Corporate Taxes - An Overview 5 th MSOP :ICSI-Hyderabad Chapter Ankem Sri Prasad Chief Tax Officer -...

55

Corporate Taxes - An Overview 5 th MSOP :ICSI-Hyderabad Chapter Ankem Sri Prasad Chief Tax Officer - Deloitte U.S. India Offices March 26, 2012

-

Upload

dana-templeman -

Category

Documents

-

view

214 -

download

0

Transcript of Corporate Taxes - An Overview 5 th MSOP :ICSI-Hyderabad Chapter Ankem Sri Prasad Chief Tax Officer -...

Corporate Taxes - An Overview

5th MSOP :ICSI-Hyderabad Chapter

Ankem Sri PrasadChief Tax Officer - Deloitte U.S. India Offices

March 26, 2012

Copyright © 2012 Deloitte Development LLC. All rights reserved.2

The best things in life are free, but soon,

the government will find a way to tax them.

Copyright © 2011 Deloitte Development LLC. All rights reserved.3

Index

I. Corporate Taxes

Introduction – Some Facts, Business & Taxes, Your role with Taxes 4 - 7

A. Overview of taxes – Compliance Management 8

B. Direct Taxes 9 - 15

C. Individual Taxation 16 - 18

D. International Taxation – Evolution, Objective, Treaty & Transfer pricing 19 - 43

E. In-Direct Taxation 44 - 49

II. Practical Challenges

A. Practical challenges and mitigating strategies50 - 54

A. Introduction

Copyright © 2012 Deloitte Development LLC. All rights reserved.5

Introduction – Some facts

In Rs. Lakh Crores Actual 2010-11

Rev Estimate 2011-12

Budget 2012-13

Revenue

Net Tax 5.74 6.46 7.76

Non Tax 3.59 2.77 3.35

Capital, Public Debt, Loans/Advances recovery, Misc cap receipts 32.29 41.14 43.98

Total Consolidated Revenue 41.62 50.37 55.09

Expenditure

General, Social, Economic Services, Grants & Payments to Union Territories

11.86 13.18 14.62

Capital Expense – Gen, Social & Eco Services 1.40 1.36 2.25

Government Public Debt, Loans/Advances 32.29 41.14 43.98

Total Consolidated Disbursements 44.15 54.32 58.59

DEFICIT 2.53 3.95 3.50

Copyright © 2012 Deloitte Development LLC. All rights reserved.6

Business and Taxes - Nexus

Business

Competition

Cost Management

Cash flow

Management

Tax

SavingsTax planning/ Management

Decision

making

Profits

Affect

Copyright © 2012 Deloitte Development LLC. All rights reserved.7

Where you play a role

YOUR ROLE

Tax Planning /

Structuring / Due

Diligence

Share Capital Issue

Dividend Taxation

Capital GainsMergers &

Acquisitions

Contracts / Agreements

Investments

Expatriate Transactions

Copyright © 2012 Deloitte Development LLC. All rights reserved.8

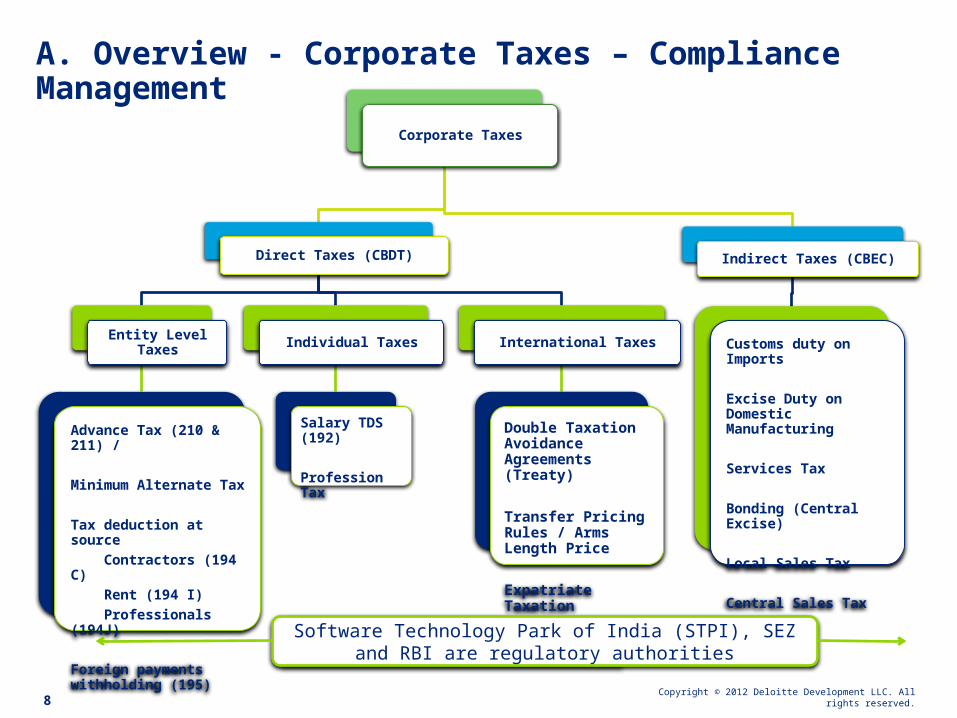

A. Overview - Corporate Taxes – Compliance Management

Corporate Taxes

Direct Taxes (CBDT)

Entity Level Taxes

Advance Tax (210 & 211) /

Minimum Alternate Tax

Tax deduction at source

Contractors (194 C)

Rent (194 I)

Professionals (194J)

Foreign payments withholding (195)

Individual Taxes

Salary TDS (192)

Profession Tax

International Taxes

Double Taxation Avoidance Agreements (Treaty)

Transfer Pricing Rules / Arms Length Price

Expatriate Taxation

Indirect Taxes (CBEC)

Customs duty on Imports

Excise Duty on Domestic Manufacturing

Services Tax

Bonding (Central Excise)

Local Sales Tax

Central Sales Tax

Software Technology Park of India (STPI), SEZ and RBI are regulatory authorities

B. Direct Taxes

Copyright © 2012 Deloitte Development LLC. All rights reserved.10

B. Direct Taxes – Entity Level Taxes (Advance Tax)

Advance Tax (Sec 210)

• Payment of advance tax by the assessee of his own accord or in pursuance of order of Assessing Officer.

