Copyright © 2014 Deloitte Tax LLP. All rights reserved. 1 IRS Audit Pitfalls Matthew Pover Deloitte...

51

Copyright © 2014 Deloitte Tax LLP. All rights reserved. 1 IRS Audit Pitfalls Matthew Pover Deloitte Tax LLP

-

Upload

diane-carr -

Category

Documents

-

view

223 -

download

7

Transcript of Copyright © 2014 Deloitte Tax LLP. All rights reserved. 1 IRS Audit Pitfalls Matthew Pover Deloitte...

Copyright © 2014 Deloitte Tax LLP. All rights reserved.1

IRS Audit Pitfalls

Matthew Pover

Deloitte Tax LLP

Copyright © 2014 Deloitte Tax LLP. All rights reserved.2

Agenda

• Setting the Stage for an IRS Examination

• Federal Issues– Non-Cash Items-fringe benefits– Worker Classification– Payroll Tax Deposit Timing & Rate– Severance FICA Refunds – Quality Stores– DOMA

• State Issues– Worker Classification– CA’s position for UI on Expats– Mobile Workforce Taxation

Copyright © 2014 Deloitte Tax LLP. All rights reserved.3

Fringe benefits

Copyright © 2014 Deloitte Tax LLP. All rights reserved.4

Fringe Benefits

• There was an update regarding company-provided mobile devices in IRS Notice 2011-72– De minimis personal use is non taxable if there are business reasons for

providing the device– Examples cite to after-hours client/supervisor calls– Taxable if providing device for goodwill of the employee or recruiting tool

• Reimbursement of personal service does not have the same outcome, although IRS may be evolving here– Business use is Ok to reimburse; guidance says expectation is not 100%

of total bill

• Consider taxable allowance as non-threatening HR position and minimal expense burden

Copyright © 2014 Deloitte Tax LLP. All rights reserved.5

Fringe Benefits

These taxable items are of IRS concern:

• Gift cards• Tablets, raffle prizesAwards and prizes

• “President’s Club, Diamond Club, Century Club”

• Spousal accompanimentAward trips

• Occasional tickets are considered di minimisSports Tickets

• Subsidy is OK; free is notCompany cafeteria

Copyright © 2014 Deloitte Tax LLP. All rights reserved.6

Fringe Benefits

These taxable items are of IRS concern:

• Subsidized gym dues are taxableWellness programs

• House hunting trips are taxable• Commuting is taxable, even if done via

flight Relocation

• Personal use• Gas cardsCompany cars

Copyright © 2014 Deloitte Tax LLP. All rights reserved.7

Worker Classification

Copyright © 2014 Deloitte Tax LLP. All rights reserved.8

Worker Classification

• Employers must withhold income taxes, withhold and pay Social Security and Medicare taxes, and pay unemployment tax on wages paid to an employee

• Employers do not generally have to withhold or pay any taxes on payments to independent contractors

• Reclassification by the IRS could result in an assessment against the business for back taxes, substantial penalties, and interest

• Employers generally have the burden of proof in disputes with the IRS

Copyright © 2014 Deloitte Tax LLP. All rights reserved.9

Worker Classification

• Former employees cannot usually be a contractor• Form 1099 & Form W-2• Form 1099 — Multiple years• Industry focus• No perpetual contracts• Leads

– IRS internal database– Contractor originated compliant– State info sharing

Copyright © 2014 Deloitte Tax LLP. All rights reserved.10

Worker Classification

Common misconceptions of worker classification:

• Project workers are not employees

• Temporary workers are not employees

• Former executives returning as “consultants” are independent contractors

Copyright © 2014 Deloitte Tax LLP. All rights reserved.11

Worker Classification

Why is worker classification important?

