Corporate Plan - Airports Company South Africa Final Corporate Plan...Corporate Plan April 2014...

26

Corporate Plan April 2014 Presentation

Transcript of Corporate Plan - Airports Company South Africa Final Corporate Plan...Corporate Plan April 2014...

Corporate Plan

April 2014 Presentation

Table of contents

1 20 Years - Timeline

2 Governance Structure

3 Core Outcomes

4 Strategic Thrusts

5 Operating Environment

6 Strategic Risks

7 Traffic Volumes

8 Economic Regulation Update

9 Financial Highlights

10 Capex

11 Funding Plan

12 Key Focus Areas

13 Conclusion

20 years of thinking forward and

embracing change

1993 1994-1998 1999-2005 2006-2008 2009 2010 2011 2012 2013

3

• 23 July 1993, the

company officially

established and 9

airports transferred to

the Company

• Airports Company

South Africa’s sole

shareholder is the

state, through the

NDoT

• Commenced

operations in 1994

• Opening of O.R.

Tambo International

Airport Central

Terminal Building

• Announcement of the

review of the

Economic Regulation

Framework

• Opening of O.R.

Tambo International

Airport Domestic

Terminal

• PIC acquires Adrisa

which owns 20% of

Airports Company

South Africa from

Aeroporti di Roma

• Adoption of Early

Debt Repayment

Strategy resulting in

R3bn being set aside

to repay debt

• New Economic

Regulatory

Committee appointed

• Government sells 25.4% of

Airports Company South Africa’s

shares to Aeroporti di Roma,

various empowerment groups,

management and employees

• Airport operator in consortium

that was awarded Mumbai

International Airport operating

concession and acquired a 10%

shareholding

• R12bn DMTN programme

registered and R2bn debut bond

issued

• Opening of international pier at

O.R. Tambo International Airport

Domestic Terminal

• Opening of Cape Town

International Airport Central

Terminal

• Completion of King Shaka

International Airport and

successful move from Durban

International Airport to new site in

just 6 hours

• Successful facilitation of the 2010

FIFA World Cup

• Updated the DMTN programme

to R30bn

• Airport operator in consortium

that was awarded the Guarulhos

International Airport operating

concession and acquired a 5.1%

shareholding

• Sale of Durban International

Airport site

• The company’s airports continue

to be recognised as leading

airports in Africa through

numerous service excellence

awards by the Airports Council

International

9th

1st

Achievements: 20 years Airport Service Awards

4

Africa’s Leading Airport

1998 1999 2000 2001 2006 2007 2008 2009 2010 2011 2012 2013

OR Tambo

International

Airport

Cape Town

International

Airport

King Shaka International

Airport / Durban

International Airport

George

Airport

Port Elizabeth

International

Airport

East

London

Airport

Upington

International

Airport

Africa Airport of the

Year Award

Airport Council International

Awards – by Region : Africa

Best Airport

Best Improved Airport

Best Regional Airport

Best Improved Regional Airport

Hall of Fame

Skytrax

Worlds Top 100 Airports

Worlds Best Domestic Airport

Worlds Best Airport by Passenger Numbers

Under 5 million

5 – 10 million

10 -20 million

28th 22nd 26th

3rd

1st

Airport Cargo Excellence –

2013 African Airport of the Yea

Governance Structure

Shareholders

Airports Company South Africa Board of Directors

Audit & Risk Remuneration &

Nomination

Treasury & Economic Regulation

Commercial Board

Social & Ethics Executive Committee

Managing Director

(Bongani Maseko)

Financial Director

(Maureen Manyama-Matome)

5

Leadership Structure

6

CEO

Governance & Assurance

Compliance. Legal & Risk

COO

HR Chief

Information Officer

Airports (Corp Office Today - Airport Ops, Aviation Services, Commercial, Support Services)

Regional Airports King Shaka International

Airport

Cape Town International

Airport

O.R. Tambo International

Airport

Corporate Affairs (Today - Brand, Communications,

Marketing, Stakeholder Management, CSI)

CFO

Group Investments Officer

(Subsidiaries, Concessions, 'Propco', 'AMS')

Company Secretary

Internal Audit

Core Outcomes

7

Sustainability

Growth

Efficiency and cost management

Relevance

Business Performance excellence

7 Strategic Thrusts

8

7 S

trate

gic

th

rusts

Deliver shareholder value

Build win-win partnerships with all stakeholders

Identifying and securing new business

Strengthening business excellence

Acceleration of sustainability and transformation programmes

Facilitation of economic regulatory legislation and funding framework

Managing and developing a high performing and engaged team

Operating Environment

9

Economic climate

Economic regulation

Aviation Industry conditions

Airport transport policy

Credit rating

Stakeholder relations

(management)

