CORPORATE OVERVIEW - Jefferies - The Global · PDF file · 2014-08-19CORPORATE...

32

Westport Innovations Inc. CORPORATE OVERVIEW stock symbols market capitalization TSX NASDAQ CAD USD WPT WPRT $1.1 billion $1.0 billion 1

Transcript of CORPORATE OVERVIEW - Jefferies - The Global · PDF file · 2014-08-19CORPORATE...

Westport Innovations Inc.

CORPORATE

OVERVIEW

stock symbols market capitalization

TSX NASDAQ CAD USD

WPT WPRT $1.1 billion $1.0 billion

1

» This presentation contains forward-looking statements that are based on the beliefs of

Westport’s management and reflect Westport’s current expectations. Investors are cautioned

that all forward-looking statements involve risks and uncertainties that could cause actual

results to differ materially from those expressed in these forward-looking statements,

including, without limitation, Westport’s ability to develop viable fuel systems; Westport’s

ability to provide the capital required for research, product development, operations, and

marketing; product development, production and commercial launch delays; changing

environmental regulations; Westport’s ability to attract and retain key personal and business

partners; competition from conventional diesel fuelled engines; and Westport’s ability to

protect its intellectual property. These factors should be considered carefully and investors

should not rely on any forward-looking statements. Investors are encouraged to review

Management’s Discussion and Analysis and the Risk Factors section in Westport’s most

recently filed Annual Information Form and filings with securities regulators for a more

complete discussion of factors that could affect Westport’s future performance. We undertake

no obligation to update or revise any forward-looking statements, whether as a result of new

information, future events or otherwise, except as required by law.

» All figures are in U.S. dollars unless otherwise stated.

Forward Looking Statements

2

» Energy transitions are enormously difficult

» Natural gas is emerging as the first significant new transportation fuel in a century

Driving a Shift to Natural Gas as a Transportation Fuel

ENERGY

• Gas exploration & production• Distribution & utilities• Fuel station owners/operators• Renewable fuels

TECHNOLOGY

• Market-spanning experience• Expansive IP portfolio• Capital light business models

TRANSPORTATION

• Engine & vehicle OEMs• Fleet operators• Shippers, transportation users• Consumers

