Copyright anbirts1 Treasury Management Policy Process and Performance.

Upload

carter-mcallisterCategory

view

225download

3

copyright anbirts 1

Capital Structure

The Big

Debate

Well can you or can’t you?

copyright anbirts 2

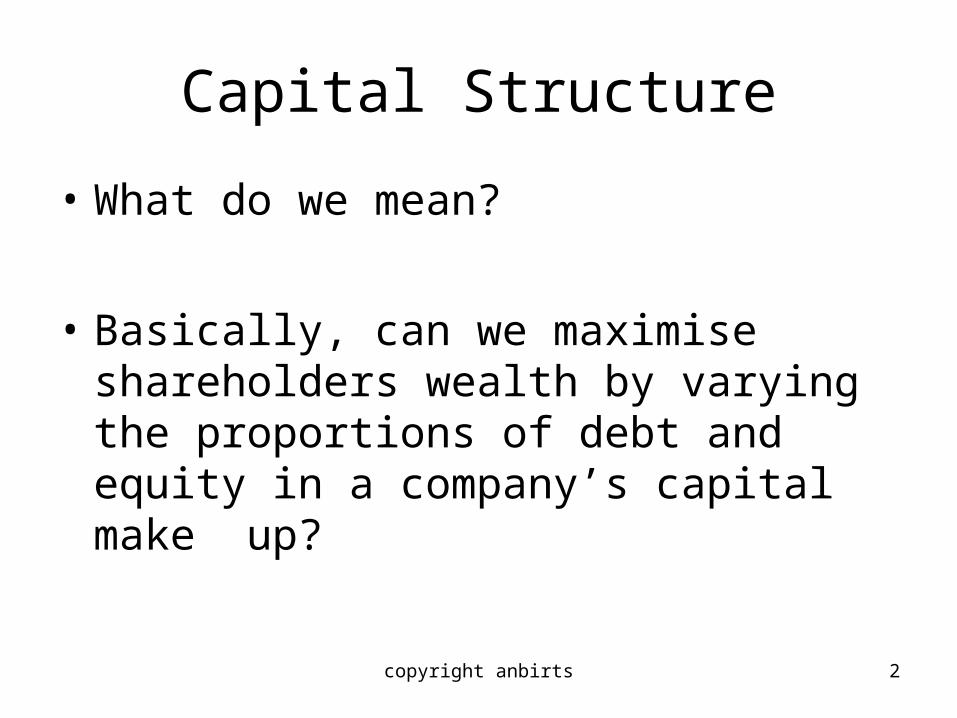

Capital Structure

• What do we mean?

• Basically, can we maximise shareholders wealth by varying the proportions of debt and equity in a company’s capital make up?

