CONCEPT PAPER FOR AN INTEGRATED CAPITAL MARKETS ARCHITECTURE IN AZERBAIJAN

51

1 CONCEPT PAPER FOR AN INTEGRATED CAPITAL MARKETS ARCHITECTURE IN AZERBAIJAN Dr. Fred Reinertz EU Short term expert capital markets architecture Baku, February 2010

-

Upload

ala-agrici -

Category

Documents

-

view

218 -

download

0

Transcript of CONCEPT PAPER FOR AN INTEGRATED CAPITAL MARKETS ARCHITECTURE IN AZERBAIJAN

8/7/2019 CONCEPT PAPER FOR AN INTEGRATED CAPITAL MARKETS ARCHITECTURE IN AZERBAIJAN

http://slidepdf.com/reader/full/concept-paper-for-an-integrated-capital-markets-architecture-in-azerbaijan 1/59

1

CONCEPT PAPER FOR AN INTEGRATED CAPITAL MARKETS ARCHITECTURE IN

AZERBAIJAN

Dr. Fred Reinertz

EU Short term expert capital markets architecture

Baku, February 2010

8/7/2019 CONCEPT PAPER FOR AN INTEGRATED CAPITAL MARKETS ARCHITECTURE IN AZERBAIJAN

http://slidepdf.com/reader/full/concept-paper-for-an-integrated-capital-markets-architecture-in-azerbaijan 2/59

2

Table of Contents

1. Introduction .......................................................................................6 2. Definitions ......................................................................................... 7

3. Information flows and information systems for securities trading .......18

4. Securities trading information flow ...................................................18

4.1. Pre-trade ........................................................................................................18

4.2. Trading ...........................................................................................................18

4.3. Post-trade .......................................................................................................18

4.4. Clearing-Settlement-Custody ........................................................................19

5. Categories of capital markets information systems ............................19

5.1. Information collection and distribution ..........................................................19

5.2. Trading tools ..................................................................................................20

5.3. Order-routing systems ...................................................................................20

5.4. Order-presentation systems ..........................................................................23

5.5. Settlement and custody systems ..................................................................23

5.6. Surveillance systems ......................................................................................25

6. The prevailing legal and regulatory framework in the EU ....................25

6.1. The main EU Directives on capital markets ....................................................25

6.2. The institutional links among capital markets operators ................................25

6.3. The role of professional capital markets participants .....................................26

8/7/2019 CONCEPT PAPER FOR AN INTEGRATED CAPITAL MARKETS ARCHITECTURE IN AZERBAIJAN

http://slidepdf.com/reader/full/concept-paper-for-an-integrated-capital-markets-architecture-in-azerbaijan 3/59

3

8.1. The Turkish model ..........................................................................................33

8.2. The Russian model .........................................................................................34

8.3. Benchmarking vis a vis the EU capital markets architectures ........................35

9. The proposed architecture for Azerbaijan ..........................................37

9.1. Action plan and time frame for implementation .............................................37

9.1.1 Global Strategy .........................................................................................37

9.1.2 Main general task ......................................................................................37

9.1.3 Main actions and priorities ........................................................................38

9.1.4 Ancillary tasks ...........................................................................................40

9.2. The capital markets operators’ positions ........................................................41

9.2.1. The Baku Stock Exchange .......................................................................41

9.2.2. The National Depository Centre ...............................................................43

9.3. The Capital Markets Regulator .......................................................................45

9.4. The professional capital markets participants ................................................45

9.4.1. The Investment firms ...............................................................................46

9.4.2. The Banks licensed to provide investment services .................................46

9.4.3. The Custodian Banks ................................................................................46

9.4.4. The professional capital markets associations .........................................47

9.5. Linkages among them ....................................................................................47

9.6. The necessary reforms from the legal and regulatory point of view ..............47

9 6 1 the operational aspects of the capital market in Azerbaijan 47

8/7/2019 CONCEPT PAPER FOR AN INTEGRATED CAPITAL MARKETS ARCHITECTURE IN AZERBAIJAN

http://slidepdf.com/reader/full/concept-paper-for-an-integrated-capital-markets-architecture-in-azerbaijan 4/59

4

0. Executive summary

The concept proposal for an architecture of a capital markets structure in Azerbaijan is placed

in the more general frame of the overall objective of the project , that aims at improving the

economic development of Azerbaijan and to reduce the dependence on the oil sector, (cit. the

TOR’s, the terms of reference of the project).

In this context, the mission of the consultant when defining the sketch of an integrated new

capital market design and structure did focus also on analysing and formulatinrecommendations to improve the existing domestic Azeri capital market with an end-state

analysis.

This concept paper should also serve the purposes of a later subsequent technology evaluation

and the development of a standard electronic IT platform for the implementation of the structural

proposals as issued.

The capital market architecture presented in this paper is feasible with the current technology, Itis based on the end-to-end functionalities of the in the actual present capital markets

embryonic elements, It takes into account all internal requirements of the market participants.

Various architectural and ethical issues are broached as well and discussed, sketching a

framework for further project work in the matter under review.

The structure itself as proposed is compliant with the actual prevailing EU regulations in matters

of capital markets organizational set-up and the due Regulatory supervision. The consultant didseek “EU acquis communautaire” adhesion of the present proposal as the necessary foundation

of the architecture. In compliance with the requirements as outlined in the TORs, the projects’

terms of reference the paper will encompass:

8/7/2019 CONCEPT PAPER FOR AN INTEGRATED CAPITAL MARKETS ARCHITECTURE IN AZERBAIJAN

http://slidepdf.com/reader/full/concept-paper-for-an-integrated-capital-markets-architecture-in-azerbaijan 5/59

5

benchmarking against best practices adopted in developed and other emerging markets, a

significant GAP analysis and elaboration of conceptual recommendations for an optimum

infrastructure.

8/7/2019 CONCEPT PAPER FOR AN INTEGRATED CAPITAL MARKETS ARCHITECTURE IN AZERBAIJAN

http://slidepdf.com/reader/full/concept-paper-for-an-integrated-capital-markets-architecture-in-azerbaijan 6/59

6

1. Introduction

The elaboration of a proposal for a capital market structure requires, in the process, the

examination and evaluation of the basic components such a common structure, this in view to

determine the usefulness of the proposed structure for the beneficiaries and the different stake-

holders of the project. Although the final beneficiaries of the proposed capital market

architecture are the market participants, the project as such was designed for duly perusal by

the Regulator, the State Committee for Securities, SCS; the National Depository Centre, NDC

and the Baku Stock Exchange BSE as the first involved parties.

The functionalities to structure, in a capital markets architecture proposal that wants to take into

account the best practice as prevailing in the EU capital markets, are well known. It must be

outlined that there is no uniform structure or type of capital markets set-up in the European

Unions’ capital markets, the Member State’s diversity is nevertheless always taking into account

the in the “EC acquis communautaire” given rules and requirements.

In Annex 1 the consultant has attached a schematic presentation of the status quo of the

structures as prevailing in the different European capital markets. It was elaborated by a project

team member and is known to the project beneficiaries. It would exceed the scope of this paper

to pass in review in full details the different architectures, as only a comparative study with pros

and cons would be a meaningful tool to opine on that issue.

It could be recommended to be undertaken only if the actual project would require a more

enhanced approach; it would require an allocation of project man days to be performed. The

consultant intends to recommend a more specific and tailor made capital market architecture for

8/7/2019 CONCEPT PAPER FOR AN INTEGRATED CAPITAL MARKETS ARCHITECTURE IN AZERBAIJAN

http://slidepdf.com/reader/full/concept-paper-for-an-integrated-capital-markets-architecture-in-azerbaijan 7/59

7

whereabouts and set up’s functionalities in more details. They often use a so called “dark pools”

approach in matters of securities trade processing. A Multilateral Trading Facility (or MTF) is a

multilateral system, operated by an investment firm or a market operator, which brings together multiple third-party buying and selling interests in financial instruments - in the system and in

accordance with non-discretionary rules - in a way that results in a contract in accordance with

the provisions of Title II in MiFID.

The appearance of MTF’s is one of several actions that aim to improve the access of small and

medium sized enterprises to capital through new share, bond and rights issues.

