Hybrid Financing Advanced Corporate Finance FINC 5880- week 6.

Upload

erik-mckenzieCategory

view

225download

6

Corporations in Financial Distress

Bankruptcy, Liquidation and Reorganization

FINC 5880 MBA - week 6-7

Managing Reorganizations

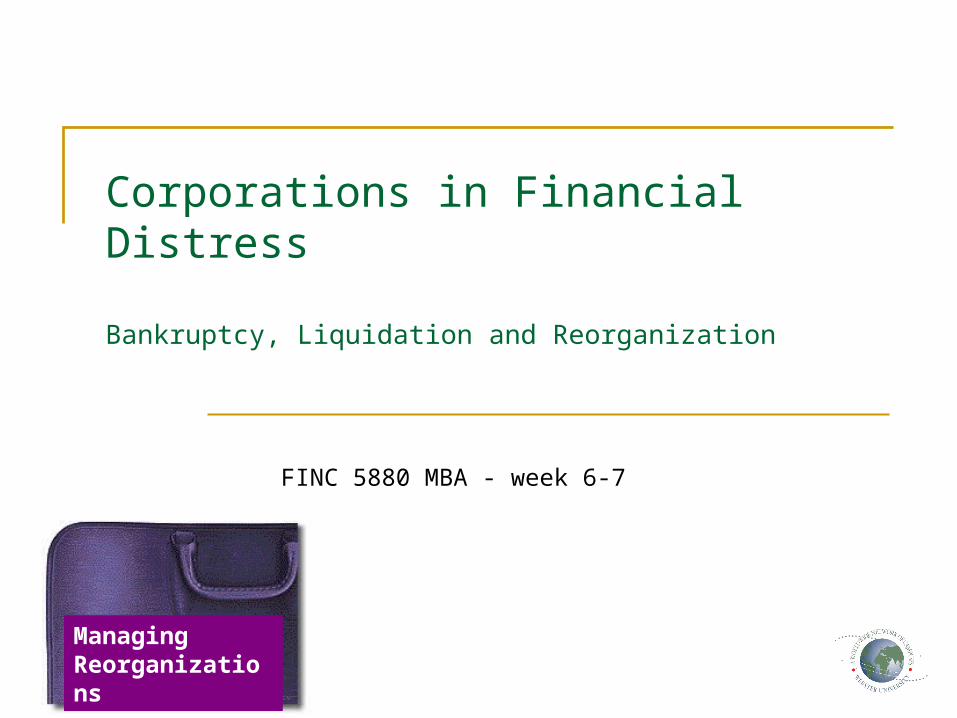

Failures that trigger reorganization Economic failure: LT

Revenue<Total Costs Business failure: terminated

businesses that still owe to creditors

Technical insolvency: the firm can not meet its current obligations

Insolvency in bankruptcy: book value of liabilities> market value of the assets

Legal bankruptcy: firm has filed for bankruptcy with the court

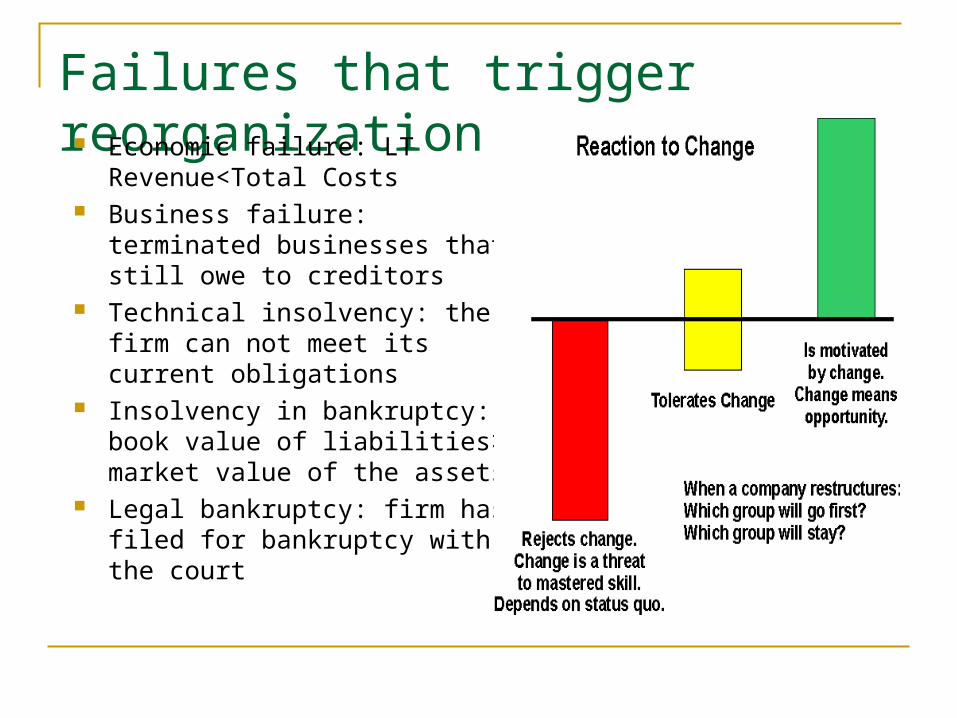

Dun&Bradstreet Inc.

There is a whole industry out there checking on companies’ credit worth…

Dun & Bradstreet NYSE: DNB is a Fortune 500 public company headquartered in Short Hills, New Jersey, USA that licenses information on businesses and corporations for use in credit decisions, B2B marketing and supply chain management. Often referred to as D&B, the company maintains information about more than 204 million companies worldwide.[1]

The largest bankruptcies

Enron Worldcom MF Global Tyco Texaco Airlines… GM Lehman Brothers MF Global Eastman Kodak

The down fall of companies often tricker the downfall of some of their customers and suppliers….

(bonus) Homework Assignment: ENRON versus GM What were the main reasons behind GM’s

filing for bankruptcy in early 2009 What were the main reasons behind

ENRON’s bankruptcy in 2001 Why are they different? What could GM have done to prevent this? What could ENRON have done?

