Constructing More Effective Defined Contribution ... · T. Rowe PR ice Constructing More Effective...

12

Retirement Insights EXECUTIVE SUMMARY According to recent research, only 15% of plan sponsors say most of their employees will be financially prepared for retirement. 1 is concern is prompting an increased focus on construction of investment lineups as a way to encourage participants to make sound saving and investing decisions. As plan sponsors evaluate their lineups, consideration should be given to fiduciary and regulatory issues, culture and employee demographics, and recent research and industry trends. is paper summarizes each of these topics. e paper also presents several best practice considerations relating to the various asset classes. e goal is twofold: (1) to help plan sponsors better understand each asset class in the context of defined contribution (DC) plans and (2) to suggest practices that may help participants avoid asset allocation mistakes, while also helping sponsors manage regulatory and fiduciary issues. Plan sponsors may want to use the questionnaire “Assessing a Current Lineup” on page 9 as a primer for a more thorough evaluation to improve investment lineups. T. ROWE PRICE Constructing More Effective Defined Contribution Investment Lineups Best Practice Considerations for Plan Sponsors By Joseph Martel, CFA, T. Rowe Price Defined Contribution Investment Specialist 1 401(k) Benchmarking Survey, 2010 Edition, Deloitte. CONTENTS What’s Driving Today’s DC Investment Lineup Decisions? ........................................... 2 Best Practice Considerations .................................................................................. 4 Appendix: Assessing a Current Lineup ............................................................................. 9 Understanding U.S. Equity Markets .................................................................... 10

Transcript of Constructing More Effective Defined Contribution ... · T. Rowe PR ice Constructing More Effective...

Retirement Insights

E x E c u t i v E S u m m a r y

According to recent research, only 15% of plan sponsors say most of their employees will be financially prepared for retirement.1 This concern is prompting an increased focus on construction of investment lineups as a way to encourage participants to make sound saving and investing decisions.

As plan sponsors evaluate their lineups, consideration should be given to fiduciary and regulatory issues, culture and employee demographics, and recent research and industry trends. This paper summarizes each of these topics.

The paper also presents several best practice considerations relating to the various asset classes. The goal is twofold: (1) to help plan sponsors better understand each asset class in the context of defined contribution (DC) plans and (2) to suggest practices that may help participants avoid asset allocation mistakes, while also helping sponsors manage regulatory and fiduciary issues.

Plan sponsors may want to use the questionnaire “Assessing a Current Lineup” on page 9 as a primer for a more thorough evaluation to improve investment lineups.

T. R o w e P R i c e

Constructing More Effective Defined Contribution Investment LineupsBest Practice Considerations for Plan SponsorsBy Joseph Martel, CFA, T. Rowe Price Defined Contribution Investment Specialist

1401(k) Benchmarking Survey, 2010 Edition, Deloitte.

CONTENTS

What’s Driving Today’s DC Investment Lineup Decisions? ........................................... 2

Best Practice Considerations .................................................................................. 4

Appendix:

Assessing a Current Lineup ............................................................................. 9

Understanding U.S. Equity Markets .................................................................... 10

2 T. R o w e P R i c e R e T i R e M e N T i N s i g h T s2 T. R o w e P R i c e R e T i R e M e N T i N s i g h T s

What’s Driving Today’s DC Investment Lineup Decisions?Early defined contribution (DC) plans were simple—generally consisting of a stable value or money market option, one fixed income (bond) option, and one or two equity (stock) options. As the DC industry grew, plans added sub-asset classes such as international and emerging market equities, high yield bonds, and small- and mid-cap equities—and some went further by dividing these into growth and value styles.

The goal was to provide a variety of choices to better diversify or to pursue tactical strategies. This is good in theory, but may not be so good in reality. Research shows that when confronted with too many choices, employees often make no decision, or they split their assets evenly across several options. Or worse, they may chase the latest high-performing options.2

Today, plan sponsors are facing important decisions about how to construct lineups to best serve the interests of their particular employee populations while also addressing fiduciary concerns.

REGULATORY AND F IDUC IARY I SSUES : A Ma jo r Fac to r In L ineup Cons t ruc t i on

Of all the considerations for plan lineup design, perhaps none is more important to plan sponsors than regulatory and fiduciary issues. For example, if a plan allows participants to direct their own investments, the plan may be exposed to liability for account losses resulting from a participant’s own investment choices. A plan sponsor may want to seek some protection by following the guidelines of Section 404(c) of the Employee Retirement Income Security Act of 1974 (ERISA). Among other requirements, a plan must satisfy the following to comply with 404(c):

1. Offer at least three different, internally diversified investment options with materially different risk and return characteristics.

