Continued from previous lecture… READING: Finish the textbook. 1.

27

Continued from previous lecture… READING: Finish the textbook. 1

-

Upload

clementine-cunningham -

Category

Documents

-

view

222 -

download

1

Transcript of Continued from previous lecture… READING: Finish the textbook. 1.

Continued from previous lecture…

READING:

Finish the textbook.

1

Brazilian President Dilma Rousseff referred to unstable capital flows as a "liquidity tsunami"

11 Apr 2012: http://www.aljazeera.com/indepth/opinion/2012/04/20124894553253392.html

2

Brazilian exports getting crushed by currency appreciation

3

Do trilemma solutions need to be compatible across countries?

• Brazil is complaining now

• Used to have a fixed XR

• Then East Asian Financial Crisis hit

• Currency value collapses under speculation (Dec 1998/ Jan 1999)

• MERCOSUR?

• Argentina’s exports become uncompetitive over night

• Argentina’s currency collapses in 2002

4

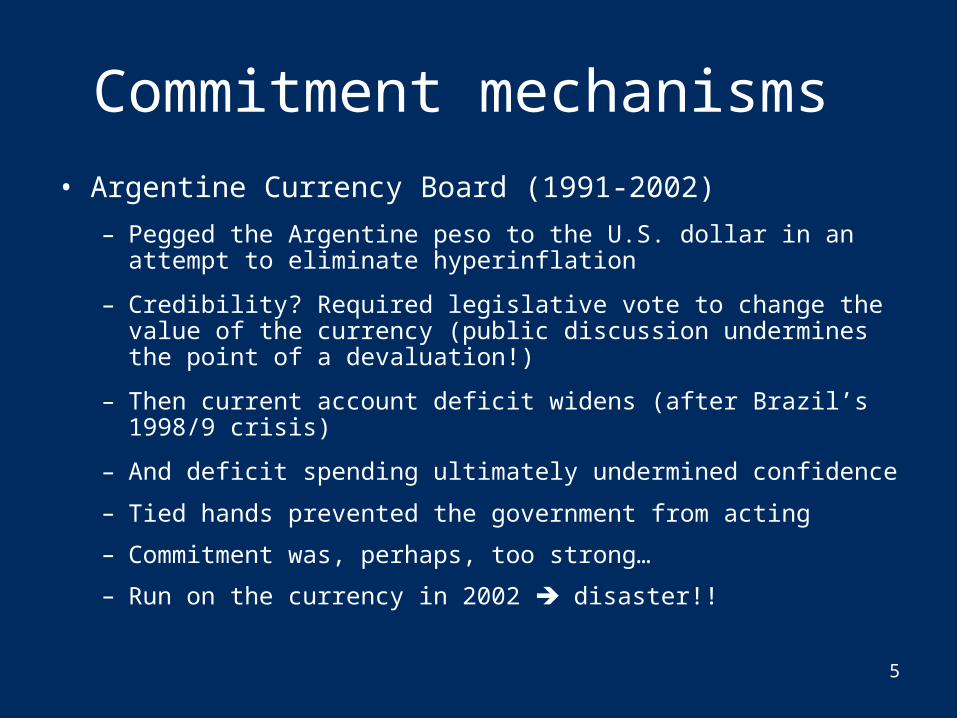

Commitment mechanisms

• Argentine Currency Board (1991-2002)

– Pegged the Argentine peso to the U.S. dollar in an attempt to eliminate hyperinflation

– Credibility? Required legislative vote to change the value of the currency (public discussion undermines the point of a devaluation!)

– Then current account deficit widens (after Brazil’s 1998/9 crisis)

– And deficit spending ultimately undermined confidence

– Tied hands prevented the government from acting

– Commitment was, perhaps, too strong…

– Run on the currency in 2002 disaster!!

5

What does a “run” look like?