Class Assignment: GM’s back to the future

Just before the trading of GM stocks halts in anticipation of a major announcement concerning the financial situation you walk in to the Corporate HQ to meet Rick Wagoner Chairman and CEO of GM.

On the agenda is a restructuring that should take place the following months

You are a top level consultant and you are asked to come up with a plan to be negotiated with all major stakeholders

Will you file for chapter 11 or seek for an out of court work out? What are your ideas about the reorganization ?

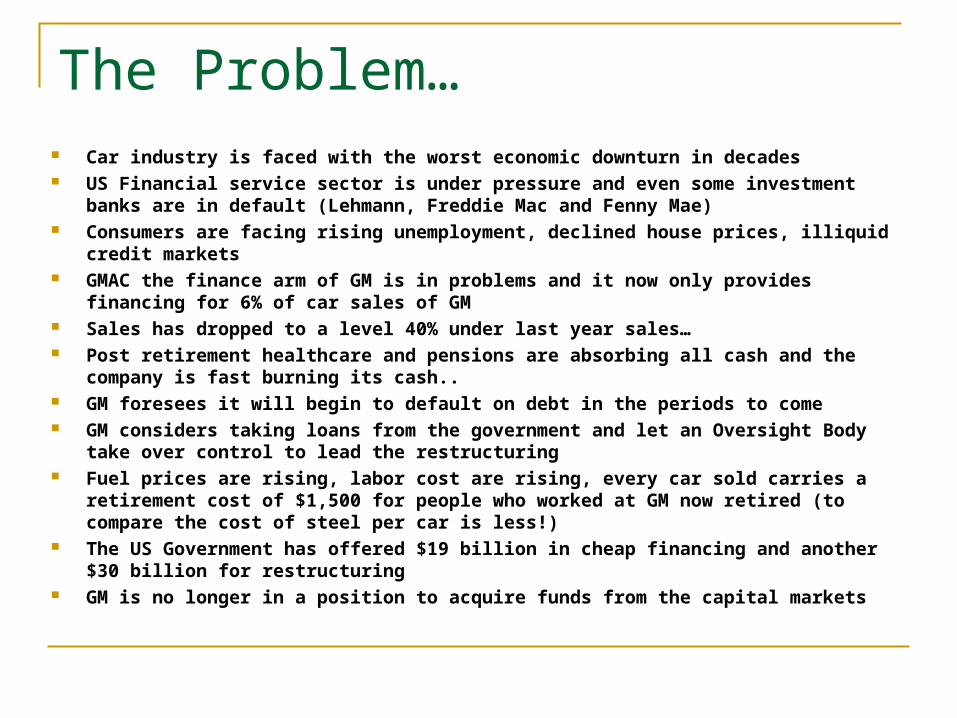

The Problem… Car industry is faced with the worst economic downturn in decades US Financial service sector is under pressure and even some investment banks are in

default (Lehmann, Freddie Mac and Fenny Mae) Consumers are facing rising unemployment, declined house prices, illiquid credit markets GMAC the finance arm of GM is in problems and it now only provides financing for 6% of

car sales of GM Sales has dropped to a level 40% under last year sales… Post retirement healthcare and pensions are absorbing all cash and the company is fast

burning its cash.. GM foresees it will begin to default on debt in the periods to come GM considers taking loans from the government and let an Oversight Body take over

control to lead the restructuring Fuel prices are rising, labor cost are rising, every car sold carries a retirement cost of

$1,500 for people who worked at GM now retired (to compare the cost of steel per car is less!)

The US Government has offered $19 billion in cheap financing and another $30 billion for restructuring