Increased audit focus

• IRS Employment Tax Research Study (began Feb 2010)

• The IRS has entered into data sharing agreements with various state agencies and the Department of Labor to increase its compliance efforts around worker misclassification

• California, New York, and Massachusetts have begun to provide referrals to the IRS regarding worker misclassification cases

New Voluntary Classification Settlement Program (VCSP) launched

• Great opportunity to resolve past worker classification issues at a reduced cost by voluntarily reclassifying workers

Copyright © 2014 Deloitte Tax LLP. All rights reserved.12

Worker Classification

Worker Payor’s withholding obligations

Independent contractors None

Common law employees Federal income tax, Social Security, Medicare, and state tax (if any)

Statutory employees* Social Security and Medicare

Statutory nonemployees** None

*Statutory employees• Independent contractors under the common law rules, but may nevertheless be treated as employees

by statute for FICA purposes• Who are they? Full-time traveling or city salespersons, full-time life insurance agents, agent-drivers

engaged in distributing certain food, home workers performing work on material or goods furnished by the employer

**Statutory Nonemployees• Treated as self-employed for all Federal tax purposes, including income and employment taxes • Who are they? Direct sellers and licensed real estate agents

Copyright © 2014 Deloitte Tax LLP. All rights reserved.13

Worker Classification

FIT definition of employee

• An “employee” is any individual who performs services for another if the relationship between the worker and the person for whom he is performing such service has the legal relationship of employer and employee

• An “employer-employee” relationship exists if the person for whom the services are performed has the right to control and direct the individual performing the services

• However, if the individual is only subject to the direction and control of another as to the result of the work and not as to the means and methods for accomplishing that result, then the individual may possibly be characterized as an independent contractor

Copyright © 2014 Deloitte Tax LLP. All rights reserved.14

Worker Classification

FICA, FUTA definition of employee

The definition of an “employee” includes four groups of workers:• Officers of a corporation• Individuals satisfying the common law definition of employee• Statutory employees• Any individual performing services included in an agreement

