Control Tower: Transforming the Supply...

26

Copyright © 2013 Accenture All Rights Reserved. Accenture, its logo, and High Performance Delivered are trademarks of Accenture. Control Tower: Transforming the Supply Chain William Kammerer Roderick Martin Managing Directors

Transcript of Control Tower: Transforming the Supply...

Copyright © 2013 Accenture All Rights Reserved. Accenture, its logo, and High Performance Delivered are trademarks of Accenture.

Control Tower:

Transforming the Supply Chain William Kammerer

Roderick Martin

Managing Directors

Copyright © 2012 Accenture. All rights reserved. 2

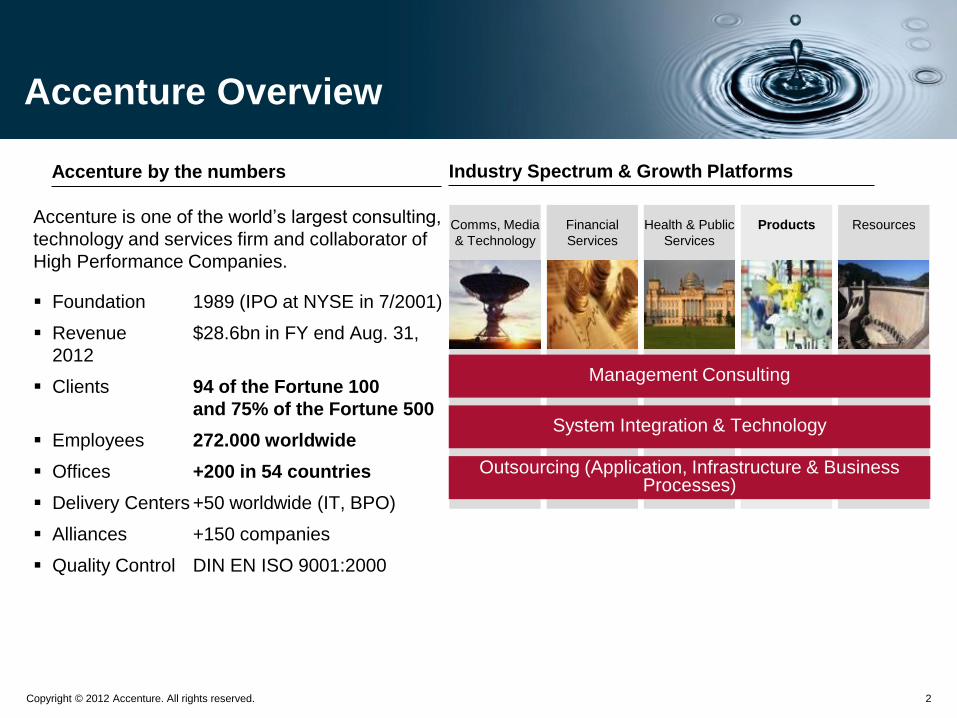

Accenture by the numbers Industry Spectrum & Growth Platforms

Accenture is one of the world’s largest consulting,

technology and services firm and collaborator of

High Performance Companies.

Foundation 1989 (IPO at NYSE in 7/2001)

Revenue $28.6bn in FY end Aug. 31,

2012

Clients 94 of the Fortune 100

and 75% of the Fortune 500

Employees 272.000 worldwide

Offices +200 in 54 countries

Delivery Centers +50 worldwide (IT, BPO)

Alliances +150 companies

Quality Control DIN EN ISO 9001:2000

Comms, Media

& Technology

Financial

Services

Products

Health & Public

Services

Resources

Management Consulting

System Integration & Technology

Outsourcing (Application, Infrastructure & Business Processes)

Accenture Overview

Copyright © 2012 Accenture. All rights reserved. 3

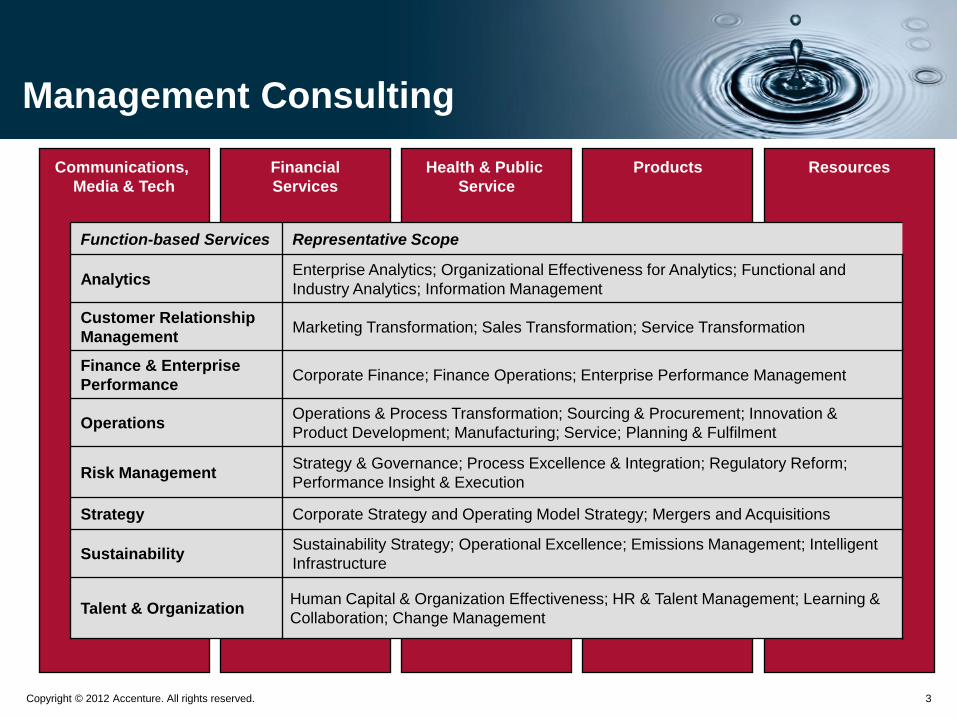

Management Consulting

Resources Communications,

Media & Tech

Financial

Services

Health & Public

Service

Products

Function-based Services Representative Scope

Analytics Enterprise Analytics; Organizational Effectiveness for Analytics; Functional and

Industry Analytics; Information Management

Customer Relationship

Management Marketing Transformation; Sales Transformation; Service Transformation

Finance & Enterprise

Performance Corporate Finance; Finance Operations; Enterprise Performance Management

Operations Operations & Process Transformation; Sourcing & Procurement; Innovation &

