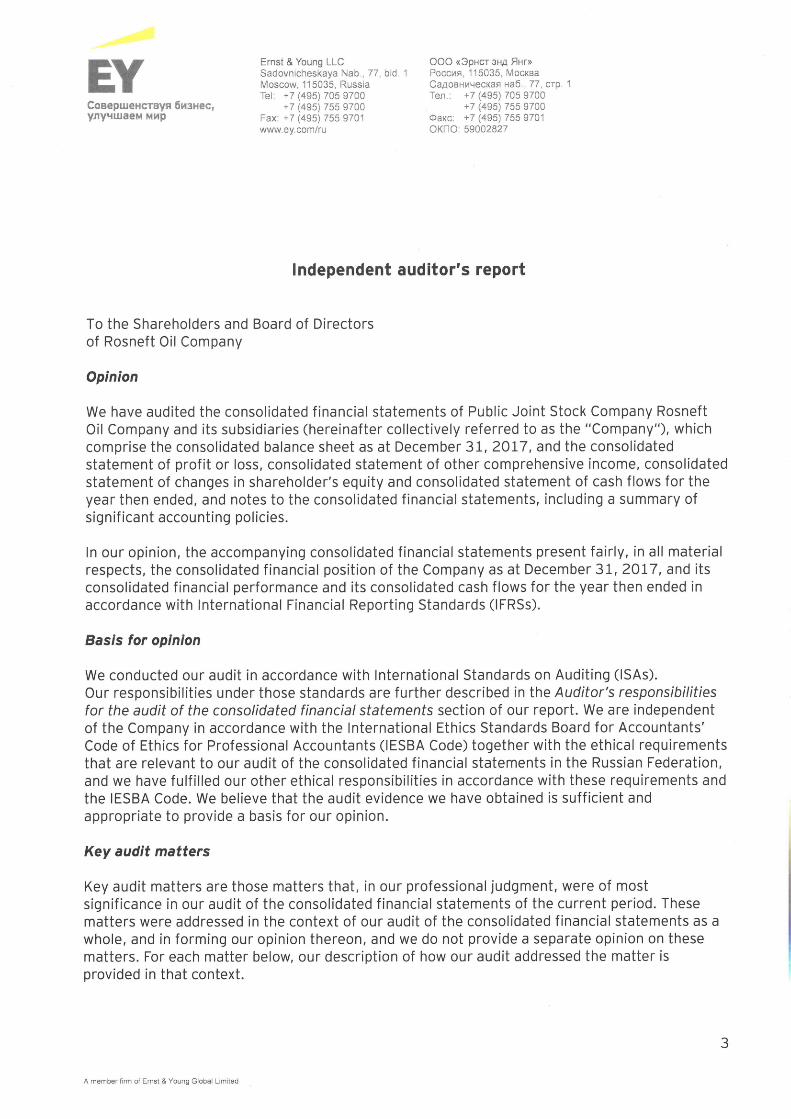

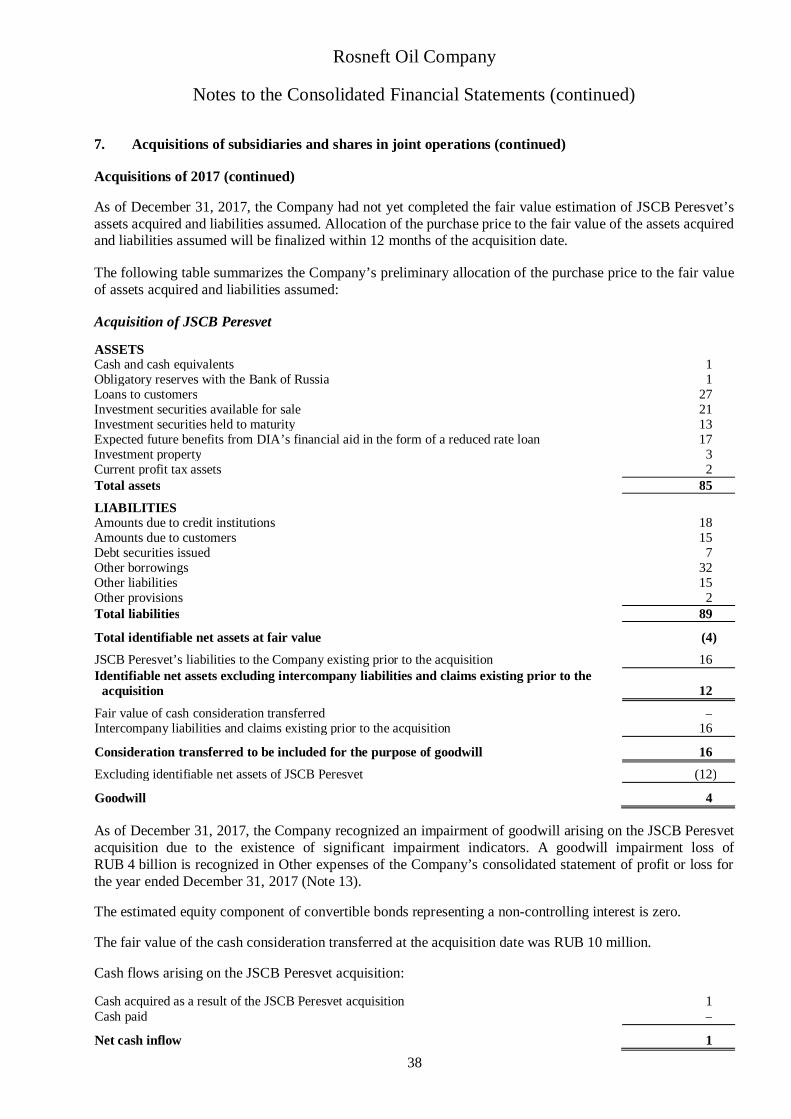

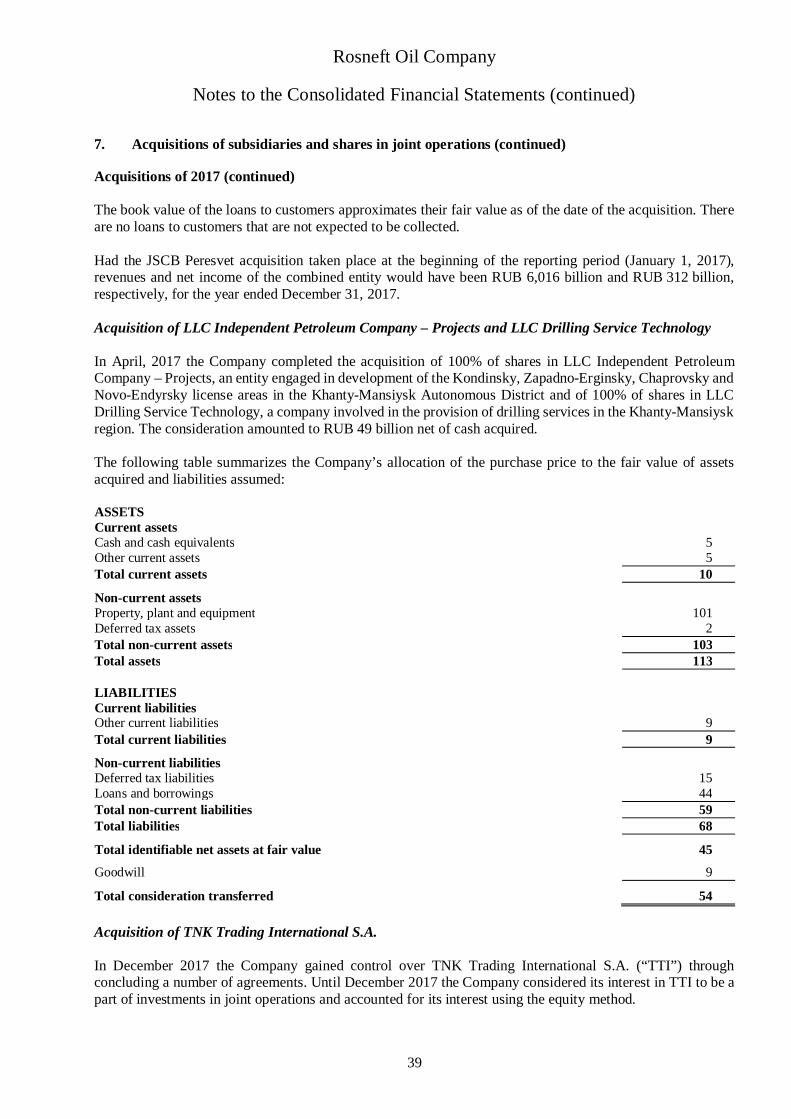

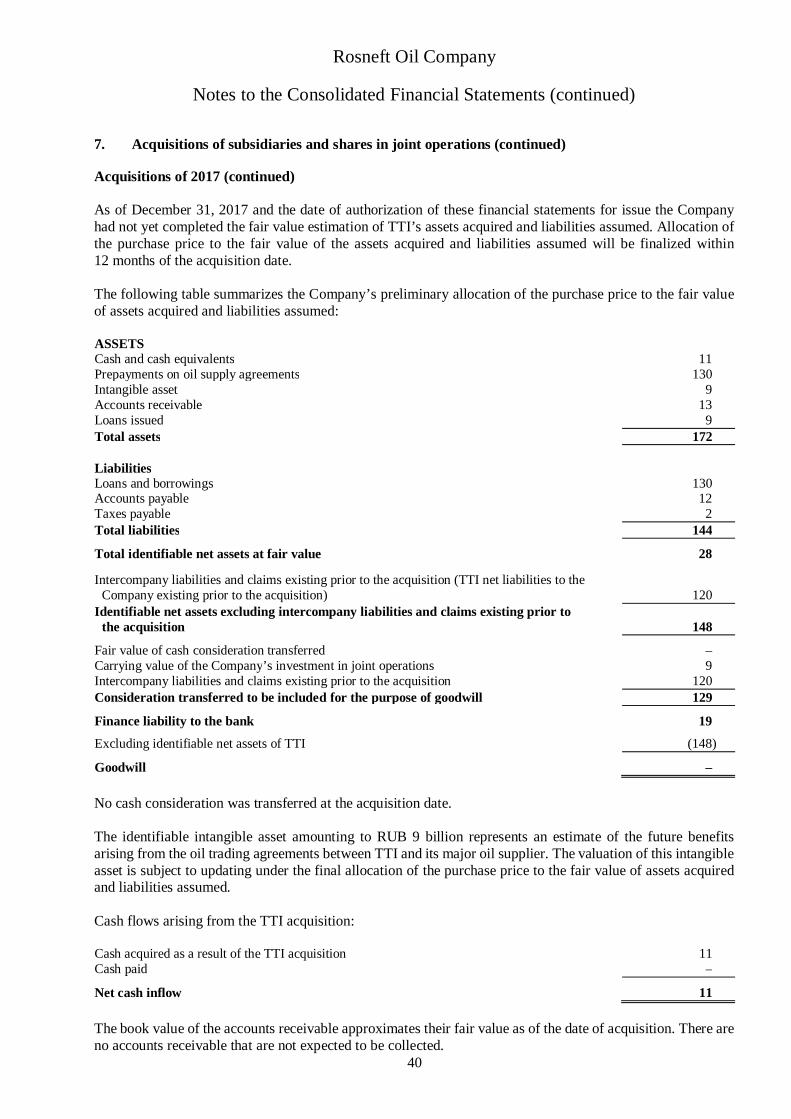

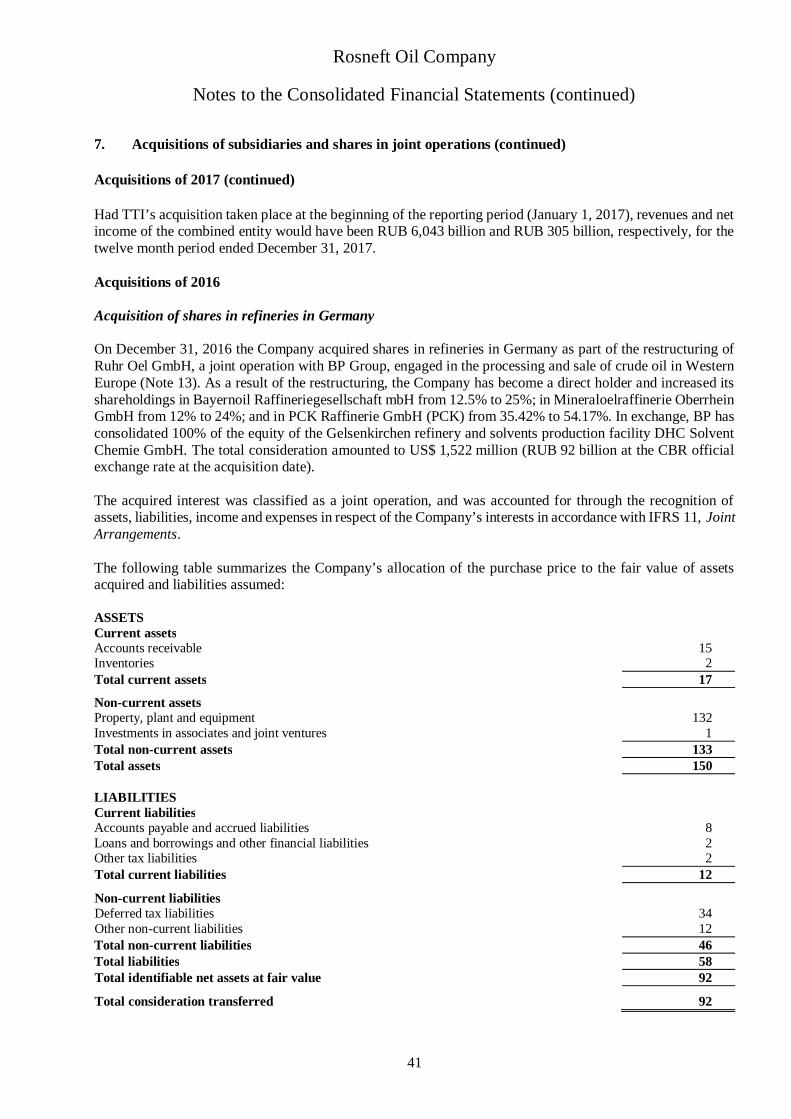

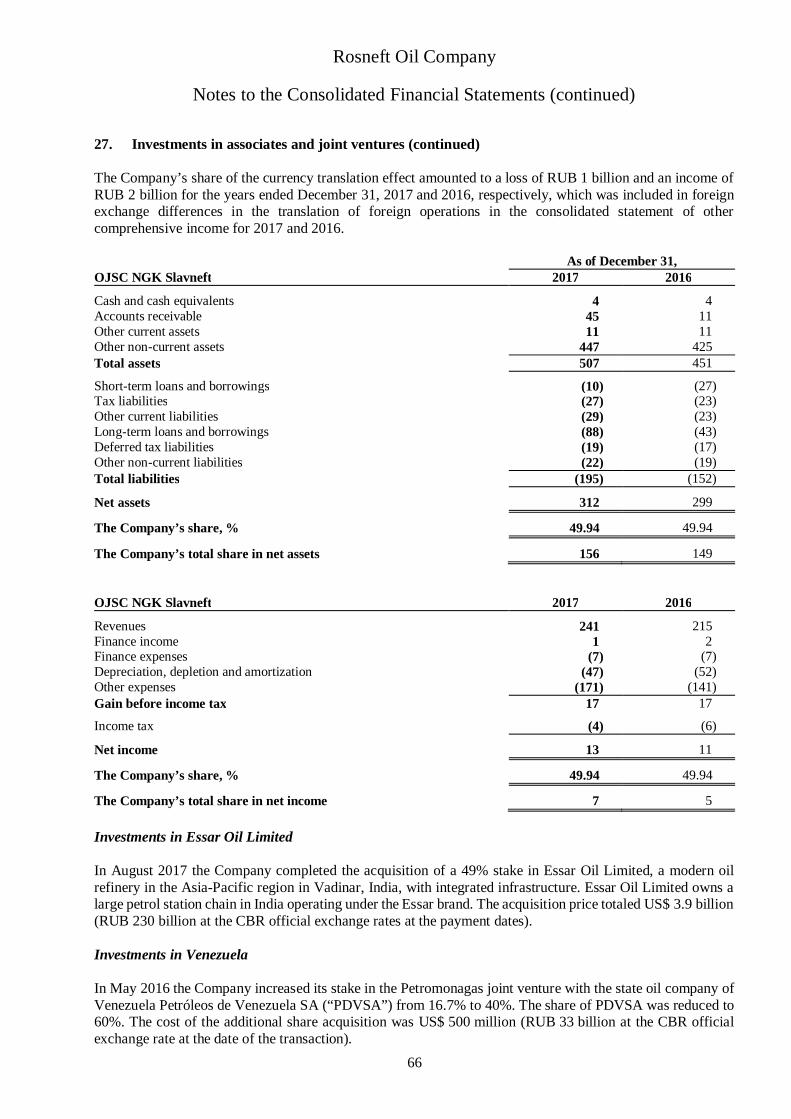

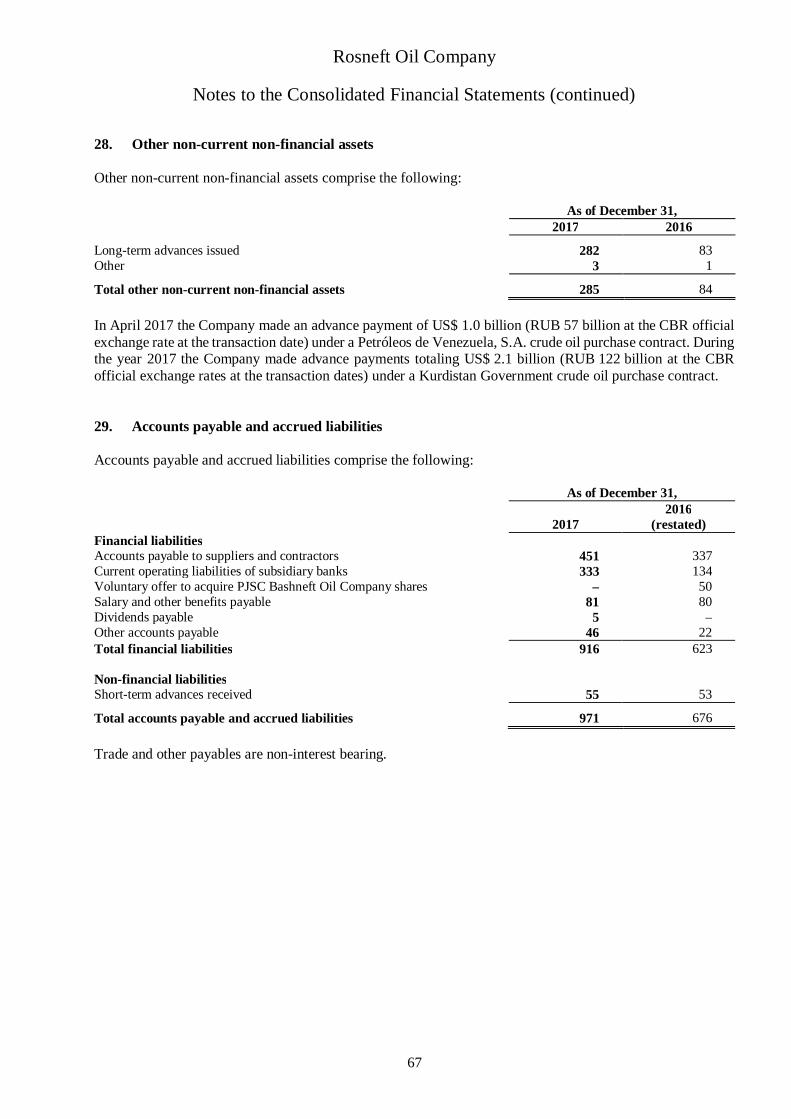

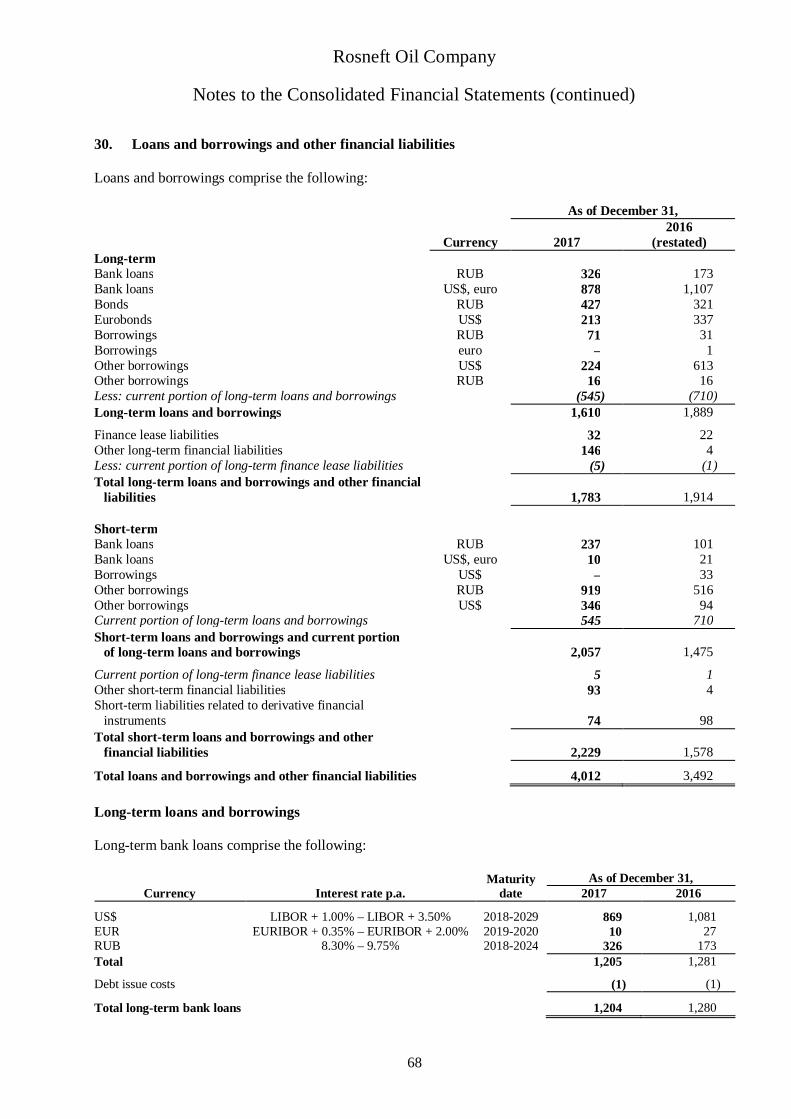

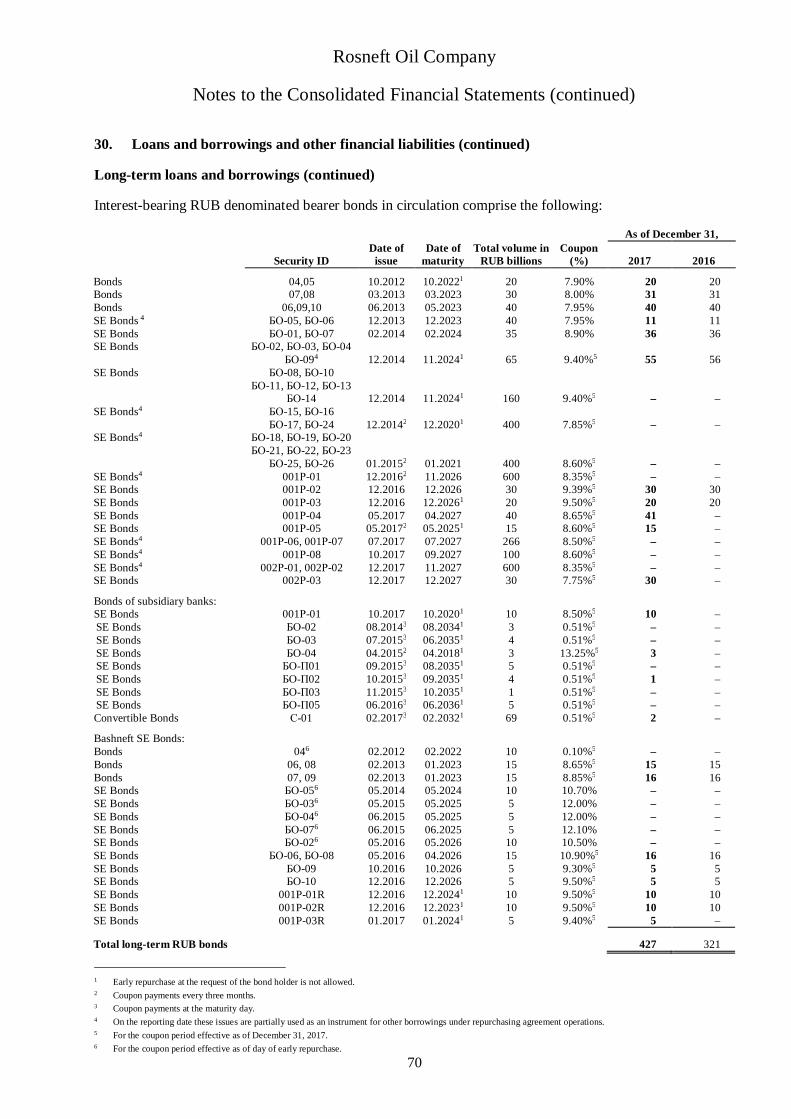

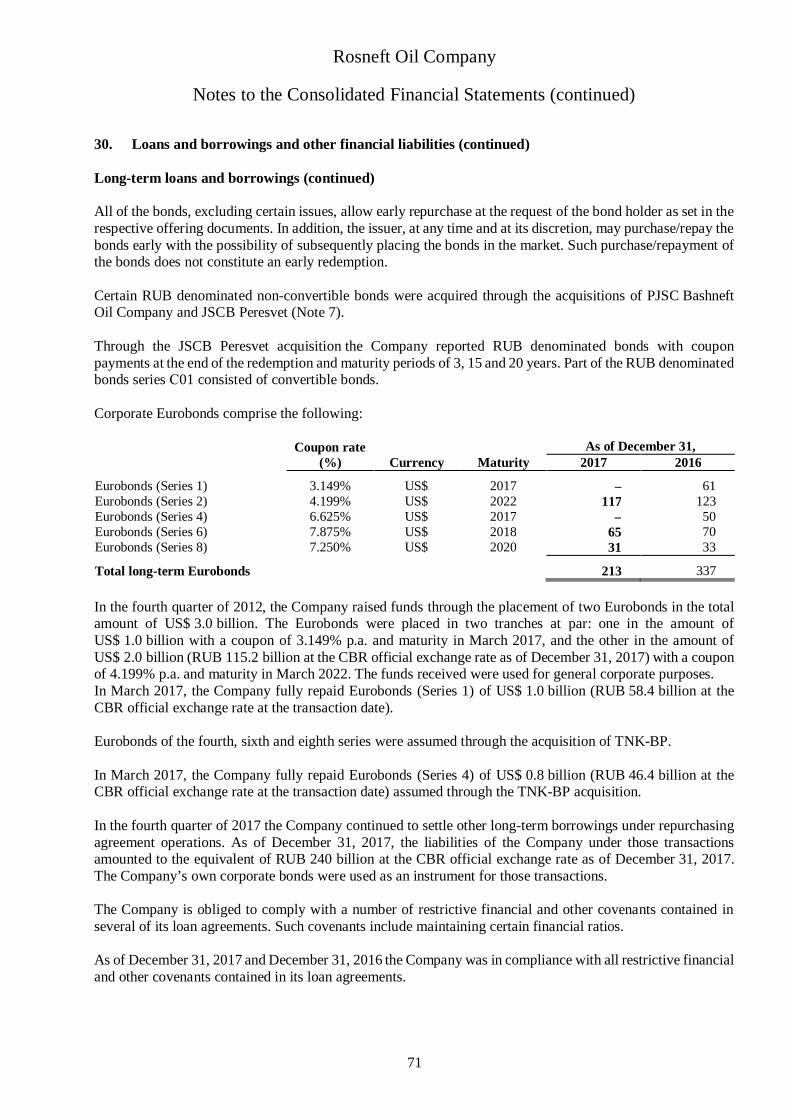

