Computing the maximum likelihood estimates: concentrated likelihood, EM ... · Computing the...

47

Computing the maximum likelihood estimates: concentrated likelihood, EM-algorithm Dmitry Pavlyuk The Mathematical Seminar, Transport and Telecommunication Institute, Riga, 13.05.2016

-

Upload

truongcong -

Category

Documents

-

view

227 -

download

0

Transcript of Computing the maximum likelihood estimates: concentrated likelihood, EM ... · Computing the...

Computing the maximum

likelihood estimates: concentrated

likelihood, EM-algorithm

Dmitry Pavlyuk

The Mathematical Seminar,

Transport and Telecommunication Institute, Riga, 13.05.2016

Presentation outline

Pavlyuk D. Computing the maximum likelihood estimates: concentrated likelihood, EM-algorithm, Riga, 13.05.2016

1. Basics of MLE

2. Pseudo-likelihood

3. Finite Mixture Models

4. The Expectation-Maximization algorithm

5. Numerical Example

2

Pavlyuk D. Computing the maximum likelihood estimates: concentrated likelihood, EM-algorithm, Riga, 13.05.2016 3

1. Basics of MLE

The estimation problem

Pavlyuk D. Computing the maximum likelihood estimates: concentrated likelihood, EM-algorithm, Riga, 13.05.2016

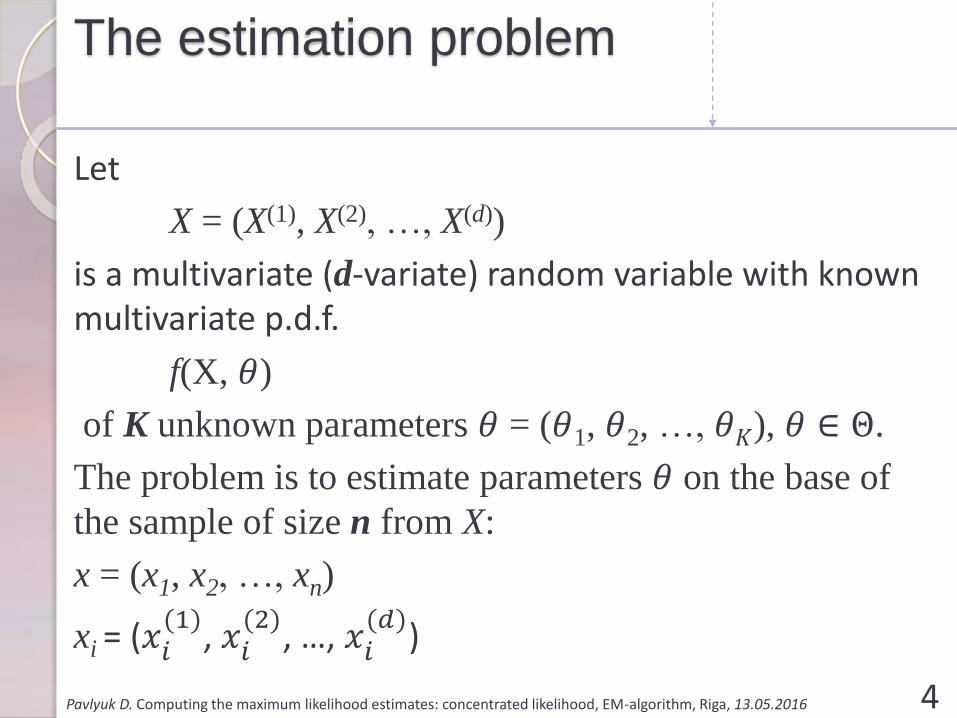

Let

X = (X(1), X(2), …, X(d))

is a multivariate (d-variate) random variable with known multivariate p.d.f.

f(X, 𝜃)

of K unknown parameters 𝜃 = (𝜃1, 𝜃2, …, 𝜃𝐾), 𝜃 ∈ Θ.

The problem is to estimate parameters 𝜃 on the base of

the sample of size n from X:

x = (x1, x2, …, xn)

xi = (𝑥𝑖(1)

, 𝑥𝑖(2)

, …, 𝑥𝑖(𝑑)

)

4

Maximum likelihood estimator

Pavlyuk D. Computing the maximum likelihood estimates: concentrated likelihood, EM-algorithm, Riga, 13.05.2016

The likelihood function 𝐿 𝜃 𝑥 represents probability of receiving the sample x given parameters 𝜃.

In case of independent observations in the sample

𝐿 𝜃 𝑥 = ෑ

𝑖=1

𝑛

𝑓 𝑥𝑖 , 𝜃

The maximum likelihood estimator is (R. Fisher, 1912+):

መ𝜃𝑚𝑙𝑒 = argmax𝜃∈Θ

𝐿 𝜃 𝑥

if a maximum exists.

5

Maximum likelihood estimator

Pavlyuk D. Computing the maximum likelihood estimates: concentrated likelihood, EM-algorithm, Riga, 13.05.2016

For computation purposes the log-likelihood function is introduced:

𝑙 𝜃 𝑥 = 𝑙𝑛𝐿 𝜃 𝑥 = 𝑙𝑛 ෑ

𝑖=1

𝑛

𝑓 𝑥𝑖 , 𝜃 =

𝑖=1

𝑛

𝑙𝑛𝑓 𝑥𝑖 , 𝜃

Good limiting statistical properties of መ𝜃𝑚𝑙𝑒:

- Consistency

- Asymptotic efficiency

- Asymptotic normality

6

Maximum likelihood estimator

Pavlyuk D. Computing the maximum likelihood estimates: concentrated likelihood, EM-algorithm, Riga, 13.05.2016

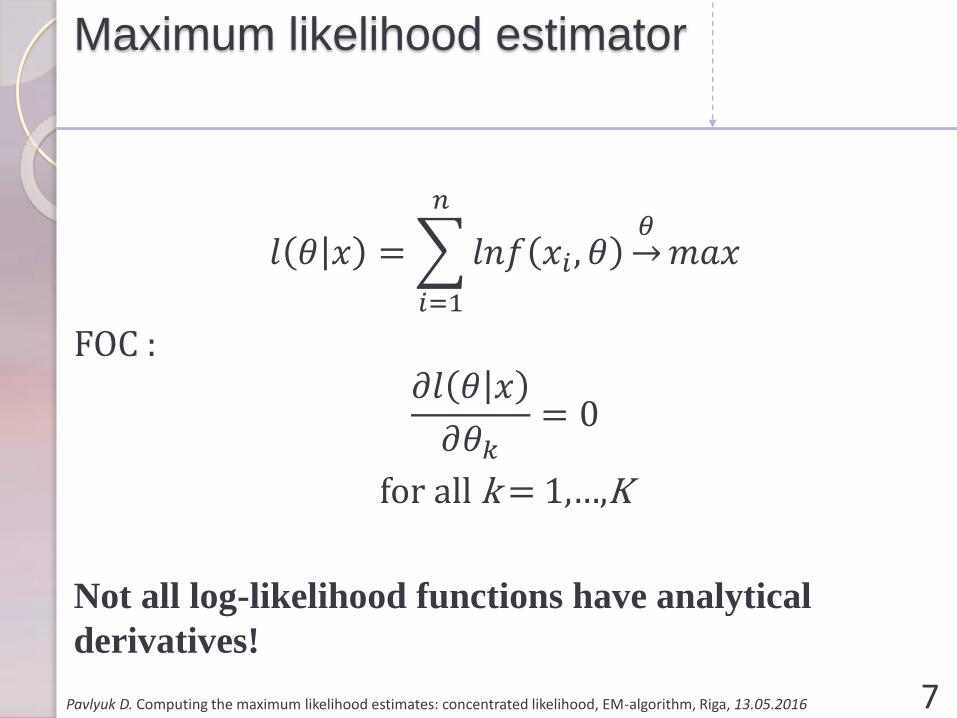

𝑙 𝜃 𝑥 =

𝑖=1

𝑛

𝑙𝑛𝑓 𝑥𝑖 , 𝜃 ՜𝜃

𝑚𝑎𝑥

FOC :𝜕𝑙 𝜃 𝑥

𝜕𝜃𝑘= 0

for all k = 1,…,K

Not all log-likelihood functions have analytical

derivatives!

