Container Shipping 2013 Market Outlook

22

Container Shipping 2013 Market Outlook Web: www.alphaliner.com E-mail: [email protected] The worldwide reference in liner shipping Shenzhen, 17 October 2012

Transcript of Container Shipping 2013 Market Outlook

Container Shipping

2013 Market Outlook

Web: www.alphaliner.com E-mail: [email protected]

The worldwide reference in liner shipping

Shenzhen, 17 October 2012

ALPHALINER Containership Market Outlook www.alphaliner.com – the worldwide reference in liner shipping © Alphaliner 1999-2012 – Contents not to be reproduced without permission

TPM Asia : October 2012

Carriers remain trapped with surplus capacity

© Alphaliner Page 1

New deliveries

Return of chartered tonnage

Scrapping increases

Charter rates drop

Surplus Capacity

Rates fall below

breakeven

Idling of surplus capacity

Rates return to breakeven

Idle capacity re-activated

The surplus

capacity trap

may last to

2014

ALPHALINER Containership Market Outlook www.alphaliner.com – the worldwide reference in liner shipping © Alphaliner 1999-2012 – Contents not to be reproduced without permission

TPM Asia : October 2012

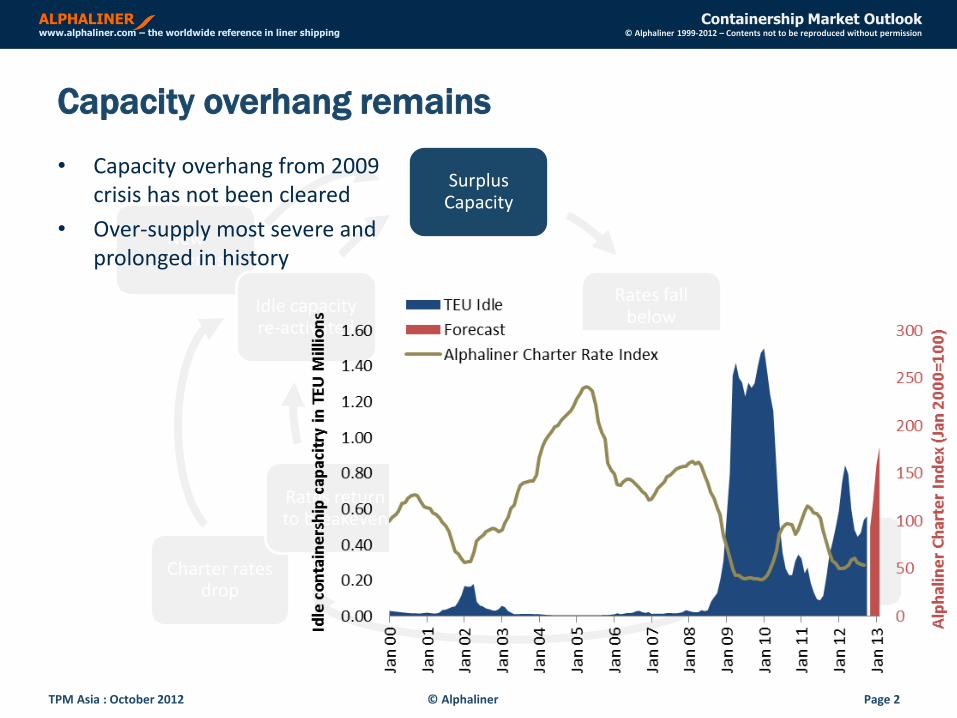

Capacity overhang remains

© Alphaliner Page 2

New deliveries

Return of chartered tonnage

Scrapping increases

Charter rates drop

Surplus Capacity

Rates fall below

breakeven

Idling of surplus capacity

Rates return to breakeven

Idle capacity re-activated

• Capacity overhang from 2009 crisis has not been cleared

• Over-supply most severe and prolonged in history

ALPHALINER Containership Market Outlook www.alphaliner.com – the worldwide reference in liner shipping © Alphaliner 1999-2012 – Contents not to be reproduced without permission

