CONTINUOUS DISCLOSURE UNDER BURSA SECURITIES LISTING REQUIREMENTS LEE SWEE SENG Advocate & Solicitor...

76

CONTINUOUS DISCLOSURE UNDER BURSA SECURITIES LISTING REQUIREMENTS LEE SWEE SENG Advocate & Solicitor LLB, LLM, MBA Notary Public Industrial Design Agent Trademarks Agent Patent Agent Certified Mediator [email protected] www.leesweeseng.com ©copyright

-

Upload

herbert-ross -

Category

Documents

-

view

216 -

download

0

Transcript of CONTINUOUS DISCLOSURE UNDER BURSA SECURITIES LISTING REQUIREMENTS LEE SWEE SENG Advocate & Solicitor...

CONTINUOUS DISCLOSURE UNDERBURSA SECURITIES

LISTING REQUIREMENTS

LEE SWEE SENG Advocate & Solicitor

LLB, LLM, MBA Notary Public

Industrial Design Agent Trademarks Agent

Patent Agent Certified Mediator

[email protected] www.leesweeseng.com

©copyright

What premium would you pay

for a company withgood governance?

The premium institutional investors would pay for a well-governed company varies by region…

30

22 22

14 13

EasternEurope/Africa

Latin America Asia WesternEurope

North America

Regions

Average premium percentage

McKinsey Global Investor Opinion Survey 2002

… and by country

4139 38

27 25 25 2422 22 21 20 20 19

16 15 14 13 13 12 11

Moro

cco

Egypt

Russia

Turk

ey

Indonesia

Chin

a

Arg

entina

Mala

ysia

Phillip

pin

es

Japan

Kore

a

Thaila

nd

Taiw

an

Italy

Sw

itzerland

US

Spain

Fra

nce

UK

Canada

Country

Average premium percentage

McKinsey Global Investor Opinion Survey 2002;2003 McKinsey/KIOD Survey on Corporate Governance

Disclosure & Transparency

Disclosure and transparency affect both a company’s operations and its performance as an investment. Operationally, rigorous disclosure and transparency systems enable management and the board of directors to allocate resources rationally and to run the business in accordance with strategic plans. In this respect, disclosure and transparency to managers and directors influence the company’s ability to generate cash flows, its intrinsic value.

OECD White Paper on Corporate Governance in Asia, 2003

Disclosure & Transparency

Release of TIMELY, TRUTHFUL and THOROUGH information promotes fair and efficient markets which determine the intrinsic value of companies.

Effective disclosure and transparency build investor confidence and address issues of directors and managers’ accountability.

Disclosure & Transparency

The intrinsic value of cash flows, combined with investors’ confidence in their ability to enjoy these cash flows, determines a company’s extrinsic, or market value.

Good systemic disclosure generates confidence in corporate credibility and market integrity.

OECD White Paper on Corporate Governance in Asia, 2003

Corporate Disclosure Policy

Bursa Securities Listing Requirements

(hereafter ‘LR’) 9.02(1):

“ … disclose to the public all material information necessary for informed investing and take reasonable steps to ensure that all who invest in its securities enjoy equal access to such information.”

6 specific disclosure policies

Immediate disclosure of material information (Chap 9 – Part C);

Thorough public dissemination (Chap 9 – Part D);

Clarification, confirmation or denial of rumours or reports (Chap 9 – Part E);

Response to unusual market activity (Chap 9 – Part F);

Unwarranted promotional disclosure activity (Chap 9 –

Part G); and Insider trading (Chap 9 – Part H).

Immediate Disclosure of Material Information

Main provision: LR9.03(1) - to be read in conjunction with LR9.05

LR9.04: Events which may require immediate disclosure

Specific immediate disclosure requirements: - LR9.19 Immediate announcements to the Exchange; - LR9.20 Announcement of corporate proposals; and - LR9.21 Dealings in quoted securities.

