Copyright © 2006 by The McGraw-Hill Companies, Inc. All rights reserved. 5-1 Economic Growth:...

83

Copyright © 2006 by The McGraw-Hill Companies, Inc. All rights reserved. 5-1 Economic Growth: History, Empirics and Theory Reading: DeLong/Olney: Macroeconomics; McGraw-Hill; 2006; Chapter 5 Next week: Chapter 4

-

date post

18-Dec-2015 -

Category

Documents

-

view

214 -

download

0

Transcript of Copyright © 2006 by The McGraw-Hill Companies, Inc. All rights reserved. 5-1 Economic Growth:...

Copyright © 2006 by The McGraw-Hill Companies, Inc. All rights reserved.5-1

Economic Growth: History, Empirics and Theory

Reading: DeLong/Olney: Macroeconomics; McGraw-Hill; 2006;

Chapter 5Next week: Chapter 4

Copyright © 2006 by The McGraw-Hill Companies, Inc. All rights reserved.5-2

Questions

Modelling economic growth:

• What are the causes of long-run economic growth?

• What is the “efficiency of labor”?• What is an economy’s “capital intensity”?• What is an economy’s “balanced-growth

path”?• What is “transitory dynamics”?

Copyright © 2006 by The McGraw-Hill Companies, Inc. All rights reserved.5-3

Questions

• How important is fast population-growth as a drag on economic (real income) growth?

• How important is a high saving rate as a cause of economic growth?

• How important is technological and organizational progress for economic growth?

Copyright © 2006 by The McGraw-Hill Companies, Inc. All rights reserved.5-4

Historical/Empirical Questions:

• Why has modern economic growth started?

• What happened post-1973? Productivity slowdown followed by productivity speed-up.– What were the causes?

• Why are some nations so (relatively) rich and other nations so (relatively) poor? What determines catching-up?

Copyright © 2006 by The McGraw-Hill Companies, Inc. All rights reserved.5-5

Policy Questions

• What policies can speed up economic growth?

• What policy mistakes can slow down economic growth?

Copyright © 2006 by The McGraw-Hill Companies, Inc. All rights reserved.5-6

Modelling Long-Run Economic Growth

• We classify the factors that generate differences in productive potentials into two broad groups– differences in the efficiency of labor

• how technology is deployed and organization is used

– differences in capital intensity• how much current production has been set

aside to produce useful machines, buildings, and infrastructure

Copyright © 2006 by The McGraw-Hill Companies, Inc. All rights reserved.5-7

Long-run Economic Growth

• Y/L depends on two factors– the economy’s capital intensity (K/Y)– the efficiency of labor (E)

• The level of Y/L is therefore

t

1

t

t

t

t EY

K

L

Y

Copyright © 2006 by The McGraw-Hill Companies, Inc. All rights reserved.5-8

Before the Industrial Revolution

• Up until 1500, there had been almost zero growth of output per worker

• After 1800, we see large sustained increases in worldwide standards of living– population growth accelerated– output per capita grew

Copyright © 2006 by The McGraw-Hill Companies, Inc. All rights reserved.5-9

Table 5.1 - Economic Growth through Deep Time

Year Population (millions) Real GDP per Capita

5000 BC 5 $ 130

1000 BC 50 160

1 AD 170 135

1000 265 165

1500 425 175

1800 900 250

1900 1,625 850

1950 2,515 2,030

1975 4,080 4,640

2000 6,120 8,175

Copyright © 2006 by The McGraw-Hill Companies, Inc. All rights reserved.5-10

Figure 5.1 - World Population Growth since 1000

Copyright © 2006 by The McGraw-Hill Companies, Inc. All rights reserved.5-11

Premodern Economies

• There are two principal reasons that there were no sustained increases in the productivity of labor before 1500– resource scarcity– expanding populations

Copyright © 2006 by The McGraw-Hill Companies, Inc. All rights reserved.5-12

Premodern Economies

• Natural resources played an important role– as populations grew, the stocks of natural

resources had to be divided among more and more people

– increases in technological capability induce increases in (human) fertility – population growth - that inevitably run into natural-resource scarcity

Copyright © 2006 by The McGraw-Hill Companies, Inc. All rights reserved.5-13

Premodern Economies

• Thomas R. Malthus (late 18th/early 19th century)

– introduced the idea that increases in technology inevitably run into natural resource scarcity• implies that increases in technology lead to

an increase in the size of the population but not to an increase in the standard of living

