Construtora Norberto Odebrecht S.A. - Cbonds

236

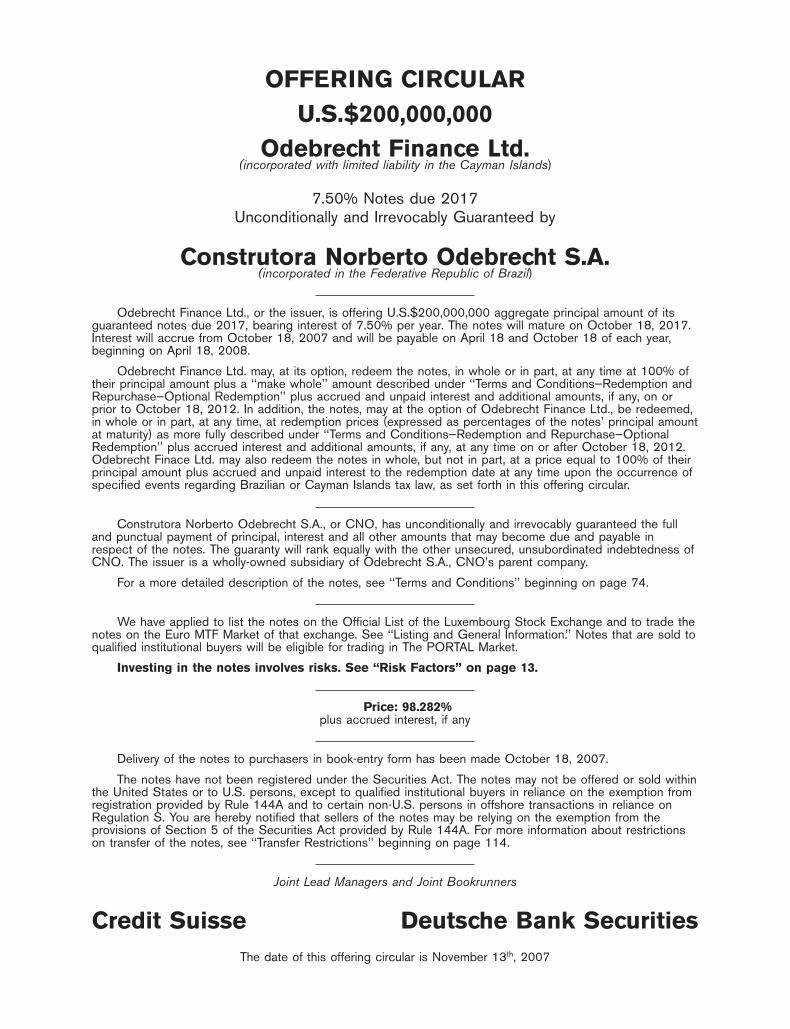

OFFERING CIRCULAR U.S.$200,000,000 Odebrecht Finance Ltd. (incorporated with limited liability in the Cayman Islands) 7.50% Notes due 2017 Unconditionally and Irrevocably Guaranteed by Construtora Norberto Odebrecht S.A. (incorporated in the Federative Republic of Brazil) Odebrecht Finance Ltd., or the issuer, is offering U.S.$200,000,000 aggregate principal amount of its guaranteed notes due 2017, bearing interest of 7.50% per year. The notes will mature on October 18, 2017. Interest will accrue from October 18, 2007 and will be payable on April 18 and October 18 of each year, beginning on April 18, 2008. Odebrecht Finance Ltd. may, at its option, redeem the notes, in whole or in part, at any time at 100% of their principal amount plus a ‘‘make whole’’ amount described under ‘‘Terms and Conditions—Redemption and Repurchase—Optional Redemption’’ plus accrued and unpaid interest and additional amounts, if any, on or prior to October 18, 2012. In addition, the notes, may at the option of Odebrecht Finance Ltd., be redeemed, in whole or in part, at any time, at redemption prices (expressed as percentages of the notes’ principal amount at maturity) as more fully described under ‘‘Terms and Conditions—Redemption and Repurchase—Optional Redemption’’ plus accrued interest and additional amounts, if any, at any time on or after October 18, 2012. Odebrecht Finace Ltd. may also redeem the notes in whole, but not in part, at a price equal to 100% of their principal amount plus accrued and unpaid interest to the redemption date at any time upon the occurrence of specified events regarding Brazilian or Cayman Islands tax law, as set forth in this offering circular. Construtora Norberto Odebrecht S.A., or CNO, has unconditionally and irrevocably guaranteed the full and punctual payment of principal, interest and all other amounts that may become due and payable in respect of the notes. The guaranty will rank equally with the other unsecured, unsubordinated indebtedness of CNO. The issuer is a wholly-owned subsidiary of Odebrecht S.A., CNO’s parent company. For a more detailed description of the notes, see ‘‘Terms and Conditions’’ beginning on page 74. We have applied to list the notes on the Official List of the Luxembourg Stock Exchange and to trade the notes on the Euro MTF Market of that exchange. See ‘‘Listing and General Information.’’ Notes that are sold to qualified institutional buyers will be eligible for trading in The PORTAL Market. Investing in the notes involves risks. See ‘‘Risk Factors’’ on page 13. Price: 98.282% plus accrued interest, if any Delivery of the notes to purchasers in book-entry form has been made October 18, 2007. The notes have not been registered under the Securities Act. The notes may not be offered or sold within the United States or to U.S. persons, except to qualified institutional buyers in reliance on the exemption from registration provided by Rule 144A and to certain non-U.S. persons in offshore transactions in reliance on Regulation S. You are hereby notified that sellers of the notes may be relying on the exemption from the provisions of Section 5 of the Securities Act provided by Rule 144A. For more information about restrictions on transfer of the notes, see ‘‘Transfer Restrictions’’ beginning on page 114. Joint Lead Managers and Joint Bookrunners Credit Suisse Deutsche Bank Securities The date of this offering circular is November 13 th , 2007

Transcript of Construtora Norberto Odebrecht S.A. - Cbonds

OFFERING CIRCULARU.S.$200,000,000

Odebrecht Finance Ltd.(incorporated with limited liability in the Cayman Islands)

7.50% Notes due 2017Unconditionally and Irrevocably Guaranteed by

Construtora Norberto Odebrecht S.A.(incorporated in the Federative Republic of Brazil)

Odebrecht Finance Ltd., or the issuer, is offering U.S.$200,000,000 aggregate principal amount of itsguaranteed notes due 2017, bearing interest of 7.50% per year. The notes will mature on October 18, 2017.Interest will accrue from October 18, 2007 and will be payable on April 18 and October 18 of each year,beginning on April 18, 2008.

Odebrecht Finance Ltd. may, at its option, redeem the notes, in whole or in part, at any time at 100% oftheir principal amount plus a ‘‘make whole’’ amount described under ‘‘Terms and Conditions—Redemption andRepurchase—Optional Redemption’’ plus accrued and unpaid interest and additional amounts, if any, on orprior to October 18, 2012. In addition, the notes, may at the option of Odebrecht Finance Ltd., be redeemed,in whole or in part, at any time, at redemption prices (expressed as percentages of the notes’ principal amountat maturity) as more fully described under ‘‘Terms and Conditions—Redemption and Repurchase—OptionalRedemption’’ plus accrued interest and additional amounts, if any, at any time on or after October 18, 2012.Odebrecht Finace Ltd. may also redeem the notes in whole, but not in part, at a price equal to 100% of theirprincipal amount plus accrued and unpaid interest to the redemption date at any time upon the occurrence ofspecified events regarding Brazilian or Cayman Islands tax law, as set forth in this offering circular.

Construtora Norberto Odebrecht S.A., or CNO, has unconditionally and irrevocably guaranteed the fulland punctual payment of principal, interest and all other amounts that may become due and payable inrespect of the notes. The guaranty will rank equally with the other unsecured, unsubordinated indebtedness ofCNO. The issuer is a wholly-owned subsidiary of Odebrecht S.A., CNO’s parent company.

For a more detailed description of the notes, see ‘‘Terms and Conditions’’ beginning on page 74.

We have applied to list the notes on the Official List of the Luxembourg Stock Exchange and to trade thenotes on the Euro MTF Market of that exchange. See ‘‘Listing and General Information.’’ Notes that are sold toqualified institutional buyers will be eligible for trading in The PORTAL Market.

Investing in the notes involves risks. See ‘‘Risk Factors’’ on page 13.

Price: 98.282%plus accrued interest, if any

Delivery of the notes to purchasers in book-entry form has been made October 18, 2007.

The notes have not been registered under the Securities Act. The notes may not be offered or sold withinthe United States or to U.S. persons, except to qualified institutional buyers in reliance on the exemption fromregistration provided by Rule 144A and to certain non-U.S. persons in offshore transactions in reliance onRegulation S. You are hereby notified that sellers of the notes may be relying on the exemption from theprovisions of Section 5 of the Securities Act provided by Rule 144A. For more information about restrictionson transfer of the notes, see ‘‘Transfer Restrictions’’ beginning on page 114.

Joint Lead Managers and Joint Bookrunners

Credit Suisse Deutsche Bank SecuritiesThe date of this offering circular is November 13th, 2007

TABLE OF CONTENTS

Page Page

ENFORCEMENT OF CIVIL LIABILITIES . . . . v MANAGEMENT . . . . . . . . . . . . . . . . . . . . . 70PRESENTATION OF FINANCIAL AND OTHER PRINCIPAL SHAREHOLDERS . . . . . . . . . . . 72

INFORMATION . . . . . . . . . . . . . . . . . . . vi RELATED PARTY TRANSACTIONS . . . . . . . 73FORWARD LOOKING STATEMENTS . . . . . . . viii TERMS AND CONDITIONS . . . . . . . . . . . . . 74EXCHANGE RATES . . . . . . . . . . . . . . . . . . x TAXATION . . . . . . . . . . . . . . . . . . . . . . . . 101SUMMARY . . . . . . . . . . . . . . . . . . . . . . . . 1 PLAN OF DISTRIBUTION . . . . . . . . . . . . . . 107RISK FACTORS . . . . . . . . . . . . . . . . . . . . 13 NOTICE TO CANADIAN RESIDENTS . . . . . . 112USE OF PROCEEDS . . . . . . . . . . . . . . . . . . 22 TRANSFER RESTRICTIONS . . . . . . . . . . . . . 114CAPITALIZATION . . . . . . . . . . . . . . . . . . . 23 VALIDITY OF NOTES . . . . . . . . . . . . . . . . 116SELECTED FINANCIAL AND OTHER INDEPENDENT AUDITORS . . . . . . . . . . . . . 116

INFORMATION OF CNO . . . . . . . . . . . . 24 LISTING AND GENERAL INFORMATION . . . 117MANAGEMENT’S DISCUSSION AND INDEX TO FINANCIAL STATEMENTS . . . . . . F-1

ANALYSIS OF FINANCIAL CONDITION APPENDIX A—SUMMARY OF PRINCIPAL

AND RESULTS OF OPERATIONS . . . . . . . 29 DIFFERENCES BETWEEN BRAZILIAN

BUSINESS . . . . . . . . . . . . . . . . . . . . . . . . 48 GAAP AND U.S. GAAP . . . . . . . . . . . . A-1THE ISSUER . . . . . . . . . . . . . . . . . . . . . . 69

You should rely only on the information contained in this offering circular. We have notauthorized anyone to provide you with different information. This offering circular may only be usedwhere it is legal to sell these notes. You should not assume that the information contained in thisoffering circular is accurate as of any date other than the date on the front of this offering circular.

Unless otherwise indicated or the context otherwise requires, all references in this offering circularto ‘‘Construtora Norberto Odebrecht S.A.,’’ ‘‘CNO,’’ ‘‘our company,’’ ‘‘we,’’ ‘‘our,’’ ‘‘ours,’’ ‘‘us’’ orsimilar terms refer to Construtora Norberto Odebrecht S.A, and all references to ‘‘Odebrecht Finance’’or the ‘‘issuer’’ refer to Odebrecht Finance Ltd., a wholly-owned subsidiary of Odebrecht S.A. and theissuer of the notes. The term ‘‘Brazil’’ refers to the Federative Republic of Brazil, and the phrase‘‘Brazilian government’’ refers to the federal government of Brazil.

We, having made all reasonable inquiries, confirm that the information contained in this offeringcircular with regard to us is true and accurate in all material respects, that the opinions and intentionsexpressed in this offering circular are honestly held, and that there are no other facts the omission ofwhich would make this offering circular as a whole or any of such information or the expression of anysuch opinions or intentions misleading in any material respect. We accept responsibility accordingly.

