CORPORATE DIRECTORY - Doray Minerals · MGI Perth Audit Services Pty Ltd Level 7, The Quadrant 1...

64

www.dorayminerals.com.au ACN 138 978 631 MINERALS LIMITED DORAY 2011 ANNUAL REPORT

Transcript of CORPORATE DIRECTORY - Doray Minerals · MGI Perth Audit Services Pty Ltd Level 7, The Quadrant 1...

www.dorayminerals.com.auACN 138 978 631

MINERALS LIMITED

DORAY

2011AnnuAl RepoRt

DIRECTORSChairman (Non-Executive) Mr Brett Fraser – appointed 23 October 2009

Managing Director Mr Allan Kelly – appointed 20 August 2009

Technical Director Mr Heath Hellewell – appointed 20 August 2009

Director (Non-Executive) Mr Jay Stephenson – appointed 20 August 2009

Director (Non-Executive) Mr Peter Alexander – appointed 5 May 2011

Director (Non-Executive) Mr Leigh Junk – appointed 5 May 2011

COMPANY SECRETARYMr Jay Stephenson – appointed 20 August 2009

REGISTERED OFFICELevel 4, 66 Kings Park Road

West Perth, Western Australia 6005

Telephone: 08 6141 3500

Facsimile: 08 6141 3599

PRINCIPAL PLACE OF BUSINESSLevel 3, 41-43 Ord Street

West Perth, Western Australia 6005

Telephone: 08 9226 0600

Facsimile: 08 9226 0633

Website: www.dorayminerals.com.au

AUDITORSMGI Perth Audit Services Pty Ltd

Level 7, The Quadrant

1 William Street

Perth, Western Australia 6000

Telephone: 08 9463 2463

Facsimile: 08 9463 2499

Website: www.mgiperth.com.au

HOME EXCHANGEAustralian Stock Exchange Limited

Exchange Plaza

2 The Esplanade

Perth, Western Australia 6000

ASX Code: DRM

SHARE REGISTRYComputershare Investor Services Limited

Level 2, Reserve Bank Building

45 St George’s Terrace

Perth, Western Australia 6000

Telephone: 1300 557 010, 08 9323 2000

Facsimile: 08 9323 2033

Website: www-au.computershare.com

CORPORATE DIRECTORY

CONTENTSHIGHLIGHTS 2

CHAIRMAN’S LETTER 3

MANAGING DIRECTOR’S LETTER 4

BOARD OF DIRECTORS 6

REVIEW OF OPERATIONS 8

ANDy WELL GOLD PROjECT 9

EXPLORATION 12

CORPORATE 15

RESOuRCE INVENTORy 16

TENEMENT SCHEDuLE 17

FINANCIAL REPORT 19

CORPORATE GOVERNANCE STATEMENT 20

DIRECTORS’ REPORT 24

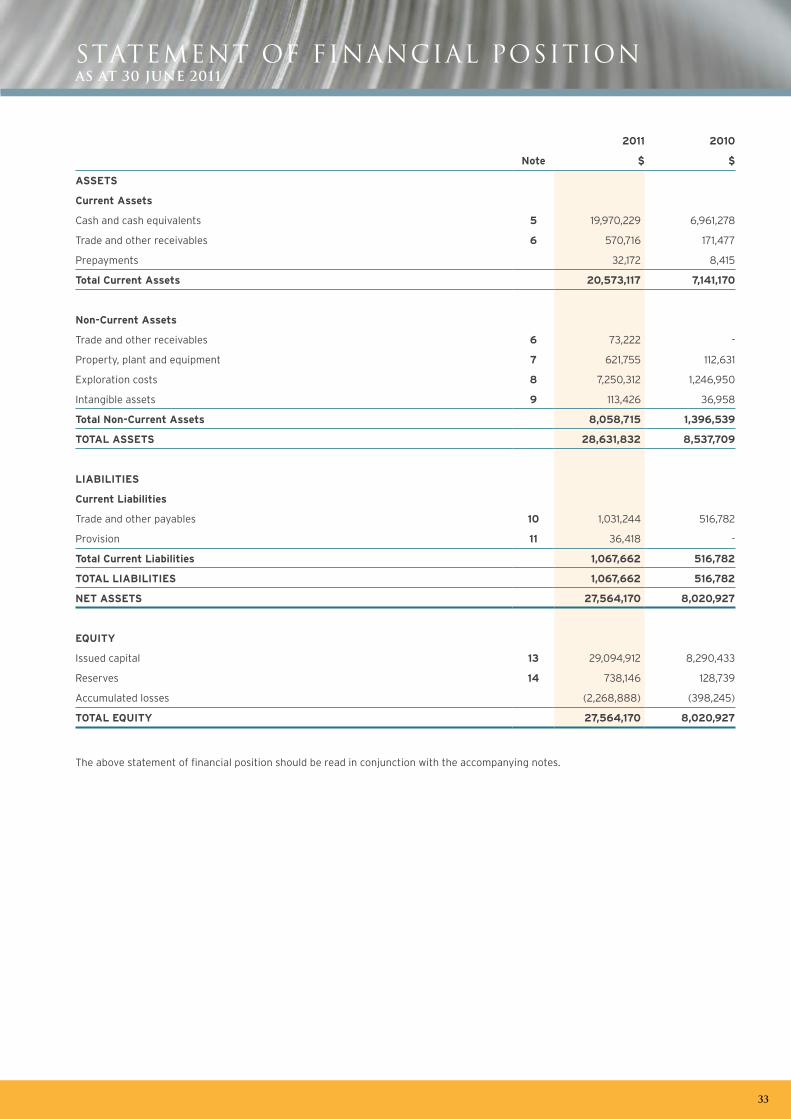

STATEMENT OF COMPREHENSIVE INCOME 32

STATEMENT OF FINANCIAL POSITION 33

STATEMENT OF CHANGES IN EQuITy 34

STATEMENT OF CASH FLOWS 35

NOTES TO THE FINANCIAL STATEMENTS 36

DIRECTORS’ DECLARATION 57

AuDITOR’S INDEPENDENCE DECLARATION 58

INDEPENDENT AuDIT REPORT 59

SHAREHOLDER INFORMATION 61

1

• Published a maiden high-grade jORC resource for the Andy Well gold project of 311,000t @ 17.5 g/t

(for contained 174,000oz) including the very high-grade Wilber Lode (211,000t @ 25.3g/t)

• Commenced a number of development activities at Andy Well, including completion of initial

metallurgical test work resulting in exceptional gravity and total gold recoveries from Wilber

• Drilling at Andy Well continued to increase both the depth and strike extents of the high-grade

Wilber Lode, along with high-grade results from additional target zones

• Completed first pass drilling campaigns at Webbs Patch and Side Well with significant results

• Completed a A$21M capital raising to underpin aggressive exploration programs

• Appointed Mr Mark Cossom as Development Manager and Mr Leigh junk and Mr Peter Alexander

as Non-Executive Directors

• Commenced aircore drilling to test various targets at Abbotts

• Approved 2011/12 budget for extensive 145,000m of new drilling

• Recognised by many commentators as “most successful IPO for 2010” based on share price

increase from listing

Table 1. Maiden JORC Resource for Andy Well Gold Project, including the very high-grade Wilber Lode deposit, released 7 February 2011,

less than 12 months after listing on the ASX.

Indicated Inferred Total Doray 80%

Tonnes Grade (g/t) Ounces Tonnes Grade (g/t) Ounces Tonnes Grade (g/t) Ounces Ounces

Quartz Vein 130,000 24.1 101,000 81,000 27.4 71,000 211,000 25.3 172,000 137,600

Shear Zone 100,000 0.8 2,000 - - - 100,000 0.8 2,000 1,600

Total 230,000 14.0 103,000 81,000 27.4 71,000 311,000 17.5 174,000 139,200

2 Doray Minerals Limited Annual Report 2011

HIGHLIGHTS

Dear Shareholders,

On behalf of the Board of Directors, I am delighted to present

Doray Minerals Limited’s (Doray or the Company) Annual Report

for the financial year ended 30 june 2011.

Reflecting on the past year, your Company has experienced many

highlights and continued to achieve stunning results. Doray has

been listed on the Australian Stock Exchange (ASX) for less than

20 months, and during that period a maiden resource was defined

which is among the highest grade gold resources in Australia.

The size and quality of the resource has enabled the Company to

commence studies to develop the project, all in a relatively short

period of time.

Delivering this pleasing position to shareholders is a committed

Board, management, and a growing team of staff, contractors

and consultants – collectively sharing the drive to achieve whilst

aligning their goals with all stakeholders in the Company. Our

Managing Director, Mr Allan Kelly, has led your Company with

clarity and determination, and I personally thank him for his

diligent efforts.

The first drill hole at Andy Well, the Wilber Lode, produced

outstanding intersections of gold mineralisation and the Board

and management moved to quickly delineate a resource of

174,000 ounces at 17.5 grams per tonne (139,200 ounces

attributable to the Company) within the first 12 months of

quotation on the ASX. The Company enjoyed amazing support

from the capital markets, successfully raising A$21 million in the

same period. Most of these funds were invested by some of the

leading financial institutions in Australia and Asia.

The Andy Well Project comprises a number of prospective

target zones that are yet to be fully tested. Mr Heath Hellewell,

Doray’s Technical Director, supported by Development Manager

Mr Mark Cossom, is focussed on the continued development

of the Wilber Lode and testing these other targets. It is our

strong belief that the Company has only scratched the surface

in determining the true scale of the opportunity at Wilber and

the wider Andy Well property.

These are exciting times for Doray. While the Andy Well

development program is a priority, the Company has an extensive

portfolio of highly prospective assets that require further

investigation, both in Western Australia and in South Australia.

your Company has commenced exploration drilling campaigns

across a number of projects in the Murchison, which is a world-

class gold province.

As the Company moves toward development of the Wilber

Lode deposit, recent appointments to the Board deliver core

competencies that will provide proper vigilance and governance to

the process and execution of a production plan, once established.

Both Mr Peter Alexander and Mr Leigh junk have extensive

experience in design, engineering, financing and execution of

significant production facilities. Their stewardship and guidance to

the Board truly strengthens the Company and has been embraced

by all stakeholders.

your Company is in excellent hands and the Board looks forward

to an active few years that should include initial production

from the Wilber Lode, a strong balance sheet and continued

development of a portfolio of exciting assets. We are working

towards driving shareholder value and guiding the Company

with strength and confidence. We look forward to liaising with

shareholders throughout the year and reporting on future

successful outcomes for Doray.

Thank you for your continued support and investment.

yours sincerely,

Brett Fraser

Chairman

3

Chairman’s Letter

Dear Fellow Shareholder,

Doray Minerals Ltd (Doray or the Company) has come a long

way in the past year and has progressed at a rapid rate with

exceptional exploration results, and development and production

plans for Andy Well underway.

Prior to listing, Doray’s Technical Director Heath Hellewell and

I saw the unrealised potential of Andy Well and were eager to

unlock the value we felt it contained. I am pleased to report that

Andy Well is now delivering consistent high-grade gold results and

it continues to repay our faith in the project.

