CONDENSED INTERIM CONSOLIDATED REPORT AT 30 … · Giorgio Sangiorgio General Management General...

155

Credito Valtellinese S.p.A. Credito Valtellinese S.p.A. Credito Valtellinese S.p.A. Credito Valtellinese S.p.A. Registered Offices in Piazza Quadrivio 8 - Sondrio, Italy Tax code and Sondrio Company Registration No. 00043260140 - Register of Banks No. 489 Parent of the Credito Valtellinese Banking Group - Register of Banking Groups No. 5216.7 Website: http://www.creval.it E-mail: [email protected] Data at 30 June 2018: Share Capital EUR 1,916,782,886.55 Member of the Interbank Guarantee Fund CONDENSED INTERIM CONSOLIDATED REPORT AT 30 JUNE 2018

Transcript of CONDENSED INTERIM CONSOLIDATED REPORT AT 30 … · Giorgio Sangiorgio General Management General...

Credito Valtellinese S.p.A.Credito Valtellinese S.p.A.Credito Valtellinese S.p.A.Credito Valtellinese S.p.A. Registered Offices in Piazza Quadrivio 8 - Sondrio, Italy

Tax code and Sondrio Company Registration No. 00043260140 - Register of Banks No. 489 Parent of the Credito Valtellinese Banking Group - Register of Banking Groups No. 5216.7

Website: http://www.creval.it E-mail: [email protected] Data at 30 June 2018: Share Capital EUR 1,916,782,886.55

Member of the Interbank Guarantee Fund

CONDENSED INTERIM CONSOLIDATED REPORT AT 30 JUNE 2018

2

COMPANY OFFICERS OF CREDITO VALTELLINESE

in office at 9 August 2018

Board of Directors

Chairman Miro Fiordi

Deputy Chairman Michele Colombo

Managing Director Mauro Selvetti

Directors Elena Beccalli

Mariarosa Borroni

Gabriele Cogliati

Giovanni De Censi

Flavio Ferrari

Maria Elena Galbiati

Paolo Stefano Giudici

Gionni Gritti

Livia Martinelli

Tiziana Mevio

Paolo Scarallo

Alberto Sciumè

Mauro Selvetti

Board of Statutory Auditors Chairman Angelo Garavaglia

Standing Auditors Giuliana Pedranzini

Luca Francesco Franceschi

Substitute Auditors Edoardo Della Cagnoletta

Giorgio Sangiorgio

General Management General Manager Mauro Selvetti

Substitute Deputy General Manager Umberto Colli

Deputy General Managers Saverio Continella

Vittorio Pellegatta

Enzo Rocca

Heads of the Main Corporate Functions

Chief Risk Officer (CRO) Fabio Salis

Chief Operating Officer (COO) Umberto Colli

Chief Lending Officer (CLO) Vittorio Pellegatta

Chief Financial Officer (CFO) Ugo Colombo

Chief Commercial Officer (CCO) Roberto Tarricone

Manager in charge of financial reporting Simona Orietti

Audit Company KPMG S.p.A.

3

Contents COMPANY OFFICERS OF CREDITO VALTELLINESE ........................................................................... 2

CONSOLIDATED HIGHLIGHTS AND ALTERNATIVE PERFORMANCE INDICATORS AT 30 JUNE

2018 ........................................................................................................... 4

ORGANISATIONAL MODEL AND BREAKDOWN OF THE CREDITO VALTELLINESE BANKING

GROUP .......................................................................................................... 6

REPORT ON OPERATIONS .................................................................................... 8 Events of bank operations during the first half of the year ........................................................................... 11

Information on the main statement of financial position items and on consolidated income statement figures .................................................................................................................................................. 15

Events after the close of the half-year .......................................................................................................... 29

Current-year outlook ................................................................................................................................... 31

CONDENSED INTERIM CONSOLIDATED FINANCIAL STATEMENTS .................................. 33

Condensed interim consolidated financial statements ...................................................... 34 Notes to the condensed interim consolidated financial statements .................................... 41

CERTIFICATION OF THE CONDENSED INTERIM CONSOLIDATED FINANCIAL STATEMENTS

PURSUANT TO ARTICLE 81-TER OF CONSOB REGULATION NO. 11971/99.................. 153REPORT OF THE AUDITORS ................................................................................ 154

4

CONSOLIDATED HIGHLIGHTS AND ALTERNATIVE

PERFORMANCE INDICATORS AT 30 JUNE 2018

STATEMENT OF FINANCIAL POSITION DATA 30/06/2018 31/12/2017 Change

(in thousands of EUR)

Loans and receivables with customers 21,434,668 16,680,944 28.50%

Financial assets and liabilities at fair value 2,134,033 4,300,828 -50.38%

Non-current assets held for sale and disposal groups 89,471 3,955 n.s.

Total assets 26,033,597 24,956,824 4.31%

Direct funding from customers 20,414,126 19,631,283 3.99%

Indirect funding from customers 10,437,811 11,273,213 -7.41%

of which:

- Managed funds 7,331,272 7,801,592 -6.03%

Total funding 30,851,937 30,904,496 -0.17%

Equity 1,493,059 1,442,094 3.53%

SOLVENCY RATIOS 30/06/2018 31/12/2017

Common Equity Tier 1 capital / Risk-weighted assets (CET1 capital ratio) 14.0% 10.6%

Tier 1 capital / Risk-weighted assets (Tier 1 capital ratio) 14.0% 10.6%

Total own funds / Risk-weighted assets (Total capital ratio) 15.5% 12.5%

FINANCIAL STATEMENT RATIOS 30/06/2018 31/12/2017

Indirect funding from customers / Total funding 33.8% 36.5%

Managed funds / Indirect funding from customers 70.2% 69.2%

Direct funding from customers / Total liabilities and equity 78.4% 78.7%

Loans and receivables with customers / Direct funding from customers 105.0% 85.0%

Loans and receivables with customers / Total assets 82.3% 66.8%

CREDIT RISK 30/06/2018 31/12/2017 Change

Net bad loans (in thousands of EUR) 228,456 657,512 -65.25%

Other net doubtful loans (in thousands of EUR) 739,678 1,540,116 -51.97%

Net non-performing loans (in thousands of EUR) 968,134 2,197,628 -55.95%

Net bad loans / Loans and receivables with customers 1.1% 3.9%

Other net doubtful loans / Loans and receivables with customers 3.5% 9.2%

Net non-performing loans / Loans and receivables with customers 4.5% 13.2%

Coverage ratio of bad loans 71.5% 62.3%

Coverage ratio of other doubtful loans 36.7% 32.3%

Coverage ratio of non-performing loans 50.9% 45.3%

Loans and receivables with customers classified under assets held for sale are not included.

5

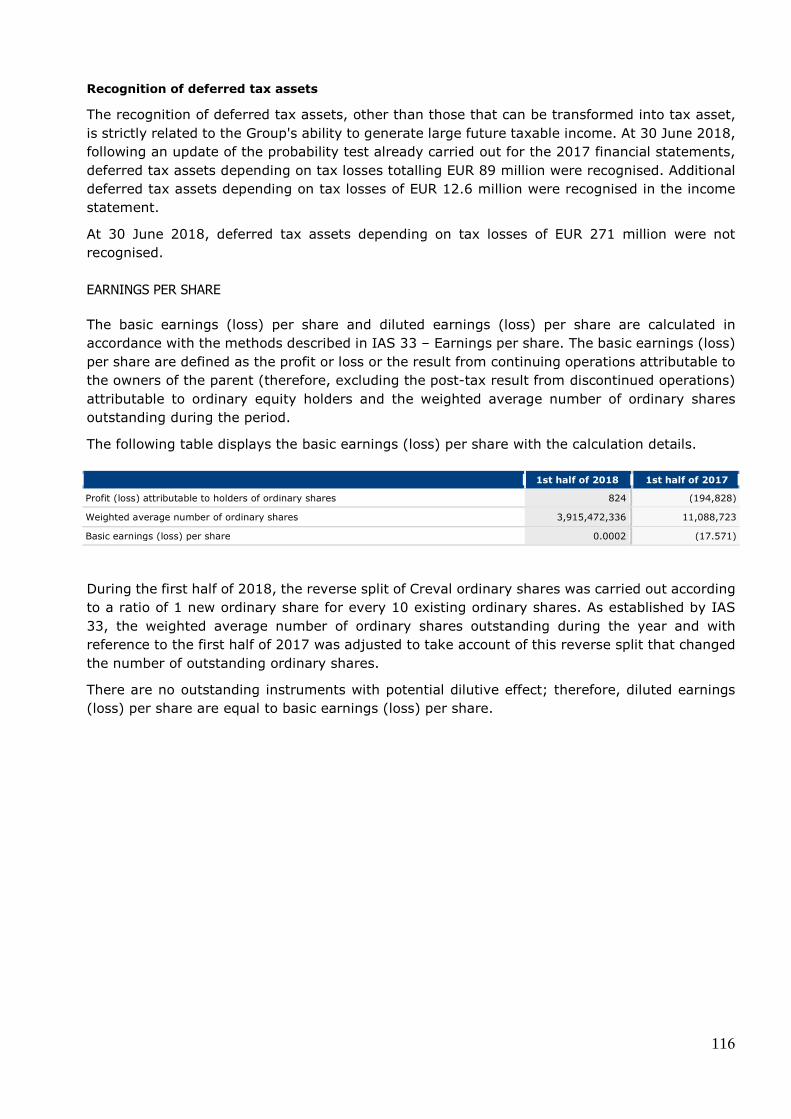

INCOME STATEMENT DATA 1st half of 2018

1st half of 2017

Change

(in thousands of EUR)

