Corsa Coal Corp. · Corsa Coal Corp. Management’s Discussion and Analysis For the nine months...

42

Corsa Coal Corp. Management’s Discussion and Analysis September 30, 2014

Transcript of Corsa Coal Corp. · Corsa Coal Corp. Management’s Discussion and Analysis For the nine months...

Corsa Coal Corp. Management’s Discussion and Analysis September 30, 2014

Corsa Coal Corp. Management’s Discussion and Analysis

For the nine months ended September 30, 2014

2

This Management’s Discussion and Analysis (“MD&A”) is dated as of November 28, 2014 and is intended to be read in conjunction with the unaudited condensed interim consolidated financial statements of Corsa Coal Corp. (“Corsa”) for the three and nine months ended September 30, 2014 and 2013 and the related notes thereto, as well as the audited consolidated financial statements of Corsa for the years ended December 31, 2013 and 2012 and the related notes thereto. References in this MD&A to “Third Quarter 2014” means the three months ended September 30, 2014; “Third Quarter 2013” means the three months ended September 30, 2013; “Nine Months 2014” means the nine months ended September 30, 2014 and “Nine Months 2013” means the nine months ended September 30, 2013; unless otherwise noted. The consolidated financial statements have been prepared in accordance with IFRS. Unless otherwise indicated, all dollar amounts in this MD&A are expressed in United States dollars and all ton amounts are short tons (2,000 pounds per ton). Please refer to “Forward-Looking Statements” below.

On July 31, 2013, Corsa completed a transaction (the “Quintana Transaction”) with Quintana Kopper Glo Investment, LLC (“QKGI”), a portfolio company of Quintana Energy Partners LP and its affiliated investment funds (collectively “Quintana”). See “Quintana Transaction” below. The result of the Quintana Transaction was Corsa becoming the legal acquirer of QKGI, QKGI becoming the legal acquiree of Corsa and Quintana becoming the controlling shareholder of Corsa. Under International Financial Reporting Standards (“IFRS”), QKGI was identified as the accounting acquirer and Corsa was identified as the accounting acquiree resulting in the Quintana Transaction being accounted for as a reverse takeover. As a result, the consolidated financial statements of Corsa are now considered a continuation of the historical consolidated financial statements of QKGI.

On August 19, 2014, Corsa completed the purchase of all of the outstanding shares of PBS Coals Limited (“PBS”). See “PBS Transaction” below. The unaudited condensed interim consolidated statements of operations and comprehensive income and cash flows of Corsa for the three and nine months ended September 30, 2014 include the results from the operations of QKGI and Corsa for the period from January 1 to September 30, 2014 and PBS from August 19 to September 30, 2014. The unaudited condensed interim consolidated statement of operations and comprehensive income and statement of cash flows of Corsa for the three months ended September 30, 2013 includes the results from the operations of QKGI for the period from July 1 to September 30, 2013 and the results from the operations of Corsa for the period from July 31 to September 30, 2013 and the unaudited condensed interim consolidated statement of operations and comprehensive income and statement of cash flows of Corsa for the nine months ended September 30, 2013 includes the results from the operations of QKGI for the period from January 1 to September 30, 2013 and the results from the operations of Corsa for the period from July 31 to September 30, 2013.

The unaudited condensed interim consolidated balance sheet of Corsa at September 30, 2014 includes QKGI, Corsa and PBS and the unaudited condensed interim consolidated balance sheet of Corsa at December 31, 2013 includes QKGI and Corsa.

Corsa Coal Corp. Management’s Discussion and Analysis

For the nine months ended September 30, 2014

3

Company Profile Corsa’s primary business is the mining, processing and selling of metallurgical and thermal coal, as well as actively exploring, acquiring and developing resource properties that are consistent with its existing coal business. The coal operations are conducted through the Northern Appalachia Division (“NAPP”) and the Central Appalachia Division (“CAPP”). NAPP, the combination of the Wilson Creek Division and PBS (see “PBS Transaction” below), is based in Somerset, Pennsylvania, U.S.A. and focused on low-volatile metallurgical coal production and sales in the Northern Appalachia coal region of the United States. See “Operations – NAPP” below. CAPP, formerly the Kopper Glo Division, is based in Knoxville, Tennessee, U.S.A. and focused on thermal coal production and sales in the Southern Appalachia coal region of the United States. See “Operations – CAPP” below. Corsa was incorporated on June 14, 2007 under the Business Corporations Act (British Columbia) and was listed on the TSX Venture Exchange (“TSX-V”) on April 17, 2008 under the symbol “CSO”. On April 27, 2011 Corsa changed its name to Corsa Coal Corp. and on June 27, 2011, Corsa continued under the Canada Business Corporations Act. Strategy Corsa’s goal is to focus on niche coal markets which command premium pricing and have a delivered cost advantage to customers, while maintaining low-cost operations and sufficient infrastructure to achieve sustainable growth. To achieve this, Corsa will:

• Operate in a safe, responsible and cost-effective manner; • Secure mining assets with low permitting risk, relatively low development costs and

infrastructure in areas which are geographically positioned at a competitive advantage to key customers and export markets;

• Diversify the customer base and balance between domestic and international markets; and • Maintain a well-capitalized balance sheet and sufficient liquidity to withstand any unexpected

downturns in coal pricing.

Highlights

• Third Quarter 2014 revenues of $45,150,000. See “Financial Results” below. • Metallurgical coal sales of 263,000 tons and thermal coal sales of 247,000 tons in Third Quarter

2014. See “Operating Results” below. • Sales guidance for metallurgical coal of 300,000 to 320,000 tons for the three months ended

December 31, 2014. See “Outlook – Metallurgical Coal” below. • Sales guidance for thermal coal of 220,000 to 250,000 tons for the three months ended December

31, 2014. See “Outlook – Thermal Coal” below. • Realized sales price of $93 per ton for metallurgical coal in Third Quarter 2014. See “Operating

Results” below. • Cash production cost per ton of $74 per ton for metallurgical coal in Third Quarter 2014. See

“Operating Results” below. • Completed the acquisition of PBS on August 19, 2014. See “PBS Transaction”.

Corsa Coal Corp. Management’s Discussion and Analysis

For the nine months ended September 30, 2014

4

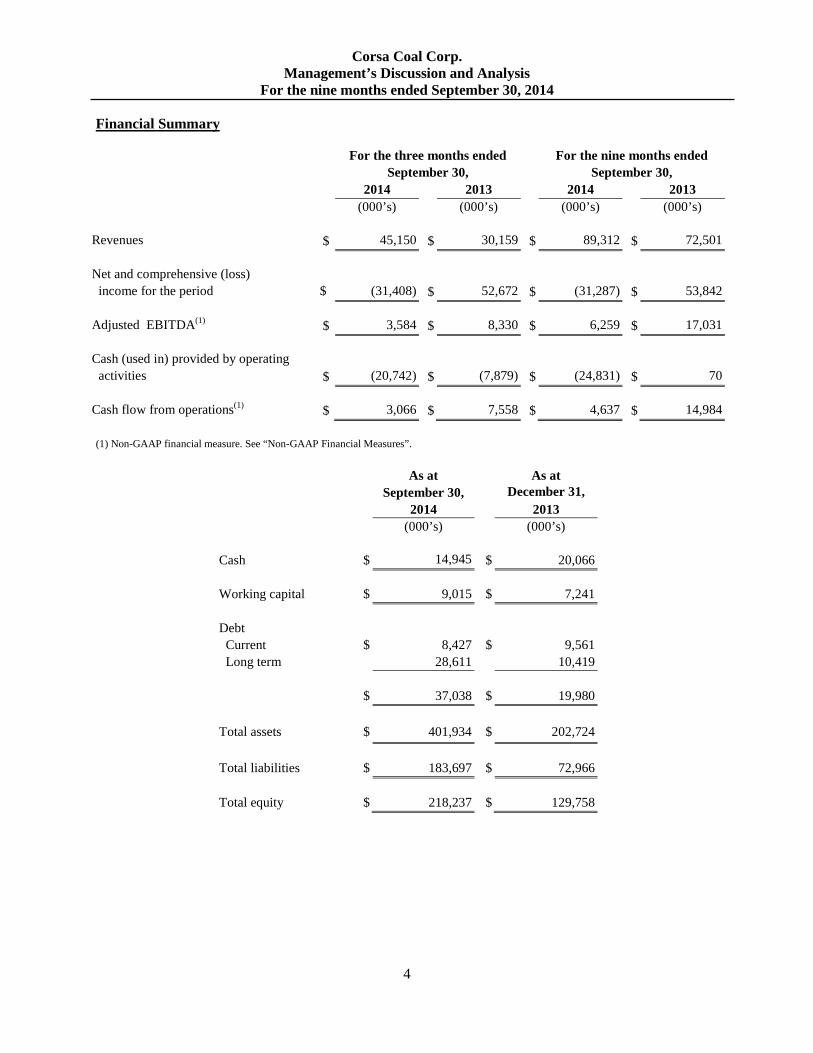

Financial Summary

For the three months ended For the nine months ended September 30, September 30, 2014 2013 2014 2013 (000’s) (000’s) (000’s) (000’s) Revenues $ 45,150 $ 30,159 $ 89,312 $ 72,501 Net and comprehensive (loss) income for the period $

(31,408) $ 52,672 $ (31,287) $ 53,842 Adjusted EBITDA(1) $ 3,584 $ 8,330 $ 6,259 $ 17,031 Cash (used in) provided by operating activities $ (20,742) $ (7,879) $ (24,831) $ 70 Cash flow from operations(1) $ 3,066 $ 7,558 $ 4,637 $ 14,984 (1) Non-GAAP financial measure. See “Non-GAAP Financial Measures”.

As at As at September 30, December 31,

2014 2013 (000’s) (000’s) Cash $ 14,945

$ 20,066

Working capital $ 9,015 $ 7,241 Debt Current $ 8,427 $ 9,561 Long term 28,611 10,419

$ 37,038 $ 19,980 Total assets $ 401,934 $ 202,724 Total liabilities $ 183,697 $ 72,966 Total equity $ 218,237 $ 129,758

Corsa Coal Corp. Management’s Discussion and Analysis

For the nine months ended September 30, 2014

5

Operations Summary

For the three months ended For the nine months ended September 30, September 30, 2014 2013 2014 2013 NAPP Division - Metallurgical coal Tons sold 263,000 73,000 401,000 73,000 Realized price per ton sold(1) $ 93 $ 96 $ 92 $ 96 Cash production cost per ton sold(1) (74) (63) (77) (63) Cash margin per ton sold $ 19 $ 33 $ 15 $ 33 CAPP Division - Thermal coal Tons sold 247,000 299,000 691,000 866,000 Realized price per ton sold(1) $ 68 $ 75 $ 68 $ 75 Cash production cost per ton sold(1) (59) (51) (58) (55) Cash margin per ton sold $ 9 $ 24 $ 10 $ 20 (1) Non-GAAP financial measure. See “Non-GAAP Financial Measures”.