2. Allow participants to transfer assets among the options as often as appropriate given the market volatility of the options.

3. Provide access to sufficient information to make informed investment decisions.

Offering a QDIA may relieve some concernsUnder the Pension Protection Act, fiduciaries are provided certain protections if they default participants into a qualified default investment alternative (QDIA). If plan sponsors wish to receive this limited protection, they should consider offering an investment option that qualifies as a QDIA according to the Department of Labor. Common QDIAs include balanced funds, target-date funds, and managed accounts.3

Every investment option comes with monitoring obligationsBeing fiduciaries, plan sponsors are tasked with selecting and monitoring the investment options available under the plan.

The greater the number and scope of investment offerings, the greater the resources needed to monitor them. This is particularly true with more esoteric asset classes, which can be more difficult to monitor due to their complexity. These monitoring obligations should be kept in mind when deciding the number and types of investment options offered in a plan.

CULTURE AND EMPLOYEE DEMOGRAPHICS : Know These Be fo re Mak ing L ineup Changes

Plan sponsors should have a clear understanding of their plan’s objective when determining its investment lineup. Each of the following factors plays a role in determining objectives.

Demographics influence number and variety of optionsDemographic factors such as age, wealth, and level of education are all factors that often determine a participant’s level of investment knowledge or ability to access or purchase outside sources of investment knowledge and expertise. For plans with participants who lack knowledge or access to appropriate information, sponsors may consider either providing additional education and guidance or limiting the number and variety of investment options.

Lack of DB plan may affect participants’ ability to take riskIf an employer does not offer a defined benefit (DB) plan or it is closed to new participants, the DC plan must serve as the primary source of retirement income for many of the participants. This could limit many participants’ ability to take risks and argues for caution when adding variety to the lineup.

2 Sheena S. Iyengar, Wei Jiang, and Gur Huberman, “How Much Choice is Too Much? Contributions to 401(k) Retirement Plans,” in Pension Design and Structure, edited by Olivia Mitchell and Stephen Utkus, Oxford University Press, 2004.

3 A managed account is an investment account that is owned by an individual investor and looked after by a hired professional money manager. In contrast to mutual funds (which are professionally managed on behalf of many mutual fund holders), managed accounts are personalized investment portfolios tailored to the specific needs of the account holder. Source: Investopedia.com.

3

On the other hand, when a DB plan serves as the primary source of retirement income, participants, in theory, have greater ability to take risks in the DC plan. In this case, the plan sponsor may want to offer a larger number and wider variety of equity options.

Is the company “paternalistic” or “individualistic?” Whether an employer promotes a paternalistic or individualistic culture often determines how limited or how expansive plan sponsors choose to make a plan’s investment lineup. Paternalistic employers may choose to limit the number of options to help avoid overwhelming employees with too many options. On the other hand, individualistic employers believe participants should not be restricted in their investment choices and may tend to offer greater choice and variety.

RESEARCH AND INDUSTRY TRENDS : Behav io ra l F inance Takes A Lead ing Ro le

A great deal of research in the field of behavioral finance continues to be conducted on participant behavior and should be considered when evaluating investment lineups.

Many participants misunderstand risk and return Participants often exhibit “myopic loss aversion,” meaning they are overly conservative and focused on the short term due to a fear of losses.4 Others are overly confident and trade in and out of “hot” asset classes, believing they can generate superior returns.5

Reducing the number of sub-asset class options may help eliminate these inappropriate behavioral problems...

Such potential behavior should be considered by plan sponsors as they evaluate and revise investment lineups. Reducing the number of sub-asset class options may help eliminate these inappropriate behavioral problems while simplifying the management of the plan.

Too many choices, unwanted consequencesRecent findings show that higher numbers of investment choices may reduce participation rates or encourage participants to simply choose the safest option, which may not always be in their best interest. In addition, studies have shown that some participants tend to over-allocate to certain asset classes when more than one choice in the category is offered.6 Plan sponsors are responding by limiting the number of choices and by offering options such as target-date or balanced funds that allow participants to diversify their retirement savings without having to select individual funds that invest in specific asset classes.

Diversification doesn’t come easy According to research by behavioral finance researchers Shlomo Benartzi and Richard Thaler, many engage in what is referred to as “naive diversification,” where they allocate assets evenly across each of the investment offerings in the plan.7 Depending on the number and type of offerings in a plan, this can lead to overly concentrated portfolios or ones with a great deal of overlap in similar assets and securities.

