Consolidated Financial Statements and - Asia Pacific Fibers · resolution of the secured debt...

137

Consolidated Financial Statements and Independent Auditors’ Report PT Asia Pacific Fibers Tbk And Its Subsidiaries December 31, 2016 and 2015

Transcript of Consolidated Financial Statements and - Asia Pacific Fibers · resolution of the secured debt...

Consolidated Financial Statements and

Independent Auditors’ Report

PT Asia Pacific Fibers Tbk

And Its Subsidiaries

December 31, 2016 and 2015

CONTENTS

Board of Directors’ Statement

Independent Auditors’ Report

Page

Consolidated Financial Statements

Consolidated Statements of Financial Position 1

Consolidated Statements of Profit or Loss and Other Comprehensive Income 4

Consolidated Statements of Changes in Equity 5

Consolidated Statements of Cash Flows 6

Notes to the Consolidated Financial Statements 7 – 126

Additional Financial Information 1 – 6

Financial Statements – Parent Entity Only Appendix

Statements of Financial Position 1

Statements of Profit or Loss and Other Comprehensive Income 4

Statemenst of Changes in Equity 5

Statements of Cash Flows 6

INDEPENDENT AUDITORS’ REPORT

No.: 042/02/WA/III/17

The Shareholders, Board of Commissioners and Directors

PT ASIA PACIFIC FIBERS Tbk.

We have audited the accompanying consolidated financial statements of PT Asia Pacific Fibers Tbk

(the “Company”) and its subsidiaries, which comprise the consolidated statement of financial position as of

December 31, 2016, and the consolidated statements of profit or loss and other comprehensive income, changes

in equity and cash flows for the year then ended, and a summary of significant accounting policies and other

explanatory information.

Management’s responsibility for the consolidated financial statements

Management is responsible for the preparation and fair presentation of such consolidated financial statements

in accordance with Indonesian Financial Accounting Standards, and for such internal control as management

determines is necessary to enable the preparation of consolidated financial statements that are free from

material misstatement, whether due to fraud or error.

Auditors’ responsibility

Our responsibility is to express an opinion on such consolidated financial statements based on our audit. We

conducted our audit in accordance with Standards on Auditing established by the Indonesian Institute of

Certified Public Accountants. Those standards require that we comply with ethical requirements and plan and

perform the audit to obtain reasonable assurance about whether such consolidated financial statements are free

from material misstatement.

An audit involves performing procedures to obtain audit evidence about the amounts and disclosures in the

consolidated financial statements. The procedures selected depend on the auditors’ judgment, including the

assessment of the risks of material misstatement of the consolidated financial statements, whether due to fraud

or error. In making those risk assessments, the auditors consider internal control relevant to the entity’s

preparation and fair presentation of the consolidated financial statements in order to design audit procedures

that are appropriate in the circumstances, but not for the purpose of expressing an opinion on the effectiveness

of the entity’s internal control. An audit also includes evaluating the appropriateness of accounting policies

used and the reasonableness of accounting estimates made by management, as well as evaluating the overall

presentation of the consolidated financial statements.

We believe that the audit evidence we have obtained is sufficient and appropriate to provide a basis for our

audit opinion.

Opinion

In our opinion, the accompanying consolidated financial statements present fairly, in all material respects, the

consolidated financial position of PT Asia Pacific Fibers Tbk and its subsidiaries as of December 31, 2016,

and their consolidated financial performance and cash flows for the year then ended, in accordance with

Indonesian Financial Accounting Standards.

Page 2

Emphasis of matter

The accompanying consolidated financial statements have been prepared assuming the Company and its

Subsidiaries will continue as a going concern. As disclosed in Note 2 to the consolidated financial statements,

as of December 31, 2016, the Company and its Subsidiaries had capital deficiency of US$ 937,566,161, while

the current liabilities exceeded its total assets by US$ 877,548,446. Total current liabilities as of

December 31, 2016 of US$ 1,108,697,962 (85% of total current liabilities) represent the secured debts. In

October 2016, the Company has submitted a revised Secured Debt Restructuring Plan (SDRP) to Secured

Creditors, but until the issuance of this consolidated financial statements, the Company has not received the

response from its Secured Creditors. In addition to that, as of the date of this report, one of the Company’s

secured creditors is PT Perusahaan Pengelola Assets (PPA) (26%) has not yet given its approval on the

restructuring plan proposed by the Company. However, Damiano Investments BV., Netherland, majority

shareholder of the Company (57.85% ownership) and majority secured debt holder (92.5%) have provided

capital expenditure facility of US$ 23,570,000 and letter of credit facility of US$ 85,729,859 for raw materials

procurement.

Damiano Investmen BV., Netherland has commited to provide the necessary financial support to the Company

to enable it to continue as a going concern. The Company’s management also continues to exert effort and

expects to obtain the resolution of the secured debt restructuring in order for the Company to obtain working

capital from banks. The consolidated financial statements do not include any adjustments that might result

from the outcome of this uncertainty.

As disclosed in Note 51 to the accompanying consolidated financial statements, the Company’s management

reclassified certain accounts on the consolidated statements of financial position as of the earliest comparative

period January 1, 2015/December 31, 2014 to conform with the presentation of consolidated financial position

as of December 31, 2016. Our audit opinion is not modified in respect of this matter.

Other matter

Our audit of the accompanying consolidated financial statements of the Company and its Subsidiaries as of

December 31, 2016 and for the year then ended was performed for the purpose of forming an opinion on such

consolidated financial statements taken as a whole. The accompanying financial information of PT Asia Pacific

Fibers Tbk (parent entity only), which comprises the statement of financial position as of December 31, 2016,

and the statements of profit or loss and other comprehensive income, changes in equity and cash flows for the

year then ended (collectively referred to as the “Parent Entity Financial Information”), which is presented as a

supplementary information to the accompanying consolidated financial statements, is presented for the purpose

of additional analysis and is not a required part of the accompanying consolidated financial statements under

Indonesian Financial Accounting Standards. The Parent Entity Financial Information is the responsibility of

management and was derived from and relates directly to the underlying accounting and other records used to

prepare the accompanying consolidated financial statements. The Parent Entity Financial Information has been

subjected to the auditing procedures applied in the audit of the accompanying consolidated financial statements

in accordance with Standards on Auditing established by the Indonesian Institute of Certified Public

Accountants. In our opinion, the Parent Entity Financial Information is fairly stated, in all material respects, in

relation to the accompanying consolidated financial statements taken as a whole.

HENDRAWINATA EDDY SIDDHARTA& TANZIL

Welly Adrianto, CPA

No. Ijin Akuntan Publik. AP. 0060

Jakarta, March 17, 2017

PT ASIA PACIFIC FIBERS Tbk

AND ITS SUBSIDIARIES

CONSOLIDATED STATEMENTS OF FINANCIAL POSITION

December 31, 2016, December 31, 2015 and January 1, 2015/December 31, 2014

1

Notes

December 31,

2 0 1 6

December 31,

2 0 1 5 *)

January 1,

2 0 1 5/

December 31,

2014*)

US$ US$ US$

ASSETS

CURRENT ASSETS

Cash and cash equivalents 3f,g,5 3,468,469 2,657,148 6,184,094

Trade receivables, net of allowance for

impairment of US$ 15,657,945 in 2016, 2015

and 2014

Third parties 3f,h,j,6 31,584,686 31,567,047 41,190,159

Related party 3f,h,j,6 – – –

Other receivables, net of allowance for

impairment of US$ 67,637,756 in 2016, 2015

and 2014

Third parties 3f,h,j,7 3,032,953 2,787,973 3,426,117

Other current financial assets 3f,h,j,8 5,906,063 5,969,375 8,693,988

Inventories 3k,9 59,691,450 61,164,596 75,507,062

Purchase advances

Third parties 10 2,330,122 6,076,917 2,338,194

Related party – – 56,031

Prepaid taxes 3v,27a 10,178,297 11,419,541 15,902,785

Prepaid expenses 3l,11 1,828,659 2,128,943 2,520,486

Total Current Assets 118,020,699 123,771,540 155,818,916

NON–CURRENT ASSETS

Non-trade receivables, net of allowance

for impairment of US$ 111,962,653 in 2016,

2015, and 2014

Third party 3f,h,j,12 39,574,362 39,032,631 45,294,138

Related party – – –

Other non-current financial assets 3f,h,j,13 998,945 991,274 1,022,539

Property, plant and equipment, net of

accumulated depreciation of US$ 1,713,765,001

in 2016, US$ 1,709,106,418 in 2015, and

US$ 1,703,166,009 in 2014 3m,n,p,14 69,647,040 61,876,082 61,365,864

Intangible Assets 3o,p,15 107,316 113,590 119,866

Deferred tax assets 3v,27d 2,801,154 6,710,119 11,750,587

Total Non–Current Assets 113,128,817 108,723,696 119,552,994

TOTAL ASSETS 231,149,516 232,495,236 275,371,910

*) As reclassified

See Note 51

The accompanying notes to the consolidated financial statements

are an integral part of the consolidated financial statements

Jakarta, March 17, 2017

Vasudevan Ravi Shankar Bonar Firman Hasiholan Sirait

President Director Director

PT ASIA PACIFIC FIBERS Tbk

AND ITS SUBSIDIARIES

CONSOLIDATED STATEMENTS OF FINANCIAL POSITION (Continued)