In the EU, there are several MTFs operational now:

POSIT, a pure dark-pool MTF operated by ITG, launched in 1998, Chi-X, launched in March

2007, Turquoise, launched in August 2008, Equiduct-Berliner Börse, NASDAQ OMX Europe,

launched in September 2008, BATS Europe , launched in October 2008, NYSE Arca Europe,

launched in March 2009, QUOTE MTF - launched 4th September 2009, NX MTF - launched in

11th December 2009 by Nomura Securities Ltd.

2. Definitions

This is a list of the most common used terms in the context of capital markets: courtesy from

Euroclear and the consultant’s definition data base, the list is long but the subject is complex,

and the info may be useful in the context.

A

Account operator

8/7/2019 CONCEPT PAPER FOR AN INTEGRATED CAPITAL MARKETS ARCHITECTURE IN AZERBAIJAN

http://slidepdf.com/reader/full/concept-paper-for-an-integrated-capital-markets-architecture-in-azerbaijan 8/59

8

on behalf of the relevant Central Bank in connection with the use of the CSD System or a

system operated by another Euroclear CSD; Cash Accounts may also be referred to in the

Euroclear Contractual Documentation as 'cash positions in Central Bank Money (CeBM).

Cash Correspondent

A financial institution that executes cash transfers on behalf of its clients.

Cash position in Central Bank Money

Balance in a central bank money account on a settlement platform operating the integrated

settlement model. Also referred to, in the context, as the Liquidity position.

CBA

Central Bank of Azerbaijan

Central bank money (CeBM)

Settlement is described as being in central-bank money if payment moves directly and

irrevocably between accounts on the books of the central bank.

CCP stands for Central counterparty

An entity that is the buyer to every seller and the seller to every buyer of a specified set of

contracts/obligation (e.g. those executed on a particular exchange). CCPs typically interpose

themselves between the counterparties to trades, acting as the buyer to every seller and the

seller to every buyer (“novation”). In order to be able to settle the novated transactions, Central

CCPS must also have direct or indirect access to the SSS, Securities Settlement Systems

8/7/2019 CONCEPT PAPER FOR AN INTEGRATED CAPITAL MARKETS ARCHITECTURE IN AZERBAIJAN

http://slidepdf.com/reader/full/concept-paper-for-an-integrated-capital-markets-architecture-in-azerbaijan 9/59

9

Payment between a Euroclear group customer using central bank money and another Euroclear

group customer using commercial bank money.

CSD

Central Securities Depositary

D

Dark pool

Dark pools of liquidity (also dark pools or dark liquidity) are crossing networks that provideliquidity that is not displayed on order books in an MTF context. This is useful for traders who

wish to move large numbers of shares without revealing themselves to the open market. Dark

liquidity pools offer institutional investors many of the efficiencies associated with trading on the

exchanges' public limit order books but without showing their actions to others. Dark liquidity

pools avoid this risk because neither the price nor the identity of the trading company is

displayed. Dark pools are recorded as over-the-counter transactions. Therefore detailed

information about the volumes and types of transactions is left to the crossing network to report

to clients if they desire and are contractually obligated.

Dark Pools in funds to line up and move large blocks of equities without tipping their hands as to

what they are up to. Modern trading platforms and the lack of human interaction has reduced

the time scale on market movements. This increased responsiveness of the price of equity to

market pressures has made it more difficult to move large blocks of stock without affecting the

price.[

Debit party

The party that gives cash or securities. In the payment chain, it may be an agent or the debtor.

F h f h i f i i i h h i l l

8/7/2019 CONCEPT PAPER FOR AN INTEGRATED CAPITAL MARKETS ARCHITECTURE IN AZERBAIJAN

http://slidepdf.com/reader/full/concept-paper-for-an-integrated-capital-markets-architecture-in-azerbaijan 10/59

10

from the seller to the buyer (delivery) occurring at the same time as final transfer of the funds

from the buyer to the seller (payment).

E

ECSDA

European Central Securities Depositories Association

End-of-month settlement (SRD)

End-of-month settlement is the opposite from rolling settlement whereby the settlement date of a party's securities transaction instruction is deferred until the end of the month. Hence, it is

possible to buy stocks without immediately settling and benefit from an anticipated rise of the

stock or to short sell the stock not yet purchased.

Escrow balance

See 'restricted balance'

ESES

Euroclear Settlement of Euronext-zone Securities

eXtensible Markup Language (XML)

Simple and very flexible text format derived from Standard Generalized Markup Language

(SGML) (ISO 8879). The eXtensible Markup Language (XML) is a W3C-recommended general

purpose mark-up language for creating special-purpose mark-up languages. Its primary purpose

is to facilitate the sharing of data across different systems, particularly systems connected via

the internet.

8/7/2019 CONCEPT PAPER FOR AN INTEGRATED CAPITAL MARKETS ARCHITECTURE IN AZERBAIJAN

http://slidepdf.com/reader/full/concept-paper-for-an-integrated-capital-markets-architecture-in-azerbaijan 11/59

11

First agent

A financial institution of the debtor that receives the payment transaction from either the accountowner or authorized party, and processes the instruction.

I

ICSD

International central securities depository

Identifiable bearer security (TPI)

Based on the French legal framework, it is a service in Euroclear France that allows an issuer of

bearer securities to request and obtain a list of, all or part of, securities' holders registered on

the custodians’ books. Certain holders declared by the custodians may have the status of

registered intermediary. (French acronym)

Infrastructure

The party that provides, through common membership, services to create a fair and open

process for the execution of transactions between trading parties, and the creation of settlement

obligations.

Instrument category

The second qualifier in the CFI - ISO 10962 classification of a security.

Instrument family

The first qualifier in the CFI - ISO 10962 classification of a security. Synonym: security family.

8/7/2019 CONCEPT PAPER FOR AN INTEGRATED CAPITAL MARKETS ARCHITECTURE IN AZERBAIJAN

http://slidepdf.com/reader/full/concept-paper-for-an-integrated-capital-markets-architecture-in-azerbaijan 12/59

12

a catalogue for present and future messages built by the industry with the above mentioned

fields and rules.

ISO 20022 Financial Services

It is a Universal Financial Industry message scheme (UNIFI) - newly published standard which

provides the usage of a common platform for the development of messages.

Issuance Account

In the ESES context, any account opened in the name of an issuer in the books of the CSD on

the debit of which all securities of a same issue which are admitted by the CSD are recorded; in

the case of dematerialized securities, all securities of the relevant issue will be recorded on the

debit of the Issuance Account; Issuance Accounts are not considered as Securities Accounts for

the purposes of the Terms and Conditions.

L

Legacy platform

One of the current input, matching, settlement and/or reporting systems in the Euroclear group’s

(I)CSDs.

Liquidity sweep

Any automated transfer of cash from a Cash Account to the corresponding RTGS Cash Account

M

Matching

It is the process for comparing the trade or settlement details provided by counterparties to

8/7/2019 CONCEPT PAPER FOR AN INTEGRATED CAPITAL MARKETS ARCHITECTURE IN AZERBAIJAN

http://slidepdf.com/reader/full/concept-paper-for-an-integrated-capital-markets-architecture-in-azerbaijan 13/59

13

Stands for an agreed offsetting of positions or obligations between counterparties. The netting

reduces a large number of individual positions or obligations to a smaller number of obligations

or positions. Netting may take several forms.

Nominee

A person or entity named by another to act on his behalf. A nominee is commonly used in a

securities transaction to obtain registration and legal ownership of a security. See 'Trustee'.

O

Omnibus account

A single Securities Account within which the Securities Account Holder co-mingles the assets of

two or more underlying clients, rather than in separate accounts with designation.

P

Payment settlement agent

An agent that executes the cash transfer upon the request of either an agreement party, or a

clearing agent.

Post-trade administrator

The party ensuring that all the details of the trade have been collected and reported, as required

to all parties involved in the trade transaction including counterparties, the investor, and

settlement parties.

Purchasing power

A settlement bank's cash position in central bank money and its collateral value of securities

8/7/2019 CONCEPT PAPER FOR AN INTEGRATED CAPITAL MARKETS ARCHITECTURE IN AZERBAIJAN

http://slidepdf.com/reader/full/concept-paper-for-an-integrated-capital-markets-architecture-in-azerbaijan 14/59

14

investor and/or to its intermediary, can be the corporate secretary for the proxy voting, reports to

the regulator on shareholder identity, and can appoint the sub-registrar.