Copyright © 2006 by The McGraw-Hill Companies, Inc. All rights reserved.5-14

The End of theMalthusian Age

• We no longer live in a Malthusian age– for at least 200 years, new technologies

and better organizations have made improvements in the efficiency of labor possible

– these improvements have not been neutralized by natural-resource scarcity

Copyright © 2006 by The McGraw-Hill Companies, Inc. All rights reserved.5-15

The End of theMalthusian Age

• Could a Malthusian age return?– suppose that the population in the 21st

and 22nd centuries grows at the same rate it did in the 20th century (1.33%)• the population will double in 72/1.33 = 54

years

• In 200 years, there would be nearly 90 billion people on earth

Copyright © 2006 by The McGraw-Hill Companies, Inc. All rights reserved.5-16

The End of theMalthusian Age

• However, it is likely that the population explosion is almost over– the United Nations predicts that the world

population will grow from over 6 billion today to around 10 billion by 2050

– after that, the population increase may stop as birth rates have been on the decline around the world

Copyright © 2006 by The McGraw-Hill Companies, Inc. All rights reserved.5-17

The End of theMalthusian Age

• What caused the end of the Malthusian age?– the pace at which inventions occurred

increased steadily

– by about 1500, technological progress passed the point at which it could offset increased scarcity of natural resources due to population growth

Copyright © 2006 by The McGraw-Hill Companies, Inc. All rights reserved.5-18

The Demographic Transition

• As material standards of living rise far above subsistence, countries undergo a demographic transition– birth rates rise– death rates fall– birth rates fall

Copyright © 2006 by The McGraw-Hill Companies, Inc. All rights reserved.5-19

Figure 5.2 - Stylized Picture of the Demographic Transition

Copyright © 2006 by The McGraw-Hill Companies, Inc. All rights reserved.5-20

The Demographic Transition

• In the world today, not all countries have gone through their demographic transitions– Nigeria, Iraq, Pakistan, and the Congo are

projected to have population growth rates greater than 2% per year over the next generation

Copyright © 2006 by The McGraw-Hill Companies, Inc. All rights reserved.5-21

Figure 5.3 - Expected Population Growth Rates, Present-2020

Copyright © 2006 by The McGraw-Hill Companies, Inc. All rights reserved.5-23

The Industrial Revolution

• The industrial revolution began the era of modern economic growth– new technological leaps revolutionized

industries and generated major improvements in living standards

• Great Britain was the center of the industrial revolution

• Other countries followed

Copyright © 2006 by The McGraw-Hill Companies, Inc. All rights reserved.5-24

The Industrial Revolution

• The new technologies were not confined to Great Britain– they spread rapidly to western Europe

and the United States– they spread less rapidly to southern and

eastern Europe and Japan

Copyright © 2006 by The McGraw-Hill Companies, Inc. All rights reserved.5-25

Figure 5.4 - Industrialized Areas of the World, 1870

Copyright © 2006 by The McGraw-Hill Companies, Inc. All rights reserved.5-26

The Industrial Revolution

• Why did the Industrial Revolution take place in Great Britain and why did it occur around 1800?– the establishment of limited government,

security of property, and freedom of contract in Great Britain after the Glorious Revolution of 1688

– the creation of modern science and the technological tradition of sustained inquiry into how the world worked

Copyright © 2006 by The McGraw-Hill Companies, Inc. All rights reserved.5-27

Shift to American Long-Run Growth, 1800-1973

• During the late 19th century, the capital-output ratio increased greatly– the creation of railroads generated the

