comprehensive financial plan for Advocis capstone

46

Comprehensive Financial Plan Young Couple Planning a Family Case Study Prepared by: <Steven M.J. McNulty> <Advocis #2088334> <Mar 25/2013> Capstone Comprehensive Financial Plan 1

-

Upload

steven-mj-mcnulty-fpsc-level-1-certificant -

Category

Documents

-

view

94 -

download

0

Transcript of comprehensive financial plan for Advocis capstone

Comprehensive Financial Plan Young Couple Planning a Family

Case Study

Prepared by:

<Steven M.J. McNulty><Advocis #2088334>

<Mar 25/2013>

Capstone Comprehensive Financial Plan 1

COMPREHENSIVE FINANCIAL PLAN – Step 1The FIRST step is to ESTABLISH THE CLIENT ENGAGEMENT in order to define the terms of the engagement.

Since this step is covered on pages 18 and 19 of the “Financial Planning Case Studies” text, you are not required to complete this section.

COMPREHENSIVE FINANCIAL PLAN – Step 2 15%The SECOND step is to identify and prioritize the client’s goals, objectives, needs, and values that have financial implications

DATA GATHERING

Goals and Objectives

After sitting down with both of you, I have outlined and prioritized your goals & objectives from the short term (0-2 yrs), medium term (3-5 yrs), and long term (6+ yrs) and attached a financial cost associated with each. The purpose of this financial plan is to formulate strategies to allow you to meet your short-term, medium-term and long-term goals and objectives, or as many of your most important goals and objectives as are feasible in your situation. The first step in that process is the identification and prioritization of these goals and objectives.

1. Finish basement at $6,000/yr for the next 2 years (short term)2. Add an ongoing expense of $4,000/yr for minor house repairs (short term)3. Purchase business from father for $100,000 at $10,000/yr for 10 years in next 2

years (short term) – there is flexibility on payment schedule

1. Start family - 1st child born at age 31 (med term)

1. Continue family - 2nd child born at age 34 (long term)2. Replace car every 6 years starting Jan 1, 2018 at a cost of $15,000 in today’s dollars

(long term)3. Pay the mortgage off by age 40 (long term)4. Retire by age 55 with retirement expenses of $60,000/yr in today’s dollars (long

term)

To further assist with the financial management analysis I will need: complete records of all bank statements domestic and abroad along with all registered/non registered accounts; All life insurance policies, group or otherwise; All wills and power of attorneys; names of all other professionals that you are dealing with; All pension information, present and from previous employers; A list of all assets, and liabilities.

It’s important to remember and understand that this financial plan is largely dependent upon the information you have provided to us, and on a number of assumptions, such as investment returns, tax and inflation rates. The plan must therefore be viewed as an educated estimate of your future situation. You should also consider that your ability to achieve these objectives will be influenced by several factors (not all captured in the financial plan), such as:

Your capacity, as a couple, to earn and save income between now and the date of your retirement (s)

The ability of your investment assets to earn income and/or grow in capital value between now and the date of your retirement, and for the duration of your retirement

Unexpected shifts between your desired asset mix and your actual asset mix due to market fluctuations and corrections

Your income sources and the continuation of government programs available in retirement

Capstone Comprehensive Financial Plan 3

The impact of factors such as inflation, long-term care costs and/or living longer than anticipated

The effect of lower than expected rates of return

The overall direction of your financial plan will be designed to assist you to move from where you are financially today to where you wish to be when you retire.

ASSUMPTIONS

This financial plan is predicted on a number of assumptions that will be used throughout the plan regarding your attitudes towards saving, investing and risk management. Additionally, assumptions are incorporated about the anticipated financial environment in which you will operate over the long-term. These assumptions may have to be adjusted over time as changing circumstances warrant, but the following are the assumptions upon which the plan is currently based. The following assumptions were provided by you through our interview, with the exception of inflation, this we had to agree on as well as the life expectancy of 90 and a return on registered investments of 7% for Chris and 5%/6% for Natalie.

Attitudes toward saving

To date, you have been able to accumulate over $45,000 ($65,000 if you include the HBP loan that has to be paid back) in investment assets (registered) in addition to the $232,000 of net equity in your home for a total net worth of roughly $278,000/298,000. This would indicate a fairly consistent, long term commitment to savings.

Risk Tolerance

Taking into consideration the financial relationship that Chris and I have had over the last seven years (since Chris was 20) and your current asset mix (90% equities, 10% fixed income-Chris and 55% equities, 45% fixed income-Natalie)) used in your registered accounts, over and above the equity in your home would fit the profile of an investor with above-average knowledge when it comes to investing and is comfortable riding out varying degrees of volatility over time. Natalie, on the other hand, is not quite as sophisticated an investor as Chris, although she is not far behind, as she attends the meetings between myself and Chris and has average knowledge of capital markets. I have labeled Chris’s investor profile as Growth +, while Natalie has been determined to be Balanced Growth.

Investment Returns

Your future investment income and growth are computed using the following rates of return, which are historically supportable, based on returns incurred In similar investments over the past five years:

Savings accounts – 0.60% Money market funds – 2.0% GIC’s – 2.8% (1 year) Individual equities – 7.00% (net of MER’s) Balanced funds – 5.55% Equity funds – 6.15% A (Growth +) investment portfolio – 7.00%

Capstone Comprehensive Financial Plan 4

A ( Balanced Growth) investment portfolio – 5.00%

Inflation

Inflation is currently running at 2.25% which is below the historical average, this should be fairly accurate as the Bank of Canada likes to keep inflation around the 2% mark. This will be the assumed rate and it will remain constant throughout the duration of the financial plan.

Some general assumptions used throughout financial plan:

Current age for Chris is 27 and Natalie is 27 as of Jan 1, 2013 Both Chris and Natalie want to retire at age 55 with retirement income of $60,000/yr

in today’s dollars Life expectancy of 90 We will use 3 time horizons 1. Age 27-55 (accumulation phase) 2. Age 56-70

(retirement is before regular age, R.R.S.P. conversion time, income gap). Age 71-90 (payout phase) will be updated with each new addition to the household (child, divorce or death in family)

C.P.P. drawings starting at age 60, with O.A.S. starting at age 67 Using a 7% return on registered investments for Chris and a 5 to 6% return on

registered investments for Natalie, 2% return on cash & equivalents Inflation of 2.25% Income tax is calculated as follows:

Income Tax AssumptionsThe first year tax calculations are based on the current CRA T1 schedule.The tax calculations beyond the first year of the projections are based on the current CRA

T1

schedule with the following assumptions:

- Tax brackets and other income thresholds are indexed at inflation

Unused TFSA room is $24,500 for Chris and $25,500 for Natalie Unused R.R.S.P. room is $18,712 for Chris and $ 7,133 for Natalie after her PA

adjustment for prior year Home buyers plan needs to start being repaid by march of 2014 at $1,333/yr for 15

yrs (which will be added to the $2220 already deposited, or elected to be part of the $2,220 already deposited )

Income from 2012 is $38,000 for Chris and $64,000 for Natalie Lifestyle expense from 2012 is $56,952 Natalie has group life (1x her salary) and disability(ST and LT) through her work and

both Chris and Natalie have health care through her employer Retirement date of Jan 1, 2041 at age 55 Added expense of $4,000/yr for minor home repairs Added expense of $10,000/yr starting 2015 for 10 year duration for purchase of

family business Will have to increased mortgage expense from $815/m to $1,166/m to pay off

mortgage by age 40 Start saving half of disposable income after mortgage and business paid off (aprox

age 41)

Capstone Comprehensive Financial Plan 5

Child 1 added on Jan 1, 2016 (age 31) Child 1 daycare (Jan 1, 2017-dec 31,2020) $1,200/m today’s dollars Child 1 pre-school (Jan 1,2021-dec 31,2022) $800/m today’s dollars Child 2 added on Jan 1, 2019 (age 34) Child 2 daycare (Jan 1,2020-dec 31,2023) $1,200/m today’s dollars Child 2 pre-school (Jan 1,2024-dec 31, 2025) $800/m today’s dollars includes reduced salary for 27 weeks (84%) in 2016 and 2019 for each tear of birth

in today’s dollars Includes EI maternity ad and parental benefits of $485/w paid for 23 weeks in 2016

and 2019 in today’s dollars Purchase of car in 6 years for $15,000 (Jan1, 2018) and every 6 years thereafter in

today’s dollars Plan for retirement expenses of $60,000/yr in today’s dollars

Capstone Comprehensive Financial Plan 6

COMPREHENSIVE FINANCIAL PLAN – Step 3 25%The THIRD step is to gather the necessary quantitative and qualitative information.

Financial Management

Through the information provided from our previous discussions, I have prepared the following statement of annual income and expenses for 2013 through 2022. The salary income projections have been indexed based on inflation of 2.25% while investment income and most expenses are indexed based on the assumptions listed on the previous page.