Operations

NAPP NAPP produces and sells low volatile metallurgical coal used for the production of coke from its mines in the Northern Appalachia coal region of the United States. The coal mined is sold to international and domestic steel producers, as well as other coal companies for blending, via railroad, trucking and barge. In addition to the mines currently in production, NAPP has a significant pipeline of projects which it anticipates developing pending the recovery of metallurgical coal prices. NAPP is centrally located in and around Somerset, Pennsylvania located approximately 70 miles from Pittsburgh, Pennsylvania and operates in Pennsylvania and Maryland. NAPP usually ships by rail, although shipping can be done by truck or barge. The preparation plants have access to both the CSX and NS rail lines and can access the Eastern Seaboard ports such as the Port of Baltimore which is 170 miles away. The location of NAPP is also consistent with Corsa’s strategy to provide a competitively lower delivered cost to key customers, including steel mills around Pittsburgh, the Great Lakes regions and Canada.

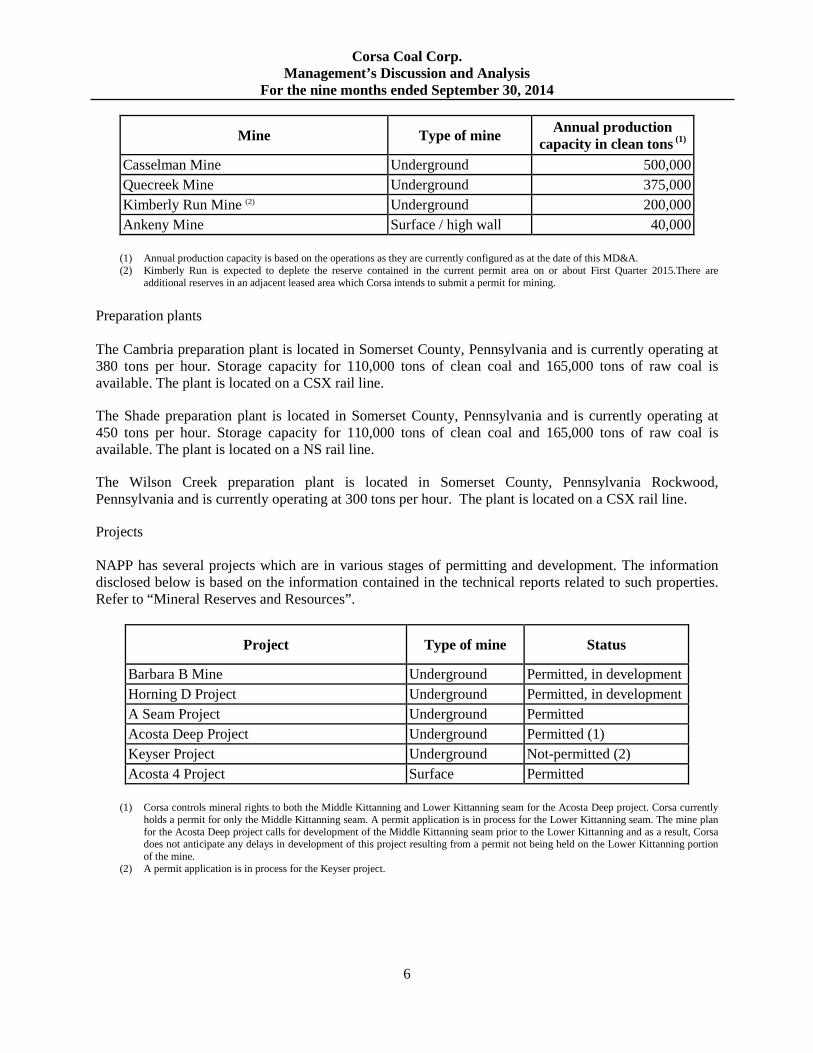

Mines NAPP currently operates one surface mine and three underground mines. The information disclosed below is based on the information contained in the technical reports related to such properties. Refer to “Mineral Reserves and Resources”.

Corsa Coal Corp. Management’s Discussion and Analysis

For the nine months ended September 30, 2014

6

Mine Type of mine Annual production capacity in clean tons (1)

Casselman Mine Underground 500,000 Quecreek Mine Underground 375,000 Kimberly Run Mine (2) Underground 200,000 Ankeny Mine Surface / high wall 40,000

(1) Annual production capacity is based on the operations as they are currently configured as at the date of this MD&A. (2) Kimberly Run is expected to deplete the reserve contained in the current permit area on or about First Quarter 2015.There are

additional reserves in an adjacent leased area which Corsa intends to submit a permit for mining.

Preparation plants The Cambria preparation plant is located in Somerset County, Pennsylvania and is currently operating at 380 tons per hour. Storage capacity for 110,000 tons of clean coal and 165,000 tons of raw coal is available. The plant is located on a CSX rail line.

The Shade preparation plant is located in Somerset County, Pennsylvania and is currently operating at 450 tons per hour. Storage capacity for 110,000 tons of clean coal and 165,000 tons of raw coal is available. The plant is located on a NS rail line.

The Wilson Creek preparation plant is located in Somerset County, Pennsylvania Rockwood, Pennsylvania and is currently operating at 300 tons per hour. The plant is located on a CSX rail line.

Projects NAPP has several projects which are in various stages of permitting and development. The information disclosed below is based on the information contained in the technical reports related to such properties. Refer to “Mineral Reserves and Resources”.

Project Type of mine Status

Barbara B Mine Underground Permitted, in development Horning D Project Underground Permitted, in development A Seam Project Underground Permitted Acosta Deep Project Underground Permitted (1) Keyser Project Underground Not-permitted (2) Acosta 4 Project Surface Permitted

(1) Corsa controls mineral rights to both the Middle Kittanning and Lower Kittanning seam for the Acosta Deep project. Corsa currently

holds a permit for only the Middle Kittanning seam. A permit application is in process for the Lower Kittanning seam. The mine plan for the Acosta Deep project calls for development of the Middle Kittanning seam prior to the Lower Kittanning and as a result, Corsa does not anticipate any delays in development of this project resulting from a permit not being held on the Lower Kittanning portion of the mine.

(2) A permit application is in process for the Keyser project.

Corsa Coal Corp. Management’s Discussion and Analysis

For the nine months ended September 30, 2014

7

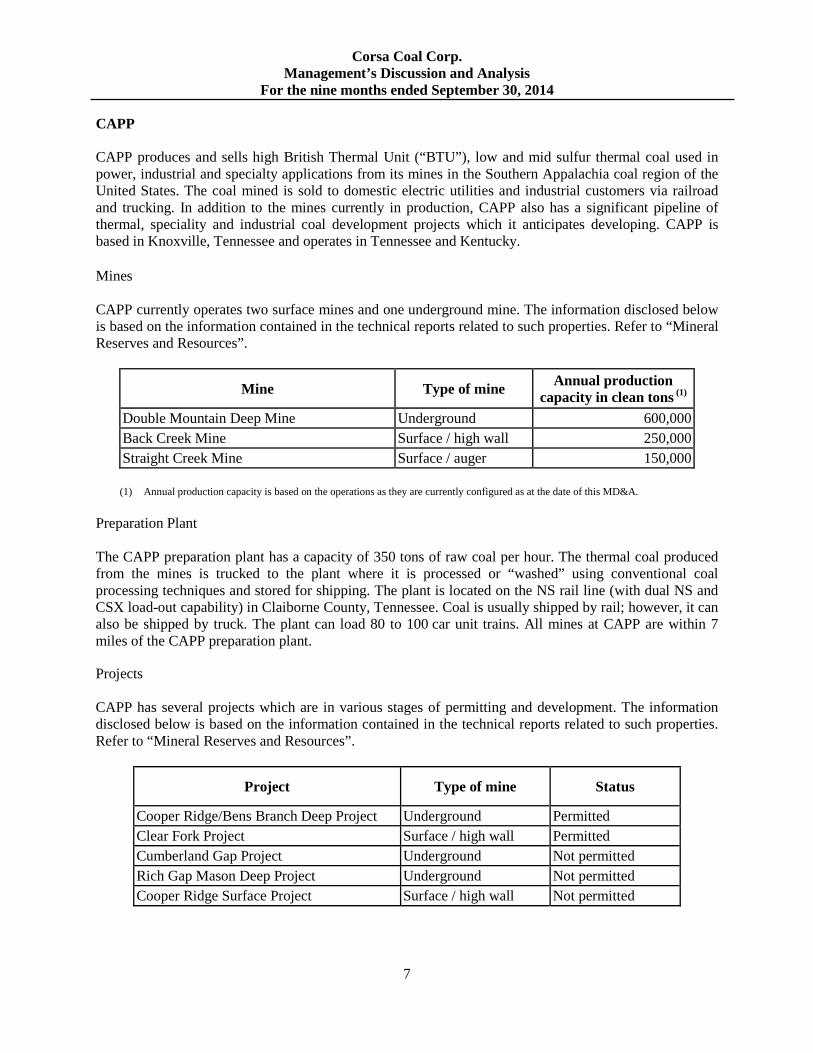

CAPP CAPP produces and sells high British Thermal Unit (“BTU”), low and mid sulfur thermal coal used in power, industrial and specialty applications from its mines in the Southern Appalachia coal region of the United States. The coal mined is sold to domestic electric utilities and industrial customers via railroad and trucking. In addition to the mines currently in production, CAPP also has a significant pipeline of thermal, speciality and industrial coal development projects which it anticipates developing. CAPP is based in Knoxville, Tennessee and operates in Tennessee and Kentucky. Mines CAPP currently operates two surface mines and one underground mine. The information disclosed below is based on the information contained in the technical reports related to such properties. Refer to “Mineral Reserves and Resources”.

Mine Type of mine Annual production capacity in clean tons (1)

Double Mountain Deep Mine Underground 600,000 Back Creek Mine Surface / high wall 250,000 Straight Creek Mine Surface / auger 150,000

(1) Annual production capacity is based on the operations as they are currently configured as at the date of this MD&A.

Preparation Plant The CAPP preparation plant has a capacity of 350 tons of raw coal per hour. The thermal coal produced from the mines is trucked to the plant where it is processed or “washed” using conventional coal processing techniques and stored for shipping. The plant is located on the NS rail line (with dual NS and CSX load-out capability) in Claiborne County, Tennessee. Coal is usually shipped by rail; however, it can also be shipped by truck. The plant can load 80 to 100 car unit trains. All mines at CAPP are within 7 miles of the CAPP preparation plant.

Projects CAPP has several projects which are in various stages of permitting and development. The information disclosed below is based on the information contained in the technical reports related to such properties. Refer to “Mineral Reserves and Resources”.