copyright anbirts 3

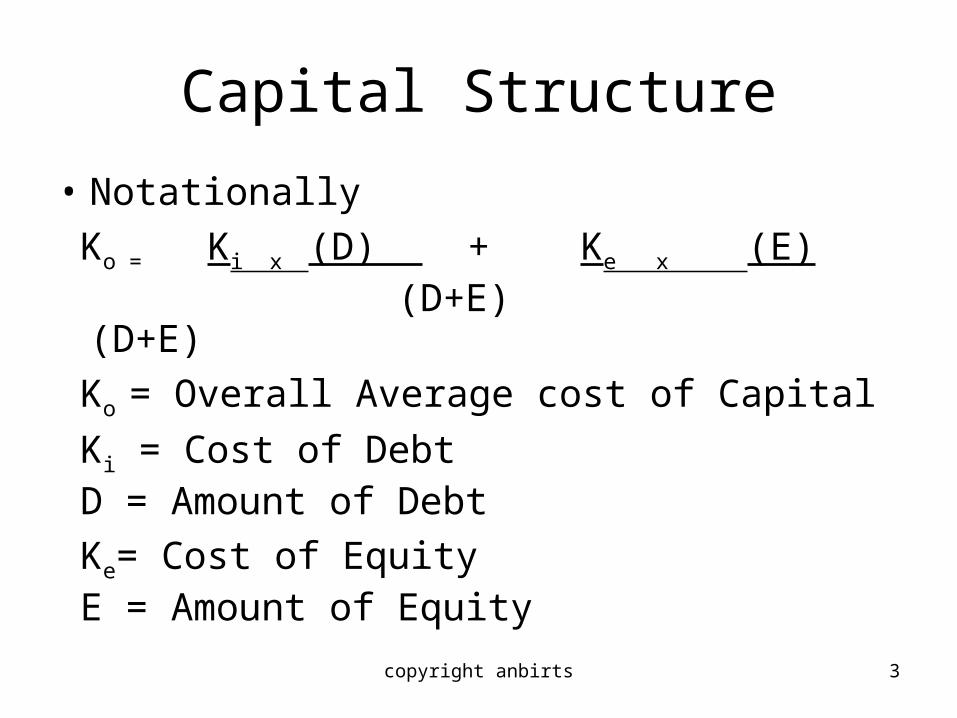

Capital Structure

• Notationally

Ko = Ki x (D) + Ke x (E) (D+E) (D+E)

Ko = Overall Average cost of Capital

Ki = Cost of Debt D = Amount of Debt

Ke= Cost of Equity E = Amount of Equity

copyright anbirts 4

Capital Structure

• As Debt is usually cheaper than equity, why is it not an open and shut case?

• Consider Return on a project = 15% Needs £200-00 of capital Cash Return = £30 If all financing is equity then obviously ROE (return on equity) = 30 = 15% 200

copyright anbirts 5

Capital Structure

• Suppose instead it is financed 50/50 debt/ equity and cost of debt = 10%

• Then: Total Return = 30 Interest cost = 10 (100 x .10) Net Return 20

ROE = 20 = 20% 100So far so good, some very happy shareholders

copyright anbirts 6

Capital Structure

• But disaster strikes and the return falls to £15• Now the returns are

Total returns = 15

Interest cost = 10

Net return = 5

ROE = 5 = 5%

100

copyright anbirts 7

Capital Structure

• Whereas if the shareholders had not been so bold and had financed all Equity

ROE = 15 = 7.5% 200

What effect has leverage had?

copyright anbirts 8

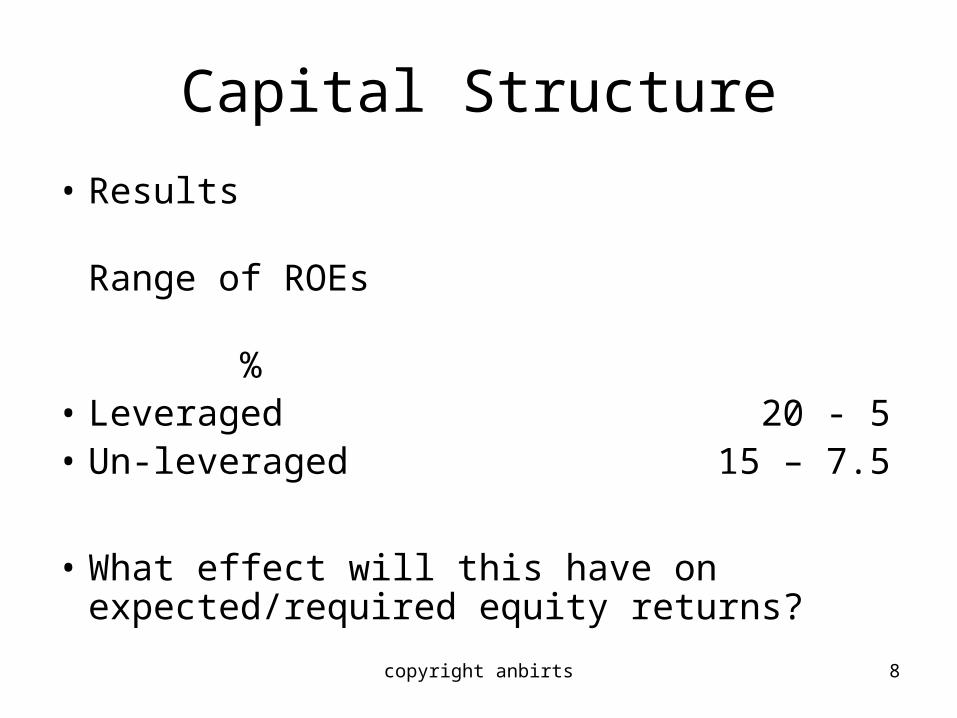

Capital Structure

• Results Range of ROEs %• Leveraged 20 - 5• Un-leveraged 15 – 7.5

• What effect will this have on expected/required equity returns?