RNC

Continuous Net Settlement

Rolling settlement

A practice in which settlement takes place a standard number of business days after the date of

the trade.

RTGS

Real-time gross settlement system

S

Securities loan / Securities lending / Securities borrowing

Securities finance mechanism that involves transferring full ownership of securities, with or

without a guarantee, with a contractual agreement that the seller will repurchase the securities

in return for the guarantee, if there is a guarantee, at an agreed price and date. The lending of

securities in an exchange for a fee. Securities lending is mostly facilitated by CSDs, but not

offered directly. (I)CSDs and banks, such as custodians that directly offer securities lending,

possess a banking license and are regulated by existing banking law.

Securities Settlement System (SSS)

A system which permits the holding and transfer of securities, either free of payment (FOP) or

against payment (Delivery Versus Payment-[DVP]).

8/7/2019 CONCEPT PAPER FOR AN INTEGRATED CAPITAL MARKETS ARCHITECTURE IN AZERBAIJAN

http://slidepdf.com/reader/full/concept-paper-for-an-integrated-capital-markets-architecture-in-azerbaijan 15/59

15

A Client which is permitted under the Standard Form Agreement it has entered into with a

Euroclear group CSD to make and/or receive payments by means of the (I)CSD Systems as a

bank for the account of itself and/or one or more other Clients in connection with the DomesticService.

Settlement Bank Client

A Client who has appointed a Settlement Bank to provide cash services in connection with the

Domestic Service.

Settlement date

Date at which the financial instruments are to be delivered or received.

Settlement Finality Directive

Directive 98/26/EC of the European Parliament and of the Council of 19 May 1998 on

settlement finality in payments and securities settlement systems.

Settlement liquidity indicator

The liquidity position of a client in the system that uses the services of a settlement bank (i.e.

the liquidity position of a settlement bank’s client, as above). It reflects the liquidity resulting from

the settlement bank client’s activity in the Securities Settlement System (SSS).

Settlement liquidity limit

The amount of liquidity or credit which a settlement bank has notified to the CSD as being

available to a settlement bank client during each Business Day.

Single Platform

8/7/2019 CONCEPT PAPER FOR AN INTEGRATED CAPITAL MARKETS ARCHITECTURE IN AZERBAIJAN

http://slidepdf.com/reader/full/concept-paper-for-an-integrated-capital-markets-architecture-in-azerbaijan 16/59

16

Securities Settlement System,should be taken to mean all institutions, in particular CSDs,

performing the Pre-settlement, Settlement and custody functions except custodians.

STP

Straight Through Processing

System Paying Agent (SPA)

The party within the CSD that is responsible for distributing resources relating to a specific

distribution to other CSD parties.

Systematic internaliser

It means an investment firm which, on an organised, frequent and systematic basis, deals on

own account by executing client orders outside a regulated market or an MTF; the concept

stems from the EU’s MiFID directive

T

TARGET2

Trans-European Automated Real- Time Gross settlement Express Transfer 2

TPI

Identifiable bearer security, a service in Euroclear France that allows an issuer of bearer

securities to request a list of beneficial owners registered in the custodians’ books.

Trade date

The date on which a market trade is executed.

8/7/2019 CONCEPT PAPER FOR AN INTEGRATED CAPITAL MARKETS ARCHITECTURE IN AZERBAIJAN

http://slidepdf.com/reader/full/concept-paper-for-an-integrated-capital-markets-architecture-in-azerbaijan 17/59

17

U

UNIFI Standard

See 'ISO 20022 Financial Services'.

V

Valuation haircut

A risk control measure applied to securities used in reverse transactions, implying that the

central bank calculates the market value of the underlying securities, reduced by a certainpercentage (haircut). The Eurosystem (European Central Bank, ECB) applies valuation haircuts

that also reflect certain characteristics of the securities, notably their residual maturity.

Voting service provider (VSP)

A service provider mandated by the Client to act on its behalf. (I.e. receipt and sending of

meeting notifications, collection of voting instructions, instructing the system agent.

8/7/2019 CONCEPT PAPER FOR AN INTEGRATED CAPITAL MARKETS ARCHITECTURE IN AZERBAIJAN

http://slidepdf.com/reader/full/concept-paper-for-an-integrated-capital-markets-architecture-in-azerbaijan 18/59

18

3. Information flows and information systems for

securities trading

There are several large professional provider of financial information in Europe, and in the US,

who are specialists in the procurement, processing and distribution of international financial

information for investment advisory services, fund administration, portfolio management,

financial analysis, securities trading and securities administration.

They maintain database of structured, encoded securities information based on a global

network of market specialists that procures real-time stock exchange information at source from

the leading financial Centres. These so called Data providers are also a source of financial

information, they provides financial news and data (e.g. facts, statistics and analysis), for

professional and individual investors through various communication channels (e.g. the internet,

magazine).

They very often act also as official numbering agency responsible for allocating security

identification numbers.(NNAs, ISIN,CUSIP etc.) There is an Association of National Numbering

Agencies (ANNA) which leads the way in introducing standards aimed at simplifying trading and

securities administration. NDC is the member in ANNA for Azerbaijan.

4. Securities trading information flow

4.1. Pre-tradeCompliant with the EU requirements in its specific MiFID directive (see below for more details

8/7/2019 CONCEPT PAPER FOR AN INTEGRATED CAPITAL MARKETS ARCHITECTURE IN AZERBAIJAN

http://slidepdf.com/reader/full/concept-paper-for-an-integrated-capital-markets-architecture-in-azerbaijan 19/59

19

MiFID the basic capital market directive in the EU requires from all professional capital market

operators to publish the price, volume and time of all trades executed in listed shares, even if

executed outside of a regulated market, unless certain requirements are met to allow for deferred publication. But disclosure is required mandatory by the directive.

4.4. Clearing-Settlement-CustodyIt can be mentioned that in matters of clearing, settlement and custody the core directive for

capital markets in the EU MiFID remains silent. Also the other directives regarding prospectus,

market abuse, and transparency are only focusing of the trading not the post-trade aspects. It is

up to the member States in the EU to act in the matter.

Between 2002 and 2005, a joint CESR (Committee of European Securities Regulators)/ESCB

(European System of Central Banks) working group developed Standards for Clearing and

Settlement systems in Europe. Following other emerging initiatives in the area of post-trading,

activities of the group were disrupted after that period.

In 2007, the CESR Members decided to establish a group of CESR experts only, the Post-

Trading Expert Group (PTEG). This group does focus on post-trading activities in the EU, where

relevant for CESR and its members. PTEG, given the responsibilities of national securities

regulators for post-trading activities in the respective Member-States, does only focus on a

number of regulatory initiatives going on in the area of post-trading, with the objective to

enhance a level-playing-field and the safety and soundness of post-trading activities within the

EU. The political support for these regulatory initiatives was reflected in the conclusions of the

EU Council on Clearing and Settlement of 9 October 2007. Prior to this, CESR had decided to

create a platform to follow these initiatives more closely, establish a place to share supervisory

experiences and, where appropriate, to respond to these initiatives.

The first major point on the agenda of the PTEG is the Code of Conduct for Clearing and

Settlement, in particular with regard to the envisaged role of regulators in this Code. The Code

8/7/2019 CONCEPT PAPER FOR AN INTEGRATED CAPITAL MARKETS ARCHITECTURE IN AZERBAIJAN

http://slidepdf.com/reader/full/concept-paper-for-an-integrated-capital-markets-architecture-in-azerbaijan 20/59

20

communication interface with the external world that provides users with a single access to a

common integrated trading platform. It enables also clients to send instructions and receive

reports in industry standard formats, using a variety of networks.

All collected data are aggregated in a layer where all quotes and trade data are put in a feed

handler as received from the exchanges, the data providers etc. …to be aggregated in a feed

handling infrastructure for connection with the trading platform for processing. The market data

layer captures the BBO best bid of r offer across markets enabling later by order routing to how

an order is split and routed and how many titles are purchased. They can derive custom

indicators based on the order or trade information. These indicators, that show momentum or

compare executed liquidity versus displayed liquidity over a time window on a per venue basis,can be easily included in the order routing module later.