3

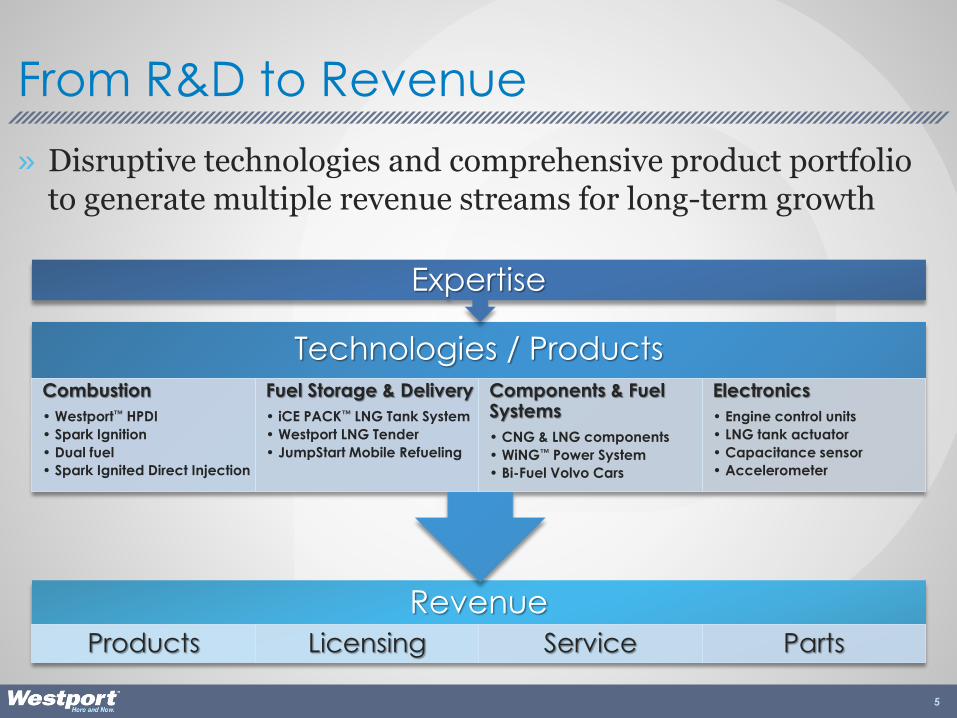

Technologies / Products

CombustionFuel Storage &

DeliveryComponents & Fuel Systems

Electronics

Expertise

Design engineering

OEM process alignment

Supply chain management

Testing and analysis

Precision manufacturing

Vehicle integration

Intellectual Property

Why Westport? Integrated Know-How

» Westport translates unique IP and expertise into an entire

spectrum of technologies and products

4

Revenue

Products Licensing Service Parts

Technologies / ProductsCombustion

• Westport™ HPDI

• Spark Ignition

• Dual fuel

• Spark Ignited Direct Injection

Fuel Storage & Delivery

• iCE PACK™ LNG Tank System

• Westport LNG Tender

• JumpStart Mobile Refueling

Components & Fuel Systems

• CNG & LNG components

• WiNG™ Power System

• Bi-Fuel Volvo Cars

Electronics

• Engine control units

• LNG tank actuator

• Capacitance sensor

• Accelerometer

Expertise

From R&D to Revenue

» Disruptive technologies and comprehensive product portfolio to generate multiple revenue streams for long-term growth

5

Financial Summary

($ in millions) CY2011 CY2012 CY2013YTD Jun 30

2014

Westport Revenue $ 100.8 $ 155.6 $ 164.0 $ 82.0

CWI Revenue 163.9 198.0 310.7 159.6

WWI Revenue 109.8 272.1 466.6 246.4

Adjusted EBITDA

Operating Business

Units (36.0) (40.3) (34.6) (0.6)

Corporate &

Technology

Investments (22.5) (42.2) (75.7) (39.0)

Westport’s Share of

Income from the JVs 17.1 16.2 13.4 0.7

Total (41.4) (66.3) (96.9) (38.9)

Consolidated including Corporate & Technology Adjusted EBITDA positive by end of 2015

Corporate & Technology

Investments for new products developed

with Volvo, Caterpillar, Weichai,

Delphi and others

Full Year Operating Business Units to be

Adjusted EBITDA positive by end of

2014

6

1. Natural gas increasingly visible as a global transportation fuel

2. Westport is the key technology provider for OEM natural gas engine

and vehicle systems with by far the largest patent position and experience

in this area.

3. Joint ventures in China and the US are the overwhelmingly dominant

engine suppliers in these markets; combined sales CAGR of 69%

2010-2013.

4. Westport invested over $239 million since 2012 in new collaborations

with global OEMs for products with Volvo, Caterpillar, Weichai, Delphi

to be delivered 2015-2017.

5. 2013 saw Westport reposition from market creation investments to

product sales. Forecast full year operating business units positive

Adjusted EBITDA by end of 2014.

7

Investment Highlights

MACRO PERSPECTIVE

» Widespread availability of low cost natural gas (as a commodity) vs.

expensive oil is driving the first new global fuel for transportation in a century

» Adoption will be driven first by high-fuel-use fleets and transportation users

seeking lower costs—not consumers

» OEMs are now engaging; this will shift the market from aftermarket

conversion to OEM factory-built vehicles

» Emerging infrastructure participants

8

Stability of Fuel Price Differential is Driving Confidence at Fleets

0.00

0.50

1.00

1.50

2.00

2.50

3.00

3.50

4.00

4.50

2010 2015 2020 2025 2030

Pri

ce

of

cru

de

oil [

U.S

. $

/bb

l]