Revising the investment lineup may be the most effective actionOf all the tools available to help plan sponsors deal with these behavioral issues, perhaps the simplest and most cost-effective is a revision of the investment lineup. By streamlining the choices and eliminating asset class overlaps, a plan sponsor can significantly reduce confusion for employees and consequently improve participation and savings rates while helping them make more appropriate allocation decisions.

4 Benartzi, Shlomo, and Richard Thaler, “Risk Aversion or Myopia? Choices in Repeated Gambles and Retirement Investments,” Management Science, Vol. 45, No. 3, pp. 364-381, 1999.

5 Liersch, Michael, “Choice in Retirement Plans: How participant behavior differs in plans offering advice, managed accounts, and target-date investments,” 2011.

6 Ibid.

7 Benartzi, Shlomo, and Richard Thaler, “Heuristics and Biases in Retirement Savings Behavior,” Journal of Economic Perspectives, Summer 2007, Vol. 21.3.

4 T. R o w e P R i c e R e T i R e M e N T i N s i g h T s

Best Practice ConsiderationsGiven the issues discussed in the preceding sections, plan sponsors may want to consider using a “building block” approach to lineup construction. Start with target-date options and a limited number of core options, and then add a brokerage window if the plan wants to provide access to additional options. The goal of the core options block is to provide a sufficient number of choices to enable participants to construct a well-diversified portfolio while limiting overlap and unintended risk taking.

B u i l d i n g B l o c k A p p r o a c h

Target-Date Options Core Options Brokerage Window

The cornerstone of the plan, providing access to professional management for asset allocation and diversification decisions.

Stable Value/Money Market Provides additional choices for a typically small subpopulation of truly self-directed investors.Fixed Income

U.S. Equity

International Equity

When evaluating the following best practice considerations, keep in mind that no two plans are exactly alike. Employee demographics and sponsor needs vary, and circumstances change over time.

1 . OFFER TARGET-DATE OPT IONS .

Target-date investment options can help satisfy the needs of participants who prefer not to make their own investment decisions. They allow participants access to diversified portfolios in which professional managers make strategic and tactical asset allocation decisions. They also provide broad diversification and periodic rebalancing. Of course, diversification cannot assure a profit or protect against loss in a declining market.

The asset allocation strategy and underlying investments vary among target-date investment managers, and plan sponsors should be aware of their target-date investment option’s approach.

...many target-date fund managers have been adding allocations to alternative, or nontraditional, asset classes...

Within equities, the majority of target-date investment options have dedicated allocations to U.S. large-, mid-, and small-capitalization stocks, developed international markets, and emerging markets. Within fixed income, most have allocations to U.S. investment-grade bonds, and some have allocations to U.S. high yield and international bonds. Additionally, many target-date investment managers have been adding allocations to alternative, or nontraditional, asset classes, such as real estate, commodities, and Treasury inflation protected securities (TIPS).

Target-date investments offer access to certain investments—emerging markets, real estate, commodities, and TIPS—that may

not be appropriate as stand-alone options in a lineup due to their complexity and volatility. The advantage of gaining exposure to these types of investments via a target-date investment option is that a professional manager makes the allocation decision. Most managers have target allocations that restrict the amount that may be allocated to an asset class. This generally prevents the type of performance chasing and over-allocating to “hot” asset classes that can be seen in participant-directed portfolios.

The principal value of target-date investment options is not guaranteed at any time, including at or after the target date, which is the approximate date when investors plan to retire. These investment options typically invest in a broad range of underlying mutual funds that include stocks, bonds, and short-term investments and are subject to the risks of different areas of the market. In addition, the objectives of target-date investment options typically change over time to become more conservative.

2 . OFFER E I THER A STABLE vALUE OR A MONEY MARKET INvESTMENT OPT ION .

Stable value and money market portfolios are the most conservative options offered in DC plans. Unlike other investment options, money market and stable value portfolios are managed to maintain stable share prices, typically with a net asset value (NAV) of one dollar per share. Their purpose is, primarily, to provide capital preservation and, secondarily, to provide income.

While they share the goal of capital preservation, their underlying investments are different. Money market funds invest in short-term instruments, such as Treasury bills, negotiable certificates of deposit, municipal obligations, and both unsecured and asset-backed commercial paper. They can also encompass more

5

complex instruments, such as repurchase agreements (repos) and dollar-denominated foreign bonds. Stable value funds, on the other hand, typically invest in short- to intermediate-term fixed income securities that are insulated from interest rate movements by contracts from banks and insurance companies. The contracts generally allow price fluctuations in the underlying securities to be amortized over the duration of the contract, helping to stabilize overall returns and maintain an NAV of one dollar per share.