7

MLE example: multivariate

normal

Pavlyuk D. Computing the maximum likelihood estimates: concentrated likelihood, EM-algorithm, Riga, 13.05.2016

For example, for the multivariate normal variable:𝑋~𝑀𝑉𝑁 𝜇, Σ𝜃𝑚𝑣𝑛 = 𝜇, Σ

𝑓𝑚𝑣𝑛 𝑥, 𝜃𝑚𝑣𝑛 = 𝜑 𝑥, 𝜇, Σ

=1

2𝜋𝑑

𝑑𝑒𝑡Σ𝑒−

12 𝑥−𝜇 𝑇Σ−1 𝑥−𝜇 =

= 2𝜋−𝑑2𝑑𝑒𝑡Σ−

12𝑒𝑥𝑝 −

1

2𝑥 − 𝜇 𝑇Σ−1 𝑥 − 𝜇

8

MLE example: multivariate

normal

Pavlyuk D. Computing the maximum likelihood estimates: concentrated likelihood, EM-algorithm, Riga, 13.05.2016

The log-likelihood function:

𝑙𝑚𝑣𝑛 𝜇, Σ 𝑥 =

𝑖=1

𝑛

𝑙𝑛𝜑 𝑥𝑖 , 𝜇, Σ =

= −𝑛𝑑

2𝑙𝑛 2𝜋 −

𝑛

2ln 𝑑𝑒𝑡Σ −

1

2

𝑖=1

𝑛

𝑥𝑖 − 𝜇 𝑇Σ−1 𝑥𝑖 − 𝜇

FOC:

𝜕𝑙𝑚𝑣𝑛 𝜇, Σ 𝑥𝜕𝜇

= 0

𝜕𝑙𝑚𝑣𝑛 𝜇, Σ 𝑥𝜕Σ

= 0

9

MLE example: multivariate

normal

Pavlyuk D. Computing the maximum likelihood estimates: concentrated likelihood, EM-algorithm, Riga, 13.05.2016

Matrix calculus (for symmetric A):

𝜕𝐵𝑇𝐴𝐵

𝜕𝐵= 2𝐵𝑇𝐴

𝜕 ln 𝑑𝑒𝑡𝐴

𝜕𝐴= 𝐴−1

10

MLE example: multivariate

normal

Pavlyuk D. Computing the maximum likelihood estimates: concentrated likelihood, EM-algorithm, Riga, 13.05.2016

𝜕𝑙𝑚𝑣𝑛 𝜇, Σ 𝑥

𝜕𝜇=

=𝜕 −

𝑛𝑑2 𝑙𝑛 2𝜋 −

𝑛2 ln 𝑑𝑒𝑡Σ −

12

σ𝑖=1𝑛 𝑥𝑖 − 𝜇 𝑇Σ−1 𝑥𝑖 − 𝜇

𝜕𝜇

=

𝑖=1

𝑛

𝑥𝑖 − 𝜇 𝑇Σ−1

Setting this to zero we obtain the pleasant result

Ƹ𝜇 Σ =1

𝑛

𝑖=1

𝑛

𝑥𝑖 = ҧ𝑥

11

MLE example: multivariate

normal

Pavlyuk D. Computing the maximum likelihood estimates: concentrated likelihood, EM-algorithm, Riga, 13.05.2016

𝜕𝑙𝑚𝑣𝑛 𝜇, Σ 𝑥

𝜕Σ=

=𝜕 −

𝑛𝑑2 𝑙𝑛 2𝜋 −

𝑛2 ln 𝑑𝑒𝑡Σ −

12

σ𝑖=1𝑛 𝑥𝑖 − 𝜇 𝑇Σ−1 𝑥𝑖 − 𝜇

𝜕Σ

=𝑛

2Σ−1 −

1

2

𝑖=1

𝑛

Σ−1 𝑥𝑖 − 𝜇 𝑥𝑖 − 𝜇 𝑇Σ−1

Setting this to zero we obtain the result

Σ =1

𝑛

𝑖=1

𝑛

𝑥𝑖 − 𝜇 𝑥𝑖 − 𝜇 𝑇

12

Pavlyuk D. Computing the maximum likelihood estimates: concentrated likelihood, EM-algorithm, Riga, 13.05.2016 13

2. Pseudo-likelihood

Pseudo-likelihood

Pavlyuk D. Computing the maximum likelihood estimates: concentrated likelihood, EM-algorithm, Riga, 13.05.2016

There are a number of suggestions for modifying the likelihood function to extract the evidence in the sample concerning a parameter of interest θA when

θ = (θA, θB).

The sample vector x is also transformed into 2 parts:

𝑥 ՜ 𝑠 = 𝑠𝐴, 𝑠𝐵

Such modifications are generally known as pseudo-likelihood functions:

• Conditional likelihood

• Marginal likelihood

• Concentrated (profile) likelihood14

Marginal likelihood

Pavlyuk D. Computing the maximum likelihood estimates: concentrated likelihood, EM-algorithm, Riga, 13.05.2016

Marginal likelihood function:

𝑓 𝑋, 𝜃 = 𝑓𝑠,𝜃 𝑠𝐴, 𝑠𝐵 , 𝜃𝐴, 𝜃𝐵 =

= 𝒇𝒎𝒂𝒓𝒈𝒊𝒏𝒂𝒍,𝑨 𝒔𝑨 𝜽𝑨 ∙ 𝑓𝑚𝑎𝑟𝑔𝑖𝑛𝑎𝑙,𝐵 𝑠𝐵 𝑠𝐴, 𝜃𝐴, 𝜃𝐵

Maximum likelihood estimates for θA are obtained by maximizing the marginal density:

𝑓𝑚𝑎𝑟𝑔𝑖𝑛𝑎𝑙,𝐴 𝑠𝐴 𝜃𝐴

Problems:

• Ignoring some of the data

• Require analytical forms of the functions 15

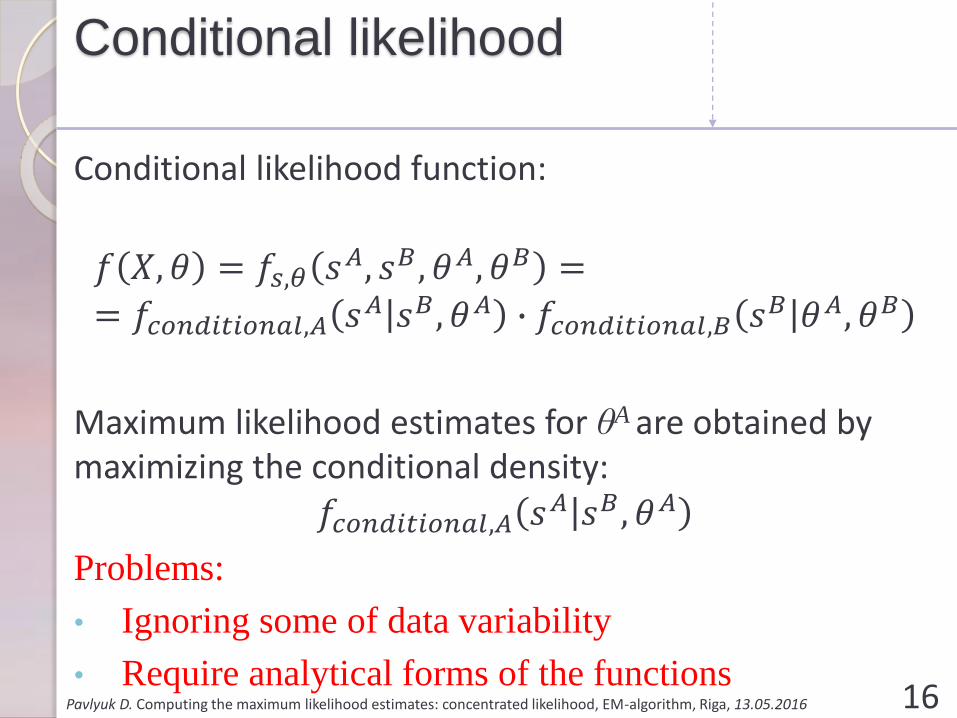

Conditional likelihood

Pavlyuk D. Computing the maximum likelihood estimates: concentrated likelihood, EM-algorithm, Riga, 13.05.2016

Conditional likelihood function:

𝑓 𝑋, 𝜃 = 𝑓𝑠,𝜃 𝑠𝐴, 𝑠𝐵 , 𝜃𝐴, 𝜃𝐵 =

= 𝑓𝑐𝑜𝑛𝑑𝑖𝑡𝑖𝑜𝑛𝑎𝑙,𝐴 𝑠𝐴 𝑠𝐵 , 𝜃𝐴 ∙ 𝑓𝑐𝑜𝑛𝑑𝑖𝑡𝑖𝑜𝑛𝑎𝑙,𝐵 𝑠𝐵 𝜃𝐴, 𝜃𝐵

Maximum likelihood estimates for θA are obtained by maximizing the conditional density:

𝑓𝑐𝑜𝑛𝑑𝑖𝑡𝑖𝑜𝑛𝑎𝑙,𝐴 𝑠𝐴 𝑠𝐵 , 𝜃𝐴

Problems:

• Ignoring some of data variability

• Require analytical forms of the functions16

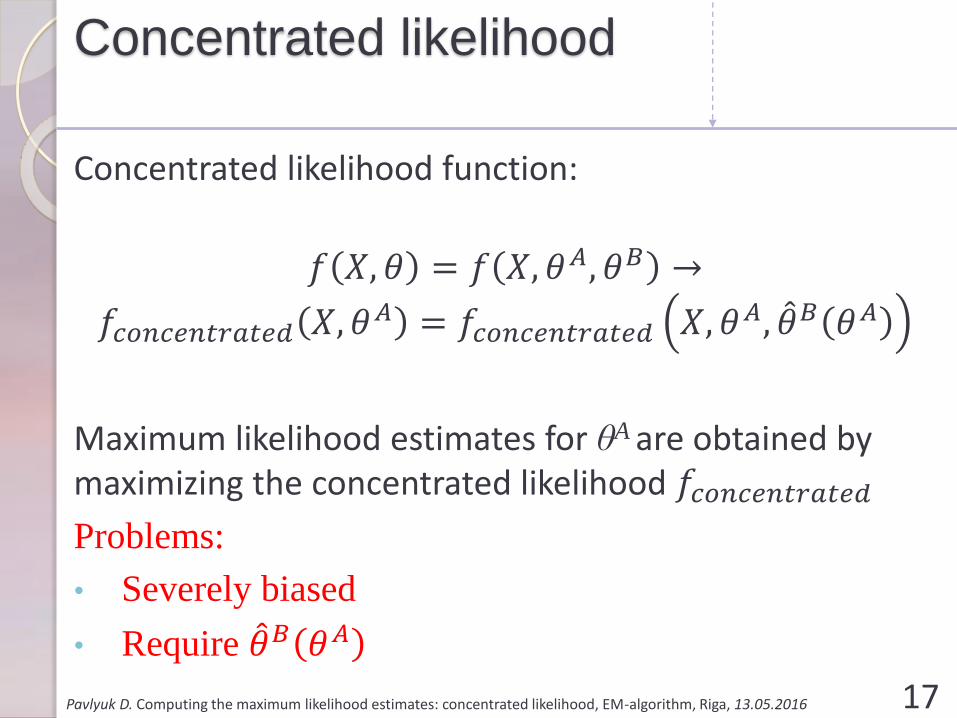

Concentrated likelihood

Pavlyuk D. Computing the maximum likelihood estimates: concentrated likelihood, EM-algorithm, Riga, 13.05.2016

Concentrated likelihood function:

𝑓 𝑋, 𝜃 = 𝑓 𝑋, 𝜃𝐴, 𝜃𝐵 ՜

𝑓𝑐𝑜𝑛𝑐𝑒𝑛𝑡𝑟𝑎𝑡𝑒𝑑 𝑋, 𝜃𝐴 = 𝑓𝑐𝑜𝑛𝑐𝑒𝑛𝑡𝑟𝑎𝑡𝑒𝑑 𝑋, 𝜃𝐴, መ𝜃𝐵 𝜃𝐴

Maximum likelihood estimates for θA are obtained by maximizing the concentrated likelihood 𝑓𝑐𝑜𝑛𝑐𝑒𝑛𝑡𝑟𝑎𝑡𝑒𝑑

Problems:

• Severely biased

• Require መ𝜃𝐵 𝜃𝐴

17

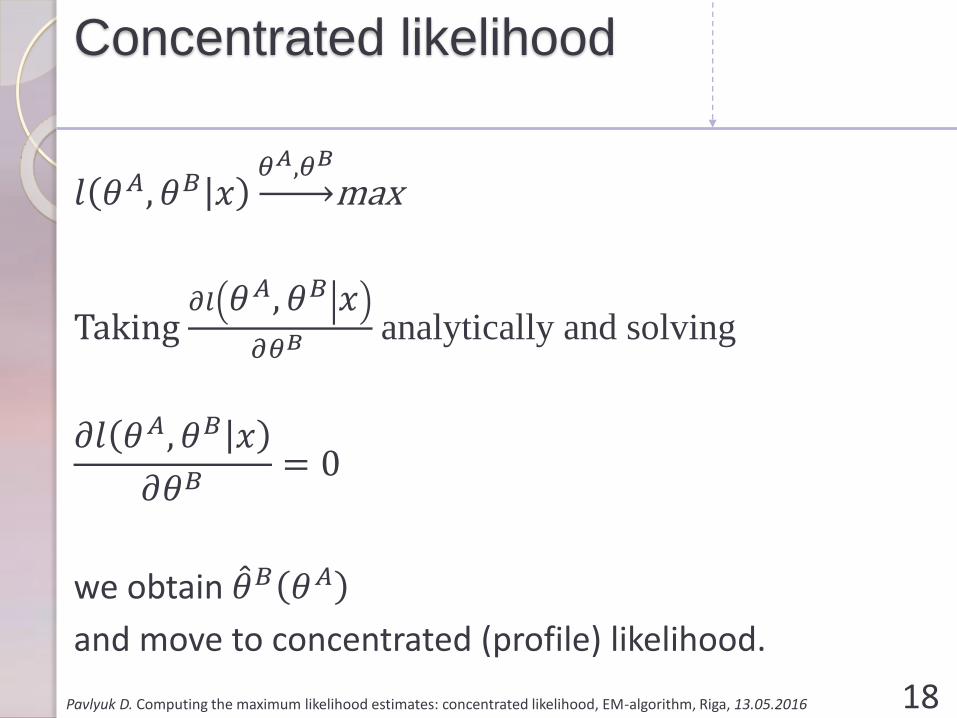

Concentrated likelihood

Pavlyuk D. Computing the maximum likelihood estimates: concentrated likelihood, EM-algorithm, Riga, 13.05.2016

𝑙 𝜃𝐴, 𝜃𝐵 𝑥𝜃𝐴,𝜃𝐵

max

Taking 𝜕𝑙 𝜃𝐴, 𝜃𝐵 𝑥

𝜕𝜃𝐵 analytically and solving

𝜕𝑙 𝜃𝐴, 𝜃𝐵 𝑥

𝜕𝜃𝐵= 0

we obtain መ𝜃𝐵 𝜃𝐴

and move to concentrated (profile) likelihood.

18

Concentrated likelihood

Pavlyuk D. Computing the maximum likelihood estimates: concentrated likelihood, EM-algorithm, Riga, 13.05.2016

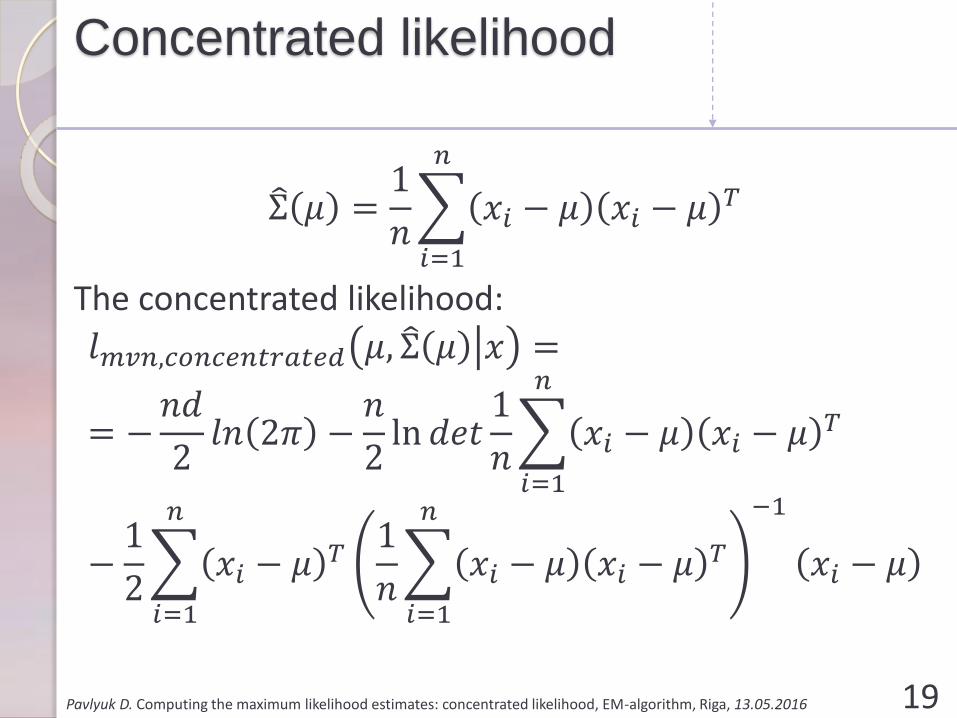

Σ 𝜇 =1

𝑛

𝑖=1

𝑛

𝑥𝑖 − 𝜇 𝑥𝑖 − 𝜇 𝑇

The concentrated likelihood:

𝑙𝑚𝑣𝑛,𝑐𝑜𝑛𝑐𝑒𝑛𝑡𝑟𝑎𝑡𝑒𝑑 𝜇, Σ 𝜇 𝑥 =

= −𝑛𝑑

2𝑙𝑛 2𝜋 −

𝑛

2ln 𝑑𝑒𝑡

1

𝑛

𝑖=1

𝑛

𝑥𝑖 − 𝜇 𝑥𝑖 − 𝜇 𝑇

−1

2

𝑖=1

𝑛

𝑥𝑖 − 𝜇 𝑇1

𝑛

𝑖=1

𝑛

𝑥𝑖 − 𝜇 𝑥𝑖 − 𝜇 𝑇

−1

𝑥𝑖 − 𝜇

19

Concentrated likelihood

Pavlyuk D. Computing the maximum likelihood estimates: concentrated likelihood, EM-algorithm, Riga, 13.05.2016

𝑙𝑚𝑣𝑛,𝑐𝑜𝑛𝑐𝑒𝑛𝑡𝑟𝑎𝑡𝑒𝑑 𝜇, Σ 𝜇 𝑥 =

= −𝑛

2𝑑 ∙ 𝑙𝑛 2𝜋 + ln 𝑑𝑒𝑡

𝑖=1

𝑛

𝑥𝑖 − 𝜇 𝑥𝑖 − 𝜇 𝑇 + 𝑑

ෝ𝜇 = argmin𝜇

ln 𝑑𝑒𝑡

𝑖=1

𝑛

𝑥𝑖 − 𝜇 𝑥𝑖 − 𝜇 𝑇

This result is quite famous in econometrics!