Price History of Diesel Fuel & CNG for Vehicles,

with EIA Projections

Actual Diesel fuel price [$/gal] Forecast Diesel fuel price [$/gal]

Actual CNG fuel price [$/DGE] Forecast CNG fuel price [$/DGE]

9

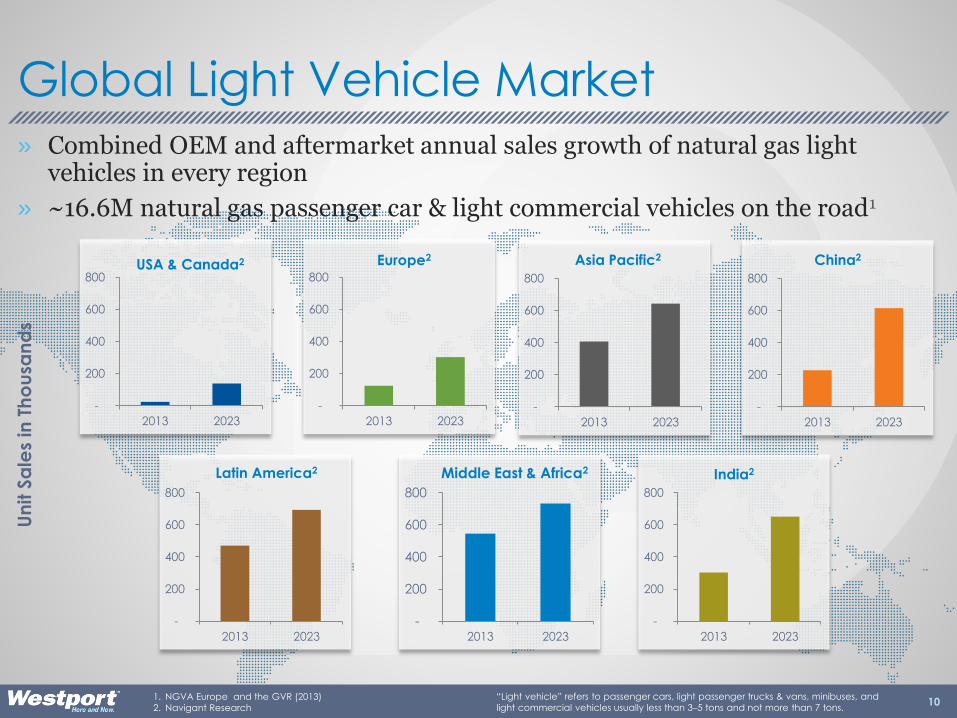

Global Light Vehicle Market

“Light vehicle” refers to passenger cars, light passenger trucks & vans, minibuses, and

light commercial vehicles usually less than 3–5 tons and not more than 7 tons.

» Combined OEM and aftermarket annual sales growth of natural gas light vehicles in every region

» ~16.6M natural gas passenger car & light commercial vehicles on the road1

1. NGVA Europe and the GVR (2013)

2. Navigant Research

-

200

400

600

800

2013 2023

USA & Canada2

-

200

400

600

800

2013 2023

Europe2

-

200

400

600

800

2013 2023

China2

-

200

400

600

800

2013 2023

India2

-

200

400

600

800

2013 2023

Latin America2

-

200

400

600

800

2013 2023

Middle East & Africa2

-

200

400

600

800

2013 2023

Asia Pacific2

Un

it S

ale

s in

Th

ou

san

ds

10

Global Markets Emerging in Every Region

1. NGVA Europe and the GVR (2013)

-

1,000

2,000

3,000

4,000

5,000

6,000

2007 2013

USA & Canada1

-

1,000

2,000

3,000

4,000

5,000

6,000

2007 2013

Europe1

-

1,000

2,000

3,000

4,000

5,000

6,000

2007 2013

China1

40%CAGR

-

1,000

2,000

3,000

4,000

5,000

6,000

2007 2013

India1

-

1,000

2,000

3,000

4,000

5,000

6,000

2007 2013

Latin America1

-

1,000

2,000

3,000

4,000

5,000

6,000

2007 2013

Middle East & Africa1

-

1,000

2,000

3,000

4,000

5,000

6,000

2007 2013

Asia Pacific1

Number of CNG & LNG Stations

11

» Majority of natural gas vehicles (NGVs) to date have been “aftermarket” conversions