The difference in underlying investments for the two types of funds results in different risk and return profiles. Even though both seek to maintain a stable NAV of one dollar, money market funds are generally considered less risky than stable value funds. This is due to the shorter duration (sensitivity to interest rate changes) of their underlying investments.8 The return difference is primarily driven by the interest rate environment. Both the level and direction of interest rates will affect the return differential. Stable value funds are less interest rate responsive, but their longer duration provides return advantages in low or declining interest rate environments. Money market funds are more interest rate sensitive, allowing them to respond more quickly to changing short-term rates. As shown in the chart below, the return

advantage of stable value funds diminishes in a rising or high interest rate environment.

Plan sponsors should consider offering either a stable value or a money market fund. Since the primary goal of each is capital preservation, there is little to no diversification benefit by offering both options. Offering both could confuse participants and lead to over-allocation to the “stability” asset class.

3 . OFFER A F I xED INCOME OPT ION—A “CORE PLUS” STRATEGY.

The “core” fixed income market is composed of U.S. Treasuries and government-related securities, mortgage-backed securities (MBS), investment-grade corporate bonds, commercial mortgage-backed securities (CMBS), and asset-backed securities (ABS). Core funds are typically benchmarked to the Barclays Capital U.S. Aggregate Index, which includes investment-grade U.S.-denominated bonds in each of these sectors.

Most core fixed income funds employ relative value strategies to identify the cheapest sectors and bottom-up security selection to identify securities within each sector. Other drivers of performance may include duration management (adjusting the portfolio’s

8 A measure of the sensitivity of the price (the value of principal) of a fixed income investment to a change in interest rates. Duration is expressed as a number of years. Rising interest rates mean falling bond prices, while declining interest rates mean rising bond prices. Source: Investopedia.com.

A n n u a l i z e d R e t u r n s

Money Market* Stable Value**8%

Dec-10Dec-09Dec-08Dec-07Dec-06Dec-05Dec-04Dec-03Dec-02Dec-01Dec-00

0%

2%

4%

6%

Please note that an investment in a money market fund is not insured or guaranteed by the FDIC or any other government agency. Although the fund seeks to preserve the value of your investment at $1.00 per share, it is possible to lose money by investing in the fund.*Lipper Money Market Funds Index. Source of Lipper data: Lipper Inc. The returns shown are net of fees.

**Hueler Pooled Fund Universe. Source of Hueler data: Hueler Inc. The Hueler Stable Value Pooled Fund Index (the “Hueler Index”) is an equal-weighted total return across all participating funds in the Hueler Analytics Pooled Fund Comparative Universe (the “Hueler Universe”). The Hueler Universe is provided by Hueler Analytics, a Minnesota-based stable value data and research firm, which has developed the Hueler Universe for use as a comparative database to evaluate collective trust funds and other pooled vehicles with investments in stable value instruments. The Hueler Universe is composed of pooled stable value funds with common investment objectives of stability of principal; the number of participating funds in the Hueler Universe may vary over the different historic periods. Hueler Index rates of return are reported gross of management fees. If performance was shown net of fees, the returns would have been lower.

6 T. R o w e P R i c e R e T i R e M e N T i N s i g h T s

sensitivity to changes in interest rates) and yield-curve positioning (forecasting moves in particular parts of the yield curve).9

In addition to the core sectors described above, the fixed income market includes out-of-benchmark sectors, such as nondollar bonds, leveraged loans, Treasury inflation protected securities (TIPS), emerging markets bonds, and high yield securities. These “plus” sectors are more volatile than “core” sectors and will have periods of extreme over- and underperformance, making them problematic as stand-alone options.

Plan sponsors may want to consider offering just one core plus option that provides broad exposure to domestic bond markets along with select exposure to high yield, nondollar, and emerging markets bonds on an opportunistic basis. There are two primary reasons for this:

n Fixed income markets may be too complex for most participants to make informed allocation decisions among several different sector-specific choices.

n The majority of fixed income managers invest across the entire asset class as opposed to being sector-specific managers. A primary reason for this is that a large portion of the value added by management of fixed income portfolios comes from decisions about allocating to the various fixed income sectors (Treasuries, corporates, etc.).

Just one core-plus fixed income option can give participants broad exposure to all areas of the fixed income market while letting professionals make the allocation decision.

4 . PROv IDE THE FULL OPPORTUNITY SET OF U .S . EqU IT IES , BUT KEEP THE NUMBER OF OPT IONS LOw.

U.S. equities are typically the largest segment of DC participant portfolios. Consequently, plan sponsors face a larger set of

decisions that involve market capitalizations, investment styles, and sector and specialty options.