20

Pavlyuk D. Computing the maximum likelihood estimates: concentrated likelihood, EM-algorithm, Riga, 13.05.2016 21

3. Finite Mixture Models

Gaussian mixture model

Pavlyuk D. Computing the maximum likelihood estimates: concentrated likelihood, EM-algorithm, Riga, 13.05.2016

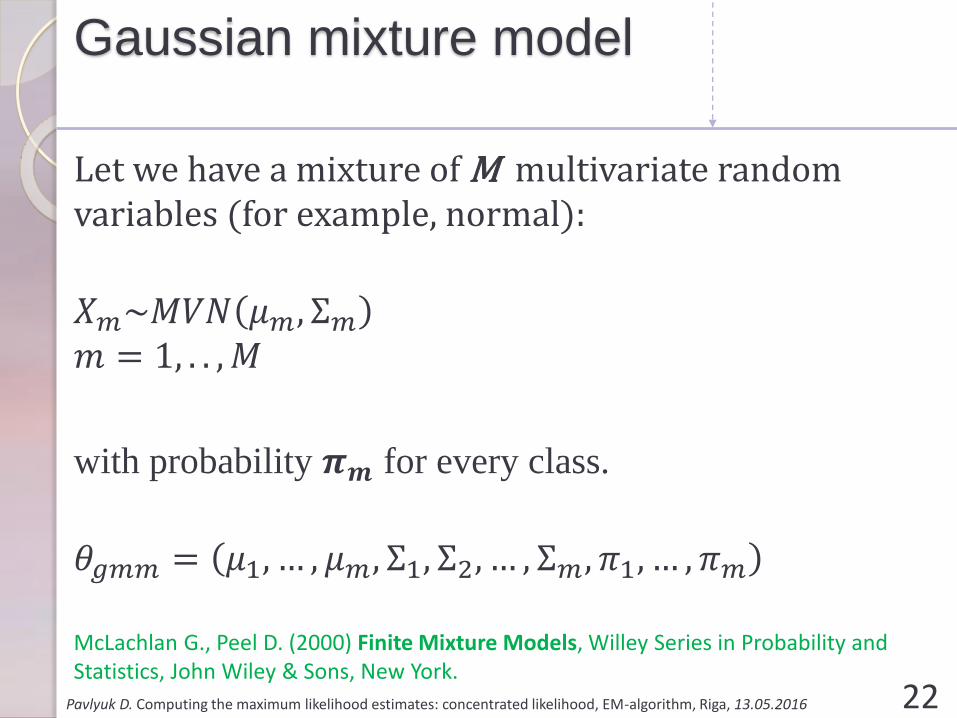

Let we have a mixture of M multivariate random variables (for example, normal):

𝑋𝑚~𝑀𝑉𝑁 𝜇𝑚, Σ𝑚

𝑚 = 1, . . , 𝑀

with probability 𝝅𝒎 for every class.

𝜃𝑔𝑚𝑚 = 𝜇1, … , 𝜇𝑚, Σ1, Σ2, … , Σ𝑚, 𝜋1, … , 𝜋𝑚

McLachlan G., Peel D. (2000) Finite Mixture Models, Willey Series in Probability and Statistics, John Wiley & Sons, New York.

22

Gaussian mixture model

Pavlyuk D. Computing the maximum likelihood estimates: concentrated likelihood, EM-algorithm, Riga, 13.05.2016

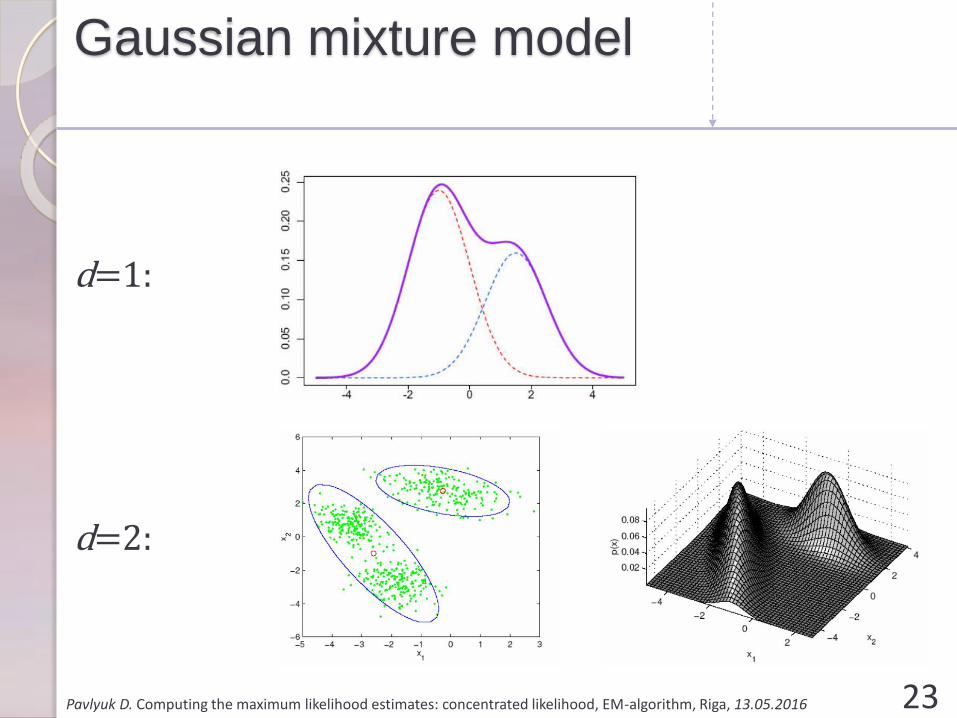

d=1:

d=2:

23

Gaussian mixture model

Pavlyuk D. Computing the maximum likelihood estimates: concentrated likelihood, EM-algorithm, Riga, 13.05.2016

• Medical applicationsSchlattmann P. (2009) Medical Applications of Finite Mixture Models, Statistics for Biology and Health, Springer

• Financial applicationsBrigo, D.; Mercurio, F. (2002). Lognormal-mixture dynamics and calibration to market volatility smiles

Alexander, C. (2004). "Normal mixture diffusion with uncertain volatility: Modelling short- and long-term smile effects"

• Image, speech, text recognitionStylianou, Y. etc. (2005). GMM-Based Multimodal Biometric Verification

Reynolds, D., Rose, R. (1995). Robust text-independent speaker identification using Gaussian mixture speaker models

Permuter, H.; Francos, J.; Jermyn, I.H. (2003). Gaussian mixture models of texture and colour for image database retrieval.

24

Gaussian mixture model

Pavlyuk D. Computing the maximum likelihood estimates: concentrated likelihood, EM-algorithm, Riga, 13.05.2016

Following the law of complete probability, the likelihood

function is

𝐿𝑔𝑚𝑚 𝜃𝑔𝑚𝑚 𝑥 = ෑ

𝑖=1

𝑛

𝑚=1

𝑀

𝜋𝑚𝜑 𝑥𝑖 , 𝜇𝑚, Σ𝑚

𝑙𝑔𝑚𝑚 𝜃𝑔𝑚𝑚 𝑥 = 𝑙𝑛𝐿𝑔𝑚𝑚 𝜃𝑔𝑚𝑚 𝑥 = 𝑙𝑛 ෑ

𝑖=1

𝑛

𝑚=1

𝑀

𝜋𝑚𝜑 𝑥𝑖 , 𝜇𝑚, Σ𝑚

=

𝑖=1

𝑛

𝑙𝑛 𝜋1𝜑 𝑥𝑖 , 𝜇1, Σ1 + ⋯ + 𝜋𝑚𝜑 𝑥𝑖 , 𝜇𝑚, Σ𝑚

The logarithm of sum prevents analytical derivatives!