delivered by third parties

» Next generation NGV OEM vehicles will be superior performance and customer

value; Westport positioned to be the dominant specialist in commercial vehicle

sector

The NGV Market is Evolving Quickly TE

CH

NO

LOG

Y

LOW

HIGH

HIGH$ / VEHICLE

MarketTransition

Components & Aftermarket(majority today)

OEM Product(fully engineered, certified)

12

0%

5%

10%

15%

20%

25%

30%

35%

40%

2012 2013 2014 2015 2016 2017 2018 2019 2020

Frost & Sullivan – High

Frost & Sullivan – Reference

Frost & Sullivan – Conservative

NPC – Reference Oil mid point

ACT Research

ACT Research1

(8 yr. CAGR 43%)

NPC2

(8 yr. CAGR 53%)

<1,700units4

>3,500units4

3–5%(~6,000–10,000 units)

Westport Analysis – Actuals

Westport – Estimated range

Urban Commercial Fleets,Truck Market in North America

Market Share of New Class 7 & 8 Natural Gas Trucks(NPC with approximate correction from VMT to vehicle units)

1. Act Research Future of Natural Gas Engines August 20122. NPC Advancing Technology, Reference Case, August

2012

3. Frost & Sullivan Strategic Outlook Truck Market 20134. Westport Analysis 13

Significant Off Road Opportunities

RAIL

MARINE

1. Morgan Stanley/Parker Bay, Westport analysis

2. UN Energy Statistics Database 2008

3. Burlington Northern 2008 Annual Report

4. Parker Bay Mobile Mining Equipment Database 2012,

Westport Analysis

5. Baker Hughes Rotary Rig Count Report, Westport analysis

6. Diesel Locomotives – Global Market Trends 2011 by SCI Verkehr GmbH, Westport analysis

7. Diesel and Gas Turbine Magazine 2011 Marine Propulsion Order Survey, Westport analysis

8. Zeus Intelligence

MINING

EXPLORATION & PRODUCTION

TARGET VEHICLES OPPORTUNITY WORLDWIDE UNITS

mine haul trucksAlmost 2 billion gallons of diesel consumed annually by the top 10 mining companies operating worldwide1

19,411 engine units4

(large mining trucks >127 ton capacity)

drill rigs andfrac pumps

Land-based rigs represent 500 million to 850 million diesel gallons per year8

13,890 engine units5

(drill rigs &frac pumps)

diesel mainline freight

locomotives

diesel passenger locomotives

Rail industry consumes 9bn gal of diesel fuel annually, half of this in North America2

Fuel represents approximately 23% of US railroad operating costs3

50,594 engine units6

(mainline locomotives)

ferries,tugboats,

PSVs,work, andcrew boats

Marine industry consumes 13bn gal of diesel fuel/year2

Emissions reduction in sensitive coastal and inland waterways are a priority

Some examples of LNG ferries and platform support vessels (PSV) in Scandinavia, but no widespreadadoption yet

25,000 engine units7

(small vessels)

