Corporate Social Responsibility

29

Corporate Social Responsibility An introduction to:

-

Upload

gay-calhoun -

Category

Documents

-

view

15 -

download

0

description

An introduction to:. Corporate Social Responsibility. Objectives for this session:. At the end of this session, you should be able to identify and describe: A definition for CSR Reasons for having a CSR programme Objections to CSR What makes a CSR programme - PowerPoint PPT Presentation

Transcript of Corporate Social Responsibility

Corporate Social Responsibility

An introduction to:

Objectives for this session:

At the end of this session, you should be able to identify and describe:

• A definition for CSR• Reasons for having a CSR programme• Objections to CSR• What makes a CSR programme• How a CSR programme is communicated• Principles of reporting for CSR• Some alternative viewpoints on CSR

Corporate Social Responsibility?

What is:

Also known as:

Corporate Citizenship

Corporate Responsibility

Responsible Business

Definition:

“Specifically, we see CSR as the voluntary actions that business can take, over and above compliance with minimum legal requirements, to address both its own competitive interests and the interests of wider society.”

Source: www.csr.gov.uk

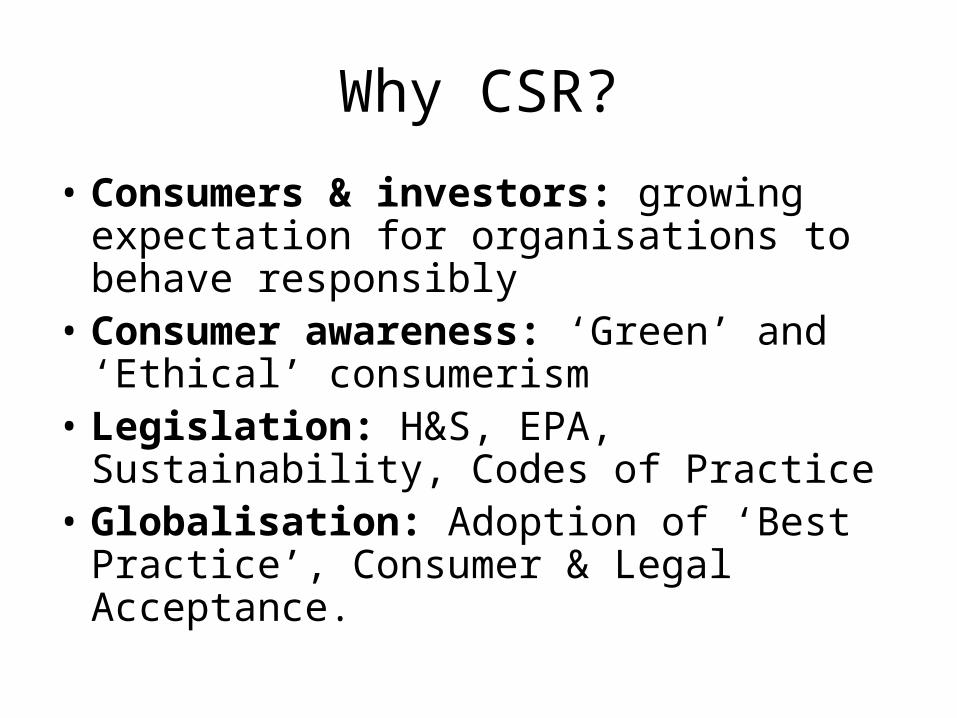

Why CSR?

• Consumers & investors: growing expectation for organisations to behave responsibly

• Consumer awareness: ‘Green’ and ‘Ethical’ consumerism

• Legislation: H&S, EPA, Sustainability, Codes of Practice

• Globalisation: Adoption of ‘Best Practice’, Consumer & Legal Acceptance.