December 31, 2016, December 31, 2015 and January 1, 2015/December 31, 2014

2

Notes

December 31,

2 0 1 6

December 31,

2 0 1 5 *)

January 1,

2 0 1 5/

December 31,

2014*)

US$ US$ US$

LIABILITIES AND EQUITY

(CAPITAL DEFICIENCY)

CURRENT LIABILITIES

Trade payables

Third parties 3r,16 11,986,713 12,241,858 25,584,407

Accrued expenses 3r,17 56,917,886 50,446,641 49,969,699

Taxes payable 3v,27b 145,695 149,767 159,621

Bank Loans 3r,18 85,729,859 88,135,716 88,250,457

Secured Debts 3r,19 947,993,134 945,081,879 957,675,525

Short – term employee benefits liabilities 3u,25 532,715 366,276 433,562

Current portion of long-term liabilities:

Credit financing payables 3q,r,22 41,718 41,379 56,131

Other short-term financial liabilities 3r,23 5,350,242 5,357,542 4,716,794

Total Current Liabilities 1,108,697,962 1,101,821,058 1,126,846,196

NON–CURRENT LIABILITIES

Borrowing from Other Financial Institutions:

Unsecured Debts and Notes Payable 3r,20 25,024,969 24,032,636 23,082,193

Working capital loans 3r,21 23,570,000 22,070,000 22,070,000

Credit financing payables 3q,r,22 67,977 5,940 47,253

Deferred revenues 3t,24 199,962 212,526 225,089

Long-term employee benefits liabilities 3u,26 11,154,807 9,759,801 12,125,149

Total Non–Current Liabilities 60,017,715 56,080,903 57,549,684

Total Liabilities 1,168,715,677 1,157,901,961 1,184,395,880

*) As reclassified

See Note 51

The accompanying notes to the consolidated financial statements

are an integral part of the consolidated financial statements

Jakarta, March 17, 2017

Vasudevan Ravi Shankar Bonar Firman Hasiholan Sirait

President Director Director

PT ASIA PACIFIC FIBERS Tbk

AND ITS SUBSIDIARIES

CONSOLIDATED STATEMENTS OF FINANCIAL POSITION (Continued)

December 31, 2016, December 31, 2015 and January 1, 2015/December 31, 2014

3

Notes

December 31,

2 0 1 6

December 31,

2 0 1 5 *)

January 1,

2 0 1 5/

December 31,

2014*)

US$ US$ US$

LIABILITIES AND EQUITY

(CAPITAL DEFICIENCY)

EQUITY (DEFICIENCY)

Share Capital

Authorized 12,357,255,040 shares at Rp 10,000 par value per Series A, Rp 1,000 par value

per Series B and Rp 40 par value per Series C in 2016, 2015 and 2014

Issued and paid up 219,696,000 Series A and

2,276,057,347 Series C in 2016, 2015, and 2014 28 635,689,316 635,689,316 635,689,316

Additional paid-in capital 3w,29 624,323,168 624,323,168 624,323,168

Retained earnings (Accumulated deficit)

Appropriated 30 2,345,301 2,345,301 2,345,301

Unappropriated (2,199,923,946 ) (2,187,764,510 ) (2,171,381,755 )

Total Capital Deficiency (937,566,161 ) (925,406,725 ) (909,023,970 )

TOTAL LIABILITIES AND

EQUITY (CAPITAL DEFICIENCY)

231,149,516

232,495,236

275,371,910

*) As reclassified

See Note 51

The accompanying notes to the consolidated financial statements

are an integral part of the consolidated financial statements

Jakarta, March 17, 2017

Vasudevan Ravi Shankar Bonar Firman Hasiholan Sirait

President Director Director

PT ASIA PACIFIC FIBERS Tbk

AND ITS SUBSIDIARIES

CONSOLIDATED STATEMENTS OF PROFIT OR LOSS

AND OTHER COMPREHENSIVE INCOME

For the years ended December 31, 2016 and 2015

4

Notes 2 0 1 6 2 0 1 5

US$ US$

REVENUES

Net sales 3x,34 355,748,940 387,053,770

Other operating revenues 3x,35 4,731,812 3,002,226

Total revenues 360,480,752 390,055,996

COST OF GOODS SOLD 3x,36 (342,580,203 ) (381,902,793 )

GROSS PROFIT 17,900,549 8,153,203

General and administrative expenses 3x,39 (15,386,149 ) (14,399,308 )

Finance costs 3x,40 (4,451,148 ) (7,863,850 )

Selling expenses 3x,38 (7,999,603 ) (10,786,487 )

Gain (loss) on foreign exchange transactions, net 3c (3,884,345 ) 11,236,898

Insurance claim settlement, net 3x,33 5,638,402 1,703,128

Gain on sale or disposal of property, plant and equipment 3x 28,669 −

Miscellaneous income, net 3x,41 1,174,884 309,069

(24,879,290 ) (19,800,550 )

LOSS BEFORE INCOME TAX (6,978,741 ) (11,647,347 )

TAX EXPENSE 3v

Current period 27c (883,641 ) (1,566,830 )

Deferred 27d (4,005,987 ) (4,572,495 )

Total tax expense 27e (4,889,628 ) (6,139,325 )

TOTAL LOSS FOR THE YEAR (11,868,369 ) (17,786,672 )

OTHER COMPREHENSIVE INCOME (LOSS),

NET AFTER TAX

Items that will not be reclassified to profit or loss:

Remeasurement of post employment benefit obligations (388,089 ) 1,871,890

Related income tax benefit (expense) 97,022 (467,973 )

Total Other Comprehensive Income (Loss), net of tax (291,067 ) 1,403,917

TOTAL COMPREHENSIVE LOSS FOR THE YEAR (12,159,436 ) (16,382,755 )

PT ASIA PACIFIC FIBERS Tbk

AND ITS SUBSIDIARIES

CONSOLIDATED STATEMENTS OF PROFIT OR LOSS

AND OTHER COMPREHENSIVE INCOME (Continued)

For the years ended December 31, 2016 and 2015

5

Notes 2 0 1 6 2 0 1 5

US$ US$

Total Net Loss Attributable to the Owners

of the Company

(11,868,369

)

(17,786,672

)

Total Comprehensive Loss Attributable to the Owners

of the Company

(12,159,436

)

(16,382,755

)

EARNING (LOSS) PER SHARE: 3y

Basic 31 (0.004 ) (0.006 )

Diluted 31 (0.004 ) (0.006 )

The accompanying notes to the consolidated financial statements

are an integral part of the consolidated financial statements

Jakarta, March 17, 2017

Vasudevan Ravi Shankar Bonar Firman Hasiholan Sirait

President Director Director

PT ASIA PACIFIC FIBERS Tbk

AND ITS SUBSIDIARIES

CONSOLIDATED STATEMENTS OF CHANGES IN EQUITY

For the years ended December 31, 2016 and 2015

6

Retained Earnings

(Accumulated deficit)

Notes

Share Capital

Additional

paid-in capital

Appropriated

Unappropriated

Total Equity

(Capital

Deficiency)

US$ US$ US$ US$ US$

Balance as of December 31, 2014 635,689,316 624,323,168 2,345,301 (2,171,381,755 ) (909,023,970 )

Total loss for the year – – – (17,786,672 ) (17,786,672 )

Other comprehensive income, net after tax – – – 1,403,917 1,403,917

Balance as of December 31, 2015 635,689,316 624,323,168 2,345,301 (2,187,764,510 ) (925,406,725 )

Total loss for the year – – – (11,868,369 ) (11,868,369 )

Other comprehensive loss, net after tax – – – (291,067 ) (291,067 )

Balance as of December 31, 2016 635,689,316 624,323,168 2,345,301 (2,199,923,946 ) (937,566,161 )

PT ASIA PACIFIC FIBERS Tbk

AND ITS SUBSIDIARIES

CONSOLIDATED STATEMENTS OF CASH FLOWS

For the years ended December 31, 2016 and 2015

7

Notes 2 0 1 6 2 0 1 5

US$ US$

CASH FLOWS FROM OPERATING ACTIVITIES

Receipt from customers 359,942,630 401,800,894

Payment to suppliers (253,401,986 ) (288,202,470 )

Payment of salaries (8,830,852 ) (8,702,467 )

Other operating cash payments, net (88,909,037 ) (96,818,606 )

Cash provided by operations 8,800,755 8,077,351

Interest received 7,40 23,557 22,622

Interest expense and bank charges paid 17,40 (3,824,705 ) (7,221,113 )

Cash receipt from insurance claim settlement 7,33 5,688,253 1,703,128

Payment of income tax 27 (2,175,977 ) (4,475,260 )

Refund of income tax 27 5,426,618 4,747,807

Net Cash Provided By Operating Activities 13,938,501 2,854,535

CASH FLOWS FROM INVESTING ACTIVITIES

Payment to acquire property, plant and equipment 14,22 (12,431,261 ) (6,450,627 )

Proceed from sale of property, plant and equipment 14,41 28,669 –

Net Cash Used In Investing Activities (12,402,592 ) (6,450,627 )

CASH FLOWS FROM FINANCING ACTIVITIES

Receipt of working capital loans 21 1,500,000 –

Payment of bank loans 18 (2,405,857 ) (114,741 )

Payment of credit financing payables 22 (69,829 ) (56,065 )

Net Cash Used In Financing Activities (975,686 ) (170,806 )

NET INCREASE (DECREASE) IN CASH

AND CASH EQUIVALENTS

560,223

(3,766,898

)

EFFECT OF FOREIGN EXCHANGE RATE 251,098 239,952

CASH AND CASH EQUIVALENTS

AT BEGINNING OF YEAR

5

2,657,148

6,184,094

CASH AND CASH EQUIVALENTS

AT END OF YEAR

5

3,468,469

2,657,148

PT ASIA PACIFIC FIBERS Tbk

AND ITS SUBSIDIARIES

NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTS

December 31, 2016 and 2015

8

1. GENERAL

a. Establishment and General Information

PT Asia Pacific Fibers Tbk (“the Company”) is engaged in manufacturing of chemical and synthetic

fiber, weaving and knitting, and other activities related to the textile industry. The Company has 2

(two) manufacturing plants, and marketed its product in both domestically and internationally, such as

in Europe, United States of America, Asia, Australia and the Middle East.

