Container Shipping & Trade 1st Quarter 2016

48

“The market was great, then it got terrible, and right now, it is stable, but at a much lower level then it should be.” Andrew Abbott, Atlantic Container Line CEO, on the transatlantic tradelane, page 14 ULCS: how big can they grow? No time to delay on container weighing preparation, warns Global Shippers’ Forum COSCOCS: the rise of a new superpower 1st Quarter 2016 www.containerst.com

-

Upload

rivieramaritimemedia -

Category

Documents

-

view

220 -

download

2

description

Container Shipping & Trade brings experienced editorial commentary to the container shipping market and provides authoritative coverage of not only container shipping but also technical features of the container ship fleet and the wider container supply chain.

Transcript of Container Shipping & Trade 1st Quarter 2016

“The market was great, then it got terrible, and right now, it is stable, but at a much lower level then it should be.” Andrew Abbott, Atlantic Container Line CEO, on the transatlantic tradelane, page 14

ULCS: how big can they grow?

No time to delay on container weighing preparation, warns

Global Shippers’ Forum

COSCOCS: the rise of a new superpower

1st Quarter 2016 www.containerst.com

Bureau Veritas,your Class for Containerships

Visit us on: www.bureauveritas.com

AP_Marine_A4-1:AP_Marine_A4-1 01/08/14 17:20 Page1

Innovate in safety, quality and energy efficiency

contents

For more articles visit www.containerst.com Container Shipping & Trade | 1st Quarter 2016

26

18

11

34

Regulars3 COMMENT

4 BEST OF THE WEB

44 LAST WORD

Market updates6 Freight rates reached historical lows last year and this trend looks set to

continue in 2016, driven by overcapacity and weak demand

8 The round of merger and acquisition activity in the container shipping industry

will have a major effect on the league table of the world’s largest box ship

owners (VesselsValue.com)

Ship description11 United Arab Shipping Co has deployed its second 18,800 teu LNG ready box

ship Al Muraykh

Trade route14 The traditionally balanced transatlantic trade has tipped as a result of the

cascading of larger vessels into this market

Customer profile18 Mandatory container weighing, market-based measures for CO2 emissions

and mega alliances are among the most pressing issues for the Global

Shippers’ Forum

Operator profile22 Hyundai Merchant Marine says it needs to restructure debt and vessel

charter fees in order to avoid bankruptcy

Regional analysis: Asia24 The launch of ULCVs has boosted transshipment development in Asia

Pacific ports

26 The merged China Shipping and Cosco container shipping unit is likely to

become the dominant carrier in the CKYHE alliance

1st Quarter 2016volume 5 issue 1

contents

Disclaimer: Although every effort has been made to ensure that the information in this publication is correct, the Author and Publisher accept no liability to any party for any inaccuracies that may occur. Any third party material included with the publication is supplied in good faith and the Publisher accepts no liability in respect of content. All rights reserved. No part of this publication may be reproduced, reprinted or stored in any electronic medium or transmitted in any form or by any means without prior written permission of the copyright owner.

Container Shipping & Trade | 1st Quarter 2016 For more articles visit www.containerst.com

Subscribe from just £199Subscribe now and receive four issues of Container Shipping & Trade every year and get even more:• supplement: Container Shipping & Trade Industry Leaders• access the latest edition content via your digital device• access to the www.containerst.com searchable archive. Subscribe online: www.containerst.com

1st Quarter 2016volume 5 issue 1

Editor: Rebecca Moore t: +44 20 8370 7797e: [email protected]

Contributer: Gavin van Marlet: +44 20 7394 7209e: [email protected]

Portfolio Manager – Media & Event Sales: Bill Cochranet: +44 20 8370 1719e: [email protected]

Head of Sales – Asia: Kym Tan t: +65 9456 3165e: [email protected]

Senior Sales Consultant: Ed Andrews t: +44 20 8530 8322e: [email protected]

Group Production Manager: Mark Lukmanjit: +44 20 8370 7019e: [email protected]

Subscriptions: Sally Churcht: +44 20 8370 7018e: [email protected]

Chairman: John LabdonManaging Director: Steve LabdonFinance Director: Cathy LabdonOperations Director: Graham HarmanEditorial Director: Steve MatthewsExecutive Editor: Paul GuntonHead of Production: Hamish Dickie

Published by:Riviera Maritime Media LtdMitre House 66 Abbey RoadEnfield EN1 2QN UK

www.rivieramm.com

ISSN 2050-7011 (Print)ISSN 2050-7178 (Online)

©2016 Riviera Maritime Media Ltd

Front cover photo credit: DP World

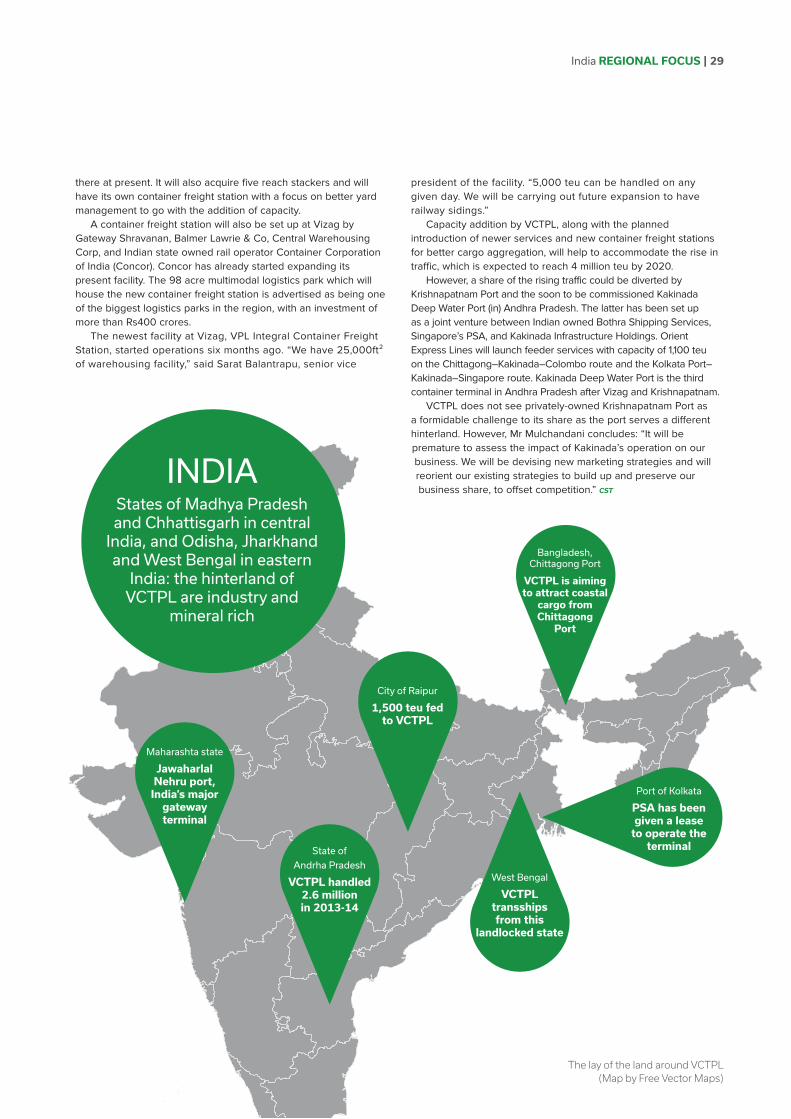

28 As the competition heats up, major initiatives are underway at India’s

Vizakha Container Terminal

Class societies 31 LNG, the next generation of ultra large container ships (ULCS) and new

software are some of the major areas being covered by class societies in the

container sector

ULCS 34 While plans are on the drawing board to create a new generation of ultra

large container vessels, ports are unlikely to be able to keep up

Ballast water treatment systems38 The countdown is on as the ballast water convention is expected to be

ratified this year, while US rules and test methods for ballast water treatment

have come under the spotlight after the USCG announced some changes

Emissions abatement41 A European feeder vessel owner has chosen the Wärtsilä hybrid scrubber for

its newbuild vessels

Fleet stats & analysis42 Feeder business is going from strength to strength, with most aspects in this

sector’s favour

Next issueMain features include:

Trade route: Transpacific

Regional analysis: Europe

Top 20 carriers

Ship operations: communications

Ship operations: reefers

Ship operations: coatings

Ship type: intra-Asia container vessels.

For more articles visit www.containerst.com Container Shipping & Trade | 1st Quarter 2016

Rebecca Moore, Editor

in the Ocean Three. If a new mega alliance is created, its after effects could lead to a further alliance reshuffle as the remaining players of the CKYHE, G6 and Ocean Three groups will be left without enough partners to offer all their services. They would be forced to create a new alliance, or alliances, in order to be able to compete.

Such an overhaul of the alliances will have shippers worried as it could have a big impact on network coverage and the services that are available.

It seems that the latest mergers will not stem the fall in rates, but it remains to be seen what impact an alliance reshuffle will have on prices. A recent Drewry Supply Chain Advisors webinar about the market reached this conclusion: “We do not expect the recent wave of industry consolidation to impact freight rates in 2016. M&A activity will not in itself impact capacity in the market and so rates. Nor is consolidation announced thus far anywhere near sufficient to reduce the very competitive nature of the market. In fact, we expect freight rates to continue to fall in 2016.”

Could the formation of COSCOCS and the acquisition of APL by CMA CGM be just the start of a wave of M&A activity within the container ship sector? There must be a good chance of this happening, with some container players currently in very weak financial situations. And key industry players believe this is the case. At the COSCOCS launch event, company chairman Xu Lirong was reported as saying that mergers were key to coping with the difficult market conditions.