Product Development; Manufacturing; Service; Planning & Fulfilment

Risk Management Strategy & Governance; Process Excellence & Integration; Regulatory Reform;

Performance Insight & Execution

Strategy Corporate Strategy and Operating Model Strategy; Mergers and Acquisitions

Sustainability Sustainability Strategy; Operational Excellence; Emissions Management; Intelligent

Infrastructure

Talent & Organization Human Capital & Organization Effectiveness; HR & Talent Management; Learning &

Collaboration; Change Management

Copyright © 2012 Accenture. All rights reserved. 4

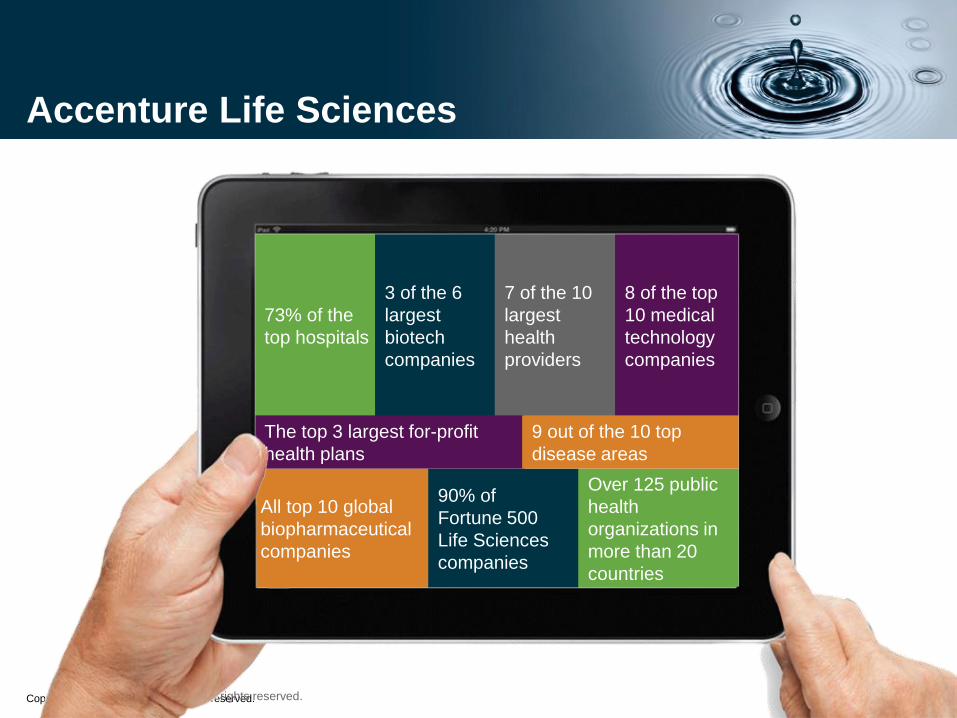

Accenture Life Sciences

73% of the

top hospitals

3 of the 6

largest

biotech

companies

7 of the 10

largest

health

providers

8 of the top

10 medical

technology

companies

Copyright © 2013 Accenture All rights reserved. 4

All top 10 global

biopharmaceutical

companies

90% of

Fortune 500

Life Sciences

companies

Over 125 public

health

organizations in

more than 20

countries

The top 3 largest for-profit

health plans

9 out of the 10 top

disease areas

Copyright © 2011 Accenture. All rights reserved. 5

Elements of Change and Impact on Supply Chain

Copyright © 2012 Accenture. All rights reserved. 6

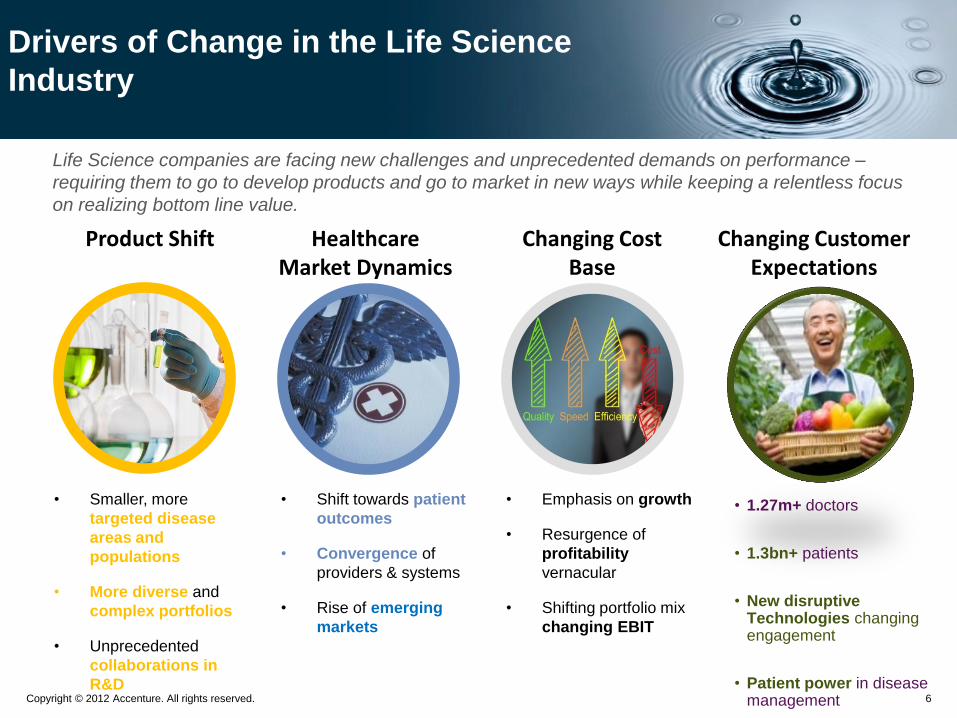

Life Science companies are facing new challenges and unprecedented demands on performance –

requiring them to go to develop products and go to market in new ways while keeping a relentless focus

on realizing bottom line value.