PT Asia Pacific Fibers Tbk was established within the framework of Domestic Capital Investment

Law No. 6 of year 1968 as amended by Law No. 12 of year 1970 based on notarial deed No. 22 dated

February 15, 1984 of Januar Tirtaamidjaja, S.H., public notary in Jakarta. The above laws were

subsequently amended by the Limited Liability Company Law of Republic of Indonesia No. 40 in year

2007 dated August 16, 2007. The deed of establishment was approved by the Minister of Justice of

Republic of Indonesia based on decision letter No. C2–6107.HT.01.01.TH.84 dated October 26, 1984

and was published in Supplement No. 3247 of State Gazette No. 72 dated September 7, 1990.

The Article of Association has been amended based on notarial deed No. 92 dated March 24, 2009 of

Sutjipto, S.H., notary in Jakarta to adjust the Company’s Article of Association with Bapepam-LK No.

IX.J.1 dated May 14, 2008 concerning the Principles of Association of Public Offering of Conduct

Equity Securities and Public Companies. The deed of establishment was approved by the Minister of

Justice of Republic of Indonesia based on decision letter No. AHU-0052618.AH.01.09.Tahun 2009

dated August 14, 2009.

The Articles of Association have been amended based on notarial deed No. 50 dated September 10,

2009 of Sutjipto, S.H., public notary in Jakarta, concerning the change in the Company’s name from

PT Polysindo Eka Perkasa Tbk to PT Asia Pacific Fibers Tbk. The deed was approved by the Minister

of Law and Human Rights of the Republic Indonesia based on decision letter No.

AHU-54294.AH.01.02.Tahun 2009 dated November 10, 2009 and the publishment in Supplement No.

21449 of State Gazette No. 77 dated September 24, 2010.

The Company’s Articles of Association have been amended based on the notarial deed No. 107 dated

February 23, 2012 of Aryanti Artisari, S.H., M.Kn., public notary in Jakarta, concerning the

implemented the Management Employee Stock Option Programme (MESOP) based on the Capital

Market and Financial Institution Supervisory Agency (BAPEPAM-LK)’s Regulation No. IX.D.4. The

deed was approved by the Minister of Law and Human Rights of Republic Indonesia based on decision

letter No. AHU-0018443.AH.01.09.Tahun 2012 dated February 29, 2012.

The Articles of Association have been amended several times. The latest amendment of the Company’s

Articles of Association was based on the notarial deed No. 30 dated July 7, 2015 of Aryanti Artisari,

S.H., M.Kn., notary in Jakarta to adjust the Company’s Article of Association with the regulation from

Otoritas Jasa Keuangan. The deed of establishment was approved by the Minister of Justice of

Republic of Indonesia based on decision letter No. AHU-AH.01.03-0954603.Tahun 2015 dated

July 31, 2015.

On February 4, 2011, the Company obtained the approval from Chairman of the Capital Investment

Coordinating Board (BKPM) in his letter No. 2/B/II/PMDN/2011 with regard to the cancellation of

approval from Chairman of the Capital Investment Coordinating Board (BKPM) in his letter

No. 249/II/PMDN.1997 dated December 2, 1997.

PT ASIA PACIFIC FIBERS Tbk

AND ITS SUBSIDIARIES

NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTS (Continued)

December 31, 2016 and 2015

9

1. GENERAL (Continued)

a. Establishment and General Information (Continued)

Further, the Company has received the approval of Chairman of the Capital Investment Coordinating

Board (BKPM) for the expansion of the Fibre capacity in Karawang side through the approval letter

No. 2/B/II/PMDN/2011 dated February 24, 2011. This project has started in the second quarter of

2012.

In accordance with Article 3 of Company’s Article of Association, the Company’s objectives and

scope of activities is mainly to engage in the manufacturing of chemical and synthetic fiber, weaving

and knitting, and other activities related to the textile industry. The Company is domiciled in Kendal,

Central Java with its plants located in Kendal, Central Java and Karawang, West Java. The Company’s

representative office is located at The East Building, 35th Floor, Jl. DR. Ide Anak Agung Gde Agung

(formerly Jalan Lingkar Mega Kuningan) Kav. E-3.2 No. 1, Jakarta. The Company started its

commercial operations in 1986.

The Company has many ongoing social activities in the local environs of its two plant location in

Semarang and Karawang which the purpose of this activity is to improve the livelihood of the

surrounding communities. In order to carry out these programmes more effectively, the Company has

established a foundation “Yayasan Asia Pacific Fibre” on January 15, 2010. The deed was approved

by the Minister of Justice and Human Rights of Republic of Indonesia based on decision letter

No. AHU-960.AH.01.04.Tahun 2010 dated March 15, 2010.

The Company’s immediate parent company is Damiano Investments BV., incorporated in Netherland,

and its ultimate parent company is ADM Capital and Spinnaker Capital Group, incorporated and

domiciled in Hong Kong and United Kingdom, respectively.

b. Public Offering of Shares, Notes Payable of the Company and its Subsidiaries

On December 14, 1990, the Company offered 12,000,000 shares to the public through Jakarta and

Surabaya Stock Exchanges, now known as Indonesian Stock Exchange.

On October 8, 1993, the Company obtained the notice of effectively from the Chairman of Capital

Market Supervisory Agency (BAPEPAM), in his letter No. S-1738/PM/1993, for its limited

offering of 184,000,000 shares through rights issue with preemptive rights to stockholders. These

shares were listed in Jakarta and Surabaya Stock Exchanges on November 1, 1993.

On December 15, 1994, the Company obtained the notice of effectively from the Chairman of

BAPEPAM, in his decision letter No. S-2027/PM/1994, for the change of par value from Rp 1,000

to Rp 500 per share.

On May 20, 1996, the Company obtained the notice of effectively from the Chairman of

BAPEPAM, in his decision letter No. S-778/PM/1996, for its offering of 1,104,000,000 shares

through rights issue II with preemptive rights to stockholders. These shares were listed in Jakarta

and Surabaya Stock Exchanges on June 10, 1996.

PT ASIA PACIFIC FIBERS Tbk

AND ITS SUBSIDIARIES

NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTS (Continued)

December 31, 2016 and 2015

10

1. GENERAL (Continued)

b. Public Offering of Shares, Notes Payable of the Company and its Subsidiaries (Continued)

On December 11, 1997, the Company obtained the notice of effectively from the Chairman of

BAPEPAM, in his decision letter No. S-2844/PM/1997, for its offering of 2,185,920,000 shares

through rights issue III with preemptive rights to stockholders. These shares were listed in Jakarta

and Surabaya Stock Exchanges on January 5, 1998.

In 1994, the Company issued US$ 125,000,000 Unsecured Senior Notes which are listed in

Luxembourg. In 1996, the Company offered to the holders of said unsecured notes to exchange

their notes with US$ 125,000,000 Guaranteed Senior Notes issued by PIFC with the Company as

the guarantor. These notes were listed in Luxembourg Stock Exchange.

In 1996, PIFC, with the Company as a guarantor, also issued US$ 50,000,000 Secured Floating

Rate Notes and US$ 260,000,000 Guaranteed Secured Notes which were listed in Luxembourg

Stock Exchange.

In 1997, PIFC, with the Company as a guarantor, issued US$ 250,000,000 Guaranteed Secured

Notes which were listed in Luxembourg Stock Exchange.

Since January 2000, the above notes issued by PIFC were delisted from Luxembourg Stock

Exchange.

Beginning of December 2004, all of the Company’s outstanding shares totaling 4,393,920,000

shares were suspended regarding the bankruptcy proceeding against the Company and delay in

submitting the required consolidated financial statements. The Company’s shares were still

suspended after the Company removes their bankruptcy. However, the Company took efforts to

remove its suspension which includes submitting Company’s future plan of actions. Further in

July 2006, all of the Company’s shares resumed trading.

In 2006, the Company converted the unsecured debt amounted to 43,144,238,750 shares as part

of the implementation of Composition Plan which have been approved and ratified by the

Commercial Court. Based on the condition issued by Indonesian Stock Exchange, the new shares

cannot be traded for 1 (one) year. Further in October 2007, the new Company’s shares were traded.

Based on the Extraordinary General Stockholders Meeting (RUPSLB) held on February 21, 2008,

the stockholders approved the reverse stock split (split down) with a ratio of 20:1 wherein 20 old

shares will become 1 new share. Reverse stock splits are conducted for the Company’s shares to

be more liquid and in line with the Company’s performance. Due to the changes in the Company’s

number of shares and par value, the Company amended its Articles of Association and the notarial

deed regarding the changes of the Company’s Article of Association had been approved by the

Minister of Justice and Human Rights on March 3, 2008. Further, based on the notarial deed of

Sutjipto, S.H., No. 122 dated February 27, 2008 regarding shares purchase as the result of reverse

stock split named PT Trimegah Securities Tbk as “Stand by Buyer”. In addition, all shares from

reverse stock were traded on March 14, 2008.