copyright anbirts 9

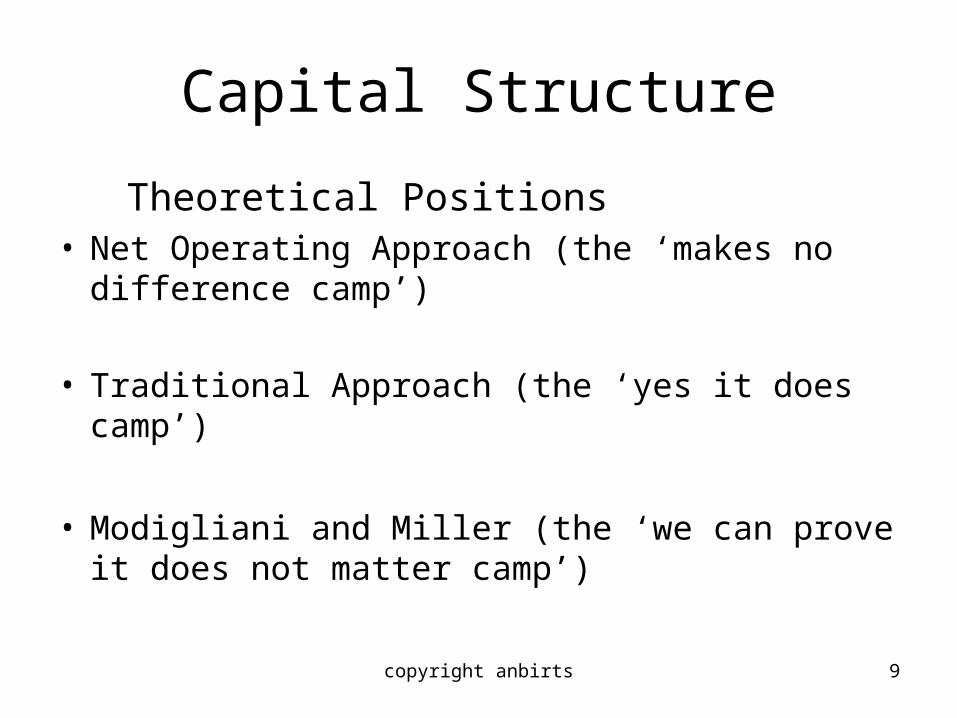

Capital Structure

Theoretical Positions• Net Operating Approach (the ‘makes no

difference camp’)

• Traditional Approach (the ‘yes it does camp’)

• Modigliani and Miller (the ‘we can prove it does not matter camp’)

copyright anbirts 10

Capital Structure

• Net Operating Approach Net operating income 1,000 Capitalisation rate (cost of Capital) .15 Total value of firm 6,667 Market value of debt (cost 10%) 1,000 Market value of equity 5,667 Earnings for equity 1,000 – 100 = 900 ROE = 900 = 15.88% 5,667