5.2. Trading toolsGlobal electronic trading is technology based. It is strategies, liquidity management tools and

advanced technology to execute trades. Trading tools must have the following capabilities:

direct execution to every major global exchange, control of order flow while maintaining

anonymity, order execution through a suite of global, qualitative algorithms designed to monitor market changes, dynamically optimize performance and avoid market impact. Sophisticated

liquidity management and advanced DMA products. Tools, access to ConvergEx ATS for block

crossing and aggregating dark liquidity (dark pools) tools. Trading platforms remain the core of

all the central integrated IT system In particular, but there are ancillary systems (AS); these

include retail payment systems, large-value payment systems, foreign exchange settlement

systems, money market systems, clearing houses and securities settlement systems (SSSs).

AS systems do usually settle their net positions either at the end of the day or at several times

during the day through an Ancillary System Interface (ASI), a standardized interface of thecommon shared IT platforms which control and distribute the information pertaining to Ancillary

Systems and, in particular, securities settlement systems activity. Continuous Net Settlement

8/7/2019 CONCEPT PAPER FOR AN INTEGRATED CAPITAL MARKETS ARCHITECTURE IN AZERBAIJAN

http://slidepdf.com/reader/full/concept-paper-for-an-integrated-capital-markets-architecture-in-azerbaijan 21/59

21

sample of an order routing system set-up and the connections with OMS etc... Order Routing

Solution consists always of two main layers – the first layer deals with the order flow and the

second layer deals containing the market data.

8/7/2019 CONCEPT PAPER FOR AN INTEGRATED CAPITAL MARKETS ARCHITECTURE IN AZERBAIJAN

http://slidepdf.com/reader/full/concept-paper-for-an-integrated-capital-markets-architecture-in-azerbaijan 22/59

22

8/7/2019 CONCEPT PAPER FOR AN INTEGRATED CAPITAL MARKETS ARCHITECTURE IN AZERBAIJAN

http://slidepdf.com/reader/full/concept-paper-for-an-integrated-capital-markets-architecture-in-azerbaijan 23/59

23

5.4. Order-presentation systemsIn this area we find now since recently now EMS, an execution management system (EMS). It is

a software-based platform that facilitates and manages the execution of securities orders,

typically through the Financial Information exchange (FIX) protocol.

EMSs have four key features: a trading blotter, connectivity, multiple destinations and real-time

market data. The trading blotter is composed of an order entry screen where users initiate and

monitor trading activity. Users can access brokers' direct-market-access (DMA) capabilities and

algorithms to carry out electronic trading strategies. The platforms enable both single-stock andportfolio trading capabilities. An EMS offers multiple destinations to which to route a trade.

Through the EMS platforms, users can connect to major exchanges, electronic communication

networks (ECNs), alternative trading systems (ATSs), crossing networks and multiple brokers.

Real-time market data enters the system from a combination of external feeds from exchanges

and market data providers and, in some cases, internal proprietary data from the EMS provider.

It is worth pointing out that, by definition, DMA platforms either are single- or limited-destination

systems. Although a number of DMA players call their order entry and management portals

EMSs, there should be a differentiation between an EMS and a pure DMA platform.

In comparison, the older traditional order management systems (OMSs) were designed as tools

to allow firms to manage and document their trading activities electronically. With an OMS, firms

easily can look back in order to analyse their orders. Since this modest beginning of OMSs as

trading blotters with FIX engines, they have extended the breadth and depth of their functionality

significantly. Today's OMSs have emerged as portfolio management systems with functionality

that ranges from pre-trade through post-trade support. The new EMSs may follow a path similar

to the one OMSs have followed through their evolution: The EMSs will increase the breadth of

their functionality, adding analytics, portfolio staging capabilities and tighter systems integration.

8/7/2019 CONCEPT PAPER FOR AN INTEGRATED CAPITAL MARKETS ARCHITECTURE IN AZERBAIJAN

http://slidepdf.com/reader/full/concept-paper-for-an-integrated-capital-markets-architecture-in-azerbaijan 24/59

24

when they meet certain conditions. SSSs either settle on a gross basis or on a net basis.

Integrated settlement model

SSSs settle transactions directly in their own system without the constant involvement of the

payment system. An interface is used at the request of clients when they want to transfer cash

into the SSS or back to the payment system. There are also settlement sub-Systems. These

systems process the settlement of instructions, manage the Securities Accounts balances and

the Purchasing Powers and provide reporting to the Clients.

Interfaced settlement model: transactions are settled using an interface between the payment

system and the SSS. As two systems are involved, they constantly communicate with eachother. The security leg is settled in the SSS while the cash leg is settled in the RTGS in the EU.

In settlement there is an internal transaction category. In a single platform context, in Euroclear

this transaction category includes: Intra-entity settlement transactions when both parties to the

transactions are members of the same (I)CSD; This covers: intra-Domestic transactions when

both parties are using the Domestic Service and transactions settle then on the books of the

primary issuer CSD or the CSD of reference of the security, intra-Full transactions when both

parties are using the Full Service and transactions settle then on the books of the custodianBank. Full-Domestic transactions when one party is using the Full Service and the other is using

the Domestic Service (i.e. one party is using a Domestic operational securities account and the

other is using a Full securities account); Domestic inter-CSD transactions when the security is

eligible in several group CSDs and one party is instructing on a depot with the primary issuer

CSD and the other is instructing on a depot with the other eligible CSD.

Securities are held with central securities depositories (CSD), who are notably responsible for

ensuring securities’ integrity. Next to the safekeeping function, CSDs enable securities’ mobility

as they operate securities settlement engines. There is usually at least one CSD and one SSS

in each EU country.

8/7/2019 CONCEPT PAPER FOR AN INTEGRATED CAPITAL MARKETS ARCHITECTURE IN AZERBAIJAN

http://slidepdf.com/reader/full/concept-paper-for-an-integrated-capital-markets-architecture-in-azerbaijan 25/59

25

In the context there is also SBI, a Broker to custodian trade affirmation system that is widely

used in the market.

5.6. Surveillance systemsIn order to face the challenge in trading surveillance and the need to detect employee fraud the

market has developed surveillance systems to prevent unauthorized trading and to avoid risks

for Financial Institutions. This kind of transactional risk management software for the financial

services industry developed in the US for surveillance and detection of employee trading fraud

solution for uncovering rogue trading in securities firms. These solutions do combine trading

surveillance and employee fraud detection this requires a proven technology and domain

expertise in the institutional and proprietary trading market. They are mostly based on a core

analytics and profiling engine and a set of flexible enterprise case management a

investigation applications, they are designed to identify trader behaviour and activities that could

be related to fraud or unauthorized activities.

6. The prevailing legal and regulatory framework in the EU

6.1. The main EU Directives on capital marketsThe main EU directive governing the capital markets is the Markets in Financial Instruments

Directive (MiFID). It is a European Union law that provides harmonized regulation for investment

services across the 30 member states of the European Economic Area (the 27 Member States

of the European Union plus Iceland, Norway and Liechtenstein).

MiFID is the cornerstone of the European Commission's Financial Services Action Plan whit

some 42 measures that did change significantly how the EU financial service markets dooperate. MiFID is the most significant piece of legislation introduced under the “'Lamfalussy”

procedure designed to accelerate the adopting of legislation based on a four-level approach as

d d b th C itt f Wi M h i d b B Al d L f l At th

8/7/2019 CONCEPT PAPER FOR AN INTEGRATED CAPITAL MARKETS ARCHITECTURE IN AZERBAIJAN

http://slidepdf.com/reader/full/concept-paper-for-an-integrated-capital-markets-architecture-in-azerbaijan 26/59

26

The institutional links among capital market operators are defined in 3 aspects: authorization,

regulation and pass-porting

Firms covered by MiFID will be authorised and regulated in their "home State" (broadly, the

country in which they have their registered office). Once a firm has been authorised, it will be

able to use the MiFID passport to provide services to customers in other EU member States.

These services will be regulated by the member state in their "home State".

To determine which firms are capital market operators under the legal MiFID frame and which

are not, MiFID distinguishes between "investment services and activities" ("core" services) and

"ancillary services" ("non-core" services).