Net interest income 178,879 198,772 -10.01%

Operating income 340,979 379,043 -10.04%

Operating costs (306,956) (255,880) 19.96%

Operating profit 34,023 123,163 -72.38%

Pre-tax loss from continuing operations (28,232) (190,523) -85.18%

Post-tax profit (loss) from continuing operations 2,545 (193,000) -101.32%

Profit (loss) for the period 824 (194,828) -100.42%

ORGANISATIONAL DATA 30/06/2018 31/12/2017 Change

Number of employees 3,902 3,819 2.17%

Number of branches 363 412 -11.89%

OTHER FINANCIAL INFORMATION 1st half of

2018 1st half of

2017

Cost/Income ratio (*) 66.5% 66.9%

(*) Figure of the first half of 2018 calculated net of non-recurring expenses related to the implementation of the "Solidarity Fund" (EUR 66,497 thousand), of ordinary and extraordinary contributions paid to SRF (EUR 12,611 thousand) and of contributions for the DTA fee (EUR 1,078 thousand); figure of the first half of 2017 calculated net of ordinary contributions paid to SRF (EUR 7,922 thousand), DTA fee contributions (EUR 1,077 thousand) and non-operating income related to the implementation of the “2016 Solidarity Fund” (EUR 6,816 thousand) With reference to the financial highlights and alternative performance indicators represented above, the amounts used for their calculation, if not specified in the notes to the tables, are indicated in “Information on the main statement of financial position items and on consolidated income statement figures”. These indicators, prepared by the management, provide additional information to investors since they facilitate the understanding of statement of financial position and income statement, they should not be considered as a replacement of those required by IAS/IFRS and are not always comparable with those provided by other banks.

6

ORGANISATIONAL MODEL AND BREAKDOWN OF THE

CREDITO VALTELLINESE BANKING GROUP

The Credito Valtellinese Banking Group currently consists of the territorial bank Credito

Valtellinese, specialised companies and special purpose companies for the provision of

services - with a view to achieving synergies and economies of scale - to all the companies

of the Group. The current group structure is graphically represented below.

*Insurance companies subject to management and coordination by Credito Valtellinese pursuant to Articles 2497 et sequitur of the Italian Civil Code. At 30 June 2018, the Credito Valtellinese Group is present in Italy with a network of 363

Branches, in eleven regions, through the territorial bank characterising the “Market

Segment”:

- Credito Valtellinese S.p.A., the Parent, present with its own network of 363 branches,

most of which - 159 - are in Lombardia, as well as in Valle d'Aosta, Piemonte, Veneto,

Trentino Alto Adige, Emilia Romagna, Toscana, Lazio, Marche, Umbria and Sicilia.

The following companies characterise the “Specialised Companies Segment”:

- Global Assicurazioni S.p.A.1, a multifirm insurance agency specialised in the brokerage

and management of standard insurance policies in favour of individuals and household

customers.

- Global Broker S.p.A.2, insurance broker specialised in the brokerage and management

of insurance policies in favour of companies.

- Creval PiùFactor S.p.A., Group company exclusively dedicated to activities granting

loans to the public pursuant to Articles 106 et sequitur of Italian Legislative Decree no. 385

of 1 September 1993 (“Consolidated Banking Act”).

- Claris Factor S.p.A., Group company dedicated to the management of business loans

and other loans pursuant to Articles 106 et sequitur of Italian Legislative Decree no. 385 of

1 September 1993 (“Consolidated Banking Act”).

1 Company subject to management and coordination by Credito Valtellinese and therefore included in the consolidation scope, even if not included in the Banking Group, pursuant to the supervisory provisions, in that it carries out insurance activities. 2 See previous note.

Credito Valtellinese Creval Sistemi e Servizi

Stelline Real Estate

Global Assicurazioni*

Global Broker*

Creval PiùFactor

MARKET SPECIALISED COMPANIES CORPORATE CENTRE

Claris Factor

7

The companies providing services complementary to banking business characterising the

“Corporate Centre Segment” complete the Group:

- Creval Sistemi e Servizi S.c.p.A. company that manages and develops activities relating

to Information and Communication Technology (ICT), organisation, back office, real estate

services and support processes.

- Stelline Real Estate S.p.A., R.E.o.Co. (Real Estate Owned Company), Group

company exclusively dedicated to asset repossessing.

8

REPORT ON OPERATIONS

The general economic framework3

The global economy continues to grow at a good pace, but some risks are materialising.

The American economy is expanding at a high rate, supported by the significant tax

incentives introduced by the Trump administration and by a monetary policy that is still

easy-going.

Europe, although remaining in an expansive cyclical phase, started the year lower than

expected; China continues to grow at rates close to 6%, albeit slightly decreasing.

During the second quarter, three drivers gained strength, which were already weighted in

the framework outlined in Prometeia's Report in March. At present, these developments do

not constitute a significant deviation from what is included in the Bank's valuations.

The first factor to be taken into consideration is related to the gradual increase in oil prices

that began in the summer of 2017: it contributed to the strengthening of inflation indices

worldwide and to a prospective shift towards greater monetary restriction by central banks.

The second feared aspect in the publication of the Prometeia scenario in March, but which

became concrete with the publication of Eurostat data on GDP of the Eurozone, is that the

growth of the main countries in the area was surprisingly below expectations in the first

quarter. In part, the slowdown reflects a return of growth to a more sustainable pace after

the exceptional result in 2017, and in part, it reflects increased uncertainty about future

prospects. Prometeia forecasts indicate that growth will continue for the coming quarters at

the pace of the beginning of the year. Therefore, the growth forecast for 2018 in the

Eurozone was revised from +2.3% to +2.1% between March and July.

The third aspect concerns the exacerbation of tensions related to the protectionist policies

of the Trump Administration compared to the scenario formulated in March. To date,

Prometeia's baseline scenario does not foresee that this escalation will trigger a real trade

war. However, it should be noted that, in this context, uncertainty among operators has

increased and is reflected in the fall in share prices in the sectors most affected. The

macroeconomic risks related to the protectionist positions of the US Administration are

related to the reduction in trade, which in turn could affect the confidence and investment

plans of companies operating in international markets.

The Italian economic scenario shows continued growth, despite signs of a slowdown in

spring.

In the first three months of this year, Italy's GDP rose by 0.3%, a slight slowdown compared

to the last quarter of 2017. Growth forecasts for 2018 were revised downwards from 1.4%

to 1.2%. The Bank of Italy estimates (consistent with the Prometeia forecast) show in the

second quarter that GDP expansion would have continued at a rate just below that of the

previous period (0.2% compared to 0.3%). In June, the Ita-coin indicator developed by the

Bank of Italy continued to fall, recording a slowdown in industrial activity and the economic

cycle. The Purchasing Managers’ Indexes give slightly more favourable signals; the latest

improved measurements restore confidence at least in the stability of expansion also in the

third quarter of the year.

3 The incorporated scenario for the measurement of the financial statements consistent with the new international

standards (IFRS 9) is based on Prometeia's Forecast Report in March 2018. For a comprehensive description of the

economic, credit and financial situation, as of the date of this report, the following documentary sources have been

used: Prometeia - Forecast Report, March 2018; Prometeia - Forecast Report, July 2018. Bank of Italy Economic

Bulletin no. 3/2018.