25

Pavlyuk D. Computing the maximum likelihood estimates: concentrated likelihood, EM-algorithm, Riga, 13.05.2016 26

4. The Expectation-Maximization

algorithm

EM-algorithm

Pavlyuk D. Computing the maximum likelihood estimates: concentrated likelihood, EM-algorithm, Riga, 13.05.2016

The expectation-maximization (EM) algorithm is a general method for finding maximum likelihood estimates when there are missing values or latent variables.

In the mixture model context, the missing data is represented by a set of observations of a discrete random variable Z that indicates which mixture component generated the observation i.

𝑧𝑖𝑚 = ቊ1, 𝑖𝑓 𝑜𝑏𝑠𝑒𝑟𝑣𝑎𝑡𝑖𝑜𝑛 𝑖 𝑏𝑒𝑙𝑜𝑛𝑔𝑠 𝑡𝑜 𝑐𝑙𝑎𝑠𝑠 𝑚,

0, 𝑜𝑡ℎ𝑒𝑟𝑤𝑖𝑠𝑒

27

EM-algorithm: GMM

Pavlyuk D. Computing the maximum likelihood estimates: concentrated likelihood, EM-algorithm, Riga, 13.05.2016

𝑧𝑖𝑚 = ቊ1, 𝑖𝑓 𝑜𝑏𝑠𝑒𝑟𝑣𝑎𝑡𝑖𝑜𝑛 𝑖 𝑏𝑒𝑙𝑜𝑛𝑔𝑠 𝑡𝑜 𝑐𝑙𝑎𝑠𝑠 𝑚,

0, 𝑜𝑡ℎ𝑒𝑟𝑤𝑖𝑠𝑒

If Z = {zim} is given,

𝑙𝑔𝑚𝑚 𝜃𝑔𝑚𝑚 𝑥 =

𝑖=1

𝑛

𝑙𝑛 𝜋1𝜑 𝑥𝑖 , 𝜇1, Σ1 + ⋯ + 𝜋𝑚𝜑 𝑥𝑖 , 𝜇𝑚, Σ𝑚

transformed to

𝑙𝑔𝑚𝑚,𝑐𝑜𝑚𝑝𝑙𝑒𝑡𝑒 𝜃𝑔𝑚𝑚 𝑥, 𝑍 =

𝑖=1

𝑛

𝑚=1

𝑀

𝑧𝑖,𝑚𝑙𝑛 𝜋𝑚𝜑 𝑥𝑖 , 𝜇𝑚, Σ𝑚 =

=

𝑖=1

𝑛

𝑚=1

𝑀

𝑧𝑖,𝑚 𝑙𝑛𝜋𝑚 + 𝑙𝑛𝜑 𝑥𝑖 , 𝜇𝑚, Σ𝑚

28

EM-algorithm

Pavlyuk D. Computing the maximum likelihood estimates: concentrated likelihood, EM-algorithm, Riga, 13.05.2016

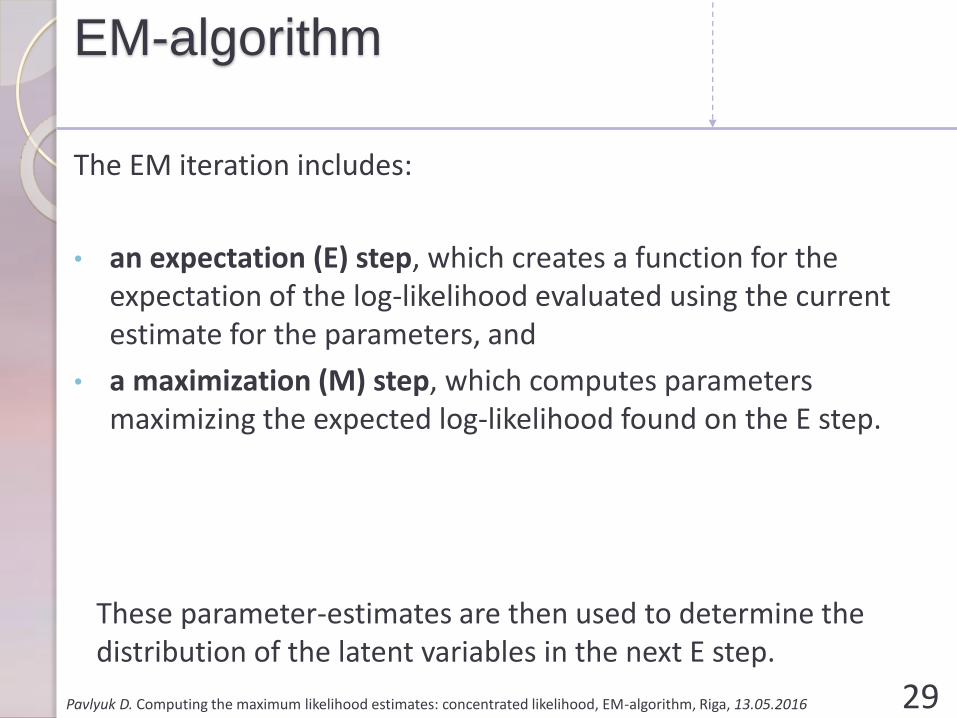

The EM iteration includes:

• an expectation (E) step, which creates a function for the expectation of the log-likelihood evaluated using the current estimate for the parameters, and

• a maximization (M) step, which computes parameters maximizing the expected log-likelihood found on the E step.

29

These parameter-estimates are then used to determine the distribution of the latent variables in the next E step.

EM-algorithm: GMM

Pavlyuk D. Computing the maximum likelihood estimates: concentrated likelihood, EM-algorithm, Riga, 13.05.2016

Assume 𝜃𝑔𝑚𝑚(0)

and move to maximization of the

expectation of the log-likelihood function:

𝐸𝑍 𝑙𝑔𝑚𝑚,𝑐𝑜𝑚𝑝𝑙𝑒𝑡𝑒 𝜃𝑔𝑚𝑚(0)

𝑥, 𝑍

=

𝑖=1

𝑛

𝑚=1

𝑀

𝐸𝑍 𝑧𝑖,𝑚 𝜃𝑔𝑚𝑚(0)

𝑙𝑛𝜋𝑚 + 𝑙𝑛𝜑 𝑥𝑖 , 𝜇𝑚, Σ𝑚

30

EM-algorithm: E-step

Pavlyuk D. Computing the maximum likelihood estimates: concentrated likelihood, EM-algorithm, Riga, 13.05.2016

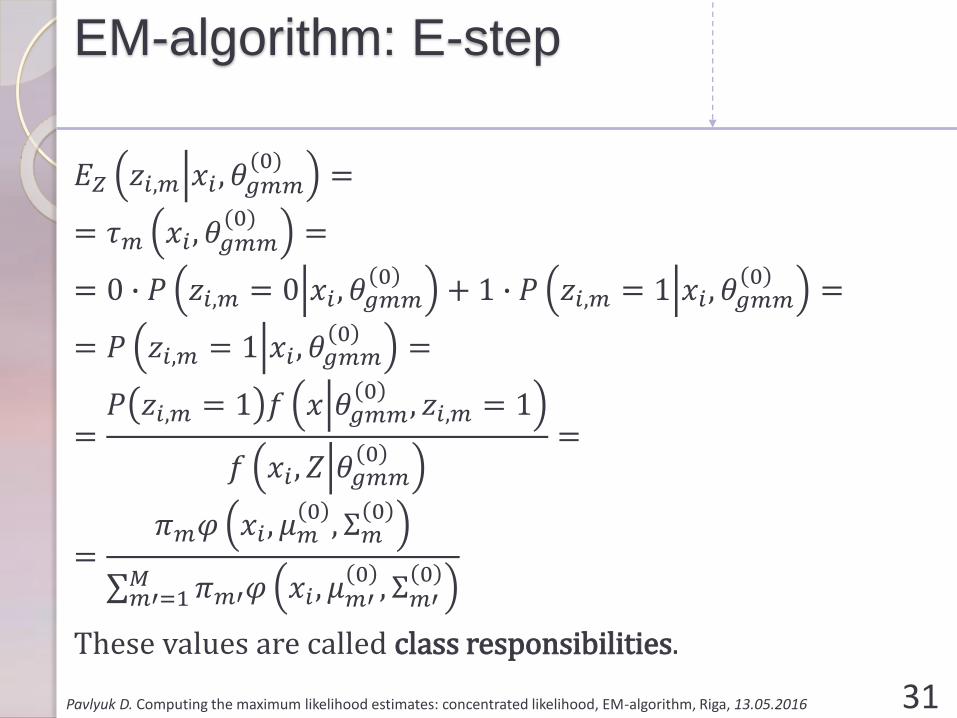

𝐸𝑍 𝑧𝑖,𝑚 𝑥𝑖 , 𝜃𝑔𝑚𝑚(0)

=

= 𝜏𝑚 𝑥𝑖 , 𝜃𝑔𝑚𝑚(0)

=

= 0 ∙ 𝑃 𝑧𝑖,𝑚 = 0 𝑥𝑖 , 𝜃𝑔𝑚𝑚0

+ 1 ∙ 𝑃 𝑧𝑖,𝑚 = 1 𝑥𝑖 , 𝜃𝑔𝑚𝑚0

=

= 𝑃 𝑧𝑖,𝑚 = 1 𝑥𝑖 , 𝜃𝑔𝑚𝑚0

=

=𝑃 𝑧𝑖,𝑚 = 1 𝑓 𝑥 𝜃𝑔𝑚𝑚

0, 𝑧𝑖,𝑚 = 1

𝑓 𝑥𝑖 , 𝑍 𝜃𝑔𝑚𝑚0

=

=𝜋𝑚𝜑 𝑥𝑖 , 𝜇𝑚

0, Σ𝑚

0

σ𝑚′=1𝑀 𝜋𝑚′𝜑 𝑥𝑖 , 𝜇𝑚′

0, Σ𝑚′

0

These values are called class responsibilities.