If a professional capital market operator performs investment services and activities, it is subject

to MiFID in respect both of these and also of ancillary services (and it can use the MiFID

passport to provide them to member States other than its home State). However if a firm only

performs ancillary services, it is not subject to MiFID (but cannot benefit from a MiFID passport).

MiFID covers almost all tradable financial products with the exception of certain foreign

exchange trades. This includes therefore commodities and derivatives but also such as freight,climate and carbon derivatives, which were not covered by the former EU investment services

directive ISD that now is now superseded by MiFID.

That part of an investment firm's (capital market operator) business that is not covered by the

above is not subject to MiFID.

6.3. The role of professional capital markets participants

MiFID requires professional capital markets participants to categorize their clients as "eligiblecounterparties", professional clients or retail clients (these have increasing levels of protection).

Clear procedures must be in place to categorize clients and assess their suitability for each type

of investment product That said the appropriateness of any investment advice or suggested

8/7/2019 CONCEPT PAPER FOR AN INTEGRATED CAPITAL MARKETS ARCHITECTURE IN AZERBAIJAN

http://slidepdf.com/reader/full/concept-paper-for-an-integrated-capital-markets-architecture-in-azerbaijan 27/59

27

The number of additional pricing sources introduced by MiFID means that financial institutions

have now to seek additional data sources to ensure that they capture as many quotes/trades as

possible.

6.4. The role of the Capital Markets RegulatorsMiFID retained the principles of the EU 'passport' introduced by the old investment services

directive ISD but innovated by introducing the concept of 'maximum harmonization' which

places more emphasis on home State supervision. This is a change from the prior EU financial

service legislation which featured a 'minimum harmonization and a mutual recognition' concept

in matters of Regulatory supervision.

'Maximum harmonization' does not permit member States to be 'super equivalent' or to 'gold-

plate' EU requirements detrimental to a 'level playing field' as done previously in some member

States when implementing EU directives.

Another regulatory change was the abolition of the 'concentration rule' in which member States

could require investment firms to route client orders through regulated markets. The capital

market Regulators are, as previously mentioned the fourth level in the “Lamfalussy procedure”,

they have to take care of compliance and enforcement of the in national rules and laws

transposed MiFID directive, the Prospectus Directive, the Market Abuse Directive and the

Transparency Directive. Under European law, a Directive has to be transposed into national

law: an EU Regulation, when issued, on the other hand, is automatically binding throughout all

member states.

7. The prevailing capital markets architectural models inthe EU

7 1 The Euroclear model

8/7/2019 CONCEPT PAPER FOR AN INTEGRATED CAPITAL MARKETS ARCHITECTURE IN AZERBAIJAN

http://slidepdf.com/reader/full/concept-paper-for-an-integrated-capital-markets-architecture-in-azerbaijan 28/59

28

7.1.2. Organisational links among various capital markets stakeholders.

Euroclear is a Settlement service provider only. Settlement is only the delivery of securities,

usually against payment, to complete a trade between two parties. Settlement as the final stepin securities transactions is vital for a good functioning of financial markets. At the time of the

settlement, the proprietary ownership becomes effective for the purchaser from a legal point of

view.

Clients of Euroclear submit an instruction telling Euroclear when, how and with whom they want

them to settle their securities transaction. Usually this is done electronically through a fast and

low-cost form of processing known as Straight-Through Processing (STP). The counterparty in

the trade also submits an instruction.

Euroclear match up the two instructions, and make sure the seller has the securities and, if

against payment, the buyer can pay. They then settle the transaction which can take different

forms depending: if it is taking place between two clients of the same Central Securities

Depository (CSD) or an International CSD (ICSD), a simple book-entry transfer is made

enabling the required simultaneous exchange of cash and securities.

Where the trade is between two counterparties in different countries, with accounts in differentICSD’s, settlement is achieved through local market settlement structures, which vary from

market to market as there is diversity in the EU capital markets.

The settlement process is also largely determined by the type of asset and market. For

example, unlike for bond and equity transactions, order routing is an essential step prior to the

settlement phase for fund orders. Within the Euroclear group, EMXCo is the provider of funds

order routing.

7.1.3. Institutional links among various capital markets stakeholders

As providers of settlement services, the Euroclear group is a horizontal organized structure that

comprises Euroclear Bank in Brussels an ICSD (International Central Securities Depository)

8/7/2019 CONCEPT PAPER FOR AN INTEGRATED CAPITAL MARKETS ARCHITECTURE IN AZERBAIJAN

http://slidepdf.com/reader/full/concept-paper-for-an-integrated-capital-markets-architecture-in-azerbaijan 29/59

29

Below a schematic graph to illustrate this capital market organization.

Horizontal structured providers of settlement and custody and horizontal providers of clearing function

Stock exchange A

Trading &Settlement

Settlement

Stock exchange B

Trading& Settlement

Stock Exchange

C

Trading &

Settlement

Clearing

Euronext

Clearing LSEClearingL CH Clernet

Brokers

Universal Banks

8/7/2019 CONCEPT PAPER FOR AN INTEGRATED CAPITAL MARKETS ARCHITECTURE IN AZERBAIJAN

http://slidepdf.com/reader/full/concept-paper-for-an-integrated-capital-markets-architecture-in-azerbaijan 30/59

30

7.2. The Clearstream model

7.2.1. IT Architecture

Clearstream uses three trading platforms: Eurex, an integrated, fully electronic derivatives

trading and clearing system. The Eurex clearing functionality also supports clearing of equities,

bonds and repos traded on the Frankfurt Stock Exchange. Xetra , the other electronic trading

platform for the cash market allows the trading of stocks on one platform – everywhere in the

world. “Link Up Markets” the third platform is a common IT infrastructure allowing for easy

implementation of links between CSD markets and introducing efficient cross-border processing

capabilities.

Clearstream is developing also a new globalized standard IT platform using open source

components, commercial third parties soft-ware and internally developed software. The design

will be modular base on a shared technical infrastructure which combines extremely low latency

with high volume. This platform will favour algorithmic trading by mitigating towards an Itanium

platform to boost output with new enhances broadcast solutions.

7.2.2. Organisational links among various capital markets stakeholdersClearstream is a wholly owned subsidiary of the Deutsche Börse. It offers two fundamentalservices to the industry:

International central securities depository (ICSD) services and the Central securities depositoryservices (CSD) for German and Luxembourgish domestic securities. It also operates now theLink Up Markets, joint venture by nine leading Central Securities Depositories (CSDs) – acommon infrastructure allowing for easy implementation of links between CSD markets,introducing efficient cross-border processing capabilities.

Clearstream also has an innovative post trade system for investment funds CFF Central Facility

for Investment Funds based on its own proprietary order-routing system Vestima +

8/7/2019 CONCEPT PAPER FOR AN INTEGRATED CAPITAL MARKETS ARCHITECTURE IN AZERBAIJAN

http://slidepdf.com/reader/full/concept-paper-for-an-integrated-capital-markets-architecture-in-azerbaijan 31/59