PT ASIA PACIFIC FIBERS Tbk

AND ITS SUBSIDIARIES

NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTS (Continued)

December 31, 2016 and 2015

11

1. GENERAL (Continued)

b. Public Offering of Shares, Notes Payable of the Company and its Subsidiaries (Continued)

On October 10, 2008, the Subsidiary’s shares (PT Texmaco Jaya Tbk) have been delisted from the

Indonesian Stock Exchange based on its letter No. S-04741/BEI.PSR/09/2008 and

Peng-004/BEI.PSR/DEL/09-2008 due to the suspension of trading shares and going concern

problem of the Subsidiary.

Since December 2, 2009, the Company’s shares in Indonesian Stock Exchange have been changed

with the new Company’s name.

Based on the Extraordinary General Stockholders Meeting (RUPSLB) held on March 24, 2009

and based on notarial deed No. 91 dated March 24, 2009 of Sutjipto, S.H., public notary in Jakarta,

the stockholders approved the issuance of 118,845,397 new authorized shares series C (5% of

issued and paid-up capital) without preemptive rights, for providing stock options to the

Company’s management and employees (Management Employee Stock Option Programme /

MESOP). The notarial deed was approved by the Minister of Justice of Republic of Indonesia

based on his decision letter No. AHU-0052619.AH.01.09.Tahun 2009 dated August 14, 2009. As

per the Company’s schedule that was reported to Indonesian Stock Exchange dated

March 17, 2009, its programme has been implemented at the latest period (February 1, 2012).

Further, based on the notarial deed No. 107 dated February 23, 2012 of

Aryanti Artisari, S.H., M.Kn., public notary in Jakarta, the Management Employee Stock Option

Programme / MESOP has been implemented with the execution price of Rp 45 each. All shares

under MESOP have been fully paid up through the Company’s bank accounts dated February 20

and February 21, 2012. It has been registered in the Indonesian Stock Exchange through

announcement No. Peng-P-00032/BEI.PPR/03-2012 dated March 5, 2012 and No. Peng-P-

00033/BEI.PPR/03-2012 dated March 7, 2012.

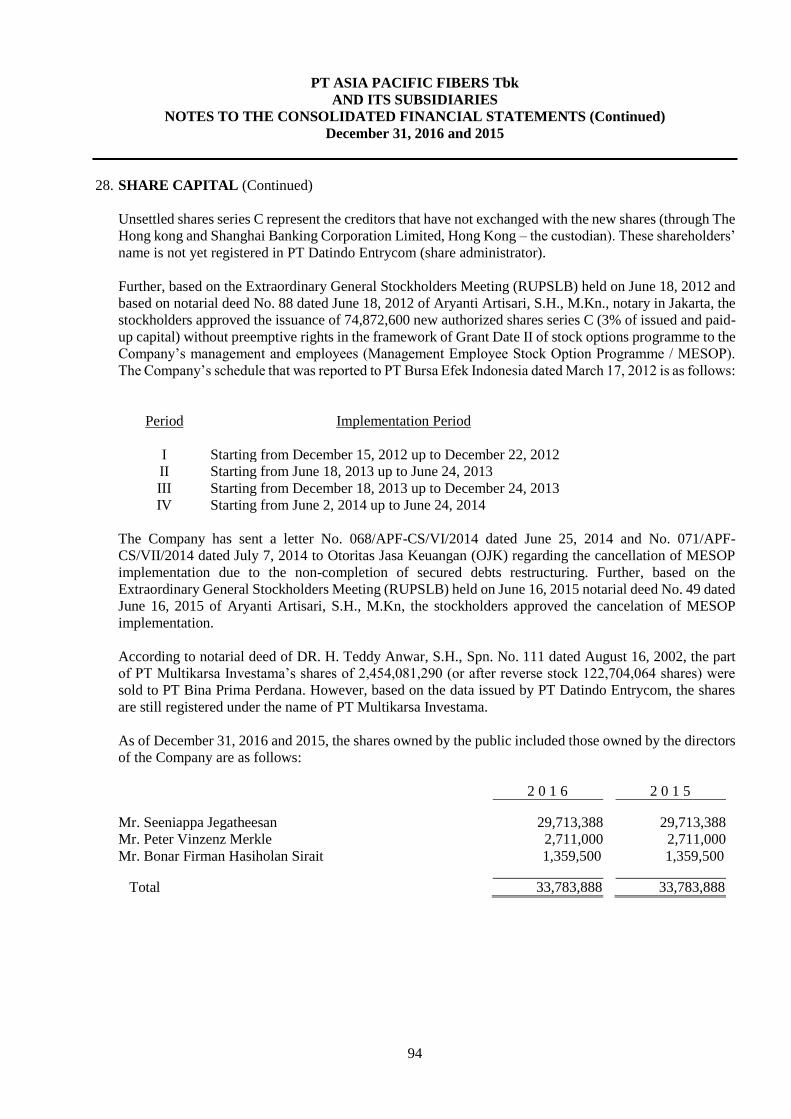

Based on the Extraordinary General Stockholders Meeting (RUPSLB) held on June 18, 2012 and

based on the notarial deed No. 88 dated June 18, 2012 of Aryanti Artisari, S.H., M.Kn., public

notary in Jakarta, the stockholders approved the issuance of 74,872,600 new authorized shares

series C (3% of issued and paid-up capital) without preemptive rights, for providing stock options

to the Company’s management and employees (Management Employee Stock Option Programme

/ MESOP). The Company has sent a letter No. 068/APF-CS/VI/2014 dated June 25, 2014 and

No. 071/APF-CS/VII/2014 dated July 7, 2014 to Otoritas Jasa Keuangan (OJK) regarding the

cancelation of MESOP implementation due to the debt restructuring is not completed so the

Company’s market price is decreasing. Based on the Extraordinary General Stockholders Meeting

(RUPSLB) held on June 16, 2015 notarial deed No. 49 dated June 16, 2015 of Aryanti Artisari

S.H., M.Kn, the stockholders approved the cancelation of MESOP implementation.

PT ASIA PACIFIC FIBERS Tbk

AND ITS SUBSIDIARIES

NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTS (Continued)

December 31, 2016 and 2015

12

1. GENERAL (Continued)

c. Subsidiaries

The Company has the following non-active subsidiaries are as follows:

Commercial Percentage of Total Assets

Subsidiaries Domicile Nature of Business Operations Ownership 2 0 1 6 2 0 1 5

% US$ US$

(in million) (in million)

PT Texmaco

Jaya Tbk (TJ)

Karawang Trading, weaving,

knitting and processing

1972 92.00 *) *)

PT Texmaco Graha Jakarta Trading of textile and 1994 91.08 *) *)

Busana (TGB) producing ready to

(99% owned by TJ) wear garments and

accessories

Polysindo International

Finance Company

BV (PIFC)

Netherlands Financial services 1994 100.00 759 759

Polysindo (Mauritius)

Ltd. (PML)

Republic of

Mauritius

Financial services Pre-

operating

100.00 – –

*) Not applicable due to PT Texmaco Jaya Tbk (TJ) and PT Texmaco Graha Busana (TGB) have been deconsolidated.

In 2001, the Company acquired 10,000 shares which represent 100% ownership in Polysindo

(Mauritius) Ltd. The shares were acquired for the amount of US$ 10,000. The difference between

the acquisition cost and the net assets of PML amounted to Rp 221,924,188 (equivalent to

US$ 21,339) was recorded as “difference on restructuring among companies under common

control” account as part of the additional paid-in capital in the consolidated statements of financial

position (Note 29).

There were no transactions between the Company and Polysindo (Maurutius) Ltd and Polysindo

International Finance Company BV during 2015 and 2014. The Company intends to close the

operation of its subsidiaries along with the restructuring of the Company.

Since April 2008, PT Texmaco Jaya Tbk (TJ) operations (Fleece division) are conducted by the

Company with tolling basis.

Since the second semester of 2004, PT Texmaco Graha Busana has halted its business operations.

PT ASIA PACIFIC FIBERS Tbk

AND ITS SUBSIDIARIES

NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTS (Continued)

December 31, 2016 and 2015

13

1. GENERAL (Continued)

d. Boards of Commissioners and Directors, Audit Committee and Employees (Continued)

The composition of board of commissioners, directors and audit committee (key management) of

the Company as of December 31, 2016 is based on the notarial deed No. 13 dated August 9, 2016

of Aryanti Artisari, S.H., M.Kn., notary in Jakarta.