possibility of supplying an entire continental market from a single factory

– this encouraged investment by entrepreneurs

Copyright © 2006 by The McGraw-Hill Companies, Inc. All rights reserved.5-28

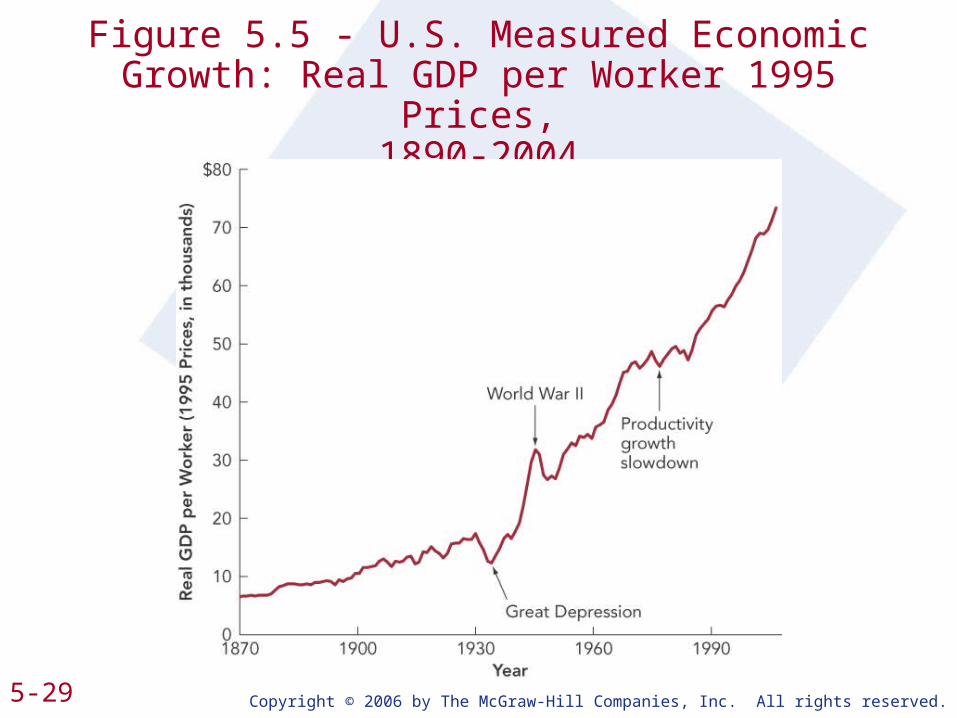

• Growth slowed slightly during the Great Depression and World War II– 1.4 percent per year from 1929 to 1950

• Growth accelerated from 1950 to 1973 (2.1 percent) – all US figures

Copyright © 2006 by The McGraw-Hill Companies, Inc. All rights reserved.5-29

Figure 5.5 - U.S. Measured Economic Growth: Real GDP per Worker 1995 Prices,

1890-2004

Copyright © 2006 by The McGraw-Hill Companies, Inc. All rights reserved.5-30

Measurement problems

• Many economists believe that official estimates of output per worker overstate inflation and understate real economic growth by 1 percent per year– national income accountants have

difficulty to value the boost to productivity and standards of living generated by new inventions (especially product innovations)

Copyright © 2006 by The McGraw-Hill Companies, Inc. All rights reserved.5-32

Factors behind Long-Run Growth, 1800-1973

• Structural changes:– a large drop in the proportion of the labor

force working as farmers occurred– new methods of travel and

communication were developed– a large number of innovative

technologies and business practices were adopted

Copyright © 2006 by The McGraw-Hill Companies, Inc. All rights reserved.5-33

US economic leadership in the 20th century

• The U.S. became the world’s leader (in terms of technology) during the 20th century because– the U.S. had an exceptional commitment

to broad-based education– the U.S. was the largest (integrated)

market in the world– the U.S. was extraordinarily rich in natural

resources– the U.S. avoided (too many) wars

Copyright © 2006 by The McGraw-Hill Companies, Inc. All rights reserved.5-34

Productivity Slowdown after 1973

• Between 1973 and 1995 measured output per worker grew in the US at only 0.6 percent per year– between 1950 and 1973, labor

productivity growth had been 2.1 percent per year

• The other major industrial economies in western Europe, Japan and Canada also experienced a slowdown in productivity

Copyright © 2006 by The McGraw-Hill Companies, Inc. All rights reserved.5-35

Table 5.3 - The Magnitude of the Post-1973 Productivity Growth Slowdown in the G-7

Economies

Output-per-Worker Annual Growth (%)

Country 1950-1973 1973-1995

United States 2.1 0.6

Canada 2.7 1.6

Japan 7.4 2.6

Britain 2.4 1.8

Germany (West) 5.7 2.0

France 4.4 1.5

Italy 4.9 2.3

Copyright © 2006 by The McGraw-Hill Companies, Inc. All rights reserved.5-36

• Suggested causes of the productivity slowdown include– the baby boom generation– the tripling of world oil prices in 1973– environmental protection measures– increased problems of economic

measurement

• The actual causes of the productivity slowdown (the weight of these factors) are still disputed

