MCX) and companies like McDonalds and Starbucks that must provide a mobile payment solution their customers accept as secure so as to avoid the damage suffered by Target last year.

Carriers The carriers are represented by ISIS, a joint venture among Verizon Wireless, AT&T Mobility, and T-‐Mobile USA to move the carriers deeper into the mobile payments arena. Carriers can control what hardware features the device manufacturers put on the devices that are distributed to the customers of these mobile network operators.

Device Manufacturers This group includes the companies that own the mobile device -‐-‐ Apple, Samsung, Motorola and others who need to build in the capabilities and features that will enable their mobile devices to fulfill the promise of mobile payments and digital wallets. This device could be in the form of phones or other wearable technologies, with secure apps that make transacting easier than it is today.

Consumers Last, and most important of all, are the consumers. Consumers will only use a mobile payment system they think is secure and is as easy as shopping today with their current card or with cash. The app has

Mobile Wallet Ecosystem Overview

Cortex MCP, Inc. All rights reserved 6

to get on their mobile device seamlessly, has to be accessible at the time of sale with minimal effort, and has to provide the cross-‐channel loyalty benefits users have come to expect. To make the consumer use their product, all of the stakeholders on the business end have to concentrate on the user experience, otherwise the consumer will rate the experience with their feet and shop at another store. All of these stakeholders have their own challenges and priorities. All (with the exception of consumers, of course) are offering solutions. A few are even collaborating. Yet there’s still widespread disagreement on a number of critical fronts. The one common point they all share: All of these factions are fighting the mobile payment war with weapons that are to date ineffective. We believe that what’s needed is a new foundation upon which all of these players can work – a platform that is hardware independent and integrates both a new secure payment methodology and ID/credential storage and verification capabilities. This is what Cortex MCP is bringing to this battle: a solution that will bring together the controller of the card, the POS and the mobile device. One will have a better sense of how this solution will work and how it differs from the current approaches as we analyze the game plans of the groups involved in the mobile payment wars.

Mobile Wallet Ecosystem Overview

Cortex MCP, Inc. All rights reserved 7

As we move through this analysis, we are assuming that mobile payments means not only paying for goods and services on a mobile phone, but paying with your phone at a physical retail outlet.

Mobile Wallet Ecosystem Overview

Cortex MCP, Inc. All rights reserved 8

Chapter 1: Card Controllers Let’s turn our attention to a group that is heavily invested in mobile payments: the card controllers. Card controllers are defined as those that own the card or account data: the card networks and their allies such as Visa, MasterCard, Discover, American Express and the acquirers); card-‐on-‐file merchants like Target, Wal-‐Mart, ToysRUs and Macys; and digital assets companies like Google, PayPal, Amazon, Facebook and Apple, that sell physical assets on-‐line with little-‐to-‐no physical POS presence (of note). While card controllers is a diverse group, the ownership of card or account data is a common denominator. By owning, we mean that they could legally own it (in terms of the networks) or just have enough control over that data that they can manipulate it for their wallet (card-‐on-‐file retailers and digital asset companies). Each of these types of card controllers have different powers, strategies, and abilities to influence the marketplace.

Card Networks We’ll begin with an analysis of those card controllers with the most power -‐-‐ the card networks, which set the regulations and pricing around the use of the primary account numbers (PANs) associated with a consumer’s credit account balance (How powerful? Visa threw off $1.2 billion in net income in Q4 alone last year).

Mobile Wallet Ecosystem Overview

Cortex MCP, Inc. All rights reserved 9

Card networks have a lot to lose as their traditional card business becomes more and more electronic and mobile. The PAN was not designed to be used this way. To combat this risk, the networks have formed an alliance, and together with EMVco, have created a new set of rules and regulations around tokenization of the PAN to ensure a more secure environment in today’s digital and mobile world to help

keep transaction volume running on their rails. Questions still remain on how these networks are going to implement this tokenization standard, who else in the ecosystem has to change in order for this to become a reality, and if this alliance can stay strong in the face of competitive pressures.