The composition of the Company’s board of commissioners and directors as of December 31,

2016 and 2015 are as follows:

2 0 1 6 2 0 1 5

Board of Commissioners:

President Commissioner : Mr Robert Clive Appleby Mr. Robert Clive Appleby

Independent Commissioners : Mr. Ir. Agus Tjahajana

Wirakusumah

Mr. Ir. Agus Tjahajana

Wirakusumah

Mr. Dono Iskandar Djojosubroto Mr. Dono Iskandar Djojosubroto

Commissioners : Mr. Christoper Ian Teague Mrs. Cheong Kamun

Mr. Christopher Robert Botsford Mr. Christopher Robert Botsford

Mr. Robert Mc Carthy Mr. Robert Mc Carthy

Board of Directors:

President Director : Mr. Vasudevan Ravi Shankar Mr. Vasudevan Ravi Shankar

Independent Directors : Mr. Bonar Firman Hasiholan

Sirait

Mr. Bonar Firman Hasiholan

Sirait

Mr. Antonius Widyatma Sumarlin Mr. Antonius Widyatma Sumarlin

Directors : Mr. Seeniappa Jegatheesan Mr. Seeniappa Jegatheesan

Mr. Peter Vinzenz Merkle Mr. Peter Vinzenz Merkle

To comply with BAPEPAM regulation No. IX.1.5 regarding the forming and work guidance of

Audit Committee, the Board of Commissioners has formed Audit Committee.

The members of the Company’s Audit Committee as of December 31, 2016 and 2015 are as

follows:

Chairman : Mr. Dono Iskandar Djojosubroto

Member : Mr. Doedy Darwin

Mr. Deddy Sutrisno

The Company’s corporate secretary as of December 31, 2016 and 2015 is Mr Tunaryo.

In February 2009, the Company formed an internal audit department to comply with

BAPEPAM-LK regulation. The head of internal audit is Mr. Yohanes Baptis Galuh Adjar

Pamungkas.

PT ASIA PACIFIC FIBERS Tbk

AND ITS SUBSIDIARIES

NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTS (Continued)

December 31, 2016 and 2015

14

1. GENERAL (Continued)

d. Boards of Commissioners and Directors, Audit Committee and Employees (Continued)

As at December 31, 2016, the Company had 3,338 permanent employees (2015: 3,062 permanent

employees). And as at December 31, 2016 and 2015, the Subsidiaries do not have permanent

employees.

e. Approval and Authorization for Issuance of Consolidated Financial Statements

The consolidated financial statements of the Company as of December 31, 2016 and for the year then

ended was approved and authorized for issuance by the Board of Directors on March 17, 2017.

2. GOING CONCERN, DEBT RESTRUCTURING AND ECONOMIC CONDITIONS

a. Going Concern

The global polyester chain witnessed a modest recovery in 2016 after hitting a bottom of its growth

cycle in 2014/15 caused by a combination of excess capacity, weaker demand growth in the key

markets, especially in China. PTA margins did not show any significant recovery during 2016 as

expected and continued to remain weak within a narrow band. In most part of the year it remained

below cash cost levels forcing older capacities to shut down. However, cotton prices have trended

upwards in the second half of the year and remained steady supported by stable supply demand gap

during the season.

Overall growth of polyester fiber continues to remain subdued at 3.70% in 2016 with the operating

rates remain at 69.6% during the year. Average polymer utilization rates have also maintained low at

just 76.1%. PTA world capacity reached 77.8 mil tonnes, almost unchanged from 2015. Hence, the

operating rates for 2016 increased to 76.5% as compared to 74% for the previous year. The continuous

mismatch in supply and demand of PTA and excessive capacities impacted PTA margins adversely.

PTA margins were under constant pressure and did not recover as expected; the average margin levels

remained at US$67/MT (spot).

The weaker consumption being shaped to some extent by the current economic scenario, slowdown in

China, key textile market and uncertainties due to commodity price crash affected the global textile

trade, dampening the demand outlook. Moreover, huge capacity additions in PTA in the past, Polyester

Fiber and Filament led to lower worldwide operating rates, impacting the performance of the polyester

industry globally. Domestic market also remained depressed due to sluggish demand and stiff price

competition through increased imports of polyester fiber and yarn from China, Malaysia and India.

Despite the market conditions, the Company continue to operate its plant at optimum capacity

supported by its strong customer base and the sustained demand from domestic market. Damiano

Investments BV., Netherland, our majority shareholders continue to provide the working capital

facility of Letter of Credit limit through Deutsche Bank, Hong Kong. Damiano also provided

additional Capex loan of US$ 1.50 million to meet certain critical capex investments.

PT ASIA PACIFIC FIBERS Tbk

AND ITS SUBSIDIARIES

NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTS (Continued)

December 31, 2016 and 2015

15

2. GOING CONCERN, DEBT RESTRUCTURING AND ECONOMIC CONDITIONS (Continued)

a. Going Concern (Continued)

The sharp drops in crude prices experienced in 2015 and its volatility (ranging between US$ 36 ~

60/barrel- Average at US$ 49/Barrel) led to significant fall in commodity prices and the feed stock

prices PX and PTA consequently pushing down the polyester chain prices. The instability in crude

prices continued during most part of the year ranging between US$ 28 ~ 52 per barrel

(Average-US$ 42/barrel), which stabilized around US$ 54 levels by the first quarter of 2017. The

prices of PX and PTA also remained volatile and moved in tandem with the crude price movement.

The spot prices of both PX and PTA for 2016 have dropped and the average prices were lower by

6.4% and 5% respectively, which in turn have pushed down the Polyester chain prices and margins

continue to remain squeezed. As a result, the sales revenue for the year 2016 has dropped significantly

to US$ 356 million as compared to US$ 387 million for the previous year. Domestic market remained

sluggish throughout the year with downstream activities slowed down on account of fall in retail

consumption and stiff price competition due to cheap imports of Polyester Fiber and Yarn. Filament

yarn prices and margins were severely affected, in particular, due to excessive supply and lack of

demand from downstream weaving and knitting sector. Hence the production of yarn was curtailed in

view of lack of demand for certain type of products. Overall drop in yarn production is 3.25% over

2015, while Fiber and Polymer production were marginally higher. The drop in the sales of 7.5% over

the previous year is primarily attributed to fall in selling price and marginally by volume. However,

Sales of Performance Fabrics division of the Company has marginally increased to US$ 8.59 million

in 2016 as compared to US$ 7.74 million for the previous year.

Nevertheless, the overall financial performance of the Company in terms of earnings before interest

and depreciation (EBITDA) improved. The Company posted a positive EBITDA of US$ 3.337 million

in 2016 as compared to a negative EBITDA of US$ 6.605 million for the previous year. The

improvement in the performance was mainly on account of outsourcing of PTA from market. The

operational losses of PTA plant due to very low margins were fully eliminated by the Company’s

strategic decision to shut down and mothball the plant till it is revamped to improve the cost efficiency

at par with the newer plants.

However, the lower earnings (EBITDA) continued to cause severe strain on the cash flow position of

the Company leading to postponement of certain maintenance projects and financial commitments.

Due to the tight cash flow situation, Company could not service the interest to its unsecured creditors

(New Notes) fully during the year. Interest amounts due for all the four quarters to unsecured creditors

were capitalized as per the approval from the majority of the creditors. Damiano Investments BV.,

Netherlands, the majority shareholders and creditors of the Company, waived the interest on LC loan

for ther year 2016 and also came forward to extend additional LC limits as an interim arrangement to

augment the working capital requirements in the light of the increasing RM prices.

PT ASIA PACIFIC FIBERS Tbk

AND ITS SUBSIDIARIES

NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTS (Continued)

December 31, 2016 and 2015

16

2. GOING CONCERN, DEBT RESTRUCTURING AND ECONOMIC CONDITIONS (Continued)

a. Going Concern (Continued)

The analysis of polyester industry trend confirmed that the bottom of the polyester cycle is over in

2014/15 and the emerging investment profile indicates that the polyester markets are on a more reliable

path of recovery globally. Global fiber industry will be determined increasingly by growth in demand

in Textiles and Apparel in Asia. Although economic growth in developed regions such as in North

America, Europe and Japan remains modest, they continue to be major consumers of downstream

textiles and apparel products sourced from Asia. Most importantly, polyester is widely accepted within

China and elsewhere in Asia by major retailers and apparel brand owners as the key performance fiber

for the higher added value technical textile sectors.

Therefore, significant growth is forecast in the many performance fabrics that are increasingly

developed in Asia for consumption in home textiles, building construction, advanced sportswear

apparel, and the fast emerging medical and hygiene textile sectors via the non-woven route.

The Company with its newly built capabilities to increase the volume of specialty products (Colored

yarns/PBT) for automotive/ home textiles applications and its strategy to enter new markets for

performance oriented textile and non-textile segments, will be able to face the competition and

improve its performance in the years to come.

Earlier, the Company’s 100% of energy requirements (both power and steam) had been met by PT

Wismakarya Prasetya (WKP), earlier. However, subsequent to bankruptcy of WKP, the Company took

the following action to ensure uninterrupted supply of power steam and Gas:

1) Acquired the ABB Gas turbine – 20 MW from WKP through Court auction with effect from

November 5, 2014.

2) Entered into a rental agreement for the rest of the facilities of WKP with the curator of PT

WKP to maintain and operate the turbines to generate power and steam for its captive use –

vide agreement dated April 16, 2014 and the subsequent amendments i) dated November 24,

2014 and ii) December 18, 2015, which are valid up to December 31, 2018.

3) Consequent to expiry of the contract for supply of Gas between PT WKP and PGN, the

Company has renewed the Gas supply contract directly with PT PGN to ensure uninterrupted

supply of Gas for operating the power plant – vide contract no 011700.PK/HK.02/USH/2014

dated June 20, 2014, which is valid through March 2018.

In 2016, the production volumes and the Capacity utilization of APF facilities in Karawang increased

marginally, while the production volume in Semarang dropped due to curtailment of production owing

to market conditions. PTA plant at Karawang was shut down temporarily from November 2015 in

view of the trading conditions as explained above and its PTA requirement is outsourced externally.