31

EM-algorithm: M-step

Pavlyuk D. Computing the maximum likelihood estimates: concentrated likelihood, EM-algorithm, Riga, 13.05.2016

𝐸𝑍 𝑙𝑔𝑚𝑚,𝑐𝑜𝑚𝑝𝑙𝑒𝑡𝑒 𝜃𝑔𝑚𝑚(0)

𝑥, 𝑍

=

𝑖=1

𝑛

𝑚=1

𝑀

𝜏𝑚 𝑥𝑖 , 𝜃𝑔𝑚𝑚(0)

𝑙𝑛𝜋𝑚 + 𝑙𝑛𝜑 𝑥𝑖 , 𝜇𝑚, Σ𝑚

FOC:

𝜕𝐸 𝑙𝑔𝑚𝑚,𝑐𝑜𝑚𝑝𝑙𝑒𝑡𝑒 𝜃𝑔𝑚𝑚(0)

𝑥, 𝑍

𝜕𝜇𝑚= 0,

𝜕𝐸 𝑙𝑔𝑚𝑚,𝑐𝑜𝑚𝑝𝑙𝑒𝑡𝑒 𝜃𝑔𝑚𝑚(0)

𝑥, 𝑍

𝜕Σ𝑚= 0,

𝜕𝐸 𝑙𝑔𝑚𝑚,𝑐𝑜𝑚𝑝𝑙𝑒𝑡𝑒 𝜃𝑔𝑚𝑚(0)

𝑥, 𝑍

𝜕𝜋𝑚= 0

32

EM-algorithm: M-step

Pavlyuk D. Computing the maximum likelihood estimates: concentrated likelihood, EM-algorithm, Riga, 13.05.2016

𝜕𝐸𝑍 𝑙𝑐𝑜𝑚𝑝𝑙𝑒𝑡𝑒 𝜃𝑔𝑚𝑚(0)

𝑥, 𝑍

𝜕𝜇𝑚=

𝑖=1

𝑛

𝜏𝑚 𝑥𝑖 , 𝜃𝑔𝑚𝑚(0) 𝜕𝜑 𝑥𝑖 , 𝜇𝑚, Σ𝑚

𝜕𝜇𝑚

=

𝑖=1

𝑛

𝜏𝑚 𝑥𝑖 , 𝜃𝑔𝑚𝑚(0)

𝑥𝑖 − 𝜇𝑚𝑇Σ−1 = 0

Ƹ𝜇𝑔𝑚𝑚,𝑚(1)

=σ𝑖=1

𝑛 𝜏𝑚 𝑥𝑖 , 𝜃𝑔𝑚𝑚(0)

𝑥𝑖

σ𝑖=1𝑛 𝜏𝑚 𝑥𝑖 , 𝜃𝑔𝑚𝑚

(0)

33

EM-algorithm: M-step

Pavlyuk D. Computing the maximum likelihood estimates: concentrated likelihood, EM-algorithm, Riga, 13.05.2016

𝜕𝐸𝑍 𝑙𝑐𝑜𝑚𝑝𝑙𝑒𝑡𝑒 𝜃𝑔𝑚𝑚(0)

𝑥, 𝑍

𝜕Σ𝑚=

𝑖=1

𝑛

𝜏𝑚 𝑥𝑖 , 𝜃𝑔𝑚𝑚(0) 𝜕𝜑 𝑥𝑖 , 𝜇𝑚, Σ𝑚

𝜕Σ𝑚=

=

𝑖=1

𝑛

𝜏𝑚 𝑥𝑖 , 𝜃𝑔𝑚𝑚(0) 𝑛

2Σ𝑚

−1 −1

2

𝑖=1

𝑛

Σ𝑚−1 𝑥𝑖 − 𝜇𝑚 𝑥𝑖 − 𝜇𝑚

𝑇Σ𝑚−1

Σ𝑔𝑚𝑚,𝑚(1)

=σ𝑖=1

𝑛 𝜏𝑚 𝑥𝑖 , 𝜃𝑔𝑚𝑚(0)

𝑥𝑖 − Ƹ𝜇𝑔𝑚𝑚,𝑚(0)

𝑥𝑖 − ො𝜇𝑔𝑚𝑚,𝑚(0) 𝑇

σ𝑖=1𝑛 𝜏𝑚 𝑥𝑖 , 𝜃𝑔𝑚𝑚

(0)

34

EM-algorithm: M-step

Pavlyuk D. Computing the maximum likelihood estimates: concentrated likelihood, EM-algorithm, Riga, 13.05.2016

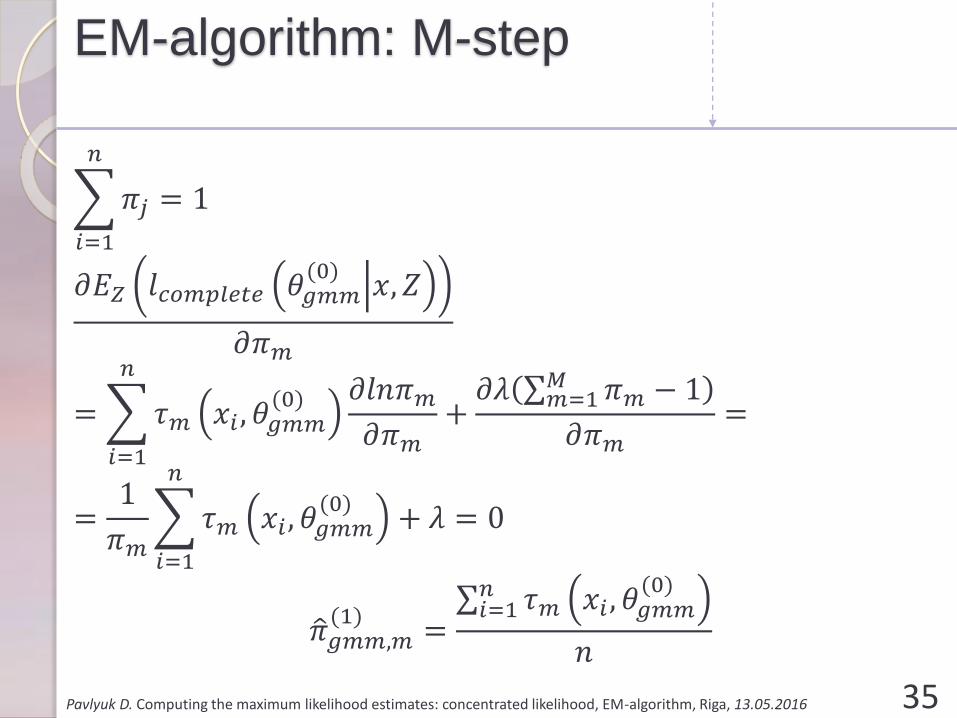

𝑖=1

𝑛

𝜋𝑗 = 1

𝜕𝐸𝑍 𝑙𝑐𝑜𝑚𝑝𝑙𝑒𝑡𝑒 𝜃𝑔𝑚𝑚(0)

𝑥, 𝑍

𝜕𝜋𝑚

=

𝑖=1

𝑛

𝜏𝑚 𝑥𝑖 , 𝜃𝑔𝑚𝑚(0) 𝜕𝑙𝑛𝜋𝑚

𝜕𝜋𝑚+

𝜕𝜆 σ𝑚=1𝑀 𝜋𝑚 − 1

𝜕𝜋𝑚=

=1

𝜋𝑚

𝑖=1

𝑛

𝜏𝑚 𝑥𝑖 , 𝜃𝑔𝑚𝑚(0)

+ 𝜆 = 0

ො𝜋𝑔𝑚𝑚,𝑚(1)

=σ𝑖=1

𝑛 𝜏𝑚 𝑥𝑖 , 𝜃𝑔𝑚𝑚(0)

