SECTION 90 OF THE INCOMETAX ACT, 1961 DOUBLE TAXATION ... file1/13/2015 Income Tax Department ...

Upload

shonda-johnsonCategory

view

213download

0

Contents of Presentation - Taxation system in IndiaBackground of Income Tax Act, 1961Proposed Direct Tax Code 2010Overview with Special reference to Personal

Taxation

Historically, income tax in India has always existed as elsewhere.

The old Income Tax Act of 1922 was replaced by the present Income Tax Act, 1961.

It was introduced after considering expert opinions of N.A.Palkhivala, P. Satyanarayan Rao , G.N.Joshi & many more.

Taxation System in IndiaThe present Income Tax Act, 1961 levies tax

on income earned by an assessee in India from different sources during financial year.

However, continuous evolution to keep pace with changes in business, to bring to the book the tax offenders and at the same time provide relief to innocent taxpayers required changes in tax laws.

Taxation System in IndiaThis necessitated amendments to Finance

legislation during the year as well as at the year end.

This resulted in complexities in operation as well as implementation of various provisions.

Diverse interpretations also added fuel to fire.

Taxation Systems in IndiaVarious committees including Tax Reform

Committee (Dr. Raja Chellia) in 1992 and Dr. Kelkar Committee in 2001 impressed upon need to reform and streamlining of Taxation Laws in India.

The objective was to simplify and rationalize the Income Tax Provisions as they stood.

The concept paper of Direct Tax Code was introduced.

Taxation System of IndiaThe original DTC had undergone various

changes with latest amendment to Direct Tax Code being proposed in August 2010.

The reforms to Direct Tax are being viewed with reference to DTC, 2010.

Direct Tax Code, 2010The present Direct Tax Code is being made

effective April 01, 2012.Hence, the provisions shall be applicable for

all the transactions carried during the Financial Year 2011-12 [April 01, 2011 to March 331,2012].

Direct Tax Code, 2010Proposed DTC is bulkier than the existing

one.It has 20 Chapters divided into nine parts.It has 319 sections and 22 schedules as

against 298 sections and 14 schedules in the existing act.

Proposed DTC will replace existing Wealth Tax Act, 1957.

Direct Tax Code, 2010It deals with –

Income TaxDividend Distribution TaxTax on Distributed IncomeBranch Profit TaxWealth TaxPrevention of Abuse of the CodeTax ManagementGeneral Provisions; ANDInterpretation of the Code.

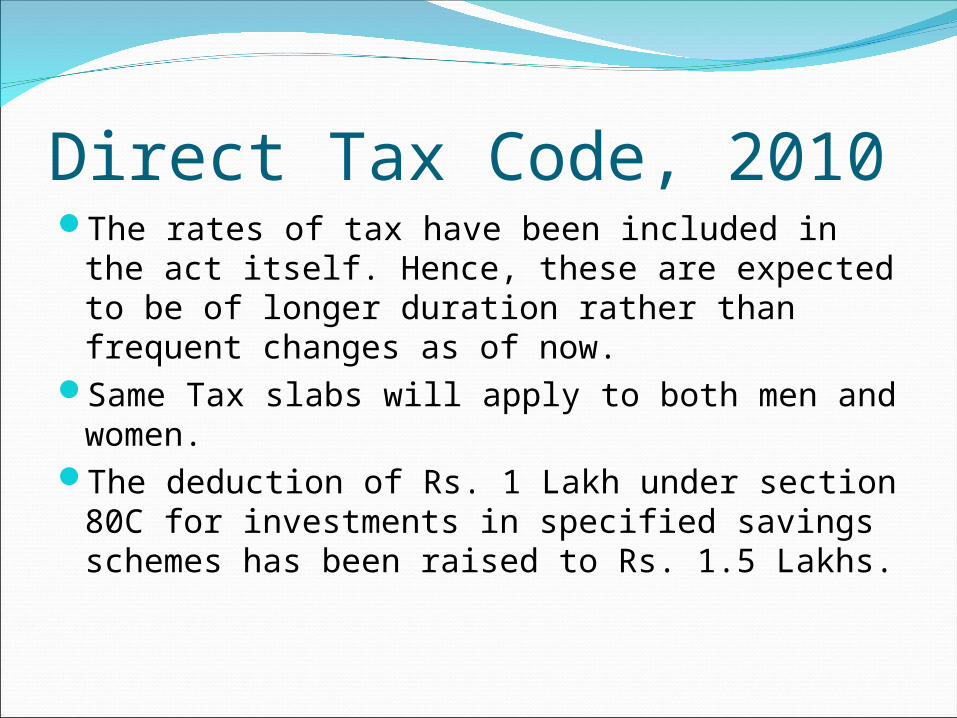

Direct Tax Code, 2010The rates of tax have been included in the act

itself. Hence, these are expected to be of longer duration rather than frequent changes as of now.