Copyright © 2006 by The McGraw-Hill Companies, Inc. All rights reserved.5-37

Figure 5.6 - Measured Real Mean Household Income in the US, by Quintile

Copyright © 2006 by The McGraw-Hill Companies, Inc. All rights reserved.5-38

Productivity Growth Speedup: The New Economy

• Since 1995, productivity growth in the U.S. has accelerated – during the second half of the 1990s it was

2.1 percent per year– in the first half of the 2000s, it is 3.8

percent per year

Copyright © 2006 by The McGraw-Hill Companies, Inc. All rights reserved.5-39

Figure 5.7 – Two-Year Growth Rates in Labor Productivity

Copyright © 2006 by The McGraw-Hill Companies, Inc. All rights reserved.5-40

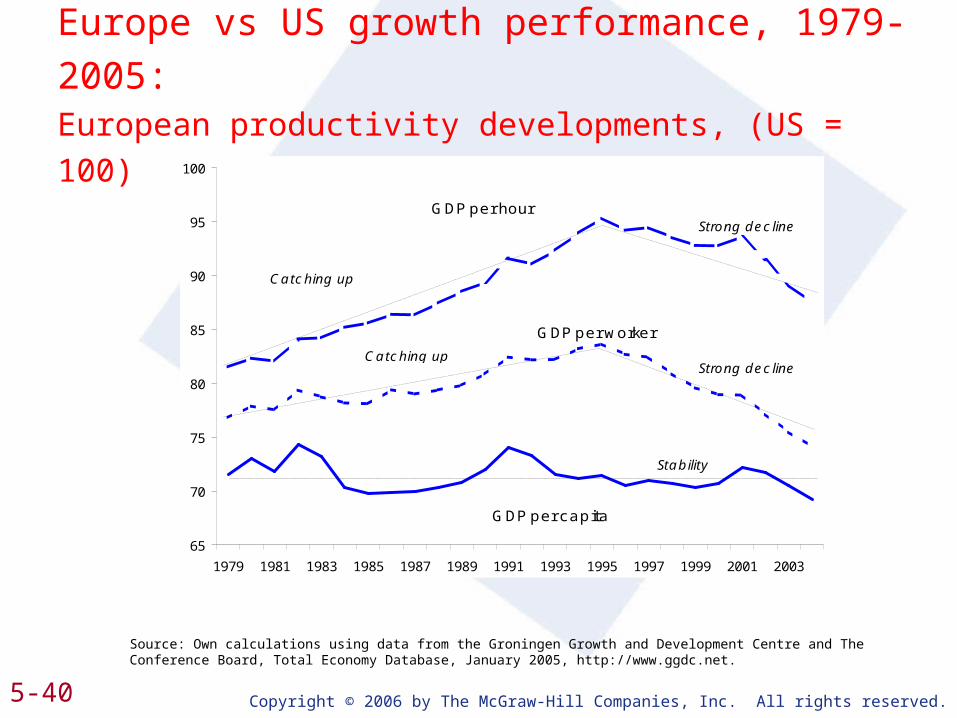

Europe vs US growth performance, 1979-2005:European productivity developments, (US = 100)

Source: Own calculations using data from the Groningen Growth and Development Centre and The Conference Board, Total Economy Database, January 2005, http://www.ggdc.net.

65

70

75

80

85

90

95

100

1979 1981 1983 1985 1987 1989 1991 1993 1995 1997 1999 2001 2003

GDP per hour

GDP per capita

GDP per worker

Catching up

Catching up fast

Strong decline

Strong decline

Stability

Copyright © 2006 by The McGraw-Hill Companies, Inc. All rights reserved.5-41

Productivity Growth Speedup: The New Economy

• Investment began rising in 1992– business fixed investment grew at almost

three times the rate of GDP• much of the additional investment has gone

to purchase computers and related equipment

• The recent acceleration in productivity growth was due to this boom in real investment

Copyright © 2006 by The McGraw-Hill Companies, Inc. All rights reserved.5-42

Productivity Growth Speedup: The New Economy

• Productivity growth continued to be quite rapid during the short recession of 2001, the uneven recovery of 2002, and the faster recovery periods of 2003 and 2004– generally productivity growth slows during a

recession– but business used investment in high-tech

equipment to continue to boost worker productivity during 2001

Copyright © 2006 by The McGraw-Hill Companies, Inc. All rights reserved.5-43

What has happened next?

• Financial turbulence• Will fast growth track be resumed?• What is the impact of globalisation?