GM is no longer in a position to acquire funds from the capital markets

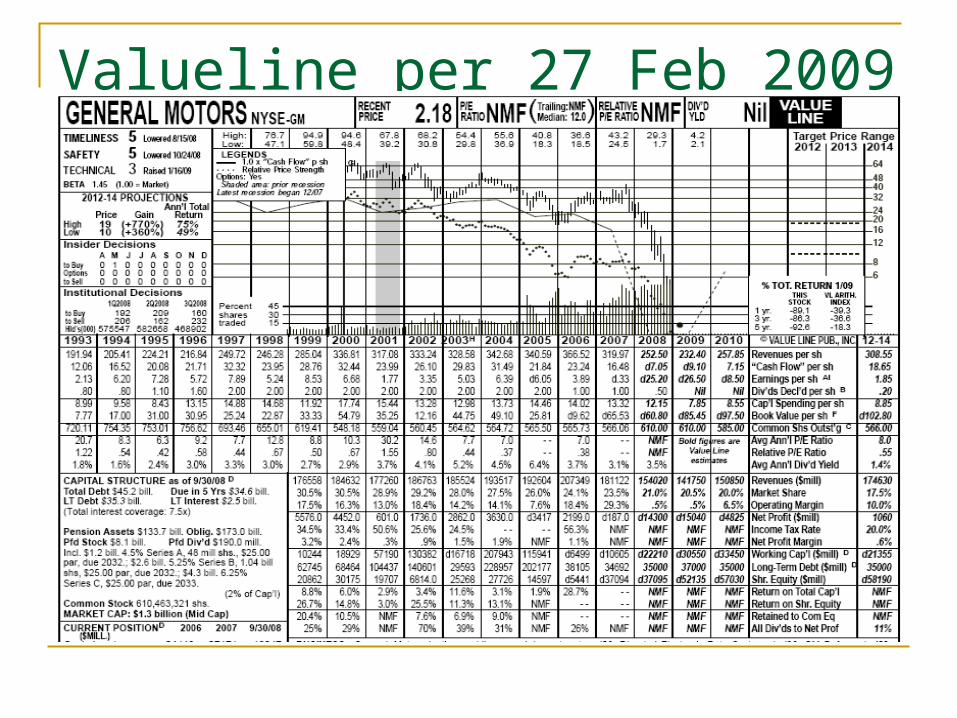

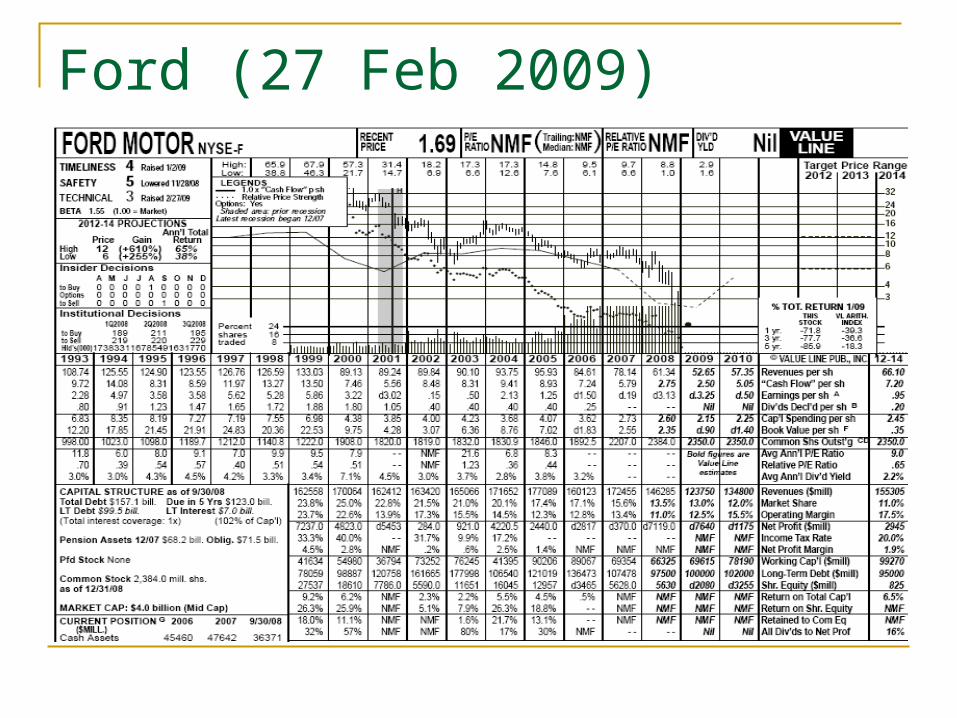

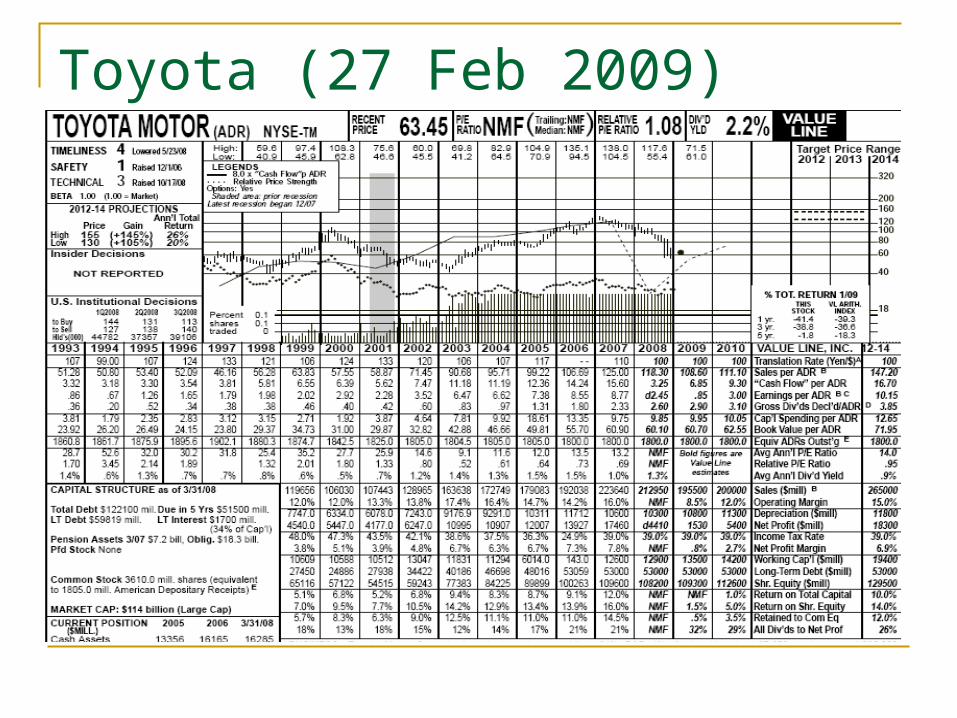

Valueline per 27 Feb 2009

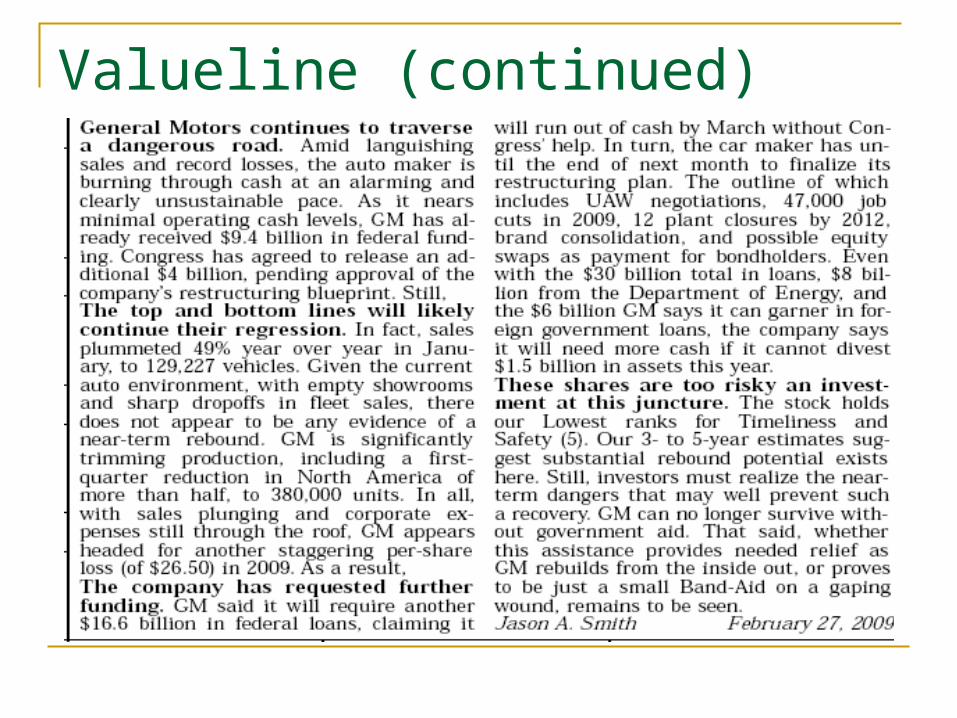

Valueline (continued)