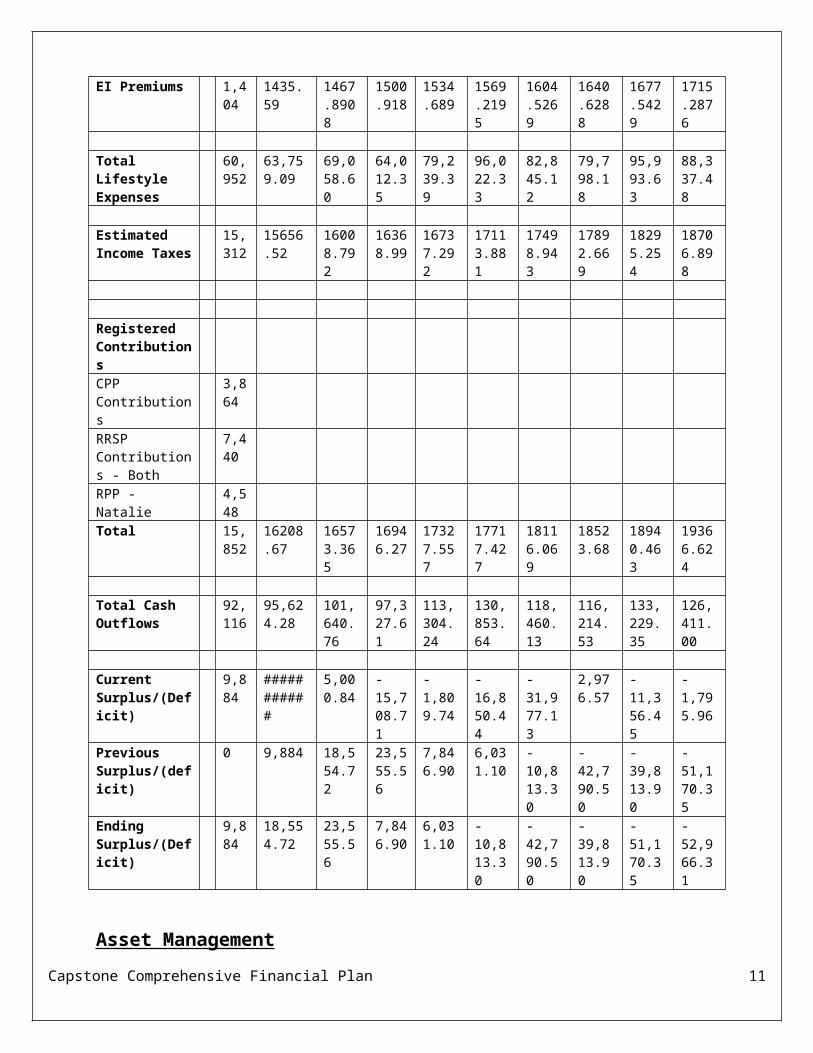

Family Cash Flow (next 10 years)

2013

2014 2015 2016 2017 2018 2019 2020 2021 2022

Cash Inflows

Employment IncomeSalary-Chris 38,0

0038,855 39,72

940,623.20

41,537.20

42,471.80

43,427.40

44,404.60

Salary-Natalie 64,000

65,440 66,912.40

40,995.70

69,957.30

71,531.40

43,055.60

74,786.50

Total Cash Inflows

102,000

104,295

106,641.60

81,618.90

111,494.50

114,003.20

86,483.00

119,191.10

121,872.90

124,615.04

Cash Outflows

Lifestyle ExpensesHousingMortgage (principal & interest)

9,780

Property taxes 3,396

Home insurance

936

Electricity 2,160

Gas 3,600

Home phone 1,020

Cell phone 1,200

Cable TV 480Internet 300Small home 4,00

Capstone Comprehensive Financial Plan 7

repairs 0Basement Reno (next 2 years)

6,000

6,000

Total Housing 32,872

33,611.60

28,232.90

28,868.10

29,517.70

30,181.80

30,860.90

31,552.30

32262.227

32988.127

FoodGroceries 4,80

0Lunch 120Alcohol 108Restaurant 192Total food 5,22

05,337.50

5,457.50

5,580.30

5,705.90

5,834.30

5,965.50

6,099.80

6237.0455

6377.379

TransportationInsurance 2,04

0Registration 120Gas 2,40

0Parking 240Repairs 960Car replacement

15,000

Total transportation

5,760

5,889.60

6,022.10

6,157.60

6,296.20

21,438

6,582.70

6,730.80

6882.243

7037.0935

LeisureSports club 264Lottery 144Vacation 2,40

0Gifts 804Newspapers 120Computer 120Total Leisure 3,85

23,938.70

4,027.30

4,117.90

4,210.60

4,305.30

4,402.20

4,501.20

4602.477

4706.0327

Health & InsuranceMortgage insurance (life/DI/CI)

720

Prescription drug/health care

240

Dental care 240Total health & Insurance

1,200

1227 1254.6075

1282.836

1311.7

1341.2132

1371.3905

1402.2468

1433.7974

1466.0578

Capstone Comprehensive Financial Plan 8

MiscellaneousClothing 756Furniture/appliances

1,980

Professional fees

504

Hair & skin care 1,008

Student loan (next 3.13 years)

7,200

7,200 7,200 600

Buying business

10,000

10,000

10,000

10,000

10,000

10,000

10,000

10,000

Other 600Child care - early year care

14,400

14,400

14,400

14,400

14,400

Child care - later year care

9,600 9,600

Total miscellaneous

12,048

12,319.10

22,596.30

16,504.70

30,662.60

31,352.50

32,057.90

27,871.20

42,898.30

34,047.50

EI Premiums 1,404

1435.59

1467.8908

1500.918

1534.689

1569.2195

1604.5269

1640.6288

1677.5429

1715.2876

Total Lifestyle Expenses

60,952

63,759.09

69,058.60

64,012.35

79,239.39

96,022.33

82,845.12

79,798.18

95,993.63

88,337.48

Estimated Income Taxes

15,312

15656.52

16008.792

16368.99

16737.292

17113.881

17498.943

17892.669

18295.254

18706.898

Registered ContributionsCPP Contributions

3,864

RRSP Contributions - Both

7,440

RPP - Natalie 4,548

Total 15,852

16208.67

16573.365

16946.27

17327.557

17717.427

18116.069

18523.68

18940.463

19366.624

Total Cash Outflows

92,116

95,624.28

101,640.76

97,327.61

113,304.24

130,853.64

118,460.13

116,214.53

133,229.35

126,411.00

Current Surplus/(Deficit)

9,884

###########

5,000.84

-15,708.71

-1,809.74

-16,850.44

-31,977.13

2,976.57

-11,356.45

-1,795.96

Previous 0 9,884 18,55 23,5 7,846. 6,031. - - - -

Capstone Comprehensive Financial Plan 9

Surplus/(deficit)

4.72 55.56

90 10 10,813.30

42,790.50

39,813.90

51,170.35

Ending Surplus/(Deficit)

9,884

18,554.72

23,555.56

7,846.90

6,031.10

-10,813.30

-42,790.50

-39,813.90

-51,170.35

-52,966.31

Asset Management

Based on the information you provided through investment and RRSP statements, as well as completion of the financial planning questionnaire, I have complied the following statement of your current assets and liabilities:

Net Worth (as of January 1, 2013)

Chris Natalie TotalASSETSNon-Registered AssetsChequing Account - joint 4,813 4,813 9,626Chequing Account - Natalie 10,000 10,000

Total Non-Registered Assets 19,626

Registered AssetsTFSA* Investment savings account 1,000 1,000RRSP* Balanced diversified fund 12,768 12,768* Equity strategic portfolio 32,694 32,694

Total Registered Assets 46,462

Principal Residence 350,000 350,000

Total Assets 388,507 27,581 416,088

LIABILITIES

Mortgage 124,569 124,569

Student loan 19,881 19,881

Total liabilities 124,569 19,881 144,450

Capstone Comprehensive Financial Plan 10

Net Worth 263,938 7,700 271,638

The following table provides an overall picture of your current investment portfolio:

Cash accounts:

Tax Free Savings Account

Projected investment values

Prepared for:

Chris Williams

Prepared by:

Student Edition

Annual Annual Unused Annual Weighted

Annual Year End

Year

Age

Deposit Maximum

Contribution

Growth Return Withdrawal

Balance

1 27 0 5,000 24,000 20 2.00% 0 1,020

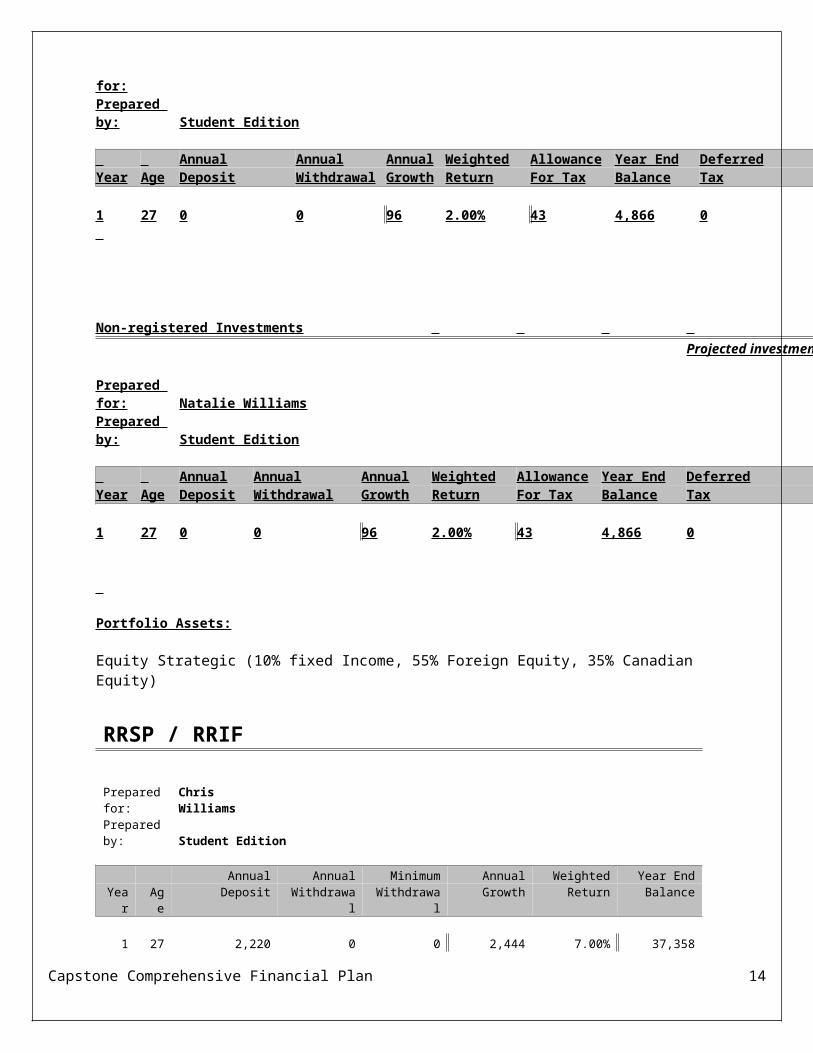

Non-registered Investments Projected investment values

Prepared for:Chris WilliamsPrepared by: Student Edition

Annual Annual Annual Weighted Allowance Year End DeferredYear Age Deposit Withdrawal Growth Return For Tax Balance Tax

1 27 0 0 96 2.00% 43 4,866 0

Non-registered Investments Projected investment values

Prepared for:Natalie WilliamsPrepared by: Student Edition

Capstone Comprehensive Financial Plan 11

Annual Annual Annual Weighted Allowance Year End DeferredYear Age Deposit Withdrawal Growth Return For Tax Balance Tax

1 27 0 0 96 2.00% 43 4,866 0

Portfolio Assets:

Equity Strategic (10% fixed Income, 55% Foreign Equity, 35% Canadian Equity)

RRSP / RRIF

Prepared for: Chris WilliamsPrepared by: Student Edition

Annual Annual Minimum Annual Weighted Year EndYear Age Deposit Withdrawal Withdrawal Growth Return Balance

1 27 2,220 0 0 2,444 7.00% 37,358

Balanced Diversified (45% fixed Income, 30% foreign Equity, 25% Canadian Equity)

RRSP / RRIF

Prepared for: Natalie WilliamsPrepared by: Student Edition

Annual Annual Minimum Annual Weighted Year EndYear Age Deposit Withdrawal Withdrawal Growth Return Balance

1 27 5,220 0 0 899.4 5.00% 18,887.4

The breakdown of investments held within the various plans is as follows:Cash and Cash Equivalent

Chris’s Bank Account 4,813Natalie’s Bank Account 4,813Chris’s TFSA 1,000 10,626

Balanced FundBalanced Diversified Fund 12,768 12,768

Equity FundEquity Strategic Portfolio 32,694 32,694

TOTAL 56,088

Capstone Comprehensive Financial Plan 12

Of your $56,088 of invested capital, at least $10,626 (18.95%) is invested in cash or cash equivalents in your chequing accounts and TFSA, $12,502 (22.3%) is invested in fixed income and $32,960 (58.76%) is invested in equities through your balanced diversified fund and the equity strategic portfolio

Risk Management

Insurance

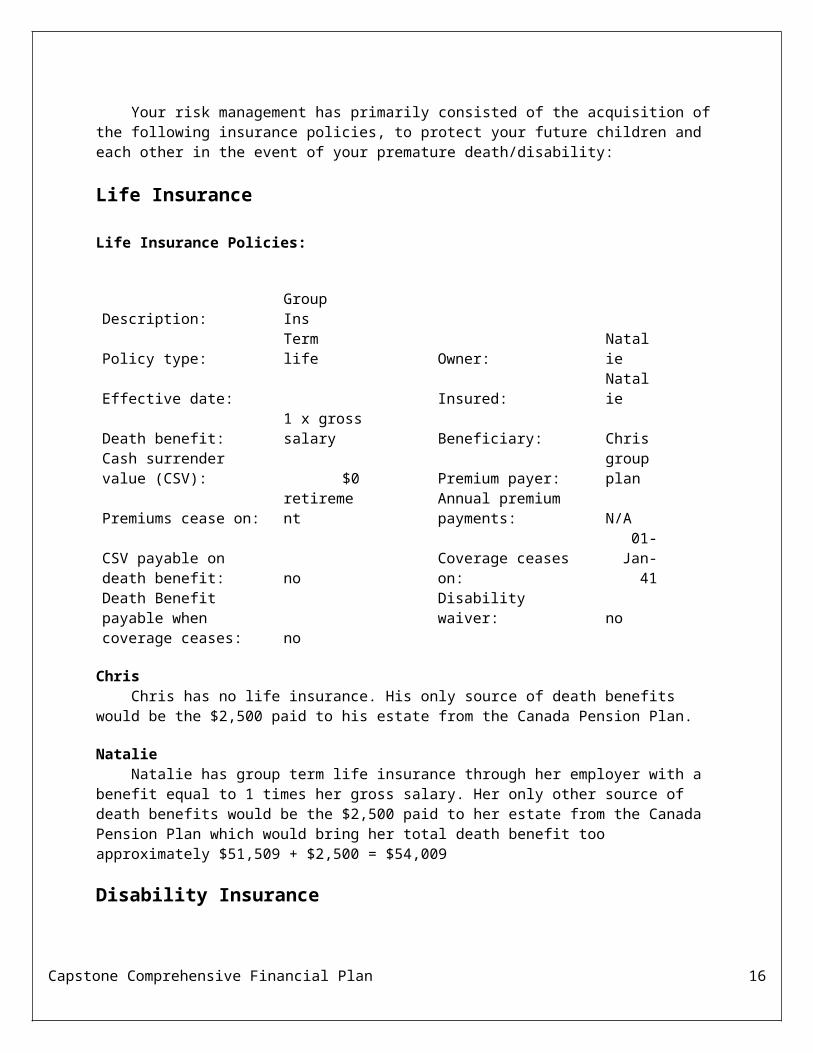

Your risk management has primarily consisted of the acquisition of the following insurance policies, to protect your future children and each other in the event of your premature death/disability:

Life Insurance

Life Insurance Policies:

Description: Group InsPolicy type: Term life Owner: NatalieEffective date: Insured: NatalieDeath benefit: 1 x gross salary Beneficiary: ChrisCash surrender value (CSV): $0 Premium payer:

group plan

Premiums cease on: retirementAnnual premium payments: N/A

CSV payable on death benefit: no Coverage ceases on:

01-Jan-41

Death Benefit payable when Disability waiver: nocoverage ceases: no

Chris Chris has no life insurance. His only source of death benefits would be the $2,500 paid to his estate from the Canada Pension Plan.

Natalie Natalie has group term life insurance through her employer with a benefit equal to 1 times her gross salary. Her only other source of death benefits would be the $2,500 paid to her estate from the Canada Pension Plan which would bring her total death benefit too approximately $51,509 + $2,500 = $54,009

Disability Insurance

In addition to your life insurance policies, you have the following group disability coverage on Natalie’s life, through her employer’s group plan:

Disability Insurance Policies:

Capstone Comprehensive Financial Plan 13

Description: Group INSURED: NataliePolicy Type: Group ST/LT disability Effective Date: Dec 31, 2012Benefits are 100% of her gross salary for the first 90 days and 70% of her gross salary thereafter until age 65 (taxable)Premiums are $0/month and end on retirement

Long-Term Care insurance

Presently neither of you has long-term care insurance to cover nursing home expenses or professional home care, if you become ill, injured or debilitated due to old age; and in need of assistance that could not be provided by your spouse; or in the event there is no surviving spouse at the time that the care is needed.

Property and casualty insurance

In addition to the other insurances you have, you have the following mortgage insurance:

Mortgage insurance policies:

Description: Mortgage insurance Insured: ChrisPolicy type: Mortgage life, disability and CI Effective date: Dec 31, 2012Policy premium: $27.79/biweeklyBenefits are that the policy covers the mortgage payments for 2 years in the event that Chris becomes disabled and pays off mortgage in the event of Chris’s death or Chris getting diagnosed with a critical illness.

