Corporate Income Tax (CIT) Value Added Tax (VAT) Vietnam ... · do real estate business): ......

22

1 © 2015 KPMG Limited, a Vietnamese limited liability company and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. AGENDA Corporate Income Tax (CIT) Value Added Tax (VAT) Vietnam taxes on real estate investment by foreign individuals Questions and discussion

Transcript of Corporate Income Tax (CIT) Value Added Tax (VAT) Vietnam ... · do real estate business): ......

1 © 2015 KPMG Limited, a Vietnamese limited liability company and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

AGENDA

Corporate Income Tax (CIT)

Value Added Tax (VAT)

Vietnam taxes on real estate investment by foreign individuals

Questions and discussion

CORPORATE INCOME TAX (CIT)

3 © 2015 KPMG Limited, a Vietnamese limited liability company and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

CIT – Legal basis

Circular No. 78/2014/TT-BTC effective from 02/08/2014, applicable for tax year 2014 onwards

• Circular No. 119/2014/TT-BTC effective from 01/09/2014 • Circular No. 151/2014/TT-BTC effective from 15/11/2014

Law No. 71/2014/QH13 effective from 01/01/2015

• Decree No. 12/2015/ND-CP effective from 01/01/2015 • Circular No. 96/2015/TT-BTC effective from 06/08/2015,

applicable for tax year 2015 onwards

4 © 2015 KPMG Limited, a Vietnamese limited liability company and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

CIT - Compliance

§ Standard CIT rate: 22% and reduced to 20% from 1/1/2016

§ Companies not regularly incur real estate transfer activities (i.e. not licensed to do real estate business): declare and pay CIT on each time of real estate transfer

§ Companies regularly incur real estate transfer activities (i.e. licensed to do real

estate business): pay provisional CIT on quarterly basis and finalisation at year end (optional to declare and pay CIT on each time of real estate transfer)

§ CIT declaration in case of advance payment collection in accordance with project schedule:

ü In case expenses corresponding to the advance payment can be determined:

provisional CIT payment of 22% on taxable income (revenue minus expenses)

ü In case expenses corresponding to the advance payment cannot be determined: provisional CIT payment of 1% on the advance payment

5 © 2015 KPMG Limited, a Vietnamese limited liability company and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

CIT – Revenue recognition

§ Revenue for rental fees collected in advance can be recognised under one of the two methods:

ü Spread the rental fees to the number of years of advance payment

ü One off

6 © 2015 KPMG Limited, a Vietnamese limited liability company and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

CIT – Deductible expenses

§ Non-cash payment rule for expenses from VND20 million and above

§ Statutory cap for A&P expenses is abolished

§ Interest from loans for investment in other companies is deductible (if charter capital is already fully contributed)

§ For real estate companies paying provisional CIT on % of advance payment collection in accordance with project schedule, A&P expenses (advertising, marketing, sales promotion and commission expenses) incurred before revenue recognition are allowed as deductible expenses in the first year of revenue recognition (i.e. when handing over the apartments to buyers)

7 © 2015 KPMG Limited, a Vietnamese limited liability company and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

CIT – Other income

§ Difference resulted from revaluating LUR should be:

ü Recorded in “other income” at once in case: - Capital contribution whereby the company receiving the LUR is allowed to

depreciate/allocate such LUR - Transfer upon merger, acquisition, conversion of enterprise form - Capital contribution for building houses/infrastructure for sale

ü Allocated to “other income” for maximum 10 years in case the LUR is contributed as fixed assets used for production or trading business activities whereby the company receiving the LUR are not allowed to depreciate/ allocate such LUR value

§ Income from transfer of capital which was previously contributed in form of LUR is required to be declared as income from transfer of LUR (i.e. if there is any gain, such gain is not allowed to offset with loss from other activities)

VALUE ADDED TAX (VAT)

9 © 2015 KPMG Limited, a Vietnamese limited liability company and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

VAT – Legal basis

Circular No. 219/2014/TT-BTC effective from 01/01/2014

• Circular No. 119/2014/TT-BTC effective from 01/09/2014 • Circular No. 151/2014/TT-BTC effective from 15/11/2014

Law No. 71/2014/QH13 effective from 01/01/2015

• Decree No. 12/2015/ND-CP effective from 01/01/2015 • Circular No. 26/2015/TT-BTC effective from 01/01/2015