We are not alone in this opinion as the market and several broking

houses have now begun to realise the significant potential of

Andy Well and Doray’s wider project portfolio.

In December 2010, Doray announced a A$21 million capital raising

through a heavily oversubscribed placement to sophisticated

and institutional investors and a Share Purchase Plan for all

eligible shareholders. The response to this capital raising was

overwhelming and was finalised in january 2011.

In February 2011, Doray announced a maiden high-grade jORC-

compliant gold resource for the Wilber Lode deposit at Andy Well,

less than 12 months after listing. The grade of this resource makes

it one of the highest grade gold deposits in Australia, whilst

excellent gravity and cyanide gold recoveries from subsequent

test work have indicated the potential for very low processing

costs and, more importantly, high profit margins.

Doray continued to accelerate its drilling program at Andy Well

throughout the year with ongoing success. We continue to see

consistent high-grade gold results from drilling within the Wilber

Lode and a number of other target zones which indicate the

potential for additional high-grade resources within the Andy

Well project area.

Project development activities geared toward the commencement

of mining at Wilber have commenced and further work will be

carried out simultaneously with continued exploration. We have

also commenced building a team of skilled and experienced

people to help move Doray towards production.

In addition to ongoing work at Andy Well, we have completed

first pass drilling programs at a number of other projects in the

Murchison, including Side Well, Webbs Patch and Abbotts. Results

from these programs have all been significant and warrant follow-

up drilling during the upcoming year. We have also commenced

planning for exploration work in South Australia.

The Company continues to evaluate potential opportunities with

the aim of creating further shareholder value. I look forward

to updating shareholders on a regular basis, as we continue

progressing the Company toward becoming a significant high-

margin, high-grade gold producer.

I would like to acknowledge the efforts of our rapidly growing

workforce in unlocking the potential of the Company’s projects

and also thank Doray’s expanding shareholder register for its

continued support of the Company.

Allan Kelly

Managing Director

4 Doray Minerals Limited Annual Report 2011

Managing Director’s Letter

5

NON-EXECUTIVE CHAIRMAN

BRETT FRASER

B.Bus, FCPA, FFin

Brett is a Certified Practising Accountant

with in excess of 25 years experience

in the finance and securities industry.

Brett has experience across the

resource, finance, media, brewing,

wine and health sectors. He has owned

business enterprises or held director and

senior management positions in these

industries.

Currently Brett is the Chairman of Drake

Resources Limited, Aura Energy Limited

and Blina Diamonds NL.

MANAGING DIRECTOR

ALLAN KELLY

BSc (Hons), Grad Cert Bus, FAAG, MAIG

Allan has over 19 years experience

in mineral exploration geology,

geochemistry and project management

throughout Australia and the Americas

and previously held senior exploration

positions with WMC and Avoca Resources

from its inception in 2002.

Allan was directly involved in the

targeting and early stage exploration

of a number of gold, nickel, IOCG and

uranium properties in Australia, Alaska

and Canada.

Allan is a Fellow and former Councillor of

the Association of Applied Geochemistry

and is a member of the Australian

Institute of Geoscientists.

TECHNICAL DIRECTOR

HEATH HELLEWELL

BSc(Hons), MAIG

Heath has over 19 years experience

in mineral exploration, geology and

project management in Australia, Africa,

Philippines and Scandinavia including

positions with De Beers and Resolute

Limited before joining Independence

Group NL in 2000. Heath was part of

the team at Independence prior to its

initial public offering and was part of

the exploration team that identified and

pegged the Tropicana area, leading to the

discovery of the Tropicana Gold Deposit.

Heath rose to the position of Exploration

Manager at Independence Group and more

recently has been Exploration Manager at

Goldsearch Limited. Heath is a member of

the Australian Institute of Geoscientists.

6 Doray Minerals Limited Annual Report 2011

Board of Directors

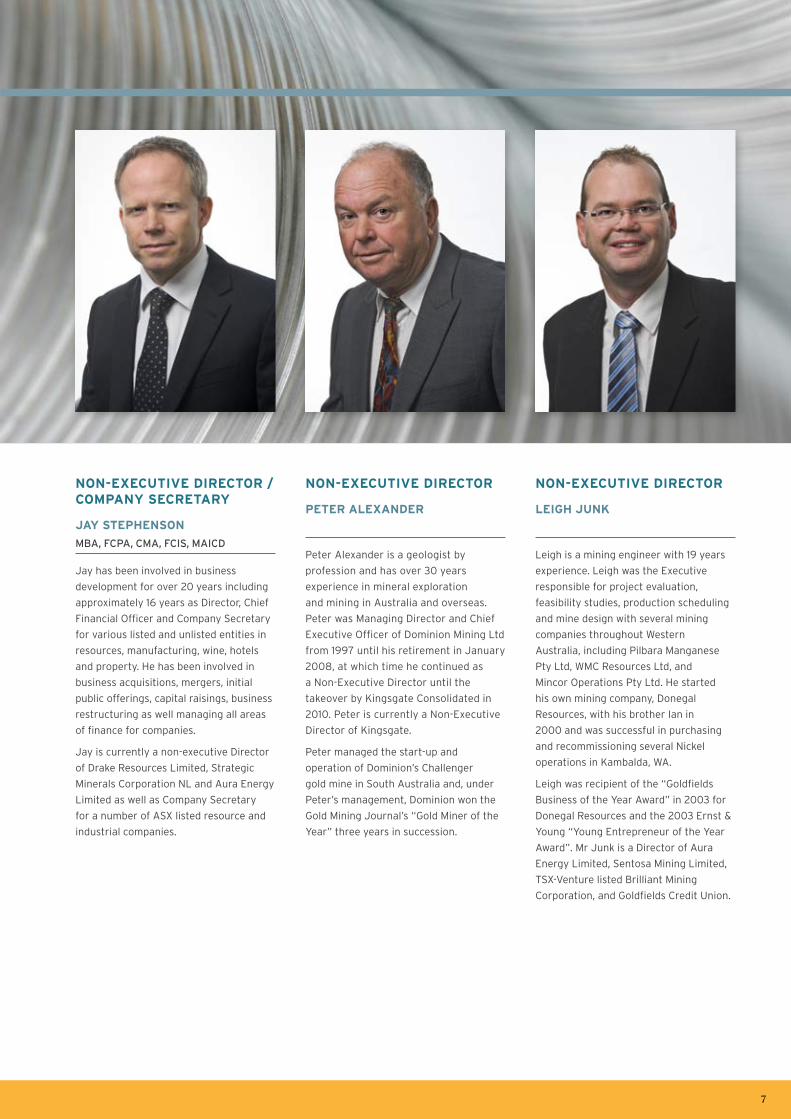

NON-EXECUTIVE DIRECTOR / COMPANY SECRETARY

JAY STEPHENSON

MBA, FCPA, CMA, FCIS, MAICD

jay has been involved in business

development for over 20 years including

approximately 16 years as Director, Chief

Financial Officer and Company Secretary

for various listed and unlisted entities in

resources, manufacturing, wine, hotels

and property. He has been involved in

business acquisitions, mergers, initial

public offerings, capital raisings, business

restructuring as well managing all areas

of finance for companies.

jay is currently a non-executive Director

of Drake Resources Limited, Strategic

Minerals Corporation NL and Aura Energy

Limited as well as Company Secretary

for a number of ASX listed resource and

industrial companies.

NON-EXECUTIVE DIRECTOR

PETER ALEXANDER

Peter Alexander is a geologist by

profession and has over 30 years

experience in mineral exploration

and mining in Australia and overseas.

Peter was Managing Director and Chief

Executive Officer of Dominion Mining Ltd

from 1997 until his retirement in january

2008, at which time he continued as

a Non-Executive Director until the

takeover by Kingsgate Consolidated in

2010. Peter is currently a Non-Executive

Director of Kingsgate.

Peter managed the start-up and

operation of Dominion’s Challenger

gold mine in South Australia and, under

Peter’s management, Dominion won the

Gold Mining journal’s “Gold Miner of the

year” three years in succession.

NON-EXECUTIVE DIRECTOR

LEIGH JUNK

Leigh is a mining engineer with 19 years

experience. Leigh was the Executive

responsible for project evaluation,

feasibility studies, production scheduling

and mine design with several mining

companies throughout Western

Australia, including Pilbara Manganese

Pty Ltd, WMC Resources Ltd, and

Mincor Operations Pty Ltd. He started

his own mining company, Donegal

Resources, with his brother Ian in

2000 and was successful in purchasing

and recommissioning several Nickel

operations in Kambalda, WA.

Leigh was recipient of the “Goldfields

Business of the year Award” in 2003 for

Donegal Resources and the 2003 Ernst &

young “young Entrepreneur of the year

Award”. Mr junk is a Director of Aura

Energy Limited, Sentosa Mining Limited,

TSX-Venture listed Brilliant Mining

Corporation, and Goldfields Credit union.

7

8 Doray Minerals Limited Annual Report 2011

REVIEW OF OPERATIONS

ANDY WELL GOLD PROJECT (DORAY 80%)Doray’s Andy Well project is located 45km north of the town of Meekatharra, towards the northern edge of the Archaean yilgarn Craton.

Prior to listing, Doray identified a number of significant historical drill results at Andy Well and recognised the potential for delineation of

a high-grade gold deposit, with the potential to be trucked to an existing treatment plant.

In March 2010, Doray announced that it had intersected spectacular gold grades within the Wilber Zone at Andy Well with its first drilling

program. Follow-up drilling throughout 2010 confirmed the existence of a very high-grade quartz lode (named the Wilber Lode) over

200m of strike and open to a depth of at least 170m below surface. During the current year great progress has been made at the Andy

Well project, with work focussed on bringing the exploration discovery of last year into production in the near future.

Drilling has been ongoing at the project with a total of 299 Aircore holes for 14,208m, 61 RC holes for 7,587m and 41 Diamond holes for

8,675m completed at the prospect during the year. This drilling has been focussed on both delineating the mineralisation sufficient to

compile an initial resource estimate for the deposit, as well as investigating the potential within proximal targets to Wilber for further

Wilber style mineralisation.

a. Maiden Resource and Development Plans

In February 2011, Doray announced a maiden resource estimate for the Wilber Lode. This estimate was based on all RC and Diamond

drilling completed on the deposit at that time, and was completed in conjunction with Cube Consulting Ltd. The interpretation was

based primarily on the quartz lode present at Wilber, with minor amounts of oxidised, shear zone-hosted material also included within

the near surface portion. The subsequent resource estimate highlighted the high grade nature of the Wilber Lode, and confirmed it as

one of the highest grade virgin gold discoveries in Australia.

Surface

sw

400m RL

300m RL

200m RL

300m RL

200m RL

ANDY WELL PROJECTWILBER SOUTH - WILBER

LONG SECTION 200m0

Legend

20-50 g/t x m

>50 g/t x m

5-10 g/t x m

0-5 g/t x m

10-20 g/t x m

Results pending

2030

0mN

2020

0mN

2010

0mN

2000

0mN

1980

0mN

1990

0mN

1970

0mN

NE

400m RL

Oxide Zone

MNDD056VisibleGold

MNDD055

Wilber Lode Resource172,000oz

(640 oz / vertical m)

Figure 1. Andy Well Project Wilber South – Wilber Long Section, as at July 21, 2011

9

The resource was defined to a depth of approximately 270m below the surface and remained open at depth and down-plunge (Figure 1).