Project Type of mine Status

Cooper Ridge/Bens Branch Deep Project Underground Permitted Clear Fork Project Surface / high wall Permitted Cumberland Gap Project Underground Not permitted Rich Gap Mason Deep Project Underground Not permitted Cooper Ridge Surface Project Surface / high wall Not permitted

Corsa Coal Corp. Management’s Discussion and Analysis

For the nine months ended September 30, 2014

8

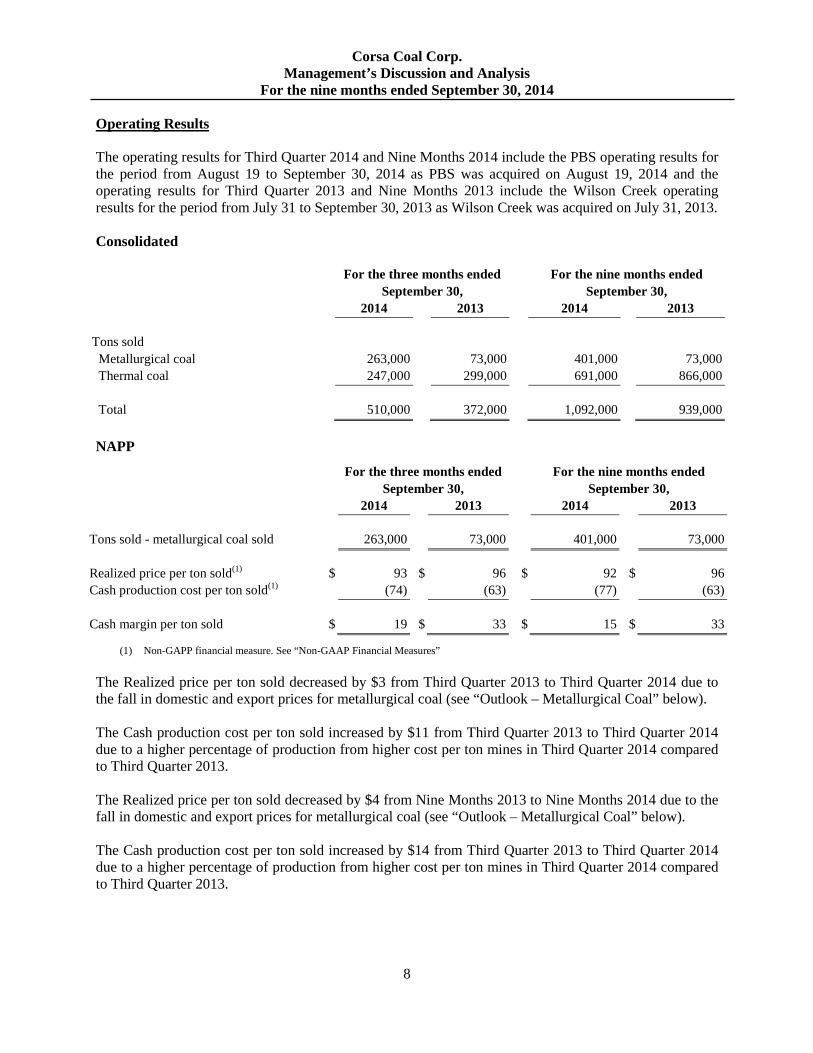

Operating Results The operating results for Third Quarter 2014 and Nine Months 2014 include the PBS operating results for the period from August 19 to September 30, 2014 as PBS was acquired on August 19, 2014 and the operating results for Third Quarter 2013 and Nine Months 2013 include the Wilson Creek operating results for the period from July 31 to September 30, 2013 as Wilson Creek was acquired on July 31, 2013. Consolidated

For the three months ended For the nine months ended September 30, September 30, 2014 2013 2014 2013 Tons sold Metallurgical coal 263,000 73,000 401,000 73,000 Thermal coal 247,000 299,000 691,000 866,000 Total 510,000 372,000 1,092,000 939,000 NAPP

For the three months ended For the nine months ended September 30, September 30, 2014 2013 2014 2013 Tons sold - metallurgical coal sold 263,000 73,000 401,000 73,000 Realized price per ton sold(1) $ 93 $ 96 $ 92 $ 96 Cash production cost per ton sold(1) (74) (63) (77) (63) Cash margin per ton sold $ 19 $ 33 $ 15 $ 33

(1) Non-GAPP financial measure. See “Non-GAAP Financial Measures”

The Realized price per ton sold decreased by $3 from Third Quarter 2013 to Third Quarter 2014 due to the fall in domestic and export prices for metallurgical coal (see “Outlook – Metallurgical Coal” below). The Cash production cost per ton sold increased by $11 from Third Quarter 2013 to Third Quarter 2014 due to a higher percentage of production from higher cost per ton mines in Third Quarter 2014 compared to Third Quarter 2013. The Realized price per ton sold decreased by $4 from Nine Months 2013 to Nine Months 2014 due to the fall in domestic and export prices for metallurgical coal (see “Outlook – Metallurgical Coal” below). The Cash production cost per ton sold increased by $14 from Third Quarter 2013 to Third Quarter 2014 due to a higher percentage of production from higher cost per ton mines in Third Quarter 2014 compared to Third Quarter 2013.

Corsa Coal Corp. Management’s Discussion and Analysis

For the nine months ended September 30, 2014

9

CAPP

For the three months ended For the nine months ended September 30, September 30, 2014 2013 2014 2013 Tons sold - thermal coal sold 247,000 299,000 691,000 866,000 Realized price per ton sold(1) $ 68 $ 75 $ 68 $ 75 Cash production cost per ton sold(1) (59) (51) (58) (55) Cash margin per ton sold(1) $ 9 $ 24 $ 10 $ 20

(1) Non-GAPP financial measure. See “Non-GAAP Financial Measures”

The Realized price per ton sold decreased by $7 from Third Quarter 2013 to Third Quarter 2014 due to the decline in regional prices for thermal coal (see “Outlook – Thermal Coal” below). The Cash production cost per ton sold increased by $8 from Third Quarter 2013 to Third Quarter 2014 due to a higher percentage of production from higher cost per ton mines in Third Quarter 2014 compared to Third Quarter 2013. The Realized price per ton sold decreased by $7 from Nine Months 2013 to Nine Months 2014 due to the decline in regional prices for thermal coal (see “Outlook – Thermal Coal” below). The Cash production cost per ton sold increased by $3 from Nine Months 2013 to Nine Months 2014 due to a higher percentage of production from higher cost per ton mines in Third Quarter 2014 compared to Third Quarter 2013.

Corsa Coal Corp. Management’s Discussion and Analysis

For the nine months ended September 30, 2014

10

Financial Results Consolidated The financial results for Third Quarter 2014 and Nine Months 2014 include the PBS financial results for the period from August 19 to September 30, 2014 as PBS was acquired on August 19, 2014 and the financial results for Third Quarter 2013 and Nine Months 2013 include the Wilson Creek financial results for the period from July 31 to September 30, 2013 as Wilson Creek was acquired on July 31, 2013.

For the three months ended For the nine months ended September 30, September 30, 2014 2013 2014 2013 (000’s) (000’s) (000’s) (000’s) Revenues $ 45,150 $ 30,159 $ 89,312 $ 72,501 Cost of sales (45,538)

(24,024) (92,827)

(59,967)

Gross margin (388) 6,135 (3,515) 12,534 Corporate and administrative expense (3,826) (1,522) (7,754) (2,808) (Loss) income from operations (4,214) 4,613 (11,269) 9,726 Finance expense (21,343) (5,497) (16,610) (6,742) Transaction expenses (1,184) (1,632) (1,891) (2,642) Bargain purchase price - 60,026 - 60,026 (22,527) 52,897 (18,501) 50,642 (Loss) income for the period before tax (26,741) 57,510 (29,770) 60,368

Current income tax expense (320) (629) (419) (2,060) Deferred income tax expense (4,347) (4,209) (1,098) (4,466) (4,667) (4,838) (1,517) (6,526) Net and comprehensive (loss) income for the period $ (31,408) $ 52,672 $ (31,287) $ 53,842 Adjusted EBITDA(1) $ 3,584 $ 8,330 $ 6,259 $ 17,031

(1) Non-GAAP financial measure. See “Non-GAAP Financial Measures”

Third Quarter 2014 Revenues Revenues increased by $14,991,000 from Third Quarter 2013 to Third Quarter 2014 as a result of NAPP increasing by $20,812,000 and CAPP decreasing by $5,821,000. See “Financial Results – Operating Segments”. Cost of sales Cost of sales increased by $21,514,000 from Third Quarter 2013 to Third Quarter 2014 as a result of NAPP increasing by $22,630,000 and CAPP decreasing by $1,121,000. See “Financial Results – Operating Segments”.

Corsa Coal Corp. Management’s Discussion and Analysis

For the nine months ended September 30, 2014

11

Corporate and administrative expense Corporate and administrative expense includes corporate expenses and general and administrative expenses relating to divisional administration. The expense increased by $2,304,000 from Third Quarter 2013 to Third Quarter 2014 as a result of NAPP increasing by $1,487,000, Corporate increasing by $828,000 and CAPP decreasing by $11,000. See “Financial Results – Operating Segments”. Finance expense Finance expense increased by $15,846,000 from Third Quarter 2013 to Third Quarter 2014 as a result of Corporate increasing by $14,228,000, NAPP increasing by $131,000 and CAPP changing by $1,487,000 from an income of $1,358,000 to an expense of $129,000. See “Financial Results – Operating Segments”. Transaction expenses Transaction expenses decreased by $448,000 from Third Quarter 2013 to Third Quarter 2014. The expenses in Third Quarter 2014 were related to the PBS Transaction and the Transaction expenses in Third Quarter 2013 were related to the Quintana Transaction. Bargain purchase gain The Bargain purchase gain was $60,313,000 in Third Quarter 2013 and there was no comparable amount in Third Quarter 2014. The Bargain purchase gain resulted from the Quintana Transaction. Current income tax expense The Current tax expense decreased by $309,000 from Third Quarter 2013 to Third Quarter 2014 as a result of lower taxable income in Third Quarter 2014. Deferred income tax expense Deferred income tax expenses increased by $138,000 from Third Quarter 2013 to Third Quarter 2014. Net and comprehensive (loss) income for the period Net (loss) income changed from an income of $52,672,000 in Third Quarter 2013 to a net loss of $31,408,000 in Third Quarter 2014. The change in net (loss) income is the result of the factors impacting the items described above and the items described in the “Financial Results – Operating Segments” section below. Adjusted EBITDA

Adjusted EBITDA decreased by $4,823,000 in Third Quarter 2014 compared with Third Quarter 2013. The primary factor for the decrease was lower realized coal prices per ton in Third Quarter 2014 compared with Third Quarter 2013. Refer to “Non-GAAP Financial Measures” for reconciliation of Adjusted EBITDA to the closest financial measure presented in Corsa’s statement of operations.