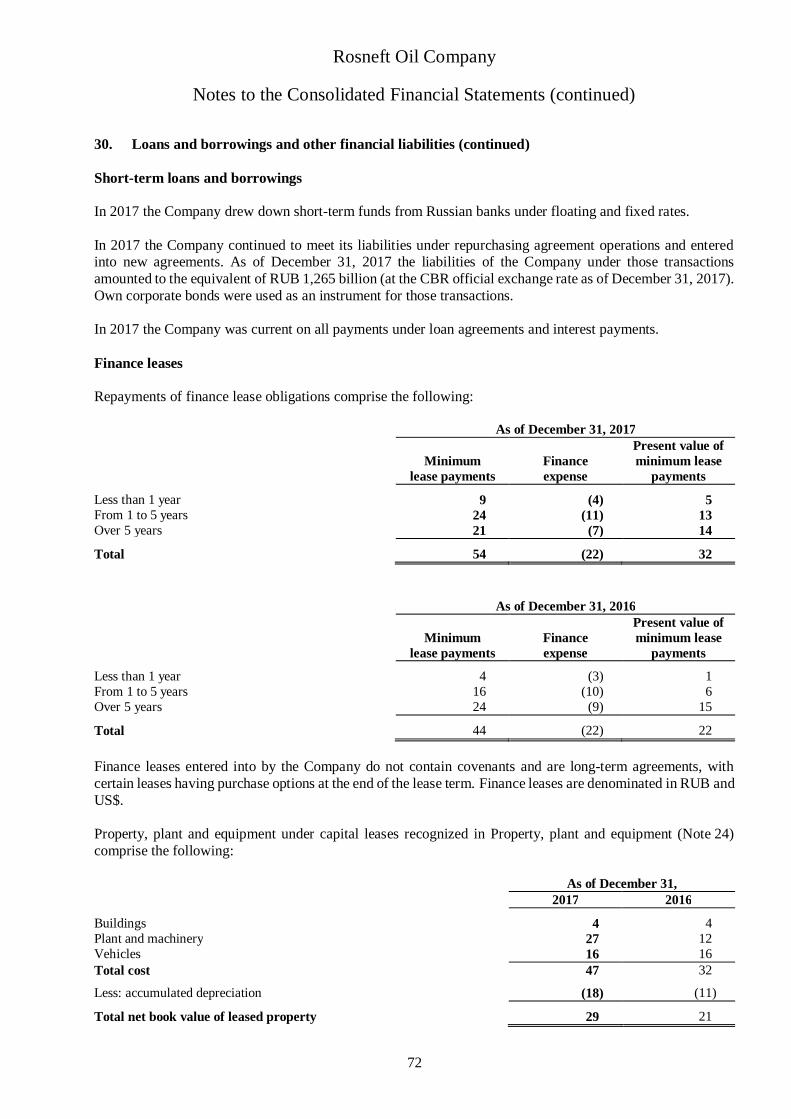

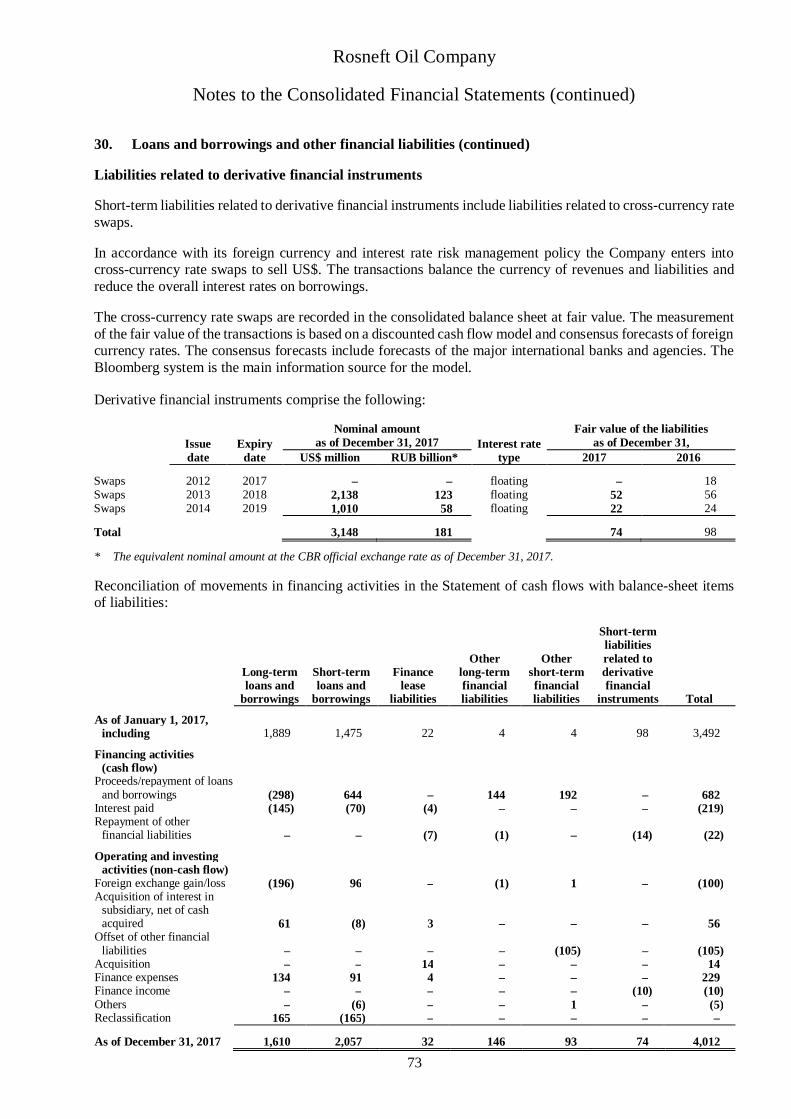

Consolidated financial statements Rosneft Oil Company … TNK-BP Limited and TNK Industrial Holdings...

91

Consolidated financial statements Rosneft Oil Company for the year ended December 31, 2017 with independent auditor’s report

Transcript of Consolidated financial statements Rosneft Oil Company … TNK-BP Limited and TNK Industrial Holdings...