copyright anbirts 11

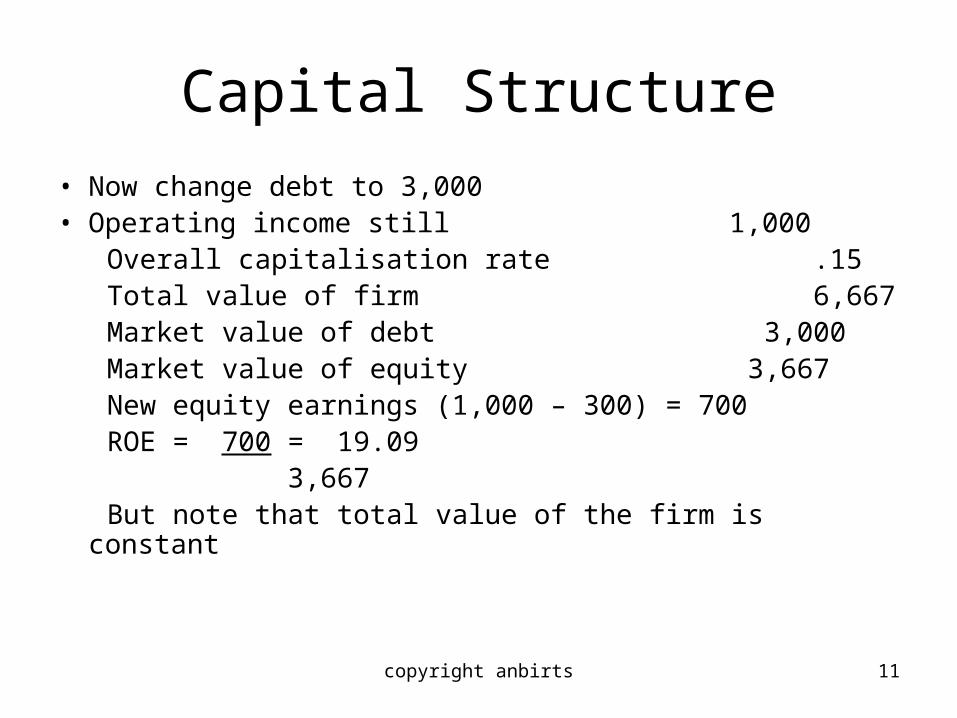

Capital Structure

• Now change debt to 3,000• Operating income still 1,000 Overall capitalisation rate .15 Total value of firm 6,667 Market value of debt 3,000 Market value of equity 3,667 New equity earnings (1,000 – 300) = 700 ROE = 700 = 19.09 3,667 But note that total value of the firm is constant

copyright anbirts 12

Capital StructureTraditional approach – assumes there is an optimal structure therefore

judicious use of leverage will increase value of firm

20

10

15

0

Ke

Ko

Ki

Leverage

%

copyright anbirts 13

Capital Structure

Arbitrage Support

• Basically the argument is i) that the company can do nothing that the shareholders cannot do for themselves and ii) that value comes from the cash flows into the company not from fiddling about within the company.

copyright anbirts 14

Capital Structure

• Arbitrage Support Co A Co BNet Op Income 10,000 10,000Interest on debt (12% pa) nil 3,600Net earnings 10,000 6,400Equity req return .15 .16Market Value of equity 66,667 40,000Market value of debt nil 30,000Total value of the firm 66,667 70,000

copyright anbirts 15

Capital Structure

• M&M would argue that it would not be possible for one company to remain ‘more valuable ‘ than the other, since the over valued company would be sold and the under valued company bought, until the prices equalise’.

• A shareholder in B would do this, replicating Bs actions

copyright anbirts 16

Capital Structure

• Investor in B (IB) owns 1% of B i.e. 400• IB sell their shares for 400 Return would have been 64 (1% of 6,400)• IB borrows 300 (1% of B’s debt) @ 12%• IB buys 1% of A for 666.7 Net position• Return on A 100.0• Less interest 36.0• Net return 64.0 same as in B but for 33.3 less personal outlay (700 – 666.7)

so could spend on more A

copyright anbirts 17

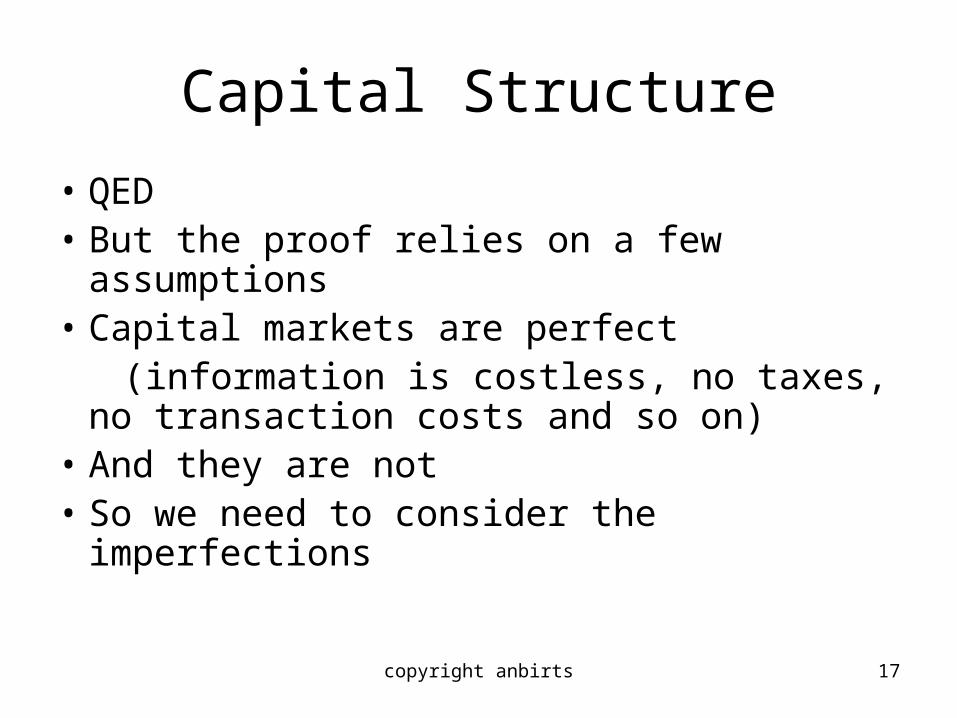

Capital Structure

• QED• But the proof relies on a few assumptions• Capital markets are perfect (information is costless, no taxes, no