𝑛

35

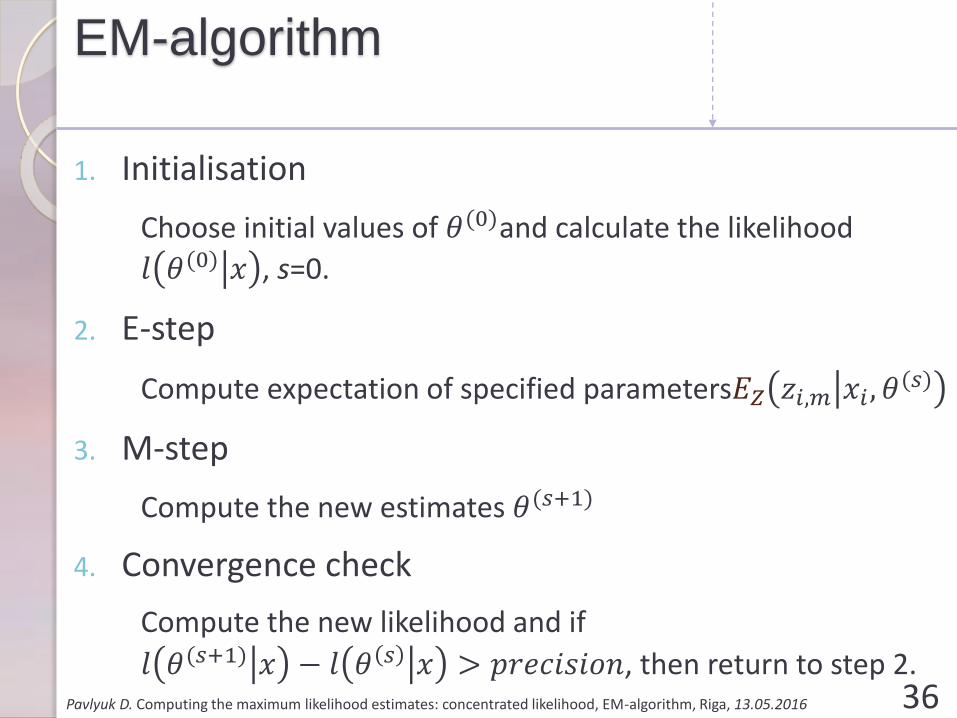

EM-algorithm

Pavlyuk D. Computing the maximum likelihood estimates: concentrated likelihood, EM-algorithm, Riga, 13.05.2016

1. Initialisation

Choose initial values of 𝜃(0)and calculate the likelihood

𝑙 𝜃(0) 𝑥 , s=0.

2. E-step

Compute expectation of specified parameters𝐸𝑍 𝑧𝑖,𝑚 𝑥𝑖 , 𝜃(𝑠)

3. M-step

Compute the new estimates 𝜃(𝑠+1)

4. Convergence check

Compute the new likelihood and if

𝑙 𝜃(𝑠+1) 𝑥 − 𝑙 𝜃 𝑠 𝑥 > 𝑝𝑟𝑒𝑐𝑖𝑠𝑖𝑜𝑛, then return to step 2.36

EM-algorithm

Pavlyuk D. Computing the maximum likelihood estimates: concentrated likelihood, EM-algorithm, Riga, 13.05.2016

Dempster, Laird, and Rubin (1977) show that the

likelihood function 𝑙 𝜃(𝑠) 𝑥 is not decreased after an

EM iteration; that is

𝑙 𝜃(𝑠+1) 𝑥 ≥ 𝑙 𝜃(𝑠) 𝑥

for s = 0,1,2, ....

See the proof in:McLachlan G.J., Krishnan T. (1997) The EM Algorithm and Extensions, Wiley. — 304 p.

37

Pavlyuk D. Computing the maximum likelihood estimates: concentrated likelihood, EM-algorithm, Riga, 13.05.2016 38

5. Numerical Example

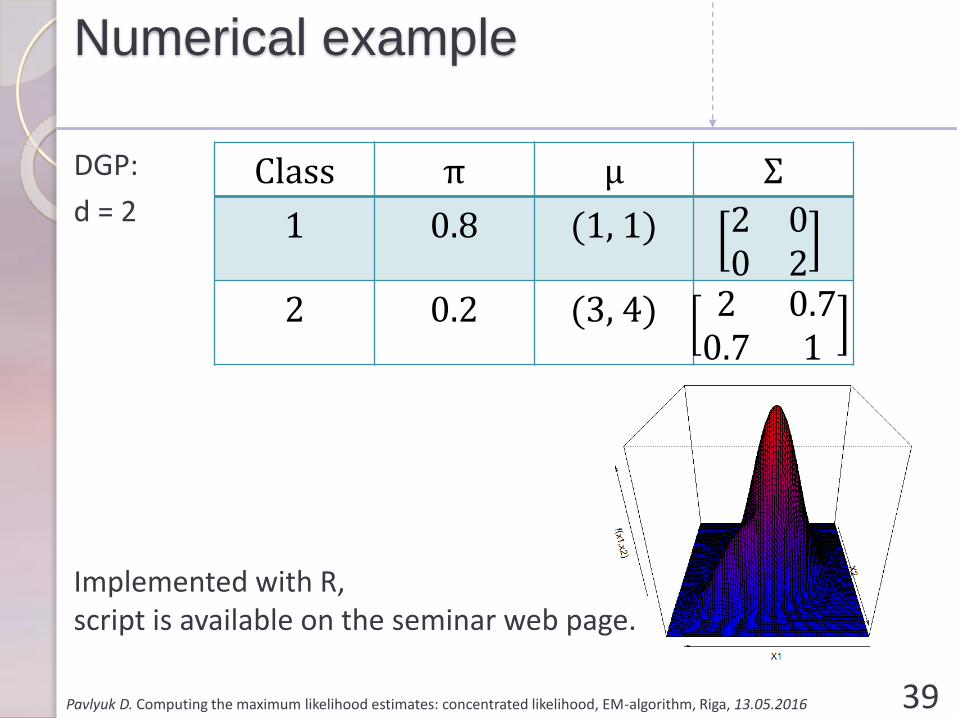

Numerical example

Pavlyuk D. Computing the maximum likelihood estimates: concentrated likelihood, EM-algorithm, Riga, 13.05.2016

DGP:

d = 2

Implemented with R,script is available on the seminar web page.

39

Class π μ Σ

1 0.8 (1, 1) 2 00 2

2 0.2 (3, 4) 2 0.70.7 1

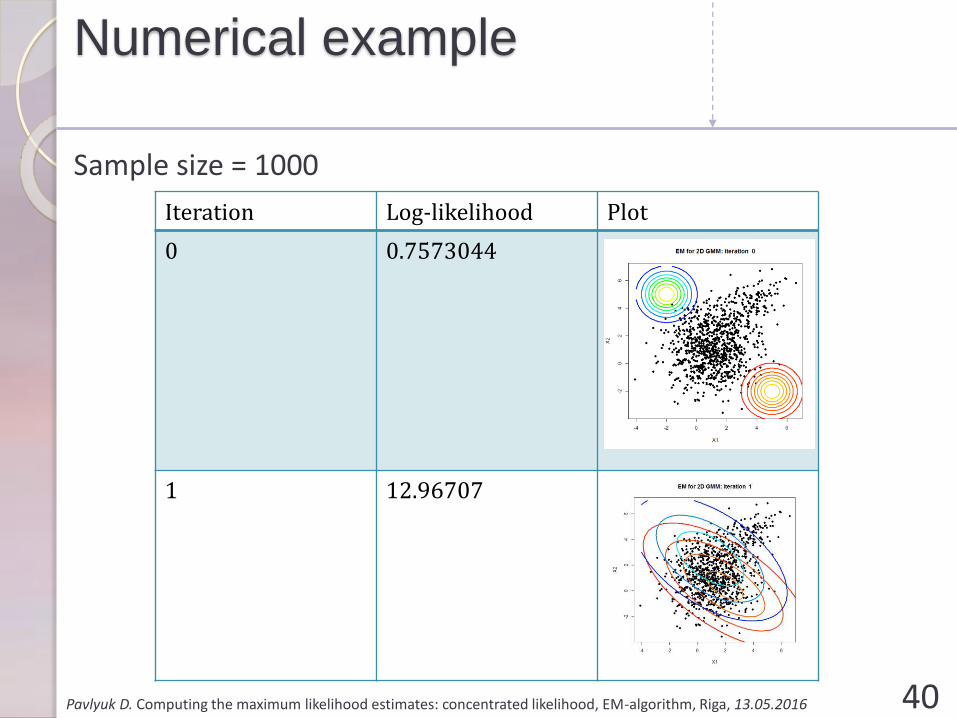

Numerical example

Pavlyuk D. Computing the maximum likelihood estimates: concentrated likelihood, EM-algorithm, Riga, 13.05.2016

