CONFERENCE & EXHIBITION - Indonesian Gas...

18

Gas Infrastructure Development: Mr. Pitak Janyapong Executive Vice President, Strategic Planning Department Gas Business Unit, PTT Public Company Limited January 29, 2015

Transcript of CONFERENCE & EXHIBITION - Indonesian Gas...

CONFERENCE & EXHIBITION

Gas Infrastructure Development:

Mr. Pitak JanyapongExecutive Vice President, Strategic Planning Department

Gas Business Unit, PTT Public Company Limited

January 29, 2015

2

I. ASEAN GAS OUTLOOK

II. NATURAL GAS DEVELOPMENT & OUTLOOK IN THAILAND

III. THAILAND INFRASTRUCTURE EXPANSION STRATEGY

SECURITY, RELIABILITY & FLEXIBILITY

ASEAN INLAND LNG HUB

IV. CONCLUSION

agenda

3

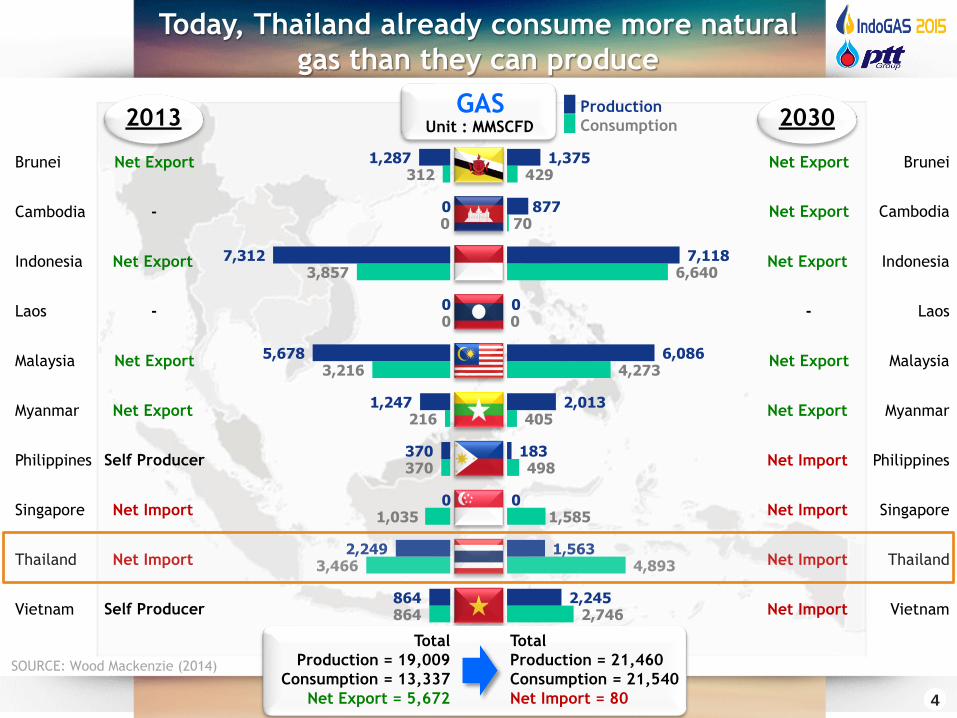

At present, ASEAN is a net exporter of natural gas, but in the future, it might become a net importer

0

5,000

10,000

15,000

20,000

25,000

2012 2013 2014 2015 2016 2017 2018 2019 2020 2021 2022 2023 2024 2025 2026 2027 2028 2029 2030

Brunei Cambodia IndonesiaLaos Malaysia MyanmarPhilippines Singapore ThailandVietnam Gas Production

(MM

SC

FD

)

SOURCE: Wood Mackenzie (2014)