• 210. (1) Every person who is liable to pay advance tax under section 208 (whether or not he has been previously assessed by way of regular assessment) shall, of his own accord, pay, on or before each of the due dates specified in section 211, the appropriate percentage, specified in that section, of the advance tax on his current income, calculated in the manner laid down in section 209.

• …

Advance Tax (Sec

211)

• Installments of advance tax and due dates• 211. 95[(1) Advance tax on the current income calculated in the manner laid down in

section 209 shall be payable by (a) all the companies…

Amount of Tax Payable Due date of installment

Not < 15% of advance tax. On or before the 15th Jun

Not < 45% of advance tax, less paid earlier. On or before the 15th Sept

Not < 75% of advance tax, less paid earlier. On or before the 15th Dec

100% of advance tax, less paid earlier. On or before the 15th Mar

Copyright © 2012 Deloitte Development LLC. All rights reserved.11

B. Direct Taxes – Minimum Alternate Tax (MAT)

MAT

(Sec 115JB)

• Special provision for payment of tax by certain companies• 115JB. (1) Notwithstanding anything contained in any other

provision of this Act, where in the case of an assessee, being a company, the income-tax, payable on the total income as computed under this Act in respect of any previous year relevant to the assessment year commencing on or after the 1.4.2011, is less than 18% of its book profit, [such book profit shall be deemed to be the total income of the assessee and the tax payable by the assessee on such total income shall be the amount of income-tax at the rate of 18%

• ..

FY 2000-

01

FY 2001-

02

FY 2002-

03

FY 2003-

04

FY 2004-

05

FY 2005-

06

FY 2006-

07

FY 2007-

08

FY 2008-

09

FY 2009-

10

FY 2010-

11

FY 2011-

12

0.00

10.00

20.00

30.00

40.00

8.48 7.65 7.88 7.69 7.84 8.4211.22 11.33 11.33

17.0019.93 20.01

39.5535.7 36.75 35.88 36.59

33.66 33.66 33.99 33.99 33.99 33.22 32.45

MAT rate Corp. tax rate

MAT & Corporate Tax Rate - A Glance

Copyright © 2012 Deloitte Development LLC. All rights reserved.12

B. Direct Taxes – Tax Deduction at Source (TDS -194C)

TDS on Contractors

(Sec 194C)

• Payments to contractors.• 15194C. (1) Any person responsible for paying any sum to any resident

(contractor) for carrying out any work (including supply of labor for carrying out any work) in pursuance of a contract between the contractor and a specified person shall, at the time of credit of such sum to the account of the contractor or at the time of payment thereof in cash or by issue of a cheque or draft or by any other mode, whichever is earlier, deduct an amount equal to

• …

TDS on Contractors

(Sec194 C)

Payment is being made or credit is given to % of TDS

Individual or a Hindu undivided family 1%

a person other than an individual or a HUF 2%

Copyright © 2012 Deloitte Development LLC. All rights reserved.13

B. Direct Taxes – Tax Deduction at Source (TDS 194 J)

TDS on Professional or Technical Services

(Sec 194J)

• Fees for professional or technical services.• 194J. (1) Any person, not being an individual or a

Hindu undivided family, who is responsible for paying to a resident any sum by way of—• (a) fees for professional services, or• (b) fees for technical services, [or]• (c) royalty, or• (d) any sum referred to in clause (va) of

section 28,• shall, at the time of credit to the payee or at payment

thereof in cash or cheque or any other mode, whichever is earlier, deduct an amount equal to ..

• Provided …Payment is being made or credit is given to % of TDS

Individual or a Hindu undivided family 10%

Where payment for services in a tax year to such person does not exceed Rs 30,000/- no tax shall be deducted

Copyright © 2012 Deloitte Development LLC. All rights reserved.14

B. Direct Taxes – Tax Deduction at Source (TDS -194-I)

TDS on

Rent

(Sec 194-I)

• Rent• 194-I. Any person, not being an individual or a Hindu

undivided family, who is responsible for paying to [a resident] any income by way of rent, shall, at the time of credit of such income to the account of the payee or at the time of payment thereof in cash or by cheque or any other mode, whichever is earlier, [deduct income-tax thereon at the rate of—

• …

TDS on

Rent

(Sec194-

I)

Payment is being made or credit is given % of TDS

for use of any machinery or plant or equipment 2 %

for use of any land / building (including factory building) / land appurtenant to a building (including factory building)/ furniture or fittings

10%

Where payment for rent in a tax year to such person does not exceed Rs 180,000/- no tax shall be deducted

Copyright © 2012 Deloitte Development LLC. All rights reserved.15

B. Direct Taxes – Tax Deduction at Source (TDS -195)

TDS on Foreign

payment

(Sec 195)

• Other sums.• 195. (1) Any person responsible for paying to a non-resident, not

being a company, or to a foreign company, any interest / any other sum chargeable under the Income Tax Act (not being income chargeable under “Salaries” ) shall, at the time of credit or payment of such income in cash or cheque or any other mode, whichever is earlier, deduct income-tax thereon at the rates in force :

• Provided…

TDS on Foreign payme

nt

(Sec 195)

Payment is being made to a foreign recipient % of TDS

Where the Foreign Party does not have a PAN 20 %

Where the Foreign Party does not have a PAN 10%

Where such Income / such payment is not taxable in India, no tax shall be deducted, however it has to be certified by a qualified chartered accountant in prescribed format