Copyright © 2006 by The McGraw-Hill Companies, Inc. All rights reserved.5-44

Modern Economic Growth around the World

• The industrial core of the world economy experienced a large increase in its level of material productivity and living standards during the 19th and 20th centuries

• Elsewhere the growth of productivity levels and living standards was slower

• The world has become a more and more unequal place

Copyright © 2006 by The McGraw-Hill Companies, Inc. All rights reserved.5-45

Figure 5.8 - World Distribution of Income Today, Selected Countries

Copyright © 2006 by The McGraw-Hill Companies, Inc. All rights reserved.5-46

Figure 5.8 - World Distribution of Income Today, Selected Countries

Copyright © 2006 by The McGraw-Hill Companies, Inc. All rights reserved.5-47

Modern Economic Growth around the World

• Convergence processes after WWII:– a number of other countries at different

levels of industrialization, development, and material productivity a century ago have now converged

– their current levels of productivity, economic structures, and standards of living are very close to those of the U.S.

Copyright © 2006 by The McGraw-Hill Companies, Inc. All rights reserved.5-48

Figure 5.9 - Convergence among the G-7 Economies: Output per Capita as a Share

of U.S. Level

Copyright © 2006 by The McGraw-Hill Companies, Inc. All rights reserved.5-49

Modern Economic Growth around the World

• By and large, the economies that have converged belong to the Organization for Economic Cooperation and Development (OECD)– group of countries that gave or received

aid under the Marshall Plan to help rebuild or reconstruct after World War II

Copyright © 2006 by The McGraw-Hill Companies, Inc. All rights reserved.5-52

Modern Economic Growth around the World

• As the OECD countries became richer, they completed their demographic transitions

• Equilibrium capital-output ratios rose• Diffusion of technology (and

consumption patterns) from the U.S. occurred

Copyright © 2006 by The McGraw-Hill Companies, Inc. All rights reserved.5-53

Modern Economic Growth around the World

• Economic growth has not been limited to OECD countries– since World War II, several countries in

east Asia have experienced stronger growth than has ever been seen anywhere in world history

– these successful east Asian countries are somewhat similar to the OECD economies in terms of economic policy and structure

Copyright © 2006 by The McGraw-Hill Companies, Inc. All rights reserved.5-54

European Income Disparities:

GDP and GDP per capita (PPP), 2005

GDP

0

10

20

30

40

50

60

70

80

90

100

0 10 20 30 40 50 60 70 80 90 100

Ukraine BelarusRussia Albania SerbiaMacedonia Bosnia and Herzegovina TurkeyBulgaria Romania Croatia Latvia Poland Lithuania Estonia Slovak Republic HungaryCzech Republic MaltaSlovenia CyprusPortugalGreeceSpainItalyGermanyFranceFinlandSw edenBelgiumUnited KingdomIcelandNetherlandsAustriaDenmarkSw itzerlandIrelandNorw ay