Consolidated financial statementsRosneft Oil Company

for the year ended December 31, 2017

with independent auditor’s report

Consolidated financial statementsRosneft Oil Company

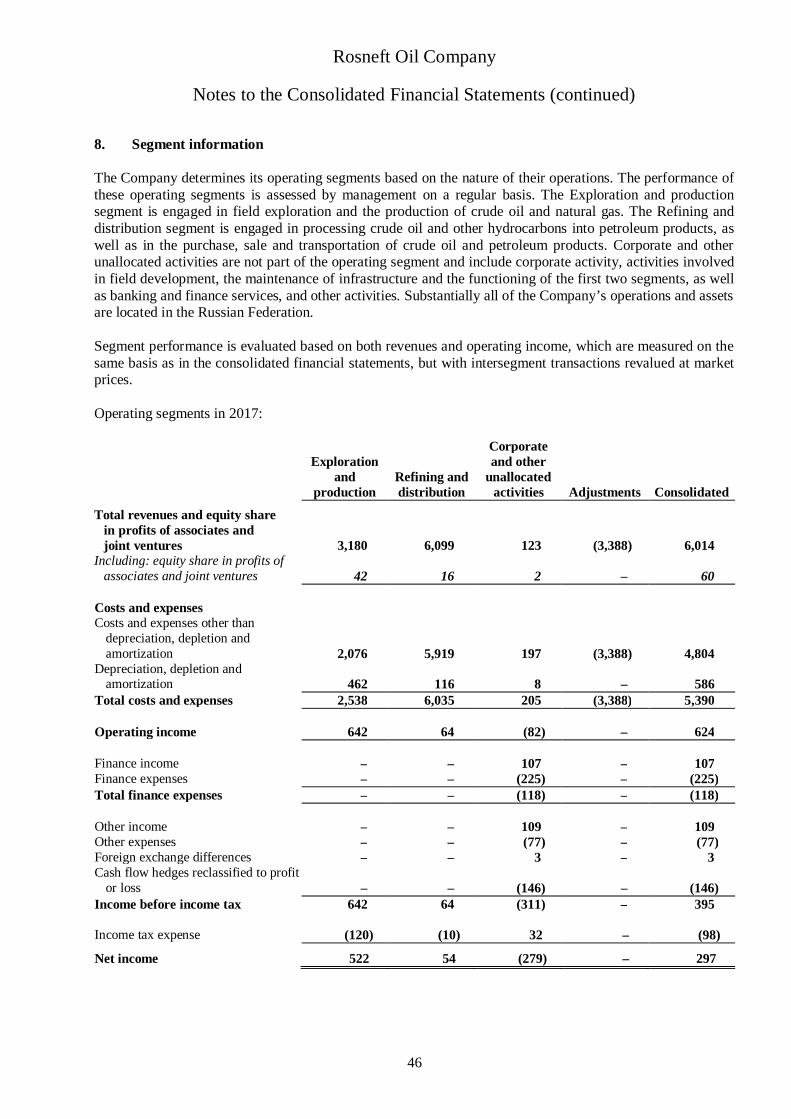

2

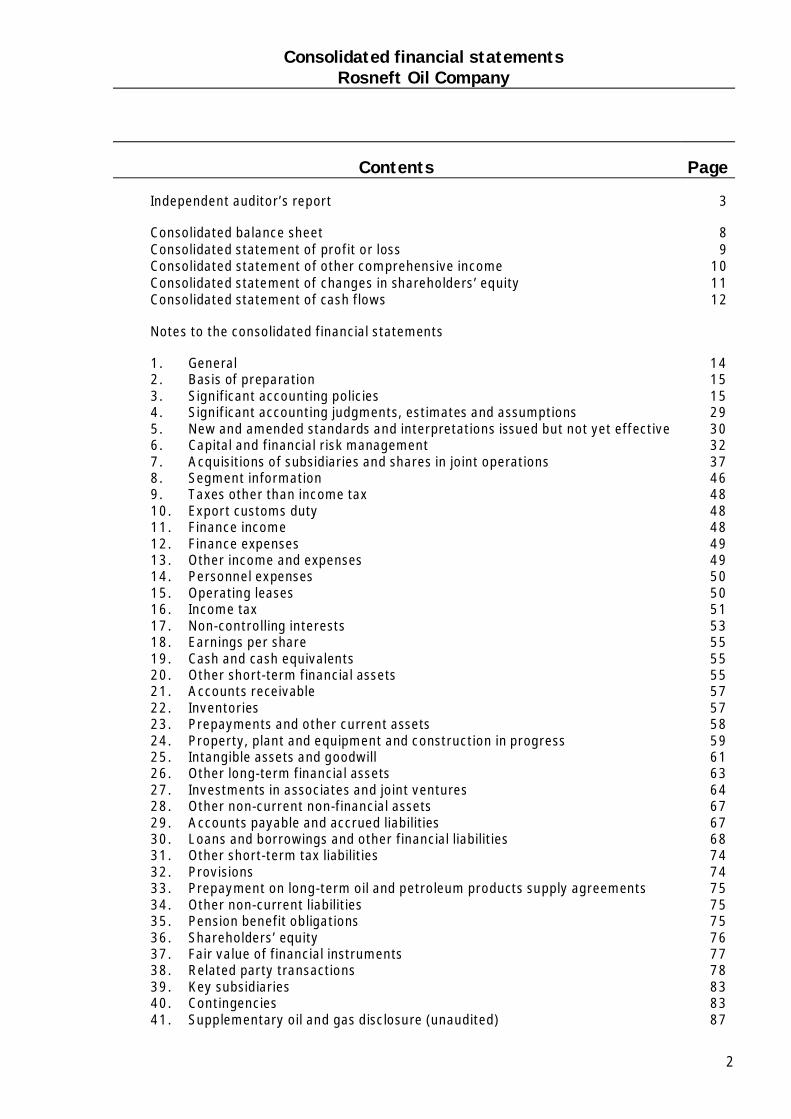

Contents Page

Independent auditor’s report 3

Consolidated balance sheet 8Consolidated statement of profit or loss 9Consolidated statement of other comprehensive income 10Consolidated statement of changes in shareholders’ equity 11Consolidated statement of cash flows 12

Notes to the consolidated financial statements

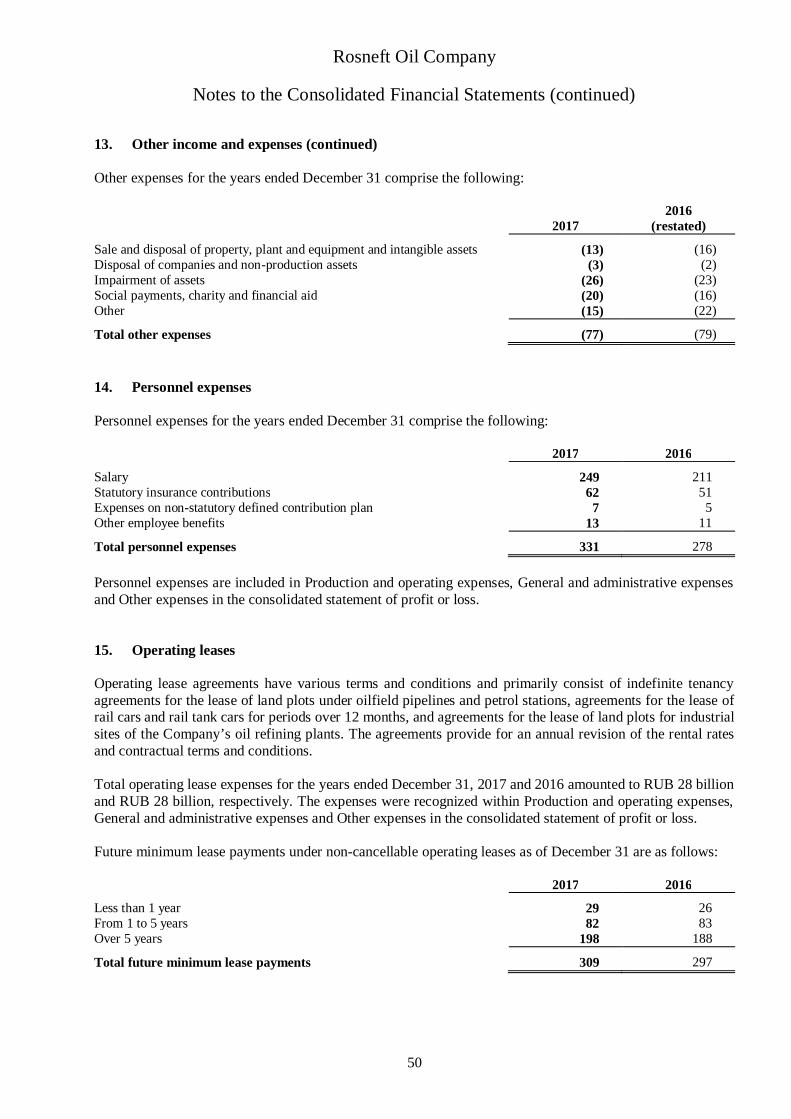

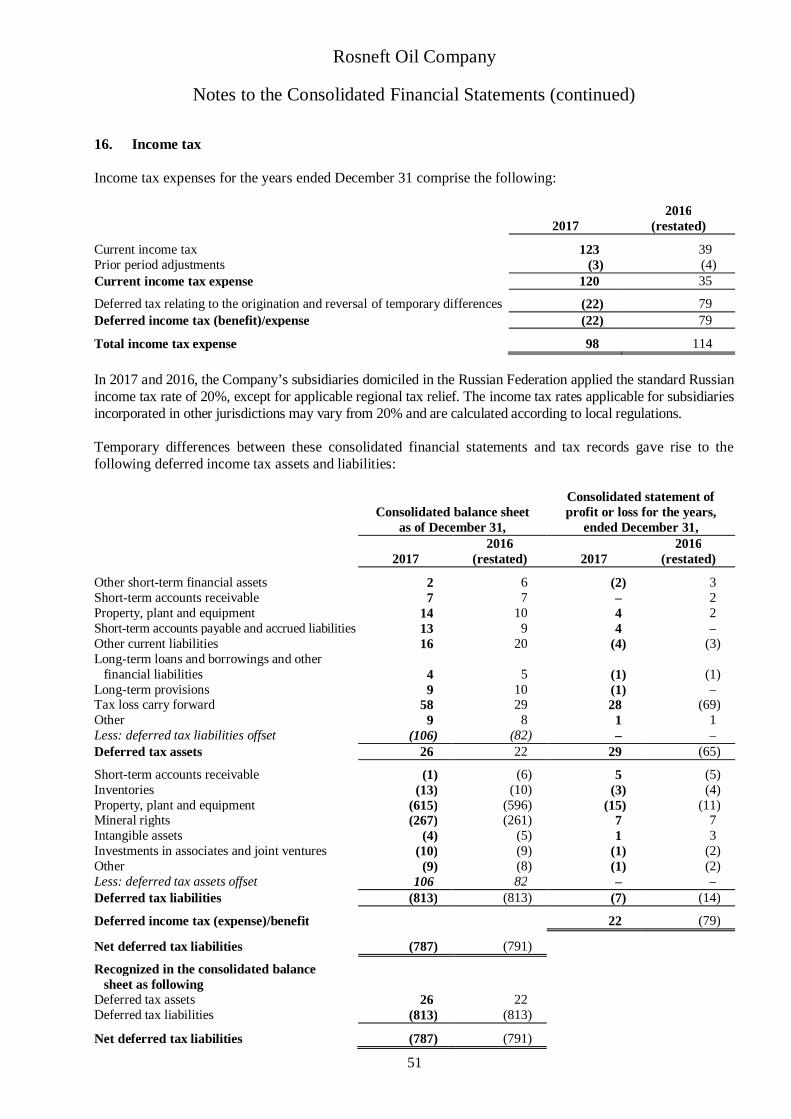

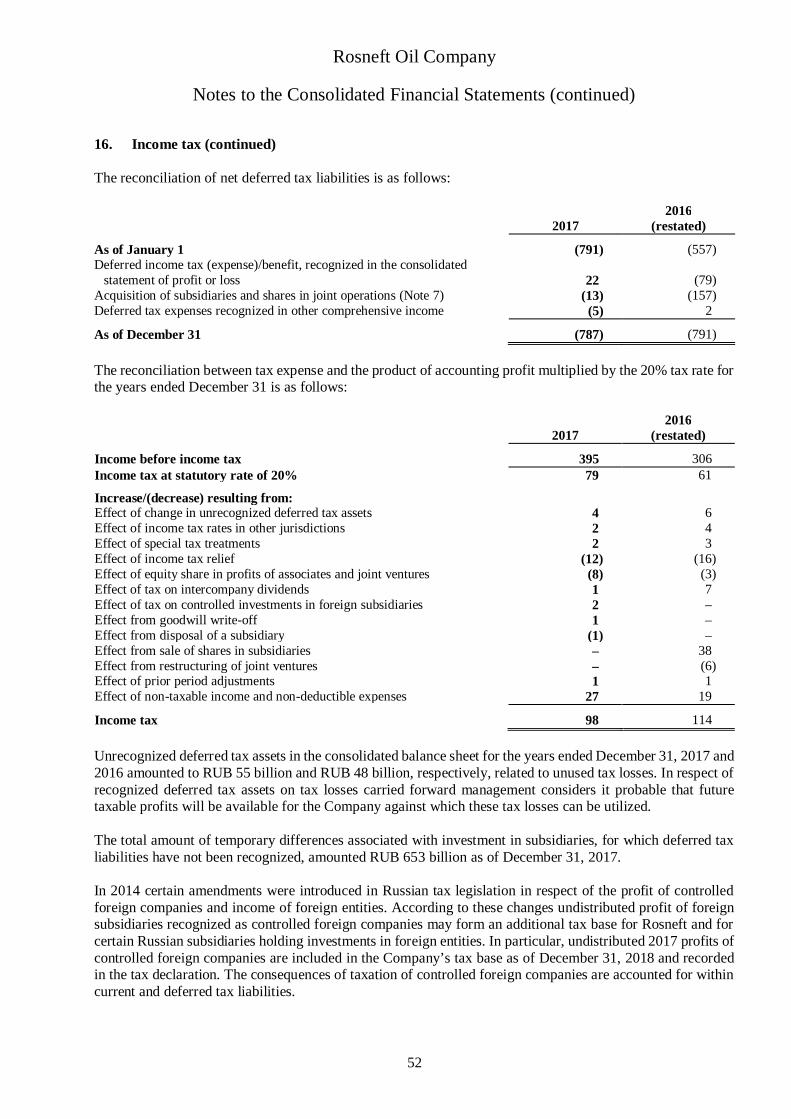

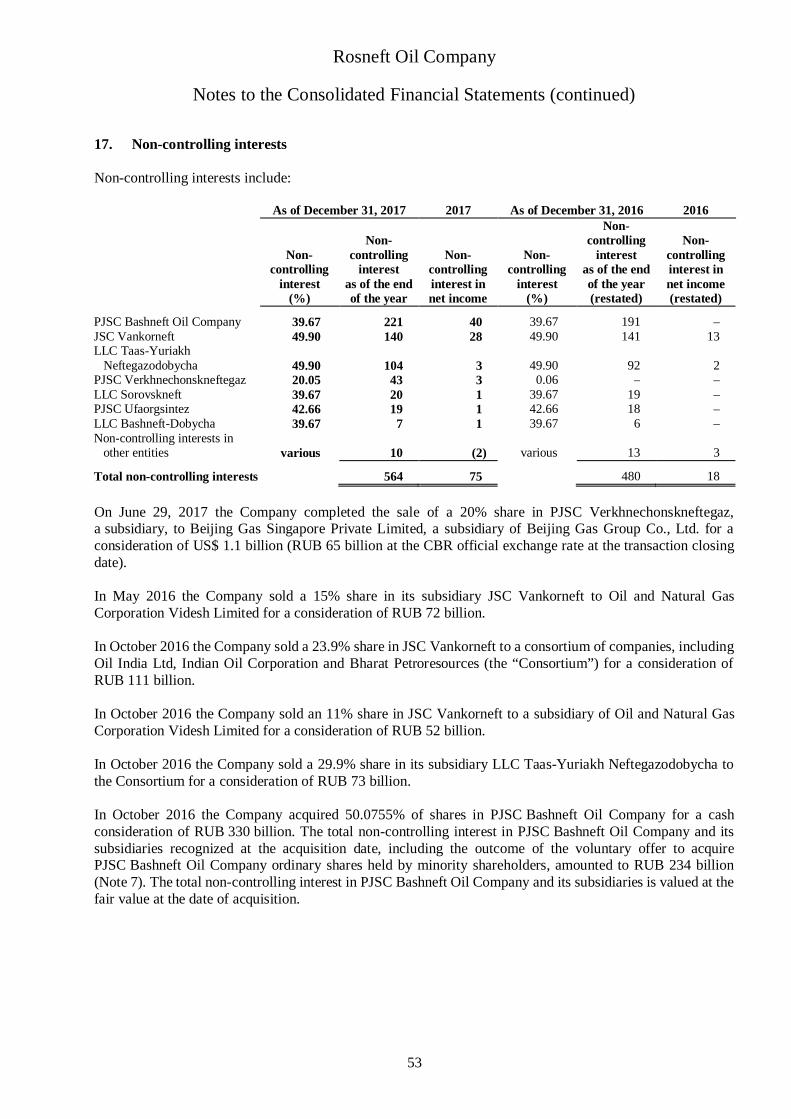

1. General 142. Basis of preparation 153. Significant accounting policies 154. Significant accounting judgments, estimates and assumptions 295. New and amended standards and interpretations issued but not yet effective 306. Capital and financial risk management 327. Acquisitions of subsidiaries and shares in joint operations 378. Segment information 469. Taxes other than income tax 4810. Export customs duty 4811. Finance income 4812. Finance expenses 4913. Other income and expenses 4914. Personnel expenses 5015. Operating leases 5016. Income tax 5117. Non-controlling interests 5318. Earnings per share 5519. Cash and cash equivalents 5520. Other short-term financial assets 5521. Accounts receivable 5722. Inventories 5723. Prepayments and other current assets 5824. Property, plant and equipment and construction in progress 5925. Intangible assets and goodwill 6126. Other long-term financial assets 6327. Investments in associates and joint ventures 6428. Other non-current non-financial assets 6729. Accounts payable and accrued liabilities 6730. Loans and borrowings and other financial liabilities 6831. Other short-term tax liabilities 7432. Provisions 7433. Prepayment on long-term oil and petroleum products supply agreements 7534. Other non-current liabilities 7535. Pension benefit obligations 7536. Shareholders’ equity 7637. Fair value of financial instruments 7738. Related party transactions 7839. Key subsidiaries 8340. Contingencies 8341. Supplementary oil and gas disclosure (unaudited) 87