Investments

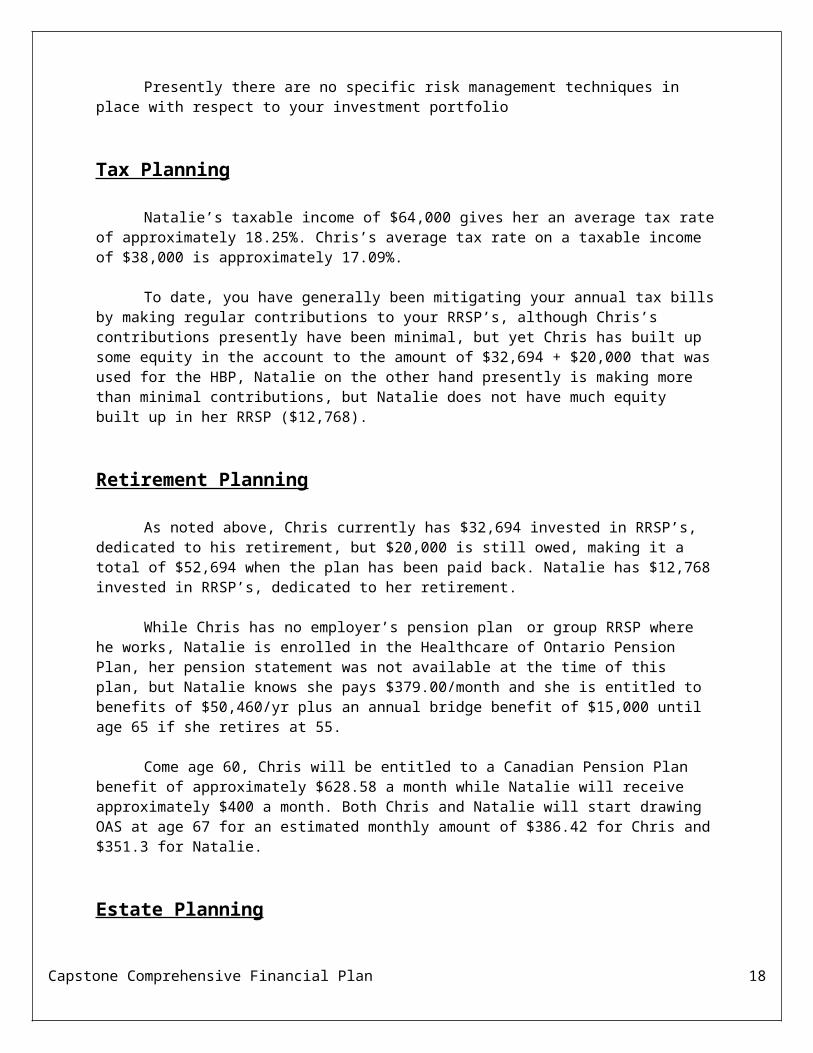

Presently there are no specific risk management techniques in place with respect to your investment portfolio

Tax Planning

Natalie’s taxable income of $64,000 gives her an average tax rate of approximately 18.25%. Chris’s average tax rate on a taxable income of $38,000 is approximately 17.09%.

To date, you have generally been mitigating your annual tax bills by making regular contributions to your RRSP’s, although Chris’s contributions presently have been minimal, but yet Chris has built up some equity in the account to the amount of $32,694 + $20,000 that was used for the HBP, Natalie on the other hand presently is making more than minimal contributions, but Natalie does not have much equity built up in her RRSP ($12,768).

Retirement Planning

Capstone Comprehensive Financial Plan 14

As noted above, Chris currently has $32,694 invested in RRSP’s, dedicated to his retirement, but $20,000 is still owed, making it a total of $52,694 when the plan has been paid back. Natalie has $12,768 invested in RRSP’s, dedicated to her retirement.

While Chris has no employer’s pension plan or group RRSP where he works, Natalie is enrolled in the Healthcare of Ontario Pension Plan, her pension statement was not available at the time of this plan, but Natalie knows she pays $379.00/month and she is entitled to benefits of $50,460/yr plus an annual bridge benefit of $15,000 until age 65 if she retires at 55.

Come age 60, Chris will be entitled to a Canadian Pension Plan benefit of approximately $628.58 a month while Natalie will receive approximately $400 a month. Both Chris and Natalie will start drawing OAS at age 67 for an estimated monthly amount of $386.42 for Chris and $351.3 for Natalie.

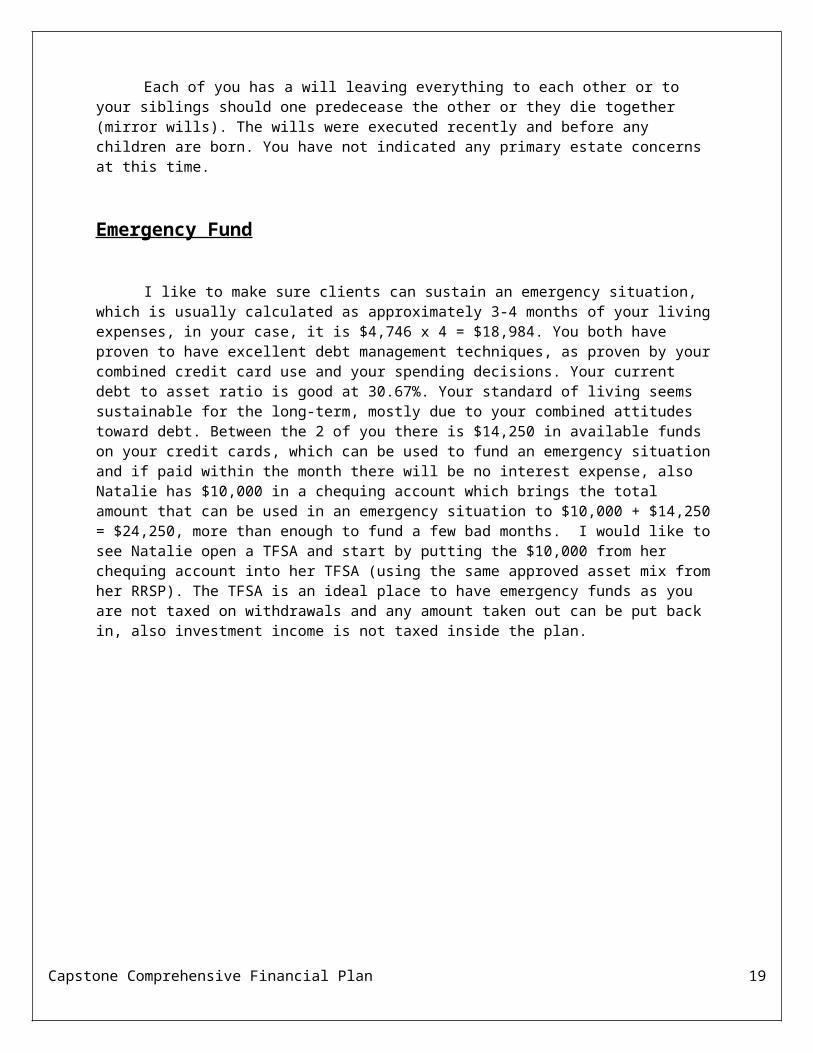

Estate Planning

Each of you has a will leaving everything to each other or to your siblings should one predecease the other or they die together (mirror wills). The wills were executed recently and before any children are born. You have not indicated any primary estate concerns at this time.

Emergency Fund

I like to make sure clients can sustain an emergency situation, which is usually calculated as approximately 3-4 months of your living expenses, in your case, it is $4,746 x 4 = $18,984. You both have proven to have excellent debt management techniques, as proven by your combined credit card use and your spending decisions. Your current debt to asset ratio is good at 30.67%. Your standard of living seems sustainable for the long-term, mostly due to your combined attitudes toward debt. Between the 2 of you there is $14,250 in available funds on your credit cards, which can be used to fund an emergency situation and if paid within the month there will be no interest expense, also Natalie has $10,000 in a chequing account which brings the total amount that can be used in an emergency situation to $10,000 + $14,250 = $24,250, more than enough to fund a few bad months. I would like to see Natalie open a TFSA and start by putting the $10,000 from her chequing account into her TFSA (using the same approved asset mix from her RRSP). The TFSA is an ideal place to have emergency funds as you are not taxed on withdrawals and any amount taken out can be put back in, also investment income is not taxed inside the plan.

Capstone Comprehensive Financial Plan 15

COMPREHENSIVE FINANCIAL PLAN – Step 4 25%The FOURTH step is to ANALYZE THE CLIENT’S FINANCIAL INFORMATION based on their stated goals, needs and priorities and identify potential opportunities and constraints and assesses information in order to formulate and evaluate financial planning strategies to develop a Comprehensive financial plan…

ANALYSIS

Financial Management

The following graphs illustrate the cash flow surplus or deficit that would result if your retirement plans were to unfold as you currently envision. The surplus/deficit is illustrated on an annual basis. Since the projection is based on assumed rates of income and investment returns, all numbers are approximate.