This offering circular does not constitute an offer to sell, or a solicitation of an offer to buy, anynote offered hereby by any person in any jurisdiction in which it is unlawful for such person to makean offer or solicitation. Neither the delivery of this offering circular nor any sale made hereunder shallunder any circumstances imply that there has been no change in our affairs or that the informationset forth in this offering circular is correct as of any date subsequent to the date of this offeringcircular.

This offering circular has been prepared by us solely for use in connection with the proposedoffering of the notes. We, as well as Credit Suisse Securities (USA) LLC and Deutsche Bank

i

Securities Inc., or the initial purchasers, reserve the right to reject any offer to purchase, in whole or inpart, for any reason, or to sell less than all of the notes offered by this offering circular.

You must (1) comply with all applicable laws and regulations in force in any jurisdiction inconnection with the possession or distribution of this offering circular and the purchase, offer or sale ofthe notes, and (2) obtain any required consent, approval or permission for the purchase, offer or saleby you of the notes under the laws and regulations applicable to you in force in any jurisdiction towhich you are subject or in which you make such purchases, offers or sales, and neither we nor theinitial purchasers have any responsibility therefor. See ‘‘Transfer Restrictions’’ for informationconcerning some of the transfer restrictions applicable to the notes.

You acknowledge that:

• you have been afforded an opportunity to request from us, and to review, all additionalinformation considered by you to be necessary to verify the accuracy of, or to supplement, theinformation contained in this offering circular;

• you have not relied on the initial purchasers or any person affiliated with the initial purchasersin connection with your investigation of the accuracy of such information or your investmentdecision; and

• no person has been authorized to give any information or to make any representationconcerning us or the notes other than those as set forth in this offering circular. If given ormade, any such other information or representation should not be relied upon as having beenauthorized by us or the initial purchaser.

In making an investment decision, you must rely on your own examination of our business and theterms of this offering, including the merits and risks involved. These notes have not been recommendedby any federal or state securities commission or regulatory authority. Furthermore, these authoritieshave not confirmed the accuracy or determined the adequacy of this offering circular. Anyrepresentation to the contrary is a criminal offense.

The offering is being made in reliance upon an exemption from registration under the SecuritiesAct, for an offer and sale of securities that does not involve a public offering. The notes are subject torestrictions on transferability and resale and may not be transferred or resold except as permittedunder the Securities Act and applicable state securities laws, pursuant to registration or exemptiontherefrom. In making your purchase, you will be deemed to have made certain acknowledgments,representations and agreements set forth in this offering circular under the caption ‘‘TransferRestrictions.’’ You should be aware that you may be required to bear the financial risks of thisinvestment for an indefinite period of time.

This offering circular may only be used for the purposes for which it has been published. Theinitial purchasers are not making any representation or warranty as to the accuracy or completeness ofthe information contained in this offering circular, and nothing contained in this offering circular is, orshall be relied upon as, a promise or representation, whether as to the past or the future.

No invitation may be made to the public in the Cayman Islands to subscribe for notes unless at thetime of invitation, the notes are listed on the Cayman Islands stock exchange.

The Luxembourg Stock Exchange takes no responsibility for the contents of this offering circular,makes no representations as to its accuracy or completeness and expressly disclaims any liabilitywhatsoever for any loss howsoever arising from or in reliance upon the whole or any part of the

ii

contents of this offering circular. This offering circular constitutes a prospectus for the purpose ofLuxembourg law dated July 10, 2005 on Prospectuses for securities.

See ‘‘Risk Factors’’ for a description of certain factors relating to an investment in the notes,including information about our business. None of us, the initial purchasers or any of our or theirrepresentatives is making any representation to you regarding the legality of an investment by youunder applicable legal investment or similar laws. You should consult with your own advisors as tolegal, tax, business, financial and related aspects of a purchase of the notes.

Notwithstanding anything in this document to the contrary, except as reasonably necessary tocomply with applicable securities laws, you (and each of your employees, representatives or otheragents) may disclose to any and all persons, without limitation of any kind, the U.S. federal income taxtreatment and tax structure of this offering and all materials of any kind (including opinions or othertax analyses) that are provided to you relating to such tax treatment and tax structure. For this purpose,‘‘tax structure’’ is limited to facts relevant to the U.S. federal income tax treatment of the offering.

INTERNAL REVENUE SERVICE CIRCULAR 230 DISCLOSURE

PURSUANT TO INTERNAL REVENUE SERVICE CIRCULAR 230, WE HEREBY INFORM YOUTHAT THE DESCRIPTION SET FORTH HEREIN WITH RESPECT TO U.S. FEDERAL TAXISSUES WAS NOT INTENDED OR WRITTEN TO BE USED, AND SUCH DESCRIPTION CANNOTBE USED, BY ANY TAXPAYER FOR THE PURPOSE OF AVOIDING ANY PENALTIES THAT MAYBE IMPOSED ON THE TAXPAYER UNDER THE U.S. INTERNAL REVENUE CODE. SUCHDESCRIPTION WAS WRITTEN TO SUPPORT THE MARKETING OF THE NOTES. TAXPAYERSSHOULD SEEK ADVICE BASED ON THE TAXPAYER’S PARTICULAR CIRCUMSTANCES FROMAN INDEPENDENT TAX ADVISOR.

NOTICE TO NEW HAMPSHIRE RESIDENTS

NEITHER THE FACT THAT A REGISTRATION STATEMENT, OR AN APPLICATION FOR ALICENSE HAS BEEN FILED UNDER CHAPTER 421-B WITH THE STATE OF NEW HAMPSHIRENOR THE FACT THAT A SECURITY IS EFFECTIVELY REGISTERED OR A PERSON ISLICENSED IN THE STATE OF NEW HAMPSHIRE CONSTITUTES A FINDING BY THESECRETARY OF STATE OF NEW HAMPSHIRE THAT ANY DOCUMENT FILED UNDER RSA421-B IS TRUE, COMPLETE AND NOT MISLEADING. NEITHER ANY SUCH FACT NOR THEFACT THAT AN EXEMPTION OR EXCEPTION IS AVAILABLE FOR A SECURITY OR ATRANSACTION MEANS THAT THE SECRETARY OF STATE HAS PASSED IN ANY WAY UPONTHE MERITS OR QUALIFICATIONS OF, OR RECOMMENDED OR GIVEN APPROVAL TO, ANYPERSON, SECURITY OR TRANSACTION. IT IS UNLAWFUL TO MAKE, OR CAUSE TO BEMADE, TO ANY PROSPECTIVE PURCHASER, CUSTOMER, OR CLIENT ANY REPRESENTATIONINCONSISTENT WITH THE PROVISIONS OF THIS PARAGRAPH.

The notes will be available initially only in book-entry form. We expect that the notes will beissued in the form of one or more registered global notes. The global notes will be deposited with, oron behalf of, The Depository Trust Company, or DTC, and registered in its name or in the name ofCede & Co., its nominee. Beneficial interests in the global notes will be shown on, and transfers ofbeneficial interests in the global notes will be effected through, records maintained by DTC and itsparticipants. We expect the Regulation S global notes, if any, to be deposited with the trustee, as

iii

custodian for DTC, and beneficial interests in them may be held through the Euroclear System,Clearstream Banking S.A. or other participants. After the initial issuance of the global notes,certificated notes may be issued in registered form, which shall be in minimum denominations ofU.S.$100,000 and integral multiples of U.S.$1,000.

Additional Information

While any notes remain outstanding, we will make available, upon request, to any holder and anyprospective purchaser of notes the information required pursuant to Rule 144(A)(d)(4)(i) under theSecurities Act, during any period in which we are not subject to Section 13 or 15(d) of the SecuritiesExchange Act of 1934, as amended, or the Exchange Act.

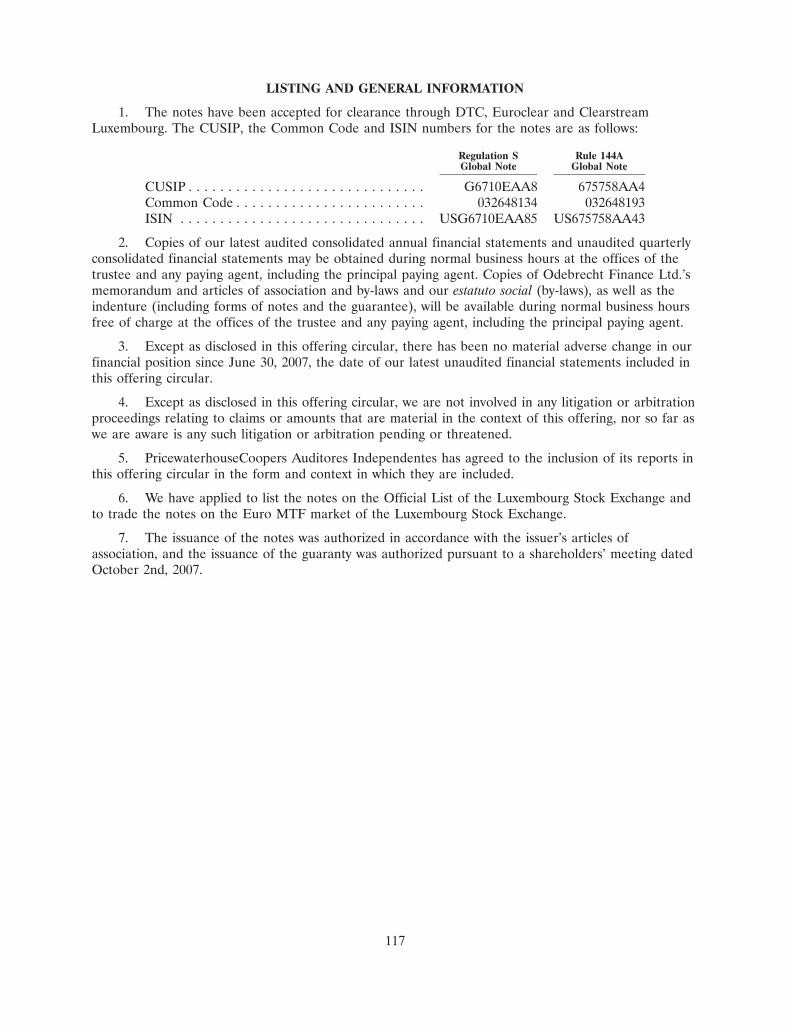

We have applied to list the notes on the Official List of the Luxembourg Stock Exchange and totrade the notes on the Euro MTF market. See ‘‘Listing and General Information.’’ We will comply withany undertakings that we give from time to time to the Luxembourg Stock Exchange in connection withthe notes, and we will furnish to the Luxembourg Stock Exchange all such information required inconnection with the listing of the notes.

iv

ENFORCEMENT OF CIVIL LIABILITIES

Cayman Islands

Odebrecht Finance Ltd. is an exempted limited liability company incorporated under the laws ofthe Cayman Islands. Odebrecht Finance Ltd. has been incorporated in the Cayman Islands because ofcertain benefits associated with being a Cayman Islands company, such as political and economicstability, an effective judicial system, a favorable tax system, the absence of exchange control orcurrency restrictions and the availability of professional and support services.

However, the Cayman Islands has a less developed body of securities laws as compared to theUnited States and certain other jurisdictions and provides significantly lesser protections for investors.All of Odebrecht Finance Ltd.’s directors and officers are nationals and/or residents of countries otherthan the United States, and all or a substantial portion of Odebrecht Finance Ltd.’s or such persons’assets are located outside the United States. As a result, it may be difficult for investors to effectservice of process within the United States upon Odebrecht Finance Ltd. or such persons or to enforceagainst them, judgments obtained in U.S. courts, including judgments predicated upon the civil liabilityprovisions of the securities laws of the United States or any state thereof.

There is no statutory enforcement in the Cayman Islands of judgments obtained in England, NewYork or Brazil. However, the courts of the Cayman Islands will recognize a foreign judgment as thebasis for a claim at common law in the Cayman Islands provided such judgment is rendered by acompetent foreign court, imposes on the judgment debtor a liability to pay a liquidated sum for whichthe judgment has been rendered, is final, is not in respect of taxes, a fine or a penalty and was notobtained in a manner and is not of a kind the enforcement of which is contrary to the public policy ofthe Cayman Islands.

Brazil

We have been advised by Souza, Cescon, Avedissian, Barrieu e Flesch Advogados, Braziliancounsel to the initial purchasers, that a final conclusive judgment of non-Brazilian courts for thepayment of money rendered thereby, subject to certain requirements described below, may be enforcedin Brazil. A judgment against either us or the issuer obtained outside Brazil would be enforceable inBrazil against us or the issuer without reconsideration of the merits, upon confirmation of thatjudgment by the Brazilian Superior Court of Justice (Superior Tribunal de Justica). That confirmation,generally, will occur if the foreign judgment:

• fulfills all formalities required for our enforceability under the laws of the non-Brazilian courts;

• is issued by a competent court after proper service of process on the parties, which service mustcomply with Brazilian law if made in Brazil, or after sufficient evidence of the parties’ absencehas been given, as required by applicable law;

• is not subject to appeal;

• is authenticated by the Brazilian consulate in the location of the non-Brazilian court;

• is translated into Portuguese by a certified translator; and

• does not violate Brazilian public policy, good morals or national sovereignty.