The Drewry Supply Chain Advisors webinar concluded: “We expect further industry consolidation over the next few years as container shipping remains very fragmented with poor financial returns. However, recent M&A activity has been driven more by the particular circumstances of individual companies than any general trend.” CST

I t has happened. The merger of Cosco and China Shipping has taken place (see pages 26-27), creating a new super power that is likely to cause a major

alliance upheaval. And it has had a huge impact on the world’s

largest shipowners, catapulting the newly created China Cosco Shipping Corp (COSCOCS) to become the largest and highest valued shipowning group in the world, pushing former number one Maersk into second position.

COSCOCS owns a whopping 828 vessels and is worth US$21.5 billion, leaving Maersk trailing with a mere 263 owned vessels and a value of US$12.2 billion, according to VesselsValue.com. MOL has been pushed from number two to third position, with 227 vessels and a worth of US$11.6 billion. (See pages 8-9).

And according to VesselsValue.com data the new company has become the second largest container shipowner in the world in terms of fleet value, displacing MSC. (These figures only take into account vessels that are directly owned by the line and do not included those they have chartered in). Cosco owns 117 box vessels with a combined value of US$4.93 billion, while China Shipping has a box fleet of 87 vessels worth a total of US$4.17 billion. According to Alphaliner, it has a combined orderbook of 36 container ships totalling 556,000 teu, to be delivered over the next three years, bringing its total fleet to over 2 million teu by the end of 2018.

All these figures point to the arrival of a new super power in the container shipping sector that is likely to have a major impact and cause an alliance shake-up. It has been reported that COSCOCS, Evergreen, OOCL and CMA CGM are in talks to create the biggest alliance yet. The creation of such a mega group would be a major challenge to the 2M alliance.

The current alliance set up sees OOCL as part of the G6, Evergreen and Cosco as CKYHE members and CMA CGM and China Shipping

COSCOCS takes on Maersk and kickstarts alliance shake-up

COMMENT | 3

4 | BEST OF THE WEB

BEST OF THE WEB containerst.com

Log onto our new, improved website to keep track of the latest industry news

Becker Marine wins German grant for Hamburg LNG pilot project

Germany’s ministry of transport and digital infrastructure has awarded a “seven-figure” grant to Becker Marine Systems’ LNG PowerPac, billed as “the world’s first flexible solution to supplying power to container ships at ports”, for a pilot project at the Port of Hamburg.

LNG PowerPac is a unit the size of two 40ft containers that combines a gas-powered generator with a 1.5MW output and a 20ft LNG ISO tank. Once the container ship is moored, standard loading equipment at the port of call lifts the PowerPac on board. There, it provides energy to the on-board power supply during layover.

The PowerPac provides 8.2 tonnes of LNG, creating “an efficient supply of energy on board for up to 30 hours”, according to Becker Marine director LNG hybrid Max Kommorowski. However, ships spending longer in port in Hamburg can use a cascading option, installing one tank container on top of the other for each PowerPac, giving up to 60 hours’ power supply.

http://bit.ly/1TMLo4u

CMA CGM largest boxship ever to call in US

CMA CGM Benjamin Franklin – the largest vessel to ever call in the US –was inaugurated in February at the Port of Long Beach.

CMA CGM said the inauguration of the 18,000 teu and 1,300ft long vessel “symbolises CMA CGM’s faith in the American economy, as well as its ambition to be a pioneer and leader in the maritime industry in the United States.”

The CMA CGM Benjamin Franklin’s Long Beach call is part of a series of four trial-calls decided by Jacques R Saadé to prepare US ports to accommodate larger vessels.

http://bit.ly/1RTkvuv

K Line’s box sector posts loss

Japanese carrier K Line has downscaled its financial results for the fiscal year ending March 2016 on the back of the widening imbalance of supply and demand in container shipping and a decrease of demand in dry bulk business.

And the carrier has revealed that for the nine months ended December 31 2015, its container business segment registered a loss of US$34.6 million ( JPY4.2 billion) compared to an income of US$15 million for the same period in 2014. Its operating revenue fell year-on-year by 4.2 per cent. Overall cargo volumes fell by 7 per cent.

http://bit.ly/1TLfFj1

NOL trims quarterly loss

NOL Group has reported a net loss of US$77 million for the fourth quarter of 2015, a small improvement from the US$85 million loss in the same quarter in 2014. On a full year basis,

NOL posted a net profit of US$707 million, which includes a one-off US$888 million gain on the sale of APL Logistics. This is its first annual profit since 2010. Excluding the sale proceeds NOL incurred a full year net loss of US$181 million, an improvement of 30 per cent compared with 2014.

Its container line APL reported a revenue of US$1.28 billion in the final quarter of 2015, a 29 per cent contraction from the year before. Average freight rates fell 22 per cent due to pressure from overcapacity in the industry. Volume slid 12 per cent in the quarter year-on-year. In response to weak global demand, APL maintained prudent management of its deployed capacity, while keeping its headhaul asset utilisation rate at 90 per cent.

NOL said its acquisition by CMA CGM is still on track to obtain the necessary anti-trust clearances by mid 2016.

http://bit.ly/1XVtQlT

Maersk Line’s 2015 profit plunges after ‘significant’ decline in freight rates

Maersk Group has seen its 2015 profit slashed compared to 2014 on the back of a widening supply-demand gap across most of its businesses in the second half of the year that led to “significant” freight rate and oil price reductions.

Drilling down into the results, Maersk Line’s profit of US$1.3 billion signified a slump of 56 per cent compared to 2014 (US$2.3 billion) and its ROIC of 6.5 per cent fell compared to 11.6 per cent in 2014. The underlying profit declined to US$1.3 billion (US$2.2 billion). A statement said that this was “due to poor market conditions leading to significantly lower freight rates, in particular in the second half of the year, only partially offset by lower bunker prices, US$ appreciation and cost efficiencies”.

http://bit.ly/1TgnMF9

Container Shipping & Trade’s website covers the latest technology and market developments within the containership sector. Our news coverage is now exclusively online and free to read. Here are some of the most popular stories covered over the last few months

Container Shipping & Trade | 1st Quarter 2016 For more articles visit www.containerst.com

The Future is ClearME-GI dual fuel done right

MAN B&W MC/MC-C Engines MAN B&W ME/ME-C/ME-B Engines MAN B&W ME-GI/ME-C-GI/ME-B-GI Engines

The new ME-GI generation of MAN B&W two-stroke dual fuel ‘gas injection’ engines are characterised by clean and efficient gas combustion control with no gas slip. The fuel flexibility and the inherent reliability of the two-stroke design ensure good longterm operational economy. Find out more at www.mandieselturbo.com

6 | MARKET UPDATES

Freight rates set to stay in the doldrumsFreight rates reached historical lows last year and this trend looks set to continue in 2016, driven by overcapacity and weak demand

The erosion and volatility of freight rates that was seen last year is set to continue in 2016, with an increase

in the idling of ships and the continued cascading of vessels, according to Drewry Shipping Consultants.

In Drewry Webinar on Container Freight Rates & Shipping Market Outlook Philip Damas, director of Drewry Supply Chain Advisers, highlighted how there had been a substantial erosion in global spot rates, which reached record lows last year. They slumped to US$1,200 per teu, with rates

as much as 40 per cent down year on year in December. He added: “There was a slight increase in January because of the Chinese New Year on 8 February, so there has been a surge of cargo ahead of this. But we believe that this increase is likely to be short-lived.”

Singling out the recent container freight spot rate trends on the east–west trades, he said: “There has been a clear downwards trend for both the Asia–Europe and Asia–US trades over the past three years and significant reductions were reached last year, with historical lows and substantial volatility.” He said that while last year and in January 2016 there were some notable general rate increases, these had “eroded over time” due to strong competition and overcapacity.

Mr Damas homed in on the intra Asia trade which has been badly affected by overcapacity: “Rates were relatively stable

after 2013 but this situation has now changed and since 2014 there has been a very substantial reduction. Rates are historically low, down 20 per cent year on year with the introduction of 25 additional intra Asia services last year.”

Emerging market trade lanes elsewhere have also suffered. Dewry’s China–Brazil freight rate benchmark shows “the most dramatic erosion of rates.” It crashed by 74 per cent in December 2015 year on year, collapsing to US$500 per 40ft. Mr Damas commented: “It is a really incredible erosion of rates, due to low load factors. Rates remain weak in the short term. I do not think they are sustainable – US$500 does not anywhere near cover the costs of shipping lines, so there may be an upwards correction.” He pointed out that carriers had previously tried to implement increases but that they had not managed to make them work.

Meanwhile, the contract freight rate market has also suffered high volatility, with a decline of 14 per cent between February and November last year according to Drewry’s contract freight rate benchmark, and a 5 per cent fall between August and November.

Global supply and demand have also been imbalanced and the oversupply of capacity against demand is set to continue. Drewry’s Container Shipping Outlook, based on its quarterly Container Forecaster, shows how the situation worsened between 2014 and 2015, with growth in demand falling from 5.3 per cent to 1.3 per cent last year. Demand is expected to strengthen a little this year with a forecast growth of 2.4 per cent. Drewry Shipping Consultants head of container research Neil Dekker explained just how dire last year’s forecast demand growth was. “That is the lowest annual volume growth in our data, apart from 2009, since we started in the 1970s.” He said that a key reason was the Asia–Europe headhaul decline in demand of 4.5 per cent, with Hong Kong registering a decline of 8-9 per cent in volumes.