One can be certain that each member of the alliance is also working with other players to hedge their bets on the outcome. The risk is just too great for any entity to put all of their eggs in one basket. Regardless, as the entities that set pricing for in-‐store versus on-‐line commerce for the most common electronic payment choice of consumers, the networks will play a key role in what technology is adopted by the industry. Merchants will not invest in accepting

Mobile Wallet Ecosystem Overview

Cortex MCP, Inc. All rights reserved 10

digital wallets at scale – not if it means increasing their cost of payment acceptance for credit and debit. The networks have powerful industry partners in the acquirers and issuers that can build up walls to protect their turf (and the top-‐line) and inhibit the integration of other mobile wallets into their POS systems. The networks have a great opportunity to maintain and grow their “share of wallet” by partnering with other wallet “brands” to ensure a steady flow of credit and debit volume in the new Omni-‐channel digital world, protecting themselves and close allies. The biggest threat to this group is that consumers will migrate to alternative payment methods that are more convenient and readily available than traditional credit and debit cards. Alternative payments take volume out of the system, but even those mobile wallet providers running on the network’s rails are changing the transaction model and have the potential to hurt revenue. LevelUp, for example has changed the game in that they have cut down on the number of transactions (and thus reducing their fees) that flow through their wallet by aggregating the month’s transactions and processing them all at once. LevelUp still pays the merchant daily, but only processes the customers’ cards once a month, avoiding multiple transaction fees. Has LevelUp scaled yet? No, and they may be taking a risk of default that can’t scale, but theirs remains a model that has others thinking

Mobile Wallet Ecosystem Overview

Cortex MCP, Inc. All rights reserved 11

about changing the payments landscape to fit a mobile and digital age. (see PayPal, Square and others) The incumbent networks have the most to lose in this scenario, not only to each other, but to alternative payment vehicles. Will they be able to see the forest for the trees? That’s a question we are all waiting to find out the answer to.

Card-‐on-‐file Merchants Visa, MasterCard, Discover, American Express and other credit card networks wield mighty swords in the mobile payment wars, but there are other card controller players that play an important role in this battle: card-‐on-‐file merchants and digital asset companies. The card-‐on-‐file group includes merchants that have both a physical POS infrastructure in place and a strong on-‐line card-‐on-‐file and rewards population – merchants like Target, Wal-‐Mart, ToysRUs and Macys (MCX anyone?). This group of card controllers is currently at the mercy of the networks, since to date all of the “cards on file” are there as a result of key entry (card not present, or CNP, rates for transactions that run over the incumbent networks). While large card-‐on-‐file merchants have leverage, in that they “own” the customer and can more easily provide a true omni-‐channel experience, the cost of accepting CNP transactions in-‐store and at scale is not tenable. One major benefit that the merchants have over the networks is that in their card-‐on-‐file systems, consumers are already comfortable putting

Mobile Wallet Ecosystem Overview

Cortex MCP, Inc. All rights reserved 12

more payment vehicles in their e-‐checkouts than just one issuer or network. These retailers need to do one of two things: • Partner with the networks to implement the tokenization plan and drive the network to a new pricing model based on the true risks post-‐tokenization, or

• Leverage their customer relationship to create a giant closed-‐loop system that ultimately cuts out the networks entirely once at scale, using the cards-‐on-‐file, private label cards, and loyalty as a starting point to create value for their consumers.

The merchants could do this individually — having already routed their private label transactions separately from the rest of the chaff within their own gateways– or they could form a group like the MCX, which was

formed with a singular purpose: to offer consumers “a customer-‐focused, versatile and seamlessly integrated mobile-‐commerce platform.” MCX is the logical big player in this space, but they face the same issues as the networks: how do competitors work together to form the alliance without reducing their market share and competitive position? We’ll take a closer look at MCX in our spotlight on merchants since MCX has a larger charter than just addressing the limitations of having legacy CNP card-‐on-‐file systems.

Mobile Wallet Ecosystem Overview

Cortex MCP, Inc. All rights reserved 13

Starbucks could be seen as an example of a card-‐on-‐file player; however, their popular app is really not a full-‐blown payment system as much as it is a loyalty program tied to a prepaid card on a mobile device. Mobile payments are not Starbucks’ focus, but if they were to try and spin off their mobile payments service, they’d do well to partner with one of the prepaid companies that has relationships with multiple retailers and can support the roll-‐out of digital prepaid. They will still have challenges related to removing the competitive advantage of sharing customer data with a third party and training clerks (not baristas) to accept this new payment method (similar to MCX). One of the key benefits card-‐on-‐file companies have over the networks is that they are not necessarily limited to offering only credit or debit cards in their digital wallets. Many consumers can and do store more than one payment vehicle to aid them in fast and easy checkout on-‐line. In the new mobile wallet milieu, all digital tender types are an option — from ACH, direct debit, even Bitcoin, or some new tender type created by MCX or other player. This provides some leverage against the networks in the threat of driving volume away from the credit networks and towards more alternative payments. This will be a key component of a future wallet, as consumers will want choice in their payment vehicle. What do Google, PayPal, Amazon.com, Facebook and Apple all have in common when it comes to the mobile wallet wars? Answer: these

Mobile Wallet Ecosystem Overview

Cortex MCP, Inc. All rights reserved 14

behemoths of the digital asset world have the steepest hill to climb when it comes to effectively competing with others that are striving to shape the future of mobile wallets in store.