• https://www.youtube.com/watch?v=iPkJH6BT7dM

6

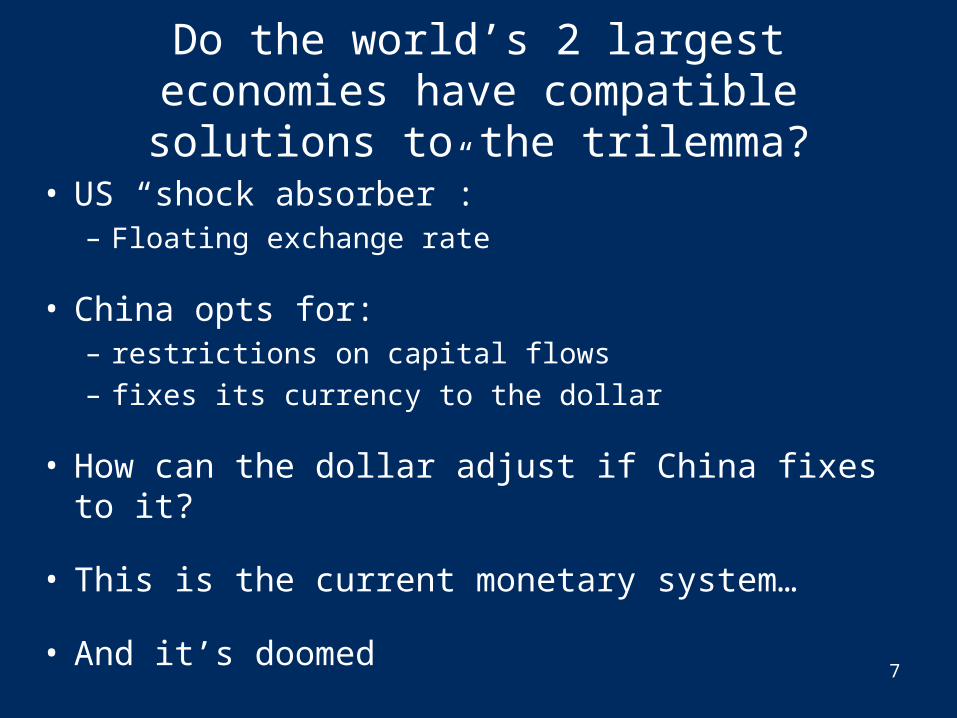

Do the world’s 2 largest economies have compatible solutions to the trilemma?

• US “shock absorber”:– Floating exchange rate

• China opts for:– restrictions on capital flows– fixes its currency to the dollar

• How can the dollar adjust if China fixes to it?

• This is the current monetary system…

• And it’s doomed 7

Exchange rates & protectionism

• “Currency manipulator” ??

• Should the WTO be involved in regulating the exchange rate?

8

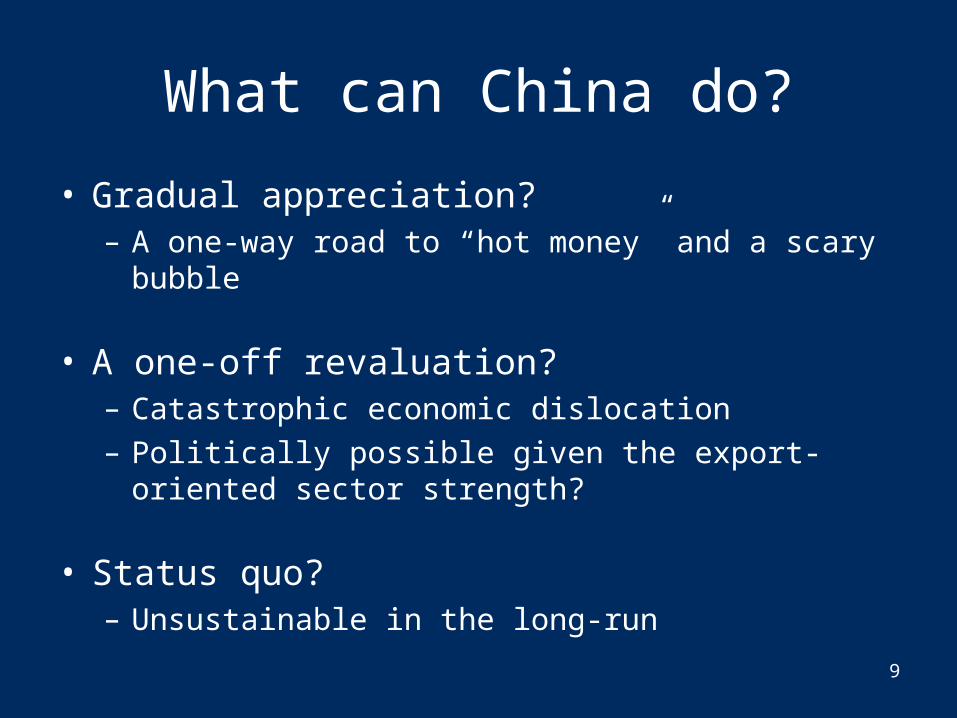

What can China do?

• Gradual appreciation?– A one-way road to “hot money” and a scary bubble

• A one-off revaluation?– Catastrophic economic dislocation– Politically possible given the export-oriented sector

strength?

• Status quo?– Unsustainable in the long-run

9

http://www.ft.com/intl/cms/s/0/7e010a5a-8324-11e1-9f9a-00144feab49a.html#axzz1rjqaPoVT

10

11

• Complaints from Mexico about Chinese currency• But even as their currency appreciated, it was far below where it

was before the crisis

12

http://www.bea.gov/newsreleases/international/transactions/transnewsrelease.htm

13

So, are global imbalances the fault of the United States?

