COPING WITH COVID-19 IN DIFFERING WAYS · March - April 2020 June 2020 Second Covid-19 wave with...

56

Allianz Research Global Economic Outlook July 2020 COPING WITH COVID-19 IN DIFFERING WAYS

Transcript of COPING WITH COVID-19 IN DIFFERING WAYS · March - April 2020 June 2020 Second Covid-19 wave with...

© Copyright Allianz

Allianz Research

Global Economic OutlookJuly 2020

COPING WITH

COVID-19 IN

DIFFERING

WAYS

© Copyright Allianz

01GLOBAL OUTLOOK

© Copyright Allianz 3

March - April 2020 June 2020

Second Covid-19 wave with targeted lockdowns by mid-2021 when a vaccine could be in place.

Haphazard opening in several emerging economies (India, Indonesia, Brazil, Mexico, Turkey,

South Africa) put them at high risk of policy mistake.

Confirmed, notably in the US and the weakest emerging markets.

Return to business as usual, beware of false starts: The global economy would operate at 70

to 80% capacity until Q4 2020.

Confirmed as confidence effects will remain impaired for longer.

Confirmed, supply chain disruptions.

A return to pre-crisis GDP levels by mid-2021: For the manufacturing and construction sectors

where social distancing is less of an issue the return was foreseen at the end of 2021 while the

services sector is was not expected until mid-2021.

Revised to Q4 2021 / Q4 2022 depending on the economy. Trade

will take a few more quarters to reach its pre-crisis given the reshoring

and protectionist growing trend.

Policy bazooka during lockdowns avoid a liquidity crisis. Insolvency wave delayed to H2 2020. Confirmed but the changes in the insolvency laws delays even

further the insolvency wave (+33% by end-2021 vs. +20% in 2020)

Policy support during deconfinement (May-July): targeted relief: shifts the focus from liquidity

to solvency support with targeted and increasingly conditional support.

Confirmed. Several European States announced a prolongation of

the relief support, mainly on partial unemployment schemes along

direct loans to most hit sectors

Policy support during recovery phase (until end-2021): from debt to cash and from deflation to

reflation.

Below expectations. Very little has been announced and no global

coordination which bodes for a lower recovery in 2021. More should

be announced in September but no bazooka expected.

Risks to our scenario (L-shape): (i) prolonged high precautionary savings (households,

companies); (ii) rise in the zombification of companies; (iii) rise in NPLs and fragile banks; (iv) rise

in social inequalities and political risk; (v) policy mistakes (sanitary, fiscal, monetary); (vi) rise in

protectionism and shorter supply chains which could structurally dampen companies margins.

Maintained at 30% probability.

Financial markets: it can still get worse before it gets better On track. Still no strong signals of reentry given the divergence

between equity and bond markets. Continue to expect strong volatility.

FROM MARCH TO JUNE: WHERE DO WE STAND?

© Copyright Allianz

COVID-19: THE PHASE 2 MARATHON

• Expand healthcare capacity (treatment, testing, monitoring)

• Fiscal / monetary safety nets to reduce downside risks & cushion economic blow

Stage 1: Full lockdowns to

'flatten the curve'

• Mass testing, tracking & isolation of new cases

• Ongoing targeted confinement measures incl. border restrictions & event bans

• Policy to focus on boosting economic recovery prospects

Stage 2: Gradual opening of national

economies• Bans on large events & border

restrictions to be eased as pandemics around the globe ends

• Ongoing fiscal & monetary policy support aimed at providing tailwind to rebound

Stage 3: Global economy getting

back on track

• Global rollout allows for return to normalcy without border restrictions, testing & bans on large events

• Policy support can be gradually withdrawn

Stage 4: Habemusvaccine!

Remember we are here!

Fresh virus outbreak –

back to stage 1

Sources: OECD, Allianz Research framework from March 20204

© Copyright Allianz

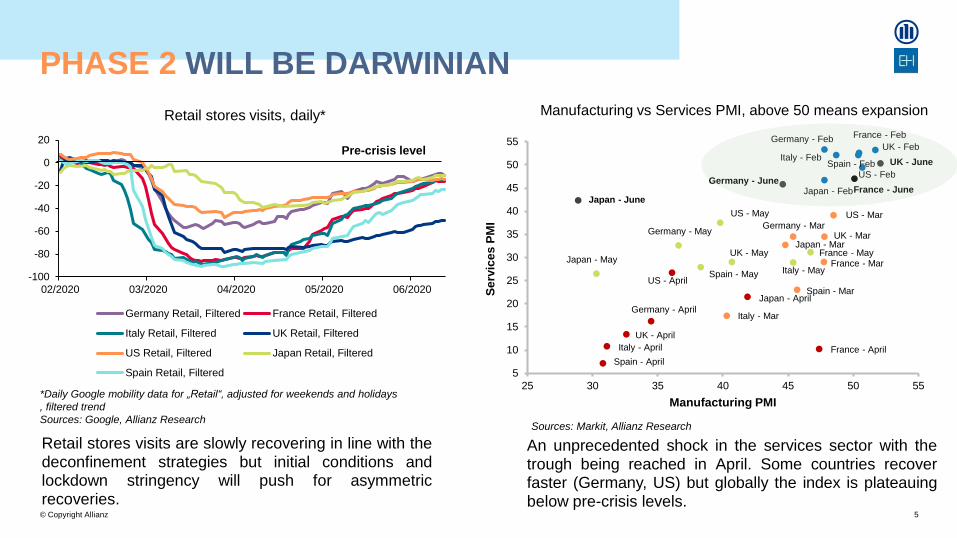

Retail stores visits are slowly recovering in line with thedeconfinement strategies but initial conditions andlockdown stringency will push for asymmetricrecoveries.

PHASE 2 WILL BE DARWINIAN

Retail stores visits, daily*

*Daily Google mobility data for „Retail“, adjusted for weekends and holidays

, filtered trend

Sources: Google, Allianz Research

5

An unprecedented shock in the services sector with thetrough being reached in April. Some countries recoverfaster (Germany, US) but globally the index is plateauingbelow pre-crisis levels.

Manufacturing vs Services PMI, above 50 means expansion

France - Mar

France - Feb

France - May

Germany - Feb

France - April

Germany - Mar

Germany - April

Germany - May

Italy - Feb

Italy - Mar

Italy - April

Spain - Mar

Spain - May

Spain - Feb

UK - Mar

UK - April

UK - May

US - Feb

US - Mar

US - April

US - May

Japan - Feb

Japan - Mar

Japan - April

Italy - May

Spain - April

UK - Feb

Japan - May

Germany - JuneFrance - June

Japan - June

UK - June

5

10

15

20

25

30

35

40

45

50

55

25 30 35 40 45 50 55

Se

rvic

es

PM

I

Manufacturing PMI

Sources: Markit, Allianz Research

-100

-80

-60

-40

-20

0

20

02/2020 03/2020 04/2020 05/2020 06/2020

Germany Retail, Filtered France Retail, Filtered

Italy Retail, Filtered UK Retail, Filtered

US Retail, Filtered Japan Retail, Filtered

Spain Retail, Filtered

Pre-crisis level

© Copyright Allianz

AUT

BEL

BRA

CHN

CZE

DNK

FRA

DEU

INDIDN

ITA

JPNMEXNLD

NOR

POL

RUS

SGP

ZAF

KOR

ESP

TUR

GBRUSA

-40

-30

-20

-10

0

10

20

0.8 0.9 1.0 1.1 1.2 1.3 1.4

Ch

an

ge i

n a

vera

ge s

trin

gen

cy i

nd

ex,

Ju

ne v

s. M

ay

Average effective R0 in June

De-confiningeven though

epidemic may not be clearly under control

0

10,000

20,000

30,000

40,000

50,000

60,000

70,000

1/22/2020 3/22/2020 5/22/2020

Europe AfricaMiddle-East North AmericaLatin America IndiaAPAC excl. India

Many countries still battle with too highR0. Cluster management and physicaldistancing measures could help cap R0for countries with previous lockdowns

It is likely to be long before allcontainment measures are removed.Stringency indices have been faster torise than decline, particularly forinternational travel.