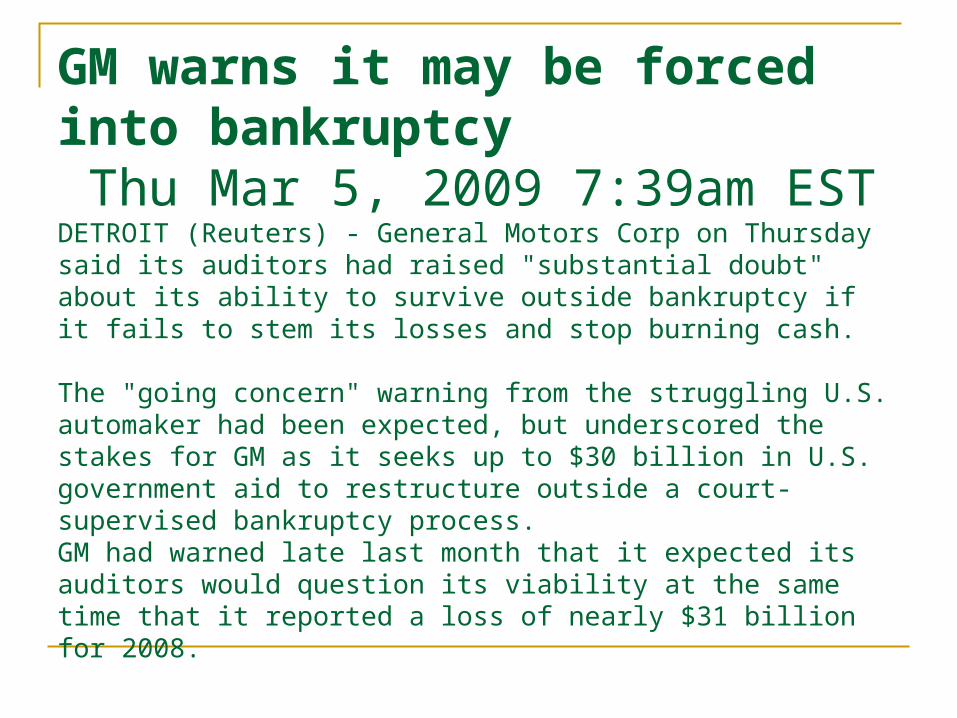

GM warns it may be forced into bankruptcy Thu Mar 5, 2009 7:39am ESTDETROIT (Reuters) - General Motors Corp on Thursday said its auditors had raised "substantial doubt" about its ability to survive outside bankruptcy if it fails to stem its losses and stop burning cash.

The "going concern" warning from the struggling U.S. automaker had been expected, but underscored the stakes for GM as it seeks up to $30 billion in U.S. government aid to restructure outside a court-supervised bankruptcy process.GM had warned late last month that it expected its auditors would question its viability at the same time that it reported a loss of nearly $31 billion for 2008.