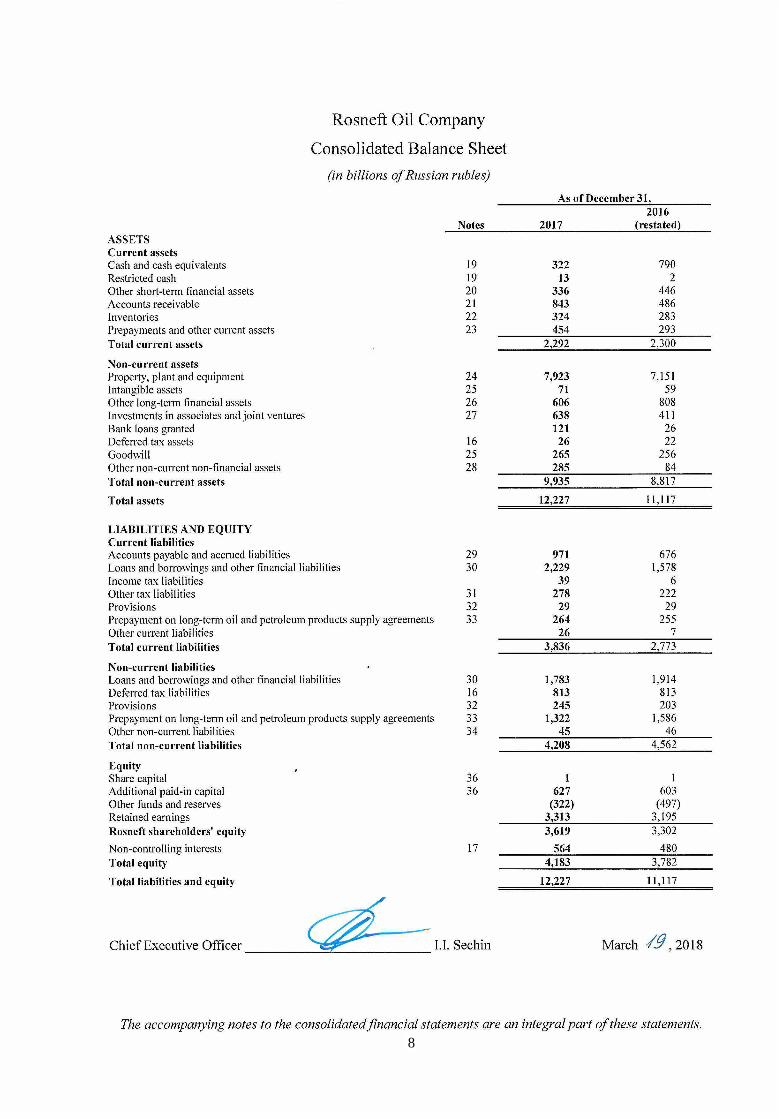

8

Rosneft Oil Company

The accompanying notes to the consolidated financial statements are an integral part of these statements.9

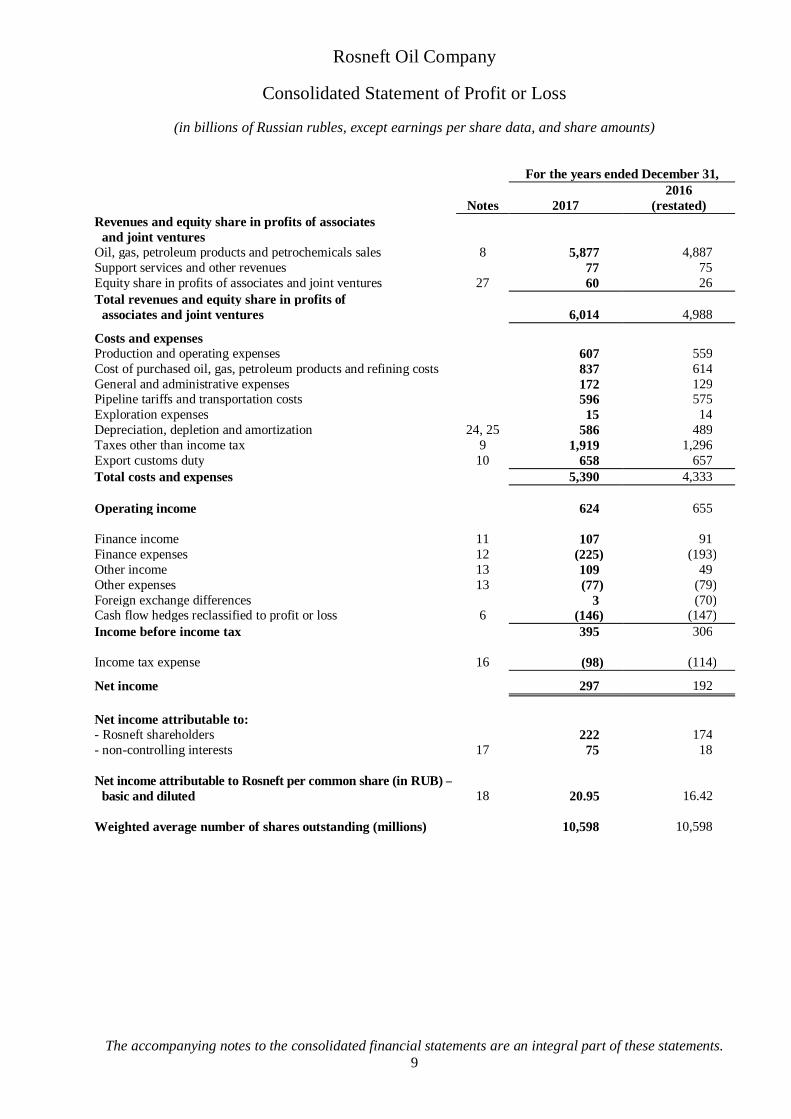

Consolidated Statement of Profit or Loss

(in billions of Russian rubles, except earnings per share data, and share amounts)

For the years ended December 31,

Notes 20172016

(restated)Revenues and equity share in profits of associates

and joint venturesOil, gas, petroleum products and petrochemicals sales 8 5,877 4,887Support services and other revenues 77 75Equity share in profits of associates and joint ventures 27 60 26Total revenues and equity share in profits of

associates and joint ventures 6,014 4,988

Costs and expensesProduction and operating expenses 607 559Cost of purchased oil, gas, petroleum products and refining costs 837 614General and administrative expenses 172 129Pipeline tariffs and transportation costs 596 575Exploration expenses 15 14Depreciation, depletion and amortization 24, 25 586 489Taxes other than income tax 9 1,919 1,296Export customs duty 10 658 657Total costs and expenses 5,390 4,333

Operating income 624 655

Finance income 11 107 91Finance expenses 12 (225) (193)Other income 13 109 49Other expenses 13 (77) (79)Foreign exchange differences 3 (70)Cash flow hedges reclassified to profit or loss 6 (146) (147)Income before income tax 395 306

Income tax expense 16 (98) (114)

Net income 297 192

Net income attributable to:- Rosneft shareholders 222 174- non-controlling interests 17 75 18

Net income attributable to Rosneft per common share (in RUB) –basic and diluted 18 20.95 16.42

Weighted average number of shares outstanding (millions) 10,598 10,598

Rosneft Oil Company

The accompanying notes to the consolidated financial statements are an integral part of these statements.10

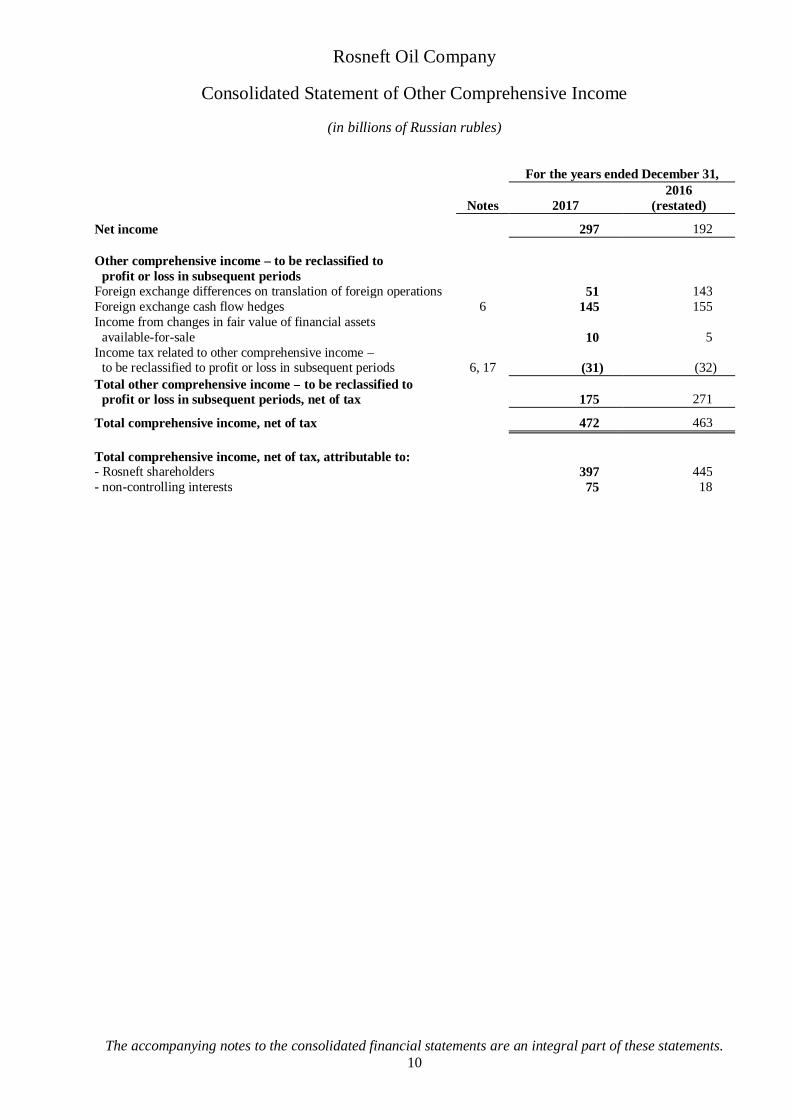

Consolidated Statement of Other Comprehensive Income

(in billions of Russian rubles)

For the years ended December 31,

Notes 20172016

(restated)

Net income 297 192

Other comprehensive income – to be reclassified toprofit or loss in subsequent periods

Foreign exchange differences on translation of foreign operations 51 143Foreign exchange cash flow hedges 6 145 155Income from changes in fair value of financial assets

available-for-sale 10 5Income tax related to other comprehensive income –

to be reclassified to profit or loss in subsequent periods 6, 17 (31) (32)Total other comprehensive income – to be reclassified to

profit or loss in subsequent periods, net of tax 175 271

Total comprehensive income, net of tax 472 463

Total comprehensive income, net of tax, attributable to:- Rosneft shareholders 397 445- non-controlling interests 75 18

Rosneft Oil Company

The accompanying notes to the consolidated financial statements are an integral part of these statements.11

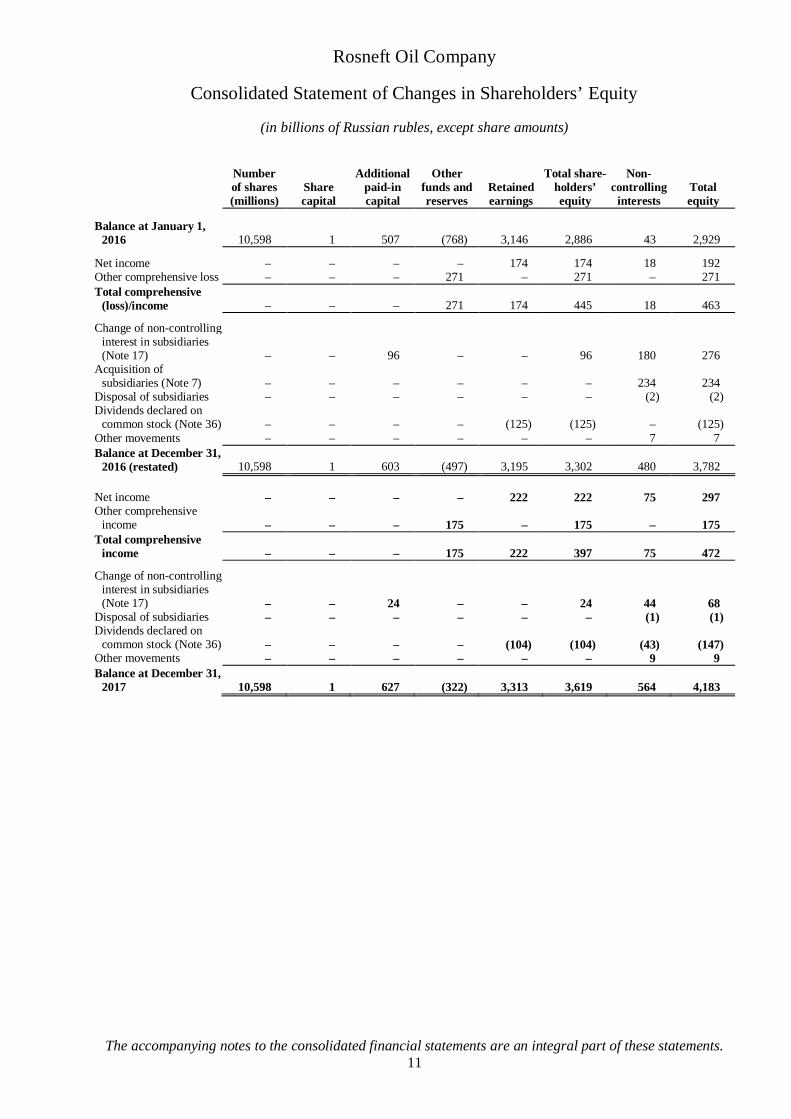

Consolidated Statement of Changes in Shareholders’ Equity

(in billions of Russian rubles, except share amounts)

Numberof shares(millions)

Sharecapital

Additionalpaid-incapital

Otherfunds andreserves

Retainedearnings

Total share-holders’equity

Non-controlling

interestsTotalequity

Balance at January 1,2016 10,598 1 507 (768) 3,146 2,886 43 2,929

Net income – – – – 174 174 18 192Other comprehensive loss – – – 271 – 271 – 271Total comprehensive

(loss)/income – – – 271 174 445 18 463

Change of non-controllinginterest in subsidiaries(Note 17) – – 96 – – 96 180 276

Acquisition ofsubsidiaries (Note 7) – – – – – – 234 234

Disposal of subsidiaries – – – – – – (2) (2)Dividends declared on

common stock (Note 36) – – – – (125) (125) – (125)Other movements – – – – – – 7 7Balance at December 31,

2016 (restated) 10,598 1 603 (497) 3,195 3,302 480 3,782

Net income – – – – 222 222 75 297Other comprehensive

income – – – 175 – 175 – 175Total comprehensive

income – – – 175 222 397 75 472

Change of non-controllinginterest in subsidiaries(Note 17) – – 24 – – 24 44 68

Disposal of subsidiaries – – – – – – (1) (1)Dividends declared on

common stock (Note 36) – – – – (104) (104) (43) (147)Other movements – – – – – – 9 9Balance at December 31,

2017 10,598 1 627 (322) 3,313 3,619 564 4,183

Rosneft Oil Company

The accompanying notes to the consolidated financial statements are an integral part of these statements.12

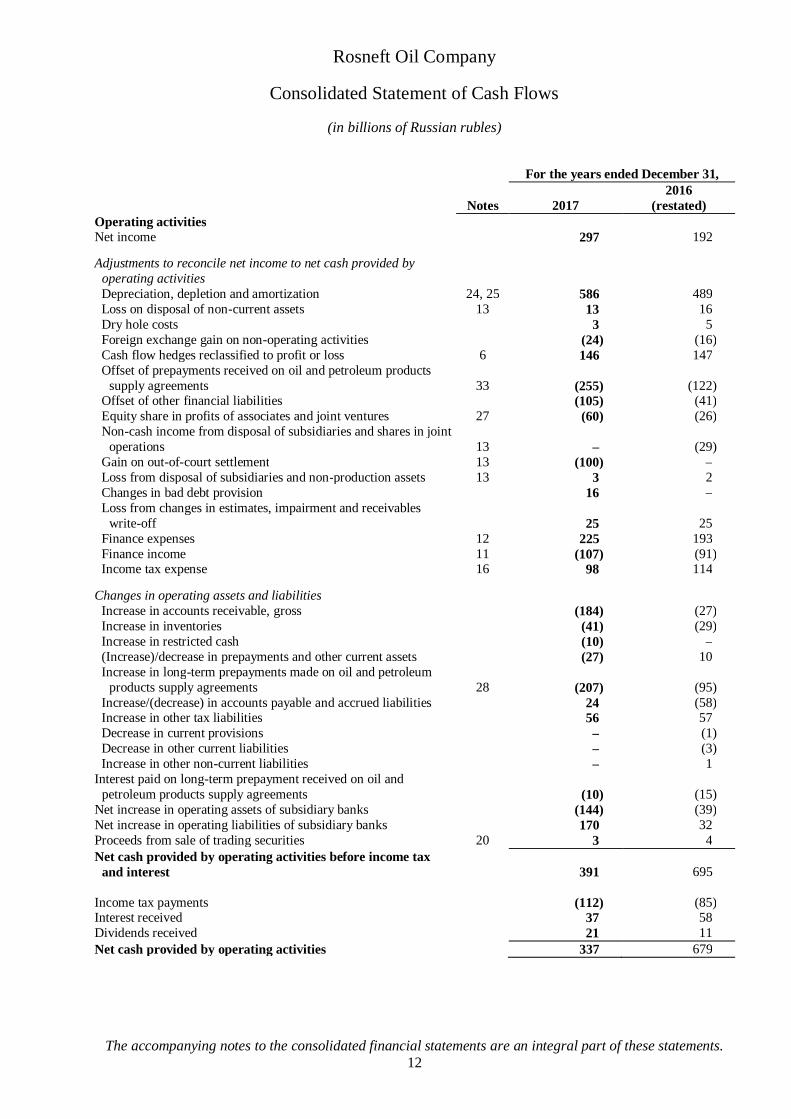

Consolidated Statement of Cash Flows

(in billions of Russian rubles)