Forecasts (cash flow)

0100,000200,000300,000400,000500,000600,000700,000800,000900,000

27 30 33 36 39 42 45 48 51 54 57 60 63 66 69 72 75 78 81 84

Other Non-taxable

Income: Natalie

Income: Chris

Lifestyle Needs

Total Needs

For the next three years (2013-2015) you will run an accumulated cash flow surplus of approximately $23,556. The basement renovation is done, but there is now the added expense of paying for the family business and an ongoing expense for small home repairs, these added expenses will reduce the amount of any surplus during the duration of payments.

The cash flow is really reduced during the child bearing years (2016, 2019), where there used to be a surplus of almost $25,000, it trends down to an accumulated deficit of almost

Capstone Comprehensive Financial Plan 16

$45,000, due to Natalie’s reduced income, where there alone is a deficit of over $15,000 in 2016 also over a $30,000 deficit for 2019.

Once the child bearing costs/income reductions are done, there starts to be more surpluses of cash flow. Starting around age 38 you will start to see these surpluses start around $4,500 and steadily increase over the next 17 years to approximately $35,000/yr at which time you will be 55, your planed retirement age.

From this point on you will be seeing some pretty significant deficits in cash flow that will surely lead to insolvency. This projection has taken into account CPP starting at 60 and OAS starting at age 67 for the both of you; however this projection has not taken Natalie’s Healthcare pension into account or the impact of selling the business at retirement, if there is any significant value created over the years, and therefore is understated for income in retirement years.

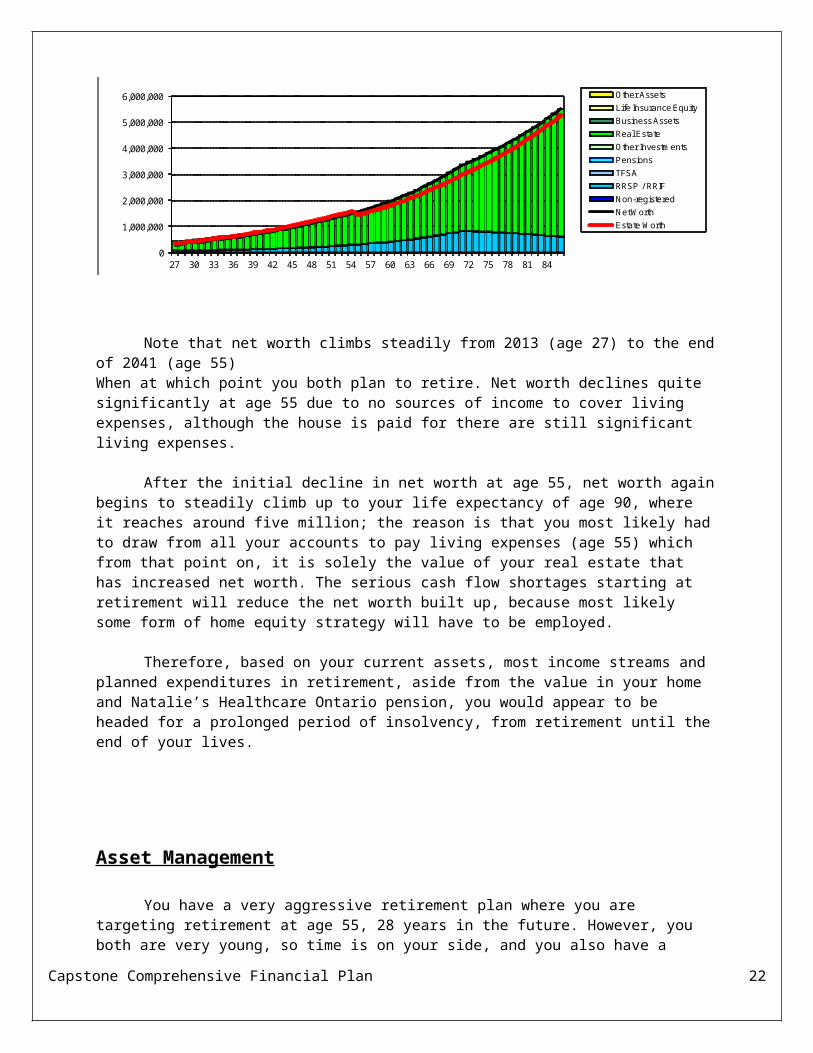

The graph below illustrates your anticipated total net worth (assets minus liabilities) for year-end 2013, extending to approximately 2076

Forecast (net worth)

0

1,000,000

2,000,000

3,000,000

4,000,000

5,000,000

6,000,000

27 30 33 36 39 42 45 48 51 54 57 60 63 66 69 72 75 78 81 84

Other AssetsLife Insurance EquityBusiness AssetsReal EstateOther InvestmentsPensionsTFSARRSP / RRIFNon-registeredNet WorthEstate Worth

Note that net worth climbs steadily from 2013 (age 27) to the end of 2041 (age 55)When at which point you both plan to retire. Net worth declines quite significantly at age 55 due to no sources of income to cover living expenses, although the house is paid for there are still significant living expenses.

After the initial decline in net worth at age 55, net worth again begins to steadily climb up to your life expectancy of age 90, where it reaches around five million; the reason is that you most likely had to draw from all your accounts to pay living expenses (age 55) which from that point on, it is solely the value of your real estate that has increased net worth. The serious cash flow shortages starting at retirement will reduce the net worth built up, because most likely some form of home equity strategy will have to be employed.

Therefore, based on your current assets, most income streams and planned expenditures in retirement, aside from the value in your home and Natalie’s Healthcare Ontario pension, you would appear to be headed for a prolonged period of insolvency, from retirement until the end of your lives.

Capstone Comprehensive Financial Plan 17

Asset Management

You have a very aggressive retirement plan where you are targeting retirement at age 55, 28 years in the future. However, you both are very young, so time is on your side, and you also have a Balanced Growth and a Growth + portfolio to reach your goals. Chris’s portfolio is ideal for his risk tolerance and therefore should not be adjusted. However, Natalie’s portfolio can be adjusted to 75% equities and 25% fixed income, this adjustment is hoped to improve the portfolio’s return from an average 5% to 6%.

Risk Management

Risk of Death

ChrisThe most immediate concern is the loss of his annual income, if Chris were to die prior

to his planned retirement date of Jan 1, 2041 (28 years in the future). After allowing for annual income tax estimated at roughly $4,793, the loss of net annual income to the family would be $33,207 ($38,000 minus taxes of approximately $ 4,793) for a maximum of 28 years, or a total of $929,796 (33,207 a year times twenty-eight years = $929,796).

While there is an income loss, there is also an estimated final expense that has not been addressed at this time. Also it would be usual for the estate plan to provide for the discharge of the family liabilities of $124,569 (mortgage) at the first death of either Chris or Natalie, for a total liability of $1,054,365(929,796 + 124,569). Most of this liability is temporary, as the need for income is reduced every year until it would terminate on Chris’s retirement in 28 years and it is anticipated that the mortgage will be paid off before 2041.

NatalieThe most immediate concern would be the loss of Natalie’s annual income, were she to

die prior to her planned retirement date of Jan 1, 2041 (28 years in the future). After allowing for annual income tax estimated at roughly $12,545, the loss of net annual income to the family would be $51,455 (64,000 minus taxes of approximately 12,545) for a maximum of 28 years, or a total of $1,440,740 (51,455 a year times twenty-eight years = $1,440,740).

While there is an income loss, there is also an estimated final expense that has not been addressed at this time. Also it would be usual for the estate plan to provide for the discharge of the family liabilities of $124,569 (mortgage) at the first death of either Chris or Natalie, also there is an outstanding student loan for $19,881, for a total liability of $1,585,190 (1,440,740 + 1 24,569 + 19,881). Most of this liability is temporary, as the need for income is reduced every year until it would terminate on Natalie’s retirement in 28 years and it is anticipated that the mortgage and student loan will be paid off before 2041.

Capstone Comprehensive Financial Plan 18

Risk of Disability

NatalieIn case you become disabled, your short-term and long-term disability coverage through

your work will provide 100% of your gross salary for 90 days and then converts to 70% of your gross salary until the age of 65. In the event of total disability, the insurance provides “own occupation” disability coverage for the first two years and “any occupation” coverage thereafter. This amount should be adequate to replace your earned income during that period, there are, however, a few issues to consider.

The first two years of disability coverage will probably be very adequate to cover expenses over that period, mainly due to the policy being “own occupation” (the most expensive and best coverage of disability insurance), the problem arises after the two year mark when the disability coverage switches to “any occupation” (the cheapest and worst of the disability coverage’s)

Depending on the wording in the insurance contract, there could be issues with the amount paid when the “any occupation” insurance kicks in after two years, this type of insurance pays benefits depending on whether you can do any type of occupation, not just your specific position you held, thus they could say that you can answer phones, for example, and therefore stop paying benefits if you decline to take this new position. If this ends up being the case then substantial income loss will affect your cash flow going forward from the time the two years is up.