In contrast to the slow growth of volumes, supply soared last year. The global fleet experienced a spurt in growth

800,000

700,000+5.3% +1.3% +2.4%

600,000

500,000

2012 2013 2014 2015F 2016F

400,000

300,000

200,000

100,000

0

Glo

bal

Dem

and

(0

00

’s t

eu)

Oceania

Africa

Latin America

Middle East & South

Asia

Europe

Container Shipping Market OutlookGlobal Demand Development

North America

Source: Drewry’s Container Forecaster (www.drewry.co.uk/publishing)

Container Shipping & Trade | 1st Quarter 2016 For more articles visit www.containerst.com

MARKET UPDATES | 7

of 8.5 per cent, with 1.2 million teu being delivered – including 40 ships with nominal capacity of 14,000 teu and over, nearly all of which were phased into the Asia–Europe trade. “Liners are having a torrid time matching supply with demand,” commented Mr Dekker. “In 2016 fleet growth will be just under 5 per cent. Looking at this simplistically, some might think that it will be possible to match this to demand, given a bit of an uptake on the demand side. But you have to look at this on a trade route level and the delivery of more and more bigger ships, most of which are going to Asia–Europe and pushing smaller ships out to Asia–Middle East and the transpacific. We see more and more vessels of 10,000-14,000 teu rolling into the transpacific as part of this cascade. Also, more 8,000-10,000 teu ships are coming into north–south routes. We have seen some awful rates in 2015 in some of these routes.

“Although demand is looking a bit better, we do not see a better picture for freight rates. It is the same old story. Lines are challenged at every trade route level to maximise supply with demand.” Indeed, contract rates are lower in 2016. Mr Dekker said: “Anecdotally, in 2016 a number of big Asia–Europe contacts that have been signed are at significantly lower rates than in 2015.”

One positive factor is the widening of the Panama Canal in 2016. “Once that happens, lines have the opportunity to reconfigure their networks, and the

possibility of upgrading from 5,000 teu to 8,000 teu, so there will be a little bit of relief for some of these bigger ships.” But he warned: “It is very important that they do not reconfigure services by bringing in too many weekly services and too much capacity all at once. Quite clearly that will have a detrimental effect on the balance between supply and demand. The

management of the deployment of these vessels is crucial for the lines.”

In terms of idled capacity, he said that 1 million teu was laid up just before the end of December, representing 4.7 per cent of the global fleet, up from 1-2 per cent at the start of 2015. “We see that increasing in 2016, but that will only be driven when lines start to lose more cash,” Mr Dekker commented.

One asset for carriers in the difficult global market has been their ability to reduce their costs, through activities such as slow steaming. Furthermore, the decrease in fuel prices has been very beneficial. “Without that gift in 2015, many people would say than the lines would not have made much profit at all,” Mr Dekker commented. “They have reduced costs at a steeper angle than the drop in overall freight rates. However, in 2016, our view is that the lines’ ability to reduce costs steeper than freight rates may be compromised.”

Reasons include the additional costs of empty repositioning back to Asia, and the potential growth of idling vessels. If a 10,000 teu ship is laid up for more than three months in Asia, reactivation costs alone are around US$500,000, Mr Dekker said, adding: “This will be a very big issue for them as we progress in 2016 and will impact on their overall profitability.” He warned: “The lower rates forecast and potential higher costs mean there may be a point in 2016 when lines start running out of cash and the number of idled ships increases.” CST

$0

$500

$1,000

$1,500

$2,000

$2,500

$3,000

Jan-13 Apr-13 Jul-13 Oct-13 Apr-14 Jul-14 Oct-14Jan-14 Apr-15 Jul-15 Oct-15Jan-15

US

$ p

er 4

0ft

Co

nta

iner

Shanghai – Rotterdam Hong Kong – Los Angeles

Recent Spot Container Freight Rate TrendsEurope & US Imports from Asia (US$ per 40ft)

Marketshare rate wars

Capacity & GRI initiatives

Marketshare rate wars

$1,400

$1,200

$1,000

$800

$600

$400

$200

2012 2013 2014 2015 2016

$0

112

110

108

106

104

102

100

98

96

US

$ p

er t

eu

Eas

t‐W

est

Su

pp

ly/D

eman

d In

dex

Weighted East-West Freight Rate incl Fuel East-West Supply/Demand Index

Freight Rate Forecast: East-West TradesSupply-Demand Vs Freight Rates

Source: Drewry’s Container Freight Rate Insight (www.drewry.co.uk/cfri) & World Container Index (www.worldcontainerindex.com)

Source: Drewry’s Container Forecaster (www.drewry.co.uk/publishing)

For more articles visit www.containerst.com Container Shipping & Trade | 1st Quarter 2016

8 | DATA ANALYSIS

Swings and roundaboutsThis year will see non-operating owners take the lion’s share of new container ship deliveries, while in 2017 carriers will return with a vengeance, writes Gavin van Marle

T he round of merger and acquisition activity that has kicked off in the container shipping industry will have a major effect on the league table of the world’s largest box ship

owners, with Chinese conglomerates becoming increasingly important players.

According to VesselsValue.com data compiled exclusively for Container Shipping & Trade, the merger between China’s two state-owned carriers, China Shipping Container Lines Co (CSCL) and China Ocean Shipping (Group) Co (Cosco), will see the resulting company become the second largest container shipowner in the world in terms of fleet value, displacing Mediterranean Shipping Co (MSC).

It should be noted that the figures quoted here only take into account vessels that are directly owned by the line and do not include those that it has chartered in – hence the inclusion of several large non-operating owners.

Under the terms of the merger Cosco – currently the third largest container shipowner, with 117 box vessels with a combined value of US$4.93 billion – will take over the container operations, while CSCL,

whose box fleet of 87 vessels is worth a total of US$4.17 billion, will manage the wet bulk and ship financing activities. Together, the two carriers will have a fleet worth US$9.1 billion, comprising 203 vessels.

And as long as CMA CGM’s take-over of APL is completed this year as expected, the French carrier, too, will leapfrog MSC with a combined fleet of 152 vessels with a total value of US$7.67 billion. Although it is one of the smaller container ship operators, APL also has the lowest ratio of chartered-in vessels of any of the top 20 carriers.

In terms of capacity that is actually operated, the two leading carriers have long been Maersk Line and MSC, in that order, with the last few years seeing MSC steadily close the gap on its Danish rival. An order last year for 20 second generation ultra large container vessels (ULCVs) worth US$2.2 billion will see Maersk push forward once more, although there are a number of units being delivered to non-operating owners in 2016 and 2017 that are likely to find employment in MSC’s fleet. So it may be that, for a time, the Geneva-headquartered line becomes the largest in terms of capacity operated.

TOP 20 LINES BY VALUE BEFORE MERGERSCOMPANY NO. TEU VALUE $M

Moller Maersk AS 262 2,021,375 12,393

MSC 197 1,229,915 5,767

COSCO 117 826,833 4,932

CMA CGM 97 757,851 4,699

Seaspan Corporation 96 696,648 4,467

Shoei Kisen 64 563,045 4,222

China Shipping Container Lines

86 696,307 4,172

Hapag Lloyd 76 577,155 3,716

Evergreen Marine Corp 111 549,716 3,542

OOCL 61 541,535 3,463

UASC 44 494,328 3,402

PIL 123 459,397 3,229

APL 55 461,994 2,979

Zodiac Maritime 52 394,311 2,759

NYK Line 66 445,916 2,685

Costamare 71 462,842 2,623

Hamburg Sud 48 322,802 2,586

Bank of Communications 23 275,577 2,346

Offen Claus-Peter 58 406,123 2,116

Eastern Pacific Shipping 36 315,401 1,978

TOP 20 LINES BY VALUE AFTER MERGERSCOMPANY NO. TEU VALUE $M

Moller Maersk AS 262 2,021,375 12,393

COSCO & CSCL 203 1,523,140 9,104

CMA CGM + APL 152 1,219,845 7,678

MSC 197 1,229,915 5,767

Seaspan Corporation 96 696,648 4,467

Shoei Kisen 64 563,045 4,222

Hapag Lloyd 76 577,155 3,716

Evergreen Marine Corp 111 549,716 3,542

OOCL 61 541,535 3,463

UASC 44 494,328 3,402

PIL 123 459,397 3,229

Zodiac Maritime 52 394,311 2,759

NYK Line 66 445,916 2,685

Costamare 71 462,842 2,623

Hamburg Sud 48 322,802 2,586

Bank of Communications 23 275,577 2,346

Offen Claus-Peter 58 406,123 2,116

Eastern Pacific Shipping 36 315,401 1,978

Grand China Intermodal 22 239,532 1,953

Yang Ming Marine Transport 52 294,572 1,914

UNMERGED MERGED

Container Shipping & Trade | 1st Quarter 2016 For more articles visit www.containerst.com

*All data provided by VesselsValue.com

The VesselsValue.com data reveals two important indicators, assuming a general two-year lead time between ordering and delivery of a vessel. Firstly – and with the benefit of hindsight – the downturn in the market that was principally caused by overcapacity began in 2014, notwithstanding a surprisingly strong peak season on the Asia-Europe trade. This suggests that carriers had begun to rein in their ordering activity in the early part of the year before being misled by the peak season which suggested a sustained recovery. The only line that placed significant orders during this period was United Arab Shipping Co (UASC), and that came as part of a complete strategic overhaul of the company.

