Corporate Presentation - Fullerton India · Corporate Presentation September - 2015 1. 2. 3. ......

29

Corporate Presentation September - 2015 1

Transcript of Corporate Presentation - Fullerton India · Corporate Presentation September - 2015 1. 2. 3. ......

Corporate PresentationSeptember - 2015

1

2

3

Strong and sustainable financial performance

High quality infrastructure,

processes & resources

Well developed footprint

Strong risk culture

Poised for accelerated growth

Q1FY16 PAT increased by 48% YoY to INR 1,847mio

Customer AUM increased by 37% YoY to INR 98,914mio

Secured assets ratio at 47.7% - provides stability in earnings

Pan India coverage

Deep skills in under banked Tier 2-6 markets

Priority Sectors comprise ~49% of disbursal

Independent risk function

Early warning signs monitoring, proactive risk management

Best in class advanced analytics

Robust governance process

Management Team with significant experience

Large investment in technology refresh

Straight through processing & Six Sigma discipline

Improving macro environment

Well capitalised; Ready for expanded avenues of growth

Leverage on new opportunities to better utilize existingdistribution and expertise

Highlights

4

Fullerton India Credit Company Ltd. [FICC]A step down subsidiary of Temasek Holdings

Fullerton Financial Holdings (FFH), the parent, was incorporated in January 2003 as a wholly owned subsidiary by Temasek Holdings (Private) Ltd

FFH has 9 operating financial services entities located across 8 countries serving 6 million customers

FFH’s vision is to develop unique business models that bring financial services closer to the underserved in emerging economies

DUBAI, UAE19 Branches195k Customers

PAKISTAN171 Branches408k Customers

INDIA445 Branches1,278k Customers

4 Provinces,Central CHINA31 Branches8k Customers

CHINA66Branches715k Customers

MYANMANR12 Branches29k Customers

CAMBODIA POST BANK31 Branches18k Customers

MALAYSIA106 Branches60k SME Customers

INDONESIA2070 Branches4.2 M Customers

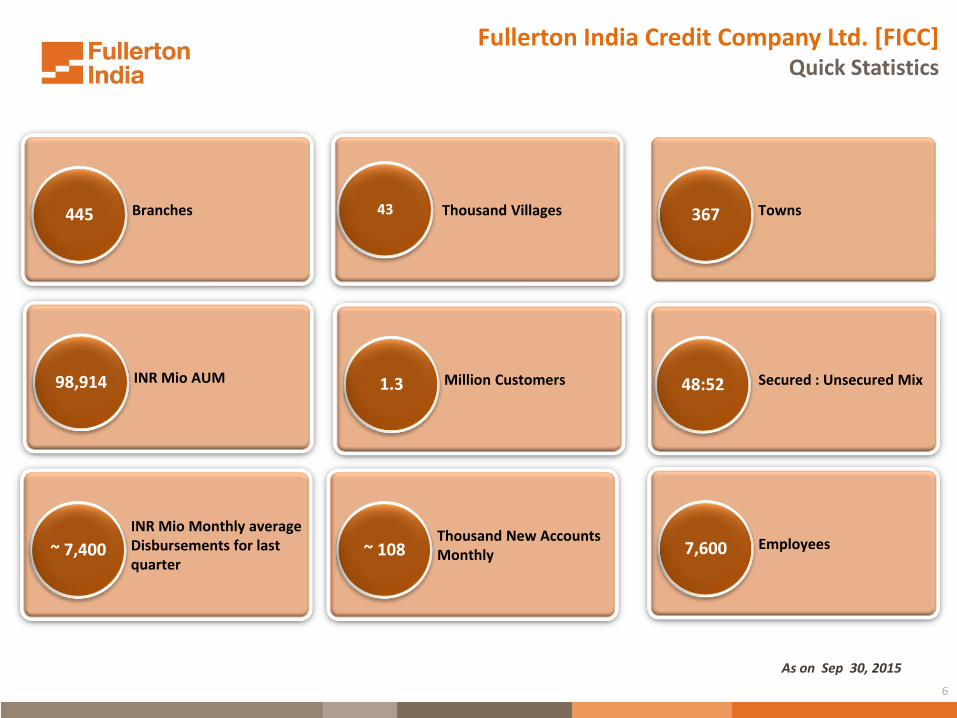

5

As on Sep 30, 2015

Branches445 Thousand Villages Towns367

INR Mio Monthly average Disbursements for last quarter

~ 7,400Thousand New Accounts Monthly~ 108 Employees7,600

INR Mio AUM98,914 Million Customers1.3 Secured : Unsecured Mix48:52

43

Fullerton India Credit Company Ltd. [FICC]Quick Statistics

6

Customers (In ‘000)