TPM Asia : October 2012

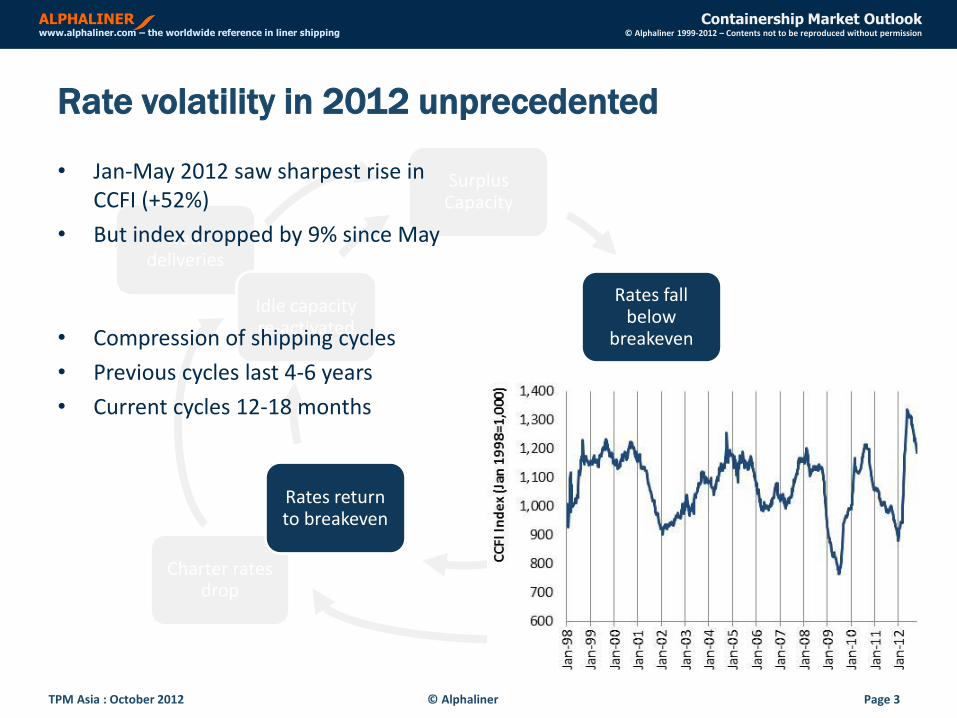

Rate volatility in 2012 unprecedented

© Alphaliner Page 3

New deliveries

Return of chartered tonnage

Scrapping increases

Charter rates drop

Surplus Capacity

Rates fall below

breakeven

Idling of surplus capacity

Rates return to breakeven

Idle capacity re-activated

• Jan-May 2012 saw sharpest rise in CCFI (+52%)

• But index dropped by 9% since May

• Compression of shipping cycles

• Previous cycles last 4-6 years

• Current cycles 12-18 months

ALPHALINER Containership Market Outlook www.alphaliner.com – the worldwide reference in liner shipping © Alphaliner 1999-2012 – Contents not to be reproduced without permission

TPM Asia : October 2012

Compression of the shipping cycle

© Alphaliner Page 4

New deliveries

Return of chartered tonnage

Scrapping increases

Charter rates drop

Surplus Capacity

Rates fall below

breakeven

Idling of surplus capacity

Rates return to breakeven

Idle capacity re-activated

• Variance of CCFI rates in 2012 highest since 1998

• High volatility due to capacity overhang

• Excess capacity returns with each recovery

• Idling/slow steaming/charter redeliveries are only temporary solutions

ALPHALINER Containership Market Outlook www.alphaliner.com – the worldwide reference in liner shipping © Alphaliner 1999-2012 – Contents not to be reproduced without permission

TPM Asia : October 2012

Compressed shipping cycle will continue in 2013

© Alphaliner Page 5

New deliveries

Return of chartered tonnage

Scrapping increases

Charter rates drop

Surplus Capacity

Rates fall below

breakeven

Idling of surplus capacity

Rates return to breakeven

Idle capacity re-activated

• Lows more severe – limited only by carriers’ capacity to stomach losses

• Highs will be short-lived

• Rate trend show long-term decline

0

200

400

600

800

1,000

1,200

1,400

1,600

Jan

-98

Jan

-99

Jan

-00

Jan

-01

Jan

-02

Jan

-03

Jan

-04

Jan

-05

Jan

-06

Jan

-07

Jan

-08

Jan

-09

Jan

-10

Jan

-11

Jan

-12

CC

FI I

nd

ex

(Jan

19

98

=1,0

00

)