ChrisChris presently has no disability insurance. If he were to become permanently disabled

tomorrow, the family would lose about $33,207 in annual after-tax income. Seeing as Chris plans to work another twenty-eight years, this would translate into a maximum total loss of $929,796 of after-tax cash flow (if the disability was permanent)—a disaster having an enormous impact on the family finances, both in the long and short term.

Long-Term care Insurance

Without any long-term care insurance you can face disastrous financial circumstances in the event that either of you sustains a debilitating injury or illness that has a long-term or permanent nature.

If an event occurs causing such an event, it could have several negative consequences:

The interruption, diminishment or cessation of income from employment or self employment

Increased costs for treatment and/or care for the debilitated spouse Disruption of routine for the healthy spouse who would have to assume the role of caregiver, likely resulting in the interruption, diminishment or cessation of his or her income from employment or self-employment Possible reduced opportunity for and enjoyment of lifestyle activities (skiing, travel, etc.) for both of you

A debilitating event occurring post-retirement would still result in increased costs for care and treatment and the disruption in retirement lifestyle for both of you.

Capstone Comprehensive Financial Plan 19

Long-term care insurance could at least provide the means to cover costs, freeing the healthy spouse to continue a normal (or near normal) work schedule.

Critical Illness

Aside from any issue of working capacity, a critical illness event like a heart attack or stroke (there are about 6 different critical illnesses) would impact your current, and perhaps future, ability to enjoy a full retirement lifestyle. Such an event could even result in a shortened life expectancy.

Without some financial protection from the impact of a critical illness, you might not have either the time or the resources to modify your circumstances (early retirement, wheelchair ramps in the home, live-in caregiver etc.) that would allow you to enjoy the kind of retirement you envisioned, this insurance pays a lump-sum that would address modifications to the home.

Property and Casualty

Presently the only details’ concerning property and casualty insurance is the mortgage insurance that Chris has in place. The mortgage insurance takes care of payments should Chris become disabled or it will pay the mortgage off if Chris gets diagnosed with a critical illness and/or dies. You might want to look at Natalie getting this insurance also, as she earns more and it would have more of an impact if the higher earner gets diagnosed with a critical illness or disability, then the lower income earner is stuck paying all the expenses.

Investments

Your investment portfolios have both been performing well, but I feel that there is one issue worth addressing:

Natalie’s registered account needs to be re-balanced to 75%equities and 25%fixed income, where I believe she will achieve a 1% improvement over her old asset mix to a new average return of 6%

The Impact of Death

The impact of a premature death of either of you would have serious immediate and long-term financial consequences.

Capstone Comprehensive Financial Plan 20

Death Occurring during the Working Years

ChrisChris’s death prior to retirement will result in the termination of his net salary income for

the balance of his working life: a potential loss of up to $929,796 in after-tax income (33,207/year, depending on when death occurs).

Also, Chris’s death would reduce the amount of retirement income available to Natalie as the sole survivor. Reducing the working years for Chris could, in turn, reduce the projected $626.58 a month in Canada Pension retirement benefits that he is projected to begin receiving when he turns 65. Natalie would then be entitled to receive a survivor’s benefit of up to 60% of Chris’s retirement pension, provided the combination of Natalie’s CPP and the survivor’s benefit do not exceed the maximum CPP benefit available at that time. Natalie

Natalie’s death prior to retirement would result in the termination of her net employment income for the rest of her working life – a possible loss of up to $1,440,740 in after-tax income ($51,455 a year, depending on when such death might occur).

Also, Natalie’s death would reduce the amount of retirement income available to Chris as the survivor. Reducing the working years for Natalie would, in turn, reduce the projected $435.42 a month in Canada Pension retirement benefits that she is projected to begin receiving when she turns 65. Chris would then be entitled to receive a survivor’s benefit of up to 60% of Natalie’s reduced retirement pension, provided the combination of Chris’s CPP and the survivor’s benefit do not exceed the maximum CPP benefit available at that time.

Death Occurring after Retirement

ChrisIf Chris’s death were to occur post-retirement, there would be no resulting loss of income

from employment, but the CPP retirement benefit payable to Natalie as a survivor’s pension would still be subject to the 60% reduction and maximum cap in her hands. However, Chris’s old age security benefits (if started) would stop at his death.

NatalieIf Natalie were to die during retirement, there would be no resulting loss of income from

employment; and the CPP retirement benefit would still be subject to the 60% reduction and maximum cap in Chris’s hands. Natalie’s old age security benefits (if started) would stop at her death.

Other Considerations

Whenever death might occur, final expenses have not been addressed and the $2,500 covered by the CPP death benefit would not cover them. You have $124,569 outstanding on your mortgage, but no credit card debt and the student loan will be paid off in 3.13 years.

Capstone Comprehensive Financial Plan 21

Summary

If either of you were to pass away during your working years, there would be a serious shortfall of after-tax income and resources to offset the liabilities and expenses incurred.

The worst scenario that we have seen is in the event of Natalie’s death, this could result in a loss of net family income of $1,585,190 when you add the need to pay mortgage and if the student loan is still outstanding (although very unlikely). Natalie has group term life insurance through her employer that pays a benefit of one times her gross salary which would equal $64,000 for the current year; this would bring the total including the CPP death benefit of $2,500 to $66,500, a shortfall of approximately $1,518,690.

Although the shortfall for Chris’s case is less severe, there is still quite a substantial shortfall. His combined maximum loss of income and resources would be calculated as $1,054,365 - $2,500 (CPP death benefit) = $1,051,865. Chris has no life insurance to replace any loss of income.

Additionally, provisions for your unborn children will have to be addressed as they come due.

Tax Planning

Neither of you are self-employed (yet), and as such can’t take advantage of as many tax deductions as people who are. However, with Chris taking over the family business, there will be at that point opportunities for tax breaks. You might want to look at the caregiver credit for possibly taking care of Natalie’s mom (if she stays with you, something that was not clear at meeting, as word was mentioned about helping out with a scooter)

Good general investment advice would see interest bearing investments and international stocks held inside registered plans, while Canadian stocks that pay dividends or bonds that accrue capital gains should be held in non-registered accounts to take advantage of favorable tax laws (dividend gross-up and capital gains inclusion rate of 50%).

You have taken advantage of tax deferral by accumulating $45,462 ($62,462 if you factor in the HBP loan repayment) in tax-deferred RRSP’s, but still have an estimated $25,845 of unused contribution room carried forward into the current taxation year.

Up until this point, only Chris has opened a TFSA and he has contributed $1,000 to date. This leaves contribution room of $24,500 for Chris and $25,500 for Natalie.

Capstone Comprehensive Financial Plan 22

Retirement Planning

NatalieTo date, Natalie has been relying primarily on her Healthcare pension to affect a

retirement plan, along with accumulated savings in her RRSP of $12,768 and government income sources; her annual retirement income package appears as follows, come age 67:

Healthcare of Ontario Pension Plan Approximately $50,460/year- (after bridge benefit is

done)Canada Pension Plan ($697.3/month) $8,374Old Age Security ($351.3/month) $4,216RRSP proceeds (RRIF/Annuity) ($12,768 at present) Unknown

ChrisWhile Chris has no entitlement to any employer’s pension plan, he has been

compensating by contributing more heavily to his RRSP. His retirement income package appears as follows, come age 67:

Canada Pension Plan ($697.3/month) $8,374Old Age Security ($386.4/month) $4,637RRSP proceeds (RRIF/Annuity) ($32,694 at present, $52,694 taking into consideration

the HBP repayment) Unknown

Estate Planning

Your current wills were just drafted after you were married and should not need to be updated until the children are born or another type of life-altering event, i.e. death, birth, loss of employment etc. You should update your wills with the addition of each child to prepare for a tragic event, in case it happens after one is born, but before the other arrives.

It wasn’t clear if either of you has power of attorney (PA) either for property or for personal care. When asked if you have wills and power of attorney in place, you replied “you were pleased to report that they had them prepared by a lawyer just after you were married”. With this information I will assume that you have them in place and understand the implications of not, however if you fail to execute powers of attorney (personal care and property) there could be delays/denials with needed medical issues and/or no access to investments.

Capstone Comprehensive Financial Plan 23

COMPREHENSIVE FINANCIAL PLAN – Step 5 20%The FIFTH step to develop and present the Comprehensive Financial Plan by FORMULATING RECOMMENDATIONS supported by appropriate analysis and synthesis to improve the client’s current and projected financial situation that work towards meeting all of their stated goals and objectives

Recommendations

Financial Management

Seeing as you start to run deficits in 2016 through to approximately 2024, you should invest all (or close to all) excess cash flow to Chris’s RRSP and then to his TFSA accumulating almost $25,000 by 2016 and continue to do so. You will have to draw from registered accounts to fund deficits, but by using Chris’s accounts (TFSA first then RRSP) the cash will be taxed at a lower marginal tax rate than Natalie’s. Chris should open a spousal RRSP for himself and have Natalie contribute her share here(keeping the same asset mix as his RRSP), as the money will hopefully be in there longer than three years as to not have it attributed back to Natalie. When Natalie contributes her share to the spousal RRSP the contribution will be more advantageous when it is withdrawn by the lower income earner. This technique has an added benefit of also paying back the HPB loan (as long as you designate these payments as HBP repayments by filling out the proper CRA form) and therefore will be available if ever needed again.