14

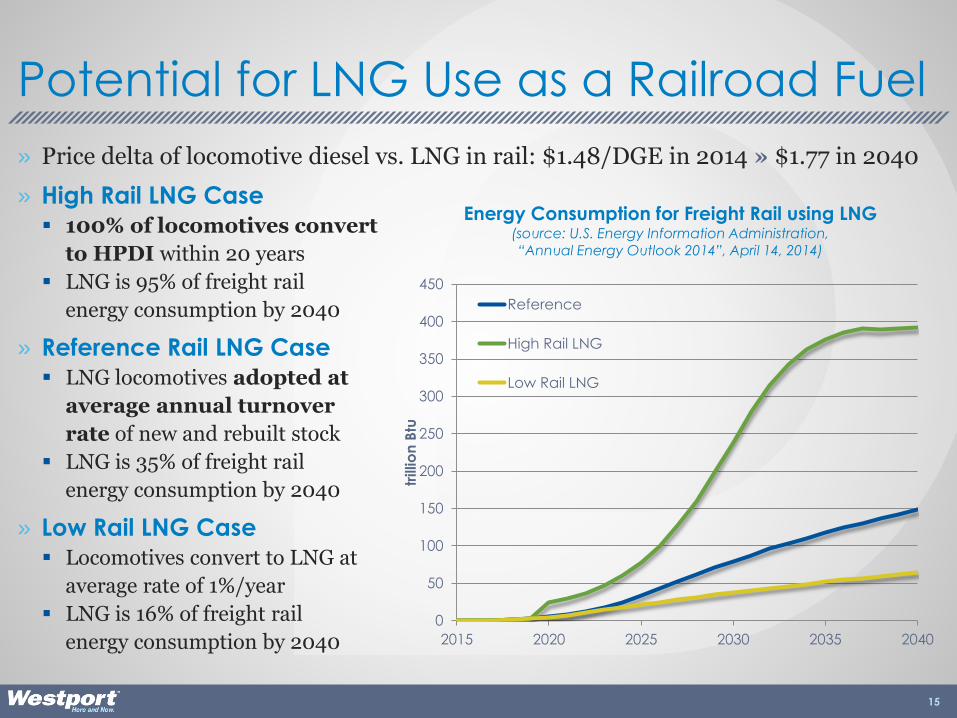

» Price delta of locomotive diesel vs. LNG in rail: $1.48/DGE in 2014 » $1.77 in 2040

» High Rail LNG Case

100% of locomotives convert

to HPDI within 20 years

LNG is 95% of freight rail

energy consumption by 2040

» Reference Rail LNG Case

LNG locomotives adopted at

average annual turnover

rate of new and rebuilt stock

LNG is 35% of freight rail

energy consumption by 2040

» Low Rail LNG Case

Locomotives convert to LNG at

average rate of 1%/year

LNG is 16% of freight rail

energy consumption by 2040

Potential for LNG Use as a Railroad Fuel

0

50

100

150

200

250

300

350

400

450

2015 2020 2025 2030 2035 2040

trillio

n B

tu

Energy Consumption for Freight Rail using LNG(source: U.S. Energy Information Administration,

“Annual Energy Outlook 2014”, April 14, 2014)

Reference

High Rail LNG

Low Rail LNG

15

TECHNOLOGIES / PRODUCTS

» Intellectual property leader

» Individual precision manufactured components up to

fully engineered complete systems for OEMs

16

» Originated at University of British

Columbia

» Strong global patent portfolio pivotal to

market leading position with OEMs

» Worldwide, Westport and its affiliates

have filed over 825 patent applications

Strong Intellectual Property Heritage Positions Westport as the Global Leader

* As of February 24, 2014 and based on the patent search results of publicly available data within the International Patent Classification F02, meeting the search term criteria: one of ("engine" or "combustion" or "injector" or "injection valve") and ("natural gas" or "methane" or "gaseous fuel") and in the claims, not ("fuel cell" or "turbine"). This chart includes issued or granted patents from: Argentina, Australia, Austria, Belgium, Brazil, Bulgaria, Canada, Ceuta and Melilla, China, Czech Republic, Denmark, European Patent Office Grants, Finland, France, Georgia, Germany, Greece, Hong Kong, Hungary, India, Ireland, Italy, Japan, Latvia, Malaysia, Mexico, Moldova, Monaco, Netherlands, OAPI grants, Philippines, Poland, Portugal, Romania, Russian Federation, Serbia, Singapore, Slovakia, Slovenia, South Africa, South Korea, Spain, Sweden, Switzerland, Taiwan, Tajikistan, Turkey, UK, Ukraine, USA, USSR, Yugoslavia, and pending published patent applications from: Canada, China, the European Patent Office, USA, and the World Intellectual Property Office.