Hot spots include Latin America, theUnited States, United Kingdom and India

NEW WAVELETS: LIGHT AND LOCALIZED LOCKDOWNS

6

Sources: Various, Euler Hermes, Allianz Research Sources: Oxford University, Euler Hermes, Allianz Research Sources: John Hopkins University, Euler Hermes, Allianz Research

De-confining: managing the effective

reproduction rate(bubble size is latest available stringency index)

Stringency indices Daily number of new Covid-19 cases (as of

5 July 2020)

0

10

20

30

40

50

60

70

80

90

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

01-2020 03-2020 05-2020 07-2020

Internationaltravel restrictions

Overallstringency index(rhs)

© Copyright Allianz

GLOBAL ECONOMY: NO RETURN TO PRE-CRISIS

LEVELS BEFORE END OF 2021Real GDP growth, %

World GDP level, Q4 2019 = 100

Sources: National sources, Euler Hermes, Allianz Research

Sources: National sources, Euler Hermes, Allianz Research

7

85

90

95

100

105

110

2019-01 2019-07 2020-01 2020-07 2021-01 2021-07 2022-01

World GDP, Q1'19 = 100

pre-Covid-19 World GDP path

Q4 2019 World GDP level

2021

World GDP growth 3.3 3.1 2.5 -4.7 4.8

United States 2.4 2.9 2.3 -5.3 3.7

Latin America 1.0 1.0 0.1 -6.8 3.1

Brazil 1.3 1.3 1.1 -7.0 3.0

United Kingdom 1.8 1.3 1.4 -13.3 5.0

Eurozone members 2.7 1.9 1.3 -9.0 6.0

Germany 2.8 1.5 0.6 -7.0 4.5

France 2.4 1.8 1.5 -10.8 7.4

Italy 1.7 0.7 0.3 -11.2 6.6

Spain 2.9 2.4 2.0 -11.0 7.0

Russia 1.8 2.5 1.3 -5.2 3.0

Turkey 7.5 2.8 0.9 -4.7 4.2

Asia-Pacific 5.2 4.7 4.2 -1.3 5.9

China 6.9 6.7 6.1 1.5 7.6

Japan 2.2 0.3 0.7 -5.7 2.2

India 7.0 6.1 4.7 -3.6 7.5

Middle East 1.4 0.9 0.3 -6.3 2.2

Saudi Arabia -0.7 2.4 0.3 -4.0 2.0

Africa 3.1 2.7 1.9 -3.1 4.0

South Africa 1.4 0.8 0.3 -7.8 5.4

* Weights in global GDP at market price, 2019

NB: fiscal year for India

2017 2018 2019 2020

Which economies will drive the global recovery? United

States, Germany and China (although a far cry compared

to GFC). Who are the laggards? United Kingdom, France,

Spain, Italy, vulnerable EM (e.g. Latin America, Turkey,

South Africa, India)

Global GDP growth, index

Radical uncertainty on

epidemiological

development, US election,

policy cliff-edge effect

© Copyright Allianz

SECTOR OUTLOOK: DIVERGENT PATH FOR THE

RECOVERY

A&D – Commercial Aerospace

Retail – Non-essential

Retail – Restaurants

Healthcare – Pharmaceuticals

Retail – Essential/Grocery

A&D – Defence Contractors

• Telecom

• Healthcare –

Equipment

• Paper & Packaging

• Cons Prod – Pack-Food/Pers

& Home Care/Agr&Ingr

• Heathcare – Services

• Utilities

• Cons Prod – Tobacco & Alcoholic Beverage

• Business & Consumer Services

• Real Estate (REITs)

• Technology

• Engineering & Construction

• Capital Goods

• Transportation – Shipping

• Building Materials

• Chemicals

• Metals & Mining

• Transport Infra – Toll Roads

• Homebuilders & Developers

• Oil & Gas

• Media & Entertainment

• Leisure – Gaming

• Transport Infra – Rail

• Leisure – Theme park and other visitor

attractions

• Cons Prod – Luxury & Discretionary

• Automotive

• Leisure – Cruise lines

• Transport Infra – Airports

• Transportation – Airlines

• Leisure – Lodging and hospitality

Return to pre-crisis levels of profitability by sector (EMEA)

As a result of Covid-19 we have downgraded a record number of sectors (325) in Q2 2020. The current crisis has led to a

downgrade of 4 in 10 of our sector risk ratings since Q4 2019. In most cases, they were triggered by two factors: the demand

shock and its direct and indirect impact on either the profitability or the liquidity outlook. The most downgraded sectors are

those in the frontlines facing Covid-19 consequences, namely transportation, automotive and retail

Sources: S&P, Euler Hermes, Allianz Research

© Copyright Allianz

Monetary policy response to the Covid-19 crisiswas strong across the world. Among majoreconomies, we estimate that the monetary impulse isthe largest in the U.S.

MONETARY BAZOOKA: UNPRECEDENTED BALANCE

SHEET EXPANSION, DIFFERENTIATED RETURNS Monetary impulse indices

Sources: National central banks, Euler Hermes, Allianz Research

9

-20

-15

-10

-5

0

5

10

15

20

09 10 11 12 13 14 15 16 17 18 19 20

United States Eurozone

China Japan

United Kingdom

As monetary policy continues to backstop sovereignand corporate bond markets to ensure favorablerefinancing conditions, the balance sheets of allmajor central banks will continue to balloon in2020/21, heading towards 50% of GDP.

Central banks‘ balance sheets (% of GDP)

Sources: Refinitiv, Allianz Research.

0

10

20

30

40

50

60

70

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

20

14

20

15

20

16

20

17

20

18

20

19

20

20

20

21

ECB (lhs) BoE (lhs)

PBoC (lhs) FED (lhs)

Forecasts

© Copyright Allianz

Fed committed to ultra forward guidance,rates near 0 through 2022: plausible. ECBprovided weak forward guidance (policypause): be aware of zombie banks

LOOKING FORWARD, EUROPE WILL HAVE TO CARE

FOR ITS BANKS10yr yields on UST & Bund vs. Fed funds

rate and ECB deposit rate (%)

Sources: Refinitiv, Allianz Research.

The most vulnerable sectors alreadyfeature elevated levels of non-performing loans and represent ahigh exposure for banks.

Distribution of banks across NPL ratio

in the EU

The Fed has only bought ~$15bn of tradedcorporate debt and provided $30bn ofcommercial paper (~$750Bn total duringthe GFC crisis). Due to the Feds’ forwardguidance, corporate spreads seem to beunderestimating corporates credit risk.

US Federal Reserve – Corporate

Securities Operations

Sources: EBA, Allianz Research

0

200

400

600

800

1000

1200

0

5

10

15

20

25

30

35

12-1

9

01-2

0

02-2

0

03-2

0

04-2

0

05-2

0

06-2

0

bps$ Bn Corporate Credit

Commercial Paper

Investment Grade Spread (RHS)

High Yield Spread (RHS)

0

10

20

30

40

50

60

0.2-1% 1-2% 2-3% 3-4% 4-10% 18-36%

Num

be

r o

f b

an

ks

NPL ratio

Sources: Refinitiv, Allianz Research.

10

© Copyright Allianz

0.0% 5.0% 10.0% 15.0% 20.0%

Spain

Italy

UK

France

China

Germany

USA

Japan

Realized fiscal relief package

Announced fiscal spending

Expected future recovery stimulus

Emergency fiscal spending ranges from 3% of GDP to18%; the recovery stimulus effort will be a key differencingfactor in the countries’ future trajectories. At the global levelUSD10.4tn of fiscal stimulus has been announced.

The size of automatic stabilizers will matter for the sizeof the fiscal stimulus packages.

FISCAL BAZOOKA: PROMPT BUT UNEQUAL IN SIZE

AND MULTIPLIERS. MORE TO COME?

Direct fiscal spending (% of GDP) Effectiveness of automatic stabilizers one year after the shock

Sources: Various, National sources, Euler Hermes, Allianz Research

NB: the degree to which a decline in market income is offset by automatic stabilizers one

year after the shock. A ratio of 100 implies that automatic stabilizers offset the shock to

market income completely, leaving aggregate household disposable income unchanged

Sources: OECD, Euler Hermes, Allianz Research

11

0

20

40

60

80

100

120

140

Neth

erlands

Germ

any

Sw

itzerlan

d

Fin

lan

d

Au

str

ia

Be

lgiu

m

Irela

nd

Fra

nce

Sw

eden

Canada

Slo

venia

UK

Italy

Cze

chia

Au

str

alia

Po

rtuga

l

Hungary

Slo

vakia

US

A

Jap

an

Sp

ain

Gre

ece

Social security contribution

Unemployment, housing and family benefits

Direct taxes

© Copyright Allianz

28%26% 25%

23% 22%21%

22%

17%

24%21% 21%

19% 18%16%

18%

12%

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

Ge

rma

ny

Ne

the

rlan

ds

Fra

nce

EU

28

Be

lgiu

m

Italy

Sp

ain

UK

Pre-lockdown During lockdown During deconfinement End-2020

In the 5 largest European countries, 9 million workers(20% of those currently partially unemployed) still face anelevated risk of becoming unemployed in 2021 becauseof the muted recovery. These “zombie jobs” require adhoc policies to avoid postponed mass unemployment.

This will continue to feed into precautionary savings. Weestimate savings rate to remain +6pp above pre-crisis levelsat the end of 2020 which represents EUR370bn of excesssavings in the EU, or 2.5% of GDP

THE REAL SECOND WAVE: ZOMBIE JOBS WILL

RESTRAIN CONSUMERS FROM SPENDINGSavings rate, % of gross disposable income

Sources: Eurostat, Allianz Research

Expected loss of employment (% of sectoral employment)

based on expected output loss by end 2021

Source: Allianz Research

-25%

-20%

-15%

-10%

-5%

0%

5%

10%

Tra

nsp

ort

Accom

odation

Constr

uctio

n

En

tert

ain

em

ent

Reta

il and W

hole

sale

Industr

y

Germany France Spain Italy UK

12

© Copyright Allianz

SOCIAL RISK ON THE RISE, FISCAL DILEMMA AHEAD?

Social risk hotspots Taxes – companies vs households (OECD average)

Sources: Euler Hermes, Allianz Research

Sources: OECD, Euler Hermes, Allianz Research

13

© Copyright Allianz

Lockdowns of business courts, temporary policy measuresto support companies and temporary changes in insolvencyregimes are pushing down official registrations ofbankruptcies for the short term – lowering the expectationsfor the full year 2020.