Throughout this period new ship prices have been in a deflationary spiral. Shipyards face the same structural issues that their customers face – there is too much shipbuilding capacity, and demand is flat. Over the last few years those most likely to place orders have been opportunistic cash buyers such as the Greek-owned firms which were able to negotiate rock-bottom prices.

It comes as little surprise that there are three Greek owners in the top 10 firms that are taking deliveries this year. Combined, the top 10 shipowners expect to receive US$7.5 billion worth of assets this year, and the three Greek firms of Costamare, Zodiac Maritime and Capital Maritime & Trading Corp account for a quarter of that.

Of course, the other notable presence in that table are the Chinese shipowners that have effectively subsidised the country’s shipyards, that could otherwise be staring down the barrel of bankruptcy. The series of orders placed by China’s Bank of Communications, which is now one of the fastest growing shipowners in the world, SinOceanic Shipping and Grand China Intermodal mean that Chinese owners will take 36 per cent of the value of the top ten.

It is ironic that at a time when carriers have come to rely increasingly on the spot market for their earnings, they have been willing to sign such long-term charter deals. Although spot rates do not determine contract rates, they do influence them in that they provide a form of benchmark. And as spot rates have hit new lows at a time when annual contracts are being negotiated, there has been a commensurately growing reluctance on the part of carriers to commit to long-term contract rates that offer such poor terms. Nonetheless, these deals are being done.

The growth of Seaspan is testament to that. The Hong Kong-headquartered shipowner, listed on the New York and Toronto stock exchanges, is currently the fifth largest shipowner in the world in terms of fleet value and will remain in that place, even after the Cosco-CSCL merger and CMA CGM’s acquisition of APL’s

owner Neptune Orient Lines are completed.The contrast that 2017 will bring could hardly be greater.

Deliveries next year are almost completely dominated by container carriers, with just two non-operating owners – Seaspan and Minsheng Financial Leasing Co – in the top ten. Their share will be just 10 vessels out of a total of 74, and only 12.4 per cent of the combined value of US$9.3 billion of the top in 2017.

For those in the carriers’ trade development departments, 2017 has the potential to be a grim year. The large number of ULCVs due to come on stream could be ruinous, particularly if there is no sustained global economic recovery this year, of which early evidence is scant. With 35 ULCVs due to be delivered in 2016, and a further 55 in 2017, representing a combined capacity of 1.5 million teu, it is little wonder that some analysts are predicting a bloodbath. Carriers do, however, have some time in which to prepare, and it would not be surprising if there was a combination of delayed deliveries, increased scrapping of older units and the return of the sight of large numbers of ships at anchor in cold lay-up.

An aside to this is the return of Islamic Republic of Iran Shipping Lines (IRISL), which has reportedly arranged US$5 billion in loans from Chinese lenders and is preparing an order for a series of 14,000 teu vessels, since US, EU and UN sanctions on its home country were lifted in mid January.

The return of carriers to the ordering scene in 2017 also explains the changes in ordering activity by flag state in that year, compared with 2016.

Nonetheless, the amount of capacity coming into the market simply does not match the capacity that needs to leave it. Last year saw a total of 176,384 teu sent to recycling yards. To some extent, the lack of tonnage being sent for scrap has to do with factors beyond the control of the shipping industry. Some two-thirds of Chinese steel producers are said to be operating at a loss and the price of steel is also in the doldrums. This means that some owners who might otherwise have been tempted to find cash buyers for their vessels prefer to hold on to assets in the hope of a better return down the line. Although this tactic contributes to the overall global fleet capacity figures, the vessels themselves are likely to be idling.

Despite the Panama Canal expansion project finding its schedule altered once more – the project is now expected to be completed in the second quarter of this year, although given its past history it could easily slip – it is likely that most scrapping activity in 2016 will resemble that of last year, with the majority being the old Panamax size. CST

TOP 10 CONTAINER LINES WITH CONTAINER DELIVERIES IN 2016 VS 20172016 2017

COMPANY NO. TEU VALUE $M COMPANY NO. TEU VALUE $M

Bank of Communications 14 160,212 1,381 Moller Maersk AS 20 261,780 2,220

UASC 8 127,491 1,068 COSCON 11 203,000 1,609

Costamare 9 114,000 971 OOCL 6 126,600 1,067

Eastern Pacific Shipping 5 96,000 798 CMA CGM 7 104,600 873

SinOceanic Shipping 10 88,000 719 MSC 6 82,400 719

Zodiac Maritime 7 76,000 710 MOL 4 80,600 680

Grand China Intermodal 6 72,000 617 Seaspan Corporation 7 73,000 667

Shoei Kisen 5 70,000 578 Evergreen Marine Corp 10 63,300 544

NYK Line 3 42,000 347 Minsheng Financial Leasing 3 57,600 486

Capital Maritime and Trading 4 37,176 334 NYK Line 4 56,000 472

For more articles visit www.containerst.com Container Shipping & Trade | 1st Quarter 2016

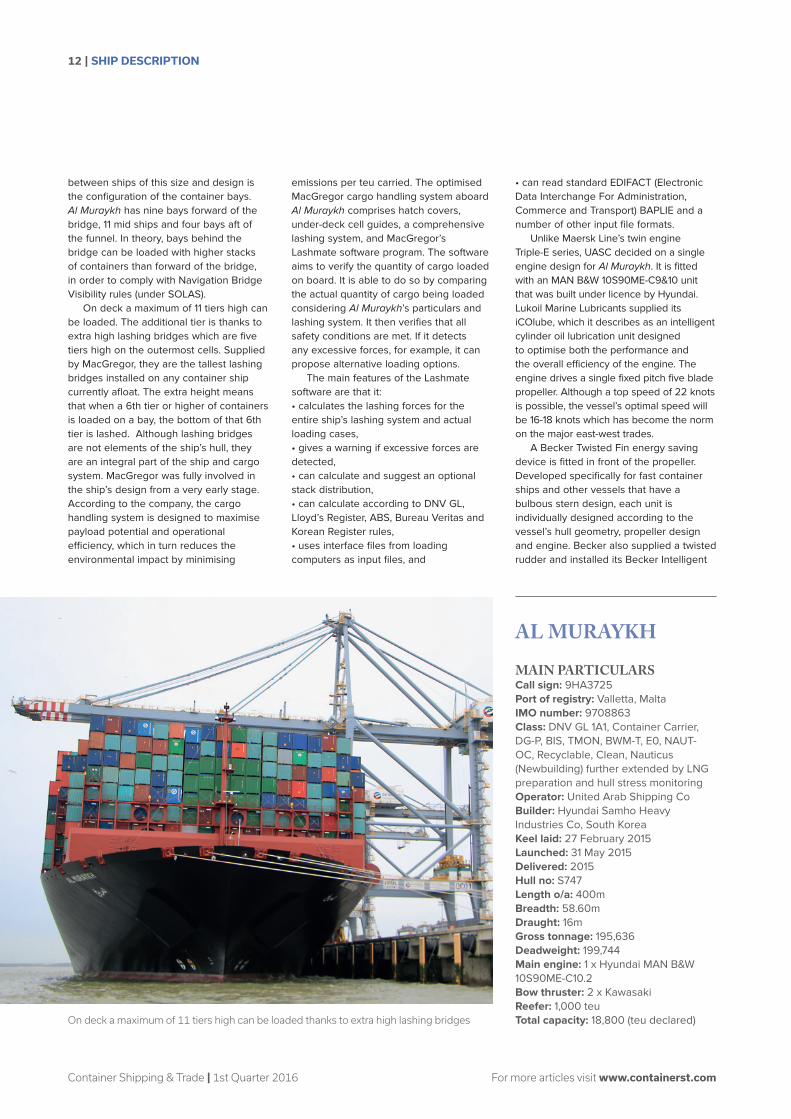

SHIP DESCRIPTION | 11

Enter UASC’s latest LNG ready giant

T hroughout the history of the container industry, shipping lines have looked to increase

their market share in two different ways. The first is by the acquisition of smaller companies. Shipping lines such as Maersk Line and CMA CGM have done this on a regular basis, most notably in recent years. The second option is to grow organically, as has Mediterranean Shipping Co (MSC).

Another shipping line that has taken the organic approach to growth in recent years is Kuwait based United Arab Shipping Co (UASC). The relatively young company was established in July 1976 by a joint shareholding comprising six Arab states – Bahrain, Iraq, Kuwait, Qatar, Saudi Arabia and the United Arab Emirates. Officially the line has its headquarters in the city of Safat, Kuwait, but since the early 1990s its commercial and operations centre has been based in vibrant Dubai.

Over the last few years it has been actively growing its presence in the global container trades. It has achieved this through a number of vessel sharing agreements with other lines, most recently becoming a founding member of the Ocean Three alliance together with China Shipping Container Lines (CSCL) and CMA CGM.

In August 2013, as part of its ambitious growth strategy, it placed an order for

17 ultra large container vessels (ULCVs). A number of shipyards tendered for the huge order, but the world’s number one shipbuilder, South Korea’s Hyundai Heavy Industries (HHI) was the successful bidder.

The landmark deal, which was the largest in UASC’s history, comprised five 15,000 teu A15 class vessels to be built at HHI’s Ulsan shipyard and five 18,800 teu A19* class vessels to be built by the Hyundai Samho Heavy Industries yard in Mokpo. The order also had options for an additional one A19 and six A15 vessels, all of which were exercised early the following year. Together with the options the total value of the order was US$2.5 billion, with all vessels being classed by DNV GL. The first A19 vessel Barzan was delivered in April 2015, followed by the second, Al Muraykh, in August.