10 © 2015 KPMG Limited, a Vietnamese limited liability company and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

• Taxable price for real estate transfer = Transfer price - Deductible LUR price

VAT – Real estate transfer

Origin of LUR Deductible LUR price

(1) LUR allocated by the State

Land use fee + compensations for land clearance in accordance with laws

(2) LUR auctioned Auctioned winning price

(3) LUR leased

Land rental + compensations for land clearance in accordance with laws

(4) LUR purchased (i) Land purchasing price at purchase + infrastructure purchasing value

Input VAT on infrastructure value that included in the deductible LUR price must not be credited

(ii) Land purchasing price at purchase

Input VAT on infrastructure may be credited

11 © 2015 KPMG Limited, a Vietnamese limited liability company and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

• Taxable price for real estate transfer = Transfer price - Deductible land price

VAT – Real estate transfer

Origin of LUR

Deductible LUR price

(5) BT contract with payment by LUR

Land price at the time of signing the BT contract If land price at signing BT contract could not be determined à Use land price determined by People’s Committee for payment of the contract

(6) Agricultural LUR acquired then transformed to residential LUR

Purchasing price of agricultural LUR + other expenses (land use fees for transforming land use purpose, PIT on behalf of the sellers)

(7) LUR contributed as capital

LUR price agreed on the capital contribution contract

Vietnam taxes on real estate investment by foreign individuals

13 © 2015 KPMG Limited, a Vietnamese limited liability company and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

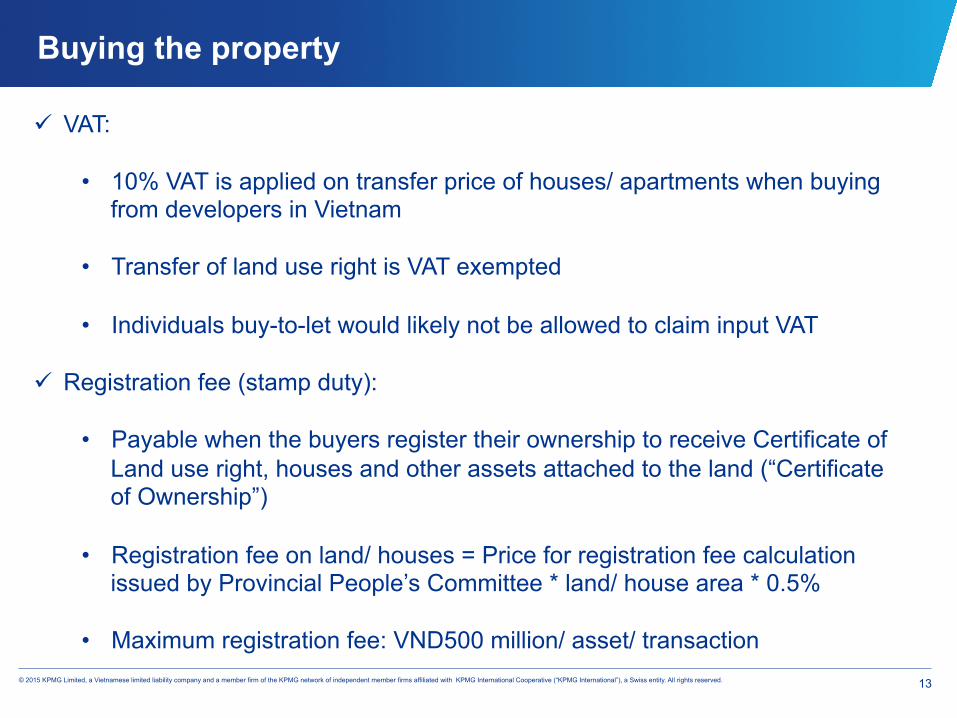

Buying the property

ü VAT:

• 10% VAT is applied on transfer price of houses/ apartments when buying from developers in Vietnam

• Transfer of land use right is VAT exempted • Individuals buy-to-let would likely not be allowed to claim input VAT

ü Registration fee (stamp duty):

• Payable when the buyers register their ownership to receive Certificate of Land use right, houses and other assets attached to the land (“Certificate of Ownership”)

• Registration fee on land/ houses = Price for registration fee calculation issued by Provincial People’s Committee * land/ house area * 0.5%

• Maximum registration fee: VND500 million/ asset/ transaction

14 © 2015 KPMG Limited, a Vietnamese limited liability company and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

Renting the property

(i) Vietnam tax residents ü Business licence tax:

• Annual tax payment of VND1 million (in case rental income is equal or more than VND1,500,000/ month)

ü VAT:

• Not applicable if rental income is or less than VND100 million/ year • VAT on rental income = total rental income * 5%

(No input VAT deduction claim)

15 © 2015 KPMG Limited, a Vietnamese limited liability company and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

Renting the property (cont.)

