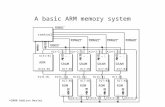

Copyright © 2008 Pearson Addison-Wesley. All rights reserved. Chapter 6 Determining Market Interest...

20

Copyright © 2008 Pearson Addison-Wesley. All rights reserved. Chapter 6 Determining Market Interest Rates

-

Upload

suzan-pope -

Category

Documents

-

view

213 -

download

1

Transcript of Copyright © 2008 Pearson Addison-Wesley. All rights reserved. Chapter 6 Determining Market Interest...

Copyright © 2008 Pearson Addison-Wesley. All rights reserved.

Chapter 6

Determining Market Interest Rates

Copyright © 2008 Pearson Addison-Wesley. All rights reserved. 6-2

Views of Bond Market

We can view the buyer of bonds and the seller of bonds in 2 ways:

1) The bond is the good: the lender is buying the bond and the borrower is selling the bond. Price = amount lender pays

2) Use of funds is the good: the borrower is buying the use of funds and pays with a promise to repay. Price = interest rate

Copyright © 2008 Pearson Addison-Wesley. All rights reserved. 6-3

Buyer

Lender buys the bond Borrower raising funds

Borrower selling bond

Lender supplying funds

Bond price Interest rate

Seller

Price

Bond is the Good Use of Funds is the Good

Copyright © 2008 Pearson Addison-Wesley. All rights reserved. 6-4

Figure 6.1 Demand for Bonds by Lenders

Copyright © 2008 Pearson Addison-Wesley. All rights reserved. 6-5

Figure 6.2 Supply of Bonds by Borrowers

Copyright © 2008 Pearson Addison-Wesley. All rights reserved. 6-6

Figure 6.3 Equilibrium in Markets for Bonds and Loanable Funds

Copyright © 2008 Pearson Addison-Wesley. All rights reserved. 6-7

Explaining Changes in Equilibrium Interest Rates

• Changes in bond demand or supply will change the bond price and interest rate.

• Theory of portfolio allocation can explain bond demand curve shifts.

• Changes in willingness and ability to borrow shifts the supply curve.

Copyright © 2008 Pearson Addison-Wesley. All rights reserved. 6-8

Figure 6.4 Shifts in the Demand for Bonds

Copyright © 2008 Pearson Addison-Wesley. All rights reserved. 6-9

Factors Shifting Increasing Bond Demand

• Higher wealth• Higher expected returns on bonds• Lower expected inflation• Lower expected return on other assets• Lower relative riskiness of bonds• Higher relative liquidity of bonds• Lower relative information costs of bonds

Copyright © 2008 Pearson Addison-Wesley. All rights reserved. 6-10

Factors Increasing Bond Supply

• Higher expected profitability of capital

• Lower business taxes

• Lower expected inflation

• Higher government borrowing

Copyright © 2008 Pearson Addison-Wesley. All rights reserved. 6-11

Figure 6.5 Shifts in the Supply of Bonds

Copyright © 2008 Pearson Addison-Wesley. All rights reserved. 6-12

Figure 6.6 Interest Rate Changes in an Economic Downturn

Copyright © 2008 Pearson Addison-Wesley. All rights reserved. 6-13

Figure 6.7 Expected Inflation and Interest Rates

Copyright © 2008 Pearson Addison-Wesley. All rights reserved. 6-14

The International Capital Market and the Interest Rate

• Closed Economy: an economy that neither borrows nor lends to foreign countries

• Open Economy: capital is mobile internationally

• World real interest rate (rw): the interest rate that is determined in the international capital market

Copyright © 2008 Pearson Addison-Wesley. All rights reserved. 6-15

Figure 6.8 Flow of Funds in an Open Economy

Copyright © 2008 Pearson Addison-Wesley. All rights reserved. 6-16

Open Economies

• Small open economy: the quantity of loanable funds supplied is too small to affect the world interest rate and the economy takes rw as given

• Large open economy: an economy that is large enough to affect the world interest rate

Copyright © 2008 Pearson Addison-Wesley. All rights reserved. 6-17

Figure 6.9 Determining the RealInterest Rate in a Small Open Economy

Copyright © 2008 Pearson Addison-Wesley. All rights reserved. 6-18

Figure 6.10 Determining the Real Interest Rate in a Large Open Economy

Copyright © 2008 Pearson Addison-Wesley. All rights reserved. 6-19

Table 6.1 Factors That Shift the Demand Curve for Bonds

Copyright © 2008 Pearson Addison-Wesley. All rights reserved. 6-20

Table 6.2 Factors That Shift the Supply Curve for Bonds

![Software Project Management - A Unified Framework [Addison Wesley]](https://static.fdocuments.in/doc/165x107/563db967550346aa9a9d041b/software-project-management-a-unified-framework-addison-wesley.jpg)