CCFI

0

200

400

600

800

1,000

1,200

1,400

1,600

Jan

-98

Jan

-99

Jan

-00

Jan

-01

Jan

-02

Jan

-03

Jan

-04

Jan

-05

Jan

-06

Jan

-07

Jan

-08

Jan

-09

Jan

-10

Jan

-11

Jan

-12

CC

FI I

nd

ex

(Jan

19

98

=1,0

00

)

FO $/tonCCFIFuel Adjusted Freight Index

• Trend even more apparent if fuel adjusted rate index

ALPHALINER Containership Market Outlook www.alphaliner.com – the worldwide reference in liner shipping © Alphaliner 1999-2012 – Contents not to be reproduced without permission

TPM Asia : October 2012

Significant new vessel deliveries due in 2013

© Alphaliner Page 6

New deliveries

Return of chartered tonnage

Scrapping increases

Charter rates drop

Surplus Capacity

Rates fall below

breakeven

Idling of surplus capacity

Rates return to breakeven

Idle capacity re-activated

• 40% are new ships of over 10,000 teu

• Driven by need to lower unit costs

• Orders have not stopped

• 1.05 million TEU already delivered YTD

• 1.41 million TEU to be delivered in 2012

• 1.77 million TEU due in 2013

ALPHALINER Containership Market Outlook www.alphaliner.com – the worldwide reference in liner shipping © Alphaliner 1999-2012 – Contents not to be reproduced without permission