C. Individuals Taxes

Copyright © 2012 Deloitte Development LLC. All rights reserved.17

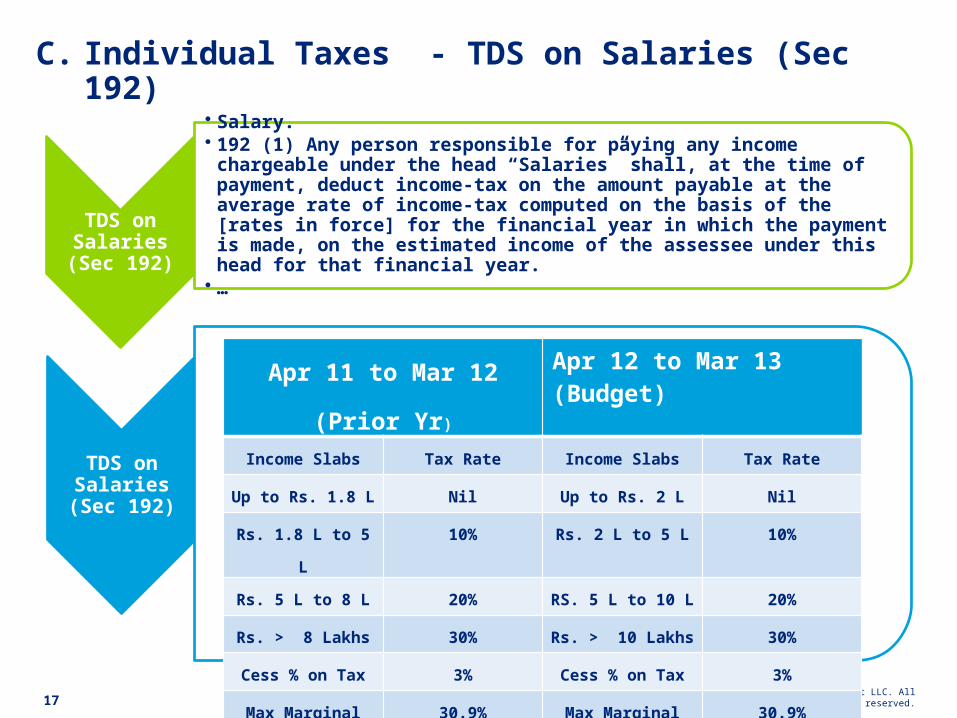

C. Individual Taxes - TDS on Salaries (Sec 192)

TDS on

Salaries

(Sec 192)

• Salary.• 192 (1) Any person responsible for paying any income chargeable under the

head “Salaries” shall, at the time of payment, deduct income-tax on the amount payable at the average rate of income-tax computed on the basis of the [rates in force] for the financial year in which the payment is made, on the estimated income of the assessee under this head for that financial year.

• …

TDS on Salaries

(Sec 192)

Apr 11 to Mar 12 (Prior Yr) Apr 12 to Mar 13 (Budget)

Income Slabs Tax Rate Income Slabs Tax Rate

Up to Rs. 1.8 L Nil Up to Rs. 2 L Nil

Rs. 1.8 L to 5 L 10% Rs. 2 L to 5 L 10%

Rs. 5 L to 8 L 20% RS. 5 L to 10 L 20%

Rs. > 8 Lakhs 30% Rs. > 10 Lakhs 30%

Cess % on Tax 3% Cess % on Tax 3%

Max Marginal Rate 30.9% Max Marginal Rate 30.9%

Copyright © 2012 Deloitte Development LLC. All rights reserved.18

C. Individual Taxes - Professional Taxes

Professional Tax

• ANDHRA PRADESH - TAX ON PROFESSIONS, TRADES, CALLINGS AND EMPLOYMENTS ACT, 1987

• The AP State Legislature empowered the local authorities to levy tax on professions, trades, callings and employments by incorporating that power in the statutes relating to local authorities i.e. the Municipal Corporations, the Municipalities and the Gram Panchayats. Thus, the levy and collection of the tax was administered by the local authorities

• Website: apvat.in

Professional Tax)

Professional Tax Slabs in AP, Maharastra & KarnatakaGross Income Rs AP Tax in Rs Maharashtra Tax in Rs. Karnataka Tax in

Rs.

Up to 5 K Nil Nil

Nil5K to 6K 60175

6K to 10K 80

10K to 15K 100

200

* 300 for February

150

15K to 20K 150200

>20K 200

D. International Taxation

Copyright © 2012 Deloitte Development LLC. All rights reserved.20

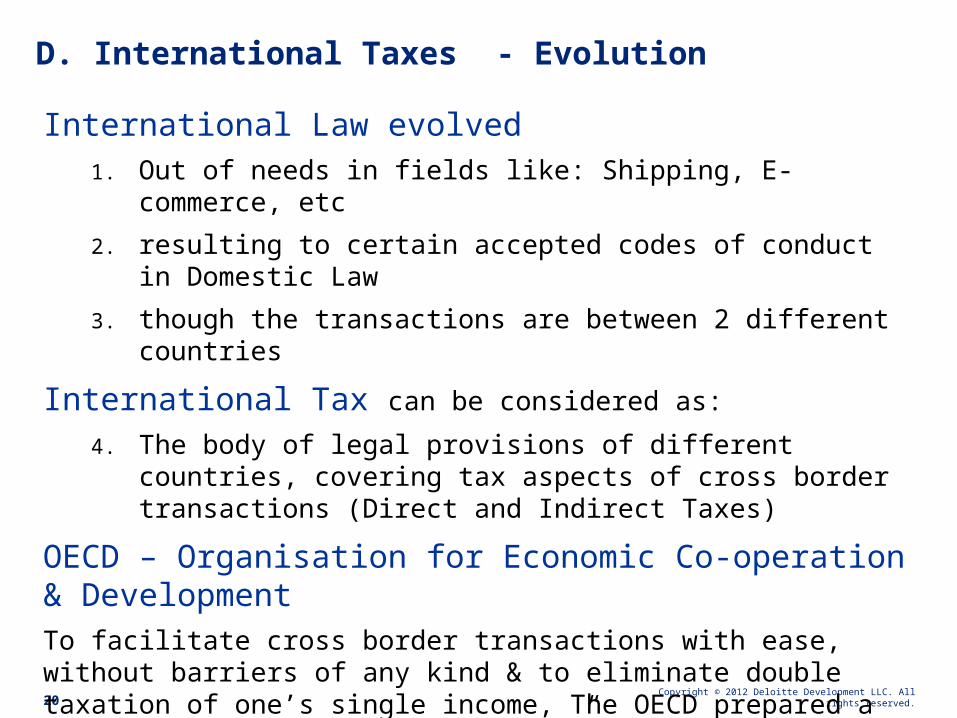

D. International Taxes - Evolution

International Law evolved1. Out of needs in fields like: Shipping, E-commerce, etc

2. resulting to certain accepted codes of conduct in Domestic Law

3. though the transactions are between 2 different countries

International Tax can be considered as:

4. The body of legal provisions of different countries, covering tax aspects of cross border transactions (Direct and Indirect Taxes)

OECD – Organisation for Economic Co-operation & Development To facilitate cross border transactions with ease, without barriers of any kind & to eliminate double taxation of one’s single income, The OECD prepared a draft called as “Model Convention” in 1977.