EU-15 and other West European countries

CIS

NMS

ACS

GD

P p

er

ca

pi t

a

SEE

GDP

Copyright © 2006 by The McGraw-Hill Companies, Inc. All rights reserved.5-55

GDP per head, real growth annual averages 1993-2000 and 2000-2006, in percent

EU-25 countries, incl. Bulgaria and Romania

0

1

2

3

4

5

6

7

8

9

EU

-15

EU

-25

Aus

tria

Bel

gium

Ger

man

yD

enm

ark

Fin

land

Fra

nce

Uni

ted

Irel

and

Luxe

mbo

urN

ethe

rland

sS

wed

en

Spa

inG

reec

eIt

aly

Por

tuga

l

Bul

garia

Cze

chE

ston

iaH

unga

ryLi

thua

nia

Latv

iaP

olan

dR

oman

iaS

lova

kia

Slo

veni

a

EU

-15

EU

-25

Aus

tria

Bel

gium

Ger

man

yD

enm

ark

Fin

land

Fra

nce

Uni

ted

Irel

and

Luxe

mbo

urN

ethe

rland

sS

wed

en

Spa

inG

reec

eIt

aly

Por

tuga

l

Bul

garia

Cze

chE

ston

iaH

unga

ryLi

thua

nia

Latv

iaP

olan

dR

oman

iaS

lova

kia

Slo

veni

a

1993-2000 2000-2006

Source: AMECO Database

Copyright © 2006 by The McGraw-Hill Companies, Inc. All rights reserved.5-56

Growth of gross domestic product: Wider Europe

% annual change, 2006 and 2006-2020 forecasts

1.1

2.31.5

2.8

4.1

5.24.8

5.2

7.36.8

6.05.8

8.9

7.4

6.1

3.2

6.86

9.6

12.1

7.1 7

2.3

4.9

6.14.6

6.5

5.6 5.2

2.6

0

2

4

6

8

10

12

14

2003 2004 2005 2006 2006-2015

EU-15 NMS-10 Bu,Ro,Cr Turkey SEE-5 Ukraine

wiiw

Copyright © 2006 by The McGraw-Hill Companies, Inc. All rights reserved.5-57

below 10000

10000 - 15000

15000 - 20000

20000 - 25000

25000 - 30000

above 30000

Regional GDP per head at

PPS, 2005

Copyright © 2006 by The McGraw-Hill Companies, Inc. All rights reserved.5-58

below 0

0 - 1

1 - 2

2 - 3

3 - 4

above 4

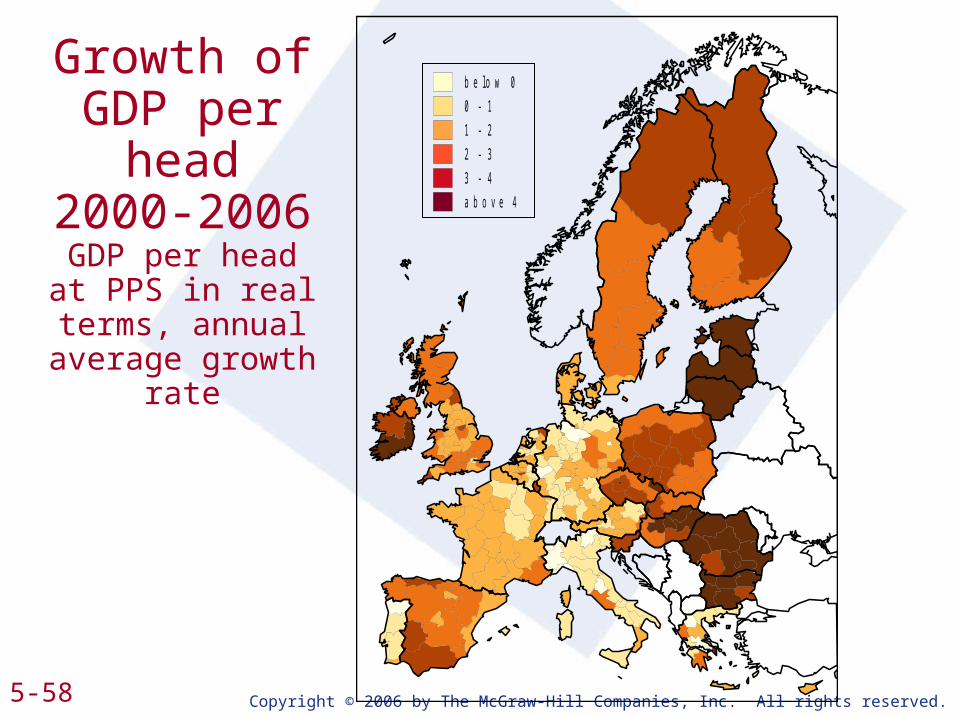

Growth of GDP per

head2000-2006GDP per head at PPS in real terms, annual average

growth rate

Copyright © 2006 by The McGraw-Hill Companies, Inc. All rights reserved.5-59

Copyright © 2006 by The McGraw-Hill Companies, Inc. All rights reserved.5-60

Modern Economic Growth around the World

• Many countries have not been so fortunate

• There has still been enormous divergence in relative output-per-worker levels over the past 100 years

Copyright © 2006 by The McGraw-Hill Companies, Inc. All rights reserved.5-61

Sources of Divergence

• The principal cause of the large variation in output per worker between countries today are differences in their equilibrium capital-output ratios– K/Y is determined by