31

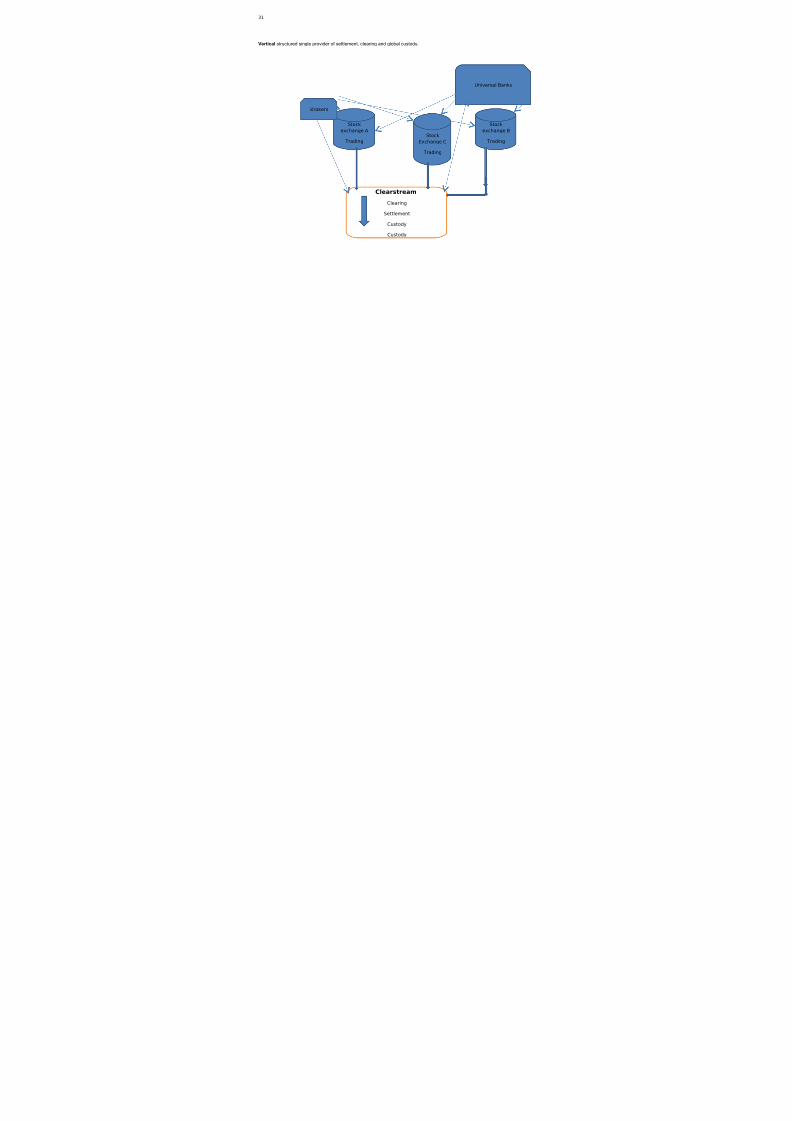

Vertical structured single provider of settlement, clearing and global custody.

Stock

exchange A

Trading

Stock

exchange B

Trading

Stock

Exchange C

Trading

Clearstream

Clearing

Settlement

Custody

Custody

Brokers

Universal Banks

8/7/2019 CONCEPT PAPER FOR AN INTEGRATED CAPITAL MARKETS ARCHITECTURE IN AZERBAIJAN

http://slidepdf.com/reader/full/concept-paper-for-an-integrated-capital-markets-architecture-in-azerbaijan 32/59

32

7.3. Comparisons between the two

The fundamental difference is reflected in the structural aspect: Clearstream has a verticalsingle provider integrated set -up structure whereas Euroclear has a horizontal approach with

several providers in matters of capital market architecture. The issue is that Clearstream is

owned by a single shareholder Deutsche Börse, while Euroclear is owned by its users the

different stock exchanges, brokers and investment banks. The fee earnings therefore are at the

level of these shareholders who act as “clearers” in the Euroclear structure leaving Euroclear

only the trading and settlement activities to handle and earn less(mostly running the services at

cost). But both architectures compete in the market to provide the lowest global processing

fees, in addition the MTF are now also more and more a competitor capital markets structure.

From this fundamental organizational difference also stems the difference in their respective

functionalities: Euroclears provides settlement only, while clearing and custody is always

mandatory provided by third parties, who in most cases of the time are also its shareholders of

Euroclear. From an economic point of view there may be a conflict of interests, as ,as

shareholders they want the best possible return, while as users they want to pay the lowest

handing fees.

Clearstream does provide the whole range of services from trading to all integrated post trading

services; settlement, clearing and custody; it is owned by the Deutsche Börse Group. In addition

both are Global Custody services providers world-wide and competitors in the European capital

markets post trade value chain services.

There is an electronic bridge between both ICSDs (Clearstream and Euroclear have also both

ICSD statuses) this interoperability has significantly contributed to attract liquidity from new

customers.

But in the last Financial crisis, in September 2009, only Clearstream was able to offer

8/7/2019 CONCEPT PAPER FOR AN INTEGRATED CAPITAL MARKETS ARCHITECTURE IN AZERBAIJAN

http://slidepdf.com/reader/full/concept-paper-for-an-integrated-capital-markets-architecture-in-azerbaijan 33/59

33

In clear the systemic risk of horizontal capital market architecture was revealed to be higher

than that of the vertical structured capital markets architecture. That major point was for

Clearstream in the competition game on the European capital markets.

During the financial crisis in 2009 clients of Euroclear were obliged to shift therefore their asset

from Euroclear to Clearstream to benefit from the Clearstream clearing facility failing Euroclear

set-ups’ ability to clear their trading transactions.

This may also explain, as mentioned above in 7.2.3, that CSDs from eight leading Central

Securities Depositories (CSDs) – Cyprus Stock Exchange (Cyprus), Hellenic Exchanges S.A.

(Greece), IBERCLEAR (Spain), Oesterreichische Kontrollbank AG (Austria), SIX SIS AG(Switzerland), STRATE (South Africa), VP SECURITIES (Denmark) and VPS (Norway) did

prefer to join Clearstreams’ Link Up Markets joint venture for leading Central Securities

Depositories (CSDs) instead of pooling up with Euroclear.

Systemic risk considerations do explain the choice in favour of Clearstream in the opinion of the

consultant.

From a strictly operational point of view, the handling of the flux of assets and cash is easier toprocess in a vertical structure, so operational risk results to be less than in a horizontal

structured architecture. Therefore a vertical capital market model has a better operability and a

better risk management capacity, compared with the horizontal capital market architecture.

Needless to say the consultant recommends for Azerbaijan the adoption of the vertical

structured capital market architecture as the better choice.

It must also be mentioned that the new MTFs in the capital markets worldwide, as mentioned

previously already by the consultant, are also vertical structures for the same obvious reasons.

8 The prevailing capital markets architectural models in

8/7/2019 CONCEPT PAPER FOR AN INTEGRATED CAPITAL MARKETS ARCHITECTURE IN AZERBAIJAN

http://slidepdf.com/reader/full/concept-paper-for-an-integrated-capital-markets-architecture-in-azerbaijan 34/59

34

Free transfer

The Stock Transfer Transactions between members vary in respect of whether the security,

which will be transferred, is dematerialized or not. Dematerialized transfers vary according to

institutions being party to the transfer.

or Electronic Security Transfer (EMKT) Transactions

EMKT is a system established within the framework of CBT Central Bank of Turkey, facilitating

the real-time execution of buy-sell, transfer and other related transactions of dematerialized

securities in an electronic environment and in an integrated manner with EFT. Brokerage

houses, which are members of TETS (Takasbank Electronic Transfer System) can join this

system through Takasbank.

TAKASBANK does also provide custody and banking services. Within the framework of central

custodian services provided all records relating to the stock certificates and investment fund

participation certificates traded in the stock exchange have been transferred to the Central

Registry Agency Inc. in accordance with the regulations of Capital Markets Board regarding

dematerialization of securities.

Physical custodian services towards the members of ISE, issuer companies and corporate

investors is continued to be provided.

In clear a vertical architecture type of an emerging market capital market organisational set-up.

The Regulator in Turkey is the CMB, or Capital Markets Board of Turkey.

8.2. The Russian modelIn Russia we have the MICEX Stock Exchange

Withi th MICEX G th CJSC “MICEX St k E h ” i th l t t k h i

8/7/2019 CONCEPT PAPER FOR AN INTEGRATED CAPITAL MARKETS ARCHITECTURE IN AZERBAIJAN

http://slidepdf.com/reader/full/concept-paper-for-an-integrated-capital-markets-architecture-in-azerbaijan 35/59

35

Currently NDC is Russia’s largest settlement and safekeeping provider.

The Moscow Interbank Currency Exchange Settlement House (MICEX SH) is a credit

organization that provides settlement banking services, including cash settlements on trades

made by financial market participants.

The MICEX Settlement House:

acting as a settlement bank, offers its clients a full range of settlement services;

it performs cash settlements in real time. Clients’ payment orders are handled and

executed immediately after their delivery to the MICEX SH;

it completes cash settlements on participants’ transactions on the day of trading;

it guarantees timely settlements and the safety of its clients’ funds;

interacts with clients throughout the entire trading day;

is one of the main exchanges trading infrastructure. Since January 1, 1997, it providesreliable and prompt cash settlements on trades made in MICEX financial markets;

it provides settlement services in all of the MICEX financial markets:

the government-backed securities market;

the corporate securities market;

the currency market;

the derivatives (standard contracts) market.