LR9.04 Examples of events which may require immediate disclosure

LR9.04(f):“the commencement of or the involvement in litigation and any material development arising therefrom”

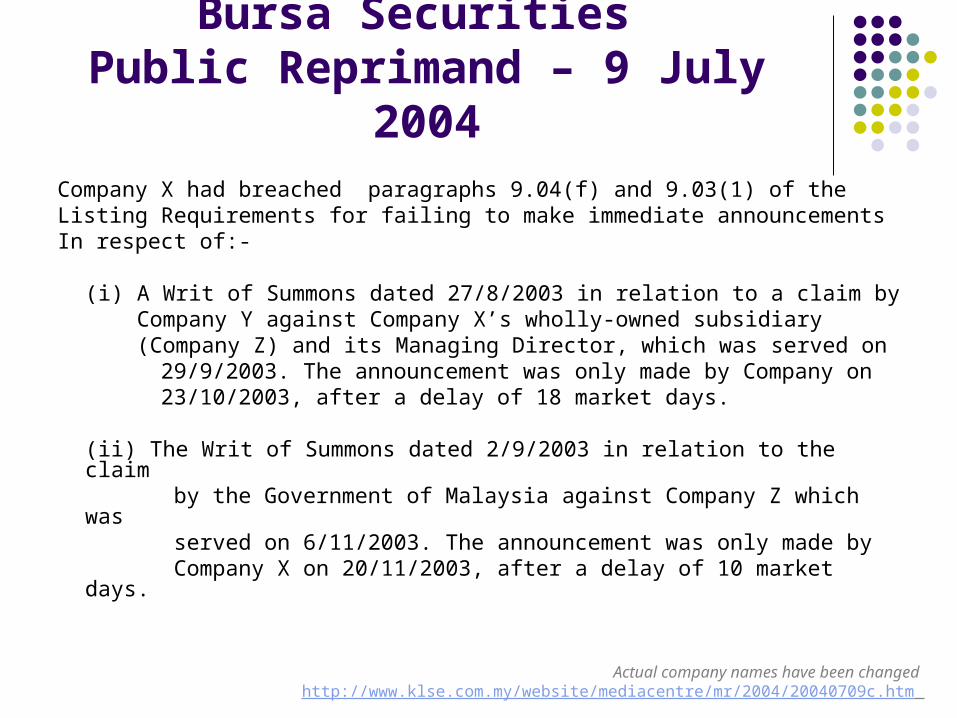

Bursa Securities Public Reprimand – 9 July 2004

Company X had breached paragraphs 9.04(f) and 9.03(1) of theListing Requirements for failing to make immediate announcementsIn respect of:-

(i) A Writ of Summons dated 27/8/2003 in relation to a claim by Company Y against Company X’s wholly-owned subsidiary (Company Z) and its Managing Director, which was served on

29/9/2003. The announcement was only made by Company on 23/10/2003, after a delay of 18 market days.

(ii) The Writ of Summons dated 2/9/2003 in relation to the claim by the Government of Malaysia against Company Z which was served on 6/11/2003. The announcement was only made by Company X on 20/11/2003, after a delay of 10 market days.

Actual company names have been changed http://www.klse.com.my/website/mediacentre/mr/2004/20040709c.htm

Conflicting Announcements

An issue:-

What if, as a consequence of

material litigation between 2 companies,

each releases conflicting announcements?

ICP vs. CEPCO: The claims

ICP’s claim: - CEPCO’s breach of contract between the

parties; - CEPCO’s specific performance of the

Management Agreement.

CEPCO’s counter-claim: - action against ICP for trespass and constructive

trusteeship

ICP vs. CEPCO: The outcome

The Court of Appeal found in favour of CEPCO and dismissed ICP’s claims with costs.

CEPCO’s 10/1/2005 Announcement

Amt. in Dispute : RM17,912,891.95 Interest Due : RM 5,221,817.23-----------------------------------------------------

RM23,134,709.18- Amt. Received: RM 6,379,772.60-----------------------------------------------------

RM16,754,936.58- Amt. Received: RM15,304,029.83----------------------------------------------------- Balance Payable : RM 1,450,906.75===============================

ICP’s 11/1/2005 Announcement

ICP consented to releasing the monies owed to CEPCO.

RM11,533,119.27 - value of CEPCO’s goods sold by ICP

- consent judgement sum

RM 2,800,178.16 - interest at 3.5% p.a.

------------------------

RM14,333,297.43 - amount paid to CEPCO on 21/5/2002

==============

Therefore, there is no outstanding amount owed to CEPCO.