40

3

Branch Coverageby city population size

…with strong presence in under banked geographies

40%+ of branches in cities with <100Kpopulation

Deep experience in areas under the Regulator’sfocus for furthering financial inclusion

25 7572 306 762

413

49

50

59

44

2

5831

0

64

8

315

122

13

1

1

34

3

6

16

5447

155

173

>5mio 1mio - 5mio 500k - 1mio 100k - 500k <100k

Urban – 218 Branches in 23 states

Rural – 227 Branches in 8 states

23 States367 Towns

43K Villages

Strong pan-India distribution networkOver 445 Branches covering 23 States…

7

Product Suite

BUSINESS LOANS

RURAL LIVELIHOOD LOANS RURAL HOUSING FINANCE TWO-WHEELER LOANS

LOANS AGAINST PROPERTYPERSONAL LOANS

COMMERCIAL VEHICLE LOANS MERCHANDISE LOANS INSURANCE

SME LOANS

RURAL ENTERPRISE LOANS

8

Technology-enabled business operations

Disaster Recovery on Cloud

CRMNext – Lead Management & Customer Service platform

BRMF - Loan management System – Rural

Bankers Realm

FinnOne – Integrated Loan Origination & Management

System - Urban

CITRIX - Desktop Virtualization

Biometric transaction device

CashTrea – Treasury Management System

9

Digitizing FICCWe have deployed cutting edge technology solutions

Further deployments planned leveraging this platform

• GPS enabled online integrated platform • Digital fingerprint authentication• Automated solutions:

For tracking customer interactions Payment processing and appropriation

First NBFC to roll out Android app for collections

10

Improved opinion from external rating agenciesKey developments recognised

Multi faceted improvements

“ … improvement in FICC’s profitability … tightened credit underwriting”

“… shift in portfolio mix to secured lending… more affluent customer segment”

“the asset quality ... improved..”

“…strong parentage”

“…company’s detailed risk analytics…”

‘”… transitioned from short term to long term … mirrors its asset profile… diversified investor base… unused committed …lines”

2015

Strengths recognized

“…strong parentage…”

“…improvement in profitabilityand operating efficiencies…”

“…strengthening of credit underwriting … risk management”

“…shift towards secured lending… more affluent customers…”

“…conservative provisioning …asset liability maturityprofile…”

AA+ AAA

11

Board of Directors

Operating Committees

ALCO Operational Risk Forum Borrowing Committee Customer Service Forum

Balance Sheet management

Agrees on funds deployment

Controls liquidity interest rate risks

Establishes operational risk appetite

Establishes framework for managing operational risk

Monitors underlying risks and remediation actions

Approves borrowing arrangements

Approves terms and conditions for borrowings

Approves pre-payments

Monitors customer experience, improving service

Enables system improvements, performance measures

Risk Oversight Committee Audit Committee Nomination & Remuneration Committee

CSR Committee

Oversees credit, market and operational risk

Approves risk appetite and credit policies

Monitors portfolio performance and approves mitigation actions

Oversees Internal controls framework

Reviews the financial statements and financial reporting process

Reviews scope, findings, reports, etc. of Internal and external audit

Oversees overall Human Capital mission and strategy.

Oversees key appointments and compensation matters

Reviews structure and composition of the Boardand recommends for changes

Recommends CSR policy, budgets, projects, etc.