It has become abundantly clear that only the most fuel efficient vessels will survive into the future, and fuel economy was a major consideration for UASC during the design process for the A19 class. Since 1997 the line has worked

closely with Hamburg based consultant and ship designer Technolog Services on the optimisation of its newbuildings. The size and capacity of its new ships have grown steadily from the initial Panamax class of 10 A4 (4,100 teu) ships launched in 1998, and the eight A7 class (7,200 teu) vessels launched in 1998, to the nine A13 class (13,500 teu) ships launched in 2010, and now the latest A15 and A19 classes.

Al Muraykh, along with the other A19 class ships, is heralded as the world’s most environmentally friendly vessel. Its design has been optimised to ensure the highest possible efficiency without compromising container capacity. It is one of the first container ships to have an overall length of 400m, its draught of 16m allows for up to 10 tiers of containers to be loaded below deck, and a breadth of 58.6m equates to 23 rows of containers wide.

As with all ships in this size bracket, Al Muraykh has the now familiar split superstructure design which maximises container intake without increasing overall dimensions. One of the main differences

UNITED ARAB SHIPPING CO HAS DEPLOYED ITS SECOND 18,800 TEU LNG READY BOX SHIP AL MURAYKH

by Andrew McAlpine

UASC is one of the first vessel owners to plan its newbuilds for LNG retrofitting

For more articles visit www.containerst.com Container Shipping & Trade | 1st Quarter 2016

12 | SHIP DESCRIPTION

between ships of this size and design is the configuration of the container bays. Al Muraykh has nine bays forward of the bridge, 11 mid ships and four bays aft of the funnel. In theory, bays behind the bridge can be loaded with higher stacks of containers than forward of the bridge, in order to comply with Navigation Bridge Visibility rules (under SOLAS).

On deck a maximum of 11 tiers high can be loaded. The additional tier is thanks to extra high lashing bridges which are five tiers high on the outermost cells. Supplied by MacGregor, they are the tallest lashing bridges installed on any container ship currently afloat. The extra height means that when a 6th tier or higher of containers is loaded on a bay, the bottom of that 6th tier is lashed. Although lashing bridges are not elements of the ship’s hull, they are an integral part of the ship and cargo system. MacGregor was fully involved in the ship’s design from a very early stage. According to the company, the cargo handling system is designed to maximise payload potential and operational efficiency, which in turn reduces the environmental impact by minimising

emissions per teu carried. The optimised MacGregor cargo handling system aboard Al Muraykh comprises hatch covers, under-deck cell guides, a comprehensive lashing system, and MacGregor’s Lashmate software program. The software aims to verify the quantity of cargo loaded on board. It is able to do so by comparing the actual quantity of cargo being loaded considering Al Muraykh’s particulars and lashing system. It then verifies that all safety conditions are met. If it detects any excessive forces, for example, it can propose alternative loading options.

The main features of the Lashmate software are that it: • calculates the lashing forces for the entire ship’s lashing system and actual loading cases,• gives a warning if excessive forces are detected,• can calculate and suggest an optional stack distribution,• can calculate according to DNV GL, Lloyd’s Register, ABS, Bureau Veritas and Korean Register rules,• uses interface files from loading computers as input files, and

• can read standard EDIFACT (Electronic Data Interchange For Administration, Commerce and Transport) BAPLIE and a number of other input file formats.

Unlike Maersk Line’s twin engine Triple-E series, UASC decided on a single engine design for Al Muraykh. It is fitted with an MAN B&W 10S90ME-C9&10 unit that was built under licence by Hyundai. Lukoil Marine Lubricants supplied its iCOlube, which it describes as an intelligent cylinder oil lubrication unit designed to optimise both the performance and the overall efficiency of the engine. The engine drives a single fixed pitch five blade propeller. Although a top speed of 22 knots is possible, the vessel’s optimal speed will be 16-18 knots which has become the norm on the major east-west trades.

A Becker Twisted Fin energy saving device is fitted in front of the propeller. Developed specifically for fast container ships and other vessels that have a bulbous stern design, each unit is individually designed according to the vessel’s hull geometry, propeller design and engine. Becker also supplied a twisted rudder and installed its Becker Intelligent

AL MURAYKH

MAIN PARTICULARSCall sign: 9HA3725Port of registry: Valletta, MaltaIMO number: 9708863Class: DNV GL 1A1, Container Carrier, DG-P, BIS, TMON, BWM-T, E0, NAUT-OC, Recyclable, Clean, Nauticus (Newbuilding) further extended by LNG preparation and hull stress monitoring Operator: United Arab Shipping CoBuilder: Hyundai Samho Heavy Industries Co, South Korea Keel laid: 27 February 2015Launched: 31 May 2015Delivered: 2015Hull no: S747Length o/a: 400mBreadth: 58.60mDraught: 16mGross tonnage: 195,636Deadweight: 199,744Main engine: 1 x Hyundai MAN B&W 10S90ME-C10.2Bow thruster: 2 x Kawasaki Reefer: 1,000 teu Total capacity: 18,800 (teu declared)On deck a maximum of 11 tiers high can be loaded thanks to extra high lashing bridges

Container Shipping & Trade | 1st Quarter 2016 For more articles visit www.containerst.com

SHIP DESCRIPTION | 13

Monitoring System (BIMS) for rudder force measurement, and HP Super, its lubrication free carrier bearing material.

Fuel savings of up to 3 per cent are expected, as well as a reduction in NOx and CO2 emissions. Preliminary calculations indicate that Al Muraykh’s Energy Efficiency Design Index (EEDI) value is close to 50 per cent below the 2025 limit set by IMO.

Gas ready and future proofFrom the very start of the development process Al Muraykh and the other vessels in the A19 series have been optimised for economy and the lowest possible fuel consumption, which in turn will lead to lower emissions. Through all the stages of their development, UASC, Technolog Services and HHI, as well as the other main suppliers, have been involved in the optimisation of the vessels. This includes an optimised hullform, and a ship-to-shore power supply solution for zero emissions at berth.

What sets these vessels apart from other ULCVs is that they are gas ready and could at some future date be retrofitted in order to run on liquefied natural gas (LNG). At an early stage UASC decided that LNG would be the preferred option, rather than investing in scrubbers and selective catalytic reduction (SCR) technology. The company is among the first vessel owners in the world to plan its newbuildings for LNG retrofitting and is the largest container line to do so. This decision has made it the potential market leader for LNG as a ship fuel because of the size of the vessels that could now be run on it.

Al Muraykh and the other ships in its class are the first vessels to receive DNV GL’s Gas Ready notation. The shipping industry considers LNG to be one of the most important alternative fuels because of its potential to help reduce shipping’s impact on the environment. Any vessel operating on LNG will greatly reduce its NOx, SOx and particulate emissions and it will also help to reduce CO2 emissions. LNG is not, however, a commercially viable alternative at present, and it will not be viable until it can be offered below the current price for heavy fuel oil (HFO). At present for certain ship types LNG can be as much as 30 per cent more expensive.

According to DNV GL, LNG is likely to be the most commercially attractive fuel option from 2020 when the price of low sulphur HFO and marine gas oil (MGO) is expected to be higher, and given the long-

term availability of natural gas.LNG as a fuel has characteristics that

have an impact on a ship’s design. Notably, it has half the density of diesel fuel, so larger storage tanks are required for the same cruising range. As LNG is not stored at high pressure the tanks can be positioned below deck. This is unlike compressed natural gas (CNG), where the tanks are at high pressure and are therefore positioned on deck – as seen in the Marlin class of new gas fuelled ships for the US carrier TOTE that were launched last year. As LNG is a liquid only at cryogenic temperatures (-163°C) it requires special storage tanks, pipe systems and handling as it will slowly evaporate when stored. Additional systems are required in order to deal with the boil off gas, as venting to air is not allowed.

Al Muraykh has been designed for future conversion to LNG via retrofitting. During the design process it became obvious that the most suitable location to install the tanks would be in the cargo hold directly in front of the engineroom, as this would require shorter pipe system routes to the LNG tank. An IMO Type B tank will have the greatest stowage density, compared to a smaller cylindrical Type C tank. A Type B tank would also be adjustable to Al Muraykh’s hull shape, ensuring that fewer container slots are lost.

The LNG plant design has been approved in principle and was obtained from DNV GL, with technical co-operation between UASC’s newbuilding team, HHI, Hyundai’s Engine & Machinery Division, and Japan Marine United Corp for the SPB (self-supporting prismatic shape Type B) LNG tank.

Al Muraykh is deployed on UASC Asia Europe Container Service 1 (AEC1) that it operates with its Ocean Three alliance partners. The service has the port rotation Qingdao–Shanghai–Ningbo–Yantian–Xiamen–Port Kelang–Felixstowe–Hamburg–Rotterdam–Zeebrugge.

On 16 December 2015 it sailed from Port Kelang bound for Felixstowe carrying a record 18,601 teu which to date is the largest number of containers carried on board any vessel at any one time. It was diverted to London Gateway and arrived on 1 January 2016. CST

*Initially UASC stated that Al Muraykh and its sisters were the A18 class, but this has recently changed to A19. In order to be up to date this article lists them as the A19 class.