Product Shift Healthcare Market Dynamics

• Smaller, more

targeted disease

areas and

populations

• More diverse and

complex portfolios

• Unprecedented

collaborations in

R&D

• Shift towards patient

outcomes

• Convergence of

providers & systems

• Rise of emerging

markets

Changing Cost Base

• Emphasis on growth

• Resurgence of

profitability

vernacular

• Shifting portfolio mix

changing EBIT

Drivers of Change in the Life Science

Industry

• 1.27m+ doctors

• 1.3bn+ patients

• New disruptive Technologies changing engagement

• Patient power in disease management

Changing Customer Expectations

Copyright © 2012 Accenture. All rights reserved. 7

Drivers of change are pulling the Supply

Chain…

Manage business cost to

serve and profitability while

reducing total supply chain

costs and complexity

Become more agile and

flexible to sense and adapt

to demand changes and

shape demand for growth

Support growth

opportunities by improving

service levels, new

markets penetration or new

services

Manage End to

End Supply Chain

Security and Risk

Meet increasing

customer

requirements and

service level goals

Ensure supply and

supplier performance

& reliability

Copyright © 2012 Accenture. All rights reserved. 8

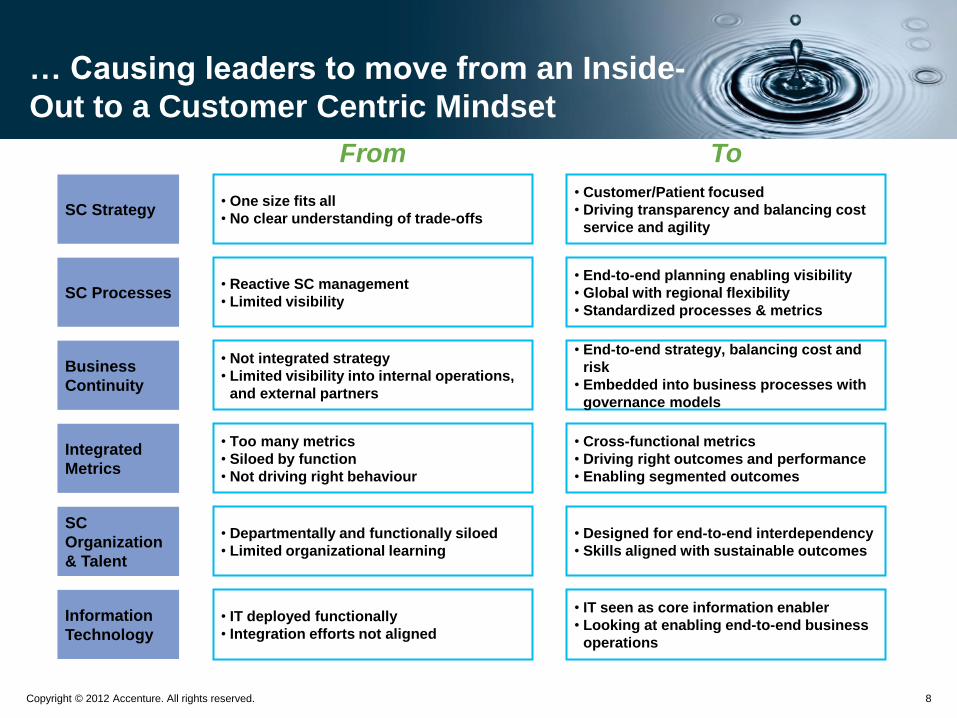

SC Strategy

SC Processes

Business

Continuity

Integrated

Metrics

SC

Organization

& Talent

Information

Technology

• One size fits all

• No clear understanding of trade-offs

• Reactive SC management

• Limited visibility

• Not integrated strategy

• Limited visibility into internal operations,

and external partners

• Too many metrics

• Siloed by function

• Not driving right behaviour

• Departmentally and functionally siloed

• Limited organizational learning

• IT deployed functionally

• Integration efforts not aligned

• Customer/Patient focused

• Driving transparency and balancing cost

service and agility

• End-to-end planning enabling visibility

• Global with regional flexibility

• Standardized processes & metrics

• End-to-end strategy, balancing cost and

risk

• Embedded into business processes with

governance models

• Cross-functional metrics

• Driving right outcomes and performance

• Enabling segmented outcomes

• Designed for end-to-end interdependency

• Skills aligned with sustainable outcomes

• IT seen as core information enabler

• Looking at enabling end-to-end business

operations

From To

… Causing leaders to move from an Inside-

Out to a Customer Centric Mindset

Copyright © 2012 Accenture. All rights reserved. 9

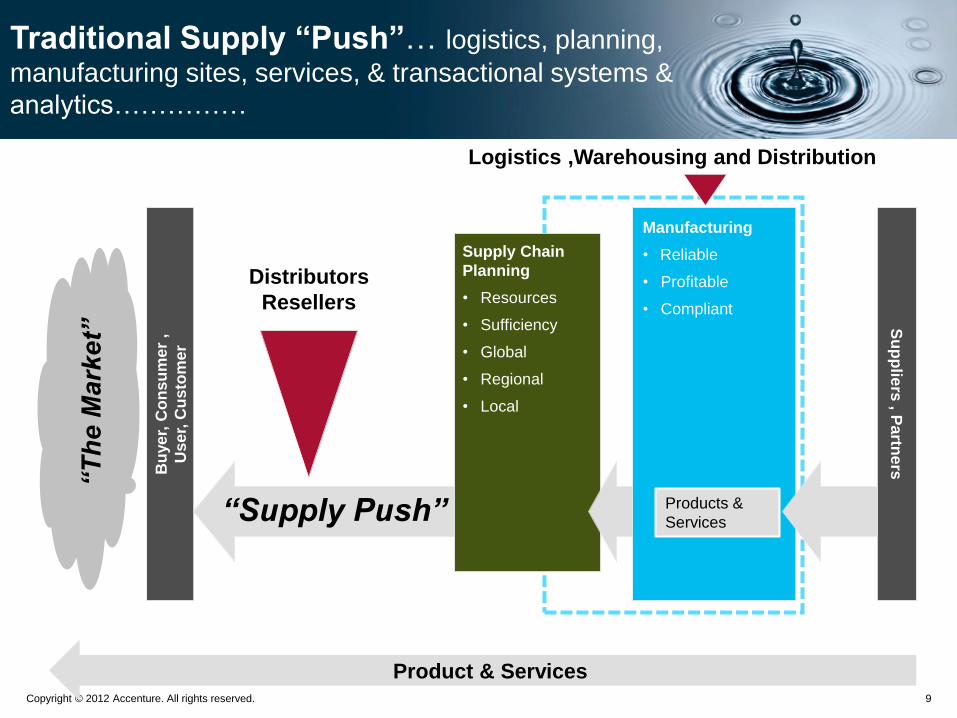

Bu

ye

r, C

on

su

me

r ,

Use

r, C

usto

me

r

Products

&

Services

“T

he

Ma

rke

t”