Corsa Coal Corp. Management’s Discussion and Analysis

For the nine months ended September 30, 2014

12

Nine Months 2014 Revenue Revenues increased by $16,811,000 from Nine Months 2013 to Nine Months 2014 as a result of NAPP increasing by $34,972,000 and CAPP decreasing by $18,161,000. See “Financial Results – Operating Segments”. Cost of sales Cost of sales increased by $32,860,000 from Nine Months 2013 from Nine Months 2014 as a result of NAPP increasing by $41,115,000 and CAPP decreasing by $8,281,000. See “Financial Results – Operating Segments”. Corporate and administrative expense Corporate and administrative expense includes corporate expenses and general and administrative expenses relating to divisional administration. The expense increased by $4,946,000 from Nine Months 2013 to Nine Months 2014 as a result of Corporate increasing by $2,953,000, NAPP increasing by $2,679,000, and CAPP decreasing by $686,000. See “Financial Results – Operating Segments”. Finance expense Finance expense increased by $9,868,000 from Nine Months 2013 to Nine Months 2014 as a result of Corporate increasing by $8,730,000, NAPP increasing by $638,000 and CAPP changing by $500,000 from an income of $110,000 to an expense of $390,000. See “Financial Results – Operating Segments”. Transaction expenses Transaction expenses decreased by $751,000 from Nine Months 2013 to Nine Months 2014. The expenses in Nine Months 2014 were related to the PBS Transaction and the Transaction expenses in Nine Months 2013 were related to the Quintana Transaction. Bargain purchase gain The Bargain purchase gain was $60,313,000 in Nine Months 2013 and there was no comparable amount in Nine Months 2014. The Bargain purchase gain resulted from the Quintana Transaction. Current income tax expense Current tax expense decreased by $1,641,000 from Nine Months 2013 to Nine Months 2014 as taxable income decreased from Nine Months 2013 to Nine Months 2014. Deferred income tax expense Deferred income tax expense decreased by $3,368,000 from Nine Months 2013 to Nine Months 2014.

Corsa Coal Corp. Management’s Discussion and Analysis

For the nine months ended September 30, 2014

13

Net and comprehensive (loss) income for the period Net (loss) income changed from an income of $53,842,000 in Nine Months 2013 to a net loss of $31,287,000 in Nine Months 2014. The change in net (loss) income is the result of the factors impacting the items described above and the items described in the “Financial Results – Operating Segments” section below. Adjusted EBITDA

Adjusted EBITDA decreased by $12,247,000 in Nine Months 2014 compared with Nine Months 2013. The primary factor for the decrease was lower realized coal prices per ton in Third Quarter 2014 compared with Third Quarter 2013. Refer to “Non-GAAP Financial Measures” for reconciliation of Adjusted EBITDA to the closest financial measure presented in Corsa’s statement of operations. Operating Segments Corsa’s three distinct operating segments are NAPP, CAPP and Corporate. The financial results of the operating segments are as follows: NAPP The financial results for Third Quarter 2014 and Nine Months 2014 include the PBS financial results for the period from August 19 to September 30, 2014 as PBS was acquired on August 19, 2014 and the financial results for Third Quarter 2013 and Nine Months 2013 include the Wilson Creek financial results for the period from July 31 to September 30, 2013 as Wilson Creek was acquired on August 19, 2013.

For the three months ended For the nine months ended September 30, September 30, 2014 2013 2014 2013 (000’s) (000’s) (000’s) (000’s) Revenues $ 28,422 $ 7,610 $ 42,582 $ 7,610 Cost of sales (29,584)

(6,954) (48,069)

(6,954)

Gross margin (1,162) 656 (5,487) 656 Corporate and administrative expense (2,070) (583) (3,262) (583) (Loss) income from operations (3,232) 73 (8,749) 73 Finance expense (230) (99) (737) (99) Net loss for the period $ (3,462) $ (26) $ (9,486) $ (26)

Third Quarter 2014 Revenues Revenues increased by $20,812,000 as a result of the increase in tons sold at the Wilson Creek Division from Third Quarter 2013 to Third Quarter 2014 and the inclusion of PBS sales from August 19 to September 30, 2014. Sales of metallurgical coal were 263,000 tons at an average realized price of $93 per ton in Third Quarter 2014 compared with 73,000 tons at an average realized price of $96 per ton in Third

Corsa Coal Corp. Management’s Discussion and Analysis

For the nine months ended September 30, 2014

14

Quarter 2013. The decrease in average realized per ton was due to the fall in domestic and export prices for metallurgical coal (see “Outlook – Metallurgical Coal” below). Cost of sales Cost of sales increased by $22,630,000 as a result of the increase in tons sold at the Wilson Creek Division from Third Quarter 2013 to Third Quarter 2014 and the inclusion of PBS sales from August 19 to September 30, 2014 and a higher percentage of production from higher cost per ton mines in Third Quarter 2014 compared to Third Quarter 2013. Corporate and administrative expense Corporate and administrative expense includes general and administrative expenses relating to divisional administration. The expense increased by $1,487,000 primarily due to the inclusion of three months of expense for Wilson Creek Division in Third Quarter 2014 compared to two months in Third Quarter 2013 and the inclusion of PBS Corporate and administrative expense from August 19, 2014 to September 30, 2014 in Third Quarter 2014. Finance expense Finance expense increased by $131,000 from Third Quarter 2013 to Fourth Quarter 2014. Net loss for the period Net loss increased by $3,436,000 from Third Quarter 2013 to Third Quarter 2014 as a result of factors impacting the items described above. Nine Months 2014 Revenue Revenues increased by $34,972,000 as a result of the increase in tons sold at the Wilson Creek Division from Nine Months 2013 to Nine Months 2014 and the inclusion of PBS sales from August 19 to September 30, 2014. Sales of metallurgical coal were 401,000 tons at an average realized price of $92 per in Nine Months 2014 compared with 73,000 tons at an average realized price of $96 in Nine Months 2013. The decrease in average realized per ton was due to the fall in domestic and export prices for metallurgical coal (see “Outlook – Metallurgical Coal” below). Nine Months 2014 includes Wilson Creek from January 1 to September 30, 2014 and PBS from August 19, 2014 to September. Nine Months 2013 includes Wilson Creek from July 31 to September 30, 2013. Cost of sales Cost of sales increased by $41,115,000 as a result of the increase in tons sold at the Wilson Creek Division from Nine Months 2013 to Nine Months 2014 and the inclusion of PBS sales from August 19 to September 30, 2014 and a higher percentage of production from higher cost per ton mines in Third Quarter 2014 compared to Third Quarter 2013. Nine Months 2014 includes Wilson Creek from January 1 to September 30, 2014 and PBS from August 19, 2014 to September. Nine Months 2013 includes Wilson Creek from July 31 to September 30, 2013.

Corsa Coal Corp. Management’s Discussion and Analysis

For the nine months ended September 30, 2014

15

Corporate and administrative expense Corporate and administrative expense includes general and administrative expenses relating to divisional administration. The expense increased by $2,679,000 primarily due to the inclusion of nine months of expense for Wilson Creek Division in Nine Months 2014 compared to two months in Nine Months 2013 and the inclusion of PBS Corporate and administrative expense from August 19, 2014 to September 30, 2014 in Nine Months 2014. Nine Months 2014 includes Wilson Creek from January 1 to September 30, 2014 and PBS from August 19, 2014 to September. Nine Months 2013 includes Wilson Creek from July 31 to September 30, 2013. Finance expense Finance expense increased by $638,000 from Nine Months 2013 to Nine Months 2014. Net loss for the period Net loss increased by $9,460,000 from Nine Months 2013 to Nine Months 2014 as a result of factors impacting the items described above. CAPP

For the three months ended For the nine months ended September 30, September 30, 2014 2013 2014 2013 (000’s) (000’s) (000’s) (000’s) Revenues $ 16,728 $ 22,549 $ 46,730 $ 64,981 Cost of sales (15,943)

(17,064) (44,727)

(53,008)

Gross margin 785 5,485 2,003 11,883 Corporate and administrative expense (491) (502) (1,186) (1,872) Income from operations 294 4,983 817 10,011 Finance (expense) income (129) 1,358 (390) 110 Net income for the period $ 165 $ 6,341 $ 427 $ 10,121

Third Quarter 2014 Revenue Revenues decreased by $5,821,000 as a result of the decreases in tons sold and average price from Third Quarter 2013 to Third Quarter 2014. Sales of thermal coal were 247,000 tons at an average realized price of $68 per ton in Third Quarter 2014 compared with 299,000 tons at an average realized price of $75 in Third Quarter 2013. The decrease in average realized price per ton was due to the decline in regional prices for thermal coal (see “Outlook – Thermal Coal” below). Cost of sales Cost of sales decreased by $1,121,000 as a result of the decreases in tons sold. The Cash production cost per ton sold (see “Non-GAAP Measures” below), a component of cost of sales, increased to $59 in Third Quarter 2014 from $51 in Third Quarter 2013 as a result of more production from higher cost mines in Third Quarter 2014 compared to Third Quarter 2013.

Corsa Coal Corp. Management’s Discussion and Analysis

For the nine months ended September 30, 2014

16

Corporate and administrative expense Corporate and administrative expense includes general and administrative expenses relating to divisional administration. The expense decreased by $11,000 from Third Quarter 2013 to Third Quarter 2014. Finance (expense) income Finance expense changed by $1,487,000 from income in Third Quarter 2013 to expense in Third Quarter 2014. The major item that contributed to the income in Third Quarter 2013 was the change in the fair value of Units repayable on demand of $1,481,000. The Units payable on demand were extinguished on July 31, 2013. Net income for the period Net income decreased by $6,176,000 from Third Quarter 2013 to Third Quarter 2014 as a result of factors impacting the items described above. Nine Months 2014 Revenue Revenues decreased by $18,251,000 as a result of the decreases in tons sold and average price from Nine Month 2013 to Nine Months 2014. Sales of thermal coal were 699,000 tons at an average realized price of $68 per ton in Nine Months 2014 compared with 866,000 tons at an average realized price of $75 in Nine Months 2013. The decrease in average realized price per ton was due to the decline in regional prices for thermal coal (see “Outlook – Thermal Coal” below). Cost of sales Cost of sales decreased by $8,281,000 as a result of the decreases in tons sold. The Cash production cost per ton sold (see “Non-GAAP Measures” below), a component of cost of sales, increased to $58 in Nine Months 2014 from $55 in Nine Months 2013 as a result of more production from higher cost mines in Nine Months 2014 compared to Nine Months 2013. Corporate and administrative expense Corporate and administrative expense decreased by $686,000 from Nine Months 2013 to Nine Months 2014. Finance (expense) income Finance expense changed by $500,000 from income in Nine Months 2013 to expense in Nine Months 2014. The major item that contributed to the income in Nine Months 2013 was the change in the fair value of Units repayable on demand of $420,000. The Units payable on demand were extinguished on July 31, 2013. Net income for the period Net income decreased $9,694,000 from Nine Months 2013 to Nine Months 2014 as a result of factors impacting the items described above.