TPM Asia : October 2012

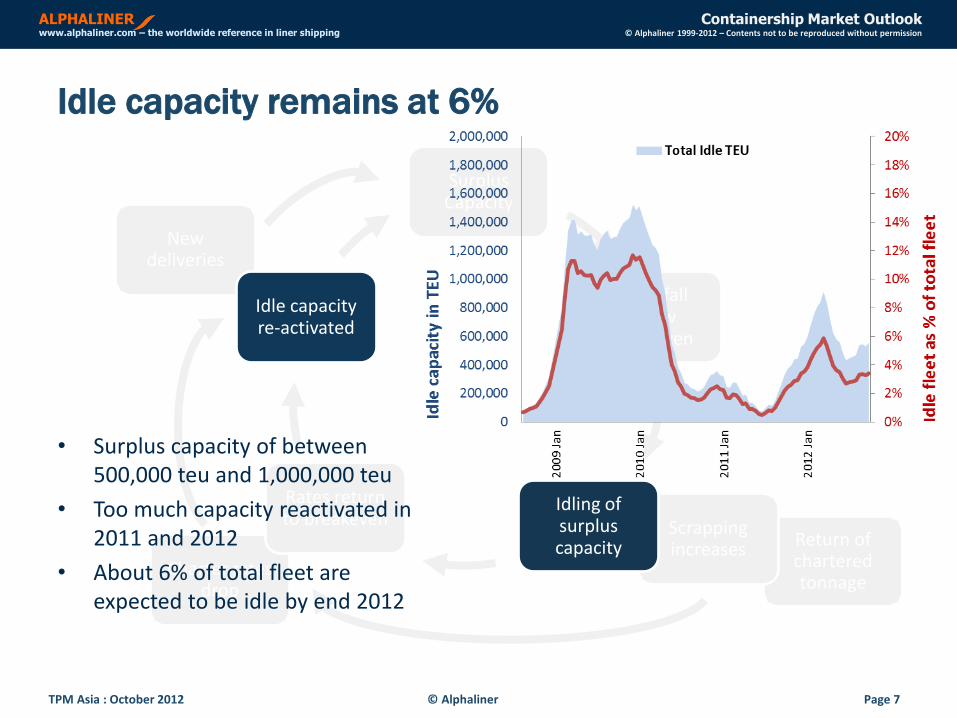

Idle capacity remains at 6%

© Alphaliner Page 7

New deliveries

Return of chartered tonnage

Scrapping increases

Charter rates drop

Surplus Capacity

Rates fall below

breakeven

Idling of surplus capacity

Rates return to breakeven

Idle capacity re-activated

• Surplus capacity of between 500,000 teu and 1,000,000 teu

• Too much capacity reactivated in 2011 and 2012

• About 6% of total fleet are expected to be idle by end 2012

ALPHALINER Containership Market Outlook www.alphaliner.com – the worldwide reference in liner shipping © Alphaliner 1999-2012 – Contents not to be reproduced without permission

TPM Asia : October 2012

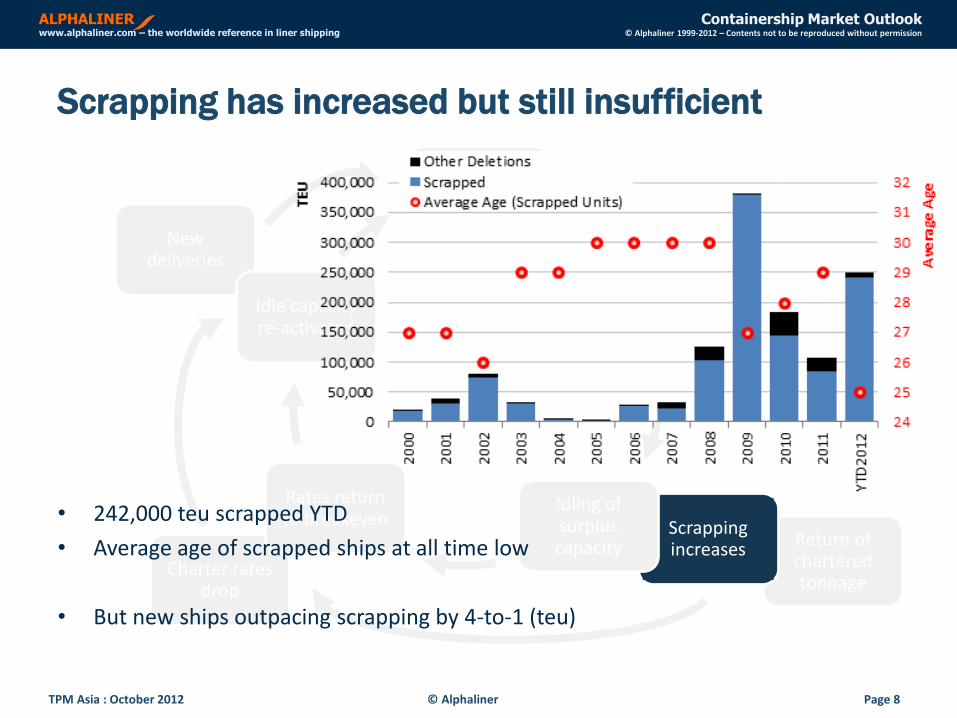

Scrapping has increased but still insufficient

© Alphaliner Page 8

New deliveries

Return of chartered tonnage

Scrapping increases

Charter rates drop

Surplus Capacity

Rates fall below

breakeven

Idling of surplus capacity

Rates return to breakeven

Idle capacity re-activated

• 242,000 teu scrapped YTD

• Average age of scrapped ships at all time low

• But new ships outpacing scrapping by 4-to-1 (teu)

ALPHALINER Containership Market Outlook www.alphaliner.com – the worldwide reference in liner shipping © Alphaliner 1999-2012 – Contents not to be reproduced without permission