Notwithstanding the foregoing, no assurance can be given that such ratification would be obtained,that the process described above could be conducted in a timely manner or that a Brazilian courtwould enforce a monetary judgment for violation of the U.S. securities laws with respect to the notes.

We have also been advised that civil actions may be brought before Brazilian courts in connectionwith this offering circular based solely on the federal securities laws of the United States and that

v

Brazilian courts may enforce such liabilities in such actions against us (provided that provisions of thefederal securities laws of the United States do not contravene Brazilian public policy, good morals ornational sovereignty). We have been further advised that a plaintiff, whether Brazilian or non-Brazilian,who resides outside Brazil or is outside Brazil during the course of the litigation in Brazil and whodoes not own real property in Brazil must post a bond to guaranty the payment of the defendant’s legalfees and court expenses, except in case of collection claims based on an instrument (which do notinclude the notes issued hereunder) that may be enforced in Brazilian courts without the review of itsmerit (tıtulo executivo extrajudicial) or counterclaims as established under Article 836 of the BrazilianCode of Civil Procedure.

The confirmation process may be time consuming and may also give rise to difficulties in enforcingthe foreign judgment in Brazil. Accordingly, we cannot assure you that confirmation would be obtained,that the confirmation process would be conducted in a timely manner or that a Brazilian court wouldenforce a monetary judgment for violation of the securities laws of countries other than Brazil.

PRESENTATION OF FINANCIAL AND OTHER INFORMATION

All references herein to the ‘‘real,’’ ‘‘reais’’ or ‘‘R$’’ are to the Brazilian real, the official currencyof Brazil. All references to ‘‘U.S. dollars,’’ ‘‘dollars’’ or ‘‘U.S.$’’ are to U.S. dollars.

Solely for the convenience of the reader, we have translated some amounts included in‘‘Summary—Summary Financial and Other Information of CNO,’’ ‘‘Capitalization’’ and elsewhere inthis offering memorandum from reais into U.S. dollars using the selling rate as reported by the CentralBank of Brazil (Banco Central do Brasil), or the Central Bank, at June 30, 2007 of R$1.9262 toU.S.$1.00. These translations should not be considered representations that any such amounts havebeen, could have been or could be converted into U.S. dollars at that or at any other exchange rate.Such translations should not be construed as representations that the real amounts represent or havebeen or could be converted into U.S. dollars as of that or any other date.

Financial Statements

CNO Financial Statements

We maintain our books and records in reais.

We prepare our consolidated financial statements in accordance with accounting practices adoptedin Brazil, or Brazilian GAAP, which are based on:

• Brazilian Law No. 6,404/76, as amended by Brazilian Law No. 9,457/97 and Brazilian LawNo. 10,303/01, which we refer to collectively as the Brazilian Corporation Law;

• the rules and regulations of the Brazilian Securities Commission, (Comissao de ValoresMobiliarios), or the CVM; and

• the accounting standards issued by the Brazilian Institute of Independent Accountants (Institutodos Auditores Independentes do Brasil).

The financial information contained in this offering circular include our consolidated financialstatements as of and for each of the years ended December 31, 2006, 2005 and 2004, which have beenaudited by our independent accountants, as stated in their report included elsewhere in this offeringcircular. Our unaudited consolidated financial statements as of and for the six-month periods endedJune 30, 2007 and 2006 are also included elsewhere in this offering circular.

The audit reports of our independent accountants in respect of our financial statements include anexplanatory paragraph regarding our relationships and transactions with related parties and the

vi

organizational restructuring in progress and an explanatory paragraph regarding the translation of thefinancial statements to U.S. dollars.

Brazilian GAAP differs in significant respects from accounting principles generally accepted in theUnited States, or U.S. GAAP. For a discussion of the significant differences relating to these financialstatements, see ‘‘Appendix A—Summary of Principal Differences Between Brazilian GAAP and U.S.GAAP.’’

Odebrecht Finance Ltd. Financial Statements

We have not included any financial statements for the issuer in this offering circular. OdebrechtFinance Ltd. was incorporated on January 30, 2007 and therefore does not have any historical financialstatements. Odebrecht Finance Ltd. will not publish financial statements, except for any financialstatements that it may be required to publish under the laws of the Cayman Islands. Currently, theissuer is not required by Cayman Islands law to publish any financial statements and does not intend topublish any financial statements. In addition, the issuer does not intend to furnish to the trustee or theholders of the notes any financial statements of, or other reports relating to, the issuer. The issuer willnot have any operations other than those related to its issuance of the notes. The issuer’s obligationsunder the notes are fully, unconditionally and irrevocably guaranteed by us.

Rounding

We have made rounding adjustments to reach some of the figures included in this offering circular.As a result, numerical figures shown as totals in some tables may not be an arithmetic aggregation ofthe figures that preceded them.

Market Share and Other Information

We make statements in this offering circular about our market share in the construction industry inBrazil and elsewhere. We have made these statements on the basis of information obtained from thirdparty sources that we believe are reliable. We derive information regarding our competitive position inthe construction industry and other information from Valor, a Brazilian newspaper, McGraw-HillConstruction Engineering News-Record, or ENR, a leading construction industry web site, and otherthird party sources and reports that we believe are reasonably reliable. Although we have no reason tobelieve that any of this information is inaccurate in any material respect, neither we nor the initialpurchasers have independently verified the construction capacity, market share, market size or similardata provided by third parties or derived from industry or general publications.

The issuer and/or the guarantor take(s) the responsibility for the correct reproduction/extraction ofthe information.

In this offering circular, all references to:

• ‘‘km’’ are to kilometers; and

• ‘‘MW’’ are to megawatts. Megawatts are units of power with one megawatt being equal to onemillion watts.

vii

FORWARD-LOOKING STATEMENTS

This offering circular contains forward-looking statements. Statements that are predictive in nature,that depend upon or refer to future events or conditions or that include words such as ‘‘expects,’’‘‘anticipates,’’ ‘‘intends,’’ ‘‘plans,’’ ‘‘believes,’’ ‘‘estimates’’ and similar expressions are forward-lookingstatements. Although we believe that these statements are based upon reasonable assumptions, they aresubject to several risks and uncertainties and are made in light of information currently available to us.

Our forward-looking statements may be influenced by factors, including the following:

• general economic, political and business conditions in the markets in which we operate, bothwithin Brazil and outside Brazil, including the level of spending for infrastructure projects of thetype that we perform and the ability of our clients to timely pay any amounts that they owe tous;

• the level of financing made available to us by the Brazilian government and by multilateralfinancial institutions for projects that we undertake;

• negotiations of claims with clients of cost and schedule variances and change orders on majorprojects;

• non-performance, default or bankruptcy of clients, joint-venture partners, key suppliers,subcontractors or financing sources;

• performance of fixed-price and other projects, where a failure to meet schedules, cost estimatesor performance targets on a timely basis could result in reduced profit margins or losses;

• interest rate fluctuations, inflation and devaluation or appreciation of the real in relation to theU.S. dollar (or other currencies in which we receive income);

• the outcome of pending litigation or arbitration proceedings;

• competition;

• our ability to obtain financing upon reasonable interest rates and terms;

• adverse financial developments that could reduce our available cash or lines of credit, or ourinability to provide adequate cash collateral for letters of credit or satisfy any other bondingrequirements from customers;

• a reduction in our credit ratings;

• volatility in the surety bond market relating to the type of projects undertaken by us;

• government regulation in certain of the countries in which we operate, including regulations thatencourage or mandate the hiring of local contractors or that require foreign contractors toemploy specific numbers of citizens of, or purchase specific quantities of supplies from, aparticular jurisdiction;

• compliance with job-safety requirements and environmental laws and regulations;

• unsettled political conditions, consequences of war or other armed conflict, civil unrest, strikes,currency controls and governmental actions in certain of the countries and regions in which weoperate, including Venezuela, Peru, Angola and the Middle East;

• severe weather, natural disasters or other force majeure events that adversely impact our businessand which could cause us to evacuate personnel, curtail our services, reduce productivity or failto deliver materials to jobsites on a timely basis in accordance with contract schedules; and

• other factors identified or discussed under ‘‘Risk Factors.’’

viii

Our forward-looking statements are not guarantees of future performance, and the actual resultsor developments may differ materially from the expectations expressed in the forward-lookingstatements. As for the forward-looking statements that relate to future financial results and otherprojections, actual results will be different due to the inherent uncertainty of estimates, forecasts andprojections. Because of these uncertainties, potential investors should not rely on these forward-lookingstatements.

We undertake no obligation to publicly update any forward-looking statement, whether as a resultof new information, future events or otherwise.

ix

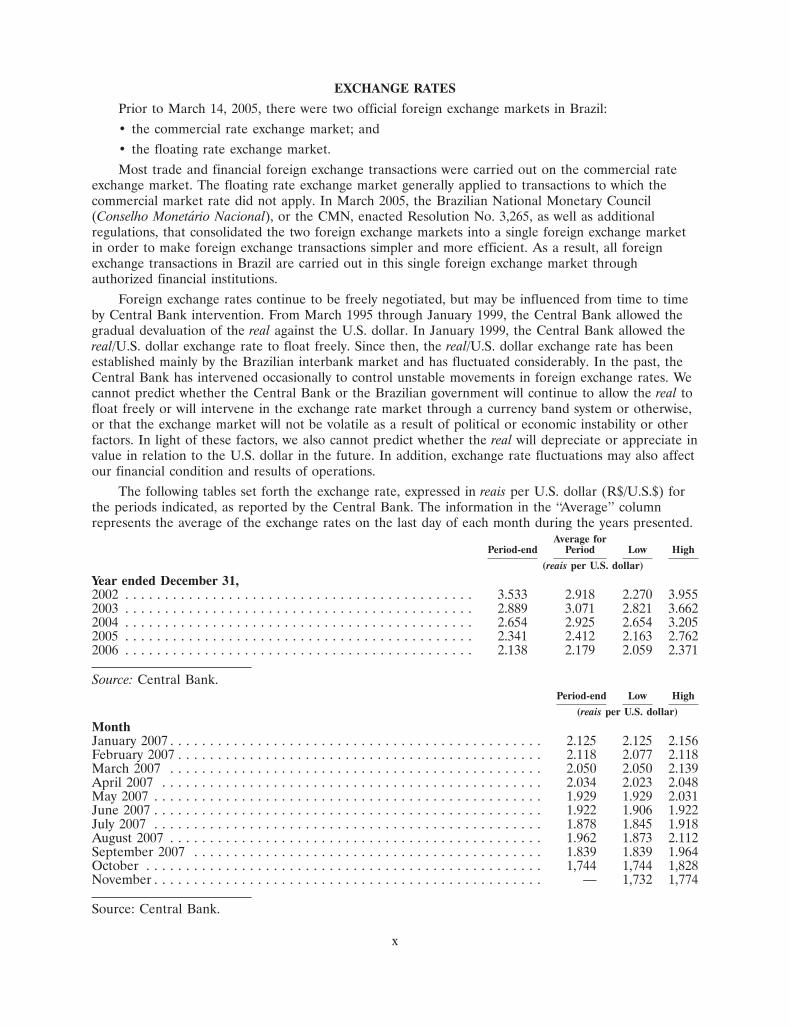

EXCHANGE RATES

Prior to March 14, 2005, there were two official foreign exchange markets in Brazil:

• the commercial rate exchange market; and• the floating rate exchange market.

Most trade and financial foreign exchange transactions were carried out on the commercial rateexchange market. The floating rate exchange market generally applied to transactions to which thecommercial market rate did not apply. In March 2005, the Brazilian National Monetary Council(Conselho Monetario Nacional), or the CMN, enacted Resolution No. 3,265, as well as additionalregulations, that consolidated the two foreign exchange markets into a single foreign exchange marketin order to make foreign exchange transactions simpler and more efficient. As a result, all foreignexchange transactions in Brazil are carried out in this single foreign exchange market throughauthorized financial institutions.

Foreign exchange rates continue to be freely negotiated, but may be influenced from time to timeby Central Bank intervention. From March 1995 through January 1999, the Central Bank allowed thegradual devaluation of the real against the U.S. dollar. In January 1999, the Central Bank allowed thereal/U.S. dollar exchange rate to float freely. Since then, the real/U.S. dollar exchange rate has beenestablished mainly by the Brazilian interbank market and has fluctuated considerably. In the past, theCentral Bank has intervened occasionally to control unstable movements in foreign exchange rates. Wecannot predict whether the Central Bank or the Brazilian government will continue to allow the real tofloat freely or will intervene in the exchange rate market through a currency band system or otherwise,or that the exchange market will not be volatile as a result of political or economic instability or otherfactors. In light of these factors, we also cannot predict whether the real will depreciate or appreciate invalue in relation to the U.S. dollar in the future. In addition, exchange rate fluctuations may also affectour financial condition and results of operations.