• the level of investment• the growth rate of the labor force

Copyright © 2006 by The McGraw-Hill Companies, Inc. All rights reserved.5-62

Sources of Divergence

• Two secondary causes of the large variation in output per worker between countries today are – openness to creating and adapting the

technologies that enhance the efficiency of labor

– the level of education today

Copyright © 2006 by The McGraw-Hill Companies, Inc. All rights reserved.5-63

Figure 5.10 - GDP-per-Worker Levels and Average Years of Schooling

Copyright © 2006 by The McGraw-Hill Companies, Inc. All rights reserved.5-64

Cause and Effect,Effect and Cause

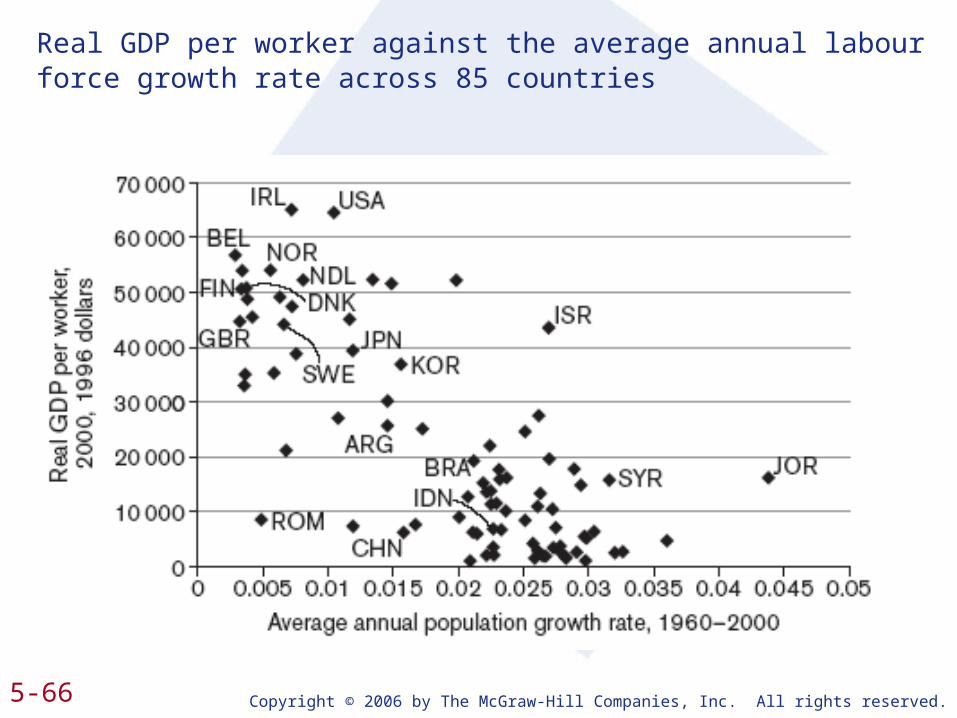

• High population growth and low output per worker go together– rapid population growth reduces the

equilibrium capital-output ratio– poor countries have not undergone their

demographic transitions

Copyright © 2006 by The McGraw-Hill Companies, Inc. All rights reserved.5-65

Figure 4.12 – The Labor Force GrowthRate Matters

Copyright © 2006 by The McGraw-Hill Companies, Inc. All rights reserved.5-66

Real GDP per worker against the average annual labour force growth rate across 85 countries

Copyright © 2006 by The McGraw-Hill Companies, Inc. All rights reserved.5-67

Figure 4.13 - Investment Shares of Output and Relative Prosperity

Copyright © 2006 by The McGraw-Hill Companies, Inc. All rights reserved.5-68

Real GDP per worker against the average investment share across 85 countries

Copyright © 2006 by The McGraw-Hill Companies, Inc. All rights reserved.5-69

Cause and Effect,Effect and Cause

• Other vicious circles can occur– poor countries will have a high relative

price for capital equipment• this implies that poor countries get less

investment out of any given effort at saving

– good education is harder to provide in poor countries

• Setting the demographic transition in motion will offset these problems

Copyright © 2006 by The McGraw-Hill Companies, Inc. All rights reserved.5-71

Hopes for Convergence

• Differences in productivity and living standards between national economies should be eroded over time due to– world trade– migration– flows of capital– developing countries entering the

demographic transition

Copyright © 2006 by The McGraw-Hill Companies, Inc. All rights reserved.5-72

Policies for Saving, Investment, and Education

• Policies to boost saving include– ensuring that savers get a reasonable

rate of return on their savings– reducing restrictions on entrepreneurship– macroeconomic stabiltiy (inflation, gov’t

debt)