2013 Net Gas Export

= 5,672 MMSCFD

2013 Total Production

= 19,009 MMSCFD

2030 Total Demand

= 21,540 MMSCFD

2030 Net Gas Import

= 80 MMSCFD

2030 Total Production

= 21,460 MMSCFD

2013 Total Demand

= 13,337 MMSCFD

4

GASUnit : MMSCFD

864

3,466

1,035

370

216

3,216

0

3,857

0

312

864

2,249

0

370

1,247

5,678

0

7,312

0

1,287

2,746

4,893

1,585

498

405

4,273

0

6,640

70

429

2,245

1,563

0

183

2,013

6,086

0

7,118

877

1,375

Production

Consumption

Brunei

Cambodia

Indonesia

Laos

Malaysia

Myanmar

Philippines

Singapore

Thailand

Vietnam

Net Export Net Export

-

2013 2030

Net Export Net Export

- -

Net Export Net Export

Net Export Net Export

Self Producer

Net Import Net Import

Net Import Net Import

Self Producer

Brunei

Cambodia

Indonesia

Laos

Malaysia

Myanmar

Philippines

Singapore

Thailand

Vietnam

Net Export

Net Import

Net Import

Today, Thailand already consume more natural

gas than they can produce

Total

Production = 19,009

Consumption = 13,337

Net Export = 5,672

Total

Production = 21,460

Consumption = 21,540

Net Import = 80

SOURCE: Wood Mackenzie (2014)

5

Natural Gas Development

Natural gas in Thailand is an

valuable resource, it is a clean

energy and a petrochemical

feedstock to value added.

As a result, demand for gas has

grown rapidly with continued

expansion of infrastructure

1981 1983 1985 1987 1989 1991 1993 1995 1997 1999 2001 2003 2005 2007 2009 2011 2013 2015 2017 2019

Power

GSP

NGV

GSP 1

Nampong P/L

GSP 2 GSP 3

Myanmar P/L

GSP 5

MMscfd

2nd P/L

GSP 4

6,000

5,000

4,000

3,000

2,000

1,000

ESP & GSP 6

LNG Terminal

Industry3rd P/L

1st P/L

4th P/L

Provincial P/L

NGV

6

Natural Gas Value Chain:Value are maximized to the sourced natural gas

C2 (Ethane)

C3 & C4 (LPG)

C5+ (NGL)

C1 (Methane)

C3 (Propane)

Fiber & Textiles

Automobile

Construction

Electrical & Electronic

Agriculture & Others

Power

Industry

NGV (CNG)

C3 & C4 (LPG)

DEMAND

Petrochemical Feedstock

GSP 1-6

& ESP

SUPPLY

N.G.

N.G

.

N.G.

C1

(Me

tha

ne

)

“To reduce import and increaseenergy efficiency”

Gulf of

Thailand

Myanmar

Onshore

LNG

Packaging

“Value Added”

LPG for household & transport

7

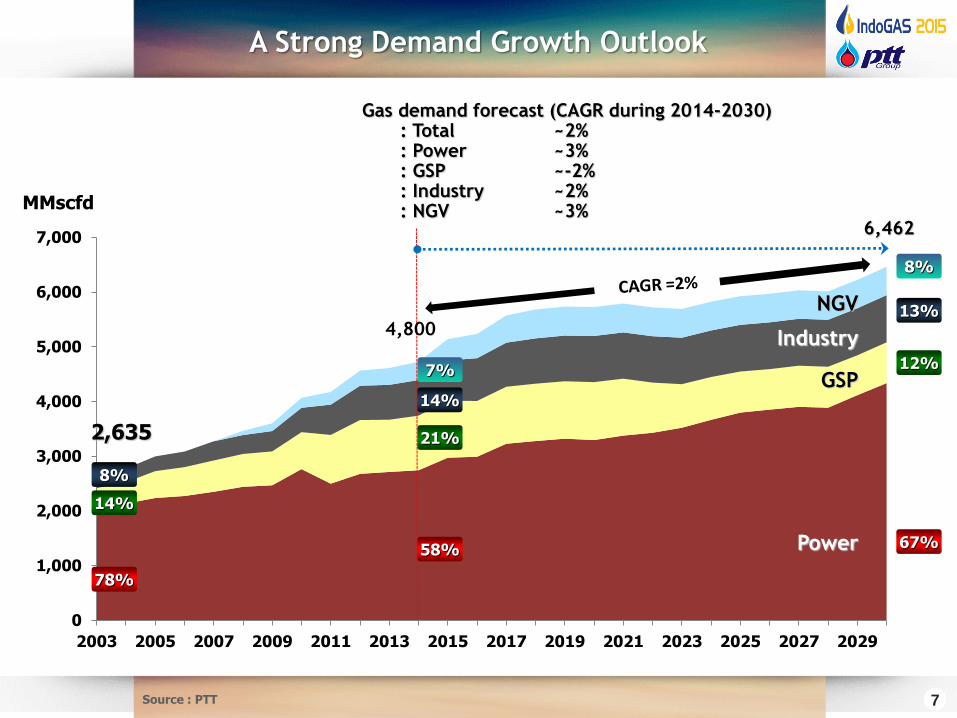

A Strong Demand Growth Outlook

Source : PTT

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

2003 2005 2007 2009 2011 2013 2015 2017 2019 2021 2023 2025 2027 2029

Power

GSP

Industry

78%

21%

8%

2,635

14%

13%

12%

58% 67%

Gas demand forecast (CAGR during 2014-2030): Total ~2%: Power ~3%: GSP ~-2%: Industry ~2%: NGV ~3%