entered into pursuant to Section 218 of the Social Security Act

Copyright © 2014 Deloitte Tax LLP. All rights reserved.15

Worker Classification

Rev. Rul. 87-41 — Twenty common law factors

1. Instructions

2. Training

3. Integration

4. Personal services

5. Hire, pay assistants

6. Continuing relations

7. Set work hours

8. Full time required

9. Employer’s premises

10. Order, sequence set

11. Oral, written report

12. Hour, week, month pay

13. Business expense pay

14. Furnish tools and materials

15. Significant investment

16. Realize profit, loss

17. More than one employer

18. Services available to public

19. Right to discharge

20. Right to terminate

Copyright © 2014 Deloitte Tax LLP. All rights reserved.16

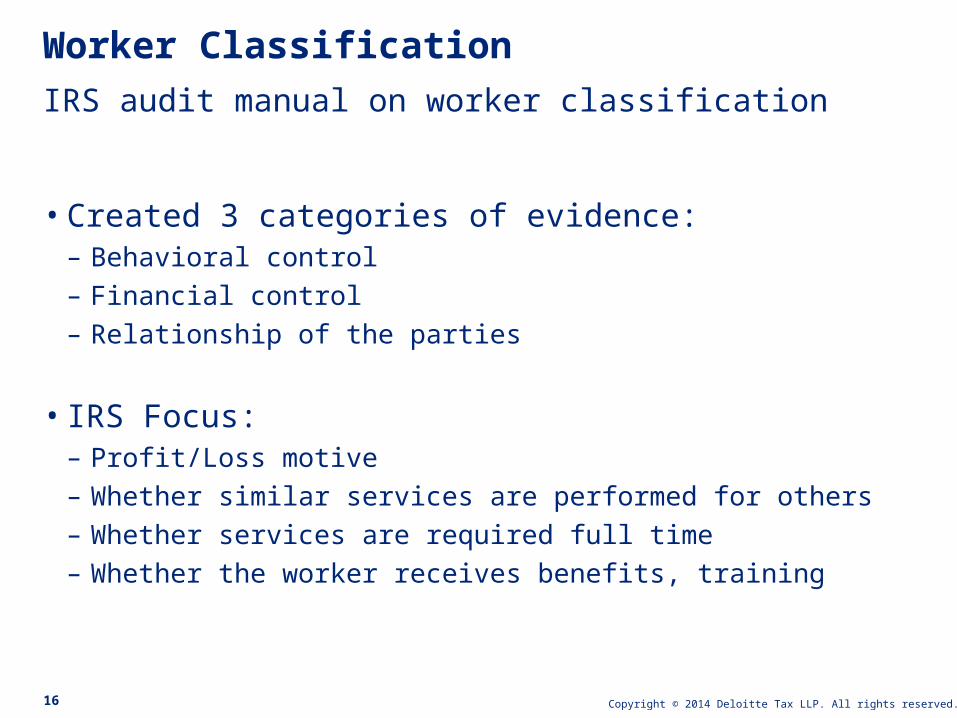

Worker Classification

IRS audit manual on worker classification

• Created 3 categories of evidence:– Behavioral control– Financial control– Relationship of the parties

• IRS Focus:– Profit/Loss motive– Whether similar services are performed for others– Whether services are required full time– Whether the worker receives benefits, training

Copyright © 2014 Deloitte Tax LLP. All rights reserved.17

Worker Classification

State unemployment ABC test

• Many states adopt the “ABC test” for state unemployment tax purposes.A. Is the worker free from control and direction in the performance of

the work

B. Are the services outside the usual course of the business for which such service is performed

C. Is the worker engaged in an independently established trade, occupation, profession, or business

• The ABC test is considered much more inclusive than the IRS test

Copyright © 2014 Deloitte Tax LLP. All rights reserved.18

• Section 530 of the Revenue Act of 1978• If the business misclassified an employee as an

independent contractor but:– Filed Form 1099 MISC,– Did not treat the worker or any similar worker as an employee after

1978, and – Has a reasonable basis

• Then the business may continue to treat the employee as an independent contractor– Retroactively and prospectively– Employment tax purposes only– Benefit plans have been drafted to exclude these workers

“Section 530 Relief”

Copyright © 2014 Deloitte Tax LLP. All rights reserved.19

• Reasonable basis:– Judicial precedent – Past IRS audit – Industry practice – Other reasonable basis

• Not available to businesses that provide the following categories of workers to clients:– Engineer – Designer– Drafter – Computer programmer – Systems analyst – Similarly skilled workers

“Section 530 Relief” (cont.)

Copyright © 2014 Deloitte Tax LLP. All rights reserved.20

• § 3509 applies where Section 530 Relief is not available and gives reduced rates for income tax withholding and the employee's share of FICA

• If failed to deduct and withhold any tax with respect to any employee by reason of misclassification, the amount of the employer’s liability for:– FIT will be equal to 1.5% of wages paid to such employee; and

– The employee portion of FICA will be determined as if the taxes imposed were 20% of the amount that should have been withheld.

– The employer portion must also be paid, as well as FUTA and State Unemployment taxes

– Amounts are double if no reporting has occurred

• Courts have ruled that reclassified individuals are eligible for employee benefits, such as stock options, deferred compensation and health coverage

Paying for misclassification

Copyright © 2014 Deloitte Tax LLP. All rights reserved.21

• Available only to businesses facing an IRS audit

• Procedure for CSP – If entitled to section 530 relief, then no assessment

– If not entitled, then auditors determine eligibility for CSP settlement offers (auditors generally take their cases to IRS Appeals at this stage)

• Eligibility for CSP – If the business meets the section 530 reporting consistency but clearly does

not meet either substantive consistency or reasonable basis test, then the CSP offer will be a full employment tax assessment for the one taxable year under examination computed using section 3509.