Corsa Coal Corp. Management’s Discussion and Analysis

For the nine months ended September 30, 2014

17

Corporate

For the three months ended For the nine months ended September 30, September 30, 2014 2013 2014 2013 (000’s) (000’s) (000’s) (000’s) Revenues $ - $ - $ - $ - Cost of sales (11)

(6) (31)

(5)

Gross margin (11) (6) (31) (5) Corporate and administrative expense (1,265) (437) (3,306) (353) (Loss) (income) from operations (1,276) (443) (3,337) (358) Finance expense (20,984) (6,756) (15,483) (6,753) Transaction expenses (1,184) (1,632) (1,891) (2,642) Bargain purchase price - 60,026 - 60,026 (22,168) 51,638 (17,374) 50,631 (Loss) income before tax (23,444) 51,195 (20,711) 50,273

Current income tax expense (320) (629) (419) (2,060) Deferred income tax expense (4,347) (4,209) (1,098) (4,466) (4,667) (4,838) (1,517) (6,526) Net (loss) income for the period $ (28,111) $ 46,357 $ (22,228) $ 43,747

Third Quarter 2014 Cost of sales Cost of sales increased by $5,000 from Third Quarter 2013 compared to Third Quarter 2014. Corporate and administrative expense Corporate and administrative expense includes corporate expenses and general and administrative expenses relating to divisional administration. The expense increased by $828,000 from Third Quarter 2013 to Third Quarter 2014. The increase was due to higher head office expenses as a result of the Quintana Transaction and the PBS Transaction and the inclusion of three months of Corporate and administrative expense in Third Quarter 2014 compared to two months in Third Quarter 2013. Finance expense Finance expense increased by $14,228,000 from Third Quarter 2013 to Third Quarter 2014. The major item that contributed to the increase was the change in the fair value of Redeemable Units which resulted in an expense of $22,276,000 in Third Quarter 2014 compared to an expense of $6,784,000 in Third Quarter 2013, an increase of $15,442,000. Subsequent to August 19, 2014, the Company will not incur any finance expense or income related to the Redeemable Units as they are no longer recognized as a financial liability. Transaction expenses Transaction expenses decreased by $448,000 from Third Quarter 2013 to Third Quarter 2014. The expenses in Third Quarter 2014 were related to the PBS Transaction and the Transaction expenses in Third Quarter 2013 were related to the Quintana Transaction.

Corsa Coal Corp. Management’s Discussion and Analysis

For the nine months ended September 30, 2014

18

Bargain purchase gain The Bargain purchase gain was $60,026,000 in Third Quarter 2013 and there was no comparable amount in Third Quarter 2014. The Bargain purchase gain resulted from the Quintana Transaction. Current income tax expense Current tax expense decreased by $309,000 from Third Quarter 2013 to Third Quarter 2014 as taxable income decreased from Third Quarter 2013 to Third Quarter 2014. Deferred income tax expense Deferred income tax expenses increased by $138,000 from Third Quarter 2013 to Third Quarter 2014. Net (loss) income for the period Net (loss) income changed from an income of $46,357,000 in Third Quarter 2013 to a loss of $28,111,000 in Third Quarter 2014 as a result of factors impacting the items described above. Nine Months 2014 Cost of sales Cost of sales increased by $26,000 in Nine Months 2013 compared to Nine Months 2014. Corporate and administrative expense Corporate and administrative expense includes corporate expenses and general and administrative expenses relating to divisional administration. The expense increased by $2,953,000 from Nine Months 2013 to Nine Months 2014. The increase was due to higher head office expenses as a result of the Quintana Transaction and the PBS Transaction and the inclusion of nine months of Corporate and administrative expense in Nine Months 2014 compared to two months in Nine Months 2013. Finance expense Finance expense increased by $8,730,000 from Nine Months 2013 to Nine Months 2014. The major item that contributed to the increase was the change in the fair value of Redeemable Units which resulted in an expense of $16,716,000 in Nine Months 2014 compared to an expense of $6,784,000 in Nine Months 2013, an increase of $9,932,000. Subsequent to August 19, 2014, the Company will not incur any finance expense or income related to the Redeemable Units as they are no longer recognized as a financial liability. Transaction expenses Transaction expenses decreased by $751,000 from Nine Months 2013 to Nine Months 2014. The expenses in Nine Months 2014 were related to the PBS Transaction and the Transaction expenses in Nine Months 2013 were related to the Quintana Transaction.

Corsa Coal Corp. Management’s Discussion and Analysis

For the nine months ended September 30, 2014

19

Bargain purchase gain The Bargain purchase gain was $60,026,000 in Nine Months 2013 and there was no comparable amount in Nine Months 2014. The Bargain purchase gain resulted from the Quintana Transaction. Current income tax expense Current tax expense decreased by $1,641,000 from Nine Months 2013 to Nine Months 2014 as taxable income decreased from Nine Months 2013 to Nine Months 2014. Deferred income tax expense Deferred income tax expense decreased by $3,368,000 from Nine Months 2013 to Nine Months 2014. Net (loss) income for the period Net (loss) income changed from an income of $43,747,000 in Nine Months 2013 to a loss of $22,228,000 in Nine Months 2014 as a result of factors impacting the items described above. Outlook Corsa’s coal sales guidance for 2014 is approximately 1,612,000 to 1,662,000 tons. This consists of metallurgical coal sales guidance of approximately 701,000 to 721,000 tons and thermal coal sales guidance of approximately 911,000 to 941,000 tons. The coal sales guidance for 2014 in Corsa’s Management’s Discussion and Analysis for the three months and six months ended June 30, 2014 was 1,700,000 tons which consisted of metallurgical coal sales guidance of approximately 830,000 tons and thermal coal sales guidance of approximately 870,000 tons. The metallurgical coal sales guidance changed due to a reduction in expected export orders and the thermal coal sales guidance changed due to a revised customer delivery schedule. Metallurgical Coal In order to make a strong and stable coke for steel companies’ production of iron, low volatile coal is a necessary ingredient in the sensitive coal blend required. The NAPP Division’s metallurgical reserve base consists entirely of premium rank low volatile coal. This unique quality gives the Company’s metallurgical coal product a secure place in the domestic and seaborne trade.

During 2013, Corsa was able to demonstrate the value of its metallurgical coal to domestic and international steel producers. As a result of the positive quality and reliability of its metallurgical coal, Corsa has been awarded supply agreements for 2014 and beyond. In Nine Months 2014, metallurgical coal sales were 401,000 tons. The metallurgical coal sales guidance for the fourth quarter of 2014 is approximately 300,000 to 320,000 tons, from the newly formed combination of Wilson Creek and PBS, of which 100% is contracted and approximately 75% is contracted. Corsa also has sales contracts for 150,000 tons in 2015 and 38,000 tons in 2016. Corsa expects to enter into sales contracts for the majority of its 2015 domestic sales volumes in the fourth quarter of 2014, consistent with industry practice.

Through the acquisition of PBS, Corsa has gained access to a significant new customer base of both domestic and international steel producers which has diversified its sales mix. Corsa has historically made sales of metallurgical coal to some of the PBS customers but a significant portion of the sales contracts acquired are new customers. Corsa is currently working with these new customers to ensure a seamless

Corsa Coal Corp. Management’s Discussion and Analysis

For the nine months ended September 30, 2014

20

transition for the delivery of the contracted sales of PBS and will continue to provide a reliable supply of metallurgical coal in the future. Current metallurgical coal prices are at level where a significant amount of global production is uneconomic. Prices in the domestic metallurgical coal markets for 2014 have fallen from 2013 levels by approximately 10% and prices for export shipments in 2014 have declined approximately 21% from 2013 levels. . As a result, a significant portion of the global seaborne coal production is being produced at a loss, a situation that many view as unsustainable. Producers have responded to these conditions and have increasingly shown supply discipline, announcing production cuts of approximately 20 million metric tonnes of production so far this year. Settlements on 2015 domestic metallurgical coal sales are starting to take place. Export pricing has been very competitive due to oversupply, particularly from Australian mines, and a weaker Australian dollar. The company is well positioned to take advantage of logistics to the domestic market with its close proximity to coke producers on the river systems easily accessed by truck or rail through Pittsburgh. Corsa’s low volatile product is highly sought after for its low pressure quality. Access to seaborne trade via a short rail distance to the Baltimore export terminals solidifies Corsa’s ability to participate when seaborne pricing is attractive.

Thermal Coal Corsa’s CAPP production is sold into the Utility and Industrial markets for the production of electricity. The CAPP reserve base exclusively consists of high BTU and high carbon content coal. These unique qualities set CAPP apart from other producers and create a niche in the Utility and Industrial marketplace. During 2013 and in Nine Months of 2014, Corsa has been successful is demonstrating to the utility consumers the value, consistency and quality of CAPP thermal production. Corsa will continue to target the Industrial market segment as Corsa continues to transition from a Utility supplier to an Industrial supplier during the remaining three months of 2014 and into calendar year 2015. Total sales of thermal coal in the Nine Months 2014 amounted to 691,000 tons. While the thermal coal market continues to outpace demand 2014, Corsa has been successful in maintaining a high level of contracted sales for the future. In 2015, Corsa’s CAPP production is 72% contracted. The thermal coal sales guidance for fourth quarter of 2014 is approximately 220,000 to 250,000 tons, of which 100% is contracted and approximately 100% is contracted and priced at an average of $67. The Company also has sales contracts in place for 650,000 tons in 2015, 500,000 tons in 2016, and subject to mutual agreement, and 500,000 tons in 2017.

Current Southeastern US utility market Thermal coal pricing has declined 5% over the course of 2014. As a result, much of the Central Appalachia coal production is below the marginal supply curve. Corsa expects Utility coal demand for Central Appalachia production to decrease in 2015. Conversely, Industrial Thermal demand grew 4% year over year for 2014. The Company expects Industrial demand to grow 1% in 2015.