Digital Asset Companies This group of card controller companies sells digital assets, or sells physical assets on-‐line with little to no physical POS presence. It is true, Apple has successful retail outlets, but its strongest infrastructure weapon in mobile payments is derived from iTunes, not in-‐store. And while this may shift, Apple will still have the same issues as the card-‐on-‐file merchants we wrote about earlier. The digital asset companies have the steepest climb because they don’t have the experience or the political power to compete in the physical POS space. These companies were built in a CNP e-‐commerce environment, and to them m-‐commerce is just one letter different from the world as they know it. In fact, it’s a completely different ball game in the US and, even more so, abroad. To have a true optimal omni-‐channel experience, one must understand not only eyeballs but foot traffic. No merchant (at scale) is going to give up their customer data to one of these players for their m-‐commerce checkout, especially if the result is a CNP transaction. One would have to show a very convincing ROI on any loyalty and advertising play to get a retailer to partner with these players when they have so many other options. Consider this: does the money one spends on Google Adwords or other marketing

Mobile Wallet Ecosystem Overview

Cortex MCP, Inc. All rights reserved 15

services really lead to actual purchases? What about up-‐sell and cross-‐sell opportunities? What’s the velocity? That’s data worth switching for.

In terms of sheer number of existing partnerships, PayPal has made the strongest in-‐roads among this group of digital asset companies via their relationship with Discover

and by retail giants like The Home Depot. But these PayPal partners are still not seeing the kind of traction they envisioned because PayPal is rightly seen as a credible threat to the other networks and their allies in taking traffic volume away from them. Realistically, PayPal can only expand its reach in the merchants that have leverage over their acquirers: tier one merchants with their own gateways and tier four and tier five merchants that are looking for a simple alternative (like PayPal Here).

In reality, no matter how many cards are on file in iTunes, Amazon or Google Play, they’ll never find their way into use at physical retail outlets without the networks making major changes that allow track data to be used, priced and stored, and changing the way merchants accept payments. One example is Google

Wallet’s secure element play, which was – by many accounts — a debacle. Verizon wouldn’t allow Google Wallet’s secure element on Android phones distributed through them, and they could only be

Mobile Wallet Ecosystem Overview

Cortex MCP, Inc. All rights reserved 16

accepted at First Data clients that are NFC enabled. The new VP of Google Payments comes from their AdWords business unit, but AdWords does not equal in-‐store experience. True, Google has been a proponent of HCE, but that’s more as a standard, and does not mean that Google Wallet will win the HCE enabled mobile wallet wars.

Amazon.com has been fairly silent, but we are also hearing that many retailers are gun shy about letting the online giant under their

kimono given Amazon’s history of exploiting their operational efficiency to take over markets they enter. Rumors are rampant that Amazon will introduce a phone of their own and have a POS terminal based on the Kindle (nice for a closed loop payment system – hint, hint), but these won’t necessarily work for businesses other than tier four and tier five merchants which are already targeted by PayPal and Square.

As mentioned earlier, Apple is enigmatic, with a user base that is drool-‐worthy, a design considered top-‐notch, and strength in the market place that is well documented. But Apple doesn’t generally play nice and share in the profits. Even if Apple gets into mobile

payments, it’s going to have to find a way to share with the incumbents or there will be all out war. Who will be willing to pay the premium Apple will demand for access to their customer base?