14%

NGV

8%

7%

6,462

MMscfd

4,800

8

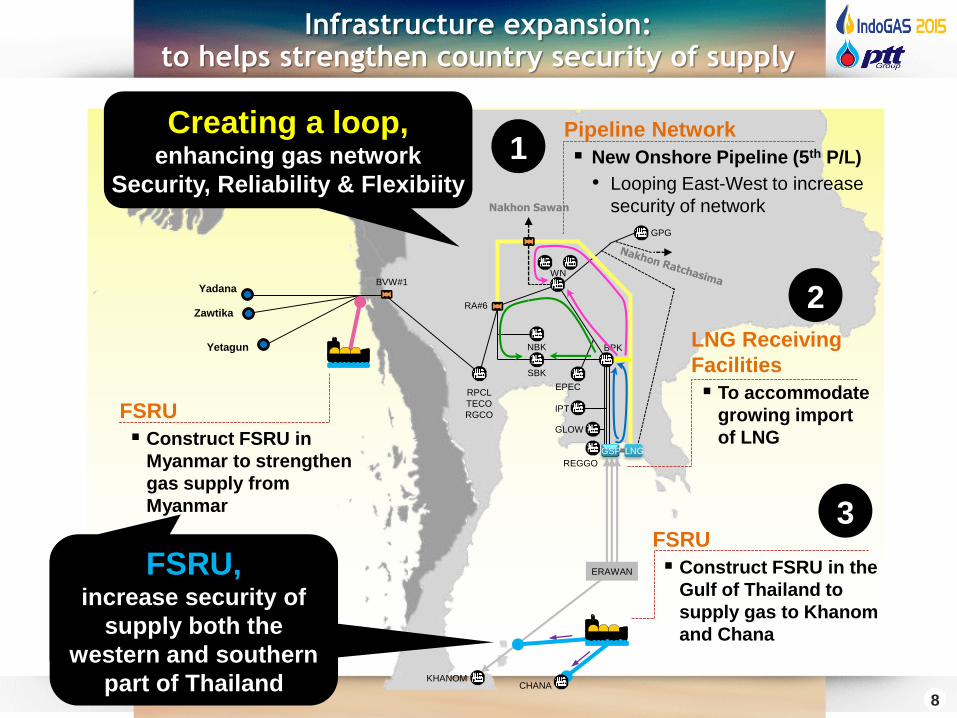

Infrastructure expansion:to helps strengthen country security of supply

Yadana

Zawtika

Yetagun

BVW#1

RA#6

RPCL

TECO

RGCO

NBK

SBK

EPEC

WN

GLOW

IPT

Nakhon Sawan

REGGO

BPK

GPG

Pipeline Network

New Onshore Pipeline (5th P/L)