TPM Asia : October 2012

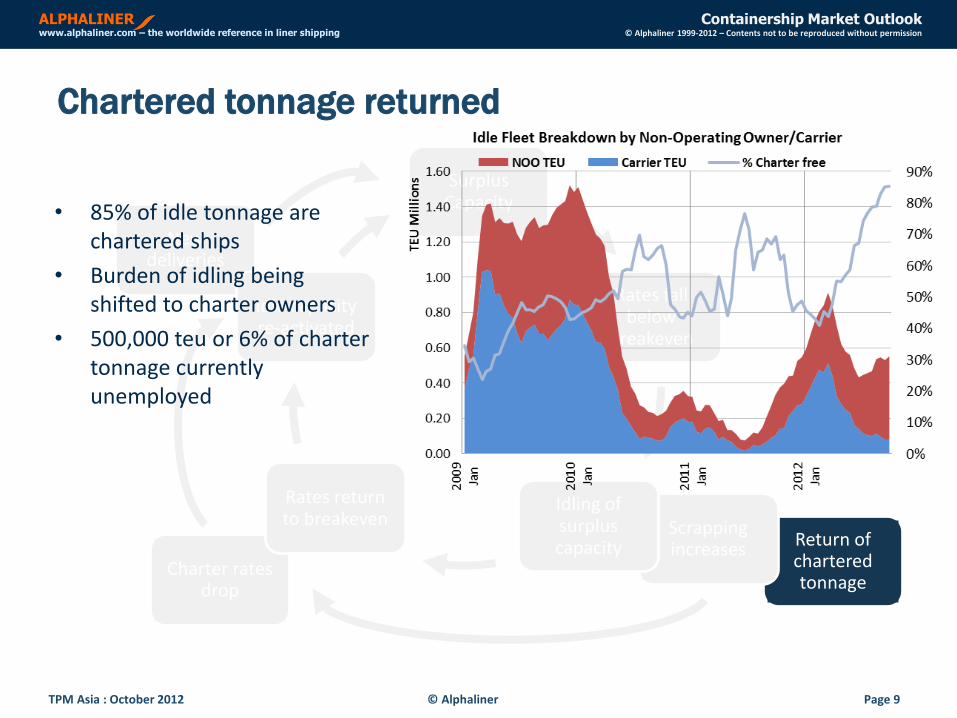

Chartered tonnage returned

© Alphaliner Page 9

New deliveries

Return of chartered tonnage

Scrapping increases

Charter rates drop

Surplus Capacity

Rates fall below

breakeven

Idling of surplus capacity

Rates return to breakeven

Idle capacity re-activated

• 85% of idle tonnage are chartered ships

• Burden of idling being shifted to charter owners

• 500,000 teu or 6% of charter tonnage currently unemployed

ALPHALINER Containership Market Outlook www.alphaliner.com – the worldwide reference in liner shipping © Alphaliner 1999-2012 – Contents not to be reproduced without permission