Mobile Wallet Ecosystem Overview

Cortex MCP, Inc. All rights reserved 17

In 10 years, POS terminals as we know them today will be as commoditized as personal laptops and desktops have become. The future of POS will be in software and security features. While Apple is poised to succeed as a hardware and mobile wallet software service provider, it’s still too early to tell how much power they will have over other players in this complex payments ecosystem. No matter how this all plays out for digital asset companies, there’s no question that this group has deep pockets and a strong desire to be like Tron’s Quorra and “evolve” into the off-‐line world. How they’ll do it has more to do with politics than technology. One final aspect of this card controller equation not yet addressed is the difference between the card data (which drives the cost of payments) and the actual customer data (value added services). Many customers own more than one card, but the networks only see the cards that are on their network, so they never get a complete picture of a customer’s habits — only their habits on that network’s products. The card-‐on-‐file retailers and digital asset companies have a broader view of the behavior of the consumer across multiple payment types (how do they spend using their Amex vs. Visa debit, vs. MC Credit Card?). There is definite value in not only controlling the card, but also in controlling the customer data, and while the merchants “own” the customer, it’s at checkout that the behavioral data gets collected.

Mobile Wallet Ecosystem Overview

Cortex MCP, Inc. All rights reserved 18

The digital asset companies and on-‐line merchants have the most experience in capturing and analyzing this data (albeit in a CNP environment), so any mobile wallet would do well to leverage that experience. This could ensure that the data is getting captured for a better customer experience, no matter how a customer buys goods with their mobile wallet — in store, via QR code at the bus stop, searching and surfing while on the bus, or while watching a commercial on their TV. Today, physical retail can only capture customer data through loyalty programs or private label cards, since they cannot store the other identifiable info they have on customers (account data from the payment vehicle). That said, merchants with a strong loyalty and on-‐line checkout process/partnerships have much to add to the mobile wallet experience.

Mobile Wallet Ecosystem Overview

Cortex MCP, Inc. All rights reserved 19

Chapter 2: Merchants Merchants are a “necessary evil” to payments professionals, or at least that seems like the attitude many take when they talk about merchant processing. In reality, it is a symbiotic relationship, with each side unable to exist without the other. Physical retail merchants can’t realistically go back to a cash-‐based system of exchange, and payments processors can’t only deal with B2B transfers. What makes it interesting is that there are inherent tensions built into the system. A merchant’s main focus is selling more products faster and cheaper. Payments companies are trying to make a living processing credit, debit and alternative payments. In order to have any innovation in how to process payments, payments companies have to convince the merchant that the change is worth it, since the merchant has the ultimate trump card: they’re the one that “owns” the customer and the checkout experience.

Mobile Wallet Ecosystem Overview

Cortex MCP, Inc. All rights reserved 20

Retail merchants have long railed against the charges foisted on them by the networks and their acquirers in an attempt to lower their cost of doing business. This is not a cooperative situation. Major retailers like Wal-‐Mart, CVS, Sears and Publix have joined forces to create a mobile alternative to the incumbent card networks, MCX. MCX has not yet come out with a product, however, it might behoove the group to create an alternative payment network association in a similar way that Visa and MasterCard were created. First, get set up as an independent association, and then create the operational network to match or exceed the existing networks in terms of speed, security and accuracy. Of all of the competitive mobile wallets in discussions today, MCX is far and away the most interesting, even without any product to discuss. MCX members own the customer, so there is a wealth of data MCX has access to in order to share/monetize/mine for the benefit of the customer (and MCX associate members.) As an association, MCX has a better political chance of convincing its member companies to invest in technology infrastructure and training than competitive mobile wallet providers. MCX also is not tied to one payment type in its wallet. MCX retailers understand the POS experience in ways that other operators in the space do not, and if they can bring that knowledge along with their marketing and e-‐commerce brethren, they have the power to make a truly compelling mobile wallet product that runs across payment to loyalty in a truly cross-‐channel experience.

Mobile Wallet Ecosystem Overview

Cortex MCP, Inc. All rights reserved 21

Their hurdles are also not to be dismissed. Regulators are sure to be watching MCX closely. Does MCX really understand all it will take to supplant the existing networks in terms of operational efficiency? As Kyoshi Mori from DoCoMo is quoted in a New York Times article, “A mistake made by many companies offering mobile payments technology is that they think primarily about how to make money instead of driving adoption of the technology first.” MCX will ultimately make money for its member companies, but it’s a great first step to identifying what technology stack their members will adopt as a replacement for mag stripe and EMV cards, as well as a launching point for new payment types MCX merchant’s customers want to use (EBT, PayPal, BitCoin). MCX has no reason, beside technical feasibility, not to support alternative methods of payment if it makes their member merchants sell more of their products faster, cheaper.