– If the business meets the section 530 reporting consistency, but has a colorable argument that it meets the substantive consistency requirement and the reasonable basis test, the offer will be an assessment of 25 percent of the employment tax liability for the audit year computed using section 3509

Classification settlement program

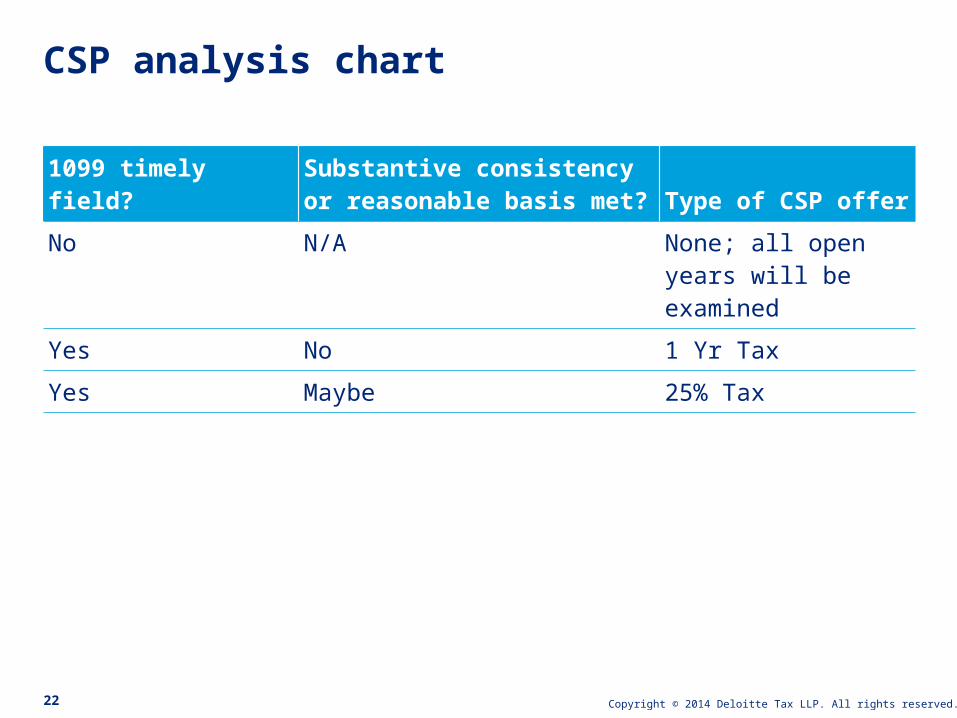

Copyright © 2014 Deloitte Tax LLP. All rights reserved.22

1099 timely field?Substantive consistency or reasonable basis met? Type of CSP offer

No N/A None; all open years will be examined

Yes No 1 Yr Tax

Yes Maybe 25% Tax

CSP analysis chart

Copyright © 2014 Deloitte Tax LLP. All rights reserved.23

• A new IRS program that allows employers to resolve past worker classification issues at a reduced cost by voluntarily reclassifying their workers

• Available to businesses, tax-exempt organizations and government entities that currently erroneously treat their workers as independent contractors, and would like to correctly treat them as employees in the future

Voluntary worker classification settlement program

Copyright © 2014 Deloitte Tax LLP. All rights reserved.24

• To be eligible, an applicant must:

i. Consistently have treated the workers in the past as nonemployees

ii. Have filed all required Forms 1099 for the workers for the previous three years

iii. Not currently be under audit by the IRS, and not currently be under audit by the DOL or a state agency concerning the classification of these workers

Eligibility for Voluntary Program

27

Copyright © 2014 Deloitte Tax LLP. All rights reserved.25

• Reduced cost – Just over one percent of the wages paid to the reclassified workers

for the past year (10% of the employment tax liability determined under the reduced rates of section 3509(a)),

• No interest or penalties • No audit on payroll taxes related to these workers for prior

years

VCSP agreements

28

Copyright © 2014 Deloitte Tax LLP. All rights reserved.26

• File Form 8952, Application for Voluntary Classification Settlement Program, at least 60 days before beginning treating the workers as employees.