transaction costs and so on)• And they are not• So we need to consider the imperfections

copyright anbirts 18

Capital Structure

Effects of imperfections

• Taxes

• Financial distress

• Bankruptcy

• Corporate/private leverage

• Non debt tax shields

copyright anbirts 19

Capital Structure• Taxes Co A Co B EBIT 2,000 2,000 Interest* - 600 Profit before tax 2,000 1,400 Taxes @ 40% 800 560 Shareholders income 1,200 840

Total income to debt andShareholders 1,200 1,440

*(5,000 of debt @ 12% in B)

copyright anbirts 20

Capital Structure

• But has this increased shareholder value?• Yes Suppose companies A and B have £8,000

of Capital. Co A would have 8,000 shares of £1-00 each• Company A’s RoE is 1,200 = 15% 8,000EPS = 15 pence, suppose PE = 6.66 Share value = 1.00

copyright anbirts 21

Capital Structure

• Company B’s Capital is:

• 5,000 debt

• 3,000 equity

• Therefore B’s RoE is 840 = 28%

3,000

EPS = 28 pence, PE is 6.66

Share value = 1.87

copyright anbirts 22

Capital Structure

A gift from the Government?• Suppose debt interest was deducted after tax. • Then• EBIT 2,000• Tax at 40% 800• Net after tax 1,200• Deduct debt interest 600• Income for shareholders 600

copyright anbirts 23

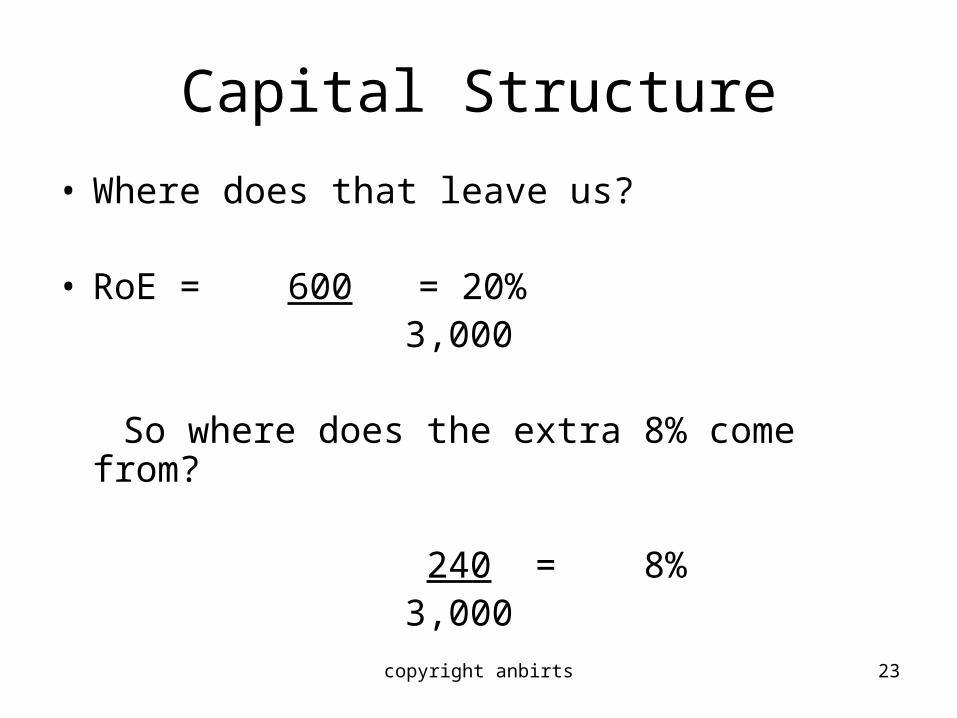

Capital Structure

• Where does that leave us?

• RoE = 600 = 20% 3,000

So where does the extra 8% come from?