For the years ended December 31,

Notes 20172016

(restated)Operating activitiesNet income 297 192

Adjustments to reconcile net income to net cash provided byoperating activitiesDepreciation, depletion and amortization 24, 25 586 489Loss on disposal of non-current assets 13 13 16Dry hole costs 3 5Foreign exchange gain on non-operating activities (24) (16)Cash flow hedges reclassified to profit or loss 6 146 147Offset of prepayments received on oil and petroleum products

supply agreements 33 (255) (122)Offset of other financial liabilities (105) (41)Equity share in profits of associates and joint ventures 27 (60) (26)Non-cash income from disposal of subsidiaries and shares in joint

operations 13 – (29)Gain on out-of-court settlement 13 (100) –Loss from disposal of subsidiaries and non-production assets 13 3 2Changes in bad debt provision 16 –Loss from changes in estimates, impairment and receivables

write-off 25 25Finance expenses 12 225 193Finance income 11 (107) (91)Income tax expense 16 98 114

Changes in operating assets and liabilitiesIncrease in accounts receivable, gross (184) (27)Increase in inventories (41) (29)Increase in restricted cash (10) –(Increase)/decrease in prepayments and other current assets (27) 10Increase in long-term prepayments made on oil and petroleum

products supply agreements 28 (207) (95)Increase/(decrease) in accounts payable and accrued liabilities 24 (58)Increase in other tax liabilities 56 57Decrease in current provisions – (1)Decrease in other current liabilities – (3)Increase in other non-current liabilities – 1

Interest paid on long-term prepayment received on oil andpetroleum products supply agreements (10) (15)

Net increase in operating assets of subsidiary banks (144) (39)Net increase in operating liabilities of subsidiary banks 170 32Proceeds from sale of trading securities 20 3 4Net cash provided by operating activities before income tax

and interest 391 695

Income tax payments (112) (85)Interest received 37 58Dividends received 21 11Net cash provided by operating activities 337 679

Rosneft Oil Company

The accompanying notes to the consolidated financial statements are an integral part of these statements.13

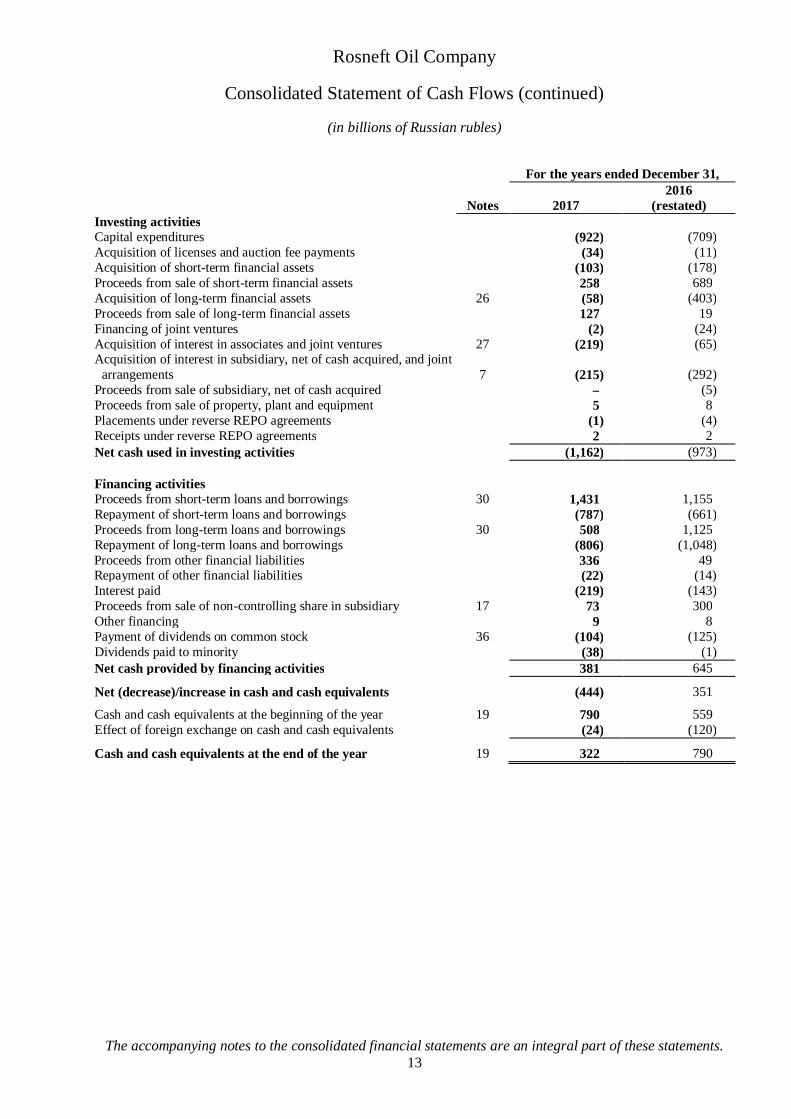

Consolidated Statement of Cash Flows (continued)

(in billions of Russian rubles)

For the years ended December 31,

Notes 20172016

(restated)Investing activitiesCapital expenditures (922) (709)Acquisition of licenses and auction fee payments (34) (11)Acquisition of short-term financial assets (103) (178)Proceeds from sale of short-term financial assets 258 689Acquisition of long-term financial assets 26 (58) (403)Proceeds from sale of long-term financial assets 127 19Financing of joint ventures (2) (24)Acquisition of interest in associates and joint ventures 27 (219) (65)Acquisition of interest in subsidiary, net of cash acquired, and joint

arrangements 7 (215) (292)Proceeds from sale of subsidiary, net of cash acquired – (5)Proceeds from sale of property, plant and equipment 5 8Placements under reverse REPO agreements (1) (4)Receipts under reverse REPO agreements 2 2Net cash used in investing activities (1,162) (973)

Financing activitiesProceeds from short-term loans and borrowings 30 1,431 1,155Repayment of short-term loans and borrowings (787) (661)Proceeds from long-term loans and borrowings 30 508 1,125Repayment of long-term loans and borrowings (806) (1,048)Proceeds from other financial liabilities 336 49Repayment of other financial liabilities (22) (14)Interest paid (219) (143)Proceeds from sale of non-controlling share in subsidiary 17 73 300Other financing 9 8Payment of dividends on common stock 36 (104) (125)Dividends paid to minority (38) (1)Net cash provided by financing activities 381 645

Net (decrease)/increase in cash and cash equivalents (444) 351

Cash and cash equivalents at the beginning of the year 19 790 559Effect of foreign exchange on cash and cash equivalents (24) (120)

Cash and cash equivalents at the end of the year 19 322 790

Rosneft Oil Company

Notes to the Consolidated Financial Statements

December 31, 2017

(all amounts in tables are in billions of Russian rubles, except as noted otherwise)

14

1. General

Public Joint Stock Company (“PJSC”) Rosneft Oil Company (“Rosneft”) and its subsidiaries (collectively, the“Company”) are principally engaged in exploration, development, production and sale of crude oil and gas andrefining, transportation and sale of petroleum products in the Russian Federation and in certain internationalmarkets.

Rosneft State Enterprise was incorporated as an open joint stock company on December 7, 1995. All assetsand liabilities previously managed by Rosneft State Enterprise were transferred to the Company at their bookvalue effective on that date together with ownership rights to other privatized oil and gas companies belongingto the Government of the Russian Federation (the “State”). The transfer of assets and liabilities was made inaccordance with Russian Government Resolution No. 971 dated September 29, 1995, On the Transformationof Rosneft State Enterprise into Open Joint Stock Company “Oil Company Rosneft”. These transfers involvedthe reorganization of assets under the common control of the State and, accordingly, were accounted for attheir book value. In 2005, the State contributed the shares of Rosneft to the share capital ofJSC ROSNEFTEGAS. As of December 31, 2005, 100% of the shares of Rosneft less one share were ownedby JSC ROSNEFTEGAS and one share was owned by the Russian Federation Federal Agency for theManagement of Federal Property. Subsequently, JSC ROSNEFTEGAS’s ownership interest decreasedthrough the additional issue of shares during Rosneft’s Initial Public Offering (“IPO”) in Russia, an issue ofGlobal Depository Receipts (“GDR”) for shares on the London Stock Exchange and the share swap completedduring the merger of Rosneft and certain subsidiaries in 2006. In March 2013 in the course of the acquisitionof TNK-BP Limited and TNK Industrial Holdings Limited, its subsidiary (collectively with their subsidiaries,“TNK-BP”), JSC ROSNEFTEGAS sold 5.66% of Rosneft shares to BP plc. (“BP”). In December 2016JSC ROSNEFTEGAS signed an agreement to sell 19.5% of Rosneft shares to a consortium of foreigninvestors. As of December 31, 2017 JSC ROSNEFTEGAS’s ownership interest in Rosneft amounted to 50%plus one share.

Under Russian legislation, natural resources, including oil, gas, precious metals and minerals and othercommercial minerals situated in the territory of the Russian Federation, are the property of the State until theyare extracted. Law of the Russian Federation No. 2395-1, On Subsurface Resources, regulates relations arisingin connection with the geological study, use and protection of subsurface resources in the territory of theRussian Federation. Pursuant to the law, subsurface resources may be developed only on the basis of a license.A license is issued by the regional governmental body and contains information on the site to be developedand the period of activity, as well as financial and other conditions. The Company holds licenses issued bycompetent authorities for the geological study, exploration and development of oil and gas blocks, fields, andshelf in areas where its subsidiaries are located.

The Company is subject to export quotas set by the Russian Federation State Pipeline Commission to allowequal access to the limited capacity of the oil pipeline system owned and operated by PJSC AK Transneft.The Company exports certain quantities of crude oil through bypassing the PJSC AK Transneft system thusachieving higher export capacity. The remaining production is processed at the Company’s and third parties’refineries for further sale on domestic and international markets.

Rosneft Oil Company

Notes to the Consolidated Financial Statements (continued)

15

2. Basis of preparation

These consolidated financial statements have been prepared in accordance with International FinancialReporting Standards, including all International Financial Reporting Standards (“IFRS”) and Interpretationsissued by the International Accounting Standards Board (“IASB”) and effective in the reporting period, andare fully compliant therewith.

These consolidated financial statements have been prepared on a historical cost basis, except certain financialassets and liabilities measured at fair value (Note 37).

Rosneft and its subsidiaries maintain their books and records in accordance with statutory accounting andtaxation principles and practices applicable in respective jurisdictions. These consolidated financial statementswere derived from the Company’s statutory books and records.

The Company’s consolidated financial statements are presented in billions of Russian rubles (“RUB”), unlessotherwise indicated.

The consolidated financial statements were approved and authorized for issue by the Chief Executive Officerof the Company on March 19, 2018.

Subsequent events have been evaluated through March 19, 2018, the date these consolidated financialstatements were issued.

3. Significant accounting policies

The accompanying consolidated financial statements differ from the financial statements issued for statutorypurposes in that they reflect certain adjustments, not recorded in the Company’s statutory books, which areappropriate for presenting the financial position, results of operations and cash flows in accordance with IFRS.The principal adjustments relate to: (1) recognition of certain expenses; (2) valuation and depreciation ofproperty, plant and equipment; (3) deferred income taxes; (4) valuation allowances for unrecoverable assets;(5) accounting for the time value of money; (6) accounting for investments in oil and gas property andconveyances; (7) consolidation principles; (8) recognition and disclosure of guarantees, contingencies,commitments and certain assets and liabilities; (9) business combinations and goodwill; (10) accounting forderivative instruments; (11) purchase price allocation to the identifiable assets acquired and the liabilitiesassumed.

The consolidated financial statements include the accounts of majority-owned, controlled subsidiaries andspecial-purpose entities where the Company holds a beneficial interest. All significant intercompanytransactions and balances have been eliminated. The equity method is used to account for investments inassociates in which the Company has the ability to exert significant influence over the associates’ operatingand financial policies. Investments in entities where the Company holds the majority of shares, but does notexercise control, are also accounted for using the equity method. Investments in other companies are accountedfor at fair value or cost adjusted for impairment, if any.

Business combinations, goodwill and other intangible assets

Acquisitions by the Company of controlling interests in third parties (or interest in their charter capital) areaccounted for using the acquisition method.

The date of acquisition is the date when effective control over the acquiree passes to the Company.

Rosneft Oil Company

Notes to the Consolidated Financial Statements (continued)

16

3. Significant accounting policies (continued)

Business combinations, goodwill and other intangible assets (continued)

The cost of an acquisition is measured as an aggregate of the consideration transferred, measured at acquisitiondate fair value, and the amount of any non-controlling interest in the acquiree. For each business combination,the Company elects whether it measures the non-controlling interest in the acquiree either at fair value or atthe proportionate share of the acquiree’s identifiable net assets. Acquisition costs incurred are expensed andincluded in administrative expenses.

Any contingent consideration to be transferred by the acquirer is recognized at fair value at the acquisitiondate. Subsequent changes to the fair value of the contingent consideration which is deemed to be an asset or aliability should be recognized within profit or loss for the period if they do not represent measurement-periodadjustments. If the contingent consideration is classified as equity, it should not be re-measured.

Goodwill is initially measured at cost being the excess of the aggregate of the consideration transferred andthe amount recognized for non-controlling interests over the fair value of net identifiable assets acquired andliabilities assumed. If the aggregate of the consideration transferred and the amount of non-controlling interestis lower than the fair value of the net assets of the subsidiary acquired and liabilities assumed, the differenceis recognized in profit or loss for the period.

Associates

Investments in associates are accounted for using the equity method unless they are classified as non-currentassets held for sale. Under this method, the carrying value of investments in associates is initially recognizedat the acquisition cost.

The carrying value of investments in associates is increased or decreased by the Company’s reported share inthe profit or loss and other comprehensive income of the investee after the acquisition date. The Company’sshare in the profit or loss and other comprehensive income of an associate is recognized in the Company’sconsolidated statement of profit or loss or in the consolidated statement of other comprehensive income,respectively. Dividends paid by the associate are accounted for as a reduction of the carrying value ofinvestments.

The Company’s net investments in associates include the carrying value of the investments in these associatesas well as other long-term investments that are, in substance, investments in associates, such as loans. If theshare in losses exceeds the carrying value of the investments in associates and the value of other long-terminvestments related to investments in these associates, the Company ceases to recognize its share in losseswhen the carrying value reaches zero. Any additional losses are provided for and liabilities are recognized onlyto the extent that the Company has legal or constructive obligations or has made payments on behalf of theassociate.

If the associate subsequently makes profits, the Company resumes recognizing its share in these profits onlyafter its share of the profits equals the share of losses not recognized.

The carrying value of investments in associates is tested for impairment by reconciling its recoverable amount(the higher of its value in use and fair value less costs to sell) to its carrying value, whenever impairmentindicators are identified.

Rosneft Oil Company

Notes to the Consolidated Financial Statements (continued)

17

3. Significant accounting policies (continued)

Joint arrangements

The Company participates in joint arrangements either in the form of joint ventures or joint operations.

A joint venture implies that the parties that have joint control of the arrangement have rights to the net assetsof the arrangement. A joint venture involves establishing a legal entity where the Company and otherparticipants have respective equity interests. Equity interests in joint ventures are accounted for under theequity method.

The Company’s share in net profit or loss and in other comprehensive income of joint ventures is recognizedin the consolidated statement of profit or loss and in the consolidated statement of other comprehensiveincome, respectively, from the date when joint control commences until the date when joint control ceases.A joint operation implies that the parties that have joint control of the arrangement have rights to the assets,and obligations for the liabilities, relating to the arrangement. In relation to its interest in a joint operation theCompany recognizes its assets, including its share of any assets held jointly, its liabilities, including its shareof any liabilities incurred jointly, its revenue from the sale of its share of the output arising from the jointoperation, its share of the revenue from the sale of the output by the joint operation, and expenses, includingits share of any expenses incurred jointly.

Cash and cash equivalents

Cash represents cash on hand, in the Company’s bank accounts, in transit and interest bearing deposits whichcan be effectively withdrawn at any time without prior notice or any penalties reducing the principal amountof the deposit. Cash equivalents are highly liquid, short-term investments that are readily convertible to knownamounts of cash and have original maturities of three months or less from their date of purchase. They arecarried at cost plus accrued interest, which approximates fair value. Restricted cash is presented separately inthe consolidated balance sheet if its amount is significant.

Financial assets

The Company recognizes financial assets in its balance sheet when, and only when, it becomes a party to thecontractual provisions of the financial instrument. When financial assets are recognized initially, they aremeasured at fair value, which is usually the price of the transaction, i.e. the fair value of consideration paid orreceived.

When financial assets are recognized initially, they are classified as one of the following, as appropriate:(1) financial assets at fair value through profit or loss, (2) loans issued and accounts receivable, (3) financialassets held to maturity, or (4) financial assets available for sale.

Financial assets at fair value through profit or loss include financial assets held for trading and financial assetsdesignated as financial assets at fair value through profit or loss at initial recognition. Financial assets held fortrading are those which are acquired principally for the purpose of sale or repurchase in the near future or arepart of a portfolio of identifiable financial instruments that have been commonly managed and for which thereis evidence of a recent pattern of actual short-term profit taking, or which are derivative instruments (unlessthe derivative instrument is defined as an effective hedging instrument). Financial assets at fair value throughprofit or loss are classified in the consolidated balance sheet as current assets and changes in the fair value arerecognized in the consolidated statement of profit or loss as Finance income or Finance expenses.