The following tables set forth the exchange rate, expressed in reais per U.S. dollar (R$/U.S.$) forthe periods indicated, as reported by the Central Bank. The information in the ‘‘Average’’ columnrepresents the average of the exchange rates on the last day of each month during the years presented.

Average forPeriod-end Period Low High

(reais per U.S. dollar)

Year ended December 31,2002 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 3.533 2.918 2.270 3.9552003 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 2.889 3.071 2.821 3.6622004 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 2.654 2.925 2.654 3.2052005 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 2.341 2.412 2.163 2.7622006 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 2.138 2.179 2.059 2.371

Source: Central Bank.Period-end Low High

(reais per U.S. dollar)

MonthJanuary 2007 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 2.125 2.125 2.156February 2007 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 2.118 2.077 2.118March 2007 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 2.050 2.050 2.139April 2007 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 2.034 2.023 2.048May 2007 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1.929 1.929 2.031June 2007 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1.922 1.906 1.922July 2007 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1.878 1.845 1.918August 2007 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1.962 1.873 2.112September 2007 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1.839 1.839 1.964October . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1,744 1,744 1,828November . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . — 1,732 1,774

Source: Central Bank.

x

SUMMARY

This summary highlights information presented in greater detail elsewhere in this offering circular. Thissummary is not complete and does not contain all the information you should consider before investing inthe notes. You should carefully read this entire offering circular before investing, including ‘‘Risk Factors’’and our financial statements. See ‘‘Presentation of Financial and Other Information’’ for informationregarding our financial statements, exchange rates and other matters.

Overview

We are the largest engineering and construction company in Latin America as measured by 2006gross revenues. We engage in the construction of large-scale infrastructure and other projects, includingthe construction of highways, railways, power plants, bridges, tunnels, subways, buildings, port facilities,dams, manufacturing and processing plants, as well as mining and industrial facilities. We provide avariety of integrated engineering, procurement and construction services to clients in a broad range ofindustries, both in Brazil and internationally. These capabilities enable us to provide clients, individuallyor as part of a consortium, with single-source, turnkey project responsibility for complex constructionprojects. We concentrate our construction activities on infrastructure projects in Brazil and in severalinternational markets, principally in Latin America and Angola, which include projects sponsored bythe public and private-sector, including concession-based projects.

We undertake projects throughout Brazil, other Latin American countries (such as Venezuela andPeru), the United States, Portugal and other countries in Africa and in the Middle East. We haveparticipated in the construction of over 176km of bridges, over 52,500 MW of hydroelectric powerplants, approximately 280 km of tunnels, over 11,200 km of roads and over 147 km of subway lines. In2006, we reported gross services and sales revenue of R$7.5 billion (U.S.$3.9 billion) and EBITDA ofR$550.1 million (U.S.$285.6 million).

We believe we are:

• The largest engineering and construction company in Latin America as measured by our grossrevenues in 2006;

• The largest exporter of services in Brazil with R$4.8 billion (U.S.$2.5 billion), or 65% of ourgross services and sales revenue in 2006, coming from outside Brazil;

• The world’s largest international builder of hydroelectric power plants, sanitary and stormsewers, water treatment plants and transmission lines and aqueducts, according to ENR asmeasured by our gross revenues in 2006;

• The world’s second largest international builder of water supply systems and the third largestinternational builder of bridges, according to ENR as measured by our gross revenues in 2006;and

• The world’s sixth largest international builder of highways, mass transit and rail, also accordingto ENR as measured our gross revenues in 2006.

Our Competitive Strengths

We believe that our main competitive strengths include the following:

Leadership Position

We are the largest engineering and construction company in Latin America as measured by 2006gross revenues. Our geographic diversification, extensive operations and leading market share in Brazilenables us to capitalize on opportunities as they arise. We are owned by the Odebrecht Group, which is

1

one of the 10 largest Brazilian-owned private sector conglomerates based on gross sales revenue in2006. The Odebrecht Group is also the controlling shareholder of Braskem S.A., or Braskem, thelargest petrochemical company in Latin America, based on average annual production capacity in 2006,and one of the six largest Brazilian-owned private sector industrial companies based on net salesrevenue in 2006. We are able to take advantage of important synergies between us and our affiliates,such as constructing facilites for Braskem in the Brazilian states of Bahia and Alagoas.

Financial Strength

We believe that our financial performance has been consistent, enabling us to rely primarily on ourcash flow from operations to grow our business. Our EBITDA margins (EBITDA as a percentage ofour net sales and services revenue) for the last three fiscal years ended December 31, 2006 were 7.2%,7.3% and 7.6%, respectively. We are focused on maintaining the relatively strong financial position wehave compared to our Brazilian competitors.

Diversification

We have expanded our business internationally in order to broaden our client base and diversifythe risk inherent in relying heavily on the Brazilian market, as well as to increase our revenuedenominated in dollars and other currencies. At June 30, 2007, we had 135 on-going projects: Brazil(75); Angola (23); Venezuela (9); Peru (6); Portugal (5); the Dominican Republic (4); the United States(3); Ecuador (2); Panama (2); Mexico (2); the Middle East (2); Argentina (1); and Bolivia (1).

The percentage of our gross service revenue derived from international projects increased fromapproximately 30% in 1992 to approximately 67% for the six-month period ended June 30, 2007. Ourdiversification provides us with revenue growth opportunities, while adequately managing our exposureto market and other risks.

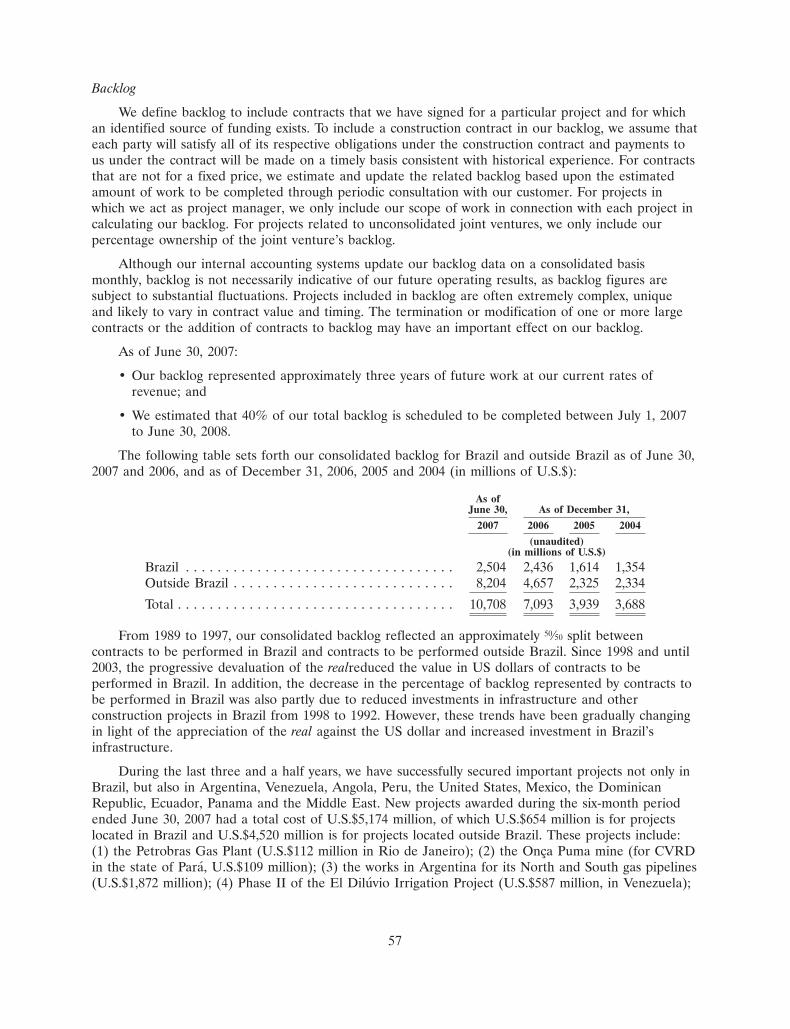

Strong and Diversfied Backlog

We define backlog to include contracts that we have signed for a particular project and for whichan identified source of funding exists but have not recognized as revenue. As of June 30, 2007, (1) ourbacklog represented approximately U.S.$10.7 billion or three years of future work and (2) we estimatethat 40% of our total backlog is scheduled to be completed between July 1, 2007 to June 30, 2008. Ourbacklog includes a diversified portfolio of engineering and construction projects among variousinfrastructure sectors, different types of construction works and numerous countries. This diversificationenables us to manage political risks associated with specific economic sectors and countries or regions.

Experienced and Professional Management Team with Strong Entrepeneurial Culture

Our management team has considerable industry experience and knowledge. We provide ourmanagement with ongoing training throughout their careers, and maintain a results-oriented corporateculture, with clear visions and responsibilities. We have decentralized the negotiation andadministration of each of our project contracts. An experienced on-site project manager is responsiblefor administering the implementation of each project contract in accordance with the project’s budget.Each of our project managers and other on-site employees is compensated based upon meetingdesignated project milestones and financial targets, which motivate them to meet their project budgets.We believe that planned delegation and decentralized decision-making enable us to better understandand satisfy our clients’ needs.

2

Our Strategy

We intend to focus on continuing to achieve steady growth and to build our competitive strengthsin order to maintain and increase our leadership in Brazil and selected other international engineeringand construction markets. The principal components of our strategy are:

Managing Political Risk

We have operated for more than two decades in many countries that have significant levels ofpolitical risk. We are currently active in Angola, Argentina, Bolivia, Brazil, the Dominican Republic,Ecuador, Panama, Peru, the Middle East and the United States. In addition, we are seeking furtheropportunities in the Middle East and North Africa (including Libya) and in certain other countries inwhich significant levels of political risk exist. For example, we have established an office in the UnitedArab Emirates and have completed the construction of a port facility in the Republic of Djibouti ineastern Africa for a client located in the United Arab Emirates, and we have just started anotherproject for this client in this port in Djibouti. We attribute our success in countries with significantlevels of political risk to the following competitive strengths:

• In countries in which we operate with significant political risk concerns, such as Latin Americancountries and Angola, we usually bid on and perform projects that are funded under Braziliantrade credit or multilateral agency credit facilities. The Brazilian government offers exportfinancing for construction and engineering services related to projects undertaken in many ofthese countries, which we rely upon as an important source of funding for our projects locatedin these countries, together with support from multilateral financial institutions, includingCorporacion Andina de Fomento, or CAF, and the Interamerican Development Bank, or theIDB. Our management believes that the higher margins we are able to earn from projects inthese countries compensate us for the political risks that we may be subject to as a result.

• We attempt to mitigate political risk through our experience and knowledge of the local marketsin which we are active and by entering into joint ventures with local companies and using localsubcontractors, suppliers and labor. By establishing partnerships with local companies andemploying local subcontractors, suppliers and labor, we attempt to integrate our operations intothe communities in which we operate.

• We generally establish long-term operations in countries in which we are active and seekappropriate project opportunities that meet our rigorous risk management criteria. Ourlong-term presence in countries such as Peru (28 years), Angola (23 years), Ecuador (21 years)and Venezuela (15 years), including during periods of social unrest or war, and our involvementin high visibility projects that are important to a country’s economy and development haveearned us goodwill with the governments of these countries. Accordingly, while otherconstruction companies avoid operating in certain of the countries in which we are active, ourmanagement believes that our extensive experience in these countries, our diversification andour extensive contractual risk assessment and risk sharing with other project participants allowsus to effectively manage the political risks presented by construction projects in these countries.In addition, to help cover certain risks, we have a comprehensive portfolio of insurance policies.

• Our strategy involves concentrating our business into more profitable markets and projects.When our management no longer believes that a particular market continues to meet ourlong-term objectives, we act to close or phase out our operations in these markets. In the 1990s,for example, we closed offices in the United Kingdom, Germany and South Africa andsubstantially reduced our operations in Colombia.

3

Enhancing Human Resources

We will continue to focus on recruiting and retaining motivated and knowledgeable employees. Webelieve that our continued growth and financial success is directly related to the experience of ourconstruction and engineering project managers, as well as our ability to attract and train our otheremployees to develop the skills necessary to manage and execute future projects.