TPM Asia : October 2012

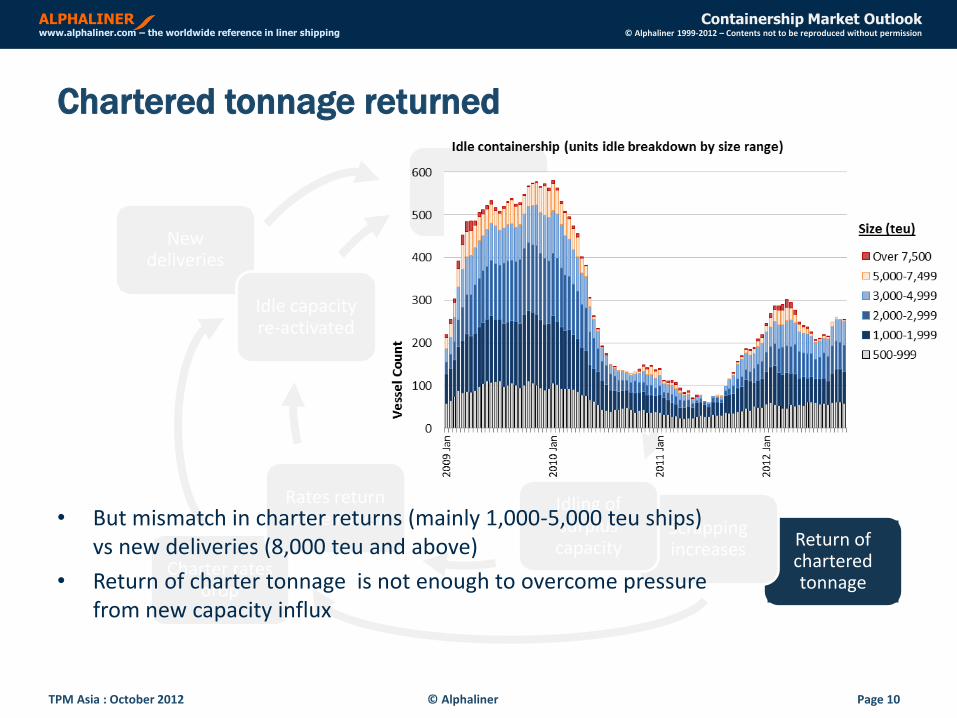

Chartered tonnage returned

© Alphaliner Page 10

New deliveries

Return of chartered tonnage

Scrapping increases

Charter rates drop

Surplus Capacity

Rates fall below

breakeven

Idling of surplus capacity

Rates return to breakeven

Idle capacity re-activated

• But mismatch in charter returns (mainly 1,000-5,000 teu ships) vs new deliveries (8,000 teu and above)

• Return of charter tonnage is not enough to overcome pressure from new capacity influx

ALPHALINER Containership Market Outlook www.alphaliner.com – the worldwide reference in liner shipping © Alphaliner 1999-2012 – Contents not to be reproduced without permission

TPM Asia : October 2012

Charter rates remain depressed

© Alphaliner Page 11

New deliveries

Return of chartered tonnage

Scrapping increases

Charter rates drop

Surplus Capacity

Rates fall below

breakeven

Idling of surplus capacity

Rates return to breakeven

Idle capacity re-activated

• Depressed charter rates will continue in 2013

• Carriers continue to take on new charters, with low charter rates

• Capacity can return on short notice

ALPHALINER Containership Market Outlook www.alphaliner.com – the worldwide reference in liner shipping © Alphaliner 1999-2012 – Contents not to be reproduced without permission

TPM Asia : October 2012

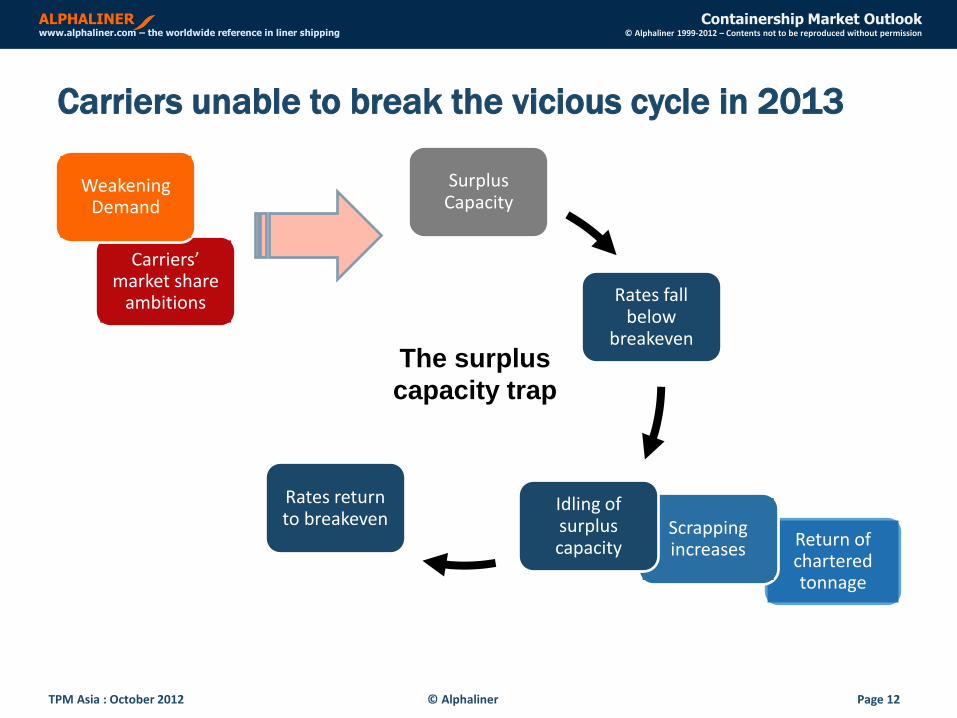

Carriers unable to break the vicious cycle in 2013

© Alphaliner Page 12

Return of chartered tonnage

Scrapping increases

Surplus Capacity

Rates fall below

breakeven

Idling of surplus capacity

Rates return to breakeven

Idle capacity re-activated

The surplus

capacity trap

Carriers’ market share

ambitions

Weakening Demand

ALPHALINER Containership Market Outlook www.alphaliner.com – the worldwide reference in liner shipping © Alphaliner 1999-2012 – Contents not to be reproduced without permission