Details of the resource classification are outlined in Table 1 below.

Indicated Inferred Total Doray 80%

Tonnes Grade (g/t) Ounces Tonnes Grade (g/t) Ounces Tonnes Grade (g/t) Ounces Ounces

Quartz Vein 130,000 24.1 101,000 81,000 27.4 71,000 211,000 25.3 172,000 137,600

Shear Zone 100,000 0.8 2,000 - - - 100,000 0.8 2,000 1,600

Total 230,000 14.0 103,000 81,000 27.4 71,000 311,000 17.5 174,000 139,200

Table 1. Maiden JORC Resource for Andy Well Gold Project, including the very high-grade Wilber Lode deposit, released 7 February 2011, less than 12 months after listing on the ASX.

During the year, work also progressed on advancing the Wilber

deposit with a view to economic evaluation and eventual

production. Project development activities geared toward

commencement of mining at Wilber were initiated in November

2010. Due to the greenfields nature of the discovery, with

no pre-existing deposit or mine nearby, all data required

generation. To date, work has been completed in the following:

• Mining Lease application for M51/870. Native title

negotiations are underway

• Comprehensive metallurgical testwork, allowing for

optimal flow sheet design for ore processing options

• Mining engineering studies examining optimal mining

extraction (OP vs uG), including interaction with

geotechnical parameters

• First pass geotechnical investigation and mining

recommendations

• Baseline flora and fauna, subterranean fauna and waste

rock characterisation studies were carried out, suitable

for Mining Proposal submission

• Three stages of hydrogeological testwork and examination

• Submission to Meekatharra Shire for a lease within

the town for a suitable lot to house a workforce

accommodation village

• Tender process initiated for design, construction and fit-

out of the accommodation village

Metallurgical testwork completed on eight samples from

Wilber demonstrated that the ore has excellent recoveries to

conventional gravity and cyanide extraction methods across

various grades and within the oxide, transitional and fresh

rock zones. In particular, test work at varying grind sizes

continually showed that recoveries in excess of 80% can be

achieved through gravity separation alone. Further tests to

ascertain bond abrasion and milling work indices indicated

that the ore has moderate grinding and abrasive properties.

Analysis of cyanide leaching properties also indicated that in

achieving high total recoveries, (average of greater than 97%),

low reagent consumption is observed.

Development work is now focussed on further refining mining

and milling scenarios for the deposit, with a view to future

Bankable Feasibility Studies and eventual construction and

commencement of mining. In addition, work will continue to

advance the granting of the Mining Lease application, as well

as completion of all required baseline environmental surveys,

to achieve full permitting and approval of the project.

b. Exploration

As well as improving the data density to enable an initial

resource estimate to be calculated, drilling continued to

investigate nearby extensions and additional deposits to

Wilber at the Andy Well project. Aircore drilling focussed

on numerous new targets, with RC drilling following up and

identifying mineralisation extensions at the Wilber South and

judy zones. Follow-up drilling at judy intersected further

high-grade mineralisation, but indicated the need to revisit

the interpretation of the orientation of mineralisation.

Drilling at Wilber South highlighted a continuation of the

Wilber trend further south of the existing Wilber resource,

with quartz vein hosted gold mineralisation intersected in

shallow RC holes over a strike of 500m south. Initial diamond

drilling immediately south of the existing Wilber resource

confirmed this trend, with Wilber style mineralisation

continuing to be discovered away from this southern margin.

In addition, diamond drilling to test the depth extents of the

Wilber resource was successful in intersecting the Wilber

Lode, with hole MNDD032 intersecting Wilber at a depth of

380m below surface – 140m (or 50% of the defined lode

depth) below the previous deepest hole.

Drilling at Wilber in the coming year will focus on extending

and upgrading the resource inventory, primarily through

strike and depth extensions, as well as targeting additional

deposits in the Wilber vicinity.

10 Doray Minerals Limited Annual Report 2011

[�

[�

[�

[�[�[�

[�

[�

[�[�

[�[�[�

[�[�

[�

[�

[�[�[�

[�

[�[�

[�

[�

[�

[�

[�

[�[�

[�

[�

[�

[�

[�

[�

[�[�

[�

[�

[�[�

[�[�[�[�[�

[�[�

[�

[�

[�[�

[�[�[�

[�[�

[�[�

[�

[�

[�

[�

667,250

667,250

667,500

667,500

667,750

667,750

7,09

7,50

0

7,09

7,50

0

7,09

7,75

0

7,09

7,75

0

7,09

8,00

0

7,09

8,00

0

7,09

8,25

0

7,09

8,25

0

7,09

8,50

0

7,09

8,50

0

LegendAll Drilling - max Au

<0.1g/t

0.1 - 0.25g/t

0.25 - 1g/t

1 - 2g/t

2 - 5g/t

[� >5g/t

Quartz Lode

0 100 200 300Meters

DORAY MINERALS LTDANDY WELL PROJECT

WILBER LODE DRILLING

Ü

WILBER LODE RESOURCE(311,000t @ 17.5g/t)

POTENTIAL SOUTHERN EXTENSIONTO WILBER LODE

11

EXPLORATIONDoray’s management team has, over the last two years, assembled an enviable portfolio of mineral properties in two of Australia’s

under-explored gold provinces; the Murchison Goldfields Region of WA and the Central Gawler Gold Province of SA. The projects are

characterised by large land positions on major mineralised structures and each presents Doray with multiple discovery opportunities.

a. Murchison Region, Western Australia

Doray’s primary focus during 2010 and 2011 has been on its

substantial portfolio of projects in the Murchison goldfields

region. Doray’s projects cover an area of approximately

1,700 square kilometres over most of the significant mineralised

regional-scale structures in the district. The Murchison region

is host to a number of major gold deposits including: Hill 50,

Big Bell, Great Fingall/Golden Crown, Tuckabianna, Reedys,

Bluebird and the Paddy’s Flat/Meekatharra deposits. The

region also affords excellent property access and various

existing and proposed treatment plants.

During the year, Doray continued to focus its efforts on the

high grade Wilber discovery at Andy Well, and this work

resulted in Doray releasing an initial jORC compliant resource

estimation for Wilber early in 2011. Based on this resource, initial

mine development scoping studies were commenced and will

continue throughout 2011. Doray continues to drill at Wilber

and programs in 2011 have defined significant mineralisation

outside the existing resource area. These new results will be

incorporated into a revised resource estimation and ultimately a

bankable feasibility study for a mine development at Wilber.

Doray also continued to add to its strategic Murchison land

position with the acquisition of a 100% interest in tenements

at Black Tank Well / Webbs Patch and Tuckanarra.

Exploration drilling also commenced on the Webbs Patch,

Side Well and Abbotts project areas during 2011.

Side Well (Doray 80%)

The Side Well project is located approximately 10km north

east of Meekatharra and 30km south of Andy Well. During

2010 / 2011 Doray completed a major 19,000m first pass

aircore drilling program over several targets at Side Well.

This drilling has returned favourable gold and base metal

results from several targets and Doray expects to undertake

further follow-up drilling at Side Well in late 2011.

Abbotts (Doray 80%)

The Abbotts project is located approximately 10km west of

Meekatharra and 40km from Andy Well. Late in the financial

year Doray commenced a program of first pass aircore drilling

to further evaluate the Abernathy Shear Zone, a major

mineralised structure identified by previous explorers at

Abbotts. Previous work along this target zone identified the

potential for large tonnage, low grade gold deposits associated

with granitic intrusives and high grade lode gold deposits.

Webbs Patch (Black Tank Well) (Doray 100%)

The Webbs Patch project is strategically located along strike

from Silver Lake Resources’ Murchison Gold project, where

Silver Lake currently plans to commence production from a

standalone production facility in early 2013.

During the year, Doray completed an initial program of RC

drilling to test previously identified gold mineralisation at the

‘Brilliant’ Prospect. The aim of this program was to determine

the potential for a shallow economic gold resource at Brilliant

and also to test a number of exploration targets at depth.

Drilling of the shallow targets downgraded the potential for

a significant shallow economic resource at Brilliant, however

the exploration potential of this prospect remains high with

significant high-grade intercepts at depth from a previously

unrecognised zone within the Brilliant trend. (Table 2.)

Webbs Patch also contains a small combined oxide and primary

gold jORC compliant resource containing 6,600 ounces.

Numerous other exploration targets have been identified at

Webbs Patch which require further drill evaluation.

Magnet North – Lake Austin (Doray 80%)

The Magnet North project is located immediately north of

the Hill 50 gold operations at Mount Magnet and covers a

total area of 165km2. The project contains numerous exciting

prospects, including the Lake Prospect, located on the north

shore of Lake Austin (10km southeast of Cue). Like Webbs

Patch, this project has significant strategic potential located

within trucking distance of existing and proposed third party,

gold production infrastructure.

The two exploration license applications which comprise this

project were granted during 2011 and Doray is progressing

relevant approvals to commence exploration activities over

this project in 2012.

Tuckanarra (Doray 100%)

In August 2010, Doray acquired a 100% interest in the

Tuckanarra project from Aspire Mining Limited. The project

area covers several priority targets defined by previous

geochemical sampling and airborne geophysics. Doray

expects to commence initial aircore drilling programs at

Tuckanarra prior to the end of 2011.

Hole ID East (MGA) North (MGA)Dip/

AzimuthFrom

(m)To

(m)Interval

(m)Au

(g/t)

WPRC016 605095 6948522 -60/120 109 110 1 7.56

WPRC017 605187 6948543 -60/120 102 103 1 144.4

Table 2. High Grade Results from new footwall target zone at “Brilliant”, Webbs Patch Project