Monitors implementation of the CSR activities

A Robust governance framework....incorporates international good practice, reinforced with oversight

12

1.1 mio Customer accounts

• Stress testing

• Risk Rating Models

• Attrition Gating; X-sell

• Recovery Scorecard

• Unstructured Big Data

• Bureau Integration

• Vintage based assessment

• Risk Grading

• Basel AIRB approach

• Geo-profiling

• Approval in Principle offerings

• Portfolio strategy for optimal risk return

• Pin code level customer insight

• Assessment of P&L volatility

• Risk based Pricing

• Retain & grow profitable relationships

• Targeted collections as lower cost

• 360 degree view of customer

• Policy & customer profile

• Segment profitability based strategies

Center of Excellence for Analytics

200+ Business Intelligence Dashboards

50 mio records analyzed for portfolio monitoring

Solution Business Value

Business and Risk AnalyticsDeeply embedded decision sciences across customer lifecycle

Information Management

Predictive Modeling

Insight & Strategy

13

Depth of management experienceBankers with deep domain experience and multinational orientation

Business & Franchise Development

Integrated Risk Management

Capital and Financial

Management

Infrastructure & Resources

Management

• Extensive local experience in Product development and Distribution in large branch networks in Rural & Urban India.

• Subject matter expertise in Retail Lending and Housing Finance

• MNC Banking and International Markets exposure

• Strong appreciation of Risk Management

• In depth experience in Risk Management in Consumer businesses in MNC Banks and in large Indian NBFC including Housing Finance

• Experience teams focused on Risk Policy, Underwriting, Operational Risk , Collections and Legal management

• Specialist team for Decision Sciences which develops Risk and Business Analytics scorecards and tools that drive business strategy

• Strong experience in Global Markets in leading MNC Banks

• Rapidly growing relationships with large Indian & MNC Banks and FIs

• Strong Financial Control experience in MNCs

• Specialised teams dedicated for FP&A, Accounting, Taxation and Company Secretarial

• Strong orientation in compliance and controls

• Strong international experience HR management in large MNC retail Financial experience

• Strong Operations capability with six sigma Process Reengineering expertise

• Advanced technology deployment and change management skills

Combined senior team experience

150+ years 150+ years 100+ years 125+ years

14

Conservative provisioning policyIndustry leading

RBI norms FICC provisioning policy

• NPA classification at 6 months overdue,decreasing progressively to 3 months byMarch 2018

• NPA at 3 months overdue

• Unsecured exposure to be provided for at 24months overdue decreasing progressively to15 months by March 2018

• Full write off for unsecured products at 4months overdue

• Secured exposure to be fully provided for at60 months decreasing progressively to 51months by March 2018

• Full write off for secured lending by 24 months

• Provisioning on standard assets is at 0.25%progressively increasing to 0.4% by March2018

• 0.4% for all urban standard assets; and 1.0% forthe rural standard assets

15

25,086 , 58%

7,077 , 16%

3,679 , 8%

3,899 , 9%

3,887 , 9%

Sep 12

22,933 25,746 30,608

39,311 47,133

33,802 36,704

41,647

47,381

51,781

56,735

62,450

72,255

86,692

98,914

Sep 13 Mar 14 Sep 14 Mar 15 Sep 15

Secured Unsecured

Micro69%

Small25%

Medium6%

Strong customer assets (AUM) growth

INR mio

Business momentumAligned to strategy

8%

(52%)

(48%)

(40%)

(60%)

..with focus on secured assets

INR mio, Percent

LAP contribution to overall increased from 16% in FY12 to 40% in Sep15

Driving financial inclusion…c.40% of new disbursement

INR mio

33,839 , 34%

39,650 , 40%

5,142 , 5%

88 , 0%

20,114 , 20%

Sep 15

Personal Loans

LAP

CV Loans

TW and Used Car

Rural Book

16Non PSL PSL

49%

59%

* Net Credit Loss includes Provision for Standard Assets and MTM Losses on Government Securities