Pursuing International Opportunities

We are the market leader for engineering and construction projects in Brazil, Angola and certainother countries in Latin America and will continue to pursue business opportunities and strategicalliances in selected projects that will improve our market share and competitiveness. We intend toleverage our experience to broaden our presence in selective international markets and to pursue anddevelop growth opportunities in these markets.

Focusing on Complex Large-Scale Construction Opportunities and Concession Projects

We seek to continue to focus on large-scale infrastructure and other complex, tailor-madeconstruction projects in Brazil. We believe there will be significant opportunities in the coming years forus in the Brazilian power, oil, transportation, water supply, sanitation and other infrastructure sectors.We believe that our domestic market knowledge, human and material resources, size, experience andexpertise enable us to continue to compete effectively for large and complex projects in Brazil. Inaddition to infrastructure projects in Brazil, we intend to concentrate our construction activities onconcession-based projects, principally in Latin America.

Offering Our Customers Differentiated Services

We will continue to seek to differentiate our company from our competitors through our capacityto offer our clients a complete range of services in the markets where we operate. Our capabilitiesencompass not only construction expertise and innovations that help to reduce completion time andimprove cost and quality controls but also extend to our substantial experience in arranging financingfor many of our engineering and construction projects.

Company History

We were founded in 1944 and commenced our operations in the northeastern region of Brazil,where we were active in the construction of industrial plants, warehouses, small dams, highways,buildings and canals. In 1970, we began to expand our operations into southern Brazil, concentratinginitially in Rio de Janeiro with the construction of the headquarters of Petrobras in 1970; Brazil’s firstnuclear power plant, the Central Nuclear de Angra dos Reis in 1971; the Rio de Janeiro internationalairport in 1971; and the Rio de Janeiro State University in 1972. In Peru, we won the contract for theconstruction of the Charcani Hydroelectric Plant in 1979. In the early 1980s, we began to expand ourwork in projects located outside Brazil. In 1984, we began the construction of the CapandaHydroelectric Project on Angola’s Kwanza river, and in 1991 we started the construction of thesouthern extension of the Metromover, part of Miami’s urban mass transportation system. In 1996, theOdebrecht Group reorganized its holdings into two principal business areas: (1) engineering andconstruction through our company; and (2) chemicals and petrochemicals through Braskem S.A. In2004, we began operations in the Middle East, completing two projects in Iraq with the United StatesArmy Corps of Engineers with a total cost of U.S.$86 million.

4

Recent Developments

Because our management intends to continue to focus on the engineering and constructionbusiness, we are currently undergoing a corporate reorganization involving the transfer of certain assetsand equity interests in our infrastructure, oil and gas and real estate businesses to other companieswithin the Odebrecht Group, which are or will become subsidiaries of Odebrecht S.A., or Odebrecht.As part of this ongoing corporate restructuring, the following two Brazilian limited liability companieshave been established as subsidiaries of Odebrecht: (1) Odebrecht Investimentos em Infra-estrutura Ltda., or OII, which has been focusing on investments in the infrastructure sector; and(2) Odebrecht Oleo e Gas Ltda., or OOG, which has been focusing on investments in the oil and gasindustry. In addition, we anticipate that Odebrecht Empreendimentos Imobiliarios Ltda., or OEI, ourcurrent subsidiary that focuses on investments in the real estate industry, will become a subsidiary ofOdebrecht S.A. prior to the end of 2008. See ‘‘Business—Corporate Reorganization.’’

On August 9, 2007, Odebrecht Overseas Limited, or OOL, successfully concluded a cash ‘‘exit’’tender offer and consent solicitation relating to its U.S.$150.0 million 11.50% notes due 2009, whichnotes were issued under the medium-term note program. OOL received tenders and consents in respectof U.S.$116,056,000 in aggregate principal amount of notes, representing approximately 77.37% of theaggregate principal amount of the outstanding medium-term notes, not including notes then-held byOOL or its affiliates. Out of this total, U.S.$107,475,000 of notes were tendered (with a ‘‘deemedconsent’’ for certain proposed amendments) and U.S.$8,581,000 remained as noteholders but agreed toconsent to these amendments. The notes were amended to conform the covenants and events of defaultof these notes to the respective covenants and events of default set forth in OOL’s outstanding 9.625%U.S.$200.0 million perpetual notes.

Principal Shareholders

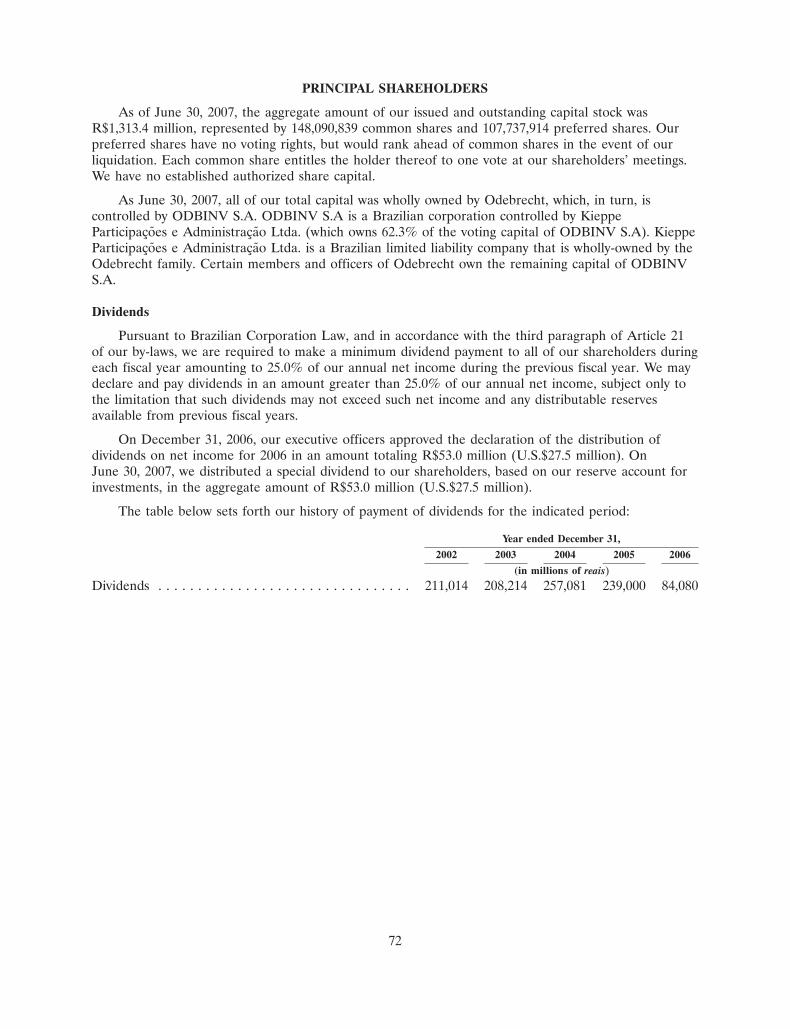

CNO

As of June 30, 2007, the aggregate amount of our issued and outstanding capital stock wasR$1,313.4 million, represented by 148,090,839 common shares and 107,737,914 preferred shares. Ourpreferred shares have no voting rights, but would rank ahead of our common shares in the event of ourliquidation. Each common share entitles the holder thereof to one vote at our shareholders’ meetings.We have no established authorized share capital.

As of June 30, 2007, 100% of our share capital was owned by Odebrecht, which, in turn, iscontrolled by ODBINV S.A. ODBINV S.A. is a Brazilian corporation that is controlled by KieppeParticipacoes e Administracao Ltda. (which owns 62.3% of the voting capital of ODBINV S.A). KieppeParticipacoes e Administracao Ltda. is a Brazilian limited liability company that is wholly-owned by theOdebrecht family. Certain shareholders and officers of Odebrecht own the remaining capital ofODBINV S.A. that is not owned by the Odebrecht family.

5

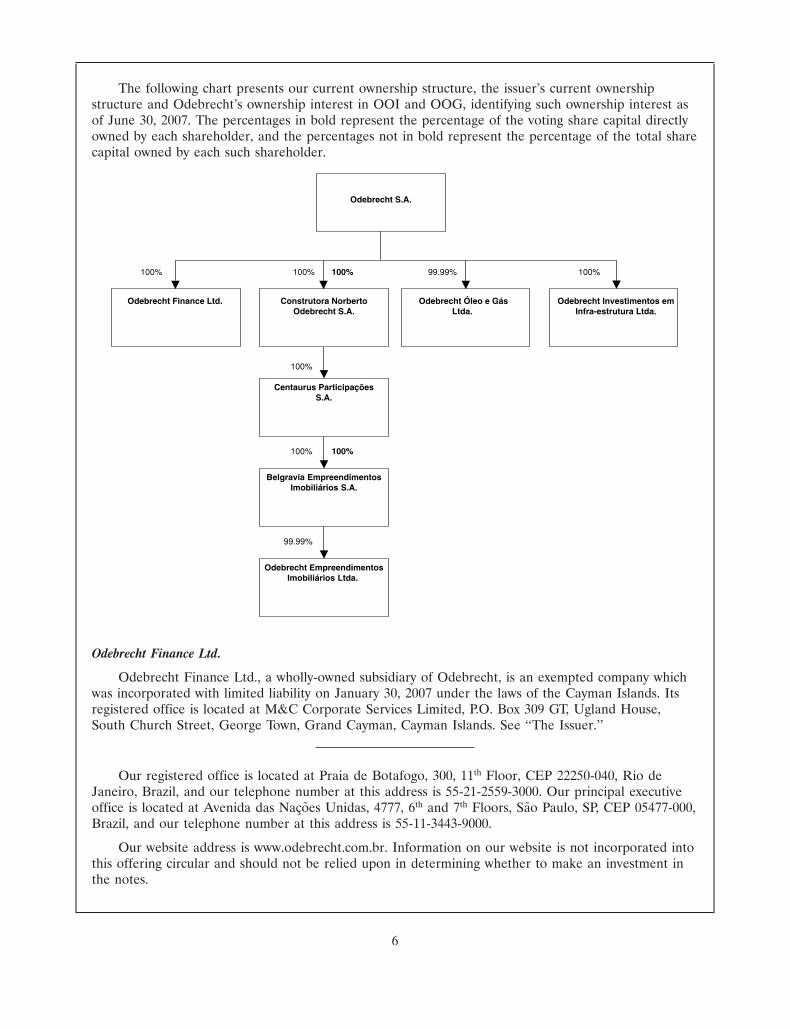

24OCT200722220830

The following chart presents our current ownership structure, the issuer’s current ownershipstructure and Odebrecht’s ownership interest in OOI and OOG, identifying such ownership interest asof June 30, 2007. The percentages in bold represent the percentage of the voting share capital directlyowned by each shareholder, and the percentages not in bold represent the percentage of the total sharecapital owned by each such shareholder.

100% 100%

Odebrecht S.A.

100%

Odebrecht Finance Ltd. Construtora NorbertoOdebrecht S.A.

99.99% 100%

Odebrecht Óleo e GásLtda.

Odebrecht Investimentos emInfra-estrutura Ltda.

100%

Centaurus ParticipaçõesS.A.

100% 100%

Belgravia EmpreendimentosImobiliários S.A.

99.99%

Odebrecht EmpreendimentosImobiliários Ltda.

Odebrecht Finance Ltd.

Odebrecht Finance Ltd., a wholly-owned subsidiary of Odebrecht, is an exempted company whichwas incorporated with limited liability on January 30, 2007 under the laws of the Cayman Islands. Itsregistered office is located at M&C Corporate Services Limited, P.O. Box 309 GT, Ugland House,South Church Street, George Town, Grand Cayman, Cayman Islands. See ‘‘The Issuer.’’

Our registered office is located at Praia de Botafogo, 300, 11th Floor, CEP 22250-040, Rio deJaneiro, Brazil, and our telephone number at this address is 55-21-2559-3000. Our principal executiveoffice is located at Avenida das Nacoes Unidas, 4777, 6th and 7th Floors, Sao Paulo, SP, CEP 05477-000,Brazil, and our telephone number at this address is 55-11-3443-9000.

Our website address is www.odebrecht.com.br. Information on our website is not incorporated intothis offering circular and should not be relied upon in determining whether to make an investment inthe notes.