240 = 8% 3,000

copyright anbirts 24

Capital Structure

Leverage

Sh

are

pri

ce

0% 100%

e+d+c+b

d+c+b

c + b

b

Optimal Range

a

b effect of increasing price of debtc effect of adjustment for risk (including NPV of bankruptcy costs)d loss of tax shield Trade off theorye cost of financial distress

Effect of Costs of Bankruptcy & Financial Distress on the Value of the Firm company value

utilising debt shield to maximum

copyright anbirts 25

Capital Structure

Debt Equity TotPrp’tion Cost aftTax Wghtd cost % wghtd

0 7 12 100

20 7 12.5 80

30 7.5 13 70

50 8 14 50

70 9.5 18 30

80 11.5 21 20

Tax Rate 30%

copyright anbirts 26

copyright anbirts 27

Capital Structure

Debt Equity TotPrp’tion Cost aftTax Wghtd cost % wghtd 0 7 4.9 0 12 100 12 1220 7 4.9 .98 12.5 80 10 10.9830 7.5 5.25 1.575 13 70 9.1 10.68

50 8 5.6 2.8 14 50 7 9.8 70 9.5 6.65 4.65 18 30 5.4 10.05 80 11.5 8.05 6.44 21 20 4.2 10.64

Tax Rate 30%

copyright anbirts 28

Capital Structure

Cost of 13Capital 12

11

10 0 50 100 Gearing/Leverage

copyright anbirts 29

Capital Structure

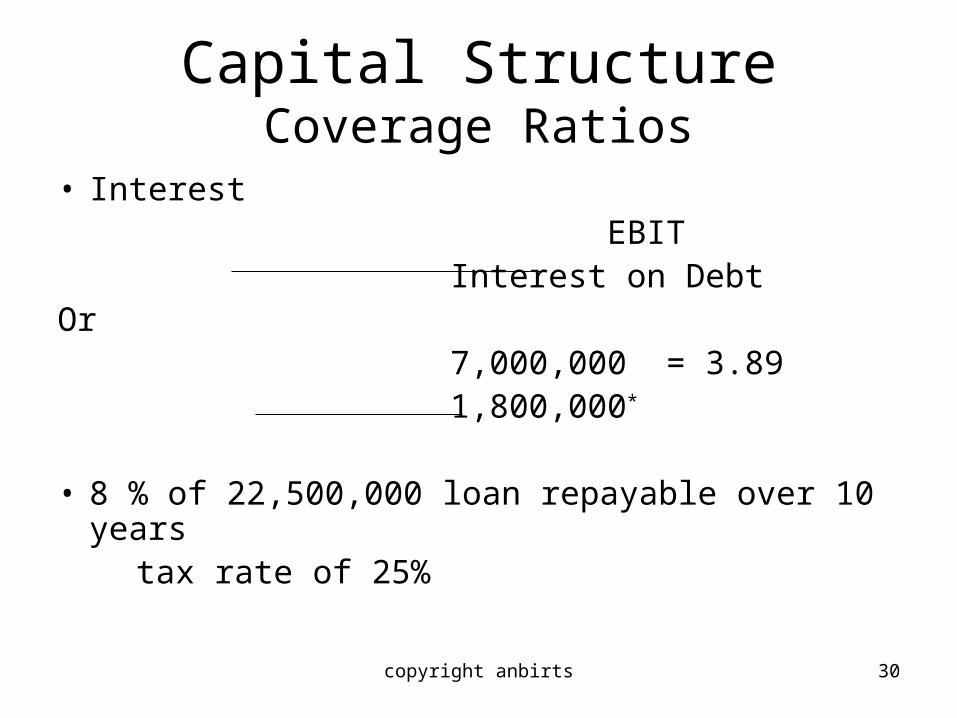

So how will we decide on leverage level?

• Industry norms

• Coverage ratios

* interest

* interest plus principal

copyright anbirts 30

Capital StructureCoverage Ratios

• Interest EBIT Interest on DebtOr 7,000,000 = 3.89 1,800,000*

• 8 % of 22,500,000 loan repayable over 10 years tax rate of 25%

copyright anbirts 31

Capital structureCoverage Ratios

• Interest plus Principal• EBIT Interest + Principal 1 – Tax Rate

7,000,000 1,800,000 + 2,250,000 = 1.46 1-.25

copyright anbirts 32

Capital StructureCoverage Ratios

But what is a suitable coverage ratio?• Variability

• Trend Analysis

• Industry Norms

• All Commitments

copyright anbirts 33

Capital Structure

• Profitability * pecking order• Size * portfolio effect * pecking order• Asset type• Volatility of earnings• International / cultural norms