Financial TrendsSignificant performance improvement

17

INR mio H1FY14 H2FY14 H1FY15 H2FY15 H1FY16 YoY %

Net Revenue 4,030 4,228 4,740 5,377 6,195 31%

Expenses 2,478 2,453 2,709 2,955 3,320 23%

Working Profit 1,552 1,775 2,030 2,421 2,874 42%

Net Credit Losses* 653 795 783 659 831 6%

Pre Tax Profit 882 997 1,247 1,763 2,043 64%

Post Tax Profit 882 997 1,247 1,763 1,847 48%

Disbursals 23,967 24,716 30,206 38,101 39,320 30%

Customer Assets (AUM) 56,735 62,450 72,255 86,692 98,914 37%

Secured Assets (%) 40.4 41.3 42.4 45.3 47.7 5.3%

Shareholder Funds 11,667 12,664 13,911 15,673 17,521 26%

Capital Adequacy (%) 22.5 22.4 20.7 19.6 19.5 (1.2%)

Branches (#) 368 397 404 437 445 10%

Improving loss coverage#

Cost to income (%)Sustainable RoA* (%) Sustainable Higher RoE* (%)

Lower credit losses (%)

Key performance indicatorsImproved efficiencies and returns

#Loss Coverage = Operating Profit/Credit Losses

Improved Net NPA

*Pre tax basis for comparable trends18

3.5% 3.5%3.8%

4.6% 4.6%

H1FY14 H2FY14 H1FY15 H2FY15 H1FY16

15.7% 16.4%18.7%

24.0% 24.8%

H1FY14 H2FY14 H1FY15 H2FY15 H1FY16

61.5%58.0% 57.2% 55.0% 53.6%

H1FY14 H2FY14 H1FY15 H2FY15 H1FY16

2.6% 2.7%2.4%

1.7% 1.8%

H1FY14 H2FY14 H1FY15 H2FY15 H1FY16

2.3x 2.3x2.6x

3.7x3.5x

H1FY14 H2FY14 H1FY15 H2FY15 H1FY16

1.6%

1.3%

1.6%1.4%

1.5%

Sep 13 Mar 14 Sep 14 Mar 15 Sep 15

Employee led CSR program for livelihood advancement and women empowerment

Income enhancing vocational training programs for urban and rural women, in fashion designing and beauty & hair care

Cattle care camps for enhancing existing livelihoods Integrated Livestock Development centres (ILD) for

holistic cattle care development, targeted at cattle breed improvement, launched 20 centres across Madhya Pradesh, Karnataka & Maharashtra

19

Jeevika-Vocational Training

No of Programs 300

Impact 7,000 Households

Pashu Vikas-Cattle Care Camp

No of Programs 36

Impact 4,000 Households

Eye check up camps for primary screening and cataract surgeries at the near by partner hospital

5-Vision Care Center for primary screening and 1-mobile vision care van,

Save The Eye

No of Programs 25

Impact 2,800 Households

Krishi Mitra-Organic Farming

No of Programs 80

Impact 900 Farmers

Promotion of organic and homestead farming enhancing adoption of environment friendly practices

HEALTH CARE SERVICES

Primary health care services through mobile medical clinics and 24X7 call center for medical emergencies, operational in 5 locations Hubli, Tumkur, Hoshangabad, Udaipur & Jaipur

Health Care Services

Impact 22,000 Patients

No of Programs 310

CSR ProjectsFY 15-16 (Apr-Sep)

19

Vocational Training Camp -’Jeevika’

Cattle Care Camp-Pashu Vikas

Krishi Mitra- Organic Farming program

Commercial Tailoring & Stitching program-

Jeevika

Health Check-up Camp

Eye Check up Camp-Save the Eye

CSR PhotoFY 15-16 (Apr-Sep)