July 1976UASC was established

Ocean Three alliance

UASC is a member

US$2.5 billion

The amount UASC’s shipbuilding contract for 17 ships is worth

17 ULCSsComprises 5 x 15,000 teu and 5 x 18,800 teu ships, with options for one more 18,800 teu and six more 15,000 ships (exercised)

BarzanFirst 18,800 teu ship delivered April 2015;

Al Muraykh is the second

For more articles visit www.containerst.com Container Shipping & Trade | 1st Quarter 2016

14 | TRADE ROUTE transatlantic

Overcapacity sends dark cloud over transatlantic stabilityThe traditionally balanced transatlantic trade has tipped as a result of the cascading of larger vessels into this market

Andrew Abbott (Atlantic Container Line): “It is ridiculous for so many lines to want to carry boxes at an outright loss”

NORTH AMERICA TO EUROPE - TEU

2014 2015Q1

691,200Q1

631,200

Q2732,000

Q2685,800

Q3669,000

Q3649,400

DE

CR

EA

SE

transatlantic TRADE ROUTE | 15

The traditionally stable transatlantic trade has lost some of its balance as a result of the cascading of larger vessels into its trade lanes last year, forcing rates down and creating overcapacity.

Atlantic Container Line (ACL) president and chief executive Andrew Abbott highlights the destabilising effect that the cascading of larger ships into the trade has had. “The Atlantic trade in January last year was perfectly balanced. It had perfect supply and demand and rates were stable. Then the big shipping lines decided to cascade bigger ships in from Asia. They added 30 per cent of capacity to the trade and basically destroyed it overnight. When rates went into free fall last summer, the big alliances pulled out half the added capacity in November. I am not sure if they are going to bring some of it back or not.”

He bemoans the situation. “The market was great, then it got terrible, and right now it is stable, but at a much lower level than it should be. I am seeing freight rate prices in the eastbound direction that are below handling cost. It is ridiculous for so many lines to want to carry boxes at an outright loss.”

ACL has been sheltered from the worst of the impact because it tends not to do business with high volume customers – the area where the rates have fallen the most.

Looking ahead, Mr Abbott comments: “While the trade has stabilised a bit, if you look at the worldwide picture Europe shows no major signs of resurgence. The US economy is ticking along ok, but it cannot survive in a vacuum, and unless Europe and Asia pick up, the US will eventually slow down again. The picture right now does not look rosy at all, and the shipping lines that have the biggest capacity will suffer the most.”

Vessels in the transatlantic trade are generally around 3,000-5,000 teu, but larger ships of 7,000-8,000 teu have been phased in from Asia. Mr Abbott says: “All it has done is mess up the supply and demand balance. People are building more mega-ships for Asia so the cascading will continue. We can survive because we are small enough to be selective about our cargo. We are much more diversified, carrying containers, cars and roro, and we have a very low cost operation. But I am afraid that most lines will see their balance sheets go into the red this year.”

He adds: “Logic says that the global operators will not want to lose money in every trade after doing so in Asia, so I do not think Atlantic rates will go much lower. But with worldwide overcapacity continuing, we will not see any profitability rebounds in the short or

medium-term,” he adds. Shipping lines pulled capacity out of the market and this helped

to halt the falling rates. Indeed, as Drewry Maritime Research’s Container Insight Weekly said; “A combination of suspended services and void sailings from November has seen carriers reverse some of the unwarranted second quarter capacity injections.” It said that the monthly slot availability for January 2016 was just five per cent above the same month in 2015 for the westbound leg, and down by one per cent for the eastbound leg. Previously, the annual comparisons had been in the high double-digit range.

But the concern is what will happen when services are resumed, such as the suspended G6 Alliance AX4 and the 2M TA4/NEUATL4 loops which are expected to be relaunched in late April. Drewry points out that this could potentially bring the total available slots back to the same leve as Q3 last year.

It summed up: “We expect spot rates in the transatlantic to continue their gradual erosion, which might get steeper if too much capacity is returned after the seasonal suspensions.”

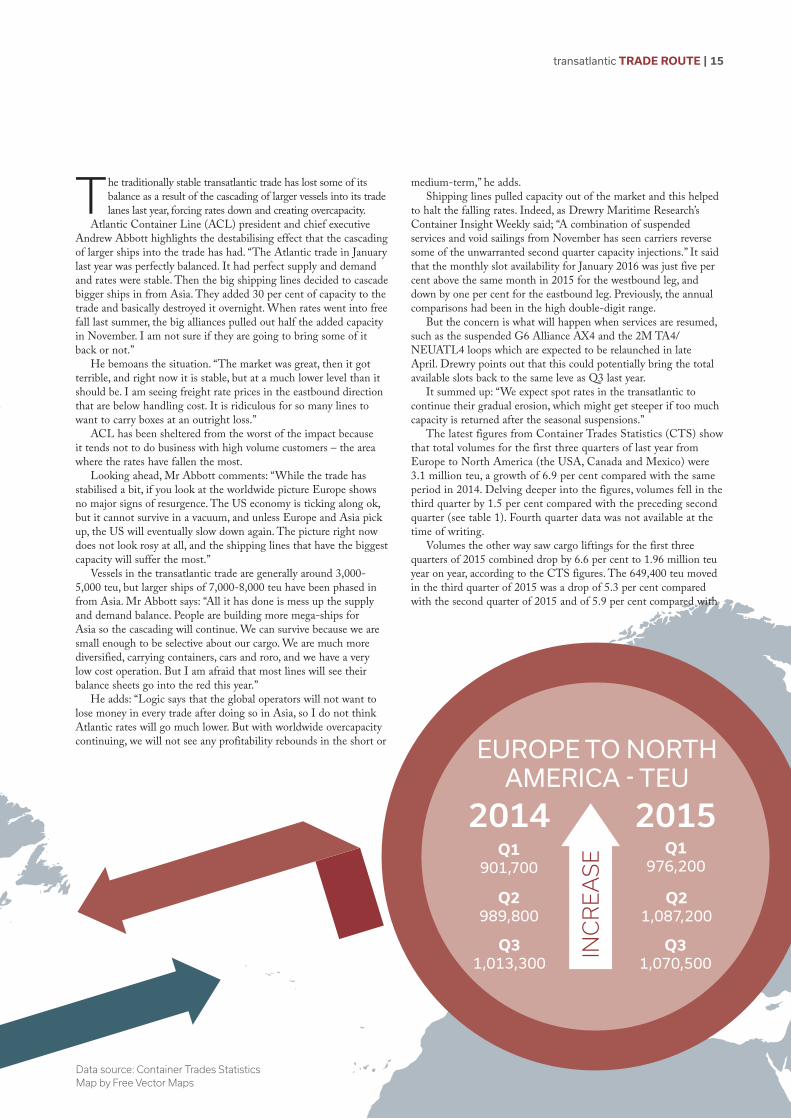

The latest figures from Container Trades Statistics (CTS) show that total volumes for the first three quarters of last year from Europe to North America (the USA, Canada and Mexico) were 3.1 million teu, a growth of 6.9 per cent compared with the same period in 2014. Delving deeper into the figures, volumes fell in the third quarter by 1.5 per cent compared with the preceding second quarter (see table 1). Fourth quarter data was not available at the time of writing.

Volumes the other way saw cargo liftings for the first three quarters of 2015 combined drop by 6.6 per cent to 1.96 million teu year on year, according to the CTS figures. The 649,400 teu moved in the third quarter of 2015 was a drop of 5.3 per cent compared with the second quarter of 2015 and of 5.9 per cent compared with

EUROPE TO NORTH AMERICA - TEU

2014 2015Q1

901,700Q1

976,200

Q2989,800

Q21,087,200

Q31,013,300

Q31,070,500

INC

RE

AS

E

Data source: Container Trades StatisticsMap by Free Vector Maps

the third quarter in 2014. CTS’s Tier 1 aggregated price index, which has a baseline of

100 points, shows that Europe to North America trade ended 2015 with a figure of 92 for December. This was weaker than the months from June onwards. In June it reached 96, rising to 97 in July before going back to 96 in August and achieving levels of 93, 95 and 95 for September, October and November respectively. The North America to Europe Tier 1 aggregated price index for North America to Europe was much lower, slumping to 78 points in December. After starting the year at 90 points in January, and climbing to 92 in April, the points trailed off, going down to 84 in September and October, then falling again to 80 in November.

The double-whammy of over capacity and the weaker European economy explains the decrease in some of the volumes and in the price index. Dean Davison, principal consultant at Ocean Shipping Consultants, part of Royal HaskoningDHV, comments: “The transatlantic is currently a tale of two trades. The eastbound route is weaker, impacted by the state of some of the key European economies affecting demand. By way of comparison, the westbound is healthier and stronger, which reflects the current economic position in the USA. I expect 2016 will be more of the same, with these overall trends likely to continue.”

And while he singled out the challenges presented by cascading, he believes that the transatlantic is still stable compared with other

trades. “There will also be a continuation of other noted industry factors. Ship cascading will continue, and there will be some over capacity, as there is in all trades. As a result, the freight rates are likely to be impacted. However, it is still a stable trade, especially in comparison with other major routes which are clearly much more unstable. So I expect the transatlantic will continue to be a route that the major liner companies remain interested in serving.”

Atlantic Star debutsAtlantic Container Line’s (ACL’s) innovative new conro ship Atlantic Star made a “very auspicious start,” according to its owner, when it went into service in mid December 2015. The entire ship was filled with cargo at a time which is normally quiet.

“Our customers wanted to put their cargo on a brand new ship. It was a very auspicious start,” observed ACL president and chief executive Andrew Abbott. Atlantic Star is the first ship in a series of five to enter service. The second is expected to be delivered in March and the final three will be phased in every two months afterwards. They will replace ACL’s entire five-ship fleet, which has been in operation since the mid 1980s. Since the arrival of Atlantic Star, Atlantic Companion has been sent for scrap.