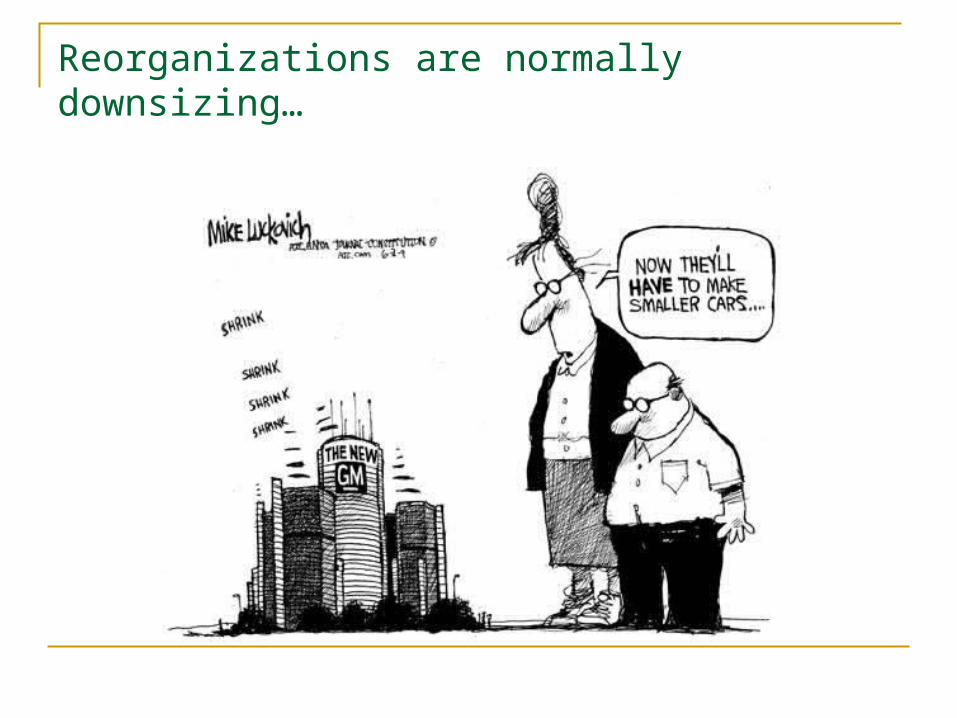

Reorganizations are normally downsizing…

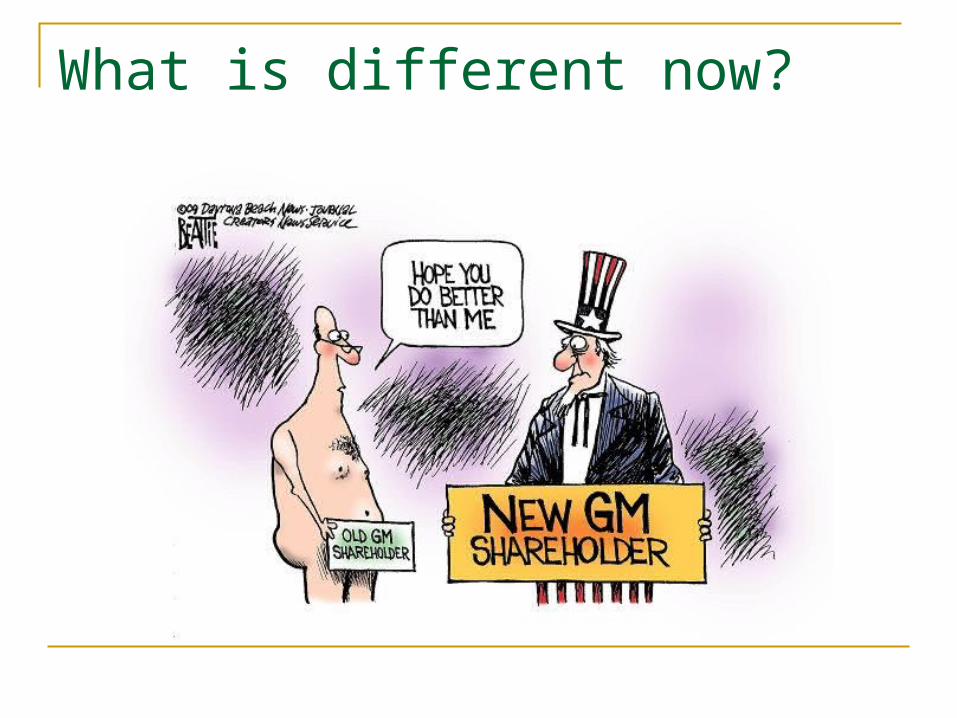

What is different now?

Ford (27 Feb 2009)

Toyota (27 Feb 2009)

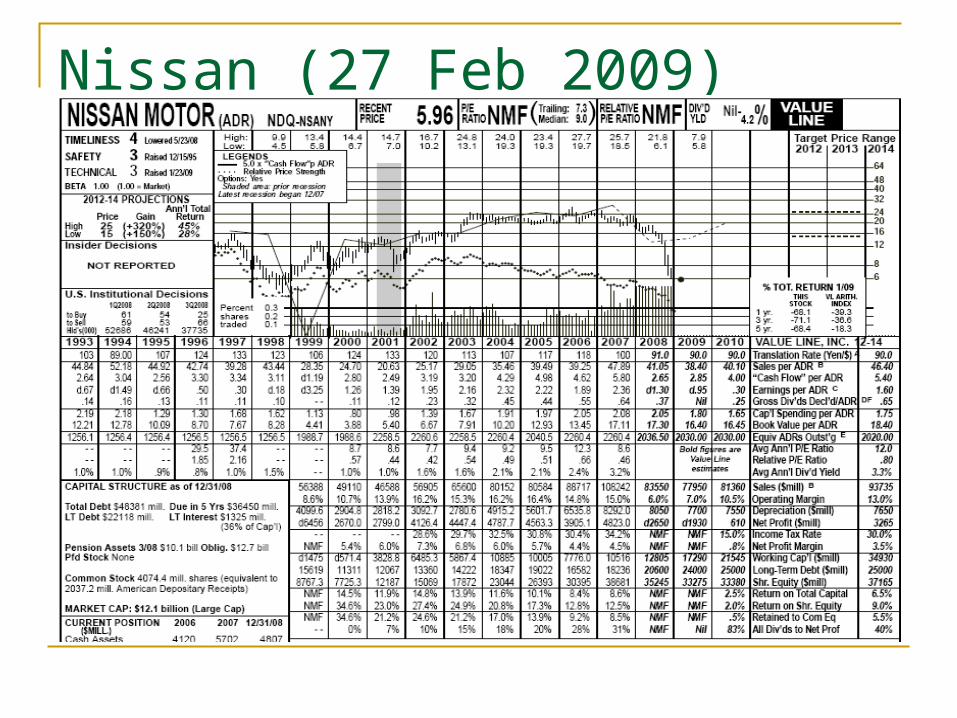

Nissan (27 Feb 2009)