Copyright © 2012 Deloitte Development LLC. All rights reserved.21

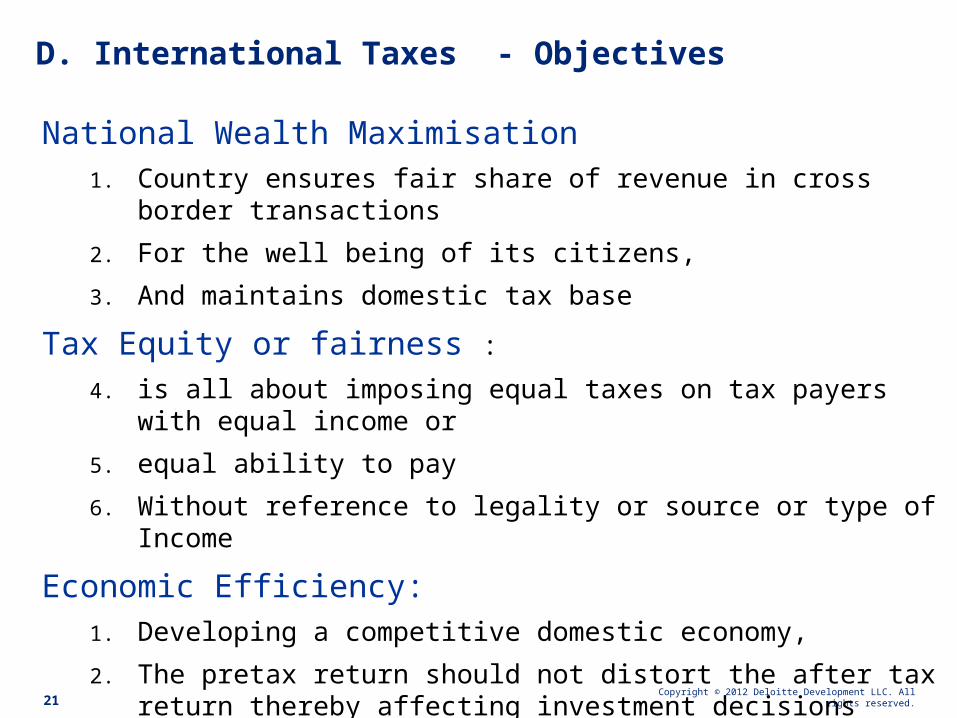

D. International Taxes - Objectives

National Wealth Maximisation1. Country ensures fair share of revenue in cross border transactions

2. For the well being of its citizens,

3. And maintains domestic tax base

Tax Equity or fairness :4. is all about imposing equal taxes on tax payers with equal income

or

5. equal ability to pay

6. Without reference to legality or source or type of Income

Economic Efficiency:1. Developing a competitive domestic economy,

2. The pretax return should not distort the after tax return thereby affecting investment decisions

Copyright © 2012 Deloitte Development LLC. All rights reserved.22

D. International Taxes - Treaty Aspects

Treaty :

is a formally concluded and ratified agreement between independent nations.

Tax Treaties between nations:

1. Is generally a matter of bargain between 2 countries,

2. Keeping in view the economic interests of the countries involved

How Treaty becomes a Law?

1. Only when it has the sanction of the constitution of the participating nations.

2. Part IV of Indian Constitution setting out the “Directive Principles of State Policy”

includes specific provision, covering International Law and treaty obligations in Article 51.

Copyright © 2012 Deloitte Development LLC. All rights reserved.23

D. International Taxes - Double Taxation

Double Taxation : It is possible that Tax payers engaged in cross

border transactions are taxed more than one (twice) on the same amount

of Income, this phenomenon is known as Double Taxation.

This led to 2 fundamental methods of Taxation under International Law:

1. Source based taxation

2. Residence based taxation

Copyright © 2012 Deloitte Development LLC. All rights reserved.24

D. International Taxes - Concept of Nexus

Connecting Factors: Income Connecting Factors:

Foreign sourced Income earned by Non residents is not taxable in India – As there is no nexus with India

Subject Connecting Factor

1. Assessee Residential Status

2. Income Source

Assessee Taxable

Indian Resident (R) World Income

Non residents /NOR’s

Only Income sourced in India is Taxable

Income Taxable

Indian sourced Income (irrespective of Assessee status)

in India

Foreign Sourced Income

Only if earned by an Indian resident

Copyright © 2012 Deloitte Development LLC. All rights reserved.25

D. International Taxes - Nexus with Income Tax Act *

Section 4 – Charging section Sec 4 (1)

Income Tax shall be charged, at that rate or those rates, for that year, in accordance with the provisions of this act, In respect of the Total Income, of the previous year, of every person

Sec 4 (2) In respect of income chargeable under clause (1), Income Tax shall be deducted at source or paid in advance, Where it is so deductible under the Act.

Copyright © 2012 Deloitte Development LLC. All rights reserved.26

D. International Taxes - Nexus with Income Tax Act ***Sec 5 (1) The Total income of any previous year, of a Sub sec (1) Resident person ; Sub sec (2) Non Resident person Includes all incomes from whatever source is derived

a) Is received or deemed to be received in India in such year,

b) Accrues or arises or is deemed to accrue or arise in India during such year,

c) Accrues or arises to him outside India during such year (For Resident Only)

Provided that, in case of a person NOR in India, under Sec 6 (6), income accruing or arising to him outside India shall not be included unless it is derived from a Business controlled or profession set up in India.

Explanation 1. Income shall not be deemed to be received by reason of the fact that it is taken into account in the Balance sheet prepared in India.

Explanation 2. Income which has been included in the total income on the basis that it is deemed to have accrued or arisen to him shall not again be so included on the basis that it is received or deemed to be received by him in India.