Product & Services

Traditional Supply “Push”… logistics, planning,

manufacturing sites, services, & transactional systems &

analytics……………

Su

pp

liers

, Pa

rtne

rs

Manufacturing

• Reliable

• Profitable

• Compliant

Supply Chain

Planning

• Resources

• Sufficiency

• Global

• Regional

• Local

Products &

Services

Distributors

Resellers

Logistics ,Warehousing and Distribution

“Supply Push”

Copyright © 2012 Accenture. All rights reserved. 10

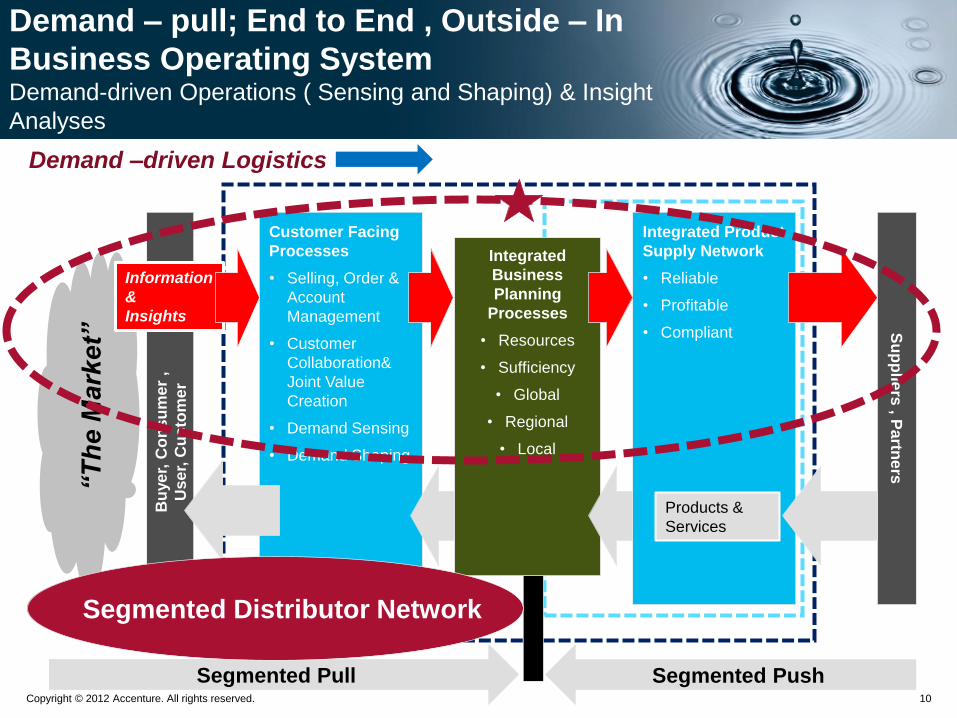

Customer Facing

Processes

• Selling, Order &

Account

Management

• Customer

Collaboration&

Joint Value

Creation

• Demand Sensing

• Demand Shaping

Bu

ye

r, C

on

su

me

r ,

Use

r, C

usto

me

r

Products

&

Services

“T

he

Ma

rke

t”

Segmented Pull Segmented Push

Demand – pull; End to End , Outside – In

Business Operating System Demand-driven Operations ( Sensing and Shaping) & Insight

Analyses

Su

pp

liers

, Pa

rtne

rs

Integrated Product

Supply Network

• Reliable

• Profitable

• Compliant

Integrated

Business

Planning

Processes

• Resources

• Sufficiency

• Global

• Regional

• Local

Products &

Services

Segmented Distributor Network

Information

&

Insights

Demand –driven Logistics

Copyright © 2011 Accenture. All rights reserved. 11

Transformation Evolution and Maturity

Copyright © 2012 Accenture. All rights reserved. 12

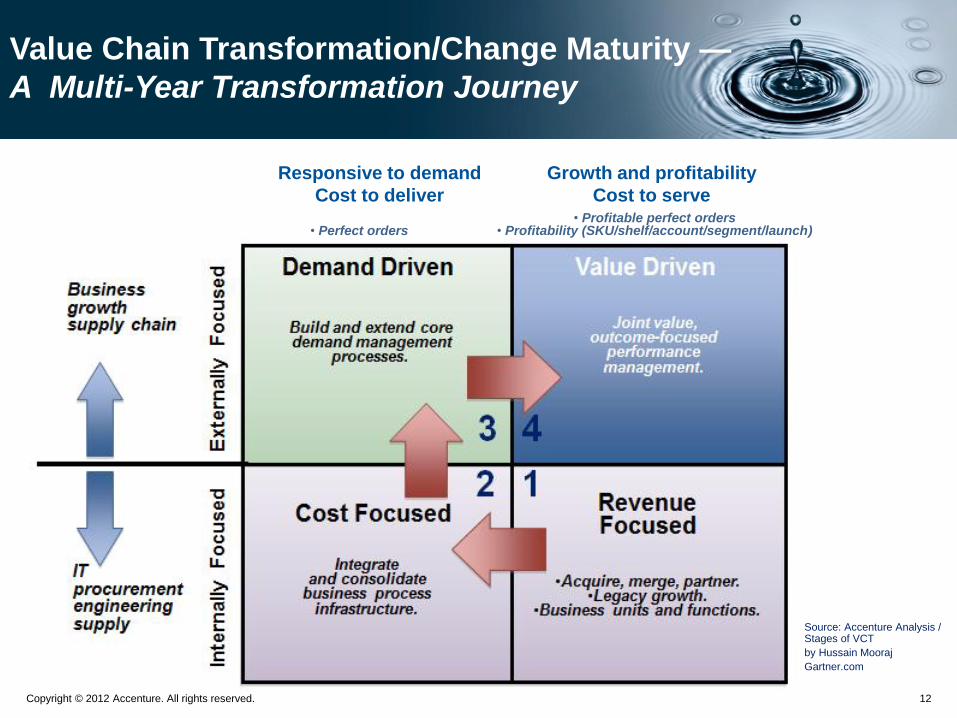

Value Chain Transformation/Change Maturity —

A Multi-Year Transformation Journey

Growth and profitability

Cost to serve

Responsive to demand

Cost to deliver

Value Driven

• Profitable perfect orders • Profitability (SKU/shelf/account/segment/launch) • Perfect orders