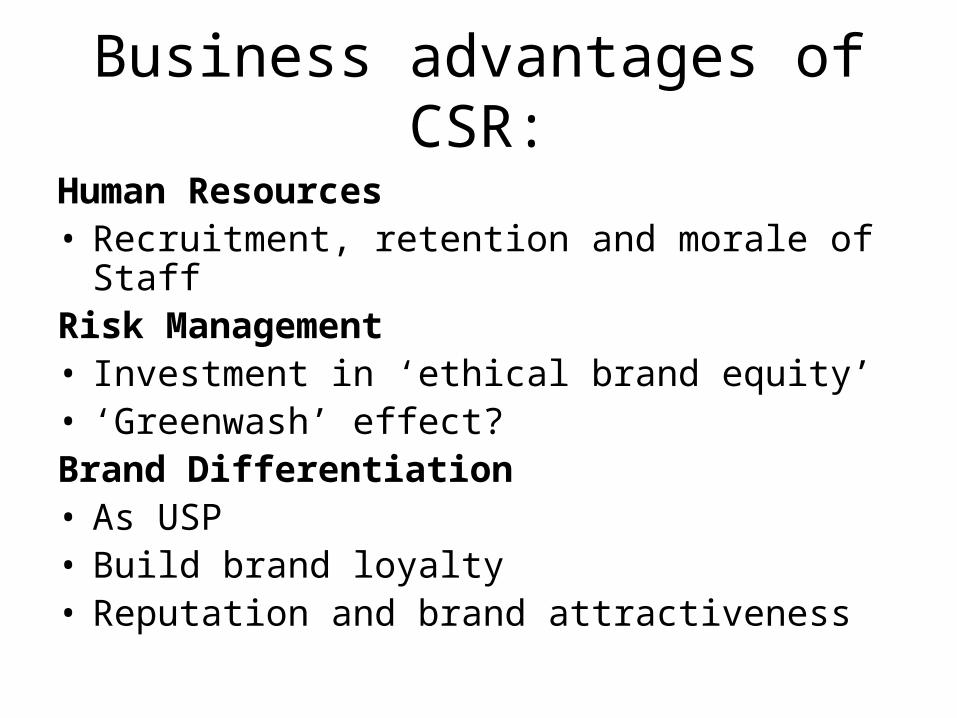

Business advantages of CSR:

Human Resources• Recruitment, retention and morale of StaffRisk Management• Investment in ‘ethical brand equity’• ‘Greenwash’ effect?Brand Differentiation• As USP• Build brand loyalty• Reputation and brand attractiveness

Business advantages of CSR:

Business Development• New markets, products and services

Resources Management• Better management and conservation of

strategic assets

Stakeholder Management• Better internal and external relationships• Freedom of operation: reduce government,

public, NGO intervention in organisation

adds value

Corporate Social Responsibility:

Why not CSR?

• May take management focus away from core business activity

• May appear cosmetic – without genuine social benefit

• May make organisation more vulnerable to revelation of bad / unethical business practice

• A restriction to free trade?

Economist, Milton Friedman says:

“The social responsibility of business is to increase its profits.”

“What does it mean to say that "business" has responsibilities? Only people can have responsibilities.”

“…in a free society there is one and only one social responsibility of business – to use its resources and engage in activities designed to increase its profits so long as it stays within the rules of the game, which is to say, engages in open and free competition without deception or fraud."