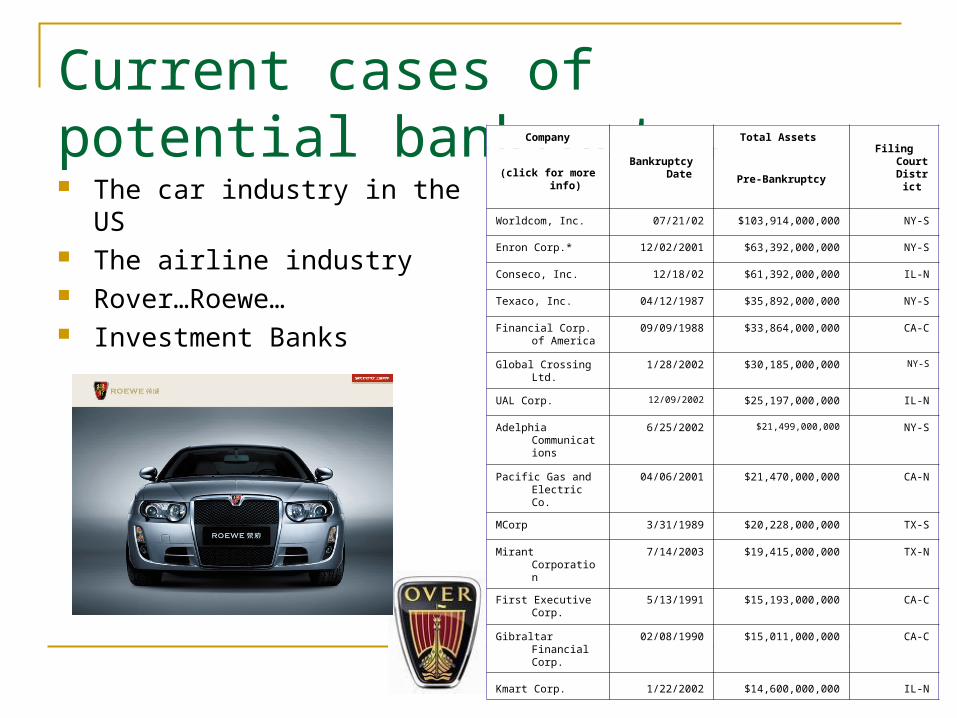

Current cases of potential bankruptcy The car industry in the US The airline industry Rover…Roewe… Investment Banks

Company

Bankruptcy Date

Total Assets Filing Court

District(click for more info) Pre-Bankruptcy

Worldcom, Inc. 07/21/02 $103,914,000,000 NY-S

Enron Corp.* 12/02/2001 $63,392,000,000 NY-S

Conseco, Inc. 12/18/02 $61,392,000,000 IL-N

Texaco, Inc. 04/12/1987 $35,892,000,000 NY-S

Financial Corp. of America

09/09/1988 $33,864,000,000 CA-C

Global Crossing Ltd. 1/28/2002 $30,185,000,000 NY-S

UAL Corp. 12/09/2002 $25,197,000,000 IL-N

Adelphia Communications

6/25/2002 $21,499,000,000 NY-S

Pacific Gas and Electric Co.

04/06/2001 $21,470,000,000 CA-N

MCorp 3/31/1989 $20,228,000,000 TX-S

Mirant Corporation 7/14/2003 $19,415,000,000 TX-N

First Executive Corp. 5/13/1991 $15,193,000,000 CA-C

Gibraltar Financial Corp.

02/08/1990 $15,011,000,000 CA-C

Kmart Corp. 1/22/2002 $14,600,000,000 IL-N

Who is next ?

GM (as forecasted) Ford (not yet) Daimler Chrysler (as forecasted) North West Airlines (as forecasted) Altria (not yet) Eastman Kodak (as forecasted) Your company?

The firm in distress; first signs

The firm can not meet its scheduled payments due to cash flow problems

The firm starts to wonder if this is temporary or a more structural issue

The firm starts to think if its worth more dead or alive

The firm considers filing under chapter 11 protection against creditors who will chase the firm’s assets

The firm starts to think of the new management that should take care of the turnaround…

Informal reorganization

Creditors work with the firm to find a solution for its problems

These problems are temporarily The debtor is perceived as a good

moral risk The debtor must present a

reasonable plan to solve its problems

General business conditions must be favourable for recovery

Informal liquidation The firm is seen to be of more

value if it liquidates The firm may still agree to partly

repay its creditors Since this is not a formal

procedure a lot of costs and interests are saved…to benefit the remaining creditors

The debtors assets are assigned to a trustee who sells the assets in a private sale or public auction

The proceeds are distributed among the creditors

Federal Laws on bankruptcy

Chapters 1,3,5,7,9, and 11 US Bankruptcy Laws

Chapters 1,3,5: general provisions Chapter 7: procedures of liquidation Chapter 9: financially distressed public

bodies Chapter 11: protection under law avoiding

creditors to chase assets of the firm

Filing under chapter 11

The company seeks protection against creditors

The company works on a reorganization plan or regulation for creditors

The company has the flexibility to negotiate with its creditors and stockholders

Reorganization Bankruptcy

Informal procedures are less costly and offer most chances of quick solutions

Two problems arise: 1) common pool problem: if a creditor

waits for the other creditors the firm has to share between the creditors if the firm forecloses on the debtor it can get priority and hold the chance of getting all what is owed back!

2) hold out problem: only if all creditors agree on getting less then what is owed they will agree not if some will hold 100% right to their credits…

Further provisions of chapter 11 Interest and principal on

delayed payments may be delayed without penalty

The firm can issue Debtor In Possession financing (DIP) this is borrowing for short term liquidity purposes

The firms managers get 120 days after filing to come up with a reorganization plan plus another 60 days to obtain agreement (the court may extend these dates)

Sharing the pie with creditors…

Absolute priority doctrine: Creditors should be compensated for their

claims in a rigid hierarchical order; Senior claims must be paid in full junior

claims may not receive a single dime

Is the reorganization viable

Future sales to be estimated Operating conditions to be

analyzed Future earnings and cash flows

to be analyzed Company value to be estimated Capital structure after chapter

11 period to be determined Firm’s securities should be

allocated to the various claimants in a fair manner

Measures taken

Debt maturity is lengthened New management team in

control Obsolete inventories to be

replaced Modernized production

equipment to improve competing strength

Stronger operations and marketing approach…

Develop and enter new markets and products…

Pre-packaged bankruptcy

Hybrid form of bankruptcy between formal and informal workout

Informal: debtor negotiates restructuring with its creditors

Formal; restructuring under chapter 11

Prepack: debtor gets creditors to agree to the reorganization plan prior to the filing for bankruptcy

Time and expense

Typical bankruptcy case takes 2 years under chapter 11 until final plan is approved by all creditors

In the meanwhile sales suffers Good employees leave the company In the meanwhile all other employees

worry about their jobs rather then work Good bankruptcy lawyers charge 650

USD+ per hour; all other costs of creditors will be imposed on the firm as well…

At some point parties may just want to settle some deal…to stop the bleeding.