Source: Accenture Analysis / Stages of VCT

by Hussain Mooraj

Gartner.com

Copyright © 2012 Accenture. All rights reserved. 13

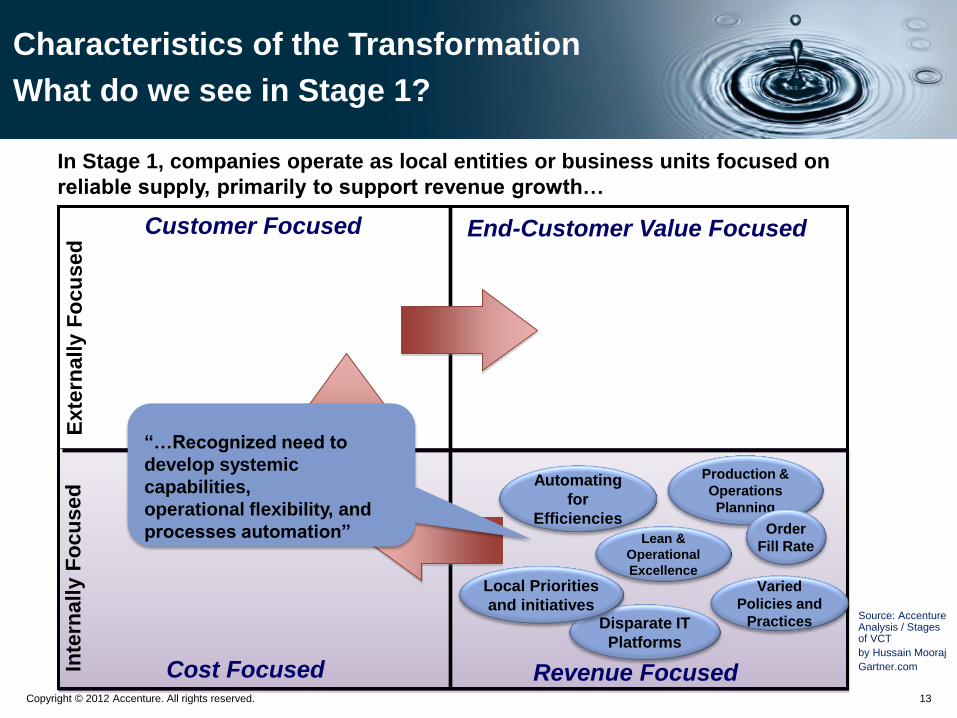

Characteristics of the Transformation

What do we see in Stage 1?

In Stage 1, companies operate as local entities or business units focused on

reliable supply, primarily to support revenue growth…

Inte

rnall

y F

ocu

sed

E

xte

rnally F

ocu

se

d

Automating

for

Efficiencies

Varied

Policies and

Practices

Cost Focused Revenue Focused

Customer Focused End-Customer Value Focused

Disparate IT

Platforms

Lean &

Operational

Excellence

Production &

Operations

Planning

Local Priorities

and initiatives

Order

Fill Rate

“…Recognized need to

develop systemic

capabilities,

operational flexibility, and

processes automation”

Source: Accenture Analysis / Stages of VCT

by Hussain Mooraj

Gartner.com

Copyright © 2012 Accenture. All rights reserved. 14

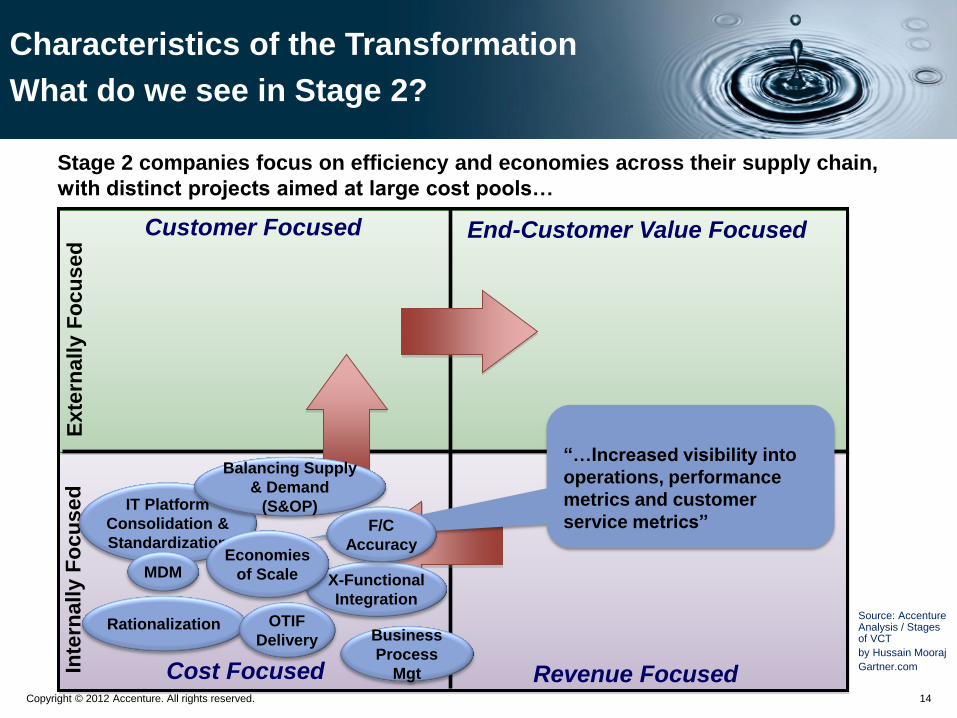

Characteristics of the Transformation

What do we see in Stage 2?

Stage 2 companies focus on efficiency and economies across their supply chain,

with distinct projects aimed at large cost pools…

Inte

rnall

y F

ocu

sed

E

xte

rnally F

ocu

sed

IT Platform

Consolidation &

Standardization

X-Functional

Integration

Cost Focused Revenue Focused

Rationalization Business

Process

Mgt

Balancing Supply

& Demand

(S&OP)