6

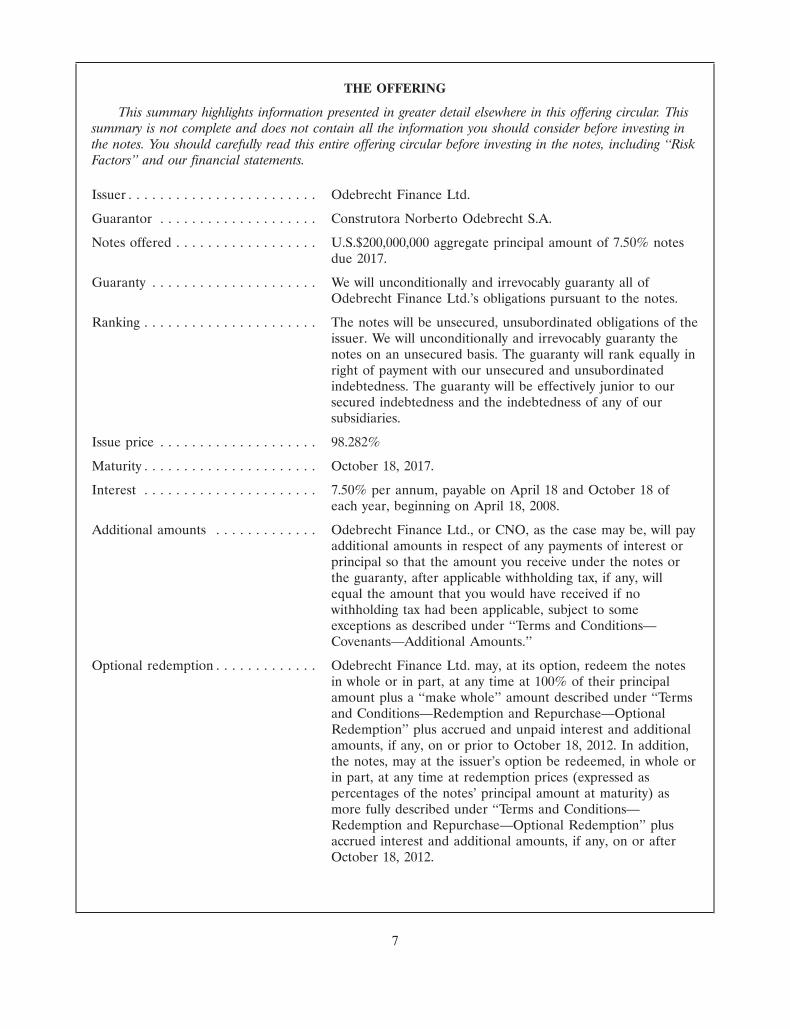

THE OFFERING

This summary highlights information presented in greater detail elsewhere in this offering circular. Thissummary is not complete and does not contain all the information you should consider before investing inthe notes. You should carefully read this entire offering circular before investing in the notes, including ‘‘RiskFactors’’ and our financial statements.

Issuer . . . . . . . . . . . . . . . . . . . . . . . . Odebrecht Finance Ltd.

Guarantor . . . . . . . . . . . . . . . . . . . . Construtora Norberto Odebrecht S.A.

Notes offered . . . . . . . . . . . . . . . . . . U.S.$200,000,000 aggregate principal amount of 7.50% notesdue 2017.

Guaranty . . . . . . . . . . . . . . . . . . . . . We will unconditionally and irrevocably guaranty all ofOdebrecht Finance Ltd.’s obligations pursuant to the notes.

Ranking . . . . . . . . . . . . . . . . . . . . . . The notes will be unsecured, unsubordinated obligations of theissuer. We will unconditionally and irrevocably guaranty thenotes on an unsecured basis. The guaranty will rank equally inright of payment with our unsecured and unsubordinatedindebtedness. The guaranty will be effectively junior to oursecured indebtedness and the indebtedness of any of oursubsidiaries.

Issue price . . . . . . . . . . . . . . . . . . . . 98.282%

Maturity . . . . . . . . . . . . . . . . . . . . . . October 18, 2017.

Interest . . . . . . . . . . . . . . . . . . . . . . 7.50% per annum, payable on April 18 and October 18 ofeach year, beginning on April 18, 2008.

Additional amounts . . . . . . . . . . . . . Odebrecht Finance Ltd., or CNO, as the case may be, will payadditional amounts in respect of any payments of interest orprincipal so that the amount you receive under the notes orthe guaranty, after applicable withholding tax, if any, willequal the amount that you would have received if nowithholding tax had been applicable, subject to someexceptions as described under ‘‘Terms and Conditions—Covenants—Additional Amounts.’’

Optional redemption . . . . . . . . . . . . . Odebrecht Finance Ltd. may, at its option, redeem the notesin whole or in part, at any time at 100% of their principalamount plus a ‘‘make whole’’ amount described under ‘‘Termsand Conditions—Redemption and Repurchase—OptionalRedemption’’ plus accrued and unpaid interest and additionalamounts, if any, on or prior to October 18, 2012. In addition,the notes, may at the issuer’s option be redeemed, in whole orin part, at any time at redemption prices (expressed aspercentages of the notes’ principal amount at maturity) asmore fully described under ‘‘Terms and Conditions—Redemption and Repurchase—Optional Redemption’’ plusaccrued interest and additional amounts, if any, on or afterOctober 18, 2012.

7

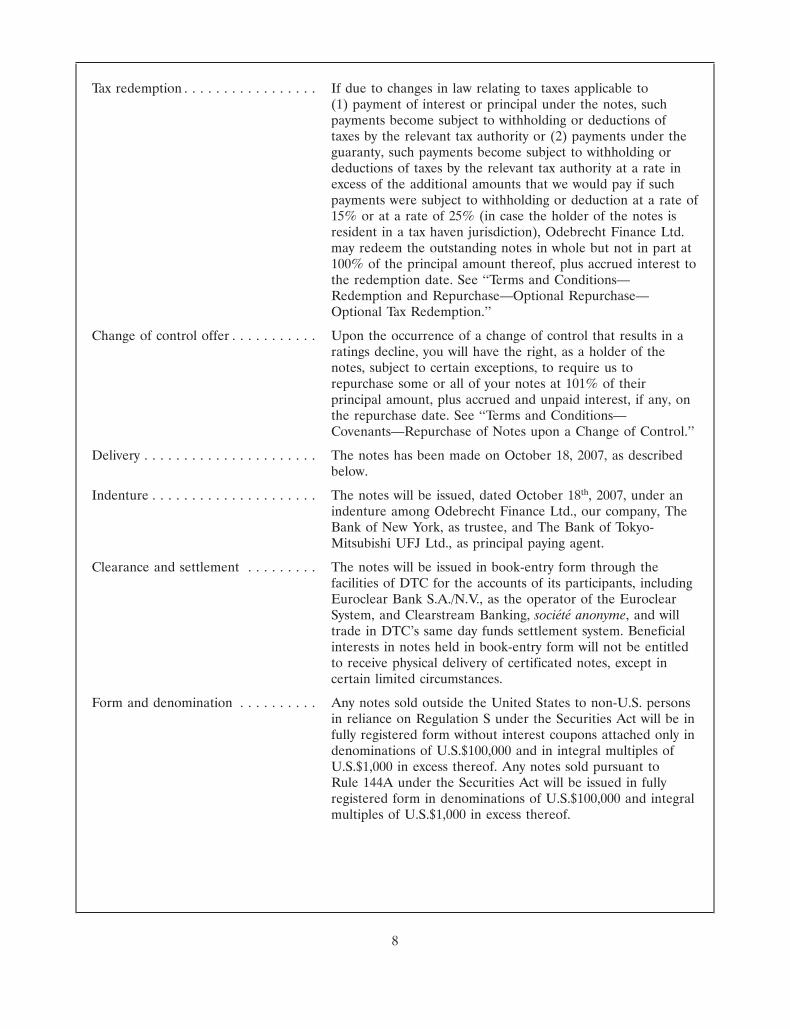

Tax redemption . . . . . . . . . . . . . . . . . If due to changes in law relating to taxes applicable to(1) payment of interest or principal under the notes, suchpayments become subject to withholding or deductions oftaxes by the relevant tax authority or (2) payments under theguaranty, such payments become subject to withholding ordeductions of taxes by the relevant tax authority at a rate inexcess of the additional amounts that we would pay if suchpayments were subject to withholding or deduction at a rate of15% or at a rate of 25% (in case the holder of the notes isresident in a tax haven jurisdiction), Odebrecht Finance Ltd.may redeem the outstanding notes in whole but not in part at100% of the principal amount thereof, plus accrued interest tothe redemption date. See ‘‘Terms and Conditions—Redemption and Repurchase—Optional Repurchase—Optional Tax Redemption.’’

Change of control offer . . . . . . . . . . . Upon the occurrence of a change of control that results in aratings decline, you will have the right, as a holder of thenotes, subject to certain exceptions, to require us torepurchase some or all of your notes at 101% of theirprincipal amount, plus accrued and unpaid interest, if any, onthe repurchase date. See ‘‘Terms and Conditions—Covenants—Repurchase of Notes upon a Change of Control.’’

Delivery . . . . . . . . . . . . . . . . . . . . . . The notes has been made on October 18, 2007, as describedbelow.

Indenture . . . . . . . . . . . . . . . . . . . . . The notes will be issued, dated October 18th, 2007, under anindenture among Odebrecht Finance Ltd., our company, TheBank of New York, as trustee, and The Bank of Tokyo-Mitsubishi UFJ Ltd., as principal paying agent.

Clearance and settlement . . . . . . . . . The notes will be issued in book-entry form through thefacilities of DTC for the accounts of its participants, includingEuroclear Bank S.A./N.V., as the operator of the EuroclearSystem, and Clearstream Banking, societe anonyme, and willtrade in DTC’s same day funds settlement system. Beneficialinterests in notes held in book-entry form will not be entitledto receive physical delivery of certificated notes, except incertain limited circumstances.

Form and denomination . . . . . . . . . . Any notes sold outside the United States to non-U.S. personsin reliance on Regulation S under the Securities Act will be infully registered form without interest coupons attached only indenominations of U.S.$100,000 and in integral multiples ofU.S.$1,000 in excess thereof. Any notes sold pursuant toRule 144A under the Securities Act will be issued in fullyregistered form in denominations of U.S.$100,000 and integralmultiples of U.S.$1,000 in excess thereof.

8

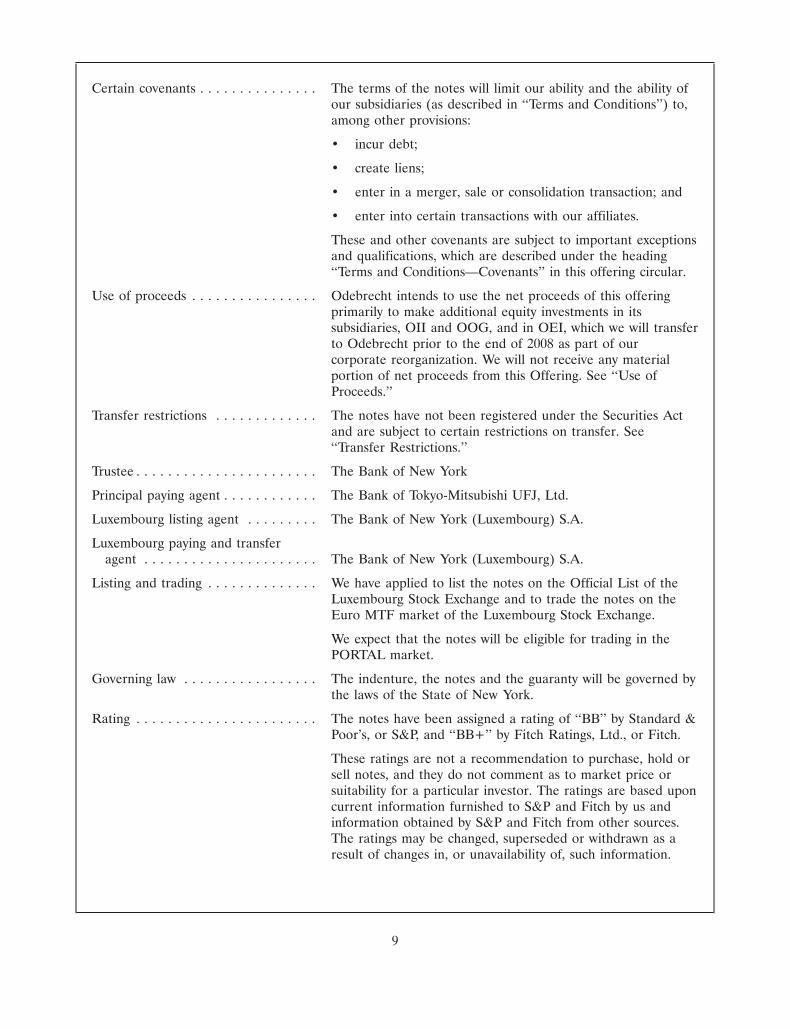

Certain covenants . . . . . . . . . . . . . . . The terms of the notes will limit our ability and the ability ofour subsidiaries (as described in ‘‘Terms and Conditions’’) to,among other provisions:

• incur debt;

• create liens;

• enter in a merger, sale or consolidation transaction; and

• enter into certain transactions with our affiliates.