• How can the US get away with running Current Account deficits year after year?

• Capital Account surpluses

• Why?

• Are we really a great place to invest?

• International Reserve Currency– The world has coordinated on the dollar

14

Her

Him Football Ballet

Football 4,3 2,2

Ballet 1,1 3,4

4>3>2>1

“Battle of the sexes”

15

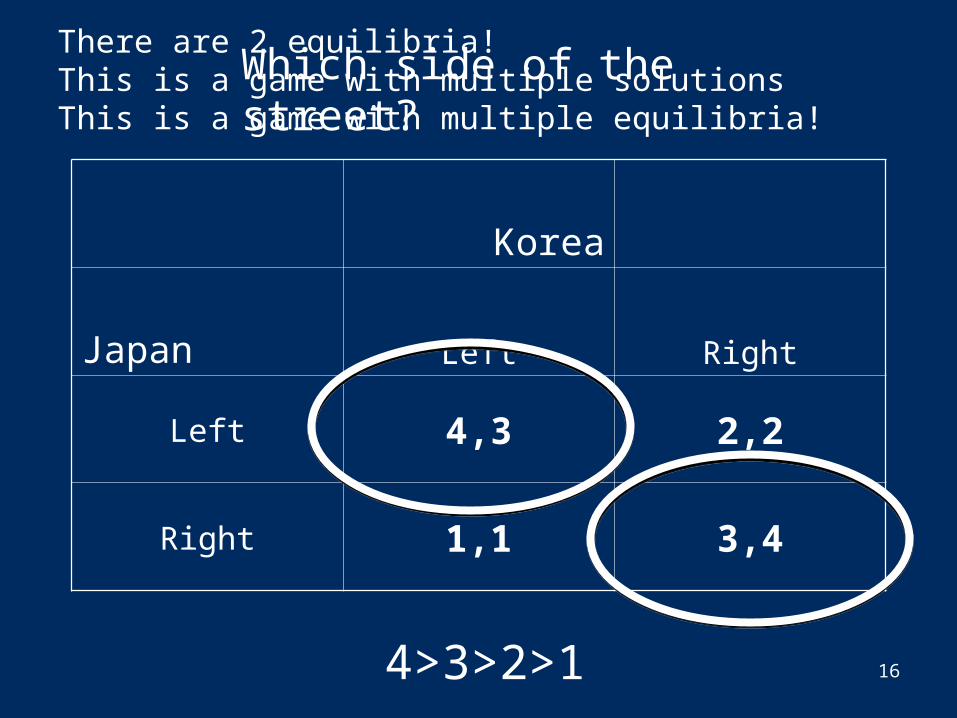

Korea

Japan Left Right

Left 4,3 2,2

Right 1,1 3,4

4>3>2>1

Which side of the street?There are 2 equilibria!This is a game with multiple solutionsThis is a game with multiple equilibria!

16

17

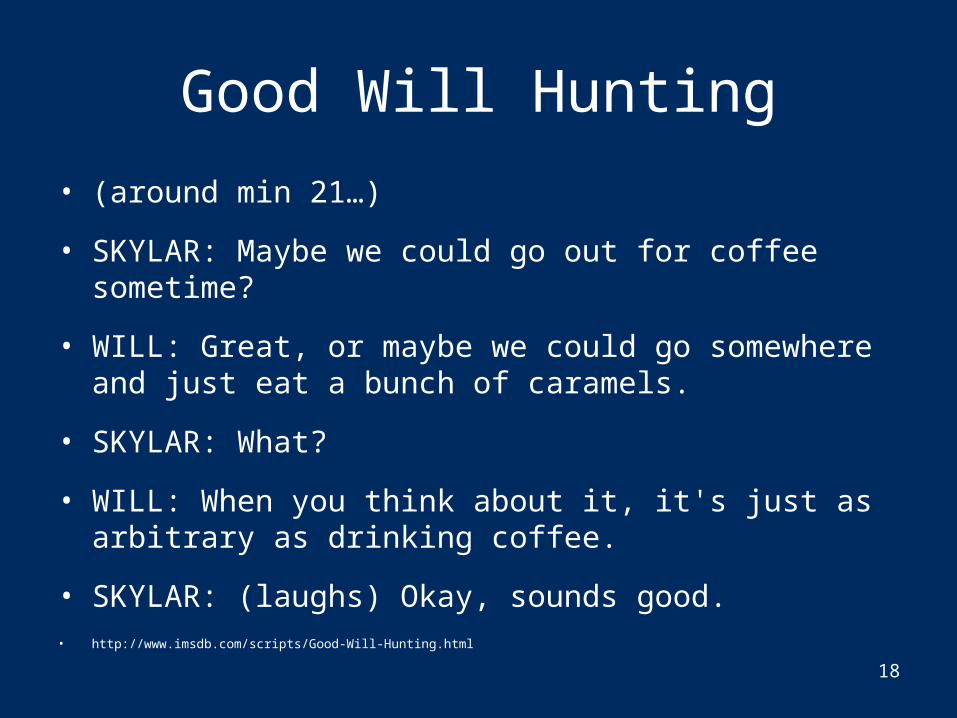

Good Will Hunting

• (around min 21…)

• SKYLAR: Maybe we could go out for coffee sometime?

• WILL: Great, or maybe we could go somewhere and just eat a bunch of caramels.

• SKYLAR: What?

• WILL: When you think about it, it's just as arbitrary as drinking coffee.

• SKYLAR: (laughs) Okay, sounds good.• http://www.imsdb.com/scripts/Good-Will-Hunting.html

18

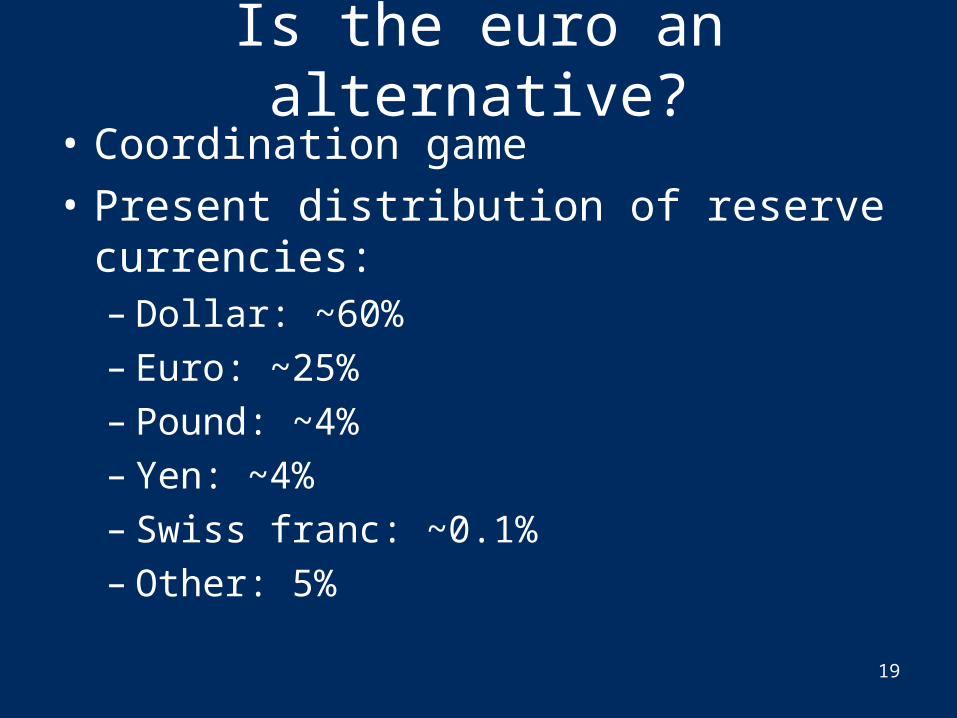

Is the euro an alternative?• Coordination game

• Present distribution of reserve currencies:– Dollar: ~60%– Euro: ~25%– Pound: ~4%– Yen: ~4%– Swiss franc: ~0.1%– Other: 5%

19

Obstacles

• A focal point: The more people who use an international currency, the more effective it is (increasing returns to scale)

• No equivalent to the US treasury bill @ the EU level

• Leadership – who bails you out?

– US track record v. EU (…Greece?)

20

Is the renminbi an alternative?

21

Be careful what you wish for…

• Benefits of international reserve currency– finance fiscal deficits– enhance international prestige– debt denoted in your own currency

• Costs of international reserve currency– Monetary policy autonomy is hindered - vast

quantities of your currency held abroad– Overvaluation leads to uncompetitive

export-oriented/import-competing sectors

22

Is the SDR an alternative?

23

In CRYPTOGRAPHY we trust?

24

25

Take-homes on Euro

• Solves the old problem that the IMF failed to solve

• Still limited as a currency– No EU level bond

• Will it become the new international reserve currency?

– Probably not any time soon

– Coordination game

– The Dollar is still “noon, Grand Central information booth”

26

Thank youWE ARE GLOBAL GEORGETOWN!

27