Economies

of Scale

OTIF

Delivery

MDM

“…Increased visibility into

operations, performance

metrics and customer

service metrics” F/C

Accuracy

Customer Focused End-Customer Value Focused

Source: Accenture Analysis / Stages of VCT

by Hussain Mooraj

Gartner.com

Copyright © 2012 Accenture. All rights reserved. 15

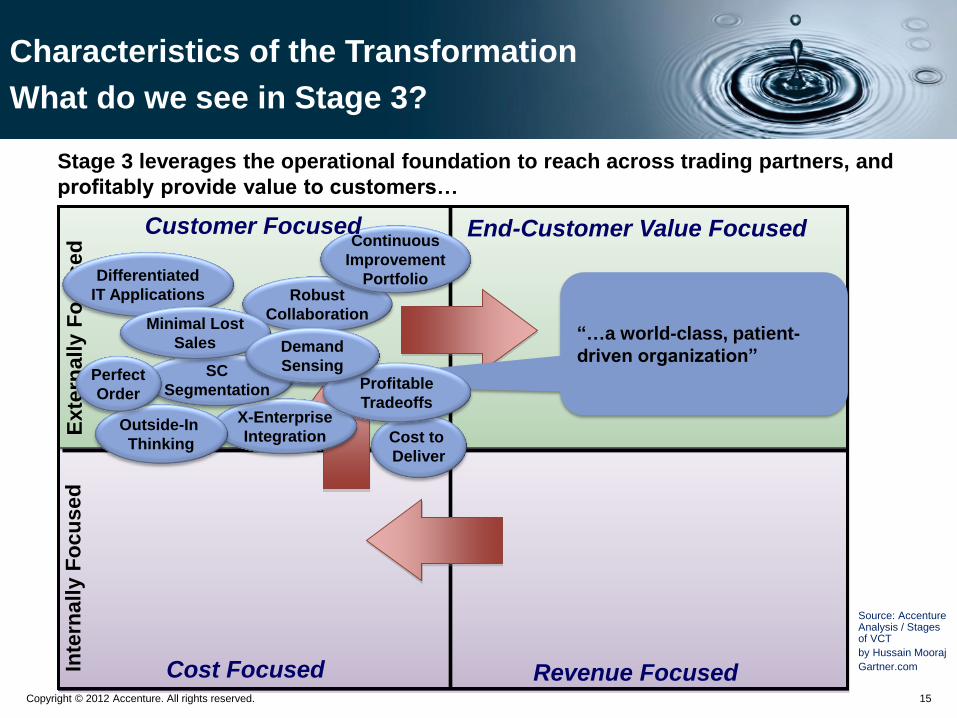

Characteristics of the Transformation

What do we see in Stage 3?

Stage 3 leverages the operational foundation to reach across trading partners, and

profitably provide value to customers…

Inte

rnall

y F

ocu

sed

E

xte

rnally F

ocu

se

d

Differentiated

IT Applications

X-Enterprise

Integration

Cost Focused Revenue Focused

Robust

Collaboration

Outside-In

Thinking Cost to

Deliver

Continuous

Improvement

Portfolio

“…a world-class, patient-

driven organization” SC

Segmentation Perfect

Order Profitable

Tradeoffs

Minimal Lost

Sales

Customer Focused End-Customer Value Focused

Demand

Sensing

Source: Accenture Analysis / Stages of VCT

by Hussain Mooraj

Gartner.com

Copyright © 2012 Accenture. All rights reserved. 16

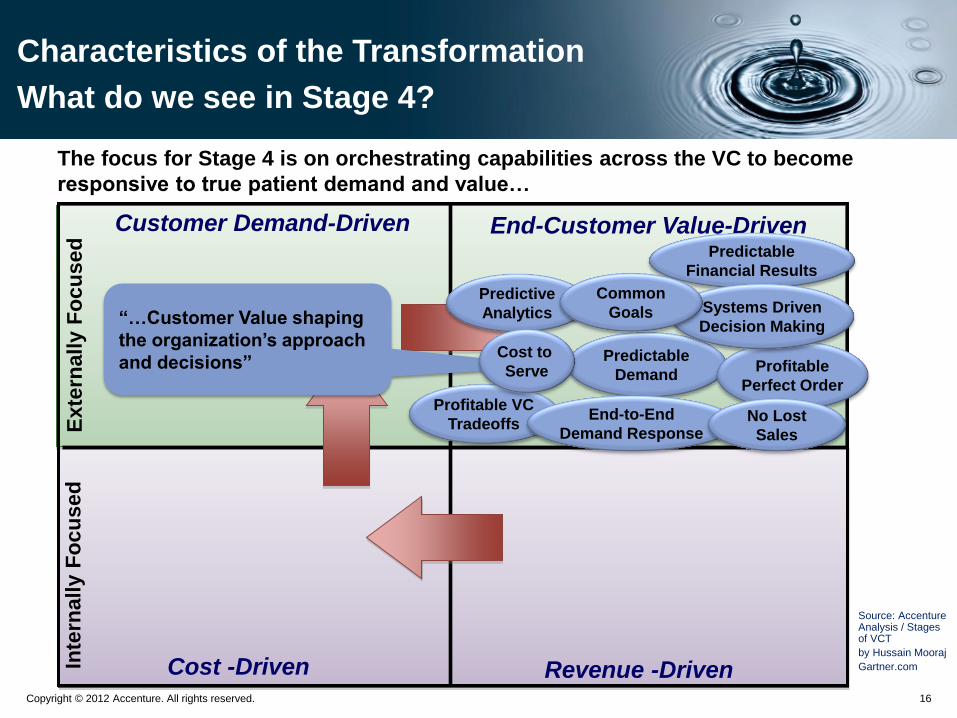

Characteristics of the Transformation

What do we see in Stage 4?