ICP’s 11/1/2005 Announcement

RM17,912,891.95 – amount in dispute claimed by CEPCO

is unexplained and unaccounted for

RM 6,379,772.60 – amount claimed by CEPCO to be

ICP’s first payment was never paid by

ICP

RM 1,450,906.75 – balance payable claimed by CEPCO

will not be made

Conflicting Announcements

Another issue:-

Conflicting announcements by different Boards of Directors of the same company

http://announcements.bursamalaysia.com/EDMS/AnnWeb.nsf/LsvAllByID/482568AD00295D0748256C1B003735C5?OpenDocument ;

http://announcements.bursamalaysia.com/EDMS/AnnWeb.nsf/LsvAllByID/482568AD00295D0748256C2300393969?OpenDocument ;

http://announcements.bursamalaysia.com/EDMS/AnnWeb.nsf/LsvAllByID/482568AD00295D0748256C2B0042BA1C?OpenDocument

LR9.04 Examples of events which may require immediate disclosure

LR9.04(l):

“the occurrence of an event of default on interest and / or principal payments in respect of loans”

Bursa Securities Public Reprimands –

23 April & 20 August 2004

Company G had on 2 separate occasions breached LR9.04(l).

Pursuant to the first reprimand, Company G was found to be in breach of LR9.04(l) and PN1/2001 paras 2.1(d) and 2.1(e) for failing to make immediate announcements in respect of the default in payment of the banking facilities by the Company as announced by it on 6/10/2003. The delay in making the relevant announcements ranged from approximately 3 months to 19.5 months.

According to the second reprimand, Company G was again found to have been in beach of the same paragraphs in respect of the default in payment of the credit facilities by the Company and its subsidiary as announced by the Company on 25/3/2004. The delay in making the relevant announcements ranged from approximately 9 to 19 months.

Actual company names have been changed http://www.klse.com.my/website/mediacentre/mr/2004/20040423d.htm http://www.klse.com.my/website/mediacentre/mr/2004/20040820g.htm

9.04 Examples of events which may require immediate disclosure

9.04(o):

“the entry into a memorandum

of understanding”

MOUs

LR9.28:

“A listed issuer must make immediate announcements to the Exchange on the status of any memorandum of understanding that has been entered into between the listed issuer and a third party and which has been previously announced at least once every quarter or more regularly, upon the occurrence of a material change, whichever is earlier.”

But…

How definite are MOUs? Do MOUs necessarily represent a change in

the status quo? Are MOUs accorded the same status as a

legal contract? Should an announcement be made when a

MOU is entered into? If so, how and what exactly should be said?

MOUs

Abdul Rahim bin Syed Mohd v Ramakrishnan Kandasamy[1996] 3 MLJ 385

In dealing with preparatory agreements, the intention of the Parties is crucial in determining its legal effects. Each case must be decided on its own facts to determine the true intention of the Parties whether they intended to be bound by the contract immediately or subject to further contract to be entered into. It is therefore not sufficient to merely look at the label attached to the preparatory agreement.

continued…

MOUs

In certain exceptional cases, it may be established from a MOU that the Parties intend an immediately binding contract to come into force, even though a formal contract is to be entered into subsequently.

If it is intended by the Parties that no legally binding obligation shall arise unless and until a formal contract is signed, the Parties are at liberty to resile from the MOU without any legal consequences flowing from such action.

Immediate Disclosure Requirements

LR9.19 Immediate announcements to the Exchange

In particular LR9.19(19):

“A listed issuer must make immediate announcements to the Exchange upon the occurrence of … any commencement of winding-up proceedings against the listed issuer or any of its subsidiaries or major associated companies …”

Bursa Securities Public Reprimand – 9 July 2004

Company Z was found to be in breach of paragraph 19.19(19) of the Bursa Securities LR for failing to make an immediate announcement that the winding-up petition was served on the company by ABC Bank (“the Petition”) on 22 December 2003. The announcement of the Petition was only made to the Bursa on 15 January 2004 after a delay of 15 market days.

Actual company names have been changed http://www.klse.com.my/website/mediacentre/mr/2004/20040709b.htm

Immediate Disclosure Requirements

LR9.19 Immediate announcements to the Exchange

LR9.19(34):“A listed issuer must make immediate announcements to the Exchange upon the occurrence of … any deviation of 10% or more between the profit after tax and minority interest stated in the announced unaudited accounts and the audited accounts, giving an explanation of the deviation and the reconciliation thereof.”

Bursa Securities Public Reprimand – 26 November 2004

Company M was found to be in breach of Paragraph 9.19(34) of the Bursa Securities LR for failing to make an immediate announcement on 31/10/2003 in respect of the explanation of the deviation between the unaudited profit after taxation and minority interest of RM2.034 million and the audited loss after tax minority interest of RM2.064 million for the Financial Year Ending 30 June 2003. The explanation of the deviation was only announced on 19 January 2004.