12 Doray Minerals Limited Annual Report 2011

13

Ç

ÇÇÇ

Ç

ÇÇ

Ç

Ç

Ç

Ç

Ç

Ç

Ç

Ç

ÇÇÇ

Ç

Ç

Ç

ÇÇ

Ç

ÇÇÇÇÇÇ

Ç

ÇÇ

ÇÇ

Ç

ÇÇ

ÇÇÇ

Ç

ÇÇ

Ç

ÇÇ

Ç

Ç

Ç

Ç

Ç

Ç

ÇÇ

ÇÇ

ÇÇ

Ç

Ç

Ç

Ç

ÇÇ

ÇÇÇ

Ç

Ç

ÇÇÇÇ

Ç

Ç

Ç

ÇÇÇ

ÇÇ

Ç

Ç

ÇÇÇ

Ç

Ç

ÇÇ

Ç

ÇÇÇ

Ç

Ç

ÇÇ

Ç

Ç

Ç

Ç

Ç

Ç

ÇÇ

Ç

Ç

Ç

Ç

Ç

Ç

Ç

Ç

Ç

Ç

ÇÇ

Ç

Ç

ÇÇ

ÇÇ

Ç

Ç

ÇÇ

Ç

Ç

ÇÇ

Ç

Ç

Ç

Ç

ÇÇ

Ç

Ç

Ç

ÇÇÇ

Ç

Ç

Ç

ÇÇ

Ç

Ç

Ç

Ç

Ç

ÇÇÇ Ç

ÇÇ

Ç

ÇÇ

ÇÇÇÇÇ

ÇÇ

ÇÇ

Ç

Ç

Ç

Ç

Ç

Ç

Ç

Ç

Ç

ÇÇÇÇ

Ç

Ç

Ç

Ç

ÇÇ

Ç

Ç

Ç

Ç

ÇÇ

Ç

Ç

ÇÇ

Ç

ÇÇÇ

Ç

Ç

Ç

Ç

Ç

Ç

Ç

Ç

Ç

ÇÇÇ

Ç

Ç

Ç

Ç

Ç

Ç

Ç

Ç

Ç

Ç

ÇÇÇÇÇ

Ç

Ç

Ç

Ç

Ç

Ç

Ç

ÇÇ

Ç

Ç

Ç

Ç

Ç

Ç

Ç

Ç

Ç

Ç

Ç

Ç

Ç

Ç

Ç

Ç

Ç

Ç

Ç

Ç

Ç

Ç

Ç

ÇÇÇ

ÇÇ

Ç

Ç

Ç

Ç

Ç

Ç

Ç

Ç

Ç

Ç

Ç

Ç

Ç

Ç

Ç

Ç

Ç

Ç

Ç

Ç

ÇÇ

Ç

Ç

ÇÇ

Ç

Ç

Ç

Ç

Ç

Ç

Ç

Ç

ÇÇ

Ç

Ç

Ç

Ç

Ç

ÇÇ

Ç

Ç

Ç

Ç

Ç

Ç

Ç

Ç

Ç

Ç

Ç

Ç

Ç

Ç

ÇÇÇÇ

ÇÇ

Ç

Ç

Ç

Ç

ÇÇÇÇ

Ç

Ç

Ç

Ç

Ç

ÇÇ

Ç

ÇÇÇ

Ç

Ç

Ç

ÇÇ

ÇÇ

Ç

Ç

Ç

Ç

Ç

Ç

Ç

Ç

Ç

Ç

Ç

Ç

Ç

Ç

Ç

Ç

Ç

Ç

ÇÇ

Ç

Ç

ÇÇ

Ç

Ç

Ç

ÇÇ

Ç

ÇÇ

Ç

ÇÇÇ

Ç

Ç

ÇÇÇÇÇ

ÇÇ

ÇÇ

Ç

ÇÇÇ

Ç

ÇÇÇÇÇ

Ç

Ç

ÇÇ

Ç

Ç

Ç

ÇÇÇ

Ç

Ç

Ç

Ç

Ç

ÇÇ

Ç

Ç

ÇÇ

Ç

Ç

ÇÇÇ

Ç

Ç

Ç

Ç

ÇÇ

Ç

Ç

Ç

Ç

Ç

ÇÇÇÇÇ

Ç

Ç

Ç

Ç

Ç

Ç

Ç

Ç

Ç

Ç

Ç

Ç

Ç

Ç

ÇÇ

Ç

Ç

Ç

Ç

ÇÇ

ÇÇ

Ç

Ç

Ç

ÇÇÇÇÇÇ

Ç

Ç

Ç

Ç

Ç

Ç

ÇÇ

Ç

Ç

ÇÇ

Ç

Ç

Ç

Ç

Ç

Ç

Ç

ÇÇ

ÇÇ

Ç

Ç

ÇÇ

ÇÇÇ

Ç

Ç

Ç

Ç

Ç

Ç

Ç

ÇÇÇÇ

ÇÇÇÇ

Ç

ÇÇÇ

Ç

ÇÇ

Ç

Ç

Ç ÇÇ

ÇÇ

Ç

Ç

Ç

Ç

ÇÇ

Ç

Ç

ÇÇÇÇ

Ç

Ç

ÇÇ

ÇÇ

Ç

Ç

Ç

Ç

Ç

Ç

ÇÇÇÇÇÇ

Ç

Ç

ÇÇ

Ç

Ç

ÇÇÇÇ

ÇÇ

Ç

Ç

Ç

ÇÇ

ÇÇ ÇÇÇÇ

Ç

Ç

Ç

Ç

ÇÇ

Ç

Ç

Ç

Ç

Ç

Ç

ÇÇ

Ç

Ç

Ç

Ç

ÇÇÇ

Ç

Ç

Ç

Ç

ÇÇÇ

Ç

Ç

ÇÇ

ÇÇ

ÇÇÇ

Ç

Ç

Ç

Ç

Ç

ÇÇ

ÇÇ

Ç

ÇÇ

Ç

Ç ÇÇ

Ç

ÇÇ

ÇÇ

Ç

ÇÇ

Ç

Ç

ÇÇ

Ç

Ç

Ç

Ç

Ç

ÇÇÇ

Ç

ÇÇÇÇÇÇÇÇ

Ç

Ç

Ç Ç

Ç

Ç

Ç

Ç

Ç

Ç

ÇÇ

ÇÇÇ

ÇÇÇ

Ç

Ç

Ç

ÇÇ ÇÇ

ÇÇÇÇ

Ç

Ç

Ç ÇÇ

Ç

Ç

Ç

Ç

ÇÇ

Ç

ÇÇ

ÇÇ

Ç

ÇÇÇÇÇ

ÇÇ

Ç

Ç

Ç

Ç

Ç

Ç

Ç

ÇÇÇ

ÇÇ

Ç

Ç

Ç

Ç

Ç

Ç

Ç

Ç

Ç

ÇÇ

ÇÇ

Ç

Ç

Ç

Ç

Ç

Ç

Ç

ÇÇ

Ç

ÇÇ

ÇÇÇ

Ç

ÇÇÇÇ

Ç

Ç

Ç

Ç

Ç

Ç

ÇÇ

ÇÇÇ

Ç

Ç

Ç

Ç

Ç

ÇÇ

Ç

Ç

Ç

Ç

Ç

Ç

ÇÇ

Ç

ÇÇ

Ç

ÇÇÇÇÇÇÇ

Ç

ÇÇÇ

Ç

ÇÇ

ÇÇÇÇÇ

Ç Ç

Ç

ÇÇÇÇ

Ç

Ç

Ç

Ç

Ç

ÇÇÇÇÇÇÇ

Ç

Ç

ÇÇ

Ç

Ç

ÇÇÇ

Ç

Ç

Ç

Ç

Ç

ÇÇ

Ç

Ç

ÇÇ

Ç

Ç

ÇÇÇ

ÇÇ ÇÇÇÇ

Ç

Ç

Ç

Ç

ÇÇ

Ç

Ç

Ç

Ç

Ç

ÇÇ

Ç

Ç

ÇÇÇ

Ç

Ç

ÇÇ

Ç

Ç

Ç

Ç

Ç

Ç

Ç

Ç

Ç

Ç

ÇÇÇ

Ç

Ç

Ç

Ç

ÇÇ

Ç

Ç

Ç

Ç

Ç

ÇÇ

Ç

Ç

Ç

Ç

ÇÇ

Ç

Ç

Ç

Ç

Ç

Ç

Ç

Ç

Ç

ÇÇ

Ç

Ç

Ç

Ç

Ç

Ç

ÇÇÇÇ

Ç

Ç

Ç

Ç

Ç

Ç

Ç

ÇÇÇÇÇ

Ç

Ç

Ç

Ç

Ç

ÇÇÇÇÇÇÇ

ÇÇÇ

Ç

ÇÇ

Ç

Ç

Ç

Ç

Ç

Ç

Ç

Ç

Ç

Ç

Ç

Ç

Ç

Ç

ÇÇ

ÇÇÇ

Ç

Ç

ÇÇ

Ç

Ç

Ç

Ç

Ç

Ç

Ç

Ç

Ç

Ç

Ç

Ç

Ç

ÇÇ

Ç

ÇÇÇÇÇÇ

ÇÇÇÇ

Ç

Ç

Ç

Ç

Ç

Ç

Ç

Ç

Ç

Ç

Ç

Ç

Ç

Ç

Ç

Ç

Ç

ÇÇÇ

ÇÇ

Ç ÇÇÇÇÇ

Ç

Ç

Ç

ÇÇ

ÇÇÇ

Ç

ÇÇÇÇÇÇÇ

Ç

Ç

Ç

Ç

Ç

Ç

ÇÇÇÇÇÇÇÇÇÇÇÇÇÇÇÇÇÇ

Ç

ÇÇ

Ç

Ç

Ç

ÇÇÇ Ç

Ç

Ç

Ç

Ç

Ç

Ç

Ç

Ç

Ç

Ç

Ç

ÇÇ

Ç

Ç

Ç

ÇÇÇÇ

ÇÇÇ

Ç

ÇÇÇ

Ç

Ç

Ç

Ç

Ç

Ç

Ç

ÇÇ

Ç

Ç

Ç

Ç

Ç

Ç

Ç

Ç

Ç

Ç

Ç

ÇÇ

Ç

Ç

Ç

Ç

ÇÇ

Ç

Ç

Ç

Ç

Ç

ÇÇÇÇÇ

ÇÇÇ

Ç

Ç

Ç

Ç

Ç

Ç

Ç

Ç

ÇÇ

Ç

Ç

Ç

Ç

Ç

ÇÇ

ÇÇÇÇ Ç

Ç

Ç

Ç

Ç

Ç

Ç

ÇÇ

Ç

Ç

Ç

Ç

Ç

ÇÇÇÇ

Ç

ÇÇ

Ç

ÇÇÇÇ

Ç

Ç

Ç

Ç

Ç

Ç

Ç

ÇÇ

Ç

Ç

ÇÇÇ

Ç

Ç

Ç

Ç

Ç

Ç

Ç

Ç

Ç

Ç

Ç

ÇÇ

Ç

Ç

Ç

Ç

ÇÇÇ

ÇÇ

ÇÇÇÇÇÇ

Ç

Ç

ÇÇ

Ç

ÇÇÇ

Ç

Ç

ÇÇÇ

Ç

Ç

Ç

Ç

Ç

Ç

Ç

Ç

ÇÇÇÇÇÇÇÇ

Ç

Ç

Ç

ÇÇÇÇÇ

ÇÇÇ

Ç

ÇÇ

Ç

Ç

Ç

Ç

Ç

Ç

Ç

Ç

Ç

Ç

Ç

Ç Ç

ÇÇÇ

ÇÇ

Ç

Ç

Ç

Ç

ÇÇ

Ç

Ç

ÇÇ

Ç

Ç

Ç

Ç

Ç

ÇÇ

ÇÇ

Ç

Ç

Ç

Ç

Ç

Ç

Ç

Ç

Ç

Ç

Ç

Ç

Ç

Ç

Ç

Ç

Ç

Ç

Ç

Ç

Ç

Ç

ÇÇ

Ç

Ç

Ç

Ç

Ç

Ç

ÇÇ

Ç

Ç

ÇÇÇÇÇÇ

Ç

ÇÇ

Ç

Ç

Ç

Ç

Ç

Ç

Ç

Ç

ÇÇ

Ç

ÇÇ

Ç

Ç

Ç

Ç

ÇÇ

Ç

Ç

Ç

Ç

Ç

Ç

ÇÇÇ

ÇÇ

ÇÇÇ

ÇÇÇÇ

Ç

ÇÇ

ÇÇÇÇÇ

Ç

ÇÇ

Ç

ÇÇÇ

ÇÇ

Ç

Ç

ÇÇÇ

Ç

Ç

ÇÇ

ÇÇ

ÇÇÇÇÇ

Ç

ÇÇÇÇÇÇ

Ç

ÇÇÇÇÇÇ

Ç

Ç

Ç

Ç

Ç

ÇÇÇÇÇÇÇÇÇ

Ç

Ç

ÇÇ

ÇÇÇÇ

Ç

Ç

ÇÇÇ

ÇÇ

Ç

Ç

ÇÇ

Ç

Ç

Ç

Ç

ÇÇÇ

ÇÇÇ

Ç

ÇÇ

Ç

ÇÇ

Ç

Ç

Ç

ÇÇ

Ç

ÇÇ

Ç

Ç

Ç

Ç

ÇÇ

ÇÇ

Ç

Ç

Ç

Ç

Ç Ç

Ç

Ç

Ç

ÇÇÇÇÇ

Ç

Ç

ÇÇÇÇÇÇÇ

Ç

Ç

Ç

Ç

ÇÇÇ

Ç

ÇÇÇ

ÇÇ

Ç

ÇÇ

Ç

Ç

Ç

Ç

Ç

Ç

Ç

Ç

Ç

Ç

ÇÇ

Ç

ÇÇ

Ç

Ç

ÇÇ

Ç

Ç

ÇÇ

Ç

Ç

Ç

Ç

Ç

ÇÇÇÇÇÇÇ

ÇÇ

Ç

Ç

Ç

Ç

Ç

Ç

Ç

Ç

Ç

Ç

Ç

Ç

ÇÇÇ

Ç

Ç ÇÇÇ

Ç

ÇÇÇ

Ç

Ç

Ç

Ç

Ç

Ç

ÇÇÇ

Ç

Ç

ÇÇÇÇÇÇÇ

Ç

Ç

Ç

Ç

ÇÇ

Ç

ÇÇ

Ç

Ç

Ç

Ç

ÇÇ

ÇÇ

ÇÇ

Ç

Ç ÇÇ

Ç

Ç

ÇÇ

Ç

ÇÇÇ

Ç

Ç

Ç

ÇÇ

Ç

Ç ÇÇÇÇ

Ç

Ç

Ç

Ç

Ç

Ç

Ç

ÇÇÇÇ

ÇÇ

Ç

Ç

ÇÇ

Ç

ÇÇ

ÇÇÇÇÇ

Ç

ÇÇ

Ç

ÇÇ

Ç

Ç

Ç

Ç

Ç

Ç

Ç

ÇÇ

Ç

Ç

Ç

ÇÇ

ÇÇ

ÇÇ

Ç

Ç

Ç

ÇÇ

Ç

ÇÇ

ÇÇ

ÇÇÇ

Ç