The new fleet is bigger, faster, more efficient and greener than the current one. At 3,800 teu the G4 vessels have double the capacity of the older G3 ships but share the same footprint. Mr Abbott says: “On the container side we have the same general dimensions but double the capacity, which means that we are getting an extra 1,900 teu for the same price.”

But it is on the roro side that the major changes can be seen. The new ships were designed with cargo handling in mind. The roro

16 | TRADE ROUTE transatlantic

COVERING ALL COASTSProviding stevedoring & terminal operationsin more than 42 U.S. ports and 80 locations

BaltimoreBaton RougeBayonneBeaumontBostonBrunswickCamdenCharlestonConcord, CACoos BayCorpus ChristiCrockettDavisvilleFreeport

GalvestonGulfportHoustonJacksonvilleLong BeachLongviewLos AngelesMiamiNew OrleansNew YorkNewarkOlympiaPhiladelphiaPort Arthur

Port CanaveralPort EvergladesPort HuenemePortland, MEProvidenceSan DiegoSavannahSunny PointTacomaTampaVancouver, WAVirginiaWilmington, DEWilmington, NC

PortsAmerica.com

transatlantic TRADE ROUTE | 17

decks have only one set of centre columns, while the decks on the older vessels have two or three. “Those multiple columns required a lot of manoeuvring in order to park cargo, and so stowage is a lot easier on Atlantic Star. Also, the main roro decks are midships, so the ramps up and down are much shallower, making cargo handling much faster and easier. In the old G3 ships the ramps were steeper, and it was much harder to get heavy cargo up and down. With the very shallow G4 ramps, you can carry virtually everything,” explains Mr Abbott.

Furthermore, the car decks on the newbuild are much higher, at over 2m, compared with 1.6m on the older ships. “This means that we have no restrictions on high-sided sports utility vehicles and minivans, as we had on the G3s.” Since the main roro deck can accommodate cargo up to 7.45m high, the vast majority of oversized cargo can receive safe, dry stowage for its transatlantic delivery.

The new ships are leading to some service changes. First, their size means that ACL can increase its swap arrangement with Hapag-Lloyd. This co-operation has been in place since 1984, and sees the two companies swap slots of 550 teu. Hapag-Lloyd takes space on every ship, while ACL spreads its slots over a number of Hapag-Lloyd services. “We are increasing our slot swap arrangement up to around 1,000 teu, to be spread out over a wider geographical area,” says Mr Abbott.

The new ships are also likely to have an influence on the ports used by ACL. Mr Abbott indicated that the company was interested in adding a South Atlantic port to the sailing rotation, but emphasises: “We are going to wait until October to see what happens with the performance of the new ships and cargo demand in our current ports before making any changes. In order to add a South Atlantic port, we would have to drop one from our current rotation. We have to be sure that the change is for the better. We are going to think long and hard before making changes.”

Summing up the impact that the new ships will have for ACL, Mr Abbott says: “We have not grown at all since our original ships came into service in the 1980s, despite the market growing. But now we can allow ourselves to gradually grow into the market as the ships are so much more efficient. Today, we really do turn away a lot of business as we just do not have the capacity. Now it will be a different picture. We can say yes to a 300 container shipment rather than no.”

He said that the new fleet will increase ACL’s market share of the transatlantic trade from 4.5 per cent today to between 8 and 9 per cent in the future. CST

ATLANTIC STAR MAIN PARTICULARSCargo access equipment (ramps, doors, hoistable decks, cell guides): MacGregorExhaust cleaning for main engine/scrubber: Alfa LavalPrime mover, shafting, propeller and rudder arrangement: Wärtsilä, BeckerAuxiliary engines: Yanmar

18 | CUSTOMER PROFILE

GSF WARNS: STATES MUST ACT NOW ON CONTAINER WEIGHING TO AVOID SUPPLY CHAIN DISRUPTION

C ontainer weighing, market-based measures to deal with CO2 and the emergence of ocean carrier mega

alliances have kept Chris Welsh, secretary general of the Global Shippers’ Forum (GSF) very busy.

NO TIME FOR DELAYIndeed the container weighing regulations loom large as they are due to take effect globally on 1 July 2016. The amendments to the SOLAS (Safety of Life at Sea) Convention require packed shipping containers to have a verified gross mass (VGM) before they can be loaded on a ship for export. It is something that GSF

MANDATORY CONTAINER WEIGHING, MARKET-BASED MEASURES FOR CO2 EMISSIONS AND MEGA ALLIANCES ARE AMONG THE MOST PRESSING ISSUES FOR THE GLOBAL SHIPPERS’ FORUM

Ultra large container ships and mega alliances are a large focus for GSF

Container Shipping & Trade | 1st Quarter 2016 For more articles visit www.containerst.com

CUSTOMER PROFILE | 19

has been involved in from day one at the International Maritime Organisation. As Mr Welsh explains to Container Shipping & Trade: “We worked constructively with stakeholders, and with their support, helped shape the legislation – most notably in securing support for a “calculated weight” compromise proposal." Indeed, “no sooner had the ink dried on the final decision”, GSF has worked with stakeholders to figure out the best way to meet these requirements. The GSF, working with its UK member, the Freight Transport Association, recommended the establishment of a working group involving all stakeholders including the UK Maritime Coast Guard Agency to develop an accreditation scheme for shippers to use the calculated method approved by the IMO.

This has been crucial, because as Mr Welsh highlights: “This is one of those issues which on the face of it sounds very simple. Shippers should know what the accurate weight of their containers are. Indeed, even though the new container rules come into play on 1 July, there has always been a legal requirement under SOLAS for shippers to make accurate declarations; this legislation however gives clarity to how this should be done and the responsibilities of the stakeholders”.

But all is not as it seems, because while as Mr Welsh says, this appears to be a “no brainer”, he highlights that it is a “lot more difficult and complex when looking deeper, largely because of how the supply chain works”.

Mr Welsh explains: “The UK working group has worked constructively to find a pragmatic solution to implementation in the UK, and the proposed accredited scheme has been highly influential internationally. For example, the approach in accepting shippers existing audit based systems upon which to make accurate VGM declarations have been accepted by other European countries such as France, Germany and Netherlands. The approach has been highly influential in implementation approaches adopted in New Zealand, South Africa, Australia and Canada.”

But there are still challenges: large parts of the world have yet to determine their enforcement and implementation approaches for verifying container weights. Mr Welsh warns: “And there are concerns about whether many regulatory authorities will be ready by 1 July 2016. It is imperative that these states get their act together as soon as possible to ensure there is a seamless transition

towards implementation of the new VGM regime to avoid disruption in the maritime supply chain.” He said that is why GSF is working together with various maritime supply chain stakeholders, such as the TT Club, International Cargo Harding Coordination Association and World Shipping Council to ensure the stakeholders are aware of their responsibilities and are fully prepared for implementation from 1 July 2016. GSF, TT Club, ICHCA and WSC have jointly produced a Frequently Asked Questions guide which is available on the GSF website. Explaining how GSF would deal with these challenges, he said: “We will intensify our communications in the lead up to 1 July, keeping a high profile in the media and produce best practice advice for shippers explaining their responsibilities and how to comply."

He warned there was no time to delay – that shippers and the rest of the maritime industry need to be preparing now, if they are to be ready for 1 July. "With less than six months to go shippers need to decide what is the best method for providing the VGM and to be talking to their carriers, forwarders, and hauliers to go through the practical logistics arrangements concerning compliance. As they dig into it, they will realise the complexity of the issue and range of choices open to them in terms of their VGM approach and will communicate this to the carrier. For carriers, there is also a responsibility to assist their customers in complying with the rules. Commendably, many carriers are providing information on their websites." But he said that the carrier community needs to reach out to customers and put in place contingency plans for shipments presented to terminals without a VGM. For example, Mr Welsh said that for every booking made from 1 July onwards, when confirming the booking the carrier could remind the shipper they will be required to make a VGM declaration, otherwise the container will not be loaded on the ship. "These are the kind of common sense contingency planning arrangements that will be necessary to avoid short-shipped consignments, delays and problems at the port terminal to ensure a smooth transition to the new regime," Mr Welsh said.

PUSH FOR SINGLE IMO CO2 MEASUREAside from container weighing, the GSF has called on the shipping industry to reach agreement on clear targets

Chris Welsh was awarded an MBE in the 2015 Queen’s Birthday Honours for services to shippers and the shipping industry

Chris Welsh MBE

Chris Welsh was appointed secretary general of the Global Shippers’ Forum with effect from 1 July 2011.

From 1996-2002 Mr Welsh was secretary general of the European Shippers’ Council where he played a prominent role in deregulating EU shipping and air cargo markets, spearheading a series of successful maritime legal cases which culminated in the repeal of anti-trust immunity for liner shipping conferences in trades to and from Europe in 2006.

Mr Welsh has held a variety of senior management roles with the UK’s Freight Transport Association (FTA), and is currently director of global and European policy. In 1992 he established FTA’s Brussels operations and in 2010 he set up FTA Ireland, an independent multimodal logistics trade association for Irish shippers and logistics interests.

Mr Welsh holds a master’s degree in business administration, and is a chartered member of the Chartered Institute of Logistics and Transport and a member of the Chartered Management Institute.