The ending of temporary factors will lead to a massive trendreversal starting in Q3 or Q4 depending on countries. Ourglobal insolvency index would surge by +35% by end of2021 i.e. +by 16% in annual average. Should policy reliefbe withdraw too fast the rises will be +5 to +10pp higher.

THE OTHER REAL SECOND WAVE: A SURGE IN

GLOBAL INSOLVENCIESInsolvency figures and forecasts

(selected countries)

EH Global Insolvency Index (yearly changes in %)

and contribution of regional indices

Sources: Euler Hermes, Allianz Research Sources: Euler Hermes, Allianz Research

14

# of years

with an

increase

CAGR

Changes

over 2007-

2009

Last

pointy/y ytd

2020 vs

2019

2021 vs

2020

2021 vs

2019

U.S. 3 45% 115% March 4% 4% 47% 7% 57%

Canada 0 - -14% April -61% -28% 15% 9% 25%

Brazil 1 25% -8% April -58% -22% 32% 10% 45%

Germany 2 6% 12% March -2% -4% 4% 8% 12%

France 3 11% 27% May -62% -36% 4% 20% 25%

United Kingdom 2 22% 48% March -11% -11% 8% 33% 43%

Italy 2 23% 52% 18% 8% 27%

Spain 3 76% 380% May -57% -57% 20% 17% 41%

The Netherlands 2 32% 74% May 6% 2% 29% 10% 42%

Russia 0 - -62% May -54% -15% 18% 5% 23%

Turkey 2 2% 4% April -1% 4% 22% 7% 31%

South Africa 3 11% 31% March -19% -6% 12% 7% 20%

China 2 12% 2% May 22% 10% 21% 16% 40%

Japan 2 9% 10% May -55% -1% 8% 5% 13%

Australia 2 16% 35% April -42% -18% 5% 5% 11%

South Korea 1 19% -13% May -53% -31% 14% -6% 6%

GLOBAL INDEX 3 16% 46% 17% 16% 35%

2007-2009 crisis 2020 Forecasts

© Copyright Allianz

-40%

-30%

-20%

-10%

0%

10%

20%

03/0

8

11/0

8

07/0

9

03/1

0

11/1

0

07/1

1

03/1

2

11/1

2

07/1

3

03/1

4

11/1

4

07/1

5

03/1

6

11/1

6

07/1

7

03/1

8

11/1

8

07/1

9

03/2

0

11/2

0

07/2

1

UK US China Germany

Companies are in a position to increase theirinvestments during the recovery phase. Increases innet savings in 2020 are the highest in Italy, the UK andFrance. But this will be dependent on renewedconfidence in a lasting restart of growth in Europe.

Public support to reduce companies’ fixed costs (lowersocial contributions, lower corporate taxes and/or fiscalincentives to invest) will be key. Expanding the stateguaranteed loan schemes into 2021 could also besupportive for future company investment.

MIND THE INVESTMENT CYCLE: CONFIDENCE MATTERS

Annual net savings by country, EURbn Total investment, y/y

Sources: Eurostat, Euler Hermes, Allianz Research Sources: National sources, Euler Hermes, Allianz Research

15

© Copyright Allianz

We find that more than 13,000 SMEs & MidCaps (7% of total) in the six biggestEurozone countries were classified zombies before Covid-19 crisis. Low equityratios for some companies has pushed them into high indebtedness since 2009,which will continue to increase thanks to State Guaranteed Loans.

This coupled with already fragile companymargins increases the zombification of thecorporate sector.

ACCELERATING TREND IN ZOMBIFICATION OF

COMPANIES COULD WEIGH ON THE RECOVERY

Sources: Bank of France, Allianz Research Sources: Eurostat, Allianz Research

Equity ratios % of total assets

0%

10%

20%

30%

40%

50%

60%

Be

lgiu

m

Sp

ain

Germ

an

y

Fra

nce

Au

str

ia

Po

rtug

al

Italy

SME Large companies

Sources: BIS, Allianz Research

Non-financial corporations’ debt, % of GDP

0%

20%

40%

60%

80%

100%

120%

140%

160%

180%

Sw

ede

n

Ne

therl

and

s

Fra

nce

Belg

ium

Ch

ina

No

rwa

y

Fin

land

De

nm

ark

Japa

n

Spain

UK

US

Ita

ly

Germ

any

2009 2019

25%

30%

35%

40%

45%

50%

20

07Q

1

20

07Q

3

20

08Q

1

20

08Q

3

20

09Q

1

20

09Q

3

20

15Q

1

20

15Q

3

20

16Q

1

20

16Q

3

20

17Q

1

20

17Q

3

20

18Q

1

20

18Q

3

20

19Q

1

20

19Q

3

EU-27 Germany FranceItaly Belgium

Non-financial corporations’ margins, % of

value added

16

© Copyright Allianz

Trade could plummet by -15% involume terms (-20% in value) due tothe Covid-19 shock on goods and –for the first time – on services.

Assumptions medium-term: reducedUS-China uncertainty but stable tariffs,no immediate threat of massivereshoring, air transport back to pre-crisis in 2023.

The oil and commodity price shock willlead to a negative price effect on tradein 2020. 2021 will see a return to 52.5after an average of 47 in 2020.

TRADE: RETURN TO PRE-CRISIS LEVELS IN 2022/ 2023

17

Sources: Sources: IHS Markit, Allianz Research Sources: International Trade Center, Allianz Research Sources: Bloomberg, Euler Hermes, Allianz Research

Global trade growth, in volume terms and

value (%, y/y)

Medium-term trade in value terms (USDtn) Oil prices and EUR/USD

0.95

1.00

1.05

1.10

1.15

1.20

1.25

1.30

20

30

40

50

60

70

80

90

100

Jun-16 Jun-17 Jun-18 Jun-19 Jun-20 Jun-21

Brent Oil price (lhs) EUR/USD (rhs)

Forecasts

3.3% 4.0%3.0%2.4%

5.5%4.2% 1.3%

-15.0%

8.0%

4.1% 3.2%2.8%

1.9%

-10.8%

-2.0%

10.1%

9.6%

-1.6%

-20%

12.2%

7.5%

5.5%

-25%

-20%

-15%

-10%

-5%

0%

5%

10%

15%

13 14 15 16 17 18 19e 20f 21f 22f 23f

Volume Price Value

18.7

15.417.0

18.7 19.3

2.5

1.1

1.8

2.12.5

0

5

10

15

20

25

30

pre-crisis 2020 2021 2022 2023

Goods Travel and transport services Other services

© Copyright Allianz

Around each recession, supply chains become aconcern. This time around, the concern has peakedamong companies and policy makers. Buildingresilience and reshoring are the new rhetoric.

Arguments in favor of reshoring Arguments against reshoring

Resilience : Reshoring creates

resilience due to lower risks, and

shorter lead times

Social discontent: Growing social

discontent could be incompatible

with reshoring, as it would entail

high labor costs passed down to the

consumer

Strategic sectors: Reshoring

specific supply chains for key

strategic sectors such as the

medical sector, similarly to the

military sector, could make sense

Risk assessment complexity:

Reshoring does not necessarily

mean de-risking: it can also mean

putting all your eggs in the same

basket, leading to excess

concentration

Flexibility: More local supply can

also enhance agility, as companies

can be more responsive to changes

in local demand.

Cost effectiveness and

incentives: Reshoring is hardly

reversible for many sectors, or at a

high cost for companies. Moreover,

Incentives for businesses to reshore

are still lacking

Innovation: Reshoring for cost-

competitiveness reasons is unlikely,

but race for product innovation is

better

Creative destruction: Reshoring is

not only job creation… it’s job

destruction through innovation, for

instance robotization.

TRADE AND RESHORING: TALKING THE TALK BUT

NOT WALKING THE WALK

Number of mentions of “supply chains” in the media

Sources: Bloomberg, Euler Hermes, Allianz Research

18

0

500

1000

1500

2000

2500

92 94 95 97 99 00 02 04 05 07 09 10 12 14 15 17 19

© Copyright Allianz 19

RISKS TO OUR OUTLOOK

H2 2020 2021 Beyond 2021

Upside

risks

Better-than-expected trade flows, tourism receipts

and recovery in the services sector (exports-exposed

economies benefit, e.g. Germany)

Stronger policy support and stimulus (e.g.

European bad bank, UK, China, etc.)

Declining financial risks in domestic financial

system, markets, external financing, etc. (e.g. Italy,

Turkey, China, India, etc.)

Appeased socio-political risks, restoring domestic

and external confidence (e.g. Brazil, Hong Kong,

etc.)

Vaccine available earlier than expected,

tourism returns to pre-crisis levels

Stronger policy stimulus, notably

improving investment and the labour market

(e.g. China, France, United Kingdom, Italy,

etc.)

Oil and commodities prices rebound

(benefitting e.g. Russia, Kazakhstan,

Azerbaijan, the GCC, Latin America, etc.)

Stronger policy stimulus and policy

coordination, resolving structural issues and

supporting potential growth (e.g. EU, Italy, China)

Exports competitiveness improving, notably on

supply chains reshoring (Central Europe, UK,

etc.)

Downside

risks

Strong lockdowns to fight a second Covid-19 wave

Protectionism and slow global trade recovery (e.g.