(i) Vietnam tax residents (cont.)

ü PIT:

• Not applicable if rental income is or less than VND100 million/ year • PIT on rental income = total rental income * 5%

(No expense deduction allowed) • No personal/ dependent deduction is allowed

16 © 2015 KPMG Limited, a Vietnamese limited liability company and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

Renting the property (cont.)

(ii) Non Vietnam tax residents ü No clear specific rules and regulations ü May likely be taxed like a resident individual lessor

17 © 2015 KPMG Limited, a Vietnamese limited liability company and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

Selling the property

ü PIT:

• 2% on gross sale proceed, including sale of asset to be formed in the future (off the plan purchase). This means tax is payable even if there is a loss on sale.

• PIT may be exempted in some cases such as − Transfer between husband and wife; parents and children including

adoptive parents and adopted children; parents-in-law and children-in-law; grandparents and grandchildren; and between siblings.

− Transfer by individuals who only have one sole residential house/ residential land use right. Note that this exemption is not applicable to transfer of asset to be formed in the future

18 © 2015 KPMG Limited, a Vietnamese limited liability company and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

Selling the property (cont.)

ü VAT:

• Individuals not carrying out registered business activities are not required to declare and pay VAT when they sell their assets, including houses, apartments and LUR

• Unclear if a property is purchased for leasing purpose, when selling it,

would VAT be applicable. Not seen in practice.

19 © 2015 KPMG Limited, a Vietnamese limited liability company and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

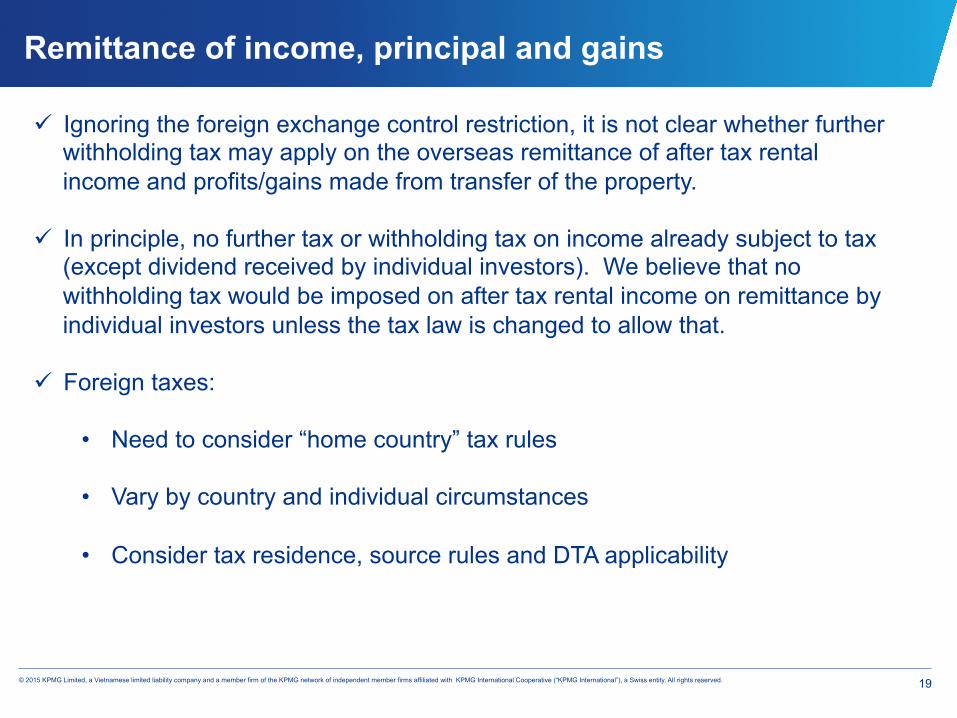

Remittance of income, principal and gains

ü Ignoring the foreign exchange control restriction, it is not clear whether further withholding tax may apply on the overseas remittance of after tax rental income and profits/gains made from transfer of the property.