“There are concerns whether many regulatory authorities will be ready by 1 July 2016. It is imperative that these states get their acts together as soon as possible to ensure there is a seamless transition towards impementation of the new regime”

For more articles visit www.containerst.com Container Shipping & Trade | 1st Quarter 2016

for maritime emissions reductions – something that has gained even more momentum since the COP21 climate change talks. The GSF has released a statement outlining its views on how the maritime sector should address the issue.

“We are concerned about what kind of MBM may be adopted in the future and how it will affect shippers. An international agreement on this through IMO would be best. However, developing an appropriate response to maritime emission reductions has been slow and no agreement has been reached in IMO. The shipping industry was open to considerable criticism in COP21, whether justified or not. Perceptions count for a lot. Unless the process for an agreed solution is speeded up, it is likely to lead for calls for tougher action and for the matter taken out of the hands of IMO altogether,” Mr Welsh commented.

Indeed, the EU is already proceeding with its own Monitoring, Verification and Reporting system in absence of an IMO agreement. Mr Welsh said that the hope was the EU will prompt a satisfactory outcome in IMO. “The EU has made it clear if agreement can be reached at IMO to its satisfaction it would modify its own arrangements to comply with the international agreement but the bottom line is, if they can’t reach agreement it will go it alone,” he added.

MEGA ALLIANCES COMPETITION WATCH Elsewhere, concerns about the mega ship and shipping alliances has formed a large focus for GSF. Mr Welsh explained: “Providing these alliances do not lead to elimination of competition and that the benefits are genuinely passed on to shippers – through for example a better range of and enhanced services and a share in the benefits of reduced costs – it may not all be bad news. Our main concern is whether existing competition policy and regulatory arrangements are sufficiently robust to deal with the new breed of alliances and co-operation agreements. Shipping is still treated differently to the rest of the economy when it comes to the assessment of co-operative agreements such as alliances, and regulators are too ready to assume that such alliances confer benefits to shippers without more carefully studying the impact. The recent publication of the

OECD report on mega ships is a good example of the kind of independent assessment needed in this area."

Indeed these concerns have led to GSF to launch an analysis on the subject – a large part of which is focused on the competition element. Mr Welsh said: “There are arguments on both sides of the debate, about whether alliances in the long term benefit shippers and carriers, or whether it would be better if there was greater merger and acquisition, leading to fewer players competing head on with each other rather than collaborating in alliances.”

This is one of the areas that the report – due to be published in spring this year – is studying. Mr Welsh explained: “There is a need for competition analysis and what more competition authorities and regulators should be looking at in these areas, which is why we are publishing a report which we hope will form the basis of a calm and level headed discussion with the shipping industry and regulators.”

In 2011 GSF member, the Freight Transport Association, urged the European Commission to investigate the possibly of price signalling through the publication of general rate increases. The increases were for similar amounts over similar time frames.

Following a three-year investigation the European Commission recently published a communication in the Official Journal of the EU confirming that the lines have offered commitments to the way prices are announced.

Mr Welsh said that the GSF welcomes the Commission bringing this case on liner shipping prices to a satisfactory close. The GSF, like the FTA, welcomes the Commission’s commitments decision and believes this will introduce a degree of transparency into maritime transport pricing for the first time.

“We welcome the fact the lines have agreed that they will cease to announce general rate increases and publish the actual prices made available to customers on an individual basis,” said Mr Welsh.

He summed up: “Shippers will respond to the Commission’s ‘market test’ consultation to ensure that the arrangements contribute towards a more rational, transparent and appropriate pricing system which is long overdue following the removal of the liner conference anti-trust immunity in 2008." CST

20 | CUSTOMER PROFILE

CONTAINER WEIGHT COUNTDOWN

1 July 2015The day regulation comes into effect requiring containers to have a verified gross mass before they can be loaded on a ship.

Accredited Shipper Approval SchemeFTA and other stakeholders developed an accreditation scheme for shippers using a calculated weight method of verification.

Two methods of verifying weight Weighing the packed container using certified and calibrated equipment or using a calculated weight method that adds up individual items separately, and then adds the tare weight of the container and packing materials, using an approved process.

Audit-based systemsShippers can use their existing audit based systems to comply with the new rules.

Accreditation successThe scheme is successful in the UK, and has been been accepted by other European countries. It will also influence container weight verification in New Zealand, South Africa, Australia and Canada.

Verification approach not uniformIt is still unclear in some countries what approach enforcement authorities will take to verifying container weights. Concern that procedures are not yet in place to make the transition to a new regime.

Shippers must act Less than four months to go and shippers who are not ready for new regulation have a lot to focus on, from communication systems to contingency plans.

Container Shipping & Trade | 1st Quarter 2016 For more articles visit www.containerst.com

What do 300 vessels do that you don’t?

THEY DEMAND HYDE MARINE.

With 20 years of BWT technology experience and more BWT installations in service than any other company in the world, count on the experience of Hyde Marine.

+1.724.218.7001 I www.hydemarine.com

FREE ACCESSTO TECHNICAL DOCUMENTATION FORMARINE & OFFSHORE PROFESSIONALS

www.containerst.com/knowledgebank

Take advantage of the Maritime Technology Knowledge Bank.

• A unique, free to access, resource for the global shipping industry • Access whitepapers and technical documentation covering every

aspect of maritime technology, equipment and new products.

tel: +30 210 4293 223 [email protected] www.register-iri.com

International Registries, Inc.in affiliation with the Marshall Islands Maritime & Corporate Administrators

the Republic of the Marshall Islands is the flag of choice for some of the world’s top shipping companies

service and quality are within your reach

We look forward to seeing you at Posidonia 2016

Visit us at Booth 4.215

22 | OPERATOR PROFILE

Hyundai on the precipice

South Korea’s second largest carrier says it needs to restructure debt and vessel charter fees in order to avoid bankruptcy, writes Gavin van Marle

It is often said that the lead up to a maritime accident can take a very long time,

but when the accident actually takes place everything suddenly seems to move very fast.

It seems to be the same with shipping companies, if the recent troubles besetting Hyundai Merchant Marine (HMM) are anything to go by. Crunch time is fast approaching for South Korea’s second largest shipping line, as lenders and the company’s senior management and major shareholders are going to have to make some urgent decisions, soon.

It has been known for some time that HMM has had problems with its balance sheet – after all, there are only a few liner companies that can genuinely claim not to have had financial concerns over the past five years – but these appear to have reached a head in the last few weeks. Shortly before this issue of Container Shipping & Trade went to press, container and dry bulk shipowners and ship brokers that have worked with the company received a letter that has sent shock waves through the industry.

“Liquidity has deteriorated to the point where HMM cannot operate without relief from the shipowners and creditors and needs to restructure in order to survive,” wrote HMM chief executive Paik Hoon Lee. He continued: “It is critical to understand that HMM’s financial difficulties cannot be solved by dealing

with its financial liabilities alone. Unless time-charter payments are significantly reduced as well, the company cannot survive.

“We envisage a consensual restructuring, in which all of our stakeholders will make an equitable contribution to the recovery of the company.” He also admitted that this will entail the company’s current shareholders seeing their existing shareholdings “significantly diluted.”

HMM’s present predicament is the culmination of several years of prolonged financial difficulties. A first turn-around attempt was made in 2013, when the Hyundai Group formulated what it described as self-help plans and began a series of asset disposals and capital raising exercises. It also introduced a new operational cost savings programme, which provided its container shipping division with an estimated KRW3,582 billion (US$2.97 billion) in additional liquidity.

But it has proved insufficient, as liner shipping analyst Alphaliner explains. “HMM is currently struggling to stay afloat in a liquidity crunch. To improve its balance sheet, HMM seeks to raise much-needed cash through the sale of various assets, including Hyundai Securities, its dry bulk shipping business, its US container terminals, and the remaining stake in Busan New Port Container Terminal.

“HMM’s financial position Figure 1. (Source: HMM nine-month results 2015)

PERCENTAGE OF LINER REVENUES

PERCENTAGE OF LINER VOLUMES

Asia-Europe

LANES

Intra-Asia

Transpacific Emerging

17.3%

29.4%

6.6%

7.1%

27.5%

23.7%

48.6%

39.8%

Container Shipping & Trade | 1st Quarter 2016 For more articles visit www.containerst.com

OPERATOR PROFILE | 23

remains precarious due to continued losses incurred by the container shipping business, and due to KRW521 billion (US$432 million) worth of loans that will mature in April and July this year. The carrier may be forced to seek court receivership should it be unable to secure creditors’ agreement to restructure debt.”

According to Freight Investor Services container derivatives broker Richard Ward, the most recent numbers show that at the end of April HMM will be required to repay one tranche of debt amounting to of KRW220.8 billion (USD$182.2 million), followed by a further repayment of KRW299.2 billion (US$249.5 million) at the end of July. Mr Lee’s letter admitted that, should creditors and shipowners not agree to new terms, the line was likely to head towards Korea’s bankruptcy court.

However, shortly after the letter’s release came confirmation from financial circles in Seoul that both KB Financial Group and Korea Investment Holdings Co have sent letters of intent to buy a controlling stake in Hyundai Securities. The 22.6 per cent stake is reportedly worth KRW300 billion (US$250 million) and could provide a much needed boost to cash reserves. It is also understood that Hyundai Group chairwoman Hyun Jeong Eun will stump up KRW30 billion (US$24.4 million) of her private fortune to further prop up the company.

Mr Ward comments: “It is clear that the Korean line has been scrambling to raise cash as it looks for some short-term relief from its liquidity woes. However, the revelations from senior management about the gravity of the situation will do little to calm any nervousness there may be about whether the liner should be treated as a going concern.”