Government Objectives

Strategic Risks

1. Real GDP growth;

2. Resilience of Airlines - fuel price and foreign exchange affects airlines more,

3. Interest rates

4. Finalization of a predictable and transparent economic regulation;

5. Succession planning;

6. National transport master plan (Natmap) and aviation policies;

7. Rate of economic recovery;

8. Fitch rating impact on cost of capital; and

9. Security of energy supply (fuel and electricity)

10

Traffic Volumes: Assumptions

-

5

10

15

20

25

30

2011A 2012A 2013A 2014F 2015E 2016E 2017E 2018E 2019E 2020E 2021E 2022E 2023E 2024E 2025E

Mil

lio

ns

Departing Passengers

Domestic International Regional Unscheduled

0

50

100

150

200

250

300

350

400

2011A 2012A 2013A 2014F 2015E 2016E 2017E 2018E 2019E 2020E 2021E 2022E 2023E 2024E 2025E

Th

ou

sa

nd

s

Aircraft Landings

Domestic International Regional Unscheduled

11

Economic Regulation

May 2011 amended

permission

Current 10 year investment plan

Capex claw-back and smoothing assumed

2012/13 2013/14 2014/15 2015/16 2016/17 2017/18 2018/19 2019/20

Promulgated tariff increase 30.6% 5.5% 5.6%

Indicative tariff increase

based on current approach

(12.0%) - - - -

Steering Committee of the Economic Regulatory Review

• Draft amendment bill scheduled to go before parliament during the 2014 calendar year

→ Merit-based appeal mechanism and enabling regulations remain the items to be agreed on

• Good progress on agreement of funding model

→ A number of aspects dependent on regulatory capacity, i.e. full-time regulatory body

Permission Application 2016 – 2020

• Submission due by 30 June 2014

• Draft approach document issued in November 2013 – awaiting final approach document

→ Positive developments such as hybrid till for non-aviation land (property development strategy) and share

investments (international strategy)

→ No pre-funding allowances expected in final approach document

• Much improved consultation process delivering on capex programme revisions and agreements on major

infrastructure developments. This is expected to reduce regulatory discretion.

12

CE v5.5 13

Financial Highlights

2015B 2016E 2017E

Departing Passengers 17.8m 18.4m 19.0m

Aircraft Landings 260 644 262 434 270 513

Tariff Increase on Previous Year 5.6% -12.0% 0%

Revenue R7.6bn R7.4bn R7.9bn

EBITDA R4.6bn R4.2bn R4.4bn

Net Profit R1.3bn R1.1bn R1.2bn

Capex R1.3bn R3.1bn R3.2bn

Return on Capital Employed

(Target 11.2 - 10.3%)

9.7%

8.0%

7.6%

Net Debt / EBITDA

(Target <3.0x)

2.1x

2.4x 2.4x

EBITDA Interest Cover

(Target >3.1x)