ÇÇÇÇ

Ç

ÇÇ

Ç

Ç

Ç

Ç

Ç

Ç

ÇÇÇ

Ç

Ç

ÇÇÇÇÇ

Ç

Ç

Ç

Ç

Ç

ÇÇ

Ç

ÇÇ ÇÇ

Ç

ÇÇ

Ç

Ç

Ç

Ç

Ç

Ç

Ç

ÇÇÇÇ

Ç

Ç

Ç

ÇÇ

ÇÇÇÇÇÇÇÇÇÇÇÇÇ

ÇÇÇÇ

Ç

ÇÇ

Ç

Ç

ÇÇ

Ç

Ç

Ç

Ç

Ç

Ç

ÇÇ

Ç

ÇÇÇÇÇÇ

ÇÇÇÇÇ

ÇÇÇÇ

Ç

Ç

Ç

Ç

Ç

Ç

Ç

ÇÇ

Ç

Ç

Ç

Ç

Ç

Ç

Ç

Ç

Ç

ÇÇ

Ç

ÇÇÇÇ

Ç

Ç

Ç

Ç

ÇÇ

Ç

Ç

ÇÇÇ

ÇÇ Ç

Ç

Ç

Ç

Ç

Ç

Ç

Ç

Ç

ÇÇÇ

Ç

Ç

ÇÇÇÇ

Ç

Ç

ÇÇ

Ç

Ç

Ç

Ç

ÇÇÇÇ

ÇÇ

Ç

Ç

Ç

ÇÇÇÇÇÇÇÇÇÇÇÇÇ

Ç

Ç

ÇÇ

Ç

ÇÇÇ

Ç

ÇÇ

Ç

Ç

Ç

Ç

ÇÇ

Ç

Ç

Ç

Ç

Ç

Ç

Ç

ÇÇ

Ç

ÇÇ

Ç

Ç

Ç

Ç

Ç

ÇÇ

Ç

Ç

Ç

ÇÇ

Ç

Ç

ÇÇÇ

Ç

ÇÇ

Ç

Ç

Ç

Ç

Ç

Ç

Ç

Ç

Ç

Ç

Ç

Ç

ÇÇÇÇ

Ç

ÇÇ

Ç

ÇÇ

Ç

Ç

Ç

ÇÇ

ÇÇ

ÇÇ

Ç

Ç

Ç

ÇÇ

Ç

Ç

Ç

Ç

Ç

Ç

Ç

Ç

Ç

Ç

Ç

Ç

Ç

ÇÇ

Ç

Ç

Ç

Ç

Ç

Ç

Ç

Ç

Ç

Ç

Ç

Ç

Ç

Ç

Ç

ÇÇ

Ç

ÇÇÇÇÇ

Ç

ÇÇÇÇÇÇÇÇ

ÇÇ

ÇÇÇÇÇÇÇ

ÇÇ

ÇÇÇÇÇÇÇÇÇ

ÇÇÇÇÇÇÇÇÇÇ

Ç

ÇÇÇÇÇ

Ç

ÇÇÇ

Ç

Ç

Ç

Ç

ÇÇÇ

ÇÇÇ

Ç

ÇÇÇ

Ç

ÇÇ

ÇÇÇ

Ç

ÇÇÇ

ÇÇÇÇ

Ç

Ç

Ç

ÇÇ

Ç

ÇÇÇ

ÇÇ

ÇÇ

Ç

Ç

Ç

ÇÇ

Ç

ÇÇÇÇÇÇ

ÇÇÇÇÇ

ÇÇ

Ç

ÇÇÇ

Ç

ÇÇ

ÇÇÇÇÇÇÇÇ

ÇÇÇÇ

ÇÇ

Ç

Ç

Ç

ÇÇ

Ç

ÇÇÇ Ç

ÇÇÇÇÇÇ

Ç

Ç

Ç

ÇÇ

Ç

ÇÇ

ÇÇÇÇ

ÇÇ

ÇÇÇÇÇÇÇÇÇ

Ç

Ç

ÇÇÇÇÇÇ

Ç

ÇÇÇ

Ç

ÇÇ

Ç

ÇÇÇ

Ç

ÇÇ

ÇÇ

ÇÇÇ

Ç

Ç

Ç

Ç

Ç

Ç

Ç

ÇÇ ÇÇ

Ç

Ç

Ç

ÇÇ

ÇÇÇ

Ç

Ç

Ç

Ç

Ç

Ç

Ç

ÇÇ

Ç

Ç

Ç

Ç

Ç

Ç

ÇÇ

Ç

Ç

Ç

Ç

Ç

Ç

ÇÇÇÇ

Ç

Ç

ÇÇÇÇ

Ç

ÇÇ

ÇÇÇÇ

Ç

ÇÇÇ

Ç

Ç

Ç

Ç

Ç

Ç

ÇÇ

ÇÇ

ÇÇÇÇ

Ç

Ç

Ç

Ç

ÇÇ

Ç

ÇÇÇ

ÇÇÇ

ÇÇÇ

Ç

ÇÇ

ÇÇ

ÇÇ

Ç

Ç

ÇÇÇÇÇÇ

Ç

Ç

Ç

Ç

Ç

Ç

Ç

Ç

Ç

Ç

Ç

Ç

ÇÇ

ÇÇ

Ç

ÇÇÇÇÇ

Ç

Ç

Ç

Ç

Ç

ÇÇ

Ç

Ç

Ç

ÇÇÇ

Ç

Ç

ÇÇ

ÇÇ Ç

ÇÇ

Ç

Ç

ÇÇ

ÇÇ

Ç

ÇÇ

Ç

Ç

Ç

Ç

Ç

Ç

Ç

ÇÇ

Ç

Ç

Ç

ÇÇ

Ç

Ç

Ç

Ç

[�

[�

[�

[�

[�

[�

[�

[�

[�[�

[�

[�

550000

550000

575000

575000

600000

600000

625000

625000

650000

650000

675000

675000

6900

000

6900

000

6925

000

6925

000

6950

000

6950

000

6975

000

6975

000

7000

000

7000

000

7025

000

7025

000

7050

000

7050

000

7075

000

7075

000

7100

000

7100

000

0 10 20 30Kilometres

DORAY MINERALS LTDMURCHISON PROJECTS

Legend[� Major gold deposit

Ç Gold Occurrence

Doray Leases

ANDY WELL

SIDE WELL

ABBOTTS

Meekatharra

Bluebird

Ü MINGAH

TUCKANARRA

COOTHARRA

LAKE AUSTIN

MAGNET NORTH

BLACK TANK WELL

WEBBS PATCH

Hill 50

Great Fingall/Golden Crown

Big Bell

Reedys

Tuckabianna

b. Central Gawler Region, South Australia

Doray’s portfolio of South Australian projects comprises

a number of prospects located within the “Central Gawler

Gold Province”, an arcuate zone of Proterozoic-aged gold

deposits and prospects identified by various South Australian

and Federal government geologists. The area is related to

the Hiltaba Suite granites, which also host most of South

Australia’s Iron Oxide Copper-Gold (IOCG) deposits.

Doray completed initial airborne geophysical surveys

and reconnaissance field programs during the year. The

Company also examined a number of acquisition and/or

joint venture opportunities in the Central Gawler during

the year and increased its tenement position to over 1,600

square kilometers, through the pegging of a number of

new tenements.

Nuckulla Hill (Doray 100%)

Nuckulla Hill is located 50km south of the Tunkillia deposit

(0.8Moz Au, 1.6Moz Ag), within the mineralised yarlbrinda

Shear Zone. Previous exploration has been limited to calcrete

sampling and sporadic drilling and the project has received

no systematic gold exploration since 1997, despite its location

adjacent to such a large undeveloped gold deposit.

During 2010, Doray completed a detailed 100m-spaced

aeromagnetic survey covering the entire 60km of the

yalbrinda Shear Zone within the Company’s leases.

The survey highlighted a number of structural targets

not effectively tested either by calcrete geochemistry or

historic drilling. Doray completed a field investigation of

a number of these targets and is currently planning to

undertake field programs to test several targets during the

current financial year.

Labyrinth (Doray 100%)

Located within the Labyrinth Shear Zone, previous exploration

highlighted a number of geochemical targets at Kingoonya

and encouraging gold results from limited historic drilling

at Hicks. Doray completed a program of regional airborne

magnetic surveys at these two areas in early 2011, along with

initial reconnaissance evaluation of targets from this survey.

