Corporate Presentation Inmarsat plc VSAT Space Segment $145m (8%) Energy VSAT Space Segment $168m...

22

Corporate Presentation Inmarsat plc June 2014

Transcript of Corporate Presentation Inmarsat plc VSAT Space Segment $145m (8%) Energy VSAT Space Segment $168m...

Corporate Presentation Inmarsat plc June 2014

Business Overview

2

Market leader in MSS today moving into VSAT markets

! Market leader

! Global coverage, L-‐band ! Mission cri6cal customer needs

! EBITDA margin 70%

! Entering established markets

! Global coverage, Ka-‐band ! Future proof exis6ng business ! Fully-‐funded plan

Strong core business and investment in new growth

Mobile Satellite Services (MSS)

VSAT ‘Global Xpress’ Services

Today: Tomorrow:

MSS markets ! 57% of MSS revenue

! 190,000 subscribers ! Drivers: Ship management

Automa6on cost savings

Crew welfare / access

Smaller vessel adop6on

3

Land Mobile

Aviation

Maritime

! 17% of MSS revenue

! 172,000 subscribers ! ~60% government business

! Drivers: Military special ops

Interna6onal aid agencies

Media: on-‐the-‐spot repor6ng

! 15% of MSS revenue

! 17,000 subscribers ! ~60% government business

! Drivers: Military, VIP aircraV

Business jets

In-‐flight passenger connec6vity

! Market leader in all sectors

! Mission cri<cal remote connec<vity

! Safety services ! Global coverage ! Strong subscriber growth ! Spare satellite in orbit ! Satellite life<mes to 2023

! Wholesale EBITDA margin ~70%

! Limited compe<<on

(1) Based on 2013 MSS revenue reported for Inmarsat Global

(1)

High barriers to entry

4

Scale needed to build a global network and fund replacement satellites Capital

Uniform global spectrums rights now extremely challenging to secure and retain Spectrum Rights

Distribu6on rela6onships with over 600 organisa6ons, providing essen6al global reach Distribu<on