3.3x

3.6x 4.0x

13

10 Year Plan Revenue Analysis & EBITDA

48%

41% 36% 36% 35%

39% 40% 41% 42% 44% 44% 44% 44% 45% 45%

0%

10%

20%

30%

40%

50%

60%

-

2,000

4,000

6,000

8,000

10,000

12,000

14,000

16,000

2011A 2012A 2013A 2014F 2015B 2016E 2017E 2018E 2019E 2020E 2021E 2022E 2023E 2024E 2025E

Revenue

Non-aeronautical revenue Aeronautical revenue Non-aeronautical revenue %

56%

63% 64% 60% 60%

56% 56% 56% 55% 52%

57% 58% 59% 60% 61%

0%

10%

20%

30%

40%

50%

60%

70%

-

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

9,000

2011A 2012A 2013A 2014F 2015B 2016E 2017E 2018E 2019E 2020E 2021E 2022E 2023E 2024E 2025E

EBITDA & EBITDA margin

EBITDA EBITDA margin

14

10 Year Plan Profit & Returns

-5%

3%

15% 16% 17%

15% 15% 14%

12%

9%

14%

16%

19% 17%

15%

-10%

-5%

0%

5%

10%

15%

20%

-500

-

500

1,000

1,500

2,000

2,500

2011A 2012A 2013A 2014F 2015B 2016E 2017E 2018E 2019E 2020E 2021E 2022E 2023E 2024E 2025E

Net profit & Net profit margin

Net profit / (loss) Net profit margin

2.9%

5.3%

7.8%

9.1% 9.8%

8.1% 7.7%

7.1% 6.7%

5.9%

7.1% 7.5% 7.7% 7.5% 7.5%

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

2011A 2012A 2013A 2014F 2015B 2016E 2017E 2018E 2019E 2020E 2021E 2022E 2023E 2024E 2025E

Return on Capital Employed

Return on capital employed Regulatory WACC

15

Capital Expenditure FY 2015 - 2017

R1.3

billion

R7.7

billion

16

-

2,000

4,000

6,000

8,000

10,000

12,000

2011A 2012A 2013A 2014F 2015E 2016E 2017E 2018E 2019E 2020E 2021E 2022E 2023E 2024E 2025E

Millio

ns

Capital expenditure (incl. capitalised interest) Capital expenditure in 2013 monetary terms

10 Year Plan Capex profile

17

CTIA: Re-

alignment of

runway & T2

ORTIA:

Midfield (all)

& fuel tanks

ORTIA:

Remote

aprons

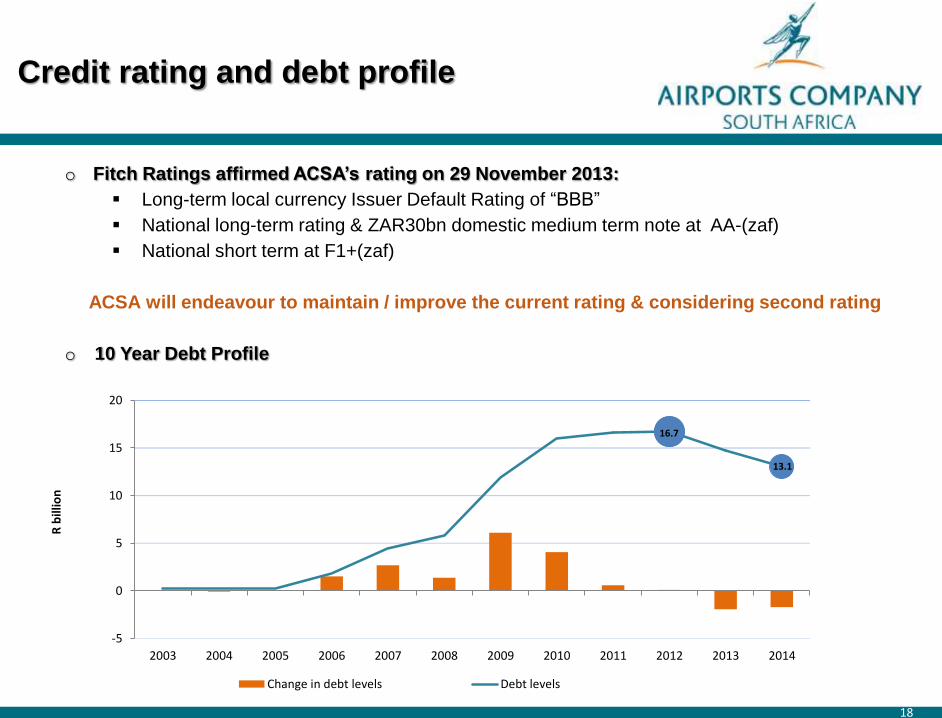

o Fitch Ratings affirmed ACSA’s rating on 29 November 2013:

Long-term local currency Issuer Default Rating of “BBB”

National long-term rating & ZAR30bn domestic medium term note at AA-(zaf)

National short term at F1+(zaf)

ACSA will endeavour to maintain / improve the current rating & considering second rating

o 10 Year Debt Profile

Credit rating and debt profile

16.7

13.1

-5

0

5

10

15

20

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

R b

illio

n

Change in debt levels Debt levels

18

Debt Book 31 March 2014

Diversified funding sources Debt composition

31 Mar 2012 31 Mar 2013 *31 Mar 2014

Total debt

consideration R16.7 bn R14.7 bn R13.1 bn

WACB 10% NACS 10% NACS 10% NACS

Gearing 60% 53% 47%

• In 2013/14 FY a total of about R2 billion mainly by repaying

• Buyback of the AIR02U (R500 million) on the 5th July 2013

• Redemption of the AIRL02 (R1.3 billion) on the 18th February 2014

19

3 Year Funding / Borrowing Plan FY 2015 - 2017

Funding Composition (Per Year)