Corsa Coal Corp. Management’s Discussion and Analysis

For the nine months ended September 30, 2014

21

PBS Transaction

Acquisition of PBS On August 19, 2014, Corsa completed the purchase of all of the outstanding shares of PBS for $53,101,000 in cash and is required to fund, except under certain circumstances, $20,000,000 of cash into escrow accounts for water treatment and certain other liabilities. Any amounts remaining in escrow, subject to certain conditions, are to be released to OAO Severstal as additional consideration. The primary purpose of the acquisition was to continue Corsa’s growth strategy focusing on low-volatile metallurgical coal and to secure additional infrastructure, operating capacity and reserves of low-volatile metallurgical coal. PBS’s operations are located adjacent to Corsa’s Wilson Creek division. Based in Somerset County, Pennsylvania, PBS commenced production in 1963 and was acquired by OAO Severstal in 2008. Its current operations include 13 developed mines (3 of which are active) and two preparation plants with access to both the CSX and Norfolk Southern Railway. Collectively, these mines sold approximately 2.5 million and 1.7 million tons of premium quality low-volatile metallurgical coal in 2012 and 2013, respectively. PBS is located 60 miles from Pittsburgh and 170 miles from the Port of Baltimore and its coal brands are well recognized by long-standing domestic and international customers. Its existing assets and infrastructure enable PBS to scale up to 3.5 million tons of saleable metallurgical production per year if market conditions warrant. Financing of PBS Transaction The consideration for the PBS Transaction was paid using equity financing and a new credit facility with residual proceeds from the equity financing and credit facility being used for purposes related to the PBS Transaction and growth capital:

• $65,425,329 was raised through a non-brokered private placement (“Private Placement”) of Common Shares of Corsa at a price of Cdn $0.15 per Common Share resulting in the issuance of 463,821,966 Common Shares of Corsa (Cdn $69,573,295, based on the exchange rate of US$1.00:Cdn$1.0634, being the Bank of Canada’s noon rate on July 3, 2014); and

• $25,000,000 was raised through a non-revolving term credit facility underwritten by Sprott Resource Lending Partnership (“SRL”).

Private Placement Pursuant to the private placement, Sprott Resource Partnership (“SRP”) acquired 236,963,302 Common Shares, for an aggregate price of approximately $33.4 million. As of the date of issuance of this MD&A, SRP holds approximately 19.9% of the outstanding Common Shares of Corsa. SRP will have certain ongoing rights including the right to nominate one member of the Corsa board of directors, subject to certain conditions. The right to nominate one member of the Corsa board of directors will terminate if SRP, together with its affiliates, ceases to hold at least 10% or more of the outstanding Common Shares of Corsa for a continuous period of at least 30 days, Quintana has provided an undertaking to vote in favor of the election of the SRP board nominee at any shareholder meeting, for so long as Quintana controlled entities own at least 20% of the outstanding Common Shares of Corsa. SRP also entered into a registration rights agreement with Corsa which provides SRP with certain registration rights for as long as it holds at least 10% of the outstanding Common Shares of Corsa.

Corsa Coal Corp. Management’s Discussion and Analysis

For the nine months ended September 30, 2014

22

Pursuant to the private placement, QEP II acquired 128,824,387 Common Shares for an aggregate price of approximately $18.1 million and QEP II – TE acquired 12,962,279 Common Shares for an aggregate price of approximately $1.8 million. As of the date of this MD&A, Quintana exercises control or direction over 578,819,438 Common Shares of Corsa, representing approximately 48.6% of the issued and outstanding Corsa Shares, and 170,316,639 Redeemable Units of WCE. Assuming the tender for redemption of all Redeemable Units and exchange for Common Shares of Corsa, Quintana would exercise control or direction over an aggregate of 749,136,077 Common Shares, representing approximately 55.0% of the then issued and outstanding Common Shares of Corsa. Pursuant to the private placement, Zebra Holdings and Investments S.á r.l. and Lorito Holdings S.á r.l., two corporations controlled by Lundin family trusts and current shareholders of Corsa, acquired an aggregate of 70,893,332 Common Shares for an aggregate price of approximately $10 million and Bank Julius Baer & Co. Ltd. acquired 14,178,666 Common Shares for an aggregate price of approximately $2 million. Credit Facility In connection with the PBS Transaction, Corsa entered into a 5-year senior secured non-revolving term credit facility in the amount of $25 million (“Facility”). The interest rate under the Facility is ten percent (10%) per annum. For the period up to and including the second anniversary of the Facility, Corsa has the option of adding any interest payable under the Facility to the principal amount or, subject to approval of the TSX Venture Exchange (“TSXV”), satisfying any interest payment by the issuance of Common Shares of Corsa (based on five day volume weighted average trading price for its Common Shares immediately prior to the last business day of the period multiplied by 105%). In addition, the Facility may be prepaid without penalty, in whole or in part, at any time after three months of interest has been paid. In consideration for the Facility, SRL issued 36.1 million Common Share purchase warrants of Corsa (“Bonus Warrants”). Each Bonus Warrant has a term of five years and is exercisable for one Common Share of Corsa at an exercise price of Cdn$0.195. The Bonus Warrants issued to SRL and the Common Shares issuable thereunder are subject to resale restrictions pursuant to applicable securities laws requirements and the policies of the TSXV and will not be freely tradable until December 20, 2014. Integration of PBS operations Corsa is combining its Wilson Creek Division and PBS into the NAPP Division to take advantage of a newly created, centrally located management team and infrastructure that as a result of the combination will result in significant cost savings for the combined entity. Given the varying chemical characteristics of the coal assets of PBS, along with those of the Wilson Creek Division, Corsa will also be able to take advantage of coal blending opportunities to further differentiate and tailor its low-volatile metallurgical coal product to customer’s specifications. Additional integration efforts are taking place to reduce operating costs, increase utilization of existing infrastructure, upgrade equipment, and adjust mine planning to the larger portfolio of mines. Corsa is currently undergoing a detailed analysis of the combined operations in order to maximize the efficiency of the operations and ensure capital and resource allocation decisions are made on a combined basis. In addition to the Wilson Creek preparation plant that is currently being operated by Company, PBS currently operates two preparation plants, with rail access to both CSX and NS service. The combination of the infrastructure is expected to give Corsa a delivered cost advantage to domestic steel producers in the Northern Appalachia area.

Corsa Coal Corp. Management’s Discussion and Analysis

For the nine months ended September 30, 2014

23

Regulatory filings Corsa filed a technical report compliant with National Instrument 43-101 National Instrument 43-101 – Standards of Disclosure for Mineral Projects (“NI 43-101”) for the acquired operations of PBS on October 14, 2014 and a business acquisition report for the PBS Transaction on November 3, 2014. Both filings are available under Corsa’s profile on www.sedar.com. Quintana Transaction On July 31, 2013, Corsa completed a transaction with QKGI, a portfolio company of Quintana, which resulted in Corsa raising a total of $40 million by way of equity subscriptions at Cdn$0.17 per Common Share and acquiring QKGI, a Tennessee-based coal producer, and Quintana having acquired a control position in Corsa. The $40 million was used to repay a $25 million credit facility outstanding at the time, transaction costs and for general corporate and growth purposes. Full details of the Quintana Transaction are included in Corsa’s management discussion and analysis for the twelve months ended December 31, 2013. The Filing Statement filed in connection with the Transaction is available under Corsa’s profile at www.sedar.com. As a result of the Quintana Transaction, QKGI New Holdings LP (“New QKGI”) and QKGI Legacy Holdings LP (“Legacy QKGI”), two entities controlled by Quintana, were issued an aggregate of approximately 377.2 million Common Shares of Corsa and QKGI Legacy Holdings LP was issued approximately 230.1 million common membership units (“Redeemable Units”) of WCE. On June 30, 2014, Legacy QKGI redeemed approximately 59.8 million Redeemable Units in exchange for Common Shares of Corsa on a one to one basis. As at September 30, 2014, Quintana entities controlled approximately 170.3 million Redeemable Units and approximately 437.0 million Common Shares of Corsa. Quintana controlled entities also acquired an additional 141,786,666 Common Shares of Corsa as part of the equity financing to fund the PBS Transaction. See “PBS Transaction” for further details. As at the date of issuance of this MD&A, assuming the tender for redemption of all Redeemable Units and exchange for Common Shares of Corsa, Quintana would exercise control or direction over an aggregate of 749,136,077 Common Shares, representing approximately 55.0% of Corsa’s then issued and outstanding Common Shares.

Changes in Directors and Officers

Following completion of the PBS Transaction, Corsa announced the appointment of George Dethlefsen as its Chief Executive Officer. Mr. Dethlefsen is currently also a director of Corsa. As part of the transition, Mr. Dethlefsen has stepped down as Managing Director of Quintana Capital Group, an entity controlled by Quintana.

Following completion of the PBS Transaction, Keith Dyke, President of Corsa, was appointed Chief Operating Officer and President and stepped down as a member of the board of directors of Corsa. Pursuant to the terms of SRP’s acquisition of Common Shares under the private placement, Arthur Einav, a nominee of SRP, was appointed to the board of directors. Arthur Einav is Managing Director, General Counsel and Corporate Secretary of Sprott Resource Corp. Mr. Einav is also General Counsel of Sprott Inc. and is a director of Independence Contract Drilling, Inc., a NYSE-listed portfolio company of Sprott Resource Corp. He holds a Bachelor of Laws degree and a Masters in Business Administration from Osgoode Hall Law School and the Schulich School of Business. He also holds a Bachelor of Science

Corsa Coal Corp. Management’s Discussion and Analysis

For the nine months ended September 30, 2014

24

degree from the University of Toronto and is a member of the Law Society of Upper Canada and the New York State Bar. Financial Condition

As at As at September 30, December 31,

2014 2013 (000’s) (000’s) Current Assets $ 82,602 $ 28,921 Non-Current Assets 319,332 173,803 Total Assets $ 401,934 $ 202,724

Current liabilities $ 73,587 $ 21,680 Non-current liabilities 110,110 51,286 Total liabilities $ 183,697 $ 72,966 Total equity $ 218,237 $ 129,758

The total assets of Corsa at September 30, 2014 were $401,934,000 compared with $202,724,000 at December 31, 2013, an increase of $199,210,000. The current assets of Corsa at September 30, 2014 were $82,602,000 compared with $28,921,000 at December 31, 2013, an increase of $53,681,000. The overall increase resulted from the increases in amounts receivable of $30,800,000, restricted cash of $4,699,000, prepaid expenses of $1,918,000 and inventories of $21,385,000 offset by a decrease in cash of $5,121,000. On August 19, 2014, Corsa acquired current assets of $33,524,000 from the PBS Transaction. The non-current assets of Corsa at September 30, 2014 were $319,332,000 compared with $173,803,000 at December 31, 2013, an increase of $145,529,000.The overall increase was primarily due to the increases in restricted cash of $43,458,000, advance royalties and other assets of $7,209,000, property, plant and equipment of $95,959,000 offset by the decrease in the deferred tax asset by $1,097,000. On August 19, 2014, Corsa acquired non-current assets of $148,639,000 from the PBS Transaction. The total liabilities of Corsa at September 30, 2014 were $183,697,000 compared with $72,966,000 at December 31, 2013, an increase of $110,731,000. The current liabilities of Corsa at September 30, 2014 were $73,587,000 compared with $21,680,000 at December 31, 2013, an increase of $51,907,000.The overall increase was due to the increases in accounts payable of $21,239,000, payable to escrow of $20,000,000, current portion of other liabilities of $7,000,000 and current portion of reclamation provision of $5,155,000 offset by decreases in current portion of notes payable of $954,000, current portion of finance lease obligations of $180,000, and the tax distribution payable of $353,000. On August 19, 2014, Corsa acquired current liabilities of $23,460,000 from the PBS Transaction.