Rosneft Oil Company

Notes to the Consolidated Financial Statements (continued)

18

3. Significant accounting policies (continued)

Financial assets (continued)

All derivative instruments are recorded in the consolidated balance sheet at fair value in either current financialassets, non-current financial assets, current liabilities related to derivative instruments, or non-current liabilitiesrelated to derivative instruments. The recognition and classification of a gain or loss that results fromrecognition of an adjustment of a derivative instrument at fair value depends on the purpose for issuing orholding the derivative instrument. Gains and losses from derivatives that are not accounted for as hedges underInternational Accounting Standard (“IAS”) 39 Financial Instruments: Recognition and Measurement arerecognized immediately in the profit or loss for the period.

Fair value is the price that would be received to sell an asset or paid to transfer a liability in an orderlytransaction between market participants at the measurement date. Subsequent to initial recognition, the fairvalue of financial assets at fair value that are quoted in an active market is defined as bid prices for assets andask prices for issued liabilities as of the measurement date.

If no active market exists for financial assets, the Company measures the fair value using the followingmethods:

· analysis of recent transactions with peer instruments between independent parties;

· current fair value of similar financial instruments;

· discounting future cash flows.

The discount rate reflects the minimum return on investment an investor is willing to accept before starting analternative project, given its risk and the opportunity cost of forgoing other projects.

Loans issued and accounts receivable include non-derivative financial instruments with fixed or determinablepayments that are not quoted in an active market, not classified as financial assets held for trading and havenot been designated as at fair value through profit or loss or available for sale. If the Company cannot recoverall of its initial investment in the financial asset due to reasons other than deterioration of its quality, thefinancial asset is not included in this category. After initial recognition, loans issued and accounts receivableare measured at amortized cost using the effective interest rate method (“EIR"), less impairment losses. TheEIR amortization is included in Finance income in the consolidated statement of profit or loss. The lossesarising from impairment or gains from impairment reversals are recognized in the consolidated statement ofprofit or loss.

The Company does not classify financial assets as held to maturity if, during either the current financial yearor the two preceding financial years, the Company has sold, transferred or exercised a put option on more thanan insignificant (in relation to the total) amount of such investments before maturity, unless: (1) the financialasset was close enough to maturity or the call date so that changes in the market rate of interest did not have asignificant effect on the financial asset’s fair value; (2) after substantially all of the financial asset’s originalprincipal had been collected through scheduled payments or prepayments; or (3) due to an isolated non-recurring event that was beyond the Company’s control and could not have been reasonably anticipated by theCompany.

Dividends and interest income are recognized in the consolidated statement of profit or loss on an accrualbasis. The amount of accrued interest income is calculated using the effective interest rate.

All other financial assets not included in the other categories are designated as financial assets available forsale. Specifically, the shares of other companies not included in the first category are designated as availablefor sale. In addition, the Company may include any financial asset in this category at the initial recognition.

Rosneft Oil Company

Notes to the Consolidated Financial Statements (continued)

19

3. Significant accounting policies (continued)

Financial liabilities

The Company recognizes financial liabilities on its balance sheet when, and only when, it becomes a party tothe contractual provisions of the financial instrument. When financial liabilities are recognized initially, theyare measured at fair value, which is usually the price of the transaction, i.e. the fair value of consideration paidor received.

When financial liabilities are recognized initially, they are classified as one of the following:

· financial liabilities at fair value through profit or loss;

· other financial liabilities.

Financial liabilities at fair value through profit or loss are financial liabilities held for trading unless suchliabilities are linked to the delivery of unquoted equity instruments.

At the initial recognition, the Company may include in this category any financial liability, except for equityinstruments that are not quoted in an active market and whose fair value cannot be reliably measured. Afterinitial recognition, however, the liability cannot be reclassified.

Financial liabilities not classified as financial liabilities at fair value through profit or loss are designated asother financial liabilities. Other financial liabilities include, inter alia, trade and other accounts payable, andloans and borrowings payable.

Subsequent to initial recognition, financial liabilities at fair value through profit or loss are measured at fairvalue, with changes in fair value recognized in profit or loss in the consolidated statement of profit or loss.Other financial liabilities are carried at amortized cost.

The Company writes off a financial liability (or part of a financial liability) from its balance sheet when, andonly when, it is extinguished – i.e. when the obligation specified in the contract is discharged, cancelled orexpires. The difference between the carrying value of a financial liability (or a part of a financial liability)extinguished or transferred to another party and the redemption value, including any transferred non-monetaryassets and assumed liabilities, is recognized in profit or loss. Any previously recognized components of othercomprehensive income pertaining to this financial liability are also included in the financial result and arerecognized as gains and losses for the period.

Certain prior period indicators have been reclassified to conform to the current year presentation. In particular,due to significant increase in the operating activities of subsidiary banks of the Company and the need forreliable and consistent reporting in the consolidated financial statements, the presentation of cash flows fromthe operating activities of subsidiary banks was revised. Such activities are now included within operatingactivities of the Consolidated Statement of Cash Flows. Further, the operating assets of the subsidiary banks,including short-term interbank deposits placed, were reclassified to Accounts Receivable, operating liabilities,including interbank loans, customer deposits, promissory notes and REPO obligations reclassified from Loansand borrowings and other financial liabilities to Accounts payable and accrued liabilities.

Earnings per share

Basic earnings per share is calculated by dividing net earnings attributable to common shares by the weightedaverage number of common shares outstanding during the corresponding period. In the absence of anysecurities-to-shares conversion transactions, the amount of basic earnings per share stated in these consolidatedfinancial statements is equal to the amount of diluted earnings per share.

Rosneft Oil Company

Notes to the Consolidated Financial Statements (continued)

20

3. Significant accounting policies (continued)

Inventories

Inventories consisting primarily of crude oil, petroleum products, petrochemicals and materials and suppliesare accounted for at the weighted average cost unless net realizable value is less than cost. Materials that areused in production are not written down below cost if the finished products into which they will be incorporatedare expected to be sold above cost.

Repurchase and resale agreements

Securities sold under repurchase agreements (“REPO”) and securities purchased under agreements to resell(“reverse REPO”) generally do not constitute a sale of the underlying securities for accounting purposes, andso are treated as collateralized financing transactions. Interest paid or received on all REPO and reverse REPOtransactions is recorded in Finance expense or Finance income, respectively, at the contractually specified rateusing the effective interest method.

Exploration and production assets

Exploration and production assets include exploration and evaluation assets, mineral rights and oil and gasproperties (development assets and production assets).

Exploration and evaluation costs

The Company recognizes exploration and evaluation costs using the successful efforts method as permitted byIFRS 6 Exploration for and Evaluation of Mineral Resources. Under this method, costs related to explorationand evaluation (license acquisition costs, exploration and appraisal drilling) are temporarily capitalized in costcenters by field (well) until the drilling program results in the discovery of economically feasible oil and gasreserves.

The length of time necessary for this determination depends on the specific technical or economic difficultiesin assessing the recoverability of the reserves. If a determination is made that the well did not encounter oiland gas in economically viable quantities, the well costs are expensed to Exploration expenses in theconsolidated statement of profit or loss.

Exploration and evaluation costs, except for costs associated with seismic, topographical, geological, andgeophysical surveys, are initially capitalized as exploration and evaluation assets. Exploration and evaluationassets are recognized at cost less impairment, if any, as property, plant and equipment until the existence(or absence) of commercial reserves has been established. The initial cost of exploration and evaluation assetsacquired through a business combination is formed as a result of purchase price allocation. The cost allocationto mineral rights to proved properties and mineral rights to unproved properties is performed based on therespective oil and gas reserves information. Exploration and evaluation assets are subject to technical,commercial and management review as well as review for indicators of impairment at least once a year. Thisis to confirm the continued intent to develop or otherwise extract value from the discovery. When indicatorsof impairment are present, an impairment test is performed.

If, subsequently, commercial reserves are discovered, the carrying value, less losses from impairment of therespective exploration and evaluation assets, is classified as oil and gas properties (development assets).However, if no commercial reserves are discovered, such costs are expensed after exploration and evaluationactivities have been completed.

Rosneft Oil Company

Notes to the Consolidated Financial Statements (continued)

21

3. Significant accounting policies (continued)

Development and production

Oil and gas properties (development assets) are accounted for on a field-by-field basis and represent(1) capitalized costs to develop discovered commercial reserves and to put fields into production, and(2) exploration and evaluation costs incurred to discover commercial reserves reclassified from explorationand evaluation assets to oil and gas properties (development assets) following the discovery of commercialreserves.

The cost of oil and gas properties (development assets) also includes the expenditures to acquire such assets,directly identifiable overhead expenses, capitalized financing costs and related asset retirement(decommissioning) obligation costs. Oil and gas properties (development assets) are generally recognized asconstruction in progress.

Following the commencement of commercial production, oil and gas properties (development assets) arereclassified as oil and gas properties (production assets).

Other property, plant and equipment

Other property, plant and equipment is stated at historical cost as of the acquisition date, except for property,plant and equipment acquired prior to January 1, 2009, which is stated at deemed cost, net of accumulateddepreciation and impairment. The cost of maintenance, repairs, and the replacement of minor items of propertyis charged to operating expenses. Renewals and betterments of assets are capitalized.

Upon the sale or retirement of property, plant and equipment, the cost and related accumulated depreciationare eliminated from the accounts. Any resulting gains or losses are included in profit or loss.

Depreciation, depletion and amortization

Oil and gas properties are depleted using the unit-of-production method on a field-by-field basis starting fromthe commencement of commercial production.

In applying the unit-of-production method to mineral licenses, the depletion rate is based on total provedreserves. In applying the unit-of-production method to producing wells and the related oil and gasinfrastructure, the depletion rate is based on proved developed reserves.

Other property, plant and equipment are depreciated using the straight-line method over their estimated usefullives from the time they are ready for use, except for catalysts which are amortized using the unit-of-productionmethod.

Components of other property, plant and equipment and their respective estimated useful lives are as follows:

Property, plant and equipment Useful life, not more than

Buildings and structures 30-45 yearsPlant and machinery 5-25 yearsVehicles and other property, plant and equipment 6-10 yearsService vessels 20 yearsOffshore drilling assets 20 years

Land generally has an indefinite useful life and is therefore not depreciated.

Land leasehold rights are amortized on a straight-line basis over their expected useful life, which averages20 years.

Rosneft Oil Company

Notes to the Consolidated Financial Statements (continued)

22

3. Significant accounting policies (continued)

Construction grants

The Company recognizes construction grants from local governments when there is a reasonable assurancethat the Company will comply with the conditions attached and that the grant will be received. The constructiongrants are accounted for as a reduction of the cost of the asset for which the grant is received.

Impairment of non-current assets

The Company assesses at each balance sheet date whether there is any indication that an asset or cash-generating unit may be impaired. If any such indication exists, the Company estimates the recoverable amountof the asset or cash-generating unit.

In assessing whether there is any indication that an asset may be impaired, the Company considers internal andexternal sources of information. It considers at least the following:

External sources of information:

· during the period, an asset’s market value has declined significantly more than would be expected asa result of the passage of time or normal use;

· significant changes with an adverse effect on the Company have taken place during the period, or willtake place in the near future, in the technological, market, economic or legal environment in whichthe Company operates or in the market to which an asset is dedicated;

· market interest rates or other market rates of return on investments have increased during the period,and those increases are likely to affect the discount rate used in calculating an asset’s value in use anddecrease the asset’s recoverable amount materially;

· the carrying amount of the net assets of the Company is more than its market capitalization.

Internal sources of information:

· evidence is available of obsolescence or physical damage of an asset;

· significant changes with an adverse effect on the Company have taken place during the period, or areexpected to take place in the near future, in the extent to which, or manner in which, an asset is used oris expected to be used (e.g., the asset becoming idle, or the useful life of an asset is reassessed as finiterather than indefinite);

· information on dividends from a subsidiary, joint venture or associate;

· evidence is available from internal reporting that indicates that the economic performance of an asset is,or will be, worse than expected. Such evidence includes the existence of:

· cash flows on acquiring the asset, or subsequent cash needs for operating or maintaining it, thatare significantly higher than those originally budgeted;

· actual net cash flows or operating profit or loss flowing from the asset that are significantly worsethan those budgeted;

· a significant decline in budgeted net cash flows or operating profit, or a significant increase inbudgeted losses, flowing from the asset;

· operating losses or net cash outflows for the asset, when current period amounts are aggregatedwith budgeted amounts for the future.

Rosneft Oil Company

Notes to the Consolidated Financial Statements (continued)

23

3. Significant accounting policies (continued)

Impairment of non-current assets (continued)

The following factors indicate that exploration and evaluation assets may be impaired:

· the period for which the Company has the right to explore in the specific area has expired during theperiod or will expire in the near future, and is not expected to be renewed;

· substantive expenditure on further exploration for and evaluation of mineral resources in the specificarea is neither budgeted nor planned;

· exploration for and evaluation of mineral resources in the specific area have not led to the discovery ofcommercially viable quantities of mineral resources and the Company has decided to discontinue suchactivities in the specific area;

· sufficient data exist to indicate that, although a development in the specific area is likely to proceed, thecarrying amount of the exploration and evaluation asset is unlikely to be recovered in full fromsuccessful development or by sale.

The recoverable amount of an asset or a cash-generating unit is the higher of:

· the value in use of an asset (cash-generating unit); and

· the fair value of an asset (cash-generating unit) less costs to sell.

If the asset does not generate cash inflows that are largely independent of those from other assets, itsrecoverable amount is determined for the asset’s cash-generating unit.

The Company initially measures the value in use of a cash-generating unit. When the carrying amount ofa cash-generating unit is greater than its value in use, the Company measures the unit’s fair value forthe purpose of measuring the recoverable amount. When the fair value is less than the carrying value animpairment loss is recognized.

Value in use is determined by discounting the estimated value of the future cash inflows expected to be derivedfrom the asset or cash-generating unit, including cash inflows from its sale. The value of the future cash inflowsfrom a cash-generating unit is determined based on the forecast approved by management of the business unitto which the unit in question pertains.

Impairment of financial assets

At each balance sheet date the Company analyzes whether there is objective evidence of impairment for allcategories of financial assets, except those recorded at fair value through profit or loss. A financial asset ora group of financial assets is deemed to be impaired if there is objective evidence of impairment as a result ofone or more events that has occurred since the initial recognition of the asset (an incurred ‘loss event’) and thatloss event has an impact on the estimated future cash flows of the financial asset or the group of financialassets that can be reliably estimated. Evidence of impairment may include (but is not limited to) indicationsthat debtors or a group of debtors are experiencing financial difficulty, default or delinquency in interest orprincipal payments, the probability that they will enter bankruptcy or other financial reorganization andobservable data indicating that there is a measurable decrease in the estimated future cash flows, such aschanges in arrears or economic conditions that correlate with defaults.

Rosneft Oil Company

Notes to the Consolidated Financial Statements (continued)

24

3. Significant accounting policies (continued)

Capitalized interest

Interest expense on borrowed funds used for capital construction projects and the acquisition of property, plantand equipment is capitalized provided that the interest expense could have been avoided if the Company hadnot made capital investments. Interest is capitalized only during the period when construction activities areactually in progress and until the resulting properties are put into operation.

Capitalized borrowing costs include exchange differences arising from foreign currency borrowingsto the extent that they are regarded as an adjustment to interest costs.

Leasing agreements

Leases, which transfer to the Company substantially all the risks and benefits incidental to ownership ofthe asset, are classified as financial leases and are capitalized at the commencement of the lease at the fairvalue of the leased property or, if lower, at the present value of the minimum lease payments. Lease paymentsare apportioned between the finance expenses and reduction of the lease liability in order to achieve a constantrate of interest on the remaining balance of the liabilities. Finance expenses are charged directly to theconsolidated statement of profit or loss.

Leased property, plant and equipment are accounted for using the same policies applied to the Company’s ownassets. In determining the useful life of a leased item of property, plant and equipment, consideration is givento the probability of the title being transferred to the lessee at the end of the lease term.

If there is no reasonable certainty that the lessee will obtain ownership by the end of the lease term, the assetshall be fully depreciated over the shorter of the lease term and its useful life. Where such certainty exists, theasset is depreciated over its useful life.

Leases where the lessor retains substantially all the risks and benefits of ownership of the asset are classifiedas operating leases. Operating lease payments are recognized as an expense in the consolidated statement ofprofit or loss on a straight-line basis over the lease term.

Asset retirement (decommissioning) obligations

The Company has asset retirement (decommissioning) obligations associated with its core business activities.The nature of the assets and potential obligations are as follows:

The Company’s exploration, development and production activities involve the use of wells, related equipmentand operating sites, oil gathering and treatment facilities, tank farms and in-field pipelines. Generally, licensesand other regulatory acts require that such assets be decommissioned upon the completion of production.According to these requirements, the Company is obliged to decommission wells, dismantle equipment, restorethe sites and perform other related activities. The Company’s estimates of these obligations are based oncurrent regulatory or license requirements, as well as actual dismantling and other related costs. Theseliabilities are measured by the Company using the present value of the estimated future costs ofdecommissioning of these assets. The discount rate is reviewed at each reporting date and reflects currentmarket assessments of the time value of money and the risks specific to the liability.

Rosneft Oil Company

Notes to the Consolidated Financial Statements (continued)

25

3. Significant accounting policies (continued)

Asset retirement (decommissioning) obligations (continued)

In accordance with IFRS Interpretations Committee (“IFRIC”) Interpretation 1 Changes in ExistingDecommissioning, Restoration and Similar Liabilities, the provision is reviewed at each balance sheet date asfollows:

· upon changes in the estimates of future cash flows (e.g., the costs of and timeframe for abandoning onewell) or the discount rate, changes in the amount of the liability are included in the cost of the item ofproperty, plant, and equipment, whereby such cost may not be negative and may not exceed therecoverable value of the item of property, plant, and equipment;

· any changes in the liability due to its nearing maturity (change in the discount) are recognized in Financeexpenses.

The Company’s refining and distribution activities involve refining operations, marine and other distributionterminals, and retail sales. The Company’s refining operations consist of major petrochemical operations andindustrial complexes. Legal or contractual asset retirement (decommissioning) obligations related topetrochemical, oil refining and distribution activities are not recognized due to the limited history of suchactivities in these segments, the lack of clear legal requirements as to the recognition of obligations, as well asthe fact that decommissioning periods for such assets are not determinable.