These and other covenants are subject to important exceptionsand qualifications, which are described under the heading‘‘Terms and Conditions—Covenants’’ in this offering circular.

Use of proceeds . . . . . . . . . . . . . . . . Odebrecht intends to use the net proceeds of this offeringprimarily to make additional equity investments in itssubsidiaries, OII and OOG, and in OEI, which we will transferto Odebrecht prior to the end of 2008 as part of ourcorporate reorganization. We will not receive any materialportion of net proceeds from this Offering. See ‘‘Use ofProceeds.’’

Transfer restrictions . . . . . . . . . . . . . The notes have not been registered under the Securities Actand are subject to certain restrictions on transfer. See‘‘Transfer Restrictions.’’

Trustee . . . . . . . . . . . . . . . . . . . . . . . The Bank of New York

Principal paying agent . . . . . . . . . . . . The Bank of Tokyo-Mitsubishi UFJ, Ltd.

Luxembourg listing agent . . . . . . . . . The Bank of New York (Luxembourg) S.A.

Luxembourg paying and transferagent . . . . . . . . . . . . . . . . . . . . . . The Bank of New York (Luxembourg) S.A.

Listing and trading . . . . . . . . . . . . . . We have applied to list the notes on the Official List of theLuxembourg Stock Exchange and to trade the notes on theEuro MTF market of the Luxembourg Stock Exchange.

We expect that the notes will be eligible for trading in thePORTAL market.

Governing law . . . . . . . . . . . . . . . . . The indenture, the notes and the guaranty will be governed bythe laws of the State of New York.

Rating . . . . . . . . . . . . . . . . . . . . . . . The notes have been assigned a rating of ‘‘BB’’ by Standard &Poor’s, or S&P, and ‘‘BB+’’ by Fitch Ratings, Ltd., or Fitch.

These ratings are not a recommendation to purchase, hold orsell notes, and they do not comment as to market price orsuitability for a particular investor. The ratings are based uponcurrent information furnished to S&P and Fitch by us andinformation obtained by S&P and Fitch from other sources.The ratings may be changed, superseded or withdrawn as aresult of changes in, or unavailability of, such information.

9

Selling restrictions . . . . . . . . . . . . . . There are restrictions on persons to whom notes can be sold,and on the distribution of this offering circular, as described in‘‘Plan of Distribution.’’

Risk factors . . . . . . . . . . . . . . . . . . . Prospective investors should carefully consider all of theinformation contained in this offering circular prior toinvesting in the notes. In particular, we urge prospectiveinvestors to carefully consider the information set forth under‘‘Risk Factors’’ for a discussion of risks and uncertaintiesrelating to us, our subsidiaries, our business, our equityholders and an investment in the notes.

10

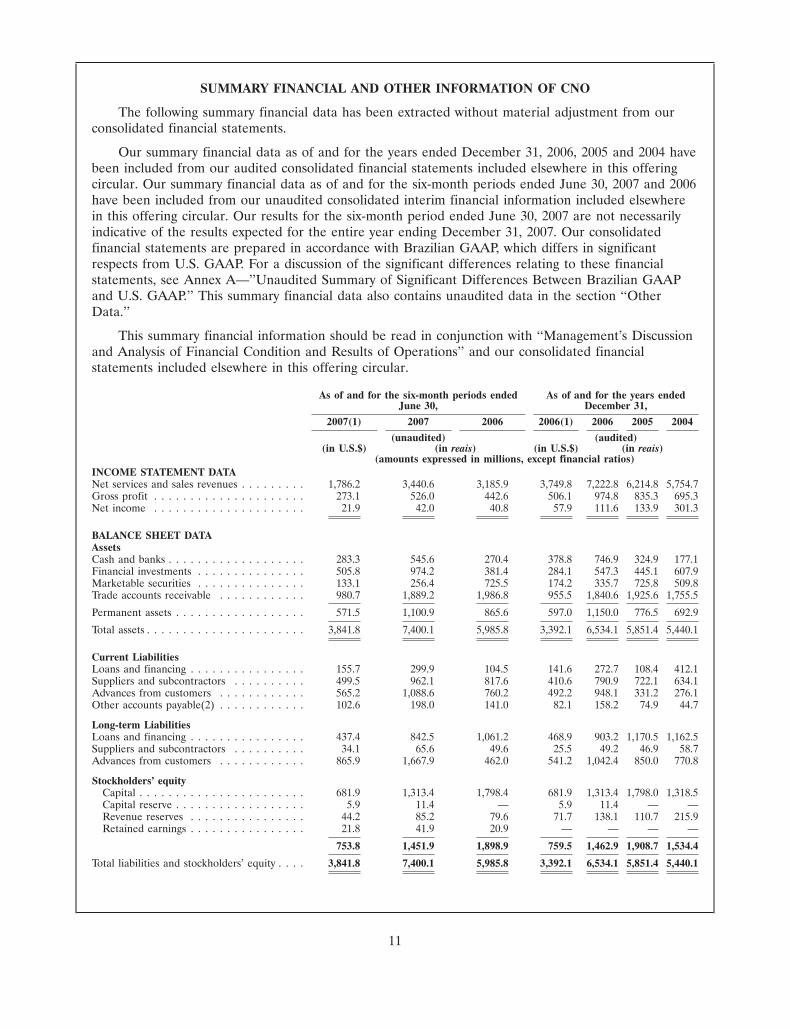

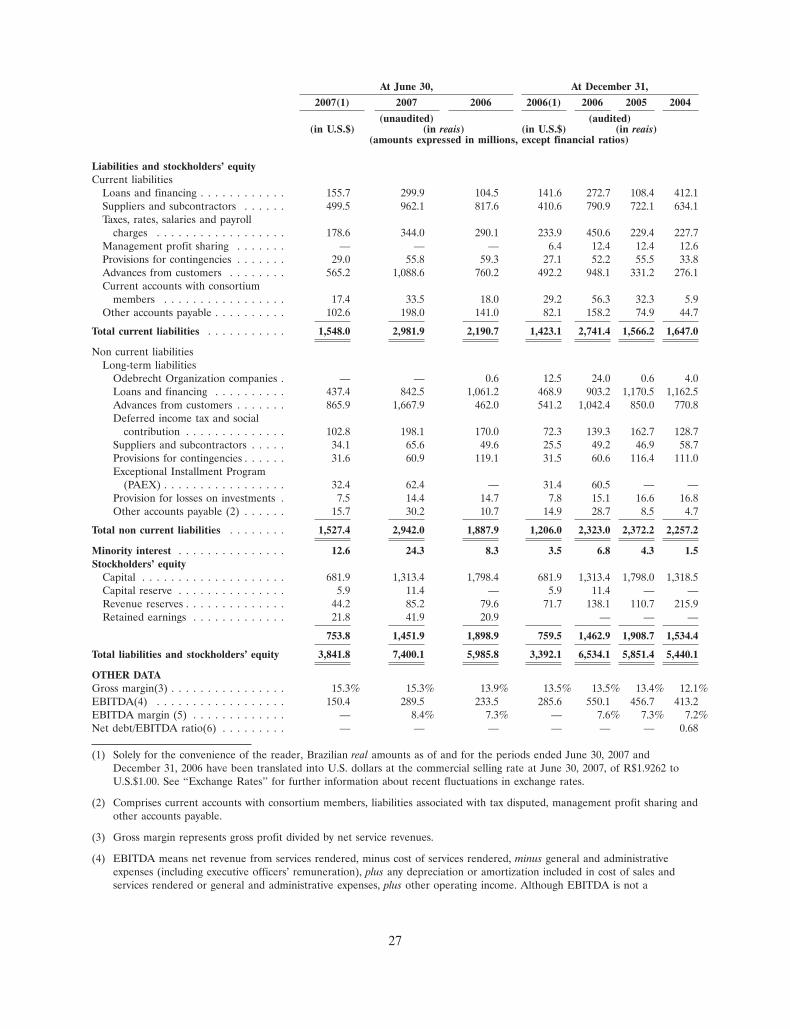

SUMMARY FINANCIAL AND OTHER INFORMATION OF CNO

The following summary financial data has been extracted without material adjustment from ourconsolidated financial statements.

Our summary financial data as of and for the years ended December 31, 2006, 2005 and 2004 havebeen included from our audited consolidated financial statements included elsewhere in this offeringcircular. Our summary financial data as of and for the six-month periods ended June 30, 2007 and 2006have been included from our unaudited consolidated interim financial information included elsewherein this offering circular. Our results for the six-month period ended June 30, 2007 are not necessarilyindicative of the results expected for the entire year ending December 31, 2007. Our consolidatedfinancial statements are prepared in accordance with Brazilian GAAP, which differs in significantrespects from U.S. GAAP. For a discussion of the significant differences relating to these financialstatements, see Annex A—’’Unaudited Summary of Significant Differences Between Brazilian GAAPand U.S. GAAP.’’ This summary financial data also contains unaudited data in the section ‘‘OtherData.’’

This summary financial information should be read in conjunction with ‘‘Management’s Discussionand Analysis of Financial Condition and Results of Operations’’ and our consolidated financialstatements included elsewhere in this offering circular.

As of and for the six-month periods ended As of and for the years endedJune 30, December 31,

2007(1) 2007 2006 2006(1) 2006 2005 2004

(unaudited) (audited)(in U.S.$) (in reais) (in U.S.$) (in reais)

(amounts expressed in millions, except financial ratios)INCOME STATEMENT DATANet services and sales revenues . . . . . . . . . 1,786.2 3,440.6 3,185.9 3,749.8 7,222.8 6,214.8 5,754.7Gross profit . . . . . . . . . . . . . . . . . . . . . 273.1 526.0 442.6 506.1 974.8 835.3 695.3Net income . . . . . . . . . . . . . . . . . . . . . 21.9 42.0 40.8 57.9 111.6 133.9 301.3

BALANCE SHEET DATAAssetsCash and banks . . . . . . . . . . . . . . . . . . . 283.3 545.6 270.4 378.8 746.9 324.9 177.1Financial investments . . . . . . . . . . . . . . . 505.8 974.2 381.4 284.1 547.3 445.1 607.9Marketable securities . . . . . . . . . . . . . . . 133.1 256.4 725.5 174.2 335.7 725.8 509.8Trade accounts receivable . . . . . . . . . . . . 980.7 1,889.2 1,986.8 955.5 1,840.6 1,925.6 1,755.5

Permanent assets . . . . . . . . . . . . . . . . . . 571.5 1,100.9 865.6 597.0 1,150.0 776.5 692.9

Total assets . . . . . . . . . . . . . . . . . . . . . . 3,841.8 7,400.1 5,985.8 3,392.1 6,534.1 5,851.4 5,440.1

Current LiabilitiesLoans and financing . . . . . . . . . . . . . . . . 155.7 299.9 104.5 141.6 272.7 108.4 412.1Suppliers and subcontractors . . . . . . . . . . 499.5 962.1 817.6 410.6 790.9 722.1 634.1Advances from customers . . . . . . . . . . . . 565.2 1,088.6 760.2 492.2 948.1 331.2 276.1Other accounts payable(2) . . . . . . . . . . . . 102.6 198.0 141.0 82.1 158.2 74.9 44.7

Long-term LiabilitiesLoans and financing . . . . . . . . . . . . . . . . 437.4 842.5 1,061.2 468.9 903.2 1,170.5 1,162.5Suppliers and subcontractors . . . . . . . . . . 34.1 65.6 49.6 25.5 49.2 46.9 58.7Advances from customers . . . . . . . . . . . . 865.9 1,667.9 462.0 541.2 1,042.4 850.0 770.8

Stockholders’ equityCapital . . . . . . . . . . . . . . . . . . . . . . . 681.9 1,313.4 1,798.4 681.9 1,313.4 1,798.0 1,318.5Capital reserve . . . . . . . . . . . . . . . . . . 5.9 11.4 — 5.9 11.4 — —Revenue reserves . . . . . . . . . . . . . . . . 44.2 85.2 79.6 71.7 138.1 110.7 215.9Retained earnings . . . . . . . . . . . . . . . . 21.8 41.9 20.9 — — — —

753.8 1,451.9 1,898.9 759.5 1,462.9 1,908.7 1,534.4

Total liabilities and stockholders’ equity . . . . 3,841.8 7,400.1 5,985.8 3,392.1 6,534.1 5,851.4 5,440.1