20

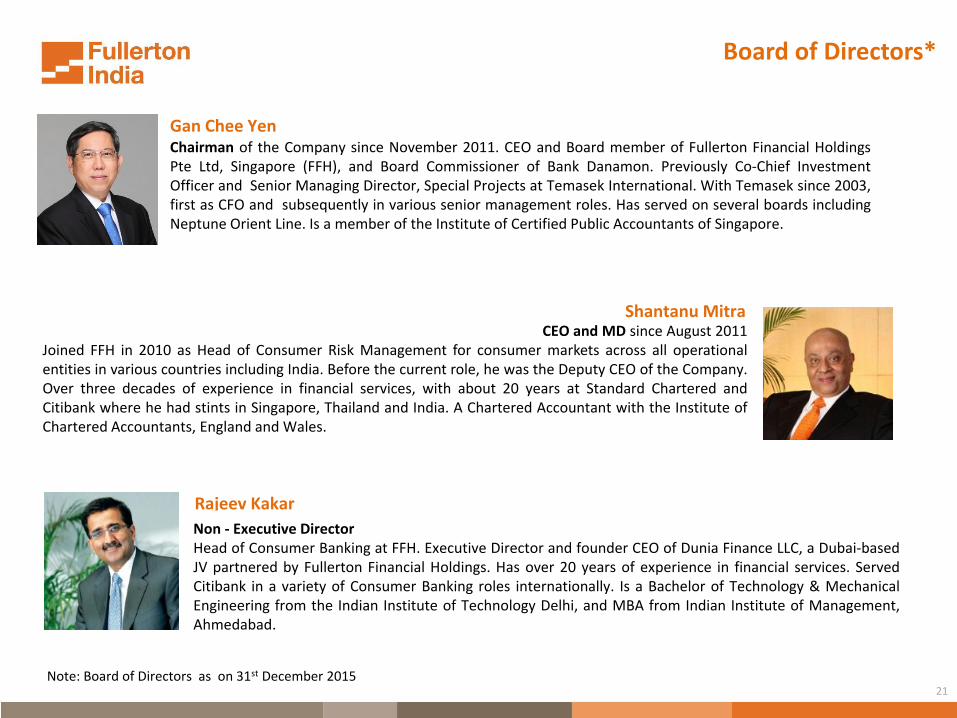

Shantanu MitraCEO and MD since August 2011

Joined FFH in 2010 as Head of Consumer Risk Management for consumer markets across all operationalentities in various countries including India. Before the current role, he was the Deputy CEO of the Company.Over three decades of experience in financial services, with about 20 years at Standard Chartered andCitibank where he had stints in Singapore, Thailand and India. A Chartered Accountant with the Institute ofChartered Accountants, England and Wales.

Gan Chee YenChairman of the Company since November 2011. CEO and Board member of Fullerton Financial HoldingsPte Ltd, Singapore (FFH), and Board Commissioner of Bank Danamon. Previously Co-Chief InvestmentOfficer and Senior Managing Director, Special Projects at Temasek International. With Temasek since 2003,first as CFO and subsequently in various senior management roles. Has served on several boards includingNeptune Orient Line. Is a member of the Institute of Certified Public Accountants of Singapore.

Rajeev Kakar

Non - Executive DirectorHead of Consumer Banking at FFH. Executive Director and founder CEO of Dunia Finance LLC, a Dubai-basedJV partnered by Fullerton Financial Holdings. Has over 20 years of experience in financial services. ServedCitibank in a variety of Consumer Banking roles internationally. Is a Bachelor of Technology & MechanicalEngineering from the Indian Institute of Technology Delhi, and MBA from Indian Institute of Management,Ahmedabad.

Board of Directors*

21Note: Board of Directors as on 31st December 2015

Kenneth Ho Tat Meng

Non - Executive DirectorMr. Kenneth Ho carries more than two decades of Consumer and Commercial Banking experience. He is agraduate in Economics from Flinders University of South Australia and a Master of Business Administrationholder from University Putra Malaysia. Currently, he is the Senor Vice President, Consumer Banking forFullerton Financial Holdings (International) Pte Ltd. Previously he was in Citibank for 10 years covering the rolesof Regional Director, Consumer Secured Lending of Citibank Asia Pacific regional office and in CitibankSingapore Ptd Ltd as Head of Autobusiness and Citibusiness (Commercial Banking). Prior to joining Citibank , healso had substantial exposure in EON Bank Berhad, Malaysia, including managing the entire Auto Loansbusiness (national) and covering numerous roles in Branch Banking as well.