Because of the reasons described above, the fair value of an asset retirement (decommissioning) obligation inthe refining and distribution segment cannot be reasonably estimated.

Due to continuous changes in the Russian regulatory and legal environment, there could be future changes tothe requirements and contingencies associated with the retirement of long-lived assets.

Income tax

Since 2012 Russian tax legislation has allowed income taxes to be calculated on a consolidated basis. The mainsubsidiaries of the Company were therefore combined into a consolidated group of taxpayers (Note 40). Forsubsidiaries which are not included in the consolidated group of taxpayers, income tax is calculated on anindividual subsidiary basis. Deferred income tax assets and liabilities are recognized in the accompanyingconsolidated financial statements in the amount determined by the Company in accordance with IAS 12Income Taxes.

Deferred tax is provided using the liability method on temporary differences at the reporting date between thetax bases of assets and liabilities and their carrying amounts for financial reporting purposes.

A deferred tax liability is recognized for all taxable temporary differences, except to the extent that the deferredtax liability arises from:

· the initial recognition of goodwill;

· the initial recognition of an asset or liability in a transaction which:

· is not a business combination; and

· affects neither accounting profit, nor taxable profit;

· investments in subsidiaries when the Company is able to control the timing of the reversal ofthe temporary differences and it is probable that the temporary differences will not reverse inthe foreseeable future.

Rosneft Oil Company

Notes to the Consolidated Financial Statements (continued)

26

3. Significant accounting policies (continued)

Income tax (continued)

A prior period tax loss planned to be used to reduce the current or future amount of income tax is recognizedas a deferred tax asset.

A deferred tax asset is recognized only to the extent that it is probable that taxable profit will be availableagainst which the deductible temporary differences can be utilized, unless the deferred tax asset arises fromthe initial recognition of an asset or liability in a transaction that:

· is not a business combination; and

· at the time of the transaction, affects neither accounting profit nor taxable profit (tax loss).

The Company recognizes deferred tax assets for all deductible temporary differences arising from investmentsin subsidiaries and associates, and interests in joint ventures, to the extent that the following two conditionsare met:

· the temporary difference will reverse in the foreseeable future; and

· taxable profit will be available against which the temporary difference can be utilized.

Deferred tax assets and liabilities shall be measured at the tax rates that are expected to apply to the periodwhen the asset is realized or the liability is settled, based on tax rates (and tax laws) that have been enacted orsubstantively enacted by the end of the reporting period.

The measurement of deferred tax assets and liabilities reflects the tax consequences that would follow fromthe manner in which the Company expects, at the end of the reporting period, to recover or settle the carryingamount of its assets and liabilities. Deferred tax assets and liabilities are offset when there is a legallyenforceable right to set off current tax assets against current tax liabilities and when they relate to income taxeslevied by the taxation authority of the same jurisdiction and the Company intends to settle its current tax assetsand liabilities on a net basis.

The carrying amount of a deferred tax asset is reviewed at each balance sheet date.

The Company reduces the carrying amount of a deferred tax asset to the extent that it is no longer probable thatsufficient taxable profit will be available to allow the benefit of part or all of that deferred tax asset to be utilized.

Deferred tax assets and liabilities are classified as Non-current Deferred tax assets and Non-current Deferredtax liabilities, respectively.

Deferred tax assets and liabilities are not discounted.

Recognition of revenues

Revenues are recognized when risks and rewards pass to the customer, which usually occurs when the titlepasses to the customer, provided that the contract price is fixed or determinable and collectability of thereceivable is reasonably assured. Specifically, domestic sales of crude oil and gas, as well as petroleumproducts and materials are usually recognized when title passes. For export sales, title generally passes at theborder of the Russian Federation and the Company covers transportation expenses (except freight), duties andtaxes on those sales (Note 10). Revenue is measured at the fair value of the consideration received or receivabletaking into account the amount of any trade discounts, volume rebates and reimbursable taxes.

Sales of support services are recognized as services are performed provided that the service price can bedetermined and no significant uncertainties regarding the receipt of revenues exist.

Rosneft Oil Company

Notes to the Consolidated Financial Statements (continued)

27

3. Significant accounting policies (continued)

Transportation expenses

Transportation expenses recognized in the consolidated statement of profit or loss represent all expensesincurred by the Company to transport crude oil for refining and to end customers, and to deliver petroleumproducts from refineries to end customers (these may include pipeline tariffs and any additional railroadtransportation costs, handling costs, port fees, sea freight and other costs).

Refinery maintenance costs

The Company recognizes the costs of overhauls and preventive maintenance performed with respect to oilrefining assets as expenses when incurred.

Environmental liabilities

Expenditures that relate to an existing condition caused by past operations, and do not have a future economicbenefit, are expensed. Liabilities for these expenditures are recorded when environmental assessments or clean-ups are probable and the costs can be reasonably estimated.

Accounting for contingencies

Certain conditions may exist as of the date of these consolidated financial statements which may further resultin a loss to the Company, but which will only be resolved when one or more future events occur or fail tooccur. The Company’s management makes an assessment of such contingent liabilities which is based onassumptions and is a matter of opinion. In assessing loss contingencies relating to legal or tax proceedings thatinvolve the Company or unasserted claims that may result in such proceedings, the Company, after consultationwith legal or tax advisors, evaluates the perceived merits of any legal or tax proceedings or unasserted claimsas well as the perceived merits of the amount of relief sought or expected to be sought therein.

If the assessment of a contingency indicates that it is probable that a loss will be incurred and the amount ofthe liability can be estimated, then the estimated liability is accrued in the Company’s consolidated financialstatements. If the assessment indicates that a potentially material loss contingency is not probable, but isreasonably possible, or is probable but cannot be estimated, then the nature of the contingent liability, togetherwith an estimate of the range of possible loss if determinable and material, would be disclosed.

Loss contingencies considered remote are generally not disclosed unless they involve financial guarantees, inwhich case the nature of the guarantee would be disclosed. However, in some instances in which disclosure isnot otherwise required, the Company may disclose contingent liabilities or other uncertainties of an unusualnature which, in the judgment of management after consultation with its legal or tax counsel, may be of interestto shareholders or others.

Taxes collected from customers and remitted to governmental authorities

Refundable taxes (excise and value-added tax (“VAT”)) are deducted from revenues. Other taxes and dutiesare not deducted from revenues and are recognized as expenses in Taxes other than income tax in theconsolidated statement of profit or loss.

VAT and excise receivable and payable are recognized as Prepayments and other current assets and Other taxliabilities in the consolidated balance sheet, respectively.

Rosneft Oil Company

Notes to the Consolidated Financial Statements (continued)

28

3. Significant accounting policies (continued)

Functional and presentation currency

The consolidated financial statements are presented in Russian rubles, which is the functional currency ofRosneft Oil Company and all of its subsidiaries operating in the Russian Federation. The functional currencyof the foreign subsidiaries is generally the U.S. dollar.

Transactions and balances

Foreign currency transactions are translated into the functional currency using the exchange rates prevailing atthe dates of these transactions. Foreign exchange gains and losses resulting from the settlement of suchtransactions and from the translation of monetary assets and liabilities denominated in foreign currenciesat year-end exchange rates are recognized in the profit or loss for the period.

Foreign exchange gains and losses resulting from the translation of monetary assets and liabilities designatedas foreign currency cash flow hedging instruments are recognized within other comprehensive income andreclassified to profit or loss in the period when the hedged item affects profit or loss.

Non-monetary items that are measured in terms of historical cost in a foreign currency are translated using theexchange rates as at the dates of the initial transactions. Non-monetary items measured at fair value in a foreigncurrency are translated using the exchange rates at the date when the fair value is determined.

The Company’s subsidiaries

The results and financial position of all of the Company’s subsidiaries, joint ventures and associates that havea functional currency which is different from the presentation currency are translated into the presentationcurrency as follows:

· assets and liabilities for each balance sheet presented are translated at the closing rate at thatreporting date;

· income and expenses for each statement of profit or loss and each statement of other comprehensiveincome are translated at average exchange rates (unless this average is not a reasonable approximationof the cumulative effect of the rates prevailing on the transaction dates, in which case income andexpenses are translated at the rate on the dates of the transactions); and

· all resulting exchange differences are recognized as a separate component of other comprehensiveincome.

Prepayment on oil and petroleum products supply agreements

In the course of business the Company enters into long-term oil supply contracts. The contract termsmay require the buyer to make a prepayment.

The Company considers long-term oil supply contracts to be regular-way sale contracts entered into andcontinued to be held for the purpose of the receipt or delivery of non-financial items in accordance withthe Company’s expected purchase, sale or usage requirements. Regular-way sale contracts are exempted fromthe scope of IAS 32 Financial Instruments: Presentation and IAS 39 Financial Instruments: Recognition andMeasurement.

Rosneft Oil Company

Notes to the Consolidated Financial Statements (continued)

29

3. Significant accounting policies (continued)

Prepayment on oil and petroleum products supply agreements (continued)

Conditions for meeting the definition of a regular-way sale are not met if either of the following applies:

· the ability to settle net in cash or another financial instrument, or by exchanging financial instruments,is not explicit in the terms of the contract, but the Company has a practice of settling similar contractsnet in cash or via another financial instrument or by exchanging financial instruments (whether withthe counterparty, by entering into offsetting contracts or by selling the contract before its exerciseor lapse);

· for similar contracts, the Company has a practice of taking delivery of the underlying goods and sellingthem within a short period after delivery for the purpose of generating a profit from short-termfluctuations in price or from a dealer’s margin.

Prepayments for the delivery of goods or respective deferred revenue are accounted for as non-financialliabilities because the outflow of economic benefits associated with them is the delivery of goods and servicesrather than a contractual obligation to pay cash or another financial asset.

Changes in accounting policies and disclosures

The accounting policies adopted are consistent with those of the previous financial year except for the adoptionof new standards and interpretations effective as of January 1, 2017.

The following amendments were applied for the first time in 2017:

· Disclosure Initiative – amendments to IAS 7 Statement of Cash Flows. The amendments requirecompanies to provide a reconciliation of financing cash flows in the statement of cash flows to theopening and closing balances of liabilities arising from financing activities (except for equity balances)in the statement of financial position. The above mentioned reconciliation is presented in Note 31 “Loansand borrowings and other financial liabilities”.

· Deferred Tax Assets for Unrealised Losses – amendments to IAS 12 Income Taxes. These amendmentsclarify how to account for deferred tax assets related to debt instruments measured at fair value.

Application of these amendments had no significant impact on the Company’s financial position or results ofoperations.

Certain prior period balances have been reclassified to conform to the current year presentation.

4. Significant accounting judgments, estimates and assumptions

The preparation of consolidated financial statements requires management to make a number of accountingestimates and assumptions that affect the reported amounts of assets and liabilities and the disclosureof contingent assets and liabilities. The actual results, however, could differ from those estimates.

Rosneft Oil Company

Notes to the Consolidated Financial Statements (continued)

30

4. Significant accounting judgments, estimates and assumptions (continued)

The most significant accounting estimates and assumptions used by the Company’s management in preparingthe consolidated financial statements include:

· estimation of oil and gas reserves;

· estimation of rights to, recoverability and useful lives of non-current assets;

· impairment of goodwill (Note 25 “Intangible assets and goodwill”);

· allowances for doubtful accounts receivable and obsolete and slow-moving inventories(Note 21 “Accounts receivable” and Note 22 “Inventories”);

· assessment of asset retirement (decommissioning) obligations (Note 3 “Significant accounting policies”,section: “Asset retirement (decommissioning) obligations”, and Note 32 “Provisions”);

· assessment of legal and tax contingencies, recognition and disclosure of contingent liabilities(Note 40 “Contingencies”);

· assessment of deferred income tax assets and liabilities (Note 3 “Significant accounting policies”,section: “Income tax”, and Note 16 “Income tax”);

· assessment of environmental remediation obligations (Note 32 “Provisions” and Note 40 “Contingencies”);

· fair value measurements (Note 37 “Fair value of financial instruments”);

· assessment of the Company’s ability to renew operating leases and to enter into new lease agreements;

· purchase price allocation to the identifiable assets acquired and the liabilities assumed(Note 7 “Acquisition of subsidiaries and shares in joint operations”).

Significant estimates and assumptions affecting the reported amounts are those used in determiningthe economic recoverability of reserves.

Such estimates and assumptions may change over time when new information becomes available, e.g.:

· more detailed information on reserves was obtained (either as a result of more detailed engineeringcalculations or additional exploration drilling activities);

· supplemental activities to enhance oil recovery were conducted;

· changes were made in economic estimates and assumptions (e.g. a change in pricing factors).

5. New and amended standards and interpretations issued but not yet effective

In May 2014, the IASB issued IFRS 15 Revenue from Contracts with Customers. IFRS 15 establishes a singleframework for revenue recognition and contains requirements for related disclosures. The new standardreplaces IAS 18 Revenue, IAS 11 Construction Contracts, and the related interpretations on Revenuerecognition. The standard is effective for annual periods beginning on or after January 1, 2018. In April 2016,the IASB issued amendments to IFRS 15, which have the same effective date as the new standard: January 1,2018. As a result of the analysis performed by the Company, the conclusion was made that there will be nosignificant impact of the standard on the consolidated financial statements.

Rosneft Oil Company

Notes to the Consolidated Financial Statements (continued)

31

5. New and amended standards and interpretations issued but not yet effective (continued)

In July 2014, the IASB issued the final version of IFRS 9 Financial Instruments. The final version of IFRS 9replaces IAS 39 Financial Instruments: Recognition and Measurement, and all previous versions of IFRS 9.IFRS 9 brings together the requirements for the classification and measurement, impairment and hedgeaccounting of financial instruments. In respect of impairment, IFRS 9 replaces the “incurred loss” model usedin IAS 39 with a new “expected credit loss” model that will require a more timely recognition of expectedcredit losses. The standard is effective for annual periods beginning on or after January 1, 2018. In October2017, the IASB issued amendments to IFRS 9 effective on January 1, 2019.

The Company is currently assessing the impact of the standard on the opening balance of retained earnings asof January 1, 2018 as a result of the shift from the “incurred loss” impairment model to “expected credit loss”model, аs well as the change in classification for certain significant financial assets of the Company – from the“amortized cost” category to the “fair value through profit or loss” category.

In September 2014, the IASB issued amendments to IFRS 10 Consolidated Financial Statements and IAS 28Investments in Associates and Joint Ventures entitled Sale or Contribution of Assets between an Investor andits Associate or Joint Venture. These narrow scope amendments clarify that a full gain or loss is recognizedwhen a transaction involves a business (whether it is housed in a subsidiary or not), and a partial gain or lossis recognized when a transaction involves assets that do not constitute a business. The IASB has postponed thedate by when the entities must change these aspects of accounting for transactions between investors and equityaccounted investees. Application of the amendments, initially planned for annual periods beginning on or afterJanuary 1, 2016, has been deferred. The Company does not expect the amendments to have a material impacton the consolidated financial statements, as their requirements are already incorporated in the accountingpolicy of the Company.

In January 2016, the IASB issued IFRS 16 Leases. IFRS 16 eliminates the classification of leases as eitheroperating leases or finance leases and establishes a single lessee accounting model. The most significant effectof the new requirements for the lessee will be an increase in lease assets and financial liabilities. The newstandard replaces the previous leases standard, IAS 17 Leases, and the related interpretations. The standard iseffective for annual periods beginning on or after January 1, 2019, with earlier application permitted forcompanies that also apply IFRS 15 Revenue from Contracts with Customers. The Company is currentlyassessing the impact of the standard on the consolidated financial statements.

In June 2016, the IASB issued amendments to IFRS 2 Share-based Payment entitled Classification andMeasurement of Share-based Payment Transactions. The amendments provide requirements for theaccounting for the effects of vesting and non-vesting conditions on the measurement of cash-settled share-based payments; share-based payment transactions with a net settlement feature for withholding taxobligations; a modification to the terms and conditions of a share-based payment that changes the classificationof the transaction from cash-settled to equity-settled. The amendments are effective for annual periodsbeginning on or after January 1, 2018, with earlier application permitted. The Company does not expect theamendments to have a material impact on the consolidated financial statements.

In September 2016, the IASB issued amendments to IFRS 4 Insurance Contracts entitled Applying IFRS 9Financial Instruments with IFRS 4 Insurance Contracts. The amendments address concerns arising fromimplementing the new financial instruments Standard, IFRS 9, before implementing the replacement Standardthat the Board is developing for IFRS 4. The amendments introduce two approaches, which should reconcilethe timing of the application of the two new standards. Under the first approach, the amendments becomeeffective on the date of first-time adoption of IFRS 9; under the second, the amendments become effective forannual periods beginning on or after January 1, 2018. The Company does not expect the amendments to havea material impact on the consolidated financial statements.

Rosneft Oil Company

Notes to the Consolidated Financial Statements (continued)

32

5. New and amended standards and interpretations issued but not yet effective (continued)

In December 2016, the IASB issued IFRIC 22 Interpretation entitled Foreign Currency Transactions andAdvance Consideration. The IFRIC addresses how to determine the date of the transaction for the purpose ofdetermining the exchange rate to use on initial recognition of the related asset, expense or income (or part ofit) on the derecognition of a non-monetary asset or non-monetary liability arising from the payment or receiptof advance consideration in a foreign currency. IFRIC 22 is effective for annual periods beginning on or afterJanuary 1, 2018, with earlier application permitted. The Company does not expect the amendments to have amaterial impact on the consolidated financial statements as their requirements are already incorporated in theaccounting policy of the Company.