The focus for Stage 4 is on orchestrating capabilities across the VC to become

responsive to true patient demand and value…

Inte

rnall

y F

ocu

sed

E

xte

rnally F

ocu

sed

Predictive

Analytics

Customer Demand-Driven End-Customer Value-Driven

Profitable VC

Tradeoffs

Predictable

Demand

End-to-End

Demand Response

Profitable

Perfect Order

Predictable

Financial Results

“…Customer Value shaping

the organization’s approach

and decisions” Cost to

Serve

Systems Driven

Decision Making

Common

Goals

No Lost

Sales

Cost -Driven Revenue -Driven

Source: Accenture Analysis / Stages of VCT

by Hussain Mooraj

Gartner.com

Copyright © 2012 Accenture. All rights reserved. 17

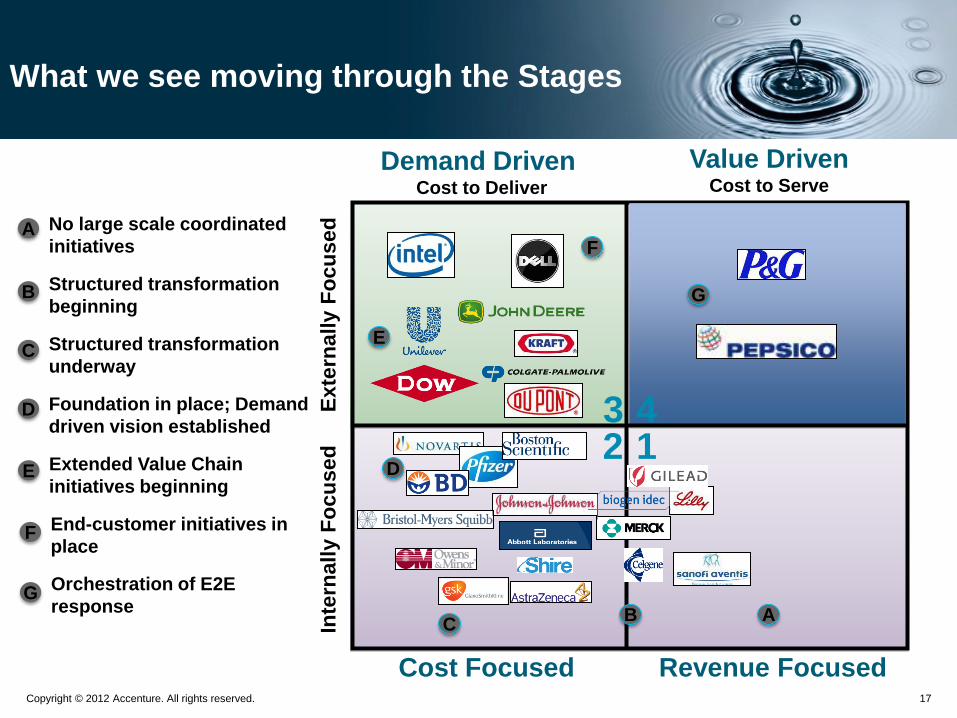

What we see moving through the Stages

Inte

rnall

y F

ocu

se

d

E

xte

rnally F

ocu

sed

Cost Focused Revenue Focused

Value Driven Cost to Serve

Demand Driven Cost to Deliver

1 2 3 4

D

C B A

A

B

C

D

Structured transformation

underway

Structured transformation

beginning

No large scale coordinated

initiatives

Foundation in place; Demand

driven vision established

E

E Extended Value Chain

initiatives beginning

F

F End-customer initiatives in

place

G

G Orchestration of E2E

response

Copyright © 2012 Accenture. All rights reserved. 18

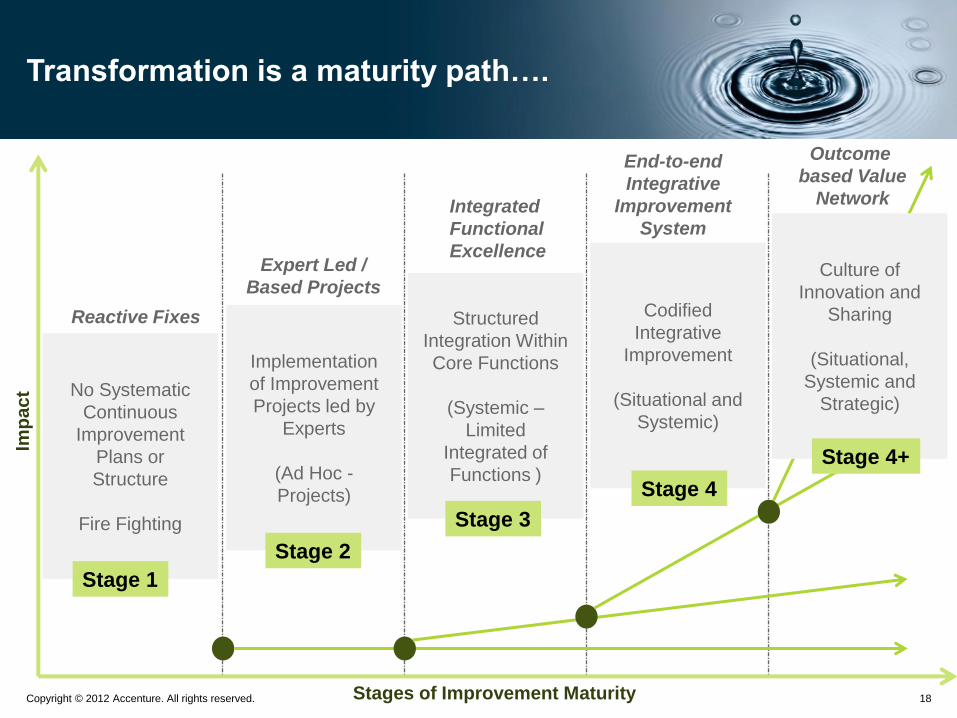

Implementation

of Improvement

Projects led by

Experts

(Ad Hoc -

Projects)

Structured

Integration Within

Core Functions

(Systemic –

Limited

Integrated of

Functions )

Codified

Integrative

Improvement

(Situational and

Systemic)

Culture of

Innovation and

Sharing

(Situational,

Systemic and

Strategic) No Systematic

Continuous

Improvement

Plans or

Structure

Fire Fighting

Transformation is a maturity path….

Stage 1

Stage 2

Stage 3

Stage 4

Integrated

Functional

Excellence

Stage 4+

Stages of Improvement Maturity

Imp

ac

t

End-to-end

Integrative

Improvement

System

Outcome

based Value

Network

Expert Led /

Based Projects

Reactive Fixes

Copyright © 2011 Accenture. All rights reserved. 19

Control Tower Framework

Copyright © 2012 Accenture. All rights reserved. 20

The Supply Chain Control Tower provides

organizations the required capabilities to

transition to next stage of maturity ...

• A set of capabilities (supply chain skills and

processes supported by advanced technology)

• Organized as a centralized shared service

• Focused to improve a specific business

objective

• An integration of supply chain processes and

tools across silos (enhanced collaboration)