The U.S. equity market is commonly divided into nine subcategories based on market capitalization and investment style (value, blend, and growth). Each of the nine subcategories has its own risk/return profile and generally can be expected to perform differently during various market and business cycles. A plan sponsor’s goal when choosing U.S. equity investment options should be to provide participants adequate exposure to the full opportunity set. How a sponsor chooses to accomplish this goal will vary.

Providing exposure to the different market capitalizations. At a minimum, a plan sponsor should provide one broadly diversified large-cap option that tracks an index like the Russell 1000 or S&P 500. Since these large-cap options make up 76% to 90% of the total value of the U.S. equity markets depending on the index, this one option can provide participants reasonably adequate exposure to the U.S. equities market. However, due to the diversification benefits and risk/return variation discussed above, participants may benefit from having exposure to dedicated mid- and small-cap options as well.

Rather than offering one investment option that invests across all capitalizations, it may be best to choose an option for each capitalization that focuses primarily on one size of the market. This would allow participants additional choice and control of their equity allocation without greatly increasing the number of options. It also allows the plan to choose options that specialize in their particular market-cap segments and to reduce the risk that one option might not perform well.

Deciding how to cover each market capitalization.A plan sponsor may use core (blend), style-specific, or a mix of choices. Here are the pros and cons each:

n Core (blend). By offering only core for each capitalization, sponsors are keeping with the theme of limiting the number of options while still allowing access to equities from each market capitalization. This limits participants’ need to make decisions and allows professional managers to decide whether to be over- or underweight certain investment styles. One disadvantage is that managers may drift to one style for an extended period, thus limiting the participants’ exposure to other styles.

n Style-specific. By using style-specific options, plan sponsors are allowing participants to make tactical allocation decisions between value and growth. Although leaving these decisions with professional managers is preferred, there are reasons why a plan may want to offer

CORE FIXED INCOME

MBSTreasury

Gov’tRelated

ABS/CMBS

Corporate

CORE PLUS FIXED INCOME

MBS

TreasuryABS/CMBS

Gov’tRelated

Plus Sectors

Corporate

Adding 20% “plus” strategies to Barclays Capital U.S. Aggregate Index

For illustrative purposes only. Individual investment options may vary.

9 Investopedia.com: “The yield curve is a line that plots the interest rates, at a set point in time, of bonds having equal credit quality, but differing maturity dates.” Up or down movements along the yield curve will result in price changes of similar bonds with different maturities. This can affect performance.

7

10 This style box was first developed by Morningstar. ©2011 Morningstar, Inc. All Rights Reserved. The information contained herein: (1) is proprietary to Morningstar and/or its content providers; (2) may not be copied or distributed; and (3) is not warranted to be accurate, complete, or timely. Neither Morningstar nor its content providers are responsible for any damages or losses arising from any use of this information.

style-specific options. First, the participants utilizing the core lineup will likely be more experienced, capable, and appreciative of the option to choose between styles. Second, and most important, because value and growth portfolios are typically diversified across sectors, the decision between value and growth does not carry as much risk as other decisions, such as sector allocation; nor does it present the complexity of bond sector selection. When adding style-specific options, sponsors need to pay particular attention to these strategies and provide education to participants on the differences, particularly in the area of small-cap equities. Small-cap value and growth funds, for example, tend to have significant sector concentrations that increase their volatility.

n Mix of core and style-specific. Sponsors do not have to take the same approach for each market capitalization. For example, a sponsor may want to offer style-specific for large-cap and mid-cap exposures but a core for small-cap. The key is to avoid offering both style-specific and core in the same market capitalization, which can lead to more confusion and chances for overlap within participant portfolios.

5 . OFFER A D I vERS IF IED INTERNAT IONAL EqU IT IES OPT ION .

International equity markets have grown significantly in recent years and now comprise about 60% of the world’s market capi-talization. This means the asset class is becoming an increasingly important part of a well-diversified participant portfolio.

Recognizing the growing opportunity set outside the U.S., the 401(k) industry has increased its attention on international options. A number of plan sponsors have recently expanded their international offerings beyond the typical broad-based options to include those that are style-specific (growth and value), market-cap focused, or dedicated to emerging markets.

While these offerings have investment merits, plan sponsors need to balance the benefits with the potential difficulties. Will participants have the ability to utilize the options appropriately? Will they understand the risks? Will the increased number of options cause confusion?

Plan sponsors who determine that the benefits outweigh the difficulties and decide to add international options should:

1. Avoid overlap with the plan’s other international options.

2. Provide additional education on the options’ differing risk/reward profiles.

Education is especially crucial when adding dedicated emerging markets and small-cap options, which are traditionally more volatile.