In December 2016, the IASB issued amendments to IAS 40 Investment Property entitled Transfers ofInvestment Property. The amendments clarify the requirements for transfers to, or from, investment property.The amendments are effective for annual periods beginning on or after January 1, 2018, with earlier applicationpermitted. The Company does not expect the amendments to have a material impact on the consolidatedfinancial statements.

In May 2017, the IASB issued IFRS 17 Insurance Contracts. IFRS 17 establishes a single framework for theaccounting for insurance contracts and contains requirements for related disclosures. The new standardreplaces IFRS 4 Insurance Contracts. The standard is effective for annual periods beginning on or afterJanuary 1, 2021. The Company does not expect the standard to have a material impact on the consolidatedfinancial statements.

In June 2017, the IASB issued IFRIC 23 Interpretation entitled Uncertainty over Income Tax Treatments. TheIFRIC clarifies that for the purposes of calculating current and deferred tax, companies should use a taxtreatment of uncertainties, which will probably to be accepted by the tax authorities. IFRIC 23 is effective forannual periods beginning on or after January 1, 2019. The Company does not expect the amendments to havea material impact on the consolidated financial statements.

In October 2017, the IASB issued amendments to IAS 28 Investments in Associates and Joint Ventures. Theseamendments clarify that the companies should apply IFRS 9 Financial Instruments, including impairmentrequirements, for the long-term investments in associates and joint ventures, which are accounted for otherwisethan using the equity method, including long-term loans given to associates and joint ventures. Theamendments are effective for annual periods beginning on or after January 1, 2019, with earlier applicationpermitted. The impact of the amendments was assessed within the assessment of the impact ofIFRS 9 Financial Instruments (see above).

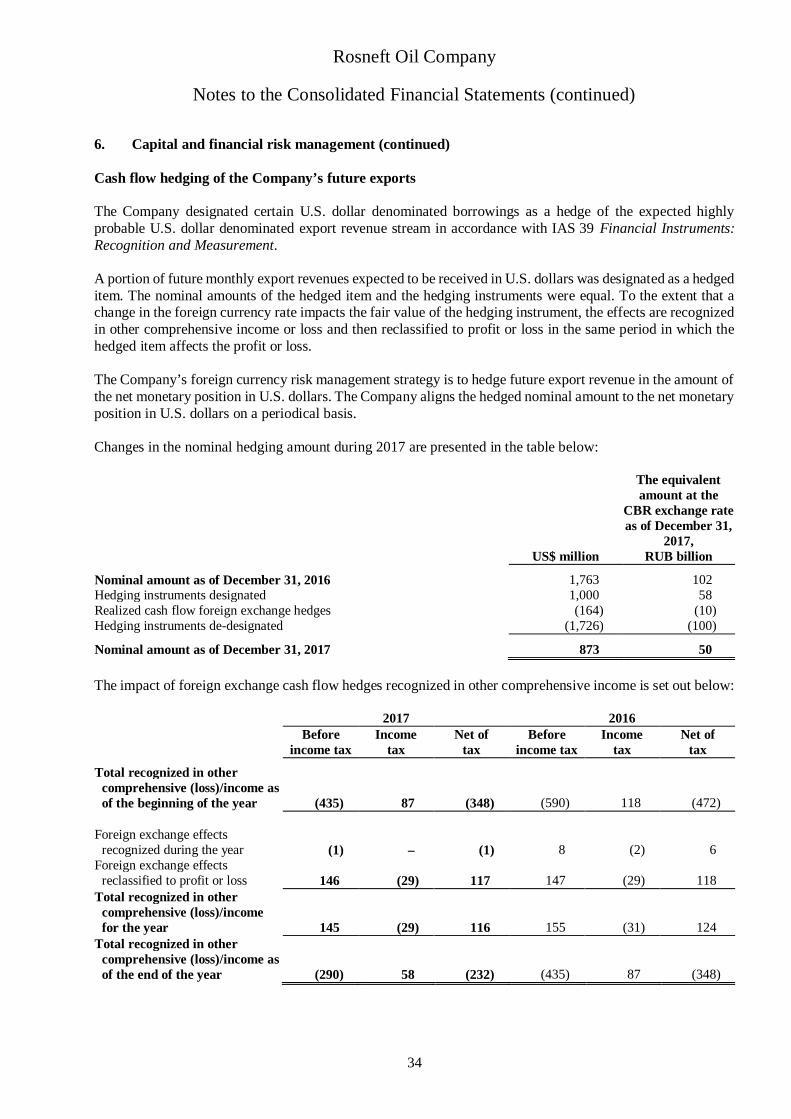

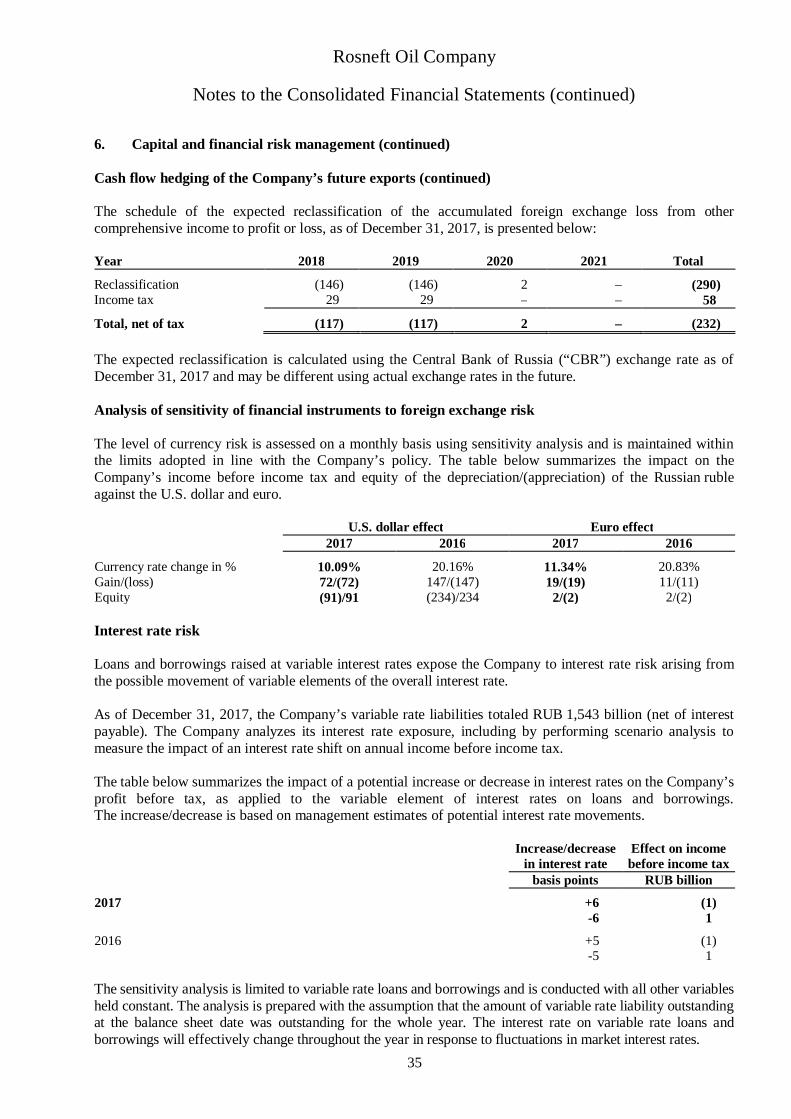

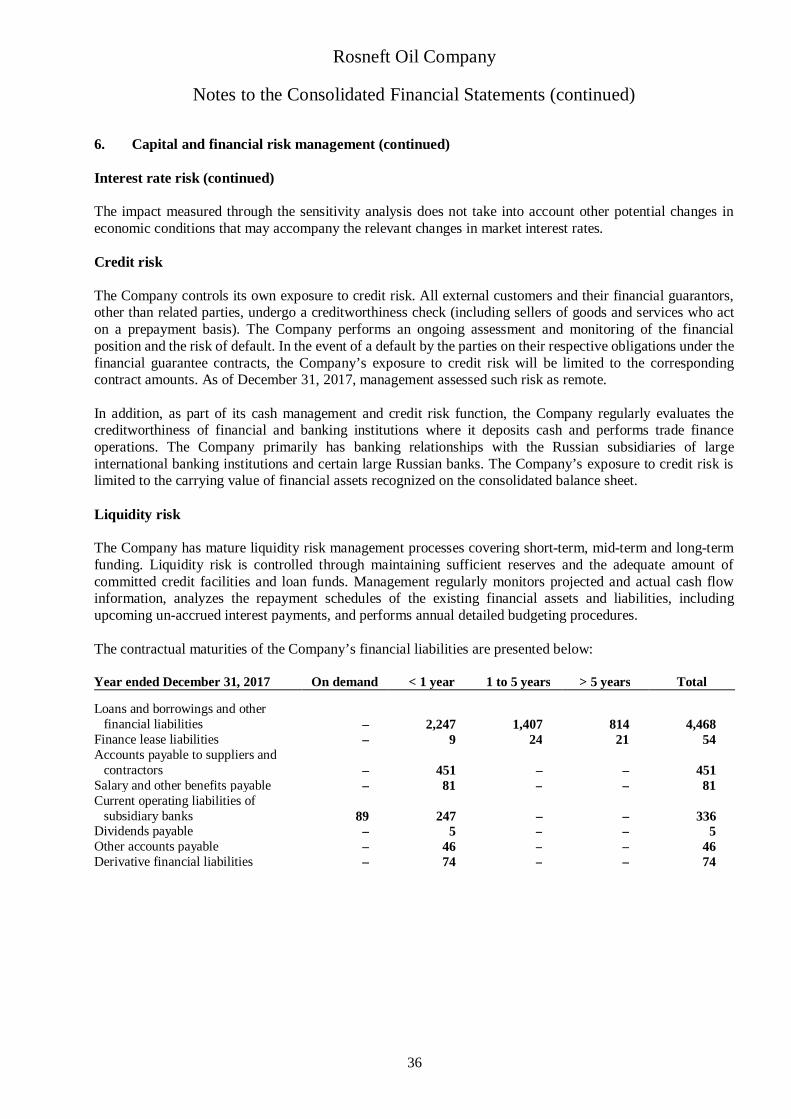

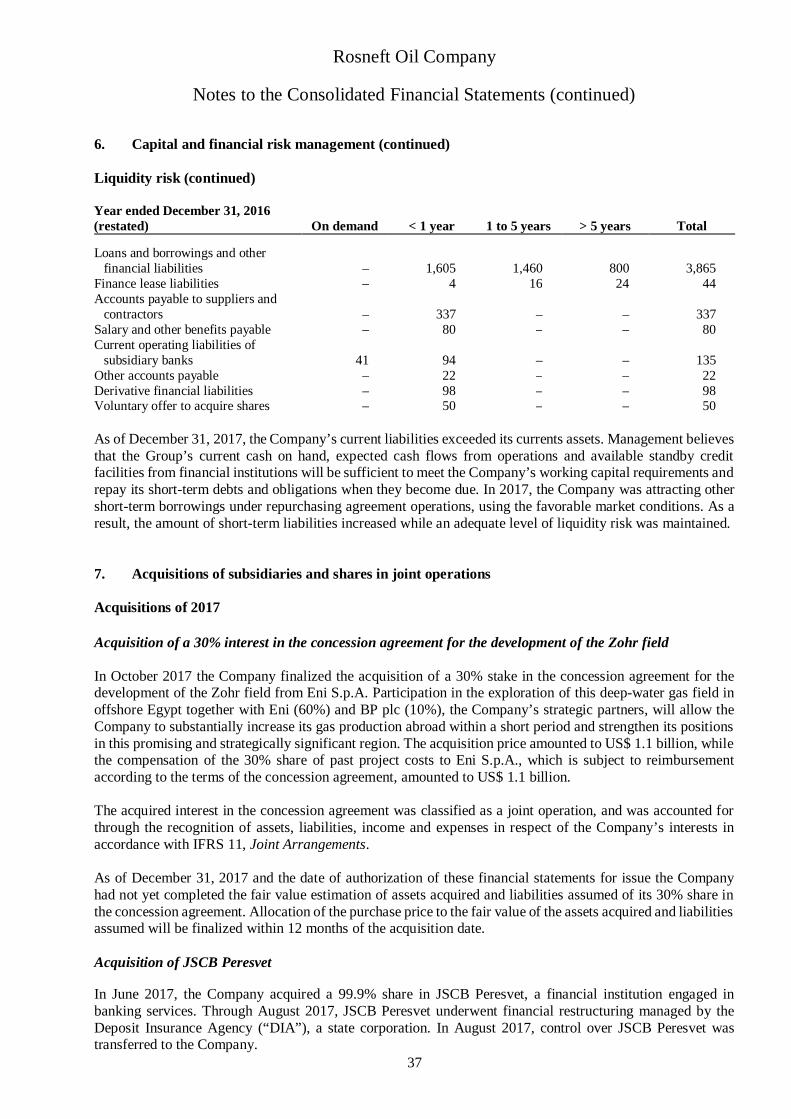

6. Capital and financial risk management

Capital management

The Company’s capital management objectives are to ensure its ability to continue as a going concern and tooptimize the cost of capital in order to enhance value to shareholders. Total capital employed and financialliabilities less liquid financial assets are non-IFRS measure.

The Company’s management performs a regular assessment of the financial liabilities less liquid financialassets to capital employed ratio to ensure it meets the Company’s requirements to fulfil the Company’scommitments and to retain strong financial stability.

Rosneft Oil Company

Notes to the Consolidated Financial Statements (continued)

33

6. Capital and financial risk management (continued)

Capital management (continued)

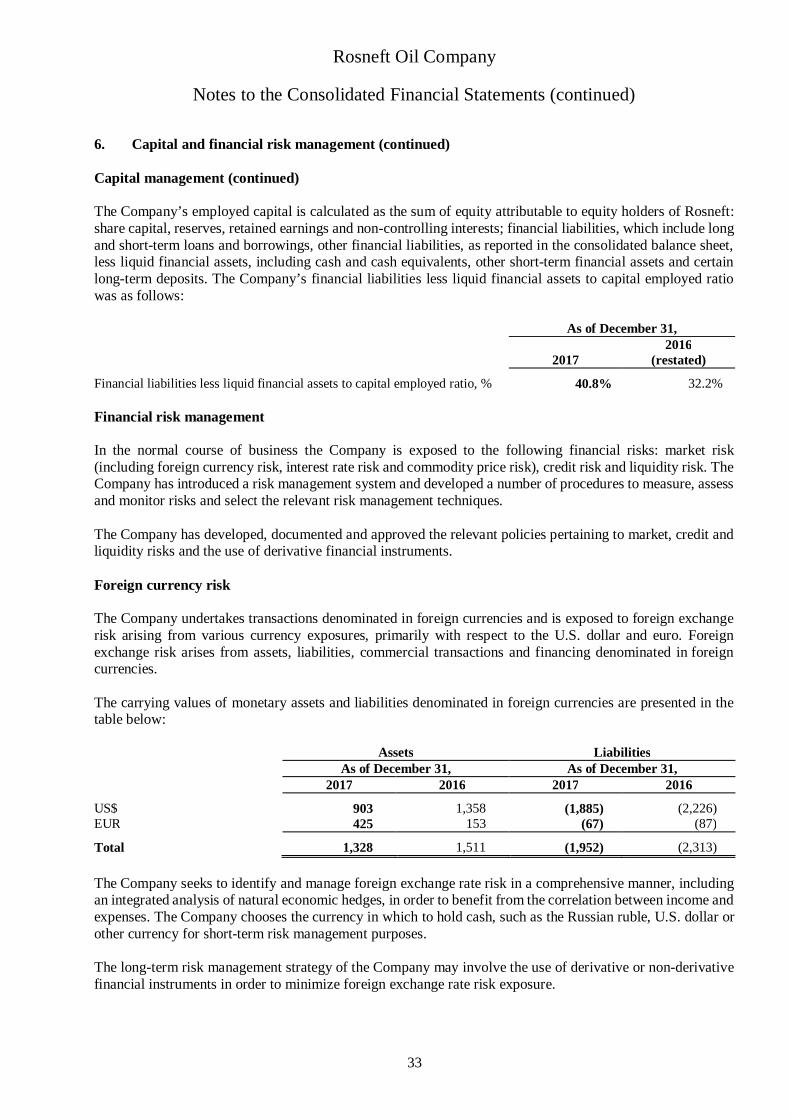

The Company’s employed capital is calculated as the sum of equity attributable to equity holders of Rosneft:share capital, reserves, retained earnings and non-controlling interests; financial liabilities, which include longand short-term loans and borrowings, other financial liabilities, as reported in the consolidated balance sheet,less liquid financial assets, including cash and cash equivalents, other short-term financial assets and certainlong-term deposits. The Company’s financial liabilities less liquid financial assets to capital employed ratiowas as follows:

As of December 31,

20172016

(restated)

Financial liabilities less liquid financial assets to capital employed ratio, % 40.8% 32.2%

Financial risk management

In the normal course of business the Company is exposed to the following financial risks: market risk(including foreign currency risk, interest rate risk and commodity price risk), credit risk and liquidity risk. TheCompany has introduced a risk management system and developed a number of procedures to measure, assessand monitor risks and select the relevant risk management techniques.

The Company has developed, documented and approved the relevant policies pertaining to market, credit andliquidity risks and the use of derivative financial instruments.

Foreign currency risk

The Company undertakes transactions denominated in foreign currencies and is exposed to foreign exchangerisk arising from various currency exposures, primarily with respect to the U.S. dollar and euro. Foreignexchange risk arises from assets, liabilities, commercial transactions and financing denominated in foreigncurrencies.

The carrying values of monetary assets and liabilities denominated in foreign currencies are presented in thetable below:

Assets LiabilitiesAs of December 31, As of December 31,

2017 2016 2017 2016

US$ 903 1,358 (1,885) (2,226)EUR 425 153 (67) (87)

Total 1,328 1,511 (1,952) (2,313)