8/7/2019 CONCEPT PAPER FOR AN INTEGRATED CAPITAL MARKETS ARCHITECTURE IN AZERBAIJAN

http://slidepdf.com/reader/full/concept-paper-for-an-integrated-capital-markets-architecture-in-azerbaijan 36/59

36

“to meet the adhesion criteria. Deficiencies were detected in the areas of prospectus directive,

market abuse and transparency: the operational aspects of the capital market structure. Actually

the vetting procedure is frozen by the EU and accession talks are suspended because theunsolved Cyprus issue.

In the case of Russia the actual structure is rather cumbersome (as resulting from the fact that it

is a horizontal structure, except the RTS who is a vertical structured type) with many entities

intervening in the market. In the end both organisational set up do not provide full DVP, which is

an absolute prerequisite requirement in an EU type of capital market structure. Deficiencies do

also exist in matters of prospectus directive, market abuse, transparency and corporate

governance

8/7/2019 CONCEPT PAPER FOR AN INTEGRATED CAPITAL MARKETS ARCHITECTURE IN AZERBAIJAN

http://slidepdf.com/reader/full/concept-paper-for-an-integrated-capital-markets-architecture-in-azerbaijan 37/59

37

9. The proposed architecture for Azerbaijan

9.1. Action plan and time frame for implementation

9.1.1 Global Strategy

The action plan starts with a day T, to be the day the decision is taken to accept the proposal

and to start the implementation of the proposal as such. We have then to differentiate between

the broader sub-strategies to be followed:

Sub strategy A-Define the structural aspects to achieve the new capital market organisational

set-up in Azerbaijan, indicate the time and means to achieve this recommended structures and

institutional frame, and

Sub strategy B- Define the operational aspects of this new capital market architecture that

must be put in place and indicate the time required, to enable the institutions and all other

capital market participants to operate in the new proposed structure,

Sub strategy C-in addition the proposed set-up capital market structure will need

appropriated IT-tool/platform. The consultant intends to recommend a modular base on a

shared technical infrastructure to combine extremely low latency with high volume. This platform

should favour algorithmic trading by mitigating towards a Itanium platform to boost output with

new enhances broadcast solutions as developed now by Clearstream, to be ready in the future,

once trading will start for real at the BSE and

Sub strategy D- to conclude the consultant intends to undertake a marketing study/ marketneeds analysis to define suitable products to be traded on the capital market that will generate

a kick-off of the stock exchange transactions in the end.

8/7/2019 CONCEPT PAPER FOR AN INTEGRATED CAPITAL MARKETS ARCHITECTURE IN AZERBAIJAN

http://slidepdf.com/reader/full/concept-paper-for-an-integrated-capital-markets-architecture-in-azerbaijan 38/59

38

In the case of Azerbaijan to set-up the legal frame the consultant recommends, would require a

simultaneous implementation of all the EU directives mentioned under 9.6 below to have the

required global legal frame duly set-up:

The consultant has drafted a graph showing the time frame for this action to be undertaken to

achieve the implementation of this legal frame, it encompasses also elaboration of supervisory

reporting frame to the Regulator SCS regarding compliance. Capacity building to exercise the

prudential supervision of the market would accompany the consultants’ action. The consultant

has elaborated a graph showing in details the time allocated to achieve the proposed

implementation. (Gantt chart in Annex 2)

Another element of the main task for the consultant is the enabling of the banks to act as

brokers in the stock exchange; this would require also elaboration of regulations and an

appropriated reporting frame to the Regulator. Banks should also be enabled to act as

custodians banks; again this will require elaboration of regulations and an appropriated

reporting frame to the Regulator. The graph illustrates the time necessary to achieve these

objectives as well.

The major work load would be for the consultant to facilitate the required change of status for NDC towards a CSD status enabled institution. This would require the consultant to elaborate

detailed proposals for rules and regulations to be implemented. Also capacity building for the

institutions involved (SCS, NDC and BSE) should be done in parallel. This is also reflected in

the detailed graph in the graph in Annex 2.

9.1.3 Main actions and priorities

As resulting from the information of the consultant in Azerbaijan, the legal frame for capital

markets transactions is based on some specific articles in the civil code. There is also a draftlaw for domestic investment funds under scrutiny. This from a capital market point of view is a

piece meal structure. It does not allow for the development of a coherent capital market.

8/7/2019 CONCEPT PAPER FOR AN INTEGRATED CAPITAL MARKETS ARCHITECTURE IN AZERBAIJAN

http://slidepdf.com/reader/full/concept-paper-for-an-integrated-capital-markets-architecture-in-azerbaijan 39/59

39

compensation scheme for all professionals such as: Investment firms, Investment advisers,

Brokers in financial instruments, Commission agents, Private portfolio managers , Professionals

acting for their own account, Market makers, Underwriters of financial instruments, Distributorsof units/shares in investment funds, Financial intermediation firms, Investment firms operating

an MTF in Azerbaijan, Miscellaneous firms other than investment firms, Registrar agents,

Professional custodians of financial instruments.

2-Authorization for the establishment of branches and freedom to provide services

3-Professional obligations, prudential rules and rules of conduct in the capital market

4-Provisions applicable to credit institutions when acting as brokers and investment

firms

Organisational requirements, Conflicts of interest, Conduct of business rules when providing

investment services to clients, Provision of services through the medium of another credit

institution or another investment firm , Obligation to execute orders on terms most favourable to

the client, Client order handling rules ,Transactions executed with eligible counterparties ,

Obligations of credit institutions and investment firms when appointing tied agents, Professionalobligations of the financial sector as regards combating money laundering and the financing of

terrorism, Obligation to cooperate with the authorities , Obligation of professional secrecy

5-Prudential supervision of the capital market

-The competent authority responsible for supervision and its tasks,Purpose of

supervision, Professional secrecy of the Regulator, Exchange of information with other

Regulators, Exchange of information with third countries.

-Supervision of investment firms on a consolidated basis: Definitions, Scope and

parameters of supervision on a consolidated basis, Form and extent of consolidation, Content of

8/7/2019 CONCEPT PAPER FOR AN INTEGRATED CAPITAL MARKETS ARCHITECTURE IN AZERBAIJAN

http://slidepdf.com/reader/full/concept-paper-for-an-integrated-capital-markets-architecture-in-azerbaijan 40/59

40

-Reorganization and winding up of certain professionals in the capital market: Definitions,

Scope, Suspension of payments: Provisions governing the opening of proceedings for

suspension of payments, Opening of proceedings for suspension of payments, Competentjurisdiction and applicable law.

Winding up: Voluntary winding up,: Provisions governing proceedings for the judicial winding

up of establishments ,Winding-up proceedings, Withdrawal of an establishment’s authorization,

Provision of information to known creditors , Lodgement of claims.

-Provisions common to reorganization measures and winding-up proceedings: Effects on

certain contracts and rights , Third parties’ rights, Reservation of title, Set-off, Nettingagreements , Repurchase agreements, Regulated markets, proof of the appointment and

powers of administrators and liquidators, Registration in a public register, Detrimental acts,

Protection of third parties, Lawsuits pending, Professional secrecy.

6-Deposit-guarantee schemes: Compensation schemes for investors in credit institutions

and investment firms

7-Penalties: Administrative fines; Criminal sanctions

9.1.4 Ancillary tasks

The consultant recommends the set-up of an integrated IT platform for the BSE and NDC

(deemed to become a CSD in the proposed architecture. This is the technical component,

corollary to the set-up of the legal and regulatory architecture of capital markets in Azerbaijan.

This requires that part time the consultant should assist the IT developers to design such an

integrated platform until the testing and launch to start after T in parallel. This is also duly

reflected in the graphical scheme in Annex 2. The time frame is 6-12 months for thedevelopment of such a platform, according IT duly consulted.

Another part time task for the consultant would be, simultaneously, assuming the proposed

8/7/2019 CONCEPT PAPER FOR AN INTEGRATED CAPITAL MARKETS ARCHITECTURE IN AZERBAIJAN

http://slidepdf.com/reader/full/concept-paper-for-an-integrated-capital-markets-architecture-in-azerbaijan 41/59

41

hub at Baumgarten covers 10% of Europe’s gas requirements. This percentage is expected to

rise further when Nabucco and the South Stream gas pipelines will be connected.