TPM Asia : October 2012

Growth is slowing

© Alphaliner Page 13

Carriers’ market share

ambitions

Weakening Demand

• Demand growth at 4-6% in 2012-2013

• Vs capacity growth of 9% in 2013

ALPHALINER Containership Market Outlook www.alphaliner.com – the worldwide reference in liner shipping © Alphaliner 1999-2012 – Contents not to be reproduced without permission

TPM Asia : October 2012

Weak headhaul volumes pose significant challenge

© Alphaliner Page 14

Carriers’ market share

ambitions

Weakening Demand

• FE-Europe volume expected to shrink by -4.2% in 2012

• FE-US volume growth still weak at 1.5%

• The two main trades will come under greatest capacity pressure

ALPHALINER Containership Market Outlook www.alphaliner.com – the worldwide reference in liner shipping © Alphaliner 1999-2012 – Contents not to be reproduced without permission

TPM Asia : October 2012

Average load factors weak

© Alphaliner Page 15

Carriers’ market share

ambitions

Weakening Demand

• Average load factor on FE-Europe only 85%

• Average load factor on FE-US at 91%

• Capacity reductions are necessary but difficult to implement

60%

65%

70%

75%

80%

85%

90%

95%

100%

Jan

-10

Ap

r-1

0

Jul-

10

Oct

-10

Jan

-11

Ap

r-1

1

Jul-

11

Oct

-11

Jan

-12

Ap

r-1

2

Jul-

12

Oct

-12

Average vessel load factor FE-Europe route (Source : Shanghai Shipping Exchange)

60%

65%

70%

75%

80%

85%

90%

95%

100%

Jan

-10

Ap

r-1

0

Jul-

10

Oct

-10

Jan

-11

Ap

r-1

1

Jul-

11

Oct

-11

Jan

-12

Ap

r-1

2

Jul-

12

Oct

-12

Average vessel load factor FE-US route (Source : Shanghai Shipping Exchange)

ALPHALINER Containership Market Outlook www.alphaliner.com – the worldwide reference in liner shipping © Alphaliner 1999-2012 – Contents not to be reproduced without permission

TPM Asia : October 2012

Carriers unable to curb appetite for capacity

© Alphaliner Page 16

Carriers’ market share

ambitions

Weakening Demand

• 19 of Top 21 carriers have new capacity coming in next 15 months

• Only UASC/Zim are without new capacity

0 50,000 100,000 150,000 200,000 250,000

APLAPM-Maersk

MSCEvergreen

Hamburg SüdHapag-Lloyd

COSCONCSCL

Hanjin ShgOOCLMOL

Yang MingPIL

CMA CGMNYK Line

HMMWan Hai

K LineCSAV

ZimUASC

New Vessel Deliveries Oct 2012-Dec 2013 (TEU)

ALPHALINER Containership Market Outlook www.alphaliner.com – the worldwide reference in liner shipping © Alphaliner 1999-2012 – Contents not to be reproduced without permission