Central Gawler Region, South Australia, project area

14 Doray Minerals Limited Annual Report 2011

CORPORATEIn December 2010, the Company announced a A$21 million

capital raising through a heavily oversubscribed placement to

sophisticated and institutional investors and Share Purchase Plan

for all eligible shareholders. On 14 December 2010, the Company

announced a placement of 8,308,000 shares at a price of

A$1.30 per share to raise A$10,800,400.

The funds will be primarily used for accelerated development

of the Andy Well project (Doray 80%) including delineation of

the Wilber Lode and other potential deposits, as well as the

systematic exploration of a number of other projects in Doray’s

highly prospective Murchison portfolio, general corporate

purposes and potential future acquisitions.

In january 2011, the Company issued 7,845,846 shares at a price

of A$1.30 per share and raised A$10,199,600 to complete the

A$21 million capital raising.

In May 2011, the Company announced the appointment of Mr Peter

Alexander and Mr Leigh junk to the Board, bringing significant

development and operations expertise to the Company.

a. Company Mission Statement & Core Values

Doray Minerals’ Mission Statement and purpose is:

“To create superior shareholder value through the discovery,

acquisition and development of world-class mineral deposits

using best practise”

The Core Values that Doray operates by include:

• We seek to provide a safe working environment and value

safety above profits

• We act with integrity at all times, respect the law and act

accordingly

• We will not engage in any illegal or unethical conduct and

refrain from potential conflicts of interest

• We respect the confidentiality of company, client and staff

information and will not use it in an unauthorised capacity

• We are committed to developing mutually beneficial

relationships with the communities we work in, including

with traditional owners

• We are committed to providing an equal opportunity

workplace free from any form of harassment

• We seek to minimise the impact of our operations on the

surrounding communities and environment

b. Community Development

Doray understands the importance of building and

maintaining relationships within the communities in which

it operates. Doray will develop further relationships and

partnerships over the coming months and years, and to

date has sponsored and supported several local events and

groups in the Murchison, including the Meekatharra Golf Day

and Meekatharra Race Club Carnival. Many other local

community sponsorships are ear-marked for the coming

12 months, as the Company works toward building more

mutually beneficial relationships and becoming an active

community member.

15

RESOURCE INVENTORY

Resource Statement 30 June 2011

Measured Indicated Inferred Total Resources Doray Total Resources

Tonnes Au Au Tonnes Au Au Tonnes Au Au Tonnes Au Au Tonnes Au Au Project (‘000s) g/t Ounces (‘000s) g/t Ounces (‘000s) g/t Ounces (‘000s) g/t Ounces (‘000s) g/t Ounces

Andy Well - - - 230 14.0 104,000 81 27.4 71,000 311 17.5 175,000 249 17.5 140,000

Webbs Patch - - - 33 5.4 6,000 11 2.3 1,000 44 4.6 7,000 44 4.6 7,000

TOTAL ALL RESOURCES - - - 263 12.9 109,000 92 24.3 72,000 355 15.9 181,000 293 15.5 146,000

Competent Person Statement

The information in this report that relates to Exploration Results is based on information compiled by Mr Heath Hellewell, Mr Allan Kelly

and Mr Mark Cossom.

The information in this report that relates to Mineral Resources is based on information compiled by Mr Cossom.

Mr Hellewell and Mr Kelly are both members of the Australian Institute of Geoscientists, whilst Mr Cossom is a Member of the Australasian

Institute of Mining and Metallurgy, and all have sufficient experience, which is relevant to the style of mineralisation and type of deposit under

consideration and to the activity, which they are undertaking. This qualifies Mr Hellewell, Mr Kelly and Mr Cossom as “Competent Persons” as

defined in the 2004 edition of the ‘Australasian Code for Reporting of Exploration Results, Mineral Resources and Ore Reserves’.

Mr Hellewell, Mr Kelly and Mr Cossom consent to the inclusion of information in this report in the form and context in which it appears.

16 Doray Minerals Limited Annual Report 2011

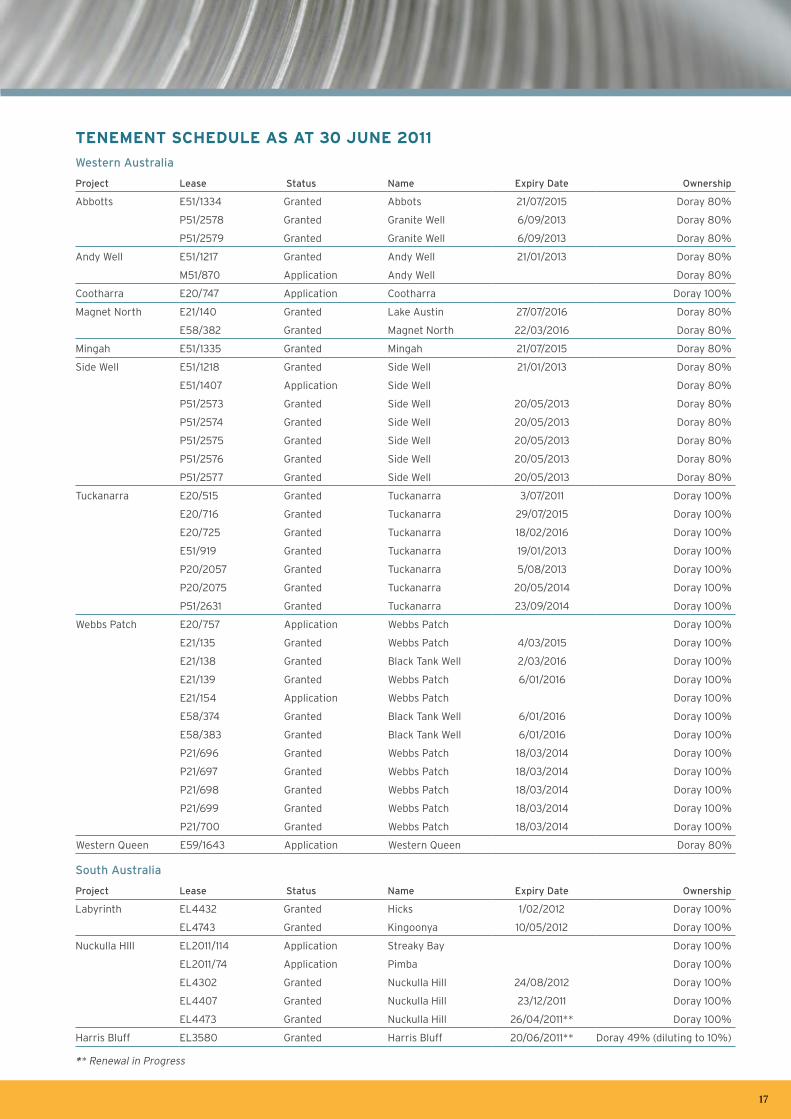

TENEMENT SCHEDULE AS AT 30 JUNE 2011

Western Australia

Project Lease Status Name Expiry Date Ownership

Abbotts E51/1334 Granted Abbots 21/07/2015 Doray 80%

P51/2578 Granted Granite Well 6/09/2013 Doray 80%

P51/2579 Granted Granite Well 6/09/2013 Doray 80%

Andy Well E51/1217 Granted Andy Well 21/01/2013 Doray 80%

M51/870 Application Andy Well Doray 80%

Cootharra E20/747 Application Cootharra Doray 100%

Magnet North E21/140 Granted Lake Austin 27/07/2016 Doray 80%

E58/382 Granted Magnet North 22/03/2016 Doray 80%

Mingah E51/1335 Granted Mingah 21/07/2015 Doray 80%

Side Well E51/1218 Granted Side Well 21/01/2013 Doray 80%

E51/1407 Application Side Well Doray 80%

P51/2573 Granted Side Well 20/05/2013 Doray 80%

P51/2574 Granted Side Well 20/05/2013 Doray 80%

P51/2575 Granted Side Well 20/05/2013 Doray 80%

P51/2576 Granted Side Well 20/05/2013 Doray 80%

P51/2577 Granted Side Well 20/05/2013 Doray 80%

Tuckanarra E20/515 Granted Tuckanarra 3/07/2011 Doray 100%

E20/716 Granted Tuckanarra 29/07/2015 Doray 100%

E20/725 Granted Tuckanarra 18/02/2016 Doray 100%

E51/919 Granted Tuckanarra 19/01/2013 Doray 100%

P20/2057 Granted Tuckanarra 5/08/2013 Doray 100%

P20/2075 Granted Tuckanarra 20/05/2014 Doray 100%

P51/2631 Granted Tuckanarra 23/09/2014 Doray 100%

Webbs Patch E20/757 Application Webbs Patch Doray 100%

E21/135 Granted Webbs Patch 4/03/2015 Doray 100%

E21/138 Granted Black Tank Well 2/03/2016 Doray 100%

E21/139 Granted Webbs Patch 6/01/2016 Doray 100%

E21/154 Application Webbs Patch Doray 100%

E58/374 Granted Black Tank Well 6/01/2016 Doray 100%

E58/383 Granted Black Tank Well 6/01/2016 Doray 100%

P21/696 Granted Webbs Patch 18/03/2014 Doray 100%

P21/697 Granted Webbs Patch 18/03/2014 Doray 100%

P21/698 Granted Webbs Patch 18/03/2014 Doray 100%

P21/699 Granted Webbs Patch 18/03/2014 Doray 100%

P21/700 Granted Webbs Patch 18/03/2014 Doray 100%

Western Queen E59/1643 Application Western Queen Doray 80%

South Australia

Project Lease Status Name Expiry Date Ownership

Labyrinth EL4432 Granted Hicks 1/02/2012 Doray 100%

EL4743 Granted Kingoonya 10/05/2012 Doray 100%

Nuckulla HIll EL2011/114 Application Streaky Bay Doray 100%

EL2011/74 Application Pimba Doray 100%

EL4302 Granted Nuckulla Hill 24/08/2012 Doray 100%

EL4407 Granted Nuckulla Hill 23/12/2011 Doray 100%

EL4473 Granted Nuckulla Hill 26/04/2011** Doray 100%

Harris Bluff EL3580 Granted Harris Bluff 20/06/2011** Doray 49% (diluting to 10%)

** Renewal in Progress

17

18 Doray Minerals Limited Annual Report 2011

Financial Report 2011FINANCIAL REPORT

19

As the framework of how the Board of Directors of Doray Minerals Limited (“Company”) carries out its duties and obligations, the Board has

considered the eight principles of corporate governance as set out in the ASX Good Corporate Governance and Best Practice Recommendations.

The essential corporate governance principles are:

1. Lay solid foundations for management and oversight;

2. Structure the Board to add value;

3. Promote ethical and responsible decision-making;

4. Safeguard integrity in financial reporting;

5. Make timely and balanced disclosure;

6. Respect the rights of shareholders;

7. Recognise and manage risk;

8. Remunerate fairly and responsibly.

1. LAY SOLID FOUNDATIONS FOR MANAGEMENT AND OVERSIGHT.

Recommendation 1.1: Formalise and disclose the functions reserved to the Board and those delegated to management.