• Special 6-year statute of limitation – For the three years beginning after the date the taxpayer has agreed

under the VCSP closing agreement

How to apply?

29

Copyright © 2014 Deloitte Tax LLP. All rights reserved.27

• Reclassification may raise many issues beyond the increased liability for federal employment taxes– Minimum wage rules– overtime pay– workman’s compensation– employee benefit plans– insurance policies – employment discrimination

Other issues

30

Copyright © 2014 Deloitte Tax LLP. All rights reserved.28

E.g. Tax Year 2010 3509(a) Rate 3509 (b) Rate

ER Share of FICA 7.65% 7.65%

EE Share of FICA 1.53% (20% of 7.65%) 3.06% (40% of 7.65%)

Total FICA 9.18% 10.71%

ITW 1.50% 3.00%

Total 10.68% 13.71%

Tax rate comparison

No Relief Section 530 Relief

CSP 1 YR CSP 25% VCSP 10%

Tax Rate 13.71% + Penalties and interest

N/A 10.68% 2.67% 1.07%

31

Copyright © 2014 Deloitte Tax LLP. All rights reserved.29

• Evaluation process– Review contractors by applying either the ABC or 20 Factor test

• Required documentation– Maintain sufficient documentation to substantiate relationship– W-9, business cards, advertisements, invoices, web page

• Written contract – Preferable drafted by the vendor

• Common misconceptions– Project workers are not employees– Temporary workers are not employees– Former executives returning as “consultants” are independent

contractors

Procedures for proper classification

33

Copyright © 2014 Deloitte Tax LLP. All rights reserved.30

Payroll Tax Deposit Timing

Copyright © 2014 Deloitte Tax LLP. All rights reserved.31

• Typically, the date the compensation becomes taxable, will trigger the employment tax liability. The deposit date for that liability, will be based on the employer’s payroll deposit filing status. – Monthly deposit schedule — deposit due by the 15th day of the following

month.

– Semi-weekly deposit schedule• If the payday falls on a Wednesday, Thursday, and/or Friday, then deposit taxes by

the following Wednesday.

• If the payday falls on a Saturday, Sunday, Monday and/or Tuesday, then deposit taxes by the following Friday

– Deposits are due on business days, if a due date falls on a Saturday, Sunday, or legal holiday, the deposit is considered timely if it is made on the following business day.

– There is a next day deposit requirement once the accrued payroll tax liability exceeds $100,000 (“one day deposit rule”)

What is the payroll deposit date?

Copyright © 2014 Deloitte Tax LLP. All rights reserved.32

Typical liability dates

• Exercise date (T+3)NQSOs:

• Exercise dateSARs:

• Vesting date (or transfer date if 83(b) election is made)RS:

• Vesting for FICA and stock delivery for FITRSUs:

Copyright © 2014 Deloitte Tax LLP. All rights reserved.33

• On March 14, 2003, a Memorandum was issued by the IRS to audit examiners to provide guidelines surrounding assessment of employment tax penalties for NQSOs.– “It has been argued that the shares (or the value of the shares) are not available to the

exerciser of the options until settlement date, and therefore no actual or constructive payment of wages takes place until that time.

– There is generally only a three day delay between time of exercise and time of settlement resulting from such exercise. In fact, under 17 C.F.R. Sec. 240.15c6-1(a), the SEC generally established a maximum three day settlement period for broker- dealer trades. There is presently no specific published guidance relative to whether the date of exercise or date of settlement is the appropriate date for considering assertion of the penalty for failure to deposit employment taxes attributable to the exercise of nonqualified stock options.”

• Under this Field Directive, auditors “should not challenge the timeliness of deposits required under Treas. Reg. § 31.6302-1(c), if such deposits are made within one day of the settlement date, as long as such settlement date does not fall more than three days from date of exercise.”