TPM Asia : October 2012

Carriers unable to curb appetite for capacity

© Alphaliner Page 17

Carriers’ market share

ambitions

Weakening Demand

• Top 21 carriers – capacity growth of 7.4% p.a. over 2008-2012 period

• A single carrier is enough to break capacity discipline and trigger a rate war

7%

12

%

9%

10

%

2%

6%

6%

7%

11

%

8%

5%

10

%

-1%

10

%

4%

4%

2%

13

%

19

%

-2%

7%

0.00

0.50

1.00

1.50

2.00

2.50

3.00

AP

M-M

aers

k

MSC

CM

A C

GM

CO

SCO

N

Eve

rgre

en

Hap

ag-L

loyd

AP

L

CSC

L

Han

jin S

hg

MO

L

OO

CL

Ham

bu

rg S

üd

NYK

Lin

e

HM

M

K L

ine

Yan

g M

ing

Zim PIL

UA

SC

CSA

V

Wan

Hai

Cap

acit

y O

pe

rate

d in

TEY

Mill

ion

s

Sep-08 Sep-12 CAGR 2008-2012

ALPHALINER Containership Market Outlook www.alphaliner.com – the worldwide reference in liner shipping © Alphaliner 1999-2012 – Contents not to be reproduced without permission

TPM Asia : October 2012

Excessive competition will remain

© Alphaliner Page 18

Carriers’ market share

ambitions

Weakening Demand

• 20 main carriers in FE-US and 19 main carriers in FE-Europe

• No indication of carrier exits in 2013

• Formation of alliances (MSC-CMA CGM, G6, CKYH ++) has reduced impetus for carrier consolidation

0 10,000 20,000 30,000 40,000 50,000 60,000 70,000 80,000 90,000

MaerskMSC

CMA CGMCOSCO

EvergreenCSCL

Hanjin ShgHapag-Lloyd

HMMOOCLUASCMOL

NYK LineAPL

K LineZim

Yang MingWan Hai

PIL

FE - Europe Weekly Capacity in nominal TEU

0 10,000 20,000 30,000 40,000 50,000 60,000 70,000 80,000 90,000

MaerskHanjin Shg

COSCOEvergreen

MSCHapag-Lloyd

APLCMA CGM

K LineYang Ming

HMMOOCLMOLNYK

CSCLZim

Wan HaiPIL

MatsonUASC

Westwood

FE - North America Weekly Capacity in nominal TEU

Weekly capacity share by carrier (Oct 2012) FE-Europe FE-North America

ALPHALINER Containership Market Outlook www.alphaliner.com – the worldwide reference in liner shipping © Alphaliner 1999-2012 – Contents not to be reproduced without permission

TPM Asia : October 2012

Carriers have limited options to curb growth

© Alphaliner Page 19

Carriers’ market share

ambitions

Weakening Demand

• Slow steaming, return of chartered tonnage and idling are only temporary solutions

• Scrapping & curbing new orders are more permanent solutions

• But capacity curbs have been ineffective so far

-15%

-10%

-5%

0%

5%

10%

15%

20%

10

11

12

13

14

15

16

17

2009Jan

2010Jan

2011Jan

2012Jan

% C

han

ge (

Ye

ar-o

n-y

ear

)

Tota

l Cel

lula

r C

apac

ity

in T

EU M

illio

ns

Capacity absorbed by ESS/SSS Idle capacityEffective Capacity YoY % change in Fleet CapacityYoY % change in Effective Capacity

Slow steaming absorbed 6% of fleet

Potential for further slow steaming

~4%

ALPHALINER Containership Market Outlook www.alphaliner.com – the worldwide reference in liner shipping © Alphaliner 1999-2012 – Contents not to be reproduced without permission

TPM Asia : October 2012

Predictions for 2013

© Alphaliner Page 20

• Rate volatility will continue

• Supply overhang will continue to dictate rates cycle in 2013

• NVO rates will be less volatile than 2012 - 3Q base rates 28% higher than 2011

• BCO rates will rise in 2013 but quantum probably lower than carrier targets

• Carriers will continue to shoot themselves in the foot

• Carrier discipline only when suffering from losses or when utilisation levels are high

• Nov GRI on FE-Europe will be followed by rate undercutting if load factors remain weak

• None of the main carriers will exit the market

• Excessive competitive will continue

• Predictions of industry consolidation are premature

ALPHALINER Containership Market Outlook www.alphaliner.com – the worldwide reference in liner shipping © Alphaliner 1999-2012 – Contents not to be reproduced without permission

TPM Asia : October 2012

End

Please send any queries to [email protected]/[email protected]

© Alphaliner Page 21

Alphaliner clients include the following top shipping lines :