Roles and Responsibilities:

The roles and responsibilities of the Board are to:

• Oversee control and accountability of the Company;

• Set the broad targets, objectives, and strategies;

• Monitor financial performance;

• Assess and review risk exposure and management;

• Oversee compliance, corporate governance, and legal obligations;

• Approve all major purchases, disposals, acquisitions, and issue of new shares;

• Approve the annual and half-year financial statements;

• Appoint and remove the Company’s Auditor;

• Appoint and assess the performance of the Managing Director and members of the senior management team;

• Report to shareholders.

Recommendation 1.2: Companies should disclose the process for evaluating the performance of senior executives.

The Board regularly reviews the performance of senior executives.

Recommendation 1.3: Provide the information indicated in the ASX Corporate Governance Council’s Guide to Reporting on Principle 1.

The evaluation of performance of senior executives takes place throughout the year.

2. STRUCTURE THE BOARD TO ADD VALUE.

Recommendation 2.1: A majority of the Board should be independent Directors.

Recommendation 2.2: The Chairperson should be an independent Director.

Recommendation 2.3: The roles of the Chairperson and Chief Executive should not be exercised by the same individual.

Recommendation 2.4: The Board should establish a Nomination Committee.

Recommendation 2.5: Companies should disclose the process for evaluating the performance of the Board, its Committees and

individual Directors.

Recommendation 2.6: Companies should provide the information indicated in the Guide to reporting on Principle 2.

MembershipThe Board’s membership and structure is selected to provide the Company with the most appropriate direction

in the areas of business controlled by the Company. The Board currently consists of six members: a Non-

Executive Chairman, a Managing Director, an Executive Director and three Non-Executive Directors.

The Non-Executive Chairman and Non-Executive Directors are considered independent.

Chairman and Managing DirectorThe Company has a Non-Executive Chairman and a Managing Director.

Nomination CommitteeThe Company has a formal charter for the Nomination Committee, however, no Committee has been appointed

to date. The Board as a whole deals with areas that would normally fall under the charter of the Nomination

Committee. These include matters relating to the renewal of Board members and Board performance. Refer to

the table of departure from best practice recommendations.

20 Doray Minerals Limited Annual Report 2011

Corporate governance STATEMENT

SkillsThe Directors bring a range of skills and backgrounds to the Board including, geological, accountancy, finance,

marketing, and stockbroking.

ExperienceThe Directors have considerable experience in business at both operational and corporate levels.

MeetingsThe Board meets when it considers it necessary to meet.

Independent professional adviceEach Director has the right to seek independent professional advice at the Company’s expense for which the

prior approval of the Chairman is required, and is not unreasonably withheld.

3. PROMOTE ETHICAL AND RESPONSIBLE DECISION-MAKING.

Recommendation 3.1: Establish a code of conduct to guide the Directors, the Chief Executive Officer (or equivalent), and any other

key executives as to:

3.1.1 The practices necessary to maintain confidence in the Company’s integrity;

3.1.2 The practices necessary to take into account legal obligations and the reasonable expectations of

shareholders;

3.1.3 The responsibility and accountability of individuals for reporting and investigating reports of unethical

practices.

Recommendation 3.2: Disclose the policy concerning trading in Company securities by Directors, Officers, and employees.

StandardsThe Company is committed to its Directors and employees maintaining high standards of integrity, and

ensuring that activities are in compliance with the letter and spirit of both the law and Company policies. Each

staff member will be issued with the Company’s Policies and Procedures manual at the beginning of their

employment with the Company.

A summary of the Company’s Share Trading Policy is included on the Company’s website.

Recommendation 3.3: Disclose in each annual report the measurable objectives for achieving gender diversity set by the Board in

accordance with the diversity policy and progress towards achieving them.

The Company believes that the promotion of diversity on Boards, in senior management and within the

organisation generally broadens the pool for recruitment of high quality Directors and employees; is likely

to support employee retention; through the inclusion of different perspectives, is likely to encourage greater

innovation; and is socially and economically responsible governance practice.

The Company is in compliance with the ASX Corporate Governance Council’s Principles & Recommendations

on Diversity. The Board of Directors is responsible for adopting and monitoring the Company’s diversity policy.

The policy sets out the beliefs and goals and strategies of the Company with respect to diversity within the

Company. Diversity within the Company means all the things that make individuals different to one another

including gender, ethnicity, religion, culture, language, sexual orientation, disability and age. It involves a

commitment to equality and to treating of one another with respect.

The Company is dedicated to promoting a corporate culture that embraces diversity. The Company believes

that diversity begins with the recruitment and selection practices of its Board and its staff. Hiring of new

employees and promotion of current employees are made on the bases of performance, ability and attitude.

Recommendation 3.4: Disclose in each annual report the proportion of women employees in the whole organisation, women in senior

executive positions and women on the Board.

Currently there are women employees in the whole organisation but not in senior executive positions or on

the Board. Given the present size of the Company, there are no plans to establish measurable objectives for

achieving gender diversity at this time. The need for establishing and assessing measurable objectives for

achieving gender diversity will be re-assessed as the size of the Company increases.

Recommendation 3.5: Provide the information indicated in the ASX Corporate Governance Council’s Guide to Reporting on Principle 3.

A summary of both the Company’s Code of Conduct and its Share Trading Policy is included on the

Company’s website.

21

4. SAFEGUARD INTEGRITY IN FINANCIAL REPORTING.

Recommendation 4.1: The Board should establish an Audit Committee.

Recommendation 4.2: Structure the Audit Committee so that it consists of:

• Only Non-Executive Directors;

• A majority of independent Directors;

• An independent Chairperson, who is not Chairperson of the Board;

• At least three members.

Recommendation 4.3: The Audit Committee should have a formal charter – Refer to Recommendation 4.1.

Recommendation 4.4: Companies should provide the information indicated in the Guide to reporting on Principle 4.

Integrity of Company’s Financial ConditionThe Company’s Chief Financial Officer will report in writing to the Board that the financial statements of

the Company for the half and full financial year present a true and fair view, in all material respects, of the

Company’s financial condition and operational results in accordance with relevant accounting standards.

Audit Committee The Company has a formal charter for an Audit and Governance Committee. The Audit Committee was

established with jay Stephenson, Peter Alexander and Leigh junk as Committee members, with jay

Stephenson as Chair. The Board as a whole deals with areas that would normally fall under the charter of the

Audit and Governance Committee.

5. MAKE TIMELY AND BALANCED DISCLOSURE.

Recommendation 5.1: Establish written policies and procedures designed to ensure compliance with ASX Listing rules disclosure

requirements, and to ensure accountability at a senior management level for that compliance.

Being a listed entity on the Australian Stock Exchange (ASX), the Company has an obligation under the ASX

Listing Rules to maintain an informed market with respect to its securities. Accordingly, the Company advises

the market of all information required to be disclosed under the Rules which the Board believes would have a

material affect on the price of the Company’s securities.

The Company Secretary has been appointed as the person responsible for communication with the ASX.

This role includes responsibility for ensuring compliance with the continuous disclosure requirements of the

ASX Listing Rules, and overseeing and co-ordinating information disclosure to the ASX, analysts, brokers,

shareholders, the media, and the public.

All shareholders have access to the annual report on the Company’s website. Shareholders who have elected

to receive a hardcopy will do so.

Recommendation 5.2: Provide the information indicated in the ASX Corporate Governance Council’s Guide to Reporting on Principle 5.

Disclosure is reviewed as a standard and routine agenda item at each Board meeting.

6. RESPECT THE RIGHTS OF SHAREHOLDERS.

Recommendation 6.1: Design and disclose a communications strategy to promote effective communication with shareholders and

encourage effective participation at general meetings.

Recommendation 6.2: Request the external auditor to attend the annual general meeting and be available to answer shareholder

questions about the conduct of the audit and the preparation and content of the auditor’s report.

The Company is committed to keeping shareholders fully informed of significant developments at the

Company. In addition to public announcements of its financial statements and significant matters, the

Company will provide the opportunity for shareholders to question the Board and management about its

activities at the Company’s annual general meeting.

The Company’s auditor will be in attendance at the annual general meeting, and will also be available to answer

questions from shareholders about the conduct of the audit and the preparation and content of the auditor’s report.

22 Doray Minerals Limited Annual Report 2011

CoRpoRAte goveRnAnCe StAteMent (continued)

7. RECOGNISE AND MANAGE RISK.

Recommendation 7.1: The Board or appropriate Board Committee should establish policies on risk oversight and management.

Recommendation 7.2: The Chief Executive Officer (or equivalent) and the Chief Financial Officer (or equivalent) to state in writing to

the Board that:

7.2.1 The statement given in accordance with best practice recommendation 4.1 (the integrity of financial

statements) is founded on a sound system of risk management and internal compliance and control

which implements the policies adopted by the Board.

7.2.2 The Company’s risk management and internal compliance and control system is operating efficiently and

effectively in all material respects.

Recommendation 7.3: The Board should disclose whether it has received assurance from the Chief Executive Officer (or equivalent)

and the Chief Financial Officer (or equivalent) that the declaration provided in accordance with section 295A

of the Corporations Act is founded on a system of risk management and internal control and that the system is

operating effectively in all material respects in relation to the financial reporting risks.

Recommendation 7.4: Provide the information indicated in the ASX Corporate Governance Council’s Guide to reporting on Principle 7.

The Board oversees the Company’s risk profile. The financial position of the Company and matters of risk are

considered by the Board on a regular basis. The Board is responsible for ensuring that controls and procedures

to identify, analyse, assess, prioritise, monitor, and manage risk are in place, being maintained and adhered to.

The Chief Financial Officer and Chief Executive Officer have stated in writing to the Board that:

• The statement given in accordance with best practice recommendation 4 (the integrity of financial

statements) is founded on a sound system of risk management and internal compliance and control which

implements the policies adopted by the Board.

• The Company’s risk management and internal compliance and control system is operating efficiently and

effectively in all material respects.

8. REMUNERATE FAIRLY AND RESPONSIBLY.

Recommendation 8.1: The Board should establish a Remuneration Committee.

Recommendation 8.2: Clearly distinguish the structure of Non-Executive Directors’ remuneration from that of executives.

Recommendation 8.3: Ensure that payment of equity-based executive remuneration is made in accordance with thresholds set in

plans approved by shareholders.

Principles used to determine the nature and amount of remunerationThe objective of the Company’s remuneration framework is to ensure reward for performance is competitive

and appropriate to the results delivered. The framework aligns executive reward with the creation of value for

shareholders, and conforms to market best practice.

Remuneration CommitteeThe Company has a formal charter for the Remuneration Committee. The Remuneration Committee was

established with Brett Fraser, Peter Alexander and Leigh junk as Committee members, with Brett Fraser as Chair.

The Board as a whole deals with areas that would normally fall under the charter of the Remuneration Committee.

Directors’ RemunerationFurther information on Directors’ and Executives’ remuneration is set out in the Directors’ Report.

Departure from Best Practice RecommendationsFrom the Company’s incorporation, the Company has complied with each of the Eight Essential Corporate

Governance Principles and Best Practice Recommendations published by the ASX Corporate Governance

Council, other than those items in the departure table below.