Germany, UK, trade hubs, etc.)

Sustained risk aversion limiting capital flows to

EMs and pressuring economies with large external

financing needs

Policy mistake (e.g. EU, France, Italy, China, India,

etc.)

Domestic imbalances correction (e.g. German real

estate, Indian financial sector)

Social risks and protests worsen

Protectionism intensifies and global trade

does not recover

Strong lockdowns to fight waves of Covid-

19 outbreaks

Political risk, policy mistakes (e.g. Italy,

EU, UK, India, HK

Sustainably higher unemployment rate,

threatening the consumer-led recovery

(Germany, China

Deteriorating bank asset quality,

sometimes leading to bailouts and feedback

loop (e.g. Italy, France, China, India

Debt distress and currency crises (some

emerging countries, e.g. in Central Europe,

Africa, Latin America)

Protectionism intensifies and calls into question

growth models (Germany, trade hubs, China,

etc.)

Debt sustainability and banking sector

concerns worsen (France, Italy, China, India,

some countries in Africa, etc.)

Lack of structural reforms or missed

opportunities cap productivity (China, India, UK,

Central Europe, etc.)

Fiscal consolidation (U.S., China, etc.)

Socio-political risks heighten

© Copyright Allianz 20

PROTRACTED CRISIS SCENARIO (30%)

1 Extended lockdown and BREXIT uncertainties may worsen outcome for UK. Source: Allianz Research

U-SHAPED RECOVERY PROTRACTED CRISIS

SCENARIO • Drastic confinement measures, taking heavy toll on economy & markets

• Sharp recession in H1 20 across DMs & several large EMs, followed by weak recovery

• Longer health crisis triggers brutal market dive

• Systemic credit event leads to liquidity crisis

• Policymakers unable to restart growth

HEALTH

POLICY• Belated & uncoordinated policies

• Persistent localized containment measures; incl. targeted travel restrictions

• Reinfections with generalized domestic confinement

• Borders closed again until end-2020

ECONOMIC

POLICY• Aggressive fiscal & monetary easing

• Direct support measures

• Even more aggressive fiscal & monetary policy

• Not very effective

ECONOMIC

IMPACT

GDP growth, % 2020 2021

World -4.7 +4.8

US -5.3 +3.7

China +1.5 +7.6

Eurozone -9.0 +6.0

UK¹ - 13.3 +5.0

Global trade

volume

2020

-15%

Insolvencies 2020-21

+33%

GDP growth, % 2020 2021

World -9.4 -0.5

US -12.0 -2.0

China -6.6 +1.8

Eurozone -20.0 -2.5

UK¹ -24.0 -5.0

BA

SE

CA

SE W

OR

ST

CA

SE

Global trade

volume

2020

-30%

Insolvencies 2020-21

+90%

© Copyright Allianz

02CAPITAL MARKETS

© Copyright Allianz

EQUITY MARKETS: A V-SHAPE RECOVERY PRICED IN

The consensus is expecting a V-shape recovery of EPS in 2020, followed by a ‘normal’ rise in 2021. It proves thedetachment between the markets and economic data. The same trend remains across the globe.

Source: DataStream, Allianz Research

S&P 500 REPORTED EPS

10

15

20

25

30

35

40

45

Dec-16 Dec-17 Dec-18 Dec-19 Dec-20 Dec-21 Dec-22

22

© Copyright Allianz 23

INCREASING DIVERGENCE BETWEEN EQUITY

PRICES AND DIVIDEND FUTURES

The path of the dividend futures follows different directions in the US and Europe. The divergence between the S&P 500 andits’ dividend futures hints that the market galloped too fast.

2,100

2,300

2,500

2,700

2,900

3,100

3,300

3,500

45

50

55

60

65

70

Dec-17 Dec-18 Dec-19 Dec-20

S&P 500 DIVIDEND FUTURES

S&P 500 dividend futures (LHS)

S&P 500 (RHS)3,500

4,000

4,500

5,000

5,500

6,000

6,500

40

60

80

100

120

140

160

180

200

Dec-14 Dec-15 Dec-16 Dec-17 Dec-18 Dec-19 Dec-20

CAC 40 DIVIDEND FUTURES

CAC 40 dividendfutures (LHS)

CAC 40 (RHS)

Source: DataStream, Allianz Research Source: DataStream, Allianz Research

© Copyright Allianz

EQUITY MARKETS: US REMAINS EXPENSIVE

Ratio of MSCI Indices in Common Currency Terms

USA / Germany S&P500 & Nominal GDP

40

60

80

100

120

140

160

180

200

196

9

197

4

197

9

198

4

198

9

199

4

199

9

200

4

200

9

201

4

201

9

202

4

Dec 1999 = 100

The overvaluation of the US equity market relative to the German equity market has reached unseen highs. A recent rally in European equity markets has slightly diminished this overvaluation. However, the US market overvaluation remains acute.

Source: DataStream, Allianz Research

100

1,000

10,000

1990 1995 2000 2005 2010 2015 2020 2025 2030

S&P 500

Level consistent withnominal GDP

24

© Copyright Allianz

Several structural leading indicators show that thedownturn market trough has not yet been reached.Looking at our proprietary EQ sector dispersion indexas an example, the current value and trend of theindicator does not show any strong signs ofimprovement and thus it does not warrant shiftingtowards a re-risking strategy.

As another example, institutional inflows into MM Fundshave historically started declining before marketsbottomed. This precondition has not yet been fulfilled.Consequently, this indicator (as it is still increasing or flat)suggests that markets have not yet reached their bottom.At this point in time, daily and weekly indicators (sentimentdriven) are showing that the market trough is alreadybehind us. However, structural indicators (Monthly andQuarterly) have not yet shown any signs of improvement.

RE-ENTERING THE MARKET: NOT YET!US – EQ Sector Dispersion Index US - Institutional Money Markets Funds

Source: Refinitiv, Allianz Research

EQ Dispersion index: Proxy for diverting returns between EQ sectors

Source: Refinitiv, Allianz Research

-60%

-40%

-20%

0%

20%

40%

60%

80%1

98

0

198

5

199

0

199

5

200

0

200

5

201

0

201

5

202

0

Relative performance EQ vs FI Index YoY (%) returnEQ sector dispersion index YoY%

-60%

-40%

-20%

0%

20%

40%

60%

80%-80%

-60%

-40%

-20%

0%

20%

40%

60%

199

0

199

5

200

0

200

5

201

0

201

5

2020

Relative performance EQ vs FI Index YoY (%) returnMMF Inst. AuM YoY (%) return (RHS - Inverted Scale)

25

© Copyright Allianz

GOVERNMENT BONDS: NO INFLATION IN SIGHT?US 10y Treasury yields

Sources: Refinitiv, Allianz Research

Model: central bank rates, smoothed central bank rates

0%

1%

2%

3%

4%

5%

6%

7% 10Y US Gov. Bond

In Sample Estimate

0.0

0.5

1.0

1.5

2.0

2.5

3.0%

10-Year US TIPS breakeveninflation rate

In the context of lower for longer central

bank rates, yields are expected to remain

on fundamental negative sloping trend.

Our proprietary model suggests that 10y

USTs will reach 1.4% by the end of 2021,

inline with our current forecast. For 2020,

we still expect 10y USTs to finish the year

at 1.0%.

-2%

-1%

0%

1%

2%

3%

4%

5%

6%

10Y Bund

In Sample Estimate

At current valuation levels we believe

inflation expectations to play the key role

moving forward, as real yields are

expected to remain subdued. Both US

and EUR inflation expectations are

currently close to the lower range of our

models. At current levels, it is possible

to buy inflation protection at a low

price.

Sources: Refinitiv, Allianz Research

Model: CPI, smoothed CPI

Sources: Refinitiv, Allianz Research

Model: central bank, smoothed central bank rates, 10y JGB, QE

US 10y Inflation Expectations German 10y Bund yields

If the bond market is still a market, it is

currently pricing a global recession and a

prolonged absence of global inflation. In

the case of the bund, we still expect 10y

bunds to finish the current year at -0.5%

and to perform a timid climb by the end of

2021 (-0.3%).

26

© Copyright Allianz

With equity markets ready for a V-shaped scenario, we still

expect 2020 performance to be on the bearish side. We believe

global equity markets will end 2020 with an ~ -20% yearly

performance. With our forecasts in mind, we understand that a

second market correction could be in the pipeline (specially in

the US). Moving forward, we expect the most vulnerable

countries to remain the laggards of the current economic

downturn. (e.g. Brazil)

Even if not all central banks have announced their willingness to take

credit risk in their balance sheets, global corporate IG & HY markets

have enjoyed a period of declining financing costs since the peak in

mid-march. At this point, we expect corporate spreads to finish the

year close to current levels but we acknowledge that corporate

spreads are vulnerable to second wave of strong widening should the

economic and pandemic data further deteriorate .