9

The March baseline scenario for Italy, assumed in the internal models and still valid, includes

a slowdown in the tax consolidation process, in line with pre-election announcements. In

any case, given the envisaged macroeconomic scenario, the path would allow a moderate

decline in public debt in relation to output, a condition of primary importance for ensuring

the stability of the country.

Recent statements by some Government representatives indicated their intention to

manage public accounts prudently and within European rules. This reassured us about the

country's prospects but, as the prices of government bonds and banking sector shares show,

it did not completely dispel the uncertainties that arose during May.

Comparing the baseline scenario of March with that published by Prometeia in July, the

forecast horizon taken as a reference to 2020 shows the increase in inflation forecasts, an

improvement in real estate prices and an upward revision of short-term interest rate

expectations. The forecasts for the spread between the Italian and German ten-year

benchmarks were revised upwards in line with the phase of instability experienced in May

related to the formation of the new government.

The Italian banking system

In the banking scenario of March, Prometeia reported that “Credit will be able to grow at a

faster rate in the three-year forecast period”. This phrase was then re-adjusted in the July

2018 Report with “A difficult recovery for credit for businesses”, which indicates greater

caution in the forecast following the rise in the risk of trade war, accentuated by the actions

carried out and threatened by the US Administration. Even though the economy has been

growing for several quarters together with investment, the credit granted to businesses has

been modest in recent quarters. Loans to households was better, supported by good lending

conditions and the stabilisation of the real estate market.

In addition to the reasons listed above, from this year there is also the introduction of the

new accounting standard IFRS 9, which envisages higher provisions for performing but “high

risk” loans, and which therefore is likely to make banks even more careful in selecting the

companies to be granted loans.

The expected acceleration in the process of reducing non-performing loans, which will lead

to an improvement in asset quality, may help to offset this trend in the coming quarters. A

process that in turn generates a positive prospective contribution to profitability.

The most recent figures show that, in Italy, the trend in bank loans, adjusted for those

securitised or otherwise disposed of, strengthened in April (3.0% from 2.4% in March).

The sustained growth of loans to Italian households continued and, for almost two years,

has been in line with the average of the countries in the Eurozone (2.9% in April).

In April, loans to businesses grew by EUR 3 billion mainly on short maturities (2.2% per

year) and the first advances confirm an increase also in May. The flow of funds in the first

four months of the year was approximately 14 billion (-5.5 billion in the same period of

2017).

In April, loans to households increased by EUR 0.7 billion (more than EUR 5 billion from the

beginning of the year), with an annual growth of 2.9%, substantially confirmed in May and

in line with the EMU average. The increase concerned loans for purchasing homes and

consumer credit (8.6% and 1.9% per year).

The rate on new loans to businesses in April fell by 7bp. The economic trend of the rate on

new loans of less than EUR 1 million, mainly addressed to SMEs, is similar, whereas, if

considered compared to April 2017, the reduction is more significant, equal to 22bp. Interest

rates on loans to households for the purchase of homes also fell (-4bp).

Bank deposits in the first four months of the year fell by EUR 7 billion (-7.2% per year) as

a result of a reduction in internal funding of EUR 17 billion, entirely attributable to a

reduction in the stock of bonds issued, and a positive contribution of foreign funding of EUR

10

10 billion. The increase in total funding of EUR 1.6 billion was accompanied by an increase

in current accounts, mainly for households, whereas, with a reduction of more than 6 billion,

the process of accumulating liquidity recorded in recent years by businesses seems to have

been interrupted.

The financial market in Italy

After a good start, 2018 was characterised by a temporary return of volatility on the stock

markets between late January and February. In fact, at the end of January, fears of an

inflationary blaze in America triggered a sharp fall in share indices, up to over 10%, and a

sharp rebound in volatility to levels that had not been experienced in years.

The Italian stock market also suffered from the January sell-off, but then began to rise again

along with all the other indices regardless of the political uncertainty that was expected both

before and after the general elections in early March. To coincide with the new government

formed in May, the uncertainty of international investors on Italy materialised again with

the rise in the spread between Italian and German government bonds to close to 300 basis

points for the ten-year maturity. The interest rate curve was characterised by a strong

growth in short-term rates, even stronger than in long-term rates. Tensions were mostly

limited to the Italian market, in that there were limited contaminating effects on other

European countries. The spread on government bonds has partly recouped but remains

higher than the values prevailing at the beginning of May.

There was no rebound in the FTSE MIB or the banking sub-index, which is the one that

suffered the most, having lost about 20% of its value since mid-May.

11

Events of bank operations during the first half of the year

The most important events that characterised the management of the Creval Group during

the first half of 2018 and that, if necessary, were the subject-matter of specific disclosures

to markets are mentioned below.

2018-2020 Business Plan

In line with established times, activities aimed at achieving priority objectives set out in the

2018-2020 Business Plan, approved in November last year, continued.

Specifically:

Equity enhancement

On 20 March 2018, with the full subscription of the newly issued shares, without the

intervention of first-allocation sub-underwriters and the underwriting syndicate, the capital

increase (“Project Renaissance”) was concluded for a total amount (including share

premium) of EUR 699,660,561.30. The transaction, approved by the Extraordinary

Shareholders' Meeting of 19 December 2017, strengthened significantly the company's

equity condition.

De-risking and asset quality actions

An agreement was signed on 6 April 2018 for the sale of a portfolio of non-performing

secured loans - consisting of credit exposures mainly to real estate companies, mostly

classified as unlikely to pay (UTP) - for a gross book value (GBV) of more than EUR 245

million, at a price higher than 43% of the GBV.

An agreement was reached on 8 May 2018 for the sale to Credito Fondiario of a portfolio of

non-performing secured loans – consisting of credit exposures mainly to real estate

companies, classified as UTP and bad loans – for a GBV of EUR 222 million, at a price close

to 41% of the GBV.

The disposal through a securitisation of a portfolio of bad debts for a Gross Book Value

(“GBV”) of approximately EUR 1.6 billion at the cut-off date (31 December 2017) was

completed on 13 June 2018 (known as “Project Aragorn”), by transferring this portfolio

to a securitisation vehicle established pursuant to Italian Law 130/99, and this vehicle

issuing three different classes of ABS securities:

- a senior tranche of EUR 509.5 million, with expected rating in line with the requirements

of the regulations relating to the State guarantee (GACS),

- a mezzanine tranche with rating and a junior tranche of EUR 66.8 million and EUR 10

million, respectively.

The securities of the senior tranche – for which the State guarantee (GACS) was requested

– are fully considered by Credito Valtellinese, whereas the mezzanine and junior tranches

were placed by 95% with an institutional counterpart at the end of a competitive process.

The Aragorn portfolio was derecognised in accounting terms in June, whereas the prudent

derecognition is subject to obtaining GACS.

With these transactions, the objective defined in the Business Plan is almost completely

achieved especially with regard to the “deconsolidation of non-performing loans for an

equivalent amount up to EUR 2.1 billion, through a new securitisation transaction (“Project

Aragorn”), with possible use of the State guarantee (GACS) for a GBV of approximately

EUR 1.6 billion and further sales of non-performing loans of EUR 500 million at the end of a

competitive process (“Project Gimli”)”.

12

The decrease in non-performing loans during the half-year was accompanied by a

strengthening of the coverage levels that, partly as a result of the impact of the first-time

adoption of IFRS 9, had risen to 50.9% at 30 June 2018 compared to 45.3% at 31 December

2017. In particular, coverage for bad loans was 71.5% (62.3% at 31 December 2017),

among the highest in the Italian banking system.

At the same time, activities aimed at the adoption of advanced AIRB models for determining

prudential requirements continued, after receipt of the authorisations from the relevant

Supervisory Authorities. The inspection of Bank of Italy for the validation of the AIRB models

was completed in the half-year.

Operational efficiency and cost control

On 16 April, an agreement was signed with the trade unions for managing redundancies,

through the use of the Solidarity Fund for the credit sector. The agreement envisaged an

early retirement plan for at least 170 employees who would have met the pension

requirements by 31 December 2024 and who would have been able to access on a voluntary

basis the extraordinary benefits of the Solidarity Fund effective as from 1 July 2018. At the

end of the period, 219 applications were received, in addition to the objective set out in the

Business Plan, which was thus fully achieved, making use only of voluntary schemes. The

219 employees had access to the benefits of the Solidarity Fund effective as from 1 July

2018. The decrease in the workforce will cut personnel costs for about EUR 9 million in 2018

and about EUR 18 million per year as from 2019, against costs for implementing the Fund

totalling approximately EUR 66.5 million, fully recognised in the income statement in the

current year.