Copyright © 2006 by The McGraw-Hill Companies, Inc. All rights reserved.5-73

Policies for Saving, Investment, and Education

• Policies to boost investment for a given level of savings include– foreign investment– allowing businesses to earn and spend

foreign exchange• reducing tariffs and quotas• subsidizing investment and expansion by

businesses that successfully compete in world markets

Copyright © 2006 by The McGraw-Hill Companies, Inc. All rights reserved.5-74

Policies for Saving, Investment, and Education

• Promoting universal access to education can provide two important benefits– a better-educated workforce is likely to be

more productive– educated women will likely pursue

opportunities outside the home• the birth rate will likely fall• the demographic transition will occur more

quickly

Copyright © 2006 by The McGraw-Hill Companies, Inc. All rights reserved.5-75

Policies for Technological Advance

• Technological progress has two components– science– research and development

• amounts to about 3 percent of GDP in the U.S., Scandinavian countries and is Lisbon target

Copyright © 2006 by The McGraw-Hill Companies, Inc. All rights reserved.5-76

Policies for Technological Advance

• Businesses conduct investments in research and development to increase profit

• Research and development is a public good– other firms can copy it– patents limit the ability of other firms to

do so

Copyright © 2006 by The McGraw-Hill Companies, Inc. All rights reserved.5-77

Policies for Technological Advance

• Governments seeking to establish patent laws face a dilemma– if the patent laws are strong, much of the

modern technology in the economy will be restricted in use

– if the patent laws are weak, profits that innovators and inventors can earn will be low• pace of technological improvement will slow

Copyright © 2006 by The McGraw-Hill Companies, Inc. All rights reserved.5-79

Government Failure• Typical systems of regulation in

developing countries have retarded development by– inducing firms and entrepreneurs to

devote their energies to seeking rents– creating systems of regulation and project

approval that have become extortion machines for manufacturing bribes for the bureaucrats

Copyright © 2006 by The McGraw-Hill Companies, Inc. All rights reserved.5-80

Government Failure• Recent thinking about the proper role

of government in economic growth:– the government has a sphere of core

competencies at which it is effective• administration of justice, maintenance of

macroeconomic stability, provision of social insurance, infrastructure development, education

– governments should limit role to their core competencies

Copyright © 2006 by The McGraw-Hill Companies, Inc. All rights reserved.5-81

Summary

• Back before the commercial revolution (before 1500 or so), economic growth was very slow– populations grew at a very slow pace– there were no significant increases in

standards of living for millennia before 1500

– humanity was caught in a Malthusian trap

Copyright © 2006 by The McGraw-Hill Companies, Inc. All rights reserved.5-82

Summary

• The way out of the Malthusian trap opened about 1500– populations grew– standards of living grew– levels of material productivity grew

Copyright © 2006 by The McGraw-Hill Companies, Inc. All rights reserved.5-83

Summary

• The Industrial Revolution was the start of the current epoch: the epoch of modern growth– starting in the mid-18th century, the pace

of invention and innovation increased• key inventions replaced human with machine

power• productivity levels boomed

Copyright © 2006 by The McGraw-Hill Companies, Inc. All rights reserved.5-84

Summary

• Economic growth as described by the standard growth model– output per worker and capital per worker

increase at a pace measured in percent per year• the pace has been extraordinarily rapid in

long-term historical perspective

Copyright © 2006 by The McGraw-Hill Companies, Inc. All rights reserved.5-85

Summary

• Productivity growth rates slowed down worldwide after 1973, causing living standards to rise more slowly in the 1970s and 1980s– several explanations have been offered

for this productivity growth slowdown, but economists generally agree the causes remain a mystery

Copyright © 2006 by The McGraw-Hill Companies, Inc. All rights reserved.5-86

Summary

• Productivity growth rates sped up after 1995 and continue at this higher pace– the acceleration was due to a boom in

real investment in computers and related equipment

Copyright © 2006 by The McGraw-Hill Companies, Inc. All rights reserved.5-87

Summary

• Looking across nations, the world is an astonishingly unequal place in relative terms– the relative gap between rich and poor

nations in material productivity is much greater than it has ever been before

Copyright © 2006 by The McGraw-Hill Companies, Inc. All rights reserved.5-88

Summary

• Combining the determinants of the balanced-growth capital-output ratio with the proximate determinants (the level of technological knowledge and average educational attainment in a country after World War II) accounts for most of the variation in the relative wealth and poverty of nations today

Copyright © 2006 by The McGraw-Hill Companies, Inc. All rights reserved.5-89

Summary

• Macro policies to increase economic growth are policies to– accelerate the demographic transition

(through education)– increase savings rates– boost the amount of real investment a

country gets for a given saving rate– increase the rate of invention or

technology transfer