50

62

65

82

85

99

102

154

201

327

Bosch

Cummins

GM

Honda

Toyota

Siemens

GE

Ford

CAT

Westport

Top 10 Companies with

Natural Gas Engine Related Patents*

Combustion

41%Fuel Storage

& Delivery

31%

Components

& Fuel

Systems

21%

Electronics

7%

Westport Patent Portfolio

Technology Breakdown

17

Westport Technology & Applications

Heavy-Duty & High Horsepower Applications Medium-Duty Applications

Bi-Fuel Vehicles Spark IgnitedDirect Injection

Advanced Dual Fuel Vehicles

18

APPLICATION

ENGINE

DISPLACEMENT FUEL / YEAR MILEAGE

FUEL

CHOICE CONSIDERATIONS

Large marineup to

25,000 Lup to 30M L

(7.9M gallons) LNG

Off-highway• locomotive• mine haul• medium marine

20 to 150 L~1,000,000 L

(264,000 gallons) LNG

Heavy-duty

vehicles• on-highway trucks

9 to 16 L~100,000 L

(26,400 gallons)> 250

miles/day

LNG

or

CNG

• range vs. return to base

• weight of tank system vs. payload needs

• grading of terrain

• fueling time

• chassis / body style impacts

• fuel supply and price

Medium-duty

vehicles• buses• refuse haulers

5 to 9 L~40,000 L

(10,500 gallons)< 250

miles/day

Light-duty vehicles• passenger cars• lights-duty trucks

up to 7 L~5,000 L

(1,320 gallons)< 250

miles/day CNG

LNG and CNG – Customer’s Choice

19

» Scalable, asset-light business model leverages OEM partners’ infrastructure

allows us to operate globally

Operating Business Units & JVs

» Profitable business,

growing

» $91.4M TTM revenue

» Sells to over 20 global

OEMs including Fiat,

Volkswagen, the GAZ

Group, Chrysler, and

Tata Motors

» Sells to aftermarket

customers in over 60

countries

Applied Technologies

» Ford QVM commercial

trucks (Westport WiNG™);

Volvo car systems

» Westport iCE PACK™;

Westport™ JumpStart

» $72.3M TTM revenue

» Moving from 1st

generation products and

R&D culture to ROI and

profit

On-Road Systems

» Rail, mining and

industrial industry focus

» $4.0M TTM revenue

» Westport LNG Tender—

works with locomotives

from all major North

American manufacturers

» Westport™ 2.4L

industrial engine for

forklift and oilfield

applications

Off-Road Systems

» Cummins Westport

• $347.7M TTM revenue

• 3yr CAGR = 38%

• Profitable

» Weichai Westport

• $454.7M TTM revenue

• 3yr CAGR = 118%

• Profitable

JointVentures

20TTM = Trailing Twelve Months

» 2014: Major focus on US trucking

industry with goal of 3% to 5%

market penetration; new ISX12 G

engine available across the

industry

» Westport has a 50% ownership

interest in Cummins Westport

with the potential to earn more

than 50% of the income based on

meeting certain sales thresholds

Cummins Westport Summary

(millions of USD except units) 2012 2013YTD Jun 30

2014

Engines sold 6,804 10,314 4,959

Revenue $ 198.0 $ 310.7 159.6

Gross margin % 31.0% 20.7% 11.3%

Gross margin % excl.

warranty adjustments(1) 39.2% 32.5% 27.0%

Operating expenses 26.1 40.7 19.8

Segment operating

income(2) 35.3 23.5 (1.8)

Westport interest 13.2 9.4 (0.4)

Capital expenditures 0.2 0.4 0.5

Notes:

1. The decrease in CWI gross margin and operating income percentage was primarily due to warranty adjustments related to the ISL G 8.9L engine.