• Looping East-West to increase

security of network

LNG Receiving

Facilities

To accommodate

growing import

of LNG

Creating a loop, enhancing gas network

Security, Reliability & Flexibiity

GSP

KHANOM

ERAWAN

LNG

1

2

FSRU

Construct FSRU in the

Gulf of Thailand to

supply gas to Khanom

and Chana

CHANA

3

FSRU

Construct FSRU in

Myanmar to strengthen

gas supply from

Myanmar

FSRU,increase security of

supply both the

western and southern

part of Thailand

9

Fourth Transmission Pipeline

42-inch diameter pipeline

Approximately 300 kilometers

Provincial Pipeline to Nakorn

Sawan

28-inch diameter pipeline

Approximately 210 kilometers

Provincial Pipeline to Nakorn

Ratchasrima

28-inch diameter pipeline

Approximately 160 kilometers

Infrastructure Expansion: Pipeline Networks1

Fifth Transmission Pipeline

10

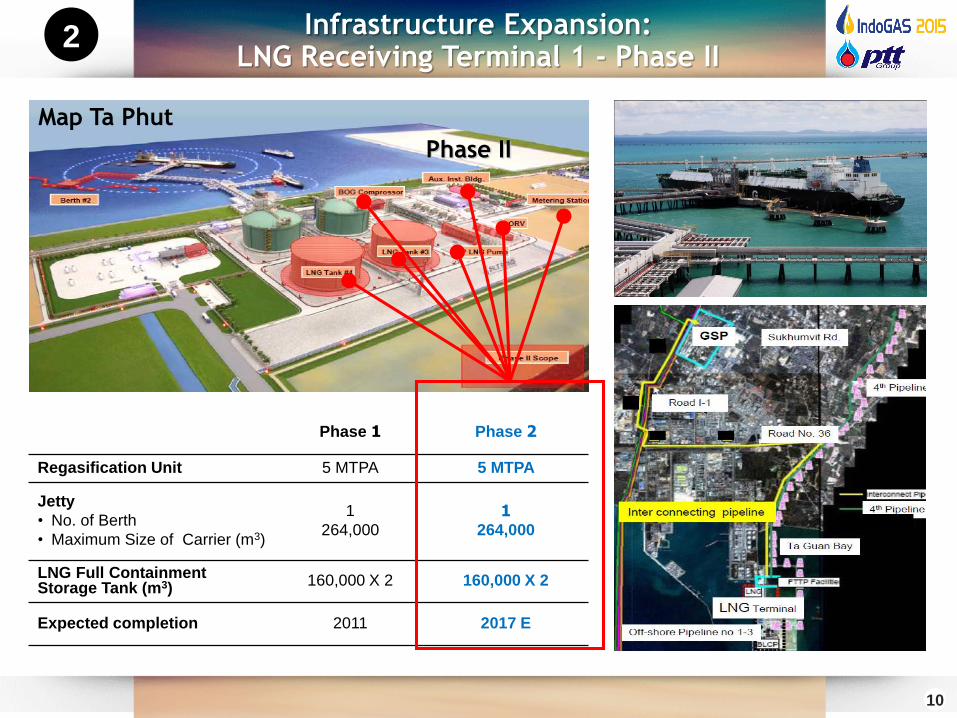

Infrastructure Expansion:LNG Receiving Terminal 1 - Phase II

2

Phase 1 Phase 2

Regasification Unit 5 MTPA 5 MTPA

Jetty

• No. of Berth

• Maximum Size of Carrier (m3)

1

264,000

1264,000

LNG Full Containment Storage Tank (m3)

160,000 X 2 160,000 X 2

Expected completion 2011 2017 E

Phase II

Map Ta Phut

11

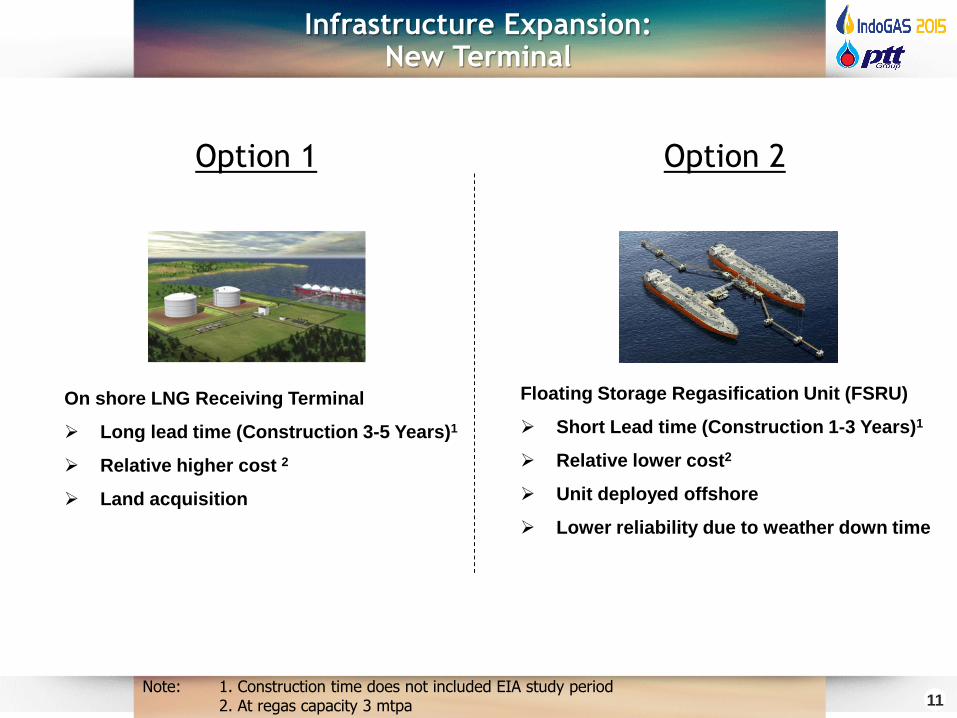

Floating Storage Regasification Unit (FSRU)