Plan sponsors who are not comfortable with the difficulties of adding more international choices should consider offering a single diversified international option. Preferably, the option would have a dedicated portion of its portfolio in emerging markets since those markets are gaining prominence. Through this one international option, participants will have sufficient access to the benefits of international equities, but without the confusion of multiple choices.

6 . M IN IM IZE SECTOR AND OTHER SPEC IALTY INvESTMENT OPT IONS .

The objective of a sector fund is to invest the majority of assets in a single sector of the economy, such as technology, energy, or real estate. While these sectors can have high return potential, they are generally more volatile than the broad market due to their concentrations. Many have wide swings in performance that can result in large participant flows in and out. The same is true of specialty strategies like gold and precious metals.

Large-Cap Value

Large-Cap Blend

Large-Cap Growth

Mid-Cap Value

Mid-Cap Blend

Mid-Cap Growth

Small-Cap Value

Small-Cap Blend

Small-Cap Growth

EqUIT IES STYLE BOx 10

8 T. R o w e P R i c e R e T i R e M e N T i N s i g h T s

A number of plans have recently added inflation-hedging options that focus on real estate, commodities, infrastructure, and treasury inflation protected securities (TIPS). While these investments—as well as other sectors and specialties—have merits, providing them as stand-alone options may not be the best way to provide access in a retirement plan.

The concern is that participants will misjudge the risks…

The concern is that participants will misjudge the risks associated with these funds and over-allocate to them, resulting in undiversified portfolios with large unintended levels of risk. It is better to allow participants exposure to the various sectors of the economy through diversified funds. This way, professional managers are deciding the sector and specialty allocations and generally limiting sector concentrations.

7. CONSIDER A SELF-DIRECTED BROKERAGE APPROACH TO HELP L IMIT THE NUMBER OF OPTIONS.

The final block of the plan lineup is the self-directed brokerage option. This provides access to additional investments for more sophisticated investors while reducing the number of options that might confuse or increase allocation risks for less sophisticated investors. Those participants who want dedicated allocations to sector or regional funds can find those via the brokerage option.

Plan sponsors may want to limit the brokerage window to only mutual funds, since individual securities introduce new levels of risk for participants. This capability to limit the access may not be available through every service provider.

P r O v i D i N G a c t i v E a N D Pa S S i v E c H O i c E S

The financial industry has long debated the merits of active versus passive management. As the debate will undoubtedly continue, it’s important to keep in mind that advocates on each side have valid arguments and supportive data—and most plans are likely to have believers on both sides. This being the case, plan sponsors may want to consider providing index choices to complement certain actively managed options, and vice versa.

Historically, most plans have included only one passive option in their lineup, typically a large-cap U.S. equity fund tracking the S&P 500 Index. The 401(k) industry has seen a recent trend of sponsors expanding the menu of index options to areas such as fixed income, international equities, and broader mid- and small-cap sectors of the U.S. equity market.

Sponsors should always be mindful, however, of potential problems caused by loading a plan with too many choices. Participants may find the array of options confusing and, therefore, allocate in ways that create unintended or inappropriate weightings for their needs. Or worse, they find the investment decision overwhelming and may delay participating.

As with all options in the investment lineup, best practices would dictate avoiding overlap in any market areas and insuring that the investment menu is clearly and effectively communicated to participants. Specifically, identifying options as actively or passively managed is recommended so that participants can readily identify the differences in the management style and make informed decisions based on their unique needs and preferences.

ConclusionWith defined contribution plans now providing the primary vehicle for retirement savings in the U.S., the structure of investment lineups has never been more important. To help participants make the most of their 401(k) plans, a plan sponsor may want to reevaluate the plan’s investment lineup and make changes aimed at encouraging better decision-making by participants. Ideally, an effective lineup would include:

n Professionally managed target-date options for those employees who would rather not deal with allocations and rebalancing over time.

n A streamlined core lineup that reduces participant confusion and limits the potential for taking unnecessary allocation risks.

n A brokerage window if some participants still want access to more sophisticated investments and have the capability to choose them wisely.

Every plan has its own unique circumstances, so it is important to evaluate the investment lineup in a thorough and professional way, taking into consideration the needs of both the sponsor and the employee base. The best practice considerations presented in this paper serve as a good starting point to identify changes that can increase plan effectiveness—and potentially improve retirement outcomes.

9

Assessing a Current Lineup

D C I n v e s t m e n t L i n e u p A s s e s s m e n tYes No Recommendations

Does the plan provide target-date options?