Sample size = 1000

40

Iteration Log-likelihood Plot

0 0.7573044

1 12.96707

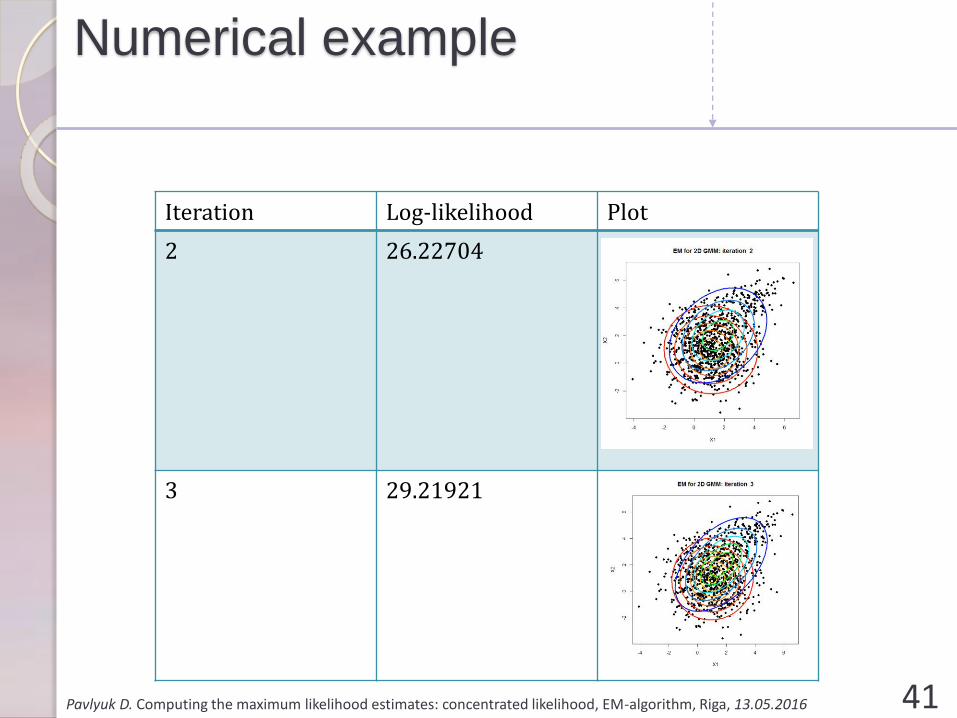

Numerical example

Pavlyuk D. Computing the maximum likelihood estimates: concentrated likelihood, EM-algorithm, Riga, 13.05.2016 41

Iteration Log-likelihood Plot

2 26.22704

3 29.21921

Numerical example

Pavlyuk D. Computing the maximum likelihood estimates: concentrated likelihood, EM-algorithm, Riga, 13.05.2016 42

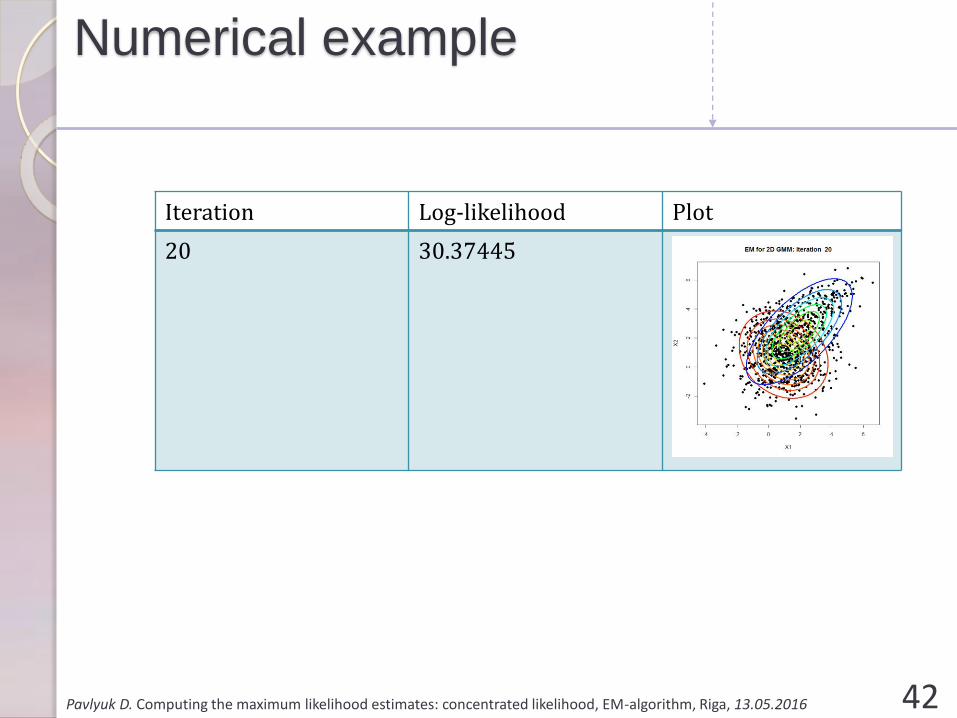

Iteration Log-likelihood Plot

20 30.37445

Numerical example

Pavlyuk D. Computing the maximum likelihood estimates: concentrated likelihood, EM-algorithm, Riga, 13.05.2016 43

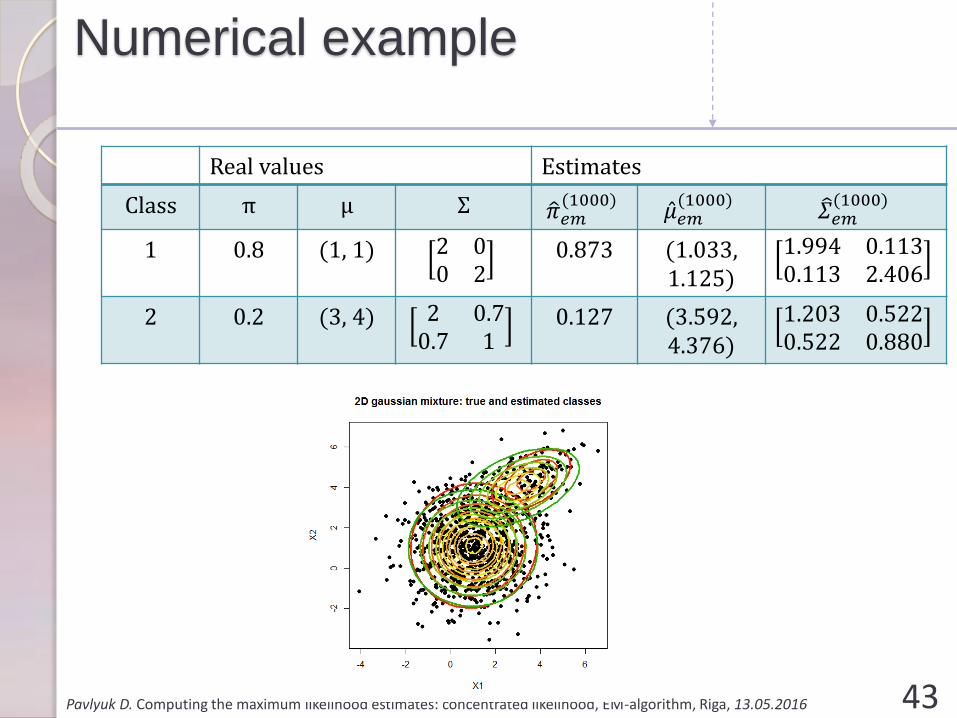

Real values Estimates

Class π μ Σ ො𝜋𝑒𝑚(1000)

Ƹ𝜇𝑒𝑚(1000) 𝛴𝑒𝑚

(1000)

1 0.8 (1, 1) 2 00 2

0.873 (1.033, 1.125)

1.994 0.1130.113 2.406

2 0.2 (3, 4) 2 0.70.7 1

0.127 (3.592, 4.376)

1.203 0.5220.522 0.880

Problems with EM

Pavlyuk D. Computing the maximum likelihood estimates: concentrated likelihood, EM-algorithm, Riga, 13.05.2016

• Local maxima

• partially solved with careful (repetitive) initial values selection

• Slow convergence (in some cases)

• Meta-algorithm

• should be adapted for every specific problem

• Singularities and over-fitting

44

After EM

Pavlyuk D. Computing the maximum likelihood estimates: concentrated likelihood, EM-algorithm, Riga, 13.05.2016

Next step:

Variational Bayes

• treat all parameters θ as missing variables

• iterate over components of missing variables (including θ) and recalculate its expectation

45

Recommended literature

Pavlyuk D. Computing the maximum likelihood estimates: concentrated likelihood, EM-algorithm, Riga, 13.05.2016

• McLachlan G., Krishnan T. (2008) The EM Algorithm and Extensions, Wiley Series in Probability and Statistics, 2nd Edition, - 400 p.

• McLachlan G., Peel D. (2000) Finite Mixture Models, Willey Series in Probability and Statistics, John Wiley & Sons, New York

• Gelman A., Carlin J., Stern H., Dunson D., Vehtari A., Rubin D. Bayesian Data Analysis, Third Edition (Chapman & Hall/CRC Texts in Statistical Science) http://www.stat.columbia.edu/~gelman/book/

46

Thank you for your attention!

Questions are very appreciated

Contacts:

email: [email protected]

phone: +37129958338