EM MARKETS: AVOIDING THE LAGGARDSEquities Corporate Debt

Sources: MSCI Indices in $ (*EMU in €), Allianz Research Sources: Bofa Indices, Allianz Research

27

40

50

60

70

80

90

100

110

12-19 01-20 02-20 03-20 04-20 05-20 06-20

100 = 31.12.2019

World United States

Eurozone EM

EM EMEA EM Asia

EM Latam Brazil

0

200

400

600

800

1000bps

World

UnitedStatesEurozone

© Copyright Allianz

While it is true that emerging market sovereign debt has

been gaining weight within the global sovereign market

universe over the past years, its consideration (from an

international investor perspective) remains that of a mid to

high risk asset. Because of that, it is subject to be sold in

high uncertainty environments. As of today, we still expect a

second wave of EM debt and equity sell-off.

The capital outflows experienced in March led to a rapid

depreciation of emerging markets currencies paired with a quick

increase in long-term sovereign yields. Due to this embedded

volatility, we believe that both exchange and long-term interest

rates will keep wandering erratically throughout 2020 remaining an

unwanted casualty of the currently unsettled short-term market

sentiment.

EM DEBT: AT THE MERCY OF SPECULATORS

EM Sovereign Debt EM Debt Flows

Sources: BofA Indices, Allianz Research Sources: IIF, Allianz Research

28

8%

10%

12%

14%

16%

84%

86%

88%

90%

92%

2006 2008 2010 2012 2014 2016 2018 2020

Developed Markets Sovereign…Emerging Markets Sovereign…

0

1

2

3

4

5

6

7

8

-15

-10

-5

0

5

10

2006 2008 2010 2012 2014 2016 2018 2020

EM Debt Flows

© Copyright Allianz

03U.S. – CHINA – EUROZONE

© Copyright Allianz

The termination of helps dedicated to absorbing theshock at a labor market level, will represent a so-called revenue – cliff.

USA: HOUSEHOLDS TO FACE A REVENUE CLIFF

Sources of revenues for households (USD bn)

Sources: Nomura, Allianz Research

30

-200

-100

0

100

200

300

Mars April May June Jul Aug Sep

Proprietors' income with IVA and CCAdjCompensation of employeesUnemployment Insurance BenefitsOther government social benefits inc. One time checksOthersPersonal income

High uncertainty and conviction that public debt willneed to be reimbursed in the future will weigh long-lastingly on households’ savings rate.

US unemployment and saving rates (%)

Philadelphia Fed, Euler Hermes, Allianz Research

0

5

10

15

20

25

30

35

0

5

10

15

20

25

30

35

05 06 07 08 09 10 11 12 13 14 15 16 17 18 19 20 21

© Copyright Allianz

The Fed has absorbed the bulk of debt newly issuedby the US government, even if it not directlyintervenes on the primary market.

We expect the US public deficit to be close to 16% ofGDP in 2020 and close to 10% of GDP in 2021. Overthe long-term, the US public debt is expected tosteadily increase whatever the outcome of theelection.

USA: THE FED WILL REMAIN A DEBT ABSORBER

US debt held by the public and Fed assets US Public debt and deficit (% of GDP)

Sources: Euler Hermes, Allianz Research Sources: Euler Hermes, Allianz Research

31

-250

0

250

500

750

1000

1250

1500

-250

0

250

500

750

1000

1250

1500

05 06 07 08 09 10 11 12 13 14 15 16 17 18 19 20 21

Net debt issued by the Government (USD bn,LHS)

Treasuries held by the Fed (monthly variation,RHS, USD bn)

-16

-14

-12

-10

-8

-6

-4

-2

70

80

90

100

110

120

17 18 19 20 21 22 23 24 25 26 27 28 29 30

Public debt, LHS

Deficit, RHS

© Copyright Allianz

0

1

2

3

4

0

1

2

3

4

90 93 96 99 02 05 08 11 14 17 20 23 26 29

Estimated potential Biden Trump

Taking into account the regime of performance of 10different macroeconomic indicators, our modelsuggests that President Trump has a 22% probabilityonly to win the next election.

Model studying the potential of growth shows thenegative impact of (much higher) public debt. To thisregard, differences between Trump and Biden are notsignificant (higher fiscal support to productivity forTrump versus active population for Biden)

US ELECTIONS: WHAT IS AT STAKE?

Probability to win US elections for incumbent President’s party

(%)

US potential growth rate

(y/y, %)

Sources: Euler Hermes, Allianz Research Sources: Euler Hermes, Allianz Research

32

0.1

0.2

0.3

0.4

0.5

0.6

0.7

0.8

0.9

0.1

0.2

0.3

0.4

0.5

0.6

0.7

0.8

0.9

65 68 71 74 77 80 83 86 89 92 95 98 01 04 07 10 13 16 19

© Copyright Allianz

TRUMP VS BIDEN ECONOMIC PLANInfrastructure Taxes Health care Jobs & wages Student debt Climate change Trade

Donald

Trump

• USD2tn "very

big and bold

plan"

• Extend 2017 tax overhaul

for individuals (USD1.5tn)

• Repeal renewable energy

tax credits

• Tax credits for U.S.

education

• Raise the Internal Revenue

Service (IRS) budget by

about USD15bn

• Deep health care

spending cuts to

Medicaid

(USD900bn) and

Medicare

(USD450bn)

•10% cut from the

2020 enacted level

for the Department

of Health and

Human Services

• Cut in drug prices

• Spur job

creation through

the USD2tn

infrastructure

plan

• USD1tn of cuts

in social,

education and

assistance

spending

• 7.8% budget

decrease for Dpt of

Education in 2021

• Eliminate Public

Service Loan

Forgiveness and

subsidized loans

• Forgive

undergrad loans

after 15 y instead

of 20 y and raise

period for graduate

loans repayment to

30 from 25 y.

• No sizable

government policy

on climate change

• Pursue

“America

First” policy.

Continuity of

current trade

policy

Joe Biden

• 10-year

USD1.3tn

infrastructure

plan

• Plan focuses

on climate

change ($400bn

for clean

energy,

research and

innovation

• Raise top income tax rate

back at 39.6% from 37% and

top corporate income rate to

28% from 21%

• Apply Social Security taxes

to earnings > USD400,000

• Tax capital gains and

dividends at ordinary rates for

those with annual incomes >

USD 1mn

• 15% minimum tax on book

income of large firms

• Double tax rate (to 21%) on

profits earned by foreign

subsidiaries of U.S. firms

• Eliminate the 400%

income cap on tax

credit eligibility and

lower the limit on the

cost of coverage to

8.5% of income

• Create a public

health insurance

• Lower eligibility age

for Medicare to 60

from 65.

• This plan will insure

more than an 97% of

Americans and cost

USD750bn

• Create "millions

of middle-class

jobs" through

infrastructure

plan

• Increase the

federal minimum

wage to $15

• increase

employment-

based green

cards from

140,000 each

year

• Cancel a

minimum of

USD10,000 of

student debt per

person

• Forgive all

undergraduate,

tuition-related

federal student

debt for low-

income and middle

class individuals

(earning up to

USD125,000)

• Achieve 100%

clean energy

economy and reach

net-zero emissions

no later than 2050.

• Join Paris

Agreement + ban

fossil fuel subsidies

• Install 500,000 EV

charging stations

nationwide by 2030

• Ban new permits

for oil and gas

drilling on federal

land and offshore

• Investing in

innovation and

the middle

classes

• Best way to

confront China

on IP + tech

transfers is by

forming a

coalition w/

allies and

partners, not

through tariffs.

33

© Copyright Allianz

0

20

40

60

80

100

120

140

-21 0 21 42 63 84 105 126 147

2016-2019 average 2020

65

70

75

80

85

90

95

100

105

110

115

-21 0 21 42 63 84 105 126

2016-2019 average 2020

40

50

60

70

80

90

100

-21 0 21 42 63 84 105 126 147

2016-2019 average 2020

Industrial activity is now probably c.5% below usual levels. On the consumption and services side, it could take longer forconfidence and households behaviours to return to normal: property transactions remain -34% below usual volumes, diningbills (including take-outs) are c.-40% below pre-outbreak and household disposable income declined by -3.9% y/y in realterms in Q1 2020 (vs. +5.8% in 2019).

CHINA RECOVERY UNEVEN AND CAPPED?

Source: Wind, Allianz Research Source: Wind, Allianz Research Source: Wind, Allianz Research

Daily average coal consumption at major

power generation groups, base 100

Traffic congestion index (across 100

cities), base 100

Property transaction volume (across 30

cities), base 100

© Copyright Allianz

After the slump in GDP growth in Q1 (at-6.8% y/y), we expect a gradualrecovery, becoming more visible in H2.We expect 2020 GDP growth at +1.5%.

Leading indicators point to theunemployment rate remaining atelevated levels (around 1pp above long-term average) for the rest of 2020.

We expect fiscal support amounting to7.1% of GDP (up from 2.7% forecastbefore the COVID-19 crisis). In terms ofmonetary policy, further injections ofliquidity and policy rate cuts are likely.

CHINA GROWTH FORECAST FOR 2020 AT +1.5%

35

Sources: National sources, Euler Hermes, Allianz Research Sources: Wind, Euler Hermes, Allianz Research Sources: PBOC, Euler Hermes, Allianz Research

Unemployment rate and leading indicator Credit impulse & PMIGDP growth (%) and contributions (pp)

-15

-10

-5

0

5

10

15

20

25

48

49

50

51

52

53

54

55

56

09 10 11 12 13 14 15 16 17 18 19 20 21

Official Manufacturing PMI

Credit impulse, 12-monthlead, rhs

45

50

55

60

65

70

75

804.6

4.8

5.0

5.2

5.4

5.6

5.8

6.0

6.2

12 13 14 15 16 17 18 19 20 21

Unemployment rate %

CKGSB survey -Recruitment index,smoothed, 7-month lead(rhs, rev)

© Copyright Allianz 36

Triggers:

• No further sanctions and retaliations between

China and the U.S.