Does the plan offer more than one “cash” investment option (stable value or money market option)?

Does the plan offer more than one fixed income option?

Does the plan offer more than one international option?

Does the plan offer more than one option in a style box?

Does the plan offer a value, growth, and core option within one market cap?

Does the plan have just a value or a growth option within one market cap, but not the other style?

Does the plan offer sector funds?

Does the plan offer a brokerage window?

The following questionnaire may help identify potential problem areas within a plan’s investment lineup. It is important to understand that a “yes” or a “no” answer is not necessarily right or wrong. Any proposed plan change should be consistent with the needs of the plan’s employee population, taking into account their long-term financial needs as well as their behavioral characteristics.

a P P E N D i x

1 0 T. R o w e P R i c e R e T i R e M e N T i N s i g h T s

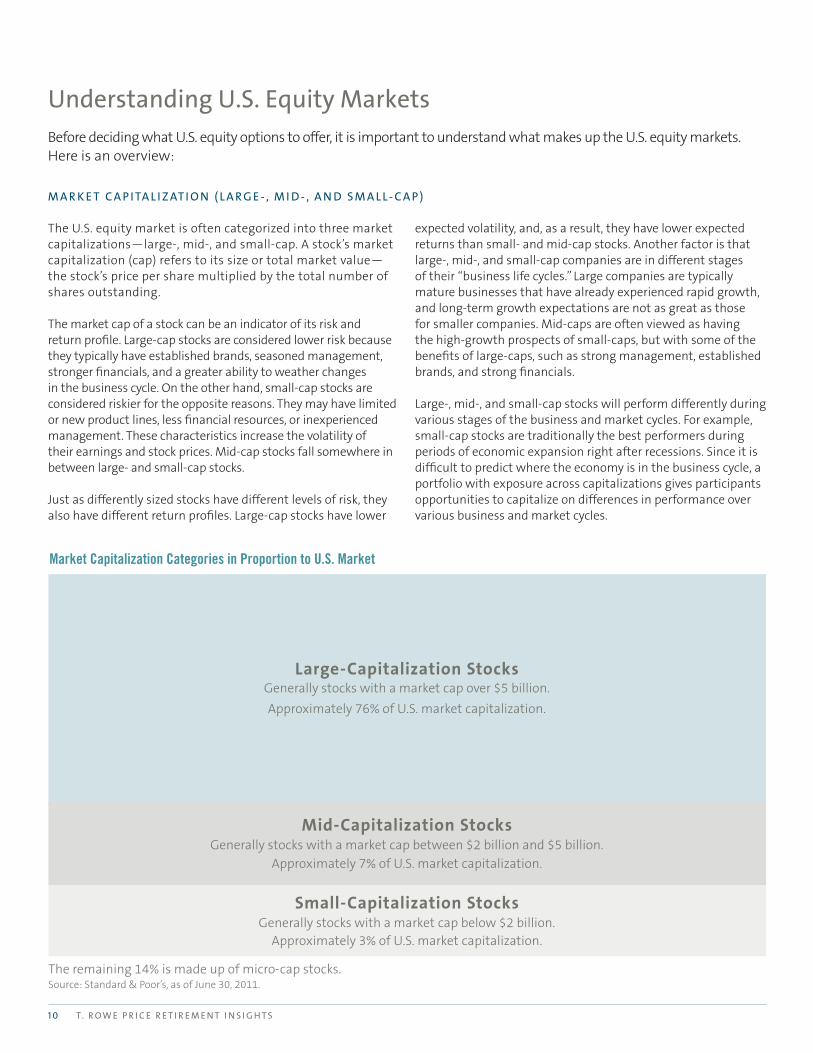

Large-Capitalization StocksGenerally stocks with a market cap over $5 billion.

Approximately 76% of U.S. market capitalization.

Mid-Capitalization StocksGenerally stocks with a market cap between $2 billion and $5 billion.

Approximately 7% of U.S. market capitalization.

Small-Capitalization StocksGenerally stocks with a market cap below $2 billion.

Approximately 3% of U.S. market capitalization.

Market Capitalization Categories in Proportion to U.S. Market

The remaining 14% is made up of micro-cap stocks.Source: Standard & Poor’s, as of June 30, 2011.

Understanding U.S. Equity MarketsBefore deciding what U.S. equity options to offer, it is important to understand what makes up the U.S. equity markets. Here is an overview:

M a R k e T c a P i Ta l i z aT i o N ( l a R g e - , M i d - , a N d s M a l l - c a P )

The U.S. equity market is often categorized into three market capitalizations—large-, mid-, and small-cap. A stock’s market capitalization (cap) refers to its size or total market value—the stock’s price per share multiplied by the total number of shares outstanding.