copyright anbirts 34

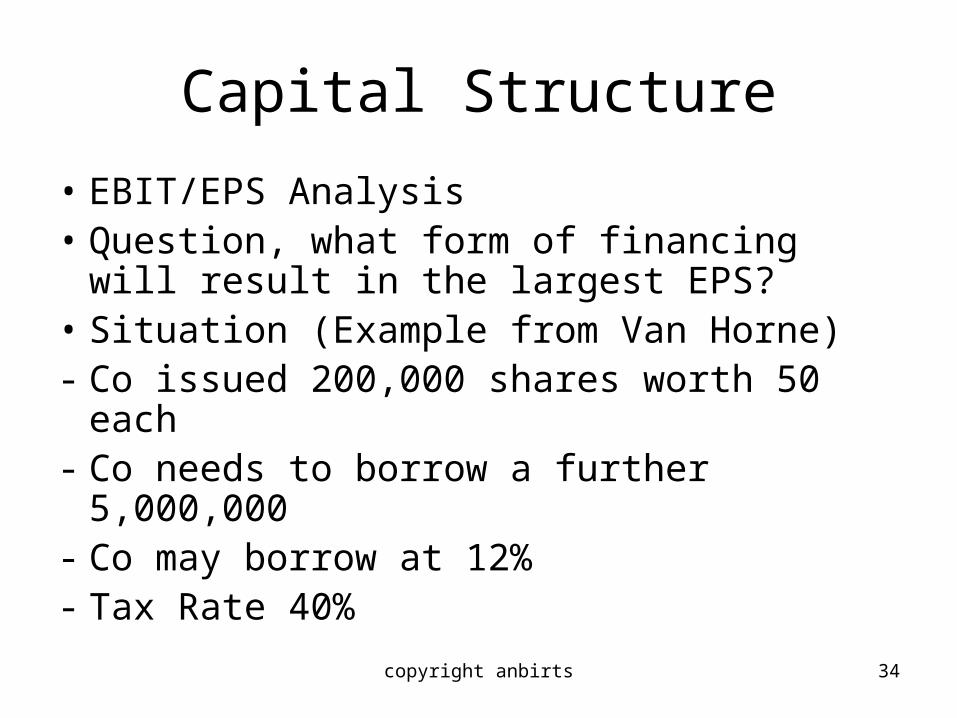

Capital Structure

• EBIT/EPS Analysis• Question, what form of financing will result

in the largest EPS?• Situation (Example from Van Horne)- Co issued 200,000 shares worth 50 each- Co needs to borrow a further 5,000,000- Co may borrow at 12%- Tax Rate 40%