Mobile Wallet Ecosystem Overview

Cortex MCP, Inc. All rights reserved 22

Chapter 3: Carriers When one considers all the carriers bring to the mobile wallet wars, this group of mobile payments stakeholders should be a major force. But that carrier advantage isn’t all that certain because of the differences in market dynamics for US carriers versus the rest of the world. Wireless carriers could have one major advantage over other mobile wallet pretenders providers, in that they have an existing fiduciary relationship with both consumers and merchants. And in many countries, the carriers often control what software (and hardware) goes on the mobile devices that connect to their network. Additionally, as iOS and Android mPOS devices become more and more prevalent as a replacement for existing POS hardware, this distribution network of carrier-‐led cash-‐in, cash-‐out points could become the defacto default solution. In some non-‐US locations, this is indeed how the system is playing out. mPesa is owned by Safaricom and Vodacom (both owned in part by

Mobile Wallet Ecosystem Overview

Cortex MCP, Inc. All rights reserved 23

Vodafone, the world’s 3rd largest carrier), and has proven to be a successful microfinancing and money transfer service. DoCoMo in Japan is also a smash hit, but getting adoption outside of its geographic region of influence is hard to see. In the US, the carriers attempted to repeat the success NTT DoCoMo had in Japan, but since they had already lost their first mover advantage, the carriers had to be reactive instead of proactive. In addition, carriers put all of their eggs in the secure element (SE) hardware basket, choosing to not collaborate with other pre-‐existing mobile payment systems, but to compete with them. This strategy has left the US carriers, through Isis, with little leverage to drive adoption of their mobile wallet. Instead of using their billing systems to drive payments and add other mobile wallet data, as DoCoMo did in Japan, that will make the consumer experience better, the carriers chose to set up roadblocks and tariffs for using their distribution network for other’s products. Carriers should be powerhouses in the mobile wallet wars. They have the distribution network, a huge card-‐on-‐file and billing system in place that ties not only to the credit network but directly into bank accounts as well, and they already have a customer base that is used to “topping up” their mobile phone minutes (huge demographic). So why do they have so little leverage in this land grab? It’s not only regulation. When Verizon and others blocked Google Wallet from installing its secure element chip on Samsung Galaxy phones running

Mobile Wallet Ecosystem Overview

Cortex MCP, Inc. All rights reserved 24

on its network, the tone was set. Instead of trying to partner with Google and other wallet providers, the carriers in the US overplayed their hand to protect Isis, their own mobile wallet offering, to compete in the nascent mobile wallet space. Isis focused exclusively on the one piece of the puzzle the carriers’ control: the consumer handset and the SE. They looked for a hardware solution, and have invested millions of dollars to pilot and roll out this solution nationwide. It might have worked except for three things: • The SE is really relatively expensive as hardware to distribute at scale,

• Merchants don’t have any incentives to invest NFC technology by turning on their NFC antennae or buying new hardware, and

• The business model requires that Isis partner with existing electronic payment providers and individual issuers to provision the secure element, or risk eating the difference between CP and CNP rates.

In the US, Isis seems to be sticking to their guns on the secure element, even though a) chances are really good that it won’t ever work with iPhones and b) Google has indicated support for HCE by changing its Android operating system to support different modes for NFC control, not just routing through the on-‐device SE. This puts the control more in the hands of app developers and handset manufacturers, and takes away control from the carriers.

Mobile Wallet Ecosystem Overview

Cortex MCP, Inc. All rights reserved 25

As a whole, carriers have the infrastructure, consumer relationships, and payment type agnosticism to provide a top-‐of-‐the-‐line mobile wallet, but in developed countries they have to learn to play with existing merchant infrastructures to gain adoption or their offerings will fall behind.

Mobile Wallet Ecosystem Overview

Cortex MCP, Inc. All rights reserved 26

Chapter 4: Device Manufacturers Device manufacturers: the only ones that can really get consumers to pick their mobile device over their leather wallet. Nobody can match the manufacturers’ closeness to the consumer as the maker of the devices consumers have with them all the time can. Why do you think Facebook tried to come out with its own phone or why Amazon wants to come out with one as well? Mobile devices (let’s just stop calling them phones since voice calls are only a small percentage of what we actually do on them -‐-‐ and we are referring to not just mobile “phones”, but wearables, and other internet ready “smart devices as well) are an umbilical cord that feeds our never-‐ending appetite for digital content and interaction. Device manufacturers and OS drivers must be included in the discussion to make the leather wallet disappear. Device manufacturers and those that control the user experience on those devices are some of the biggest names in industry today. Apple, Google, Samsung, Microsoft, HTC, even BlackBerry all are trying to win consumers over with the best user