Addressing the issue of paying off mortgage before age 40 while starting a family along with purchasing the business – While it may seem advantageous to also try to pay off the mortgage by age 40 it is not feasible as you already start to run a cash flow deficit by 2015 that continues for the next eleven or so years. You presently pay $815 a month for your mortgage according to the cash flow statement you submitted, in order to pay off mortgage by the time you turn 40 you will have to increase payments to $1,166 a month (using TVM calculations), this is $351 a month more than you are paying presently.

If you can secure a loan (for an amount equal to the student loan) against the equity in your home that beats the rate charged for your student loan (there should be no problem as you have over 25% equity built up in your home), then you can pay off the student loan and extend your repayment timeframe, thereby lowering monthly expenses and freeing up some cash flow. There are a lot of options once you unlock the equity in your home, i.e. paying off more expensive debt, investing in ideal risk approved investments or even just using it to fund cash flow deficiencies.

The sooner something like this “loan against equity” happens the more advantageous it is, as it will have longer to grow (provided it is a loan and used for appropriate risk approved investments, this technique also has the added benefit that the interest incurred on the loan is tax deductible) and earn a return. The specific strategy using this” loan for value against home equity” is very complicated and I would like to come up with something that I could present at our next meeting that could help deal with the serious cash flow shortages in your retirement years (age 55 onward).

Capstone Comprehensive Financial Plan 24

Asset Management

As stated earlier the only concern I have with your asset mix is with Natalie’s portfolio. She currently has an asset mix consisting of 45% fixed income and 55% equities, but I‘d like to re-adjust it to 25% fixed income and 75% equities. I feel that this re-adjustment will introduce a 1% increase in your average return, which will bring your rate of return for your registered account from 5% to 6%. This re-adjustment might also present some tax savings, depending on where specific investments are placed.

As stated in the last section, using your principal residence to acquire a loan against the equity built up in your home is a technique I will present at our next meeting.

No other property is mentioned on the asset side, this is better that overstating values, as it will give a more accurate statement of the true value of your assets.

Risk Management

We/you should meet with your life insurance advisor as soon as possible, to re-evaluate your policies. The first major concern is that Chris has no life insurance; to protect Natalie, the unborn children and/or pay for any final expenses should he pass away.

The mortgage should be discharged before age 50 (approximately 22 years in the future) and Chris has mortgage life, disability and critical illness insurance in place in case a tragic event occurs. Natalie should consider this same insurance for herself, if she were to predecease Chris all the burden of the finances would fall on him, this insurance would protect the both of you.

You will each need individual term insurance coverage to protect against the family income shortfall (up to $1,440,740 in total for Natalie and $929,796 for Chris) in the event of the death of either to you prior to retirement.

Dealing with disability insurance—Natalie should look into trying to keep her “own occupation” after the two years are up, or at least a “regular occupation” this will help protect you from being forced to take on employment below your pay grade. Other than that, Natalie is protected from disability, Chris on the other hand, needs to get short-term (possibly) and long-term disability insurance. A “regular occupation” or to save money it could be a “any occupation”; also it will want to cover 2/3 of income ($2,090), there most likely will be a 90-day waiting period if you go without the short-term insurance, also there might just be a five year benefit period.

Capstone Comprehensive Financial Plan 25

Tax Planning

There are many tax planning techniques to help minimize your current and future taxes and, by doing so, will maximize the value of your investment funds and your estate. The three main strategies I will suggest are: deductions, deferring taxes and dividing income.

Deductions

One good suggestion to increase current tax deductions is to contribute more to your RRSP’s each year. In addition to contributing more to your RRSP’s, you should also consider “playing catch-up” by utilizing some of your contribution carry-forward room ($18,712 for Chris and $7,133 for Natalie). Chris should open a self-directed spousal RRSP and have Natalie contribute her contributions here.

There is little else that the two of you can do to maximize your current deductions, although you could consider reducing expenses associated with your non-deductible debt by paying off, first, your highest interest loan (Natalie’s student loan) $19,881, and then, as is practical, the outstanding balance of $124,569 on your home mortgage.

Deferment of Taxes

Contributing more to your RRSP’s will not only give rise to current tax deductions, but will also shelter your accumulated investment capital from current taxation laws, optimizing its pre-tax compounding ability.

All contributions should be accelerated by one year, so that contributions for the 2013 taxation year is made at the beginning of the 2013 calendar year, therefore increasing by one year the amount of time your investment will be able to accrue on a tax-deferred basis.

At such a time as when you have maximized your RRSP contributions, which are tax deductible, you should each consider contributing to a tax-free savings account (with Natalie opening one). These contributions are not tax-deductible, but the income accrued on investments is still sheltered from tax and is not taxable to the plan holder when withdrawn.

Dividing Income

Currently you both are in different marginal tax brackets (Chris at approximately 20% and Natalie at 32.98%). This difference will likely remain throughout your working lives. Given that Natalie will be receiving benefits from her healthcare pension plan in retirement, and Chris will have no corresponding pension, Natalie will likely also be taxed at a higher marginal rate when you are both retired. Considering this, opportunities for tax savings through income splitting (the shifting of taxable income from Natalie to Chris, to be taxes at a lower rate) will exist.

Capstone Comprehensive Financial Plan 26

Here are a several more general techniques that should benefit you in retirement:

CPP assignment

Through the CPP (assignment) retirement pension sharing, once you are age 60 and (presumably) in receipt of the pension, you may equalize your pensions. This would result in the payment (and taxation) of a portion of Chris’s pension (50% of the difference between the two) to Natalie, with some corresponding tax savings, assuming that Natalie is then in the lowermarginal tax bracket. The projected difference in your CPP benefits at age 60 is only $2,743 a year (7,543 – 4,800), of which only $1,371.5 could be shifted from Chris to Natalie. Assuming a 13% tax-rate differential between Chris and Natalie, this would save you $178.3 in annual taxes.

Pension Splitting

When the payout of Natalie’s Healthcare Ontario pension plan begins, she will be permitted to allocate up to 50% of the annual pension to Chris for tax purposes. As long as Chris is in a lower marginal tax bracket, tax savings will result. There is no correspondingrequirement for Chris to allocate any of his qualifying retirement income (such as RRIFpayments) to Natalie in return. Natalie’s Healthcare Ontario pension at age 55 is projected to be $54,460/year plus an annual bridging benefit of $15,000 until age 65, 50% ($27,730) of which could be taxed in Chris’s hands. Assuming the same 13% tax rate differential, pension splitting would save you $3,604 a year in taxes.

Spousal RRSP

As mentioned earlier in this plan, RRSP contributions made by Natalie to a “spousal” plan in Chris’s name would help to increase his retirement income resources, and keep his more in line with hers. When the RRSP is converted to an income stream in retirement, the tax burden on withdrawals should be lower when reported in Chris’s hands.

Retirement Planning

The most important decision to be faced over the course of the next 28 to 63 years will be when to commence your various forms of retirement income – Natalie’s Healthcare Ontario pension, CPP, OAS and cash flow from your RRSP’s and TFSA’s

Presently we have no idea as to when Natalie’s pensions’ “normal” start date would occur; all we know is that she is scheduled to receive a projected $54,460/year plus an annual bridging benefit of $15,000 until age 65, if she retires at 55.

Chris and Natalie could both start their CPP retirement benefits as early as age 60, in 2047. Doing so would help to compensate for both of you retiring five years before, when employment income would have stopped. Taking the pension prior to age 65 will result in a reduction of the assumed age 65 pension benefit

Old age security (OAS) will start at age 67 for both of you, in 2054, at an amount of $4,216/year for Natalie and $4,637/year for Chris.

Capstone Comprehensive Financial Plan 27

You can commence receiving income from your RRSP’s at any time (because they are not locked-in) as long as you start the payout process before the end of the year you turn 71 (in 2057) . You can do anything you want with the money in the plan, but the most widely used tax advantaged options consist of: income taken from plan in the form of periodic withdrawals, converting the proceeds of the RRSPs to annuities or by converting the RRSPs to registered retirement income funds (RRIFs). For the time being, any consideration of income from the RRSPs has been left out, until we see where income shortfalls might occur, calculate their magnitude and consider how to best deal with them.

Very serious shortfalls in cash flow during retirement begin at age 55 and continue indefinitely until your projected life expectancy of 90. These shortfalls steadily increase over this timeframe, I hope to have a viable solution for you at our next meeting, as mentioned earlier, but there are still a few options to consider that could be provided for in a number of ways: consider creating a non-registered retirement fund (keeping the same asset mix as your registered accounts) and then making withdrawals from this portfolio first, because the tax reporting would be less and leaving your RRSP’s intact for as long as possible will optimize the tax-deferred accrual of investment income within these plans; by borrowing against the equity in your home; or by Natalie/Chris working longer than planned, perhaps to age 60, in 2046.