Orbital loca6ons can take years to secure and may not be available Orbital Slots

Inmarsat has established market access over 33 years of opera6ons Licensing

33 years technical excellence and provision of global safety services Reputa<on

Multiple challenges for any new entrant

At least 6 years for a new competitor to enter the market

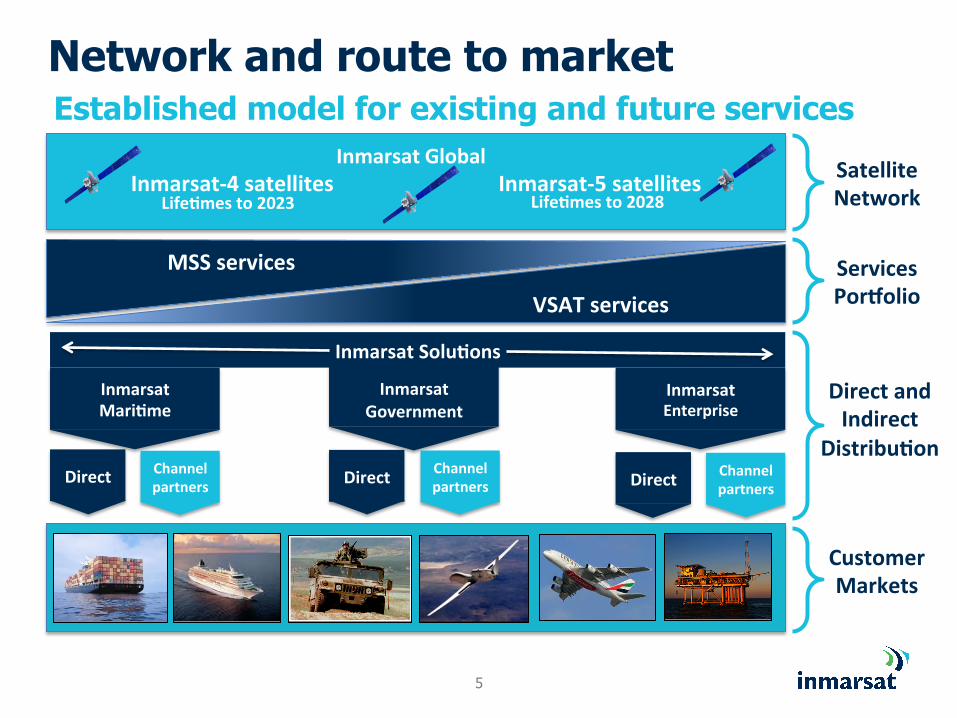

Network and route to market

5

Established model for existing and future services

Inmarsat

Government Inmarsat Mari<me

Inmarsat Enterprise

Inmarsat-‐4 satellites Inmarsat-‐5 satellites

Inmarsat Solu<ons

Inmarsat Global

MSS services

VSAT services

Satellite Network

Services PorXolio

Direct Channel partners

Life<mes to 2023 Life<mes to 2028

Direct and Indirect

Distribu<on

Customer Markets

Direct Direct Channel partners

Channel partners

High-quality end customer base

6

Enterprise Maritime

Supplying mission-critical applications to a diverse end user base

Government / Military International Aid

Global coverage

2014

$1.9bn market

size

50 MB/s

$1.6bn cost

3 satellites Ka-band

Global Xpress overview

! Global coverage complete in 2014

! Future proof global MSS franchise

! Expansion of ac<vi<es into established, growing adjacent VSAT markets

! $1.9bn established market opportunity

! Significant capacity pre-‐commitments

! 30% of cumula<ve 5-‐year plan revenues secured

! Distribu<on agreements signed

! $700m of financing from Ex-‐Im Bank

! Total cost $1.6bn including spare satellite

7

World’s first global mobile VSAT service

8

Our Strategy Operational progress matched by commercial readiness

! L-band growth via Inmarsat-4, Alphasat & Inmarsat-6

! Further growth & diversity via Inmarsat-5 & GX

Safety and redundancy

Capacity and speed

Solutions Ecosystem - driving value-adds for end users

Inmarsat 4 & 6

Core L-band services Highly mobile, agile and resilient

Inmarsat 5

Core Ka-band services High capacity, high speed

! Empower a high-value solutions ecosystem centred on Inmarsat

! Reorganised for proximity, agility & efficiency

8

Business unit structure provides strategy implementation on a market-by-market basis

Maritime VSAT Space

Segment $145m (8%)

Energy VSAT Space

Segment $168m (9%)

Enterprise Consumer

Retail Other

Segments $944m (50%)

US DoD, ROW Gov't commercial

FSS $643m (34%)

VSAT wholesale satellite capacity purchases

2010 - $1.9bn* Maritime

VSAT Space Segment $135m (10%) Energy

VSAT Space Segment $152m (11%)

Enterprise Consumer

Retail Other Segments

$576m (42%)

US DoD, ROW Gov't, commercial FSS $502m

(37%)

2008 - $1.4bn*

Global Xpress market opportunity

2008 to 2010 CAGR • Mari6me ~4% • Energy ~5% • Government ~13%

VSAT wholesale satellite capacity purchases

* $1.4bn for 2008 and $1.9bn for 2010 represent the total VSAT wholesale satellite capacity purchases for the year indicated. These es6mates are based on the Comsys VSAT Report (11th and 12th edi6ons, respec6vely), taking total Service Revenue ($5.4bn and $7.3bn, respec6vely) adjusted for managements’ es6mates of hardware revenue, retail mark-‐up and value added services.

Historical growth rates • Mari6me ~22% • Energy ~9% • Government ~7%

9

Adjacent established markets with growth

Further growth options

10

! High growth market opportunity >$250m ! Strategic partnerships with SkyWave and ORBCOMM

! Suited to L-‐band network ! Compe<tor market share opportunity ! Significant product development completed

M2M Services

Further growth options

11

GX Avia<on will provide speeds of up to 49 Mbps to aircraf, which has the poten<al to support live feeds from the internet, innova<ve applica<ons for the crew and passengers and offers airlines a future-‐proof op<on with broadband capacity for growth ! 400% increase in connected aircraf expected in the next decade

! New global services enable a whole new genera<on of affordable equipment.

! Upcoming launch of SwifBroadband HDR; higher rate communica<ons to or from the aircraf

! Upcoming enhancements include SBB for helicopters and approved Safety Services using SBB

In-flight Connectivity

Financial Summary

Financial overview

! Highly cash genera<ve core business with growth ! Largely fixed opera<ng costs ! ~70% core EBITDA margin