The operating network optimisation plan was defined, with the closure of a further 50

branches from 27 May 2018, and the transformation of 4 branches into branches of the

“Bancaperta” line. The total number of branches is therefore 363, in line with the target

structure of the operating network of 350 branches at the end of 2018 set out in the business

plan.

On 18 June, the deed of merger into Credito Valtellinese S.p.A. of Credito Siciliano S.p.A.

was signed (“Project One Bank”). The merger was legally effective as from 25 June 2018

as established in the deed of merger.

On 29 June 2018, the acquisition of 100% of the share capital of Claris Factor S.p.A. by

Veneto Banca S.p.A. in compulsory winding-up was completed for a consideration of EUR 5

million. The acquisition of Claris Factor will make it possible to achieve the development

targets for factoring operations more quickly and effectively, particularly once the merger

of Claris Factor S.p.A. and Creval PiùFactor S.p.A., a company of the Creval Group

specialising in the factoring sector, has been completed by the end of 2018.

The plan to merge CrevalPiù Factor into Claris Factor - which after the merger will be known

as CrevalPiù Factor - was approved by the Boards of Directors of the companies concerned

on 8 August 2018.

Development of the business model - Reorganisation of bancassurance activities

Still in line with the objectives set out in the 2018-2020 Strategic Plan, activities aimed at

defining a new operating model for the bancassurance business continued during the half-

year. These activities led to the definition of long-term strategic partnerships with Crédit

Agricole Assurances SA (“CAA”) in the Life segment and with the Insurance Group Ri-Fin

S.r.l. (“Rifin”) in the Non-Life segment, respectively.

For details of these agreements - signed on 24 July 2018, i.e. after the end of the half-year

- please refer to the specific section of this report.

13

The operational structure, the customers and the commercial

performance indicators

The territorial network

At 30 June 2018, the branches forming the territorial network of Credito Valtellinese are

363 as represented below.

Other distribution channels

The following other distribution channels complete the operational structure:

ORGANISATIONAL DATA 30/06/2018 31/12/2017 Change

Number of ATMs 534 558 -4.30%

Number of POS 26,711 27,162 -1.66%

Bancaperta line users 291,998 283,864 2.87%

Interbank Corporate Banking contracts 17,932 17,836 0.54%

At the end of June 2018, “active” Internet users in the Creval Group - customers who have

performed at least one transaction in the last six months - total 291,998, compared to

283,864 at the end of December of the prior year, with an increase of 2.87%.

CREDITO

VALTELLINESE 363

159 BRANCHES 8 BRANCHES

12 BRANCHES

6 BRANCHES

25 BRANCHES

2 BRANCHES

94 BRANCHES

30 BRANCHES

8 BRANCHES

18 BRANCHES

1 BRANCH

14

Commercial performance indicators

At 30 June 2018, the retention rate is equal to approximately 95.29%, whereas the cross-

selling indicator - equal to 3.91 products on average per customer (calculated on the basis

of the “ABI method”), attests also a high degree of optimisation of commercial relations.

The personnel

At the end of June 2018, the registered workforce of the companies included in the

consolidation scope of the Group consisted of 3,894 collaborators (compared to 3,957

resources at the end of 2017). These include 13 collaborators employed by companies or

entities outside the Group, among them Fondazione Gruppo Credito Valtellinese, Global

Assistance, the Pension Fund for the Employees of the Credito Valtellinese Group and Cerved

Group.

In terms of professional categories, the total workforce of 3,894 can be broken down as

follows:

- 50 executives;

- 1,501 middle managers;

- 2,343 workers in other professional categories.

Workforce by contract category at 30 June 2018

EXECUTIVES

1.3%

MIDDLE MANAGERS

38.5%

PROFESSIONAL

CATEGORIES

60.2%

EXECUTIVES

MIDDLE MANAGERS

PROFESSIONAL CATEGORIES

15

Information on the main statement of financial position items and on consolidated income

statement figures

The interim results are commented upon in summary format, drawn up on a consolidated

basis, reclassified according to the presentation criteria considered most appropriate for

presenting a fair view of the Group's operating performance.

The aggregates and reclassifications regarding items of the financial statements as

envisaged in Bank of Italy Circular no. 262/05 as amended are detailed in the Notes to the

financial statements.

The period of comparison, referring to the 2017 financial year, has been restated in a

reclassified form based on the new financial statements included the 5th update of Bank of

Italy Circular no. 262/05 that implements IFRS 9 with the consequent changes introduced

in other international accounting standards, and considers the new international accounting

standard IFRS 15 “Revenue from Contracts with Customers”. The accounting balances at 31

December 2017 were reclassified to the new accounting items without applying the new

classification and measurement criteria. The notes to the financial statements show the

effects of the first-time adoption of IFRS 9 and contain reconciliation statements.

The reclassified consolidated statement of financial position is shown below. (in thousands of EUR)

ASSETS 30/06/2018 31/12/2017 Change

Cash and cash equivalents 150,237 197,829 -24.06%

Financial assets at fair value through profit or loss 243,265 20,681 n.s.

Financial assets at fair value through other comprehensive income

2,026,565

4,419,352

-54.14%

Loans and receivables with banks 596,586 2,033,413 -70.66%

Loans and receivables with customers 21,434,668 16,680,944 28.50%

Hedging derivatives - 199 -100.00%

Equity investments 25,167 24,371 3.27%

Property, equipment and investment property and intangible assets (1)

487,760 486,524 0.25%

Non-current assets held for sale and disposal groups 89,471 3,955 n.s.

Other assets (2) 979,878 1,089,556 -10.07%

Total assets 26,033,597 24,956,824 4.31%

(1) Include the items "90. Property, equipment and investment property" and "100. Intangible assets" (2) Include the items “110. Tax assets” and “130. Other assets"

16

(in thousands of EUR)

LIABILITIES 30/06/2018 31/12/2017 Change

Due to banks 3,124,573 3,143,189 -0.59%

Direct funding from customers (1) 20,414,126 19,631,283 3.99%

Financial liabilities held for trading 198 713 -72.23%

Hedging derivatives 135,599 138,691 -2.23%

Other liabilities 622,929 421,399 47.82%

Provisions for specific purpose (2) 242,602 174,103 39.34%

Equity attributable to non-controlling interests 511 5,352 -90.45%

Equity (3) 1,493,059 1,442,094 3.53%

Total liabilities and equity 26,033,597 24,956,824 4.31%

(1) Includes items "10. Financial liabilities at amortised cost: b) Due to customers; c) Securities issued". (2) Includes items "60. Tax liabilities, “90. Post-employment benefits" and "100. Provisions for risks and charges" (3) Includes items "120. Valuation reserves", "150. Reserves", "160. Share premium reserve", "170. Share capital", "180. Treasury shares", and "200. Profit (loss) for the period".

Loans and receivables with customers

At 30 June 2018, loans and receivables with customers amounted to EUR 21.4 billion

(of which EUR 4.9 billion in government bonds) compared to EUR 16.7 billion at 31

December 2017. Excluding government bonds and adjustments made at the time of FTA of

IFRS 9, the aggregate increased by 2.8%, mainly as a result of the increase in new

disbursements in the half-year, which totalled EUR 1.2 billion, up 13% year-on-year (of

which EUR 712 million in the second quarter, up by more than 40% compared to the

previous quarter), confirming the ongoing recovery of commercial activity. Credit quality

also improved: EL “expected loss” equal to 34bp for the “individuals” segment and 29bp for

the “SME and corporate” segment.

(in thousands of EUR) 30/06/2018 31/12/2017 Change

Current accounts 2,230,798 2,022,049 10.32%

Reverse repurchase agreements 307,479 712,064 -56.82%

Mortgages 9,422,792 9,309,630 1.22%

Credit cards, personal loans and salary-backed loans 221,013 264,821 -16.54%

Finance leases 350,208 377,218 -7.16%

Factoring 145,088 - -

Other loans 1,891,453 1,319,920 43.30%

Debt instruments 5,897,703 477,614 n.s.

Total net performing loans and receivables 20,466,534 14,483,316 41.31%

Bad loans 228,456 657,512 -65.25%

Unlikely to pay 642,410 1,436,787 -55.29%

Past due non-performing loans 97,268 103,329 -5.87%

Total net non-performing loans and receivables 968,134 2,197,628 -55.95%

Total net loans and receivables 21,434,668 16,680,944 28.50%

17

Net non-performing loans not reclassified to assets held for sale (Non-Performing Exposure,

NPE) totalled EUR 968 million at the end of the period, down by EUR 1.2 billion (-56%)

compared to EUR 2.2 billion at the end of December 2017. The decrease is due to the sale

of non-performing loans during the half-year and to the adjustments made at the time of

FTA of IFRS 9.