Board of Directors*

Renu ChalluIndependent Director

Ms. Renu Challu is a seasoned banker with decades of experience in Commercial and Investment Banking. Shewas with the State Bank of India (SBI) for more than 38 years serving in variety of positions. Some of thepositions held at SBI include President & COO at SBI Capital Markets, MD & CEO at SBI DFHI, MD of State Bankof Hyderabad and Deputy MD, Corporate Strategy and New Business Development. She is on the Board ofmany other companies and is a partner in 5th Bridge Data Technologies LLP.

Independent Director Ms. Pillai, a 1972 batch IAS officer held a number of senior positions in the Government of India and the StateGovernment of Kerala for 40 years. She handled the Industry and Finance portfolios for nearly twenty years. Inthe Centre, she worked in the Ministries of Industry, Corporate Affairs, Labour and Employment .She contributednotably to reforms in Industrial and Foreign Direct Investment policies as also in formulating the National SkillDevelopment Policy. In Kerala, as Principal Secretary Finance she worked to achieve enhanced developedoutcomes, coupled with efficient fiscal management. Earlier as CMD, Kerala Finance Corporation she dealt withproject financing to SMEs. Her last assignment was as Member Secretary (in the rank of Minister of State),Planning Commission, Government of India. She is currently Director on the Boards of Jubilant Life Sciences andInternational Travel House Ltd.

Sudha Pillai

22

Milan Robert Shuster

23

Independent Director Dr. Shuster, is a professional with decades of experience in the banking sector. He is currently Chairman ofthe Audit Committee at Bank Danamon Indonesia. He served at Asian Development Bank, ING Bank,National Bank of Canada, Nippon Credit Bank in various capacities. After working as the President and CEOof P. T. Bank PDFCI, he served Bank Danamon Indonesia in various capacities. He became its president andCEO and later its Independent Commissioner. He has also served many other entities in Directorial andadvisory capacities. He holds Ph.D. in International Economics and Law from University of Oxford. He alsoholds Master of Law from London School of Economics and Bachelor of Business Administration from IveyBusiness School.

Board of Directors*

23

Premod ThomasIndependent Director

Mr. Thomas’s strength lies in the areas of corporate governance in a listed company environment,performance and risk management and corporate finance. He commenced his professional career with Bank ofAmerica and worked with them for twelve years specialising in risk management, corporate finance andcorporate banking. Later he joined the Tirtamas Group where he was responsible for the Group’s debt andequity fund raising and management. In 1998 he joined Temasek Group of companies and worked with themover two assignments. After 6 years with Temasek Group, he joined Standard Chartered Bank, Singapore as thehead of the Asia Governance. In 2009 he joined Hong Leong Group of Malaysia as a group CFO and later on hewas posted to London to manage the hotel group. He stepped down from his executive role in 2014 to pursueinterests in Advisory and NED assignments.

* Board of Directors is as on 31st Jan, 2016

24

Anand NatarajanHead of Strategy and Business Execution

Anand is the Head of Strategy and Business Execution for Fullerton India. In this role, he is responsible for the overall corporate strategy of the company and its subsidiaries covering Risk, Operations, Technology, Analytics and Digital Initiatives. Anand is a Chartered Accountant and Cost Accountant, with an MBA from the Henley Business School. He joined Fullerton India in Jan 2016 from ANZ Bank, Indonesia, where he served as Chief Operating Officer, responsible for retail, institutional, branch and credit operations, technology and infrastructure, contact centre and service, procurement and property management and enterprise-wide operational risk management. Previously, Anand was the Chief Operating Officer for Fullerton India with responsibilities of Treasury, Finance and Operations. Anand has held various leadership positions in his 23 years with Standard Chartered Bank, where he served as Head of Global Markets Operations India, Head Securities Services South Asia, Chief Operating Officer Consumer Banking, Head Country /BPO Operations and Regional Credit Officer Middle East, Pakistan and Africa and as the Chief Risk Officer for Consumer Banking, India and South Asia.

Leadership Team

Rakesh MakkarExecutive Vice President & Head – Business & Marketing

Rakesh spearheads Fullerton India's Urban and Rural business, in addition to heading the Marketing & CSR functions. He has over two decades of valuable experience including new business and brand launches while developing dynamic sales teams, product and distribution networks. Prior to joining Fullerton India, Rakesh was the Chief Distribution Officer and Management Committee member at DHFL. His earlier stints include Future Money as Chief Executive Officer, Citigroup and as a consultant for a Vietnamese Bank on consumer finance. Rakesh is a qualified national rank holder Chartered Accountant and an MBA.