The overall capacity utilization was, however, maintained around 90% in both the facilities.

In addition, the Company’s financial condition in 2016 showed the following:

Total comprehensive loss for the year amounting to US$ 12,159,436

Negative working capital amounting to US$ 990,677,263

Capital deficiency amounting to US$ 937,566,161

PT ASIA PACIFIC FIBERS Tbk

AND ITS SUBSIDIARIES

NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTS (Continued)

December 31, 2016 and 2015

17

2. GOING CONCERN, DEBT RESTRUCTURING AND ECONOMIC CONDITIONS (Continued)

a. Going Concern (Continued)

Subsidiary’s Operations (PT Texmaco Jaya Tbk):

Consequent to declaration of bankruptcy of PT Texmaco Jaya by the commercial court of Jakarta on

August 19, 2011 as per the court order 10/PKPU/2010/PN.NIAGA.JKT.PST Jo No:

71/PAILIT/2010/PN.NIAGA.JKT.PST, the management of the company and enforcement of the

liquidation process was under the team of curators appointed by the Court and monitored by the

supervisory judge. The Curator and the Commercial Court of Jakarta had acknowledged and registered

the receivable amount of Rp 1,106,832,761,717 as unsecured debt. The liquidation process of the

Company’s subsidiary is still under progress.

In the meantime, the Court has approved continued operation of its Fleece division as a going concern

with a view to maintain the value of the bankrupt assets. In accordance with the Court approval and

pursuant to the tolling agreement between the team of curators and PT Asia Pacific Fibers Tbk, the

Fleece division continued to be operated on tolling basis.

Pursuant to PSAK 10 (Revised 2010), the Company and its Subsidiaries has determined US dollar as

its functional currency as predominant financial transaction such as Sales, Purchases, Pricing etc., are

transacted in dollar currency. Hence the Company and its Subsidiaries has chosen to prepare and

present its financial statements in US Dollar currency effective January 2012. The financial statements

for the year 2016 and 2015 was prepared in accordance with the guidelines provided under PSAK 10

paragraph 27-34 and paragraph 61-62.

The accompanying financial statements have been prepared on a going concern basis, and do not

include any adjustment that might result from the outcome of these uncertainties. Related effects will

be reported in the financial statements as they become known and can be estimated. To date, the

Company, in running its operations is supported through the letter of credit facility and other working

capital loans from Damiano Investments BV., Netherland and through the confidence and support of

its suppliers and customers. In addition, Damiano Investments BV., Netherlands confirmed that it will

provide the assistance to the Company in obtaining letter of credit facilities until such time that the

Company can secure a credit facility from banks on its own. Damiano Investments BV., Netherland

has also provided the requisite funds for the Company’s maintenance capital expenses programs in

2016 through its Third Loan Agreement.

b. Debt Restructuring

Secured Debt

In response to our continuous appeal and discussions with Ministry of Finance (MoF)/PT Perusahaan

Pengelola Asset (PPA) for a restructuring solution of Secured Debt, Ministry of Finance had appointed

a high-level committee lead by Mandiri Sekuritas (Investment and Security division of the state-owned

Bank – Bank Mandiri) to study and recommend a restructuring proposal for the Texmaco group debts

including PT Asia Pacific Fibers secured debt to the Ministry for its review and approval.

PT ASIA PACIFIC FIBERS Tbk

AND ITS SUBSIDIARIES

NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTS (Continued)

December 31, 2016 and 2015

18

2. GOING CONCERN, DEBT RESTRUCTURING AND ECONOMIC CONDITIONS (Continued)

b. Debt Restructuring (Continued)

Secured Debt (Continued)

Accordingly, the Committee had several rounds of discussion with the Management and Majority

shareholders of the Company on various restructuring under the given conditions. The committee had

undertaken financial and legal due diligence of the Company and also done technical evaluation and

valuation of the Company’s assets with a view to formulate a suitable restructuring proposal. During

the bilateral discussions with the committee, APF had emphasized the need for an immediate solution

to the issue and requested that APF to be de-linked from Texmaco group in as much as it is no more

an affiliate company and the Majority shares are held by Damiano BV, who are the majority creditors

of the Company as well.

After a several rounds of discussions and considering the current conditions and various other

economic factors, the Company had submitted an updated Secured Debt Restructuring proposal to the

Committee and the MoF during October 2016. The final restructuring plan proposed by the Company

envisages conversion of the entire secured debt into equity through debt equity swap. The broad terms

of the Secured Debt Restructuring Proposal (SDRP) are as follows:

a) 100% of the Secured Debt of MoF/BPP will be either converted into 15 - Year, 0% Coupon

Mandatory Convertible Bonds (MCB) for a value equivalent to 100% of the Principal value of the

debt (as per the terms set out below), or

b) Directly convert the entire debt in to 24.49% of the expanded equity of the Company (Post

Restructure)

c) 100% of all other Secured Debts comprising of Secured Bonds, Ex – Banks bilateral loans will be

converted into equity as below:

i. All Secured Bonds to be converted into 69.26% of the equity

ii. Other Secured Debts to be converted into 3.08% of the equity

d) All accrued interest/ penalties on the Secured Debt up to the date of restructure will be fully

waived.

Terms of the MCB

a) Face value of the MCB will be equal to the 100% value of the MoF/BPP debt.

b) The tenor of the MCB is 15 years with 0% Coupon rate.

c) The restructured MCB of BPP and MoF will be denominated in Rupiah (IDR). The

debts denominated in currencies other than IDR will be converted into Rupiah (IDR)

using the exchange rate (BI Middle rate) prevailing at the date of restructure.

d) At holder’s option, MCBs can be converted in to Equity any time after expiry of 36/60

months from the date of issue of the MCB;

e) MCB is classified as a quasi-equity instrument.

PT ASIA PACIFIC FIBERS Tbk

AND ITS SUBSIDIARIES

NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTS (Continued)

December 31, 2016 and 2015

19

2. GOING CONCERN, DEBT RESTRUCTURING AND ECONOMIC CONDITIONS (Continued)

b. Debt Restructuring (Continued)

Secured Debt (Continued)

In March 6, 2017, PT Asia Pacific Fibers Tbk established a wholly owned subsidiary Asia Pacific

Fibers Hong Kong Limited, a private limited company established under the laws of the Hong Kong

Special Administrative Region (“HKSAR”) with corporate registration number 2493881 and its

registered office in Hong Kong.

The new subsidiary Company, Asia Pacific Fibers Hong Kong Limited through the execution of Deed

Poll will voluntarily assume liability of the Issuer and/or Guarantor in respect of the secured bonds of

US$ 682.5 million. This is intended to facilitate the restructuring of (inter alia) the Notes through a

scheme of arrangement pursuant to sections 673 and 674 of the Companies Ordinance (Cap 622 of the

law of the HKSAR) (“Scheme”) and otherwise in a manner that is beneficial to the Company, the

Company and each of their respective stakeholders, including (but not limited to) the holders of the

Notes.

The Company has recently made considerable progress towards resolving these issues with the

Government of Indonesia and now seeks to push ahead with a restructuring of the Notes, which will

help facilitate acceptance and implementation of any restructuring plan agreed with the Government

of Indonesia. The last 15 years of protracted inability to achieve a restructuring of its secured debt,

have eroded the Company’s ability to service the original level of its secured debt. However, there

remains significant value in the Company’s business which can be made available to creditors under

any restructuring. Such a restructuring will also pave the way for the Company to achieve a sustainable

capital structure which will allow it to continue and grow its business with new capital expenditure

and other initiatives which will benefit all of its stakeholders (which include public shareholders

currently holding over 40% of the Company’s equity).

The Company’s ability to restructure the Notes is constrained by the fact that the restructuring would

require unanimous consent from holders of the Secured Bond Holders. However the Company has

been unable to identify a small percentage (of around 1-2%) of such holders which it believes may be

inactive, either being liquidated or no longer exist or in the case of individuals being deceased.

As is clear from the above, the Company is committed to implementing a restructuring which is fair

to all holders of the Notes, but has been frustrated by the inability to identify or contact a very small

minority of holders of the Notes to obtain the required approvals for such a restructuring. Accordingly,

the Company has obtained professional advice as to the various options available to it to effect a

restructuring in a manner that is fair to all stakeholders, but also allows it to bind unidentified holders

of the Notes who do not provide affirmative consent. The Company has considered that a Scheme in

HKSAR would be the most appropriate options for implementing a restructuring the secured bonds.

PT ASIA PACIFIC FIBERS Tbk

AND ITS SUBSIDIARIES

NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTS (Continued)

December 31, 2016 and 2015

20

2. GOING CONCERN, DEBT RESTRUCTURING AND ECONOMIC CONDITIONS (Continued)

b. Debt Restructuring (Continued)

Secured Debt (Continued)

The advantages of this scheme of restructuring are:

(a) Management of the Company will remain free to run the business and operations of the Company

while any scheme is being proposed and implemented;

(b) The Company has been advised that a scheme may be used to bind unidentified holders of the

Notes who do not provide affirmative consent so long as the Scheme is supported by the requisite

majorities of holders of the Notes and sanctioned by the relevant court after a hearing on fairness;

(c) The key creditors of the Company are managed by fund managers who have offices in Hong Kong

and are subject to supervision of, or registration with, the Hong Kong Security and Futures

Commission; and bind dissenting secured creditors of the Company (including minority holders of

the Notes).