Same Tax slabs will apply to both men and women.

The deduction of Rs. 1 Lakh under section 80C for investments in specified savings schemes has been raised to Rs. 1.5 Lakhs.

Personal Tax Slabs

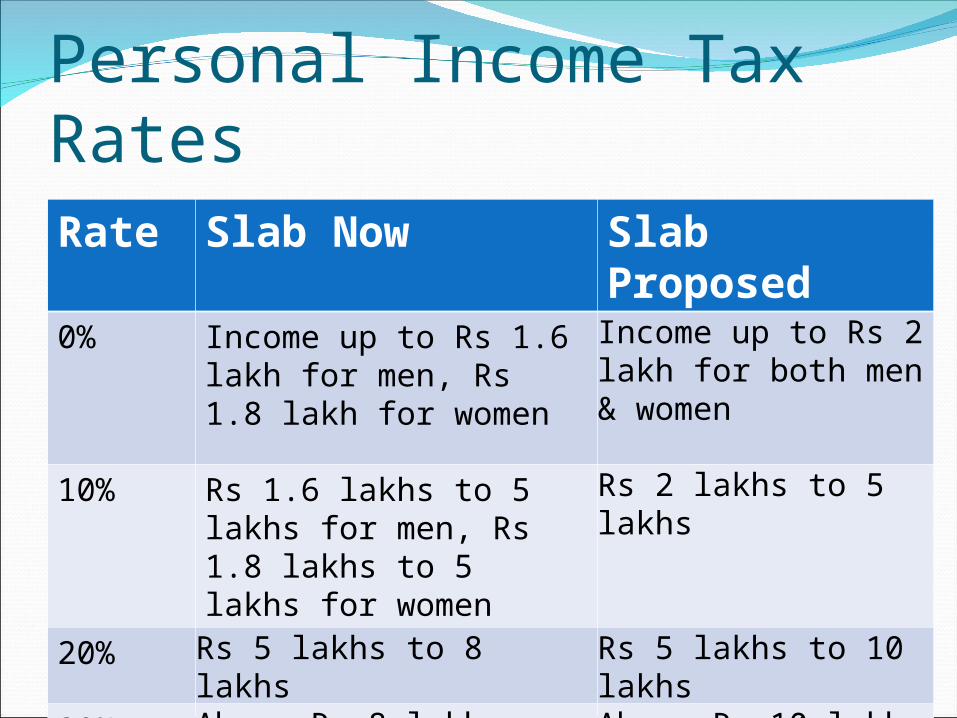

Personal Income Tax RatesRate Slab Now Slab

Proposed0% Income up to Rs 1.6 lakh for men, Rs 1.8 lakh for womenIncome up to Rs 2 lakh for both men & women10% Rs 1.6 lakhs to 5 lakhs for men, Rs 1.8 lakhs to 5 lakhs for womenRs 2 lakhs to 5 lakhs

20% Rs 5 lakhs to 8 lakhs Rs 5 lakhs to 10 lakhs30% Above Rs 8 lakhs Above Rs 10 lakhs

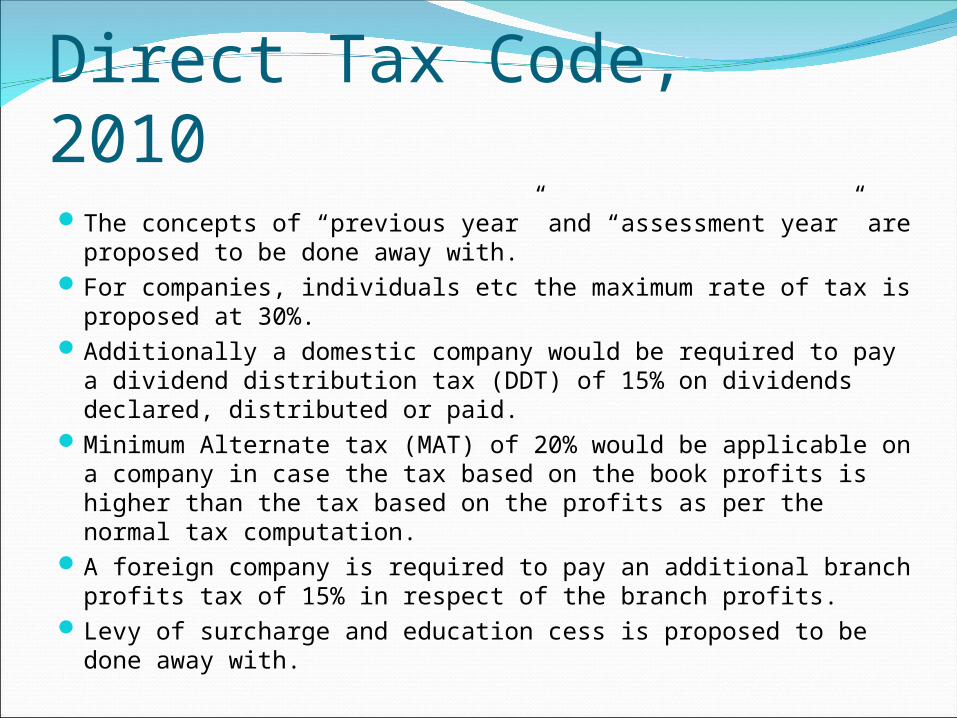

Direct Tax Code, 2010The concepts of “previous year” and “assessment year” are

proposed to be done away with.For companies, individuals etc the maximum rate of tax is

proposed at 30%. Additionally a domestic company would be required to pay a

dividend distribution tax (DDT) of 15% on dividends declared, distributed or paid.

Minimum Alternate tax (MAT) of 20% would be applicable on a company in case the tax based on the book profits is higher than the tax based on the profits as per the normal tax computation.

A foreign company is required to pay an additional branch profits tax of 15% in respect of the branch profits.

Levy of surcharge and education cess is proposed to be done away with.

Residence - CompanyIn the case of a company, it is proposed that the

company shall be resident in India if it is an Indian company or if the place of effective management (POEM) is in India.

POEM has been defined to mean the place where the board of directors or executive directors make their decisions or the place where such executive directors or officers of the company perform their functions and the board of directors routinely approves the commercial and strategic decisions taken by such executive directors or officers.

Residence - IndividualIn all cases, other than an individual, the

persons would be a resident in India, if the place of control and management of the affairs, at any time of the year is situated wholly, or partly, in India.

Computation of Total IncomeIncome from Ordinary Sources

Income from Special Sources

Income from Employment

Income of Non-Residents

House Property Income

Winning from Race-Horses

Business Income Winnings from Lottery

Capital Gains

Residuary Sources

Personal TaxesChanges in income slabs which will result in incremental savings in tax.

The concept of Not ordinarily resident is removed. The condition of 729 days has been retained to determine the taxability of overseas income of an individual

A person not entitled to HRA is allowed a deduction of rent paid up to 10% of GTI or INR 2,000 per month & other conditions as may be prescribed

Exemption for medical expenses has been increased to INR 50,000.

Contribution to approved funds is deductible to the extent of INR 1 lakh.

Deduction for insurance premium (not exceed five percent. of the capital sum assured), Health Insurance covered & Tuition fees to the extent of INR 50,000.

Wealth tax to be levied at 1% for wealth in excess of INR 10 million

Capital GainsIncome from all investment assets to be computed

under the head „Capital gains. Investment asset to include any capital asset which is not a business capital asset, any security held by a Foreign Institutional Investor and any undertaking or division of a business.

Distinction between short-term investment asset and long-term investment asset on the basis of the length of holding of the asset to be eliminated.

No tax on gains on transfer of shares of a company or unit of equity oriented fund that are held for more than one year and such transfer is chargeable to Securities Transaction Tax (“STT”). STT would be chargeable on transfer of equity shares of a company or a unit of an equity oriented fund.