• Mainland China sends clear signals that

business regulatory environment in Hong

Kong will not change, and significantly

increases investment in Hong Kong to help

recovery

Economic impact:

• In the short-term: stronger recovery of Hong

Kong economy, with GDP growth forecasts

in 2020 and 2021 increasing to -4.2% and

+7.9% respectively.

• In the medium-term: back to pre-Covid-19

and pre-2019 protests normal.

Improving environment

(10%)

Triggers:

• Disruption of business environment due to

China’s national security law in Hong Kong,

strong retaliation against U.S. actions (e.g.

on U.S. FDI into Hong Kong), along with long

term trend of developing regional trade and

financial hubs in the mainland.

• The U.S. treats Hong Kong as mainland

China for trade and direct investment, and is

followed by other developed countries

Economic impact:

• In the short-term: damaged business and

consumer sentiment jeopardize the recovery.

GDP growth forecasts in 2020 and 2021

falling to -6.6% and +0.8% respectively.

• In the medium- to long-term: Divestment of

U.S. firms, stock of FDI could decline by

almost half in coming five years (nearly

USD20bn). Not necessarily compensated by

FDI from mainland China, as focus is on

domestic hubs.

Deteriorating environment

(25%)

Scenario:

• China’s national security law theoretically

threatens the independence of Hong Kong’s

legal system, but its implementation does not

disrupt the business environment

• U.S. actions include financial sanctions on

Chinese officials involved in the national

security law, tightening of visa requirements,

exports restrictions to Hong Kong

Economic impact :

• In the short-term: continued small-scale

protests in Hong Kong. Impact of trade

sanctions is limited (less than 1% of Hong

Kong GDP if same tariff hikes as those

applied to mainland China over 2018-19).

Hong Kong’s 2020 and 2021 GDP growth

forecasts revised down to -5.9% and +4.1%

from -4.7% and +4.5% respectively.

• In the medium-term: U.S. FDI to Hong Kong

slows, but without divestment. FDI from

mainland China accelerates.

The ‘New Normal’

(65%)

HONG KONG SCENARIOS AS OF JULY 2020

© Copyright Allianz

Germany France Italy Spain UK

Lockdown lengths

(weeks)

6 8 10 10 12

Lockdown

strictness*

73 89 87 81 73

Lockdown

strictness x length

439 713 866 806 874

Fiscal stimulus

(% of GDP)

7.5% 6.7% 4.5% 2.5% 5%

Services

(% total gross

value added)

69.3% 78.9% 73.9% 74.8% 79.8%

EUROZONE: UNITED THEY FELL, DIVIDED THEY WILL

RISE -9% IN 2020, +6% IN 2021Key factors driving short-term economic performance

Looking at selected key drivers of divergence (policydecisions on lockdown length & strictness, fiscal responseeconomic features such as the size of the service sector)explains which the UK, Spain and Italy will lag the otherEurozone countries and in particular Germany.

The Eurozone economy has passed the trough, but high-frequency indicators are suggesting that the recovery willbe gradual, drawn-out and uneven across countries. OnAverage pre-crisis GDP will not be reached before 2023.

Sources: Allianz Research. *Note: Oxford stringency index

37

Retail Sales

Index: February 2020=100

Sources: Refinitiv, Allianz Research

© Copyright Allianz

EUROZONE: FISCAL POLICY NOW FIRING FROM TWO

CYLINDERS – PLUS 0.4% PER YEAR

Growth shock vs. net transfers from EU recovery fund

Sources: EU Commission , Refinitiv, Allianz Research

National fiscal policy continues to lead the policyresponse in the Eurozone. The Eurozone budget deficitwill rise to 10% in 2020 and still come in at 4% in 2021,with none of the large Eurozone countries complyingwith the Maastricht 3% limit over the forecast horizon.

In addition the economies most affected by the Covid-19 crisis – as well as those with lower GDP per capita –look set to receive some much needed fiscal tailwind forinvestment from the EU recovery fund. We estimate thatGDP levels on average could be boosted by 0.4% peryear over the next 5 years.

AustriaBelgium

Bulgaria

Croatia

Cyprus

Czechia

Denmark

Estonia

Finland

France

Germany

Greece

Hungary

Ireland

Italy

Latvia

Lithuania

Luxembourg

Malta

Netherlands

Poland

PortugalRomaniaSlovakia

Slovenia

Spain

Sweden

0%

2%

4%

6%

8%

10%

12%

14%

-13% -12% -11% -10% -9% -8% -7% -6%

EU

re

co

ve

ry fu

nd

re

ce

ipts

–lo

an

s &

gra

nts

(%

GD

P)

Revision in 2020 GDP growth forecast (ppts)

38

-14

-12

-10

-8

-6

-4

-2

0

2

4

Eurozone Germany France Italy Spain

2019 2020 2021

Government balance (% of GDP)

Sources: Refinitiv, Allianz Research

© Copyright Allianz

Firms‘ appetite for loans has risen dramatically in H1 2020– thanks to governments extending generous stateguarantees. Meanwhile the demand for housing andconsumer loans is hinting at an anemic recovery.

Loan take up is for now driven mostly by imminent liquidityneeds in the face of sharply lower business revenues.Investment for now is not a priority – especially in the moreaffected Southern Eurozone countries.

EUROZONE: FIRMS’ LOAN DEMAND DRIVEN BY

LIQUIDITY NEEDS, INVESTMENT ON THE BACKBURNERECB Q2 Bank Lending Survey: Overall demand for

loans & credit lines by enterprises (Net balance)ECB Q2 Bank Lending Survey: Drivers for

loan demand by enterprises

Sources: ECB, Refinitiv, Allianz Research Sources: ECB, Refinitiv, Allianz Research

-50

-40

-30

-20

-10

0

10

20

30

40

EZ-19 DE FR IT SP

Fixed investment

Inventories & working capital

-80

-60

-40

-20

0

20

40

60

80

100

120

Q1 Q2 Q1 Q2 Q1 Q2 Q1 Q2 Q1 Q2

Eurozone Germany France Italy Spain

NFC Housing Consumption

39

Loans given under State Guarantees

Sources: National sources, Allianz Research

0%

10%

20%

30%

40%

50%

60%

70%

80%

Sp

ain

Fra

nce

UK

Italy

Germ

any

Take-up of loan guarantee schemes(% total)

Loan guarantee schemes (% ofGDP)

© Copyright Allianz

Germany is an early-opener however a subdued growthoutlook for its key trading partners – EU & non-EU – willkeep a lid on the recovery, particularly in manufacturing.The consumer however appears more resilient, andconstruction is a key trump. After a -7% contraction in2020, GDP will grow 4.5% in 2021.

German fiscal policy is playing in a league of its own insize, timing and composition. The latest stimulus packageaimed at providing tailwind to the recovery should addaround 1ppts to GDP growth in 2020 and another 0.5pptsin 2021.

DE FR IT ES UK

Taxes

VAT √ x x x √

Income x x x x x

Corporate √ x √ √ √

Spending

Household cash transfers √ √ x x x

Job rentention scheme √ √ √ √ √

Car scrappage scheme √ √ √ √ √

Vulnerable sector support √ √ √ √ √

Public investment √ √ √ x √

GERMANY: LEADING THE RECOVERY BUT MIND

INDUSTRIAL & TRADE HEADWINDSGermany vs. Eurozone: Economic confidence in May Germany: Strong & timely tailwind for the imminent recovery

(fiscal stimulus: announced, expected, unlikely)

Sources: EU Commission, Refinitiv, Allianz Research. Source: Allianz Research

-50

-40

-30

-20

-10

0

Con

su

me

rs

Ma

nu

factu

rin

g

Se

rvic

es

Con

str

uction

Eurozone

Germany

40

© Copyright Allianz

-60

-40

-20

0

20

40

60

80

100

01-0

4

01-0

5

01-0

6

01-0

7

01-0

8

01-0

9

01-1

0

01-1

1

01-1

2

01-1

3

01-1

4

01-1

5

01-1

6

01-1

7

01-1

8

01-1

9

01-2

0

Consumer prices, next 12 monthsMajor purchases intentions, next 12 monthsUnemployment, next 12 months

41

FRANCE: WILL THE CONSUMER SAVE THE DAY?

Sources: INSEE, Allianz Research

Consumer confidence

Sources: INSEE, Allianz Research

Private consumption (% change vs. Feb 2020)

-7.2

-90

-70

-50

-30

-10

10

30M

arc

h

Ap

ril

Ma

y

Total Food

Manufactured goods Durables

Clothing Energy

Consumer spending is recovering in May, relativelystronger than in other European countries.

However, there are doubts that this would be sustainablegiven rising in unemployment fears

© Copyright Allianz

Major consumption shock in H1, investment still sufferingfrom uncertainty and funding constraints due to bankingvulnerability. Trade balance worsening due to strongdecline in tourism receipts and world trade. Relativemoderate rebound in 2021 due with GDP remaining 3%below pre-crisis level.