The committee has subsequently submitted its interim report and recommendations to the Ministry of

Finance for its decision and final direction. While the majority creditors are in agreement with the

above proposal. It is expected that a final decision by MoF/PPA on restructuring will be taken very

soon.

Unsecured Debt

The Company has executed the restructuring agreement with the unsecured creditors as approved by

the creditors and ratified by the Court. Accordingly, the total unsecured loans after the restructuring

stands at US$ 18,670,630 plus unpaid capitalized interest until November 2016 of US$ 6,354,338.56

or amounted to US$ 25,024,968.56.

The Company has taken all the required corporate actions towards the implementation of the

Composition Plan (“Peace Plan”) as approved by the unsecured creditors of the Company and ratified

by the Commercial Court. The steps involve the issuance of the new debts secured or unsecured in

exchange of the old unsecured debts and issuance of shares for the reduction of the principal amount

of debts as per the terms of the Composition Plan. The Company has reduced its unsecured debts as

per the Composition Plan and increased its share capital as additional capital pending allotment to the

creditors. The Company has appointed The Hongkong and Shanghai Banking Corporation Limited,

Hong Kong to act as its Fiscal Agent, Paying Agent and Trustees for its new unsecured notes which

are euro-cleared.

PT ASIA PACIFIC FIBERS Tbk

AND ITS SUBSIDIARIES

NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTS (Continued)

December 31, 2016 and 2015

21

2. GOING CONCERN, DEBT RESTRUCTURING AND ECONOMIC CONDITIONS (Continued)

b. Debt Restructuring (Continued)

Unsecured Debt (Continued)

In January 2015, the Company sought and got the approval of its Unsecured New Note Holders for

the extension of its maturity from February 2015 to February 2018. The details are as below:

Redemption Date

Redemption Table (Revised for PIK)

Subject to PIK Outstanding Redemption Redemption

% Request Amount Amount

February 15, 2005 US$ 18,670,630.00 US$ 18,670,630.00 0.00%

to November 15, 2016 US$ 6,354,338.56 US$ 25,024,968.56 0.00%

February 15, 2018 US$ 23,773,720.13 US$ (1,251,248.43) 5.00%

February 15, 2019 US$ 19,394,350.63 US$ (4,379,369.50) 17.50%

February 15, 2020 US$ 15,014,981.13 US$ (4,379,369.50) 17.50%

February 15, 2021 US$ 10,635,611.64 US$ (4,379,369.50) 17.50%

February 15, 2022 US$ 5,630,617.93 US$ (5,004,993.71) 20.00%

February 15, 2023 US$ 0.00 US$ (5,630,617.93) 22.50%

US$ 25,024,968.56 US$ (25,024,968.56) 100.00%

c. Economic Condition

Indonesia’s economic growth in 2016 recorded 5.02% better than that in 2015 at 4.88% in 2015, but

marginally lower than the prediction by Bank Indonesia at 5.2%. Economic growth in 2016 was

primarily supported by domestic consumption growth and investment performance improvement.

Domestic consumption grew relatively strong, supported by controlled inflation. Indonesia’s economy

has weathered recent global financial volatility and is well placed to mitigate future risks to its growth

outlook bolstered by solid economic fundamentals and policy reforms.

Exports declined marginally in monetary terms US$ 144.43 billion in 2016, as compared to the

previous year realization of US$ 150.37 billion in 2015 recording a dip of 3.95%, thought in terms of

volume it recorded an increase of 0.66% y-o-y. Hence, the dip in exports were primarily triggered by

low prices for key export commodities such as coal, metal minerals, rubber and crude palm oil. Import

trade value also dropped by 4.94% to US$ 136.65 billion as compared US$ 142.69 billion. Drop in

import of Capital goods, raw materials and intermediary inputs indicates slowdown in domestic

manufacturing activities. On the other hand, there is significant increase in consumer goods imports

clearly indicating growth in consumption.

The fall in crude prices continued thru’ 1st quarter of 2016 and hit a low of US$ 28/ per barrel in

February 2016, but gradually recovered and stabilized around US$ 50/Barrel by end of the year. Crude

prices continue to recover and remained stable in Q1 2017 around US$ 54/Barrel, indicating some

stability and recovery in commodity segment.

PT ASIA PACIFIC FIBERS Tbk

AND ITS SUBSIDIARIES

NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTS (Continued)

December 31, 2016 and 2015

22

2. GOING CONCERN, DEBT RESTRUCTURING AND ECONOMIC CONDITIONS (Continued)

c. Economic Condition (Continued)

The inflation in 2016 was quite moderate at 3.02% well below the BI targeted rate of 4±1% (yoy) and

as compared to 3.38% for the previous year. The drop in the oil prices and the prices of key

commodities are the primary reason for the drop in the inflation.

Indonesia trade balance continue to be in surplus for second year in row at US$ 8.78 billion in 2016

as compared to US$ 7.67 for the previous year. The current account deficit fell from US$ 17.5 billion

(2.0% of GDP) in 2015 to US$ 16.3 billion (1.8% of GDP) in 2016 supported by improvement in

goods and services trade performances.

Indonesian currency remained resilient through the year and relatively stable backed by solid economic

growth and better economic outlook going forward. Bank Indonesia's benchmark rupiah rate (Jakarta

Interbank Spot Dollar Rate, abbreviated JISDOR) appreciated 0.27 percent at IDR 13,436 per US

dollar by end of December 2016. In full-year 2016 the currency of Indonesia appreciated 2.60 percent

against the US dollar. BI has lowered its key interest rate (BI Rate) four times during the period from

January 1, 2016 till July 21, 2016 by 100 basis point (from 7.50% to 6.50%) in consistent with the

macro-economic stability of the Country.

The ambitious tax amnesty launched by the Government of Indonesia during the year entered its third

phase in Q1- 2017 and the resultant tax revenues positively contributed to lower the budget deficit in

2016.

Going forward, Bank Indonesia estimates that economic expansion will continue in 2017. The

improving commodity price development and ongoing global economic improvement are expected to

be able to support export performance of Indonesia. With solid domestic demand and global increase,

investment is estimated to continuously improve. Interest rate decrease is also expected to be able to

boost domestic consumption and investment performance, which is supported by the implementation

of Government Policy Package. On the other hand, utilization of monetary easing space in a measured

way by maintaining macro-economic and financial system stability will also strengthen economic

growth momentum in the future.

However, external factors such as ongoing financial volatility coupled with sluggish trade and subdued

growth in advanced economies, continued deceleration of China’s economy, global policy uncertainty,

particularly concerning global trade agreements and the pace of interest rate normalization in the US

are the possible risks to the future growth outlook.

Domestic manufacturing sector is expected to recover with the help of supporting measures by the

government to boost the battering domestic manufacturing industries, especially to TPT sector to

improve its competitiveness. Government concerted efforts to protect the domestic industries by

imposing restriction on illegal imports, anti-dumping duties on Fiber and yarn, rationalization of

import duties etc. are expected to revive the growth prospects. The impact of capital injections

provided to selected state-owned enterprises (SOEs) dealing with infrastructure development is

expected yield results in the coming years. In addition, the government has introduced a number of

fiscal measures to support investment and export.

PT ASIA PACIFIC FIBERS Tbk

AND ITS SUBSIDIARIES

NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTS (Continued)

December 31, 2016 and 2015

23

3. SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES

The significant accounting policies of the Company and its subsidiaries adopted in preparation of the

consolidated financial statements are set below:

a. Basis of Preparation of the Consolidated Financial Statements

The consolidated financial statements of PT Asia Pacific Fibers Tbk have been prepared in accordance

with the Indonesian Financial Accounting Standards (“SAK”) comprising of the Statements of

Financial Accounting Standards (“PSAK”) and its Interpretation Financial Accounting Standards

(“ISAK”), issued by the Board of Financial Accounting standard of the Indonesia Institute of

Accountant (“DSAK – IAI”), and the regulations and guidelines for financial statement presentation

established by Financial Service Authority (“OJK” for merly BAPEPAM – LK) No. VIII.G7 regarding

“Emiten or Public Company’s Financial Statements Presentation and Disclosure Guidelines as included in

the appendix of the Decision Degree of the chairman of BAPEPAM – LK No KEP-347/BL/2012 dated

June 25, 2012.

The consolidated financial statements for the years ended December 31, 2016 and 2015 have been

prepared in accordance with PSAK No. 1 (Revised 2013), “Presentation of Financial Statements”. In

accordance with PSAK No. 1 (Revised 2013), the consolidated statement of profit or loss and other

comprehensive income has been presented in the consolidated financial statements. The Company and

its Subsidiaries have been elected to present all items of income and expense in the single statement.

And in relation to the amendment to PSAK No. 4, “Separate Financial Statements”, the Company

has measured investment in subsidiaries using cost method.

As of August 19, 2011, the Commercial Court had declared that the Subsidiary (PT Texmaco Jaya Tbk)

is bankruptcy and insolvency effective on September 26, 2011. Effective this period, the Subsidiary

becomes subject to the control of the Court, and causing the Company loss its controls.

The consolidated financial statements have been prepared on the historical cost basis of accounting,

except for the certain accounts are prepared based on the other measurement that are more fully

described in the accounting policies below. The consolidated financial statements are prepared under

the accrual basis of accounting, except for the consolidated statement of cash flows.