Estate Planning

You need to update your wills once your first child is born, or before a life-altering event occurs and if powers of attorney are not enacted on each other (personal care and for property), then they should be at the earliest convenience. Each of your new wills should make provisions for the allocation of your net estate to your children at the last death.

Your powers of attorney for property should name each other as the other’s attorney since you both have a good working knowledge of your finances and investments. Consideration should be given to also naming an alternate attorney — perhaps your oldest child, if suitable — to act in the event one of you cannot.

With respect to the powers of attorney for personal care, it would be usual for a couple to name each other as attorney, with perhaps your eldest child, or eldest two children, named to act as alternate.

You are each the beneficiary of each other’s RRSP and that is fine, both for tax andprobate purposes, since the RRSP can “roll” tax-free to the survivor at the first death and assetspassing outside the estate (as the RRSPs would) are not subject to probate fees.

Capstone Comprehensive Financial Plan 28

Alternatives

Your cash flow and net worth graphs presented earlier in this financial plan indicate a cash flow shortage in the medium-term 2016 – 2019, with the strategies suggested I think that these cash flow shortages can be dealt with, the real problem comes later on in your life from age 55 onward. During retirement there is an awkward phase where no income is coming in (other than the returns generated in registered accounts) either through employment or government benefits. I don’t feel that you will be able to meet your retirement objectives by continuing on your current path, any kind of success would be dependent upon leveraging the equity in your home and you could easily find yourself insolvent if investment rates were to be lower, or inflation was to be higher than expected. With very little safety-net built into the plan, an interruption of income in the next several years, or an unexpected increase in expenses, could easily make your projected lifestyle unattainable.

Many of the recommendations outlined on the previous pages could help you to improve your equity position in retirement, but alone they still would not likely be able to guarantee your ability to achieve the retirement lifestyle you desire. There are, however, some additional steps that you should consider as an alternative to your current plan:

Buying Business

Buying the business is one of the larger expenditures expected during your life, and seeing as there is flexibility in the payments, I would suggest extending them as long as possible. The purchase of the business is not a loan and as such has no interest rate associated with it, this is advantageous as you can extend payments and incur no extra cost in doing so. Adjusting the payments from $10,000/year for ten years to $5,000/year for twenty years, this will free up a lot of extra cash flow for the next ten years and allow you to invest the excess.

Delay Having Kids

The most extreme scenario would see that no children would be born, this would free up a lot of extra cash flow, not to mention the benefit of not having reduced income for the child bearing years (2016 and 2019), which alone can account for most of the cash flow shortage in the medium-term. Another fairly extreme scenario would see you only have one child; this would still free up a lot of cash flow and a good piece of the medium-term shortfall from income reduction. One other scenario would see you have both the children, just at times of greater financial stability and where you have accumulated more of an asset base. Also delaying the timeframe between child births, by extending it one year, from having children three years apart (creates a $24,000 expense in one year) to having them four years apart, by doing this you will not have to pay for later years child care while paying for younger years child care (at the same time), thereby reducing expenses for that year.

Retirement Date

Adjusting your retirement date is one of the simplest techniques to employ, of course it s also difficult to accept. It is easy because it does not affect the projections or anything else and it is something you can decide on the fly. Extending your retirement date past your targeted

Capstone Comprehensive Financial Plan 29

retirement date of Jan 1, 2041, would obviously, extend your cash flow surpluses during your working years and therefore enhance your net worth at retirement. Working longer will also have the added benefit of enhancing Natalie’s Healthcare Ontario pension benefits in retirement (by restricting the reduction of her pension through a later start date) and enhance both of your CPP retirement benefits because you would be contributors for a few more years than if retiring early.

Throughout this plan we saw how your cash flow (thus affecting your net worth) will be seriously imperiled in the medium term and then again through retirement (age 55 onward) because your expenditures are greater than your income sources. The graphs below illustrate how extending your working lives, and some other modifications to your retirement plan, could mitigate the risk.

Alternate Scenarios

1. If the both of you were to retire at age 60 (2046) instead of at age 55 and put off having kids. Your cash flow never hits deficit levels until retirement and even then you will have had more excess cash to put in investments to cover the retirement expenses. This is a very extreme scenario as you will work five years longer and never have the family you envisioned.

Cash Flow (pro-forma)

-800,000-700,000-600,000-500,000-400,000-300,000-200,000-100,000

0100,000

27 30 33 36 39 42 45 48 51 54 57 60 63 66 69 72 75 78 81 84

Income Excess

Income Deficiency

Net Worth (pro-forma)

0

1,000,000

2,000,000

3,000,000

4,000,000

5,000,000

6,000,000

27 30 33 36 39 42 45 48 51 54 57 60 63 66 69 72 75 78 81 84

Other AssetsLife Insurance EquityBusiness AssetsReal EstateOther InvestmentsPensionsTFSARRSP / RRIFNon-registeredNet WorthEstate Worth

Capstone Comprehensive Financial Plan 30

2. However, if both of you kept working until age 65 (2051) and still had your expected children. There are still the deficits in the medium-term, but the cash flow accumulation phase is greater and longer, allowing for the diversion of excess cash flow to an investment account. This is a fairly extreme scenario as you will be working for ten years longer than envisioned.

Cash Flow (pro-forma)

-800,000-700,000-600,000-500,000-400,000-300,000-200,000-100,000

0100,000

27 30 33 36 39 42 45 48 51 54 57 60 63 66 69 72 75 78 81 84

Income Excess

Income Deficiency

Net Worth (pro-forma)

0

1,000,000

2,000,000

3,000,000

4,000,000

5,000,000

6,000,000

27 30 33 36 39 42 45 48 51 54 57 60 63 66 69 72 75 78 81 84

Other AssetsLife Insurance EquityBusiness AssetsReal EstateOther InvestmentsPensionsTFSARRSP / RRIFNon-registeredNet WorthEstate Worth

I’m not going to recommend either of these scenarios as they don’t take into effect all the considerations of the asset mix re-adjustment or any of the tax-saving techniques mentioned above, these scenarios are an idea of how “adjusting” (the retirement date is easily adjusted)your financial plans can provide a retirement that you envisioned.

Capstone Comprehensive Financial Plan 31

COMPREHENSIVE FINANCIAL PLAN –Step 6 10%The SIXTH step is to IMPLEMENT the financial plan by presenting an ACTION PLAN based on the recommendations set out in the COMPREHENSIVE FINANCIAL PLAN.

Implementation

Action Plan

Set up a TFSA for Natalie as soon as possible-Jan 29, 2013

Set up a spousal RRSP for Chris as soon as possible – Jan 29, 2013

Set up all registered/non-registered accounts to have the same allocation in risk approved investments.-Jan 29,2013

Talk to your lawyer to update wills when a life-altering event happens, I.E. birth, death, divorce-Mar 1, 2013

Talk to qualified life insurance professional for proper products for the both of you-Mar 1 ,2013

I will work out which specific investments we will use for asset mix -Mar 1,2013

I will work on and present at our next meeting the “loan for value using home equity” strategy mentioned earlier.

A few factors to consider that could change projection

Housing market could collapse Inflation could increase above 2.25% Portfolio might not perform as predicted Re-investment risk, when it’s time to invest the market might be worse/better

Changes in clients circumstances that can change projection

Divorce Death New additions to family Change in risk profile Change in time horizon

I would like to set the next meeting date on Mar 1, 2013. At this time you should have talked to your other professionals along with setting up the accounts; and I will have chosen the

Capstone Comprehensive Financial Plan 32

appropriate investments and put together the “loan for value using home equity” strategy. After this meeting we will set up yearly reviews, unless a life-altering event occurs, then we will have to meet at that point. The answer to your question you had regarding keeping your business a proprietorship or incorporating, is if you don’t perceive any value after you retire, then there are just a couple reasons to incorporate: liability issues in case of law suits or if you decide to pass the business on to your kin (corporations live forever and sole-proprietorships die with the proprietor.

Capstone Comprehensive Financial Plan 33

COMPREHENSIVE FINANCIAL PLAN – Overall 5%APPENDICESAll financial reports / statements used to support your analysis and recommendations must be inserted within the COMPREHENSIVE FINANCIAL PLAN Template document. Any supplemental reports may be included within your document or in the Appendix of your submission with additional commentary regarding how these reports support your conclusions and add value to the information you provide to the client.

Note: Any financial reports / statements sent separately will NOT be considered when marking your COMPREHENSIVE FINANCIAL PLAN.

Capstone Comprehensive Financial Plan 34

![IT331 Network Development Capstone Project [Onsite]thespringergroup.yolasite.com/resources/IT331_Appendix_A.pdf · Network Development Capstone Project Appendix A—Capstone Project](https://static.fdocuments.in/doc/165x107/5aa073e07f8b9a62178e2123/it331-network-development-capstone-project-onsite-development-capstone-project.jpg)