2. Gross margin less operating expenses

Joint Ventures

21

» Weichai Westport JV commenced July 2010; Westport has 35% interest

» Focus on improved efficiencies in JV supply chain while trying to keep up with significant growth profile

JV represents beach head creating NG market in China for other product introductions from Westport while participating in JV’s profitability

Continued Growth in China

(millions of USD except units) 2012 2013YTD Jun 30

2014

Engines sold 22,025 38,138 20,198

Revenue $ 272.1 $ 466.6 $ 246.4

Gross margin % 9.1% 8.0% 6.1%

Operating expenses 15.0 22.8 11.1

Segment operating income 9.8 14.5 4.0

Westport 35% interest 2.9 4.3 1.2

Joint Ventures

» Current priorities

Launch Westport HPDI technology in China

Sale of components to JV and other vehicle OEMs

Expand product offerings with differentiated technology

22

Advanced Vehicle Components

High pressure

CNG lines

CNGcylinder

valve

filling valve & external CNG

filling valve

CNG & LPG reducer

Fuel injection rail

CNG & LPG filter

Electronic controls

Applied Technologies

23

Whole System Solutions:Ford Trucks and Volvo Cars

» Westport WiNG™ Power System

Dedicated CNG or bi-fuel (natural gas/gasoline)

Westport is now Ford’s largest partner under the Qualified Vehicle Modifier (QVM) program

Operational efficiencies by consolidating under one roof Q1 2014

» Volvo Car

Volvo V70 wagon & Volvo V60 sportwagon

Bi-fuel: CNG/biomethane or petrol (gasoline)

Installed inside Volvo’s main production centre in Gothenburg, Sweden

Export market opportunity

On-Road Systems

24

» First deliveries underway

» High average selling price ~$800K to $1.2 million

» > 10,000 gallons LNG capacity—provides longer range than a diesel locomotive, reducing the need for LNG refuelling infrastructure and refuelling stops

» Supports one or two locomotives, reducing the capital investment required to move to LNG

Westport LNG Tender

Gas Supply Moduleproprietary cryogenic

components deliver low or high pressure fuel

LNG Storage VesselIndustry standard

40’ “Cold” LNG tank

Universal ConnectionCompatible with locomotives from leading manufacturers

Off-Road & Industrial

25

INVESTMENT OVERVIEW

» Growth strategy

» Path to profitability

» Investing in the future of natural gas technologies

» Key milestones

26

Westport Growth Strategy

» Lead New & Differentiated

Technologies Combustion & engine development Fuel storage & delivery Components & fuel systems Electronics

ex: HPDI, spark ignited, advanced dual fuel

» Expand Application

Segments Medium duty urban vehicles (buses,

refuse trucks, delivery Heavy-Duty Trucks Light duty fleets Locomotives, other off-road enginesex: GAZ , Tata, Weichai, CAT

» Increase Systems Solutions Add new OEM relationships Broaden content with current OEMs Implement vertical integration

ex: Strong relationships with top natural gas

car producers such as Volkswagen and Fiat

» Geographic Expansion Market leader in North America,

Europe, China

Target emerging markets such as India,

Russia, Africa, South America

ex: Tata, Weichai, GAZ

27

$(8.9)

$(1.6)

$1.0

$(16.0)

$(14.0)

$(12.0)

$(10.0)

$(8.0)

$(6.0)

$(4.0)

$(2.0)