Liquidation in bankruptcy

The company is worth more dead then alive: chapter 7 explains how to share the assets over the creditors:

Secured creditors (pledged/ collateral) Legal fees Expenses incurred before trustee is appointed Wages to workers up to 3 months prior to the filing Payments for contributions to pension plans Claims for customer deposits (max $900 pp.) Taxes (federal, state ) General creditors Preferred stockholders Common stockholders

Predicting the likelihood of bankruptcy

Multiple Discriminant Analysis (MDA) Discriminant function is described as:

Z= a+b1(current ratio)+b2(debt ratio)

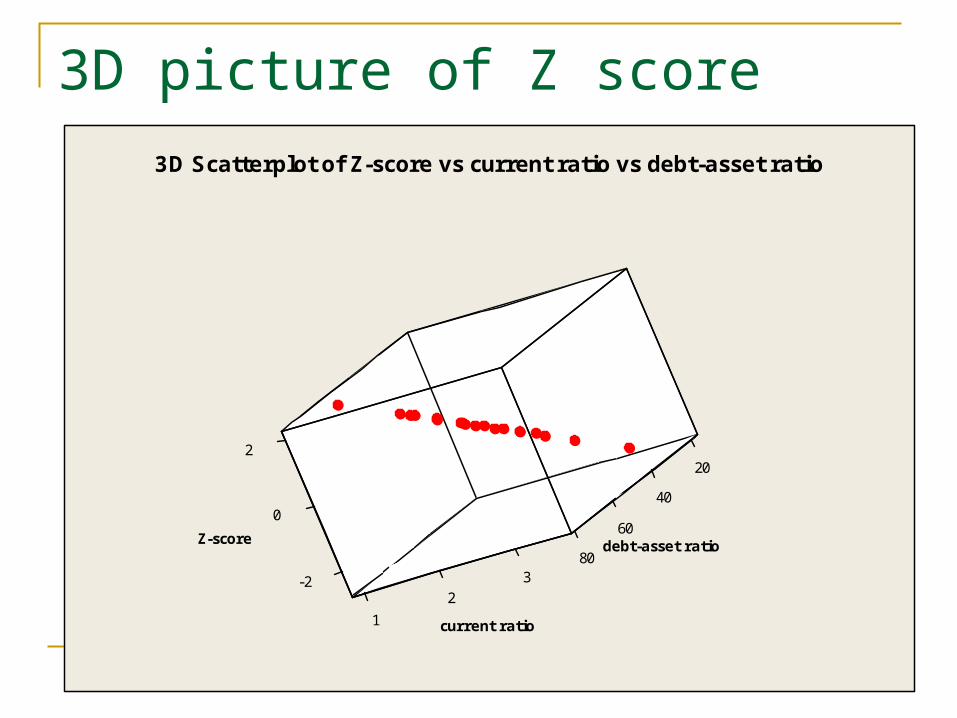

Z=z score; multiple regression based on data of the book gives; Z= -0.3877-1.0736(current ratio)+.0579(debt ratio)

Discriminant analysis defines a boundary between current ratio and debt ratio defining high and low probabilities of bankruptcy

The lower the Z score the less likely bankruptcy Financial Institutions use their own criteria for

the value of Z

3D picture of Z score

20

Z-score

-2

0

1

40

2

debt-asset ratio

2

current ratio

60

380

3D Scatterplot of Z-score vs current ratio vs debt-asset ratio

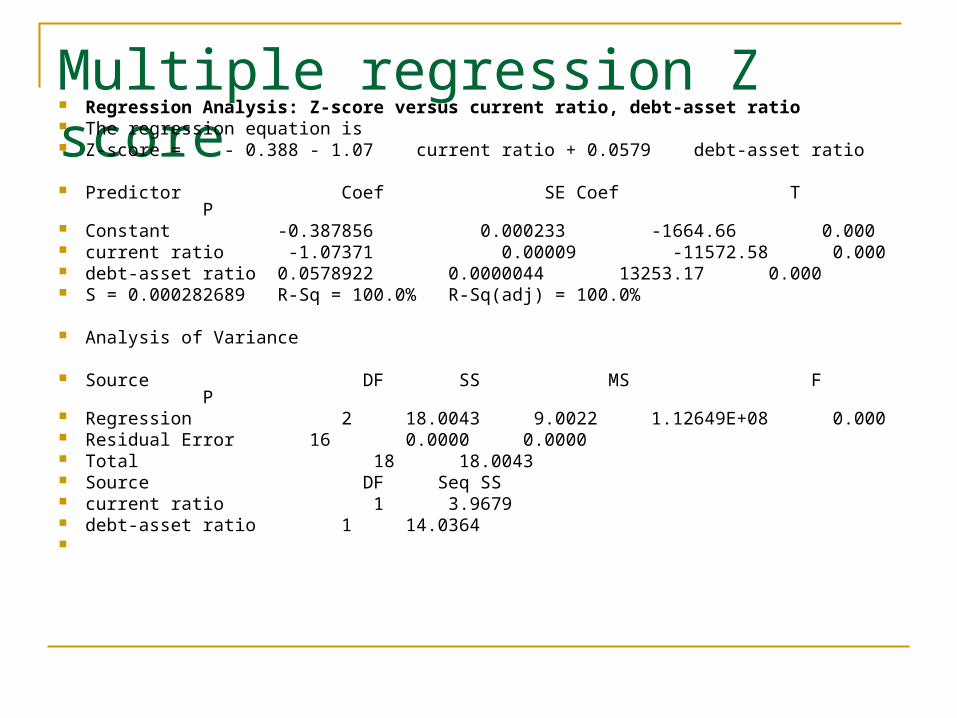

Multiple regression Z score Regression Analysis: Z-score versus current ratio, debt-asset ratio The regression equation is Z-score = - 0.388 - 1.07 current ratio + 0.0579 debt-asset ratio

Predictor Coef SE Coef T P Constant -0.387856 0.000233 -1664.66 0.000 current ratio -1.07371 0.00009 -11572.58 0.000 debt-asset ratio 0.0578922 0.0000044 13253.17 0.000 S = 0.000282689 R-Sq = 100.0% R-Sq(adj) = 100.0%