Capital GainsFifty percent of the capital gains are allowed as

deduction on transfer of shares of a company or unit of equity oriented fund that are held for a period of one year or less and such transfer is chargeable to STT.

The base date for determining the cost of acquisition to be shifted from 1 April 1981 to 1 April 2000. Consequently, all unrealized capital gains on assets between 1 April 1981 and 31 March 2000 not to be liable to tax.

Cost of acquisition to be Nil, if cannot be determined or ascertained for any reason.

Anti- abuse provisions –General Anti Avoidance Rules

The characteristics of the originally proposed rules have been retained.

Additionally it is proposed that an arrangement would be presumed for obtaining a tax benefit would include reduction in tax base including increase in losses. The provisions would be applicable as per the guidelines to be framed by the Central Government.

Further the definition of lacking commercial substance has been amended to clarify that obtaining tax benefit cannot be the only criteria for applicability of GAAR.

Income from house property Income from house property on the basis of gross rent

i.e. the amount of rent received or receivable contractually for the financial year

Deduction on account of interest on housing loan in case of a self occupied property (subject to an upper limit of `150,000) as well as pre- construction/ acquisition period interest in five equal installments

no relief has been provided for the principal amount of repayment of loan as is prevailing in Section 80C of the present Income-tax Act

standard deduction on account of repairs and maintenance has been reduced from the existing 30% of (gross rent less municipal taxes) to 20% of gross rent

Wealth TaxAll assessees are covered other than a nonprofit

organization. At present only few assets are covered. However,

the proposed code proposes to add tax also on following specified assets – Archaeological collections, Drawings, sculptures or any other work of

Art. Watch having value in excess of Rs 50000/-. Interest in foreign trust or any other body located outside India

(Whether incorporated or not) other than a foreign company. Equity or preference shares held by a resident in a CFC. Cash in hand in excess of ` 2,00,000/- in case of an individual. Bank deposits outside India, in case of individuals and HUFs, and in the

case of other persons, any such deposit not recorded in the books of account.

Criticism – Many experts are seeking an answer to the question,

‘Do we need the new code in the present form?’The new DTC may not reduce litigation but might as

well provide new controversies and more room for litigations and disputes.

A company may be treated as ‘resident’ in India even if its effective management is partly situated in India. This being subjective, may lead to controversies.

In cases of prosecution, the minimum fine has been prescribed at Rs. 50,000/- as against ‘NIL’ in the present act.

Criticism contd. . . Commissioner (Appeals) has been restricted

to consider matters considered by AO as against the wide power in the existing act.

General Anti Avoidance Rules have been prescribed in such a manner to cast duty on assessee to prove that his affairs were not entered into for avoidance of tax.

Other administrative provisions also are under criticism.

Sum up – DTC has proposed simplifications which are

not so simple.The changes in the DTC Draft within 1 year

leaves one wondering as to the fate of future contents or changes till DTC replaces present Income Tax Act, 1961.

Personal Taxation has brought relief to individuals.

Rules as to withholding tax have been more or less retained same.

![Taxation of Charitable Trustsvoiceofca.in/.../document/13_07_16_CharitableTrusts... · Taxation of Charitable Trusts Educational Institutions [Under Income Tax Act, 1961] ... Levy](https://static.fdocuments.in/doc/165x107/5f876b3ff09240756f284049/taxation-of-charitable-taxation-of-charitable-trusts-educational-institutions-under.jpg)

![KSA Model Exam TAX INTER NEW ANSWER KEY › docs › model › TAXATION NEW ANS... · 2019-04-25 · Less: Depreciation allowable under the Income-tax Act, 1961 [See Working Note]](https://static.fdocuments.in/doc/165x107/5f0f05fd7e708231d4421b52/ksa-model-exam-tax-inter-new-answer-key-a-docs-a-model-a-taxation-new-ans.jpg)

![INCOME-TAX ACT, 1961€¦ · INCOME-TAX ACT, 1961 * [43 OF 1961] [AS AMENDED BY FINANCE ACT, 2008] An Act to consolidate and amend the law relating to income-tax and super-tax BE](https://static.fdocuments.in/doc/165x107/6097f37f4534cb51153b4a4c/income-tax-act-1961-income-tax-act-1961-43-of-1961-as-amended-by-finance.jpg)