In detail, net bad loans amounted to EUR 228.5 million, down by 65% from EUR 657.5

million at the end of 2017; net unlikely to pay reached EUR 642.4 million, down by 55%

from EUR 1,436.8 million at the end of 2017; net past due non-performing loans reached

EUR 97.3 million, down by 6% from EUR 103.2 million at the end of 2017. The coverage

ratio of non-performing loans (excluding those reclassified to discontinued operations) stood

at 50.9%, up compared to 45.3% of 31 December 2017 despite the disposals made. If we

also include removals, the total coverage ratio rises to 53.8%.

(in thousands of EUR)

30/06/2018 31/12/2017

Gross amount

Impairment losses

Carrying amount

coverage % Gross

amount Impairment

losses Carrying amount

coverage %

Non-performing loans

Bad loans 801,812 -573,356 228,456 71.5% 1,745,548 -1,088,036 657,512 62.3%

Unlikely to pay 1,054,153 -411,743 642,410 39.1% 2,162,940 -726,153 1,436,787 33.6%

Past due non-performing loans 114,393 -17,125 97,268 15.0% 112,347 -9,018 103,329 8.0%

Total non-performing loans 1,970,358 -1,002,224 968,134 50.9% 4,020,835 -1,823,207 2,197,628 45.3%

Performing loans - stage 1 18,641,418 -31,986 18,609,432 0.17% 14,545,619 -62,303 14,483,316 0.43%

Performing loans - stage 2 1,943,891 -86,789 1,857,102 4.46% - - -

Total loans and receivables with customers

22,555,667 -1,120,999 21,434,668 18,566,454 -1,885,510 16,680,944

The coverage ratio is calculated as the ratio between impairment losses and the gross amount.

Loans and receivables with customers classified under assets held for sale are not included.

Assets held for sale, equal to EUR 89 million, are mainly represented by non-performing exposures held for sale (known as “Project Gimli 2”).

The coverage ratio of performing loans and receivables with customers is 0.75% excluding government bonds.

Funding from customers

Direct funding amounted to EUR 20.4 billion, recording an increase of 4.0% compared to

31 December 2017 and 3.1% compared to 31 March 2018. Specifically, there was an

increase in the current accounts and deposit accounts component and an increase in

deposits with central counterparties (Cassa Compensazione e Garanzia); the decline in the

retail and institutional bond component continued in line with the policy of reducing the

most expensive forms of funding.

(in thousands of EUR) 30/06/2018 31/12/2017 Change

Current accounts and sight deposits 12,513,006 12,273,362 1.95%

Reverse repurchase agreements 4,457,886 3,129,229 42.46%

Term deposits 841,816 808,772 4.09%

Other 544,677 630,238 -13.58%

Due to customers 18,357,385 16,841,601 9.00%

Securities issued 2,056,741 2,789,682 -26.27%

Total direct funding from customers 20,414,126 19,631,283 3.99%

18

Indirect funding amounted to EUR 10.4 billion compared to EUR 11.3 billion at the end of

December 2017. The negative trend of the markets had an impact on the aggregate,

especially in the second quarter of the year, which affected both managed and administered

components.

(in thousands of EUR) 30/06/2018 31/12/2017 Change

Asset management 1,350,383 1,821,728 -25.87%

Mutual funds 3,250,892 3,229,276 0.67%

Insurance funds 2,729,997 2,750,588 -0.75%

Total Managed funds 7,331,272 7,801,592 -6.03%

Assets under administration 3,106,539 3,471,621 -10.52%

Total indirect funding 10,437,811 11,273,213 -7.41%

Financial assets and liabilities at fair value

Financial assets at fair value amounted to EUR 2.1 billion. Of these, EUR 1.9 billion were

represented by Italian government bonds, mainly recognised in the portfolio of Financial

assets at fair value through other comprehensive income. The valuation reserve on

securities recognised as financial assets at fair value through other comprehensive income,

recorded among equity items net of tax effects, was negative for EUR 35.9 million and

almost entirely related to government bonds.

(in thousands of EUR) 30/06/2018 31/12/2017 Change

Financial assets and liabilities at fair value through profit or loss

Debt instruments 13,162 15,716 -16.25%

Equity instruments and OEIC units. 229,529 4,447 n.s.

Derivative financial instruments with positive fair value 574 518 10.81%

Total assets 243,265 20,681 n.s.

Derivative financial instruments with negative fair value -198 -713 -72.23%

Total assets and liabilities 243,067 19,968 n.s.

Financial assets at fair value through other comprehensive income

Debt instruments 1,961,769 4,170,863 -52.96%

Equity instruments 64,796 248,489 -73.92%

Total 2,026,565 4,419,352 -54.14%

Hedging derivatives -135,599 -138,492 -2.09%

Financial assets and liabilities 2,134,033 4,300,828 -50.38%

The liquidity position

The counterbalancing capacity at 3 months on 8 August 2018 amounted to EUR 5.4 billion

(of which EUR 3.1 billion unencumbered), an increase compared to the figure at 31 March

2018 of EUR 4.3 billion, thanks to the securitisation of performing mortgage and unsecured

loans granted to small and medium-sized enterprises, which was completed on 30 July, for

a total amount of EUR 1.5 billion.

19

Equity investments

The total carrying amount of equity investments at 30 June 2018, accounted at equity, was

EUR 25 million.

The portfolio represents only equity investments in companies subject to joint control and

to significant influence - companies in which Credito Valtellinese has a direct or indirect

holding of at least 20% of voting rights, “potential” voting rights or, albeit with a lower

percentage, has the power to influence financial and management policy through specific

legal positions.

The main equity investments are summarised below.

% equity investment

30/06/2018 31/12/2017

Carrying amount (thousands of EUR)

Generalfinance S.p.A. 46.81% 16,005 15,906

Global Assistance S.p.A. 40.00% 5,073 4,734

Creset - Crediti, Servizi e Tecnologie S.p.A. 40.00% 2,561 2,508

Other 1,528 1,223

Total 25,167 24,371

20

Equity attributable to the owners of the parent

The equity attributable to the owners of the parent at 30 June 2018 amounted to EUR 1,493

million compared to EUR 1,442 million at 31 December 2017. The tangible equity

attributable to the owners of the parent at 30 June 2018 amounted to EUR 1,448 million

compared to EUR 1,398 million at 31 December 2017.

The statement of reconciliation between the Parent's equity and profit (loss) for the period

and the corresponding amounts resulting from the consolidated financial statements at the

same date, is illustrated below.

(in thousands of EUR)

30/06/2018 31/12/2017

Equity

of which: profit

(loss) for the period

Equity of which:

profit (loss) for the year

Balances as per parent financial statements 1,511,525 (9,957) 1,469,702 (325,468)

Investee results as per Separate financial statements:

- consolidated on a line-by-line basis 16,097 16,097 (706) (40,706)

- equity accounted 1,299 1,299 1,279 1,279

Amortisation of positive differences:

- past years (491) - (491) -

Differences compared to carrying amounts for:

- companies consolidated on a line-by-line basis (37,565) - (68,217) -

- equity investment impairment reversal - - 40,000 40,000

- equity-accounted companies 2,352 - 1,669 -

Adjustment to dividends collected during the period:

- on retained earnings - (6,961) - (7,263)

Other consolidation adjustments:

- elimination of intra-group profit and loss 344 751 (1,100) 2

- other adjustments (502) (405) (42) 307

Balances as per Consolidated financial statements 1,493,059 824 1,442,094 (331,849)

21

Own funds and capital ratios

In pursuance of the transitional regime (“phased in”), Common Equity Tier 1 (CET1) was

equal to EUR 1,939 million, against risk-weighted assets (RWAs), calculated with the

standard method, of EUR 13,892 million. Total own funds amounted to EUR 2,158 million.

The phased-in capital ratios amounted to:

- 14.0% for CET1 ratio

- 14.0% for Tier 1 ratio

- 15.5% for Total Capital ratio.

Those requirements were well above the SREP minimum levels envisaged for 2018:

- 7.075% for CET1 ratio,

- 8.813% for Tier 1 ratio,

- 11.125% for Total Capital ratio.

The fully loaded CET1 ratio coefficient at 30 June 2018 was 10.2%.