Rajesh Krishnamoorthy

Chief Risk Officer

Rajesh is responsible for Enterprise Risk Management, Legal and Compliance functions in Fullerton India. A management graduate, Rajesh joined Fullerton India in September 2013 and comes with over 18 years of post-qualification experience in the financial services sector across consumer and commercial lending. Prior to Fullerton India, Rajesh was the Chief Risk Officer at Bajaj Finance Limited. His other stints include working in risk management domains at HSBC Ltd., GE Countrywide, Prime Financial and First Leasing.

Leadership Team

Ravindra RaoChief Operating Officer

Ravindra comes with 20 years of experience in Risk Management and Business function. He has been with Fullerton India since September 2011 and has headed Credit Policy & Underwriting, Collections, Fraud Risk, Operational Risk, Legal and Compliance, Mortgage and SME business. As COO, he is now responsible for Operations, Customer Service, Technology, etc. Prior to joining Fullerton India, Ravindra was heading Collections & Fraud Control for South Asia in Standard Chartered Bank. He has held senior positions at HDFC Bank, ABN Amro.

25

Swaminathan SubramanianHead- Human Resource

Swaminathan is an engineer from Jadavpur University, Kolkata and an MBA from XLRI. He joined Fullerton India in May 2013 to lead the Human Capital and Training function. Swami has over 18 years of HR experience across Asia, Africa & Middle East markets. He has held various leadership positions including Head of HR for Retail Banking, Barclays- Africa and Head of Compensation & Benefits, Standard Chartered Bank, South Asia and more recently as HR lead for Corporate & Investment Banking Operations & Technology with JP Morgan Chase, India.

Ajay is a Chartered Accountant with over 18 years' experience in audit & financial services. Starting his career with A. F. Fergusons & Co, he moved to CitiFinancial as part of the start-up team to launch their retail finance business in India. At Citi Financial he handled the risk and operations functions for 3 years and later took over as a Regional Business Head. After 8 years at Citi Financial, he joined Fullerton India in 2005 as part of the start-up team. Ajay is now Head - Sales and Distribution for the Retail Business and oversees distribution of the company's key products of Personal Loans, two-wheeler & used car loans and mortgages.

Ajay PareekExecutive Vice President - Sales & Product, Urban Business

Leadership Team

Deepak is an Electrical Engineer with a Masters in Management from Jamnalal Bajaj Institute, Mumbai. In his work experience of 18 years he has handled diverse roles including Quality Assurance, Sales and Distribution, Debt Collections, Operational Risk and Audit. After successful stints at Cable Corporation, HCL Infosystems and Citibank he joined Fullerton India in 2007 as Head – Retail Collections. Deepak manages Internal Audit at Fullerton India.

Deepak PatkarHead, Internal Audit

26

ContactFullerton India Credit Company Ltd.Floor 6, B Wing, Supreme IT Park,Powai,Mumbai 400 076INDIA

Phone: +91 22 6749 1234

www.fullertonindia.com27

Your Preferred

Financial Partner

28

Glossary

Abbreviation Expanded Form

AUM Assets Under Management

Bio Billion

CAGR Compound Annual Growth Rate

CEO Chief Executive Officer

CIBIL Credit Information Bureau (India) Ltd

CP Commercial Paper

CSR Corporate Social Responsibility

CV Commercial Vehicle

CAR Capital Adequacy Ratio

FICC Fullerton India Credit Company

FY Financial Year

INR Indian Currency

KYC Know Your Customer

LAP Loan against property

Mio Million

NCD Non-convertible Debenture

NPA Non Performing assets

ORM Operational Risk Management

PBT Profit Before Tax

PL Personal Loan

RoA Return on Assets

RoE Return on Equity

SME Small and Medium Scale Enterprises

SAP Standard asset provision

YoY Year on Year

YTD Year Till date

ALCO Asset-Liability Committee

29