Analysis of Variance

Source DF SS MS F P Regression 2 18.0043 9.0022 1.12649E+08 0.000 Residual Error 16 0.0000 0.0000 Total 18 18.0043 Source DF Seq SS current ratio 1 3.9679 debt-asset ratio 1 14.0364

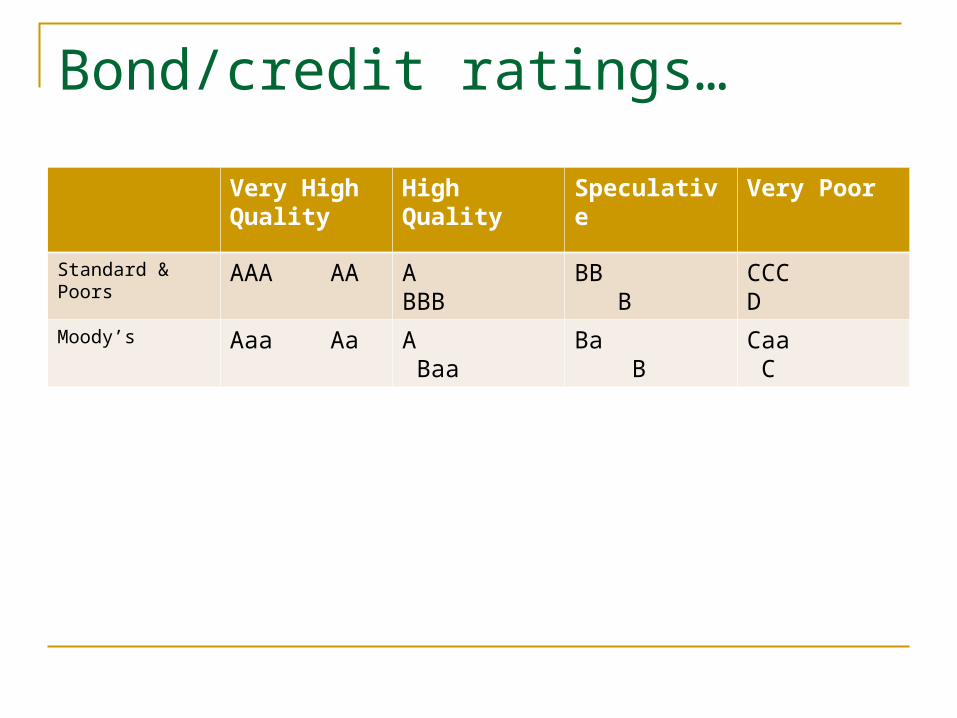

Bond/credit ratings…

Very High Quality

High Quality Speculative Very Poor

Standard & Poors AAA AA A BBB BB B CCC D

Moody’s Aaa Aa A Baa Ba B Caa C

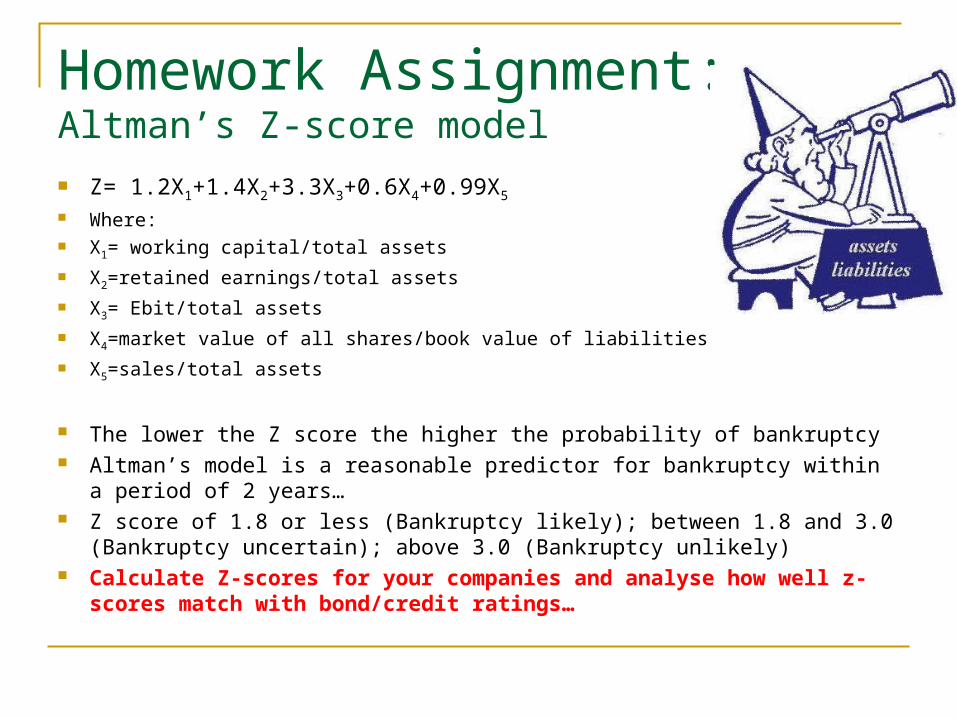

Homework Assignment:Altman’s Z-score model

Z= 1.2X1+1.4X2+3.3X3+0.6X4+0.99X5

Where: X1= working capital/total assets

X2=retained earnings/total assets

X3= Ebit/total assets

X4=market value of all shares/book value of liabilities

X5=sales/total assets

The lower the Z score the higher the probability of bankruptcy Altman’s model is a reasonable predictor for bankruptcy within a period of 2

years… Z score of 1.8 or less (Bankruptcy likely); between 1.8 and 3.0 (Bankruptcy

uncertain); above 3.0 (Bankruptcy unlikely) Calculate Z-scores for your companies and analyse how well z-scores

match with bond/credit ratings…

When using MDA

Collect your own data from the industry in question

Run your model/use Altman’s predictors Test for significance and fit Define critical zone… Predict future for case on hand…

(bonus) Assignment: Z-score and Altman’s MDA

Calculate the Z-score for your company

Calculate Altman’s MDA Calculate similar scores for

the main competitors

Based on your findings which competitor is relatively most likely to go bankrupt earlier than the others…