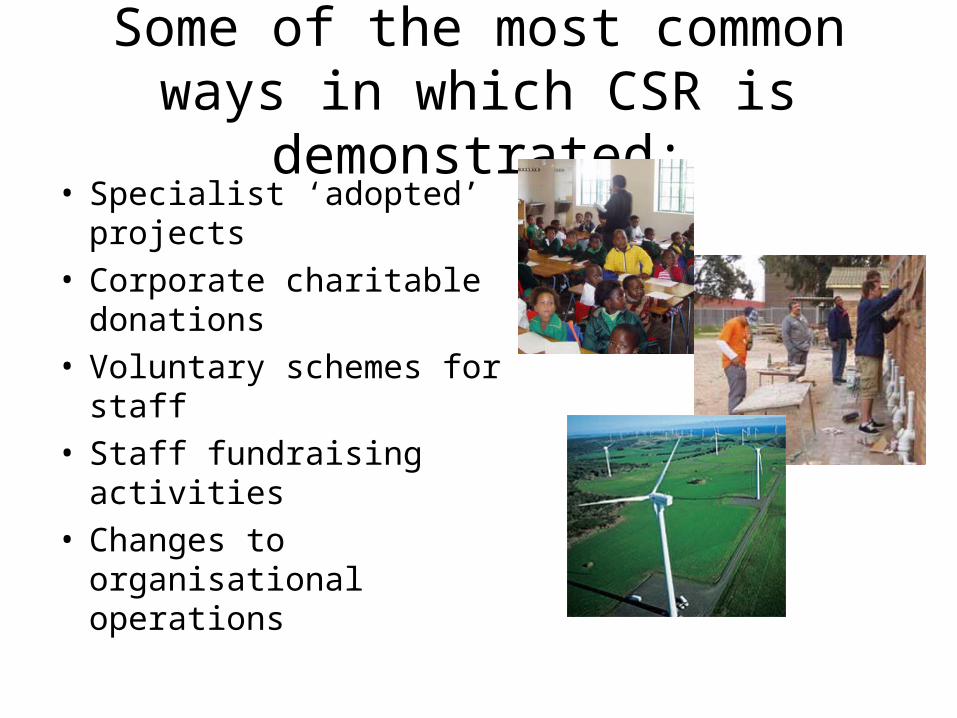

Some of the most common ways in which CSR is demonstrated:

• Specialist ‘adopted’ projects

• Corporate charitable donations

• Voluntary schemes for staff

• Staff fundraising activities• Changes to organisational

operations

The four components of CSR:

• Economic

• Legal

• Ethical

• Discretionary

Communicating Corporate Social Responsibility

General values statement

• Organisations should develop a general values statement which reflects their stance towards CSR

• This may form part of a more comprehensive Mission Statement

• Should define ethical framework that guides the accomplishment of the overall mission of an organization within a society