Corsa Coal Corp. Management’s Discussion and Analysis

For the nine months ended September 30, 2014

25

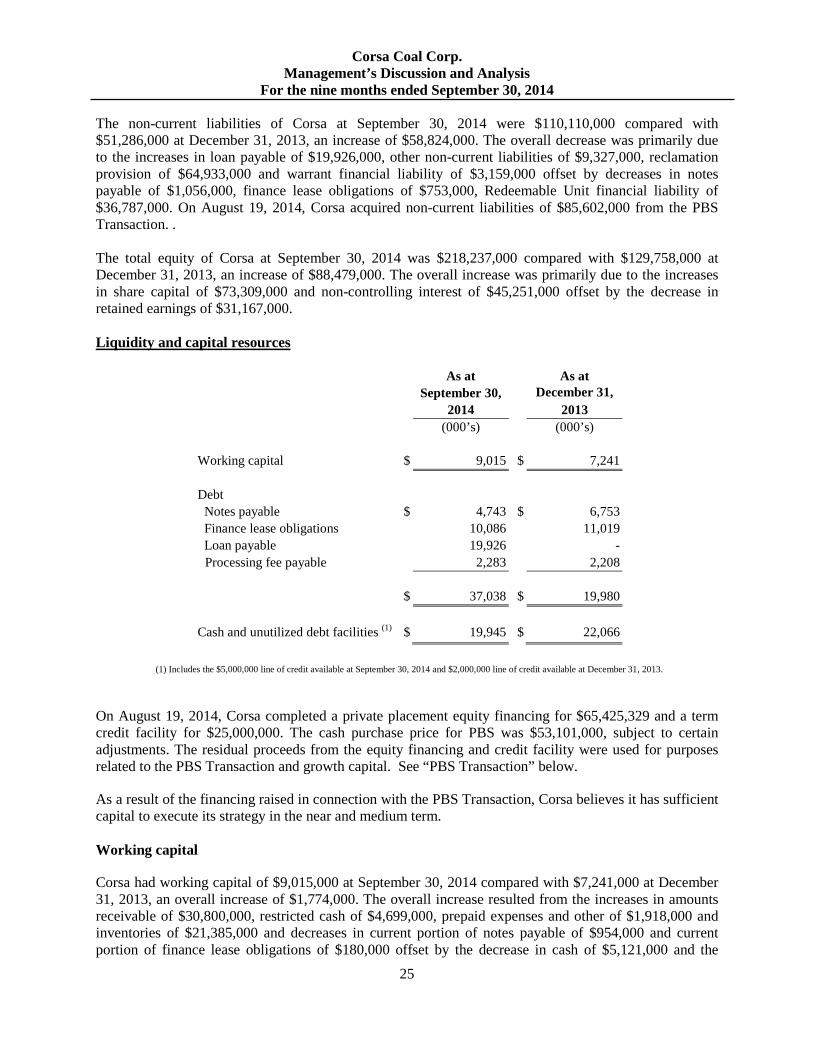

The non-current liabilities of Corsa at September 30, 2014 were $110,110,000 compared with $51,286,000 at December 31, 2013, an increase of $58,824,000. The overall decrease was primarily due to the increases in loan payable of $19,926,000, other non-current liabilities of $9,327,000, reclamation provision of $64,933,000 and warrant financial liability of $3,159,000 offset by decreases in notes payable of $1,056,000, finance lease obligations of $753,000, Redeemable Unit financial liability of $36,787,000. On August 19, 2014, Corsa acquired non-current liabilities of $85,602,000 from the PBS Transaction. . The total equity of Corsa at September 30, 2014 was $218,237,000 compared with $129,758,000 at December 31, 2013, an increase of $88,479,000. The overall increase was primarily due to the increases in share capital of $73,309,000 and non-controlling interest of $45,251,000 offset by the decrease in retained earnings of $31,167,000. Liquidity and capital resources

As at As at September 30, December 31,

2014 2013 (000’s) (000’s) Working capital $ 9,015 $ 7,241 Debt Notes payable $ 4,743 $ 6,753 Finance lease obligations 10,086 11,019 Loan payable 19,926 -

Processing fee payable 2,283 2,208 $ 37,038 $ 19,980

Cash and unutilized debt facilities (1) $ 19,945 $ 22,066

(1) Includes the $5,000,000 line of credit available at September 30, 2014 and $2,000,000 line of credit available at December 31, 2013.

On August 19, 2014, Corsa completed a private placement equity financing for $65,425,329 and a term credit facility for $25,000,000. The cash purchase price for PBS was $53,101,000, subject to certain adjustments. The residual proceeds from the equity financing and credit facility were used for purposes related to the PBS Transaction and growth capital. See “PBS Transaction” below.

As a result of the financing raised in connection with the PBS Transaction, Corsa believes it has sufficient capital to execute its strategy in the near and medium term. Working capital

Corsa had working capital of $9,015,000 at September 30, 2014 compared with $7,241,000 at December 31, 2013, an overall increase of $1,774,000. The overall increase resulted from the increases in amounts receivable of $30,800,000, restricted cash of $4,699,000, prepaid expenses and other of $1,918,000 and inventories of $21,385,000 and decreases in current portion of notes payable of $954,000 and current portion of finance lease obligations of $180,000 offset by the decrease in cash of $5,121,000 and the

Corsa Coal Corp. Management’s Discussion and Analysis

For the nine months ended September 30, 2014

26

increase in accounts payable of $21,239,000, payable to escrow of $20,000,000, current portion of other liabilities of $7,000,000 and current portion of reclamation provision of $5,155,000. Sources of Cash During Third Quarter 2014 and Nine Months 2014, the primary sources of cash for Corsa were revenue collections, the private placement equity financing (see PBS Transaction) and the term credit facility (see “PBS Transaction” for further details). Cash flows Third Quarter 2014 Operating activities In Third Quarter 2014, the cash used by operating activities was $20,742,000 compared with cash provided of $7,879,000 in Third Quarter 2013, a change of $28,621,000. The cash provided by operating activities before changes in non-cash working capital balances related to operations in Third Quarter 2014 was $1,171,000 compared with $5,416,000 in Third Quarter 2013. The changes in non-cash working capital balances related to operations in Third Quarter 2014 used cash of $21,913,000 and provided cash of $2,463,000 in Third Quarter 2013. Investing activities The cash used in investing activities in Third Quarter 2014 was $62,753,000 compared with cash provided of $8,989,000 in Third Quarter 2013, a change of $71,742,000. In Third Quarter 2014, restricted cash used cash of $8,653,000 and the PBS transaction used cash of $50,639,000. Cash acquired under the Quintana Transaction was $9,827,000 in Third Quarter 2013. Property, plant and equipment additions used cash of $2,823,000 in Third Quarter 2014 compared with $777,000 in Third Quarter 2014. Financing activities In Third Quarter 2014, cash provided by financing activities was $87,810,000 compared with cash used of $6,164,000 in Third Quarter 2013, a change of $93,974,000. Proceeds from equity financing provided cash of $65,425,000 and proceeds from loan payable provided cash of $25,000,000 in Third Quarter 2014. In Third Quarter 2014, cash used for notes payable was $368,000 compared with $557,000 in Third Quarter 2013 and the cash used for Finance lease was $1,337,000 in Third Quarter 2014 compared with $738,000 in Third Quarter 2013. Nine Months 2014 Operating activities In Nine Months 2014, the cash used by operating activities was $23,990,000 compared with cash provided of $11,866,000 in Nine Months 2013, a change of $35,856,000. The cash provided by operating activities before changes in non-cash working capital balances related to operations in Nine Months 2014 was $840,000 compared with $11,796,000 in Nine Months 2013. The changes in non-cash working capital balances related to operations in Nine Months 2014 used cash of $24,830,000 compared with $70,000 in Nine Months 2013.

Corsa Coal Corp. Management’s Discussion and Analysis

For the nine months ended September 30, 2014

27

Investing activities The cash used in investing activities in Nine Months 2014 was $64,421,000 compared with cash provided of $7,834,000 in Nine Months 2013, a change of $72,255,000. In Nine Months 2014, restricted cash used cash of $6,195,000 and the PBS transaction used cash of $50,639,000. Cash acquired under the Quintana Transaction was $9,827,000 in Nine Months 2013. Property, plant and equipment additions used cash of $7,006,000 in Nine Months 2014 compared with $1,932,000 in Nine Months 2014. Financing activities In Nine Months 2014, cash provided by financing activities was $83,290,000 compared with cash used of $7,979,000 in Nine Months 2013, a change of $91,269,000. Proceeds from equity financing provided cash of $65,425,000 and proceeds from loan payable provided cash of $25,000,000 in Nine Months 2014. In Nine Months 2014, cash used for notes payable was $2,150,000 compared with $1,492,000 in Nine Months 2013 and the cash used for finance lease was $3,722,000 in Nine Months 2014 compared with $1,618,000 in Nine Months 2013. Capital expenditures

Corsa’s future spending on property, plant and equipment at its operations will be dependent on cash on hand and equipment financing that Corsa obtains. In Second Half , Corsa anticipates that it will upgrade the capital equipment currently utilized at the PBS operations which will be funded from cash on hand as well as finance leases, where determined appropriate by Corsa. The timing of development of Corsa’s coal properties will be dependent on market demand.

Debt Corsa has certain covenants it is required to meet under its finance lease obligations and certain notes payable. Certain measures included in the covenant calculations are not readily identifiable from Corsa’s consolidated income statement or consolidated balance sheet. These measures are considered to be Non-GAAP financial measures and as such, a further description of the covenant calculations is included in Corsa’s MD&A for the twelve months ended December 31, 2013. Corsa was in compliance with all covenants as at September 30, 2014.

Corsa Coal Corp. Management’s Discussion and Analysis

For the nine months ended September 30, 2014

28

Contractual obligations Corsa has the following contractual obligations:

Payments due by period Carrying

value as at September 30, 2014

Less than 1 to 4 to After 5

Total 1 year 3 years 5 years years

Accounts payable and accruals $ 30,272 $ 30,272 $ 30,272 $ - $ - $ -

Payable to escrow 20,000 20,000 20,000 - - - Notes payable 4,473 4,938 3,721 1,217 - - Finance lease obligations 10,086 10,706 4,911 5,120 675 - Loan payable 19,926 37,500 2,500 5,000 30,000 - Processing fee payable 2,283 3,000 - - - 3,000 Other non-current liabilities 20,407 20,407 8,000 8,000 2,000 2,407 Reclamation provision 72,821 106,820 7,936 11,052 10,519 77,313 Financial warrant liability 3,159 - - - - - Other commitments - 25,980 5,640 6,780 6,780 6,780 Purchase commitments

on capital equipment - 305 305 - - - Operating leases and other obligations - 6,905 3,371 3,004 531 - Total $ 183,697 $ 266,834 $ 86,656 $ 40,173 $ 50,505 $ 89,500

Non-GAAP Financial Measures This MD&A reports certain financial measures, not recognized under IFRS (“GAAP”), as used by management and readers of this MD&A to evaluate the historical performance of Corsa. Since certain non-GAAP financial measures may not have a standardized meaning and may not be comparable to similar measures presented by other companies, the non-GAAP measures are clearly defined, quantified and reconciled with their nearest GAAP measure. The financial measures referred to this MD&A, namely EBITDA (earnings before deductions for interest, taxes, depreciation and amortization);Adjusted EBITDA (EBITDA adjusted for other operating costs, stock-based compensation finance expense, interest expense, transaction expenses and bargain purchase gain); cash flow from operations; net coal sales revenue; realized price per ton; cash production cost and cash production cost per ton, are not measures recognized by GAAP. Management uses EBITDA, Adjusted EBITDA, Cash flow from operations, Realized price per ton and Cash production cost per ton as internal measurements of operating performance for Corsa’s mining and processing operations. Management believes these non-GAAP measures provide useful information for investors as they provide information in addition to the GAAP measures to assist in their evaluation of the operating performance of Corsa.