ü In principle, no further tax or withholding tax on income already subject to tax

(except dividend received by individual investors). We believe that no withholding tax would be imposed on after tax rental income on remittance by individual investors unless the tax law is changed to allow that.

ü Foreign taxes:

• Need to consider “home country” tax rules • Vary by country and individual circumstances • Consider tax residence, source rules and DTA applicability

20 © 2015 KPMG Limited, a Vietnamese limited liability company and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

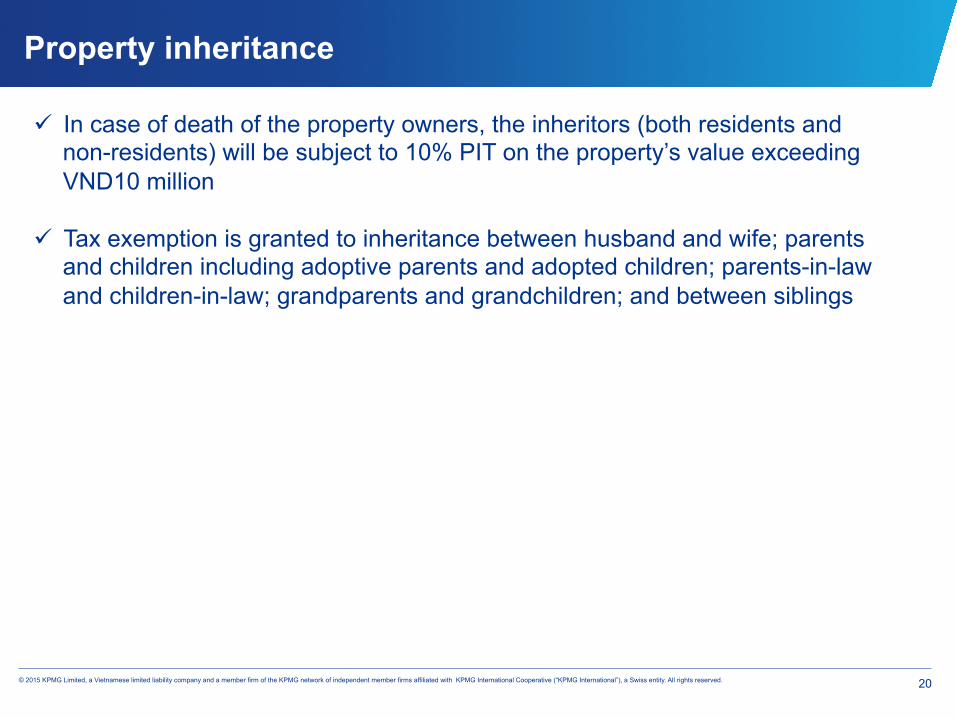

Property inheritance

ü In case of death of the property owners, the inheritors (both residents and non-residents) will be subject to 10% PIT on the property’s value exceeding VND10 million

ü Tax exemption is granted to inheritance between husband and wife; parents

and children including adoptive parents and adopted children; parents-in-law and children-in-law; grandparents and grandchildren; and between siblings

QUESTIONS AND DISCUSSION

THANK YOU

![Minimum Alternate Tax & Dividend Distribution Tax ... · Minimum Alternate Tax & Dividend Distribution Tax – Overview and Key issues. Section I ... Apollo Tyres Limited vs CIT [2002]](https://static.fdocuments.in/doc/165x107/5ac18cb77f8b9a5a4e8d443c/minimum-alternate-tax-dividend-distribution-tax-alternate-tax-dividend-distribution.jpg)

![RNM ALERT VOL.XXX MAY 2011 · 2016. 10. 28. · [Source: Mohan Meakin Limited vs. CIT (Delhi High Court)ITA No.405/2007] Sec40(a)(ia): Amounts not Deductible - Deduction of Tax at](https://static.fdocuments.in/doc/165x107/611d694511610c5b27583165/rnm-alert-volxxx-may-2016-10-28-source-mohan-meakin-limited-vs-cit-delhi.jpg)