Actual company names have been changed http://www.klse.com.my/website/mediacentre/mr/2004/20041126a.htm

Meaning of Material Information

Main provision: LR9.03 Material information:- information that is reasonably

expected to have an effect on:

- the “price, value or market activity” of securities (LR9.03(2)(a)); or

- securities holder / investor’s decision (LR9.03(2)(b)).

LR9.03(3): general (though not exhaustive) scope of material information

Withholding of Material Information

Main provision: LR9.05

Withholding of material information only in exceptional circumstances

When in doubt, “ … the presumption must always be in favour of disclosure.” (LR9.05(2))

What are exceptional circumstances?

When immediate disclosure would prejudice the ability of the listed issuer to pursue its corporate objectives (LR9.03(3)(a));

When the facts are in a state of flux and a more appropriate moment for disclosure is imminent (LR9.03(3)(b));

Where company or securities may restrict the extent of permissible disclosure (LR9.03(3)(c )).

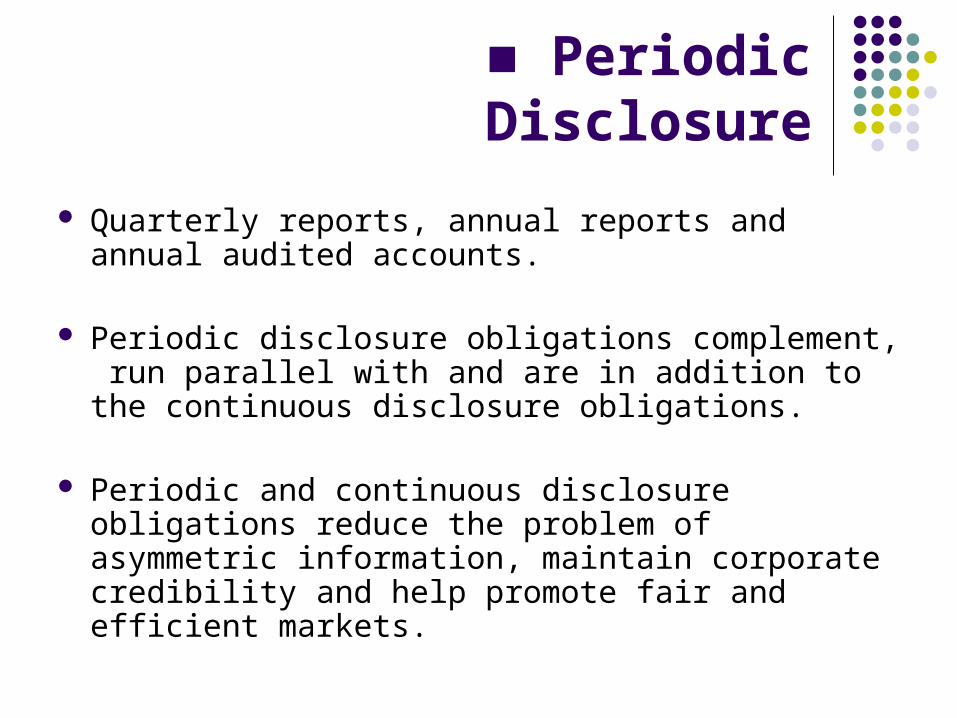

Periodic Disclosure

Quarterly reports, annual reports and annual audited accounts.

Periodic disclosure obligations complement, run parallel with and are in addition to the continuous disclosure obligations.

Periodic and continuous disclosure obligations reduce the problem of asymmetric information, maintain corporate credibility and help promote fair and efficient markets.

Delays in submission of periodic disclosure documents

2003 - 18 out of 78 (23.1%) public reprimands for failure to

furnish Annual Audited Accounts on time, the highest fine being RM54,000.

- 6 out of 78 (7.7%) public reprimands for failure to furnish Annual Reports on time, the highest fine being RM28,750.

- 6 out of 78 (7.7%) public reprimands for failure to furnish Quarterly Reports on time, the highest fine being RM57,000.

Best Practicesin Corporate Disclosure

Published in July 2004. - available online at Bursa Malaysia Securities Berhad’s

(“Bursa Securities”) website:<http://www.klse.com.my/website/documents/CDBP-final2004.pdf>

Developed with close reference to the disclosure requirements stated in the Bursa Securities Listing Requirements and other securities laws in Malaysia, as well as international practices from various jurisdictions which were adopted to suit the local environment.