The consolidated statements of cash flows are prepared using the direct method and present the sources

and uses of cash and cash equivalents according to operating, investing and financing activities. Cash

and cash equivalents consist of cash on hand, cash in banks and deposits with original maturities

of 3 (three) months or less.

The reporting currency used in preparation of the consolidated financial statements is

US Dollar (“US$”), which is also the Company’s functional and presentation currency. All figures

presented in the consolidated financial statements are stated at absolute amounts of US$, unless

otherwise specified. Refer to Note 3c for the information on the functional currency.

The Company has received approval from Bank Indonesia with letter No. 17/1192/DKSP dated

August 11, 2015 for translating using US$ as currency of transaction until July 2016 in relation

to Bank Indonesia rule No. 17/3/PBI/2015. Further, based on letter from Bank Indonesia

No. 18/1145/DKSP/Srt/B dated August 18, 2016, the Company has received the permission to extend

using US$ as currency of transaction.

PT ASIA PACIFIC FIBERS Tbk

AND ITS SUBSIDIARIES

NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTS (Continued)

December 31, 2016 and 2015

24

3. SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES (Continued)

b. Principles of Consolidation

(a) Subsidiaries

Subsidiaries are all entities (including structured entities) which the Company has control. The

Company controls an entity when the Company is exposed to, or has rights to, variable returns

from its involvement with the entity and has the ability to affect those returns through its power

over the entity. Subsidiaries are fully consolidated from the date on which control is transferred to

the Company. They are de-consolidated from the date on which than control ceases.

The Company applies the acquisition method to account for business combinations. The

consideration transferred for the acquisition of a subsidiary is the fair value of the assets

transferred, the liabilities incurred to the former owners of the acquireee and the equity interests

issued by the Company. The consideration transferred includes the fair value of any asset or

liability resulting from a contingent consideration arrangement. Identifiable assets acquired and

liabilities and contingent liabilities assumed in a business combination are measured initially at

their fair values at the acquisition date.

The Company recognises any non – controlling interest in the acquiree on an acquisition-by-

acquisition basis, either at fair value or at the non – controlling interest’s proportionate share of

the acquiree’s net assets. Non – controlling interest is reported as equity in the consolidated

statement of financial position, separate from the owner of the parent’s equity.

Acquisition-related costs are expensed as incurred.

If the business combination is achieved in stages, at the acquisition date fair value of the acquirer’s

previously held equity interest in the acquiree is re-measured to fair value at the acquisition date

through profit or loss.

Any contingent consideration to be transferred by the Company is recognized at fair value at the

acquisition date. Subsequent changes to the fair value of the contingent consideration that is

deemed to be an asset or liability is recognized in accordance with PSAK 55 (Revised 2011)

“Financial Instrument: Recognition and Measurement” in the consolidated statements of profit or

loss and other comprehensive income. Contingent consideration that is classified as equity is not

re-measured, and its subsequent settlement is accounted for within equity.

The excess of the consideration transferred the amount of any non – controlling interest in the

acquiree and the acquisition-date fair value of any previous equity interest in the acquiree over the

fair value of the identifiable net assets acquired is recorded as goodwill. If the total of consideration

transferred, non-controlling interest recognised and previously held interest measured is less than

the fair value of the net assets of the subsidiary acquired in the case of a bargain purchase, the

difference is recognised directly in the statement of profit or loss and other comprehensive income.

Inter – company transactions, balances and unrealised gains on transactions between group

companies are eliminated. Unrealised losses are also eliminated. When necessary amounts

reported by subsidiaries have been adjusted to conform to the Company’s accounting policies.

PT ASIA PACIFIC FIBERS Tbk

AND ITS SUBSIDIARIES

NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTS (Continued)

December 31, 2016 and 2015

25

3. SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES (Continued)

b. Principles of Consolidation (Continued)

(b) Changes in ownership interests in subsidiaries without change of control

Transactions with non-controlling interests that do not result in loss of control are accounted for

as equity transactions. The difference between the fair value of any consideration paid and the

relevant share acquired of the carrying value of net assets of the subsidiary is recorded in equity

and attributable to owners of the Company. Gains or losses on disposals to non-controlling

interests are also recorded in equity.

(c) Disposal of subsidiaries

When the Company ceases to have control, any retained interest in the entity is re-measured to its

fair value at the date when the control is lost, with the change in carrying amount recognized in

the consolidated statements of profit or loss and other comprehensive income. The fair value is

the initial carrying amount for the purposes of subsequently accounting for the retained interest as

an associate, joint venture or financial asset.

In addition, any amounts previously recognized in other comprehensive income in respect of that

entity are accounted for as if the Company had directly disposed of the related assets or liabilities.

This may mean that amounts previously recognized in other comprehensive income are

reclassified to consolidated profit or loss.

c. Foreign Currency Transaction and Balances

Functional and presentation currency

Items included in the consolidated financial statements of each of the Company and its

Subsidiaries are measured using the currency of the primary economic environment in which the

entity operates (“functional currency”).

The consolidated financial statements are presented in US Dollar, which is the functional and

presentation currency of the Company and its Subsidiaries.

Transactions and balances

Foreign currency transactions are translated into US Dollar using the exchange rates prevailing at

the dates of the transactions. At each reporting date, monetary assets and liabilities denominated

in foreign currencies are translated into US Dollar using the closing exchange rate. Exchange rate

used as benchmark is the rate which is issued by Bank Indonesia.

Foreign exchange gains and losses resulting from the settlement of such transactions and from the

translation at period-end exchange rates of monetary assets and liabilities denominated in foreign

currencies are recognized in the consolidated statements of profit or loss and other comprehensive

income.

PT ASIA PACIFIC FIBERS Tbk

AND ITS SUBSIDIARIES

NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTS (Continued)

December 31, 2016 and 2015

26

3. SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES (Continued)

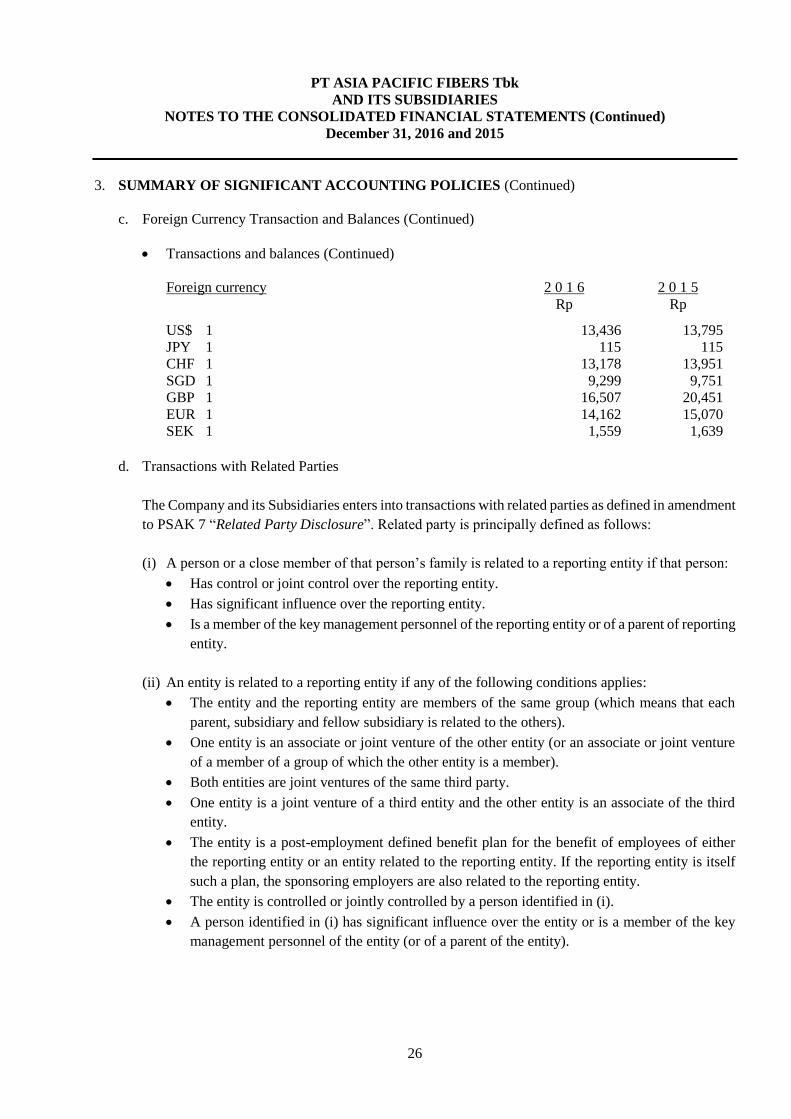

c. Foreign Currency Transaction and Balances (Continued)

Transactions and balances (Continued)

Foreign currency 2 0 1 6 2 0 1 5

Rp Rp

US$ 1 13,436 13,795

JPY 1 115 115

CHF 1 13,178 13,951

SGD 1 9,299 9,751

GBP 1 16,507 20,451

EUR 1 14,162 15,070

SEK 1 1,559 1,639

d. Transactions with Related Parties

The Company and its Subsidiaries enters into transactions with related parties as defined in amendment

to PSAK 7 “Related Party Disclosure”. Related party is principally defined as follows:

(i) A person or a close member of that person’s family is related to a reporting entity if that person:

Has control or joint control over the reporting entity.

Has significant influence over the reporting entity.

Is a member of the key management personnel of the reporting entity or of a parent of reporting

entity.

(ii) An entity is related to a reporting entity if any of the following conditions applies: