Conference Call Full Year 2015 Results - indocement.co.id Release/2016/03. Maret... · ASI includes...

20

Conference Call Full Year 2015 Results 29 March 2016 Christian Kartawijaya, CEO Tju Lie Sukanto, CFO Disclaimer: Information presented here is not intended for further publication

Transcript of Conference Call Full Year 2015 Results - indocement.co.id Release/2016/03. Maret... · ASI includes...

Conference Call Full Year 2015 Results 29 March 2016

Christian Kartawijaya, CEO

Tju Lie Sukanto, CFO

Disclaimer: Information presented here is not intended for further publication

Indonesian Cement Industry 2015 Landscape Lafarge Indonesia

1.8 mio ton Semen Bosowa

5.4 mio ton

Semen Baturaja

2.0 mio ton

Semen Indonesia

14.4 mio ton

Semen Puger

0.5 mio ton

Semen Kupang/Merah Putih

0.6 mio ton

Jui Shin

1.6 mio ton

Semen Indonesia

7.8 mio ton

Holcim Indonesia

11.4 mio ton

Semen Indonesia

8.2 mio ton

Merah Putih

0.8 mio ton

Indocement

20.5 mio ton

Total Cement Capacity in 2015:

78.6 mio tons Source: ASI and internal estimation

Anhui Conch

1.3 mio ton

Conference Call Full Year 2015 Results

Slide 2

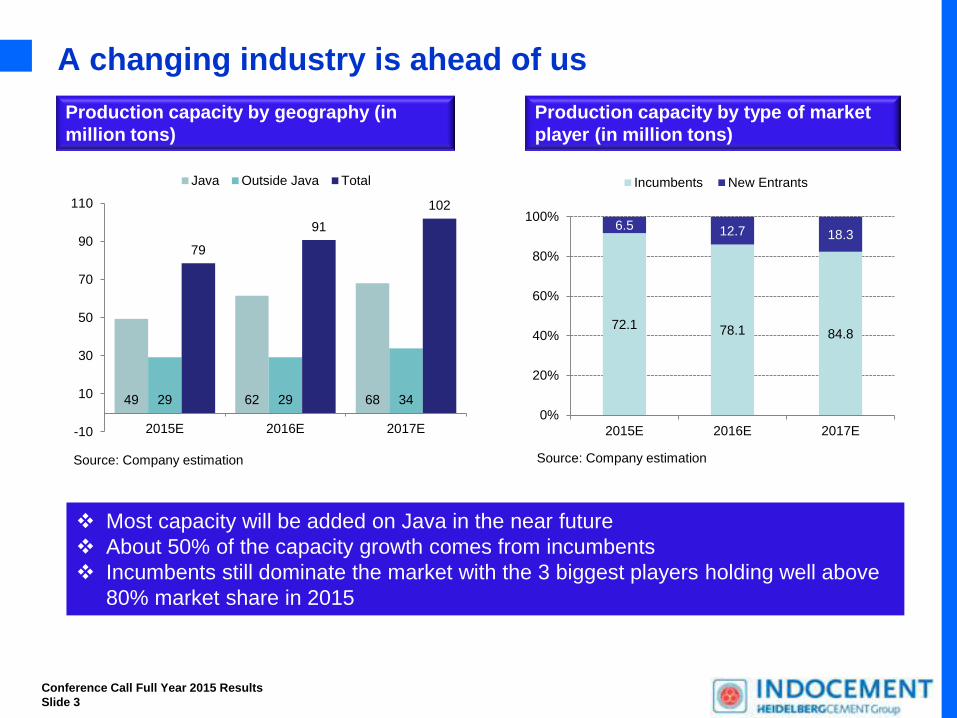

A changing industry is ahead of us

49 62 68 29 29 34

79

91

102

-10

10

30

50

70

90

110

2015E 2016E 2017E

Java Outside Java Total

Conference Call Full Year 2015 Results

Slide 3

72.1 78.1 84.8

6.5 12.7 18.3

0%

20%

40%

60%

80%

100%

2015E 2016E 2017E

Incumbents New Entrants

Most capacity will be added on Java in the near future

About 50% of the capacity growth comes from incumbents

Incumbents still dominate the market with the 3 biggest players holding well above

80% market share in 2015

Source: Company estimation Source: Company estimation

Production capacity by type of market

player (in million tons)

Production capacity by geography (in

million tons)

47.1 47.5 47.5 47.5 46.1 44.9 44.9 44.9 48.7

50.9 54.1

60.2 64.2

72.2

78.0

90.5

103.1

113.3 116.1

122.4 126.0

131.5 133.5

26.0 27.2 27.7 30.2 31.5 31.9

34.2 38.1 38.4

40.8

48.0

55.0 58.0 59.9 61.0

64.1 68.5

75.4

82.9 87.9

93.2

98.8

104.7

111.0

117.7

12.5 4.7 1.7 9.2 4.3 1.3 7.0 11.4 0.9 6.2 17.7 16.6 7.8 4.3 -3.0 5.0 7.0 10.0 10.0 6.0 6.0 6.0 6.0 6.0 6.0

Domestic Supply Domestic Demand Growth

Demand/Supply Outlook: Oversupply Market

Export

Consumption per

capita = 248kg Comparison:

Malaysia: 639 kg

Thailand: 564 kg

Vietnam: 502 kg

Consumption

per capita =

413kg

CAGR 2001-2015: 6.3% CAGR 2016-2025: 7.0%

Source: ASI and internal estimation

Conference Call Full Year 2015 Results

Slide 4

Yearly Volume & % Growth of Cement Consumption in

Indonesia of 15 years

vs GDP movement year by year

Source: Indonesian Cement Association, BPS Statistic

Conference Call Full Year 2015 Results

Slide 5

27.2 27.5 30.2 31.5 32.1

34.2

38.1 39.1 40.8

48.0

54.9 58.0

60.0 60.4

4.4% 4.7% 5.1% 5.6% 5.4%

6.3% 6.1%

4.6%

6.1% 6.5% 6.8% 5.7%

5.1% 4.7%

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

14.0%

16.0%

18.0%

20.0%

-

10.0

20.0

30.0

40.0

50.0

60.0

70.0

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

Domestic consumption (LHS) Cement growth % (RHS) GDP growth % (RHS)

In million tons

Indonesia’s Infrastructure Budget

114

146 156 153

224

314

27%

7%

-2%

46%

40%

-10%

0%

10%

20%

30%

40%

50%

0

50

100

150

200

250

300

350

Real 2011 Real 2012 Real 2013 Real 2014* Real 2015* 2016 budget

Infrastructure Budget (IDR tr) Growth of Infrastructure Budget (RHS)

Conference Call Full Year 2015 Results

Slide 6

There is a clear commitment to additional infrastructure

development which is urgently needed in Indonesia

Source: Citi

Infrastructure Projects (Java Area) and our Participation

No. ProjectsProject

Started

Project

Finished

Total

KM

Concrete

Used M3

1 Toll road Sorean - Pasir Koja Oct-15 May-17 8.5 80,000

2 Toll road Solo Kertosono Aug-15 Dec-16 7.0 1,500,000

3 Toll road Antasari - Depok - CMNP Mar-15 Mar-17 12.0 180,000

4 Toll road Bogor - Ciawi - Sukabumi section 2 and 3 Oct-15 Oct-17 10.0 210,000

5 Toll Serpong - Balaraja Apr-16 Apr-19 58.0 208,000

6 Cisundawa Mar-16 Mar-16 60.0 980,000

7 High speed railway Apr-16 Apr-19 150.0 230,000

8 Bandara Kertajati Apr-16 Apr-17 40,000

9 Toll Bawen - Solo Mid 2016 Mid 2018 17.6 352,000

10 PLTU Batang Mid 2016 Mid 2019 200,000

11 PLTU Tg Jati II Mid 2016 Mid 2019 250,000

12 Cisongkam Dam Mar-16 Mar-20 1,000,000

5,230,000

Conference Call Full Year 2015 Results

Slide 7

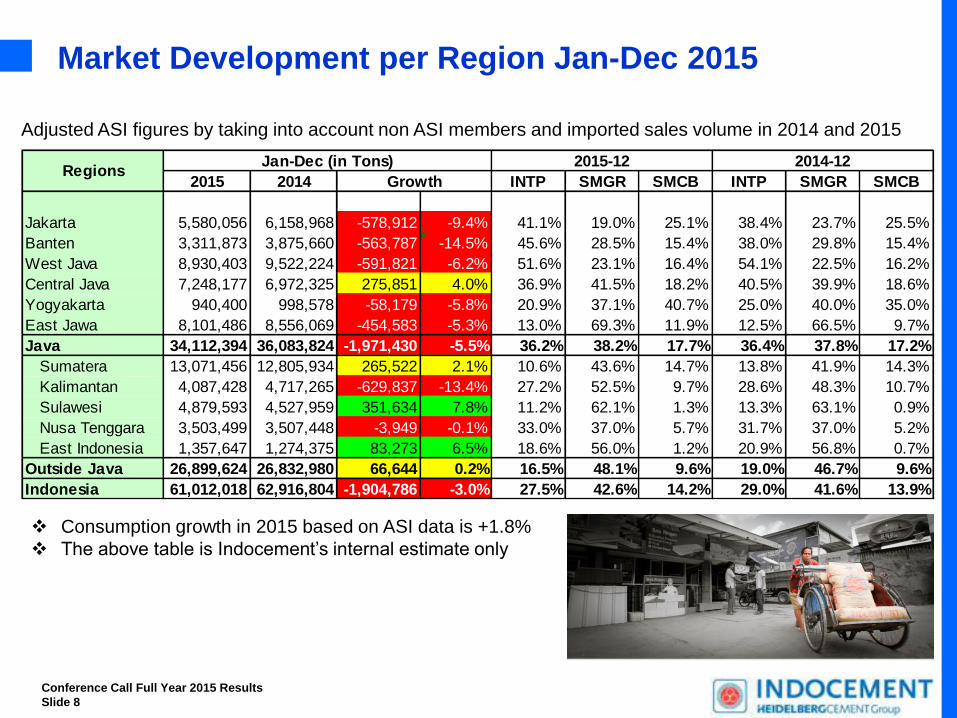

Market Development per Region Jan-Dec 2015

Jan-Dec (in Tons) 2015-12 2014-12

2015 2014 Growth INTP SMGR SMCB INTP SMGR SMCB

Jakarta 5,580,056 6,158,968 -578,912 -9.4% 41.1% 19.0% 25.1% 38.4% 23.7% 25.5%

Banten 3,311,873 3,875,660 -563,787 -14.5% 45.6% 28.5% 15.4% 38.0% 29.8% 15.4%

West Java 8,930,403 9,522,224 -591,821 -6.2% 51.6% 23.1% 16.4% 54.1% 22.5% 16.2%

Central Java 7,248,177 6,972,325 275,851 4.0% 36.9% 41.5% 18.2% 40.5% 39.9% 18.6%

Yogyakarta 940,400 998,578 -58,179 -5.8% 20.9% 37.1% 40.7% 25.0% 40.0% 35.0%

East Jawa 8,101,486 8,556,069 -454,583 -5.3% 13.0% 69.3% 11.9% 12.5% 66.5% 9.7%

Java 34,112,394 36,083,824 -1,971,430 -5.5% 36.2% 38.2% 17.7% 36.4% 37.8% 17.2%

Sumatera 13,071,456 12,805,934 265,522 2.1% 10.6% 43.6% 14.7% 13.8% 41.9% 14.3%

Kalimantan 4,087,428 4,717,265 -629,837 -13.4% 27.2% 52.5% 9.7% 28.6% 48.3% 10.7%

Sulawesi 4,879,593 4,527,959 351,634 7.8% 11.2% 62.1% 1.3% 13.3% 63.1% 0.9%

Nusa Tenggara 3,503,499 3,507,448 -3,949 -0.1% 33.0% 37.0% 5.7% 31.7% 37.0% 5.2%

East Indonesia 1,357,647 1,274,375 83,273 6.5% 18.6% 56.0% 1.2% 20.9% 56.8% 0.7%

Outside Java 26,899,624 26,832,980 66,644 0.2% 16.5% 48.1% 9.6% 19.0% 46.7% 9.6%

Indonesia 61,012,018 62,916,804 -1,904,786 -3.0% 27.5% 42.6% 14.2% 29.0% 41.6% 13.9%

Regions

Adjusted ASI figures by taking into account non ASI members and imported sales volume in 2014 and 2015

Consumption growth in 2015 based on ASI data is +1.8%

The above table is Indocement’s internal estimate only

Conference Call Full Year 2015 Results

Slide 8

13,576 14,259 13,745 16,427 14,076 14,868 14,050 16,916

13,626 14,088

15,411

17,882

10,000

11,000

12,000

13,000

14,000

15,000

16,000

17,000

18,000

19,000

Q1 Q2 Q3 Q4

2013 2014 2015

Market has surpassed the trough

Positive market development in Q3 and Q4

Clear indication that infrastructure spending has picked-up and

trend is expected to continue

Source: ASI, incl. imports

+9%

ASI includes data from new members of Merah Putih and Juishin starting in 2015

In thousand tons

Market sales development

+16%

Conference Call Full Year 2015 Results

Slide 9

Indocement sales development in line with our strategy

Continued trend of lower sales

volume development than

market development

Margin orientation

New market players

Capacity share

Domestic Sales in ‘000 tons FY Domestic Sales

2013: 17,975 m tons +0.5%

2014: 18,499 m tons +2.9%

2015: 17,052 m tons -7.7%

Export Sales in ‘000 tons

Exports still significantly lower

than domestic sales

Potential for more exports in

low demand periods

3,000

3,500

4,000

4,500

5,000

5,500

Jan-Mar Apr-Jun Jul-Sep Oct-Dec

2013 4,219 4,514 4,187 5,054

2014 4,296 4,676 4,226 5,301

2015 3,947 4,300 3,965 4,870

10

67

106

34

17 26

78

35

21

52

74 66

0

20

40

60

80

100

120

Jan-Mar Apr-Jun Jul-Sep Oct-Dec

2013 2014 2015

FY Export Sales

2013: 217 t tons

2014: 156 t tons

2015: 213 t tons

Conference Call Full Year 2015 Results

Slide 10

14,459 14,568 12,943

3,517 3,931

4,109

2,000

4,000

6,000

8,000

10,000

12,000

14,000

16,000

18,000

20,000

2013 2014 2015

Bag Bulk

The importance of bulk sales increases

Strong concrete demand expected due to Government infrastructure spending

Indocement positions itself as a reliable partner for infrastructure projects

providing quality bulk cement and concrete at timely delivery

Stronger focus on increasing bulk sales

High bulk volume in Jakarta

Indocement benefits from proximity to Jakarta

24%

76%

19%

81%

21%

79%

In thousand tons

Bag/bulk sales composition Jan - Dec

Conference Call Full Year 2015 Results

Slide 11

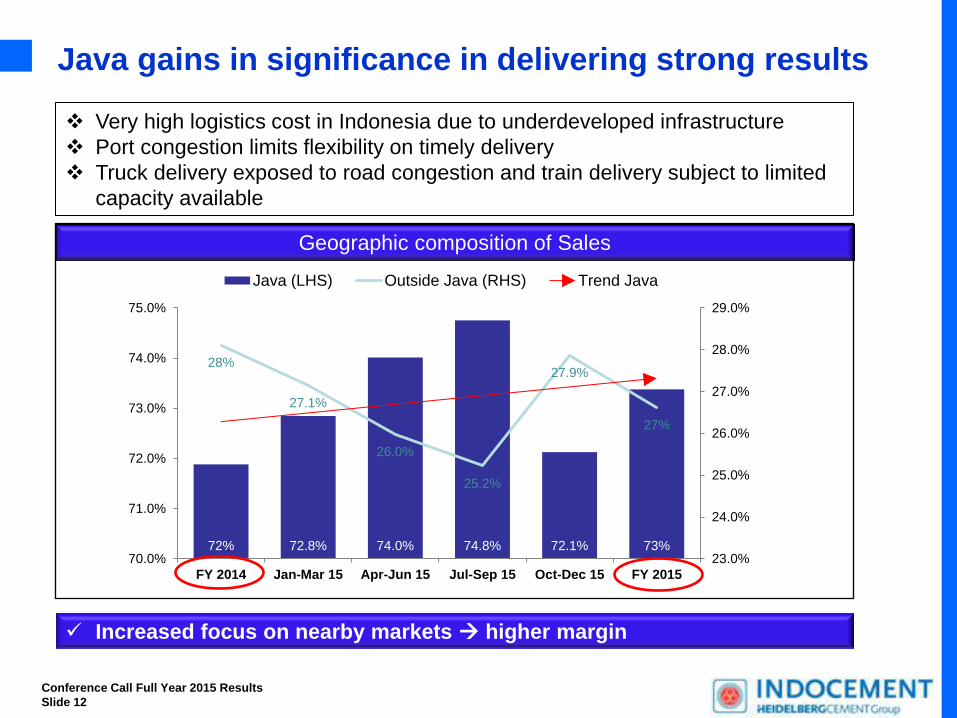

Java gains in significance in delivering strong results

Very high logistics cost in Indonesia due to underdeveloped infrastructure

Port congestion limits flexibility on timely delivery

Truck delivery exposed to road congestion and train delivery subject to limited

capacity available

Increased focus on nearby markets higher margin

Geographic composition of Sales

72% 72.8% 74.0% 74.8% 72.1% 73%

28%

27.1%

26.0%

25.2%

27.9%

27%

23.0%

24.0%

25.0%

26.0%

27.0%

28.0%

29.0%

70.0%

71.0%

72.0%

73.0%

74.0%

75.0%

FY 2014 Jan-Mar 15 Apr-Jun 15 Jul-Sep 15 Oct-Dec 15 FY 2015

Java (LHS) Outside Java (RHS) Trend Java

Conference Call Full Year 2015 Results

Slide 12

Financial Result

Consolidated Statement of Comprehensive Income

January to

December 31, 2015

January to

December 31, 2014

in IDR mio in IDR mio in IDR mio in %

(Restated)

Net Revenues 17,798,055 19,996,264 (2,198,209) -11.0%

Cost of Revenues -9,888,919 -10,890,037 1,001,118 -9.2%

Gross Profit 7,909,136 9,106,227 (1,197,091) -13.1%

% of Net Revenues 44.4% 45.5%

Operating Expenses -2,879,720 -3,226,452 346,732 -10.7%

Other Operating Income 27,514 121,094 (93,580) -77.3%

Operating Income 5,056,930 6,000,869 (943,939) -15.7%

% of Net Revenues 28.4% 30.0%

EBITDA 6,010,646 6,879,092 (868,446) -12.6%

% of Net Revenues 33.8% 34.4%

Finance Income 562,856 790,122 (227,266) -28.8%

Equity in net earnings of

associated companies - net25,325 24,487 838 3.4%

Final Income Tax -535 -842 307 -36.5%

Income before Income Tax 5,644,576 6,814,636 (1,170,060) -17.2%Income Tax Expense - Net -1,287,915 -1,521,220 233,305 -15.3%

Income for the Period 4,356,661 5,293,416 (936,755) -17.7%

% of Net Revenues 24.5% 26.5%

Variance

Conference Call Full Year 2015 Results

Slide 13

Sound margin development in 2015

Despite a competitive environment Management delivered on its margin

guidance by taking respective initiatives early on during the year:

Operational Excellence program

Fix cost reduction program

Managing efficient kiln utilization

INTP EBITDA margin development

New market entrants leading to higher competition and pricing pressure but

Indocement delivers superior margin development compared to peers

INTP Gross margin development

34.8% 34.5% 34.0% 33.8%

25%

27%

29%

31%

33%

35%

37%

39%

Jan-Mar Jan-Jun Jan-Sep Jan-Dec

2013 2014 2015

44.5% 45.0%

44.6% 44.4%

40%

41%

42%

43%

44%

45%

46%

47%

48%

Jan-Mar Jan-Jun Jan-Sep Jan-Dec

2013 2014 2015

Conference Call Full Year 2015 Results

Slide 14

Favorable cost development helped to partly offset

negative development from pricing

Fuel and power positively impacted by lower coal price and by running the most efficient

kilns in 2015 but negatively impacted from weakening Rupiah and higher electricity

price after significant increase starting May 2014

Future operation of new kiln P14 in 2016 will provide a significant potential on improving

manufacturing cost

Fuel and Power composition in % Composition of Manufacturing cost as %

Trend

40.0%

50.0%

60.0%

70.0%

80.0%

90.0%

100.0%

2013 2014 2015

Fuel Power

50/50

Fuel and power composition moved

from 60/40 to 50/50

Conference Call Full Year 2015 Results

Slide 15

25.7 9.9 44.1 20.3 26.1 10.4 43.4 20.2 0

10

20

30

40

50

Raw Materials Direct labor Fuel and Power Man. Overhead

Jan-Dec 2014 Jan-Dec 2015in %

Balance Sheet Consolidated Statement of Financial Position

Conference Call Full Year 2015 Results

Slide 16

December 31, 2015 December 31, 2014

in IDR mio in IDR mio in IDR mio %

(Restated)

Assets

Current Assets 13,133,854 16,087,370 (2,953,516) -18%

Non-current Assets 14,504,506 12,797,265 1,707,241 13%

Total Assets 27,638,360 28,884,635 (1,246,275) -4%

Liabilities and Equity

Current Liabilities 2,687,743 3,260,559 (572,816) -18%

Non-current Liabilites 1,084,667 1,047,063 37,604 4%Total Liabilities 3,772,410 4,307,622 (535,212) -12%

Equity attributable to Owners of

the Partent Entity 23,865,950 24,577,013 (711,063) -3%

Non-controlling interest - - -

Total Equity 23,865,950 24,577,013 (711,063) -3%

Total Liabilites and Equity 27,638,360 28,884,635 (1,246,275) -4%

Variance

1 brownfield project with capacity of 4.4 mio ton and investment cost of Rp5.5 – 6

trillion – first clinker by end of Q1/2016

1 unit an aero derivative gas turbine (ADGT) to supply 73 MW (including power supply

from Steam Turbine to Citeureup factory with electricity cost cheaper than current PLN

cost – GT & Steam turbine will run in full by Q3/2016

1 Cement and packing terminal in Pontianak to strengthen our bagged cement supply

in West Kalimantan area – ready by Q2/2016

2 greenfield or brownfield project with each capacity of 2.5 mio ton one in Central Java

(under appeal process for Environmental permit issues) and one in outside Java

16.6 30-33 17.1 18.6 20.6 25

2005 2007 2010 2014 2016 2020/2025

Million Tons

+ 0.6 mt + 1.5 mt + 1.9 mt

+ 4.4 mt

+ 5-8 mt

Strategically well positioned to capitalize on further demand

Capacity Expansion & Future Investment to participate

in Industry Growth

Conference Call Full Year 2015 Results

Slide 17

Outlook for 2016

National market 2016 estimated to grow about 3%-5%

Strong concrete and bulk cement demand anticipated due to Government's infra

projects

− Secured our concrete market by having good andesite quarry and sand supply from

Ketapang and Belitung by signing exclusive LT supply contract with local partners

Several new market players expected to enter the market

Possible price pressure in weak quarters but stabilizing trend in stronger months

Commodity prices expected to stay at current level but further weakening of

Rupiah anticipated

P14 will be ramped up quickly to capitalize on cost savings

Clinker exports will be done in low demand periods

Lower Capex spending due to finalization of our brownfield project P14

Strong balance sheet with no gearing provides sufficient headroom for leading

the market well especially in our home market

Conference Call Full Year 2015 Results

Slide 18

Challenges in Year 2016 onward How to win in a very tight Competitive Cement Market?

Cost Management

In Land: Traffic & Truck Availability

Train & Vessels: Double-handling cost; limited deep water Port

Strong Brand & Corporate Image

High Quality, Availability & Excellent Customer Services

Strong 40 year Distributorship network

• Infrastructure

Development in

Java & Outside Java

• Domino-effect for

residential/ housing

development after

infrastructure is

fully developed

• More sophisticated

design of

infrastructure &

building (MRT, Dam,

& 50-60 stories

building) require

high quality cement

& concrete

Conference Call Full Year 2015 Results

Slide 19

For Better Building Thank you

Indocement 40th Anniversary –

Strong and Reliable in Developing the Nation

Conference Call Full Year 2015 Results

Slide 20