Best Practicesin Corporate Disclosure

Aimed at providing some recommendations that could be integrated as part of the policies and procedures in ensuring that listed companies’ disclosure obligations are in line with that required under the Bursa Securities Listing Requirements.

Also intended to assist companies to move beyond making minimum disclosures.

Best Practicesin Corporate Disclosure

Although compliance with Best Practices is voluntary, companies are encouraged to adopt and integrate them into their own disclosure practices, polices and procedures to build and maintain corporate credibility and investor confidence.

Attention should be focused on the substance, and not form, of Best Practices.

Best Practices

1. Establish written policies and procedures (“Company Disclosure Policies and Procedures (CDPP)”) that encompass the Corporate Disclosure Policy and other requirements relating to corporate disclosure as set out in the Bursa Securities Listing Requirements (“Bursa Securities Disclosure Requirements”)

Best Practices 1

The CDPP should essentially promote the disclosure of material information that is accurate, clear, timely and complete.

It should also provide for the clear roles and responsibilities of directors, management, employees and all other relevant persons with regards to handling and disclosing material information.

Best Practices

2. The CDPP should deal specifically with procedures for maintaining confidentiality, preventing abuse of undisclosed material information and monitoring and responding to market rumours, leaks and inadvertent disclosures.

Best Practices 2

The CDPP should provide for procedures to maintain the confidentiality of material information that has yet to be made generally available.

It should also ensure that such material is not abused by persons connected directly or indirectly with the company by clearly setting out the possible civil and criminal sanctions.

A set of procedures should be developed for responding to market rumours, leaks and inadvertent disclosures.

Best Practices

3. A senior officer should be appointed to oversee and coordinate disclosures to make sure the company complies with the Bursa Securities Disclosure Requirements; including disclosure of information to analysts, institutional investors, the media and the investing public and create awareness amongst the directors, management and employees on the CDPP.

Best Practices 3

A ‘corporate disclosure manager’ who is:

- at senior management level;

- familiar with the company’s operations; and

- possess sufficient understanding of the Listing Requirements and securities laws.

Best Practices 3

She/he should oversee and maintain accurate records of all disclosure of material information by the company to the investing public, as well as keep up to date with any pending material development concerning the company.

The corporate disclosure manager’s degree autonomy or independence is the discretion of the company.

Best Practices

4. Ensure that only designated persons are the company’s spokespersons.

Best Practices 4

Authorised spokespersons should be aware that they must not disclose material information that has not been previously made public to a select few, such as analysts and institutional investors.

The corporate disclosure manager should arrange and coordinate, together with the authorised spokespersons, briefings to the investment community and the media on any disclosure of material information.

Best Practices

5. Ensure due compliance with the CDPP.

Best Practices 5

Procedures to monitor and ensure due compliance with the CDPP by the board of directors, management and employees should be put in place.

Factors contributing to non-compliance should be examined and problems rectified.

Enforcement is critical in ensuring due compliance with the CDPP

Best Practices

6. Ensure that those who are responsible for disseminating material information to the investing public, exercise due diligence in making sure that the information to be released is accurate, clear, timely and complete.

Best Practices 6

The CDPP must have in place a proper verification process that enables material information to be verified by competent designated officers, including the corporate disclosure manager (to ensure compliance with securities law and the Listing Requirements), before it is disclosed to the investing public.

Best Practices

7. Ensure that due care is observed when briefing and responding to analysts, institutional investors, the media and the investing public.

Best Practices 7

Procedures to be observed at Briefings and Review

Handling unanticipated questions - the ground rules include confining answers

to clarification of material information that has been publicly released and being aware of the need to avoid disclosing additional or new material information.

Best Practices 7

Responding on financial projections and reports

- a company must comment on errors in factual information, but the company need not comment on opinions made by the analysts.

Provide equal access to briefing materials

Best Practices

8. The company should take advantage of current information technology to disseminate relevant information to the investing public.

Illustrative examples of Announcements

Case Study: Media Report

“GMI Berhad is currently riding on the back of the market talk of its acquisition of an education-based company, ART Sdn Bhd, as part of its expansion plan in venturing into the education sector. GMI is reportedly in the midst of discussions with several property owners to build 2 campuses in Klang Valley. This augurs well with GMI’s plans as it has been awarded a contract by a large international conglomerate to conduct various programmes for more than 10,000 of its employees. At the same time, GMI may make a general offer for the shares of EDU Berhad, a leading player in the provision of twinning programmes in Klang Valley.”