-

2.00

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4

millio

ns

28

Achieved Operating Business Units Adjusted EBITDA Goal Ahead of Plan

Average $(9.4)M

2012 2013 2014

OPERATING BUSINESS UNITS ADJUSTED EBITDA

» Full year operating

business units to be

positive Adjusted

EBITDA by end of

2014

29

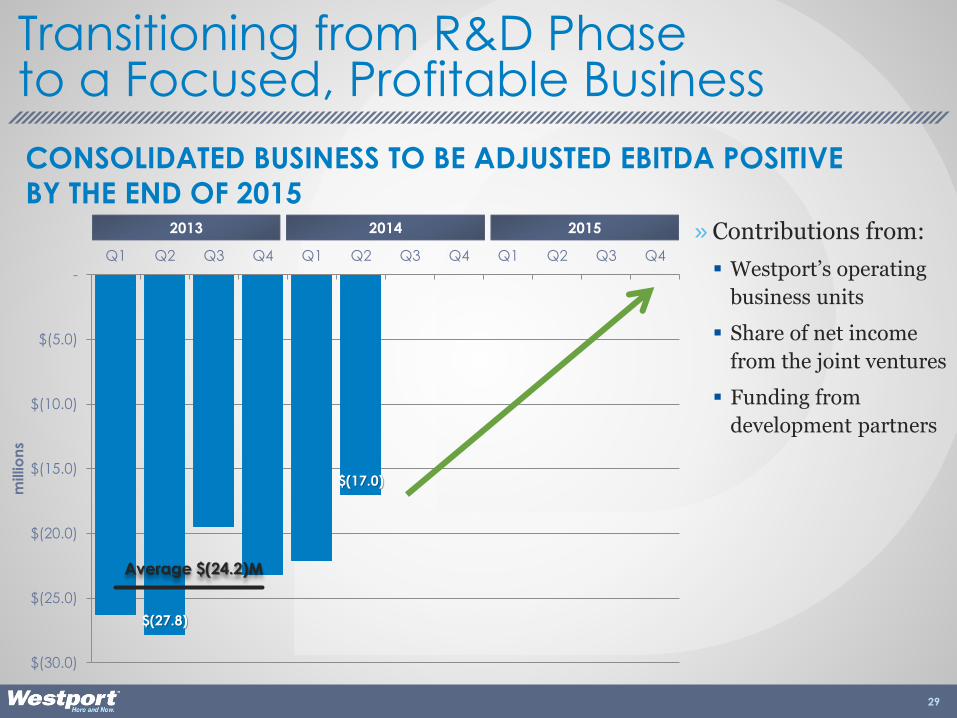

Transitioning from R&D Phaseto a Focused, Profitable Business

$(27.8)

$(17.0)

$(30.0)

$(25.0)

$(20.0)

$(15.0)

$(10.0)

$(5.0)

-

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4

millio

ns

Average $(24.2)M

CONSOLIDATED BUSINESS TO BE ADJUSTED EBITDA POSITIVE

BY THE END OF 2015

» Contributions from:

Westport’s operating

business units

Share of net income

from the joint ventures

Funding from

development partners

2013 2014 2015

» Westport has invested over $239M since 2012

Co-investing with OEMs to develop a portfolio of new natural gas vehicle technologies and related systems and components

Investments with 3 to 5 year development cycles from start of development to product sales

Careful management of future programs and capital allocation designed to deliver high margin returns

30

Investing in Next Generation Products

Off-Road

9%

Trucking

39%Automotive

27%

Advanced

Engineering

14%Capital

Expenditure

11%

Breakdown of Investments

» 2014

First full year of sales for CWI’s new truck engine, the ISX12 G

First HPDI 2.0 trucks delivered with Weichai and Shaanqi in China

First HPDI locomotive delivered with CN in Canada, first deliveries of LNG fuel tenders to CN

Profitable expansion of Ford and Volvo car business including first international sales by Volvo; new Volvo V60 product

iCE PACK LNG systems deliveries to ISX12 G customers

Full year positive Adjusted EBITDA from operations

» 2015 Westport’s consolidated business to be Adjusted EBITDA positive

by end of the year

Key Milestones

31

Strong

First-Mover

Advantage

Valuable Strategic &

Business

Alliances

Capital

Efficient &

Scalable

Business

Model

Talented & Experienced

Management

Team

westport.com

» Pure-play global leader for natural gas as a

transportation fuel

32