Short Lead time (Construction 1-3 Years)1

Relative lower cost2

Unit deployed offshore

Lower reliability due to weather down time

On shore LNG Receiving Terminal

Long lead time (Construction 3-5 Years)1

Relative higher cost 2

Land acquisition

Infrastructure Expansion:New Terminal

Note: 1. Construction time does not included EIA study period 2. At regas capacity 3 mtpa

Option 1 Option 2

12

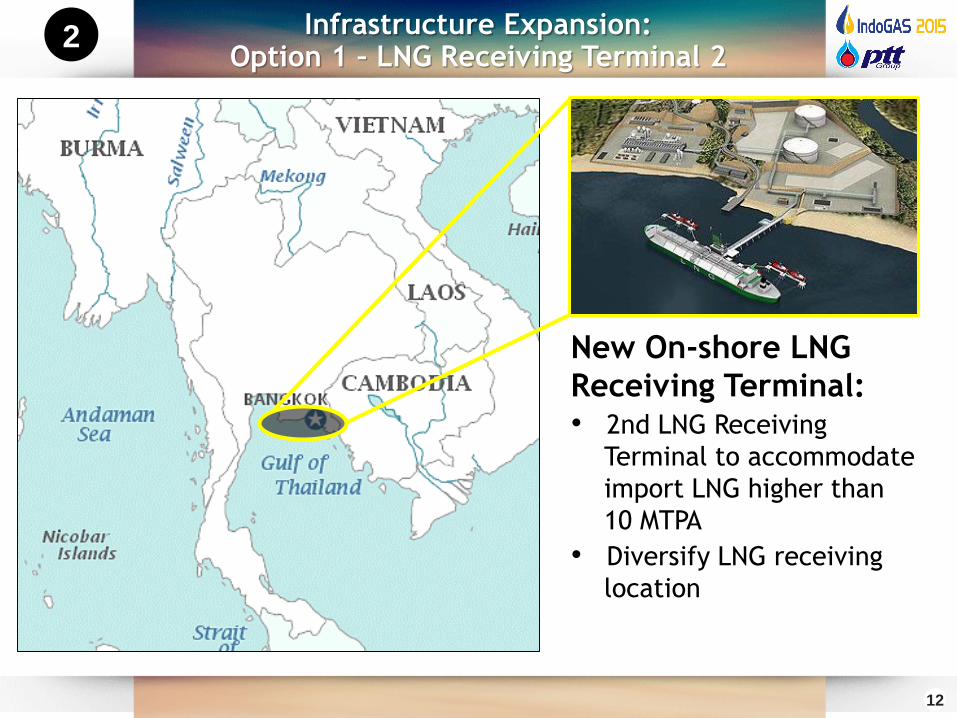

2 Infrastructure Expansion:Option 1 – LNG Receiving Terminal 2

New On-shore LNG

Receiving Terminal:• 2nd LNG Receiving

Terminal to accommodate

import LNG higher than

10 MTPA

• Diversify LNG receiving

location

13

FSRU

(Floating Storage

and Regasification

Unit):Supply Southern Part of

Thailand to increase security

of supply

Infrastructure Expansion:Option 2 - FSRU

3

CHANA

POWER PLANT

14

Thailand: Asean Energy Hub

1. Supply LNG as

alternative fuel

of Diesel

2. Construct LNG

station

MY and ID supply

natural gas to Asean

Thailand as a Center

of inland LNG Supply

15

UpstreamLook for investment for operator or non-operator with partners

Liquefaction

Invest in Projects with LNG equity lifting (N.A., East Africa project)

Shale Gas Development in N.A.

Shipping

Invest with strategic partner

in shipping business

Supporting global LNG portfolio

(LNG Trading portfolio)

Regasification

Gas Distribution

Invest in LNG receiving terminal in other countries

Downstream of LNG business value chain : LNG satellite

Explore Opportunity to Invest in LNG Value Chain

16

Conclusion:Natural gas still the fuel for choice and Thailand will..

be a center of inland LNG supply

strengthen its Infrastructure to increase Security, Reliability & Flexibility