Best Practices in Corporate Disclosure, 2004

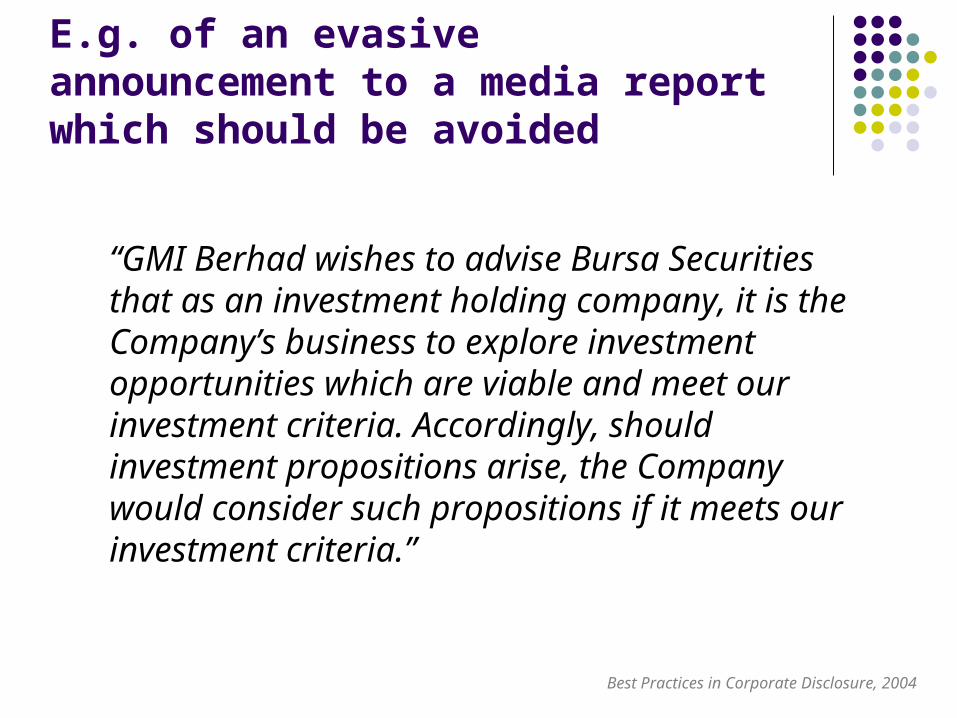

E.g. of an evasive announcement to a media report which should be avoided

“GMI Berhad wishes to advise Bursa Securities that as an investment holding company, it is the Company’s business to explore investment opportunities which are viable and meet our investment criteria. Accordingly, should investment propositions arise, the Company would consider such propositions if it meets our investment criteria.”

Best Practices in Corporate Disclosure, 2004

E.g. of an announcement to CONFIRM a rumour or report containing material information

“GMI Berhad wishes to confirm the reported articles as quoted above as true on the acquisition of an education-based company, namely ART Sdn Bhd. The details of the acquisition of ART Sdn Bhd are as follows:

[To provide full details of acquisition of ART Sdn Bhd, which should include the information prescribed under Appendix 10A of the Bursa Securities Listing Requirements]

…

Best Practices in Corporate Disclosure, 2004

E.g. of an announcement to CONFIRM a rumour or report containing material information

…

Further GMI wishes to confirm that it is engaging in preliminary discussions with some property owners to either acquire or lease their properties for 2 academic campuses in Klang Valley, one in Petaling Jaya and the other in Ampang, Kuala Lumpur. However, no formal agreement has been reached as at to date.

GMI will make the appropriate announcement to Bursa Securities in a timely manner in accordance with the Bursa Securities Listing Requirements should there be any further development on this matter.”

Best Practices in Corporate Disclosure, 2004

E.g. of an announcement to CLARIFY a rumour or report containing inaccurate material information

“GMI Berhad, having made due and diligent enquiry with the board of directors and major shareholders of the company, wishes to clarify that the company has merely tendered its bid to SPACE Ltd to conduct various technical and non-technical programmes mandatory for all its employees.

As at to date, the company has not received any award from the SPACE Ltd in relation to the project.

GMI Berhad will make the appropriate announcement to Bursa Securities in a timely manner in accordance with the Bursa Securities Listing Requirements, should there be any further development on this matter.”