Public debt will increase strongly in 2020 due to fiscalmeasures and GDP drop (165% GDP). Debtsustainability is not at risk in the short term as ECBcontains risk of rising yield/spreads. Debt/GDP willremain above 140% for long period of time (~10y).

ITALY: NO REPEAT OF 2012-14, WATCH OUT FOR

POLITICAL AND MARKET HEADWINDSGDP by component, % Public debt in % of GDP (contributions)

Sources: Refinitiv, Allianz Research Sources: Refinitiv, Allianz Research

42

-15.0

-10.0

-5.0

0.0

5.0

10.0

15.0

12 13 14 15 16 17 18 19 20f 21f

Households GFCF GovernmentStocks Net Trade real GDP

Forecast

50

100

150

200

-20.0

0.0

20.0

40.0

07 08 09 10 11 12 13 14 15 16 17 18 19 20f 21f

Stock-flow adj. Impact of real growth on debtImpact of inflation on debt One-offsInterest Primary deficitChg. Debt/GDP ratio Debt/GDP ratio (rhs)

Forecast

© Copyright Allianz

THE UK: SMALL IS THE “NEW DEAL”, BREXIT-

CONSTRAINED*?

0

5

10

15

20

25

30

35

40

45

11 12 13 14 15 16 17 18 19

Thousands

SME LARGE

New loans to corporates, GBPbn

Sources: ONS, Allianz ResearchSources: ONS, Allianz Research

Real GDP during the recession,

100 = pre-recession peak

75

80

85

90

95

100

0 1 2 3 4 5

Early 80s recession (peak = Q4 79)

Early 90s recession (peak = Q2 90)

Late 00s recession (peak = Q1 08)

Current recession (peak = Jan 20)

3 years and

3months5 years and 3

months

6 years

2 years and 9

months

Sources: ONS, Allianz Research

Real wage growth, y/y

-8%

-6%

-4%

-2%

0%

2%

4%

6%

05

06

07

08

09

10

11

12

13

14

15

16

17

18

19

20

43*After 4 long years of Brexit negotiations, we expect a 5th one. Soft Brexit (70%) by Jan 2022

© Copyright Allianz

04EMERGING MARKETS

© Copyright Allianz

4%8%

9%16%

19%

25%

26%

29%

32%

39%

43%

45%60%72%84%

89%

89%

94%110%

113%

126%

132%

144%

161%

169%

18

8%2

18%

229%

356%

39

4%

0%

100%

200%

300%

400%

Net portfolio flows to EM dropped sharply to a record

low of -USD 89 bn in March. But moderate rebound

already in April (+USD23bn), May (+USD2bn) and

June (first estimate +USD33bn).

In Turkey and Argentina, gross external financingrequirements rose further from around 250% at end-2019.

EMERGING MARKETS: CAPITAL FLOWS BOTTOMING

OUT BUT RISKS OF SUDDEN STOPS STILL REMAIN

Emerging Markets: Net portfolio flows by region (USD bn) Emerging Markets: Gross external financing requirement

(% of FX reserves)

Sources: National statistics, IIF, Allianz Research estimates Sources: IHS Markit, Allianz Research

45

-100

-80

-60

-40

-20

0

20

40

60

80

100

Jan 18 Jul 18 Jan 19 Jul 19 Jan 20

Africa & Middle East Emerging Europe

Latin America Emerging Asia ex China

China

© Copyright Allianz

Turkey has by far burned the most FX reserves this

year to defend its currency – albeit with limited

success. Net FX reserves dangerously low now.

Watch out for Brazil, South Africa and Mexico.

Some EMs have begun to purchase government bonds to

ensure smooth functioning of bond markets and sufficient

liquidity for banks to support private sector credit. This is mostly

different from QE in AEs and much smaller in scale. Indonesia,

Turkey, Brazil, Poland and Croatia require monitoring.

EMERGING MARKETS: THE COVID-19 QE PROGRAMS

COULD ENDANGER CENTRAL BANKS’ CREDIBILITY Exchange rate changes vs. FX reserves changes Government bond purchase programs in EMs

Sources: IHS Markit, Allianz Research Sources: National statistics, IHS Markit, Allianz Research

46

Poland

Indonesia

Romania

Hungary

Malaysia

Mexico

-35%

-30%

-25%

-20%

-15%

-10%

-5%

0%

5%

10%

-25% -20% -15% -10% -5% 0% 5%

Chile

South Africa

Russia

Egypt

India

Brazil Saudi Arabia

Turkey

Colombia

FX

res

erv

es

(c

ha

ng

e Y

TD

in

%)

LCU vs. USD (change YTD in %)

Turkey 8,25% 9,4% Secondary 10,1% 63,8%

Indonesia 4,25% 2.8% ** Primary & secondary 38,6% 21,3%

Poland 0,10% 4,2% Secondary 23,4% 49,5%

Croatia 2,50% 3,4% Secondary na na

Thailand 0,50% 2,4% Secondary 17,2% 14,5%

Philippines 3,25% 1,6% Secondary na na

Colombia 3,25% 1,1% Secondary 24,5% 27,9%

India 4,00% 0,8% Secondary 3,6% 12,1%

South Africa 3,80% 0,7% Secondary 37,2% 35,3%

Hungary 0,75% 0,3% Secondary 18,6% 62,1%

Romania 1,75% 0,2% Secondary 19,3% na

Costa Rica 0,75% Has started *** Secondary na na

Brazil 2,25% Announced, not started Secondary 10,4% 29,4%

Chile 0,50% Announced, not started Secondary na 52,6%

Czechia 0,25% Announced, not started Secondary 40,6% 34,5%

Malaysia 2,00% Announced, not started Unspecified 25,3% 32,5%

* Both public and private debt. ** Bank Indonesia already owns about 15% of tradable government bonds.

*** Central Bank of Costa Rica was authorized and approved purchases of up to 0.7% of GDP .

Primary / secondary

market?

Size (% of GDP,

purchased since March)

Inflationary

riskCountry Policy rate

Gov. bond purchases by Central Bank Foreign-

owned local

gov. bonds

(% of total)

Total FX-

denominated

debt (% of

GDP) *

© Copyright Allianz

Easing currency pressures allowed rate cuts.

CBs in PL, TR, HU and RO began to purchase

government bonds to ensure smooth functioning

of bond markets and sufficient liquidity for banks

to support private sector credit. This is different

from QE in AEs and much smaller in scale.

Direct fiscal stimulus is still modest.

Public finances will deteriorate but remain

manageable overall.

EMERGING EUROPE: UNEVEN ROOM FOR POLICY

MANOEUVER

47

Sources: Sources:

Monetary policy accommodation Fiscal stimulus and public debt (% of GDP)

18%

12%

6%5% 5% 4% 3%

2%1%

0%

10%

20%

30%

40%

50%

60%

70%

80%

0%

5%

10%

15%

20%

Czechia

Pola

nd

Turk

ey

Ro

man

ia

Hu

nga

ry

Ru

ssia

Slo

vakia

Bulg

aria

Ukra

ine

Loans/loan guarantees Direct stimulus

Public debt ratio (rhs)

All economies in the region will be in recession.

The depth of recession is influenced by the size

and efficiency of policy measures (lockdowns

and stimulus) and, importantly, the dependence

on export of goods and services.

Sources:

Real GDP growth (%)

2019 2020 2021

Emerging Europe 2.3 -5.3 4.0

Poland 4.1 -4.1 4.2

Czechia 2.6 -7.5 5.9

Romania 4.1 -5.5 3.9

Hungary 4.9 -5.0 4.7

Slovakia 2.3 -8.5 6.4

Croatia 2.9 -7.0 6.0

Bulgaria 3.4 -5.1 5.0

Slovenia 2.4 -7.0 6.0

Lithuania 3.9 -6.4 6.0

Latvia 2.2 -7.1 6.2

Estonia 4.3 -6.8 6.0

Turkey 0.9 -4.7 4.2

Russia 1.3 -5.2 3.0

Ukraine 3.2 -6.9 4.8

-1%0%1%2%3%4%5%6%7%8%9%-900

-800-700-600-500-400-300-200-100

0100

Ukra

ine

Turk

ey

Czechia

Ru

ssia

Pola

nd

Ro

man

ia

Hu

nga

ry

Bulg

aria

Slo

vakia

Rate cuts since March Rate cuts in Jan-Feb

Current policy rate (rhs) Gov. bond purchases(% of GDP; rhs)

47

© Copyright Allianz

Huge net portfolio investment outflows in Jan-Apr

2020. Plus significant net bank debt outflows (which

were already negative in the previous four full years).

.

Net FX reserves dwindled to less than USD20bn in

May 2020 as the CB burned reserves to defend the

lira – with limited success. Expect currency

turbulences in H2 2020.

TURKEY: ANOTHER BOP CRISIS ON THE HORIZON?

Current and capital account (% of GDP) FX reserves (USD bn)

Note: 2020 data refer to January-April 2018.

48

-25%

-20%

-15%

-10%

-5%

0%

5%

10%

00 02 04 06 08 10 12 14 16 18 20

Net external bank borrowing

Net portfolio inv. inflows

Net FDI inflows

Current account balance0

20

40

60

80

100

120

140

160

07 08 09 10 11 12 13 14 15 16 17 18 19 20

Gross FX reserves Net FX reserves Gold

© Copyright Allianz

No country will escape recession, du tothe stringent lockdowns (esp. Argentina,Peru and Chile), exposure tocommodities & global trade integration.