Copyright © 2012 Deloitte Development LLC. All rights reserved.27

D. International Taxes - Income deemed to Accrue/Arise*

Sec 9 (1) The following Income shall be deemed to accrue or arise in India

Sec 9 (I) (i) Income accruing or arising thru

From a business connection in India,

Income from any property in India,

Income from any asset or any source in India ,

Transfer of capital asset situated in India

Sec 9 (I) (ii) Income under head Salaries earned in India

Sec 9 (I) (iii) Income under head Salaries paid by Govt. of India to a citizen outside

India

Sec 9 (I) (iv) Dividends by Indian company outside India

Sec 9 (I) (v) Income by way of Interest

Sec 9 (I) (vi) Income by way of Royalty

Sec 9 (I) (vii) Income by way of Fees for technical Services

Copyright © 2012 Deloitte Development LLC. All rights reserved.28

D. International Taxes - Business Connection

Sec 9 (1) Explanation 2. It is declared that “business connection” shall include any business activity carried out thru a person acting on behalf of a NR

a) ..Trader of goods b) ..Stockist c) authorized representative

Provided that such “business connection” shall not include any business with

Dependant agentIndependent agent acting in the ordinary course of his business

Sec 9 (1) Explanation 3. Attribution Rule (only so much of income attributable to operations carried out in India shall be deemed to accrue or arise in India).

Business connection Requires continuity of action between a R in India and a NR who receives

profit , Transaction must be of a commercial nature intimately linked with the

business of a NR, contributing to an NR’s Profit Isolated transactions between a R and NR will not constitute a business

connection.

Copyright © 2012 Deloitte Development LLC. All rights reserved.29

D. International Taxes - Model Treaty

Article 1 – Persons Covered :

Article 2 – Taxes Covered

Article 3 – General Definitions : Person, Company, Enterprise of a contracting state, International Traffic, Competent Authority, National

Article 4 – Resident

Article 5 – Permanent Establishment

1. Basic rule PE – Criteria is : “Fixed place of Business”

2. Construction PE - Criteria is : “Time and activities carried on”

3. Agency PE - Criteria is : “legal and economic dependence”

4. Service PE – Most India treaties have this clause

Article 6 – Income from Immovable property

Article 7 – Business Profits

Article 8 – Shipping, Inland waterways, Transport and Air Transport

Article 9 – Associated Enterprises

-

Copyright © 2012 Deloitte Development LLC. All rights reserved.30

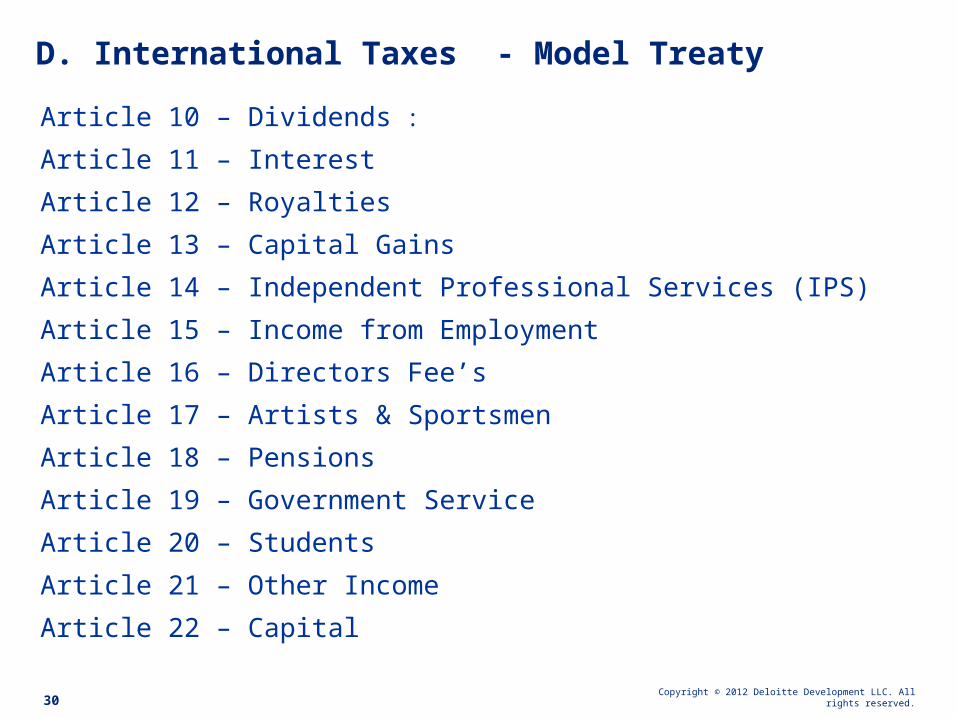

D. International Taxes - Model Treaty

Article 10 – Dividends :

Article 11 – Interest

Article 12 – Royalties

Article 13 – Capital Gains

Article 14 – Independent Professional Services (IPS)

Article 15 – Income from Employment

Article 16 – Directors Fee’s

Article 17 – Artists & Sportsmen

Article 18 – Pensions

Article 19 – Government Service

Article 20 – Students

Article 21 – Other Income

Article 22 – Capital

Copyright © 2012 Deloitte Development LLC. All rights reserved.31

D. International Taxes - Model Treaty

Article 23 – Methods for elimination of Double Taxation:

Article 24 – Non Discrimination

Article 25 – Mutual Agreement Procedure

Article 26 – Exchange of Information

Article 27 – Assistance in collection of Taxes

Article 28 – Members of Diplomatic Mission

Article 29 – Territorial Extension

Article 30 – Entry into force

Article 31 – Termination

Copyright © 2012 Deloitte Development LLC. All rights reserved.32

D. International Taxes - Article 4 (Tie Breaker Test)

Resident

Individual Corporate

Art 4 (1) & (2)

Domicile, Residence,Place of management

Resident in both states

Permanent home in both states

b) State in which individual has a Centre of Vital

InterestNo

Centre of vital interest in both

states

c) State in which individual is a nationalNo

National in both states

Competent Authorities of the contracting states will

settle.No

a) State in which individual has a Permanent HomeNo Corporate Resident in

both states

Corporate is resident of State in which it is registeredNo

Corporate is the resident of that state in which it has its place of

effective management

No

Copyright © 2012 Deloitte Development LLC. All rights reserved.33

D. International Taxes - Transfer Pricing

Basics:

• Transfer Pricing is the process of setting prices for intra-group transactions

• All stakeholders of a business may question intra-group / inter-unit prices

• Commonly questioned by Government as a stakeholder and therefore need for specific legislation