Corsa Coal Corp. Management’s Discussion and Analysis

For the nine months ended September 30, 2014

29

EBITDA and Adjusted EBITDA The calculation and reconciliation of non-GAAP EBITDA and non-GAAP Adjusted EDITDA to Net (loss) income is as follows:

For the three months ended For the nine months ended September 30, September 30, 2014 2013 2014 2013 (000’s) (000’s) (000’s) (000’s) Net (loss) income $ (31,408) $ 52,672 $ (31,287) $ 53,842 Amortization expense 7,248 3,709 14,791 7,297 Interest expense 460 125 772 291 Income tax expense 4,667 4,838 1,517 6,526 EBITDA (19,033) 61,344 (14,207) 67,956 Other operating costs 53 (24) 1,651 (24) Stock-based compensation 497 32 1,086 32 Finance expense 21,343 5,497 16,610 6,742 Interest expense (460) (125) (772) (291) Transaction expenses 1,184 1,632 1,891 2,642 Bargain purchase gain

- (60,026) - (60,026)

Adjusted EBITDA $ 3,584 $ 8,330 $ 6,259 $ 17,031

Cash flow from operations The calculation and reconciliation of non-GAAP Cash flow from operations to Cash (used in) provided by operating activities is as follows:

For the three months ended For the nine months ended September 30, September 30, 2014 2013 2014 2013 (000’s) (000’s) (000’s) (000’s) Cash (used in) provided by

operating activities $ (20,742) $ 7,879 $ (23,990) $ 11,866 Transaction expenses 1,184 1,632 1,891 2,642 Cash spent on reclamation activities 711 510 1906 546 Changes in non-cash working capital balances related to operations 21,913 (2,463) 24,830 (70) Cash flow from operations $ 3,066 $ 7,558 $ 4,637 $ 14,984

Corsa Coal Corp. Management’s Discussion and Analysis

For the nine months ended September 30, 2014

30

Realized price per ton The calculation and reconciliation of net coal sales revenue to coal sales revenue and the calculation of Realized price per ton (net coal sales revenue divided by the tons sold) is as follows: NAPP

For the three months ended For the nine months ended September 30, September 30, 2014 2013 2014 2013 Metallurgical coal sales revenue $ 27,269,000 $ 7,610,000 $ 41,429,000 $ 7,610,000 Transportation costs (2,885,000) (604,000) (4,386,000) (604,000) Net metallurgical coal sales revenue $ 24,384,000 $ 7,006,000 $ 37,043,000 $ 7,006,000 Metallurgical coal tons sold 263,000 73,000 401,000 73,000 Realized price per ton $ 93 $ 96 $ 92 $ 96 CAPP

For the three months ended For the nine months ended September 30, September 30, 2014 2013 2014 2013 Thermal coal sales revenue $ 16,728,000 $ 22,549,000 $ 46,730,000 $ 64,891,000 Transportation costs - - - - Net thermal coal sales revenue $ 16,728,000 $ 22,549,000 $ 46,730,000 $ 64,891,000 Thermal coal tons sold 247,000 299,000 691,000 866,000 Realized price per ton $ 68 $ 75 $ 68 $ 75

Corsa Coal Corp. Management’s Discussion and Analysis

For the nine months ended September 30, 2014

31

Cash production cost per ton sold The calculation and reconciliation of cash production cost to cost of sales and the calculation of cash production cost per ton (cash production costs divided by the tons of coal sold) is as follows: Consolidated

For the three months ended For the nine months ended September 30, September 30, 2014 2013 2014 2013 Cost of sales(1) $ 45,538,000 24,024,000

$ 92,827,000 $ 59,967,000

Amortization expense (7,248,000) (3,709,000) (14,791,000) (7,297,000) Transportation costs (2,885,000) (604,000) (4,386,000) (604,000) Other operating costs (53,000) 24,000 (1,651,000) 24,000 Tolling and other revenue (1,153,000) - (1,153,000) - Cash production cost $ 34,199,000 $ 19,735,000 $ 70,846,000 $ 52,090,000 (1) Please refer to Note 13 to the consolidated financial statements at September 30, 2014 for the components of cost of sales. NAPP

For the three months ended For the nine months ended September 30, September 30, 2014 2013 2014 2013 Cost of sales $ 29,584,000 6,954,000

$ 48,069,000 $ 6,954,000

Amortization expense (5,980,000) (1,761,000) (10,477,000) (1,761,000) Transportation costs (2,885,000) (604,000) (4,386,000) (604,000) Other operating costs (30,000) (2,000) (1,197,000) (2,000) Tolling and other revenue (1,153,000) - (1,153,000) - Cash production cost $ 19,536,000 $ 4,587,000 $ 30,856,000 $ 4,587,000 Clean tons sold Metallurgical coal 263,000 73,000 401,000 73,000 Cash production cost per ton sold $ 74 $ 63 $ 77 $ 63

Corsa Coal Corp. Management’s Discussion and Analysis

For the nine months ended September 30, 2014

32

CAPP For the three months ended For the nine months ended September 30, September 30, 2014 2013 2014 2013 $ $ $ $ Cost of sales 15,943,000 17,064,000 44,727,000 53,008,000 Amortization expense (1,257,000) (1,942,000) (4,283,000) (5,531,000) Transportation costs - - - - Other operating costs (23,000) 26,000 (455,000) 26,000 Tolling and other revenue - - - - Cash production cost $ 14,663,000 $ 15,148,000 $ 39,989,000 $ 47,503,000 Clean tons sold Metallurgical coal 247,000 299,000 691,000 866,000 Cash production cost per ton sold $ 59 $ 51 $ 58 $ 55 Outstanding Share Data The following table sets forth the particulars of Corsa’s fully diluted share capital as of the date of this MD&A.

Number of Common Shares Common Shares issued and outstanding 1,190,770,362 Common Shares issuable upon exercise of stock options 52,851,667 Common Shares issuable upon redemption of redeemable units 170,316,639 Common Shares issuable upon exercise of stock purchase warrants 36,100,000 Total 1,450,038,668

Summary of Quarterly Results The following table sets out certain information derived from Corsa’s condensed interim consolidated financial statements for each of the eight most recently completed quarters. Reference is made to this MD&A under the heading “Financial Results”; Corsa’s Management’s Discussion and Analysis for the three months and six months ended June 30, 2014; Corsa’s Management’s Discussion and Analysis for the three months ended March 31, 2014; Corsa’s Management’s Discussion and Analysis for the year ended December 31, 2013; Corsa’s Management’s Discussion and Analysis for the three and nine months ended September 30, 2013 and the QKGI Management’s Discussion and Analysis for the three and six months ended June 30, 2013 and the QKGI Management’s Discussion and Analysis for the three months ended March 31, 2013, all available under Corsa’s profile at www.sedar.com for a discussion of factors that have caused variations in the information presented below over the eight most recently completed quarters.

Corsa Coal Corp. Management’s Discussion and Analysis

For the nine months ended September 30, 2014

33

Quarter ended Quarter ended Quarter ended Quarter ended September 30, June 30, March 31, December 31, 2014 2014 2014 2013 Revenues (000’s) $ 45,150 $ 24,319 $ 19,843 $ 28,855 Net (loss) income (000’s) $ (31,408) $ 692 $ (573) $ (3,196) Earnings per share - basic $ (0.00) $ 0.00 $ (0.00) $ (0.00) - diluted $ (0.00) $ 0.00 $ (0.01) $ (0.00) Quarter ended Quarter ended Quarter ended Quarter ended September 30, June 30, March 31, December 31, 2013 2013 2013 2012 Revenues (000’s) $ 30,159 $ 21,121 $ 21,221 $ 20,577 Net (loss) income (000’s) $ 52,672 $ 361 $ 809 $ (24) Earnings per share - basic $ 0.09 $ 0.00 $ 0.00 $ (0.00) - diluted $ 0.07 $ 0.00 $ 0.00 $ (0.00)

Off-Balance Sheet Arrangements Corsa does not have any off-balance sheet arrangements as of the date of this MD&A. Related party transactions Related party transactions include any transactions with employees, other than amounts earned as a result of their employment, transactions with companies that employees or directors either control or have significant influence over and transactions with companies who are under common control with Corsa’s largest shareholder, Quintana. Transactions with related parties included in the statement of operations and comprehensive income of Corsa are summarized below:

For the three months ended For the nine months ended September 30, September 30, 2014 2013 2014 2013

(000’s) (000’s) (000’s) (000’s) Royalties (i) $ 967 $ 1,235 $ 3,410 $ 3,845 Mining equipment lease (ii) 244 242 725 728 Management fee (iii) - 25 - 150 $ 1,211 $ 1, 502 $ 4,135 $ 4,723

(i) During the three and nine months ended September 30, 2014, Corsa paid royalties to related

parties who are commonly controlled by Quintana or employees of Corsa in the amount of

Corsa Coal Corp. Management’s Discussion and Analysis

For the nine months ended September 30, 2014

34

$967,000 and $3,410,000, respectively (2013 - $1,235,000 and $3,845,000) for coal extracted from mineral properties where the surface or mineral rights of the specific property are leased by Corsa and owned by the related party.

(ii) During the three and nine months ended September 30, 2014, Corsa also paid lease payments to related parties who are controlled by a director and an officer of Corsa for use of mining equipment owned by the related party amounting to $244,000 and $725,000, respectively (2013 – $242,000 and $728,000). These amounts were included in cost of sales in the condensed interim statement of operations and comprehensive income.

(iii) During the three and nine months ended September 30, 2013, Corsa paid a management fee of

$25,000 and $150,000, respectively, to an affiliated entity related through common ownership. On July 31, 2013, the agreement requiring the management fee was terminated and no fee was paid during the three and nine months ended September 30, 2014. These amounts were included in cost of sales on the condensed interim statement of operations and comprehensive income.