Mobile Wallet Ecosystem Overview

Cortex MCP, Inc. All rights reserved 27

experience for what is becoming less and less a mobile phone and more and more a mobile computing device. But as of yet, payments are still not the main focus of the mobile “phone.” These multinational players, some of which have tentacles in other parts of the mobile payments ecosystem, control the most basic and most distributed part of the mobile payments landscape; one that app developers (AKA everyone else) is trying to get around -‐-‐ the consumer’s immediacy of interaction with the device. If one of the most significant tenets about mobile wallet adoption is that it has to be just as easy if not easier than whipping out a wallet and swiping a card, the device folks have to play a role. We all know that more clicks or actions you ask a shopper to complete, the more likely it is that the shopper will abandon the cart. Device manufacturers can help (or hinder) other applications from being in what is referred to as the sphere of intimacy: those precious few apps that get front-‐page real estate and aren’t lost somewhere in the myriad of apps, virtually indistinguishable from one another. For any digital wallet to be successful it has to be so easy to use that the payment part should be close to invisible and payment should just happen with as little friction and steps as possible (unless otherwise required by the consumer). Don Kingsborough of PayPal has repeated it many times. For some consumers, that makes sense, and for retailers it definitely does. But there is also a market for consumers that are watching every penny. Device manufacturers and OS drivers

Mobile Wallet Ecosystem Overview

Cortex MCP, Inc. All rights reserved 28

can make the leather wallet disappear, but only if they make the OS accommodating to the consumer so that the information they need is literally at their fingertips. And that means not just payment but coupons, offers, receipts, membership cards, loyalty cards, and other forms of identification. This doesn’t mean foisting only one payment method on the consumer either. They want choice and multiple ways to pay. This cross-‐functional “wallet” has to be useful and available, and making that happen will be up to the device manufacturers (and app developers). Google has the Google Wallet tied to not only the Play store, which makes sense, but also to Google checkout on-‐line. This gives Google a leg up in being able to drive an Omni-‐channel experience for the brands that buy into Google as their payment provider (and take advantage of Google Adwords to drive consumer in-‐store). On the device, however, Google’s Android OS is open source, so the actual manufacturers can create alternatives. For example, Samsung has created its own version of app store and is trying to drive its users to load their payment information on its own wallet to compete more directly with Apple’s Passbook, but that still leave how it will be accepted as a question mark. Speaking of Apple, it all seems like a black box. Apple has more cards on file than Amazon and that’s a powerful tool, but it remains to be seen if Apple can turn that asset into a lever to open up in-‐store payments anywhere but its own retail outlets. On-‐line and on-‐device?

Mobile Wallet Ecosystem Overview

Cortex MCP, Inc. All rights reserved 29

Sure, it makes sense. Peer to peer? Even more so. But trying to convince The Home Depot or Yum Brands to accept Apple’s Passbook in-‐store? It’s going to take more than iBeacon for that integration to happen. Apple <could> be a huge enabler of mobile payments in-‐store in general if they choose to use technologies that existing merchants use and let app developers have access to those controllers. Apple could (and would) monetize that in their MFI program, getting revenue for using the NFC controller, or iBeacon, but until then, we just have to wait and see. Microsoft and BlackBerry are both relatively fringe players in this market now, but could still drive innovation. Many POS systems today (and many ATMs) run on a Windows platform. Is there some way Microsoft could leverage that fact into a cleaner integration than competitors? Maybe. One other benefit the device manufacturers have is that they are not tied to one payment type or vehicle. That’s not their bread and butter, so they could provide a solution that’s just as easy for the consumer to use their credit card, as debit, as bank draft or BitCoin. Will device manufacturers win the wallet wars? Not alone. They are heavy influencers of those that own their devices, the consumers, and can make or break a wallet with built in features or create roadblocks. They are platforms and standard bearers, giving all of their app developers a common platform to create the user experience, but they

Mobile Wallet Ecosystem Overview

Cortex MCP, Inc. All rights reserved 30

too have to make money. As with all of the other players in the ecosystem, the device guys are looking for a way to add value and monetize their hardware and operating systems as they become more and more vital to a consumer’s daily life. The handheld computer we walk around with is no longer just a phone and we don’t just talk on it. Talk, text, converse, transact, search, learn, share, capture. The device that allows consumers to get what they want better than the others will win, and the wallet that wins will be on that device.