• A set of lean capabilities targeting improvements

in transportation, inventory, warranty, customer

service, and SG&A

• A capability to monitor the execution of supply chain

activities, perform ‘what if’ analysis, and

dynamically respond to changes

A Control Tower is…

Copyright © 2012 Accenture. All rights reserved. 21

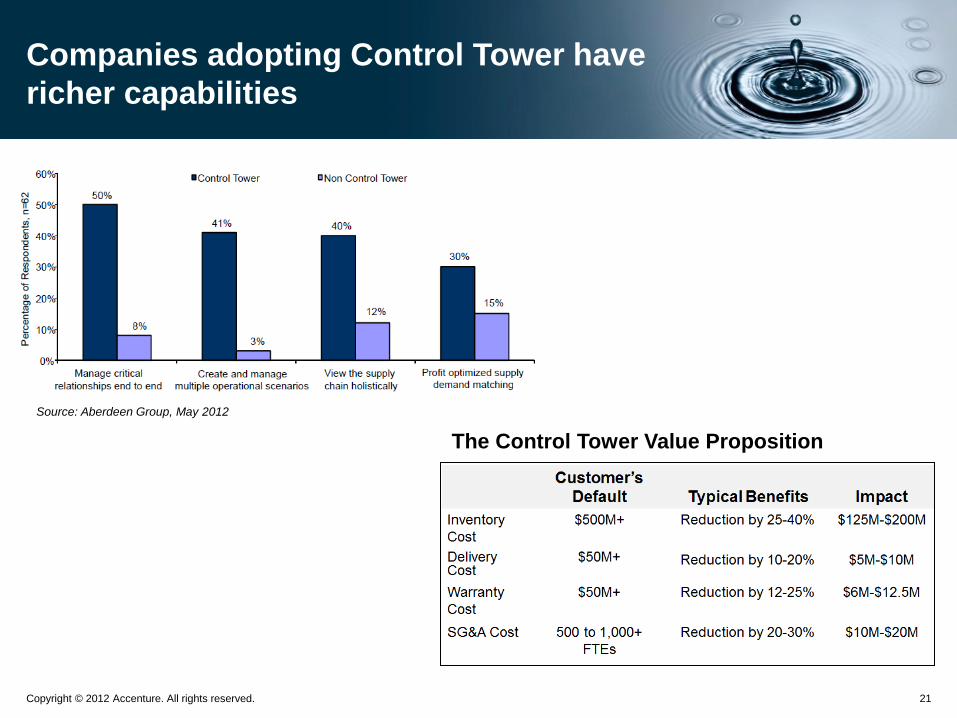

Companies adopting Control Tower have

richer capabilities

Source: Aberdeen Group, May 2012

The Control Tower Value Proposition

Copyright © 2012 Accenture. All rights reserved. 22

Establishing a Supply Chain Control

Tower

High initial investment High CapEx for technologies and facility

Complex integration effort

Long lead time to operationalize Potential multi-year endeavor, often super ceded by more short-term, urgent projects

Difficult to maintain Challenges with technology maintenance, upgrades and attaining and retaining talent

Advances in Technology Cloud and SaaS models are making the application integration efforts easier

Economies of Scale As more suppliers and partner are on-boarded into various visibility platforms, the effort is simplified for subsequent control towers

Control Tower “as a service” Service providers who can provide some/all of the functions available “as a service”

Historical Barriers Developments that are breaking down

these barriers

Copyright © 2012 Accenture. All rights reserved. 23

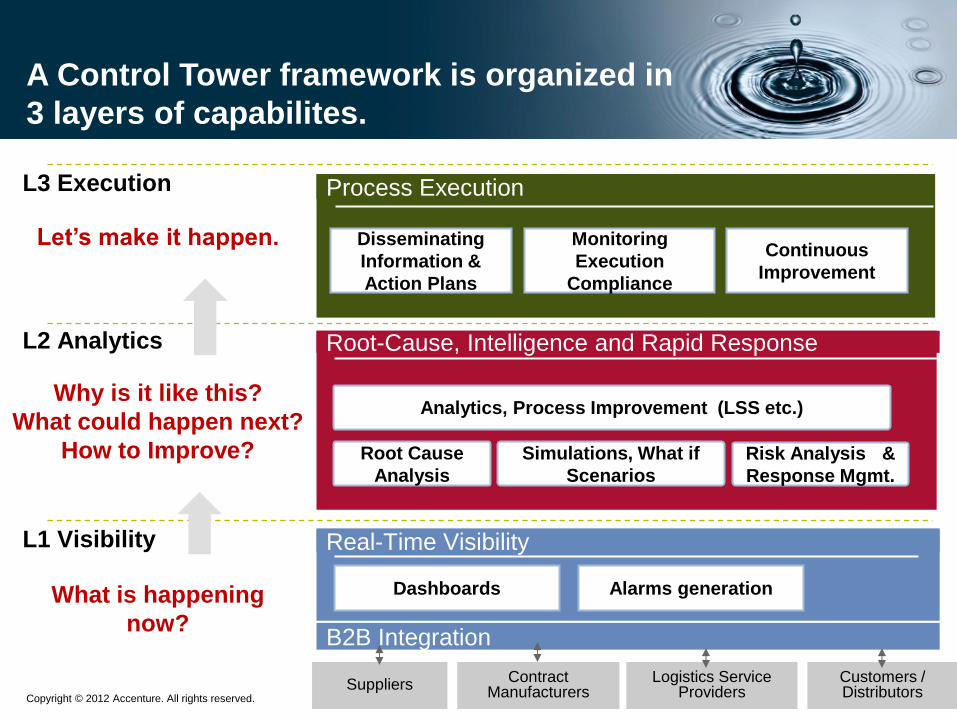

A Control Tower framework is organized in

3 layers of capabilites.

Let’s make it happen.

Why is it like this?

What could happen next?

How to Improve?

What is happening

now?

L1 Visibility

L2 Analytics

L3 Execution

Dashboards Alarms generation

B2B Integration

Suppliers Contract

Manufacturers Logistics Service

Providers Customers / Distributors

Real-Time Visibility

Root-Cause, Intelligence and Rapid Response

Process Execution

Disseminating

Information &

Action Plans

Monitoring

Execution

Compliance

Continuous

Improvement

Root Cause

Analysis

Simulations, What if

Scenarios

Risk Analysis &

Response Mgmt.

Analytics, Process Improvement (LSS etc.)

Copyright © 2012 Accenture. All rights reserved. 24

Ecosystem of vendors supporting Control

Towers - Sample

Copyright © 2012 Accenture. All rights reserved. 25

Who are a few leaders?

Unilever has setup control tower to give visibility and management control for their multiple transport

movements across Europe. It is now able to offer higher customer service at lower cost and with lower

carbon emissions.

The Control Tower platform gives Pfizer the ability to measure the flow of product, orders, and shipments to

establish fact-based sets and ongoing indicators of actual supply chain behavior.

L’Oréal Control Tower system allows it to synchronize information with all its vendors and thereby respond

much faster to market events.

The technology giant's global command centers coordinate parts logistics and field technicians to respond

swiftly to customers' requests.

P&G had installed 'control towers' to handle its distribution structures globally.

“The concept has produced enough savings in distribution costs that the control towers have paid for

themselves” - P&G executive

Copyright © 2011 Accenture. All rights reserved. 26

Questions and Discussion

Thank You !