The gas exchange should bring transparency and flexibility in the gas prices that actually are

resulting from long term contracts between European suppliers and Gazprom. This initiative

seems to be an attempt to emulate the actual existing Caspian Oil & Gas Exchange.

The require time for this task for the consultant is also reflected in the graph in Annex 2 and is

scheduled over a period of two years.

9.2. The capital markets operators’ positionsThe position of the different operators is shown in the context of the proposed new proposal

architecture of the capital market in Azerbaijan.

9.2.1. The Baku Stock Exchange

The stock exchange should share the common integrated IT platform that need to be put in

place to make the capital market operational in Azerbaijan. The core element of any capital

market; the Baku Stock Exchange must necessarily be endowed exclusively and compulsory

with all securities trading in the Azerbaijan capital market architecture proposal of theconsultant.

It is understood that under securities’ the consultant regroups all eligible items to be traded on a

stock exchange: from plain vanilla securities like stocks and bonds, that are currently on a case

by case dealt in, already sporadically now, to derivatives, commodities and currencies that could

be eligible at a later stage, once the market develops.

This encloses also private deals done on listed equities that should and must be duly notified tothe Baku Stock Exchange compulsory.

The consultant recommends to formulate policy recommendations as mentioned under 9.1 on

8/7/2019 CONCEPT PAPER FOR AN INTEGRATED CAPITAL MARKETS ARCHITECTURE IN AZERBAIJAN

http://slidepdf.com/reader/full/concept-paper-for-an-integrated-capital-markets-architecture-in-azerbaijan 42/59

42

The Baku Stock exchange necessarily should also be vested to initiate the clearing and

settlement functions as these post-trade chains technical functionalities are required to be

located under the responsibility of the Stock exchange given the requirements of the EUregulations.

A stock exchange under EU rules must be regulated, operating regularly (no sporadic trading as

actually in the Baku Stock Exchange ref. “Reflection paper on an “ad hoc” capital market

architecture in Azerbaijan” December 2009) and open to the public. This is defined in more

details as meaning:

The stock exchange must be “regulated”; under EU rules the essential characteristic of aregulated market is the clearing, which presupposes the existence of a central market

organization for the processing of orders. Such a market may also be distinguished by

multilateral order matching (general matching of bids and offers enabling the setting of a single

price), transparency (maximum information distribution amongst buyers and sellers giving them

the possibility to follow the evolution of the market, so that they may ensure that their orders

have been carried out at current conditions) and the neutrality of its organizer (the organizers’

role must be limited to recording and supervision).

In addition EU rules require a stock exchange to be “recognized”, the stock exchange must be

recognized by a State or by public Authority which has been delegated by that State or by

another Entity which is recognized by the State or by that public Authority, such as a

professional Association.

“Operating regularly” as already previously mentioned securities admitted to this market must be

dealt in at certain fixed frequency and “open to the public” the securities dealt thereon must be

accessible to the public: they must be able to acquire and sell the quoted items.

In that regard an assessment of the fulfilment of the before mentioned requirements must be

d t k d ti l d i d t l ith th i t T t i

8/7/2019 CONCEPT PAPER FOR AN INTEGRATED CAPITAL MARKETS ARCHITECTURE IN AZERBAIJAN

http://slidepdf.com/reader/full/concept-paper-for-an-integrated-capital-markets-architecture-in-azerbaijan 43/59

43

technically speaking: as deals/transactions cannot fail, as all transaction elements (cash/

securities) must be present before initiating the dealing in the stock exchange. Therefore this

eliminates any failed trades at the end of the post-trade value chain.

These recommended reforms to be addressed as outlined under NDC by an appropriated

presidential decree approach in matters legal handling. The institution empowered to act under

the decree being the State Committee for Securities.

9.2.2. The National Depository Centre

The National Depository Centre, NDC in the Azerbaijan capital market architecture should have

the pivotal role, as in the EU capital market structural architecture.

In the EU the key participants in any reform of Clearing & Settlement are those, whose roles are

integral to the process, i.e. Central Counterparties (Clearing), Central Securities Depositories

(Settlement & Custody) and Central Banks (cash settlement, collateral etc.).

However, these are generally not retail service providers and access to their services is

provided through wholesale service providers such as Custodians (Global and Domestic) and

Clearing Members (Global and Self Clearing). Investment Managers and Brokers are also

important participants but only as initiators of Clearing & Settlement activity through trading and

investment.

In the case of Azerbaijan a first pre-requisite would be that the NDC would compulsory become

the provider of the custody function in the capital market for all listed securities in Azerbaijan:

the CSD for Azerbaijan. This recommendation is within the scope of actual project aims. It

carries as corollary a compulsory dematerialization to be the standard for those securities

seeking a listing and trading at the Baku Stock Exchange. No CSD, is involved in supervisingcustodian banks in the EU/EEA area. All securities traded in Azerbaijan (inclusive State or

Government securities should fall under the jurisdiction of the CSD). The Azerbaijan CSD

should exclusively deal with other CSD abroad and with the ICSD and the Global custodians

8/7/2019 CONCEPT PAPER FOR AN INTEGRATED CAPITAL MARKETS ARCHITECTURE IN AZERBAIJAN

http://slidepdf.com/reader/full/concept-paper-for-an-integrated-capital-markets-architecture-in-azerbaijan 44/59

44

domestically with brokers and banks. As outlined, OTC transactions must be mandatory under

the jurisdiction of CSD, the same as the other trades.

The National Depository Centre, NDC in the Azerbaijan capital market architecture should have

a pivotal role, as in the EU capital market structural architecture as the central clearing house,

which is an important mandatory attribute of a CSD beside netting, and the settlement. OTC

falls under the jurisdiction of the CSD as well as mandatory these transactions must be reported

to the CSD.

This could be achieved in several steps: the first requirement would be the enactment of the

basic new capital market law draft proposal as made by the consultant. This would require timeto elaborate; time to go through the legislative procedure, Parliament etc. Based on the example

in Romania, that needed to meet the EU criteria in matters capital market organization for not

delaying the EU accession further, all, so called “EU reforms” were simply addressed by issuing

a presidential decree enacting all EU legislation to be applicable in Romania, after a specified

date. Thereby Romania did gain the time to elaborate detailed organic laws, ministerial decrees

and regulations to implement in domestic law all the EU acquis communautaire. To avoid a

difficult transition this kind of approach could be recommended by the consultant: the State

Committee for Securities becoming the institution to issue instructions rules etc…under apresidential decree pertaining to organize the proposed capital market structure in Azerbaijan.

The SCS would be empowered to issue binding rules and regulations that at a later stage could

be repelled by specific organic law when elaborated, issued and superseding these rules. The

transformation from NDC to CSD status could result from a simple rule issue based on the

presidential decree from the SCS.

CSD should hold securities and enable securities transactions to be processed through book

entry. In Azerbaijan its home country, CSD should provide processing services for trades of

those securities that it holds in final custody, and in this function it is referred to as “the issuer

Central Securities Depository” A CSD can also process services as an intermediary in cross-

8/7/2019 CONCEPT PAPER FOR AN INTEGRATED CAPITAL MARKETS ARCHITECTURE IN AZERBAIJAN

http://slidepdf.com/reader/full/concept-paper-for-an-integrated-capital-markets-architecture-in-azerbaijan 45/59

45

As outlined previously, to reduce the transition time and resulting legal insecurity, the

presidential decree approach could also be used to address the creation of a National Central

Registrar in Azerbaijan, to be formalized at a later stage by the consultants’ elaboration of aspecific basic law for later implementation.

In case all joint stock companies shares should be kept only in dematerialized form at the

Central Registrar as done for instance in France. In this case the Central Registrar deals with

final owners no broker, no custodian bank, no fronting possible, but restricted to the domestic

market in Azerbaijan.

In France this is handled under TPI as an example: (TPI stands for Identifiable bearer security in

French, a service that allows an issuer of bearer securities to request a list of beneficial owners

registered in the custodians’ books.)

The Central Registrar is also the only institution were liens and pledges over securities can be

registered this cannot be done in CSDs as they deal not at retail level.

The main argument is to ascertain the title for shareholders/investors and guarantee corporate

governance in all aspects. A Central Registrar could also extend its registration to bondholders

(public or private), the argument in favour is again corporate governance: bondholders are