copyright anbirts 35

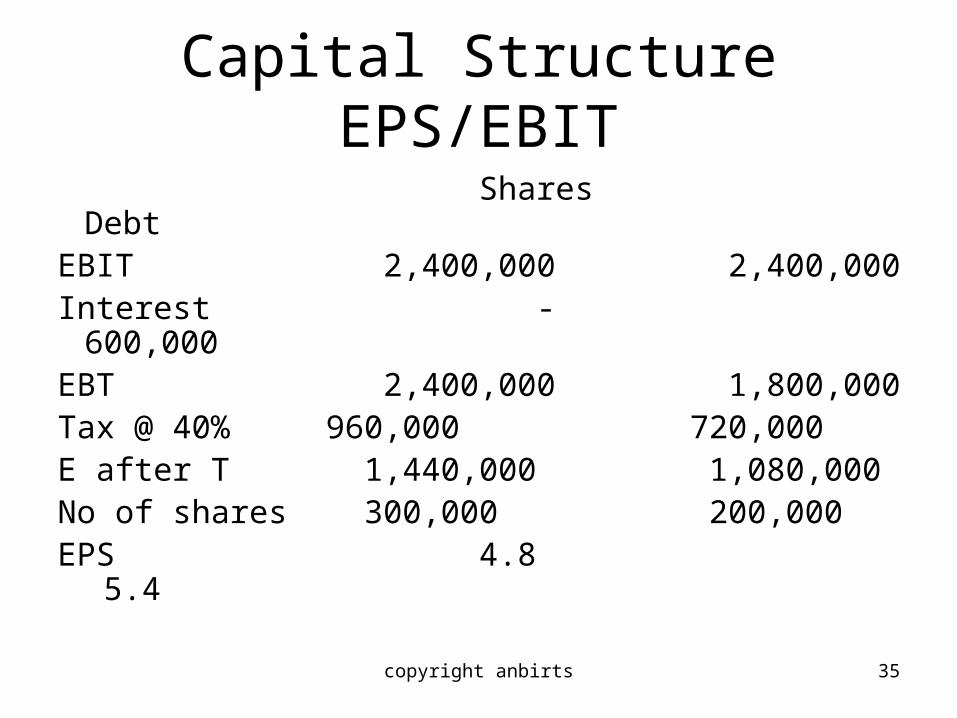

Capital StructureEPS/EBIT

Shares DebtEBIT 2,400,000 2,400,000Interest - 600,000EBT 2,400,000 1,800,000Tax @ 40% 960,000 720,000E after T 1,440,000 1,080,000No of shares 300,000 200,000EPS 4.8 5.4

copyright anbirts 36

Capital StructureEPS/EBIT

• Break Even Point

E 6P 5S 4 3 * 2 1 0 EBIT 1 2 3 4 5 6 Millions

copyright anbirts 37

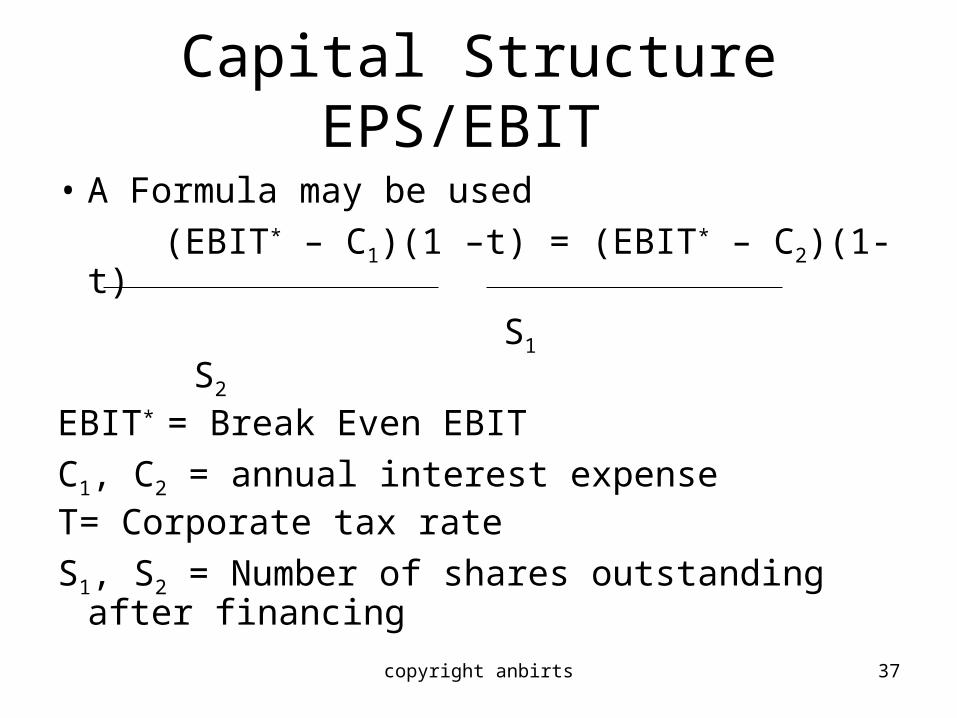

Capital StructureEPS/EBIT

• A Formula may be used

(EBIT* – C1)(1 –t) = (EBIT* – C2)(1-t)

S1 S2

EBIT* = Break Even EBIT

C1, C2 = annual interest expenseT= Corporate tax rate

S1, S2 = Number of shares outstanding after financing

copyright anbirts 38

Capital StructureEPS/EBIT

• (EBIT* - 0)(.6) = (EBIT* - 600,000)(.6) 300,000 200,000 .6(EBIT*)(200,000) = .6(EBIT*)(300,000) – .6(600,000)(300,000)60,000EBIT* = 108,000,000,000EBIT* = 1,800,000

copyright anbirts 39

Cost of CapitalObjective is to minimise cost of capital

Risk Free Rate

Types Debt Sources

Cost of Capital

Equity

Risk ReturnDividend

Capital growth

-Market - Environment

-Business - Portfolio

-Political

Capital Structure