• OECD recommends the Arm's length principle for setting Transfer Prices

Copyright © 2012 Deloitte Development LLC. All rights reserved.34

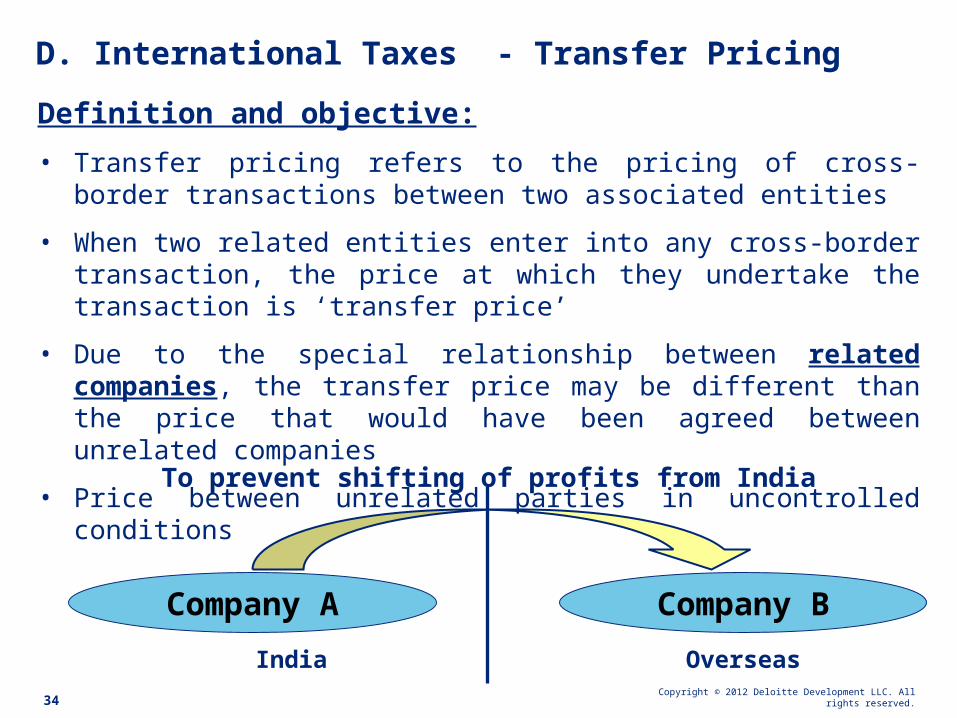

D. International Taxes - Transfer Pricing

Definition and objective:

• Transfer pricing refers to the pricing of cross-border transactions between two associated entities

• When two related entities enter into any cross-border transaction, the price at which they undertake the transaction is ‘transfer price’

• Due to the special relationship between related companies, the transfer price may be different than the price that would have been agreed between unrelated companies

• Price between unrelated parties in uncontrolled conditions is known as the “arm’s length” price (ALP)

Company A Company B

India Overseas

To prevent shifting of profits from India

Copyright © 2012 Deloitte Development LLC. All rights reserved.35

D. International Taxes - Transfer Pricing in India

International Transactions

between

Associated Enterprises

at

Arms Length Price

supported by

Extensive contemporaneous documentation

Copyright © 2012 Deloitte Development LLC. All rights reserved.36

D. International Taxes - Transfer Pricing in India

International Transaction:

• Between non-resident and non-resident

• Between non-resident and resident

• Normally not between resident and resident

Copyright © 2012 Deloitte Development LLC. All rights reserved.37

D. International Taxes - Transfer Pricing in India

Arms Length Price:• Law requires an “Arms Length Price” (‘ALP’) to be

established

• ALP means price applied in uncontrolled conditions (open market price)

• Determined as an Arithmetic Mean of uncontrolled prices (or margins)

• Flexibility accorded to taxpayer to adopt any price within (+/-) 5% of the arithmetic mean

(Budget 2012 clarified, cannot be considered a standard deduction)

©2011 Deloitte Touche Tohmatsu India Private Limited

Arm’s length price

• As per Section 92F, “Arm’s length price” means a price which is applied or proposed to be applied in a transaction between persons other than associated enterprises, in uncontrolled conditions

38

Controlled Transaction

Uncontrolled Transaction(ALP)

Enterprise A

Unrelated Enterprise B

Related Enterprise C

• “Arm’s length price” would be similar price charged to Unrelated Enterprise in an uncontrolled Transaction

• The ALP can vary by 5% of the Arithmetic Mean of more than one price (Budget 2012 clarified, cannot be considered a standard deduction)

Copyright © 2012 Deloitte Development LLC. All rights reserved.39

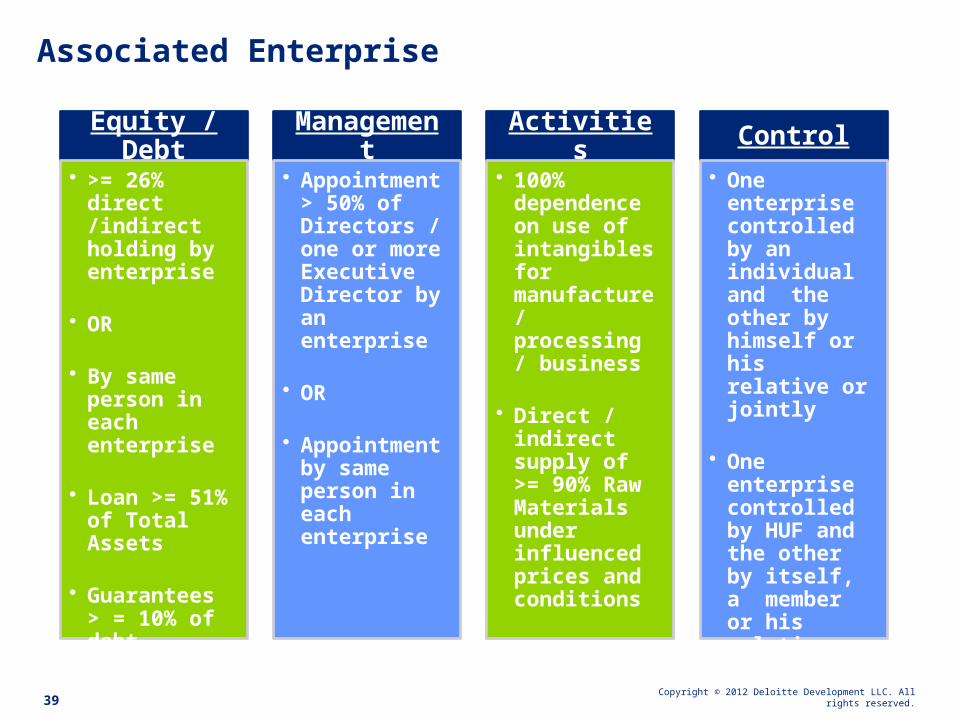

Associated Enterprise

Equity / Debt

• >= 26% direct /indirect holding by enterprise

• OR

• By same person in each enterprise

• Loan >= 51% of Total Assets

• Guarantees > = 10% of debt

• > 10% interest in Firm / AOP / BOI

Management

• Appointment > 50% of Directors / one or more Executive Director by an enterprise