Mobile Wallet Ecosystem Overview

Cortex MCP, Inc. All rights reserved 31

Chapter 5: Consumers

Consumers are a fickle bunch. One of the first things one learns in business school is “don’t sell to consumers, they don’t understand business and cannot be trusted to make a rational business decision.” Oh how true it is -‐-‐ yet in order for mobile payments to take off, it’s all about the consumer and making the consumer happy. So much for b-‐school. As was mentioned in the introduction, while all other players have their trump cards, strengths and

weaknesses, the ultimate arbiter of if a mobile wallet will work or not is the consumer. No matter how cool the technology might be, or how collaborative players might be to come up with a solution, if it doesn’t resonate with consumers and isn’t ready to gain widespread adoption it will go the way of the Sony Betamax. For a consumer to switch from their current behaviors, they have to have a very compelling reason. So far, none of the mobile wallets have

Mobile Wallet Ecosystem Overview

Cortex MCP, Inc. All rights reserved 32

really nailed that “killer app” that sweeps the nation (and world) to really effect change. The Starbucks app is the closest, but it’s limited to one brand, one loyalty play. Google hasn’t done it (yet), Apple has taken their sweet time to enter the market, Square is losing their shirts, and others that might have the inside track are too worried about market share and competition to really think about the customer. What will be the killer app? We don’t know, but we do know that without continuous investment in pilots, trials and experiments on not only the user experience, but the underlying technology that app won’t be found. The “holy grail” of wallet technology is something that goes across mobile operating systems and form factors, works on multiple merchant configurations, leverages omni-‐channel experiences and has more than just payments. We may think so, but payments just aren’t that sexy to the average consumer. Marketing and loyalty programs are. We need to learn what it will take for a critical mass of people to leave their leather at home and invest in making that a reality because if the consumer doesn’t bite, it’s back to the drawing board. One of the key complaints about any mobile wallet is that it’s a technology in search of a problem. We would disagree. The iPhone was not “needed.” There was no problem it solved, but once it came to market, a whole new world of possibility was opened up.

Mobile Wallet Ecosystem Overview

Cortex MCP, Inc. All rights reserved 33

Integrating on-‐line, mobile and in-‐store experiences has not happened yet at scale so we don’t know all of the wonderful things we can do with it, but some in the industry can see how that experience can excite the imagination and drive consumer behavior. Who will be the visionary who will break through all of the existing clutter and create something consumers will love? What if there isn’t that visionary with deep enough pockets, strong enough will, and politically savvy to get their product out in the marketplace so the general population notices? If the industry as a whole takes a reactive, cautionary approach, consumers and merchants won’t be able to really take advantage of the infrastructure, already built, to improve the commercial experience. It’s not about payments. It’s the whole thing: The entire purchase funnel. From awareness, consideration, trial, purchase loyalty and repurchase. All can be improved with the data and experiences available via having an omni-‐channel strategy that takes mobile as an integral part of bringing the on-‐line world into the physical. Consumer interactions on-‐line or on-‐mobile should translate directly in the in-‐store experience. Click or tap an ad or offer and that activity should be tracked and accounted for when that consumer enters a store and completes the purchase funnel. Consumers deserve this experience no matter what device their carrying, or if it is on-‐line or not. Tokenization is one way to bring PAN based payments to the mobile world, but the wallet is so much more than just a placeholder

Mobile Wallet Ecosystem Overview

Cortex MCP, Inc. All rights reserved 34

for debit and credit cards. Consumers will demand a choice for their payment types, from the traditional, to alternative, and a wallet must have the architecture to adapt and adopt. Merchants shouldn’t be penalized for arbitrary risk designations that are no longer relevant in today’s mobile world. Everyone can still get paid for the services they perform, but the value of those services may change with this new milieu. Consumers are the top of the food chain who rule the ecosystem. They decide which players live, which will die. But consumers are a fickle bunch, and having the best technology won’t necessarily win the war without also having sound strategy and knowing where to put your resources for the biggest bang for the buck. The mobile wallet wars are still in the early skirmish days. Alliances have yet to really form, and sides taken. Consumers don’t yet know what is available to them, but once they start demanding certain omni-‐channel experiences, only those companies that are primed and ready to take advantage of those demands will win, the rest will be a footnote to history like the Betamax.