(in thousands of EUR) 30/06/2018 31/12/2017

Common Equity Tier 1 capital (CET1) 1,939,044 1,374,187

Tier 1 Capital 1,939,044 1,374,187

Total Own Funds 2,157,913 1,623,293

Credit risk and counterparty risk 989,681 927,007

Credit valuation adjustment risk 1,010 1,072

Settlement risks - -

Market risks 12,967 987

Operational risk 107,663 106,436

Other calculation elements - -

Total capital requirements 1,111,321 1,035,502

Risk-weighted assets 13,891,518 12,943,781

Common Equity Tier 1 capital / Risk-weighted assets (CET1 capital ratio) 13.96% 10.62%

Tier 1 capital / Risk-weighted assets (Tier 1 capital ratio) 13.96% 10.62%

Total own funds / Risk-weighted assets (Total capital ratio) 15.53% 12.54%

22

Income statement

The reclassified consolidated income statement is shown below.

(in thousands of EUR)

ITEMS 1st half of

2018 1st half of

2017 Change

Net interest income 178,879 198,772 -10.01%

Net fee and commission income 139,422 142,316 -2.03%

Dividends and similar income 1,867 2,876 -35.08%

Profit (loss) of equity-accounted investments (1) 1,299 158 n.s.

Net trading and hedging income (expense) and profit (loss) on sales/repurchases (2) 16,473 24,221 -31.99%

Other operating net income (3) 3,039 10,700 -71.60%

Operating income 340,979 379,043 -10.04%

Personnel expenses (193,432) (134,315) 44.01%

Other administrative expenses (4) (100,957) (107,711) -6.27%

Depreciations/amortisations and net impairment losses on property, equipment and investment property and intangible assets (5)

(12,567) (13,854) -9.29%

Operating costs (306,956) (255,880) 19.96%

Net operating profit 34,023 123,163 -72.38%

Net impairment losses for credit risk and gains/losses from amendments to contracts (6)

22,202 (328,562)

-106.76%

Losses on sale/repurchase of financial assets at amortised cost (7)

(95,220) (13,411)

n.s.

Net accruals to provisions for risks and charges (4,575) (40,493) -88.70%

Net gains/losses on sales of investments and property, equipment and investment property measured at fair value (8)

(19)

68,780 -100.03%

Badwill (9) 15,357 - n.s

Pre-tax loss from continuing operations (28,232) (190,523) -85.18%

Income taxes 30,777 (2,477) n.s.

Post-tax profit (loss) from continuing operations 2,545 (193,000) -101.32%

Profit for the period attributable to non-controlling interests (1,721) (1,828) -5.85%

Profit (loss) for the period 824 (194,828) -100.42%

(1) Profit of equity-accounted investments include profit (losses) of equity-accounted investments included in item 250 “Net gains (losses) on equity investments”; the residual amount of that item is included in gains on sales of investments, together with item 280 “Net gains (losses) on sales of investments" (2) Includes item “80. Profits (Losses) on trading”, “90. Net hedging income (expense)”, “100. Profits (losses) on sale or repurchase of: b) financial assets at fair value through other comprehensive income; c) financial liabilities” and “110. Profits (Losses) on other assets and liabilities at fair value through profit or loss: a) financial assets and liabilities at fair value; b) other financial assets mandatorily measured at fair value through profit or loss” (3) Other income and costs correspond to item “230. Other operating net income” net of the following reclassifications (4) Other administrative expenses include recoveries of taxes and other recoveries recognised in item "230. Other operating net income" (EUR 21,686 thousand in the first half of 2018 and EUR 25,718 thousand in the first half of 2017) (5) Depreciation/amortisation and net impairment losses on property, equipment and investment property and intangible assets include items "210. Depreciation and net impairment losses on property, equipment and investment property", "220. Amortisation and net impairment losses on intangible assets" and the accumulated depreciation of costs incurred for leasehold improvements included in item "230. Other operating net income" (EUR 500 thousand in the first half of 2018 and EUR 688 thousand in the first half of 2017) (6) Include items “130. Net impairment losses for credit risk relating to: a) financial assets at amortised cost; b) financial assets at fair value through other comprehensive income” and “140. Gains/losses from amendments to contracts without derecognition” (7) Includes item "100. Profit (Loss) on sale or repurchase of: a) financial assets at amortised cost" (8) Includes the residual amount of item "250. Net gains on sales of investments" not included among profit (losses) of equity-accounted investments together with item "280. Net gains (losses) on sales of investments" and item "260. Net result of property, equipment and investment property and intangible assets at fair value" (9) Includes the badwill recognised in item "230. Other operating net income"

23

In the first half of 2018, net interest income reached EUR 178.9 million, compared to EUR

198.8 million in the first half of 2017. The figures are not fully comparable as a result of the

application of IFRS 9 and the impact of the transfers of bad loans and unlikely to pay (UTP)

portfolio.

Net fee and commission income amounted to EUR 139.4 million, down year-on-year

(-2.0%) mainly due to the decrease in components relating to current accounts and

collection and payment services, partially offset by the increase in management, trading

and consulting fees (+3.7% year-on-year).

Net trading and hedging income (expense) and profit (loss) on sales/repurchases

stood at EUR 16.5 million.

Operating income reached EUR 341 million compared to EUR 379 million of the same

corresponding period.

Operating costs stood at EUR 307 million compared to EUR 256 million of 2017.

Personnel expenses amounted to EUR 193.4 and include EUR 63.5 million of extraordinary

expenses relating to early retirement plan set forth in the trade-union agreement signed on

16 April. The first half of 2017 benefited from a positive component of EUR 7.5 million

(“NASPI” - Nuova Assicurazione Sociale per l’Impiego contribution). Net of these

components, personnel expenses decreased by 9.5% year-on-year, incorporating savings

related to voluntary redundancies through the sector’s Solidarity Fund last year. Other

administrative expenses amounted to EUR 101 million and included extraordinary

expenses for a total of EUR 9.5 million recognised in the second quarter, of which EUR 3.4

million relating to the extraordinary contribution paid to the Single Resolution Fund and EUR

6.1 million relating to the securitisation of non-performing loans (ARAGORN Project). Net of

these extraordinary items, other administrative expenses fell by 11.0%.

The net operating profit reached EUR 34 million.

The item net impairment losses for credit risk (determined on the basis of IFRS 9 and

positive for EUR 22.2 million, including reversals of impairment losses relating to non-

performing loans not subject to transfer) together with Profit (loss) on sale/repurchase

of financial assets at amortised cost (negative for EUR 95.2 million and referring to the

sale of non-performing loans during the half-year) resulted in a negative value of EUR 73

million, of which EUR 57 million refer to adjustments to ordinary loans that express an

annualised cost of credit of 69bps (excluding government bonds from loans and receivables

with customers).

Badwill of EUR 15.4 million refers to the result of the purchase price allocation relating to

the acquisition of Claris Factor completed on 29 June.

Taking into account net accruals to provisions for risks and charges of EUR 4.6 million, the

pre-tax loss from continuing operations is negative for EUR 28.2 million.

Income taxes were positive for EUR 30.8 million and include EUR 12.6 million relating to the

recognition of previously unrecognised DTAs, against the probability test carried out on the

approval of the results at 30 June 2018. After deducting the profit attributable to non-

controlling interests, net profit for the period was EUR 0.8 million. ROA stood at 0.01%.

24

Related party transactions, risks and going concern prospects

Related party and intra-group transactions

The matter is mainly regulated:

- by Article 2391-bis of the Italian Civil Code, whereby the governing bodies of companies

resorting to the equity market adopt, according to general principles indicated by

Consob, rules that assure “the transparency and substantial and procedural correctness

of related party transactions” carried out directly or through subsidiaries;

- by the “Related Party Transaction Regulation” adopted by Consob with resolution no.

17221 of 12 March 2010, as amended, (hereinafter also the “Consob Regulation”),

implementing the delegation contained in Article 2391-bis of the Italian Civil Code, as

well as, in relation to the specific business;

- by the provisions of Article 136 of the Consolidated Banking Act - as amended by Italian

Legislative Decree no. 72 of 12 May 2015 - on obligations of banking representatives;

- by the supervisory provisions issued by the Bank of Italy on December 2011 on risk

assets and conflicts of interest of banks and banking groups with respect to “Associated

Parties” (9th update to Circular 263 of 27 December 2006 - hereinafter also referred to

as the “Bank of Italy Regulation”), provisions that complement what is provided by the

Consob regulation.

In compliance with the combined provision of the above-mentioned regulations, the Board

of Directors approved the “Procedures concerning Related Party Transactions and Associated

parties” (hereinafter also the “RPT Creval Procedures”), in the last updated version, effective

as from 27 November 2017. The RPT Creval Procedures establish the procedures and rules

for ensuring transparency and substantive and procedural correctness in related party

transactions carried out directly by Credito Valtellinese or by means of its subsidiaries. They

also comply with the applicable regulations of the Bank of Italy on risk assets and conflicts

of interest towards associated parties.