• OR

• Appointment by same person in each enterprise

Activities

• 100% dependence on use of intangibles for manufacture / processing / business

• Direct / indirect supply of >= 90% Raw Materials under influenced prices and conditions

• Sale under influenced prices and conditions

Control

• One enterprise controlled by an individual and the other by himself or his relative or jointly

• One enterprise controlled by HUF and the other by itself, a member or his relative or jointly

Methods for Arm’s length price determination

Indian law provides for application of following methods:

Comparable Uncontrolled Price method (CUP): Comparison of actual price

Resale Price Method (RPM): Comparison of gross margin for a distributor

Cost Plus Method (CPM): Comparison of gross margin for a manufacturer / service provider

Profit Split Method (PSM): Sharing of profits among entities sharing proportionately in risks in a highly integrated operation

Transaction Net Margin Method (TNMM): Comparison on a net (operating) profit basis

40

No priority of methods; flexibility granted to tax-payer for selection of Most Appropriate Method

Copyright © 2012 Deloitte Development LLC. All rights reserved.

Transfer Pricing Rules

Rule 10B Arms’ Length Price

• Sets out General Applicability of all five transfer pricing methods

• Comparability criteria defined

Rule 10C

Most Appropriate

Method

• Flexibility of choice depending on facts and circumstances

• Sets out the factors to be considered in selecting the ‘most appropriate’ method

Rule 10D

Documentation

• Mandatory / Supplementary Documentation requirements prescribed

• If aggregate value of the transactions does not exceed Rs. 10 million -documentation requirements are relaxed

Rule 10E

Accountants

Report

• Accountant's Report required as prescribed

• To assist the Assessing officer in selecting cases for scrutiny

Rule 10A - Defines certain expressions

41

Copyright © 2012 Deloitte Development LLC. All rights reserved.

Contemporaneous Documentation

Step wise process

42

Group Overview:

This section of the TP Report discusses the following:

Multinational group profile of which assessee enterprise is a part;

Ownership structure and share holding pattern of the assessee enterprise with details of shares or other ownership interest

Industry Analysis:

The Industry analysis of the company covers the following

A broad description of the business of the client and the industry in which the client operates, and of the business of the associated enterprises with whom the client has transacted

Economic AnalysisFunctional Analysis

Group Overview and Industry Analysis

Determination of ALP

Copyright © 2012 Deloitte Development LLC. All rights reserved.

Contemporaneous Documentation

Step wise process

43

Functional Analysis:

• A functional analysis enables mapping of the economically relevant facts and characteristics of transactions between associated enterprises with regard to their functions, assets and risks. Hence a functional analysis facilitates characterization of the associated enterprises and assists in establishing a degree of comparability with similar transactions in uncontrolled conditions.

Economic Analysis:

• This section provides the following details:

Value of international transactions

Selection of MAM (Most Appropriate

method

Bench marking Process

Adjustments

Determination of ALP

Result:• Maintain Documentation to comply with the Transfer Pricing Regulations in India

• To establish that the international transactions of the Company are at arm’s length as prescribed in the Indian Regulations

D. Indirect Taxes

Copyright © 2012 Deloitte Development LLC. All rights reserved.45

D. Indirect Taxes – Overview

VAT

• Tax on commodities/ Goods

Service Tax

• Tax on services

Customs duty

• Tax on imports / exports

Central

Excise

Duty

• Tax on locally manufactured goods

Copyright © 2012 Deloitte Development LLC. All rights reserved.46

D. Indirect Taxes – Customs duty on Imports / Exports

Custom

s duty

• Customs duty is applicable on Import transactions• Refer to customs tariff act 1975 Part II for rates of duty applicable• Part II of the Import tariff act is categorized into 98 chapters • Part II of the Import tariff act also has a list of Generally exempted items• Part III The second schedule covers Export Tariff & corresponding