The market cap of a stock can be an indicator of its risk and return profile. Large-cap stocks are considered lower risk because they typically have established brands, seasoned management, stronger financials, and a greater ability to weather changes in the business cycle. On the other hand, small-cap stocks are considered riskier for the opposite reasons. They may have limited or new product lines, less financial resources, or inexperienced management. These characteristics increase the volatility of their earnings and stock prices. Mid-cap stocks fall somewhere in between large- and small-cap stocks.

Just as differently sized stocks have different levels of risk, they also have different return profiles. Large-cap stocks have lower

expected volatility, and, as a result, they have lower expected returns than small- and mid-cap stocks. Another factor is that large-, mid-, and small-cap companies are in different stages of their “business life cycles.” Large companies are typically mature businesses that have already experienced rapid growth, and long-term growth expectations are not as great as those for smaller companies. Mid-caps are often viewed as having the high-growth prospects of small-caps, but with some of the benefits of large-caps, such as strong management, established brands, and strong financials.

Large-, mid-, and small-cap stocks will perform differently during various stages of the business and market cycles. For example, small-cap stocks are traditionally the best performers during periods of economic expansion right after recessions. Since it is difficult to predict where the economy is in the business cycle, a portfolio with exposure across capitalizations gives participants opportunities to capitalize on differences in performance over various business and market cycles.

1 1

i N v e sTM e N T sT y l e ( va l u e , g R o w T h , a N d b l e N d )

The terms value and growth are often used to classify and differ-entiate investment managers, as well as industries and individ-ual stocks. Similar to market capitalization, investment style can be used as an indicator of potential risk and return.

Value managers tend to focus on the price of an asset. They focus on stocks with higher dividend yields and lower relative price multiples, such as price-to-earnings and price-to-book ratios. The theory is that the market sometimes undervalues a security or prices it below its intrinsic value and that the price will revert to its true value, resulting in capital gains. However, there is always the possibility that the market will not recognize a security’s underlying value for an unexpectedly long time, if at all. Value portfolios tend to contain higher weights to sectors such as financials and utilities.

Growth managers focus on the earnings, particularly the growth of earnings. They generally invest in stocks with earnings growth rates greater than those of competitors, their industry, or the market. The theory is that above-average earnings growth will

lead to price-to-earnings (P/E) multiple expansion (an increase in share price) due to expected higher earnings. Because growth stocks typically have higher valuations and lower dividend yields than slower-growth or cyclical stocks, their prices could decline further in market downturns. Growth portfolios tend to contain higher weights in sectors such as technology and consumer discretionary.

Value and growth investment styles tend to provide exposure to different parts of the market and have different risk and return profiles. Additionally, both styles will go through market cycles, where one will outperform the other.

The line between value and growth can be blurry. There are times when stocks and industries that are typically associated with one investment style appear to fit more appropriately with the other. This also applies to investment options. There are investment options that blend value and growth strategies. These are often referred to as “core” or “market-oriented” investment options.

05169-2097 109598 1/12

T. Rowe Price Retirement Plan Services, Inc., is a recognized industry leader dedicated to helping your employees prepare for a more financially secure retirement. With extensive research and development efforts, we anticipate emerging trends and provide innovative solutions that transform participant behavior. With world-class service and award-winning technology and education, we seek to provide participants with the best possible plan experience. In short, our priority is the success of your participants.

r E t i r E W i t H c O N F i D E N c E ®

This article has been prepared by T. Rowe Price Retirement Plan Services, Inc., for informational purposes only. T. Rowe Price (including T. Rowe Price Group, Inc., its affiliates, and its associates) does not provide legal or tax advice. Any tax-related discussion contained in this article, including any attachments, is not intended or written to be used, and cannot be used, for the purpose of (i) avoiding any tax penalties or (ii) promoting, marketing, or recommending to any other party any transaction or matter addressed herein. Please consult your independent legal counsel and/or professional tax advisor regarding any legal or tax issues raised in this article.

T. Rowe Price Investment Services, Inc., distributor, T. Rowe Price mutual funds.

i F y O u W O u l D l i k E t O l E a r N m O r E a b O u t D c P l a N i N v E S tm E N t S ,

c O N ta c t y O u r t. r O W E P r i c E D c i N v E S tm E N t r E P r E S E N tat i v E .

Call 1-800-922-9945 to request a prospectus, which includes investment objectives, risks, fees, expenses, and other information that you should read and consider carefully before investing.