Best Practices in Corporate Disclosure, 2004

E.g. of an announcement to DENY a rumour or report containing erroneous material information

“GMI Berhad, having made due and diligent enquiry with the board of directors and major shareholders of the company, wishes to state that the statement is not true as the company has no plan to make such general offer. Further, the company is not involved in any negotiation with any party which may trigger a general offer for the shares in EDU Bhd.”

Best Practices in Corporate Disclosure, 2004

Common Offences and Penalties

Out of the 326 investigation cases initiated and carried out on Public Listed Companies during the financial year ended 31/12/2003, 169 (51.8%) were due to failure in complying with disclosure requirements.

Investigation Cases initiated during the FYE 31/12/2003

48%

40%

1%

3% 5% 2%1%

Failure to comply w ith the policy on Response to Unusual Market Activity/Failure to promptly provide information ordocuments to the ExchangeFailure to comply w ith requirements on Corporate Disclosure Policy and Immediate Announcements

Failure to comply w ith Approved Accounting Standards

Failure to release Quarterly Reports on time

Failure to furnish Annual Audited Accounts on time

Failure to furnish Annual Reports on time

Others

Bursa Securities Annual Report 2003

Enforcement action taken against PLC for FYE 31/12/2003

Total number of actions taken: 201 - Actions relating to disclosure requirements:

140 (69.7%)

Various enforcement actions: - Caution & impress - Private reprimand - Public reprimand - Public reprimand & fine