! Fully-‐funded investment programme

! Modest leverage at peak of investment cycle

! Long-‐term dividend policy in place

! Eight year history of dividend growth

Free cash flow expansion follows investment phase

13

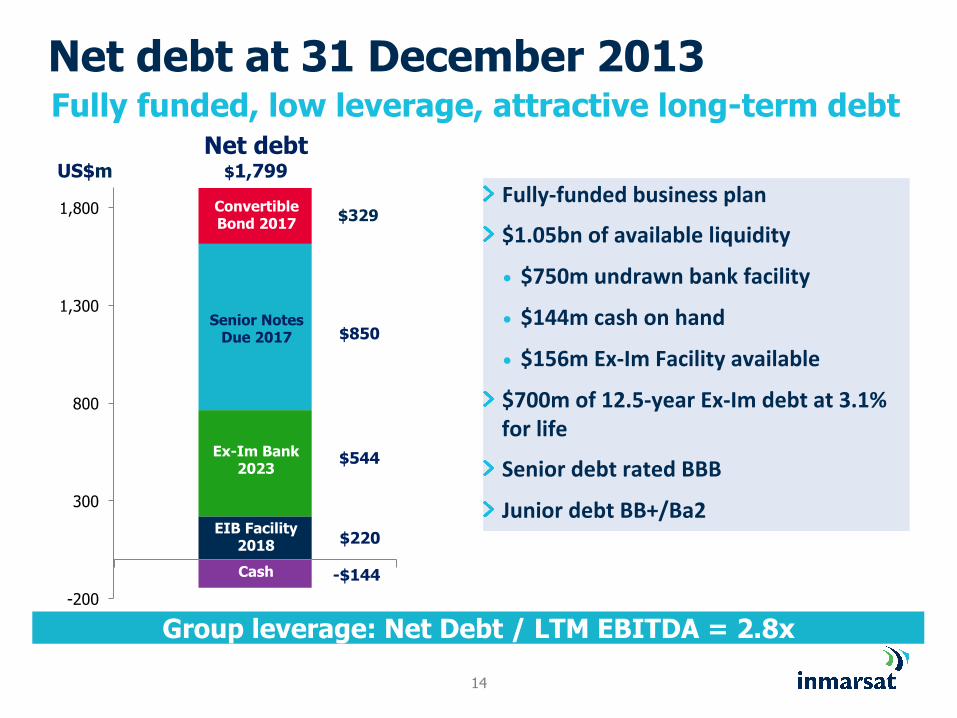

Net debt at 31 December 2013

! Fully-‐funded business plan ! $1.05bn of available liquidity • $750m undrawn bank facility

• $144m cash on hand

• $156m Ex-‐Im Facility available

! $700m of 12.5-‐year Ex-‐Im debt at 3.1% for life

! Senior debt rated BBB ! Junior debt BB+/Ba2

14

-200

300

800

1,300

1,800

EIB Facility 2018

Ex-Im Bank 2023

Senior Notes Due 2017

Cash

Convertible Bond 2017

US$m

$850

$544

-$144

$1,799

$329

$220

Net debt Fully funded, low leverage, attractive long-term debt

/ / Group leverage: Net Debt / LTM EBITDA = 2.8x

Appendix

316 332384

432495

556 530 545 562

491 500557

635695

747 755 776 795

0

100

200

300

400

500

600

700

800

900

1,000

0

100

200

300

400

500

600

700

800

900

1,000

2005 2006 2007 2008 2009 2010 2011 2012 2013EB

ITDA

Reve

nues

Maritime Land Aviation

Leasing Other EBITDA

Revenue CAGR: 6.2%

Inmarsat Global record of growth Historical revenue and EBITDA growth

(64%)

(68%)

(66%) (69%)

(71%)

Sector CAGR

2005–2013

Maritime 6%

Land Mobile 1%

Aviation 22%

Leasing 4%

Revenue growth by sector

($ in millions) ($ in millions)

Notes: Other Income excludes revenue from LightSquared. ( ) denotes EBITDA / revenue margin (excluding LightSquared).

(74%) (70%)

16

(71%)

(70%)

Maritime market overview

! Commercial mari<me market • Represents 75,421 vessels

• Total addressable market today 20,000 vessels

• Only 5,247 have VSAT installed today

! Other poten<al mari<me markets • Fishing: 32,669 vessels

• Inland: 18,033 vessels

• Leisure: 1,028,000 vessels

* Source: Comsys Report, 3rd Edition, 2012

1,071 5,020

11,749

30,717

14,295

7,505

5,064

Commercial Ships by Type*

Passenger

Container

Miscellaneous

Bulk/Dry Cargo

Tankers

O & G Maritime

Pass / Cargo

17

Maritime market can grow in MSS and VSAT

XpressLink take-up

! Significant fleets commipng to XpressLink ! Mul<-‐year agreements – five years standard ! >800 installa<ons ! Total installed VSAT base 1,478 ships (XL and legacy VSAT) • Revenue > $70m pa, EBITDA margin 15-‐20% • Significant and growing margin expansion opportunity

! Acquisi<on of Globe Wireless to increase XL installa<on capability • Adds established Value Added Services capability

18

XpressLink is a market-leading Maritime VSAT service

IsatPhone Pro

19

Cumulative net adds since 2011*

* Based on change in billable commercial voice subscribers for each quarter end as reported in Iridium SEC filings on form 10-Q/10-K for the applicable period. Active IsatPhone Pro subscribers for Inmarsat.

! IsatPhone Pro >86,000 ac<ve subscribers ! >10% market share by units ! IsatPhone outselling market leader ! Reignited growth in land voice revenue afer years of decline

Taking market share from competitors

IsatPhone 2 ISatPhone Pro

FY 2013 MSS revenue breakdown by sector FY 2013 revenue breakdown by type

2013 revenue breakdown

FY 2013 revenue by business line

Aviation 15%

Leasing 11%

Maritime 57%

Land 17%

Leasing 11%

Data 76%

Voice 13%

Inmarsat Global

Inmarsat Solutions

20

Broadband & Other MSS 50%

Inmarsat MSS 50%

Q & A