Example: Organisational Focus

JP Morgan Chase

Example: Environmental Focus

Coca Cola

Example: Customer Focus

Home Depot

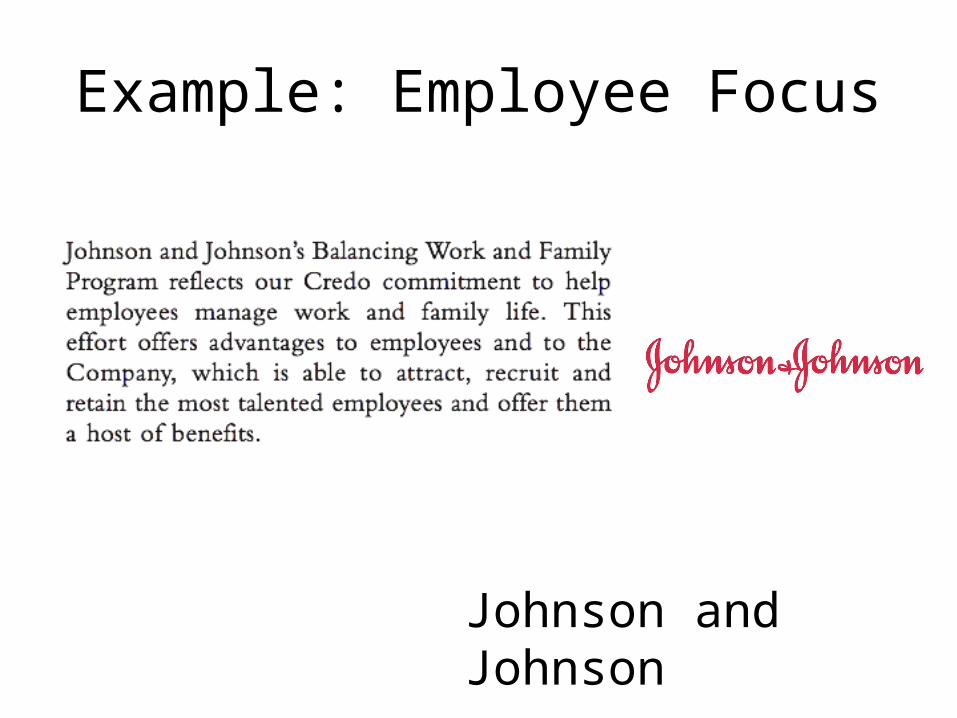

Example: Employee Focus

Johnson and Johnson

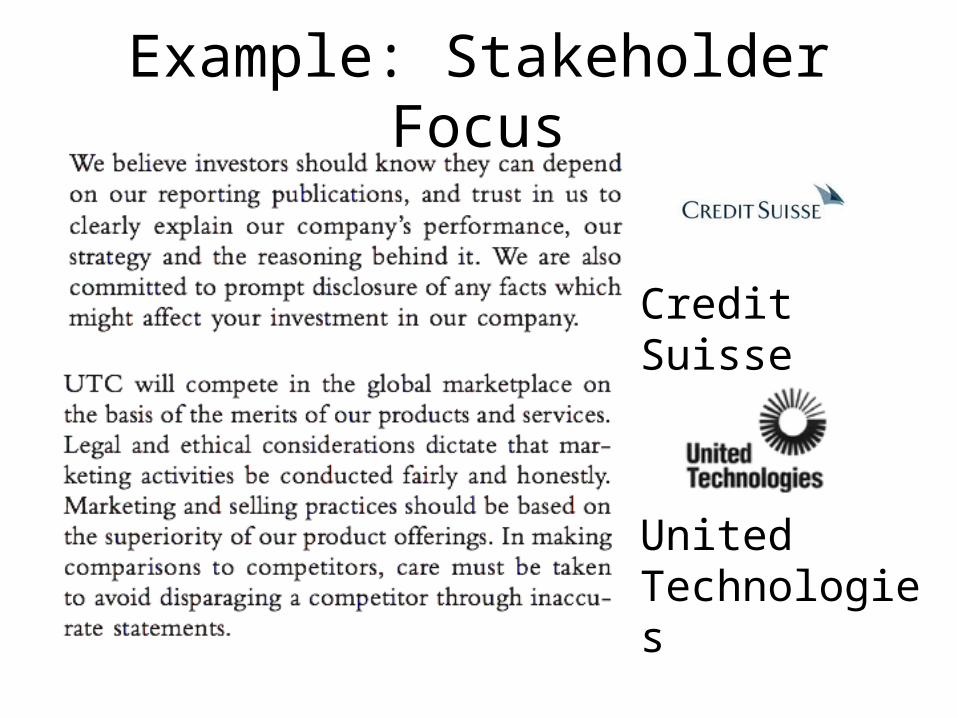

Example: Stakeholder Focus

Credit Suisse

United Technologies

Example: Social Focus

Bristol-Myers Squibb

Reporting CSR:

CSR projects may be administered and communicate achievements via:

• A dedicated CSR section or department

• The HR department

• Business development section

• Public Relations department

• Directly via CEO and / or Board of Directors

Reporting Formats:The ‘Triple Bottom Line’

This means expanding the traditional reporting framework to take into account performance in terms of:

• Social (People)

• Environmental (Planet), as well as

• Financial (Profit)

Reporting Formats:The ‘Triple Bottom Line’

• Concept developed by John Elkington in 1994

• Expects organisations to be responsible to ‘stakeholders’ interests rather than ‘shareholders’ profit

• Related concepts:– Full-cost accounting– Social entrepreneurialism– Social and natural capital

Other sources for CSR reporting:

‘Sustainability Guidelines’ developed by the Global Reporting Initiative

(www.globalreporting.org)

SA800 certification developed by the international human rights organisation Social Accountability International.

(www.sa-intl.org)

Other sources for CSR reporting:

The Green Globe programme for ‘benchmarking, certification and performance improvement’, based on Agenda 21 proposals from the 1992 Rio Earth Summit

(www.greenglobe.org)

ISO 14000 international environmental management standards

(www.14000.org)

Other sources for CSR reporting:

The United Nations Global Compact (UNGC) framework and mechanism designed to encourage businesses to adopt CSR policies

(www.unglobalcompact.org)

The FTSE 4 Good Index – measures the performance of companies who meet globally recognised CSR standards.

(www.ftse.com/Indices/FTSE4Good_Index_Series)

Alternative sources of information:

www.corpwatch.org

www.naomiklein.org

In conclusion:In this session we have looked at:• What is CSR• Why CSR is likely to be come more widely

adopted• The business case for CSR• The Value Statement (Customer, Employee,

Stakeholder and Social focus)• Reporting and Accountability options for CSR

including the ‘Triple Bottom Line’ concept• CSR and social criticism of international

organisations