Recommendation Reference – ASX Guidelines

Notification of Departure Explanation for Departure

2.4, 2.5 , 2.6 A separate Nomination

Committee has not

been formed

The Board considers that the Company is not currently of a size

to justify the formation of a Nomination Committee. The Board

as a whole undertakes the process of reviewing the skill base

and experience of existing Directors to enable identification of

attributes required in Directors.

23

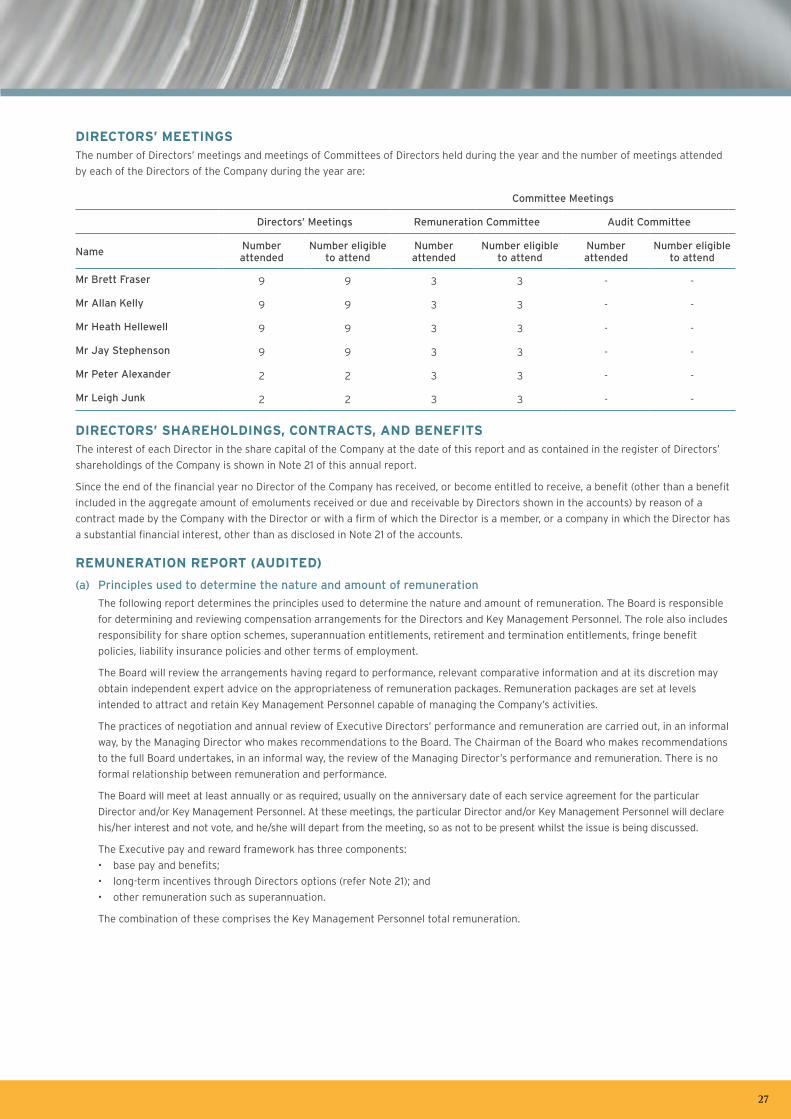

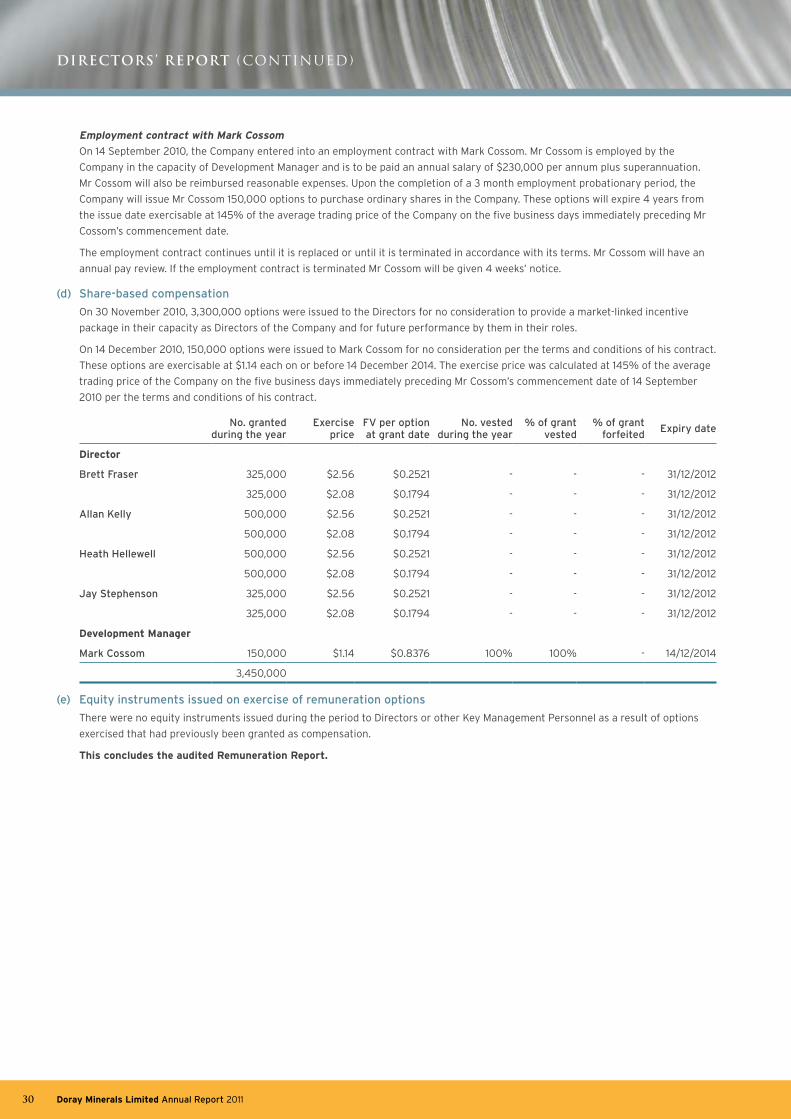

your Directors present their report on Doray Minerals Limited (“the Company”) for the year ended 30 june 2011.

DIRECTORSThe following persons were Directors of the Company and were in office for the entire period, and up to the date of this report, unless

otherwise stated:

Mr Brett Fraser (Independent Non-Executive Director and Chairman, appointed on 23 October 2009)

Mr Allan Kelly (Managing Director, appointed on 20 August 2009)

Mr Heath Hellewell (Technical Director, appointed on 20 August 2009)

Mr jay Stephenson (Independent Non-Executive Director, appointed on 20 August 2009)

Mr Peter Alexander (Independent Non-Executive Director, appointed on 5 May 2011)

Mr Leigh junk (Independent Non-Executive Director, appointed on 5 May 2011)

COMPANY SECRETARYMr jay Stephenson (Non-Executive Director, appointed on 20 August 2009)

PRINCIPAL ACTIVITYThe principal activity of the Company during the year was to acquire, explore and develop properties that are highly prospective and

underexplored for gold.

RESULTS OF OPERATIONSThe loss of the Company for the year after tax amounted to $1,870,643 (2010: $398,245).

SIGNIFICANT CHANGES IN THE STATE OF AFFAIRSIn late December 2010, the Company was acknowledged by a number of commentators to be the most successful IPO of 2010.

On 31 August 2010, the Company issued 200,000 fully paid ordinary shares at a price of $0.75 per share to Aspire Mining Limited as

consideration for 100% purchase of the Black Tank Well and Tuckanarra gold projects in Western Australia. The Black Tank Well project is

adjacent to Doray’s existing Webbs Patch gold project and covers the southern continuation of the highly prospective Tuckabianna-Webbs

Patch greenstone belt.

In December 2010, the Company announced a $21 million capital raising through a heavily oversubscribed placement to sophisticated and

institutional investors and Share Purchase Plan for all eligible shareholders. On 14 December 2010, the Company announced a placement

of 8,308,000 shares at a price of $1.30 per share to raise $10,800,400. The funds will be primarily used for accelerated development

of the Andy Well project (Doray 80%) including delineation of the Wilber Lode and other potential deposits, as well as the systematic

exploration of a number of other projects in Doray’s highly prospective Murchison portfolio, general corporate purposes and potential

future acquisitions.

In january 2011, the Company issued 7,845,846 shares at a price of $1.30 per share and raised $10,199,600 to complete the $21 million

capital raising.

On 7 February 2011, the Company announced a maiden resource for the Wilber Lode, within the Andy Well Project (Doray 80%). The

combined Inferred and Indicated resource for the Wilber Lode totals 311,000t @ 17.5g/t for a total of 174,000 contained ounces.

On 5 May 2011, the Company announced the appointment of Mr Peter Alexander and Mr Leigh junk to the Board as Non-Executive

Directors, bringing significant operational experience to the Board.

During the year ended 30 june 2011, a total of 3,350,000 options were exercised to purchase 3,350,000 fully paid ordinary shares at

$0.20 per share.

No other significant changes in the nature of the Company’s activities have occurred during the year.

DIVIDENDSNo dividends were declared or paid during the period and the Directors do not recommend the payment of a dividend.

INDEMNITIESThe Company, for a premium of $18,800, has taken out an insurance policy to cover its Directors and Officers to indemnify them against

any claims and negligence. The Company has agreed to indemnify the current Directors and Officers for all liabilities to another person,

except where the liability arises out of conduct involving a lack of good faith. The agreement stipulates that the Company shall meet the

full amount of any such liabilities, including costs and expenses.

SIGNIFICANT EVENTS AFTER THE REPORTING DATENo matters or circumstances have arisen since the end of the financial year which significantly affected or could significantly affect the

operations of the Company, the results of those operations, or the state of affairs of the Company in future financial years.

24 Doray Minerals Limited Annual Report 2011

DIRECTORS’ REPORT

PROCEEDINGS ON BEHALF OF THE COMPANYNo person has applied for leave of Court to bring proceedings on behalf of the Company or intervene in any proceedings to which the

Company is a party for the purpose of taking responsibility on behalf of the Company for all or any part of these proceedings.

The Company was not a party to any such proceedings during the period.

INFORMATION ON DIRECTORS

Mr Brett Fraser Non-Executive Director and Chairman from 23 October 2009

Qualifications B.Bus, FCPA, FFin

Experience Mr. Fraser has in excess of 25 years experience in the finance and securities industry. Mr. Fraser has

experience across the resource, finance, media, brewing, wine and health sectors. Mr. Fraser has owned

business enterprises or held director and senior management positions in these industries.

Interest in shares

and options

Shares Direct holding Nil

Indirect holding 103,313

Options Direct holding 1,650,000

Indirect holding Nil

Special Responsibilities Chair of Remuneration Committee

Directorships held in

other listed entities

Currently Mr. Fraser is the Chairman of Drake Resources Limited, Aura Energy Limited and Blina Minerals NL.

Mr Allan Kelly Managing Director from 20 August 2009

Qualifications BSc (Hons), Grad Cert Bus, FAAG MAIG