Field audit memorandum

Copyright © 2014 Deloitte Tax LLP. All rights reserved.34

• Underpayment penalty– 2% — One to five days late;

– 5% — Six to 15 days late; and

– 10% for more that 16 days late

• Weekends and holidays are included when calculating penalties

Penalties

Copyright © 2014 Deloitte Tax LLP. All rights reserved.35

• The IRS uses a First In First Out system to assign deposits, and will attribute a deposit to the most recent tax liability, even if a deposit was missed and the deposit actually relates to a later-dated liability. Unfortunately, this can cause a cascading penalty.

• Taxpayers can designate to which tax period they want a specific deposit applied within 90-days of receipt of a notice of penalty.

• The IRS does allow a “safe-harbor” shortfall if the shortfall is no more then the greater of $100 or 2% of the amount due, so long as the original deposit is made timely, and the shortfall is made up by the ‘make-up date.’– Example: A is required to make a deposit of $1,000 on June 15 and is a semi-

weekly depositor. A makes a deposit of $900 on June 15 and would be required to make the additional $100 deposit by the first Wednesday or Friday occurring on our after July 15th. Because the shortfall is $100 and they have made up the deposit by the make-up date, no penalties are assessed.

Penalties

Copyright © 2014 Deloitte Tax LLP. All rights reserved.36

• Executives– 39.6% supplemental withholding applies once the individual

exceeds $1M in supplemental wages for the year

– W-4 withholding is not available for supplemental wages at that point

• Exempts– It is possible for an employee to submit a W-4 claiming

exemption from income tax withholding

– Must be renewed each calendar year

– Does not suppress FICA

Withholding for executives and exempts

Copyright © 2014 Deloitte Tax LLP. All rights reserved.37

U.S. Domestic business travelers

Copyright © 2014 Deloitte Tax LLP. All rights reserved.38

• Many states have not established a de minimus reporting threshold, which creates administrative challenges to achieving full compliance.

• Many states define the employer withholding obligations as an approximation of what the employee is anticipated to owe in taxes.

• Standard deductions and/or personal exemptions may provide a de minimus limit for determining when a tax filing obligation arises.

What are the concerns with domestic travel?U.S. Domestic business travelers

Copyright © 2014 Deloitte Tax LLP. All rights reserved.39

U.S. Domestic business travelers (cont.)

California Connecticut

Very aggressive regarding non-resident wage withholding and tax remittances

No De Minimis threshold

De Minimis threshold14 days

Illinois New York

No De Minimis threshold De Minimis threshold14 days

December 2, 2009 CT issued Announcement 2009(9) requiring employer wage reporting and tax withholding for non-residents working 14 or more days in CT throughout the year

Has quite ‘favorable’ non-resident guidelines — Especially if firm is not located anywhere in IL

Uses an informal calendar year de minimis threshold for state tax withholding for a non-resident working in New York as reported in its state Field Audit Guidelines issued July 1, 2004 and TSB-M-12(5)I issued on July 5, 2012

Copyright © 2014 Deloitte Tax LLP. All rights reserved.40

U.S. Domestic Travelers: Suggested Employer Practices

Withholding for active employees should be in location(s) where work is or was performed (because the Company likely has nexus there).

• Even if this is a temporary work location.

• Even if it’s a jurisdiction in which the employee is a non-resident.

• Even if it requires looking back to prior periods for sourcing (bonus/equity)

Copyright © 2014 Deloitte Tax LLP. All rights reserved.41

U.S. Domestic Travelers: Suggested Employer Practices

Assuming the Company has nexus there, withholding for active employees should be in location(s) where employee is a resident:

• If there is no tax assessed in the actual work state.

• If there’s a higher tax rate assessed in the residence state than in the work state, then often the difference in work state and residence state should be withheld in the residence state.