In accordance with current regulations, the document is published on the website,

http://www.gruppocreval.com – Corporate Governance section – Corporate documents.

Still on the basis of the provisions of the Bank of Italy Regulation, the Board of Directors of

the Parent approved the “Policy regarding controls on risk activities and on conflicts of

interest towards associated parties” (hereinafter also the “Policy”), document that defines

the internal policies regarding controls on risk activities and on conflicts of interest towards

associated parties, and was made known to the Ordinary Shareholders' Meeting held on 27

April 2013, subsequently amended with Board resolution of 9 December 2015.

The Policy describes, in relation to the operational features and the strategies of the Bank

and of the Group, the business segments and the types of business relations, also other

than those implying the assumption of risk assets, in relation to which conflicts of interest

may arise, as well as the safeguards inserted in the organisational structures and in the

internal control system to ensure constant compliance with prudential limits and the above

decision-making procedures. The document also summarises the principles and rules

applicable to transactions with associated parties that were used for the preparation of the

relevant Procedures.

With reference to intra-group transactions, relations with companies in the Credito

Valtellinese Banking Group were established within an organisational model - as widely

illustrated in this report – based on which each legal entity focuses only on its own core

25

business, in an industrial framework that offers effective and efficient management of

overall Group resources.

This approach aims to achieve any form of synergy among the companies of the Group,

assures to all members the access to specialised high-quality services and makes it possible

to achieve significant economies of scale to reduce operating costs relating to activities and

common services.

The common focus of activities and specialist services is regulated on the basis of

appropriate intra-group contractual agreements, which concern in particular the provision

of services by the parent to the subsidiary companies in the sector of finance, insurance,

legal and corporate affairs, administrative, accounting and management, internal auditing,

risk management and compliance, management and administration of the Personnel. The

contracts between specialised and complementary companies and the other companies of

the Group concern the management of the information system, the organisational and back

office services, the payment systems in Italy and abroad, the management of real estate

assets, the design and construction of real estate works, and the technical support to the

disbursement of credit and leasing.

The financial effects are regulated on the basis of specific contractual agreements that, with

the main objective of optimising synergies and economies of scale and purpose at the Group

level, refer to long-term objective and constant parameters, distinguished by material

transparency and fairness. The quantification of the expected fees for services was defined

and formalised according to tested parameters that take into account actual utilisation by

each user company.

The Board of Directors is exclusively responsible for the definition of intra-group contractual

agreements and approval and possible amendment of the related economic conditions.

No atypical or unusual transactions, with Group companies or related parties - as defined

by Article 2427, second paragraph, of the Italian Civil Code, or according to the IFRS

endorsed by the European Union - that impacted significantly on the financial position or

results of operations of the company has taken place during the financial year.

Detailed information on intra-group and related party transactions, including information on

the effects of transactions or existing positions with such counterparties on the statement

of financial position and on the income statement, accompanied by summary tables of such

effects, are contained in the Notes to the condensed interim consolidated financial

statements.

26

Risk management

In accordance with the Supervisory provisions, the Credito Valtellinese Group adopted a

detailed and strong internal control system (consisting of rules, functions, structures,

resources, processes and procedures) the aims of which are reducing the risk within the

limits indicated in the framework of reference for determining the risk appetite (RAF),

prevention of the risk that the Banks of the Group are involved, even unintentionally, in

illegal activities (such as money laundering, usury and terrorist financing) and compliance

of the transactions with the law and supervisory regulations, as well as with policies,

regulations and internal procedures.

The internal control and risk management system, regulated by the prudential supervisory

regulations and by the company policy defined in the “Control coordination document”, is

broken down in the company's control functions set up with the Parent and based in the

following functions:

- compliance and anti-money laundering;

- risk control and validation;

- internal revision.

In order to maintain adequacy over time, the risk control units as a whole are assessed and

checked in terms of completeness, adequacy, functionality and reliability by the indicated

functions. The appropriate development and corrective actions of any deficiency are

identified and planned at the management level, discussed and screened in the Risk

Committee and submitted to Corporate Bodies responsible for strategy, management and

control. Overall, the coordinated action of governance, organisation, risk management and

internal control system make it possible to obtain a full picture and an adequate

management of the assumed risk and the awareness, looking ahead, of the expected risk.

As part of the internal control system, the Group developed and standardised specific

controls, including in particular:

- the “RAF”, which consists of “the reference framework that establishes - consistent with

the maximum risk that can be undertaken, the business model and the strategic plan -

the risk appetite, the tolerance thresholds, the risk limits, the risk governance policies,

the reference processes needed to define and implement them”. At the same time, it is

a management tool that supports the achievement of the set objectives and is integrated

with strategic and operational planning, and a tool for control that identifies any overruns

of the set limits;

- the risk management process, defined in compliance with RAF and intended as “all the

rules, procedures, resources (human, technological and organisational) and control

activities for identifying, measuring or assessing, monitoring, preventing or mitigating

as well as notifying the suitable superiors of all risks assumed or which may be assumed

in the various segments, at company and group portfolio level, applying integrated logic,

also mutual inter-relations and the development of the external scenario”. The

operational limits to the assumption of various types of risk and the related reporting

processes are consistent with the risk appetite defined within the Risk Appetite

Statement and with the development of the economic scenario;

- the Internal Capital Adequacy Assessment Process (ICAAP) and Internal Liquidity

Adequacy Assessment Process (ILAAP), the results of which are summarised in this

Report that represents, on the one hand, the point of convergence and synthesis of the

equity, economic and financial plans of the risk management, capital management and

liquidity management and that, on the other hand, is an essential instrument supporting

strategic planning and the implementation of the corporate decisions;

27

- the Contingency Funding and Recovery Plan (CFRP), which describes the procedures to

be followed and the actions to be taken in the event of situations of severe stress or

significant deterioration of the liquidity profile, or the possibility of such situations

occurring. This framework envisages the activation of an intervention plan, according to

two critical levels, following an evaluation and escalation process starting from a set of

systemic and intolerant indicators; funding sources are also identified and the

management levers that the Bodies designated to govern the crisis can activate in order

to restore a normal liquidity position. The aim of CFRP is to manage a short-term liquidity

crisis limited to this profile. The Restructuring plan, on the other hand, supervises

situations of significant deterioration in the economic sustainability and financial

situation of the Group.

Detailed information on the general characteristics of the control systems, the risk

management, measurement and control policies are contained in the Notes to the 2017

Consolidated Financial Statements (Part E – Information on risks and hedging policies) and

in the informative report on the third pillar at 31 December 2017 made available on the

Group's website at www.gruppocreval.com.

Information on main risks and uncertainties to which the Group is exposed

Strategic decisions regarding risk management at Group level are taken by the Parent's

corporate bodies, taking account of the specific operations and related risk profiles of each

Bank/Company of the Group, in order to implement an integrated and consistent risk

management policy. In this context, the Parent defines and approves the Group Risk

Appetite Framework (RAF) and Risk Appetite Statement (RAS), in application of Bank of

Italy Circular no. 285/2013, Part I, Title IV, Chapter 3.

At 30 June 2018, the Group's exposure to risks was consistent with the risk appetite.

For detailed information on the Group's exposure to risks, please refer to the section

Information on risks and related hedging policies.

28

Information on disputes

For detailed information on disputes, tax or otherwise, and on the main pending legal

actions, please refer to the Notes to the condensed interim consolidated financial

statements.

Information on business outlook, with a special reference to going concern

assumptions

With regard to the going concern assumption, the Board of Directors confirms its reasonable

expectations that the company and the Group will remain a going concern in the foreseeable

future and, consequently, confirms that the condensed interim consolidated report was

prepared on a going concern basis.

As regards the requirements relating to impairment testing and uncertainties in the use of

estimates, please refer to the information provided in the special sections in the Notes to

the condensed interim consolidated financial statements.

29

Events after the close of the half-year

Reorganisation of Bancassurance activities

In line with the objectives set out in the 2018-2020 Strategic Plan, the bank redefined its

operating model for the bancassurance business, signing long-term strategic partnerships

with Crédit Agricole Assurances SA (“CAA”) in the Life segment and with the Insurance

Group Ri-Fin S.r.l. (“Rifin”) in the Non-Life segment.