11

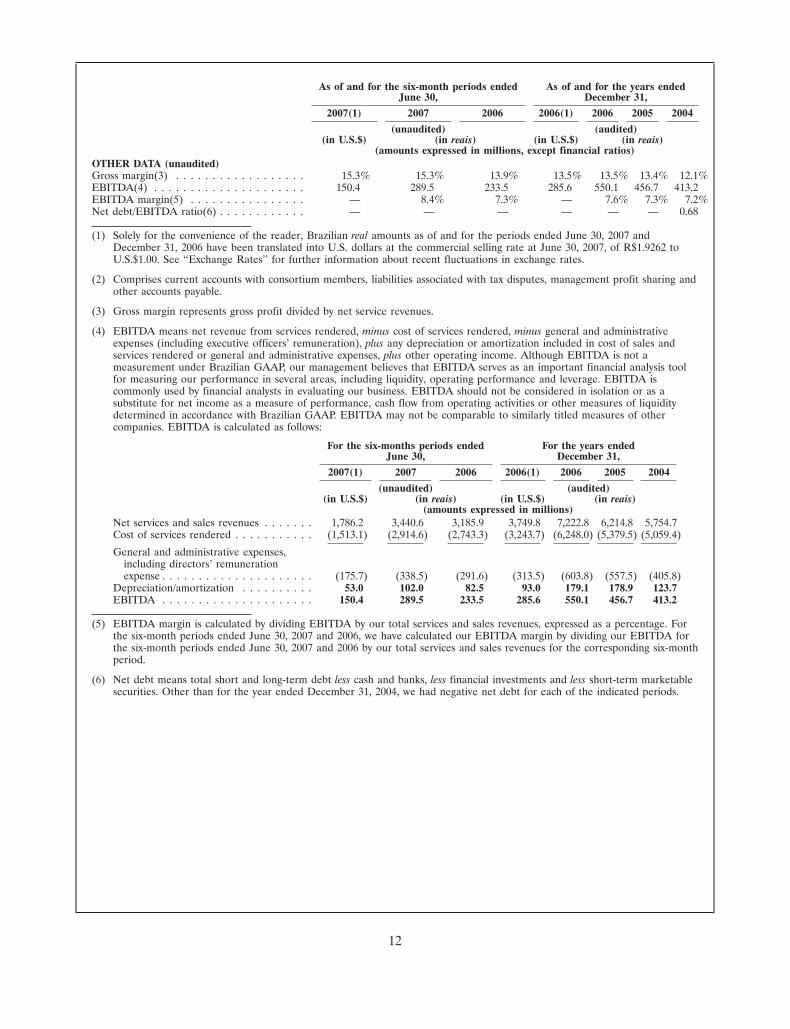

As of and for the six-month periods ended As of and for the years endedJune 30, December 31,

2007(1) 2007 2006 2006(1) 2006 2005 2004

(unaudited) (audited)(in U.S.$) (in reais) (in U.S.$) (in reais)

(amounts expressed in millions, except financial ratios)OTHER DATA (unaudited)Gross margin(3) . . . . . . . . . . . . . . . . . . 15.3% 15.3% 13.9% 13.5% 13.5% 13.4% 12.1%EBITDA(4) . . . . . . . . . . . . . . . . . . . . . 150.4 289.5 233.5 285.6 550.1 456.7 413.2EBITDA margin(5) . . . . . . . . . . . . . . . . — 8.4% 7.3% — 7.6% 7.3% 7.2%Net debt/EBITDA ratio(6) . . . . . . . . . . . . — — — — — — 0.68

(1) Solely for the convenience of the reader, Brazilian real amounts as of and for the periods ended June 30, 2007 andDecember 31, 2006 have been translated into U.S. dollars at the commercial selling rate at June 30, 2007, of R$1.9262 toU.S.$1.00. See ‘‘Exchange Rates’’ for further information about recent fluctuations in exchange rates.

(2) Comprises current accounts with consortium members, liabilities associated with tax disputes, management profit sharing andother accounts payable.

(3) Gross margin represents gross profit divided by net service revenues.

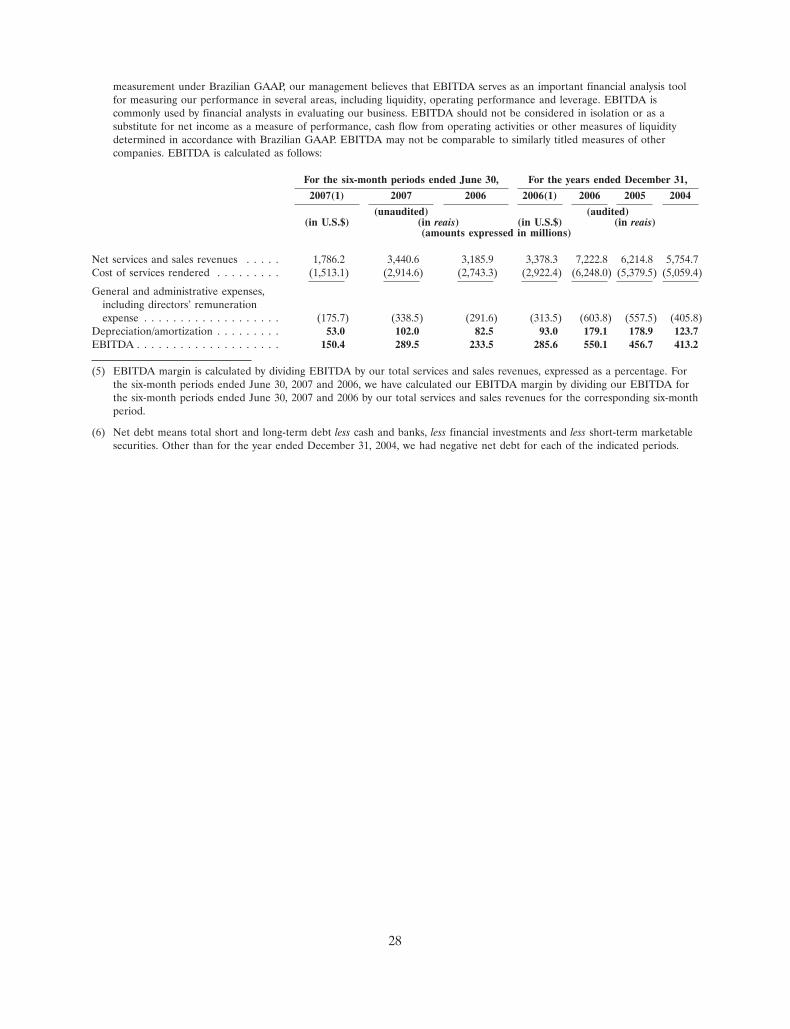

(4) EBITDA means net revenue from services rendered, minus cost of services rendered, minus general and administrativeexpenses (including executive officers’ remuneration), plus any depreciation or amortization included in cost of sales andservices rendered or general and administrative expenses, plus other operating income. Although EBITDA is not ameasurement under Brazilian GAAP, our management believes that EBITDA serves as an important financial analysis toolfor measuring our performance in several areas, including liquidity, operating performance and leverage. EBITDA iscommonly used by financial analysts in evaluating our business. EBITDA should not be considered in isolation or as asubstitute for net income as a measure of performance, cash flow from operating activities or other measures of liquiditydetermined in accordance with Brazilian GAAP. EBITDA may not be comparable to similarly titled measures of othercompanies. EBITDA is calculated as follows:

For the six-months periods ended For the years endedJune 30, December 31,

2007(1) 2007 2006 2006(1) 2006 2005 2004

(unaudited) (audited)(in U.S.$) (in reais) (in U.S.$) (in reais)

(amounts expressed in millions)Net services and sales revenues . . . . . . . 1,786.2 3,440.6 3,185.9 3,749.8 7,222.8 6,214.8 5,754.7Cost of services rendered . . . . . . . . . . . (1,513.1) (2,914.6) (2,743.3) (3,243.7) (6,248.0) (5,379.5) (5,059.4)

General and administrative expenses,including directors’ remunerationexpense . . . . . . . . . . . . . . . . . . . . . (175.7) (338.5) (291.6) (313.5) (603.8) (557.5) (405.8)

Depreciation/amortization . . . . . . . . . . 53.0 102.0 82.5 93.0 179.1 178.9 123.7EBITDA . . . . . . . . . . . . . . . . . . . . . 150.4 289.5 233.5 285.6 550.1 456.7 413.2

(5) EBITDA margin is calculated by dividing EBITDA by our total services and sales revenues, expressed as a percentage. Forthe six-month periods ended June 30, 2007 and 2006, we have calculated our EBITDA margin by dividing our EBITDA forthe six-month periods ended June 30, 2007 and 2006 by our total services and sales revenues for the corresponding six-monthperiod.

(6) Net debt means total short and long-term debt less cash and banks, less financial investments and less short-term marketablesecurities. Other than for the year ended December 31, 2004, we had negative net debt for each of the indicated periods.

12

RISK FACTORS

Prospective purchasers of notes should carefully consider the risks described below, as well as the otherinformation in this offering circular, before deciding to purchase any notes. Our business, results ofoperations, financial condition or prospects could be negatively affected if any of these risks occurs, and asa result, the trading price of the notes could decline and you could lose all or part of your investment.

Risks Relating to the Issuer

The issuer’s ability to make payments on the notes depends on its receipt of payments from us.

The issuer’s principal business activity is to act as a financing vehicle for Odebrecht’s activities andoperations. The issuer has no substantial assets. Holders of the notes must rely on our operations topay amounts due in connection with the notes. The ability of the issuer to make payments of principal,interest and any other amounts due on the notes is contingent on its receipt from us of amountssufficient to make these payments, and, in turn, on our ability to make these payments. In the eventthat we are unable to make such payments for any reason, the issuer will not have sufficient resourcesto satisfy its obligations under the indenture governing the notes.

Risks Relating to Our Company

International and political events may adversely affect our operations.

A significant portion of our revenue is derived from construction projects undertaken in Brazil andcertain other emerging market economies, including other countries in Latin America, the Middle Eastand Angola, which exposes us to significant risks inherent in operating in these economies. These risksinclude:

• expropriation and nationalization of our assets in a particular jurisdiction or related to a specificproject;

• political and economic instability;

• social unrest, acts of terrorism, force majeure, war or other armed conflict;

• inflation;

• currency fluctuations, devaluations and conversion restrictions;

• confiscatory taxation or other adverse tax policies;

• government activities that limit or disrupt markets, restrict payments or limit the receipt ortransfer of funds; and

• government activities that may result in the indirect deprivation of rights.

Many of the countries in which we operate have significant levels of political risk, includingAngola, the Dominican Republic, Ecuador, Peru and Venezuela. For example, civil disturbances inAngola periodically interrupted the construction of the Capanda Hydroelectric Project in Angola fromSeptember 1992 through the first half of 1998 and again in 1999. In addition, we are seekingopportunities in the Middle East and elsewhere in which there are significant levels of political andoperational risks.

A significant portion of our services are contracted on a fixed-price basis, subjecting us to risks, including costover-runs and operating cost inflation.

We contract to provide services principally on a ‘‘unit price’’ basis or on a fixed-price basis, withboth unit price and fixed-price (or lump sum) contracts accounting for approximately 95.0% of our

13

gross revenues during the six-month period ended June 30, 2007 and 93.0% of our gross revenues for2006. With fixed-price contracts, we bear the risk of unanticipated increases in the cost of equipment,materials or manpower due to inflation or unforeseen events, such as difficulties in obtaining adequatefinancing or required governmental permits or approvals, project modifications creating unanticipatedcosts or delays caused by local weather conditions (or other natural phenomena) or suppliers’ orsubcontractors’ failure to perform. In addition, we sometime bear the risk of delays caused byunexpected conditions or events, subject to the protection of standard force majeure provisions andinsurance policies contracted for a project. Our failure to estimate accurately the resources and timerequired to complete a particular fixed-price project, or our inability to complete our contractualobligations (or applicable milestones) within the contracted time frame, could have a material adverseeffect on our business, results of operations and financial condition.

Decreases in governmental spending and capital spending by our customers may materially adversely affect us.

Our business is directly affected by changes in governmental and private-sector spending andfinancing for infrastructure projects and by variations in capital expenditures by our customers.Accordingly, reductions in available governmental and private-sector spending and financing forinfrastructure projects may have a material adverse impact on our results of operations and financialcondition. Economic downturns generally lead to decreases in the number of new projects awarded, aswell as delays or cancellations of major projects awarded (but not commenced), which could have amaterial adverse effect on our business, results of operations and financial condition.

Decrease in availability of Brazilian governmental and multilateral financial institution funding may adverselyaffect us.

Many of our construction projects are financed by the Brazilian government and by multilateralfinancial institutions. A decrease in the level of financing available from the Brazilian government forservice exports or from multilateral financial institutions for infrastructure projects in the marketswhere we are active may materially and adversely affect our results of operations and financialcondition.

Delays in receipt of payment for public sector projects may materially adversely affect us.

We contract to provide services principally on a ‘‘unit price’’ basis or on a fixed-price basis, withboth unit price and fixed-price (or lump sum) contracts accounting for approximately 93% of our grossrevenues for 2006.