Copyright © 2014 Deloitte Tax LLP. All rights reserved.42

U.S. Domestic Travelers: Suggested Employer Practices

Find an owner of the process

• Tax or Finance are the likely candidates

Bring relevant team members

• Tax, Payroll, Stock Admin, Legal

Don’t limit the analysis to payroll

• Nexus: Corporate income, sales, and use taxes

Copyright © 2014 Deloitte Tax LLP. All rights reserved.43

U.S. Domestic Travelers: Suggested Refinements for 2014

Find travelers

• Trip reports from corporate travel desk

• Accounts payable expense reports

• Administrative assistant calendars

• Hint: Start at top of executive hierarchy and work down from there; include sales teams

• Watch “move-ins” and “move-outs”

Copyright © 2014 Deloitte Tax LLP. All rights reserved.44

U.S. Domestic Travelers: Suggested Refinements for 2014

Analyze Exposure: Consider elements

• All compensation (cash, equity, taxable fringe, etc.)

• Estimate state penalty of 10% for failure to withhold

Permanent v. Temporary Transfer

• Taxable living expenses if paid for permanent or long-term assignment

Gross-Up/Tax Preparation Assistance

Copyright © 2014 Deloitte Tax LLP. All rights reserved.45

Other federal issues

Copyright © 2014 Deloitte Tax LLP. All rights reserved.46

• IRS clarified that for federal purposes, a same-sex marriage valid in a U.S. state, District of Columbia, U.S. territory, or a foreign country will be recognized for U.S. federal tax purposes.

• Applies regardless of current state of residence.

• Applies to all federal tax provisions where marriage is a factor.

• Amended tax returns may be filed for open statute of limitations year(s)—generally 2010 and later.

• 2010 statutes expired on April 15, 2014

DOMA impact: Rev. Rul. 2013-17

Copyright © 2014 Deloitte Tax LLP. All rights reserved.47

• File Form 941-X for the 4thQ of each open year

• Write “WINDSOR” on the top of Page 1

• Correct applicable Social Security and Medicare wages/tax

• No refund of FIT

• W-2c’s are required

DOMA impact: Notice 2013-61 - Prior Year Refund

Copyright © 2014 Deloitte Tax LLP. All rights reserved.48

• Severance is subject to FICA

• Supplemental unemployment benefit (SUB) plans can be exempt from FICA, but they are distinguishable from severance.

• Continue to withhold FICA on severance payments.

• No action item on previously filed refund claims.

Severance is subject to FICA -Supreme Court decided in favor of IRS

Copyright © 2014 Deloitte Tax LLP. All rights reserved.49

Matthew PoverManagerDeloitte Tax LLP+1 [email protected]

Contact information

Copyright © 2014 Deloitte Tax LLP. All rights reserved.50

This presentation contains general information only and Deloitte is not, by means of this presentation, rendering accounting, business, financial, investment, legal, tax, or other professional advice or services. This presentation is not a substitute for such professional advice or services, nor should it be used as a basis for any decision or action that may affect your business. Before making any decision or taking any action that may affect your business, you should consult a qualified professional advisor. Deloitte shall not be responsible for any loss sustained by any person who relies on this presentation.

Copyright © 2014 Deloitte Tax LLP. All rights reserved.51

About DeloitteDeloitte refers to one or more of Deloitte Touche Tohmatsu Limited, a UK private company limited by guarantee, and its network of member firms, each of which is a legally separate and independent entity. Please see www.deloitte.com/about for a detailed description of the legal structure of Deloitte Touche Tohmatsu Limited and its member firms. Please see www.deloitte.com/us/about for a detailed description of the legal structure of Deloitte LLP and its subsidiaries. Certain services may not be available to attest clients under the rules and regulations of public accounting.

Copyright © 2014 Deloitte Development LLC. All rights reserved.Member of Deloitte Touche Tohmatsu Limited