Mobile Wallet Ecosystem Overview

Cortex MCP, Inc. All rights reserved 35

Looking Ahead We welcome your feedback and opinions on the mobile wallet ecosystem we’ve presented here. And we encourage you to follow developments in this space, as there will be many – and these developments will be significant. In fact, we believe the mobile wallet developments over the next 3 years will determine the next 30. As stated earlier, the players in the mobile wallet ecosystem are becoming increasing aware that as we move forward, new approaches to these consumer challenges are needed – approaches that at the same time address the concerns and questions facing merchants, card controllers, device manufacturers and carries. Only then, will we realize the full potential of mobile wallets. To hear more about these developments and to learn more about a mobile wallet technology that promises to address these challenges – and unlock this potential – please visit www.cortexmcp.com.

Mobile Wallet Ecosystem Overview

Cortex MCP, Inc. All rights reserved 36

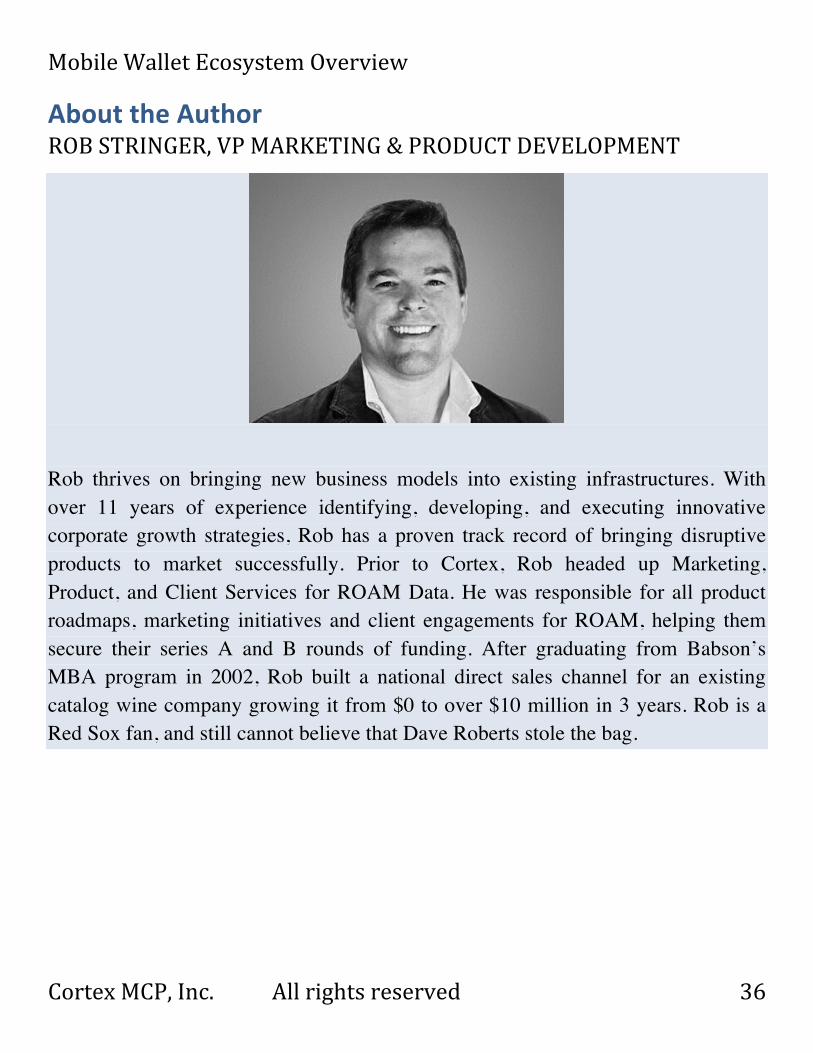

About the Author ROB STRINGER, VP MARKETING & PRODUCT DEVELOPMENT

Rob thrives on bringing new business models into existing infrastructures. With over 11 years of experience identifying, developing, and executing innovative corporate growth strategies, Rob has a proven track record of bringing disruptive products to market successfully. Prior to Cortex, Rob headed up Marketing, Product, and Client Services for ROAM Data. He was responsible for all product roadmaps, marketing initiatives and client engagements for ROAM, helping them secure their series A and B rounds of funding. After graduating from Babson’s MBA program in 2002, Rob built a national direct sales channel for an existing catalog wine company growing it from $0 to over $10 million in 3 years. Rob is a Red Sox fan, and still cannot believe that Dave Roberts stole the bag.