Funding Requirements (2015E -2017E)

5 195

2 300

7 494

0

1000

2000

3000

4000

5000

6000

7000

8000

Available cash Gross debt financing Total capex

69%

31%

1 288

1 781 2 125

1 300 1 000

-500

500

1500

2500

3500

2015E 2016E 2017E

Cash Flow Debt

■ Funding up to financial year end 31 March 2015

■ No debt funding required

■ Funding up to financial year end 31 March 2016 &

2017

■ Required

– Funding R2.3 billion

■ Sources

– Domestic Debt Capital Markets (DMTN)

– Refinance AIR03 maturing 2016

– Commercial Paper

– Tap AIR02 maturing 2023

– Issue new benchmark bond

– Bank credit facilities and financing

– Development Finance Institutions (DFIs)

Debt Funding Required & Sources

20

Refinancing Strategy FY 2015

0

500

1000

1500

2000

2500

3000

3500

4000

R m

illi

on

Fixed rate bonds Inflation linked bonds Bank Loans

Floating Rate Notes DFI Loans (DBSA, INCA & AFD) Funding space

■ Investor Appetite – 2013 Road show

■ Existing Maturity Profile Gaps

■ Factors Assessed

– Time to maturity (duration),

– Trading price

– Redemption volume

– Spread above benchmark government

bond

■ Maturity Gap Areas

– 2022E (8yrs)

– 20125E (10yrs)

– 2031E (16yrs)

Debt Maturity Profile Gaps Refinancing Considerations

21

10 Year Funding / Borrowing Plan FY 2015 - 2025

Capital Expenditure

– R55 billion

New Debt Funding Requirement

– R29 billion (53% funding of capex)

Credit Ratings to be maintained at current levels as projected credit matrix are within an

investment grade credit rating

Funding Sources

– Domestic Debt Capital Market issuances through R30 billion registered DMTN

– Bank funding through facilities and loans

– Development Finance Institution financing

– Export Credit Agency (ECA) backed funding

– International bond issuances and private placements

– Project Financing

22

10 Year Plan Credit Metrics

6.1

4.1

2.9 2.6

2.1 2.4 2.4 2.8 2.9 3.2 3.0

3.3 3.7 3.7

3.1

0.0

1.0

2.0

3.0

4.0

5.0

6.0

7.0

Net Debt / EBITDA

Net debt / EBITDA Target (below this line)

62% 60% 53%

49% 43% 41% 40%

44% 44% 45% 46% 49% 52% 51%

48%

0%

10%

20%

30%

40%

50%

60%

70%

Net Debt / Capitalisation

Net debt / Capitalisation Target (below this line)

1.7

2.2

2.9 3.3 3.4

3.6 4.0

3.7

3.1 3.0 3.3 3.1

2.8 2.7 2.9

0.00.51.01.52.02.53.03.54.04.5

EBITDA Interest Cover

EBITDA interest cover Target (above this line)

23

Key focus areas

FY 2015

24

Deliver shareholder value

Issue of Minority Shareholders

Finalise model to secure new business in Africa and other emerging markets

Unlock value potential in land at ACSA airports

Acceleration of sustainability and transformation programmes

Facilitation of economic regulatory legislation and funding framework

Managing and developing a high performing and engaged team

Key focus areas FY 2015 - 2017

o Strengthened the stakeholder engagement process;

o Continued admiration of passengers and airlines for its customer focussed services

and facilities;

o Delivered on the imperatives of the government agenda (transformation and

sustainability programmes);

o Job Creation

o Delivered on the BBBEE codes of good practice

o Contributed to economic growth;

o Established ‘ring-fenced’ property development and international investment

businesses;

o Achieved a respected presence in emerging markets;

o Optimised its infrastructure and efficient processes;

o Enabled information technology platforms; and

o Developed a transformed workforce that is energetic.

25

Conclusion

1. Key risks for delivering this plan remain

o GDP growth; and

o economic regulation

2. The following ever changing economic elements to be closely monitored:

o fuel price;

o interest rates;

o foreign exchange rates; and

o cost of borrowing

3. The implementation of new capacity infrastructure dependant on favourable

economic conditions

4. Stakeholder management with industry, economic regulator and Investors will be

maintained

5. ACSA will maintain its course to meet shareholder expectations

26