In this regard, note that the following were signed on 24 July 2018:

- the Framework Agreement between Creval and Rifin aimed at restructuring the existing

agreements, reorganising the co-equity investments held by Creval and Rifin in the

companies Global Assicurazioni, Global Assistance S.p.A. (“Global Assistance”) and Global

Broker S.p.A. (“Global Broker”), as well defining two new distribution agreements with the

aforesaid insurance companies of the Rifin Group, relating to the Non-Life bancassurance

business, and to the insurance brokerage activity on Creval customers (the “CV/Rifin

Agreement”), both exclusively and for a duration of 15 years.

Upon completion of the CV/Refin Agreement, against a total disbursement of EUR 34 million

to Rifin, in relation to the purchase and sale of the equity investments, Creval will hold: i)

100% of the share capital of Global Assicurazioni and ii) 30% of the share capital of Global

Broker. The Rifin Insurance Group will hold: i) 100% of the insurance company Global

Assistance, specialised in non-life bancassurance products in particular, ii) 100% of the

multifirm agency (Nuova) Global Assicurazioni S.p.A., which was set up following the

demerger of the business unit of Global Assicurazioni and specialised in non-life

bancassurance processes and products, and iii) 70% of Global Broker, an insurance

brokerage company with a special focus on SME, private and public customers.

The closing of the transaction is expected by the end of 2018 and is subject to the

authorisations of the competent Supervisory Authorities (IVASS and Antitrust Authority).

- the Framework Agreement between CreVal and Crédit Agricole Assurances SA (“CAA”) for

the launch of an exclusive long-term partnership in the life insurance business (“CV/CAA

Agreement”). The partnership will provide CAA, through its Italian subsidiary Crédit Agricole

Vita S.p.A. (“CA Vita”), with access to CreVal's network for the distribution of all savings

and investment insurance products as well as certain protection segment products for a

duration of up to 15 years. As part of the transaction, CAA will purchase 100% of the share

capital of Global Assicurazioni S.p.A. (“GA”), a company that, following the restructuring by

the current shareholders (Creval and Rifin) as detailed above, at the closing date will be

wholly owned by CreVal and will exclusively include the business related to the life insurance

policies distributed on the CreVal network.

The total consideration paid by CAA for the acquisition of GA will be EUR 80 million, of which

EUR 70 million paid by CAA at the closing and EUR 10 million deferred, payable at the end

of the fifth year subject to the achievement of previously agreed objectives.

In order to strengthen the long-term strategic partnership, the agreement provides for CAA

to purchase a non-controlling interest in CreVal of 5%. Moreover, the parties agreed that

they will consider, in the medium term, the possibility of extending the partnership between

the CASA Group and CreVal to other business areas. In this situation, the CASA Group could

consider increasing its share in CreVal to 9.9%.

As a result of the CV/CAA Agreement and the CV/Rifin Agreement, the performance of which

remains subject to completion, among other things, of the authorisations of the competent

30

Supervisory Authorities, Global Assicurazioni and Global Broker will leave the Creval Group's

scope of consolidation.

For the sake of full disclosure, on 27 July 2018 CAA announced that it had completed the

acquisition of the 5% equity investment in Creval.

Merger by incorporation of the subsidiary Creval Sistemi e Servizi into Credito

Valtellinese

On 26 July 2018, the Board of Directors of Creval and of the subsidiary Creval Sistemi e

Servizi (“CSS”) resolved to carry out the merger by incorporation of CSS into Credito

Valtellinese S.p.A.

The Merger is part of the 2018-2020 Strategic Plan, as part of the objectives for simplifying

the corporate structure and optimising the cost structure. The Transaction follows on from

the merger of Credito Siciliano into the Parent, which was finally completed (effective as

from 25 June 2018), as well as from the previous mergers of the other territorial banks of

the Group, in line with the creation of the so-called “single bank”. Following the mergers

mentioned above, the consortium company CSS now provides almost all of its services to

the Parent and is 99.08% owned directly and indirectly by it. Therefore, in this context, the

Merger will allow benefits to be achieved in terms of cost synergies and organisational

streamlining, as well as greater coordination between IT and business areas.

The merger is to be implemented through the simplified system set forth in Article 2505 of

the Italian Civil Code on the assumption that, at the date of effectiveness of the Merger, all

CSS shares, i.e. 100% of the share capital of CSS, are owned by Creval. The transfer of

CSS shares to Credito Valtellinese will take place on the basis of the pro-rata book equity

of CSS, in accordance with its articles of association.

Once the Authorisation has been obtained and the statutory procedure has been completed,

the merger is expected to become effective by the end of the current financial year.

Industrial partnership as part of the activities relating to loans against pledges in

Italy

On 9 August 2018, Credito Valtellinese S.p.A., Dorotheum Beteiligungs GmbH

(“Dorotheum”) and the company indirectly controlled by the latter Custodia Valore - Credito

su Pegno S.p.A. (“Custodia Valore”) announced that they have signed an agreement for the

creation of an industrial partnership as part of the activities relating to loans against pledges

in Italy.

The partnership will be implemented by means of Custodia Valore, company created through

the acquisition by Dorotheum of the business dedicated to loans against pledges of the

UniCredit Group.

In particular, the Transaction envisages (i) a capital increase of Custodia Valore, with the

exclusion of the right of option reserved to Creval, to be released through the contribution

of the Creval business unit dedicated to loans against pledges, in exchange for a non-

controlling interest equal to 22% of the share capital of Custodia Valore and (ii) the provision

by Creval of information technology and support services to Custodia Valore.

Therefore, at the end of the Transaction, the share capital of Custodia Valore will be held by

the Dorotheum Group (78%) and Creval (22%).

31

Creval undertook to grant credit facilities to Custodia Valore to support ordinary activities,

its business growth as well as to support the acquisition, by Custodia Valore, of some

instrumental properties included in the scope. For Creval, the Transaction will allow it to

enter into a partnership with one of the main European leaders in the market of loans against

pledges and is part of the initiatives envisaged by the 2018-2020 Strategic Plan for the

valuation of non-core assets aimed at increasing the bank's comprehensive income and

further strengthening the capital ratios. In fact, the partnership will allow to make a net

capital gain estimated to date in EUR 44.5 million with a positive impact on the Group CET1

capital ratio estimated in about 5 basis points.

Industrial partnership in the salary-backed loan market

On 9 August 2018, Creval, Cassa di Risparmio di Asti S.p.A. (“CR Asti”) and Bonino 1934

s.r.l. (“Bonino”) signed a Term sheet concerning the essential terms and conditions that will

regulate: (i) the purchase by Creval of a 9.9% equity investment in the share capital of

Pitagora S.p.A. (“Pitagora”); by signing at the same time the shareholders' agreements that

will envisage, among other things, the representation of Creval in the Board of Directors of

Pitagora, as well as (ii) the revision and renewal for five years of the existing sales

agreement by and between Pitagora and Creval for the promotion of salary-backed loan

agreements (“CQS”), with important objectives of disbursement on the Creval network.

The purchase of the Equity investment and the signing of the Sales Agreement represent,

as a whole, an important opportunity for Creval to increase its exposure to the CQS market,

a growing market that could also benefit, in the future, from a significant revision - in a

favourable sense - of the levels of capital absorption. The increase in Creval's exposure will

take place through: (i) the acquisition of an equity investment in the share capital of a

leading operator in the sector, with the consequent expected return also in the light of the

business plan of Pitagora. (ii) the expected increase of the disbursed CQS through the Creval

branches, thanks also to the commercial support provided by Pitagora, and (iii) the granting

of funding lines that may be granted to Pitagora, contributing to the recovery of net interest

income at the end of the de-risking process carried out by Creval.

Therefore, for Creval, the Transaction is part of the progressive strengthening and expansion

of the offer dedicated to retail customers and - in line with the provisions of the 2018-2020

Strategic Plan - may lead to an increase in comprehensive income to be achieved in

particular through the development of Creval's penetration in the consumer credit market

and the consequent increase in the capacity to generate fees and commissions.

Subject to the completion of the usual due diligence activities and the definition of final

agreements in the light of what has already been agreed in the Term Sheet, the closing of

the Transaction is expected by November 2018.

The acquisition of the Equity investment will have negligible effects (approximately 1bp) on

the level of Creval's fully loaded CET1 ratio at 31 March 2018.

Current-year outlook

Globally, there are still favourable prospects for the continuation of the current expansionary

phase despite the slowdown in the first quarter of this year. The Eurozone economy is

expected to continue to grow, although downside risks remain, notably from global

protectionist measures that could affect the growth in exports. The outlook for the Italian