Breakdown: Caution & impress

A3%

B67%

Others24%

F3%

E0%

C3%

D0%

A

B

C

D

E

F

Others

(A) Response to Unusual Market Activity / Prompt information to the Bursa

(B) Requirements on Corporate Disclosure Policy & Immediate Announcements

(C) Approved Accounting Standards

(D) Quarterly Reports(E) Annual Audited Accounts(F) Annual Reports

Bursa Securities Annual Report 2003

75.7% of all Caution and Impress actions were taken for breaching

some form of disclosure requirement

Breakdown: Private reprimand

(A) Response to Unusual Market Activity / Prompt information to the Bursa

(B) Requirements on Corporate Disclosure Policy & Immediate Announcements

(C) Approved Accounting Standards

(D) Quarterly Reports(E) Annual Audited Accounts(F) Annual Reports

A0%

F0%

E0%

C1%

D0%

Others52%

B47%

A

B

C

D

E

F

Others

Bursa Securities Annual Report 2003

48.6% of all Private Reprimand actions were taken for breaching

some form of disclosure requirement

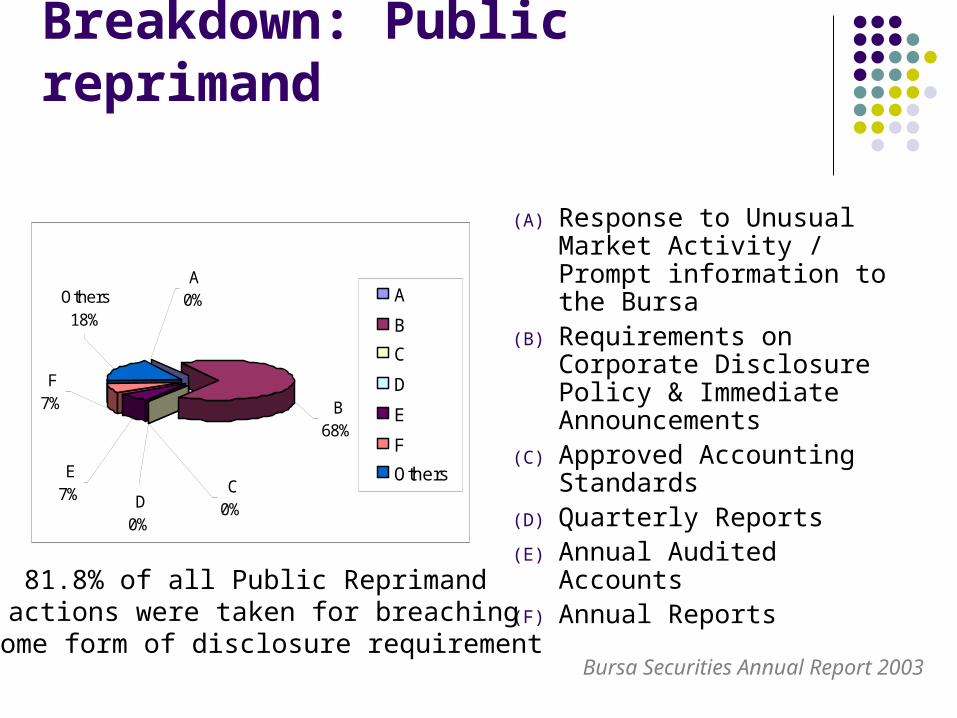

Breakdown: Public reprimand

(A) Response to Unusual Market Activity / Prompt information to the Bursa

(B) Requirements on Corporate Disclosure Policy & Immediate Announcements

(C) Approved Accounting Standards

(D) Quarterly Reports(E) Annual Audited Accounts(F) Annual Reports

Bursa Securities Annual Report 2003

F7%

E7% C

0%D0%

Others18%

B68%

A0% A

B

C

D

E

F

Others

81.8% of all Public Reprimand actions were taken for breaching

some form of disclosure requirement

Breakdown: Public reprimand & fine

(A) Response to Unusual Market Activity / Prompt information to the Bursa

(B) Requirements on Corporate Disclosure Policy & Immediate Announcements

(C) Approved Accounting Standards

(D) Quarterly Reports(E) Annual Audited Accounts(F) Annual Reports

Bursa Securities Annual Report 2003

87.2% of all Public Reprimand & Fineactions were taken for breaching

some form of disclosure requirement

F10%

E41%

C0%

D15%Others

13%

B21%

A0% A

B

C

D

E

F

Others

Common Offences and Penalties

Bursa Securities issued 32 public reprimands in 2004 for various breaches of the Listing Requirements.

Almost all offences were a result of breaching Chapter 9 Continuing Disclosure Requirements.

17 out of the 32 reprimands included penalties which involved fines that ranged from RM3,000 to RM400,000.

Public Reprimands by Bursa Securities in 2004

Public Reprimands by Bursa Securities in 2004

0

1

2

3

4

5

Offence - breach of

Fre

quen

cy

Public Reprimands with Penalties by Bursa Securities in 2004

Public Reprimands with Penalties by Bursa Securities in 2004

01234567

9.22(1) 9.23(b) 9.03(1) 9.23(a) 9.04(f) 9.04(l) 9.16(1) PN1/2001para

2.1(d)

PN1/2001para

2.1(e)

9.11(1)

Offence - breach of

Fre

quen

cy

Offences – breach ofFrequency

Listing Requirement Section

9.22(1) Quarterly Report Periodic Disclosure 6

9.23(b)Submission of Annual Audited

Accounts and Annual Report

Periodic Disclosure 6

9.03(1) Disclosure of Material InformationImmediate Disclosure of Material Information

4

9.23(a)Submission of Annual Audited

Accounts and Annual Report

Periodic Disclosure 3

9.04(f)Examples of Events which Require Immediate Disclosure

Immediate Disclosure ofMaterial Information

2

9.04(l)Examples of Events which Require Immediate Disclosure

Immediate Disclosure of Material Information

2

9.16(1)Content of Press or Other PublicAnnouncement

Preparation of Announcements 2

PN 1/2001 para 2.1(d)

(affects 9.03 & 9.04)Immediate Disclosure of Material Information

2

PN 1/2001 para 2.1(e)

(affects 9.03 & 9.04) Immediate Disclosure of Material Information

2

9.11(1) Unusual Market ActivityResponse to Unusual MarketActivity

1

Total number of separate offences 26

Graphically…

50%

40%

7% 3%

Periodic Disclosure

ImmediateDisclsoure ofMaterial Information

Preparation ofAnnouncements

Unusual MarketActivity

Periodic Disclosure Offences: 15 (50%)Immediate Disclosure Of Material Information Offences:12 (40%)

Conclusion

Given the high incidence of breaches of disclosure requirements, companies are strongly urged to adopt the Best Practices in Corporate Disclosure.

Create an environment that maintains corporate credibility, investor confidence and market efficiency.

Conclusion

“In today’s globalised environment, investors can easily switch their investments across companies and markets. Corporate governance acts as a mode of brand differentiation. Thus a reputation for high standards of corporate governance and transparency is all the more important for emerging economies that are still forging their reputation in the global investing community, where typically not as much resources are devoted to comprehensive coverage of smaller markets. In short, good corporate governance is not a luxury; it is a necessity.”

Zarinah Anwar & Kar Mei Tang, “Building a Framework for Corporate Transparency – Challenges for Global Capital Markets and the Malaysian Experience”

International Accountant, February 2003

THE ENDTHANK YOU