exemption notifications

Customs

duty

Copyright © 2012 Deloitte Development LLC. All rights reserved.47

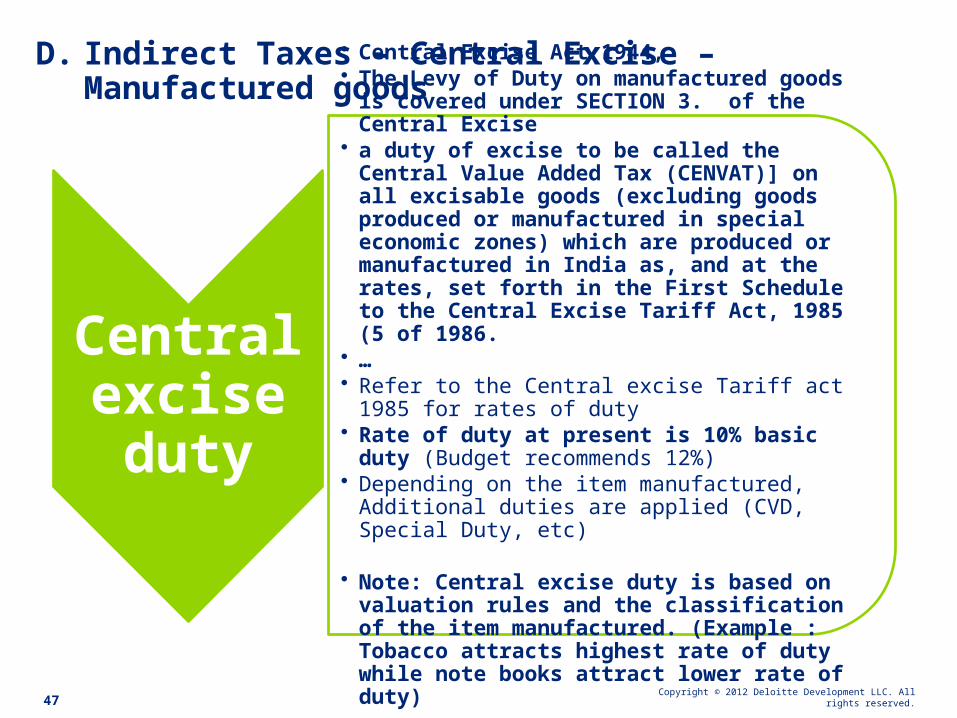

D. Indirect Taxes – Central Excise – Manufactured goods

Central

excise duty

• Central Excise Act 1944,• The Levy of Duty on manufactured goods is

covered under SECTION 3. of the Central Excise• a duty of excise to be called the Central Value

Added Tax (CENVAT)] on all excisable goods (excluding goods produced or manufactured in special economic zones) which are produced or manufactured in India as, and at the rates, set forth in the First Schedule to the Central Excise Tariff Act, 1985 (5 of 1986.

• …• Refer to the Central excise Tariff act 1985 for rates of

duty • Rate of duty at present is 10% basic duty (Budget

recommends 12%)• Depending on the item manufactured, Additional

duties are applied (CVD, Special Duty, etc)

• Note: Central excise duty is based on valuation rules and the classification of the item manufactured. (Example : Tobacco attracts highest rate of duty while note books attract lower rate of duty)

Copyright © 2012 Deloitte Development LLC. All rights reserved.48

D. Indirect Taxes – Services Tax

Service Tax

• Service Tax is administered under chapter V of the Finance Act and governed by rules of Central Excise Act

• Sec 65 covers the definition of services, • 121 services are covered, more services are

being added in the Budget 2012• Budget 2012 introduced the a negative list of

17 services not taxable• There are more exempted services covered by

various notifications from time to time• Rate applicable for the services is specified in

Sec 66 of Finance Act currently specified at 12% w.e.f 1st Apr 2012

• Service Tax Returns to be filed half yearly in prescribed format (ST 3 return)

• Service Tax payments have to be made online

Copyright © 2012 Deloitte Development LLC. All rights reserved.49

D. Indirect Taxes – VAT (Local Sales Tax)

Local

Sales

Tax

• AP VAT Act 2005• An act to provide for and consolidate the law relating to levy of

value added tax on sale or purchase of goods in the state of Andhra Pradesh and for matters connected therewith and incidental thereto..

• Charging sec is Sec 4..• Sale is taxed..

Local Sales

tax

II. Knowledge management, Appellate Hierarchy and Practical challenges

Copyright © 2012 Deloitte Development LLC. All rights reserved.51

Knowledge Management

Respective Acts

Income Tax Rules, Central Excise Rules, Customs rules

Circulars and notifications

Advance rulings

Case laws (SC, HC, Tribunal)

Concept Papers

Committee reports

Clarifications & FAQ’s

Press Information Bureau releases

Copyright © 2012 Deloitte Development LLC. All rights reserved.52

Appellate Hierarchy

Tax filing A O CIT (A)

ITAT

High Court Supreme Court

MAP

If selected for

audit Normal course

AO — Assessing officer; CIT(A) — Commissioner Income Tax (Appeals); ITAT — Income Tax Appellate Tribunal (Highest Fact finding Authority)MAP — Mutual Agreement Procedure (USA and India Government level negotiation); NA — Not Applicable

DC — Deputy Commissioner; CCE(A) — Commissioner Customs & Central Excise(Appeals); Comm. – Jurisdictional Commissioner, CESTAT — Customs, Excise & Service Tax Appellate Tribunal (Highest Fact finding Authority)

Income Tax Hierarchy

Service Tax Hierarchy

Refund

Application

by Assessee

Notice/PH DC CCE(A) High CourtSupreme

CourtCESTAT

Remand

Refund can be sanctioned by any of the authorities

EA 2000

AuditNotice/PH

DC(A) CCE(A)

High CourtSupreme

CourtCESTAT

CENVAT Refund Procedure

CENVAT Audit Procedure

Comm.

Copyright © 2012 Deloitte Development LLC. All rights reserved.53

Practical Challenges

Manage EGO’s of Revenue officials,

Systems automation by Revenue wings,

not fully automated

Software related challenges

Frequent changes in forms / formats

Statutory due dates / conflicting holidays

Internal revenue targets – How realistic?

Availability of authorized signatories

Teams knowledge, application of correct

rates, classification / chapter issues

Right and appropriate documentation

New notifications, clarifications, advance

rulings & court judgments

Retrospective amendments to law

Specifics Generic Challenges

PAN not available of service provider

Service Tax Registration #

Typographical errors, 95% PAN rule, TAN

mismatch

Application of correct TDS sections, rates,

amount deducted vs paid

Correctly filling the forms (assessment

year, Section, range, lower rates etc)

Lower deduction certificate (with amount

& period limitation)– Interpretation issues

E-TDS filings center's working hours

Online filing requirements, not all banks

notified to collect taxes

Revisions / Revised filing requirements

Digital signature requirements

Questions

About DeloitteDeloitte refers to one or more of Deloitte Touche Tohmatsu Limited, a UK private company limited by guarantee, and its network of member firms, each of which is a legally separate and independent entity. Please see www.deloitte.com/about for a detailed description of the legal structure of Deloitte Touche Tohmatsu Limited and its member firms. Please see www.deloitte.com/us/about for a detailed description of the legal structure of Deloitte LLP and its subsidiaries. Certain services may not be available to attest clients under the rules and regulations of public accounting.

Copyright © 2011 Deloitte Development LLC. All rights reserved.Member of Deloitte Touche Tohmatsu Limited

![50 MANAGEMENT SKILLS ORIENTATION PROGRAMME [MSOP]€¦ · 15/12 months Training completion certificate with Sponsorship letter of ICSI. Certificate of 15 days training with specialized](https://static.fdocuments.in/doc/165x107/5f6fd4d328da0e3e68351420/50-management-skills-orientation-programme-msop-1512-months-training-completion.jpg)