As money supply (M2, a measure ofliquidity) has shot up, so has credit tothe private sector, indicating the pass-through of the stimulus to companies.

The policy focus was on debt financerather than unemployment support. Weexpect significant informal and formaljob losses in Latin America as a result.

LATAM: DEEP RECESSION, STIMULUS AT WORK, BUT

LARGE JOB LOSSES AHEAD

49

Sources: IMF, Euler Hermes, Sources: Macrobond, Euler Hermes Sources: Macrobond, Euler Hermes, Allianz Research

GDP growth, y/y, % Real credit to the private sector (%, y/y) Unemployment rate (%)

-30%

-20%

-10%

0%

10%

20%

30%

40%

08 09 10 11 12 13 14 15 16 17 18 19 20

Argentina Mexico

Brazil Colombia

2016 2017 2018 2019 2020 2021

Argentina -2.1 2.7 -2.5 -2.2 -8.1 5.5

Brazil -3.3 1.3 1.3 1.1 -7.0 3.0

Chile 1.7 1.2 3.9 1.0 -5.2 2.2

Colombia 2.1 1.4 2.5 3.3 -5.3 3.7

Mexico 2.9 2.1 2.1 -0.3 -7.5 2.6

Peru 4.1 2.5 4.0 2.2 -9.0 6.0

Latin

America-0.1 1.8 1.5 0.7 -6.5 3.1

© Copyright Allianz

As of June, despite easing of lockdowns, confidencehas barely recovered; this bodes ill for industrialproduction; overall, activity is still 26% below pre-crisis levels, which signals a sluggish recovery.

The Economic Policy Uncertainty index is at itshighest since early 2017. At the exit of the crisis,further tensions between the central administrationand Congress + local governors could halt reforms.

BRAZIL: CRISIS MISMANAGEMENT AMPLIFIES

RECESSION; POLITICAL RISK HEIGHTENED

Business confidence and industrial production (%y/y) Economic Policy Uncertainty Index

Sources: IHS Markit, Euler Hermes, Allianz Research Sources: Macrobond, EPU, Euler Hermes, Allianz Research

50

-30%

-20%

-10%

0%

10%

20%

30%

25

35

45

55

65

75

10 11 12 13 14 15 16 17 18 19 20

Business confidence

Industrial production, total (volume)

© Copyright Allianz

We have revised down GDP growth forthe Asia-Pacific region from +4.2% priorto the global pandemic to -1.3% in 2020(after 4.3% in 2019).

Global trade should overall remainunder pressure this year, but exposureto China could be comparativelysupportive.

Different initial conditions and economicstructures require varying levels ofpolicy supports. India, Indonesia,Vietnam and Thailand could do more toprotect employment.

ASIA-PACIFIC: PRAGMATICALLY RESYNCHING WITH

CHINA?

51

Source: National Statistics, Euler Hermes, Allianz Research Sources: IMF, Euler Hermes, Allianz Research Source: World Bank, Euler Hermes, Allianz Research

Real GDP growth (%) Exports of main 14 economies in APAC Fiscal stimulus (% of GDP)

2020 2021 2020 2021

Asia-Pacif ic 4.3 -1.3 5.9 -0.6 6.5

Australia 1.8 -4.3 3.3 -5.0 3.5

China 6.2 1.5 7.6 1.8 8.5

Hong Kong -1.3 -5.9 4.1 -4.7 4.5

India 4.2 -3.1 7.3 1.1 7.5

Indonesia 5.0 -1.5 6.2 0.9 6.7

Japan 0.7 -5.7 2.2 -5.7 2.2

Malaysia 4.3 -3.3 5.9 -3.2 6.2

New Zealand 2.2 -4.8 3.9 -5.2 3.0

Philippines 6.1 -2.7 7.6 -2.6 7.7

Singapore 0.7 -5.1 4.5 -4.1 4.9

South Korea 2.0 -1.5 3.6 -2.5 4.5

Taiw an 2.7 -0.3 3.4 -2.0 4.7

Thailand 2.4 -6.0 5.4 -4.1 6.6

Vietnam 6.9 2.3 6.0 3.1 6.7

2019New forecasts Old forecasts JP

SG

MY

HK

AUNZ

CN THVN

IN

ID

KR

PHTW

0

2

4

6

8

10

12

14

16

18

20

0 25 50 75 100

Fis

ca

l su

pp

ort

(%

of G

DP

)

Share of informal employment in total employment (%)

-15

-5

5

15

25

35

12 13 14 15 16 17 18 19 20

Total exports, 3-month %y/y

Exports to U.S.

Exports to EU

Exports to China

© Copyright Allianz

India has started to de-confine, even though datasuggest the epidemic is not yet controlled. Thismeans that activity resumption could be even slowerthan in other economies.

Risks are skewed on the downside. Policy leeway islimited by twin deficits, and a vulnerable financialsystem. In the medium run, we are more concernedabout India’s financing requirements.

INDIA: -3.1% GDP GROWTH IN FY2020-21, WITH

DOWNSIDE RISKS

High frequency indicators Twin deficits (as % of GDP)

Sources: Bloomberg, National statistics, Euler Hermes, Allianz Research Sources: IHS, Euler Hermes, Allianz Research

52

42

39.7%

8.5%

-28%

-7%

75

14,831

39

35.9%

27.1%

-65%

-32%

100

15,403

103

42.8%

7.5%

0%

-4%

10

0

Consumer sentiment index

Labour participation rate

Unemployment rate

Workplace mobility(vs. pre-crisis)

Electricity consumption%y/y

Lockdown stringency index

Daily Covid-19 cases

1 MarchCrisis peakLatest (mid-June)

-14%

-12%

-10%

-8%

-6%

-4%

-2%

0%

2%

4%

90 93 96 99 02 05 08 11 14 17 20

Fiscal balance

Current account balance Forecasts

© Copyright Allianz

Huge export losses to be expected across the regionin 2020, in particular in oil exporting countries. Onlymoderate recovery in 2021 as oil output is unlikely tobe ramped up.

All economies in the region will be in recession in2020, at diverging degrees. The slowdown/recessionwill be much stronger than in 2009.

MIDDLE EAST: TRIPLE SHOCK OF COVID-19, OIL PRICE

SLUMP AND OUTPUT CUTS HITS EXPORTS AND GROWTH

Potential export changes in 2020-21 (goods and services, USD bn) Real GDP growth (%)

Sources: IMF, Celem, IHS Markit, Allianz Research Sources: National statistics, IHS Markit, Allianz Research forecasts

53

2009 2019 2020 2021

Middle East 0.1 -0.2 -6.8 2.2

GCC -1.1 0.7 -4.6 1.8

Saudi A. -2.1 0.3 -4.0 2.0

UAE -5.2 1.7 -6.0 1.5

Qatar 12.0 -0.2 -2.3 2.0

Kuwait -7.1 0.4 -6.2 1.5

Oman 6.1 0.5 -6.5 2.2

Bahrain 2.5 1.8 -4.4 2.0

Non-GCC 1.8 -1.4 -9.9 2.7

Iran 0.0 -7.6 -15.0 3.0

Israel 1.0 3.3 -4.5 3.3

Iraq 3.4 3.9 -10.0 3.0

Lebanon 10.2 -6.5 -13.0 -2.0

Jordan 4.5 2.0 -3.0 2.4

28

25

3

10

7

4

3

5

-1

-105

-101

-39

-31

-14

-13

-8

-5

-4

-120 -100 -80 -60 -40 -20 0 20 40

Saudi Arabia

UAE

Kuwait

Qatar

Israel

Oman

Bahrain

Jordan

Lebanon

2020f 2021f

© Copyright Allianz 54

GCC: FISCAL AND EXTERNAL POSITIONS WILL

MARKEDLY WORSEN AGAIN, AS IN 2015-2016Fiscal and current account breakeven oil prices 2020f (USD/bbl)

The currency pegs limit both monetary and fiscal policy leeway.

The oil price slump translates directly into lower fiscal revenues in local

currencies since the exchange rate does not work as an automatic

stabilizer.

Hence, all GCC economies except the UAE will run twin deficits in 2020.

Sources: IMF, IIF, Allianz Research

95

86

75

6661

51

85

75

53

28

56

50

0

20

40

60

80

100

120

Bahrain Oman SaudiArabia

UAE Kuwait Qatar

Fiscal accountbreakeven oil price

Current accountbreakeven oil price

Average Brent oil price fore-cast for 2020: 47 USD/bbl

Fiscal and external balances in the GCC

Saudi Arabia, the UAE, Qatar and Kuwait have large SWFs, which can

act as buffers against the revenue shocks and softening the risk of non-

payment. But Bahrain and Oman have relatively small SWFs.

Bahrain ran already out of policy buffers in 2017 and has since

“survived” thanks to financial support from Saudi Arabia and UAE.

Oman is likely to follow in the next years. => Downgrade to C3.

Sources: IMF, IHS Markit, Allianz Research

Cu

rren

t acco

un

t b

ala

nce (

% o

f

GD

P)

Fiscal balance (% of GDP)

BahrainKuwait

Oman

QatarSaudi Arabia

UAE